Crypto World

Gnosis Pay reveals hidden flaw behind $1.5 million crypto hack

Gnosis Pay has revealed that a software flaw dating back to October 2023 enabled the $1.5 million exploit of its card safe infrastructure, while confirming that all affected users have been fully reimbursed.

Summary

- Gnosis Pay traced its $1.5 million hack to a Zodiac software flaw that had existed since October 2023.

- The company reimbursed all affected users, restored services within days, and continues recovering about $300,000.

- The incident adds to growing scrutiny of crypto security as firms and governments respond to rising cyber threats.

According to a postmortem published by Gnosis Pay on Friday, the vulnerability was traced to version 3.4.0 of the Zodiac smart contract framework and had remained undiscovered since Oct. 30, 2023.

The company said the weakness was exploited on June 1, allowing attackers to gain control of about $1.5 million in digital assets held across its decentralized self-custodial payment network.

The report states that Gnosis Pay’s monitoring systems, operated by treasury manager NOCA, detected the first unauthorized transfer at 06:17 UTC on June 1. Engineers identified the root cause within two hours of the initial alert, after which the company suspended card services, temporarily halted its bridge to Gnosis Chain, and shared attacker wallet addresses with stablecoin issuers to help trace the stolen funds. Gnosis Pay also notified external projects that could have been exposed to the same vulnerability.

Funds restored after staged recovery

Following the incident, Gnosis Pay restored customer access in several phases. The company said the first affected accounts regained access to their balances and payment cards by the night of June 3 after new card-safe modules had been deployed. Installation continued over the following days, restoring service for 99% of users by June 6, while the remaining accounts were recovered shortly afterward.

Gnosis Pay said it absorbed the financial losses itself, leaving customers with no losses from the exploit. According to the postmortem, the attackers stole mostly GNO, EURe, USDC.e, and several other digital assets. The company added that roughly $300,000 worth of assets had not yet been recovered and recovery efforts remain ongoing.

The report also disclosed that 5,281 wallets holding at least $1 were affected by the exploit. Gnosis Pay published the attacker’s wallet address used during the incident, identifying it as 0x5a7…7a35, while explaining that the exploit targeted two components within its card safe infrastructure, the Delay Module and the Roles Module.

Smart contract exploits continue to pressure crypto platforms

The disclosure comes as security incidents continue to affect crypto infrastructure providers. As crypto.news reported earlier, Humanity Protocol recently confirmed it is repositioning toward enterprise artificial intelligence products after a $36 million exploit accelerated an internal restructuring that had already been under consideration for several months.

During an interview, Humanity Protocol founder Terence Kwok said the company had been reviewing its long-term direction for six to nine months before the breach. He explained that the exploit sped up those plans, while adding that digital identity will remain central because enterprise AI systems will require reliable ways to verify people and credentials.

Meanwhile, concerns over crypto-related cybercrime have also reached government leaders. Earlier, G7 leaders issued a joint statement after their summit in Evian-les-Bains, France, calling for coordinated action against North Korea’s cryptocurrency thefts and cybercrimes.

The statement linked the issue to long-standing concerns that stolen digital assets have helped finance Pyongyang’s nuclear and ballistic missile programs under international sanctions, a claim repeatedly supported by Western governments and blockchain analytics firms.

Bitcoin options traders faced another large expiry on July 3, with 31,000 BTC contracts settling at a notional value of about $1.9 billion.

Summary

- Bitcoin options expiry keeps $60K support in focus as traders demand short-term downside protection.

- Ether options show heavier put demand, pointing to stronger hedging needs around the $1,700 area.

- Weak ETF flows and cautious derivatives positioning keep crypto’s Q3 outlook under pressure.

GreeksLive said in a July 3 update that the batch had a put-call ratio of 0.7 and a maximum pain point of $61,000.

The same update showed 135,000 ETH options expiring with a notional value of about $230 million. Ether’s put-call ratio stood at 1.29, while its maximum pain level was $1,650. The higher put ratio showed stronger demand for downside protection in ETH than in BTC.

Bitcoin reclaims $60K, but risks remain

Bitcoin moved back above the $60,000 level this week, but options data still showed a defensive market. GreeksLive said BTC gamma exposure was concentrated around $60,000, while ETH gamma exposure was centered near $1,700. Those zones may keep short-term price action tied to key strike levels.

In a separate market note, GreeksLive said BTC’s 25-delta skew remained negative across short-term maturities. The firm said puts continued to trade at a premium to calls, with the strongest demand focused on near-term contracts. That suggests traders are hedging immediate downside risk rather than changing long-term expectations.

ETF flows add pressure to sentiment

The cautious options setup follows several weeks of weak spot demand. Bitcoin recently reclaimed $60,000 after softer U.S. macro expectations and easing oil prices helped risk assets recover. However, the same report noted that U.S. spot Bitcoin ETF outflows continued to weigh on the rebound.

Previously, crypto.news reported that Bitcoin struggled to break above $60,000 as options flows and ETF selling kept buyers cautious. The report said U.S. spot Bitcoin ETFs saw nearly $1.79 billion in weekly outflows, their largest withdrawal of 2026.

Earlier expiries showed the same pattern

The July 3 expiry was smaller than last week’s end-of-quarter event, when BTC and ETH faced about $11 billion in expiring options. That larger settlement kept the $60,000 to $62,000 BTC range under close watch as traders tracked hedging flows around major strikes.

As previously reported, another June expiry put the same $60K support zone in focus. GreeksLive said at the time that downside dealer exposure was concentrated near $60,000 to $62,000. The latest data shows that level remains important even after BTC’s mild recovery.

Q3 outlook stays defensive

GreeksLive said in its July 3 post that the crypto market’s Q3 outlook remained weak as attention shifted toward U.S. stocks, artificial intelligence, semiconductors, and tokenized U.S. stock products. The firm also said Bitcoin’s “long-term downtrend has not yet ended,” pointing to selling pressure from large holders and ETFs.

CoinGlass options data also showed total BTC options open interest falling after the large quarterly expiry. Lower open interest can reduce market depth in options, but it does not remove hedging pressure when traders keep paying for puts.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

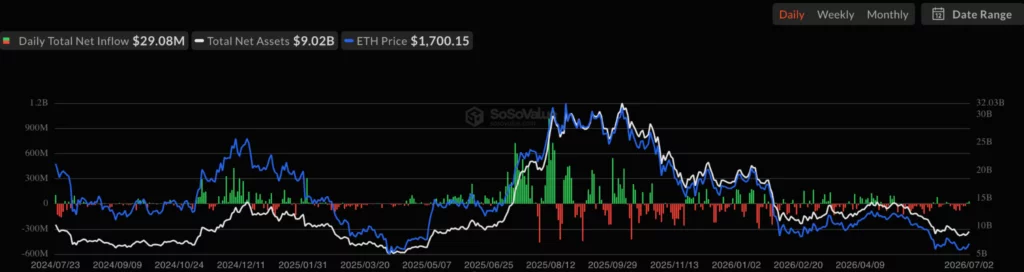

Ethereum price traded near $1,715 on July 3, according to crypto.news price data, after rising more than 6% over 24 hours.

Summary

- Ethereum reclaimed $1,700 as ETF inflows returned, but exchange netflows still warn of selling pressure.

- Monthly TD Sequential signals suggest seller exhaustion, while MACD and RSI show early recovery momentum.

- Binance withdrawal spikes point to accumulation, but rising open interest keeps volatility risk elevated.

The move pushed ETH back above the $1,700 area, a level traders have watched closely after weeks of selling pressure.

The rebound came as U.S. spot Ethereum ETFs returned to inflows. On July 2, spot Ethereum ETFs recorded total net inflows of $29.08 million, according to SoSoValue data. BlackRock’s ETHA led the group with $29.74 million in net inflows, while Grayscale’s ETHE recorded outflows of $2.75 million.

The token had already been eyeing a $1,700 breakout after July 1 ETF inflows returned. That earlier shift helped ease pressure around the $1,500 support region, but ETH still needed a stronger move above $1,700 to improve its short-term chart.

The next area to watch is $1,800. A clean move above that level could show that buyers are gaining control after the recent drawdown. Failure to hold $1,700 may return focus to $1,650 and then the lower support region near $1,500.

Ethereum Technical indicators improve

Ethereum’s short-term indicators are showing better momentum. The MACD histogram is positive near 19.33, while the MACD line sits around -49.01 and above the signal line near -68.34. That confirms the recent bullish crossover has gained strength.

