Crypto World

Binance outflows triple as ETH withdrawals hit 3-year high

Binance recorded about $1.23 billion in net outflows during the week beginning June 29, according to DefiLlama data reported by Cointelegraph. The figure was up 207% from about $400 million in the previous week.

Summary

- Binance ETH withdrawals hit a three-year high as users moved coins away from the exchange.

- Weekly Binance outflows tripled to about $1.2b while monthly exits reached nearly $3.2b.

- Analysts linked the spike to accumulation, MiCA uncertainty and short-term positioning around Ethereum’s rebound.

The exchange also recorded about $3.2 billion in monthly net outflows. The move showed that users were moving more funds away from the world’s largest crypto exchange by trading volume.

The outflows came as market focus turned to Ethereum withdrawals from Binance. Data from CryptoQuant showed more than 166,000 ETH withdrawal transactions in one day.

https://x.com/cryptoquant_com/status/2072980165341401496?s=20

CryptoQuant community analyst Darkfost said the level had not been seen in more than three years. The spike marked the highest Binance ETH withdrawal transaction count since March 2023.

ETH withdrawals point to accumulation

Darkfost said the move “could reflect genuine demand building around the $1,500 level.” He said some investors may have taken exposure and moved funds off the exchange instead of keeping them ready for short-term trading.

Exchange withdrawals can suggest long-term holding when users move assets into private wallets. Still, the data does not confirm one clear reason. Some withdrawals may also come from short-term positioning, risk control or platform changes.

Crypto.news reported that ETH reclaimed the $1,700 area as ETF inflows returned. The report also said Binance withdrawal spikes pointed to possible accumulation, while rising open interest kept volatility risk active.

Ether also recovered during the same period. Cointelegraph reported that ETH rose about 12.5% over seven days and traded near $1,766 at publication time, while Bitcoin gained about 4.3%.

MiCA rules add pressure on Binance

The withdrawals also came during a key regulatory change in Europe. The European Union’s MiCA framework entered full force on July 1, requiring crypto firms to hold proper authorization to serve users across the bloc.

Crypto.news reported that Binance reassured EU users as the changes began. Binance said affected users’ assets remained safe and held on a one-to-one basis.

Binance CEO Richard Teng said users would still have access to communicated options, including withdrawals. His comments came after the exchange missed the full MiCA licensing deadline and adjusted some services in the region.

Crypto.news also reported that Binance would suspend most services for EU residents after failing to secure a MiCA license by the deadline. The report said withdrawals remained available and described the move as a suspension, not a permanent exit.

CEX flows remain split

Other centralized exchanges also recorded weekly outflows. Cointelegraph reported that Bitfinex saw about $407.5 million in outflows, while Gate recorded about $214.3 million. OKX and Bybit also posted smaller weekly exits.

Inflows were more limited and spread across fewer platforms. Crypto.com recorded about $63 million in net inflows, while HashKey Exchange added about $53.3 million. KuCoin, Gemini and Bitvavo also saw smaller inflows.

The flow data showed a split market. Some users moved funds away from large trading venues, while others shifted assets to different platforms. The pattern matched a week shaped by ETH’s rebound, MiCA changes and cautious market positioning.

As of then, Binance’s ETH withdrawal spike remains open to more than one reading. It may show accumulation near lower ETH levels, but it also reflects a market where users are watching regulation, exchange access and short-term price risk closely.

South Africa’s Revenue Service has published draft guidance on how crypto assets should be taxed under the country’s current tax laws. The proposal seeks public feedback until August 31, 2026, before SARS moves toward a final version.

Summary

- SARS says crypto is not currency, keeping digital assets inside income and capital gains rules.

- The draft treats trades, swaps and crypto payments as possible tax events under current law.

- Public comments remain open until August 31 as South Africa clarifies crypto tax reporting.

The draft does not create a new crypto tax law. It explains how current rules under theIncome Tax Act, 1962 may apply to people who buy, sell, swap, spend, mine, stake or receive crypto assets.

SARS says the guide covers selected income tax and capital gains tax issues linked to crypto. It also says the draft does not deal with value-added tax, meaning VAT treatment remains outside the scope of this document.

Crypto treated as an asset, not money

The draft repeats SARS’ long-held position that crypto assets are not legal tender or foreign currency. Instead, SARS treats them as intangible assets for tax purposes.

The agency said “crypto assets are not ‘currency’ and, consequently not ‘foreign currency’.” That wording matters because it places crypto inside current income and capital gains rules rather than foreign exchange rules.

Crypto.news previously reported that SARS had already viewed crypto as an asset of an intangible nature. The new draft expands that position into a more detailed guide for taxpayers.

The draft says tax treatment depends on the facts of each case. A person who trades often may face income tax treatment, while a long-term holder may fall under capital gains tax if the facts support that view.

Trades, swaps and spending may trigger tax

The draft guide says selling crypto for fiat may create a tax event. It also covers crypto-to-crypto swaps, crypto payments for goods or services, mining, staking, airdrops, hard forks and decentralized finance activity.

SARS places strong weight on the taxpayer’s intention. It says officials may assess why a person bought the asset, how long they held it, how often they traded and what they planned to do with it.

The agency said “a taxpayer’s intention regarding an asset may change over time.” This means a person may start as a long-term holder but later act more like a trader if their behavior changes.

The draft also says donations tax may apply because crypto can fall within the meaning of property. That may matter when a person gives crypto away without receiving payment in return.

Reporting pressure grows as adoption rises

SARS already says normal income tax rules apply to crypto assets. Taxpayers must declare crypto gains or losses in the tax year in which they receive or accrue them.

