Crypto World

SpaceX Stock Falls 35% From Peak Even After Nasdaq-100 Inclusion

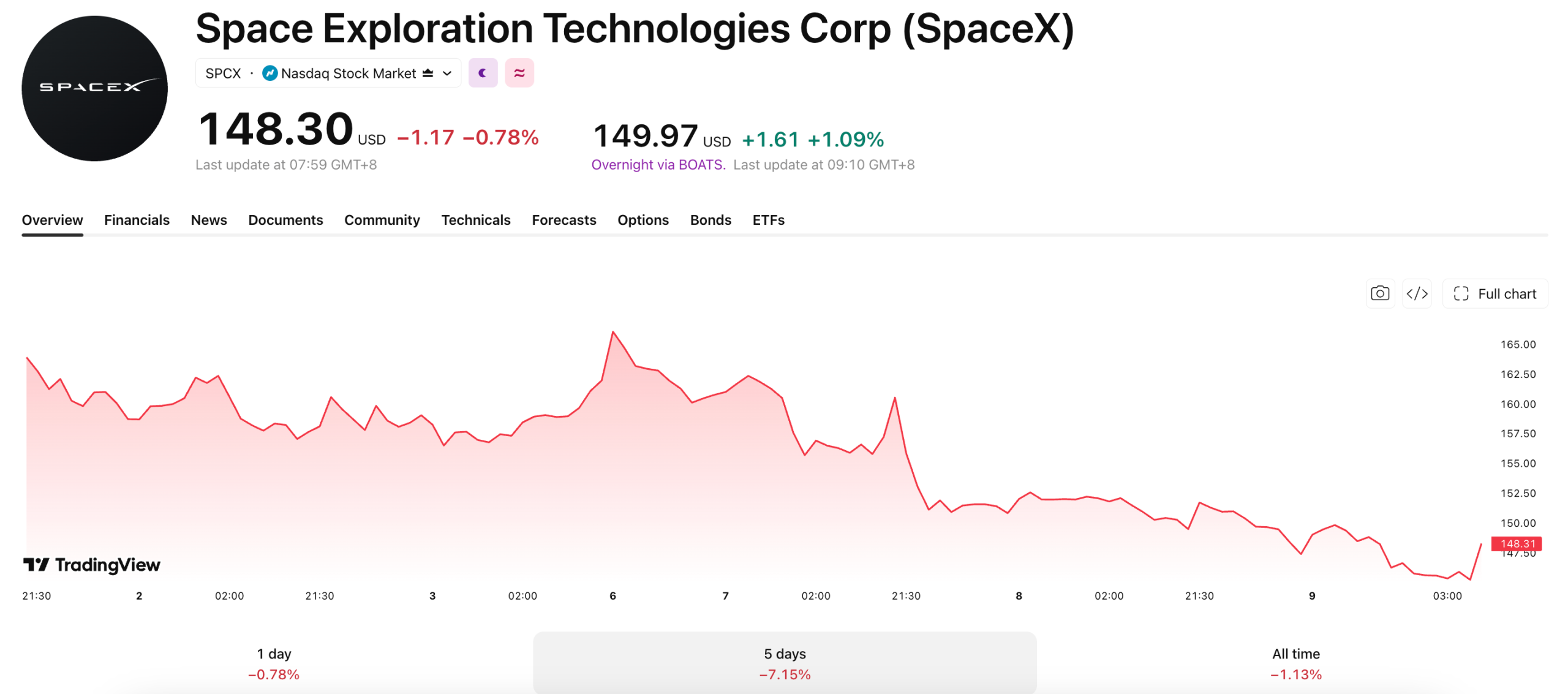

SpaceX (SPCX) shares have fallen as much as 35% from their post-IPO peak of $225.64. The drop came just days after the company joined the Nasdaq-100, as heavy selling offset forced index buying.

The stock closed at $148 on July 8, below its $150 debut price for a second straight session. That erased nearly all the gains SpaceX made since its record June 12 listing.

A Sell-The-News Pattern for SPCX

SpaceX’s Nasdaq-100 inclusion required index-tracking funds to buy shares, even though the company keeps a small public float. That mechanical demand did not stop investors from selling into the news.

This is a familiar pattern, as Palantir saw the same thing happen after it joined the Nasdaq-100 in late 2024. Its shares dropped about 25% over the following weeks.

A Trillion-Dollar Valuation Under Pressure

The pullback still leaves SpaceX with a market capitalization near $1.9 trillion. The company posted about $18.7 billion in revenue in 2025, up about 33% year over year. That puts its valuation at roughly 100 times sales.

Starlink drove much of that growth. SpaceX’s satellite internet unit generated more than $11 billion in 2025, about 61% of total revenue. It remains the main support for the company’s trillion-dollar valuation.

SpaceX still lost money last year. The company reported a $4.9 billion net loss in 2025 and $4.3 billion more in the first quarter of 2026. Heavy spending on its xAI artificial intelligence unit and on Starship development continues to weigh on cash flow.

Wall Street has largely stayed bullish since the Nasdaq-100 inclusion. Morgan Stanley, Bernstein, RBC, and UBS all initiated coverage with buy-equivalent ratings. MoffettNathanson took a neutral stance, and CFRA recommended that investors sell.

Starlink’s profit growth may determine how much further the stock can fall. Investors will likely watch whether that business can outpace SpaceX’s mounting AI and rocket-development costs.

The post SpaceX Stock Falls 35% From Peak Even After Nasdaq-100 Inclusion appeared first on BeInCrypto.

Robinhood built a blockchain for tokenized stocks and institutional-grade real-world assets. In its first week, the chain did $570 million of volume against $21.68 million of liquidity, a 26-to-1 ratio that exists nowhere else in DeFi, and most of it was memecoin speculation. This is the launch-week autopsy: what the numbers actually show, what the chain was built for versus what it is being used for, and whether bought liquidity and degen volume can become a real economy.

Summary

- Robinhood Chain processed $570 million in launch week trading volume with just $21.68 million in liquidity as memecoin activity dominated early network usage.

- The blockchain launched for tokenized stocks and real world assets but early growth was driven largely by incentive backed DeFi deposits and speculative trading.

- The report says Robinhood’s long term success will depend on whether tokenized stocks become an active onchain market after launch incentives begin to fade.

Robinhood Chain launched its public mainnet on July 1 with the most institutional framing a blockchain has ever worn: an Arbitrum-based layer 2 built to institutional standards, 95 tokenized stocks trading around the clock, Chainlink as official oracle, BitGo custody, a zero-fee stock-token exchange built by the dYdX team, and a keynote in London titled The World is Flat. The pitch was unambiguous. This is the chain where real-world assets live, where NVDA becomes loan collateral, where the brokerage account and the DeFi protocol finally merge.

Then the first week’s data arrived, and it described a different chain entirely.

Launch-day volume hit $570 million against total value locked of just $21.68 million, a 26-to-1 turnover ratio that does not exist anywhere else in decentralized finance at comparable scale; mature venues run at or below 1-to-1. The volume was not tokenized Apple changing hands between institutions. By every on-chain accounting, it was overwhelmingly memecoin speculation, degens doing what degens do on any new chain with an airdrop-shaped incentive structure. A week in, TVL has climbed past $240 million, driven mostly by Morpho lending and Ethena farming against a 7% yield incentive, roughly 4 million transactions have produced about $57,000 in protocol revenue, and Robinhood’s own CEO has been openly, cheerfully inviting the crypto casino in to bootstrap the network built for Wall Street’s assets.

This piece is the autopsy of that opening week. It works through what the 26-to-1 ratio actually measures and why it stopped analysts cold, the gap between the chain’s stated purpose and its observed usage and why that gap is partly deliberate strategy, the anatomy of the incentive-bought TVL and what history says about whether mercenary capital converts, the genuinely novel pieces underneath the noise, and the specific numbers that will show, over the next quarter, whether Robinhood built an economy or rented a crowd.

What 26-to-1 actually measures

Start with the ratio, because it is the week’s headline statistic and it is widely misread in both directions. Volume-to-TVL compares how much trading a venue processes against how much capital sits in it providing liquidity. A ratio near 1-to-1, typical for mature exchanges, means the liquidity base turns over about once a day. Robinhood Chain’s launch day turned its entire liquidity base over twenty-six times.