The broader signal is not fully bullish yet because both MACD lines remain below the zero line. This means downside pressure has eased, but the token has not confirmed a full trend reversal. Traders usually look for MACD follow-through toward the zero line before calling a stronger recovery.

The RSI also improved. It stood near 51.85, above its moving average near 38.12. This move above 50 shows buyers are starting to regain control after a weak June.

Crypto analyst Ali Charts said the token has printed a monthly TD Sequential buy signal. In his view, the signal suggests seller exhaustion on a higher timeframe. He also said ETH is approaching a long-term support area near $1,100, which he described as the bottom boundary of Ethereum’s multi-year channel.

Ali Charts pointed to $3,000 as a mid-range recovery target if that lower channel holds. He also placed the broader channel ceiling near $5,000. Those levels are long-term technical targets, not short-term price calls.

ETH/BTC setup draws attention

Ethereum’s performance against Bitcoin is also drawing attention. Crypto Rover said an ETH/BTC golden cross is forming, with the 50-week moving average moving toward a cross above the 100-week moving average. He said the last similar signal in 2021 came before ETH outperformed Bitcoin.

That setup matters because ETH has lagged Bitcoin during the broader market decline. A stronger ETH/BTC pair would show that capital is rotating back toward Ethereum rather than only following Bitcoin’s rebound.

Derivatives data also shows rising activity. According to Coinglass data, ETH volume rose 14.48% to $44.74 billion, while open interest increased 10.64% to $24.54 billion. Options volume climbed 30.19% to $1.41 billion, and options open interest rose 6.67% to $4.43 billion.

Rising open interest can support stronger price moves when buyers lead the market. It can also raise liquidation risk if leveraged positions build too quickly. For that reason, the current derivatives setup points to more volatility rather than a clean bullish trend.

On-chain signals remain mixed

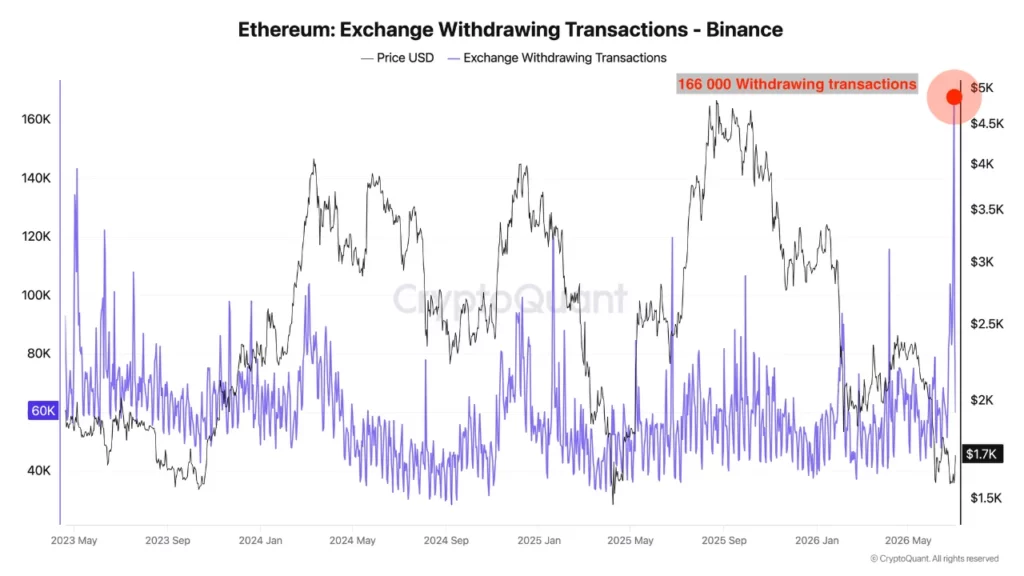

CryptoQuant analyst Darkfost said Binance ETH withdrawal transactions hit their highest level in three years. Binance reportedly logged more than 166,000 withdrawal transactions in one day as ETH rebounded from the $1,500 area.

Exchange withdrawals can point to accumulation when users move coins into self-custody. They can also show funds moving into DeFi for yield. Darkfost said some withdrawals may also reflect confusion around MiCA rules that took effect on July 1, even though withdrawals were not frozen.

Another CryptoQuant analyst, PelinayPA, gave a more cautious reading. The analyst said Binance ETH exchange netflow remained positive at +12,938 ETH, meaning more ETH was moving into the exchange than leaving it. Positive netflow can create selling risk because coins on exchanges are easier to sell.

That contrast keeps the short-term outlook balanced. Withdrawal transactions suggest some users may be accumulating. Positive netflow and rising open interest suggest selling pressure and leverage have not disappeared.

Institutional activity adds support

Ethereum also has support from corporate and institutional activity. As crypto.news reported, Ethereum Institutional launched with backing from BitMine, SharpLink, Joe Lubin, and other contributors to support adoption by banks, asset managers, custodians, and financial firms.

BitMine has continued building its Ethereum treasury. As previously reported, BitMine added 27,084 ETH, lifting its holdings to more than 5.7 million ETH, or about 4.7% of Ethereum’s supply.

SharpLink has also kept buying during weakness. The company bought another 10,000 ETH for $16.1 million as Ethereum tested lower support.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

BTSE has officially entered Indonesia’s regulated crypto market through the launch of BTSE Indonesia after completing the rebranding of local exchange NVX.

Summary

- BTSE has launched a regulated cryptocurrency exchange in Indonesia through a joint venture and the rebranding of NVX.

- The OJK license allows the platform to offer IDR deposits, withdrawals, trading pairs, and other regulated digital asset services.

- The launch comes as Indonesia continues tightening oversight of its cryptocurrency sector with new compliance rules for market participants.

According to an official announcement issued on July 3, the new platform has been established as a joint venture between BTSE Group and PT Aset Kripto Internasional, combining BTSE’s trading infrastructure with local operations focused on customer growth, partnerships, marketing, and sales.

Operating under a license issued by Indonesia’s Financial Services Authority (OJK), BTSE Indonesia is authorized to function as a Digital Financial Assets and Crypto Assets Trading Operator (PAKD). The approval places the exchange among the limited number of regulated entities permitted to offer cryptocurrency trading services in the country while complying with anti-money laundering requirements and customer asset protection rules.

With the regulatory approval in place, BTSE Indonesia can work with Indonesian banks and payment providers to support Indonesian rupiah (IDR) deposits, withdrawals, currency conversions, and IDR trading pairs. The company said the license also creates a path to introduce additional regulated products, including futures trading, subject to rules issued by Indonesian authorities.

Under the partnership, BTSE Group will provide the exchange’s trading engine, liquidity, and underlying technology, while the Indonesian entity will manage local commercial operations using its market knowledge and domestic business relationships.

“Indonesia has everything it takes to be Asia’s next major crypto hub; the population, the demand, and now the regulatory framework. What it needs now is the right combination of global infrastructure and local expertise. That’s exactly what this joint venture delivers,” said Jeff Mei, Chief Operating Officer of BTSE Group.

According Stephanie Kusnadi, Chief Strategy Officer of BTSE Indonesia, added the integration with BTSE gives the company access to global exchange technology while allowing it to continue operating as a platform built around local regulatory requirements and user needs.

Indonesia continues tightening crypto oversight

The launch comes as Indonesia continues introducing new rules for its digital asset industry. In June, the OJK issued Financial Services Authority Regulation No. 6 of 2026, requiring social media influencers who recommend cryptocurrencies and other digital financial assets to obtain competency certification unless they already hold another qualifying license.

Under the same regulation, influencers may promote only digital assets listed on authorized exchanges, while promotional campaigns must be conducted through licensed financial services businesses that remain responsible for the content. The new requirements place additional compliance obligations on digital asset firms operating in Indonesia’s regulated market.

Last month, Cardano’s ADA collapsed below $0.14, the lowest level since the end of 2020. Meanwhile, its market capitalization briefly plummeted to roughly $5 billion, leaving the asset temporarily out of crypto’s top 20 club.

The bulls, though, managed to halt the free fall and even stage an impressive comeback. Here’s what happened and the possible catalysts behind the resurgence.

Green Week for ADA

As of press time, the token is worth almost $0.17, representing a 17% increase over the past 7 days. Perhaps the most evident reason pushing ADA higher is the broader market rebound following de-escalation news out of the Middle East.

Bitcoin (BTC) soared to $62,000, while Ethereum (ETH) surged past $1,700 amid reports that Iran and the USA are set to hold the next round of direct talks in the third week of July after the funeral of the supreme leader Ali Khamenei.

