Business

3,000 sockets for West Northants

The humble lamp post is about to start paying its way. West Northamptonshire is to host one of the UK’s largest local on-street electric vehicle charging programmes, with more than 3,000 sockets, most of them fitted to existing lamp columns, due to start appearing on residential streets from mid 2026.

West Northamptonshire Council has appointed operator Char.gy to lead the rollout following a competitive procurement process. The programme is funded through the Government’s Local Electric Vehicle Infrastructure (LEVI) Fund and backed by substantial private investment, with competitive user tariffs promised.

The target market is clear: residents who rely on on-street parking and have no way of charging at home. That group includes a sizeable slice of the small business community, from sole traders running a van off the kerb to employees weighing up whether an electric company car is practical without a driveway.

For SME owners, charging access is often the deciding factor in whether electrifying a vehicle, or a whole fleet, stacks up. The rollout also lands amid a wider policy shift towards kerbside infrastructure, after ministers redirected £400 million towards on-street chargers in underserved areas, and as workplace charging becomes a benefit employees increasingly expect.

Aviation, Maritime and Decarbonisation Minister Keir Mather said: “Drivers in West Northamptonshire will soon have thousands more reasons to go electric, with over 3,000 new public charge points rolling out thanks to £2.85m of government funding.

“We know charging availability is one of the biggest barriers to switching, which is why we’re tackling it head on with over £600 million to rapidly expand the UK’s charging network so drivers can charge at home or on the go with confidence, wherever they are.”

The lamp column approach is the quietly clever part. By bolting chargers to existing council and parish infrastructure, the programme avoids the cost and disruption of digging up pavements, an approach the council says will keep the rollout cost-effective while supporting the area’s long-term sustainability ambitions.

Locations were selected through an evidence-based process prioritising residents without off-street parking, alongside sites suggested by residents themselves. Parish councils are being consulted to ensure the network is fair, accessible and sustainable.

Cllr Nigel Stansfield, Cabinet Member for Environment, Recycling and Waste at WNC, said: “This is a transformative investment in our area’s future. By delivering thousands of accessible, convenient and fairly priced on-street charging points, we are making it easier for residents to choose cleaner travel and invest in electric vehicles if they choose to.

“Working with Char.gy allows us to scale up quickly using existing infrastructure and ensure our communities are well-prepared for the increasing demand for electric vehicles.”

John Lewis, Char.gy’s chief executive, said the scheme would “make a real difference to people across West Northamptonshire who don’t have driveways or home chargers. By using lamp columns on residential streets, the Council is bringing charging closer to where people live, without major disruption to neighbourhoods.”

One caveat for those doing the sums: public charging still attracts 20 per cent VAT against 5 per cent for home charging, a gap currently the subject of a legal battle between HMRC and charge point operators that could yet reshape the economics of kerbside charging.

Residents and local businesses will be kept updated on installation timelines and site locations through WNC’s dedicated webpages and Char.gy’s website.

Jamie Young

Jamie Young is Senior Reporter at Business Matters, covering SME finance, employment law and Westminster policy since 2016. He has reported on every Budget and Autumn Statement since 2018, helped make sense of the ‘covid era’ and the bounce-back loan scheme from launch through the fraud investigations, and broke the magazine’s coverage of the 2024 late-payment reforms. He joined Business Matters straight from completing his BA in Administration from Exeter University and is NCTJ-qualified. Reach him at jyoung@cbmeg.co.uk

Watt recently apologised to staff and investors for the “many mistakes” made in the management of the company, admitting that it tried to diversify too quickly.

Brewdog’s brash marketing style had regularly sparked controversy, but the firm also faced criticism for its treatment of investors and staff.

A 2022 a BBC Disclosure investigation uncovered claims of inappropriate behaviour by Watt towards female staff, and revealed that Brewdog violated import laws and fabricated many of its marketing stories.

In 2024, the firm faced a backlash after revealing it would no longer hire new staff on the real living wage, instead paying the lower legal minimum wage.

Watt denied any wrongdoing alleged in the film and threatened to sue the BBC. He later said he sometimes missed social cues because he has autism.

A complaint to broadcasting regulator Ofcom was rejected.

Brewdog said it was putting in a range of measures to improve workplace culture following the release of the programme.

Tilray and Second Best have been asked to comment on Watt’s letter.

