Crypto World

What is realized price? Bitcoin’s on-chain cost basis

Market price tells you what Bitcoin is worth right now. Realized price tells you what the market actually paid for it. When spot falls below that line, the whole market is underwater, and history says that is where bottoms tend to form.

Summary

- Realized price is the average price at which all circulating Bitcoin last moved on-chain, which makes it a measure of the market’s aggregate cost basis rather than its current value.

- It is calculated by dividing realized capitalization, the sum of every coin valued at the price it last moved, by the circulating supply.

- When the market price sits above realized price, holders in aggregate are in profit; when it falls below, the aggregate market is underwater, a condition that has historically appeared near cycle bottoms.

- Realized price is the foundation of a family of on-chain metrics, including MVRV and the MVRV Z-score, that analysts use to judge whether Bitcoin is overvalued or undervalued.

- It is a context tool, not a timing signal: realized price can fall, it relies on assumptions about coin movement, and it works best cross-checked against other data.

Realized price is one of the most useful on-chain metrics for understanding where Bitcoin sits in its market cycle, and it answers a question the ordinary price chart cannot: what did the market actually pay for its coins? While the market price shows what Bitcoin is worth at this moment, realized price shows the average cost basis of every coin in circulation, based on the last time each one moved on the blockchain. That distinction turns realized price into a kind of break-even line for the whole market, and the relationship between spot price and that line has historically marked periods of profit, loss, and, at the extremes, major tops and bottoms. This explainer covers what realized price is, how it is calculated, why it matters, and where its limits lie.

Realized price versus market price

The starting point is the difference between two ways of valuing the same coins. Market price is simple: it is the current trading price of Bitcoin, and market capitalization is that price multiplied by the number of coins in circulation. It reflects the latest sentiment, updated tick by tick, and it swings with every wave of buying and selling. It tells you what the market thinks Bitcoin is worth right now.

Realized price takes a different approach. Instead of valuing every coin at today’s price, it values each coin at the price it held the last time it moved from one wallet to another on-chain. The assumption is that when a coin moves, it is changing hands at roughly the market price of that moment, which approximates the price its current holder paid. Summing all of those individual last-moved values, and dividing by the supply, gives the average on-chain cost basis of the entire market. That is realized price.

The practical effect is that realized price strips out short-term sentiment. A sudden rally or crash changes the market price immediately, but it barely moves realized price, because most coins have not changed hands at the new level. Realized price only shifts as coins actually move at new prices, so it behaves like a slow-moving average of what holders paid. This is why analysts treat it as a measure of the market’s underlying economic reality rather than its momentary mood, and why the gap between the two prices carries so much information.

How realized price is calculated

Realized price is built on a companion metric called realized capitalization, or realized cap. To construct realized cap, you take every unit of Bitcoin and assign it the price it held the last time it moved on-chain, then add all of those values together. For Bitcoin, whose ledger is made of unspent transaction outputs, every output has a recorded last-moved price, which makes this calculation precise. Realized cap is therefore the sum of the whole market’s cost basis, an aggregate of what everyone effectively paid.

Realized price is then simply realized cap divided by the circulating supply. If realized cap represents the total dollars the market has committed to its coins, realized price represents the average dollars per coin. The concept traces back to work by on-chain analysts around 2018, when realized cap and the ratios built on it were introduced to bring cost-basis thinking into Bitcoin cycle analysis.

A simplified worked example makes it concrete. Imagine a tiny network of just four coins that last moved at prices of $20,000, $40,000, $60,000, and $80,000. The realized cap is the sum, $200,000, and the realized price is that divided by four coins, or $50,000. Now suppose the current market price is $45,000. The market price sits below the realized price of $50,000, which means that, on average, holders paid more than the coins are currently worth. In aggregate, the market is underwater. Scale that logic up to Bitcoin’s millions of coins and years of transaction history, and you have a single number that tells you whether the average holder is sitting on a gain or a loss.

Why realized price matters: the market’s cost basis

The value of realized price comes from what the gap between it and the market price reveals. When the market price is above realized price, the average holder is in profit, because coins are worth more than they last moved for. When the market price is below realized price, the average holder is at a loss, sitting on unrealized losses across the market. Realized price therefore acts as an aggregate break-even line, and crossing it in either direction is a meaningful event.

That break-even framing has real behavioral consequences. When the market trades below realized price, a large share of holders are underwater, and history shows this dampens natural selling: many people are reluctant to sell at a loss, so supply from ordinary holders tends to dry up. At the same time, the holders who do capitulate and sell at a loss during these periods are often selling to longer-term, value-oriented buyers near cycle lows. This is the emotional churn of a bottom, where weak hands give way to strong ones, and realized price is the line that defines who is above water and who is not.

On the other side, when the market price runs far above realized price, most of the supply sits on large paper gains, which makes the market more sensitive to profit-taking. A market where nearly everyone is deeply in profit has more potential sellers waiting, which is one reason extreme readings of the gap have historically aligned with cycle tops. Realized price, in other words, does not just tell you the market’s cost basis; it tells you something about the pressure of latent buying and selling built into the current price.

Realized price at cycle bottoms

The most watched use of realized price is as a bottoming indicator. Historically, the periods when Bitcoin’s market price fell below its realized price have been rare and have tended to cluster around major cycle lows. Because falling below realized price means the aggregate market is underwater, it usually coincides with deep bear-market sentiment, capitulation, and negative news, exactly the conditions that have, in past cycles, preceded strong recoveries. Buying Bitcoin during these below-cost-basis stretches has, in hindsight, produced some of the best long-term returns in its history.

The mechanism behind this is the churn of holders described above. As the market grinds below realized price, holders who cannot tolerate losses sell to value investors who are willing to accumulate at prices below the market’s average cost. That transfer of coins from weaker to stronger hands is a hallmark of a maturing bottom. Eventually, selling pressure exhausts, and as the market recovers, the price climbs back above realized price into the next expansion phase. Realized price thus behaves like a floor that the market probes during capitulation and reclaims during recovery.

It is important to be precise about what this does and does not promise. A drop below realized price has historically marked value zones, but it is not a guarantee of an immediate bottom, and the market can trade below its cost basis for an extended period during a deep bear market. Realized price identifies when the average holder is underwater, which is a necessary feature of past bottoms, but not a precise timing tool for the exact low. It tells you the market is in a historically significant zone, not the day it will turn.

The metric family: MVRV and the MVRV Z-score

Realized price and realized cap are the foundation for a broader set of on-chain valuation tools, and understanding the family helps you use any one of them. The most common is MVRV, the market-value-to-realized-value ratio, which divides market cap by realized cap. MVRV expresses the same information as the realized-price gap in ratio form: an MVRV above one means the market trades above its cost basis, and below one means it trades below it. Historically, MVRV readings below one have marked some of the best buying opportunities, while very high readings have marked cycle tops.

A refinement is the MVRV Z-score, which takes the difference between market cap and realized cap and normalizes it by the historical volatility of market cap. This adjustment makes it easier to compare extremes across different cycles, because it measures how unusual the current deviation is relative to Bitcoin’s own history instead of in raw dollar terms. The Z-score has been notably effective at flagging cycle tops, historically identifying major highs within a couple of weeks, and its lower band has marked deep-value bottoms.

Analysts also split these metrics by holder cohort. Short-term and long-term realized prices separate coins by age, often at a threshold around 155 days, to compare the cost basis of recent buyers against seasoned holders. When the short-term holder cost basis breaks below the long-term one, or when the market trades between them, it signals stress or transition. Related metrics such as the spent output profit ratio, which tracks whether coins are moving at a profit or loss, and measures of supply in profit or loss, round out the toolkit. The lesson is that realized price is rarely used alone; it is the anchor for a system of cost-basis metrics.

Reading realized price today

Realized price is most talked about during downturns, and a deep drawdown is exactly when it becomes most relevant. When Bitcoin falls far from a prior all-time high, the market price approaches and can breach the realized price, pushing the aggregate market toward or below its cost basis. That is the moment analysts start citing realized price heavily, because it frames the central question of a bear market: is the market simply underwater in a historically normal way that has preceded recoveries, or is something more structural at work?

Reading it well means treating realized price as context rather than a trigger. If the market is trading near or below realized price, the metric tells you the average holder is close to break-even or underwater, which historically has been a zone of value and reduced selling pressure. It does not tell you the exact bottom, and it must be weighed against the wider environment, including liquidity conditions, demand from buyers such as funds and treasuries, and the behavior of long-term holders. A market below realized price with returning demand is a very different picture from one below realized price with demand still fleeing.

The most useful habit is to watch realized price alongside its relatives and the flows around it. Is spot above or below realized price, and by how much? What is MVRV or the Z-score saying about how extreme the deviation is? Are long-term holders accumulating or distributing? Combining realized price with those cross-checks turns a single line into a genuine read on the market’s cost-basis health, which is far more informative than the spot chart alone during the fear and noise of a downturn.

