Crypto World

Evernorth expands into Japan as $1B XRP treasury plan moves forward

Evernorth has launched a Japanese-language presence as the digital asset treasury company expands its work around XRP.

Summary

- Evernorth launched Japanese-language channels while its Nasdaq merger remains subject to regulatory and shareholder approval.

- SBI’s $200 million commitment gives Evernorth a direct link to Japan’s established XRP financial network.

- The Japan account promises market analysis without price forecasts, keeping its launch focused on information.

The firm introduced a dedicated account for local updates and market analysis. In its opening message, Evernorth said, “Japan believed in XRP early on. Together, we will build from here.” The statement describes the company’s position, but it does not confirm a new office, license, product launch or investment in Japan.

The company said the account will explain market movements in simple terms and provide professional information. It also said it “will not discuss prices.” That limit keeps the channel away from direct XRP forecasts. Evernorth has not released details on staffing, partnerships or services tied to the Japanese account.

The launch currently centers on communication and local engagement rather than a disclosed operating unit. The company presents the channel as a regional information service, while its website still lists San Francisco as its primary location in the United States.

SBI links Evernorth to Japan’s XRP market

Japan already holds a central place in Ripple’s business network through SBI Holdings. SBI and Ripple formed SBI Ripple Asia in 2016 to develop payment services across Japan and the broader region.

SBI has also supported XRP-linked products, shareholder benefits and digital asset services through its financial companies. As crypto.news recently reported, Japan has built a broad regulated XRP ecosystem through SBI-led payment, stablecoin and tokenization projects.

SBI also committed $200 million to Evernorth’s planned transaction, according to company filings. Ripple, Pantera Capital, Kraken and Arrington Capital are among the other named backers.

The Japan channel gives Evernorth a direct way to speak with a market where SBI already operates banking, securities and crypto businesses. However, neither company has announced a separate Japanese treasury vehicle or local fundraising plan.

Nasdaq listing remains under review

Evernorth plans to go public through a merger with Armada Acquisition Corp. II. The combined company expects to trade on Nasdaq under the ticker XRPN if the deal closes. Evernorth says the transaction has more than $1 billion in committed capital and aims to build a large public XRP treasury. As crypto.news reported in June, Evernorth filed an amended registration statement with the U.S. Securities and Exchange Commission.

The listing has not received final approval. An SEC filing states that the registration statement is not yet effective. Armada shareholders must also approve the merger, and the parties must meet other closing terms.

The company’s expected Nasdaq debut, treasury size and use of proceeds remain forward-looking plans. Evernorth reported 473 million XRP in earlier filings, but the dollar value changes with XRP’s market price.

Japan expansion follows broader Ripple activity

Evernorth’s Japan launch comes as Ripple and SBI add more regulated digital asset services in the country. In June, Ripple and SBI launched the RLUSD stablecoin in Japan after approval from the Financial Services Agency. SBI VC Trade provides local access under Japan’s payment rules. SBI has also moved to acquire Bitbank, adding another exchange business to its wider crypto operation.

These developments create a familiar market for Evernorth, but the company has not said how its Japanese presence will connect with RLUSD, SBI VC Trade or Bitbank. Its public material focuses on XRP treasury management, lending, liquidity and participation in the XRP Ledger ecosystem. The new account may support education and business outreach, while the planned Nasdaq merger remains the company’s main corporate step.

Crypto World

XRP Price Prediction: Brad Garlinghouse Considered Shutting Down Ripple and Giving XRP to Shareholders

Ripple almost pulled the plug on itself. Brad Garlinghouse said this week that he and co-founder Chris Larsen seriously discussed shutting the company after the SEC sued in 2020. Instead of fighting, Ripple would have handed its XRP holdings to shareholders on a pro rata basis. XRP price now trades around $1.07, down about 2% over the past 24 hours, and the prediction barely blinked.

Speaking at the University of Kansas School of Business, Garlinghouse admitted shutting down felt like the simpler choice. No company would have meant no lawsuit. Yet Ripple decided to stay in the fight because walking away would have cost hundreds of employees their jobs.

"We almost decided to shut down the company when the SEC sued us." —

– Brad Garlinghouse, @Ripple CEO, Kansas University, published Jul 8, 2026. pic.twitter.com/kvbe2gnkmU

Eri ~ Carpe Diem (@sentosumosaba) July 11, 2026

Eri ~ Carpe Diem (@sentosumosaba) July 11, 2026

That decision was anything but cheap. Ripple spent about $150 million on legal fees during the four-year battle. Garlinghouse said they kept going because the company had people depending on it, not because they knew the court would side with them. That’s a lot of money to spend on a “maybe.”

The case finally turned in Ripple’s favor when Judge Analisa Torres ruled that XRP itself is not a security. The court also found that some institutional sales broke securities laws, leaving both sides to settle the remaining issues later. With the legal fight behind it, Garlinghouse’s latest comments show Ripple came much closer to disappearing than most people ever knew.

Discover: The Best Crypto to Diversify Your Portfolio

XRP Price Prediction: Break Above $1.17 or Is Consolidation the Base Case?

XRP is stuck in a narrow range, and neither buyers nor sellers have taken control. It is trading around $1.10 after moving between $1.07 and $1.11 over the past day. During the past week, the token has swung between $1.07 and $1.17, showing traders are still waiting for a reason to pick a side.

For now, support sits near $1.07, where buyers have stepped in several times. On the upside, $1.12 to $1.17 remains the ceiling. XRP has knocked on that door more than once, but the answer has been the same. Not today.

A break above $1.17 with stronger volume could shift momentum toward $1.25. Until then, the path of least resistance looks sideways. As long as $1.07 holds, the chart still gives bulls something to work with, even if it feels like watching paint dry.

If XRP loses $1.07 on a daily close, attention could quickly turn to the psychological $1.00 level. That would erase the recent range and put buyers back on defense.

Meanwhile, Ripple’s legal victory and Garlinghouse’s latest comments have done little to move the needle. It seems the market has already filed that story away and is waiting for the next headline.

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

Bitcoin Hyper Targets Early-Stage Positioning as XRP Trades Sideways at $68B Market Cap

XRP’s consolidation at a $68–69 billion market cap is a structural ceiling problem, not a catalyst problem. Meaningful percentage moves from here require either a sector-wide re-rating or Ripple-specific news of substantial scale. That’s the math at large-cap valuations. Traders looking for asymmetric upside are increasingly scanning earlier in the risk curve, which is where Bitcoin Hyper is drawing attention.

Bitcoin Hyper ($HYPER) is positioning as the first Bitcoin Layer 2 with Solana Virtual Machine (SVM) integration, a combination that targets Bitcoin’s three core limitations simultaneously: slow transactions, high fees, and the near-total absence of programmability.