Another catalyst could be the excitement surrounding a Cardano upgrade scheduled to go live on July 6. Namely, this is the RealFi Phase 1 Testnet, described as “the first public step toward next-generation stablecoin infrastructure” on the project.

“Crypto’s clearest success story has scaled as money. But not as capital. Hundreds of billions of dollars sit idle in stablecoins: No utility. No impact on the real economy. We think that’s a problem worth solving – and the Testnet is where we start. During Phase 1, participants can explore the platform, use its core features, and share feedback that will directly shape the protocol. This is collaborative infrastructure-building in public, and we want you involved,” the announcement reads.

Speaking about the upcoming effort was Cardano’s founder, Charles Hoskinson, who called it “the largest upgrade” in the project’s history.

Numerous analysts noted ADA’s revival, arguing it has more fuel left to post further gains. X user Sssebi claimed the token “is on fire” and envisioned a short-term pump to $0.20, while Nehal predicted a jump to $0.23, provided the price holds above $0.16.

Not so Fast

ADA’s recovery shouldn’t be seen as a guaranteed start of a new bull run, as the crypto market remains quite unstable and vulnerable to another severe pullback.

The asset’s Relative Strength Index (RSI) reinforces the bearish outlook. The technical analysis tool, which ranges from 0 to 100, has risen above 70, indicating that ADA is in overbought territory and due for a possible correction. Conversely, ratios below 30 are considered buying opportunities.

The post Why is Cardano (ADA) Up 15% in a Week? appeared first on CryptoPotato.

The artificial intelligence sector is currently dealing with a severe training data bottleneck, especially as centralized technology monopolies are locking out early stage developers from high-quality information pipelines. Decentralized data infrastructure platform Perceptron is trying to address this structural bottleneck by deploying a decentralized infrastructure layer that crowdsources web information through everyday user devices.

Summary

- Perceptron is using idle consumer bandwidth to collect publicly available web data and provide lower cost AI training datasets.

- The platform says its network spans more than 150 countries and rewards contributors while verifying data quality before it is supplied to enterprise clients.

- Perceptron has launched a $10 million AI Data Fund to help developers access data infrastructure and accelerate the development of AI models.

Modern day media is entirely focused on highlighting how leading names in the artificial intelligence space are constantly deploying next-generation hardware systems to buff up their raw computing power. But one of the least talked about operational constraints is the quality of the training data that makes up the core foundation of any functional AI model.

The problem is that with the vast majority of open-web content already thoroughly harvested, aggressive corporate control over public application programming interfaces has locked the remaining foundations of dataset collection behind exorbitant multi-million dollar paywalls. It has essentially become a prohibitively expensive exclusive privilege for a handful of massive tech monopolies.

For the tech giants that are currently leading the AI race, securing these high cost information pipelines aren’t much of a financial challenge, but what about the underfunded innovators? Without the necessary budgets, early-stage startups are left struggling to build competitive products.

“OpenAI pays approximately $60 million to $100 million per year to companies like Reddit and Twitter in order to be able to access data through APIs,” Perceptron Co-Founder & CEO, Peter Anthony told crypto.news during a recent interview.

“Many new AI projects out there don’t have budgets to be able to spend $60 million to $100 million to be able to access data. If you build the best model in the world, it’s pretty useless if it doesn’t have access to good quality data. You could be the smartest kid at school, but if you’re not able to access any books, you don’t really have very much information to present.”

Anthony realized that this market asymmetry leaves room for alternative infrastructure that would serve the independent market segment, which eventually led him to co-found Perceptron, a platform which plans on using idle consumer bandwidth to solve “the data bottleneck problem” AI is suffering from right now.

“The majority of the world’s data has already been accessed and scraped, but there’s a lot of data that’s kind of hidden behind different places that are not yet accessible, so we’re gathering data and positioning ourselves to be able to provide data for AI companies at a reduced cost,” Anthony explained.

Harvesting the idle bandwidth

But what is this idle bandwidth that Perceptron plans to leverage? Anthony explained that this is the unrecognized economic asset that everyday users constantly produce through routine digital browsing, only to watch major corporations extract and profit from it.

“Right now, every time you and I use the internet on our phones, our computers, we’re generating data. That data gets collected, packaged into massive datasets by companies like Google, and sold for millions, sometimes billions of dollars. Yet you and I never see a cent of that value.”

What Perceptron has done is to completely flip this extractive model on its head. They have built a network spanning more than 150 countries comprising roughly 800,000 nodes, and these nodes are powered by individual users who are simply running a browser extension on Chrome or an application on their Android devices.

While these endpoint installations don’t scrape private digital files or provide the firm with sensitive personal telemetry, it instead secures localized geographic perspectives, which Anthony described as “different vantage points” on the open web, which can then be extracted in small pieces and combined into one meaningful dataset.

“It’s very important that we focus on the fact that it’s not using individuals’ data, it’s not tapping into your own personal data and information, but let’s say right now you’re in Malawi. When you’re looking at a particular website, I could go and look at the same website, but chances are, because I’m in Dubai, we’re going to see a different kind of set of results. All we’re gaining from this situation is being able to use your computer to look at something like a normal web page, or whatever it might be.”

To illustrate, Anthony noted that if a corporate client requires a dataset of healthcare-related social media posts from the US, Perceptron can coordinate across its global node mesh to extract individual public posts without interfacing with restrictive enterprise APIs.

Because this data is already freely accessible to the public via any standard web browser, routing the collection through individual terminal nodes legally sidesteps commercial paywalls. Once these minor data packets are retrieved, the network transfers the unrefined data back to a centralized server where specialized artificial intelligence models scrub and audit the information for quality control.

“By doing this, we can cut down the cost significantly that is currently being charged by a lot of the big centralized companies like Google.”

Powered by an economic loop that incentivizes quality network participants

The next question is why would anyone volunteer their hardware to a network like this, and the answer is straightforward, a shared value loop ensuring that these nodes earn points for their passive connectivity that are scheduled to convert into native crypto tokens down the line.

According to Anthony, this distributed model ”will enable them to earn points” that act as a direct metric of their network contribution, and therefore “whenever there’s revenue generated by the company, tokens will get fed back into the ecosystem” to sustain a cyclic economic loop.

“There will also be tokens set aside that are used for buying back tokens,” he added.

However, not everyone running a node essentially qualifies for consistent rewards, as there’s the ever-present challenge of quality control, which can compromise dataset integrity if left unchecked.

Perceptron addresses this by routing gathered packets back to a centralized server, where automated algorithms systematically evaluate the inputs against target benchmarks before releasing any compensation.

Further, Anthony said that the startup recently acquired a company specializing in transaction and payment verification software to structurally automate this validation process.

To further engage network participants while also driving the creation of data sets, Perceptron also plans to launch a structured Data Questing platform, which will allow contributors to turn active human effort into unique training inputs.

“We aim to effectively be able to build datasets and create datasets that are currently not available through centralized processes,” Anthony added.

The end goal

Over the long haul, Anthony said he would like to see the network transition to a business intelligence-focused model that is able to provide deep-layer analytics for enterprise clients.

“The difference is that traditional datasets are static, they’re collected once and quickly become outdated. But there’s an enormous amount of data being generated every time you interact with anything online, and right now, most of it is simply going to waste,” Anthony said.

“One single server trying to monitor all these different users can’t really gather meaningful intelligence at that scale. What we need is a shift toward distributed business intelligence, so we can actually improve services across things like e-commerce, trading, and much more.”

Perceptron has also launched a $10 million AI Data Fund, through which the platform expects to fund independent developers and support the deployment of “actual projects that are providing real services.” Under the terms of the program, selected engineering teams receive five weeks of dedicated data infrastructure assistance and up to 5 TB of real-world data free of charge to accelerate the optimization of early-stage AI models.

“The goal is to support projects as they grow and their data requirements increase. We can become one of their go-to providers, it’s both an investment in the broader ecosystem and a way for us to build consistent, long-term revenue,” Anthony noted.

As of publication time, Anthony said Perceptron is already actively supplying diverse data products to a variety of commercial enterprises. The network provides extensive image datasets to text-to-video generative platforms, including a company called Everlyn AI, to train models to accurately synthesize visual content.

Beyond that, the project is also moving past standard image compilation, as the platform has entered the sentiment analysis sector by tracking public discourse across Twitter, YouTube, and digital asset markets. Analyzing this public sentiment helps crypto firms and exchanges build tracking tools that give early signals to preempt sudden price swings.