The bearish reading treats the number as fake: volume without liquidity is churn, wash-adjacent hot-potato trading in tokens with no depth, exactly what memecoin launch frenzies produce, and it says nothing about durable demand. The bullish reading treats it as extraordinary demand outrunning supply: more people wanted to trade on this chain, immediately, than its nascent pools could properly serve, which is the opposite of the usual new-chain failure mode of incentivized liquidity sitting idle with no one to trade against.

The honest reading is narrower than both. High turnover on thin liquidity is characteristic of exactly one market condition: speculative launch trading, where participants are trading the newness itself, tokens minted hours earlier, positions held minutes, price impact on every fill because the pools are shallow. The ratio measures intensity, not quality, and its collapse over subsequent days, as TVL grew tenfold while volume normalized, is the pattern resolving toward ordinary proportions. What the launch-day number genuinely proved is distribution: Robinhood pointed 28 million customers and the entire crypto-native trading class at a new chain, and enough of them showed up in hour one to produce turnover no organic launch has matched.

Distribution was always the thesis behind corporate chains, the pattern this publication mapped when the land grab formed; week one was the thesis producing a data point.

Built for BlackRock, opened by degens

The gap between the chain’s marketing and its usage deserves direct examination, because it is the week’s real story and it is more strategic than embarrassing.

What Robinhood built is legible in the architecture. The chain is a permissionless Arbitrum Orbit layer 2 with the RWA stack bolted in from day one: 95 stock tokens with Chainlink price feeds and proof-of-reserve, a dedicated zero-fee stock DEX, Uniswap deploying a flagship AMM as core public liquidity, lending markets where equity tokens post as collateral, and wallet distribution across 120 countries. It is, structurally, the most complete attempt yet at the thing crypto has promised for years: equities as composable on-chain assets rather than walled tokens.

What the chain hosted in week one is equally legible: memecoin launches and rotation, farmed lending deposits, points-and-yield tourism. And the company’s response was the telling part: no distancing, no dismay. The CEO publicly courted the degen crowd, the 7% DeFi yield was aimed squarely at capital that follows incentives, and a perps venue pledged $11 million of its token to Robinhood users with doubled points for wallet trading. Robinhood, whose original business was built on making speculation frictionless for retail, understands with complete clarity what its crypto peers learned expensively: chains do not bootstrap on institutional assets, because institutions arrive last. They bootstrap on speculation, because speculators arrive first, generate the fees, stress-test the infrastructure, and produce the activity metrics that make the institutional sales deck credible. The memecoin casino is not a corruption of the RWA strategy. It is its funding round.

The precedent is Base, which launched amid a memecoin frenzy widely mocked at the time and converted the initial degen wave into the largest corporate-chain economy in crypto. The counter-precedents are the dozens of incentive-launched L2s whose mercenary capital departed with the emissions, leaving ghost chains with impressive cumulative-volume screenshots. Which path Robinhood Chain walks is precisely what the next quarter’s data decides, and the fork between the paths runs through one question: whether anything on the chain gives the tourists a reason to become residents.

The stack underneath: what was actually shipped

Beneath the launch-week noise sits an architecture worth cataloguing precisely, because it is the part that persists after the tourists rotate, and several of its choices are quietly consequential.

The base decision is Arbitrum Orbit: Robinhood Chain is a permissionless Ethereum layer 2 using Arbitrum’s technology, settling to Ethereum for security, launched to mainnet after a February testnet that processed millions of transactions.

Permissionless matters here more than the marketing admits: any developer can deploy on the chain without Robinhood’s approval, which is why the memecoin economy could appear on day one uninvited, and it is also the property that separates this launch from the private-chain experiments banks have run for a decade.

Robinhood chose to build a public place it does not fully control, accepting the degen influx as the price of credibility with the DeFi protocols whose presence, Uniswap, Morpho, 1inch, Lighter, Arcus from the dYdX team, constitutes the actual product shelf.

The asset layer is the differentiator: 95 stock tokens at launch, NVDA, GOOG, AAPL among them, issued by Robinhood, priced and bridged by Chainlink’s oracle and cross-chain infrastructure with proof-of-reserve attestation, custodied through BitGo integration, and tradable through a zero-fee dedicated stock DEX alongside the general-purpose venues. The design collapses the historical trade-off of tokenized equities, offshore issuers with thin trust versus onshore institutions with no distribution, by putting a regulated, household-name broker behind the issuance and 28 million existing customers behind the demand, in 120 countries at launch. Every previous stock-token attempt failed on one of those two legs.

And the incentive layer is the bootstrap engine: the 7% DeFi yield on chain deposits, the Lighter perps integration with its $11 million token pledge and doubled points through the Robinhood Wallet, maker-fee cuts for US crypto traders, and the European expansion of commodity, ETF, and FX perpetuals at up to 10x leverage across 30 markets. Read together, the incentives are not scattered promotions; they are a funnel, each one converting a different existing Robinhood customer type, the yield-seeker, the perps trader, the stock investor, into an on-chain user whose activity accrues to rails the company owns. The launch week tested the funnel’s intake. The quarter tests its filter.

A detail inside the asset layer rewards a closer look, because it encodes the strategy’s regulatory sophistication. The stock tokens are not one product but a jurisdictional lattice: issuance entities, disclosure documents, and availability differ by region, with the European lineage descending from the SpaceX and OpenAI tokenized products Robinhood piloted there in 2025 as proof of concept. The pilots mattered twice over: they tested the legal wrapper under MiCA-era rules before betting the chain on it, and they taught the company which regulators would engage rather than object, knowledge that is itself a moat, since every competitor contemplating the same product must now either replicate two years of jurisdiction-by-jurisdiction groundwork or license someone else’s. The chain launch, seen through this lens, was the moment previously scattered regulatory assets were composed into a single architecture, which is why the company could ship 95 tokens to 120 countries on day one while better-resourced rivals ship white papers.

What the chain cannot yet answer

Honesty requires the list of open questions the architecture has not resolved, because several are structural rather than cosmetic.

The first is the sequencer and control question every corporate chain carries: Robinhood operates the chain’s infrastructure, and a permissionless network whose ordering, upgrades, and asset issuance all route through one regulated American company is decentralized in exactly one layer and centralized in the ones above it. The arrangement is standard for the corporate-chain era and immaterial to daily users, and it is the lever regulators will reach for first, which matters more here than on any predecessor because of what the chain hosts.

The second is the geofence paradox. The stock tokens ship to 120 countries and conspicuously not to the United States, where the line between a compliant synthetic and an unregistered security remains undrawn; Robinhood’s own home market gets the chain but not its flagship asset. A permissionless network carrying jurisdiction-gated assets is a truly novel compliance object, enforcement happens at the issuance and interface layers while the rails stay open, and whether that architecture satisfies regulators or provokes them is unresolved and, for the chain’s central product, existential.

The third is liquidity depth versus product promise. Around-the-clock equity trading and stock-collateral lending are only as good as their books, and week-one depth in the stock tokens was a rounding error against the memecoin flow. The products that justify the chain exist as listings; whether they exist as markets is precisely what the autopsy’s dashboard is built to detect.

The $240 million question: what bought TVL is worth

The TVL trajectory, $21.68 million at launch to past $240 million within the week, is the week’s second headline, and it needs the same forensic treatment as the first.

Decompose the growth and it is dominated by two flows: deposits into Morpho lending markets and Ethena-linked strategies, both farming the advertised 7% yield and whatever points programs shadow it. This is professional, rotational, incentive-seeking capital, the same capital that has toured every new chain’s launch incentives for three years, and its arrival proves exactly one thing: the incentives are competitive. Its departure, when yields normalize, is the base case, and every analysis of incentive programs across the L2 era finds the same shape: TVL tracks emissions up and tracks them down, with retention determined not by the size of the bribe but by what got built while the bribe ran.