The architecture delivers sub-second finality on top of Bitcoin’s security layer, with a decentralized canonical bridge handling BTC transfers. Presale price sits at exactly $0.013683, with $33 million raised to date. Staking is live with high APY for early participants.

For traders who followed XRP’s legal arc from 2020 through settlement, the comparison to early-stage asymmetric bets isn’t lost.

Research Bitcoin Hyper at the official presale before the current price tier closes.

Discover: The Best Token Presales

The post XRP Price Prediction: Brad Garlinghouse Considered Shutting Down Ripple and Giving XRP to Shareholders appeared first on Cryptonews.

Metaplanet has officially launched Metaplanet Securities, turning its completed acquisition of Siiibo Securities into a regulated digital asset investment banking business built around Bitcoin-backed financial products.

Summary

- Metaplanet has launched Metaplanet Securities after completing its acquisition of Siiibo Securities.

- The new regulated business will develop Bitcoin backed bonds and digital credit products under Project Nova.

- JPYC and Progmat are working with Metaplanet on a Bitcoin backed digital credit ecosystem for Japanese investors.

According to Metaplanet, the new subsidiary succeeds the Tokyo-based brokerage acquired for JPY 2.1 billion, completing a transaction first announced in June.

The company said the business will operate under a Type I Financial Instruments Business Operator licence regulated by Japan’s Financial Services Agency, giving it the legal framework to structure and distribute securities products linked to digital assets.

Rather than limiting its strategy to holding Bitcoin on its balance sheet, Metaplanet said the securities business will focus on financial engineering and regulated investment products designed for Japan’s capital markets. The company described the launch as the next step in Project Nova, its long-term plan to build Bitcoin-focused financial services.

Project Nova moves toward product development

Metaplanet Securities has also introduced Project Nova as its first major initiative under the new structure. The company said it intends to develop a digital credit ecosystem with yen stablecoin issuer JPYC and tokenization platform Progmat by using its Bitcoin treasury as credit-enhancement collateral for digital corporate bonds and structured credit products.

The proposed framework would combine Progmat’s security token infrastructure with JPYC’s stablecoins to support continuous trading, near-instant settlement and automated daily interest calculations. According to Metaplanet, the products are intended for both institutional and retail investors seeking regulated, yen-denominated exposure to Bitcoin-backed yields.

Earlier this month, Metaplanet, JPYC, Progmat and Metaplanet Securities launched a joint study to examine whether Bitcoin could serve as collateral or a credit-enhancement asset for blockchain-based credit instruments. The participants said at the time that they would evaluate product design, settlement, regulation, investor protection, and technical requirements before making any decision on issuance.

The companies also stated that no launch date, yield structure, product terms or distribution plans had been approved, and any future offering would require internal approvals together with discussions with regulators.

From Bitcoin treasury to financial products

Project Nova builds on Metaplanet’s effort to generate income from its growing Bitcoin reserves instead of treating the asset solely as a treasury holding. The company previously said the strategy views Bitcoin as productive collateral that can support financial products within Japan’s regulated securities framework.

The acquisition of Siiibo Securities, announced in June and completed on July 13, gave Metaplanet control of an established online corporate bond platform together with an existing investor network. Company information released during the acquisition process said Siiibo had supported more than 40 companies and over 100 bond issuances, primarily through private placement corporate bonds and venture debt financing.

Meanwhile, Metaplanet has continued expanding its Bitcoin treasury while building the new business. The company disclosed on July 10 that it held 43,000 BTC after purchasing 2,823 BTC during the second quarter. It has also said it plans to increase its holdings to 210,000 BTC by the end of 2027 while developing financial products backed by those reserves.

Key takeaways

- Pi Network (PI) fell another 6% on Monday after dropping 7% the previous day, extending its prolonged downtrend.

- Retail participation continues to weaken, with Open Interest falling below $9 million, signaling declining leveraged trading activity.

- Analysts warn that ongoing token unlocks could continue to pressure prices if supply outpaces demand.

Pi Network (PI) remained under heavy selling pressure on Monday, falling around 6% after suffering a 7% decline in the previous trading session.

The continued weakness reflects fading retail participation, declining leveraged positions, and concerns that ongoing token unlocks could keep supply ahead of demand.

Technical indicators also suggest the correction may not be over, with the token approaching a key support level near $0.075.

Retail demand continues to fade

Recent derivatives data points to weakening interest among traders. According to CoinAnk, Pi Network’s Open Interest (OI) declined to $8.48 million on Monday from $8.91 million a day earlier.

The drop in Open Interest indicates that traders are closing leveraged positions rather than opening new ones, reflecting reduced confidence and lower speculative activity around the token.

Pi Network price analysis: Bears target the $0.075 support

Technically, Pi Network has remained in a persistent downtrend since late April, forming a falling channel pattern on the daily chart.

The latest decline has pushed the token closer to the channel’s lower support trendline around $0.075.

If sellers successfully break below this level, the next significant support is located near $0.0679, which corresponds to the 1.618 Fibonacci extension measured from the previous decline between $0.1998 and $0.1183.

Technical momentum continues to favor the bears. The Relative Strength Index (RSI) has fallen to approximately 10, placing the asset deep in oversold territory and highlighting the intensity of the recent selling pressure.

Meanwhile, the Moving Average Convergence Divergence (MACD) remains below the zero line, with both the MACD and signal lines trending lower while negative histogram bars continue expanding.

Together, these indicators suggest bearish momentum remains firmly in control despite increasingly oversold conditions.

The immediate focus remains on the $0.075 support level. A decisive breakdown below this area could accelerate losses toward $0.0679, reinforcing the prevailing downtrend.

On the upside, if buyers manage to defend support and trigger a rebound, PI could first target the 1.272 Fibonacci extension at $0.0961, followed by the important $0.1000 psychological resistance.

Until stronger buying activity returns, however, Pi Network’s technical outlook continues to favor additional downside as weak retail demand and expanding token supply weigh on market sentiment.

Japanese payments adoption is moving from small pilots toward more practical, merchant-ready stablecoin use. Lawson, one of Japan’s best-known convenience-store chains, will trial yen-denominated stablecoin payments inside a real store checkout flow this August, while Netstars has launched a service that lets merchants accept multiple stablecoins as payment options.

Together, the two developments highlight how Japan’s regulated stablecoin environment is increasingly focused on integration details—how payments happen at the register, how merchants settle in yen, and what wallet or infrastructure customers need.

Key takeaways

- Lawson will run an August trial of yen-denominated stablecoin payments at a Tokyo location, using HashPort’s non-custodial wallet and Lawson’s existing point-of-sale system.

- The Lawson pilot is designed to test whether stablecoins can fit smoothly into standard convenience-store checkout operations without merchants managing crypto wallets.

