Crypto World

EU Parliament Approves ‘Chat Control,’ Exempts E2EE Until 2028

The European Parliament has voted to advance parts of the EU’s “chat control” regime, allowing tech companies to scan messages for child sexual abuse material until 2028. The measure—widely criticized by privacy and cryptography advocates—was set to expire in April, forcing lawmakers to decide whether to extend it.

While a majority backed the plan, the outcome was narrowly shaped by parliamentary procedure. According to HowTheyVote, 276 lawmakers supported the extension to stop it being rejected, while 314 voted against extending it. With the rejection threshold requiring 361 votes, the regulation moved forward after failing to secure enough opposition.

Key takeaways

- The Parliament’s vote revives the expired “Chat Control 1.0” framework, with scanning permitted until 2028.

- A carve-out was approved for communications where end-to-end encryption is used or will be used, excluding them from the rules in the relevant context.

- Because the regulation now goes to the EU Council, implementation ultimately depends on ministers from member states.

- Negotiations on a permanent “Chat Control 2.0” are set to resume in September, keeping encryption and scanning scope at the center of the fight.

What the Parliament approved—and what it tried to limit

EU lawmakers on Thursday largely voted against extending the “chat control” regulation, often described by critics as a form of mass surveillance. The mechanism allows certain forms of message scanning aimed at detecting child sexual abuse material. Supporters argue that the objective is essential for protecting children and disrupting the distribution of abusive content.

However, Parliament also approved an exemption aimed at preserving encryption. The decision excludes “communications to which end-to-end encryption is, has been or will be applied,” according to the exemption text referenced in the Parliament’s adopted materials (see TA-10-2026-0266_EN). For advocates of strong cryptography, this was framed as a meaningful limitation—though not an end to the broader scanning framework.

Pirate Party MEP Markéta Gregorová, whose party pushed for the amendment, called the result “a bittersweet victory.” In remarks cited by the Greens/EFA, she said the amendment secured “an absolute majority” in favor of protecting encryption, while “voluntary mass scanning unfortunately passed.”

Why the vote matters for messaging encryption and compliance

The controversy around “chat control” stems from how it interacts with encryption design. Encryption—especially end-to-end encryption—prevents service providers from reading message contents. Critics argue that forcing or incentivizing scanning undermines that core security principle, even when applied in narrowly defined circumstances.

Even with the end-to-end exemption, the Parliament’s action keeps the EU’s compliance direction moving toward detection mechanisms that may require changes to how platforms handle reporting, detection, and risk management. For developers and infrastructure teams, the immediate relevance is not only legal compliance but also how systems are architected to distinguish between encrypted traffic and other forms of communication, and how detection workflows are implemented without weakening privacy guarantees.

For users, the practical impact is uncertain: the measure advances to the Council, and the final shape will depend on how member states interpret and negotiate the text. Still, the policy direction—scanning permission extending through 2028—signals that the EU is not backing away from the core approach.

How “Chat Control 1.0” was extended after its April expiry

The Thursday vote is part of a process triggered by the expiry of the framework in April. As the rules lapsed, messaging services such as WhatsApp were allowed to adopt their own voluntary approaches to identify and respond to the sharing of abusive material, rather than being bound by an EU-wide framework.

Earlier in the week, on Tuesday, the Parliament voted using a rarely used urgent procedure to return to the question of whether to extend the legal basis. That followed a March decision where Parliament had rejected a temporary extension while a permanent “Chat Control 2.0” proposal was being discussed. In March, the European People’s Party—Parliament’s largest political group—had faced opposition over amendments that would have restricted the scope of scans. Yet in the urgent procedure vote on Tuesday, the group revived the extension push.

The internal political dynamics reflected the broader split in Parliament: while there was strong resistance to extending the scheme without changes, the voting threshold meant that the final outcome still leaned toward continuation of the framework.

Next phase: Council review and renewed “Chat Control 2.0” talks

After Thursday’s approval, the legislation with amendments will be sent back to the Council of the EU. The Council—comprised of member state ministers—must decide whether to approve or reject the text, which means the extension is not fully settled until negotiations complete.

Meanwhile, the fight is expected to continue. Earlier coverage noted that the political conflict over a permanent “Chat Control 2.0” is only beginning. As negotiations resume in September, lawmakers are reported to be divided over whether any scanning should be targeted or applied broadly.

For the crypto sector and privacy-focused communities, the critical uncertainty is how negotiators reconcile two competing goals: child safety and the preservation of message privacy at the protocol level. The end-to-end encryption exemption is a notable development, but the fact that voluntary mass scanning still cleared the procedural hurdle suggests that further rounds could again reshape the balance between compliance and cryptographic protections.

Readers should watch the Council’s stance and the September negotiations closely, because the final “Chat Control 2.0” design will determine whether encryption carve-outs remain meaningful in practice—or whether the scope of scanning expands again during final implementation.

HashKey Exchange said on Aug. 3 that JPMorgan Chase approved its application to open a client funds account, giving the Hong Kong licensed crypto platform another banking route for customer money segregation and U.S. dollar settlement.

Summary

- HashKey received JPMorgan approval to open a segregated client funds account supporting dollar settlement services.

- HashKey says it became Asia’s first licensed digital asset exchange approved for this JPMorgan account.

- DBS activated a separate HashKey customer funds account on June 30 for fiat settlement services.

- Hong Kong rules require foreign currency client money to remain segregated in the same currency.

- HashKey has not disclosed when the JPMorgan account will become operational for customer transaction services.

Parent company HashKey Holdings said the approval would connect the exchange more closely with international banking infrastructure. The announcement did not disclose the account’s launch date, expected balances, supported payment routes or commercial terms.

HashKey JPMorgan account adds a new dollar channel

HashKey said the account would strengthen the stability and transparency of its U.S. dollar funding channels. It also expects the arrangement to support settlement for institutional clients and investors using its regulated exchange.

The company described HashKey Exchange as “the first” licensed digital asset exchange in Asia approved to open this type of JPMorgan account. That remains a company claim. The announcement confirms approval to open an account, rather than the start of live customer deposits and withdrawals.

In addition, the account is designed to hold customer money separately from HashKey’s operating funds. Hong Kong’s Securities and Futures Commission requires licensed virtual asset platforms to keep foreign currency client money in segregated accounts denominated in the same currency.

Hash Blockchain Limited, which operates HashKey Exchange, appears on the SFC’s list of licensed virtual asset trading platforms. The regulator granted its licence in November 2022. The SFC also states that licensing does not guarantee a platform’s performance or creditworthiness.

Moreover, the JPMorgan approval follows HashKey’s June 30 activation of a customer funds account with DBS Bank. The DBS arrangement supports fiat deposits, withdrawals and transaction settlement. It also includes same name virtual accounts for automated fund identification and reconciliation.

DBS was Singapore’s largest bank, with assets of about $697.77 billion at the end of 2025, according to S&P Global Market Intelligence. JPMorgan retained fifth place in S&P’s worldwide ranking. HashKey’s use of both banks gives it separate links to major Asian and U.S. dollar banking infrastructure.

