Crypto World

Coinbase’s fastest product ever: prediction markets

Coinbase spent 2025 losing an argument about what it was. Trading volumes softened, the stock fell from $419.78 in July to the mid-$160s, and the market delivered its verdict on a company whose revenue still rose and fell with bitcoin: a leveraged bet on crypto activity, priced accordingly. Then in December it launched four new businesses at once, including one nobody had asked it for.

Summary

- Coinbase prediction markets reached $100 million in annualized revenue in under two months.

- The product’s early growth reflects Coinbase’s distribution advantage through existing funded accounts.

- Most prediction market volume is tied to sports, complicating the category’s information-market framing.

- State regulators are challenging sports-related event contracts as illegal gambling.

- The real test is whether volume holds after the World Cup and legal challenges progress.

By the first quarter of 2026, that one had passed $100 million in annualized revenue in under two months. Coinbase called prediction markets one of the fastest scaling products in its history, which is a striking claim from a company that once onboarded a country’s worth of retail traders in a single bull run. It sits in the same quarterly report as a $394.1 million net loss and revenue down to $1.43 billion from $2.03 billion a year earlier.

That juxtaposition is the whole story. Coinbase’s fastest growing product is not crypto. It is an event contract business that mostly trades sports, launched into a category that Kalshi and Polymarket have already scaled to volumes exceeding America’s legal sportsbooks, and that attorneys general in at least four states are currently arguing is illegal gambling.

What the $100 million number actually measures

Precision first, because the figure is doing rhetorical work that deserves inspection.The metric is annualized revenue, meaning a run rate extrapolated from a short period, not $100 million collected. The window was less than two months from a December 2025 launch. Coinbase disclosed the figure in its first quarter 2026 shareholder materials alongside the claim that retail derivatives annualized revenue exceeded $200 million and that derivatives volume over the trailing twelve months had grown 169% year over year. Every one of those numbers is a rate, and rates from launch windows measure enthusiasm as much as they measure business.

Against Coinbase’s own scale, $100 million annualized is roughly 7% of a single quarter’s total revenue projected across a year. It is not, on its own, a company changing number. What makes it interesting is the derivative: how fast the line rose, from zero, in a category the company entered late, against two incumbents with years of liquidity advantage. Growth that steep from a standing start is either a real demand signal or a launch spike with a decay curve, and the two look identical for exactly one quarter.

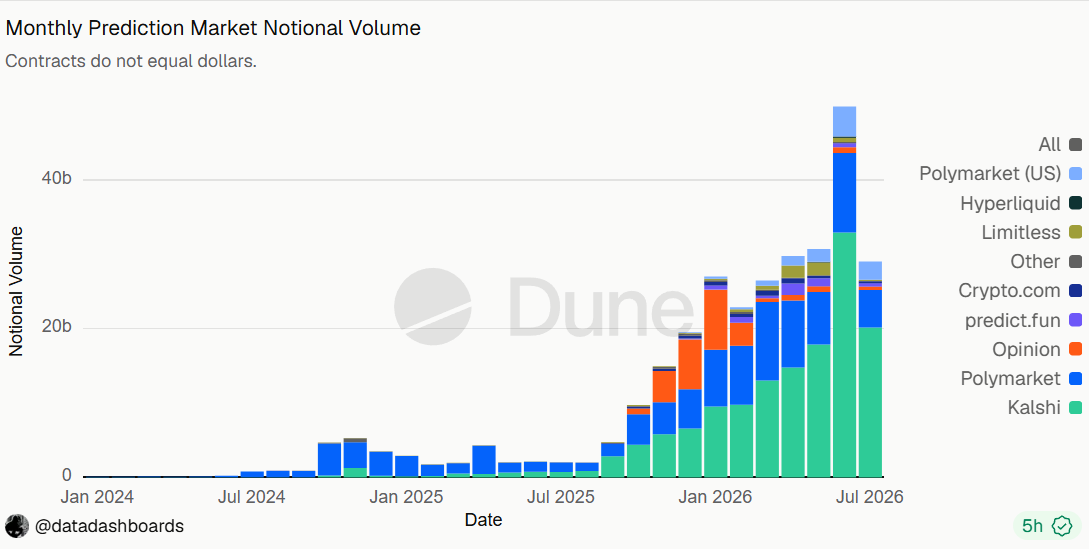

The context that makes the bullish reading credible is the sector data. Combined monthly trading volume across Kalshi and Polymarket rose from under $5 billion in September 2025 to roughly $24 billion by April 2026, according to a Pew Research analysis of figures from The Block. For scale, legal American sportsbooks handled around $14 billion a month on average across 2025. Prediction markets, a category that spent a decade as an academic curiosity and a regulatory orphan, now move more money monthly than the entire regulated sports betting industry that lobbied for a decade to exist.Coinbase did not create that demand. It arrived after the demand was proven and applied the one thing the incumbents lack: an existing base of funded accounts.

How the category got here

The speed of prediction markets’ arrival is easy to underrate, because the idea is old and the business is not.Event contracts existed for decades as academic instruments and offshore curiosities. Intrade, Augur, PredictIt: small, legally embattled, intellectually respected, commercially irrelevant. The turn came in October 2024, when a United States court ruled that Kalshi could legally offer election contracts, and the platform relaunched within hours, thirty two days before a presidential election. The press coverage that followed did what a decade of academic papers had not, and gave the category a proof of concept moment in front of a mass audience.

What followed was a distribution war instead of a product war. Kalshi launched sports contracts across all fifty states in January 2025. A March 2025 partnership put Kalshi’s markets in front of Robinhood’s twenty seven million funded brokerage accounts, and Super Bowl volumes alone exceeded $1 billion. Polymarket acquired QCEX, a CFTC registered contract market and clearing organization, creating a legal path back to American users. Google Finance began embedding live odds. Prediction market prices started appearing in mainstream news coverage as though they were data, which drove users back to the platforms, which deepened the markets, which made the prices better data.