The tax authority also says failure to declare taxable crypto income can lead to interest and penalties. It has broad legal powers to collect third-party financial data during tax checks.

South Africa has also adopted theCrypto-Asset Reporting Framework. Under CARF, crypto service providers must collect and report selected user and transaction data to SARS.

The first CARF reporting period runs from March 1, 2026, to February 28, 2027. SARS says individual taxpayers do not file CARF reports directly, but they must still declare crypto transactions in their income tax returns.

The draft arrives as South Africa remains one of Africa’s larger crypto markets.Chainalysis said South Africa received about $26 billion in crypto value over a one-year period covered in its 2024 regional report.

The public comment window gives users, tax advisers and crypto firms time to respond. For now, SARS is seeking clearer treatment under existing law, not a separate tax system for digital assets.

Key Takeaways

- Micron’s Q3 results showed revenue of $41.46 billion, representing a 346% year-over-year surge, with earnings per share of $25.11 crushing expectations by more than $4.

- CEO Sanjay Mehrotra explained to Jim Cramer that the memory chip supply crisis is structural rather than cyclical, with new manufacturing facilities delayed until 2027–2028.

- Both HBM3E and HBM4 memory products are completely sold out through 2027, supported by $22 billion in advance customer deposits from hyperscalers.

- The company has delivered over $1 billion in HBM4 shipments and asserts technological superiority over competitors SK Hynix and Samsung in DRAM and NAND sectors.

- MU shares are currently trading around $970, retreating from their 52-week peak of $1,255, while maintaining approximately 244% gains year to date.

Micron Technology (MU) shares are hovering near $970, having pulled back from the 52-week high of $1,255 reached on June 25, yet the stock maintains impressive gains of approximately 244% year to date. Despite the recent decline, the fundamental narrative remains robust — a point CEO Sanjay Mehrotra emphasized during his appearance on Jim Cramer’s Mad Money on June 30.

Cramer posed the question dominating investor sentiment: what’s the timeline for resolving the memory shortage? Mehrotra’s response was unambiguous.

“The industry requires greenfield capacity. This means brand new construction of clean rooms. Those clean rooms require substantial time from initial groundbreaking to producing the first wafers.”

The company’s initial Idaho fabrication facility will begin wafer production by mid-2027, with full-scale manufacturing ramping predominantly throughout 2028. A secondary Idaho fab becomes operational by late 2028. The New York manufacturing site follows subsequently. Translation: the supply constraints persist for years.

Cramer previously highlighted Micron’s Q3 performance as among the most impressive earnings surprises he’s witnessed. The figures validate that assessment. Revenue totaled $41.46 billion, representing a 346% year-over-year increase from $9.30 billion. Non-GAAP earnings per share reached $25.11, surpassing the $20.78 consensus estimate. Free cash flow climbed to a company record of $18.30 billion.

The Q4 outlook is equally remarkable: $50 billion in projected revenue, approximately 86% gross margins, and anticipated EPS of $31.00.

HBM4 Technology Breakthrough

Both HBM3E and HBM4 memory products are entirely sold out through the end of calendar year 2027, with order backlogs already stretching into 2028. Major hyperscalers have deposited $22 billion in advance payments to guarantee future supply.

During the earnings conference call, Mehrotra revealed that Micron had already delivered over $1 billion worth of HBM4 products. This milestone transcends simple revenue metrics — it represents a technological achievement. HBM4 ranks as the most sophisticated memory product globally to manufacture, and Micron stands as the sole U.S.-based producer delivering it at commercial scale.

When Cramer directly questioned whether Micron had overtaken SK Hynix and Samsung, Mehrotra responded definitively: “Regarding DRAM and NAND technology, we maintain clear technology leadership.” The company currently holds approximately 65,000 patents.

Cramer also highlighted the valuation opportunity. Despite the substantial rally, MU shares trade at less than eight times earnings.

Domestic Manufacturing Expansion

Micron has pledged $200 billion toward U.S.-based manufacturing and research and development initiatives, targeting the creation of over 90,000 jobs. Additionally, the company is investing $300 million in developing a domestic semiconductor workforce through apprenticeship programs, community college partnerships, and university collaborations.

Cramer mentioned Morris Chang’s assertion that U.S. chip production costs exceed Taiwan’s by 50%. Mehrotra countered by referencing Micron’s current Manassas, Virginia facility, which already manufactures advanced memory solutions for automotive, defense, medical, and aerospace applications.

Addressing the consumer segment, Mehrotra acknowledged that surging AI data center demand is constraining availability for smartphone and PC memory, driving up consumer device prices. He noted that Micron maintains approximately 40% of its business in consumer markets to preserve portfolio diversification.

MU trades at $970 as of July 2, with fourth-quarter guidance projecting $50 billion in revenue and EPS of $31.00 approaching.

“If we don’t have a euro on the blockchain, the banks will use the dollar because it’s there, it’s available and it has a lot of liquidity,” Sell told CoinDesk. Rather than each bank issuing its own euro stablecoin, Qivalis is encouraging them to work together in a single shared network.

Sell said Qivalis is not trying to compete directly with USDC. Its goal is to give European banks, businesses and payment firms a regulated euro alternative as tokenized finance expands. That would allow institutions to settle in euros rather than converting assets into dollars and back again.

As more banks join, the consortium also benefits from the same network effects driving USDC’s adoption. “The more banks we have in the consortium, the better. Our network has stronger network effects,” Sell said.

Investing in infrastructure

Agant’s MacKenzie said he sees the same trend emerging in the U.K.

Banks are no longer focused only on digital assets, he said. Instead, they are investing in the infrastructure needed to connect stablecoins with traditional finance for payments, treasury operations and settlement. Businesses generally prefer settling obligations in their own currencies, he said, rather than converting into U.S. dollars first.