The limits of realized price

Realized price is powerful, but it comes with important caveats that separate careful analysts from those who misread it. The first is that it is not a timing tool. A market can trade below realized price for months during a severe bear market, so the metric identifies a value zone, not a turning date. Treating a single break below realized price as a signal to expect an immediate bottom has caught out many people who underestimated how long capitulation can last.

The second caveat is that realized price can fall, which surprises people who assume cost basis only rises. When holders sell heavily at a loss, those coins move at the new lower prices, which drags the aggregate cost basis, and therefore realized price, downward. In a deep enough decline, realized price itself declines, so a level that looked like firm support can drift lower. Realized price is a moving line shaped by holder behavior, not a fixed floor. There are also structural quirks: the metric assumes a coin moving between wallets represents a change of ownership at market price, which is not always true, since exchange transfers and internal shuffles can move coins without a real sale. Lost coins that can never move again also sit in the calculation at old prices, gently distorting it.

The final and most important caveat is that realized price should never be read in isolation. Its creators and the analysts who use it consistently pair it with other data: the spent output profit ratio, supply in profit or loss, exchange inflows and outflows, and the derivatives structure that can make the spot picture misleading. Different chains need different adjustments, and even for Bitcoin the metric works best as one input among several. Used that way, as a cost-basis thermometer read alongside its family and the surrounding flows, realized price is one of the most reliable tools in on-chain analysis. Used alone as a precise buy or sell signal, it will disappoint.

Realized price across holder cohorts and other assets

The aggregate realized price is the headline number, but the concept becomes more powerful when it is broken down, and understanding that adds real depth. Analysts often split realized price by holder cohort, most commonly separating short-term holders from long-term holders using a coin-age threshold around 155 days. Short-term holder realized price tracks the cost basis of recent buyers, who tend to be more reactive, while long-term holder realized price tracks the cost basis of seasoned holders, who tend to hold through volatility. The short-term line usually sits closer to the market price and often acts as nearer-term support or resistance, while the long-term line moves slowly and marks a deeper floor.

Reading the two cohorts together tells a story the aggregate hides. In a healthy uptrend, the market price sits above both cohorts’ cost bases, so almost everyone is in profit. When the market falls below the short-term holder cost basis, recent buyers move underwater first, which historically pressures the group most likely to panic-sell. When it falls all the way below the long-term holder cost basis, even seasoned holders are underwater, a condition seen only in the depths of bear markets and often near major bottoms. Watching which cohort’s line the price is testing gives a finer read than the single aggregate number.

The concept also extends beyond Bitcoin, though with adjustments. For Ethereum, which uses an account-based ledger instead of Bitcoin’s unspent-output model, data providers approximate address-level cost bases and aggregate them, preserving the spirit of cost-basis valuation. Ethereum also requires care around its supply: the fee burn introduced by its network upgrades reduces effective supply over time, and staking flows change what counts as circulating, so realized price and its ratios need burn-adjusted and staking-aware supply figures to be accurate. The same idea applies to other large assets, always with chain-specific quirks.

The takeaway is that realized price is not a single rigid number but a lens that can be focused. Aggregate realized price gives the market-wide cost basis; cohort realized prices reveal which groups of holders are in profit or pain; and adapting the metric to other chains extends its usefulness across the market. Used at these finer resolutions, and always with awareness of each chain’s supply mechanics, realized price becomes a far richer tool than the single line most people first encounter.

Frequently Asked Questions

What is realized price in simple terms?

Realized price is the average price at which all Bitcoin in circulation last moved on-chain, which makes it a measure of the market’s aggregate cost basis, or what holders effectively paid. Unlike the market price, which reflects the latest trading value, realized price only changes as coins actually move at new prices, so it behaves like a slow-moving average of the market’s break-even level.

How is realized price calculated?

Realized price is realized capitalization divided by the circulating supply. Realized cap is found by valuing every coin at the price it held the last time it moved on-chain and summing those values. So if four coins last moved at $20,000, $40,000, $60,000, and $80,000, realized cap is $200,000 and realized price is $50,000, the average on-chain cost basis.

What does it mean when Bitcoin trades below realized price?

It means the aggregate market is underwater, with the average holder sitting on an unrealized loss because coins are worth less than they last moved for. Historically, these periods have been rare and clustered near cycle bottoms, coinciding with capitulation and deep bearish sentiment. They have often marked strong long-term value zones, though not a precise date for the low.

Is realized price a reliable bottom signal?

It is a useful context tool, not a precise timing signal. Falling below realized price has historically marked value zones near cycle lows, but the market can trade below its cost basis for an extended period in a deep bear market. Realized price tells you the average holder is underwater, a common feature of past bottoms, but it should be combined with other data before drawing conclusions.

How is realized price related to MVRV?

They express the same idea in different forms. MVRV, the market-value-to-realized-value ratio, divides market cap by realized cap, so an MVRV below one means the market trades below its cost basis, the same message as spot falling below realized price. The MVRV Z-score refines this by normalizing the gap for volatility, making it easier to spot extreme highs and lows across different cycles.

Can realized price go down?

Yes. Realized price rises as coins move at higher prices, but it can also fall. When holders sell heavily at a loss, those coins move at lower prices and drag the aggregate cost basis, and therefore realized price, downward. This means realized price is a moving line shaped by holder behavior, not a fixed floor, and a level that looked like support can drift lower in a deep decline.

What is the difference between realized price and realized cap?

Realized cap is the total, and realized price is the per-coin average. Realized cap sums the value of every coin at the price it last moved, giving the market’s aggregate cost basis in dollars. Realized price divides that total by the circulating supply to give the average cost basis per coin. Realized cap is compared with market cap; realized price is compared with the market price.

What are the main limitations of realized price?

It is not a timing tool, since markets can stay below it for months. It can fall when holders sell at a loss, so it is not a fixed floor. It assumes coins moving between wallets represent real ownership changes at market price, which is not always true, and lost coins distort it. Because of these quirks, it works best alongside other metrics like SOPR, supply in profit or loss, and exchange flows.

Disclaimer: This article is for information and educational purposes only and does not constitute financial, investment, or trading advice. On-chain metrics describe historical patterns that may not repeat, and cryptocurrency prices are highly volatile. Nothing here is a recommendation to buy or sell any asset. Always do your own research and consider consulting a qualified professional before making financial decisions. Information is accurate as of July 2, 2026, and may change.

CFTC Chair Michael Selig criticized Illinois lawmakers over a new 0.2% tax on crypto transactions, saying the state had moved against financial technology at the wrong time.

Summary

- Illinois’ 0.2% crypto tax drew sharp CFTC criticism before its planned 2027 start date.

- The law requires broker registration, monthly reports, and tax collection on covered digital asset activity.

- Federal crypto tax and market structure talks are moving while Illinois pursues its own rule.

In a July 1 statement, Selig said Illinois lawmakers “slammed the brakes on technological progress” when they approved the measure.

The tax forms part of Illinois’ fiscal 2027 budget and is set to take effect on Jan. 1, 2027. It applies to certain digital asset activity carried out by brokers, including exchange, transfer, custody, and wallet services. The rule has drawn criticism from crypto firms, policy groups, and some market figures.

Selig says state risks falling behind

Selig said blockchains could change how value moves across markets, much as the internet changed how information moves. He argued that tokenized assets may cover commodities, currencies, stocks, and bonds. His statement said Illinois could place residents and businesses at a disadvantage if the state taxes crypto transfers differently from other financial activity.

The CFTC chair also said Illinois lawmakers “decided they know better” than federal lawmakers working on crypto market rules. His comments came as Washington continues to review market structure bills, tax proposals, and agency roles. The remarks show a growing split between state-level tax policy and federal efforts to set national digital asset rules.

Brokers face new duties

Illinois’ Digital Asset Tax Act requires brokers to register with the Illinois Department of Revenue before covered activity begins. Brokers must collect the tax as a separate line item and file monthly reports on covered digital asset activity.

The law can also reach firms outside Illinois if they serve users in the state. Tax advisers have said customer records, mailing addresses, IP addresses, and other data may help decide whether activity falls under Illinois rules. That has raised questions about how exchanges, wallet firms, and custody providers will track and apply the tax in practice.

Industry criticism grows

Previously, crypto.news reported that Strategy co-founder Michael Saylor called the Illinois tax a “Big Mistake” after Governor JB Pritzker signed the budget. Industry groups also warned that the law could raise costs for users and push crypto firms away from the state.

Some critics have focused on the design of the tax. They argue that it applies to activity itself, not only to profits or capital gains. Others have raised concerns about routine wallet transfers, broker reporting systems, and whether the rule treats digital assets differently from stocks, bonds, or derivatives.

Federal talks add pressure

The Illinois dispute comes while Congress reviews broader crypto tax rules. As previously reported, lawmakers have split the Digital Asset PARITY Act into seven tax discussion drafts covering stablecoin payments, mining, staking, lending, wash-sale rules, charitable donations, and disclosure duties.