What retention would require here is specific, and it is where the chain’s genuine novelty lives. If stock tokens actually acquire lending markets, a holder borrowing stablecoins against tokenized NVDA at scale, then Robinhood Chain hosts a product that exists nowhere else at brokerage distribution, and the capital servicing that market is not mercenary; it is doing business unavailable elsewhere. The early Morpho markets are the embryo of exactly that, and their composition, how much collateral is stock tokens versus recycled farm assets, is the single most informative series on the chain. The same test applies to the perps and the around-the-clock equity trading: weekend price discovery in tokenized stocks is a real product with real demand, and its volumes, separated from the memecoin churn, are the number that would vindicate the architecture.

There is also a stakeholder in the week’s data that costs Robinhood nothing and gained the most: Arbitrum. Ten percent of chain fees flow to the Arbitrum ecosystem, 8% directly to the ARB token holders’ treasury, and ARB rallied double digits on the confirmation, repricing Orbit’s sell-shovels business model on the strength of its biggest customer. Whatever Robinhood Chain becomes, the launch already validated the arms-dealer layer beneath it, and every future corporate chain negotiation starts from the precedent this deal set.

One comparative frame calibrates the launch against its true peers. Base, the reigning corporate-chain success, needed months to reach the TVL Robinhood Chain gathered in a week, and needed a memecoin summer nobody planned to find its first population; Tempo, Stripe’s entry, launched to a $5 billion private valuation with a fraction of the day-one activity; and the exchange chains of the prior cycle mostly never produced a week this loud at any point in their lives. On pure launch metrics, Robinhood’s is the strongest corporate-chain debut on record. The caveat is that launch metrics have never once predicted which chains matter, Base’s own opening weeks looked nothing like its eventual economy, and the survivorship graveyard is full of record-setting first weeks. The debut bought Robinhood the one thing debuts can buy, attention at zero marginal cost, and attention converts on the strength of what the next section prices.

The revenue reality, and who is actually paying

The $57,000 of week-one protocol revenue deserves more attention than its size suggests, because it prices the entire strategic argument. Against roughly 4 million transactions, it implies fees around a cent and a half each, deliberately subsidized throughput, and against the incentive spend, the 7% yield alone implies eight figures annually at current TVL, it makes the chain a straightforwardly negative-margin operation. That is not a criticism; it is the model. Robinhood’s brokerage was built the same way, zero commissions as customer acquisition with monetization layered behind, and the chain repeats the architecture: give away blockspace and trading, own the wallet, the issuance, the order flow, and eventually the financialization of assets that today sit inert in brokerage accounts. The 10% of fees flowing to Arbitrum makes the arithmetic even starker, Robinhood is running the subsidy and sharing the gross, and the fact that it agreed to those terms is itself information: the company is pricing the chain as distribution infrastructure whose payoff arrives elsewhere on the income statement, in custody, in spreads, in the international expansion the launch bundled, and in whatever a tokenized-stock franchise is worth if the geofence ever lifts.

For HOOD shareholders, who marked the stock up 8% on launch, the bet is therefore legible and long-dated: the market is not paying for $57,000 of weekly protocol revenue; it is paying for the option that a regulated broker with 28 million customers becomes the venue where equities’ on-chain era happens, ahead of the exchanges, ahead of the banks, and ahead of the incumbent settlement rails converging on the same destination from the other side. Options expire worthless more often than not. This one, uniquely among the corporate chains, has a product no competitor currently ships at any price, which is why the autopsy’s verdict on week one is neither the bulls’ triumph nor the bears’ farce, but a colder finding: the experiment is correctly designed, expensively funded, and entirely unresolved.

What the autopsy actually concludes

Strip the week to findings and there are four.

First, distribution is real and unprecedented: no chain launch has converted a corporate user base into on-chain activity this fast, and the 26-to-1 anomaly, whatever its quality, is a measure of reach no organic launch has produced. Second, the usage is currently almost entirely the wrong usage by the chain’s own mission statement, and the company is deliberately, rationally farming it as bootstrap fuel, with Base as the playbook and a graveyard of incentive chains as the warning. Third, the novel product, equities as live DeFi collateral at brokerage distribution, exists in embryo on the chain right now, is the only thing on it that competitors cannot copy with a bigger incentive budget, and is barely measurable yet beneath the speculative noise. Fourth, the protocol revenue, $57,000 against $570 million of volume, quantifies the bootstrap phase’s honest economics: the chain is currently a loss-leading customer-acquisition channel, as every corporate chain is at this stage, and its P&L matters less than whose customers it is acquiring.

The dashboard for the next quarter follows directly. Watch stock-token volumes and their share of total activity, the series that separates the mission from the noise. Watch Morpho collateral composition for equity tokens posted against real borrowing. Watch TVL through the first incentive step-down, the date bought capital reveals its intentions. Watch weekend and after-hours equity-token trading, the product’s unique selling point performing or not. And watch the regulatory perimeter, because the chain’s strangest feature, permissionless rails carrying geofenced assets that Robinhood’s own American customers cannot touch, is a standing invitation for exactly the scrutiny that the pending market-structure framework may or may not resolve in time.

The launch week, in the end, measured everything except the thing that matters. It proved Robinhood can summon a crowd, which was never in doubt, and it deferred the question of whether it can keep one, which is the entire bet. The 26-to-1 ratio will be forgotten in a month. The ratio to watch is slower and duller: real-world-asset activity as a share of everything else, week over week, the line on which a brokerage’s blockchain either becomes the first chain where Wall Street’s assets actually live, or joins the long list of well-funded venues that mistook a launch party for a population.

Three postscripts complete the record. The first is about the week’s strangest juxtaposition: on the same days the memecoins churned, the chain’s stock tokens quietly did something no US brokerage asset has done, traded through a weekend, and the Monday reconciliation between the tokens’ weekend drift and the cash open passed without incident, a small, unglamorous proof that the market-hours plumbing works. The second is about talent as a tell: the stock DEX was built by the team behind dYdX, Uniswap committed a flagship deployment, not a fork, and the protocols that arrived day one are DeFi’s first tier, not its mercenaries, which says the builders, at least, priced the distribution as real. The third is about time: Robinhood spent two years and several acquisitions assembling this launch, Bitstamp for exchange rails, WonderFi for licensing, the European tokenized-equity pilots as rehearsal, and companies that build that deliberately do not usually judge themselves on week one.

Neither should the autopsy. The body on the table is not the chain; it is the launch narrative, both the institutional one the keynote sold and the casino one the data showed, and the finding is that both died of the same cause: prematurity. What Robinhood Chain is will be decided by the dullest quarter of retention data in the company’s history, and for once in crypto, everyone, company included, has agreed in advance to be graded on it.

For readers building the tracking sheet, the sources are all public: the chain’s explorer and TVL dashboards for the composition series, the incentive program’s published terms for the step-down dates, the stock DEX’s volumes for the mission metric, and Robinhood’s quarterly filings for whatever the company chooses to disclose about the economics it is currently subsidizing in silence. The launch was loud. The verdict will be quiet, and it is already accumulating, block by block, in exactly those four places.

And a final calibration on the number that started it all: by the time this piece publishes, the 26-to-1 ratio has already normalized into the single digits as TVL caught up with volume, which is the healthiest possible fate for an anomaly, becoming ordinary. Launch statistics are weather. The climate is what the dashboard above measures, and it has a quarter to declare itself.

One housekeeping note for the record: the figures in this autopsy, launch-day volume, TVL trajectory, transaction counts, and revenue, are drawn from public dashboards and on-chain data as reported in the launch week, and the fastest-moving of them will be stale within days, which is the nature of autopsies performed on living subjects. The framework travels; the numbers should be refreshed at the reader’s end.

The chain will publish its own verdict, block by block, whichever way it goes; few experiments in finance grade themselves this publicly, and fewer still have agreed to.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Digital asset markets are volatile and you can lose your entire investment. Figures are current as of July 9, 2026, and may change. Always do your own research.

Elon Musk once again captured investor attention with a blunt claim on X. He said SpaceX “will be worth more than the rest of Earth” if the company accomplishes its long-term goals.

Here is what Musk means, how the market values SpaceX today, and why the vision matters.

What Musk’s Bold SpaceX Claim Actually Means

Market cap is the total value of a company’s outstanding shares, calculated by multiplying its share price by the number of shares outstanding. Musk is not describing SpaceX’s value today, but a far larger future potential tied to a space-based economy.

Follow us on X to get the latest news as it happens.