That may be the impetus for introducing non-dollar stablecoins, such as Societe Generale’s EUR CoinVertible (EURCV), Credit Agricole’s EURXT and Qivalis’ impending offering. But existing is insufficient. It’s how the bank deploys the stablecoin to its customers that will determine its success.

Michael Saylor thinks Bitcoin (BTC) will win the next decade by doing almost nothing. No new features. No faster blocks. The executive chairman of Strategy says the base layer should barely change while the financial system reorganizes around it.

His nine Bitcoin predictions add up to one contrarian bet. Where most technology projects chase speed and new features, Saylor argues Bitcoin should do the opposite and force everything else to adapt to it.

Change Less, Matter More

The network matters more everywhere else, he believes, precisely because it refuses to change at its core.

1. Bitcoin evolves by changing less.

Most tech projects race to ship. Saylor wants the opposite for Bitcoin. Its job, he says, is to move slowly and not break, leaving wallets, layers, and institutions to handle the fast-moving parts.

The base layer hardens while everything built on top competes and iterates. He treats that restraint not as stagnation but as the source of Bitcoin’s strength, pointing to the same fixed rules that have run without interruption since 2009.

2. The protocol gets harder to change.

Saylor calls hard consensus Bitcoin’s immune system, since any change to the base layer needs overwhelming agreement from nodes, miners, and users.

That bar has only risen with time. The last major upgrade, Taproot, activated back in 2021, and nothing comparable has followed.

The current Bitcoin soft fork debate over spam and ordinals shows how fiercely even modest changes get fought today, echoing the block-size wars that divided the community years earlier. For Saylor, that resistance is a feature, not a flaw.

From Digital Capital to Digital Money

3. Bitcoin is digital capital, not digital cash.

Forget buying coffee with it. Saylor frames Bitcoin as scarce global capital built for final settlement rather than everyday spending. About 20 million of its 21 million coins already exist, and no authority can print more.

Bitcoin’s spot price sits near $62,700, about 50% below its record near $126,000 from October 2025, yet he argues the long-term case is unchanged.

Treasuries, collateral, and large settlements belong on the base layer, while smaller payments can run on the faster networks layered above it.

4. Capital flows, not halvings, drive the cycle.

The halving no longer runs the show, Saylor says. The 2024 halving cut new issuance to 3.125 Bitcoin per block, but supply is no longer the main story.

Since US spot ETFs launched in January 2024, demand has turned increasingly institutional, moving with balance sheets rather than retail hype.

BlackRock’s iShares Bitcoin Trust alone grew from $51.5 billion to $67.4 billion in net assets during 2025, according to its annual filing.

In Saylor’s view, capital flows now set the trajectory that halvings once seemed to dictate.

5. Digital credit turns capital into money.

Here is the chain reaction Saylor sees happening. Digital capital enables digital credit, and credit in turn enables new forms of digital money.

He points to gold and real estate, which grew far more useful once banks, lenders, and markets were built around them over the past century.

Bitcoin, he argues, is now entering that same phase of financialization. The main difference is speed, since the plumbing is being built on open networks rather than paper and vaults.

Interfaces, Risks, and the Road to 2036

6. The interfaces become the battleground.

Everyone will want Bitcoin, but few will hold it the same way. Self-custody, ETFs, banks, and credit products all compete to sit between people and their coins.

Saylor says the real fight is keeping that exposure tied to actual Bitcoin rather than IOUs. Even critics of his model warn about too much paper Bitcoin stacked on top of a limited supply.

It is a danger the 2022 collapse of FTX made concrete, and one the 2014 Mt. Gox failure had already foreshadowed.

7. Five real risks define the work ahead.

Saylor does not pretend the path is clean. He names five threats to watch. They are protocol corruption, paper Bitcoin, custodial centralization, regulatory capture, and a shaky fee market.

The last one matters most over time, because the block subsidy keeps halving toward zero, so transaction fees must eventually pay for network security.

Recent warnings about leverage risk around large corporate holders suggest the paper-claims danger is already here, not merely theoretical.

8. Mining becomes energy infrastructure.

Mining turns raw electricity into monetary security, and Saylor expects it to keep maturing into a serious energy business. Since China’s 2021 ban scattered the industry, much of it relocated to the US and other markets, growing more industrial and better capitalized.

The strongest operators will win on power contracts, grid relationships, and balance sheets, not simply faster machines. Increasingly, miners act as flexible buyers of surplus or stranded power, turning otherwise wasted energy into revenue.

9. Bitcoin anchors global finance by 2036.

By 2036, Saylor expects Bitcoin to sit on the balance sheets of individuals, companies, and governments alike. That shift has already started.

In March 2025, a US executive order created a Strategic Bitcoin Reserve built from coins seized in criminal and civil cases, with a stated policy of never selling them.

If more states follow, he argues, Bitcoin becomes a neutral reserve asset that anchors credit and settlement worldwide.

Follow us on X to get the latest news as it happens

The vision is bold, and Saylor is far from a neutral observer. Strategy, the firm once called MicroStrategy, holds more than 847,300 BTC worth over $53 billion, per its filings.

That single corporate stash is roughly 4% of all the coins that will ever exist. Whether the rest of the world chooses to build on a foundation that refuses to change may decide Bitcoin’s next decade.

Bitcoin’s job is not to become everything. Bitcoin’s job is to be the thing that does not change,” Saylor concluded.

The post 9 Things Michael Saylor Believes About The Next Decade for Bitcoin appeared first on BeInCrypto.