Moreover, Federal agencies are also reviewing crypto market rules. The SEC and CFTC opened a joint rules review covering derivatives, margining, and market structure questions. Against that backdrop, Selig’s criticism frames the Illinois tax as a state-level move that may clash with wider federal attempts to build clearer rules for digital assets.

Microsoft is investing $2.5 billion in a new operating business that embeds 6,000 engineers and industry experts directly inside enterprise customers to build and run AI systems.

The company, called Microsoft Frontier Company, launched on Thursday. It ties its work to measurable business results.

How the Microsoft Frontier Company Works and Who Runs It

The unit delivers what Microsoft calls Frontier Transformation. Experts embed with customers to co-design, deploy, and continuously improve AI systems at scale.

Follow us on X to get the latest news as it happens

Judson Althoff, CEO of Microsoft’s Commercial Business, positioned the effort beyond standard industry practice. He argued it combines deep industry knowledge with enterprise AI engineering.

“This goes beyond what has been labeled as Forward-Deployed Engineering, and will be the largest, most capable, outcome-driven engineering organization in the industry,” he said.

Microsoft Frontier Company will include salespeople, support staff, technical consultants, and forward-deployed engineers already at the company, many with experience in specific industries, CNBC reported.

The company stressed that customers keep control of their own intelligence. It pledged that client data will not be used to train models in ways that erode a customer’s competitive edge.

The platform also stays model-diverse. Customers can run models from OpenAI, Anthropic, Microsoft, open source, or specialized industry options for each task. Rodrigo Kede Lima will serve as president of the new organization.

Microsoft Enters a Crowded AI Deployment Race

The launch puts Microsoft in a fast-growing market. Rivals have moved quickly to sell hands-on AI deployment, not just tools.

Amazon Web Services committed $1 billion to its own deployment venture two days earlier. Both OpenAI and Anthropic also launched their own deployment ventures in May.

The OpenAI Deployment Company is a standalone entity backed by more than $4 billion in funding. Anthropic teamed up with Goldman Sachs, Blackstone, and Hellman & Friedman on a $1.5 billion venture to deploy Anthropic’s Claude AI model directly inside businesses.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Microsoft Commits $2.5 Billion to New AI Deployment Business appeared first on BeInCrypto.

Binance has moved a step closer to returning to the Philippine market after the country’s Securities and Exchange Commission granted final approval for its local partner BlockShoals Technologies to begin regulatory sandbox testing.

Summary

- The Philippine SEC has granted final sandbox approval to BlockShoals, moving Binance closer to a regulated return to the local market.

- BlockShoals will complete a 90 day integration with a licensed local provider before Binance backed user onboarding begins.

- The approval covers SEC sandbox testing, while separate BSP licensing requirements for crypto services remain in place.

In a post on X, Binance co-founder and Chief Customer Service Officer Yi He said the exchange had officially entered the Philippine market, while an accompanying SEC document showed that BlockShoals Technologies Inc. had received final approval to launch financial product and service testing under the Commission’s Strategic Regulatory Sandbox (Stratbox) framework.

SEC approves sandbox rollout

Under the approval, BlockShoals will operate using a crypto-asset intermediary model that allows users in the Philippines to access selected products and services through its global crypto-asset service provider partner, Binance.

The SEC document stated that BlockShoals must first complete system integration with a local virtual asset service provider during an initial 90-day phase before proceeding with the approved testing program.

Once that integration is completed, the testing plan will move forward under regulatory oversight and applicable safeguards, including user registration and onboarding through Binance as its global CASP partner, according to the SEC approval.

The final approval follows the SEC’s earlier clearance of BlockShoals’ Stratbox application in November 2025, after the company fulfilled the remaining regulatory requirements set by the Commission.

BSP licensing question remains

The latest SEC approval comes weeks after the Bangko Sentral ng Pilipinas clarified that neither Binance nor BlockShoals currently holds a Virtual Asset Service Provider license required for certain crypto payment and transaction services.

As previously reported by crypto.news, the BSP said participation in the SEC’s Stratbox program does not replace the need for a separate central bank license because the two regulators oversee different parts of the country’s financial sector. The central bank also noted that BlockShoals would need to integrate with a licensed domestic VASP before onboarding users through Binance’s infrastructure could begin.

While Yi He described the development as Binance’s official entry into the Philippines, the SEC approval itself authorizes BlockShoals to begin sandbox testing and identifies Binance as its global CASP partner. The document does not state that Binance has obtained a Philippine VASP license.

Binance has been working to strengthen its regulatory position in several jurisdictions. On July 1, the exchange told affected European Union users that withdrawals and other account options would remain available as MiCA-related service changes took effect, while it continued pursuing authorization to operate under the bloc’s new crypto rules.

Bitcoin price has rebounded above $60,000 after easing oil prices and softer U.S. macro expectations lifted risk appetite, though persistent ETF outflows continue to threaten the recovery.

Summary

- Bitcoin price has reclaimed $60,000 as easing oil prices and improving macro sentiment triggered a relief rally.

- Persistent U.S. spot Bitcoin ETF outflows continue to weigh on institutional demand despite the rebound.

- Technical charts show room for further gains above $61,000, but failure to hold $60,000 could revive selling pressure.

According to data from crypto.news, Bitcoin (BTC) price climbed from a low near $58,300 to around $60,600 over the past 24 hours as investors responded to softer inflation expectations and improving sentiment across global markets.

Risk assets also benefited from progress in indirect U.S.-Iran talks, while Brent crude slipped below $71 a barrel after oil shipments through the Strait of Hormuz accelerated and concerns over supply disruptions eased. Lower energy prices reduced inflation worries, giving cryptocurrencies room to recover after June’s sharp sell-off.

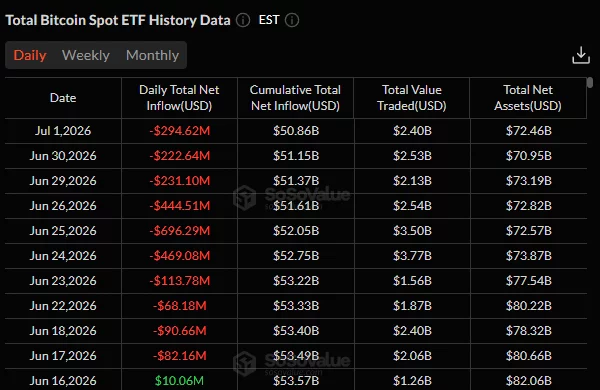

The rebound comes after one of Bitcoin’s weakest months in recent years. U.S. spot Bitcoin ETFs recorded another $294.6 million in net outflows on July 1 after losing $222.6 million, $231.1 million and $444.5 million during the previous three sessions, extending a streak of institutional withdrawals that has removed billions of dollars from the sector in recent weeks. Those redemptions have continued to offset improving macro sentiment by forcing ETF issuers to sell underlying Bitcoin into the market.

Federal Reserve policy also remains a key obstacle. Although traders welcomed recent dovish remarks, interest rates remain elevated, and expectations for policy easing have been pushed further into the future. Higher Treasury yields continue to compete with non-yielding assets such as Bitcoin, while institutional capital has increasingly flowed toward U.S. technology and artificial intelligence stocks instead of digital assets.

Bitcoin must reclaim $62.7K and $65K to strengthen the recovery

Bitcoin’s 1-day chart shows price rebounding from the 100% Fibonacci retracement near $57,826 after briefly testing the lower boundary of a multi-month decline. The recovery has lifted RSI from deeply oversold territory to around 40, suggesting selling pressure has eased without yet confirming a trend reversal.

Even after reclaiming $60,000, Bitcoin continues to trade below all key moving averages clustered between roughly $62,400 and $75,100, leaving major resistance overhead.

The 4-hour chart paints a more constructive short-term picture. Bitcoin has reclaimed the Supertrend support near $57,700 while the Aroon Up reading has climbed above 78%, with Aroon Down slipping below 43%, suggesting buyers have regained short-term control after the late-June washout.

Bitcoin price has also returned above psychological support at $60,000, though sustained buying will still be needed to challenge resistance around $61,000 before the larger moving-average cluster comes into view.