His reasoning traces back to a January 2026 post. There, Musk argued that space industries “will vastly exceed the value of all of Earth.” Furthermore, he pointed to solar energy as the core driver of that exponential growth.

The math behind his vision is striking. Humanity could eventually harness roughly 100,000x more solar energy than it uses today. Moreover, that would consume less than one millionth of the Sun’s total energy output across the solar system.

For context, the global economy generates around $100 trillion in annual GDP. The IMF projects 2026 output closer to $109 to $110 trillion. Musk believes orbital manufacturing, asteroid mining, and Mars colonies could shatter those earthly limits entirely.

“SpaceX will be the world’s first $10 Trillion company. Calling it,” analyst Nic Cruz Patane said on X

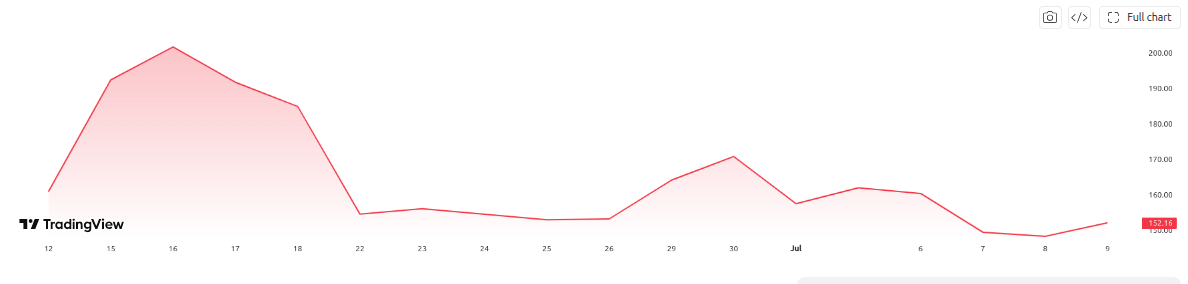

SPCX Fell 32% From Its ATH: What’s Next

The current market reflects strong belief, but also caution. SpaceX shares trade near $153, with a market cap close to $2 trillion, according to TradingView data. However, the stock has corrected roughly 32% from its June all-time high of $225.

Musk’s message carries both philosophical and strategic weight for markets. SpaceX’s ultimate goal is to make humanity a multiplanetary species. As a result, vehicles like Starship are critical to building a self-sustaining presence beyond Earth.

The vision also fuels speculation about deeper Tesla integration. JPMorgan recently described a potential merger between SpaceX and Tesla as “strategically coherent.” Moreover, the bank cited strong synergies across artificial intelligence, robotics, energy, and transportation.

However, that path faces real obstacles. JPMorgan also flagged significant regulatory hurdles, particularly in China. Consequently, any merger would require navigating complex approvals across multiple jurisdictions before unifying leadership and accelerating innovation.

Short-term technical signals remain mixed but are being closely watched. The stock recently tested key support near $145 to $150 after its steep post-IPO correction. Traders are eyeing a possible recovery if that support level continues to hold firmly.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights.

Beyond daily price action, investors keep betting on Musk’s ambition. SpaceX debuted with the largest IPO in history in June. Still, questions remain about execution timelines, costs, and the technical risks associated with his interplanetary economic vision.

The ultimate test lies ahead. Time and operational milestones will determine whether SpaceX can transcend not only its competitors, but the very economic boundaries of Earth itself, as Musk boldly predicts for the coming decades.

The post Elon Musk Bets SpaceX Will Outvalue Earth, SPCX Says Not Yet appeared first on BeInCrypto.

The European Parliament has voted to advance parts of the EU’s “chat control” regime, allowing tech companies to scan messages for child sexual abuse material until 2028. The measure—widely criticized by privacy and cryptography advocates—was set to expire in April, forcing lawmakers to decide whether to extend it.

While a majority backed the plan, the outcome was narrowly shaped by parliamentary procedure. According to HowTheyVote, 276 lawmakers supported the extension to stop it being rejected, while 314 voted against extending it. With the rejection threshold requiring 361 votes, the regulation moved forward after failing to secure enough opposition.

Key takeaways

- The Parliament’s vote revives the expired “Chat Control 1.0” framework, with scanning permitted until 2028.

- A carve-out was approved for communications where end-to-end encryption is used or will be used, excluding them from the rules in the relevant context.

- Because the regulation now goes to the EU Council, implementation ultimately depends on ministers from member states.

- Negotiations on a permanent “Chat Control 2.0” are set to resume in September, keeping encryption and scanning scope at the center of the fight.

What the Parliament approved—and what it tried to limit

EU lawmakers on Thursday largely voted against extending the “chat control” regulation, often described by critics as a form of mass surveillance. The mechanism allows certain forms of message scanning aimed at detecting child sexual abuse material. Supporters argue that the objective is essential for protecting children and disrupting the distribution of abusive content.

However, Parliament also approved an exemption aimed at preserving encryption. The decision excludes “communications to which end-to-end encryption is, has been or will be applied,” according to the exemption text referenced in the Parliament’s adopted materials (see TA-10-2026-0266_EN). For advocates of strong cryptography, this was framed as a meaningful limitation—though not an end to the broader scanning framework.

Pirate Party MEP Markéta Gregorová, whose party pushed for the amendment, called the result “a bittersweet victory.” In remarks cited by the Greens/EFA, she said the amendment secured “an absolute majority” in favor of protecting encryption, while “voluntary mass scanning unfortunately passed.”

Why the vote matters for messaging encryption and compliance

The controversy around “chat control” stems from how it interacts with encryption design. Encryption—especially end-to-end encryption—prevents service providers from reading message contents. Critics argue that forcing or incentivizing scanning undermines that core security principle, even when applied in narrowly defined circumstances.

Even with the end-to-end exemption, the Parliament’s action keeps the EU’s compliance direction moving toward detection mechanisms that may require changes to how platforms handle reporting, detection, and risk management. For developers and infrastructure teams, the immediate relevance is not only legal compliance but also how systems are architected to distinguish between encrypted traffic and other forms of communication, and how detection workflows are implemented without weakening privacy guarantees.

For users, the practical impact is uncertain: the measure advances to the Council, and the final shape will depend on how member states interpret and negotiate the text. Still, the policy direction—scanning permission extending through 2028—signals that the EU is not backing away from the core approach.

How “Chat Control 1.0” was extended after its April expiry

The Thursday vote is part of a process triggered by the expiry of the framework in April. As the rules lapsed, messaging services such as WhatsApp were allowed to adopt their own voluntary approaches to identify and respond to the sharing of abusive material, rather than being bound by an EU-wide framework.

Earlier in the week, on Tuesday, the Parliament voted using a rarely used urgent procedure to return to the question of whether to extend the legal basis. That followed a March decision where Parliament had rejected a temporary extension while a permanent “Chat Control 2.0” proposal was being discussed. In March, the European People’s Party—Parliament’s largest political group—had faced opposition over amendments that would have restricted the scope of scans. Yet in the urgent procedure vote on Tuesday, the group revived the extension push.

The internal political dynamics reflected the broader split in Parliament: while there was strong resistance to extending the scheme without changes, the voting threshold meant that the final outcome still leaned toward continuation of the framework.

Next phase: Council review and renewed “Chat Control 2.0” talks

After Thursday’s approval, the legislation with amendments will be sent back to the Council of the EU. The Council—comprised of member state ministers—must decide whether to approve or reject the text, which means the extension is not fully settled until negotiations complete.

Meanwhile, the fight is expected to continue. Earlier coverage noted that the political conflict over a permanent “Chat Control 2.0” is only beginning. As negotiations resume in September, lawmakers are reported to be divided over whether any scanning should be targeted or applied broadly.

For the crypto sector and privacy-focused communities, the critical uncertainty is how negotiators reconcile two competing goals: child safety and the preservation of message privacy at the protocol level. The end-to-end encryption exemption is a notable development, but the fact that voluntary mass scanning still cleared the procedural hurdle suggests that further rounds could again reshape the balance between compliance and cryptographic protections.

Readers should watch the Council’s stance and the September negotiations closely, because the final “Chat Control 2.0” design will determine whether encryption carve-outs remain meaningful in practice—or whether the scope of scanning expands again during final implementation.

