Crypto World

CASHCAT’s $226M question as NOXA launchpad goes dark

For five consecutive days, a launchpad that did not exist a month ago collected more protocol fees than Pump.fun. On its best day, NOXA took in $2.33 million while the Solana incumbent, the platform that has minted eleven million tokens and defined an entire market cycle, managed $575,500.

Summary

- NOXA briefly out-earned Pump.fun and became Robinhood Chain’s dominant launchpad before its website went offline.

- CASHCAT’s $226 million market capitalization depends less on token mechanics than on attention, discovery, and launchpad infrastructure.

- The outage did not stop CASHCAT from trading, but it threatened the interface that drives creator fees, discovery, and momentum.

- Locked liquidity protects against one kind of rug, but it does not protect a memecoin from losing attention.

- The real test is whether NOXA’s interface, fee claims, and market share recover before competitors absorb its launchpad flow.

NOXA had launched more than 60,000 tokens, captured roughly 75% of all deployments on Robinhood Chain, and pulled 267,642 unique wallets onto a network that went live on July 1. Its flagship asset, a cat themed memecoin named CASHCAT, had run to a market capitalization of $226 million.Then the website went down. It stayed down for two days.Not the chain. Not the pools. Not the tokens. The front end, the thing that made all of it legible, the interface where creators claimed fees and buyers found what was trending and the entire machinery of manufactured urgency lived. It returned an error, and it kept returning an error while the market it had built continued trading without it.

The official explanation is a Cloudflare problem. The team’s account remains active, telling users a new site is in testing and that creator fees will be claimable through the interface once it goes live. Nothing in the public record contradicts that account. Nothing in the public record confirms it either, and in a market where the base rate for launchpad tokens dying is somewhere around 98%, two days of silence from the infrastructure holding a nine figure ecosystem is not a neutral event. It is a live experiment in what a memecoin is actually worth when the machine that made it stops answering.That experiment has a number attached, and the number is $226 million.

What CASHCAT is, and why it exists

Cash Cat was the original name Robinhood’s founders considered for the company, a detail preserved in a decade old tweet from chief executive Vladimir Tenev and in an early mascot the brokerage used before it became a mainstream financial institution. When Robinhood launched its own layer 2 network on July 1, the mascot was sitting there, unclaimed, perfectly formed as a memecoin premise: the discarded name of a company now worth tens of billions, revived on that company’s own chain.

Somebody launched it on NOXA. It worked spectacularly. CASHCAT rose more than 5,530% over seven days and more than 1,400% in a single twenty four hour stretch, hitting an all time high near $0.1418 while bitcoin fell roughly 2% over the same window, which is the clearest possible evidence that nothing macro was driving it. Onchain analysts surfaced the trades that make these markets self sustaining: one wallet turned $838 into $1.05 million over twenty days, another converted $86 into $1.6 million. Tenev himself posted about the chain’s ability to host both memecoins and real world assets, and attention did the rest.

There were no exchange listings. There was no protocol upgrade, no partnership, no treasury, no roadmap, and no team in any conventional sense. There was a joke about a company’s abandoned name, deployed on that company’s chain, at the exact moment the chain became interesting. That is the entire fundamental basis of a $226 million asset, and stating it plainly is not a criticism. It is a description of the category, one that governs the whole meme coins sector and has for years. Attention was the product, and the product sold.

The launchpad that ate Robinhood Chain

NOXA’s rise is the more revealing half of the story, because it exposes how much of a memecoin ecosystem is infrastructure rather than tokens.NOXA Fun is a hybrid launchpad. Where Pump.fun runs a custom bonding curve and migrates liquidity to an open exchange at graduation, NOXA deploys an ERC-20 and adds single sided liquidity to a Uniswap V3 pool in one transaction, making the token tradable on a public exchange from its first block. The liquidity position is locked permanently in a locker contract that never moves and cannot be pulled, which removes the classic liquidity drain rug and eliminates the migration window that has historically been the riskiest moment in a bonding curve launch. On its own terms the design is more conservative than the model it competes with, and understanding why requires knowing how liquidity pools and automated market makers actually work.

The platform layered on protections as it scaled: anti-vampire measures, anti-bundling detection, multi wallet controls, iterating fast enough that observers noted it week by week. Its native token, deployed on a different chain entirely and pending migration, carried a fully diluted valuation of $11 to $12 million after the team burned about 40% of supply, against $11 million in cumulative fees across four days. Pump.fun’s fully diluted valuation, for comparison, sits near $1.5 billion.

That gap is the valuation paradox the market has been arguing about all week. A platform earning at the rate of the category leader, valued at under 1% of it. There are three readings and they cannot all be right. The bullish one says the market has not repriced yet and NOXA is the most obvious mispricing on any chain. The structural one says fee run rates from a chain in its second week are not a business, they are a spike, and pricing a spike at Pump.fun multiples would be insane. The dark one says the discount is the market’s estimate of how likely the whole thing disappears.

Two days of downtime moved that argument out of theory.It is worth noting how quickly the market found the argument in the first place. Traders were circulating the fee-to-valuation gap within days of NOXA’s rise, framing it as an obvious mispricing against Pump.fun. That enthusiasm is itself information: a discount this visible on an asset this liquid is rarely a gift. Markets price launchpad tokens cheaply for the same reason they price mining stocks cheaply during a boom, because everyone can see that the current rate of extraction has nothing to do with the durable rate.

The mechanics of a two week fee explosion

The scale of what NOXA collected deserves unpacking, because the number is doing something other than what it appears to do.Launchpads earn on activity. A creation fee when a token deploys, a share of trading fees on every swap through the pool, and in NOXA’s structure, fees flowing from Uniswap V3 positions at the 1% tier that the platform’s tokens use. None of that revenue depends on any token succeeding. It depends only on churn, and churn is exactly what a brand new chain with a retail audience and 19,000 daily deployments produces in abundance. Across four days the platform booked roughly $11 million against a token valued at $12 million, which reads as an obvious arbitrage until you ask the question underneath: is that four day rate a business or a weather event?

The comparison to Pump.fun cuts both ways here. Pump.fun’s $1.5 billion valuation rests on two years of proven durability across multiple attention cycles, a graduated exchange of its own, a completed billion dollar token sale, and a fee base that survived the collapse of the memecoin mania that created it. NOXA has a fortnight, on a chain with a fortnight, in the single most favorable conditions any launchpad will ever see: a novel network, a mainstream brand halo, no competitors holding entrenched positions, and a flagship token running 5,000% in a week. Annualizing that is not analysis. It is extrapolation from a peak.

Which is why the outage is such an efficient test. If the fee run rate was a business, it survives two days offline and resumes. If it was a weather event, the two days are the whole event, and the rate never returns because the conditions that produced it were never repeatable. The market gets its answer within a week, and it gets it cheaply, which almost never happens in this asset class.

What the outage actually threatens

Here is the part that matters for CASHCAT holders, and it is more subtle than it first appears.The tokens are fine. That is not a reassurance; it is a technical fact with sharp edges. CASHCAT is an ERC-20 on Robinhood Chain, trading against a Uniswap V3 pool whose liquidity is locked in a contract that operates whether or not anyone can load a website. Uniswap does not need NOXA. The chain does not need NOXA. Any wallet can interact with the pool directly, and any aggregator can route to it without the launchpad’s involvement or permission. In the strict sense, a launchpad outage cannot touch the assets it launched, and anyone claiming CASHCAT holders are trapped has confused the interface with the market.

