Crypto World

What Is cross-margining in crypto trading?

Cross-margining lets your whole account balance backstop every open trade, so a winning position can keep a losing one alive. It is more capital-efficient than isolated margin, and it can also wipe out your entire account in one bad move. Here is how it works.

Summary

- Cross-margining is a margin mode in which all the funds in your account act as shared collateral for all your open positions, so gains and spare equity in one position can support a losing one.

- It contrasts with isolated margin, where a fixed amount of collateral is locked to each position and losses are capped to that amount.

- Cross margin is more capital-efficient and can delay liquidation, but it puts your entire account at risk, because a large enough loss can be covered from the whole balance and trigger a portfolio-wide liquidation.

- Traders generally use cross margin for hedged, offsetting, or core positions, and isolated margin for speculative, high-risk, or single bets where they want a hard loss cap.

- The same principle scales to institutions, where prime brokers cross-margin positions across entire asset classes, using assets like stablecoins as shared collateral.

Cross-margining is a way of managing collateral in leveraged trading where your entire account balance backs all of your open positions at once, instead of each trade standing on its own. In practice, that means the profit or spare equity in one position can be used to support another that is losing, which can keep trades alive through volatility. The trade-off is that your whole account is exposed: a large enough loss draws on the entire balance and can liquidate everything. Cross margin is one of the two main margin modes offered on crypto trading platforms, the other being isolated margin, and understanding the difference is essential to managing risk. This explainer covers how margin trading works, how cross and isolated margin differ, a worked example, the pros and cons, and how the same idea operates at the institutional level.

Margin trading basics: leverage, collateral, liquidation

Cross-margining only makes sense once the basics of margin trading are clear. Margin trading means borrowing funds to open a position larger than your own cash balance would allow. The money you put up is the margin, and it serves as collateral for the borrowed funds. Leverage describes how much larger your position is than your own capital: at five-to-one leverage, a trader controls a position five times the size of their margin. Leverage amplifies everything, so both gains and losses grow in proportion to the position size instead of the smaller amount of capital actually committed.

Two thresholds govern a margin position. The initial margin is the collateral required to open the position. The maintenance margin is the minimum equity that must be kept to hold it open. As long as the position’s equity stays above the maintenance margin, the trade continues. If the market moves against the position enough that equity falls below the maintenance margin, the platform issues a margin call or, more commonly in crypto, moves straight to liquidation.

Liquidation is the forced closure of a position when its equity drops below the maintenance requirement. The platform’s liquidation engine closes the position at market prices, sometimes in partial steps, to prevent the account from going negative. Because leverage magnifies losses, liquidation can happen fast: at high leverage, a small adverse price move can wipe out the margin buffer entirely. This is the central risk of all margin trading, and the choice between cross and isolated margin is fundamentally a choice about how liquidation is calculated and how much of your account is exposed to it.

Cross margin versus isolated margin: the core difference

The two margin modes differ in one crucial respect: what pool of collateral backs each position. In cross margin, all the funds in your account form a single shared pool that backs every open position together. Unrealized profits and spare equity from one position can flow to support another that is drawing down, which can delay or prevent the liquidation of the losing trade. The account is managed as one book, and liquidation becomes a portfolio-level event that depends on the combined equity of everything you hold.

In isolated margin, collateral is ring-fenced to each position individually. You decide how much of your funds to assign to a specific trade, and that amount is the maximum you can lose on it. If the position is liquidated, only its allocated collateral is lost, and the rest of your account, including your other positions, is untouched. Isolated margin gives you a predictable, per-trade liquidation price and a hard cap on the damage any single idea can do, at the cost of not being able to draw on the rest of your balance to save a position.

The consequence is a clear trade-off between capital efficiency and risk containment. Cross margin uses your capital more efficiently, because idle equity and winning positions automatically backstop losing ones, and it tends to produce fewer forced liquidations on individual legs. But it places your entire account on the line, since a bad enough move can consume the whole balance. Isolated margin sacrifices efficiency for control: each position is walled off, so a single blow-up cannot spread, but you must actively manage collateral and accept more frequent single-position liquidations. Neither is inherently better; the right mode depends on the strategy.

A worked example

A concrete example makes the difference tangible. Imagine a trader with a $15,000 account who wants to open a leveraged long position on Bitcoin with an initial margin requirement of $5,000. Under cross margin, the entire $15,000 backs the position, giving a $10,000 buffer above the initial requirement. That large cushion makes liquidation far less likely on a normal pullback, because the whole account absorbs the drawdown. If the trader also holds other positions, profits on those can further support the Bitcoin trade. The catch is that if the combined account equity falls below the maintenance level, the liquidation engine can close positions and consume the full $15,000, not just a slice of it.

Now run the same trade under isolated margin. The trader allocates exactly $5,000 to the Bitcoin position and no more. If Bitcoin falls and the position is liquidated, the maximum loss is that $5,000, and the remaining $10,000 in the account is safe, available for other trades or simply preserved. The liquidation price is predictable and tied only to that position’s collateral. The downside is that the position has a much thinner buffer, so it will be liquidated sooner than the cross-margined version, since it cannot draw on the rest of the account to survive a dip.

The example shows the core tension. Cross margin gave the Bitcoin trade a bigger cushion and a better chance of surviving volatility, but it risked the entire $15,000. Isolated margin capped the loss at $5,000 but liquidated the position more readily. A trader who is confident and wants staying power, and who is comfortable risking the whole account, leans cross. A trader who wants a firm loss limit on a specific, uncertain bet leans isolated. The same $15,000 produces very different risk profiles depending on the mode chosen.

The pros and cons of cross-margining

Cross-margining has real advantages that explain its popularity among active and professional traders. Its main strength is capital efficiency: because all equity backs all positions, none of your capital sits idle behind a single trade, and winning positions automatically support losing ones. This produces a smoother equity curve and fewer forced exits on individual legs, which is especially valuable for hedged or offsetting strategies where one position is meant to counterbalance another. It is also simpler to monitor in one sense, since you watch a single account-level margin level instead of tracking collateral on many separate positions.

The disadvantages are equally real and more dangerous if ignored. The defining risk is that your entire account is exposed: once combined equity falls below the maintenance margin, liquidation can consume the whole balance, not a contained portion. This becomes acute when positions are correlated, which is common in crypto, where many assets move together. In a sharp, broad sell-off, several cross-margined positions can lose at once, draining account equity rapidly and triggering a cascade of liquidations across the book. A single violent move can therefore wipe out everything, where isolated margin would have contained the damage.

Cross margin also carries a psychological hazard. Because the shared pool makes positions feel more resilient, it can tempt traders to over-leverage, opening larger positions than they should because the buffer looks generous. That temptation, combined with the whole-account exposure, is how traders turn a manageable loss into a total one. The mode rewards discipline and punishes its absence. Used carefully within a hedged framework, cross margin is efficient and forgiving of ordinary volatility; used carelessly with correlated, over-leveraged bets, it is the fastest route to a blown-up account.