- Netstars launched “Stablecoin Pay” for merchants, initially supporting USDC, USDT, and JPYC via the Solana and Polygon networks.

- Netstars says its setup helps merchants price and settle in yen while customers pay with dollar-denominated stablecoins, aiming to reduce crypto and exchange-rate handling for merchants.

Lawson and HashPort test stablecoin checkout in a real store

On Monday, blockchain company HashPort said it has signed an agreement with Lawson and telecom group KDDI to conduct a trial at the Lawson Takanawa Gateway City store in Tokyo. According to HashPort’s announcement on PRTimes, participants will use HashPort’s non-custodial wallet, while the store will process payments through HashPort’s point-of-sale integration—without the store needing to open or manage crypto wallets.

The stated goal is practical: determine how stablecoin payments can be integrated into Japan’s everyday retail infrastructure, specifically within the checkout flow of a convenience store. That matters because “accepting crypto” can look very different at the register compared with an online checkout, especially when merchants want predictable operations and minimal changes to store systems.

Before expanding beyond the pilot, the companies plan to evaluate integration requirements, checkout operations, payment processing times, and whether the wallet experience is usable for customers. The emphasis on operational metrics suggests the trial is as much about systems fit as it is about payment settlement.

Netstars rolls out a merchant service for multi-stablecoin payments

In a separate move, Netstars launched a merchant-facing product called Stablecoin Pay. The company’s announcement, also published on PRTimes, opens applications for merchants that want to offer multiple stablecoins as payment options.

Stablecoin Pay initially supports three stablecoins: USDC, USDT, and JPYC (a yen-denominated stablecoin). Netstars says these can be used through the Solana and Polygon networks, with MetaMask as the supported wallet. The company set its merchant payment fee at 0.98% and said it plans to add more wallet and blockchain support over time.

Netstars also described how the service is intended to work from a merchant operations perspective. It says that merchants can use existing payment terminals in most cases and manage product pricing, sales records, and settlement in yen even when customers pay with dollar-denominated stablecoins. In its framing, that reduces the need for merchants to hold crypto or handle exchange-rate complexity.

Netstars’ timeline also matters for context. The company’s commercial launch follows earlier trials it ran using USDC payments—first at Tokyo’s Haneda Airport from January to February, and later at a trading-card store in Himeji starting in April, according to Netstars’ trial references. The new merchant service marks a step from location-based tests toward a broader offer aimed at business operators.

Japan’s stablecoin rules are shaping real-world product design

Both projects land in the context of Japan’s evolving stablecoin regulatory landscape. Japan introduced a dedicated stablecoin framework on June 1, 2023, when amendments to the Payment Services Act and related laws took effect. The framework created regulatory categories for fiat-linked stablecoins and requires intermediaries operating in certain capacities to register with Japan’s Financial Services Agency.

Subsequent regulatory milestones have helped specific stablecoin products become usable in Japan. Coverage noted that USDC received regulatory approval for distribution in March 2025. JPYC later registered as a fund transfer service provider that August—before the stablecoin launched in October, based on prior reporting.

For merchants and payment providers, the practical takeaway is that regulatory compliance increasingly informs product architecture. Netstars’ approach—settling in yen while accepting multiple stablecoins—reflects a design choice that keeps everyday commerce consistent for retailers. HashPort and Lawson’s trial similarly focuses on minimizing merchant operational burden by routing payment processing through an integrated point-of-sale flow and using a non-custodial customer wallet.

What to watch next for stablecoin payments in Japan

As these trials and merchant products progress, the key uncertainties are less about whether stablecoins can be transferred and more about whether the entire user-and-merchant workflow feels seamless. For Lawson’s pilot, readers should watch reported integration and checkout performance metrics—especially usability and processing time. For Netstars’ Stablecoin Pay, monitoring merchant onboarding, additional supported wallets and blockchains, and continued evidence of smooth yen settlement will indicate whether multi-stablecoin payments can scale beyond early pilots.

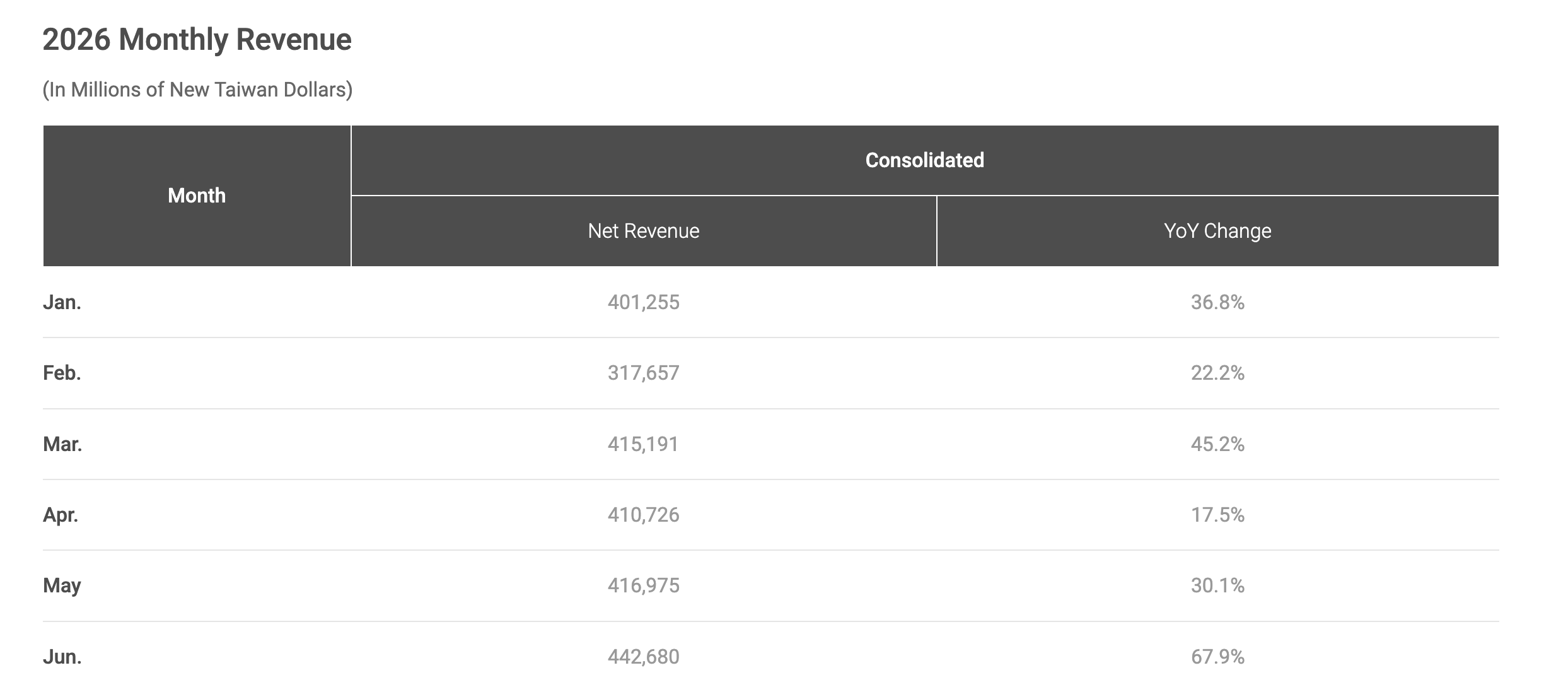

Taiwan Semiconductor Manufacturing (TSMC), the world’s largest contract chipmaker, reported June revenue of T$442.68 billion ($13.78 billion).