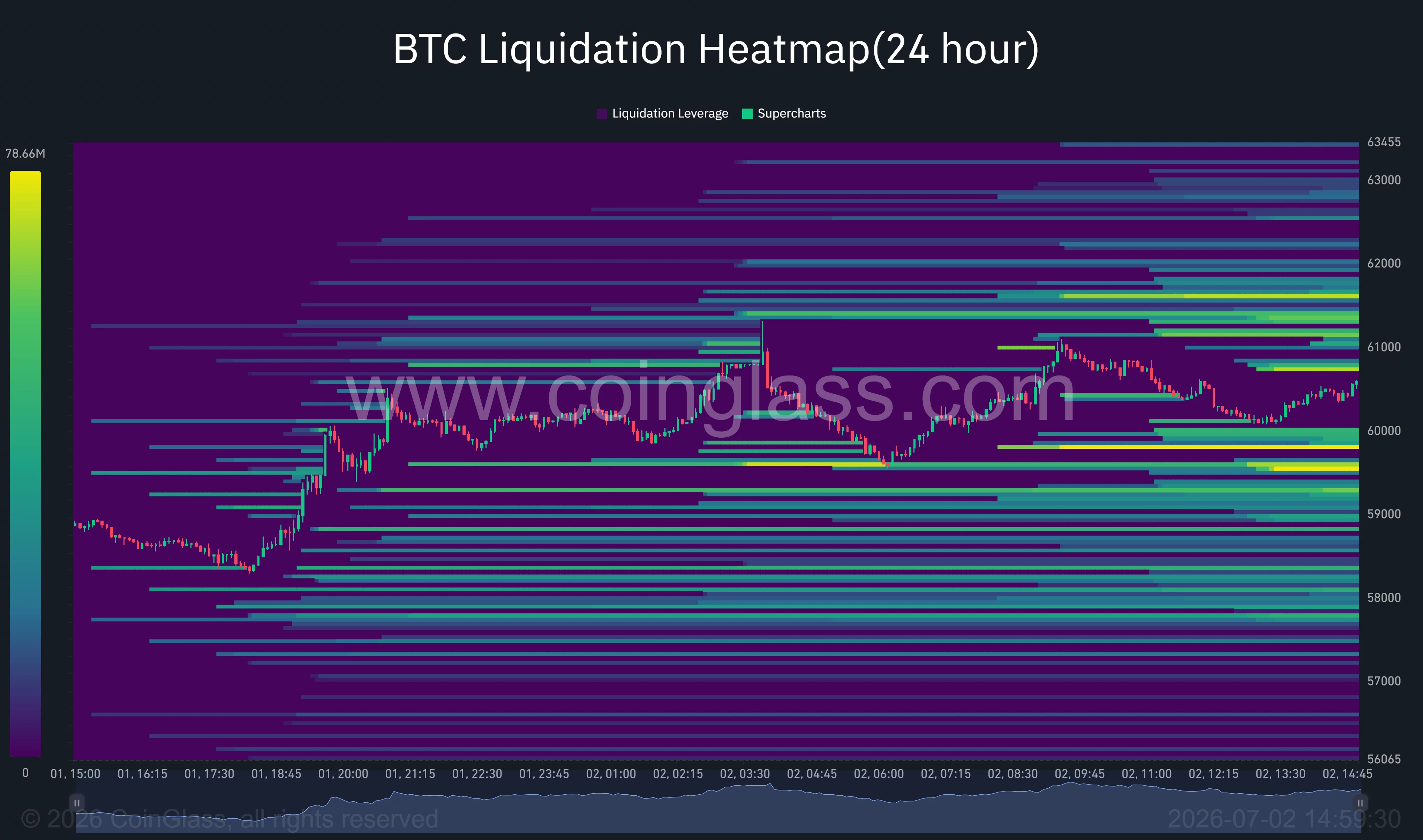

Derivatives positioning shows traders remain heavily focused on nearby liquidation levels. CoinGlass’ 24-hour heatmap highlights dense short liquidation clusters between $61,000 and $61,800, suggesting a move through that range could accelerate buying as bearish positions are forced to close. On the downside, equally large long liquidation pockets sit around $59,500 and $58,000, creating potential downside magnets if Bitcoin loses its recent gains.

According to analyst Ted Pillows, the latest advance should still be treated cautiously.

“This is just a relief rally, which often happens after a 30% crash. Bitcoin’s key levels are $62,700 and $65,000, which must be reclaimed for another lower high before a new cycle low.”

Commenting on the shorter-term setup, analyst Altcoin Sherpa noted that Bitcoin looks constructive on lower time frames while price remains above current support, although he added that he would not feel confident until Bitcoin decisively breaks above $65,000 on higher-time-frame charts.

ETF selling and macro risks could quickly reverse the recovery

Several downside risks continue to threaten Bitcoin’s rebound. Continued spot ETF redemptions remain the most immediate concern, particularly if institutional demand fails to return after June’s record wave of outflows. Corporate developments have also weighed on sentiment after Strategy revised its capital policy to permit token sales, raising concerns that one of Bitcoin’s largest corporate holders could eventually add supply to the market.

Macro and geopolitical uncertainty also remain unresolved. While oil prices have retreated on improving U.S.-Iran negotiations, any disruption to talks or renewed tensions around the Strait of Hormuz could quickly push energy prices higher and revive inflation concerns.

On the technical side, failure to defend the $60,000 area would expose the $59,500 and $58,000 liquidation zones, while a break below June’s low near $57,800 would invalidate the current relief rally and reopen the path toward fresh cycle lows.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

The International Monetary Fund has said tokenization could change how financial markets settle trades, manage payments, and record ownership.

Summary

- Tokenization can speed settlement, but weak standards may split liquidity across competing financial platforms worldwide.

- Major banks are testing tokenized deposits as regulated rails for faster institutional payment settlement systems.

- Regulators must define ownership, code oversight, and settlement finality before tokenized markets scale globally.

In a July 2 blog post, Tobias Adrian, the IMF’s financial counselor and director of the Monetary and Capital Markets Department, said policy choices made now will decide whether tokenized finance “strengthens or fragments” the financial system.

Adrian said tokenization is more than a tool for faster payments. It moves assets and liabilities onto shared digital ledgers, where execution, clearing, and settlement can happen at the same time. That could reduce delays in markets that still depend on separate systems, manual checks, and later reconciliation after trades close.

Faster markets bring new risks

The IMF said tokenization can make settlement faster and payments cheaper, but it can also change where risk sits. In traditional markets, delays give banks, brokers, and supervisors time to respond to errors or stress. In tokenized markets, smart contracts can move payments, collateral, and ownership within moments.

That speed can remove old buffers. Automated margin calls, instant redemptions, and 24/7 settlement could make liquidity needs appear faster than firms can manage them. Adrian warned that risk could move away from bank balance sheets and toward the platforms, code, and service providers that run tokenized markets.

Banks test tokenized settlement rails

The warning comes as large financial firms move tokenization deeper into regulated finance. As crypto.news reported, major U.S. banks are backing a tokenized deposit network through the Clearing House, with a launch targeted for the first half of 2027. The system would allow banks to settle tokenized deposits around the clock while keeping deposits inside the banking sector.

Recent market activity also shows that tokenization is spreading into securities. As previously reported, Securitize tokenized its own NYSE-listed shares on Solana and Avalanche on the day it began public trading. Ondo Finance also brought BlackRock’s IVV ETF and Micron shares onto Ethereum through a model designed to keep the underlying securities inside regulated U.S. custody.

Regulators weigh ownership and code oversight

The IMF said tokenized finance needs clear rules on settlement assets, platform governance, interoperability, and the role of central banks. It also said legal clarity matters because investors must know whether tokenized records prove ownership, whether settlement is final, and which court has authority when markets cross borders.

In the United States, regulators are already reviewing tokenized securities. As crypto.news reported, the SEC has explored an innovation exemption for tokenized securities that could let some blockchain-based products trade under tailored rules. Later, the agency reportedly delayed the proposal after exchanges raised questions about shareholder rights and ownership verification.

The IMF’s message adds a global policy layer to that debate. Faster settlement may improve market systems, but weak standards could split liquidity across competing platforms. If tokenized assets move across borders in real time, supervisors may also have less time to respond during stress.

Adrian said central banks, regulators, and market operators must decide how tokenized finance should use public and private money. They must also decide how platforms should connect and how critical smart contracts should be supervised. Without common rules, tokenization may stay split across separate systems instead of becoming a safer settlement model for global finance.