What the outage threatens is everything around the token. Creator fees accrue through the platform, and the team’s own statement acknowledges that claiming them requires the interface, meaning revenue owed to thousands of token deployers currently sits behind a domain that does not resolve. Discovery collapses without the front end: new tokens launch elsewhere, existing tokens lose the trending feeds and progress bars that manufacture the urgency these markets run on. And the flywheel reverses. Onchain data already showed new memecoin creation on Robinhood Chain climbing past 19,500 in a day while competing launchpads including flap.sh, trensh.today, and bankr absorbed share that NOXA could not defend from behind an error page.

So the honest framing of the risk is not that CASHCAT stops trading. It is that CASHCAT stops mattering. A memecoin’s value is the attention flowing through it, the attention is manufactured by an interface, and the interface has been offline for the two most valuable days a two week old ecosystem will ever have.

Is this a rug?

The question is being asked openly, and it deserves a rigorous answer rather than a vibe.Take the case for calm first. The team is publicly communicating during the outage, which is close to disqualifying as rug behavior: the defining feature of an exit is silence, deleted accounts, and vanished channels, not status updates about a staging environment. Liquidity is locked by design and cannot be withdrawn, so the single most common rug mechanism is architecturally unavailable here. The platform burned 40% of its own token supply days before going dark, an odd move for anyone planning to sell the rest. Cloudflare outages are real, routine, and have taken down far larger properties than a two week old launchpad. And the underlying economics are absurd for an exit: a platform earning millions in fees per day has vastly more to gain from staying online than from disappearing with whatever sits in a fee contract.

Now the case for concern. Two days is a long outage for an infrastructure problem that the operator attributes to a third party content delivery network, and it is exactly as long as it takes for competitors to take a market. Creator fees being unclaimable during the outage means real money is unreachable for real users, whatever the cause, and the promise to make them claimable “once the new site goes live” converts a technical failure into a trust exposure with no deadline attached. The platform’s own token lives on a different chain pending migration, which is an added moving part at precisely the wrong moment. And the category’s history is unkind: the industry’s canonical rug taxonomy distinguishes hard rugs, where developers vanish, from soft rugs, where involvement gradually decays while the thing quietly dies, and soft rugs look exactly like an infrastructure problem that never quite resolves.

The evidence, weighed honestly, favors the boring explanation. A team executing an exit does not typically burn its own supply, lock its liquidity permanently, post status updates, and abandon a business printing seven figures a day. But the market is not pricing the probability of a rug. It is pricing the probability of irrelevance, which is a different and much higher number, and two days offline in a launchpad war is how irrelevance starts.

There is also a category error worth naming, because it is corrupting the discourse around this. A rug is an act by an identifiable party who takes something they controlled and should not have taken. A collapse is a market outcome in which nobody did anything wrong and the money disappears regardless. Memecoin markets produce collapses at overwhelming rates without any fraud involved, which means most tokens that go to zero were never rugged, they were simply correct valuations of nothing arriving on schedule. Applying the word rug to a launchpad outage flattens that distinction and, more practically, sets holders up to look for the wrong evidence. They watch for a villain when the thing actually killing their position is indifference.

What would settle it is specific and observable. Watch whether the new interface ships and creator fees actually become claimable. Watch whether NOXA’s fee share recovers or whether flap.sh and its peers keep the ground. Watch the team’s wallets. Watch whether Robinhood Chain’s daily token creation stays near Solana’s or reverts once the novelty burns off. None of those require trusting anyone’s statement.

What the numbers actually say about the ecosystem

Look past the fees at the composition of the activity, and a less flattering picture emerges.More than 60,000 tokens launched through NOXA. Of those, the platform’s own interface displays a handful with meaningful market capitalizations, headed by CASHCAT, with the rest of the visible field clustering in the hundreds of thousands or low millions and the long tail invisible entirely. Peak single day volume of $252.9 million across the platform, with a single project accounting for $224 million of a comparable day, means the flagship was not one asset among many. It was the market, and everything else was noise around it.

That concentration is the ecosystem’s actual risk profile. A launchpad whose fee base is one token’s trading is not a platform, it is a single asset’s plumbing, and its revenue lives or dies with the attention on that one asset. The 640,000 unique holder addresses and 267,000 wallets NOXA brought onto Robinhood Chain are impressive as a distribution achievement and mostly irrelevant as a durability signal, because holders of a token that ran 5,000% in a week are not users, they are a queue.

None of this is unique to NOXA. It describes Pump.fun’s first year, Four.Meme’s ascendancy, LetsBonk’s arrival, and every launchpad that has ever briefly topped a fee chart. What is unique here is the timing: a platform reached that concentration and then lost its interface, in the same fortnight, on a chain that had no proven alternative for anyone to fall back to. The stress test arrived before the structure was finished.

The dependency nobody priced

Strip the specifics away and the CASHCAT situation exposes a structural feature of this entire market that the fair launch ideology obscures.

The pitch for permissionless launchpads is that they remove intermediaries. No gatekeepers, no vetting, no company standing between a creator and a market. Bonding curves and locked liquidity mean the platform cannot rug you, which the industry has treated as the end of the argument about platform risk.

It is not. The platform cannot take your tokens, and it does not have to. It can simply stop generating the attention that gives them value, and the tokens will die exactly as thoroughly as if it had drained the pool. Locked liquidity protects the mechanism and does nothing for the market. A permanently locked Uniswap position holding a token nobody is looking at is a monument, not an asset. The lock guarantees you can always sell. It guarantees nothing about whether anyone will be there to buy, and those are the only two facts that matter, in that order.

This is the same lesson that keeps arriving in different costumes. When a DAO’s treasury drained through a governance process working exactly as designed, the failure was not in the code, a dynamic crypto.news traced in detail in its account of how BonkDAO lost $20 million in a single vote. When BNB Chain’s Four.Meme briefly flipped Pump.fun on daily revenue, the lesson was that launchpad dominance is a function of where attention currently lives and nothing more durable than that. Infrastructure risk in crypto is rarely custodial. It is attentional, and no audit measures it.

CASHCAT holders own an asset with permanently locked liquidity on a chain backed by a publicly traded brokerage, launched through a platform with better rug protections than the category leader, and every one of those facts is true and none of them answers the only question that determines their outcome, which is whether anyone is still looking in a month.

Robinhood’s problem, arriving on schedule

There is a second party to this that has said nothing, and its position gets more uncomfortable by the day.Robinhood Chain launched as infrastructure for onchain finance and real world asset tokenization. What it got in its first fortnight was a memecoin casino, more than $3 billion in decentralized exchange volume, honeypot tokens proliferating fast enough that cross chain provider Relay Protocol began publicly blocking them, and a scam token that used the hijacked accounts of SpaceX and Starlink to rob buyers on its rails, an episode that arrived within weeks of SpaceX joining the Nasdaq-100 with its trade already running on crypto rails. NOXA, the largest single application on the chain, states plainly in its own interface that it is an independent project not affiliated with Robinhood Markets.

That disclaimer is doing an enormous amount of work. It is legally accurate and commercially irrelevant. A retail brokerage’s brand is on the chain, retail users are the audience, and the flagship asset of the ecosystem is literally named after the company’s original name and modeled on its own former mascot. Robinhood did not build CASHCAT, did not endorse it, and under the architecture it chose, cannot remove it. It will nonetheless own every consequence in the public reading, and its silence through both the SCATMAN affair and the NOXA outage suggests a company that has not decided what it wants to say, or has decided that saying anything invites the responsibility it structured the chain to avoid.