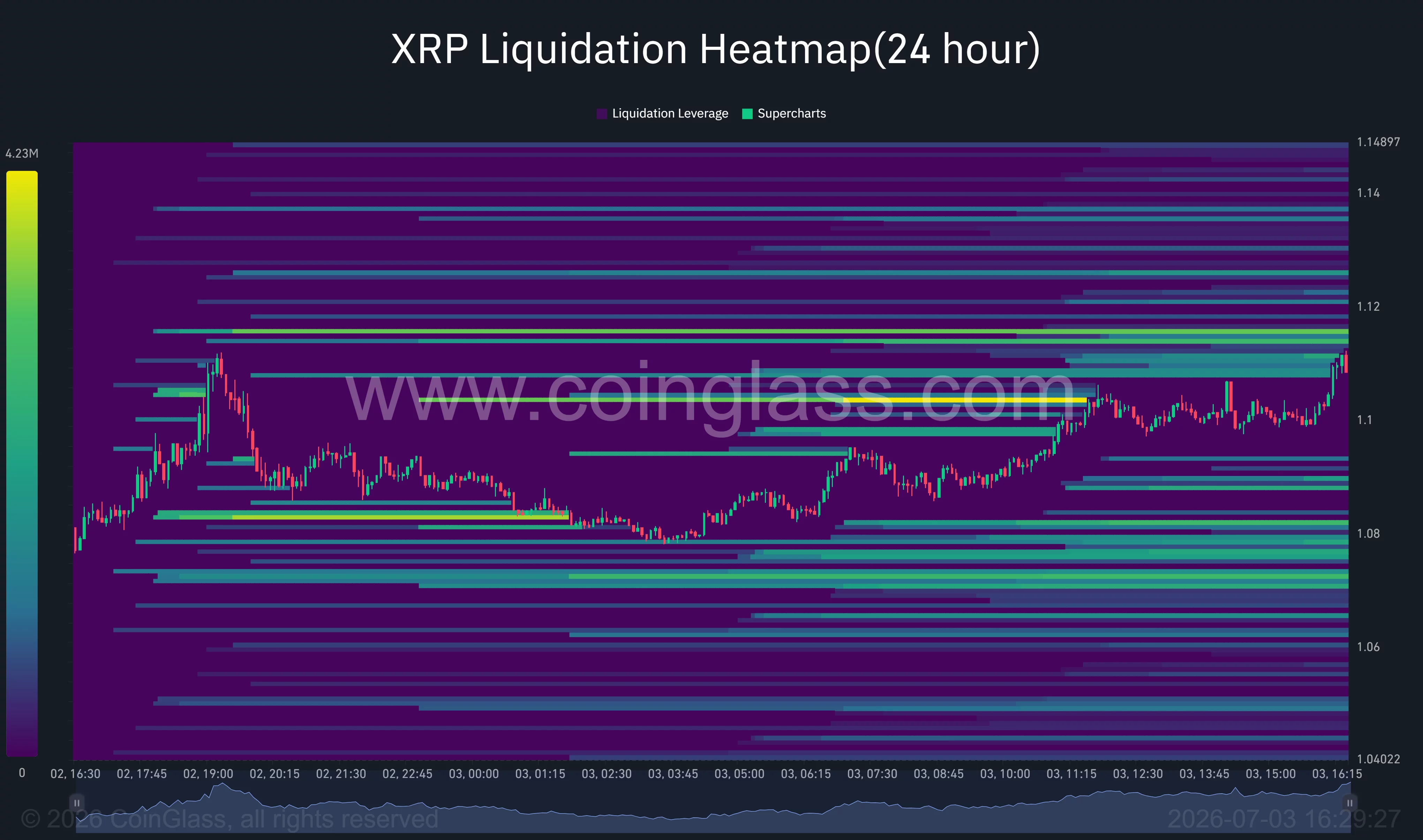

XRP price has climbed to a three-day high after Ripple’s European expansion and a fresh Supertrend buy signal revived bullish sentiment.

Summary

- XRP price climbed to a three-day high as Ripple’s European expansion and stronger market sentiment boosted buying.

- A breakout above a month-long downtrend and a fresh Supertrend buy signal strengthened the bullish outlook.

- Short liquidation clusters above $1.11 could fuel further gains, while $1.05 remains a key support level.

According to data from crypto.news, XRP (XRP) price rose as much as 3% to an intraday high of $1.11 on July 3, extending its recovery from around $1.02 on July 1. The latest rebound follows Ripple’s regulatory progress in Europe, improving macro sentiment, and a bullish technical reversal that has encouraged buyers to return after weeks of sustained selling pressure.

Since July 1, the market has continued to price in the company’s European expansion after Ripple Payments launched under preliminary Crypto-Asset Service Provider approval through the European Union’s Markets in Crypto-Assets framework.

The development arrived just as some competing platforms scaled back parts of their European offerings to comply with MiCA rules, strengthening Ripple’s position in one of crypto’s fastest-growing regulated markets.

At the same time, investors largely dismissed concerns surrounding Ripple’s monthly 1 billion XRP escrow release after recognizing that most of the unlocked tokens are traditionally returned to escrow rather than sold into the market.

Bitcoin’s stabilization above the $61,000 area has also provided a more supportive backdrop for altcoins after weeks of heavy selling pressure. Risk appetite improved further as easing geopolitical tensions helped push crude oil prices to multi-month lows while softer U.S. economic data reinforced expectations that the Federal Reserve could begin easing monetary policy later this year.

These macro developments have encouraged investors to rotate back into higher-beta digital assets after June’s defensive positioning.

Technical breakout puts $1.12 and $1.15 into focus

XRP’s technical structure has improved materially over the past two sessions. On the 1-day chart, price has broken above a descending trendline that had capped every rally since late May, ending more than a month of lower highs. The breakout has carried XRP back toward the $1.12 resistance area after reclaiming the psychologically important $1.10 level.

The 4-hour chart reinforces that bullish shift. XRP has reclaimed its Supertrend indicator near $1.05, while the MACD has completed a bullish crossover with expanding positive histogram bars. Price has also cleared horizontal resistance around $1.075 and is now approaching the next overhead supply zone near $1.125.

A decisive move above that barrier could expose the $1.15 region, while the Supertrend support near $1.05 and former resistance at $1.075 now serve as the first downside cushions.

Commenting on the setup, analyst Ali Martinez wrote in a July 3 X post:

“The SuperTrend indicator has just flashed a buy signal on XRP for the first time since mid-June. The last buy signal preceded a 14% rally.”

Martinez also noted that the indicator had correctly identified the previous 19% and 16% declines, adding weight to the latest reversal signal.

Derivatives positioning has also shifted in favor of bulls. CoinGlass liquidation data shows one of the largest short liquidation clusters sitting just above the current price between roughly $1.11 and $1.12.

XRP has already begun pushing into that liquidity pocket, increasing the probability of additional forced buying if resistance breaks. Beyond that zone, another concentration of leveraged positions sits closer to $1.14, creating a potential path for an extended short squeeze should momentum continue.

On-chain sentiment has strengthened alongside the technical recovery. Sharing data from Santiment, Whale Factor highlighted that XRP’s average trading returns have fallen to their lowest level in roughly 12 years, leaving both short-term and long-term holders underwater.

Historically, deeply negative MVRV readings have often coincided with major accumulation periods before meaningful recoveries. As Whale Factor summarized, “The more frustrated the crowd the faster the snap back when sentiment turns.”

Key risks remain despite the improving trend

The recovery still faces several hurdles before a sustained uptrend can be confirmed. The $1.12-$1.15 region contains multiple layers of technical resistance and dense leveraged positioning that could trigger renewed selling if buyers fail to force a breakout.

Any deterioration in Bitcoin’s price, a resurgence in geopolitical tensions that lifts energy prices, or stronger-than-expected U.S. economic data that delays Federal Reserve rate cuts could quickly reduce appetite for altcoins.

On the charts, a fall back below $1.075 would weaken the current breakout, while a loss of the Supertrend support near $1.05 would place the recent bullish thesis under pressure and raise the risk of another retest of the $1.00 psychological support.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Several major South Korean companies have said they were listed as members of the Open USD (OUSD) stablecoin alliance despite not formally agreeing to participate.

Summary

- Several South Korean companies said they did not formally join the Open USD alliance despite being listed as members.

- Companies including Samsung Electronics and Dunamu said they had only discussed possible participation and had not made any commitment.

- Open Standard said OUSD will let participating firms share reserve income through a consortium based stablecoin model.

According to a report by Chosun Biz, several Korean companies named as participants in the Open USD consortium said they had not held official discussions with the project’s issuer and only became aware of their inclusion after local media reports.