Employers will have to publish salary information in job adverts under government plans to rewrite anti-discrimination laws.

Details of other job conditions could also have to be disclosed to candidates, under the draft proposals.

Ministers argue greater transparency will help people navigate the jobs market and could prevent future pay discrimination claims.

However, details of exactly what salary information will have to be shared are yet to be hammered out.

Officials plan to consult on whether exact salaries will have to be displayed, or potentially a pay range or “benchmark rate” for open roles.

They also plan to ask industry groups whether information beyond basic salary, such as bonuses, should be made available.

Employers that do not publish a job advert for a role would have to give candidates the information in writing prior to a job interview.

In a policy document, the Cabinet Office said salary information would help jobseekers make informed application decisions, and improve the hiring process for companies by weeding out candidates with “misaligned pay expectations”.

Citing various academic studies, it also said transparency would help prevent “unequal outcomes” when salaries are offered to successful applicants.

“When pay is opaque, salary decisions can be influenced by stereotypes – such as stereotypes of women, ethnic minorities, or disabled people,” it added.

Business

JP Morgan moving closer to a milestone no bank has ever reached: A $1 trillion market value

It would also show how far the bank has pulled ahead of its rivals under CEO Jamie Dimon, who has led the lender for nearly two decades.

Record profit lifts shares

JPMorgan shares touched a record high on Tuesday after the bank reported a strong quarterly performance. The lender posted the highest profit ever by a US bank, helped by strength across its businesses.JPMorgan has a larger balance sheet than most peers and has built leadership across investment banking, consumer banking, credit cards, trading and lending. That gives it more ways to benefit when markets improve and when consumer activity remains steady.

The latest boost has come from Wall Street dealmaking. Investment banking activity has picked up as companies return to mergers, acquisitions and capital market transactions. If deal volumes stay strong through the rest of 2026, JPMorgan could see further gains in fees and earnings.CFO Jeremy Barnum said the bank’s investment banking pipeline was robust, adding that current activity levels were encouraging more activity.

Also Read: ‘We faltered, did not move quickly:’ How IBM CEO Arvind Krishna’s statement led to $70 billion wipeout

Jamie Dimon premium

JPMorgan’s rise has also been tied closely to Dimon. Investors have long assigned what is often called a “Jamie premium” to the stock, reflecting confidence in his leadership, risk control and ability to steer the bank through crises.

Dimon took charge before the global financial crisis and helped JPMorgan emerge stronger than many rivals. The bank has since used its size, capital strength and brand to gain market share.

The board has stepped up succession planning in recent years, but Dimon’s influence remains a major part of the stock’s appeal. Investors continue to see JPMorgan as the best-run large US bank.

Valuation test for investors

At around $940 billion in market value, JPMorgan is already far ahead of other global banks. But getting to $1 trillion will also raise expectations.

The stock trades at 14.63 times expected earnings over the next 12 months, compared with 13.58 times for the S&P 500 banks index, according to Reuters.

For years, trillion-dollar valuations were mostly reserved for technology companies. JPMorgan’s push toward that level shows how dominant the bank has become in global finance.

(Disclaimer: Recommendations, suggestions, views and opinions given by the experts are their own. These do not represent the views of Economic Times)