The permissionless design that made the chain’s launch explosive is the same design that makes the next fortnight unmanageable. That is not a contradiction anyone has solved, on any chain, including the ones without a brokerage’s name on them.

Where this lands

Three outcomes are live, and the market is currently paying for the middle one.NOXA returns, ships the new interface, unlocks creator fees, and reclaims its share. The outage becomes a footnote, the valuation paradox resolves upward, and CASHCAT trades on whatever attention Robinhood Chain retains once its novelty is priced. This is the likeliest single outcome and the least interesting.

NOXA returns and the market has moved. The fees flowed to flap.sh and the rest during the blackout, the trending feeds rebuilt themselves elsewhere, and NOXA is a large historical fee number attached to a platform nobody defaults to anymore. CASHCAT survives as an artifact of a moment, drifting on whatever residual community persists. This is the outcome that history most often delivers, because attention is the least loyal asset in this market and switching costs between launchpads are effectively zero. A creator chooses a platform in seconds and abandons it just as fast.

NOXA does not return in a form anyone trusts. The creator fees stay unclaimed, the explanation stays thin, and a two week old chain learns that its dominant application was a single point of failure with a status page. CASHCAT’s locked liquidity keeps a market technically alive at a price that reflects nobody caring.

The tokens survive all three scenarios. That is precisely the point that the fair launch pitch never quite says out loud: survival of the contract and survival of the value are unrelated propositions, and the second one depends entirely on infrastructure that owes its users nothing and can go dark for two days without breaking a single promise it ever made.The $226 million question is not whether CASHCAT can still be traded. It is whether $226 million was ever a fact about the token, or a fact about the launchpad, briefly measured through it.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Figures on protocol fees, token counts, market capitalizations, and wallet activity derive from third party sources including DefiLlama, Dune, Lookonchain, and platform interfaces, not from audited disclosures. No rug pull has been confirmed and the platform attributes its outage to a third party service failure. Details reflect information current as of July 14, 2026, and are subject to change. Always do your own research.

Stripe and private equity firm Advent International have reportedly made a joint bid to buy PayPal Holdings, putting a major payments player directly in the middle of a fast-consolidating digital payments race.

According to Reuters, the offer would include about $50 billion in committed financing and would value PayPal at $60.50 per share, a figure described by sources as representing a 28% premium to PayPal’s Tuesday closing price. Both PayPal and Stripe declined to comment.

Key takeaways

- Reuters reports Stripe and Advent International have made a joint offer to acquire PayPal at $60.50 per share.

- The bid reportedly comes with roughly $50 billion in committed financing.

- The proposal would represent about a 28% premium versus PayPal’s Tuesday closing price.

- Both companies have been expanding crypto and stablecoin-related capabilities, which could be strategically relevant if a deal advances.

- PayPal stock rose in Wednesday premarket trading on the news, but the longer-term outcome depends on regulatory and shareholder processes.

A potential reshaping of mainstream payments

At the center of the report is a classic strategic question: whether large-scale payments infrastructure and consumer payment reach can be combined under one umbrella to compete more effectively with mobile-first options.

Reuters said the offer was made by Stripe alongside Advent International and referenced sources familiar with the matter. The proposed per-share price would imply a significant premium, and PayPal shares reflected that immediately—rising 11.3% to $52.73 in Wednesday premarket trading, according to Yahoo Finance data. Still, PayPal is described as having gained about 14% over the past month while remaining down 35% year-over-year, underscoring how investors are still weighing turnaround risk against growth prospects.

Why PayPal is back in the acquisition spotlight

This would be Stripe’s second attempt to acquire PayPal. Earlier reporting by Bloomberg in February said Stripe held preliminary acquisition talks with PayPal as PayPal faced increased competitive pressure from smartphone-based payment services such as Google Pay and Apple Pay.

What’s notable here is the timing: instead of focusing only on traditional payment processing, the competitive landscape increasingly includes payment rails that can move quickly into new settlement and compliance frameworks. That environment raises the stakes for any acquirer—especially one with a track record of building payment infrastructure across different use cases, from merchant processing to stablecoin-enabled settlement.

Stablecoins as a shared strategic direction

The acquisition rumor lands at a moment when both PayPal and Stripe have been pushing deeper into stablecoin activity, a sector that is increasingly viewed as an extension of payment networks rather than a standalone crypto experiment.

PayPal introduced its PYUSD stablecoin in 2023. CoinMarketCap data cited in the report shows PYUSD peaked at a market capitalization of about $4.2 billion in February 2026 before falling to roughly $2.85 billion. While PYUSD is described as one of the 10 largest stablecoins, it remains far behind leaders including Tether’s USDt and Circle’s USDC.

Stripe, meanwhile, has been building stablecoin-related infrastructure for payments and accounts. The report notes that Stripe has offered stablecoin-based accounts globally since May 2025, and that its stablecoin infrastructure platform, Bridge, received conditional approval to operate as a federally chartered national trust bank under the US Office of the Comptroller of the Currency on Feb. 17.

Stripe has also accelerated adoption through partnerships. In March, Visa said it would expand its stablecoin card partnership with Stripe-owned Bridge to more than 100 countries across Europe, Asia-Pacific, Africa, and the Middle East by the end of the year—an expansion that signals how stablecoins are being positioned to integrate into broader consumer payment flows.

What investors should monitor next

Even if the offer progresses, the path from a reported bid to a completed acquisition depends on standard deal mechanics: due diligence, agreement on terms, shareholder approval, and regulatory review. For crypto-adjacent investors, the stablecoin angle adds another layer of uncertainty—whether a combined company would streamline stablecoin strategy, expand payment settlement capabilities, or maintain separate roadmaps.

In the near term, the most important question is whether PayPal’s board engages meaningfully with the proposal and how competitors and regulators respond to a transaction that would unite large consumer payment distribution with stablecoin-enabled infrastructure. Readers should also watch the market’s reaction for signs of whether investors treat the news as a genuine path to consolidation or as a typical M&A rumor that may not clear the next hurdles.

XRP price prediction is back in focus as it trades around $1.11, up about 3.6% over the past 24 hours. It remains pinned beneath a resistance zone that has rejected several intraday rallies this week.

So far, this has been more of a slow grind than a breakout. But Ripple’s reported alignment with the x402 Foundation to support RLUSD-powered AI payments is giving the long-term story another boost.

The x402 initiative positions RLUSD, Ripple’s dollar-backed stablecoin, as a settlement asset for autonomous AI agents. That narrative gained traction after the XRP Ledger processed more than one million agentic transactions using a fixed network fee of 0.0002 XRP per transaction. Meanwhile, the x402 Foundation includes major companies such as AWS, Google, Visa, Mastercard, Stripe, Circle, and Coinbase, showing the project has serious industry backing rather than just marketing buzz.

At the same time, macro conditions have become a little friendlier. June’s US consumer inflation rate came in at 3.5% year over year, matching expectations after energy prices pulled the monthly index lower. That eased some concerns over tighter monetary policy and helped improve sentiment across equities and crypto.

Ripple’s payments narrative has been building for months, and RLUSD continues to expand its footprint. However, the price still needs to confirm the story. Until buyers force a clean breakout, XRP remains stuck in wait-and-see mode, with the fundamentals knocking while the chart keeps the door only slightly open.

Discover: The Best Token Presales

XRP Price Prediction: Break $1.15 This Week?

XRP trades around $1.11, after climbing roughly 3.5% over the past 24 hours. The session ranged between $1.06 and $1.12, while its market capitalization sits near $69 billion. Price is still coiling beneath $1.12, which often means the market is storing energy before making its next move.