By February 2026, geopolitics had taken over from crypto as the volume driver. A single contract on whether the United States would strike Iran attracted $73 million, the largest geopolitical market in Polymarket’s history, and the platform set a single day volume record of $425 million on February 28, surpassing its Election Day 2024 peak. The category had escaped its founding use case.

Coinbase launched in December 2025, roughly fourteen months after the court ruling that made the category viable and two months after ICE announced its Polymarket investment. That is late by crypto standards and early by any other. The company did not spot the trend. It waited for the trend to be proven and then applied the largest retail distribution base in American crypto to it, which is a different decision and arguably a better one.

Why it worked, and what that says about Coinbase

The mechanics of a prediction market are not the interesting part, and crypto.news has covered what a prediction market is and how event contracts settle in detail. The interesting part is distribution.

Kalshi and Polymarket had to acquire every user they have. Coinbase had millions of funded accounts already holding balances, already verified, already accustomed to a trading interface. Adding an event contracts tab to that base is not a product launch in any meaningful sense. It is a shelf placement. The company’s December expansion, which added stocks, commodity futures, perpetual futures, and prediction markets simultaneously, was an explicit bet that distribution beats product in retail finance, and the first quarter’s numbers say the bet is paying.

That thesis has a name inside the company, the Everything Exchange, and prediction markets are its proof of concept. Coinbase’s argument is that a user who trades bitcoin, equities, perpetual futures, and the World Cup through one login is worth vastly more than a user who trades only crypto, and is vastly harder to lose to a competitor. Analysts covering the stock have picked up the framing directly: Cantor Fitzgerald noted that investors increasingly view prediction markets as the next growth leg for platforms like Coinbase and Robinhood precisely because traditional crypto trading volumes are softening. The product is not a hedge against the crypto business. It is a hedge against crypto.

The acquisition tells the same story. In December, Coinbase agreed to buy The Clearing Company, a prediction markets startup founded that same year on a $15 million seed round, for an undisclosed sum. That is not a technology purchase. A company with Coinbase’s engineering base does not need a one year old startup to build binary contracts. It is a purchase of regulatory positioning and domain staff, which tells you what Coinbase thinks the scarce resource in this category actually is.

The thing nobody wants to say about the volume

Here is the part that complicates every bullish framing: this is mostly sports betting.Sports has accounted for roughly 80% of Kalshi’s total trading volume since July 2024, and in March 2026 the figure was closer to 87%. Sports, politics, and crypto together account for 91% of Kalshi’s global volume and 90% of Polymarket’s. The 2026 World Cup has been described by analysts as the largest gambling event in history, and the numbers support it: Kalshi cleared more than $30 billion in June volume, up over 70% from May’s $17.9 billion, running above $1 billion a day since the tournament opened on June 11. Polymarket set a record $10.8 billion in the same month. Sector wide daily volume rose roughly 75% from the tournament’s start. Open interest reached $1.8 billion by the end of June, a 54% monthly increase.

Look at Coinbase’s own prediction markets interface on any given day this month and the composition is unambiguous. World Cup outcomes clearing $16 million on a single match. Total points in a basketball game. LeBron James’s next team. What a reality television cast will say during a finale. Somewhere in the mix sit contracts on the Federal Reserve’s July decision and where bitcoin closes, the markets that justify the category’s intellectual case, and they are dwarfed by the ones that do not.

The information markets argument, that event contracts aggregate dispersed knowledge into a price that beats polls and pundits, is real and demonstrably useful. Prediction market odds on the CLARITY Act have become the industry’s most watched barometer of the bill’s fate, a dynamic crypto.news examined in its coverage of the Senate showdown, and Google Finance now embeds live Polymarket and Kalshi odds directly. That is genuine market infrastructure performing a genuine public function.

It is also roughly a tenth of the volume. The other nine tenths is people betting on football, and the honest description of Coinbase’s fastest growing product is that it is a sportsbook with better epistemics attached as a garnish.

The regulatory bill is already in the mail

Which is why the legal exposure is not a tail risk. It is the central case.On April 23, Wisconsin sued Kalshi, Polymarket, Robinhood, Crypto.com, and Coinbase over sports related event contracts, arguing they function as sports wagers and violate state gambling law, and seeking orders to stop them being offered in the state. New York and Illinois have opened their own fronts. Nevada’s gaming regulators sued Kalshi in February. Arizona’s attorney general filed in March. The industry’s federal position rests on the Commodity Exchange Act and a CFTC that withdrew proposed restrictions in January 2026 and issued Polymarket a no-action letter, which is a strong federal hand and precisely the kind of hand that invites a preemption fight rather than settling one.

The structural problem is that states run gambling. That authority is old, jealously guarded, and enormously lucrative, and the sector’s entire growth story consists of routing around it by calling a bet on a football match a commodity derivative. Regulators have already delayed event contract ETFs while they decide whether these products belong in retail fund wrappers at all. Kalshi has been penalizing congressional candidates for betting on their own races, which is exactly the sort of headline that writes state legislation.

Coinbase now sits as a named defendant in that fight, and it does so having just lost its chief legal officer: Paul Grewal, the architect of the company’s regulatory strategy through the SEC years, exited on the eve of the CLARITY endgame. The company entered the most legally contested growth category in American finance and changed the driver at the same moment.

What the incumbents’ numbers say about the ceiling

The most useful way to size Coinbase’s opportunity is to look at what the leaders have already built, because it frames both the prize and the problem.Kalshi’s disclosed figures are extraordinary for a company that was a niche regulated venue two years ago: $178 billion annualized volume, annualized revenue above $1.5 billion, institutional trading volume up 800% in six months, a $22 billion valuation on a $1 billion round led by Coatue. Polymarket carries an $8 billion valuation with the New York Stock Exchange’s parent company on the cap table. Neither is public, so neither faces quarterly scrutiny of whether the growth is durable, which is a structural advantage Coinbase does not have.

Those numbers cut two ways for Coinbase. On one hand they prove the category can support a real business at scale, which is the entire bull case: if Kalshi generates $1.5 billion annualized, a $100 million run rate from a standing start is a beginning, not a ceiling. On the other hand they describe exactly how far behind Coinbase is, and in venue businesses the gap tends to widen instead of closing. Liquidity is the product. The deepest book gets the largest orders, which deepens it further, and a $4,500 ticket that clears at a two cent spread on the leading venue moves the price six cents somewhere thinner. Traders do not choose venues for the interface.