ArtMarie/E+ via Getty Images

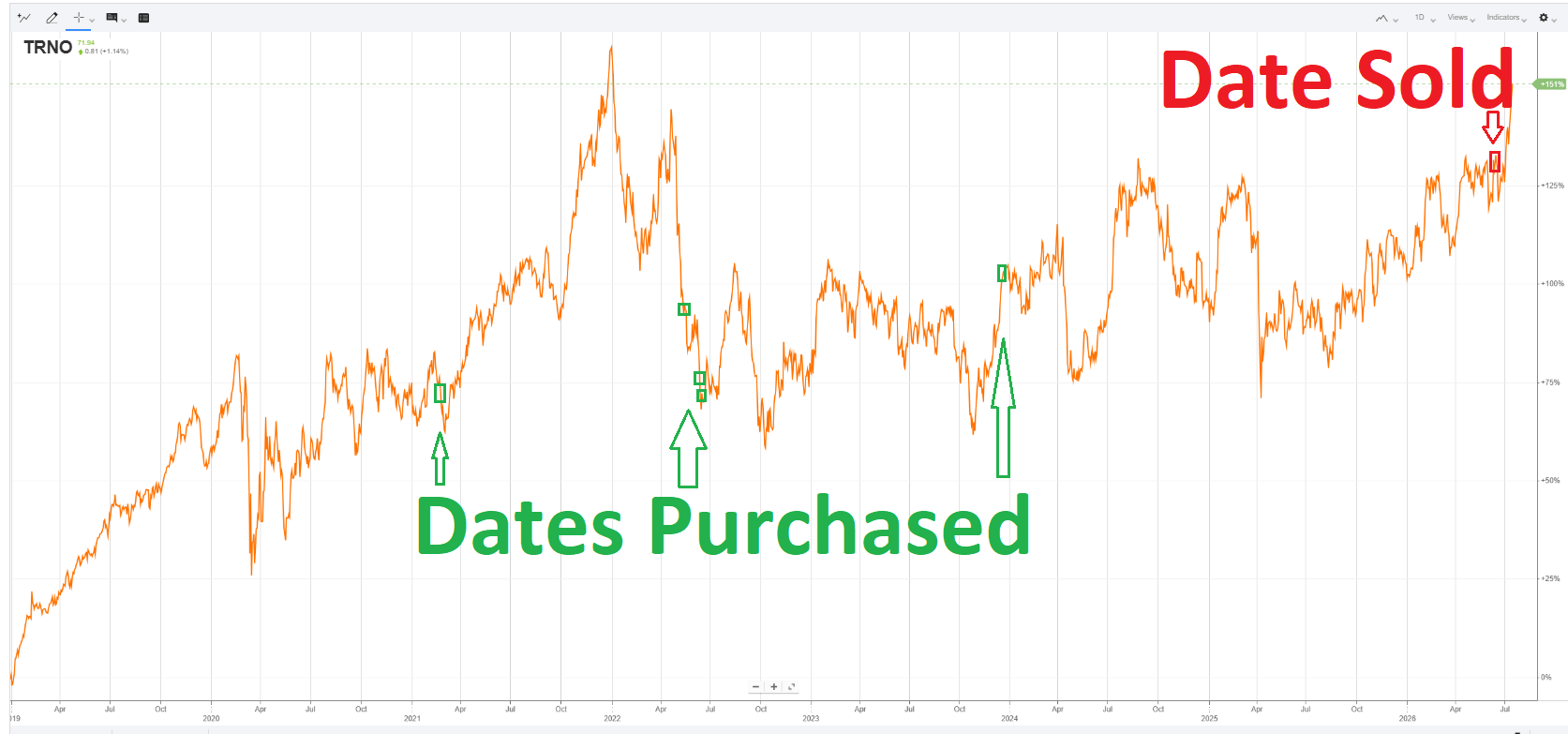

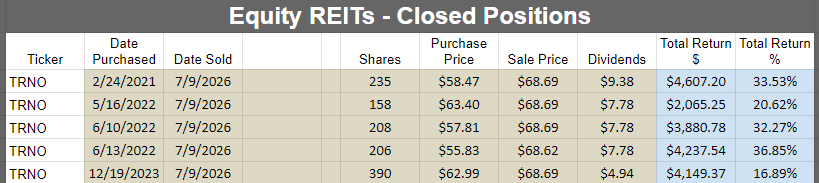

We recently closed out of our position in Terreno (TRNO) and wanted to walk readers through our thought process and how we look at the company today.

The REIT Forum

We sold shares on 7/9/2026. For readers interested, we will post all the sales at the end of the article.

Seeking Alpha

Before we sold, Terreno was flirting with the border between our neutral/overpriced ranges. Shares were trading at 31.4x consensus forward AFFO. Technically, it’s probably a little bit lower if we factor in that Q2 2027 AFFO per share will probably be higher than Q2 2026 AFFO per share. However, even adjusting for higher AFFO, the multiple would still be very large.

July 9th Thought Process

Terreno has been one of my favorite REITs for several years. I viewed it as a great long-term position. However, I am looking at shares trading over 30x forward AFFO while the 2-year Treasury is over 4% (4.16% presently), the 10-year is at 4.535%, and the 30-year is at 5.054%. I’m feeling a bit skeptical about multiples around 30x AFFO (or higher) in this environment. If we assume that REITs with more “normal” growth levels typically trade around 14x to 20x AFFO, then we have to assume several years of strong growth. While that’s certainly possible, I wouldn’t want to use it as the base scenario.