Prediction market Polymarket applied for a license to offer U.S. users margin trading, enabling them to place bets with less upfront capital, Bloomberg reported Thursday.

Polymarket’s U.S. affiliate, Coming Home GBA LLC, filed for a futures commission merchant license with the National Futures Association, Bloomberg said, citing a company representative. Polymarket will also require authorization from the Commodity Futures Trading Commission (CFTC) for changes to its rulebook that would allow trading without fully collateralized positions.

Prediction market platforms like Polymarket and Kalshi offer yes-or-no wagers on the outcomes of events, such as weather, sports and elections. Margin trading lets investors open positions with less upfront capital, a practice common in traditional markets. Kalshi received clearance to offer margin trading in March.

Polymarket’s application comes as prediction markets continue to grow. Volumes hit $51 billion last year and are on pace to reach about $240 billion in 2026. Wall Street broker Bernstein recently said it expects volume to rise to $1 trillion by 2030 as the sector evolves from niche wagering into wide-based “information markets” spanning sports, crypto, politics and the economy.

Crypto World

Bitcoin trades above key technical support as 307 day consolidation nears historic record

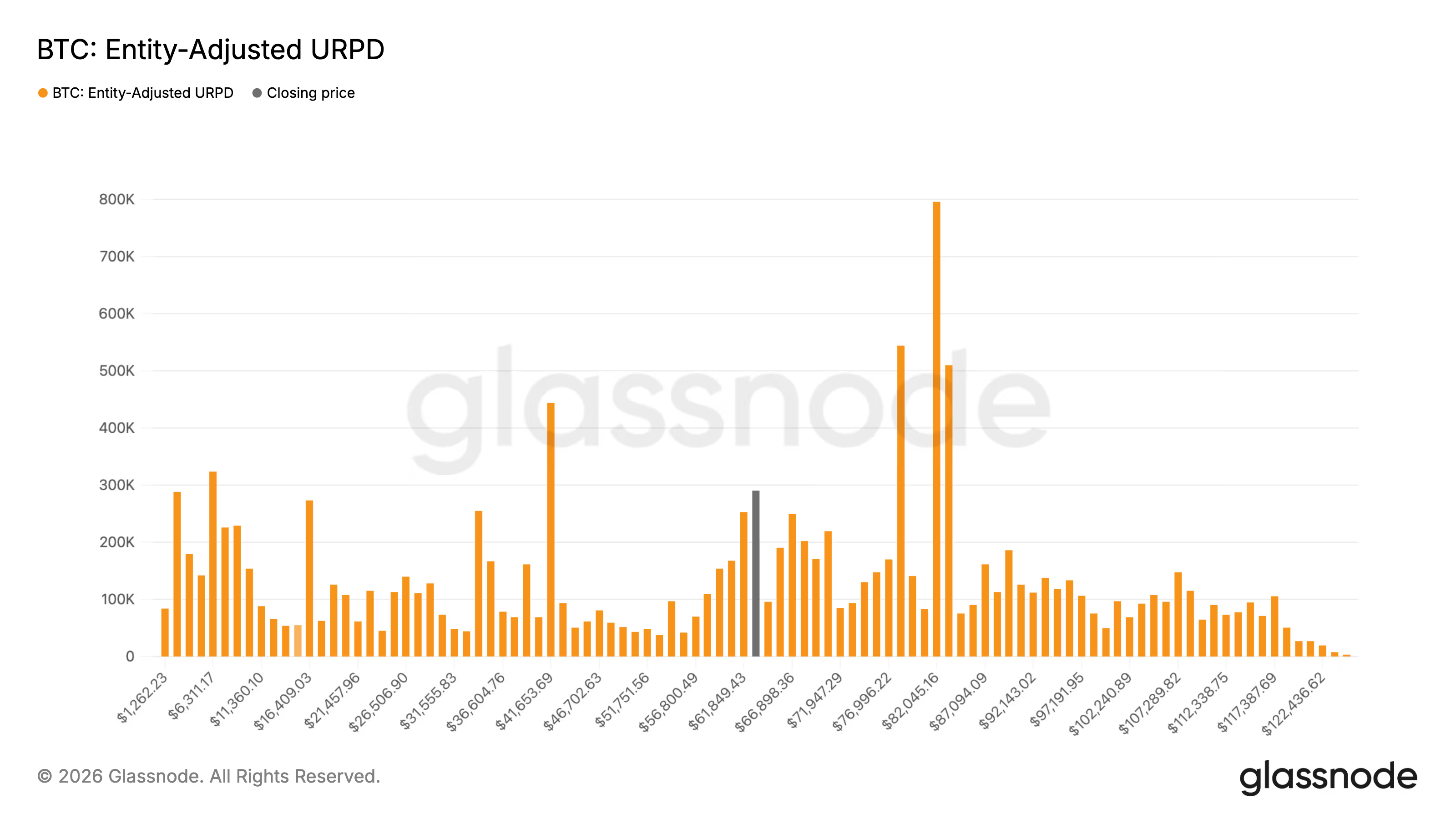

Bitcoin is trading around $64,000, marking 307 days within the $60,000- $70,000 range.

The consolidation range is now the third longest period spent in any $10,000 price band in bitcoin’s history, behind only the $10,000-$20,000 and $20,000-$30,000 ranges during the bear markets of 2018 and 2022 respectively, according to Glassnode data.

From a technical perspective, bitcoin continues to trade above its 200-week moving average, currently around $62,873. Historically, prolonged moves below this level have been short lived, making it a closely watched gauge of the long term trend.

Despite holding near $64,000, bitcoin remains roughly 50% below its all-time high reached in October.

Onchain data also points to a significant area of support. Glassnode’s Entity Adjusted UTXO Realized Price Distribution, which tracks the price at which bitcoin last changed hands between economic entities, shows that about 6% of the circulating supply sits between $58,000 and $64,000.

Whether this range ultimately resolves higher or lower remains uncertain, but the prolonged sideways trading has established one of bitcoin’s largest cost-basis clusters to date.

“The four companies will examine issues in product design, the need for proof-of-concept initiatives, and the possibility of future issuance,” Metaplanet said in a statement. “At this time, nothing has been determined regarding issuance timing, terms, yield, product details, distribution methods, or the form of collaboration.”

Japan’s traditional credit market leans in favor of large corporations with public bond offerings. Mid-sized and growth companies often face high costs and operational burdens around issuance, sales, investor management, interest payments and redemptions, according to Metaplanet.

Digital credit could open the debt market to these smaller companies, bridging traditional capital markets with onchain technology, enabling 24/7 global trading and settlement, holder-level rights management, automated pro-rata interest calculations and transparent onchain payments/redemptions.

Key roles

Each company is bringing its own strength to the table. Metaplanet and its securities arm will design and create the new products that combine bitcoin with credit offerings. They’ll also handle selling them to investors, communicating with customers, and managing everything afterward.

JPYC will explore the use of its stablecoin in the process, making sure it can be used smoothly for payments and redemptions.

Progmat will provide a secure, regulated system for turning the products into digital tokens on the blockchain. This includes tracking ownership, handling transfers, and connecting everything to the stablecoin payments system.

TLDR

- SK Hynix completed a historic $26.5 billion capital raise through US markets, setting a record for foreign company listings

- The offering saw oversubscription exceeding seven times available shares, signaling robust investor interest

- Trading commenced on Nasdaq today under ticker symbol “SKHY”

- Despite recent 25% decline over two weeks, SK Hynix stock has surged 680% year-over-year

- Capital will finance manufacturing expansion and equipment purchases to address AI semiconductor demand

On Thursday, South Korean memory chip manufacturer SK Hynix set its American Depositary Receipts at $149 apiece, successfully completing a landmark $26.5 billion fundraising that represents the biggest US listing ever achieved by an international corporation. The semiconductor producer issued 177.9 million ADRs, with individual units representing one-tenth of a common share traded in Seoul.

Trading activity for the new listing launched today on Nasdaq, where shares trade under the ticker symbol “SKHY.”

Investor enthusiasm for the offering proved substantial. According to a source with direct knowledge of the transaction, demand from institutional and retail buyers exceeded available shares by more than sevenfold, although SK Hynix refrained from providing official commentary regarding pricing dynamics or subscription levels.