The report said Open Standard announced on June 30 that it had introduced OUSD, a U.S. dollar-backed stablecoin scheduled for launch later this year. The organization said around 140 financial and payment companies from around the world, including Visa, Mastercard, BlackRock, Google and several South Korean firms, would join the consortium. Rather than operating as a decentralized autonomous organization or an equity-based venture, the consortium is expected to function as a cooperative network.

Among the Korean companies listed were Samsung Electronics, Dunamu, Shinhan Financial Group, KakaoBank, K Bank, Hyundai Card, KB Kookmin Card, BC Card, Hana Card, Samsung Card, Woori Card, NH Nonghyup Card and Hanwha.

Several of those companies, however, disputed the implication that they had officially joined.

Samsung Electronics told Chosun Biz it had not held formal consultations with Open Standard and did not know what role it would have within the consortium. Dunamu, Shinhan Financial Group and K Bank also said they had only been asked whether they would be interested in participating and had responded that they would review the proposal.

One company representative told the publication the firm only learned it had been identified as a consortium member through domestic news coverage. The representative added that its response to Open Standard had simply been that it would consider participation if the project developed further, making the company’s inclusion unexpected.

OUSD proposes shared reserve revenue model

Open Standard said OUSD is being developed as a payment and settlement stablecoin operated collectively by participating companies instead of being controlled by a single issuer.

According to the company, participating firms will be able to mint OUSD by depositing U.S. dollars into Open Standard’s reserve account and redeem tokens by returning them to the issuer. The company also said consortium members will be able to mint and redeem OUSD without fees or volume limits.

The project’s revenue model also differs from existing stablecoin issuers. Open Standard said reserve income generated from assets backing OUSD will be distributed to participating partners after operating costs are deducted, unlike issuers such as Tether and Circle, which retain reserve earnings.

Following Open Standard’s announcement that about 140 global companies would participate, Chosun Biz reported that some participants in South Korea’s digital asset industry suggested the project could emerge as a challenger to the stablecoin market currently dominated by Tether’s USDT and Circle’s USDC. However, statements from several companies indicate that at least some of the announced participants have not formally committed to joining the consortium.

Zcash’s planned Ironwood network upgrade in late July is facing a potential scheduling squeeze, after Shielded Labs raised concerns that some parts of the ecosystem may not have enough time to prepare both for Ironwood and for a separate, major software migration.

According to Jason McGee, executive director of Shielded Labs, two large tasks are converging: exchanges, mining pools, and wallet operators must coordinate an infrastructure change as well as the Ironwood activation that is intended to restore confidence in Zcash’s shielded circulating supply. McGee said in a Zcash community forum post that ecosystem participants may have insufficient time to safely deploy and audit the updated systems.

Key takeaways

- Shielded Labs warns that Ironwood’s late-July activation could be delayed because major ecosystem upgrades are being requested at the same time.

- Zcash developers are simultaneously moving away from zcashd toward the Z3 stack (Zebra, Zaino, Zallet), which may require operator changes.

- Ironwood is designed to replace the Orchard shielded pool with a new private pool and add an accounting checkpoint to help verify circulating-supply limits.

- McGee said no final delay has been set, and developers continue security review and system verification work.

Why Ironwood exists: fixing a privacy-pool accounting problem

Ironwood was proposed after researchers discovered an “infinity” bug in Orchard, Zcash’s primary shielded transaction pool. The issue, as described by earlier reporting from Cointelegraph on the Orchard vulnerability emergency upgrade, suggested that an attacker could theoretically create an unlimited number of counterfeit ZEC tokens inside the pool without triggering detection.

Developers emphasized that there was no evidence Orchard had been exploited. Still, because Orchard’s privacy features make it impossible to independently prove that no fake coins were created, Zcash needed a structural change that would let users verify that the shielded circulating supply remains within intended bounds.

Ironwood’s mechanism: a new private pool and supply checkpointing

Ironwood is intended to open a replacement private pool that prevents new activity inside Orchard. As described in earlier coverage of how Ironwood would work, funds leaving Orchard would then pass through an accounting checkpoint designed to stop withdrawals that would imply more ZEC exiting than originally entered.

The practical outcome is that Ironwood should allow ecosystem participants to verify that circulating supply stays inside Zcash’s specified limits, addressing the core trust gap that remained after the Orchard fix.

The other big change: retiring zcashd for the Z3 stack

While Ironwood targets the shielded pool layer, Zcash is also asking infrastructure providers to replace the longtime node and wallet software, zcashd, with a new tooling collection called the Z3 stack. The stack includes Zebra for network node operation, Zaino for providing blockchain data to applications, and Zallet for wallet-related functions.

In documentation about the deprecation of zcashd, Zcash notes that some functions currently offered by zcashd will not have direct replacements, meaning operators may need to modify their systems. The shift is not simply a branding upgrade: it changes how nodes and wallet services integrate with the Zcash network.

McGee’s central warning is that this migration is colliding with Ironwood’s timeline. In his account, some infrastructure providers believe they can complete their transitions by late July, while others still need more time—particularly because not every component is considered production-ready yet.

What Shielded Labs says could happen next

McGee said that Zallet and Zaino were still under development and were not ready for production use at the time of his forum post. The implication is that operators who rely on those tools—or need to rework their workflows around them—may not be able to reach safe readiness by the scheduled activation window.

At the same time, McGee stressed that no delay has been finalized. That matters for traders and users because it leaves room for planning to continue under the expectation of an eventual Ironwood rollout while the ecosystem weighs whether preparation and review can be completed in time.

Zcash founder Zooko Wilcox also weighed in on the status of the work. In a separate discussion on the Zcash community forum, Wilcox said security reviews had not found additional serious bugs so far and that developers are continuing efforts to verify the new system ahead of Ironwood activation. He also acknowledged that the upgrade process involves more than just the shielded pool change itself, reflecting the broader engineering work around Zcash infrastructure.

Notably, the story shows an imbalance between what the upgrade is meant to solve quickly—restoring confidence in shielded supply—and the time it takes to make the broader ecosystem modifications safely, including software replacement and audits by third-party providers.

As late July approaches, the most important watch items are whether Shielded Labs’ concerns translate into an official timing change, and whether infrastructure operators confirm they can complete the Z3 stack migration alongside Ironwood requirements—especially given that some components were described as not yet production-ready at the time of McGee’s comments.

For the first time in the tournament’s near-century of history, a crypto exchange sits inside FIFA’s official partner ecosystem. Six billion viewers, sixteen host cities, one industry trying to prove it has outgrown the arena-naming era. Here is what the deal actually is, and what it has to survive.

Summary

- Kraken became FIFA’s first official crypto exchange supporter, marking the first time a crypto exchange has joined the tournament’s official partner ecosystem.

- The partnership focuses on fan engagement through activations, education, and onboarding as Kraken looks to turn World Cup viewers into long term users.

- The sponsorship reflects a more regulated and compliance focused approach to crypto sports marketing following the industry’s high profile sponsorship failures in 2021 and 2022.

On June 9, 2026, two days before the biggest World Cup ever staged kicked off, FIFA announced something that would have sounded like satire during the last tournament: an official crypto exchange partner. Kraken, through its parent company Payward, became the Official Crypto Exchange Supporter of the FIFA World Cup 2026, the first designation of its kind in the competition’s nearly one hundred years.

The timing was almost comically last-minute. FIFA was still adding sponsors in the final weeks before kickoff, slotting Kraken into the partner stable alongside a Colombian courier company and Salesforce. But the category was brand new, the exclusivity real, and the stage without equal: 48 teams, 104 matches, 16 host cities across the United States, Canada, and Mexico, and a projected cumulative audience of more than six billion people across seven weeks. When Qatar hosted in 2022, crypto’s World Cup presence amounted to Crypto.com signage and a fan token hangover. Four years later, the industry has a seat inside the official partner ecosystem of the most-watched event on Earth.

Whether that seat is worth having is the more interesting question, because crypto’s history with marquee sports sponsorship is a graveyard with famous headstones. This deal is structured differently, arrives in a different market, and will be judged by a different metric. It might still fail. But it will fail or succeed on new terms.

What the deal actually is

Strip away the press-release language and the arrangement has four defining features.

First, it is a category-exclusive partnership with the governing body itself, not with a team, a venue, or a broadcaster. No other exchange can hold the crypto exchange designation for this tournament. That distinction matters commercially: Coinbase, Binance, and the rest of the industry spent years accumulating club deals and stadium naming rights, and Kraken jumped the queue to the sport’s top table in a single announcement.