Banking access supports HashKey’s institutional expansion

HashKey has expanded its regulated platform and traditional finance connections since listing in Hong Kong in December 2025. Its offering raised gross proceeds of HK$1.607 billion, about $206 million, before listing costs. JPMorgan was among the joint sponsors of the offering.

As crypto.news previously reported, HashKey opened the IPO with a target of up to $215 million before final pricing. In related coverage, JPMorgan and HashKey later joined a Hong Kong Monetary Authority group studying rules and infrastructure for tokenized bonds.

HashKey also merged the separate HashKey Exchange and HashKey Global applications into one portal in July. The company said jurisdictional controls still separate users and products across Hong Kong, Singapore, Dubai and Bermuda.

The JPMorgan account does not expand HashKey’s crypto licence or allow the exchange to serve restricted U.S. customers. Its stated purpose is to add another regulated banking channel for fiat funds connected to the exchange.

The next verified milestone will be account activation. HashKey has not said when customers can use the JPMorgan route, which currencies will be available at launch or whether access will begin with institutional clients before reaching other eligible users.

American Bitcoin Corp., the Bitcoin miner co founded by Eric Trump and majority owned by Hut 8, reported a $57.2 million net loss for the second quarter on Aug. 3.

Summary

- American Bitcoin reported a $57.2 million loss after recording $71.2 million in digital asset losses.

- Bitcoin holdings rose 14% to 8,002 BTC, including 3,090 BTC pledged under Bitmain purchase agreements.

- Mining output reached a record 932 BTC while quarterly revenue increased 8% to $67 million.

- American Bitcoin’s mining cost remained near $36,500 per coin, broadly unchanged from the previous quarter.

- Adjusted EBITDA improved to a $45 million loss from a $91.3 million loss in March.

The result included a $71.2 million loss on digital assets, even as the company delivered record production and expanded its reserve to approximately 8,002 BTC, according to its official quarterly results.

The loss narrowed from $81.8 million in the first quarter. Revenue increased from $62.1 million to $67 million, while adjusted EBITDA remained negative at $45 million, compared with a $91.3 million loss three months earlier.

American Bitcoin’s asset loss drove the quarterly deficit

The digital asset loss remained the largest expense in the quarter. It fell from $117.2 million in the first quarter to $71.2 million but still exceeded American Bitcoin’s entire quarterly mining revenue. Depreciation and amortization added another $28.2 million, while general and administrative expenses reached $7.7 million.

The $71.2 million figure is an accounting loss recorded within operating expenses. It should not be confused with the cost of producing Bitcoin or automatically treated as an equivalent cash outflow. American Bitcoin did not disclose how much of the loss resulted from completed transactions during the quarter.

The company also recorded an $18.3 million gain on derivatives, reducing its loss before taxes to $55.7 million. Its adjusted EBITDA calculation excludes several items, including depreciation, derivative gains and stock compensation.

American Bitcoin warns that adjusted EBITDA is a company defined measure and should not replace results reported under generally accepted accounting principles.

Record mining raised revenue while costs stayed flat

American Bitcoin mined approximately 932 BTC during the quarter, up from 817 BTC in the first quarter. The result marked its highest quarterly production since the business launched in March 2025 and represented about 26% of all Bitcoin it has mined since then.

Revenue per Bitcoin mined fell about 5% to $71,900 as Bitcoin prices weakened. However, the cost to mine each coin remained near $36,500, compared with $36,200 in the previous quarter. The company attributed the increase to higher energy expenses at selected locations.

Based on the reported $67 million in revenue and $34 million in direct revenue costs, mining gross profit was approximately $33 million. That produces a margin of roughly 49%, supporting management’s statement that the figure remained close to 50% despite a 12% quarterly decline in Bitcoin’s price.

The operational fleet reached about 58,999 miners with 25 EH/s of computing power. American Bitcoin also completed the energization of 11,298 newer machines at Hut 8’s Drumheller location in April, adding approximately 3.05 EH/s.

Nearly 39% of the Bitcoin reserve remains pledged

American Bitcoin’s holdings increased by approximately 981 BTC during the quarter, rising from 7,021 BTC to 8,002 BTC. Mining produced 932 BTC, accounting for most of the increase.

However, not all 8,002 BTC are freely available. Approximately 3,090 BTC, or nearly 39% of the reserve, remain pledged under miner purchase agreements with Bitmain. American Bitcoin still includes those coins in its total because it retains redemption rights and continued economic exposure.

The company’s first quarter SEC filing classified the pledged holdings as restricted Bitcoin. It also recorded a miner purchase liability of $364.3 million as of March 31. The latest results did not provide an updated liability figure for June 30.

The company acquired large batches of Bitmain equipment through agreements that allowed it to pledge Bitcoin instead of paying the full purchase price in cash. Redemption periods generally run for about 24 months, although some extension options may apply.

Reserve growth has not removed pressure on ABTC shares

American Bitcoin said its satoshis per share increased 11% to approximately 10,989 during the quarter. Holdings grew 14%, while outstanding shares increased about 3%.

The figures account for the one for fifteen reverse stock split completed in July. According to the company’s SEC filing on the split, issued shares fell from approximately 1.09 billion to about 73 million. Split adjusted trading began on July 6 under the existing ABTC ticker.

As crypto.news previously reported, American Bitcoin’s reserve surpassed 8,000 BTC in July as the company continued accumulating coins despite pressure on its share price. The earlier update also showed that the reverse split raised ABTC’s quoted price without changing its underlying market value.

ABTC had fallen more than 95% from its peak by mid July. The decline came even as the company expanded its Bitcoin reserve and lowered its production cost compared with late 2025.

Chief Executive Mike Ho said the company believes Bitcoin’s “long term compounding will outperform our cost of capital.” Eric Trump said its objective was “relentless growth.” Both statements describe management’s expectations rather than assured financial results.

The company’s Aug. 3 earnings call and any later SEC filing could provide further details about Bitmain liabilities, mining expansion and the treatment of its digital asset losses. Investors will also be watching whether higher production can move adjusted EBITDA toward profitability without requiring the company to sell its Bitcoin reserve.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Orbs launches OIP-9, its first governance vote to establish the Orbs DAO and advance protocol decentralization.

Summary

- Orbs launched OIP-9, its first formal community vote, to establish an initial DAO governance framework.

- Staked token holders would vote through Snapshot, while multisig wallets would implement approved community decisions.

- The proposal starts with limited authority and allows responsibilities to move gradually toward community control.

Orbs has announced OIP-9, its first formal community governance vote. The online proposal asks eligible participants to establish the Orbs DAO and approve its initial governance framework. It aims to move defined protocol decisions toward the community through a phased process. Holders of tokens staked in the Orbs Proof-of-Stake contract would vote through Snapshot.