Bitcoin traded near $62,675 on July 5, according to crypto.news market data. The asset was up about 0.1% over 24 hours and 4.03% over seven days. Its market cap stood near $1.26 trillion, while 24-hour volume was about $17.57 billion.

Summary

- Bitcoin trades near $62,675 as traders test whether the weekly 200MA can still hold firm.

- Saylor’s “digital energy” post added a macro angle while technical analysts focused on resistance overhead.

- ETF inflows and short squeezes lifted sentiment, but weak volume keeps confirmation limited for now.

The latest 24-hour range showed Bitcoin moving between $62,462 and $63,383. That kept BTC close to the $63,000 area after a short-term rebound from the late-June low near $58,000 to $59,000.

Michael Saylor added to the wider market discussion with a short post on X, saying “Bitcoin is Digital Energy.” The comment came days after he argued that Bitcoin’s long-term role depends on capital markets, credit and institutional adoption.

Shorts cleared near $63K

Trader Daan Crypto Trades said Bitcoin shorts were cleared twice as price moved toward $63,000 on July 4. He called the move a “classic short squeeze,” where sellers are forced to close positions as price rises into a crowded short zone.

He also raised doubt over the next move, asking whether “$62.6K (Weekly 200MA) holds as support” or whether the move only cleared liquidity before another pullback. That level now sits near the center of the short-term Bitcoin debate.

Crypto.news reported that Bitcoin had already rebounded near $61,700 after U.S. spot Bitcoin ETF inflows returned. The report said BTC needed to reclaim $62,800 and $65,000 to confirm stronger bullish momentum.

That framework remains useful as price trades near $63,000. Holding above the weekly 200MA may support the recovery, while a failure could bring attention back to $60,000 and the late-June low area.

Falling wedge keeps breakout hopes alive

Analyst BATMAN said Bitcoin remains inside a daily falling wedge while the RSI shows a bullish divergence. In simple terms, price made lower lows, but momentum did not fall with the same force.

The analyst said this may show that bearish pressure is fading. He also pointed to the $67,500 to $71,000 area as a bearish imbalance above current price, where Bitcoin may seek liquidity if a confirmed breakout occurs.

The daily BTC/USDT setup shows a short-term recovery after the bounce from the $58,000 to $59,000 zone. The latest daily candle was slightly red near $62,700, showing hesitation after the rebound.

The Parabolic SAR sits below price near $58,126, which keeps the short-term structure supportive. A move below that area would weaken the recovery and bring sellers back into focus.

Momentum improves, but volume stays weak

The MACD has improved. The histogram is positive near 589.52, and the MACD line is above the signal line. This shows that bullish momentum has returned after the recent bounce.

Still, both MACD lines remain below the zero level. That means the wider trend has not fully turned bullish. It shows recovery momentum, not a confirmed trend change.

Volume also remains low at about 4.24K BTC on the chart reviewed. That limits confirmation behind the rebound. For a stronger move, Bitcoin would need higher volume and a clear break above the $63,000 to $65,000 resistance zone.

source: TradingView

The downside levels remain clear. Bitcoin must hold $62,600 to keep the short-term squeeze alive. Below that, traders may watch $60,000, then the $58,100 to $58,500 zone near the Parabolic SAR and recent lows.

Saylor’s Bitcoin view meets market caution

Saylor’s “digital energy” post fits his wider Bitcoin view. Crypto.news recently reported that Saylor has called for balance between adoption, innovation and stability as companies, banks and governments build around Bitcoin.

Crypto.news also reported that Saylor has argued Bitcoin’s old four-year cycle is losing control, with capital flows now shaping BTC more than miner issuance alone. That view places more weight on ETF flows, corporate treasury moves and credit markets.

For now, the market remains technical and cautious. Bitcoin has squeezed shorts and recovered from late-June lows, but it still needs a clean move above $65,000 to improve the broader chart.

Until that happens, the key test is simple. BTC must hold the weekly 200MA near $62,600, defend the $60,000 area, and attract stronger volume before traders can treat the rebound as more than a liquidity move.

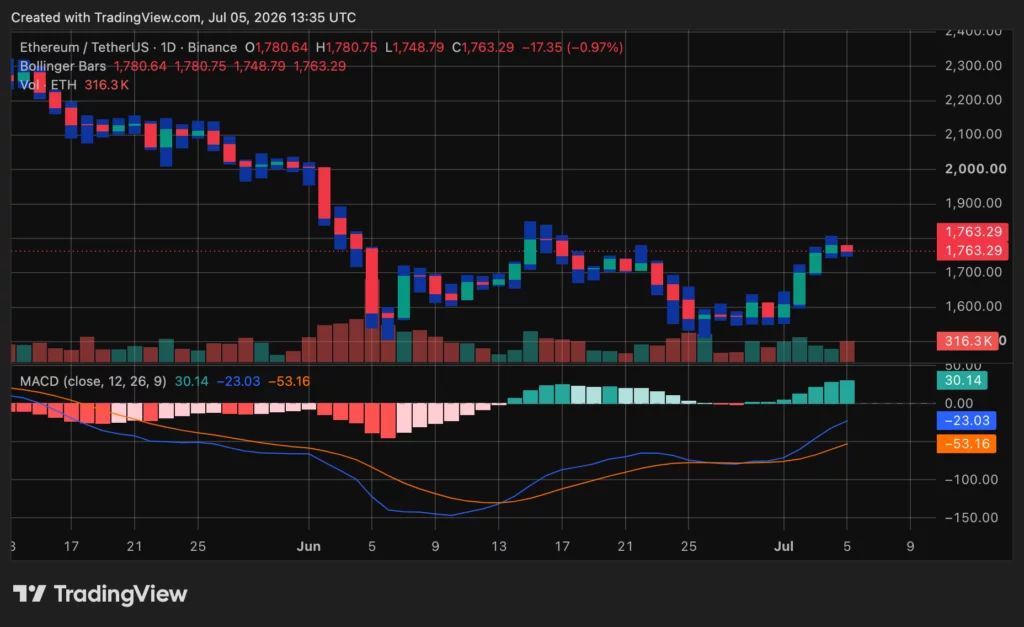

Ethereum traded near $1,764.43 on July 5, according to crypto.news market data. The token was up 0.2% over 24 hours and 11.58% over seven days. Its market cap stood near $212.91 billion, while 24-hour volume was about $11.16 billion.