When to use cross versus isolated

The choice between the modes should follow the strategy rather than habit. Cross margin fits situations where positions offset or support one another. Hedging programs, basis trades, pairs trades, and market-making all benefit from a shared collateral pool, because a gain on one leg naturally cushions a loss on another, and pooling the collateral reduces the chance of an unnecessary single-leg liquidation. Core positions that a trader intends to hold through volatility also suit cross margin, since the deeper buffer provides staying power. In these cases, the whole-account exposure is an acceptable trade for the efficiency and resilience gained.

Isolated margin fits the opposite situations. Speculative, event-driven, or high-volatility bets, and single-ticket trades where the outcome is uncertain, are better ring-fenced, so that if the idea fails it cannot damage the rest of the account. A trader taking a focused shot on a volatile small-cap token, for instance, can cap the loss at a fixed amount and sleep easily knowing the rest of the balance is safe. Isolated margin also suits newer traders building discipline, because it enforces a hard maximum loss per trade and makes the risk of each position explicit.

Many experienced traders combine both in a core-satellite structure. They run cross margin on a core book of hedged or offsetting positions that benefit from pooled equity, while keeping speculative satellite trades in isolated buckets with fixed loss caps. This keeps the core capital-efficient without letting a single high-risk bet sink the whole account. The practical rule is to match the mode to the intent of each trade: shared exposure for positions designed to work together, walled-off exposure for standalone bets you want to contain. Some platforms even offer a smart cross margin that nets opposite-direction positions across products, further improving efficiency for hedged books.

Cross-margining at the institutional level

The same principle that governs a retail trader’s account scales all the way up to the largest institutions, and it is worth seeing the connection. When a hedge fund or trading firm operates through a prime broker, the broker cross-margins the firm’s positions across entire asset classes, netting exposures in digital assets, foreign exchange, derivatives, and fixed income so the firm posts collateral against the combined risk of its whole book rather than each position separately. This is cross-margining as a foundation of professional trading, and it is a major reason institutions value prime brokers: it frees up enormous amounts of capital that would otherwise sit idle.

Crypto has begun importing this institutional version. Prime brokers serving digital assets now let clients cross-margin crypto positions against traditional exposures, and stablecoins have started to play the role of shared collateral in that system. Ripple’s RLUSD, for example, has been positioned as a stablecoin that enables cross-margining between digital assets and traditional markets through institutional prime brokerage, letting a firm post the token as collateral recognized across both worlds. That is the same idea a retail trader meets in a cross-margin account, applied at the scale of institutional portfolios spanning many markets.

Seeing the two levels together clarifies what cross-margining really is: a method for treating a collection of positions as a single risk pool to use capital more efficiently. For a retail trader, the pool is the account balance backing a handful of trades. For an institution, it is a multi-asset book backed by cash and collateral like stablecoins across a prime broker. The mechanics and the stakes differ by orders of magnitude, but the core logic, and the core trade-off between efficiency and concentrated risk is identical.

The risks you must respect

Whatever the level, cross-margining demands respect for a specific set of risks, and ignoring them is how accounts are lost. The first is correlation risk. Crypto assets frequently move together, so a broad sell-off can push multiple cross-margined positions into loss simultaneously, draining shared equity far faster than a single position would. The very diversification that looks like safety can become a synchronized drawdown when markets turn risk-off together, and the shared pool that was meant to cushion individual losses instead absorbs many at once.

The second is liquidation and leverage risk. Because cross margin can make positions feel durable, it invites higher leverage, and higher leverage means a smaller adverse move can breach the maintenance margin. When that happens in cross mode, the liquidation is a portfolio-level event that can close multiple positions and consume the whole account. Flash crashes and liquidation cascades, where forced selling drives prices lower and triggers still more liquidations, are especially dangerous, and thin order books during such events can cause execution at prices far worse than expected. The market has seen sharp, leverage-driven cascades wipe out over-extended traders in minutes.

The disciplined response is to size positions conservatively, avoid over-leverage, and match the margin mode to the trade. Use cross margin for genuinely hedged or core positions where offsetting exposure justifies the shared pool, and isolate speculative or high-beta bets so a single failure cannot spread. Set alerts and plan collateral top-ups in advance instead of reacting during a crash. Cross-margining is a powerful tool for capital efficiency, but it concentrates risk at the account level, and the traders who use it well are the ones who never forget that the whole balance is on the line.

Frequently Asked Questions

What is cross-margining in simple terms?

Cross-margining is a margin mode where all the funds in your trading account act as shared collateral for all your open positions at once. Profits and spare equity from one position can support another that is losing, which can delay liquidation. The trade-off is that your entire account is exposed, so a large enough loss can be covered from the whole balance and liquidate everything.

How is cross margin different from isolated margin?

In cross margin, your whole account balance backs every position, so gains on one can cushion losses on another, but your entire account is at risk. In isolated margin, a fixed amount of collateral is locked to each position, capping the loss on that trade to the allocated amount and protecting the rest of your account. Cross is more efficient; isolated is more contained.

Which is better, cross or isolated margin?

Neither is universally better; it depends on the trade. Cross margin suits hedged, offsetting, or core positions that benefit from a shared collateral pool and staying power. Isolated margin suits speculative, event-driven, or single high-risk bets where you want a hard loss cap. Many traders use both, running cross margin on a core book and isolating speculative satellite trades.

What is the main risk of cross-margining?

The main risk is that your entire account is exposed. Once combined equity falls below the maintenance margin, liquidation can consume the whole balance rather than a contained amount. This is especially dangerous with correlated crypto assets, where a broad sell-off can push several positions into loss at once, draining shared equity quickly and triggering a portfolio-wide liquidation.

Can cross-margining cause bigger losses?

It can, because it puts the full account balance behind your positions. In a sharp, correlated downturn or a flash crash, multiple cross-margined positions can lose simultaneously and a portfolio-level liquidation can wipe out the entire account. Cross margin can also tempt traders to over-leverage because the shared buffer feels generous, which magnifies losses when the market turns.

What is a maintenance margin?

The maintenance margin is the minimum equity you must keep to hold a leveraged position open. As long as equity stays above it, the position continues. If the market moves against you and equity falls below the maintenance margin, the platform liquidates the position. In cross margin, this is calculated at the account level; in isolated margin, it is calculated for each position separately.

Do institutions use cross-margining?

Yes, at large scale. When institutions trade through a prime broker, the broker cross-margins their positions across entire asset classes, netting exposures in digital assets, foreign exchange, derivatives, and fixed income so the firm posts collateral against the combined risk of its whole book. Stablecoins such as RLUSD have started to serve as shared collateral in this institutional cross-margining system.

How can I use cross-margining safely?

Match the mode to the trade: use cross margin for hedged or core positions where offsetting exposure justifies the shared pool, and isolate speculative or high-volatility bets. Size positions conservatively, avoid over-leverage, set liquidation alerts, and plan collateral top-ups in advance. Always remember that in cross mode, your entire account is on the line, so discipline about leverage and position size is essential.