The proposal marks the next stage in Orbs’ governance evolution following more than seven years of protocol development and nearly four years of on-chain governance. During that time, the network has grown into a live Layer-3 infrastructure powering decentralized finance applications and execution products across multiple blockchain ecosystems. The governance proposal formalizes the role of the community in overseeing the protocol through a structured, phased approach that prioritizes both decentralization and operational security.

Ran Hammer, Vice President of Business Development at Orbs, said the proposal is designed to balance decentralization with the community’s governance capabilities. According to Hammer, it establishes a governance framework with clearly defined authority from the outset while enabling the community to gradually assume greater responsibility over time. He added that the approach is intended to lay the groundwork for the next phase of the Orbs ecosystem.

Under OIP-9, governance participation will initially be open to holders of tokens staked in the Orbs Proof-of-Stake contract. The DAO will operate through community proposals and Snapshot voting, with approved decisions implemented through dedicated DAO-controlled multisig wallets. If approved, the DAO will initially oversee selected network parameters governing the Proof-of-Stake infrastructure, Guardian certification and revocation, approval of major protocol upgrades, and approval of new protocol deployments and network-level product modules. Together, these responsibilities are designed to give the community meaningful authority over the network while keeping the initial scope focused and manageable.

Rather than attempting to decentralize every aspect of the protocol at once, the proposal adopts a progressive governance model that expands community responsibility over time. Future governance proposals may address areas including protocol revenue, treasury management, liquidity strategies, grants, burn mechanisms, and broader tokenomics as the DAO develops operational experience and governance processes.

To help ensure network stability during the transition, the proposal also includes a limited emergency mechanism allowing the Orbs core team to respond when immediate action is required, and community voting is not feasible. Any use of these emergency powers would subsequently require ratification through DAO governance, preserving transparency and community oversight.

Orbs presents the vote as a step from existing governance participation toward formal DAO authority. Approval would create the initial foundation, while later votes could widen the community’s role through future proposals covering economic and operational areas not included initially as the governance framework develops gradually through later voting cycles.

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

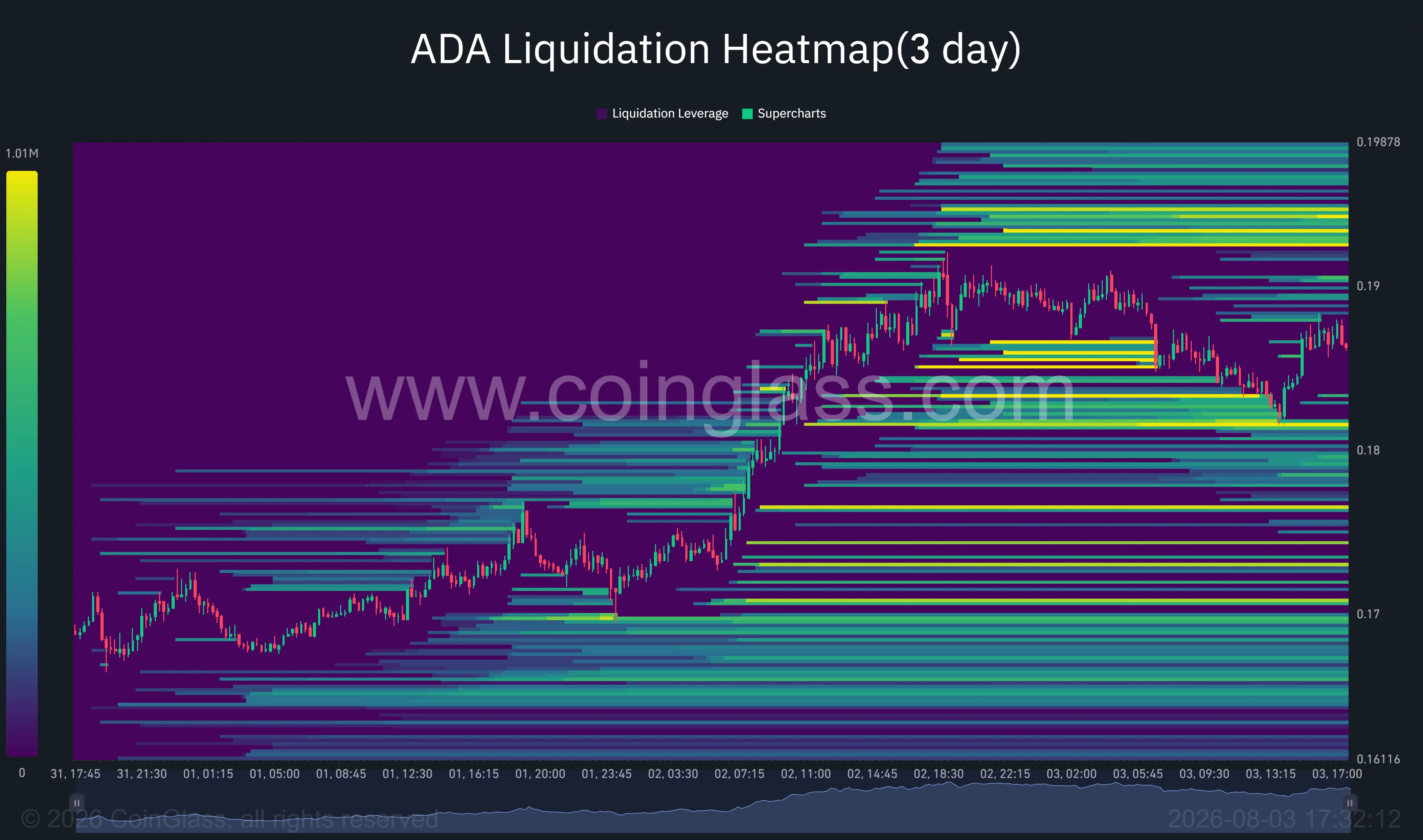

Cardano price rallied as high as $0.190 after whales accumulated 240 million ADA, while a bullish reversal pattern pointed to a possible extension toward $0.208.

Summary

- Cardano whales accumulated more than 240 million ADA over five days, according to Santiment data.

- ADA climbed about 22% from its July low before pulling back to approximately $0.186.

- A 4-hour inverse head-and-shoulders pattern carries a potential $0.208 price target.

- Liquidation clusters near $0.193–$0.195 could attract price if buyers reclaim $0.190.

Cardano price trims gains after reaching $0.190

According to data from crypto.news, Cardano (ADA) price traded near $0.186 on Aug. 3 after touching an intraday high of $0.190, extending its recovery from the July 8 low near $0.154.

The move left ADA roughly 20% above that floor, although profit-taking emerged after the token tested the upper boundary of its recent trading range. The daily candle was down about 1.4% at the time of the chart snapshot.

ADA’s latest advance also pushed it above the Bollinger Bands’ 20-day moving average at $0.1688. The level had contained several recovery attempts during July and may now serve as medium-term support.