Summary

- Ethereum remains trapped between $1,700 support and $1,800 resistance as liquidation clusters frame price action.

- Vitalik Buterin’s Lean Ethereum roadmap focuses on STARKs, quantum resistance, privacy and future scalability.

- ETH’s MACD shows improving momentum, but weak volume keeps a confirmed bullish reversal out of reach.

The latest daily range showed ETH moving between $1,751.18 and $1,801.59. That placed the token close to the $1,800 resistance area after a recovery from the June low near $1,500.

ETH/USDT remains in a broader downtrend from the May highs. Still, the short-term chart has improved after buyers defended the $1,500 region and pushed price back above $1,700.

Liquidation clusters keep ETH boxed in

Traders are watching two large liquidity zones around Ethereum. One sits above price near $1,800 to $1,830, while another sits below around $1,700. This keeps ETH inside a narrow range where quick moves can reverse fast.

One trader said, “As long as Ethereum stays in this range, I’d expect chop and fakeouts.” The same view points to a bigger move only after one side of the liquidity zone gets cleared.

Crypto.news previously reported that Ethereum liquidation heatmap data showed large leverage clusters near $1,700 to $1,760 and another major zone near $1,800. Those levels remain close to the current price range.

Professor Crypto also said ETH has started to build momentum after defending the $1,500 area. He said bulls need to reclaim and hold $1,800 before the market can target $1,900 to $2,000.

Momentum improves, but confirmation is limited

The daily chart shows ETH struggling to extend above $1,780 to $1,800. The latest candle opened near $1,780.64, reached $1,780.75, and dipped to $1,748.79 before stabilizing.

Nearby support sits around $1,700. A loss of that level could return focus to $1,600 and then $1,550. A clean break above $1,800 may bring $1,830 to $1,850 into focus.

The MACD continues to improve. The histogram is positive near 30.20, while the MACD line stays above the signal line. That shows short-term bullish momentum.

Still, the MACD line remains below zero. This means ETH is in a recovery phase, not a confirmed trend reversal. Volume near 315,730 ETH also remains moderate, so buyers still need stronger activity to confirm continuation.

Source: TradingView

Crypto.news reported that Ethereum recently targeted $1,800 after a rare TD buy signal. The report also said failure to hold $1,700 could return focus to $1,650 and the lower support area near $1,500.

Vitalik’s Lean Ethereum roadmap adds long-term focus

Ethereum’s price action also came as Vitalik Buterin shared a new long-term roadmap called Lean Ethereum. The plan focuses on faster verification, stronger security and better scalability over the next several years.

The roadmap includes native recursive STARKs, post-quantum cryptography, new virtual machine designs and a larger state architecture. Reports also said the upcoming Glasterdam upgrade may raise Ethereum’s gas limit.

The plan does not guarantee short-term price gains. It does, however, shift part of the discussion away from daily ETH moves and toward Ethereum’s technical future.

For now, ETH traders remain focused on the same near-term levels. Ethereum needs to hold $1,700, break $1,800, and attract stronger volume before the recovery can target the $1,900 to $2,000 zone.

Key Takeaways

- ASTS shares are hovering near $85.13, while optimistic projections suggest a fair value reaching $170 — approximately 50% upside from present levels

- Recent achievements include full operational status for BlueBird satellites and establishment of a subsidized joint venture with Rakuten in Japan

- CNBC’s Jim Cramer labeled ASTS “a great speculative stock,” expressing confidence the firm could achieve profitability in under two years

- While Pictet Asset Management boosted holdings by 146.8% during Q1, Wall Street consensus remains at “Reduce” with a mean target of $85.09

- Company insiders have liquidated more than $280 million in stock over the past quarter, with the CFO alone selling $4.3 million worth in June

AST SpaceMobile (ASTS) started Friday’s session at $85.13, almost perfectly aligned with the Street’s consensus price objective of $85.09 — creating an intriguing juncture for evaluating the investment opportunity.

The satellite communications company has experienced significant developments recently. The firm’s BlueBird satellite constellation has achieved full operational capability, while simultaneously finalizing a Japanese joint venture partnership with Rakuten that includes government financial support. These represent tangible achievements for an enterprise still advancing toward full commercial deployment.

Looking at recent performance, ASTS gained 19.15% over the trailing week. However, extending the timeframe to 30 days reveals a contrasting narrative — shares declined 20.65% across that period. The 12-month view shows an 86.69% advance, demonstrating substantial longer-term appreciation despite recent volatility.

The Bull Case: $170 Valuation Target

An optimistic analyst framework establishes fair value at $170 per share — representing nearly 100% potential appreciation from current trading levels. This projection depends on AST successfully expanding its BlueBird satellite network, transforming carrier agreements into stable recurring revenue streams, and ultimately achieving telecommunications-scale operations. The valuation employs a 7.108% discount rate.

The company’s financial position lends some credibility to this outlook. According to March 31, 2026 figures, AST maintained approximately $3.5 billion in cash reserves, with management stating no plans for additional convertible debt issuance during the current year. For a company in aggressive expansion mode, this represents considerable financial flexibility.