Disclaimer: This article is for information and educational purposes only and does not constitute financial, investment, or trading advice. Margin trading involves a high risk of loss, including the potential loss of your entire account, and is not suitable for all investors. Nothing here is a recommendation to trade or use any strategy. Always do your own research and consider consulting a qualified professional before trading on margin. Information is accurate as of July 2, 2026, and may change.

TLDR:

- Ironwood testnet activates with two independent consensus implementations built by separate teams.

- Zcash reduced ten-note wallet migration times from around 15 minutes to about 2.5 minutes.

- Multi-transaction signing now supports more than 11 transactions through a single QR code.

- Mainnet activation could occur around July 21 as audits and ZIP specifications near completion.

Zcash is moving forward with its Ironwood network upgrade after confirming a scheduled testnet activation. The update introduces new consensus changes and major wallet performance improvements ahead of a planned mainnet deployment.

Development teams have also completed two independent consensus implementations for the upgrade. The work marks one of the most advanced testnet preparations recorded for a Zcash network upgrade.

Zcash Ironwood Testnet Upgrade Brings Dual Consensus Implementations

Zcash developer Dev announced that the Ironwood testnet upgrade would activate on July 4. The release includes two independently developed consensus implementations.

One implementation came from Valar Group, while the other was built by the Zcash Foundation. According to Dev, the Valar Group version has already entered the audit process.

The teams also released a desktop wallet fork that supports migration testing on the testnet. Users with Keystone development devices can update firmware and test migration functions before the mainnet launch.

The upgrade introduces multi-transaction signing through a single QR code. Dev said the feature required extensive work behind the scenes and represented a major technical milestone for the testnet.

Contributors from zodl also participated in the process. The group worked on technical specifications, wallet libraries, circuit updates, and application programming interfaces supporting Ironwood.

Zcash Wallet Performance Improves Ahead of Mainnet Activation

Development updates shared by Dev showed major gains in wallet migration performance. The time needed to complete a ten-note migration fell from around 15 minutes to approximately two and a half minutes.

Inbound QR scanning dropped from three minutes to one minute. Loading and transaction review declined from two minutes to 45 seconds.

The signing process posted the largest improvement. Signing time fell from roughly nine minutes to about 37 seconds.

Outbound QR scanning also became faster. The process now takes about 10 seconds compared with roughly one minute previously.

In a separate update, Zcash developer Sean Bowe said all Ironwood consensus rule changes had been implemented and were undergoing audits.

He added that the specifications and Zcash Improvement Proposals, known as ZIPs, were approaching their final state.

Bowe also said developers expected readiness for a mainnet activation around July 21. He confirmed that the official testnet activation was scheduled for the following day and noted that the Zebra release supporting Ironwood should become available around the same time.

According to Bowe, sufficient mining hash rate already signals technical readiness for the mainnet upgrade. He noted that some wallets may not support Ironwood immediately, although alternative options and testnet preparation time remain available before activation.

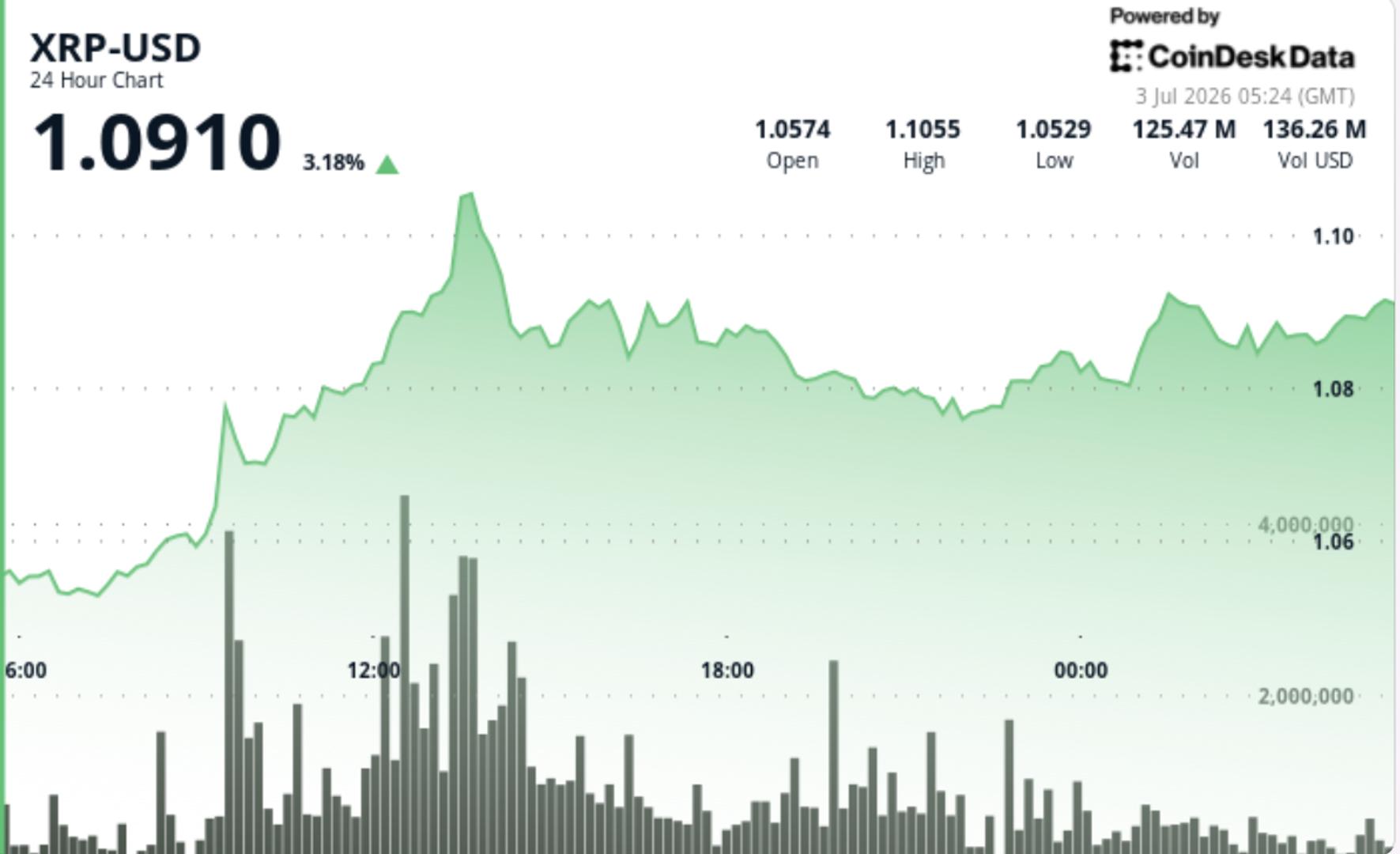

XRP is starting to build a higher base above $1 following last week’s sell-off. The token edged higher through the U.S. session, held $1.08 on repeated tests and pushed toward $1.10 before sellers slowed the move. That keeps the setup constructive, but still unfinished, with traders watching whether the latest accumulation turns into a clean breakout.