AFFO Estimates And Multiple

Our sheets are currently using a forward estimate of $2.19.

If we were to use AFFO estimates for the next 4 quarters starting with Q3 2026, then the consensus estimate would increase to $2.25. That’s better, but not substantially better.

Even if we use the $2.25 value, at $68.68 shares would be trading a hair over 30.5x forward AFFO estimates.

If we use $2.18 or $2.19, the multiple is 31.36x or 31.50x, respectively.

That’s a pretty high multiple given the Treasury yields. While I still really like TRNO, I felt it was prudent to harvest gains here.

The REIT Forum

Note: TRNO has rallied even higher since we closed our position. As of 7/15/2026, shares are at $72.09.

Why TRNO Can Achieve A High Multiple

Our thesis played out well with the industrial real estate portfolio delivering strong growth in same property NOI (Net Operating Income). That drove significant growth in AFFO per share, which supports TRNO trading at pretty high multiples of AFFO per share. The market likes seeing strong growth across several key indicators. However, the valuation still hit a point where I felt it was prudent to just take the gains.

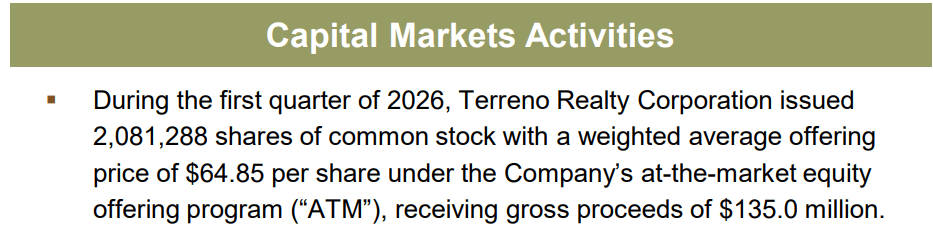

Issuing Shares

TRNO was issuing equity during Q1 2026:

TRNO

They felt it was reasonable to issue it at $64.85, and I agree with them. That was a very reasonable price for choosing to issue new equity. Issuing at $68.68 (5.9% higher) would make even more sense. That’s the right choice for management as they look to maximize value for shareholders.