The one asymmetry favoring Coinbase is that it does not need to win. Kalshi and Polymarket are prediction market companies whose valuations demand category dominance. Coinbase is a distribution company for which event contracts are one surface among several, and a permanent third place at a $300 million run rate would still be a good outcome against a product that cost almost nothing to launch. The strategic question is not whether Coinbase beats Kalshi. It is whether the surface stays legal and whether the flow stays after the tournament.

The case for Coinbase

Take the bull argument at full strength, because it is not weak.Diversification is working, measurably. Coinbase’s crypto trading volume market share hit an all time high of 8.6% in the first quarter while it simultaneously stood up four new business lines, which is not the behavior of a company losing its core. Retail derivatives passed $200 million annualized. Prediction markets passed $100 million. The company shipped eighteen products in six months, a pace Rosenblatt called impressive while assigning a $240 target, and Bernstein reiterated a Street high $330 on the strength of the platform thesis. Ark Invest bought $44 million of stock into the June selloff.

The regulatory position is also stronger than the headlines imply. Coinbase’s whole institutional identity is being the compliant venue, and it enters this category as a CFTC regulated participant with an acquired specialist team, not as a crypto native platform improvising legality. If the state challenges resolve into a federal framework, the winners are the operators with the cleanest regulatory posture, which is precisely the position Coinbase has spent a decade and hundreds of millions of dollars purchasing.

And the strategic logic is sound on its own terms. Prediction markets were the most funded category in crypto in the first half of 2026, drawing $1.85 billion of $7.1 billion across the top ten categories, ahead of exchanges at $1.57 billion and artificial intelligence at $1 billion. Venture capital is rarely early and rarely wrong about direction, only about timing. Intercontinental Exchange, the owner of the New York Stock Exchange, announced a strategic investment in Polymarket at an $8 billion valuation, with reported commitments ranging up to $2 billion. Kalshi raised $1 billion from Coatue at a $22 billion valuation on $178 billion of annualized volume and over $1.5 billion of annualized revenue. When the NYSE’s parent and a $22 billion private company are both in the category, calling it a fad requires arguing that the smartest capital in two industries is confused.

Sitting out was never an option that produced a better outcome than participating. A Coinbase that watched Kalshi build a $22 billion business adjacent to its own funded accounts, and did nothing, would be facing a harder set of questions this quarter than the ones it faces now.

The case against

Now the other side, which is mostly about what happens after the World Cup ends.The category’s growth curve has already broken once. Combined Kalshi and Polymarket lifetime volume crossed $150 billion in April, and the same month ended a seven month streak of monthly growth. Polymarket’s active traders fell from more than 733,000 in March to roughly 643,000 in April. The June record was not organic reacceleration. It was a global tournament that occurs every four years, and it concludes this month. A business whose volume rises 75% on a World Cup will discover what its baseline is in August, and there is no version of that discovery that flatters the annualized figures currently being quoted.

The competitive position is also weaker than the growth rate suggests. Coinbase is third at best in a category where liquidity compounds: Kalshi took roughly 80% of June volumes, Polymarket holds 97% of political markets and about half of non-sports open interest. Deeper books attract larger traders, which deepen the books. Coinbase brings distribution, and distribution wins customers, but it does not on its own win the flow that makes a venue the price. Meanwhile Kalshi and Polymarket are both pushing into perpetual futures, which is to say they are attacking Coinbase’s business while Coinbase attacks theirs, and Coinbase’s derivatives business is far more valuable than its event contracts business.

Then the numbers underneath. Coinbase lost $394.1 million in the first quarter. Revenue fell 30% year over year. The price to earnings ratio sits near 69, price to sales near 7.6, and Barclays maintains an Underweight with a $107 target on the argument that new products cannot offset muted crypto volumes. The stock is down 53% over twelve months and 31% year to date, and the Coinbase Premium, the spread between bitcoin’s price on Coinbase and Binance, has been negative for fifty consecutive days, the market’s plainest statement that American demand is not returning soon. Against a $1.43 billion quarter and a $394 million loss, $100 million annualized from event contracts does not close a gap. It decorates one. Even quadrupled, it would not return the company to profitability on its own, and quadrupling assumes the World Cup was a floor.

And the deepest objection is definitional. Coinbase’s mission statement concerns economic freedom and updating a century old financial system. Its fastest scaling product lets people bet on Love Island. There is no rule requiring a company’s growth engine to match its stated purpose, and plenty of firms have quietly funded their mission with something less noble. But a company arguing to Congress that digital assets deserve their own market structure, while deriving its best growth from event contracts that four state attorneys general call gambling, is carrying a contradiction that its opponents in that argument will not be too polite to name.

The bet underneath the bet

What Coinbase actually did in December was not diversify. It changed what business it is in, and the prediction markets number is the first evidence the change is real.For a decade the company was a bet on crypto adoption. Volumes up, revenue up; volumes down, revenue down; the stock traded as a levered proxy and everyone understood the deal. The Everything Exchange rejects that identity. It says Coinbase is a distribution business that happens to have been founded on crypto, that a funded account with a trading interface is the asset, and that whatever the account holder wants to trade is a detail. Stocks, commodity futures, perps, event contracts, and tokenized real world assets are not five strategies. They are one strategy with five surfaces.

Prediction markets validate that thesis harder than any of the others, because the company had no advantage there except distribution. No technology edge, no first mover position, no liquidity, no brand association with event contracts at all. It shipped a tab and cleared $100 million annualized in seven weeks. If distribution alone can do that in a category with entrenched incumbents, the thesis is not marketing.

One more thing the quarter proved, quietly. Coinbase shipped stocks, commodity futures, perps, and event contracts in a single month and none of them broke. For a company whose operational reputation was built entirely on custody and spot trading, executing a four product launch without an incident is a competence signal that no analyst target captures. The Everything Exchange was always plausible as a slide. The first quarter is the first evidence it is plausible as an engineering organization.