This marked a 67.9% year-on-year jump, the fastest monthly growth of 2026, driven by artificial intelligence (AI) chip demand.

AI Demand Powers Record Revenue For The Chipmaker Giant

June sales rose 6.2% from May and pushed second-quarter revenue to T$1.27 trillion, or $39.62 billion. That total topped the T$1.264 trillion estimate compiled by LSEG from 20 analysts. Dollar figures reflect an exchange rate of 32.13 New Taiwan dollars to the US dollar.

Follow us on X to get the latest news as it happens

The monthly figures show clear acceleration. June’s 67.9% growth far outpaced February’s 22.2% and April’s 17.5%, signaling that customers are pulling orders forward amid intensifying AI infrastructure spending.

First-half revenue reached T$2.4 trillion, about $74.99 billion, up 35.6% year-on-year. Notably, in six months, TSMC has already earned about 63% of its entire 2025 revenue of T$3.81 trillion.

TSMC held roughly 73% of the global pure-foundry market in the first quarter, according to Counterpoint Research.

The monthly figures did not include profit or margin details. The chipmaker will disclose full second-quarter earnings on Thursday, July 16. Analysts expect a 58.8% rise in second-quarter net profit, per LSEG.

The revenue is now locked and public, so Thursday’s call cannot surprise on the top line. The only market-moving variable left is the outlook.

Investors will watch whether management raises the full-year guide above its current 30% growth floor and whether it lifts capex again. That decision is the AI capital-spending ceiling question in another form heading into July 16.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Chipmaker Giant’s June Revenue Jumps 68% in Strongest Month of 2026 appeared first on BeInCrypto.

Crypto World

AI chips and bitcoin show how powerful structural trends can still produce severe corrections

The term “paradigm shift” is often applied casually to what may simply be rapid rotations between fashionable assets, the latest example being the AI-driven semiconductor boom.

Hyperscalers such as Amazon (AMZ) and Google (GOOG) are spending heavily on data centres containing thousands of AI accelerators. These systems require enormous quantities of high-bandwidth memory for processing and NAND flash for storage, tightening supply and lifting chip prices.

Micron Technology (MU) produces DRAM, NAND and other memory products, while Sandisk (SNDK) specialises in NAND flash and solid-state storage. Micron rose roughly 700% year over year, and Sandisk gained more than 4,000%. Both have subsequently retreated from their peaks, illustrating how quickly enthusiasm can reverse.

The excitement created the largest U.S. IPO of all-time in SpaceX (SPCX), while SK Hynix (00060), a leading supplier of high-bandwidth memory, raised $26.5 billion through the largest-ever U.S. listing by a foreign company. Its ADRs initially surged, but subsequent volatility exposed the risks of buying into peak optimism with SK Hynix down 15% during Asia market hours.

Speaking at the University of Kansas School of Business this week, Ripple chief executive Brad Garlinghouse told a story the company kept to itself for more than five years.

Summary

- Ripple seriously considered shutting down after the SEC lawsuit and distributing its XRP holdings to shareholders.

- The abandoned plan clarifies the separation between Ripple the company and XRP the token.

- Ripple’s decision to fight cost roughly 150 million dollars in legal fees but produced a precedent the broader industry now uses.

- The counterfactual giveaway would have removed Ripple’s XRP overhang but also stripped the token of Ripple’s institutional growth story.

- The confession reframes XRP’s current thesis as an entanglement between company success, token supply, legal precedent, and ledger adoption.

In December 2020, days after the Securities and Exchange Commission sued Ripple and named Garlinghouse and co-founder Chris Larsen personally, the two men seriously weighed a plan to end the fight before it began: wind the company down, distribute Ripple’s enormous XRP holdings to shareholders on a pro rata basis, and inform the regulator that the entity it was suing no longer existed and no longer held the asset in question. In Garlinghouse’s words, the government had infinite power and resources, and shutting down was the easier path. What tipped the decision the other way was not confidence in winning. It was that dissolution would have put hundreds of employees out of work.

The disclosure landed with corroboration and a correction. David Schwartz, Ripple’s longtime chief technology officer, said outside lawyers advised leadership in that period that the company was done, unsavable, and that the executives should cut a deal to save themselves, and he argued the SEC named Garlinghouse and Larsen personally as a calculated pressure tactic, since suing two men concentrates the incentive to fold in a way that suing a corporation does not. When outlets amplified the story into capitulation headlines, Schwartz pushed back, saying his earlier comments were being stretched and that he never claimed the shutdown was on the verge of happening. Garlinghouse, for his part, attached a number to the road actually taken: roughly 150 million dollars in legal fees over four years, disclosed publicly for the first time.

A confession this old is not news about the past. It is a lens on the present, because the plan Ripple shelved in December 2020 is a nearly perfect thought experiment about what XRP is. Every question that hangs over the token in 2026, whether it is a claim on Ripple’s success, what the company’s supply overhang means, and why the price ignores the company’s triumphs, gets sharper when run through the world where the giveaway happened. This feature takes the confession seriously as history, then uses it as the analytical instrument it accidentally is.

December 2020: the decision as it actually looked

The context deserves reconstruction, because hindsight has sanded off how bleak it was. Three days before Christmas 2020, the SEC filed suit alleging Ripple had conducted a seven-year unregistered securities offering by selling XRP, raising more than 1.3 billion dollars, and it charged Garlinghouse and Larsen individually for their own sales. The complaint did not merely threaten a fine. It asserted that the company’s core asset, held by the billions on its balance sheet, was itself the violation. Exchanges reacted immediately: major US venues delisted or suspended XRP within weeks, liquidity fled, and the token, then comfortably in the market’s top five, lost most of its value while the rest of crypto rallied into the 2021 bull market.