The ADRs were established at a 2.7% premium relative to SK Hynix’s three-day average trading price preceding the offering.

SK Hynix stock advanced 5% during Thursday’s Seoul trading session, even as shares have retreated approximately 25% across the most recent two-week period. Notwithstanding this recent correction, the stock maintains remarkable gains of 680% over the trailing twelve months.

The company’s forward price-to-earnings multiple for the next twelve months currently stands at 5.5 times — representing a decline from 7.9 times recorded at October’s conclusion — while American competitor Micron trades at 6.66 times forward earnings.

This Nasdaq listing strategy aims partially to narrow the existing valuation disparity. Micron has traditionally enjoyed advantages from immediate access to American capital markets, despite commanding smaller market share across essential memory product categories.

“SK Hynix leads on share and Nvidia proximity, Micron competes on power efficiency, US positioning, and momentum from third place,” said Daniel Newman, CEO of Futurum Group.

Funds generated through this capital raise will support construction of additional manufacturing facilities and procurement of advanced equipment necessary to accommodate accelerating artificial intelligence chip requirements.

Why Investors Are Paying Attention

SK Hynix commands the leading position globally in high-bandwidth memory chip production — essential components integrated into cutting-edge processors that drive AI data centers worldwide.

Nvidia CEO Jensen Huang confirmed last month that SK Hynix would continue as Nvidia’s primary supplier, adding that prevailing chip supply constraints are anticipated to persist for multiple years ahead.

“As long as there is demand for graphic processors and AI data centers, SK Hynix is indispensable,” said Yoo Hoi-jun, an electrical engineering professor at KAIST.

According to Rolf Bulk, head of semiconductors at Futurum Equities, the HBM market is forecast to expand from approximately $65 billion during the current year to $120 billion by 2027, ultimately reaching roughly $290 billion by decade’s end in 2030.

Listing Comes at a Crossroads for Chip Stocks

The semiconductor sector overall has experienced some momentum loss during recent weeks, as market participants express concerns about the trajectory of AI infrastructure spending expansion affecting the industry.

SK Hynix’s market debut is drawing scrutiny as an indicator of whether strong demand for memory chip manufacturers persists. Market observers and industry analysts view this listing as a gauge for the broader artificial intelligence investment landscape.

“SK Hynix holds the edge in production scale and maturity. Since demand is far outweighing supply, they have had tremendous pricing power,” said Ken Mahoney, CEO of Mahoney Asset Management.

SK Hynix’s market capitalization surpassed $1 trillion in its domestic Korean market during May. Both SK Hynix and Samsung have now joined the exclusive circle of companies valued above $1 trillion, a group that includes Nvidia, Apple, Microsoft, and Alphabet.

South Korea’s government announced initiatives in June targeting over $880 billion in collaborative investment with SK Hynix and Samsung to advance the nation’s semiconductor and artificial intelligence infrastructure.

HSBC has completed its first blockchain-based issuance of a digitally native structured product, using tokenized U.S. dollar-denominated notes in a private placement for institutional investors in Hong Kong.

Summary

- HSBC completed its first blockchain based issuance of a digitally native structured product through a private placement in Hong Kong.

- Marketnode supported the transaction by issuing the notes on blockchain and managing digital payment flows between HSBC and the investor.

- The pilot builds on Hong Kong’s growing tokenization efforts as financial institutions continue testing blockchain for capital markets.

According to HSBC, the pilot transaction involved U.S. dollar-denominated structured notes issued in Hong Kong with support from Asia-Pacific digital market infrastructure operator Marketnode, which acted as both the tokenisation agent and digital paying agent.

By issuing the notes directly on blockchain, Marketnode enabled digital issuance while also managing payment flows between HSBC and the investor. HSBC said the pilot tested how tokenisation can make the issuance, settlement, administration, and servicing of structured products more efficient for institutional markets.

Speaking about the transaction, Suvir Loomba, regional head of securities services for Asia at HSBC and a board member of Marketnode, said the issuance builds on the bank’s digital asset work and demonstrates how it is working with market participants to develop practical blockchain solutions for institutional finance.

Loomba added that tokenisation can simplify multiple stages of a structured product’s lifecycle, including issuance, settlement, administration, and ongoing servicing.

“As one of the leading issuers of structured products in Asia, we see clear potential for tokenisation to improve the efficiency of issuance, settlement and servicing, whilst creating a more scalable foundation for future product innovation,” HSBC’s head of institutional sales for Asia, Patrick Boumalham, said in an accompanying statement.

According to HSBC, the structured product pilot forms part of its digital assets strategy and demonstrates how blockchain technology can be applied to improve capital markets processes for institutional participants.

Hong Kong continues to build tokenised markets

The latest pilot adds to Hong Kong’s ongoing push to bring traditional financial products onto blockchain infrastructure.

In June, the Hong Kong Monetary Authority established a tokenized bond expert group after the government issued more than HK$6.8 billion ($868 million) in tokenized bonds across several offerings. The group includes HSBC, JPMorgan Securities, Standard Chartered, UBS, Ant Digital, HashKey Group, and other market participants, and is examining legal frameworks, market practices, and infrastructure needed to expand tokenized bond activity.

HSBC has also continued to strengthen its digital asset presence in the city. In April, the bank became one of the first institutions to receive a Hong Kong Monetary Authority stablecoin issuer license under the city’s new regulatory framework, allowing it to issue regulated stablecoins alongside Standard Chartered-backed Anchorpoint Financial.

Bitcoin (BTC) institutional demand is “not yet strong” despite positive inflows to the US spot Bitcoin exchange-traded funds (ETFs).

Key points:

- Bitcoin ETF flows reverse a ten-day losing streak, but analysis warns that demand remains weak.

- An “overwhelming” sell-off is nonetheless over, says Swissblock.

- Overall BTC demand shows a clear gap between spot and derivatives trends.