Support remains around $1.05 to $1.06, where buyers have repeatedly shown up. Meanwhile, resistance stretches from $1.11 to $1.15, and sellers have defended that area more than once. Trading activity has also picked up, hinting at accumulation, although a convincing close above $1.12 would strengthen that case.

Three scenarios still stand out. The bullish path begins with a daily close above $1.15, opening the door toward the $1.20 to $1.30 area over time. The base case keeps XRP chopping between $1.07 and $1.13 as traders digest macro data. Sometimes the market just likes to make everyone wait.

The bearish case is equally simple. A decisive break below $1.05, backed by strong volume, would hand momentum back to sellers and could send XRP toward the mid $0.90s. While longer-term forecasts remain constructive, the near-term still belongs to the charts.

Trade XRP on BYBIT, and Don’t Miss Out on Our $1,000 USDT Airdrop

Maxi Doge Targets Early Mover Upside as XRP Tests Key Levels

XRP at $1.10 with a $68 billion market cap is a legitimate holding, but the asymmetric upside that early XRP adopters captured is structurally unavailable at this size. That math drives traders to scan earlier stages of the cycle.

Technical analysis on XRP suggests the next meaningful move may take weeks to materialize, which is exactly the window that presale positions are designed to exploit.

Maxi Doge ($MAXI) is an ERC-20 meme token built around a deliberately absurd but surprisingly coherent concept: a 240-lb canine juggernaut channeling 1000x leverage trading energy, with community mechanics that go beyond a simple meme pump.

The project has raised $4.8 million at a current presale price of $0.0002829, with dynamic staking APY available to holders. Standout features include holder-only trading competitions with leaderboard rewards, a Maxi Fund treasury allocated to liquidity and partnerships, and a meme-first marketing strategy built on viral gym-bro culture.

Explore the Maxi Doge presale here.

Discover: The Best Crypto to Diversify Your Portfolio

The post Ripple Joins x402 Foundation to Advance RLUSD AI Payments: Will XRP Price Benefit? appeared first on Cryptonews.

The Czech Finance Ministry added Polymarket to its list of unauthorized online gambling websites on Monday, requiring internet service providers (ISP) to block access.

The ministry listed the prediction market’s website under the country’s Gambling Act, which prohibits operators from offering unlicensed online gambling services to Czech users.

Under the Gambling Act, ISPs must block access to websites included on the ministry’s blacklist within 15 days of publication of the name.

Polymarket is a prediction market where users trade contracts tied to the outcomes of future events. The platform gained global attention during the 2024 US presidential election, with its markets widely cited as a gauge of election sentiment.

Polymarket and rival Kalshi have been restricted by regulators across the European Union, including in France, Germany, Poland, Romania and Spain.

Polymarket did not immediately respond to Cointelegraph’s request for comment.

Prediction markets face watchdog scrutiny beyond Europe

Regulators in several jurisdictions argue that some prediction market contracts amount to unlicensed gambling or fall under existing financial market rules.

On July 3, the European Securities and Markets Authority (ESMA) warned that many prediction market contracts could already fall under existing restrictions on binary options if they meet the definition of financial instruments.

The regulator said companies cannot avoid EU financial rules simply by marketing binary-style products as “event contracts” rather than derivatives. ESMA said the assessment depends on a contract’s characteristics rather than how they are marketed, adding that firms offering qualifying contracts to retail investors may already be subject to national restrictions implementing the bloc’s 2018 binary options ban.

ESMA also said companies offering such products to professional clients may need authorization under the Markets in Financial Instruments Directive, or MiFID II.

Related: Wall Street banks tighten prediction market rules for staff as insider fears spread

Outside the EU, prediction markets have faced similar regulatory action in Australia, Indonesia and Singapore.

In the US, Kalshi and Polymarket have been targeted by regulators in several states over allegations that their event contracts constitute illegal gambling, while the Commodity Futures Trading Commission maintains such products fall under its exclusive jurisdiction as federally regulated derivatives.

The dispute has resulted in conflicting court rulings and prompted calls for Congress to clarify whether sports and political event contracts should be regulated as gambling or federally regulated derivatives.

Magazine: Strategy became a symbol of the dot-com crash: Could history repeat?

Payments giant Stripe offered to buy PayPal (PYPL) in a deal worth $53 billion, the Financial Times reported on Wednesday.

San Francisco-based Stripe made the $60.50-a-share offer in tandem with private equity firm Advent International, according to the report, which cited two people familiar with the matter.

The bid represents a premium of around 28% on PayPal’s closing price of $47.37 on Tuesday. The New York-listed payments provider’s shares have surged over 18% to $56.10 in pre-market trading.

The bid follows an earlier expression of interest, though PayPal has been reluctant to engage with the offer thus far, the FT said.

Neither PayPal, Stripe nor Advent immediately responded to CoinDesk’s request for comment.

Stripe and PayPal are among the most prominent mainstream financial companies bringing stablecoins to traditional payment mechanisms. Stablecoins are digital tokens pegged to the value of a traditional financial asset, usually a fiat currency.

PayPal’s stablecoin PYUSD is the eighth-largest in the sector with a market capitalization of $185 million, according to CoinGecko data. The industry is dominated by Tether’s USDT at $184 billion.

Stripe’s historical focus was on embedding the second-largest stablecoin, Circle Internet’s USDC, into its payments infrastructure.

It has recently moved toward offering stablecoin and other blockchain-based services more independently, developing with its own mainnet, Tempo. The company also joined the Open USD venture alongside Mastercard, Visa and BlackRock to develop a new stablecoin, which could pose a serious challenge USDC.

Japan has enacted sweeping amendments to its financial laws that classify cryptocurrencies as financial products, opening the door to lower crypto taxes, domestic exchange-traded funds and stricter market oversight.

Summary

- Japan has passed a law classifying cryptocurrencies as financial products under the Financial Instruments and Exchange Act.

- The legislation creates a path for a 20% crypto tax rate, domestic crypto ETFs and stricter insider trading rules.

- Penalties for unregistered crypto businesses will increase, with implementation set to begin after the law is promulgated.

According to Japan’s public broadcaster NHK, the House of Councillors approved the amendments to the Financial Instruments and Exchange Act on Wednesday, completing the bill’s passage through both chambers of the Diet.

The legislation creates a separate legal category for crypto assets alongside traditional financial products such as stocks and bonds. Until now, cryptocurrencies had been regulated under the Payment Services Act as a payment method rather than as investment products.

Among the changes, the amended law introduces insider trading restrictions for crypto transactions, requires annual disclosures from issuers of certain crypto assets, and increases penalties for unregistered businesses.

CoinPost reported that the maximum prison sentence for operating without registration will increase from three years to 10 years, while the maximum fine will rise from 3 million yen to 10 million yen, or about $18,500 to $61,600.

Tax changes and ETF framework move forward

Beyond market conduct rules, the amendments establish the legal basis for separate taxation of crypto gains at an effective rate of about 20%, together with a three-year loss carry-forward deduction. Japan currently treats crypto profits as miscellaneous income, with tax rates reaching as high as 55%.

According to CoinPost, those tax provisions are expected to take effect in January 2028 because enforcement is scheduled to begin during the 2027 fiscal year.

The legislation also creates the foundation for issuing domestic spot cryptocurrency exchange-traded funds. CoinPost said the Japan Exchange Group is considering the first local crypto ETF listings as early as 2027, with traditional financial institutions expected to serve as issuers. The report added that approval of spot bitcoin ETFs has not yet been confirmed.