Garlinghouse also supplied a detail that explains the depth of the grievance. He met SEC officials four times between 2017 and 2019, without a lawyer, and was never told the agency might treat XRP as a security. Whatever one makes of the legal merits, the company’s leadership experienced the suit as a rule invented retroactively, which shaped its willingness to litigate a case its own counsel called unwinnable.

Against that backdrop, the dissolution plan was not madness. It was the advice. Distribute the XRP, dissolve the entity, moot the case. The government cannot enjoin a company that does not exist, and the personal claims against two wealthy defendants would have become vastly easier to settle without an operating business generating fresh alleged violations every quarter. The plan failed the only test the founders applied to it, the employees, and Ripple chose instead to spend 150 million dollars proving the agency wrong.

The outcome vindicated the choice, though less cleanly than the folklore suggests. In July 2023, Judge Analisa Torres ruled that XRP is not in itself a security and that Ripple’s programmatic sales on public exchanges were not securities transactions, the industry’s most important judicial win of the enforcement era. But she also found that direct institutional sales violated securities law, and the final judgment carried a 125 million dollar civil penalty plus a permanent injunction against repeating unregistered institutional sales. A 2025 attempt by both sides to soften the outcome, cutting the penalty to 50 million and dissolving the injunction, was rejected by Torres because final judgment had already been entered, and the appeals were dropped, with the Second Circuit closing the case on August 22, 2025. Ripple won the war and still pays the reparations, a nuance the company’s celebratory framing tends to omit, as crypto.news noted in its review of how the case actually ended.

The alternate history: what the giveaway world would have looked like

Now run the counterfactual, because it is unusually clean. Suppose the founders had taken the lawyers’ advice in December 2020.

XRP does not die in that world. The XRP Ledger was already decentralized in the sense that mattered operationally: independent validators, open-source software, no ability for Ripple to halt or reverse it. The token would have kept trading, and the SEC’s case would have collapsed into personal claims against two defendants with every incentive to settle quickly. Ironically, the giveaway might have produced the regulatory clarity holders craved years earlier, because a token with no sponsoring company selling it is a far weaker securities case, the exact logic that later animated the Torres distinction between institutional sales and blind exchange transactions.

What XRP loses in that world is everything the 2026 bull case is made of. No Ripple means no On-Demand Liquidity corridors, no RLUSD stablecoin, no 1.25 billion dollar Hidden Road acquisition placing Ripple Prime inside the DTCC ecosystem, no 75-license regulatory portfolio, no MiCA authorization opening 30 European countries, a build-out crypto.news chronicled as it completed this month. It also means no concentrated lobbying force: Ripple’s 25 million dollar contribution to the industry’s political machine helped produce the legislative environment the CLARITY Act now moves through. The token would have become something like a payments-flavored Litecoin, a functioning ledger with a distributed supply, a passionate community, and no institutional narrative whatsoever.

And here is the uncomfortable part of the exercise: it is not obvious the price would be lower. The giveaway would have distributed roughly half the total supply, the escrowed billions, to shareholders in a single event, ugly in the short run but terminal for the overhang that has shadowed the market ever since. No monthly escrow releases. No company treasury whose sales the market prices in perpetually. No ambiguity about whether buying the token is buying exposure to the company. The 2026 market puts XRP near 1.09 dollars while Ripple has its most productive year in history, and the leading explanation for that disconnect is precisely that the token is not a claim on the company that owns it. The counterfactual world would have made that separation formal in 2020 and repriced it once, instead of rediscovering it every cycle.

The pressure mechanics: why naming two men nearly worked

Schwartz’s claim about the SEC’s strategy deserves unpacking, because it explains why the shutdown option got as far as a serious boardroom conversation.

Enforcement actions against corporations are wars of attrition that companies can rationally fight; legal fees are an operating expense, and the entity’s decision-makers are spending shareholder money on shareholder problems. Naming executives personally changes the arithmetic entirely. Garlinghouse and Larsen faced individual claims over their own XRP sales, meaning their personal fortunes, their futures in regulated finance, and their exposure to individual judgments were on the table alongside the company’s. The standard playbook response, the one the lawyers recommended, is for the individuals to settle personally and let the company negotiate from weakness. Schwartz’s reading is that the agency structured the complaint to trigger exactly that sequence: pressure the men, collapse the defense, collect the precedent.

The dissolution plan was, in a strange way, the most aggressive possible counter to that playbook. Rather than settling to protect themselves, the founders considered removing the corporate target entirely while keeping their personal defenses intact, a move that would have converted the SEC’s leverage into a stranded lawsuit against two individuals over a token no company sponsored. That they got as far as pricing the option before rejecting it on employment grounds says something rarely visible from outside: the decision to fight was not a legal calculation, and it was made against legal advice. Companies write press releases about conviction. The confession describes something closer to a coin flip weighted by payroll, which is both less heroic and considerably more believable.

The four-year fight that followed set the template the rest of the industry ran. Coinbase’s litigation posture against the same agency, down to the discovery offensives and the public refusal to settle, was Ripple’s playbook executed with a bigger balance sheet, and the enforcement retreat of 2025 that freed both companies traces directly to the precedent risk Ripple’s partial win created. The 150 million dollars bought more than one company’s survival. It bought the industry’s proof of concept that the agency could lose.

The Japan control group: the one place the counterfactual ran forward

There is a live experiment that approximates the world where XRP thrives on utility with minimal dependence on American legal outcomes, and it has been running for years in Japan.

Through the SBI partnership, Japan built what no other market has: production remittance corridors settling in XRP, bank-facing infrastructure, retail brokerage distribution, and now the first trust-type yen stablecoin alongside a formal RLUSD launch, an integration deep enough that crypto.news called Japan the only country actually using XRP. Japanese demand persisted through the SEC years precisely because it never depended on the SEC; the token’s status there was settled by local regulation long before Torres ruled. Korea shows a paler version of the same pattern, with XRP consistently ranking as the second most traded asset on Upbit.

The Japan case matters to the counterfactual because it shows what the giveaway world’s ceiling might have looked like: a token that works, in specific corridors, where local institutions committed, with a price driven by usage and regional retail rather than by a global institutional narrative. That ceiling is real and unimpressive relative to the 2026 thesis. XRP’s claim on a repricing runs through ETFs, CFTC classification, DTCC-adjacent infrastructure, and European licensing, all of which required a living, litigating, license-collecting Ripple. The confession, in other words, describes the fork between a token that would have merely survived and a token that might matter. The market’s frustration is that five years after the fork, the price cannot yet tell the difference.

What the confession explains about the token today

Read as an analytical instrument, the shelved plan clarifies four things that XRP holders argue about constantly.