News Background

• XRP wallet creation rose to 4,941 daily addresses, the strongest single-day growth in 14 weeks.

• Bullish social sentiment reached a three-month high, with positive comments outnumbering bearish ones by 3.7 to 1.

• Ripple completed its scheduled 1 billion XRP escrow unlock without a meaningful price shock.

• XRP’s move tracked the broader crypto market closely, with idiosyncratic variance against CD5 staying well below the level that would suggest a major asset-specific catalyst.

Price Action Summary

• XRP rose from $1.0611 to $1.0894 during the 24-hour session, gaining 0.62%.

• The token established higher lows at $1.0552, $1.0589 and $1.0799, showing buyers stepped in at progressively higher levels.

• Volume rose 26.92% above the seven-day average, pointing to steady participation around the move.

• The strongest push came at 13:00 UTC, when volume reached 117.5 million XRP, about 142% above the 24-hour average.

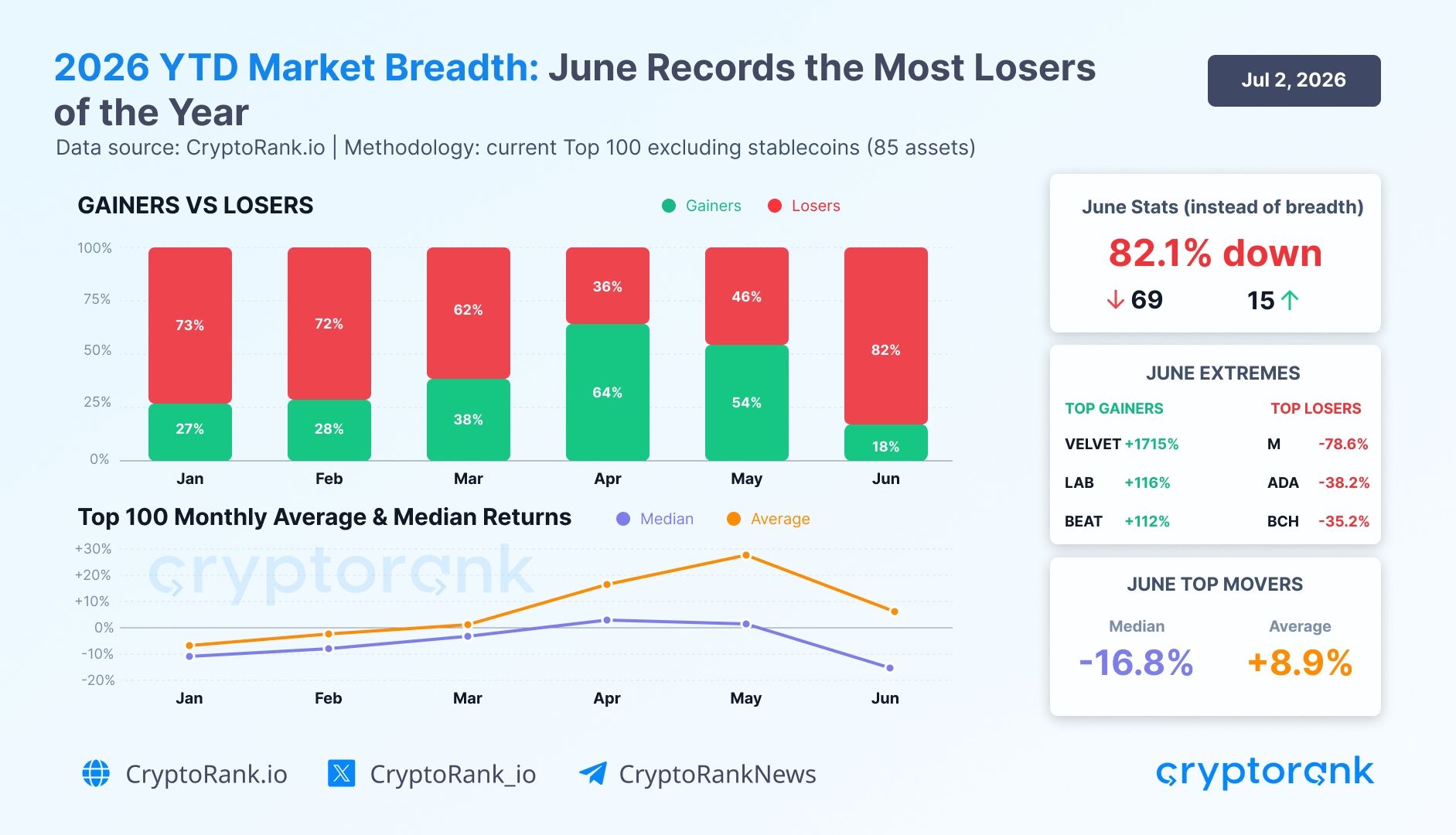

Roughly 82.1% of the top-100 crypto assets declined in June, the worst market breadth of 2026, even as the group’s average return stayed positive.

That split defined the month. A single outlier lifted the average into positive territory while the median return dropped 16.8%, according to a second-quarter recap from CryptoRank.

A Headline Average That Hid the Damage

Across the current top-100 assets excluding stablecoins, CryptoRank recorded a positive average return of 8.9% for June. That figure reflected a single outlier rather than the broader market.

“The market breadth data shows a clear deterioration in participation across the current non-stablecoin Top 100 assets. In June, breadth weakened to its worst level of 2026 so far,” the report read.

Follow us on X to get the latest news as it happens

The report noted that the average was affected by Velvet (VELVET), which surged 1,715% during the month, lifting the aggregate. The 25-point gap between the positive average and the negative 16.8% median showed how few tokens carried the upside.

Besides VELVET, other top gainers included LAB (LAB) at 116% and Audiera (BEAT) at 112%. June also reversed a stronger start to the quarter.

April saw 64% of top-100 assets gain, the best month of 2026. Meanwhile, May showed a more fragile structure, and the June breakdown confirmed the reversal.

Weakness Reached Major Crypto Narratives in June

The decline was not limited to the largest assets. Across all traded tokens with 24-hour volume of more than $1 million, every one of the eight tracked narratives posted a negative median return.

Layer 2 chains led the losses at -24.9%, followed by Decentralized Physical Infrastructure Networks (DePIN) at -24.8% and Layer 1 chains at -22.8%.

“All 8 tracked narratives posted negative median returns, with losers outnumbered gainers in nearly every category, confirming that the market remained defensive and narrow through Q2 without a broad recovery in breadth,” CryptoRank said.

The gainers-versus-losers split showed how narrow the market became. Decentralized Finance (DeFi) recorded 42 gainers against 117 losers, while Artificial Intelligence (AI) posted 21 gainers against 35 losers.