Following promulgation, the law is expected to take effect within one year, while cabinet ordinances and supervisory guidelines will determine how the new rules are implemented.

Crypto reforms accompany Japan’s Web3 strategy

The legislation follows a series of government efforts to strengthen Japan’s digital asset sector alongside its startup agenda.

Earlier this month, Prime Minister Sanae Takaichi told attendees at WebX 2026 that Web3 forms part of Japan’s national innovation strategy rather than a standalone crypto initiative. As previously reported by crypto.news, she said the conference gives founders, investors and companies opportunities to build new business partnerships, although her address did not announce new funding or immediate regulatory measures.

The government’s Comprehensive Startup Support Package, introduced in 2025, seeks to expand startup financing through public and private institutions, while Japan’s five-year startup plan targets annual startup investment of about 10 trillion yen by fiscal 2027. Alongside those initiatives, lawmakers have continued advancing crypto reforms designed to bring digital assets closer to traditional financial markets through tax changes and an ETF framework.

Coinbase head of platform, Rob Witoff, said that the company estimates between 95% and 100% of its code is written by or with large language models. It is a figure that stood at 40% just five months ago in February. The jump represents one of the strongest public disclosures of AI adoption from a major publicly listed financial technology company.

Witoff described AI coding as effectively universal across the company, with employees using LLM-powered tools daily for drafting, refactoring, testing, reviewing, debugging, and generating boilerplate.

For sensitive infrastructures like cryptography and core security systems, Witoff acknowledged that human oversight remains central. Coinbase operates trading systems, custody infrastructure, wallets, compliance tools, and blockchain integrations where software errors carry direct financial and regulatory consequences.

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

Armstrong’s Leaner Operating Model

The disclosure follows Coinbase’s May 2026 restructuring, which cut approximately 14% of the company’s workforce, or around 700 employees. CEO Brian Armstrong linked the change to AI, saying AI had “dramatically” changed how work gets done and that Coinbase needed to return to startup speed with AI at its core. Armstrong also stated that engineers were using AI to accomplish in days what previously required entire teams working for weeks.

Coinbase’s earlier estimate in February was that AI was involved in about 40% of its code, and the company says it has since moved to nearly all-code AI assistance in a matter of months.

Supporters argue that AI-assisted development could improve COIN’s operating leverage if a smaller engineering team can ship and maintain products at equivalent or greater velocity.

Under that scenario, margins could improve while development cycles become shorter. What remains unquantified is the long-term maintenance and security cost of running financial infrastructure increasingly developed with AI assistance, a variable that critics argue the industry has not yet stress-tested at scale.

Discover: The Best Token Presales

The 40% to 95% Coinbase Vibe Coding Shift

The term vibe coding describes developers accepting AI output with minimal scrutiny. Coinbase’s model, as Witoff described it, emphasizes supervised AI assistance rather than unreviewed production output: AI can be used for drafting, refactoring, testing, reviewing, debugging, and generating boilerplate, while engineers remain responsible for oversight and deployment in production environments.

That nuance is easy to lose in the headline number. Coinbase’s claim is that code is written by or with LLMs, with engineers retaining responsibility for oversight and deployment. The adoption of AI tools across the crypto industry continues to accelerate, while formal guidance and governance frameworks are still evolving.

Coinbase adoption curve, from experimental productivity tool to near-universal operating model in under a year, mirrors the pattern seen at AI-native startups, but at the scale of a regulated, publicly listed exchange.

The competitive implication for peers is not trivial: a crypto exchange that can prototype, iterate, and ship with fewer employees has a structural speed advantage in a market where product velocity directly correlates with user acquisition and trading volume.

The layoffs complicate the narrative. Connecting 700 job cuts to AI productivity gains is exactly the kind of framing that draws regulatory and political scrutiny. Today, Armstrong has leaned into it explicitly rather than softened the connection.

For now, the primary variable is whether Coinbase’s supervised AI-assisted model holds up at scale, and whether the company’s security and reliability record supports the productivity claims once audited under pressure.

Discover: The Best Crypto to Diversify Your Portfolio

The post Brian Armstrong Reveals Coinbase is 95% Vibe Coded By AI appeared first on Cryptonews.

Bitcoin (BTC) can hit up to $80,000 by August, a new prediction says as data lays out key nearby BTC price levels.

Key points:

- Bitcoin can continue to $70,000 and higher next month if it clears nearby resistance, says new analysis.

- Market participants identify the most significant support and resistance levels now circling spot price.

- A macro tide could be the spark to ignite the next move higher this week.

BTC price roadmap sees $68,000 within two weeks

In an X update on Wednesday, crypto trader and analyst Michaël van de Poppe said that BTC/USD was successfully defending “crucial” support.

“It’s holding the crucial level at $61,000 and flipping important MAs for support, indicating that there’s more momentum on the horizon,” he wrote, referring to moving average trend lines.

“I’m expecting to see a rally to $68,000 in the next 1-2 weeks, followed by a continuation towards $75,000-80,000 in August.”