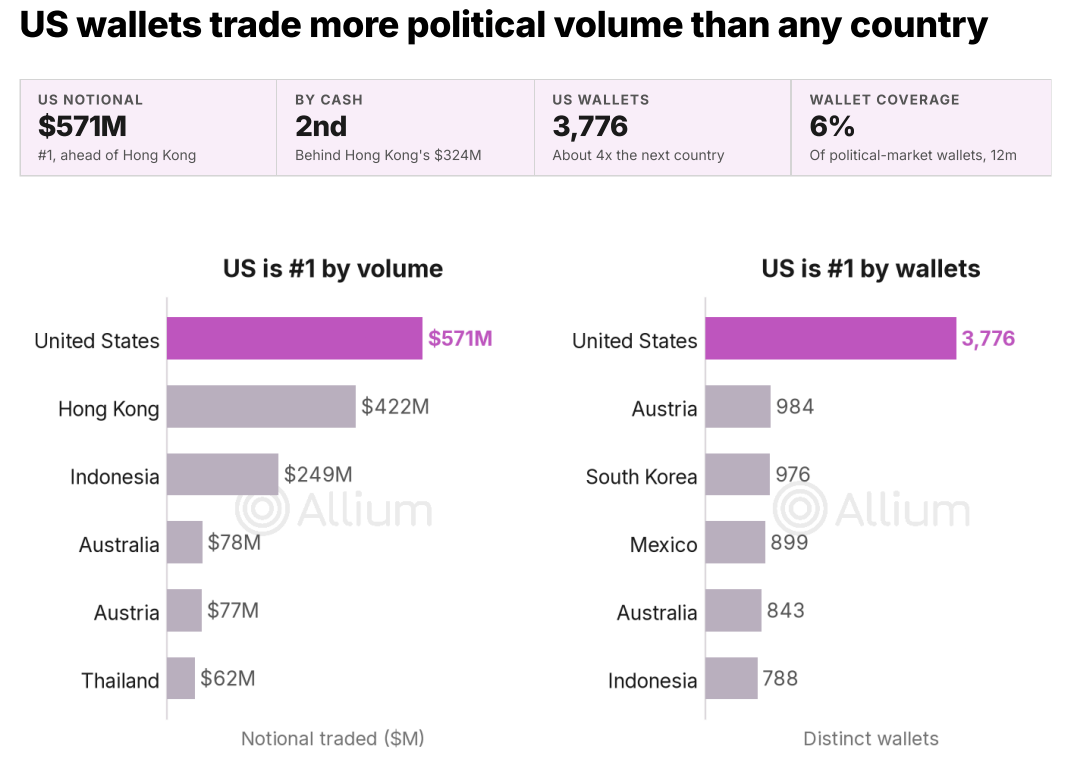

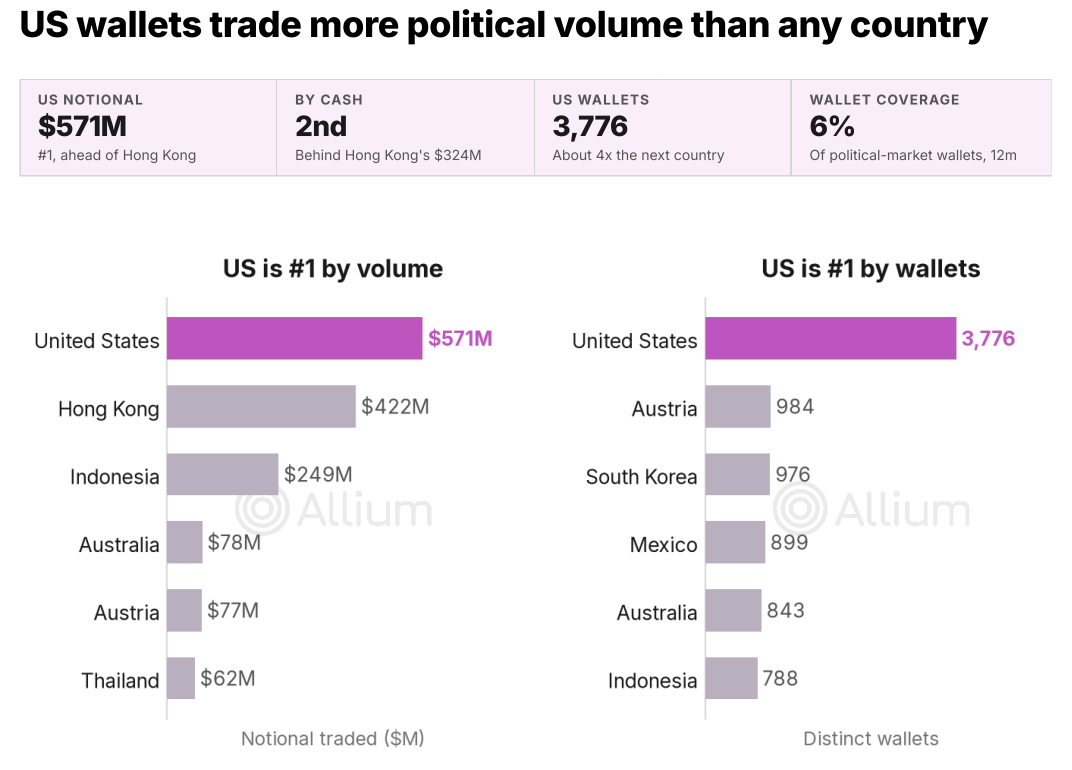

US-based users are the biggest political bettors on Polymarket, despite the crypto-based prediction market’s efforts to restrict US citizens from using the decentralized platform, according to new research.

Blockchain research firm Allium estimated in a report published on Thursday that US-based users are the single biggest political market of any country by contracts traded and wallet count on Polymarket — not to be confused with Polymarket US, which is a US-regulated platform that launched in December with a narrower set of markets.

“Blocking access did not end US participation; it made the US the largest single political market on Polymarket by volume,” the report said. “The demand is still there, now offshore and beyond US oversight.”

The data suggests that Polymarket’s efforts to restrict US users from its global platform have not entirely worked, adding to an expanding list of headaches for the company in the fast-growing predictions market sector, which is under legal and political scrutiny.

Polymarket was forced to cut off US users’ access to its global platform as part of a $1.4 million settlement with the Commodity Futures Trading Commission in 2022.

Allium based its figures on the 6% of wallets it tagged with a country, meaning the data should be seen as directional only. Source: Allium

Allium found that US users are more interested in foreign conflict-related markets than the rest of the platform’s users, with five of the US cohort’s top 12 markets by notional volume relating to the Iran war.

It also shows a lesser interest in election-related markets, which is a category of prediction markets allowed on Kalshi and Polymarket US.

“US money pours into foreign wars, lately Iran, and largely skips the elections the global crowd trades,” said Allium.

Cointelegraph contacted Polymarket for comment.

Polymarket’s effort to geoblock US users

Allium’s figures align with another study published in June by Rutgers University statistician Harry Crane, who estimated that 30% of trading volume on Polymarket comes from the US.

Crane estimated that people based in the US sent between $10.6 billion and $26.7 billion through Polymarket between May 2025 and April 2026, despite Polymarket blocking US-based IP addresses and VPNs, which could be used to skirt the block.

The researcher looked at the times of day the trades were made and the markets in which the trades were made to link certain trades to US users.

An excerpt of Polymarket’s FAQ page on its geographic restrictions. Source: Polymarket

Polymarket has reportedly been clamping down on users who use VPNs by blocking certain IP addresses tied to VPN services, The Information reported in May.

Related: Polymarket hit by $2.9M theft, users to be refunded

Where is Polymarket blocked?

Polymarket is completely blocked in more than 34 countries, the latest being Spain, which blocked local users from Polymarket and Kalshi as a “precautionary measure” as authorities open an investigation into whether the companies are operating without necessary licensing.

Another four countries, including Singapore, Thailand, Taiwan and Poland, are in “close only,” meaning users in these countries can close existing positions but cannot open new trades.

There are also four restricted regions, Ontario in Canada, Crimea, Donetsk and Luhansk in Ukraine, where Polymarket is blocked but is available elsewhere in the country.

Magazine: Bitcoin slides to $58K, XRP hits $1 but onchain data promising: Market Moves

Securitize became a publicly traded company on the New York Stock Exchange Thursday, July 2, immediately tokenizing its common stock on Solana (SOL).

The move lands alongside a separate governance shift on Solana, where validators gained a formal, stake-weighted voting process for protocol decisions. Both moves come as SOL posted strong gains, up 19.3% over the past week.

Securitize Brings Its NYSE Debut Onchain

Securitize completed its merger with Cantor Equity Partners II and opened trading on the NYSE under the ticker SECZ on Thursday. This is part of its broader tokenized asset expansion across multiple chains.

“We have long said that public equities are moving onchain”

— Carlos Domingo, Founder and CEO of Securitize

Blockchain data from RWA.xyz tracked roughly $295 million in tokenized SECZ shares at launch. Securitize said the tokens represent the same shares trading on the NYSE, not a synthetic wrapper.

Additionally, access is limited to eligible U.S. investors who pass identity checks.

Validators Gain a Formal Vote

Separately, the Solana Foundation activated Solana Governance Proposals on July 1. Ultimately letting validators with at least 100,000 staked SOL submit proposals.

The framework separates broad directional questions from the technical upgrades developers already handle. Furthermore, it lets individual delegators override their validator’s vote.

Together, the two developments show Solana courting institutional issuers and their own validator bases at once. Whether tokenized SECZ shares draw meaningful onchain trading volume will shape how far this new strategy goes.

The post Solana Gets NYSE Boost as SOL Jumps 19% on Securitize Listing appeared first on BeInCrypto.

Michael Burry disclosed a fresh basket of shorts against Tesla, Nvidia, Caterpillar, Applied Materials, and the semiconductor sector on June 30. Within days, several of those same corners of the market started cracking.