The price briefly moved above the upper Bollinger Band, located near $0.1846. Trading outside the band reflects strong momentum, but it can also indicate that the rally has become stretched in the short term.

Bollinger Bandwidth rose to 0.0262 as the bands expanded, confirming that volatility returned after several weeks of consolidation. The increase supports the breakout but also raises the risk of larger intraday reversals.

Whale accumulation helped fuel the ADA rally

Large holders were a central driver of the move. Analyst Ali Martinez cited Santiment data showing that whales accumulated more than 240 million ADA over five days.

“Whales loaded up. Cardano took off,” Martinez wrote.

The reported holdings increased from around 14.1 billion ADA to more than 14.3 billion ADA during the period. That accumulation coincided with a roughly 22% price increase, suggesting that large buyers absorbed supply as ADA recovered.

The rally also followed Cardano’s July 18 protocol upgrade and the network’s transition toward its next development phase. Expectations surrounding future scaling work, including Ouroboros Leios, added a fundamental catalyst to the whale-led move.

Cardano is also approaching six months of CME futures trading on Aug. 9. That milestone could become relevant to prospective US spot ADA exchange-traded fund applications under generic listing requirements, although it would not guarantee regulatory approval.

US traders will therefore be watching whether the futures record strengthens the case for broader regulated ADA investment products. Any ETF progress would still depend on the filing structure and applicable SEC requirements.

ADA inverse head-and-shoulders targets $0.208

The 4-hour chart shows ADA completing an inverse head-and-shoulders pattern between July 10 and Aug. 2. The formation includes two rounded shoulders near $0.160 and a deeper head around $0.154.

ADA broke above the pattern’s $0.1808 neckline on Aug. 2 and subsequently reached $0.190. The measured distance between the head and neckline is approximately $0.0274.

Adding that distance to the breakout point produces an upside target near $0.2083, about 12% above the current price. A sustained 4-hour close above $0.190 would strengthen the case for that extension.

Money flow remains supportive. The 4-hour Chaikin Money Flow reading stood at 0.16, showing that buying pressure continued to outweigh selling pressure despite the pullback.

However, the Aroon indicator presents a more cautious near-term picture. Aroon Down stood at 57.14%, while Aroon Up had fallen to zero, suggesting that the breakout’s immediate upward momentum was cooling.

Analyst Gerla also identified an inverse head-and-shoulders formation on the daily chart after a bullish RSI divergence played out. That broader pattern places the immediate resistance zone around $0.190–$0.195.

ADA must convert that area into support before the market can target $0.208. Failure to hold the $0.1808 neckline would weaken the bullish pattern and expose the 20-day average at $0.1688.

Liquidation levels could determine ADA’s next move

The 3-day liquidation heatmap shows dense leveraged positions on both sides of the current price, creating conditions for continued volatility.

The nearest downside liquidity sits around $0.181–$0.183, close to the inverse head-and-shoulders neckline. A decline into that zone could trigger long liquidations before buyers attempt another defense.

Larger pools of liquidity appear above the market between approximately $0.193 and $0.195. These levels could act as short-term price magnets if ADA retakes $0.190, but they may also generate resistance as short positions are closed and traders take profits.

Additional overhead liquidity extends toward $0.198, while lower clusters are visible near $0.176 and $0.170. This leaves ADA inside a broad leveraged range where a break on either side could accelerate the next move.

The bullish scenario requires ADA to remain above $0.1808 and close decisively above $0.195. That would open a path toward the pattern target at $0.2083.

A close below $0.1808 would indicate that the breakout is losing strength. In that case, $0.1688 becomes the main support, followed by the lower Bollinger Band near $0.153.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Stacks explores Bitcoin staking and DeFi growth as investors assess STX’s 2026 potential amid efforts to bring more Bitcoin capital into productive use.

Summary

- Stacks faces a key 2026 test as its Bitcoin staking plans aim to expand BTC utility and STX demand.

- STX price predictions focus on whether Stacks can unlock Bitcoin liquidity through native staking and DeFi.

- Stacks eyes Bitcoin yield expansion as its upcoming staking system could drive new demand for STX.

Any Stacks (STX) price prediction for 2026 increasingly turns on a question bigger than short-term market momentum: can Stacks convert a small share of Bitcoin’s largely underused capital base into recurring demand for STX?

The gap is large. DeFiLlama currently tracks about $4.35 billion in total value locked across the Bitcoin category against a Bitcoin market capitalization of roughly $1.33 trillion, equal to only about 0.3%. Stacks is positioning its planned self-custodial Bitcoin staking system as one route for bringing more BTC into productive use without requiring holders to bridge or wrap their coins.

STX already serves as the native asset used to pay transaction fees on Stacks and participate in the network’s existing Stacking system. Its expanding role also supports the case for STX as capacity to grow Bitcoin native finance, particularly as Stacks develops new ways for Bitcoin holders to put their capital to work. The proposed Bitcoin staking design would mean that participants would lock BTC on Bitcoin Layer 1 and pair it with STX worth approximately 5% of the BTC position to create a protocol bond. The current design targets about 3% annualized yield in BTC, funded by Bitcoin committed by Stacks miners through Proof of Transfer, or PoX.

The attraction is easy to understand. Stacks says PoX has distributed more than 4,200 BTC to stackers since 2021, giving the proposed product an existing source of Bitcoin-denominated rewards rather than a new emissions-funded incentive. The key caveat is timing: Bitcoin staking was operating on a private testnet as of July 16, 2026, with mainnet activation still ahead.

How Bitcoin staking could create direct STX demand

The strongest part of the STX token fundamentals case is the proposed protocol-bond requirement.

Under the current design, every BTC position entering Bitcoin staking needs a corresponding STX position worth roughly 5% of the Bitcoin being bonded. That creates a direct relationship between BTC participation and the amount of STX needed to access staking capacity.

At the roughly $66,200 BTC price recently tracked by DeFiLlama, 5,000 BTC entering the system would require about $16.6 million in paired STX value. A 50,000 BTC cohort would imply about $165.5 million, assuming the approximate 5% ratio remains in place. Those figures are illustrations rather than forecasts: the STX-to-BTC ratio is designed to become market-driven, and the protocol limits capacity based on its ability to support reward obligations.

That distinction matters for any STX crypto analysis. Protocol-bond demand would be tied to use of the system rather than a marketing campaign or discretionary token incentive. Yet it would not automatically translate into equivalent open-market buying. Participants could source STX through exchanges, over-the-counter transactions, existing holdings or future financing arrangements.

Even so, the mechanism gives STX a measurable demand channel. More BTC entering protocol bonds would require more STX capacity under the current model, while lower participation would produce less demand. That makes adoption of Bitcoin staking one of the clearest variables to watch when assessing the token.

Why lockups and network use matter for STX tokenomics

Demand is only one side of the equation. The proposed bonding structure could also reduce the amount of STX readily available for trading during each bonding period.