The unresolved question is whether the surface Coinbase chose to prove it on survives contact with American law. That is not a question the company can engineer its way out of, and it will be answered in courtrooms in Wisconsin, Nevada, and Arizona instead of in a shareholder letter. The fastest growing product in Coinbase’s history is also the one whose existence a growing list of state governments disputes, and the company is discovering, again, that being right about where the demand is has never been the same as being allowed to serve it.August will settle the first half of it. The World Cup ends, the volume normalizes, and the market finds out whether $100 million annualized was a business or a tournament. The courts will take longer.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Revenue figures cited are annualized run rates disclosed by Coinbase, not realized revenue. Sector volume, valuation, and market share data derive from third party sources including The Block, Pew Research Center, CryptoRank, and company disclosures, and some reported figures vary between sources. Litigation described is ongoing and no outcome should be inferred. Details reflect information current as of July 14, 2026, and are subject to change. Always do your own research.

U.S. inflation slowed more than expected in June, giving risk assets fresh support after months of pressure from rising energy costs.

Summary

- US inflation cooled to 3.5% in June, beating forecasts as falling energy prices drove relief.

- Bitcoin rebounded toward $65,000 after softer CPI reduced immediate pressure for tighter Federal Reserve policy.

- Core inflation eased to 2.6%, while renewed Middle East tensions keep future energy risks elevated.

The annual Consumer Price Index fell to 3.5% from 4.2% in May, marking its first decline in five months and coming below the 3.8% market forecast.

The U.S. Bureau of Labor Statistics reported that consumer prices fell 0.4% from May, the largest monthly decline since April 2020. Core inflation, which removes food and energy costs, eased to 2.6% annually from 2.9% and remained unchanged during June.

Falling energy prices drive inflation lower

Energy prices remained 15.7% higher than a year earlier, but that was well below the 23.5% increase recorded in May. Gasoline inflation slowed to 26.7% annually, while the broader energy index fell sharply during June as oil markets received temporary relief from easing U.S.-Iran tensions.

Gasoline prices fell 9.7% during the month, helping offset increases in food and shelter costs. Food prices rose 0.2% from May and 3% from a year earlier. Shelter costs increased 0.1% monthly and remained one of the main areas where prices continued moving higher.

The headline decline also came in much stronger than economists expected. Markets had forecast a 0.1% monthly fall, compared with the reported 0.4% drop. Core CPI also beat expectations for a 0.2% monthly increase and a 2.8% annual gain.

Bitcoin rebounds as inflation fears ease

Bitcoin moved higher following the softer inflation report. As reported, BTC climbed nearly 5% to an intraday high of about $64,830 before trading near $64,560. The move followed a decline below $62,000 as renewed tensions between the U.S. and Iran weighed on markets.

The softer CPI data reduced immediate concerns that persistent inflation could force the Federal Reserve into tighter monetary policy. U.S. stock futures also moved higher, Treasury yields declined and the dollar weakened following the release. Bitcoin joined the broader recovery in risk assets.

Before the report, crypto.news reported that Bitcoin was trading near $62,500 as investors weighed higher oil prices and the possibility of another inflation surprise. The June CPI reading removed part of that immediate concern, although energy markets remain a source of uncertainty.

Core CPI gives markets another positive signal

Core inflation falling to 2.6% gave investors another measure of easing price pressure. The reading remains above the Federal Reserve’s long-term 2% inflation goal, but its decline from 2.9% showed that the June slowdown was not limited entirely to energy.

The next U.S. CPI report, covering July, is scheduled for Aug. 12. Markets will watch whether lower inflation continues or whether renewed increases in oil and gasoline prices reverse part of June’s decline.

Energy risks remain despite softer June CPI

The inflation report reflects economic conditions during June, when a temporary easing in U.S.-Iran tensions helped lower energy prices. Since then, renewed hostilities have again raised concerns about oil supplies and future transportation costs.

That leaves Bitcoin and other risk assets exposed to both inflation data and geopolitical developments. June’s softer CPI has eased near-term inflation pressure and supported Bitcoin’s recovery, but the next direction will depend on whether energy prices stay contained and whether the broader decline in core inflation continues.

Stripe and private equity firm Advent International have reportedly submitted a joint offer to acquire PayPal for more than $53 billion.

Summary

- Stripe and Advent reportedly offered $60.50 per PayPal share, valuing the payments company above $53 billion.

- The proposed acquisition has $50 billion in bank financing, but PayPal has not responded publicly.

- A deal would combine PayPal’s PYUSD ecosystem with Stripe’s rapidly expanding global stablecoin payment infrastructure network.

The proposed deal would combine two major payments businesses as stablecoins and digital settlement become a larger part of the global financial sector.

Reuters reported that Stripe and Advent offered $60.50 for each PayPal share. The price represents a roughly 28% premium to PayPal’s Tuesday closing price. About $50 billion in bank financing has been committed to support the proposed transaction, according to people familiar with the discussions.

Stripe and Advent seek equal ownership of PayPal

Under the proposal, Stripe and Advent would each hold an equal stake in PayPal rather than dividing the company into separate businesses. The offer was reportedly submitted earlier in July after an initial approach in April.

PayPal, Stripe and Advent declined to comment on the reported talks. Reuters said PayPal had not responded to the latest proposal when the report was published. The sources also warned that there is “no certainty” that discussions will result in a completed transaction.

The reported $53 billion valuation comes after a sharp decline in PayPal’s market value from its 2021 peak. The company has faced stronger competition across checkout, digital wallets and alternative payment methods. New CEO Enrique Lores began restructuring the business after taking over in March.

PayPal is reorganizing around payments and crypto

PayPal reorganized its operations in April into three main units covering checkout, Venmo consumer financial services, and payments and crypto. The company reported first-quarter revenue of $8.35 billion, up 7%, while payment volume increased 8% on a currency-neutral basis to about $464 billion.

Its crypto business includes PayPal USD, or PYUSD, a dollar-backed stablecoin issued by Paxos. PayPal says the token is backed by dollar deposits, U.S. Treasuries and similar cash equivalents and can be exchanged for dollars through its platform.