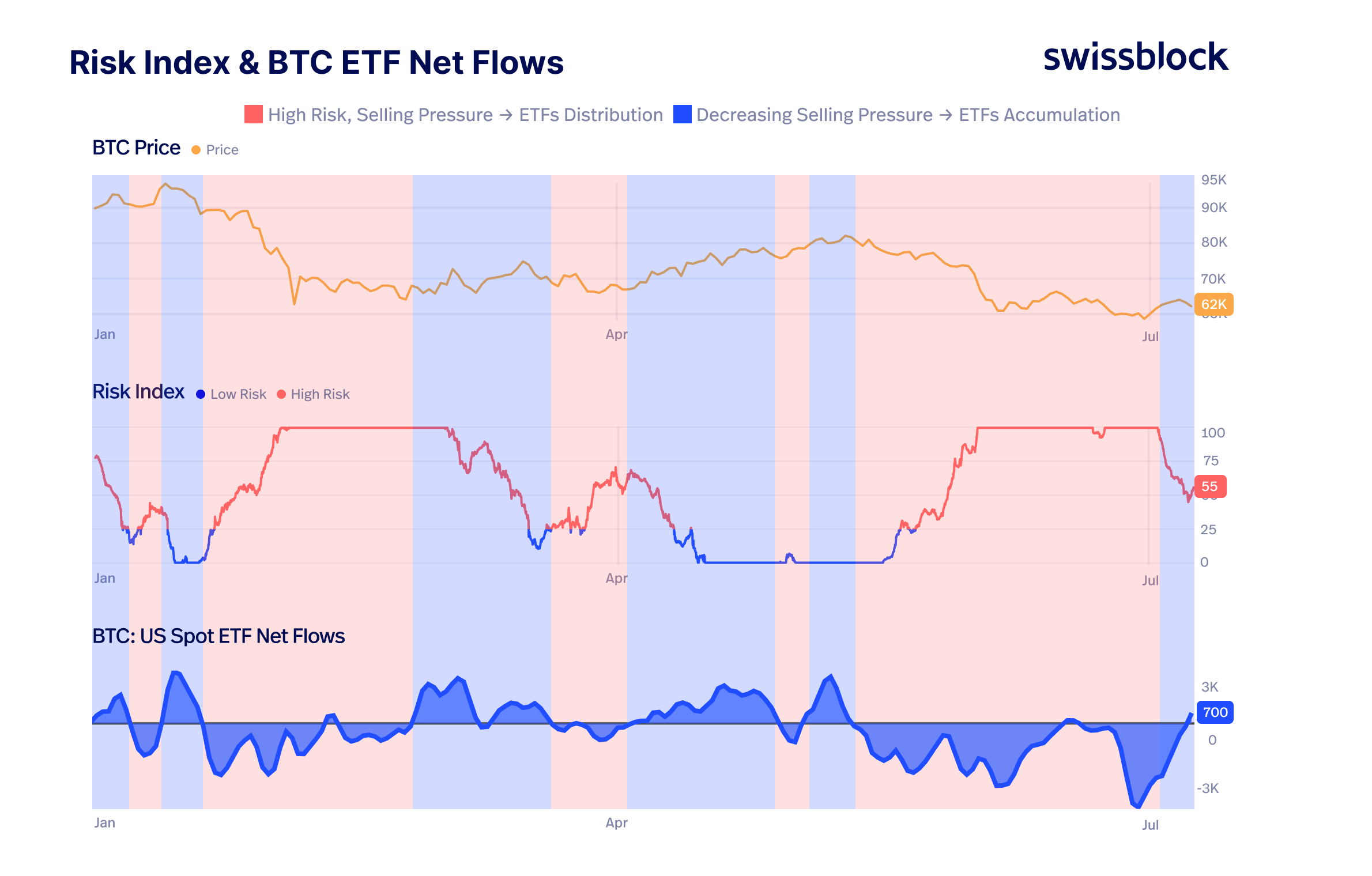

Swissblock on Bitcoin ETF outflows: “The storm has passed”

In new X commentary on Thursday, crypto investment company Swissblock called an end to the “most overwhelming” ETF sell-off in history.

“The storm has passed: The most overwhelming ETF distribution wave of this bear market has ended,” it wrote.

“As Bitcoin Risk continues easing from Capitulation Risk, Spot ETF flows have turned slightly positive again.”

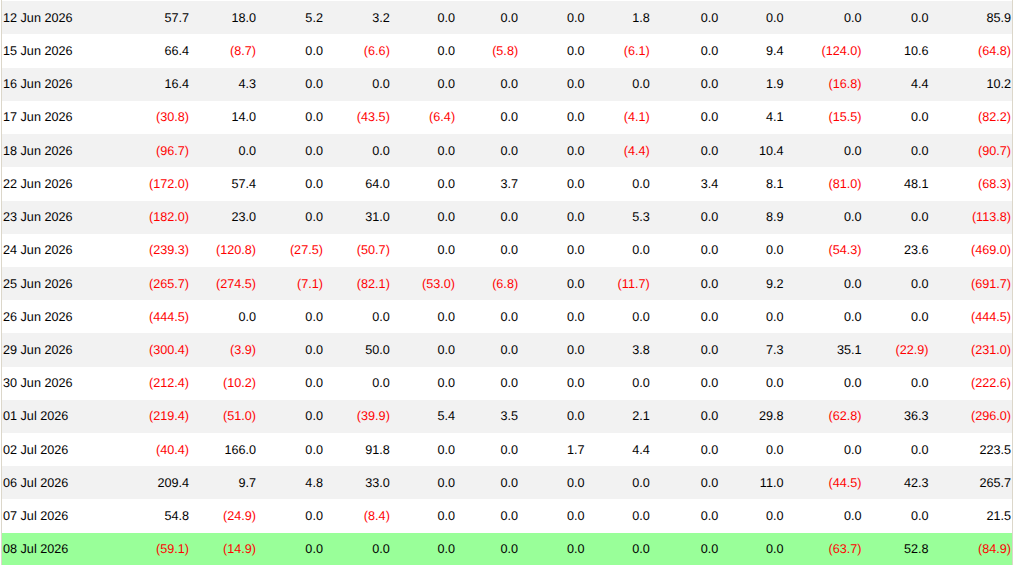

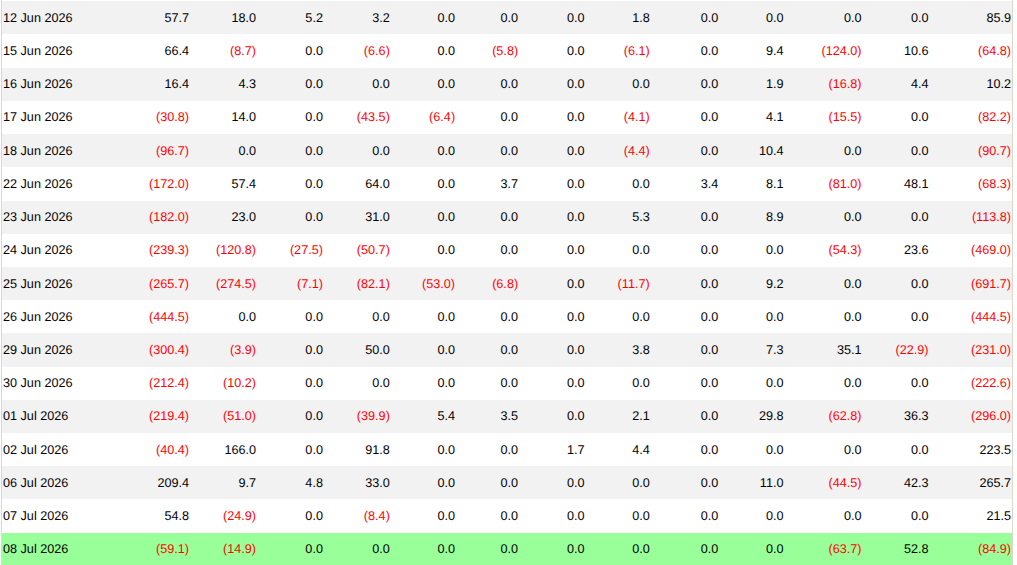

Beginning June 17, the ETFs saw ten straight days of net outflows totaling $2.7 billion, data from UK-based investment company Farside Investors confirms.

The cohort then began to reverse the trend, and saw over $500 million of net inflows over three trading days before a net $84.9 million outflow for Wednesday.

US spot Bitcoin ETF netflows (screenshot). Source: Farside Investors

Swissblock described the results as a “caveat” to the recovery signal.

“ETF accumulation is positive, but not yet strong. Institutional conviction is not returning with full force,” it added.

“Has the storm passed? Or is Bitcoin simply in the eye of the storm?”

US spot Bitcoin ETF netflows. Source: Swissblock/X

Bitcoin spot markets fail to match futures demand rebound

As Cointelegraph reported, analysis sees overall demand as a key stumbling block on the way to a bullish market recovery.

Related: BTC speculators in focus as analysis says ‘textbook Bitcoin bottom’ is underway