The Setup: Burry’s Basket Built on One Thesis

Burry laid out his positions in a Substack post titled “Trading Post June 30, 2026.” He framed them as a single bet against an overheated AI cycle, not isolated stock picks. He called the semiconductor index “a pure form of overvaluation” and rolled his SOXX puts out to March 2027.

He also disclosed new shorts on Tesla at $416.22 and Caterpillar at $1,060.98, a stock he had never shorted before despite trading it profitably on the long side for years.

The Philadelphia Semiconductor Index was already trading more than 65% above its 200-day moving average when Burry made his call. He compared the stretch to conditions last seen during the dot-com era.

What’s Happened Since

Days later, reports surfaced that Meta is building a business called Meta Compute to lease out its surplus AI data center capacity to outside customers. Investors read the move as a signal that compute supply may be catching up with demand.

On Thursday, July 2, the Philadelphia Semiconductor Index dropped more than 6%, its steepest single-day fall in recent memory. The selloff spread to Samsung and SK Hynix in Asia and briefly triggered a circuit breaker on South Korea’s Kospi.

Memory and storage names took the hardest hits. SanDisk sank almost 20% in the past five session. Seagate and Micron also slid on fears of a supply glut as Samsung and SK Hynix ramp up new capacity. Micron’s fundamentals remain strong, with fiscal third-quarter revenue up 346% year over year. Even so, the stock has given back a chunk of its 2026 gains.

Tesla fell 7.5% that same Thursday, its worst single session in nearly a year. The drop came despite Tesla reporting Q2 deliveries of 480,126 vehicles, well above Wall Street’s consensus estimate. Traders treated the beat as a sell-the-news event. The stock had already run up more than 13% over the four sessions before the report.

A Coincidence Worth Watching, Not Yet a Verdict

None of this proves Burry’s short basket caused the moves. The chip selloff traces to Meta’s compute-leasing plans. Tesla’s drop lines up with a classic sell-the-news pattern around its delivery report, not any catalyst tied to Burry directly.

Still, the timing is notable. Burry’s basket touched nearly every name now under pressure. Caterpillar, his other first-ever short, still trades at a trailing price-to-earnings ratio of 53.

Whether this marks the start of the correction Burry is positioning for, or just a rough week for a handful of stretched valuations, should become clearer as Tesla’s July 22 earnings and the next round of AI capex commentary land.

The post Burry Called a Bubble Days Ago and Now AI & EV Stocks Are Already Cracking appeared first on BeInCrypto.

The AI model its own maker says can find and exploit software flaws better than almost any human is back online. It arrives in the middle of crypto’s worst year for hacks. Here is what actually changes, and what the panic gets wrong.

Summary

- On July 1, 2026, Anthropic restored global access to Claude Fable 5 after the U.S. lifted export controls, while the less-restricted Mythos 5 returned only to a set of vetted U.S. organizations through a program called Glasswing.

- Anthropic markets Mythos-class models as able to find and exploit software vulnerabilities more effectively than any other model and than all but the most skilled human experts, and says the models surfaced more than 10,000 high-severity flaws in important software.

- The alarm in crypto is that cheap, fast, AI-driven vulnerability discovery turns unaudited protocols and small forks into easy targets, in a year when hacks have already drained more than $840 million.

- The skeptical view, shared by some security experts and by Anthropic’s own review, is that the models mostly accelerate known attack types, social engineering, exposed keys, and misconfigurations, instead of inventing new ones, and that weaker models can do much of the same work.

- The same capability that helps attackers also helps defenders, through faster audits and patching, which is why the near-term risk is real while the long-run balance is contested.

The model built to find software flaws is back, and it landed in the worst possible year for the industry with the most to lose. On July 1, 2026, Anthropic restored access to Claude Fable 5 worldwide after the U.S. Department of Commerce lifted the export controls that had forced the model offline in June, while its more powerful sibling, Mythos 5, returned only to a set of vetted organizations. The timing is what makes it a crypto story. Anthropic describes Mythos-class models as able to find and exploit vulnerabilities better than nearly any human, and crypto is in the middle of a record run of hacks, with billions in assets sitting inside publicly visible code that an AI can read at machine speed.

This piece separates what these models actually change from what the panic gets wrong, and it does so without treating a single headline as the whole picture. The central question is not whether AI makes crypto security riskier; it does. The harder question is where the added risk actually sits, whether it is in smart contracts themselves, bridges, human operations, signing flows, or the speed at which attackers can now move from disclosure to exploit. The answer is less cinematic than the fear, but more useful for anyone holding funds or building protocols.

What came back, and what did not

The distinction between the two models is the first thing to get right, because they are not equally available. Fable 5 is the public, safeguarded member of the Mythos class, released in June 2026 and priced at roughly twice the cost of Anthropic’s prior flagship. It returned to global users on July 1 across Anthropic’s platforms. Mythos 5 is the less-restricted version that carries the full cyber capability, and it did not return to the public.

Anthropic restored Mythos 5 only to a set of vetted U.S. organizations that operate and defend critical infrastructure, through an opt-in program called Glasswing, following government approval in late June. So the model most crypto observers worry about is not the one now sitting behind a consumer subscription. The distinction matters because public access changes the risk surface very differently from vetted critical-infrastructure access. A powerful model in the hands of security teams is not the same thing as a powerful model available to every attacker with a credit card.

The episode that pulled both offline is worth understanding, because it colors the risk debate. In June, researchers at Amazon showed a jailbreak that got Fable 5 to identify software vulnerabilities and write exploit code, and the U.S. government responded with an emergency export-control order that Anthropic complied with by disabling the models entirely, since it could not restrict access by nationality in real time. The controls were lifted at the end of June, and access returned in the first days of July, with Fable 5 global and Mythos 5 limited. Anthropic’s own account of the incident cuts against the loudest fears: its review, conducted with the government, found that the reported technique did not reveal a uniquely Mythos-level capability, and that several weaker models could reproduce the same vulnerabilities.

The company argued the capability had been oversold, and it deployed a new safety classifier it says blocks the specific technique in more than 99% of cases, routing risky cybersecurity prompts to a weaker model in fewer than 5% of sessions. That is the company’s framing, and it matters, but it is not the whole story either. The point for crypto is narrower: even if public access is constrained, the capability exists, it is improving, and weaker models already reproduce parts of it. That means the security problem cannot be solved by focusing on one model alone.

What Mythos-class models can actually do

The capabilities that alarmed the security world are real and documented, not hypothetical. Under its restricted program, Mythos-class models reportedly surfaced more than 10,000 high and critical-severity vulnerabilities in systemically important software, and found critical flaws across more than 1,000 open-source projects, including widely used components such as the Linux kernel and a popular media library. In one cited case, the model generated a working proof-of-concept exploit for a complex issue in under 31 minutes. Cloudflare reported that an earlier Mythos preview chained bugs into working exploits across more than 50 of its code repositories before refusing to produce a live demonstration.

The capability that most changes the math for defenders is speed. Anthropic has warned that the window between a vulnerability being disclosed and being exploited is collapsing, in some cases from days to hours. Its researchers concluded that a single operator with this class of model could turn a month of software patches into working exploits in a single afternoon, for a cost measured in a few thousand dollars. Security practitioners have started describing the shift as moving from an era of N-days, where attackers had weeks or months after a disclosure, to something closer to N-hours.

When a patch ships, it also reveals the flaw it fixes, and a model that can read the patch, understand the bug, and build an exploit in hours compresses the defender’s response window dramatically. None of this is the same as inventing a new class of attack. It is acceleration and scale. The model reads public code, compares versions, summarizes audits, and reasons about weaknesses faster and cheaper than a human team, which lowers the cost and expertise needed to do work that skilled attackers already do.

That distinction, acceleration rather than invention, is the fault line the entire debate runs along. For crypto teams, the practical implication is brutal: slow patching, stale dependencies, and unaudited forks become more dangerous when attackers can automate the boring parts of vulnerability discovery. The frontier model does not need to be magical to change the economics. It only needs to make the existing attack pipeline cheaper and faster.

Why crypto is uniquely exposed

Crypto sits in the blast radius for reasons specific to how it works. Smart contracts are public by design: the code that controls billions of dollars is visible on-chain for anyone, including an AI, to read and analyze. Bridges, the infrastructure that moves assets between blockchains, concentrate the collateral of many chains into a single set of contracts and message-verification systems, which makes them the highest-value targets in the space. An attacker who can scan code at machine speed has an unusually rich, unusually open field in crypto compared with closed corporate systems.

The backdrop is a genuinely bad year. Crypto has lost more than $840 million to hacks in 2026, with some tallies putting the figure past $940 million across more than 120 incidents, and April alone set a record near $600 million. The two largest losses tell the story of where the damage comes from. Kelp DAO lost roughly $292 million when attackers forged a cross-chain message on its bridge, exploiting a setup that let a single compromised node approve fraudulent withdrawals.