The pattern pointed to a defensive market. Bitcoin (BTC) dominance held near 56% at quarter-end as capital rotated away from weaker altcoins.

Whether June marks a base or another leg lower depends on breadth recovering in the second half.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Crypto’s Positive June Average Masked an 82% Decline Across Top Assets appeared first on BeInCrypto.

Russia’s central bank says the digital ruble is ready for a Sept. 1 rollout, keeping the country’s central bank digital currency plan on schedule.

Summary

- Russia’s Sept. 1 digital ruble rollout moves ahead despite EU sanctions targeting related financial infrastructure.

- Bank rules require major lenders and large retailers to support digital ruble payments in stages.

- U.S. lawmakers are moving toward a temporary CBDC ban while Russia expands state digital money.

Governor Elvira Nabiullina said “everyone is ready” for the launch, according to a July 2 report by RIA Novosti.

The digital ruble will circulate alongside cash and non-cash rubles, not replace them. The Bank of Russia has said people will be able to open digital wallets through banking apps connected to its platform. It has also said individuals will not pay fees on digital ruble transactions.

The rollout begins with banks and large merchants

The Bank of Russia’s timeline requires major banks to offer digital ruble services from Sept. 1, 2026. Large retailers with annual revenue above 120 million rubles must also accept digital ruble payments from that date.

The rules will expand in stages. Banks with universal licenses and retailers with annual revenue above 30 million rubles must join from Sept. 1, 2027. Other banks and smaller retailers will follow from Sept. 1, 2028, while very small merchants will remain exempt.

Sanctions pressure frames the rollout

The launch comes as the European Union has already moved against Russia-linked digital finance. In its 20th sanctions package, the EU Council banned transactions involving RUBx and all EU support for the development of the digital ruble. It linked the measures to Russia’s war against Ukraine and wider concerns over sanctions evasion.

In addition, the EU also proposed broader restrictions on foreign crypto services tied to Russian sanctions evasion. That plan followed growing scrutiny of ruble-linked crypto rails, including platforms and tokens that authorities say may support cross-border payments outside Western controls.

Russia has tested digital ruble use cases for more than a year. As previously reported, the Central Bank of Russia piloted digital ruble smart contracts in Tatarstan, including tests on conditional spending for public funds. The latest timeline shows that Moscow now wants to move the project from testing into broader payment use.

U.S. policy moves in the opposite direction

Russia’s CBDC push contrasts with U.S. policy, where lawmakers have moved toward a temporary ban on a Federal Reserve digital dollar. As crypto.news reported, the 21st Century ROAD to Housing Act would block the Fed from creating a CBDC or similar asset through 2030 if it becomes law.

The U.S. debate reflects concerns over privacy, state control, and the role of private stablecoins. The Russian approach is different. Moscow is building a state-run digital currency while also testing other digital asset rules for trade and financial access under sanctions.

A February report by Jack Jarmon for the Australian Institute of International Affairs said Russia could face limits if it relies on Bitcoin or other proof-of-work assets to bypass sanctions. The report pointed to old power infrastructure and limited access to foreign technology. Those limits may explain why the digital ruble remains central to Moscow’s state-led payment strategy.

The Sept. 1 launch will test whether Russia can drive adoption among banks, merchants, and users. Nabiullina said the central bank wants the digital ruble to be “in demand by people and businesses” and “convenient.”

For now, the rollout places Russia among the countries pushing CBDCs forward while sanctions and U.S. policy debates keep digital state money under close review.

eToro has led a $12.5 million strategic funding round in Extended, an onchain exchange for perpetual futures.

Summary

- eToro’s Extended investment links Zengo self-custody tools with onchain perpetual futures trading access for users.

- Jump Crypto joined the round as brokerages move deeper into decentralized derivatives and market infrastructure.

- Perp DEX growth is pulling trading platforms toward self-custody, tokenized assets, and onchain execution.

Extended announced the round in a July 2 post on X, saying eToro led the investment and Jump Crypto also joined the deal.

Meanwhile, the funding is tied to a partnership between Extended and Zengo, the self-custody wallet eToro acquired earlier this year. The companies plan to work on access to global financial markets through onchain infrastructure. eToro said the partnership will explore ways to connect traditional financial assets with decentralized trading venues.

Self-custody becomes part of the plan

Zengo gives eToro a direct route into self-custody products. The wallet uses multi-party computation technology, which removes the need for seed phrases while still giving users control over assets. It also supports swaps, staking, and access to decentralized applications.

eToro completed its Zengo acquisition on April 30 while reporting a sharp drop in crypto trading profit. The company said at the time that Zengo would support its plan to connect traditional financial products with onchain systems. The Extended deal now gives that plan a derivatives-focused path.

Extended builds onchain perps market

Extended was founded by former Revolut employees and opened trading to all users in late 2024. In its public launch announcement, the company said it planned to add unified margin with technical support from StarkWare.

The exchange is built on StarkWare’s StarkEx scaling engine. It focuses on perpetual futures, a type of derivative contract that has no expiry date. Extended says its model supports self-custody trading while aiming to keep execution fast enough for active traders. That structure places it between centralized crypto futures venues and fully decentralized trading platforms.

Perps growth draws larger firms

Perpetual futures remain one of the largest crypto trading markets. As crypto.news reported, CoinGecko’s 2026 Crypto Perpetuals Report found that perp DEX open interest share rose from 3.6% in early 2025 to 13.5% in 2026. The same report showed Binance and OKX still leading centralized perps trading, even as decentralized venues gained share.

That growth has drawn more attention from brokers and trading apps. Previously, crypto.news reported that Robinhood launchedperpetual futures tied to commodities, ETFs, and currencies for eligible European users. The rollout showed how crypto-style trading tools are moving into traditional markets.

Deal follows weaker crypto trading income

The investment comes after eToro reported lower crypto-related trading profit in the first quarter of 2026. As reported by crypto.news, crypto generated $13 million in profit during the quarter, or about 5% of eToro’s total net trading profit of $258 million. That was down from $46 million in the same period in 2025.

The Extended round shows that eToro is still building around digital assets despite weaker short-term crypto revenue. The company is using Zengo to strengthen its self-custody stack and Extended to enter onchain derivatives more directly.

Moreover, the move also places eToro closer to a market where trading apps, crypto exchanges, and decentralized platforms are competing for users who want faster access, direct asset control, and broader exposure to global markets.

Blockchain technology has evolved rapidly over the past decade, giving rise to hundreds of networks optimized for different use cases. Some prioritize speed, others focus on security, privacy, scalability, or specialized applications like gaming and decentralized finance (DeFi). While this diversity has fueled innovation, it has also created one of Web3’s biggest challenges: blockchain silos.

Today, the industry is moving toward a future where blockchains no longer operate as isolated ecosystems. Instead, they’re becoming interconnected networks that can communicate, exchange assets, and share data seamlessly. This shift could redefine how decentralized applications (dApps), users, and institutions interact with blockchain technology.