As previously reported, PYUSD recently expanded natively to Polygon through the network’s Open Money Stack. The integration gives businesses access to stablecoin payments, settlements, fiat conversion and compliance infrastructure through one system.

Stripe has built its own stablecoin infrastructure

A takeover would also bring PayPal’s crypto payment products into a company that has invested heavily in stablecoin infrastructure. Stripe acquired Bridge, a stablecoin platform, in a deal valued at about $1.1 billion, expanding its ability to support digital dollar issuance and payments.

As reported by crypto.news, the Bridge transaction marked one of Stripe’s largest moves into crypto infrastructure. Stripe has since supported stablecoin payment projects across several major technology platforms and blockchain networks.

Stripe was valued at $159 billion in a February employee and shareholder tender offer. That valuation gives the privately held company a larger reported market value than PayPal under the current takeover proposal.

Potential deal arrives as payments companies seek scale

The reported bid comes during wider consolidation across global payments. Companies are seeking greater scale while expanding into cross-border transfers, business payments, artificial intelligence and blockchain settlement.

Stablecoins have become part of that shift. As previously reported, Stripe, PayPal, Visa, Mastercard and other payment companies have expanded their use of blockchain-based dollars for settlement and money transfers.

A completed takeover could place PayPal’s consumer payments network, Venmo and PYUSD alongside Stripe’s merchant infrastructure and stablecoin technology. However, the proposal remains preliminary. PayPal has not publicly accepted the offer, and the parties have not announced a formal acquisition agreement.

The reported bidders are seeking to move discussions forward before the end of July, according to the original report. Any agreement would still face detailed negotiations and likely regulatory review before completion.

Base network creator Jesse Pollak says he is stepping back from leading the Base App, after concluding that an earlier push toward social applications was a “wrong bet” for the Ethereum layer-2’s growth. In a post on X on Wednesday, Pollak argued that Base moved too slowly in areas that are now central to DeFi competition, including prediction markets and perpetual futures.

Pollak also said he will return leadership of the Base App to Coinbase, with Jordan Fish—better known on X as “Cobie”—taking over that role, while Pollak focuses on the Base blockchain itself.

Key takeaways

- Jesse Pollak said Base’s social-app strategy failed to deliver traction, and admitted the team made a “wrong bet.”

- Pollak cited Base’s lag behind competitors in scaled prediction markets and perpetual futures despite having offerings in both categories.

- Base App leadership is expected to shift back to Coinbase, with Cobie (Jordan Fish) resuming oversight of the product.

- The network’s current emphasis remains on finance-focused use cases such as trading, payments, tokenization, and AI agent tooling.

- Coinbase CEO Brian Armstrong recently acknowledged that “content coins” “didn’t work,” reinforcing the broader pivot away from social-first narratives.

From social to finance: Pollak’s rationale

Pollak’s comments provide a clearer explanation for the changes Base has been making earlier this year. Base initially positioned itself around social products, aiming to bring crypto to a wider audience through apps and creators. Pollak named examples of those early social thrusts, including Farcaster, Zora, and miniapps, reflecting a belief that engagement and content distribution could drive mainstream adoption.

However, Pollak said the market “disintegrated completely,” and that Base ended up behind in “key areas” that have become more important for users looking for financial utility. In his post, he pointed to Base’s decentralized derivatives presence—mentioning perps, with a nod to Avantis—and prediction markets, noting that both were “well behind scaled competitors.”

For investors and traders, the timing of this self-assessment matters: it signals a second attempt to align the chain’s product priorities with the demand that tends to concentrate liquidity, volume, and user retention in DeFi. Rather than doubling down on social distribution, Pollak frames the next phase around assets and trading-related infrastructure.

Leadership transition for the Base App

Beyond strategy, Pollak also addressed internal ownership. He said he will return leadership of the Base App to Coinbase, specifically under Jordan Fish (“Cobie”). At the same time, he said he will focus on the Base blockchain itself rather than the consumer-facing application layer.

That split highlights a common tension in L2 ecosystems: whether growth is best driven by consumer app ecosystems or by strengthening on-chain markets and standards that attract liquidity. By stepping back from the Base App, Pollak appears to be aligning resources more heavily toward the underlying chain and the financial primitives that developers can build on top of.

Coinbase’s earlier acknowledgment of “content coins”

Pollak’s post landed just days after Coinbase CEO Brian Armstrong said content coins “didn’t work.” Armstrong described it as a mistake that needed to be corrected, urging a shift in direction.

That acknowledgement aligns with Base’s earlier operational pivot. In February, Base sunset its Creator Rewards program and Farcaster-powered social feed as part of a move toward more tradable assets. Pollak had also previously characterized the Base App as an “imperfect Farcaster client,” underscoring that even when social-oriented features existed, they were not yet meeting the scale demanded by the market.

The Creator Rewards effort, launched in July 2025, was intended to turn engagement into rewards—making the network’s social activity economically meaningful. Pollak’s latest comments suggest that the rewards model did not overcome the broader competitive advantages held by chains and apps with more established financial depth.

What Base is building now: stablecoins, AI agents, and token standards

While Pollak criticized the earlier social emphasis, Base’s recent technical direction remains focused on tokenization and AI tooling—areas that can support both DeFi and new forms of user interaction.

Last week, Base activated its B20 token standard on mainnet, according to coverage earlier this month. The B20 framework introduces a native approach designed to support stablecoins, tokenized real-world assets (RWAs), and other fungible tokens.

In May, Base launched Base MCP (Model Context Protocol). The tool is intended to let users manage crypto directly from an AI model’s chat interface, and to interact with crypto protocols through the same interface, including Morpho, Moonwell, Uniswap, Aerodrome, Avantis, Bankr, and Virtuals. The practical implication is that AI agents may become a more natural interface layer over existing DeFi functionality, lowering the friction between user intent and on-chain execution.

Base has also said it is upgrading core systems ahead of an “AI agent economy” as part of a 2026 roadmap. In that context, Base highlighted RWA tokenization, stablecoins, and prediction markets as key growth areas—precisely the categories Pollak now says Base must compete in more effectively.