Drift Protocol lost about $285 million not to a code bug but to a six-month social engineering operation that ended in compromised administrative keys. Bridges have accounted for the largest share of losses, and North Korean groups have been linked to a large portion of the total. That pattern is the key context for the AI debate, because it shows where crypto actually bleeds. The biggest 2026 losses came less from novel smart-contract bugs than from human error and operational failure: social engineering, exposed keys, flawed signing flows, and misconfigured infrastructure.

Any assessment of what a Mythos-class model changes has to start from that reality, not from the image of an AI writing an exotic new exploit from scratch. The crypto risk surface is not only code. It is bridges, multisigs, admin keys, custody practices, signing devices, deployment scripts, and teams that still operate under startup-style security despite controlling institutional-scale money. AI makes that whole surface easier to search.

The alarm case

The bearish read is straightforward and has serious voices behind it. Simon Dedic, a well-known crypto investor, warned that a public Mythos-class model could sharply lower the cost and expertise needed to find exploitable flaws in smart contracts, and that unaudited protocols would become, in his words, sitting ducks. The argument is about barriers. Finding a subtle vulnerability in a contract used to require rare skill and considerable time.

If a model compresses that to hours and pennies, the population of people capable of attacking a weak protocol expands enormously, and the long tail of small projects, forks, and unaudited contracts becomes far more exposed. The numbers give the argument weight. Analysts have linked part of 2026’s elevated hacking losses to the growing use of advanced AI in identifying vulnerabilities, and the trend line points toward more automated, faster reconnaissance. In this view, even if the very best human attackers gain little, the marginal attacker gains a great deal, and crypto has no shortage of marginal attackers or of weak targets for them to point a capable model at.

The alarm is less about the top of the skill curve and more about how many more people can now operate near it. That is why small DeFi forks, rushed launches, and unaudited protocols are the obvious danger zone. A well-resourced protocol with continuous audits and strong operational controls may use AI defensively. A copy-paste fork with weak key management may simply become easier to attack.

The skeptics’ case

The counterargument is equally serious, and it comes from builders and from Anthropic itself. Michael Egorov, the founder of a major decentralized exchange, argued that smart contracts typically contain only a few thousand lines of code and are already well understood by human auditors and existing AI tools, so a more capable model changes less about direct contract exploits than the panic suggests. In his view, operational security failures and supply-chain attacks are the larger risk, and those are not primarily a smart-contract-analysis problem. That view fits the loss data, where administrative compromises and bridge failures dominate the largest incidents.

Anthropic’s post-incident review reinforces the skeptical case from an unexpected direction. The company found that the jailbreak technique that triggered the export controls did not reveal a uniquely Mythos-level capability, and that weaker models, its own and others, could reproduce the same vulnerability findings. If a capability is broadly available across many models rather than locked inside one frontier system, then restricting or releasing that single system changes less than it appears to. The skeptics do not claim the models are harmless; they claim the marginal danger of any one release is smaller than the headlines imply, because the underlying capability is diffuse and because the hardest part of most real attacks is not finding the flaw.

That is an important distinction for crypto readers. The risk is not “Claude Mythos appears, therefore every DeFi protocol is suddenly doomed.” The risk is that AI-assisted security analysis is becoming normal across many models, countries, and toolchains, which means attackers and defenders alike will have faster vulnerability discovery available. In that world, the question shifts from whether one model should be online to whether crypto teams can patch and harden faster than adversaries can scan and exploit.

The part everyone agrees on

Between the alarm and the skepticism sits a consensus, and it is the most useful part of the debate. Security experts broadly agree that advanced AI will not invent fundamentally new categories of crypto hack, but will dramatically speed up the attacks that already dominate the loss tables: social engineering, exposed keys, and flawed signing flows. A model does not need to hand over a finished exploit to change the economics of an attack. It can read public repositories, compare old and new versions of software, summarize audit reports, and draft convincing messages designed to catch the small operational mistakes humans make.

As one analysis put it, these exploits remain rooted in social engineering and human error; AI did not create that reality, it made it visible and accelerated it to machine speed. That reframing points straight at the 2026 loss data. The Drift and Kelp attacks, the two largest of the year, were an operational compromise and a bridge-verification failure, not clever new contract bugs. A model that accelerates reconnaissance, scans for the weakest key path or the sloppiest signing flow, and helps craft the human-facing part of an attack makes exactly those failure modes cheaper and faster to exploit.

The practical implication is that the defense that matters most is not writing unbreakable contracts, but hardening the human and operational layer where the money actually leaks. That means keys, signing steps, privileged accounts, dependencies, cross-chain message verification, and incident response. It also means treating every public disclosure and every patch as a race. In an N-hour world, yesterday’s slow security process becomes tomorrow’s exploit window.

The defensive flip side

The same capability that worries defenders can also serve them, which is why the long-run balance is genuinely contested. A model that finds vulnerabilities faster than humans is, pointed the other way, an audit tool that finds them before attackers do. Anthropic has argued that AI will eventually favor defenders in cybersecurity, while conceding that the transition will be turbulent, and it restored the restricted Mythos 5 specifically to organizations that defend critical infrastructure through its security program. That is the defensive version of Glasswing: put the best tools in the hands of teams whose job is to patch before adversaries exploit.

One incident has become the reference point for both sides. In early June 2026, a critical vulnerability in a privacy coin’s shielded pool was discovered using Anthropic’s Opus 4.8, a model a generation below the Mythos class. The flaw, if exploited, could have allowed unlimited minting of the token, and it had eluded expert cryptographers for roughly four years. The token dropped more than 35% on the disclosure.

The lesson cuts both ways: a weaker model catching a four-year-old flaw shows how much AI can strengthen defense, and also how much latent, undiscovered risk sits in code that a stronger model could surface, for good or ill. Faster discovery is a defensive gift when a friendly party finds the bug first and a catastrophe when an attacker does. Which side wins any given race depends on who is scanning, how fast teams can patch, and whether defenders adopt the tools as aggressively as attackers will.

What crypto users and teams can actually do

The useful response to all of this is not panic but hardening, and most of it is advice that held before any model returned. For individual users, the recurring guidance from security researchers is concrete: revoke unused token approvals, since every outstanding approval grants a contract permission to move your funds, and tools exist to review and cancel them. Move significant holdings into self-custody and cold storage, so that the keys controlling real money sit somewhere a compromised laptop cannot reach, and treat any unaudited protocol as a higher risk than it looked a year ago. When approving a transaction, use a device with a trusted screen that shows what is actually being signed, because if AI accelerates the scouting phase, the final signing step becomes the moment that matters most.

For teams and protocols, the priorities follow from where the losses come from. Rapid patch management matters more in an N-hour world, because the window between a disclosure and a working exploit is shrinking, so shipping and applying fixes quickly is now a security control in itself. Continuous auditing beats one-time audits, and using AI-driven analysis on your own code before attackers do is increasingly a baseline instead of an edge. Above all, harden the operational layer: secure key management, tighten signing flows, limit privileged access, and scrutinize dependencies and cross-chain message verification, because that is where the year’s biggest breaches actually happened.

Over-reliance on any single external model carries its own risk, so teams are stress-testing multiple tools instead of betting on one. The same caution applies to exchanges and custodians, where exchange security is not just a proof-of-reserves page but a question of controls, custody, liabilities, and operational discipline. For protocols experimenting with AI agents in crypto, the lesson is even sharper: automation expands what software can do, but also expands what must be secured. The more autonomy a system has, the more dangerous weak permissions and signing flows become.

The honest conclusion is that the return of these models changes the tempo of an existing problem more than it introduces a new one. Crypto was already losing record sums to human error, operational failure, and bridge design long before Fable 5 came back online. Capable AI makes the reconnaissance faster, the attacks cheaper, and the response window shorter, which is a real near-term headwind for a chronically insecure industry. It also puts a powerful audit tool in defenders’ hands, which is the reason the long-run outcome is a race instead of a verdict.

The protocols and users who treat the moment as a prompt to fix the operational basics will be the ones best placed whichever way that race runs. The ones still relying on one-time audits, permissive approvals, weak admin keys, and slow patch cycles are the obvious targets. AI did not create those weaknesses. It just made them easier to find.

Frequently asked questions

What is Claude Mythos 5?

Claude Mythos 5 is a frontier AI model from Anthropic that the company describes as its most capable for cybersecurity, marketed as able to find and exploit software vulnerabilities more effectively than any other model and than all but the most skilled human experts. It is the less-restricted version of the Mythos class. Its safeguarded public sibling is called Fable 5. Mythos 5 is available only to vetted organizations, not the general public.

Why did the models go offline and come back?