What Are Blockchain Silos?

A blockchain silo exists when a network operates independently without native communication with other blockchains. Assets, data, and smart contracts remain confined to their respective ecosystems.

For example:

- Bitcoin primarily serves as a secure store of value.

- Ethereum powers a vast ecosystem of smart contracts.

- Solana focuses on high-speed transactions.

- BNB Chain emphasizes affordable and scalable DeFi.

- Avalanche offers customizable blockchain infrastructure.

Each blockchain has unique strengths, but moving assets or information between them has traditionally required third-party bridges or centralized exchanges.

This fragmentation often creates unnecessary complexity for users and developers alike.

The Problems Caused by Blockchain Silos

1. Fragmented Liquidity

Liquidity scattered across multiple blockchains reduces capital efficiency. Instead of one unified financial ecosystem, liquidity is divided among separate networks, making markets less efficient.

2. Poor User Experience

Managing several wallets, switching networks, paying different gas fees, and learning multiple interfaces discourages mainstream adoption.

3. Limited Application Potential

Developers often build applications for a single blockchain, restricting access to users and liquidity from other ecosystems.

4. Security Risks

Traditional cross-chain bridges have become attractive targets for hackers. Billions of dollars have been lost through bridge exploits over the past several years, highlighting the need for more secure interoperability solutions.

The Rise of Blockchain Interoperability

Instead of competing in isolation, blockchain ecosystems are increasingly embracing interoperability—the ability for different blockchains to communicate securely.

Modern interoperability solutions aim to allow:

- Cross-chain asset transfers

- Cross-chain messaging

- Shared liquidity

- Multi-chain smart contract execution

- Unified user experiences

Rather than forcing users to choose one blockchain, interoperability allows them to benefit from many simultaneously.

Technologies Driving the End of Silos

Cross-Chain Messaging

Instead of merely transferring tokens, cross-chain messaging enables smart contracts on one blockchain to trigger actions on another.

This opens the door to far more sophisticated decentralized applications.

Interoperability Protocols

Dedicated interoperability layers provide standardized communication between independent blockchains.

These protocols reduce fragmentation while allowing each network to maintain its own security and governance.

Chain Abstraction

One of the biggest emerging trends is chain abstraction.

Instead of asking users to manually manage networks, wallets, bridges, and gas tokens, applications handle the complexity behind the scenes.

Users simply interact with the application while the infrastructure determines the optimal blockchain for each transaction.

Intent-Based Architecture

Intent-based systems allow users to specify their desired outcome rather than manually executing every blockchain interaction.

For example:

Instead of bridging tokens, swapping assets, and staking manually, a user simply requests:

“Stake my stablecoins in the highest-yield lending protocol.”

The protocol automatically completes every required cross-chain action.

Benefits of an Interoperable Future

Better Capital Efficiency

Assets can move freely across ecosystems, creating deeper liquidity and more efficient markets.

Improved User Experience

Users no longer need to understand every blockchain’s technical details. Applications become as simple as traditional fintech apps.

More Powerful Applications

Developers gain access to users, assets, and services across multiple chains, enabling richer decentralized applications.

Greater Ecosystem Collaboration

Instead of competing for users, blockchain networks can specialize while remaining connected through shared infrastructure.

Challenges That Still Need Solving

Although interoperability has advanced significantly, several challenges remain.

Security

Cross-chain infrastructure must maintain strong security guarantees without introducing centralized trust assumptions.

Standardization

The industry still lacks universal standards for messaging, identity, and asset transfers across every blockchain.

Scalability

As interoperability grows, systems must efficiently process increasing volumes of cross-chain communication.

Governance

Coordinating upgrades across multiple decentralized ecosystems remains a complex challenge.

What This Means for DeFi

The end of blockchain silos could dramatically reshape decentralized finance.

Future DeFi platforms may automatically source liquidity from multiple chains, optimize yields across ecosystems, and execute transactions wherever conditions are most favorable—all without requiring users to manually bridge assets or switch networks.

This could make decentralized finance significantly more accessible to everyday users while improving efficiency for institutional participants.

Beyond DeFi: A Unified Web3

Interoperability extends far beyond finance.

Potential applications include:

- Cross-chain gaming assets

- Portable digital identities

- Interoperable NFTs

- Multi-chain DAOs

- Unified social networks

- Enterprise blockchain integration

- AI agents coordinating across decentralized ecosystems

Rather than existing as separate blockchain islands, these services could operate within one connected Web3 ecosystem.

Conclusion

The next phase of blockchain evolution isn’t about finding a single “winning” blockchain—it’s about enabling all blockchains to work together.

As interoperability protocols, chain abstraction, and intent-based systems mature, users may no longer need to think about which blockchain they’re using. Just as internet users rarely consider which servers deliver a website, future Web3 users may simply interact with applications while the underlying infrastructure seamlessly coordinates across multiple networks.

The end of blockchain silos represents more than a technical milestone. It marks the transition from isolated blockchain ecosystems to a truly interconnected decentralized internet—one where assets, applications, and information flow freely across networks, unlocking the full potential of Web3.

REQUEST AN ARTICLE

U.S.-linked wallets appear to be the largest political trading group on Polymarket’s global platform, even though the platform lists the United States as a blocked country.

Summary

- U.S.-linked wallets dominate Polymarket political trading despite geoblocks, according to new Allium on-chain research findings.

- Researchers say offshore activity raises fresh oversight questions as prediction markets face tougher global controls.

- Polymarket restrictions list the United States as blocked, but demand appears to continue offshore globally.

Blockchain data firm Allium said in a July 3 report that the U.S. was the biggest national political market by contracts traded among wallets it could link to a country.

The firm said its data covered only about 6% of wallets with country tags, so the results should be treated as directional. Still, Allium said the pattern was clear enough to show that US demand did not disappear after access blocks. “Blocking access did not end U.S. participation,” the report said. It added that activity had moved offshore and outside direct U.S. oversight.

Geoblocks face fresh questions

Polymarket’s own geographic restriction page says the platform is unavailable in the United States and other blocked countries. It also says users must not use VPNs or similar tools to bypass location rules. The page lists 33 fully blocked countries, along with several regions where trading is not allowed.

That policy traces back to earlier U.S. enforcement. In 2022, the Commodity Futures Trading Commission ordered Polymarket to pay a $1.4 million civil penalty and wind down markets that did not comply with US rules. The platform later developed a separate U.S.-regulated product, while the global platform continued to block U.S. users.

Trading patterns point to politics and conflict

Allium said U.S.-linked wallets on Polymarket showed more interest in foreign conflict markets than the wider platform. Five of the top 12 markets by notional volume for the U.S.-linked group related to the Iran war, according to the report. “U.S. money pours into foreign wars,” Allium said, while adding that U.S.-linked traders showed less interest in election markets.

A separate analysis by Rutgers statistician Harry Crane reached a similar view in June. Crane estimated that U.S. users may account for about 30% of total Polymarket volume by studying sports preferences and trading times. His work said Polymarket’s activity pattern looked global, but still showed a large U.S. share.