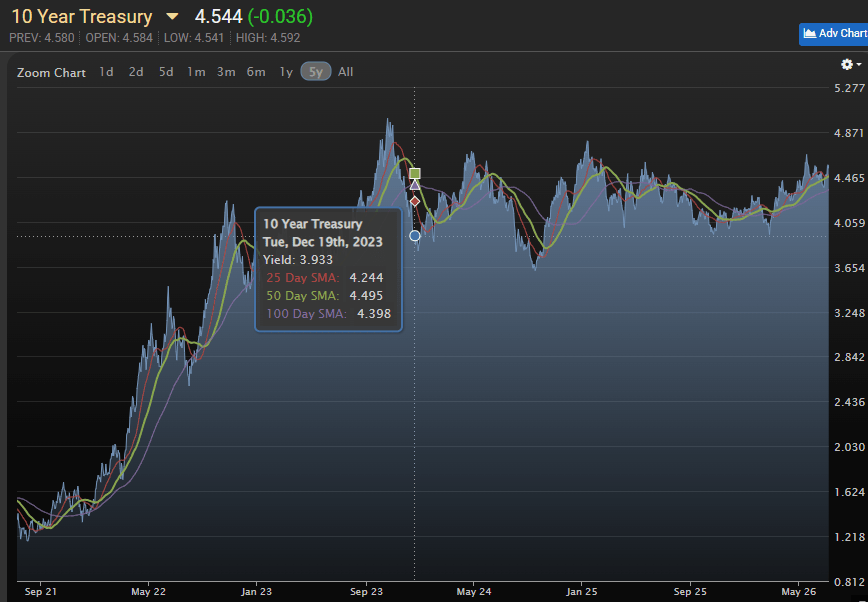

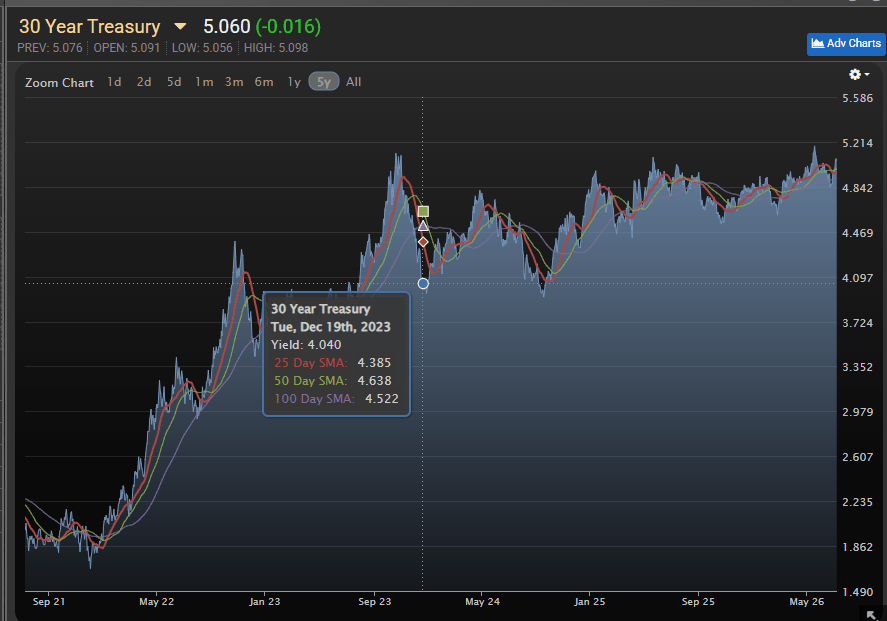

Impact Of Treasury Rates

The last time I purchased TRNO was in 2023 at $62.99. That’s not dramatically lower than the current price. The AFFO multiple was similar. What changed?

Well, the interest rate scenario changed quite a bit as shown by the 10-year and 30-year Treasury rates:

MBSLive

MBSLive

The 10-year Treasury yield is up 60 basis points (that means 0.60%) and currently trending higher (based on the current yield relative to the moving averages). The 30-year is up just over 100 basis points and also in a trend higher.

That feels ugly. It’s been less of an issue for TRNO since they have such little debt on their balance sheet. Consequently, they have been less exposed to interest rate pressure than most equity REITs. However, it makes it harder to justify high multiples.

Adjusted EBITDA/Total Enterprise Value

Doing a full model for “Market Implied Cap Rate” is pretty slow. In theory it seems like it would be quick to update, but in practice it can get messy doing quarter after quarter.

A simpler method is calculating adjusted EBITDA to Total Enterprise Value. It is less precise (which is negative), but it factors in overhead (which is positive).

Often there won’t be preferred stock or minority interest, which makes it even simpler.

The bigger question is simply which version of EBITDA we want to use. Do we use the most recent quarter? Do we try to run a forward estimate? Sometimes the answers matter a great deal, and sometimes they don’t. In this case, the picture is pretty clear regardless. One adjustment I really like to make, though, is to revise “adjusted EBITDA” by deducting stock-based compensation. That’s fundamentally overhead by another name.

Goal Of Calculation

This is a way to approximate the amount of adjusted EBITDA the company is producing relative to the total value assigned to the company.

It can be a quick way to compare REITs. However, investors should be aware that all REITS do not simply deserve to trade at the same valuation. That would be silly. Some properties are simply more desirable, and some management teams are superior. For now I’m simply going to refer to adjusted EBITDA minus stock-based compensation as “revised EBITDA.” I wanted to compare TRNO with Rexford (REXR).

Using Q1 2026, I came to the following estimates when removing stock-based compensation:

-

TRNO at $68.62 has a revised EBITDA yield of 3.96%. This is why it makes sense for TRNO to issue shares.

-

REXR at $34.42 has a revised EBITDA yield of 6.12%. This is why it makes sense for REXR to repurchase shares.

Note: We don’t want to use growth rates in adjusted EBITDA or revised EBITDA unless we control for the expected change in the shares outstanding and net debt outstanding.

That’s the gap in valuation. It is very material.

Hypothetically, what if REXR climbed all the way to our “overpriced” level? The revised EBITDA yield would drop from 6.12% to 4.79%.

Final Thoughts

I expect that TRNO will do a better job (than REXR) of growing every metric over the next year or two. However, I don’t expect it to be remotely large enough to offset the enormous gap in these valuation metrics.