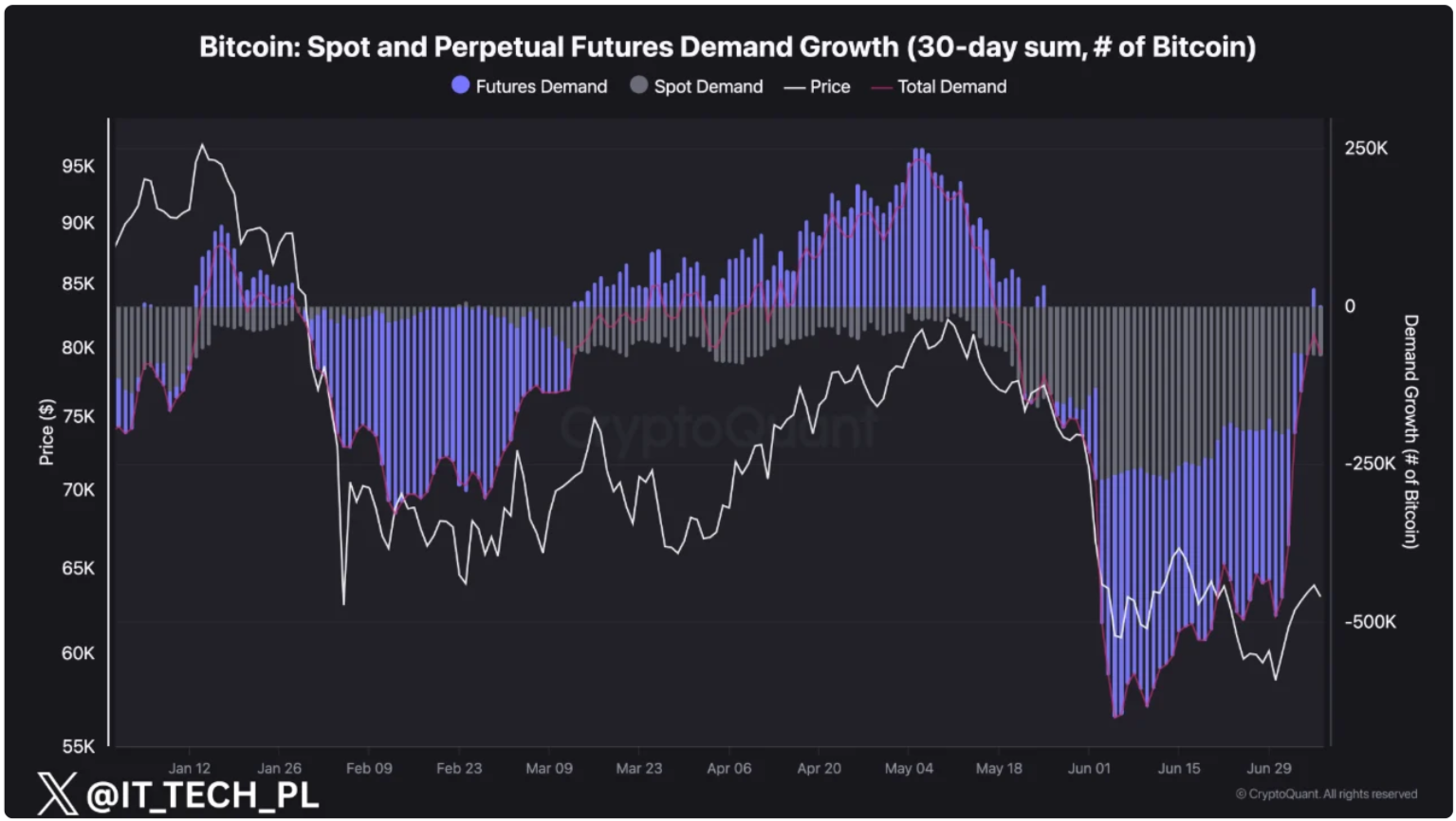

In fresh research for onchain analytics platform CryptoQuant this week, contributor IT Tech saw conditions partially improving, albeit with a clear divide between spot and derivatives markets.

“A week ago, the 30-day cumulative demand was close to -500K BTC. Today, it’s recovered to roughly -75K BTC,” they summarized.

In that time, futures demand went from -295,000 BTC to a “slightly positive” figure, while spot demand stayed negative.

“This tells us something important. The latest bounce has been driven primarily by derivatives traders, while spot buyers are still relatively cautious,” IT Tech commented.

“Historically, the strongest and most sustainable rallies begin when both futures and spot demand move higher together.”

Bitcoin demand comparison (screenshot). Source: CryptoQuant

Thai police uncovered a crypto-laundering scheme in which one suspect’s wallet processed more than $122.5 million in proceeds from romance scams, as part of a global INTERPOL sweep.

The international police organization’s Operation First Light 2026 ran from January 15 to April 30. It targeted social engineering scams and the money laundering that sustains them.

INTERPOL Says Global Fraud Crackdown Uncovered 142,000 Victims

According to the news release, the global anti-fraud operation spanned 97 countries and territories, resulting in the arrest of 5,811 suspects and the interception of approximately $293 million in illicit proceeds.

Investigators identified more than 142,000 victims and froze 31,014 bank accounts linked to fraudulent activity. The operation also led to the resolution of 23,715 cases, while authorities issued 99 notices and diffusions.

INTERPOL said the operation highlighted how social engineering scams and financial fraud have grown into a significant transnational threat, impacting individuals, businesses, and governments worldwide.

“Social engineering scams continue to pose a significant threat to our society. Criminal syndicates exploit human psychology to manipulate their targets, and no nation can stay safe unless all countries are equipped and committed to jointly fighting back,” Tomonobu Kaya, Director of the INTERPOL Financial Crime and Anti-Corruption Centre, said.

Follow us on X to get the latest news as it happens

Crypto Money Laundering at the Center of a Global Sweep

The operation also highlighted several significant cases uncovered by participating countries. In Thailand, police arrested two suspects tied to a crypto laundering scheme that funneled funds from romance scams.

The operators used cross-chain token swaps to break the trail between blockchains. One suspect, aged 20, controlled a wallet that processed more than $122.5 million in 10 months, according to investigators.

In Palau, officials deported 22 people linked to hotel-based scam centres that leaned on crypto and illegal gambling sites. Enforcement stretched across several countries.

In Eswatini, police arrested 82 people and broke up a network running illegal gambling, laundering, and impersonation scams. Authorities in Singapore and Oman used I-GRIP to block a $6.6 million transfer linked to a business email compromise scam.

The cases reflect the growing role of cryptocurrency in cross-border fraud and money laundering schemes. They also highlight the increasing reliance on international cooperation to track illicit funds, dismantle criminal networks, and disrupt scams that span multiple jurisdictions.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Global INTERPOL Crackdown Exposes Crypto Laundering Behind Romance Scams appeared first on BeInCrypto.

Politics Home Article | What Is Keir Starmer’s Legacy?

Cebu City to host 2027 Fiba Women’s Asia Cup

Govee 21-inch Smart Ceiling Light Ultra review: price, features

-

Fashion7 days ago

Fashion7 days agoWeekend Open Thread: High Hopes

-

NewsBeat5 days ago

NewsBeat5 days agoTaylor Swift and Travis Kelce wedding staffer hilariously struggles to keep her cool while checking in megastars

-

Crypto World7 days ago

Crypto World7 days agoStandard Chartered Secures MiCA License as ESMA Adds 37 New Crypto Firms

-

Fashion4 days ago

Fashion4 days agoOpen Thread: What Great Books Have You Read Recently?

-

Politics7 days ago

Politics7 days agoThe House | “Reframing the debate from a binary discussion of winners and losers”: Yuan Yang reviews ‘We Are Not Machines’

-

Fashion23 hours ago

Fashion23 hours agoLoro Piana Fall 2026 Enters Houston’s Art Scene

-

News Videos3 days ago

News Videos3 days agoWhats Hidden Inside This Cash Register? #treasure #reselling #money

-

Tech3 days ago

Tech3 days agoAnthropic’s new “J-lens” reveals a silent workspace inside Claude that mirrors a leading theory of consciousness

-

Crypto World7 days ago

Crypto World7 days agoESMA Expands Crypto Register by 37 Firms Following MiCA Transition Period

-

Business4 days ago

Business4 days agoAXT Shares Jump Nearly 14% as Semiconductor Materials Maker Rebounds on AI-Linked Indium Phosphide Demand

-

Sports3 days ago

Sports3 days agoJoshua Pacio ‘more complete’ ahead of ONE rematch vs Malachiev

-

Crypto World4 days ago

SK hynix (000660.KS) Stock Dips as $28B Nasdaq ADR Offering Drives AI Memory Expansion

-

Crypto World5 days ago

Crypto World5 days agoSouth Africa proposes crypto tax guidance under existing rules

-

News Videos4 days ago

News Videos4 days agoBest Time to Enter Small Caps Right Now? Another Bull Run? | Financially Free

-

Tech5 days ago

Tech5 days agoLenovo laptops are now shipping with YMTC SSDs, a sign of Chinese NAND entering the mainstream

-

Sports3 days ago

We have punished the disrespect

-

News Videos4 days ago

News Videos4 days agoAvoid entering in FOMO #bitcoin #cryptocurrency #trading #scalping

-

Tech2 days ago

Tech2 days agoAnthropic brings Claude Cowork to mobile and web as usage data shows most users aren’t coding

-

Tech6 days ago

Tech6 days agoNeuralink Threads Its Way Straight Through the Brain’s Armor

-

Crypto World4 days ago

Crypto World4 days ago$1,000 Credit Alert! BlockDAG X Exchange Pre-Registration Now Officially Open, Polkadot Dips & Zcash Rebounds

You must be logged in to post a comment Login