First, it is the cleanest statement ever made of the company-token separation. The founders’ plan treated Ripple’s XRP as a distributable asset, like cash on a balance sheet, not as equity in the enterprise. That is the correct frame, and it cuts both ways. Holders do not own Ripple’s payments revenue, its licenses, or its prime brokerage; they own units of the asset Ripple also happens to hold in size. Every cycle, the market relearns this by watching company milestones fail to move the price. The confession shows the founders understood the separation so completely that they were prepared to monetize it as an exit.

Second, it reframes the supply overhang as a choice that keeps being made. Ripple could have distributed its holdings in 2020. It can, in principle, distribute or burn them today. Instead it maintains the escrow system, releasing up to a billion tokens monthly and relocking most, preserving the treasury as the company’s war chest. The comparison to Strategy’s Bitcoin position, which Garlinghouse himself invited when he attacked Michael Saylor’s model, runs deeper than either CEO admits, a parallel crypto.news explored: both firms sit atop token treasuries whose value depends on markets they simultaneously supply. The difference is that Ripple’s treasury predates its products, which means the company’s incentives and its holders’ interests align only where ledger usage is concerned, and the confession is a reminder that leadership has always known where the exit is.

Third, it explains the community’s political intensity. The XRP holder base is famous for treating regulatory fights as existential, and the confession validates the instinct: the fight was existential, the company nearly chose not to have it, and the entire institutional arc since, the ETFs with their 1.49 billion dollars in inflows, the bank pilots, the ledger’s climb toward institutional credit through the lending amendment now gathering validator support that crypto.news is tracking, exists because two founders decided a payroll mattered more than legal advice. Communities remember near-death experiences. This one now has the CEO’s own account of how near it was.

Fourth, it quietly indicts the enforcement-first era better than any lobbying campaign. A regulator’s lawsuit, built on a theory a judge later rejected at its core, came within one boardroom conversation of dissolving an American company, erasing hundreds of jobs, and, by the mechanics described above, possibly leaving the token itself legally cleaner than litigation ever made it. Whatever the CLARITY Act’s fate in the coming three weeks, Garlinghouse’s story is the case study its advocates will cite for a decade: rules invented by enforcement nearly produced an outcome no rule intended.

Why tell the story now: the timing of a five-year-old secret

Executives do not disclose near-death experiences by accident, and the timing of this one rewards a cynical read alongside the charitable one.

The charitable read is simple: the war is over, the appeals closed in August 2025, and a business school audience is exactly where a founder processes the hardest decision of his career into a leadership lesson. Nothing about the venue or the content suggests coordination, and the Schwartz back-and-forth, with the former CTO correcting the most breathless headlines within a day, has the messy texture of an unplanned story escaping its container.

The cynical read notices what the story does for Ripple’s current agenda. The company is spending this exact month arguing, through its lobbying network and the broader industry coalition, that the CLARITY Act must pass before the August recess because enforcement-era ambiguity nearly destroyed legitimate American companies. A first-person account from a sitting CEO, with a dollar figure attached, of how close ambiguity came to dissolving a firm the courts later largely vindicated is the single most persuasive artifact that argument could ask for, and it surfaced three weeks before the decisive Senate window. Whether or not the timing was designed, the story will be used, and Garlinghouse, among the most message-disciplined executives in crypto, understands precisely what he put into circulation and when.

The 150 million dollar figure itself does double duty. As a grievance, it quantifies the cost of regulation by lawsuit. As a signal, it prices the moat: that is what it cost to buy the Torres precedent, the four-year head start on institutional relationships, and the standing to pursue a bank charter while competitors were still negotiating consent orders. Ripple can afford to publicize the number because the number is, in the company’s framing, an investment that paid. The firms that settled early saved the fees and inherited none of the case law. Litigation as capital expenditure is a strange category, and Ripple’s disclosure this week is the closest thing to an audited return the industry has seen.

There is also an audience inside the company’s own cap table. Ripple has intermittently explored a public listing, and a founder narrating the darkest moment as a story of conviction, payroll loyalty, and vindication is writing the first chapter of an eventual prospectus narrative, one where the 2.3 billion dollar question of what the company is worth gets answered by public markets that will, inevitably, price the XRP treasury and the operating business as separable things. The confession pre-frames that separation on management’s terms: the treasury as an asset the founders could have distributed and chose to steward instead. Whenever the listing conversation becomes real, this week’s story is the one bankers will quote.

The symbolism budget: from near-dissolution to a Jayhawks jersey

The venue of the confession supplied its own punchline. Days before Garlinghouse spoke at Kansas, his alma mater’s athletic program unveiled a five-year sponsorship making XRP the first cryptocurrency ever stitched onto the jerseys of a major college team. The company that considered making its token an orphan in 2020 now pays to embroider it on the Jayhawks.

The jersey is trivial; the trajectory is not. Ripple in 2026 is chasing a national bank charter and direct access to Federal Reserve payment rails, running regulated payments across Europe, and operating inside the clearing infrastructure of American equities. It is, deliberately and expensively, becoming part of the financial system that tried to end it. That is the strategic meaning of the 150 million dollar figure Garlinghouse disclosed: the fee was not just for survival, it purchased the standing to build all of this under a favorable precedent. Companies that settle do not get to write the case law their industry relies on. Torres’ programmatic-sales ruling is cited in every token classification argument in America, and it exists because Ripple paid to litigate a question everyone else settled around.

How the market metabolized the confession

The price action around the disclosure was its own small case study in what moves this token and what does not.

XRP traded near 1.09 dollars through the news cycle, down about 1.4 percent on the day, statistically indistinguishable from the broader tape. A story that would have cratered the market in 2021, the CEO admitting the company nearly dissolved, produced no measurable panic, and the pockets of social media alarm that did flare were extinguished within hours by Schwartz’s clarification. On-chain, the week showed the opposite of fear: Binance spot flows on July 7 ran 64.9 million XRP in against 49.2 million out, a net buying imbalance of roughly 15.7 million tokens, and a bullish divergence formed above the 1 dollar level even as the headlines circulated. The holder base heard the founders once considered abandoning the token, and bought.

Two explanations fit, and both are probably operating. The first is maturity: after a settled lawsuit, launched ETFs, and a completed appeals process, the 2020 decision is archaeology, priced at zero because it resolved years ago. The second is more interesting and connects to everything above: the market may have understood, faster than commentators did, that the confession was bullish framing. A treasury the founders considered distributing and instead spent five years and 150 million dollars defending is a treasury management believes in. The asset the company almost orphaned is the asset it now stitches onto jerseys, builds credit markets around, and carries toward a bank charter. Revealed preference, over five years and against legal advice, is a stronger signal than any roadmap, and revealed preference is exactly what the story documents.