We currently view TRNO as overpriced despite the company’s strong execution. Even after our sale, shares continued climbing. We’ll continue watching the company closely because it’s still one of my favorite REITs. I simply don’t like today’s valuation. Here is the record of our sale:

The REIT Forum

OpenTheBooks CEO John Hart joins Varney & Co. to discuss long-term Social Security and Medicare deficits as fiscal pressures mount.

Social Security beneficiaries are expected to see a larger cost-of-living adjustment (COLA) in 2027 amid persistently high inflation this year, a new report finds.

An analysis by The Senior Citizens League (TSCL) predicts that the 2027 COLA will be 3.8%, or 1 percentage point higher than the 2026 COLA of 2.8%, based on the latest consumer price index (CPI) inflation data released on Tuesday. TSCL estimated that if the projected 3.8% COLA took effect today, average benefits would rise by $73.62 from $1,937.53 to $2,011.15.

The estimate of a 3.8% COLA was the same as last month’s prediction, and is down slightly from the 3.9% projection made in April.

By law, the annual Social Security COLA is calculated using the Bureau of Labor Statistics’ CPI inflation data for the months of July, August and September. The announcement of the final COLA amount typically occurs in mid-October with the agency’s release of September inflation data.

Social Security benefits could rise 3.8% in 2027, according to the latest estimate of next year’s COLA. (Getty Images/iStock)

“We’re seeing inflation on the rise when more than half of seniors already can’t afford basic living standards,” said TSCL Executive Director Shannon Benton after the release of the group’s June estimate that also projected a 3.8% COLA for 2027.

“We’re talking about food, a roof over their head, and transportation. Many seniors already have to skip doctor’s appointments due to costs, which costs all of us more in the long run when we swap preventative care for emergency care,” she added.

SOCIAL SECURITY HAS LESS THAN 10 YEARS BEFORE RESERVES ARE EXHAUSTED, NEW TRUSTEES REPORT WARNS

Social Security COLA aims to keep benefits on pace with inflation. (Wesley Lapointe/For The Washington Post via Getty Images)

The latest CPI inflation data showed prices were up 3.5% from a year ago in June, a level that’s well above the Federal Reserve’s 2% target and creates significant pressure on household budgets as wage gains may not keep up with the rising cost of living.

The CPI-W, which is the version of the inflation metric used in calculating Social Security’s COLA, was up 3.5% from a year ago in June.

A larger COLA would also exacerbate the financial issues facing Social Security, which is on a path that would result in the insolvency of a key trust fund that could in turn cause benefit cuts.

AMERICANS RETHINK SOCIAL SECURITY TIMING AS LONGER LIFESPANS AND INSOLVENCY FEARS RAISE THE STAKES

Social Security’s key trust fund is facing depletion in 2032, which would prompt automatic benefit cuts if Congress doesn’t act. (Getty Images/stock)

The nonpartisan Committee for a Responsible Federal Budget (CRFB) estimated in May that a 3.8% COLA in 2027 would worsen Social Security’s fiscal shortfall by about $300 billion over the next decade and advance the insolvency of a key trust fund by three months from late 2032.

Once the trust fund is depleted, the Social Security Administration will be required by law to cut benefits to match incoming payroll tax revenues, which CRFB estimates will result in a 25% cut for beneficiaries that would “erase almost a decade’s worth of COLA increases.”

Verizon: Executing Amid Industry Uncertainty, Raising My Target

Oakmark Select Fund Q2 2026 Commentary

Britain’s biggest companies are getting quicker at paying their bills. New official statistics show the time large businesses take to pay their suppliers has fallen, and the proportion of invoices paid late dropped to 15 per cent in 2025, down from 25 per cent when records began in 2018.

For the small firms that sit at the bottom of long supply chains, the numbers represent rare good news on an issue that has dogged the sector for decades. Late payments cost the economy £11 billion every year and result in thousands of business closures, with the immediate impact falling on owners’ ability to pay staff, cover costs and invest in growth.

The figures, published by the Government this week, draw on data reported under the Reporting on Payment Practices and Performance Regulations 2017, which require large UK businesses to disclose their payment practices, policies and performance twice a year. The information is publicly available, meaning any small supplier can check a prospective customer’s payment record before signing a contract.

The picture is not uniform. London has consistently recorded the shortest payment times and among the lowest proportions of invoices paid late of any region or nation. Manufacturing, by contrast, has consistently reported the longest payment times and the highest proportions of late invoices of any sector, a sore point for the thousands of SMEs supplying parts and services into industrial supply chains.