Protocol bonds are designed around an approximately six-month term. The paired STX remains locked for that period and cannot simultaneously be used elsewhere. Stacks’ design includes an early-exit path for BTC, but an exiting participant forfeits remaining yield and the paired STX stays committed for the original term.

That creates a possible supply-compression effect if Bitcoin staking attracts meaningful participation. New STX demand could arrive at the same time as bonded tokens become temporarily unavailable to the market.

STX also remains the gas asset for the network. Every transaction, including lending, swaps and other smart-contract activity, requires STX for fees. If Bitcoin staking brings more users and capital into Stacks-based applications, transaction demand could add another source of token utility alongside the protocol-bond requirement.

The Bitcoin DeFi flywheel, and where it can break

Stacks already has a live DeFi base, which gives new capital somewhere to move if Bitcoin staking reaches mainnet and gains users. DeFiLlama currently tracks about $86 million in Stacks DeFi TVL, with Zest Protocol accounting for roughly $69 million. Zest separately reports around 800 BTC deposited in its Stacks market and says deposits previously peaked above $100 million.

That existing activity matters because the broader STX thesis extends beyond the first protocol bond. The project’s stated model assumes that, if STX rises in value during a six-month bond, a participant may need fewer STX tokens to support the same BTC value in a later bonding period. The unused STX could then be redeployed into lending markets, decentralized exchanges or other applications.

That outcome is possible, but it is not automatic. Participants may sell surplus STX, hold it, hedge the exposure or choose not to renew a bond. The strength of the proposed flywheel therefore depends on user behavior as much as protocol design.

The same reflexivity can also work in reverse. Stacks’ own Bitcoin staking materials identify a circular relationship between STX value, miner economics, staking capacity and BTC yield. Stronger network activity can support miner incentives and deepen the ecosystem, while weaker STX economics or lower miner bids can pressure yields. The protocol proposes capacity limits, reserve buffers and a staged rollout to manage that risk, but those tools cannot remove market risk entirely.

What an STX price prediction for 2026 must account for

The structural case for STX is clearer than a simple narrative that Bitcoin DeFi growth will automatically lift the token. The proposed staking design creates a specific mechanism that could connect BTC inflows to STX demand, and the six-month bond could temporarily tighten liquid supply. Existing DeFi applications also give additional capital practical uses beyond staking.

The main challenge is that the most important catalyst is still being tested. Stacks announced on July 16 that partners were running the PoX-5 mechanism on a private testnet ahead of mainnet activation. The target BTC yield is also not guaranteed, while participants face STX price exposure and a long bond term. New smart-contract code adds another execution risk that the staged launch is intended to address.

For that reason, a credible STX price prediction 2026 thesis should treat Bitcoin staking as a potential demand engine rather than an established source of sustained buying. The strongest evidence will come after launch: how much BTC enters protocol bonds, how much STX becomes locked, whether users renew their positions, and whether the added capital increases real activity across Stacks.

FAQ

What makes STX different from other yield tokens?

STX is not simply a token issued as a staking reward. It is the native gas asset of Stacks, an asset used in the network’s existing Stacking system, and the proposed capacity asset for Bitcoin staking protocol bonds. The reflexive element comes from the possibility that BTC participation creates STX demand, bonded STX reduces liquid supply and greater ecosystem activity creates additional transaction demand. That loop remains dependent on adoption and network economics.

How does Bitcoin staking create demand for STX?

The proposed protocol requires participants to pair BTC with STX worth approximately 5% of the Bitcoin position. As more BTC enters the system, more STX value would be required under the current design. If a later bonding cycle needs fewer STX tokens because the token has appreciated, participants could redeploy the surplus elsewhere, though the protocol does not require them to do so.

What happens to STX when the Bitcoin DeFi ecosystem grows?

More activity can increase demand for STX as the network’s gas asset and can create more places to deploy STX across lending, trading and liquidity applications. Under the proposed Bitcoin staking model, stronger BTC participation could also increase demand for bonded STX. The effect on price remains dependent on adoption, liquidity, issuance, market conditions and the health of miner economics.

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

Boltz, a non-custodial Bitcoin swap provider, has paused its service “until further notice,” citing what it describes as a sharp rise in automated, AI-assisted probing attempts against its infrastructure. In a statement published on X, the team said multiple exploits over recent months were contained individually, but that the pace of attacker iteration has begun to outstrip the ability of a small security team to find and patch issues quickly.

The pause arrives amid broader concern across crypto that AI capabilities—when paired with automation—can compress the time between vulnerability discovery and real-world exploitation. Boltz also emphasized that the shutdown is an operational decision rather than a response to customer losses, stating that no user funds have been at risk due to the non-custodial nature of its swaps.

Key takeaways

- Boltz is disabling swaps temporarily after reporting an accelerated pattern of “automated AI-assisted probing” in recent months.

- The company says its team cannot patch vulnerabilities quickly enough relative to attacker iteration speed, despite containing prior exploits.

- Boltz states that swaps are cryptographically secured and non-custodial, and that no user funds have been at risk.

- Solana’s security leadership has argued for “autonomous defense” to match threats operating at machine speed.

Boltz pauses swaps as automated probing intensifies

In its X post, Boltz attributed the decision to a “steady increase” in automated AI-assisted attempts to probe its systems over the course of this year. The firm said it has dealt with several exploits during that period; while each incident was contained, the overall pattern—attackers iterating faster than the service’s ability to remediate—has become difficult to manage.

“Over the past months… we have dealt with several exploits. Each was contained, but the pattern is clear: attackers now iterate faster than a team our size can find and patch.”

After reviewing security scans, Boltz said it cannot responsibly re-enable swaps while it is still being actively targeted by multiple groups, and while fixes are in progress. The company also described a recent acceleration, stating that within just a few days it saw a “drastic acceleration” in attacks and does not believe the asymmetry will reverse soon.

For users, the practical implication is straightforward: swap execution is paused, and the company is effectively prioritizing security remediation over service continuity. For builders and investors, Boltz’s decision is another sign that as threats become more automated, smaller teams running open-source infrastructure may face rising operational risk—especially when patch cycles are measured against attacker speed rather than human-led testing schedules.

Non-custodial design remains, but swap operations are suspended

Boltz’s service enables non-custodial, trustless atomic swaps, including transfers between Bitcoin mainnet and Bitcoin-related layers such as Lightning Network and Liquid Network. Because the swaps are non-custodial, Boltz said users retain full control of assets throughout the process.

The company stressed that, despite the security incidents it has described, no user funds have ever been at risk. Boltz’s reasoning is tied to its cryptographic approach: the swap mechanism is built so that custody is not transferred to Boltz in a way that would expose users to direct theft of funds.

Boltz also said its API will remain available to process refunds, and that its support team will continue to be reachable. That matters for downstream users and integrators because it suggests the pause is focused on swap re-enablement rather than an abrupt cessation of all related functionality.

“What we are seeing is a major paradigm shift for Bitcoin services operating on an open source stack, and it needs careful analysis. Do not expect swap services to resume shortly.”