Yet valuation concerns persist. The price-to-book ratio stands at 12.2x, dramatically exceeding the US telecom sector’s 1.6x average. Even relative to immediate competitors at 12.6x, the premium appears justified only marginally. This represents an elevated multiple for an enterprise still generating substantial losses.

Wall Street Split, Executives Exiting

Analyst opinions vary considerably. Roth MKM maintains a buy recommendation with a $108 price target. Barclays holds an underweight stance at $65. Deutsche Bank downgraded from buy to hold while reducing its target to $106. UBS remains neutral at $80. MarketBeat’s aggregated consensus settles on “Reduce.”

First quarter results disappointed investors. AST disclosed a per-share loss of $0.66, substantially missing the consensus forecast of -$0.23. Revenue totaled $14.73 million versus analyst expectations of $39.01 million. Despite year-over-year revenue expansion of 1,952%, the significant shortfall drew attention.

Insider transaction activity has been uniformly negative. Over the previous three months, company insiders liquidated more than 3.1 million shares totaling approximately $280.6 million. CFO Andrew Martin Johnson sold 45,809 shares at $93.81 per share on June 11, decreasing his position by 8.34%.

Institutional activity presents a contrasting picture. Pictet Asset Management expanded its stake by 146.8% in Q1, concluding the quarter holding 79,666 shares worth $6.6 million. Total institutional ownership represents 60.95% of outstanding shares.

Jim Cramer offered his perspective recently, characterizing ASTS as “a great speculative stock” while expressing belief the company could reach profitability within a two-year horizon. He positioned it as a high-risk, high-conviction play — emotion-driven rather than data-driven.

The 52-week trading range extends from $36.08 to $133.86. The 50-day moving average sits at $87.38 while the 200-day moving average is $89.44. Current analyst projections anticipate a full-year per-share loss of $1.47.

South Africa’s tax authority, the South African Revenue Service (SARS), has published draft guidance that explains how crypto assets should be taxed under the country’s existing income tax and capital gains tax frameworks. The proposed rules—released on Wednesday—aim to offer interpretive clarity rather than create entirely new obligations.

In a draft notice issued for public comment, SARS indicates that many common crypto activities, including trading, swapping and using crypto to pay for goods or services, are likely to be treated as disposals for tax purposes. However, the tax outcome would still depend on the taxpayer’s specific facts and circumstances, with the guidance stressing that intention and conduct over time matter.

Key takeaways

- SARS says crypto should generally be treated as an intangible asset, not legal tender or foreign currency, for tax purposes.

- Many crypto activities may trigger tax events because they can be viewed as disposals under existing income tax and capital gains tax rules.

- Whether someone is a trader or a long-term investor hinges on behavior, transaction frequency, and the purpose of holding crypto.

- The draft also suggests crypto can potentially fall under donations tax if transferred as “property,” with donation tax rates between 20% and 25% depending on value.

- The guidance is open for public comment until August 31 and is not yet final law.

Why SARS is issuing draft crypto tax guidance

The publication of draft guidance marks another step in South Africa’s effort to bring greater consistency to crypto taxation. SARS says the intent is to clarify how the existing tax regime applies to crypto, particularly under the Income Tax Act, 1962, along with capital gains tax principles.

That matters for local holders because tax treatment can affect how individuals and businesses account for crypto-related gains and losses—especially when transactions involve frequent trading or payments. SARS also noted in 2024 that at least 5.8 million residents held crypto assets, underscoring the scale of potential compliance implications if the guidance is adopted.

Crypto is treated as property, not currency

A central theme in the draft is how SARS characterizes crypto assets legally for tax purposes. According to the guidance, crypto assets are not treated as legal tender or foreign currency. Instead, SARS describes them as intangible assets—“not ‘currency’” and therefore not “foreign currency.”

The guidance draws a line between the asset and its function. While crypto can be used in ways that resemble money—such as trading, settlement, or payment—it is still framed as a distinct tax object. That distinction can be important because different categories of assets may be taxed under different rules, and the tax analysis may change depending on how SARS views the nature of the instrument involved.

Disposals, trading activity, and the role of intent

The draft repeatedly returns to the idea that many real-world crypto actions are economically similar to selling or exchanging an asset, which under tax law can amount to a disposal. SARS states that most crypto activities—including trading, swapping and spending—are generally treated as disposals and may trigger tax events.

At the same time, SARS cautions that the tax treatment will not be uniform for everyone. A key determinant is the taxpayer’s intention. The guidance explains that classification as a trader versus a long-term investor depends on behavior, including how often transactions occur and why the crypto is being held.

SARS also highlights that intention is not necessarily static. In the agency’s view, tax assessment should consider the taxpayer’s intention:

- at the time of acquisition,

- at the time of selling or disposing, and

- while holding the asset—recognizing that a person’s purpose can change over time.

This approach implies that taxpayers who rotate between investment and active trading could face different outcomes for different periods or different lots, depending on the evidence available. SARS says this requires a broad assessment of all relevant facts and circumstances, which may increase the importance of record-keeping—particularly for frequent traders and those who use crypto for payments rather than holding it untouched.

Potential reach to donations tax

The draft guidance also extends beyond routine trading and investing. SARS indicates that crypto assets may fall within South Africa’s donations tax rules because the assets are treated as “property” under tax law.

Under the framework described in the guidance, donations tax rates range from 20% to 25%, depending on the value of the donation. While the draft does not claim that every crypto transfer will automatically be subject to donations tax, it signals that SARS is prepared to treat certain transfers as taxable events in the context of property transfers, not just in the context of sale-like disposals.