Second, it is tournament-wide rather than asset-specific. Kraken’s branding attaches to the event, meaning every fixture from the group stage to the final doubles as an impression. The activation window runs the full June 11 to July 19 tournament, and it opened a day early with the FIFA World Cup 2026 Countdown Concert series, a multi-city music event on the eve of the opening match that put the exchange in front of fans before a single ball was kicked.

Third, the deal is structured around fan engagement instead of pure signage. The announced program centers on activations and product experiences across the host cities and Europe: ticket giveaways, educational programming, and onboarding experiences meant to convert viewers into account holders. FIFA’s chief business officer Romy Gai framed the partnership as a fan experience play, and Payward and Kraken co-CEO Arjun Sethi supplied the thesis statement, arguing that football and open financial systems share the same borderless logic and that six billion people watching the same game is the natural audience for money that works the same way everywhere.

Fourth, nobody is saying what it costs. Financial terms remain undisclosed, which is standard for FIFA supporter-tier arrangements but leaves the return-on-investment math to outside guesswork.

The deal did not come from nowhere. Kraken has run a sports playbook for years: partnerships with Tottenham Hotspur, Atletico Madrid, and RB Leipzig in football, a Formula 1 arrangement with Williams Racing running since 2023, and ambassador relationships with transfer-news oracle Fabrizio Romano and World Cup winner Lukas Podolski. The FIFA deal is that strategy graduating from clubs to the institution that governs the sport.

Where a Supporter sits in FIFA’s food chain

The word Supporter in Kraken’s title is doing specific work, and decoding it clarifies both what the exchange bought and what it did not.

FIFA sells commercial access in tiers. At the top sit FIFA Partners, the multi-cycle, global relationships of the Coca-Cola and Adidas variety, with rights spanning every FIFA property. Below them, World Cup Sponsors buy tournament-level global rights for a single edition. Supporters occupy the third tier, typically with regional rather than fully global rights packages; Kraken’s activation footprint concentrating on North America and Europe fits the template, covering the host region and the exchange’s core growth markets while leaving Asia and Latin America outside the headline scope. Salesforce and the Colombian logistics firm Inter Rapidisimo joined at similar levels in the same late window.

The tier matters for cost-benefit math. Supporter packages run at a fraction of Partner economics, historically in the low tens of millions for a tournament cycle against the hundreds of millions that top-tier global deals command. Nobody outside the deal knows Kraken’s number, but the structure suggests the exchange bought the maximum symbolic value, first and only crypto exchange in FIFA history, at the minimum viable rights tier, which is either shrewd procurement or clever hedging depending on how the activation performs. The category exclusivity is the asset with option value: if the tournament converts, Kraken holds the incumbent’s chair when the 2030 rights negotiation starts, and category incumbents historically get first refusal.

There is a precedent inside the tournament itself for how crypto categories evolve. Crypto.com entered the FIFA ecosystem as a Qatar 2022 sponsor when the industry was still radioactive from that year’s collapses, and its presence was mostly signage. Four years later, the category has a named exchange tier, a blockchain running FIFA’s own collectibles, and a prediction market partner. Commercial categories at mega-events tend to ratchet: once a governing body books the revenue, the line item survives, and the only question is which company’s logo fills it.

The 2021 wave, and why it drowned

To measure how different this deal is, run the tape back to the last time crypto money flooded sports.

Between early 2021 and mid-2022, the industry committed billions to sports marketing in the space of eighteen months. Crypto.com paid $700 million for twenty years of naming rights to the former Staples Center and layered UFC, Formula 1, and World Cup deals on top. FTX put $135 million on the Miami Heat arena, bought the naming rights to MLB umpire patches, sponsored Mercedes in F1, and made Tom Brady and Steph Curry brand faces. Coinbase became the NBA’s exclusive crypto platform partner. Binance signed African football legends and Italian club deals. Even mid-tier exchanges bought jersey patches and stadium signage, and Kraken itself entered the era with its Tottenham, Atletico, and RB Leipzig arrangements.

The wave’s logic was customer acquisition at mania prices: exchanges were earning record trading fees, retail was pouring in, and sports offered the largest untapped audiences on Earth. The unwinding was faster than the building. FTX’s deals became bankruptcy-court exhibits, with the Heat arena renamed and the Mercedes logos removed mid-season. Crypto.com’s commitments, signed at the top, became the textbook case of pro-cyclical marketing. League partners quietly let crypto deals lapse; the NBA relationship wound down; jersey patches vanished. By 2023, sports business publications ran post-mortems on the crypto sponsorship era as a closed chapter, and the surviving deals, Kraken’s F1 and club portfolio among them, kept notably lower profiles.

The lesson the survivors internalized was not that sports marketing fails. It was that sports marketing amplifies whatever the sponsor already is. FTX’s sponsorships did not cause its fraud, they broadcast it; Crypto.com’s deals did not cause the bear market, they timestamped it. Amplification cuts the other way too, which is the bet Kraken is now making: a compliance-forward, fifteen-year-old exchange amplified across six billion impressions projects durability, provided the underlying story holds.

The 2021 wave drowned because the sponsors’ fundamentals could not survive their own visibility. That is the specific failure mode this deal was structured to avoid, and the one that remains entirely in Kraken’s hands.

The ghosts this deal has to outrun

Any analysis of crypto sports marketing has to walk through the cemetery first, because the industry’s previous splashes at this scale ended as cautionary tales.

FTX put its name on the Miami Heat arena and collapsed into fraud proceedings; the county spent months legally scrubbing the branding off the building. Crypto.com committed $700 million to rename the Staples Center and stack UFC sponsorships at the exact peak of the 2021 mania, a timing decision that became shorthand for bull-market excess within a year. Fan tokens sold to supporters during the Qatar cycle bled value the moment the tournament ended. By early 2023, crypto sports marketing was the punchline in every retrospective about the bubble.

The comparison Kraken has to defeat is not really about logos. It is about what the sponsorships revealed: companies buying legitimacy with customer deposits at cycle tops. Three structural differences give this deal a fighting chance at a different ending.

The buyer is different. Kraken is one of the longest-operating exchanges in the industry, founded in 2011, serving users in more than 190 countries, and it spent the FTX era being the boring firm that published proof-of-reserves. Its parent Payward has been expanding into regulated territory, including opening tokenized US IPO access to retail investors this spring.

The market is different. The deal was struck during a drawdown, with Bitcoin near $61,000, sentiment indexes in fear territory, and the market trading like leveraged tech exposure, not during a euphoria top. Sponsorships signed in bear conditions tend to be priced on strategy instead of vanity.

The counterparty is different. FIFA accepting a crypto exchange into its official ecosystem, after watching the FTX era unfold, is itself the reputational signal. Governing bodies are conservatism machines; their sign-off implies diligence that a stadium landlord never performs.

None of that guarantees the deal works. It only means the failure modes of 2021 do not map cleanly onto 2026.

The tournament crypto built around the deal

What makes this genuinely crypto’s first World Cup is not the Kraken logo alone. It is that the sponsorship sits inside a tournament where blockchain infrastructure runs through nearly every commercial layer.

FIFA moved its own collectibles platform, FIFA Collect, onto a custom Avalanche-based network it calls the FIFA Blockchain, built to carry digital collectibles and ticketing features. ADI Predictstreet operates as FIFA’s first official prediction market partner, running on Chainlink oracle infrastructure. And beyond the official perimeter, the parallel economy has been enormous: prediction markets processed billions in World Cup wagers, with combined June volume across the major venues hitting $44.8 billion, a story we cover in depth in our companion feature on Polymarket’s tournament.

The fan token layer adds the retail texture. Chiliz-powered Socios tokens tied to national teams have traded through every knockout swing: Portugal’s $POR token, now available omnichain including on Solana, moves with every Cristiano-era nostalgia run, while Argentina’s $ARG volume climbs as the favorites advance. The pattern is well documented and brutal: engagement spikes during group stages, peaks in knockouts, and collapses when a side goes home. Elimination is a token event. A team’s exit can crater its token overnight, which makes fan tokens less an investment class than a volatility instrument wearing a scarf. The Qatar cycle wrote the reference chart: national team tokens ran up through the group stage, peaked around the knockouts, and gave back most of the move within weeks of the final, a decay curve every trader in this market now prices from memory. Traders sizing positions around match outcomes are effectively running event-driven strategies with concentrated single-name risk, closer to cross-margined derivatives exposure than to holding a fan club card, and the thin liquidity means exits get expensive at exactly the moments everyone wants one.