At the time of writing, DefiLlama data showed Boltz’s total value locked at $180,860, providing a snapshot of the service’s on-chain footprint while it remains paused.

Why AI-driven automation raises the patching bar

Boltz’s announcement reflects a recurring theme in crypto security: when attackers can automate discovery and testing, the window for defenders to respond shrinks. The firm’s complaint is not only that vulnerabilities exist, but that the attack pattern is now iterative and fast enough that a small team cannot keep up with the remediation workload—even when individual exploits are contained.

This tension between offense speed and defense capacity is also echoed by Solana Foundation’s security leadership. Earlier coverage of Solana Foundation’s chief information security officer, Michael Coates, pointed to a need to move beyond purely human-scaled security processes. In July, Coates told Cointelegraph that the industry has reached a “tipping point” where humans cannot scale to meet AI-enabled threats.

“The only path forward we have is to have autonomous defense that operates at the speed of machines.”

That framing helps explain why Boltz’s response may be longer-term than a routine patch cycle. If defenders can’t reliably close the loop faster than attackers probe and iterate, even “contained” incidents may signal an ongoing risk environment rather than an isolated problem.

Boltz’s operational decision also mirrors comments from other crypto-adjacent services dealing with frequent exploitation. PayPerQ, an AI prompt-payment platform that accepts payment in Bitcoin and other cryptocurrencies, said it has been fighting off exploits every other week for several months and believes many could be AI-powered. The company described the current situation as “very dangerous,” reinforcing the idea that AI assistance may be becoming a force multiplier for attackers.

What investors and users should watch next

Boltz has not offered a timeline for re-enabling swaps, and its statement explicitly cautions that swap services should not be expected to resume shortly. The key question for users is whether Boltz can reduce the probing-to-patching gap through changes to its security posture—such as tighter monitoring, faster remediation pipelines, and more automated defenses—before attacker iteration once again outpaces its team size.

For the broader Bitcoin ecosystem, Boltz’s pause is a timely reminder that non-custodial design can limit direct user fund exposure, but it does not eliminate operational and reliability risks. Readers should watch for how quickly Boltz can restore swap functionality, and whether the industry’s push toward machine-speed security becomes a practical requirement rather than a theoretical goal.

Strategy has sold 1,638 Bitcoin for $104.7 million after redirecting part of the proceeds toward preferred-stock dividends and share repurchases while increasing its U.S. dollar reserve.

Summary

- Strategy sold 1,638 Bitcoin for $104.7 million to fund STRC dividends and share repurchases.

- The company increased its U.S. dollar reserve to about $4 billion while raising another $290.6 million through MSTR stock sales.

- Strategy’s Bitcoin holdings now stand at 842,138 BTC as it continues prioritizing STRC support over new Bitcoin purchases.

An SEC filing submitted on Monday showed the company sold the Bitcoin between July 27 and Sunday at an average price of $63,957 per coin. Strategy allocated $52.4 million from the sale to dividend payments on its STRC perpetual preferred stock, while another $52.3 million went toward repurchasing STRC shares.

Following the transaction, Strategy’s Bitcoin holdings declined to 842,138 BTC acquired at a combined cost of approximately $63.5 billion.

The filing also disclosed that Strategy raised another $290.6 million by selling MSTR common shares during the same reporting period. Of that amount, $250 million was added to the company’s U.S. dollar reserve, $28.9 million funded additional STRC repurchases, and $11.7 million increased its cash balance.

Executive Chairman Michael Saylor said in a post on X that Strategy repurchased $81.2 million worth of STRC stock during the period and extended the company’s U.S. dollar funding runway by 57 days to roughly 2.3 years.

Bitcoin sale follows Strategy’s revised capital plan

The latest disposal comes after Strategy introduced a new capital framework at the end of June that allows Bitcoin sales to support preferred-stock dividends, debt obligations, approved security repurchases and the company’s dollar reserve.

Earlier SEC filings showed the company also sold 3,588 Bitcoin for approximately $216 million on July 6 and disclosed another sale of 32 Bitcoin in early June, its first reported Bitcoin disposal since a tax-related transaction in 2022.

Recent company updates had already pointed to a change in capital allocation. During its second-quarter earnings call on July 31, Executive Chairman Michael Saylor said Strategy would no longer direct every available dollar toward immediate Bitcoin purchases, choosing instead to maintain both cash and Bitcoin on its balance sheet.

Chief Executive Phong Le also said during the earnings call that Strategy would hold off on additional Bitcoin purchases while STRC continued trading below its $100 stated value.

By July 26, the company had built a $3.75 billion U.S. dollar reserve, which has now increased to about $4 billion after the latest stock sales. Strategy previously said the reserve is intended to cover preferred dividends and debt-related obligations unless the board approves another use.

STRC remains the company’s immediate priority

Supporting STRC has become a central part of Strategy’s financing plan because the preferred security is one of the vehicles it uses to raise capital for Bitcoin purchases.

Yahoo Finance data showed STRC traded at $89.40 during Monday’s pre-market session, leaving it 10.6% below its $100 stated value. MSTR shares were also down 0.9% before the opening bell.

A lower STRC price can make future fundraising through preferred-share sales less effective. The company has previously acknowledged that it wants the security to trade close to its stated value before resuming more aggressive Bitcoin accumulation.

Earlier this month, Strategy confirmed it would keep STRC’s annual dividend rate at 12% for August despite the preferred stock remaining below par. Under a revised policy adopted on June 29, management now considers factors including market price, competing yields, Bitcoin volatility, credit spreads and cash-reserve coverage instead of automatically raising the dividend whenever STRC trades below $100.

The company has increasingly relied on discounted share buybacks rather than repeated dividend increases. Earlier disclosures showed it repurchased roughly $25 million worth of STRC between July 20 and July 26, while nearly $1 billion remained available under its preferred-securities repurchase authorization.

Cash reserve has continued expanding while Bitcoin purchases pause

The latest filing indicates Strategy is still directing fresh capital toward strengthening liquidity even as it trims part of its Bitcoin position.

Most of the $290.6 million raised from MSTR share sales was added to the company’s dollar reserve, bringing the balance to approximately $4 billion as of Sunday. According to Saylor’s update, the additional liquidity extended the reserve’s ability to support dividend and interest obligations by nearly two months.

The approach follows management’s earlier comments that preserving funding flexibility could ultimately support future Bitcoin purchases rather than deploying all available capital immediately.

CryptoQuant founder and CEO Ki Young Ju argued in a June 24 post on X that Strategy should temporarily pause Bitcoin acquisitions, rebuild its cash reserves and adopt a more systematic purchase framework after estimating that the company’s dividend coverage had fallen sharply.

The company’s actions since then have largely centered on rebuilding liquidity, repurchasing discounted STRC shares and maintaining the preferred dividend instead of expanding its Bitcoin holdings.