BTC/USDT one-day chart. Source: Michaël van de Poppe/X

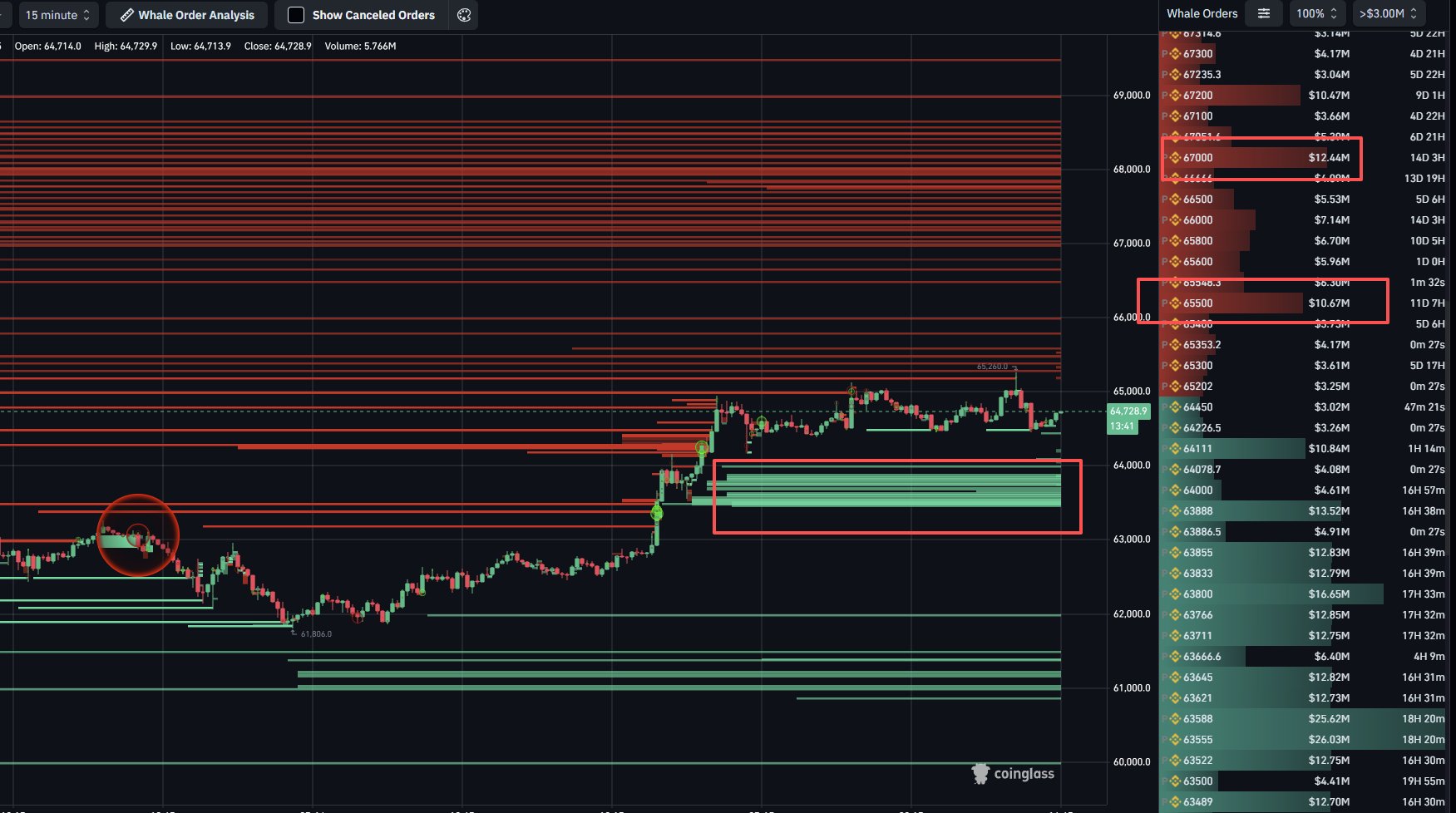

Van de Poppe’s first target coincides with exchange order-book liquidity hurdles that price would encounter if it were to break out of its local range.

Updating X followers on whale orders, monitoring resource CoinGlass showed the area at $67,000 and above as key for the cohort. Support, meanwhile, sat principally between $63,500 and $63,800.

BTC/USDT 15-minute chart with whale orders. Source: CoinGlass

Others remained cautious, with declining spot-market volume causing suspicion about the strength of the latest gains.

“Wouldn’t get excited about this pump, this can easily end up being a failed auction above value area,” commentator Exitpump warned on Tuesday.

BTC/USDT perpetual contract one-hour chart. Source: Exitpump/X

Previously, trader and analyst Rekt Capital warned that July strength should reverse by August as Bitcoin repeats standard bear-market behavior.

QCP Capital: Crypto market still needs “conviction”

In market research issued on Monday, trading company QCP Capital suggested that a macro “catalyst” could be all that was needed to propel crypto higher.

Related: Bitcoin bear market will bottom when two-month RSI metric hits zero, trader predicts

As Cointelegraph reported, the coming days will see the release of key US inflation data prior to the Federal Reserve’s decision on interest-rate changes at the end of the month. Tuesday’s data came in below expectations, helping to send Bitcoin back toward $65,000.

“Should this week’s macro data and earnings continue to validate the bullish narrative, improving risk sentiment could spill over into digital assets as investors rotate into markets that have lagged the broader equity rally,” QCP wrote.

“Until then, crypto appears caught between supportive long-term fundamentals and a market still waiting for conviction.”

Commodity-linked currencies strengthened after US inflation data came in weaker than expected. The Consumer Price Index (CPI) slowed to 3.5% year-on-year in June, below the 3.8% forecast, while core inflation eased to 2.6% versus expectations of 2.8%. On a monthly basis, headline CPI unexpectedly fell by 0.4%, while core CPI was unchanged. The moderation in inflationary pressure increased expectations that the Federal Reserve may adopt a more accommodative policy stance, putting pressure on the US dollar and supporting both the Australian and Canadian dollars against the greenback.

However, despite the weaker US dollar, the next move in USD/CAD will largely depend on the Bank of Canada’s policy decision. Later today, the central bank will announce its interest rate decision, publish its updated Monetary Policy Report, and hold a press conference with the Governor. If policymakers maintain a cautiously hawkish tone on inflation, the Canadian dollar could receive additional support. Conversely, a more dovish message may limit CAD gains despite the broader weakness in the US dollar.

Market participants will also focus on the release of the US Producer Price Index (PPI), which will provide further insight into inflation trends following the softer CPI report. In addition, US crude oil inventory data could influence USD/CAD, as oil prices traditionally have a significant impact on the Canadian dollar.

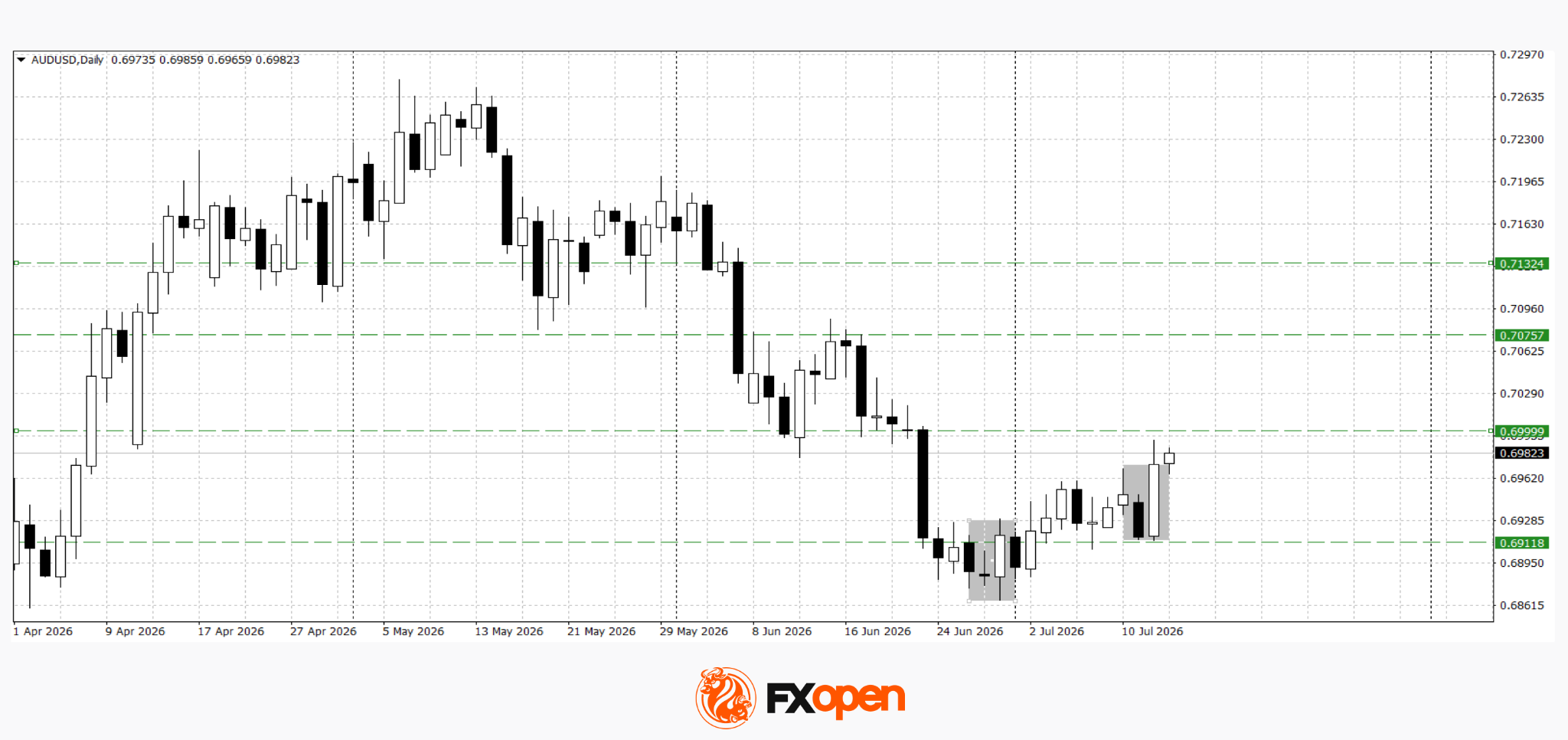

AUD/USD

The AUD/USD pair continues to develop the bullish engulfing reversal pattern. Yesterday, buyers managed to test the key resistance level around 0.7000. If the pair secures a sustained break above this level, the rally could extend towards the 0.7080–0.7130 area. The bullish scenario would be invalidated by a move below 0.6900.