The remaining question is the one the counterfactual sharpens rather than answers: having kept the treasury, the company, and the token bound together, Ripple owns the burden of making the binding pay. Ledger usage, RLUSD settlement flows, corridor volume, and the classification the CLARITY Act would confer are the mechanisms that would finally route company success into token demand. The confession proves nothing about whether they will. It does settle the older argument about intent. The founders looked at a world where XRP floated free of Ripple, priced it against a payroll, and chose the harder, entangled path. Five years and 150 million dollars later, the entanglement is the investment thesis, the escrow is the overhang, the precedent is the moat, and the token that was almost given away trades at a dollar while the company that almost gave it away has never been stronger. Alternate histories do not pay dividends, but this one earns its keep: it is the rare counterfactual that explains the actual world better than the actual world explains itself.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

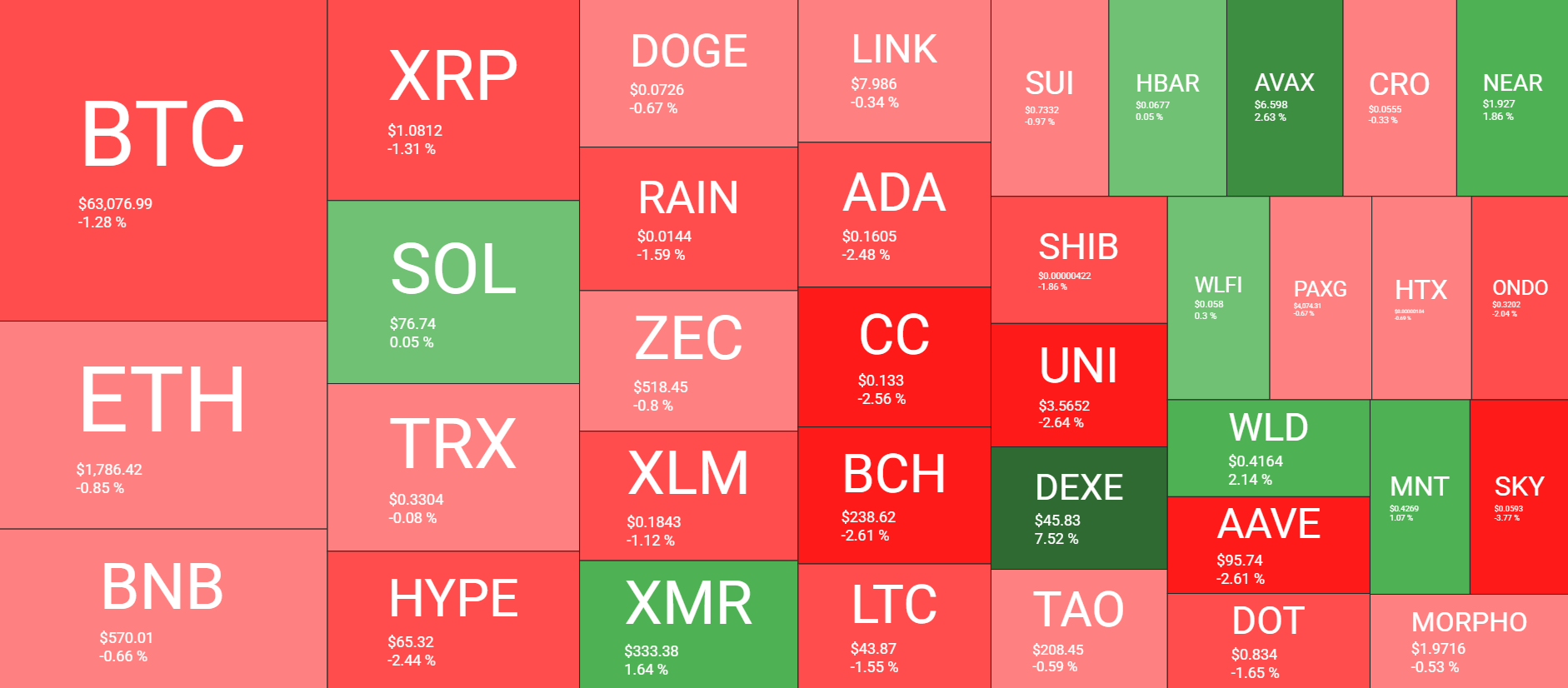

After a relatively quiet weekend, bitcoin’s price dipped by nearly two grand on Monday morning as the market priced in the new attacks in the Middle East.

Most larger-cap alts have followed suit with similar daily losses, with XRP dropping below the crucial $1.10 support, and ETH failing at $1,800.

BTC Slipped Below $63K

Bitcoin reacted well to the July 1 dip below $58,000 and quickly reclaimed the $60,000 line. It kept climbing in the following days and jumped to $64,000 on July 6. However, Strategy’s latest and biggest sale resulted in a major leg down, as BTC slumped to $61,200 in hours.

Unlike the previous such occasion, though, the cryptocurrency rebounded swiftly after the initial FUD and jumped to $64,400 on Tuesday. Another rejection followed after the US and Iran broke their ceasefire and launched new rockets against each other.

This time, BTC was able to halt the free-fall at $61,600 and went on a minor rally at the end of the week. The culmination came on Saturday morning with a surge to $64,600, which became a new multi-week peak. BTC stood at around $64,000 for most of the weekend, but dipped earlier today to $62,400 as the consequences of the latest set of attacks between the US and Iran were felt across all markets.

It has rebounded to just over $63,000 as of now, but its market cap has dropped to $1.265 trillion on CG. Its dominance over the alts has increased slightly to 56.7%.

PI, APX Dump Hard

Pi Network’s native token doesn’t seem to be able to catch a break these days, marking consecutive all-time lows. The latest came hours ago with a nosedive to $0.086, solidifying its major correction as the asset is down by over 97% since its ATH marked last year.

APX is the other big loser today, dropping by over 25%. In contrast, BEAT has gained 20% while DEXE has doubled down on its major rally as of late.

ETH failed at $1,800, BNB is back to $570, while XRP dipped to a multi-day low at $1.07 before it rebounded slightly. HYPE, RAIN, DOGE, ZEC, and XLM are also slightly in the red, while SOL and XMR are with insignificant gains.

The total crypto market cap has shed over $20 billion in the past 24 hours and is now below $2.240 trillion on CG.

The post PI and APX Crater by Double Digits, BTC Price Dipped Below $63K: Market Watch appeared first on CryptoPotato.

Japanese convenience-store operator Lawson plans to test yen-denominated stablecoin payments at a Tokyo location in August, examining whether stablecoin payments can work inside a standard convenience store checkout flow.

On Monday, blockchain company HashPort said it had signed an agreement with Lawson and telecom group KDDI to conduct the trial at the Lawson Takanawa Gateway City store. Participants will use HashPort’s non-custodial wallet, while the store will process payments through the company’s point-of-sale system without needing to open or manage crypto wallets.