In his Wednesday post, Pollak said the goal is to position Base as a blockchain for global finance, aiming to be the place where the world’s money settles over the next century. While that statement is aspirational, it clarifies the narrative shift: the network is attempting to anchor itself in financial infrastructure rather than primarily in creator-led engagement.

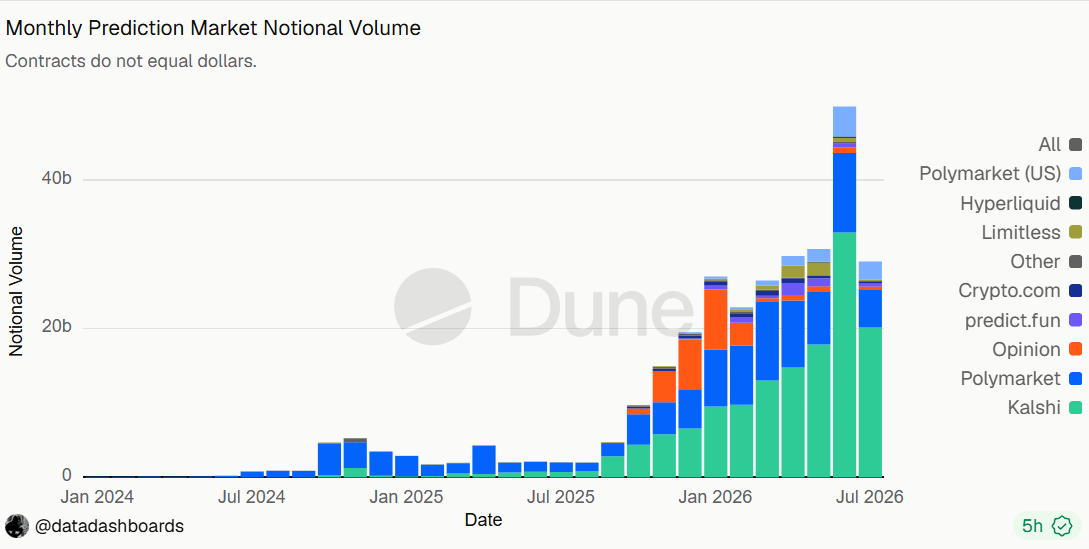

In parallel with the emphasis on trading and markets, the article noted that Limitless Exchange’s monthly notional volume is only a fraction of larger competitors, citing Dune Analytics. That kind of gap helps explain why Pollak pointed to derivatives and prediction markets as areas requiring faster scaling: if volume and notional activity remain comparatively small, users and liquidity providers have less incentive to route activity through the L2.

Why the pivot could matter next

Base’s latest moves may be best understood as a reallocation of attention toward where DeFi demand is already proven—liquidity, tradability, and execution. What remains uncertain is how quickly Base can close the scale gap in prediction markets and perpetual futures, and whether the B20 token standard and AI agent tooling will translate into measurable user activity rather than just product launches. Readers should watch for evidence of rising volume, broader adoption of stablecoin and RWA tooling, and whether Base App product changes under Cobie translate into renewed momentum.