Analysts and investors remain focused on Strategy’s funding model

Strategy reported an $8.22 billion net loss during the second quarter after recording an $8.32 billion unrealized loss on its Bitcoin holdings under fair-value accounting rules. Even so, management maintained that the accounting loss did not change the company’s long-term Bitcoin strategy.

During the earnings call, executives said restoring STRC closer to its $100 stated value would take priority before new Bitcoin purchases resume.

Benchmark and H.C. Wainwright both maintained buy ratings following the quarterly results, although Benchmark lowered its price target.

The firms said Strategy’s cash reserve, preferred-share repurchases and financing strategy could strengthen its ability to raise capital in the future, while continuing to note that the company’s outlook remains closely linked to Bitcoin prices and investor demand for its preferred securities.

Cointelegraph is committed to providing independent, high-quality journalism across the crypto, blockchain, AI, and fintech industries.

All news, reviews, and analyses are produced with full journalistic independence and integrity. For more details on our standards and processes, please read our Editorial Policy.

Circle Internet Group has received a downgrade from Morgan Stanley, which has lowered its rating to Underweight from Equal Weight and reduced its price target to $38 from $106 after cutting long-term expectations for USDC growth.

Summary

- Morgan Stanley downgraded Circle to Underweight and cut its price target from $106 to $38.

- The brokerage lowered its USDC circulation forecasts for 2027 and 2028, citing slower stablecoin growth and pressure on reserve income.

- Circle shares fell about 6% in premarket trading after the downgrade, while TD Cowen initiated coverage with a Buy rating and an $82 price target.

- Morgan Stanley said real world stablecoin payments remain limited despite rising industry adoption.

- The downgrade comes days after Circle secured a New York trust charter and ahead of its second quarter earnings report.

Morgan Stanley said the downgrade follows lower forecasts for USDC circulation and concerns that Circle’s earnings model could face pressure as reserve income becomes more sensitive to slower stablecoin growth and increasing competition from tokenized cash products.

Circle shares fell about 6% in premarket trading on Monday to $58.81 after the research note was published, even as another Wall Street firm took the opposite view by initiating coverage with a bullish rating.

https://x.com/wallstengine/status/2084212465739653360

Morgan Stanley expects slower USDC expansion

Morgan Stanley reduced its assumptions for USDC circulation by about 33% for 2027 and 44% for 2028, arguing that the stablecoin has not expanded as quickly as previously expected. The brokerage also lowered its GAAP earnings-per-share estimates to around 3% below consensus for 2027 and roughly 20% below consensus for 2028.

According to analyst James Faucette, Circle’s reserve-income business faces increasing pressure because tokenized money market funds and tokenized deposits could compete for the same capital that would otherwise remain in USDC. The report also argued that USYC, Circle’s tokenized money market fund, carries structurally lower economics than its reserve-income business.

Morgan Stanley further said Circle’s OpenUSD initiative introduces shared governance and reserve economics that increase the cost of maintaining USDC distribution, while agentic payment activity remains too small to contribute meaningfully to revenue. The brokerage estimated that agentic payments have fallen to roughly $41,900 in daily volume, implying an average transaction size of about $0.24.

The brokerage also questioned Circle’s long-term growth target, saying USDC has “effectively not grown” since the third quarter of last year despite management’s objective of averaging 40% annual growth across market cycles.

Stablecoin payments remain limited, report says

While payment companies including Mastercard and Stripe have expanded their stablecoin offerings, Morgan Stanley said commercial adoption has yet to produce meaningful transaction volumes outside a handful of use cases.

Drawing on data from McKinsey, the brokerage noted that stablecoins processed roughly $35 trillion in adjusted transaction volume during 2025. Only about $390 billion represented identifiable real-world payments, however, with most activity still tied to crypto trading and transfers rather than commerce.

Morgan Stanley said payment activity continues to be concentrated in cross-border business transactions, remittances and stablecoin-linked card spending. According to the report, those use cases have yet to generate the durable balances and recurring transaction economics needed to offset pressure on Circle’s reserve-income model.

TD Cowen has taken the opposite view on Circle

Offering a contrasting assessment, TD Cowen initiated coverage of Circle with a Buy rating and an $82 price target, arguing that investors may be underestimating the company’s ability to develop into a financial infrastructure platform beyond stablecoin issuance.

Analyst Bryan Bergin said Circle is building products across payments, treasury services, tokenized real-world assets, interoperability and developer infrastructure, which could diversify revenue over time alongside USDC circulation.

TD Cowen also described Circle as a way for investors to gain exposure to institutional adoption of stablecoins and the modernization of financial infrastructure.

Wall Street remains closely divided on the stock. LSEG data shows that 16 of the 30 analysts covering Circle currently rate the shares Hold or Sell, while the remaining 14 recommend Buy or Strong Buy.

Regulatory progress has continued despite investor concerns

The downgrade arrives only days after Circle strengthened its regulatory position in the United States by securing a limited-purpose trust charter from the New York Department of Financial Services for Circle Internet Trust Company LLC, operating as Circle New York Trust.

Circle said the state approval complements the federal trust bank authorization it received from the Office of the Comptroller of the Currency in July. While the OCC-approved Circle National Trust is expected to provide fiduciary digital asset custody services, the company has said USDC issuance will continue through its New York trust entity before gradually transitioning under its approved regulatory structure.

Chief executive Jeremy Allaire previously said obtaining a New York trust charter had been a long-standing objective because of the regulatory clarity provided by the NYDFS framework. Circle has also said the approval builds on its relationship with the regulator, which dates back to 2015 when it became the first company to receive a BitLicense.

The regulatory milestones have not translated into sustained support for the stock. Circle shares ended July 31 down 2.54%, and on the same day Cathie Wood’s ARK Invest purchased 109,129 Circle shares across three exchange-traded funds, increasing its exposure to the stablecoin issuer ahead of the company’s scheduled second-quarter earnings release on Aug. 5.

Investors are also watching the proposed Clarity Act, which is expected to establish a regulatory framework for the U.S. cryptocurrency industry. Morgan Stanley’s latest report indicates that, despite improving regulatory oversight, future performance will still depend on USDC adoption, transaction activity, and Circle’s ability to generate revenue beyond reserve income.

Crypto World

As Wall Street accelerates blockchain adoption, SHR Miner opens access to AI-powered computing, offering daily earnings of up to $1,500

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

SHR Miner explores the rising demand for computing infrastructure as blockchain adoption expands across tokenized assets, stablecoins, and financial services.

Summary

- SHR Miner expands AI-powered cloud infrastructure, offering users automated access to distributed computing resources worldwide.

- It combines AI scheduling and renewable energy to provide global access to digital infrastructure services.

- SHR Miner enables users to access global computing resources without hardware through its AI-driven infrastructure platform.

Blockchain adoption is entering a new stage as major financial institutions move tokenized assets and stablecoin settlement closer to real-world deployment.

The Depository Trust & Clearing Corporation recently completed live production transactions involving tokenized U.S. Treasuries, equities, collateral, securities lending and repo settlement. Around 40 financial and technology organizations participated, including BlackRock, Goldman Sachs, JPMorgan, Circle and Fireblocks.