In June 2026, researchers showed a jailbreak that got Fable 5 to identify vulnerabilities and write exploit code, and the U.S. government issued an emergency export-control order. Anthropic disabled both models globally because it could not restrict access by nationality in real time. The controls were lifted at the end of June, and access returned in early July, with Fable 5 restored globally and Mythos 5 limited to vetted U.S. organizations. The important distinction is that the public model and the restricted cyber model did not come back under the same access rules.

Can these AI models really hack crypto protocols?

They can accelerate the work attackers already do rather than invent new attacks. Mythos-class models reportedly found more than 10,000 high-severity flaws in important software and can build a proof-of-concept exploit in under an hour. In crypto, the larger effect is speeding up reconnaissance and the human-facing parts of attacks, since the biggest 2026 losses came from social engineering, exposed keys, and operational failures instead of novel contract bugs. That makes unaudited protocols, weak bridge setups, and poor key management especially exposed.

How much has crypto lost to hacks in 2026?

Crypto has lost more than $840 million to hacks in 2026, with some tallies exceeding $940 million across more than 120 incidents, and April alone set a record near $600 million. The two largest losses were Kelp DAO at about $292 million from a bridge message forgery and Drift Protocol at about $285 million from a social engineering operation that compromised administrative keys. Those examples matter because they show where the real losses are coming from: not only code flaws, but operational and verification failures. AI makes those weak points easier to find and exploit faster.

Does AI make crypto hacks fundamentally worse?

The consensus among many security experts is that AI accelerates and scales existing attack types instead of creating new ones. It lowers the cost and expertise needed to find flaws, which most exposes unaudited protocols and small projects. Skeptics, including some builders and Anthropic’s own review, argue the marginal danger of any single model is smaller than headlines suggest, since weaker models can do similar work and the hardest part of most attacks is not finding the flaw. The risk is therefore less about one model suddenly changing everything and more about AI-assisted hacking becoming broadly available.

Can AI also help defend crypto?

Yes, and that is the contested part of the debate. The same ability to find vulnerabilities fast makes AI a powerful audit tool when defenders use it first. In one case, a weaker model discovered a four-year-old critical flaw in a privacy coin’s shielded pool before it was exploited. Anthropic argues AI will eventually favor defenders, while admitting the transition will be turbulent, so the outcome depends on who adopts the tools faster.

What should crypto holders do to protect themselves?

Security researchers recommend revoking unused token approvals, moving significant holdings into self-custody and cold storage where keys sit offline, and treating unaudited protocols as higher risk. When signing transactions, use a device with a trusted screen that shows exactly what is being approved. These steps address the human and operational failures that account for most real losses, which AI mainly accelerates instead of replacing. The goal is to reduce the number of places where an attacker can turn a mistake into a transfer.

Is Mythos 5 available to the public now?

No. After the export controls were lifted, Anthropic restored the safeguarded Fable 5 to global users, but the less-restricted Mythos 5 returned only to a set of vetted U.S. organizations that defend critical infrastructure, through an opt-in program. The company says it will work to expand access over time, but the model with the full cyber capability is not behind a consumer subscription. Public users may have access to stronger AI tools than before, but not to the same unrestricted Mythos 5 setup described in the security program.

Disclaimer: This article is for information and educational purposes only and does not constitute financial, investment, legal, or security advice. It describes an evolving situation involving AI capabilities and cybersecurity risk, and details may change. Nothing here is a recommendation to buy, sell, or use any specific model, asset, or service. Always do your own research and consult qualified professionals for security decisions. Information is accurate as of July 2, 2026, and may change.

Bitcoin (BTC) dominance currently trades at 58.55% and tests the floor of a range that has held since August 2025. A confirmed breakdown would target 55.5%, the level many traders link to the start of a broad altcoin rotation.

The Crypto Fear and Greed Index sits predominantly in Extreme Fear recently, while the Altcoin Season Index remains neutral at 45. BeInCrypto reviews the weekly and daily BTC.D charts to assess whether the long-awaited altcoin season is finally near.

Bitcoin Dominance Breaks Its Multi-Year Uptrend

The weekly chart shows a long-term ascending parallel channel that dates back to late 2022. Bitcoin dominance broke down from this structure in August 2025, ending a multi-year uptrend. The breakdown initiated a sideways period that lasted until April 2026.

In May 2026, the metric rallied back to resistance near 61% and faced a firm rejection. BeInCrypto flagged this area when dominance first broke above 60% in April. BTC.D now trades back inside the former range, below the 0.236 Fibonacci retracement at 59.63%.

The Fibonacci ladder points to downside targets at 55.66%, 52.44%, and 49.23%. A popular trader on X shared a similar roadmap, calling 55% the trigger level for altcoin moves and 46.74% his final target. His last level sits lower because he anchors the retracement differently.

Daily Chart Points to a 55.5% Breakdown Target

Zooming in, the daily chart reveals a horizontal parallel channel between roughly 58% and 60.75% that also goes back to August 2025. Dominance now sits on the channel floor and tests a potential bearish breakdown.

Moreover, an ascending trendline from the September 2025 low broke down in June 2026. BTC.D retested the line as resistance in late June and turned lower. The failed retest adds a third bearish signal and pressures the relative position of altcoins, which have trailed Bitcoin since 2020.

If the channel gives way, the measured target sits near 55.5%. This projection converges with the weekly 0.382 Fibonacci support at 55.66%, creating a strong confluence zone. However, the daily Relative Strength Index (RSI) grinds higher near 40 and remains neutral, so the move still needs confirmation.

Extreme Fear Meets a Neutral Altcoin Season Index

Sentiment adds a contrarian layer to the technical picture. The Crypto Fear and Greed Index printed 19 while Bitcoin still hovered between $60,000 and $61,000, up from 11 July 1, and 12 last week. The gauge has spent a full month in Extreme Fear after June’s correction, driven by a hawkish Fed, geopolitical tensions, and record ETF outflows.

Historically, prolonged readings below 20 have clustered near market bottoms. The index hit a record low of five in February 2026.

Meanwhile, the Altcoin Season Index from BlockchainCenter stands at 45, almost exactly halfway between Bitcoin season and altcoin season. The index flags altseason only when 75% of the top 50 coins beat Bitcoin over 90 days.

No true altcoin season has arrived since the current dominance structure formed in late 2022. Some experts argue the rotation cannot start until global liquidity expands again.

Bitcoin trades near $61,616, up 2.4% in the last 24 hours, according to CoinGecko. For altcoin holders, the setup remains binary. A weekly close below 55.66% would validate the rotation thesis, while a reclaim of 59.63% would keep capital parked in Bitcoin.

The post Bitcoin Dominance Tests Key Support: Is the Long-Awaited Altcoin Season Finally Near? appeared first on BeInCrypto.

my financial condition right now

Why is Sumitomo Chemical stock surging today?

CFTC chair blasts Illinois over ‘punitive’ crypto tax

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Staud – Corporette.com

-

Politics7 days ago

Politics7 days agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Crypto World3 days ago

Crypto World3 days agoStrategy authorizes up to $1.25B in Bitcoin sales under new capital plan

-

Business7 days ago

Business7 days agoAsia stock markets slide as tech shares slump

-

News Videos4 days ago

News Videos4 days agoMAJOR BITCOIN & MARKET UPDATE!!!! (MUST WATCH ASAP!!!)

-

Tech3 days ago

Tech3 days agoAnonymous researcher drops 0-day ‘exploitarium’ repo

-

Crypto World6 days ago

Crypto World6 days agoCoinbase, Circle Deepen Crypto Stock Losses Despite Resilient S&P 500

-

Business3 days ago

Business3 days agoAustralia treasurer says alleged access of prime minister’s bank data ’incredibly concerning’

-

Crypto World6 days ago

Crypto World6 days agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Sports6 days ago

Sports6 days agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Tech5 days ago

Tech5 days agoBluekit phishing kit adopts browser-in-the-middle for login theft

-

Crypto World7 days ago

Crypto World7 days agoTether (USDT) Passes Ether in Market Cap as ETH Drops Toward $1.5K

-

Crypto World7 days ago

Crypto World7 days agoHyperliquid Named on Singapore MAS Investor Alert Register

-

Tech6 days ago

Tech6 days agoRussian hackers now target Signal backup recovery keys

-

Crypto World6 days ago

Crypto World6 days agoRTX holders must register wallets before token distribution begins

-

Sports2 days ago

Sports2 days agoBroncos roster: OL Ben Powers (No. 74) entering final year of contract

-

Business3 days ago

Business3 days agoThe AI boom won’t burst all at once. It will pop in ‘rolling bubbles’: Macquarie

-

Tech5 days ago

Tech5 days agoClaude Code turned every engineer into three. Now companies need more product thinkers

-

Crypto World7 days ago

Crypto World7 days agoSpaceX Called a Market Top Signal Just 2 Weeks After Its $86 Billion IPO

-

Tech5 days ago

Tech5 days agoSilicon Valley paid to kill AI regulation, now it wants the rules back

You must be logged in to post a comment Login