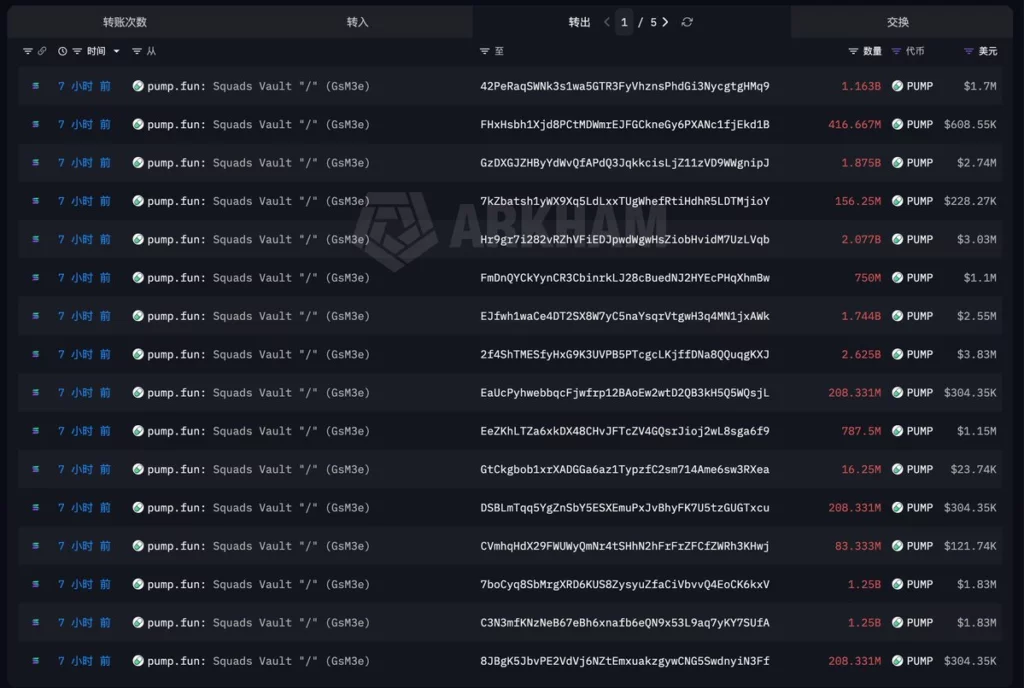

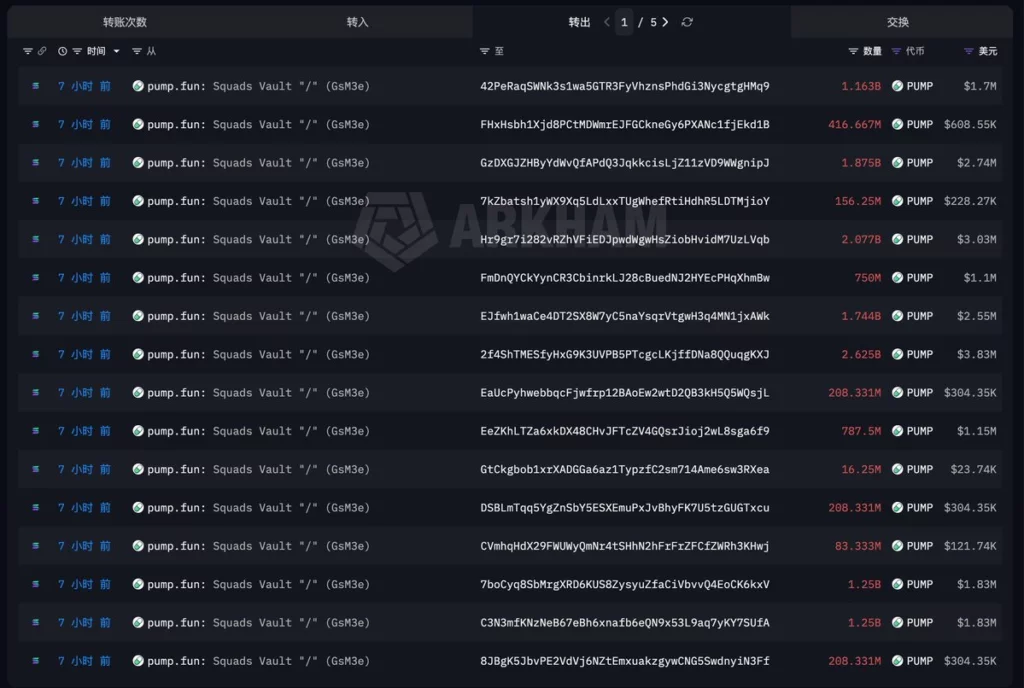

Pump.fun has completed its first major team and investor token distribution after a one-year lockup ended.

Summary

- Pump.fun unlocked 57.279 billion PUMP tokens worth $86.49 million across 121 team and investor wallets.

- The first distribution follows a one-year lockup and begins a three-year vesting cycle for insiders.

- Unlocked tokens became transferable, but on-chain movements do not confirm recipients sold them into markets.

On-chain tracking showed 57.279 billion PUMP tokens, valued at about $86.49 million at the time of the transfers, moving to 121 wallets on July 15.

Wu Blockchain reported that the transfers marked the start of a three-year vesting period for team and investor allocations. The event makes a large amount of previously locked PUMP transferable, although wallet distributions alone do not show whether recipients intend to sell.

Source: EmberCN

Pump.fun distributes 57.279 billion PUMP

On-chain analyst Yu Jin tracked two large sources behind the distribution. One address released 52.039 billion PUMP worth about $78.58 million, while another released 5.24 billion tokens valued at approximately $7.91 million. The tokens then moved across 121 wallets.

The first distribution represents about 14% of PUMP’s current circulating supply of roughly 400 billion tokens. CoinGecko showed PUMP trading around $0.0016 after the unlock, with the token still recording a double-digit 24-hour gain when checked. The price action shows that an unlock does not automatically result in immediate selling.

Three-year vesting period begins after one-year lockup

The distribution comes one year after Pump.fun launched PUMP through a major token sale. As previously reported, the project’s original token allocation reserved 20% of supply for the team and 13% for existing investors.

The latest on-chain data indicates that those allocations have now entered their three-year release period after the initial one-year lockup. The full amount will not necessarily enter circulation at once. Vesting schedules typically release tokens in stages, while the recipients decide whether to hold, transfer or sell their unlocked assets.

Actual distribution follows closely watched PUMP unlock

The event had been on traders’ calendars before the first transfers appeared. As previously reported, scheduled data had pointed to an 82.5 billion PUMP unlock worth about $130 million around the end of the initial cliff. The first observed team and investor distribution instead moved 57.279 billion tokens across 121 wallets.

The difference shows why scheduled unlock figures and on-chain token movements may not always match on a specific day. Unlock calendars track when tokens become eligible for release, while blockchain transfers show when assets actually move between addresses. Further distributions may therefore remain possible during the wider vesting cycle.

PUMP supply pressure meets strong market activity

The unlock adds new potential supply at a time when PUMP continues to see active trading. CoinGecko recorded more than $100 million in 24-hour volume when checked, with the token’s market capitalization near $650 million and around 400 billion tokens listed as circulating.

Pump.fun has also used token buybacks to reduce available supply. Earlier crypto.news coverage tracked the program after it began buying PUMP from the market in 2025. The latest unlock creates the opposite supply force by making previously restricted team and investor allocations transferable.

The key question for the market is how recipients handle the newly available tokens. Distribution to 121 wallets does not prove that 57.279 billion PUMP has entered exchanges or been sold. Further wallet movements and exchange deposits would provide clearer evidence of whether the unlock is creating direct selling pressure.

With the one-year lockup now over, PUMP has entered a longer period of scheduled team and investor vesting. Traders will now watch subsequent distributions, exchange inflows and trading volume as more allocated tokens become available over the next three years.

TeraWulf shares have dropped more than 7% after New York ordered a one-year pause on new environmental permits for large-scale data centers.

Summary

- TeraWulf shares fell more than 7% after New York paused new environmental permits for large data centers.

- The company said its Lake Mariner and Lake Hawkeye projects are not affected by the governor’s executive order.

- TeraWulf continues expanding its AI business after signing a 20 year Anthropic lease expected to generate about $19 billion in contracted revenue.

According to an executive order signed by New York Governor Kathy Hochul on Tuesday, the state will temporarily stop issuing new environmental permits for certain large data center projects while regulators prepare a statewide framework to assess their environmental impact.

The order gives the Department of Public Service up to one year to complete a Generic Environmental Impact Statement, which will establish standards for future data center developments. The governor’s office said the review will examine electricity demand, water use and quality, and air quality before the moratorium is lifted.

Alongside the executive order, Hochul said she is also pursuing legislation to remove sales tax exemptions currently available to large data centers across New York.

Investors reacted quickly to the announcement. TeraWulf’s Nasdaq-listed shares closed down 7.08% at $19.41 on Tuesday.