The on-pitch product has cooperated with the commercial one. England’s Round of 32 comeback against DR Congo, sealed by two late Harry Kane goals, was the country’s first World Cup win from behind since the 1966 final and played out under Kraken-branded boards to a global broadcast audience. DR Congo’s first knockout appearance since 1974, Cape Verde emerging from a group containing Spain and Uruguay, and a bracket pointing toward a possible France and Argentina rematch have kept audiences, and therefore impressions, at maximum through three weeks.

What Kraken actually has to sell the fans it reaches

Awareness only converts if there is a product on the other end of the funnel, and the shape of Kraken’s 2026 product surface explains why the exchange believed a mass-audience play was worth buying now instead of in 2021.

The core exchange remains the anchor: spot trading across the majors in 190-plus countries, with the fifteen-year operating history and proof-of-reserves posture doing the trust work that a first-time depositor needs. Around it, the offering has widened into exactly the products a football fan is likelier to want than an order book. Payward opened tokenized access to US IPOs for retail investors this spring, part of a broader tokenized equities push that turns “invest in things you know” into an on-chain pitch. Staking products give the passive audience a reason to hold instead of churn. Payments and card products make a funded account useful between trades. And the Formula 1 and club partnerships already taught the firm which fan-facing mechanics convert, knowledge now being redeployed at tournament scale.

The sequencing matters more than any single product. A ticket-giveaway sign-up costs the fan nothing and creates a verified account; an app install during a host-city activation puts the exchange one notification away; a first deposit, even a small one, starts a relationship whose lifetime value the exchange measures in years. This is the standard consumer fintech ladder, and the World Cup is functioning as its top rung.

The 2021 wave mostly bought the billboard and skipped the ladder. The difference between those two designs is the difference between impressions and customers, and it is the entire operational thesis of this deal.

Running the numbers on success and failure

Since the fee is undisclosed, precise return math is impossible, but the scenario logic is straightforward enough to sketch, and it clarifies what a win would even look like.

Assume a Supporter-tier package in the low tens of millions, consistent with FIFA’s historical tier structure. Consumer crypto exchanges have paid anywhere from $50 to several hundred dollars to acquire a funded account through paid channels during competitive periods. At a blended $100 acquisition cost equivalent, a mid-tens-of-millions deal needs a few hundred thousand funded accounts across the seven-week window and its afterglow to beat Kraken’s alternative marketing spend, a conversion rate measured in the low ten-thousandths of the six-billion-viewer audience. Framed that way, the bar is strikingly low, which is precisely why exchanges chased sports at mania prices last cycle.

The catch is in the words funded and retained. Sign-ups from giveaways are cheap and mostly worthless; deposits are the product, and deposit behavior among sports-acquired users is the great unknown. The Qatar-cycle evidence says event-driven crypto interest decays within weeks. The counter-evidence from this tournament, majority-newcomer participation in prediction markets, regulated on-ramps in most target jurisdictions, says the friction that killed past funnels has thinned. Kraken’s dashboard will settle it privately; the public will read the answer in whether the exchange renews for 2030 and whether competitors bid the category up.

Renewal is the tell, and it arrives on a public calendar. Nobody re-buys a failed sponsorship at a mega-event, and nobody with a functioning commercial team lets a working one go to a rival.

The only metric that matters

Six billion cumulative viewers is a marketing number. The business question is narrower and colder: how many of them open a Kraken account, and at what acquisition cost relative to the undisclosed fee.

This is where the fan engagement structure earns its keep or does not. Signage builds recall; activations build funnels. Ticket giveaways require sign-ups. Product experiences at host-city events end with an app install. Educational programming is onboarding content wearing a lanyard. Every mechanism in the announced program points at conversion, which means the deal’s success is measurable in a way the arena-naming era never was, even if only Kraken and Payward see the dashboard.

The skeptical read has real evidence behind it. Sports viewers are not natural traders, and the crossover audience may be smaller than the impression counts imply. The Panama fixture drew $1.76 million in prediction market wagers while the on-chain response in adjacent assets barely registered, and even England’s marquee comeback produced no meaningful fan token volume for either side, a reminder that attention and allocation are different behaviors. Seasonal decay is the default outcome for tournament-driven crypto activity, with the Qatar cycle as the controlling precedent.

The optimistic read has newer evidence. Prediction market user studies during this tournament found a majority of active participants had no prior on-chain history at all, direct proof that the World Cup is reaching people crypto never touched. Regulatory infrastructure that did not exist in 2022, from MiCA in Europe to spot ETFs and commodity classifications in the US, means a curious viewer in most of Kraken’s target markets can now act on the curiosity legally and simply. The funnel from broadcast to wallet has never had fewer broken steps.

Three host countries, three rulebooks

There is also a jurisdictional wrinkle the tournament map makes vivid, and it deserves its own accounting because no previous sponsor in this category ever had to solve it.

The United States hosts the majority of matches, including the final, and offers Kraken its most valuable and most complicated market. Federal clarity has improved dramatically since 2022, with commodity classifications, spot fund approvals, and the ETF flow battle now shaping institutional allocation, but the state layer remains a patchwork: adjacent products like event contracts face active gaming-commission litigation in more than a dozen states, and marketing rules for financial products vary by jurisdiction in ways that make a uniform national activation legally impossible.

Canada brings provincial securities regulators with registration regimes that have already pushed several international exchanges out of the market entirely; operating activations in Vancouver and Toronto means satisfying regulators that have historically been among the strictest in the G7. Mexico sits at the other extreme, with a fintech law that predates the modern crypto industry and enforcement capacity that leaves large gray zones.

Europe, the other half of the activation footprint, is paradoxically the easy part. MiCA gives Kraken a single passportable framework across the EU, which is why a fan in Austria or Germany can move from broadcast to funded account with less regulatory friction than a fan in the host countries themselves. The asymmetry is a small preview of the industry’s strange 2026 geography: the tournament is in North America, but the cleanest conversion funnel runs through Brussels.

For Kraken, the patchwork is a cost. For the category, it is a moat. Any rival weighing a bid for the 2030 slot now knows the compliance overhead a global football activation carries, and incumbency in that knowledge is worth almost as much as the logo rights.

The scoreboard after the final

Crypto’s first World Cup has already produced its symbolic result: the industry is inside the perimeter, on the boards, in the partner list, treated by the sport’s governing institution as a normal commercial category rather than a reputational hazard. Given where crypto sports marketing stood three years ago, that alone is a recovery arc worth noting.

The financial result stays open past July 19. If Kraken converts even a sliver of six billion impressions into funded accounts, the deal becomes the template, and the 2030 tournament will have exchanges bidding for the category the way airlines bid for alliance slots. If the activity decays on schedule and the funnel leaks, the deal joins a quieter graveyard, the one for sponsorships that were merely expensive instead of catastrophic, and the industry learns that legitimacy and growth are separate purchases.

Either way, the precedent is set and cannot be unset. A World Cup now comes with a crypto exchange the way it comes with an airline and a soft drink. Whether that turns out to be the moment adoption bent upward or just the most expensive brand-awareness campaign in the industry’s history is a question with a hard deadline: the next four years, starting at full time on July 19. For a sector that measures its own maturity in cycles, the 2026 tournament will be remembered as the one where crypto stopped crashing the party and got printed on the invitation.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Digital asset markets are volatile and you can lose your entire investment. Always do your own research. Information current as of July 3, 2026.

Billions of dollars in prediction market positions settle every month based on a machine for deciding truth that most traders have never examined. This guide explains how UMA’s optimistic oracle turns real-world events into on-chain payouts, why the system usually works, the cases where it has failed spectacularly, and the rival settlement designs trying to replace it.

Prediction markets had their breakout year in 2026. Combined volume across the major venues hit $44.8 billion in June alone, driven by a World Cup that turned Polymarket into a multi-billion-dollar sportsbook. The trading side of these platforms is easy to understand: shares in Yes or No, priced between zero and one dollar, paying out one dollar if you are right. The hard part is invisible until it breaks. Someone, or something, has to decide what actually happened.

That decision layer is called resolution, and it is the load-bearing wall of the entire sector. A prediction market is only as good as its ability to decide truth, and a blockchain cannot observe the real world. It cannot see who won an election, whether a company sold an asset, or whether a bill passed. The bridge between reality and the smart contract is an oracle, and for the largest on-chain prediction market, that oracle is UMA. Understanding how it works, and how it fails, is the single most useful piece of due diligence a prediction market trader can do.