Key events for AUD/USD:

- Today at 14:00 (GMT+3): US MBA Mortgage Market Index

- Today at 15:30 (GMT+3): US Producer Price Index (PPI)

- Today at 15:45 (GMT+3): Speech by FOMC member John Williams

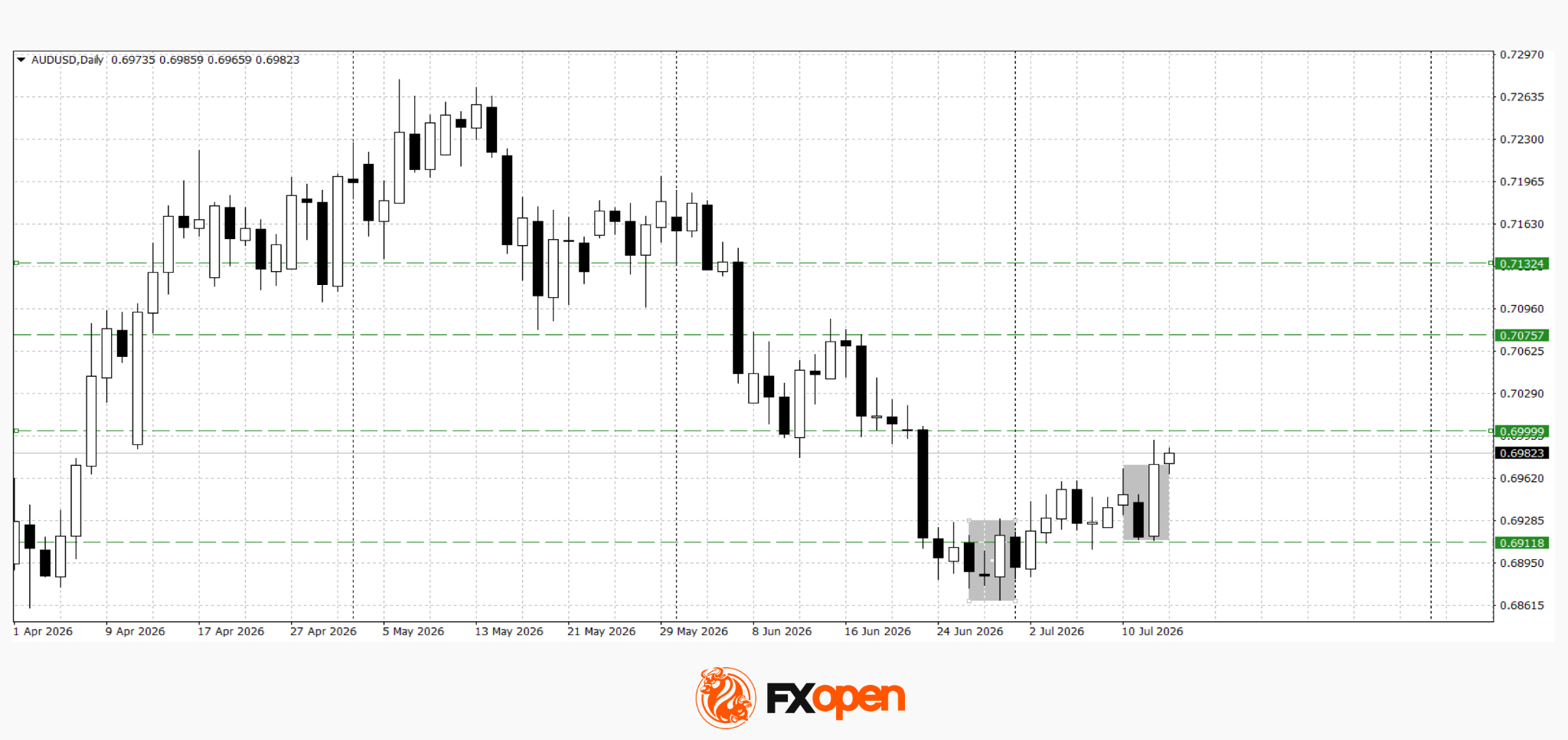

USD/CAD

Following confirmation of the bearish tower top reversal pattern, selling pressure on USD/CAD intensified, reinforced by the weaker-than-expected US inflation data. As a result, the pair declined below 1.4100. Technical analysis suggests there is scope for a further move lower towards the 1.3960–1.4020 area. A decisive break back above 1.4120 could revive the bullish outlook.

Key events for USD/CAD:

- Today at 16:45 (GMT+3): Bank of Canada interest rate decision

- Today at 17:30 (GMT+3): US Crude Oil Inventories

- Today at 17:30 (GMT+3): Bank of Canada press conference

Overall, the weaker US inflation report strengthened expectations of a more accommodative Federal Reserve, weighing on the US dollar and supporting commodity-linked currencies. However, the next moves in AUD/USD and USD/CAD will depend on upcoming economic data and the Bank of Canada’s policy guidance.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Just a few short years ago, the crypto hype was strong. VCs were eager to pour money into solutions for scalability, data availability, and any number of buzzwords.

Since then, the advent of powerful AI models and prolonged bear markets have taken the wind out of crypto’s sails and many chains which promised the future are now as good as forgotten.

One keen-eyed X user, crypto marketer Stacy Muur, noted the staggering $500 million invested across six blockchain projects which, together, have produced a total of just $360 in blockchain fees in the past 24 hours.

Read more: AscendEx shutdown: Uncertainty over withdrawals as hot wallets lack funds

The claim caught Protos’ eye, so we took a look at the six companies to see where it all went wrong.

Berachain

Berachain is a blockchain born as a spinoff of the 2021-era Bong Bears NFT collection. It claims to be the first proof-of-liquidity based chain, and aims to be a “growth engine for onchain businesses.”

The project raised a total of $142 million across two rounds in 2023 and 2024.

However, according to its most recent EoY statement, the project has struggled amidst issues with sentiment, shrinking crypto-native TAM and “increased skepticism around the value of infrastructure as a whole.”

Since launching in early 2025, its BERA token is down 98%.

Berachain was among the networks caught up in November’s devastating Balancer hack, leading validators to temporarily halt the network.

Later that same month, it was revealed that one of the backers, Brevan Howard’s Nova Digital, was granted a one year, risk-free refund right on its $25 million investment.

Read more: Balancer exploit drains $129M in DeFi disaster

Celestia

Celestia was seen as a hot ticket back in 2023 when “data availability” was the buzzword du jour.

Part of the Cosmos ecosystem, it promises bespoke, high throughput, modular chains “for companies with internet-scale traffic.”

It raised first $1.5 million in 2021, a further $50 million in 2022 and finally $100 million in 2024.

Its much-hyped token launch was one of the first rays of light following a deep bear market sparked by the catastrophic crypto collapses of 2022.