The pilot aims to explore how stablecoin payments can be integrated into Japan’s existing retail infrastructure while shielding merchants from much of the operational complexity associated with accepting digital assets.

The companies plan to assess integration requirements, checkout operations, payment processing times and wallet usability before considering broader applications.

Netstars launches multi-stablecoin merchant service

Separately, Japanese payments company Netstars launched Stablecoin Pay on Monday, opening applications from merchants seeking to accept multiple stablecoins as payment options.

The service initially supports USDC, USDT and the yen-denominated JPYC through the Solana and Polygon networks, with MetaMask as the supported wallet. Netstars set the merchant payment fee at 0.98% and said it plans to add more wallets and blockchains.

With the service, merchants can use existing payment terminals in most cases and handle product pricing, sales records and settlement in yen, even when customers pay with dollar-denominated stablecoins. Netstars said this removes the need to hold crypto or manage exchange rates.

The commercial launch follows Netstars trials involving USDC payments at Tokyo’s Haneda Airport from January to February and at a trading-card store in Himeji from April.

Related: Japanese lender launches Bitcoin-backed loans of up to $6.2M

The move from limited pilots to a merchant-facing service comes as Japanese companies build more consumer-facing products around the country’s regulated stablecoin market. On June 1, 2023, Japan introduced a dedicated framework for stablecoins when amendments to the Payment Services Act and related laws took effect.

The rules created regulatory categories for fiat-linked stablecoins and require businesses acting as intermediaries to register with the Financial Services Agency.

The framework was followed by regulatory approval for USDC distribution in March 2025 and by JPYC’s registration as a fund transfer service provider that August, before the stablecoin was launched in October.

Magazine: Has Bitcoin bottomed for this cycle? Analysts say ‘not yet’

After several strongly positive weeks, USD/CAD has stalled over the past few sessions, entering a phase of uncertainty.

On the dollar side, Fed Chair Kevin Warsh has struck a firm tone, reaffirming the 2% inflation target and pushing back against political pressure to cut rates, while sticky PCE inflation near 4% keeps hike odds alive for September. Yet June payrolls came in softer and speculative USD positioning looks stretched, raising doubts on how much further the rally can extend. Markets will also watch upcoming US CPI and PPI releases closely, as either gauge could reinforce the Fed hike case or, if softer, cap dollar strength.

The loonie’s story is similarly mixed. Canada’s June jobs report beat expectations, reducing the odds of a BoC cut, yet the currency remains capped by falling oil prices, subdued inflation, and unresolved CUSMA trade uncertainty. Two currencies face both genuine support and headwinds, leaving USD/CAD hostage to this week’s BoC decision and incoming US data—a backdrop that aligns well with what the chart itself is showing.

USD/CAD Technical analysis

As the 4H chart shows, USD/CAD has traded within a well-defined ascending channel since May’s lows, and is now consolidating just below recent swing highs. The Fibonacci retracement drawn from that low to the July high offers a useful reference for the levels ahead.

Bullish Scenario

As long as price holds above the ascending trendline and defends the former resistance, now turned support, in the 1.4100 area, the broader uptrend structure remains firmly intact, and this pause looks far more like healthy consolidation than an early reversal signal. A confirmed bounce off the trendline, followed by a decisive push back above the recent swing high near the 1.4250 area, would validate continued bullish control and open the way for USD/CAD to extend its rally into fresh highs for the move, keeping the dollar’s medium-term strength against the loonie firmly in place.

Bearish Scenario

A clean, sustained break below the ascending trendline would mark the first real technical warning sign, shifting near-term momentum decisively lower. In that case, the 0.382 and 0.5 Fibonacci retracement levels would become the first meaningful support tests, coinciding with the psychological 1.3900-1.4000 range. Losing these levels could expose a deeper slide towards the 0.618 retracement—an area that would confirm a genuine correction of the entire May-to-July rally rather than a simple pullback, and would put the pair’s medium-term bullish structure into serious question.

With price sitting right on the ascending trendline, the coming sessions could prove decisive in determining where USD/CAD heads next.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Ranking potential World Cup finals: Does anything top a France-Argentina rematch?

Newton’s Cradle Isn’t Really Perpetual

Lifeline confirms cyber incident exposed data

-

Fashion7 days ago

Fashion7 days agoOpen Thread: What Great Books Have You Read Recently?

-

News Videos6 days ago

News Videos6 days agoWhats Hidden Inside This Cash Register? #treasure #reselling #money

-

Fashion4 days ago

Fashion4 days agoLoro Piana Fall 2026 Enters Houston’s Art Scene

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Nutriplenish Leave-In Conditioner

-

Crypto World7 days ago

Crypto World7 days ago$1,000 Credit Alert! BlockDAG X Exchange Pre-Registration Now Officially Open, Polkadot Dips & Zcash Rebounds

-

Tech6 days ago

Tech6 days agoAnthropic’s new “J-lens” reveals a silent workspace inside Claude that mirrors a leading theory of consciousness

-

News Videos7 days ago

News Videos7 days agoBest Time to Enter Small Caps Right Now? Another Bull Run? | Financially Free

-

Business7 days ago

Business7 days agoAXT Shares Jump Nearly 14% as Semiconductor Materials Maker Rebounds on AI-Linked Indium Phosphide Demand

-

Sports6 days ago

Sports6 days agoJoshua Pacio ‘more complete’ ahead of ONE rematch vs Malachiev

-

Sports4 days ago

Sports4 days ago2026 Genesis Scottish Open Thursday TV coverage: Round 1

-

Tech5 days ago

Tech5 days agoAnthropic brings Claude Cowork to mobile and web as usage data shows most users aren’t coding

-

Crypto World7 days ago

Crypto World7 days agoSK hynix (000660.KS) Stock Dips as $28B Nasdaq ADR Offering Drives AI Memory Expansion

-

News Videos7 days ago

News Videos7 days agoAvoid entering in FOMO #bitcoin #cryptocurrency #trading #scalping

-

Sports3 days ago

Sports3 days agoSuper Eagles star Moses Simon opens up on Liverpool transfer regret

-

Sports6 days ago

We have punished the disrespect

-

Crypto World6 days ago

Crypto World6 days agoBinance lists Strategy’s STRC stock as company expands Bitcoin funding

-

Tech4 days ago

Tech4 days agoCharacter.AI enters the microdrama arena with its own productions, but there’s a twist

-

Tech6 days ago

Tech6 days ago9 Best Keyboards (2025), Tested and Reviewed

-

Business6 days ago

Business6 days agoEnbridge: AI Tailwind Priced In (Rating Downgrade)

-

News Videos6 days ago

News Videos6 days ago“What’s going on?!” Carl Froch discusses Floyd Mayweather Jr financial issues

You must be logged in to post a comment Login