The oracle problem, event edition

Crypto solved one version of the oracle problem years ago. Price feeds from networks like Chainlink and Pyth deliver asset prices on-chain by aggregating data from many independent publishers. That works because prices are public, continuous, machine-readable, and available from dozens of redundant sources.

Event markets break every one of those assumptions. The questions are one-off rather than continuous. The answers often live in press releases, court rulings, regulatory filings, or a referee’s whistle. And the phrasing matters enormously: a market asking whether a politician says a specific word five times needs a resolution process that can read, interpret, and withstand challenge. No price feed can answer questions like that. What the sector needed was an oracle for arbitrary facts, with a built-in way to contest wrong answers.

Enter UMA and optimistic verification

UMA, short for Universal Market Access, is an oracle protocol built by Risk Labs. Its core product, the Optimistic Oracle, resolves outcomes for Polymarket’s main venue, which cleared around $14 billion in monthly volume during the World Cup peak. The word optimistic describes the design philosophy: submitted answers are assumed true unless someone challenges them, with economic incentives doing the policing instead of a central referee.

The flow for a typical Polymarket market runs through a version of the oracle called OOv2, and it has four stages:

- Request. When a market’s end conditions are met, the market contract asks the oracle for the outcome, referencing the exact resolution criteria written when the market was created.

- Proposal. A proposer submits the answer, Yes or No, and posts a bond of $750 in USDC. If the proposal is wrong, the bond is forfeited. If it stands, the proposer earns a reward.

- Challenge window. The proposal sits open for two hours. Anyone who believes it is wrong can dispute it by posting a matching bond.

- Escalation. If a dispute lands, the question goes to UMA’s Data Verification Mechanism, the DVM, where UMA token holders research the question and vote on the correct answer. Voters who side with the final outcome earn rewards; voters who miss or vote against it lose a slice of their stake. The DVM’s ruling is final, the losing bond pays the winner, and the market settles.

To make that concrete, follow one uncontested market through its whole life. A market opens asking whether a central bank cuts rates at its June meeting, with resolution criteria naming the official statement as the source. Traders price Yes at 70 cents through the month. The decision lands at 2 p.m., the statement confirms a cut, and within minutes an approved proposer submits Yes with the $750 bond. For two hours, anyone on earth with a matching bond could object; nobody does, because the statement is public and unambiguous. The window closes, the oracle reports Yes to the market contract, and every Yes share becomes redeemable for one dollar in USDC. Total elapsed time from event to payout: under three hours, no human authority involved, no appeal needed. That is the experience for the overwhelming majority of markets, and it is why the system scaled.

The bond arithmetic deserves a sentence of its own, because it is the whole security model in miniature. Seven hundred fifty dollars sounds trivial next to markets carrying tens of millions in open interest, and read one way, it is: a wrong proposal on a whale-scale market risks $750 to potentially swing a payout worth thousands of times that. The design’s answer is that the bond does not defend the market alone, the challenge window does. A false proposal only profits if nobody in the world notices for two hours, on a venue where every large market has thousands of position holders watching resolution like hawks and a matching bond waiting for whoever catches the error. The bond prices the cost of forcing a dispute, not the value of the market, and the escalation layer is supposed to carry the real weight. That framing also locates the true weak point precisely: the system is only as strong as the layer disputes escalate to.

The percentages favor the happy path. Roughly 99% of assertions since 2021 have gone undisputed, meaning most markets settle in the two-to-four-hour window after an event without any human argument. The system processes upward of 7,000 proposals per month, and Risk Labs has automated much of the pipeline: language models draft proposals for around half a cent per request, and bots like OOTruthBot summarize evidence threads and flag suspicious submissions, cutting routine resolution from hours to seconds.

Inside the DVM: what a token vote actually looks like

Since the DVM is the backstop everything escalates to, its mechanics deserve a closer look than most traders ever give them.

When a dispute triggers a vote, the question enters a voting round for UMA token holders who have staked into the voting system. Voting runs in two phases. In the commit phase, each voter submits an encrypted vote, hidden from everyone including other voters, which prevents late voters from simply copying the visible majority. In the reveal phase, voters decrypt and publish what they committed. Votes are weighted by staked tokens, and the outcome that carries the stake-weighted majority becomes the oracle’s answer.

The incentive design is the load-bearing part. Voters who land with the final outcome earn rewards from protocol emissions. Voters who miss a round or land against the outcome lose a slice of their stake. The design intends to pay for diligence, and it mostly does, but it carries a known theoretical flaw inherited from every majority-rewarded oracle: the profitable strategy is voting with the expected majority, not with the truth, and in ordinary cases those two targets coincide. The failure cases are the ones where they separate, and where a large holder can make the majority whatever they need it to be.

There is also a timing cost. An undisputed market settles within hours; a disputed one waits for the full commit and reveal cycle, stretching resolution to days while positions stay frozen and traders argue in evidence threads. For anyone holding size, a dispute is not just a risk to the payout but a lockup on capital.

In November 2025 the system got its most significant overhaul, the Managed Optimistic Oracle V2. MOOv2 restricted the right to propose resolutions to 37 pre-approved addresses, a mix of Risk Labs staff and Polymarket users with high historical accuracy, while keeping disputes open to anyone. The change targeted premature and spam proposals, which had been a chronic source of delays and gamesmanship. Proposing became curated; challenging stayed permissionless.

Where the machine breaks

The design has one structural soft spot, and 2026 has stress-tested it in public: the final arbiter is a token vote, and tokens can be bought, concentrated, and conflicted. The numbers behind that concern are not speculative. A Wall Street Journal investigation published in May found that in most disputed Polymarket markets, more than half of the UMA votes came from the ten largest wallets. At least 60% of active UMA voters could be linked to live Polymarket accounts, and roughly one in five disputes had at least one voter with a financial stake in the market they were ruling on. The dispute pipeline itself is swelling: Polymarket logged more than 1,150 disputed markets in the first five months of 2026, already past its full-year 2025 total.

Two cases show what that looks like in practice.

The first was a 2025 market on a United States minerals agreement, where a single large UMA holder cast five million tokens across three accounts, about 25% of the vote in that dispute round, pushing a contested market to resolve early against the plain reading of events. Traders on the wrong side of that ruling lost roughly $7 million. The vote was legal under the system’s rules. That was precisely the criticism.

The second came in June 2026 and drew more than $60 million in volume: a market asking whether Strategy would sell any Bitcoin by May 31. A regulatory filing published on June 1 disclosed that the company had sold 32 BTC between May 26 and May 31 at an average price of $77,135, its first disposal since 2022, inside the market’s cutoff. Two proposed resolutions were challenged, the question escalated to a token vote, and the market ultimately resolved No. Shares tracking the documented answer traded at 12 cents while the dispute ran. Critics across the industry framed the episode as a structural verdict: when ambiguous rules meet concentrated voting power, the payout can diverge from the facts, and the holders of the settlement token can be the same people holding positions in the market being settled.

None of this means most markets resolve wrongly. The overwhelming majority settle cleanly and fast. It means the tail risk is governance-shaped: the worst outcomes cluster in high-volume, ambiguously worded markets where a motivated whale has both the tokens and the position.

Why Polymarket keeps the system anyway

Given the 2026 dispute record, the obvious question is why the largest on-chain venue has not replaced its oracle. The answer is a stack of practical reasons that critics tend to skip.

The happy path really is that good. Ninety-nine percent of markets settling within hours, at a cost of fractions of a cent per automated proposal, across every category from elections to award shows, is a service level no alternative currently matches for open-ended questions. Deterministic settlement cannot touch subjective markets at all, and regulated clearing brings jurisdiction constraints that would gut the international product.

The system also iterates. MOOv2 was a direct response to the proposal-spam era and measurably cut premature resolutions. The language model pipeline and evidence bots were responses to speed and quality complaints. Bond sizes, challenge windows, and proposer sets are all tunable parameters, and Risk Labs has shown willingness to tune them under pressure. Whether tuning can fix a voting-power concentration problem is the open question, since the DVM backstop itself is the part no parameter change reaches.

And there is a structural argument: for a venue whose regulatory story leans on decentralization, outsourcing truth to an external token-holder process is a feature. Polymarket does not decide outcomes, and that sentence has legal value. The company’s answer to the United States market was not to change the oracle but to split the product, running the domestic venue through a CFTC-regulated framework while the international book kept UMA. The two-track structure is itself a verdict on where each settlement model belongs.

The rival designs

The dispute wave has made resolution architecture a competitive battleground, and three alternative models are now live at scale.