Despite initially surging around 10x in its first months to an all-time high of over $20, TIA eventually bled approximately 98%, sitting today at $0.40.

Scroll raised a total of $83 million over three funding rounds, the latest of which brought the Ethereum L2 to a $1.8 billion valuation in March 2023.

It made just $24 in fees yesterday.

The zkEVM layer two hit a peak TVL of $585 million as users enthusiastically farmed an ultimately disappointing airdrop. In the aftermath, the network lost around 75% of its TVL within a couple of months.

There’s currently just under $12 million on the chain.

Eclipse

Eclipse billed itself as “Solana on Ethereum,” an SVM layer two network which would pair Solana’s performance with Ethereum’s liquidity.

Developer Eclipse Labs raised a total of $65 million, most of which came in a $50 million Series A, led by Placeholder and Hack VC, in March 2024.

DeFiLlama data shows the chain’s TVL peaking at almost $50 million in late February last year. It’s currently down to just $1.15 million, a drop of approximately 98%.

The project’s most recent blog post is from a year ago, announcing the launch of its token ES, and an airdrop. Eclipse Labs has since pivoted to development of The Human API, a marketplace for AI agents to hire humans.

Sonic

Launched as Fantom by controversial developer Andre Cronje, founder of DeFi stalwart Yearn Finance, the fast, low-cost network migrated to Sonic in 2024. It raised a total of $61 million across six rounds between 2018 and 2024, according to ICODrops.

As Fantom, it took a hit in the Multichain debacle, with many bridged assets depegged from their native versions.

Fantom’s peak TVL reached a staggering $7.9 billion in 2022 and now sits at just under $5 million. Sonic’s hit $1.2 billion last spring, but has since dropped to $16 million.

Cronje’s involvement with Sonic terminated last month and he’s spent much of the last 18 months building Flying Tulip.

Read more: Andre Cronje says someone stole his code to build a $1B DeFi project

Manta

ZK-focused Manta raised a total of $60 million across four rounds between 2021 and 2023.

Its TVL chart is dramatic, highlighting an intense, heavily gamified airdrop campaign, which saw over $650 million poured into the chain.

Just a few weeks before its peak, TVL sat at under $20 million. Likewise, within four months, it was back below $50 million once again. Today, just $4 million is held on the chain.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

The United Kingdom has set an early 2027 target to issue its first digital sovereign bond on distributed-ledger infrastructure, becoming the first G7 country to launch government debt in tokenized form.

Summary

- The UK plans to issue its first blockchain based sovereign bond by early 2027 through HSBC’s Orion platform.

- The Digital Gilt Instrument will operate inside the Bank of England and FCA Digital Securities Sandbox.

- The move comes as the UK expands cooperation with the US on stablecoins, tokenized assets and cross border financial markets.

According to Chancellor Rachel Reeves, who announced the plan during her annual Mansion House speech, the government intends to follow the first issuance with additional digital gilt sales if the pilot progresses as expected.

The Digital Gilt Instrument, or DIGIT, will be a sterling-denominated government bond issued on HSBC’s Orion blockchain platform. It will operate within the Bank of England and Financial Conduct Authority’s Digital Securities Sandbox, a testing environment created for digital securities.

The Treasury introduced the pilot in 2024 to examine whether distributed-ledger technology could shorten settlement times, reduce reconciliation work and lower operating costs across government debt markets. HSBC secured the mandate to operate the platform in February after issuing more than $3.5 billion of digital bonds through Orion.

Speaking at the same event, Bank of England Governor Andrew Bailey said the central bank will work toward making DIGIT eligible as collateral in its market operations. According to Bailey, that step could support tokenized repurchase agreements while allowing banks to use the security in central bank funding transactions.

The Treasury has not disclosed the size, maturity, coupon, investor eligibility, or settlement asset for the bond. Officials said the initial issuance will sit outside the government’s conventional gilt financing program.

Digital bond plans follow tokenization push

The planned bond sale comes as the UK expands its work on tokenized financial markets beyond pilot projects.

Earlier this week, the UK and the United States published a joint statement committing to closer cooperation on stablecoin regulation, cross-border payments and tokenized finance through the Transatlantic Taskforce for Markets of the Future.

According to the joint statement, both governments plan to explore how regulated stablecoins issued in one country could access the other market while maintaining separate domestic regulatory frameworks. The two countries also agreed to seek common approaches for tokenized securities settlement and examine whether stablecoins or tokenized money market funds could serve as collateral in clearing markets.

The statement said stablecoins presented as money should maintain at least a one-to-one backing with high-quality liquid assets, while reserve assets should remain separate from issuers’ corporate funds. Officials also said holders should receive timely redemptions and clear legal protections if an issuer fails.

Although the stablecoin agreement does not create automatic market access or mutual recognition, it outlines a framework for regulators to reduce unnecessary barriers to cross-border tokenized financial services while each country completes its own regulatory process.

Medallion locks in EPS strategy

Stripe and Advent reportedly bid $53B to acquire PayPal

Flavor Flav’s SHE Weekend Set To Take Over Las Vegas This Week

-

Fashion6 days ago

Fashion6 days agoLoro Piana Fall 2026 Enters Houston’s Art Scene

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Nutriplenish Leave-In Conditioner

-

Sports6 days ago

Sports6 days ago2026 Genesis Scottish Open Thursday TV coverage: Round 1

-

Sports5 days ago

Sports5 days agoSuper Eagles star Moses Simon opens up on Liverpool transfer regret

-

Tech6 days ago

Tech6 days agoCharacter.AI enters the microdrama arena with its own productions, but there’s a twist

-

News Videos15 hours ago

News Videos15 hours agoXRP BOMBSHELL… XRP OMBOARDED FOR TRANSACTIONS!!!

-

Tech1 day ago

Tech1 day agoGet Your ESP32 Sunny Side Up With This Solar Dev Board

-

Tech15 hours ago

Tech15 hours agoDark Secrets Emerge When Jailbreaking LLMs

-

News Videos6 days ago

News Videos6 days agoCrypto Just Entered Its Most Important 6-Month Candle (Could Decide Everything!)

-

NewsBeat6 days ago

NewsBeat6 days agoMajor update after Huntingdon train attack as man enters plea

-

News Videos2 days ago

News Videos2 days agohow to make coin bank box with cardboard #scienceproject #money #diy #shorts

-

Sports7 days ago

Sports7 days ago39-year-old Djokovic wins five-hour thriller to enter Wimbledon semis | Other Sports News

-

Tech6 days ago

Tech6 days agoLevel Infinite Launches Gangstar Mirage City in India with Pre-Registrations

-

Tech2 days ago

Tech2 days agoCloudflare Precursor Watches Your Mouse and Keyboard To Decide If You Are Human

-

Tech6 days ago

Tech6 days agoEntra passkey enrollment vishing targets Microsoft 365 users

-

Crypto World6 days ago

Crypto World6 days agoDeFi Dashboard Zapper to Shut Down After 7 Years

-

Crypto World6 days ago

Crypto World6 days agoMark Cuban-Backed DeFi Dashboard Zapper Shuts Down After 7 Years

-

Tech6 days ago

Tech6 days agoClaude’s New Reflect Dashboard Wants To Help You Log Off Of Claude

-

Crypto World7 days ago

Crypto World7 days agoFed minutes June 2026: officials split on rates

-

Tech6 days ago

Tech6 days agoHackers can use 9 of the most popular AI tools to assemble massive botnets

You must be logged in to post a comment Login