The improvement comes as the Government’s Commercial Payments (Late Payments) Bill makes its way through Parliament, promising the toughest payment regime in the G7 and the most significant reforms to payment practices in more than 25 years. Business Secretary Peter Kyle has already vowed the legislation will not be watered down in the face of corporate lobbying.

Emma Jones, the Small Business Commissioner, who marked her first year in the role last month, said the figures showed businesses deserved credit for changing their behaviour, but that the job was far from finished.

“Small firms tell me, and our research has shown, that they spend too many precious hours chasing debt. This is limiting capacity to focus on growth, and we want to change that. These figures show that businesses have made a conscious effort to change and improve their payment practices and that should be recognised and celebrated. But the data also shows the need for improvement in key sectors for our economy. I therefore welcome the Commercial Payment Bill and the measures it will take to improve payment performance across the country.”

Her office also manages the Government’s Fair Payment Code, a tiered awards scheme designed to drive best practice and improve payment performance. Signatories include HSBC, Barclays, NatWest and Lloyds, alongside Heathrow Airport, AstraZeneca, Aviva, AXA, BT and Welsh Water.

The direction of travel is encouraging, though few business owners will be breaking out the bunting just yet. Even at 15 per cent, roughly one in every seven invoices sent to a large customer is still settled late, and UK firms logged record levels of overdue invoices last year, leaving SMEs more than £100 billion out of pocket. The test of the new regime, when it arrives, will be whether that stubborn final seventh can be shifted too.

Amy Ingham

Amy is a newly qualified journalist specialising in business journalism at Business Matters with responsibility for news content for what is now the UK’s largest print and online source of current business news.

London’s business community has given the Chancellor’s Mansion House speech a warm reception on paper and a stark warning in the small print: almost half of the capital’s firms believe the Government’s current approach will make economic growth worse, not better.

Rachel Reeves used her third Mansion House address on Tuesday evening to unveil a package aimed squarely at smaller firms, including a new UK Export Finance guarantee scheme to help small businesses start exporting and an expansion of the British Business Bank’s Growth Guarantee Scheme, more than doubling the SME lending it supports to £3.5 billion a year and increasing the number of businesses helped from 8,000 to 20,000. Lloyds, NatWest and Allica Bank have each committed £1 billion of SME lending over the next three years on the back of the changes.

For the London Chamber of Commerce and Industry, that is the right medicine. Whether it arrives in time, and survives a change of government, is another matter.

Karim Fatehi OBE, the LCCI’s chief executive, said the Chamber “welcomes measures to improve access to finance for businesses, encourage innovation and strengthen the UK’s position as a global financial centre – positive steps which recognise the vital role London’s business community and economy plays in driving growth in every postcode.”

But the underlying mood among members is far from buoyant. According to the LCCI’s latest survey data, 49 per cent of London businesses believe the Government’s current approach to the economy will worsen UK economic growth.

“The Chancellor was right to emphasise the importance of economic stability,” Fatehi said. “As the country prepares for a new government, maintaining business confidence is critical. The next government must provide early certainty businesses need to plan for the future.”

The focus on SME finance will resonate well beyond the capital. Many smaller firms have ambitious plans to invest and export but, as Fatehi put it, “continue to face significant barriers to securing finance”, a problem compounded by pandemic-era borrowing that has left the average small business debt load at double pre-Covid levels, hampering access to new finance.

The Chamber’s sharpest message, though, was reserved for whoever occupies Downing Street next. “The next government must avoid further increases to the cost of doing business,” Fatehi said, “giving firms the confidence that they will not face additional tax or regulatory burdens, and delivering meaningful business rates reform rather than further delay. Sustainable growth cannot be achieved if rising costs continue to undermine businesses’ ability to operate.”

That call lands on well-trodden ground. Reeves has long acknowledged the case for overhauling a system she admits leaves the economy feeling “stuck”, promising to remove the cliff edges in business rates that penalise small firms taking on a second site. Business groups argue delivery has yet to match the rhetoric.

On Europe, the LCCI backed the Chancellor’s push for deeper ties with the EU, with Fatehi arguing that “London’s internationally connected economy needs a pragmatic new relationship that reduces barriers to trade, improves labour mobility and makes it easier for businesses to operate across borders.” That echoes mounting evidence that post-Brexit trade friction is worsening for exporters, with smaller firms bearing the brunt.