Visa has also expanded its digital asset strategy with a stablecoin platform designed to help banks and fintech companies issue, transfer and manage stablecoins across blockchain networks.

These developments indicate that blockchain is no longer limited to cryptocurrency trading. It is becoming part of the infrastructure used for payments, asset settlement and global financial operations.

As blockchain and artificial intelligence adoption accelerate simultaneously, demand for data centers, computing power, energy systems and automated digital infrastructure is also increasing.

SHR Miner connects users to the infrastructure economy

The SHR Miner AI-powered digital infrastructure platform allows users to access distributed computing resources without purchasing or maintaining physical mining equipment.

Founded in the United Kingdom in 2018, the platform operates more than 150 data centers and infrastructure nodes across a network serving over five million users in more than 180 countries and regions.

Users can register online, select an infrastructure contract and monitor daily settlement information through a mobile or browser-based dashboard.

No mining hardware, technical configuration or equipment maintenance is required.

- AI-powered scheduling: Computing resources are automatically allocated across global nodes according to performance, energy costs and operating conditions.

- Advanced algorithm capability: SHR Miner uses deep reinforcement learning, temporal convolutional networks and graph neural networks to analyze infrastructure and digital asset data.

- Renewable-energy operations: The platform combines hydroelectric, solar and wind energy with AI-based energy scheduling.

- Automated risk management: Internal systems analyze market and blockchain data, optimize capital allocation and monitor operational risks.

- Multi-asset support: Supported assets include BTC, ETH, DOGE, USDT, USDC, XRP, SOL, LTC and BCH.

- Cloud-based access: Users can view contracts, rewards and resource information entirely online.

Use case: Moving beyond short-term trading

Daniel M., a cryptocurrency user from Canada, previously relied mainly on spot trading and spent several hours each day monitoring Bitcoin and Ethereum price movements.

After joining SHR Miner, he first claimed the platform’s $15 new-user computing-power reward and used the introductory contract to understand the dashboard and daily settlement process.

He later selected the MICROBT WhatsMiner M66 contract:

- Contract amount: $3,000

- Duration: 15 days

- Listed daily reward: $40.80

- Listed contract reward: $612.00

The calculation was straightforward:

$40.80 × 15 days = $612.00

Daniel did not need to purchase a physical mining machine, arrange cooling systems or manage electricity and maintenance costs. The contract information and daily settlement results were displayed directly in the SHR Miner application.

“I wanted a simpler way to participate without constantly watching market charts,” Daniel said. “The platform allowed me to view the contract and daily results directly from my phone.”

Five selected SHR Miner contracts

Users can explore SHR Miner’s available cloud computing contracts and choose an entry level based on their preferred participation scale.

| Contract | Entry Amount | Duration | Daily Reward | Listed Contract Reward |

| MICROBT WhatsMiner M66 | $3,000 | 15 days | $40.50 | $607.50 |

| Bitcoin Miner S21 XP Imm | $5,000 | 25 days | $70.50 | $1,762.5 |

| Bitcoin Miner S21e XP Hyd | $10,000 | 35 days | $151.00 | $5,285 |

The tiered structure allows new users to begin with a lower-cost contract before deciding whether to access additional computing capacity.

For example:

$70.5 per day × 25 days = $1,762.5 with the Bitcoin Miner S21 XP Imm contract.

$151 per day × 35 days = $5282 with the Bitcoin Miner S21e XP Hyd.

Claim a limited-time $15 new-user reward

Eligible new users can currently receive a $15 free computing-power reward after registering with SHR Miner.

The process involves three simple steps:

Register → Claim the $15 reward → Download the application

Users can then view available infrastructure contracts and daily settlement information through the cloud dashboard.

New users can create an SHR Miner account and claim the $15 computing-power reward before exploring the platform’s available infrastructure services.

A new phase of digital infrastructure

As blockchain becomes part of the global financial system and artificial intelligence drives greater demand for computing resources, the infrastructure behind these technologies is becoming increasingly important.

SHR Miner combines global computing nodes, automated resource scheduling, renewable-energy management, and cloud-based access to provide users with a simpler way to participate in the emerging digital infrastructure economy.

No hardware purchase. No equipment maintenance. No specialist technical background.

Discover the future of AI-powered digital infrastructure with SHR Miner.

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

Bold and Beautiful 2-Week Spoilers Aug 3-14: Steffy Unleashes Fury While Bill Presses On!

Dave Ramsey Acquires Financial Audit For $100 Million

Popeyes announces opening date of third Belfast location in heart of the city centre

-

Business5 days ago

Business5 days agoWhy Trees Belong on the Risk Register

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Wit & Wisdom

-

Politics3 days ago

Politics3 days agoMeta enters AI-training agreement with far-right ‘propaganda rag’ Newsmax

-

Entertainment6 days ago

Entertainment6 days ago‘Stargate’ Creator’s New Sci-Fi Series Returns for Season 3 Tomorrow

-

Crypto World2 days ago

Crypto World2 days agoMicroStrategy Post-Earnings CLARITY Act Push Could Add New Catalyst for Its Stock

-

Politics7 days ago

Politics7 days agoThe Part of the Electric Transition Nobody Wants to Discuss

-

Business6 days ago

Business6 days agoMajor shareholder moves on Canyon

-

Crypto World3 days ago

Crypto World3 days agoXRP Ledger v3.3.0 brings five institutional features

-

News Videos5 days ago

News Videos5 days agoBitcoin Enters the 3rd Stage of the Bear Market

-

Crypto World6 days ago

Crypto World6 days agoKraken Enables Retail Access to Jersey Mike’s IPO via Tokenized Shares

-

Politics5 days ago

Politics5 days agoReform UK betrays West Mids residents by running from party pledges

-

Politics4 days ago

Politics4 days agoLuke Littler’s dominance sparks GOAT debate

-

News Videos6 days ago

News Videos6 days agoClaude: Build Financial Dashboards in Minutes (2026)

-

Sports4 days ago

Sports4 days agoSeema Kaliramna Wins Discus Throw Bronze, Takes India’s CWG Medals Tally To 17

-

Business6 days ago

Business6 days agoJohnson & Johnson agrees to $5.5B settlement over talc cancer claims

-

Crypto World2 days ago

Crypto World2 days agoCrypto PAC spending tops $2M in Michigan House race

-

Crypto World3 days ago

Crypto World3 days agoNew York sues Kalshi over prediction market gambling

-

Business4 days ago

Business4 days agoTrump Announces Hamas Disarmament Agreement as Iran Strikes Kuwait Air Base and US Attacks Pause Overnight

-

Tech6 days ago

Tech6 days agoGemini can now summarize the messiest comment threads in Google Docs

-

Tech2 days ago

Tech2 days agoESET tracks rise in malicious AI skills and adaptable malware

You must be logged in to post a comment Login