What happens next: comment period and broader market context

The guidance is not final legislation. SARS says the draft is open for public comment until August 31, and the agency positions it as interpretive clarity rather than an attempt to introduce new legal obligations.

For market participants, this timing is significant. Many taxpayers will be deciding how to interpret their existing tax position in the lead-up to any final version of the rules. If the final guidance meaningfully narrows or expands the application of concepts like intention, disposal treatment, or property classification, taxpayers may need to adjust accounting methods and documentation practices accordingly.

South Africa is also one of Africa’s most active crypto markets. According to Chainalysis’ October 2024 report, the country received about $26 billion in crypto value during the one-year period covered by the study. Chainalysis also found that institutional and professional-sized transactions were the largest contributors, particularly from late 2023 through the first quarter of 2024, pointing to a gradual shift toward larger and more structured activity.

That trend can heighten the importance of clear tax rules for compliance. As trading volumes rise and more professional participation enters the market, inconsistency or uncertainty in how transactions are classified can translate into larger compliance risks—making guidance like SARS’s particularly relevant not only for retail investors but also for intermediaries and more active market participants.

As the August 31 comment deadline approaches, holders, traders, and businesses will want to watch for how SARS responds to submissions and whether the final version tightens the standard for determining intent, the treatment of swaps and payments, and the boundaries between trading and long-term investing.

Key Takeaways

- NBIS shares surged 19.5% in June before erasing most gains during early July trading

- First quarter 2026 revenue skyrocketed 684% compared to the prior year, with full-year guidance exceeding $3 billion

- Strategic partnership with Meta Platforms valued at $27 billion plus support from Nvidia have fueled investor enthusiasm

- Year-to-date gains stand at 158%, though shares have retreated 16% in the most recent five-day period to approximately $215

- Analyst consensus leans toward Moderate Buy with a mean price target of $237.38, suggesting roughly 10% potential upside

Nebius Group (NBIS) has emerged as a 2026 market leader. This AI-focused cloud infrastructure provider has delivered a remarkable 158% gain since January, with shares more than quadrupling over the trailing twelve months. However, recent volatility serves as a stark reminder of the stock’s unpredictable nature.

Shares experienced a 19.5% June rally before surrendering nearly all those advances during the opening week of July. Trading at approximately $215.62 as of July 5, NBIS declined almost 6% in a single session.

Recent selling pressure intensified following a Bloomberg report suggesting Meta Platforms might monetize its surplus computing resources. Certain market participants interpreted this news as potentially problematic for neocloud providers like Nebius. However, counterarguments emphasized that AI computational demand continues to significantly exceed available supply.

The situation carries notable complexity — Meta simultaneously represents one of Nebius’ most significant clients. Their collaboration encompasses a $27 billion commitment, with Meta supporting approximately 300 MW of AI infrastructure capacity. Additionally, Nvidia CEO Jensen Huang has actively facilitated connections between AI-focused enterprises and Nebius, further validating the company’s market position.

Astronomical Revenue Expansion

The financial performance of Nebius presents compelling evidence of growth. Second quarter 2025 revenue totaled merely $105 million. By the fourth quarter, annualized revenue reached a run rate of $1.25 billion. The first quarter of 2026 showcased extraordinary 684% year-over-year revenue acceleration.

Executive leadership now projects 2026 revenue will surpass $3 billion, with projections suggesting another potential doubling throughout 2027. Supporting this trajectory requires substantial data center infrastructure expansion.

Contracted power capacity projections have escalated dramatically from a minimum 1 GW last August to exceeding 4 GW currently. Nebius has already locked in 1.2 GW of power resources and real estate for a Pennsylvania-based AI facility. The company also formalized a strategic alliance with Bloom Energy to deploy supplementary power infrastructure for ongoing data center construction.

Analyst Community Remains Divided

Skepticism persists regarding current valuation sustainability. NBIS has achieved approximately $55 billion in market capitalization, representing an aggressive multiple even against projected 2027 revenue figures.

Northland analyst Nehal Choksi maintains a Buy rating alongside a $248 price target, highlighting Nebius’ strategic pivot toward more profitable AI-native clientele as justification for optimism. He views the Tavily acquisition as enhancing customer value propositions.

Morgan Stanley’s Josh Baer presents a contrasting perspective. His Hold rating accompanies a $144 price target — substantially below present trading levels. While Baer recognizes customer momentum, he contends that near-term objectives appear overly ambitious, citing unproven profitability metrics and substantial additional bookings needed to achieve guidance.

The Street’s aggregate assessment registers as Moderate Buy, comprising six Buy recommendations and four Hold ratings. The consensus price target of $237.38 suggests approximately 10% appreciation potential from current pricing.

Competitor CoreWeave operates within identical market segments, and any deceleration in AI infrastructure investment could disproportionately impact NBIS compared to the broader technology sector.

The stock’s 52-week trading range spanning $43.89 to $299.86 provides clear evidence of the extraordinary volatility investors have navigated.

Key Takeaways

- CRM shares opened Friday at $165.94, reflecting a ~41% decline year-to-date and a ~58% drop from the late-2024 high

- Guggenheim shifted its stance from Neutral to Buy, establishing a $228 target and arguing valuations reflect an “Armageddon” baseline

- Analyst consensus averages Moderate Buy, with a mean target near $254 — suggesting potential gains of 55%–57%

- Q1 results topped forecasts: EPS reached $3.88 against $3.13 estimates, while revenue hit $11.13B, climbing 13.3% year-over-year

- The company’s AI portfolio — spanning Agentforce and Slack-integrated agents — now drives more than $2.3B in ARR

Shares of Salesforce (CRM) began Friday trading at $165.94, marking a steep year-to-date decline of approximately 41% and a roughly 58% retreat from the late-2024 high around $276.80. The downturn stems primarily from investor anxiety that AI-powered agents might render conventional CRM platforms redundant.