Fatehi’s parting shot was aimed at day one of the next administration. “The priority for the next government must be turning ambition into action, using the policy levers at its disposal to get London growing,” he said. “A thriving capital is fundamental to the success of the UK economy, generating investment, jobs and prosperity across the country. It is essential the new government recognises this from day one.”

For SME owners, the takeaway is twofold. Cheaper, more available credit and export support are on the way. But with a new occupant of No 10 imminent, the price of that support, in tax, rates and regulation, remains anyone’s guess.

Amy Ingham

Amy is a newly qualified journalist specialising in business journalism at Business Matters with responsibility for news content for what is now the UK’s largest print and online source of current business news.

ClearBridge is a leading global asset manager committed to active management. Research-based stock selection guides our investment approach, with our strategies reflecting the highest-conviction ideas of our portfolio managers. We convey these ideas to investors on a frequent basis through investment commentaries and thought leadership and look forward to sharing the latest insights from our white papers, blog posts as well as videos and podcasts.

Stanford Study Examines Manipulation in Polymarket Bitcoin Contracts

When is the World Cup 2026 final? Date, kick-off time, location and venue

Salesforce’s Agentforce isn’t winning over clients, KeyBanc analysts claim

No Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

Renter of Home in Anne Heche Crash Denies Settlement With Son

Weekend Open Thread: Staud – Corporette.com

What is Cryptocurrency? Difference in Digital Currency and Cryptocurrency explained | Economy UPSC

Low Salary Build Wealth with These 3 Smart Money Habits | Financial Tips #shorts#youtubeshorts

Speak Proverbs Over Your Finances | Prayer For Financial Breakthrough and Provision | Morning Prayer

-

Fashion6 days ago

Fashion6 days agoLoro Piana Fall 2026 Enters Houston’s Art Scene

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Nutriplenish Leave-In Conditioner

-

Sports6 days ago

Sports6 days ago2026 Genesis Scottish Open Thursday TV coverage: Round 1

-

Sports6 days ago

Sports6 days agoSuper Eagles star Moses Simon opens up on Liverpool transfer regret

-

Tech6 days ago

Tech6 days agoCharacter.AI enters the microdrama arena with its own productions, but there’s a twist

-

Politics8 hours ago

Politics8 hours agoYoung campaigners urge incoming PM to act on outdoor junk food ads

-

News Videos1 day ago

News Videos1 day agoXRP BOMBSHELL… XRP OMBOARDED FOR TRANSACTIONS!!!

-

Tech2 days ago

Tech2 days agoGet Your ESP32 Sunny Side Up With This Solar Dev Board

-

Tech24 hours ago

Tech24 hours agoDark Secrets Emerge When Jailbreaking LLMs

-

News Videos7 days ago

News Videos7 days agoCrypto Just Entered Its Most Important 6-Month Candle (Could Decide Everything!)

-

Tech6 days ago

Tech6 days agoLevel Infinite Launches Gangstar Mirage City in India with Pre-Registrations

-

NewsBeat6 days ago

NewsBeat6 days agoMajor update after Huntingdon train attack as man enters plea

-

News Videos2 days ago

News Videos2 days agohow to make coin bank box with cardboard #scienceproject #money #diy #shorts

-

Tech2 days ago

Tech2 days agoCloudflare Precursor Watches Your Mouse and Keyboard To Decide If You Are Human

-

Entertainment3 hours ago

Entertainment3 hours agoDisney’s Most Ambitious Failed Star Wars Attraction Is Coming to SDCC

-

Tech7 days ago

Tech7 days agoEntra passkey enrollment vishing targets Microsoft 365 users

-

Crypto World7 days ago

Crypto World7 days agoDeFi Dashboard Zapper to Shut Down After 7 Years

-

Crypto World1 day ago

Ripple, Coinbase, Circle Join Linux x402 Foundation to Help Shape AI Payments

-

Entertainment2 hours ago

Entertainment2 hours agoVicki Gunvalson Defends Discussing Heather Dubrow’s Money

-

Crypto World7 days ago

Crypto World7 days agoMark Cuban-Backed DeFi Dashboard Zapper Shuts Down After 7 Years

You must be logged in to post a comment Login