Rules tighten as markets grow

The report comes as prediction markets face wider regulatory pressure. As crypto.news reported, the CFTC is preparing new prediction market rules that could affect Polymarket and Kalshi. The proposed review process would give regulators more tools to assess event contracts tied to politics, sports, and real-world events.

Previously, crypto.news reported that Spain moved to block Polymarket and Kalshi over gambling license concerns. That action followed similar blocks or restrictions in several other countries. As crypto.news reported in May, Polymarket also said it had no plan to require mandatory KYC on its main global market, even as legal and sanctions pressure increased.

The latest Allium report adds a new point to that debate. If U.S. users still reach global markets despite geoblocks, regulators may ask whether location controls can work at scale. For Polymarket, the data may add pressure at a time when the platform is also dealing with security concerns, including a recent $2.9 million frontend theft that led to promised user refunds.

The issue also puts Polymarket’s split model under closer review. Its U.S.-regulated platform offers a narrower product set, while global markets still draw interest from users who appear to be in blocked regions. That gap may become harder to defend if more data show steady activity from restricted jurisdictions.

US users remain the most active force behind Polymarket’s political prediction markets, even after the platform moved to geoblock Americans from its global, decentralized service. New analysis from blockchain research firm Allium finds that the United States is the largest single country for political contracts on Polymarket when measured by trading volume and wallet participation—suggesting the demand simply shifted outside formal US oversight.

The findings add another layer to the regulatory and compliance challenges surrounding Polymarket, which has already faced scrutiny from US authorities and was compelled to restrict access under a settlement with the Commodity Futures Trading Commission (CFTC) in 2022.

Key takeaways

- Allium’s report ranks the US as Polymarket’s biggest political market by both contracts traded and wallet count.

- Despite access restrictions, the study argues that US demand did not disappear—it moved offshore.

- US traders appear more drawn to foreign conflict-related markets, with Iran-war themes dominating the top US markets by volume.

- Election-focused markets attract less US participation on the global Polymarket, where such markets are comparatively more prominent on Kalshi and Polymarket US.

- Independent research has previously estimated a large share of Polymarket activity originates from the US, even with geoblocking and VPN countermeasures.

US activity persists after Polymarket’s geoblock

Allium’s analysis, published on Thursday, estimates that US-based users form the largest single political crowd on Polymarket across all countries it tracks. The report emphasizes that this is based on tagged wallets—specifically, the 6% of wallets Allium could associate with a country—so the figures are directional rather than definitive.

Still, Allium frames the result as a clear outcome of Polymarket’s restrictions. Blocking access, the firm argues, did not stop US participation; instead, it concentrated it into a way that makes the US look even larger by volume within the offshore-access model.

“Blocking access did not end US participation; it made the US the largest single political market on Polymarket by volume,” the report said. “The demand is still there, now offshore and beyond US oversight.”

This is an important distinction for investors and market participants watching the political prediction market space: the restriction regime may be affecting where and how US users participate, but it has not eliminated US influence over global outcome bets.

Foreign conflict markets draw more US bets than elections

Allium’s breakdown suggests that US participants disproportionately favor foreign conflict-related topics. In the report’s assessment, five of the top 12 markets for US users by notional volume relate to the Iran war.

At the same time, US interest in election-related markets appears comparatively weaker on Polymarket’s global platform. Allium notes that election markets are a category that is allowed on Kalshi and Polymarket US—meaning the global audience’s incentives and the market landscape may differ from what US users most actively trade.

“US money pours into foreign wars, lately Iran, and largely skips the elections the global crowd trades,” said Allium.

For readers tracking adoption and behavior in prediction markets, the takeaway is not just who is trading, but what they are trading. If US demand continues to show up most strongly in geopolitical risk and away from election positioning, that may shape how liquidity, volatility, and information demand evolve across the different platforms.

Polymarket US vs. the global platform: restrictions and regulatory pressure

Allium’s report also clarifies an often-confused distinction: Polymarket US is a US-regulated platform launched in December and offers a narrower selection of markets. The research discussed here concerns the global Polymarket environment, where access was curtailed for US users.

Polymarket was forced to cut off US users from its global platform as part of a $1.4 million settlement with the CFTC in 2022. That enforcement backdrop has continued to cast a spotlight on how prediction market operators handle jurisdictional boundaries and user verification.

Cointelegraph previously reported that US policy makers and regulators have raised concerns about Polymarket, including issues connected to its marketing and compliance approach. Those broader concerns remain relevant in light of Allium’s findings that US involvement has not gone away—only changed form.

Evidence from other researchers: US share remains large

Allium’s results align with an earlier study by Rutgers University statistician Harry Crane. In a June publication, Crane estimated that 30% of Polymarket trading volume comes from the US, despite Polymarket blocking US-based IP addresses and VPNs that can be used to bypass geofencing.

Crane’s analysis estimated that US-based traders sent between $10.6 billion and $26.7 billion through Polymarket between May 2025 and April 2026. The researcher tied activity to likely US participants by comparing trade timing and the specific markets where trades occurred.

There have also been reports that Polymarket has moved to clamp down on VPN usage by blocking certain IP addresses associated with VPN services, reinforcing the idea that the company is actively attempting to reduce circumvention. However, the existence of US-heavy participation in outcome bets—whether directly or via offshore access—suggests countermeasures may not be fully effective.

Where Polymarket is blocked and where it is “close only”

Geographic restrictions are not limited to the United States. Polymarket is completely blocked in more than 34 countries, with Spain cited as the latest example where authorities took action as a “precautionary measure” while investigating whether the companies are operating without necessary licensing.

In an additional tier, four countries—including Singapore, Thailand, Taiwan, and Poland—operate under “close only” rules. In those jurisdictions, users can close existing positions but cannot open new trades.

Polymarket also maintains restricted regions within countries, according to published information: Ontario in Canada, and Crimea, Donetsk, and Luhansk in Ukraine, where Polymarket is blocked locally but remains accessible elsewhere in the same nation.

These layers of access—complete blocks, close-only allowances, and region-level restrictions—highlight how uneven enforcement and licensing frameworks can be across jurisdictions. For traders, it means the practical reach of a prediction market can remain broader than what top-line policy statements might suggest.

Going forward, the key question is how Polymarket will adapt its geoblocking and compliance tooling as scrutiny grows. Readers should watch whether enforcement tightens enough to materially change participation patterns—or whether US influence continues to reappear offshore in ways that keep global political markets effectively driven by the same demand.

CFTC Chair Michael Selig criticized Illinois lawmakers over a new 0.2% tax on crypto transactions, saying the state had moved against financial technology at the wrong time.

Summary

- Illinois’ 0.2% crypto tax drew sharp CFTC criticism before its planned 2027 start date.

- The law requires broker registration, monthly reports, and tax collection on covered digital asset activity.