Yet a growing number of Wall Street voices believe the market has overreacted.

This week, Guggenheim analyst John DiFucci elevated CRM from Neutral to Buy, establishing a $228 price objective. His rationale: trading at approximately 3.7x recurring revenue and 11x EV/NTM free cash flow, the valuation assumes perpetual 5% business contraction — a scenario he deems implausible.

Citigroup likewise moved Salesforce to Buy this week, joining a widening group of analysts convinced the correction has exceeded rational bounds.

Current Street consensus shows Moderate Buy, with 28 Buy ratings, 6 Hold recommendations, and 4 Sell calls.

The mean price objective hovers around $254, pointing to approximately 55%–57% potential appreciation from present levels. Citizens JMP maintains the Street’s highest conviction with a $315 target.

Strong Q1 Results and Forward Outlook

Salesforce delivered Q1 figures on May 27th that surpassed Wall Street projections. Earnings per share landed at $3.88, topping the $3.13 consensus by $0.75. Revenue totaled $11.13 billion, representing 13.3% year-over-year growth and edging past the $11.05 billion forecast.

For fiscal 2027, management projects full-year EPS in the $14.060–$14.120 range. Second-quarter fiscal 2027 guidance calls for EPS between $3.250 and $3.270.

The stock trades within a 52-week range of $146.32 to $276.80. The 50-day moving average currently stands at $173.23, while the 200-day moving average registers at $197.71.

AI Product Suite Driving Material Revenue

Despite apprehension surrounding AI-driven disruption, Salesforce’s proprietary AI offerings are already delivering substantial financial contributions. The product lineup — encompassing Agentforce, Data 360, Slack-integrated AI agents, and Headless 360 APIs — currently generates north of $2.3 billion in rapidly expanding annual recurring revenue.

This metric serves as a focal point for analysts arguing the enterprise isn’t merely protecting existing market share — it’s actively capturing emerging opportunities.

On the institutional front, Kepler Cheuvreux Suisse SA expanded its CRM position by 284.1% during Q1, acquiring an additional 12,568 shares to reach a total stake of 16,992 shares valued around $3.17 million.

Vanguard Group maintains 89.8 million shares worth approximately $23.8 billion. State Street controls 50 million shares, with institutional investors collectively representing 80.43% of outstanding equity.

Salesforce distributed a $0.44 quarterly dividend per share on July 2nd, equating to a $1.76 annualized payout and yielding roughly 1.1%.

The board greenlit a $25 billion buyback authorization in March, permitting repurchases of up to 14.1% of outstanding shares via open market transactions.

HC Wainwright took a contrarian stance, lowering CRM to Negative on June 18th — representing one of just four Sell-rated opinions currently assigned to the stock.

South Africa proposes crypto tax guidance under existing rules

17 Loose Sundresses for Women Over 55 on Amazon

How to Solve the Puzzle 1120 Easily

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: High Hopes

-

Politics2 days ago

Politics2 days agoThe House | “Reframing the debate from a binary discussion of winners and losers”: Yuan Yang reviews ‘We Are Not Machines’

-

Crypto World5 days ago

Crypto World5 days agoStrategy authorizes up to $1.25B in Bitcoin sales under new capital plan

-

News Videos7 days ago

News Videos7 days agoMAJOR BITCOIN & MARKET UPDATE!!!! (MUST WATCH ASAP!!!)

-

Tech6 days ago

Tech6 days agoAnonymous researcher drops 0-day ‘exploitarium’ repo

-

News Videos5 days ago

News Videos5 days agoHow to Build INSANE Live Financial Dashboards With Claude

-

Business5 days ago

Business5 days agoAustralia treasurer says alleged access of prime minister’s bank data ’incredibly concerning’

-

NewsBeat10 hours ago

NewsBeat10 hours agoTaylor Swift and Travis Kelce wedding staffer hilariously struggles to keep her cool while checking in megastars

-

Business6 days ago

Business6 days agoThe AI boom won’t burst all at once. It will pop in ‘rolling bubbles’: Macquarie

-

Sports4 days ago

Sports4 days agoBroncos roster: OL Ben Powers (No. 74) entering final year of contract

-

NewsBeat5 days ago

NewsBeat5 days agoPresenter Caroline Flack’s brother Paul Flack dies aged 55

-

Crypto World3 days ago

Crypto World3 days agoBinance stock trading tops $1B in first month after launch

-

Crypto World3 days ago

Crypto World3 days agoAlibaba-affiliate Ant Group enters the humanoid robot market with 12 deals

-

NewsBeat3 days ago

NewsBeat3 days agoNew exhibition reflects five decades of movement between island of Ireland and GB

-

Crypto World4 days ago

Crypto World4 days agoAirdrop Registration Becomes Key Focus For Remittix As RTX Launch Updates Approach

-

Business4 days ago

Business4 days agoMeta Platforms Stock Jumps 7% Today as Bloomberg Reports Company Plans to Enter the Cloud Business

-

Business2 days ago

Business2 days agoWhat a 10 Percent Drop Means for Buyers, Sellers and Renters

-

Crypto World3 days ago

Crypto World3 days agoBinance Re-Enters Philippines As EU MiCA Rules Restrict Access

-

Tech3 hours ago

Tech3 hours agoLenovo laptops are now shipping with YMTC SSDs, a sign of Chinese NAND entering the mainstream

-

Crypto World2 days ago

Crypto World2 days agoStandard Chartered Secures MiCA License as ESMA Adds 37 New Crypto Firms

You must be logged in to post a comment Login