- Federal crypto tax and market structure talks are moving while Illinois pursues its own rule.

In a July 1 statement, Selig said Illinois lawmakers “slammed the brakes on technological progress” when they approved the measure.

The tax forms part of Illinois’ fiscal 2027 budget and is set to take effect on Jan. 1, 2027. It applies to certain digital asset activity carried out by brokers, including exchange, transfer, custody, and wallet services. The rule has drawn criticism from crypto firms, policy groups, and some market figures.

Selig says state risks falling behind

Selig said blockchains could change how value moves across markets, much as the internet changed how information moves. He argued that tokenized assets may cover commodities, currencies, stocks, and bonds. His statement said Illinois could place residents and businesses at a disadvantage if the state taxes crypto transfers differently from other financial activity.

The CFTC chair also said Illinois lawmakers “decided they know better” than federal lawmakers working on crypto market rules. His comments came as Washington continues to review market structure bills, tax proposals, and agency roles. The remarks show a growing split between state-level tax policy and federal efforts to set national digital asset rules.

Brokers face new duties

Illinois’ Digital Asset Tax Act requires brokers to register with the Illinois Department of Revenue before covered activity begins. Brokers must collect the tax as a separate line item and file monthly reports on covered digital asset activity.

The law can also reach firms outside Illinois if they serve users in the state. Tax advisers have said customer records, mailing addresses, IP addresses, and other data may help decide whether activity falls under Illinois rules. That has raised questions about how exchanges, wallet firms, and custody providers will track and apply the tax in practice.

Industry criticism grows

Previously, crypto.news reported that Strategy co-founder Michael Saylor called the Illinois tax a “Big Mistake” after Governor JB Pritzker signed the budget. Industry groups also warned that the law could raise costs for users and push crypto firms away from the state.

Some critics have focused on the design of the tax. They argue that it applies to activity itself, not only to profits or capital gains. Others have raised concerns about routine wallet transfers, broker reporting systems, and whether the rule treats digital assets differently from stocks, bonds, or derivatives.

Federal talks add pressure

The Illinois dispute comes while Congress reviews broader crypto tax rules. As previously reported, lawmakers have split the Digital Asset PARITY Act into seven tax discussion drafts covering stablecoin payments, mining, staking, lending, wash-sale rules, charitable donations, and disclosure duties.

Moreover, Federal agencies are also reviewing crypto market rules. The SEC and CFTC opened a joint rules review covering derivatives, margining, and market structure questions. Against that backdrop, Selig’s criticism frames the Illinois tax as a state-level move that may clash with wider federal attempts to build clearer rules for digital assets.

Microsoft is investing $2.5 billion in a new operating business that embeds 6,000 engineers and industry experts directly inside enterprise customers to build and run AI systems.

The company, called Microsoft Frontier Company, launched on Thursday. It ties its work to measurable business results.

How the Microsoft Frontier Company Works and Who Runs It

The unit delivers what Microsoft calls Frontier Transformation. Experts embed with customers to co-design, deploy, and continuously improve AI systems at scale.

Follow us on X to get the latest news as it happens

Judson Althoff, CEO of Microsoft’s Commercial Business, positioned the effort beyond standard industry practice. He argued it combines deep industry knowledge with enterprise AI engineering.

“This goes beyond what has been labeled as Forward-Deployed Engineering, and will be the largest, most capable, outcome-driven engineering organization in the industry,” he said.

Microsoft Frontier Company will include salespeople, support staff, technical consultants, and forward-deployed engineers already at the company, many with experience in specific industries, CNBC reported.

The company stressed that customers keep control of their own intelligence. It pledged that client data will not be used to train models in ways that erode a customer’s competitive edge.

The platform also stays model-diverse. Customers can run models from OpenAI, Anthropic, Microsoft, open source, or specialized industry options for each task. Rodrigo Kede Lima will serve as president of the new organization.

Microsoft Enters a Crowded AI Deployment Race

The launch puts Microsoft in a fast-growing market. Rivals have moved quickly to sell hands-on AI deployment, not just tools.

Amazon Web Services committed $1 billion to its own deployment venture two days earlier. Both OpenAI and Anthropic also launched their own deployment ventures in May.

The OpenAI Deployment Company is a standalone entity backed by more than $4 billion in funding. Anthropic teamed up with Goldman Sachs, Blackstone, and Hellman & Friedman on a $1.5 billion venture to deploy Anthropic’s Claude AI model directly inside businesses.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Microsoft Commits $2.5 Billion to New AI Deployment Business appeared first on BeInCrypto.

The Most Underappreciated Marvel Movie Is Getting A Surprise Sequel

Politician who investigated spyware abuses had his phone hacked with Pegasus spyware

WORST dressed guests at Taylor Swift and Travis Kelce’s star-studded wedding party

-

Fashion7 days ago

Fashion7 days agoWeekend Open Thread: Staud – Corporette.com

-

Politics7 days ago

Politics7 days agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Crypto World3 days ago

Crypto World3 days agoStrategy authorizes up to $1.25B in Bitcoin sales under new capital plan

-

Business7 days ago

Business7 days agoAsia stock markets slide as tech shares slump

-

News Videos4 days ago

News Videos4 days agoMAJOR BITCOIN & MARKET UPDATE!!!! (MUST WATCH ASAP!!!)

-

Tech3 days ago

Tech3 days agoAnonymous researcher drops 0-day ‘exploitarium’ repo

-

Crypto World6 days ago

Crypto World6 days agoCoinbase, Circle Deepen Crypto Stock Losses Despite Resilient S&P 500

-

Business3 days ago

Business3 days agoAustralia treasurer says alleged access of prime minister’s bank data ’incredibly concerning’

-

Crypto World6 days ago

Crypto World6 days agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Sports6 days ago

Sports6 days agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Tech5 days ago

Tech5 days agoBluekit phishing kit adopts browser-in-the-middle for login theft

-

Crypto World7 days ago

Crypto World7 days agoTether (USDT) Passes Ether in Market Cap as ETH Drops Toward $1.5K

-

Crypto World7 days ago

Hyperliquid Named on Singapore MAS Investor Alert Register

-

Tech6 days ago

Tech6 days agoRussian hackers now target Signal backup recovery keys

-

Crypto World7 days ago

Crypto World7 days agoRTX holders must register wallets before token distribution begins

-

Sports2 days ago

Sports2 days agoBroncos roster: OL Ben Powers (No. 74) entering final year of contract

-

Business3 days ago

Business3 days agoThe AI boom won’t burst all at once. It will pop in ‘rolling bubbles’: Macquarie

-

Tech5 days ago

Tech5 days agoClaude Code turned every engineer into three. Now companies need more product thinkers

-

Crypto World7 days ago

Crypto World7 days agoSpaceX Called a Market Top Signal Just 2 Weeks After Its $86 Billion IPO

-

Tech6 days ago

Tech6 days agoSilicon Valley paid to kill AI regulation, now it wants the rules back

You must be logged in to post a comment Login