Despite the market reaction, TeraWulf said the order does not affect its existing operations or development timeline in the state.

Paul Prager, TeraWulf’s founder and chief executive officer, echoed that view in a post on X, saying the company is evaluating on-site power generation for the Lake Hawkeye project, which he said aligns with the governor’s priorities for new electricity generation.

AI business continues to expand

While its New York projects remain unchanged, TeraWulf continues to grow its artificial intelligence and high-performance computing business.

Last week, the company signed a 20-year lease agreement with Anthropic for its Justified Data campus in Hawesville, Kentucky. TeraWulf said the agreement is expected to generate about $19 billion in contracted revenue over its full term.

As crypto.news previously reported, the company is also preparing to raise about $3.5 billion through leveraged loans and high-yield bonds to finance construction of the Kentucky AI campus. Bloomberg reported that Morgan Stanley is expected to lead the financing, although final terms have not been announced.

According to TeraWulf, the Kentucky facility will support about 401 megawatts of critical computing capacity, with initial operations expected in the second half of 2027 and full deployment planned for early 2028.

The company’s latest financial results also show how its revenue mix is changing. During the first quarter of 2026, TeraWulf reported $21 million in high-performance computing lease revenue, exceeding digital asset mining revenue of just under $13 million for the first time. Total quarterly revenue stood at $34 million, compared with $34.4 million a year earlier.

TeraWulf has said its AI infrastructure business is designed to provide more predictable contracted income while continuing to use its existing power and data center assets developed during its bitcoin mining operations.

Ark Invest has expanded its exposure to Circle and Block while cutting its Robinhood position, adding nearly $15.4 million worth of shares across the three companies.

Summary

- Ark Invest bought nearly $13.9 million worth of Circle shares and added to its Block position.

- The investment firm sold about $3.15 million worth of Robinhood shares as the stock moved higher.

- The latest trades continue Ark’s recent pattern of buying selected stocks after price declines while rebalancing portfolio holdings.

According to Ark Invest’s latest daily trading disclosure, the investment firm purchased 220,012 shares of Circle Internet Group across its ARK Innovation ETF (ARKK), ARK Next Generation Internet ETF (ARKW), and ARK Fintech Innovation ETF (ARKF). Based on Tuesday’s closing price of $63.22, the acquisition was worth about $13.9 million.

The same filing showed Ark also bought 19,029 shares of Block Inc. through ARKW and ARKF. Valued at roughly $1.52 million using Tuesday’s closing price of $79.99, the purchase came as the blockchain-focused fintech company ended the session up 1.61%.

On the selling side, the firm trimmed its Robinhood Markets position by 27,742 shares. With Robinhood closing 3.27% higher at $113.45 on Tuesday, the sale was valued at about $3.15 million.

Circle purchase comes after recent price slide

Circle edged up 0.35% on Tuesday but remained down 24.17% over the past month after a sharp decline earlier in July following the launch of the Open USD stablecoin project.

The recent weakness has divided analysts. While some continue to hold a positive view on the stablecoin issuer, Mizuho downgraded Circle to Underperform from Neutral and lowered its price target to $50 from $85. The brokerage said competition from Open USD could pressure Circle’s business over time.

The latest purchase also extends a pattern seen in recent weeks. On June 26, Ark increased its holdings in Circle, Coinbase, Bullish, and Robinhood after all four stocks finished the session lower, adding about 9,264 Circle shares, 9,014 Coinbase shares, 9,136 Bullish shares, and 35,023 Robinhood shares as prices weakened.

Earlier portfolio updates showed a similar approach. Ark bought roughly $18.4 million worth of Coinbase after the exchange operator’s shares had fallen for nearly a month, accumulated more than $4.4 million of Bullish stock during a multi-session decline, and added about $32.5 million worth of SpaceX following a drop of more than 16% from its post-listing peak.

Unlike the latest Circle purchase, the Robinhood transaction moved in the opposite direction. The brokerage’s shares gained more than 3% on Tuesday, and Ark reduced its position after previously buying additional Robinhood shares during periods of weakness.

Ark manages its exchange-traded funds under a portfolio rule that limits any single holding to no more than 10% of a fund’s assets. As stock prices change, the firm periodically rebalances positions to keep those weightings within its target range.

Ripple has burned another 10 million RLUSD tokens, extending a run of treasury operations that has reduced the circulating supply of its dollar-backed stablecoin.

Summary

- Ripple burned another 10 million RLUSD as circulating supply fell roughly 20% from May’s peak.

- Repeated treasury burns reduced RLUSD supply, though redemptions do not automatically signal weaker stablecoin adoption.

- Ripple continues expanding RLUSD through AI payments and growing XRP Ledger trading and settlement activity.

Blockchain data reported on July 14 showed the tokens moving from the RLUSD Treasury to a null address, permanently removing them from circulation.

The latest operation follows 10 million-token burns recorded on July 13, twice on July 10, and once each on July 9, July 8, July 7 and July 6. Ripple also minted 20 million RLUSD on July 6. The sequence shows active supply management as redemptions and new issuance change the amount available onchain.

RLUSD supply falls from its late-May peak

RLUSD’s market capitalization now stands near $1.52 billion. That is about $380 million below its late-May peak near $1.9 billion, representing a decline of roughly 20% in circulating value.

A lower stablecoin supply does not automatically show weaker adoption. Fiat-backed stablecoins expand when issuers create tokens against new dollar deposits and contract when holders redeem tokens for cash. Burns therefore record the removal of redeemed supply rather than directly measuring transaction demand or user growth.

Repeated burns follow active treasury management

The latest burn adds to several similar transactions within little more than one week. According to the reported Ripple Stablecoin Tracker data, at least 80 million RLUSD has been burned since July 6, while 20 million tokens were minted during the same period.

Those transactions show how quickly stablecoin supply can change when large holders redeem or issue tokens. The movements do not explain who redeemed the RLUSD or why. Ripple has not publicly tied the recent burns to one customer, market event or change in its wider stablecoin strategy.

Ripple expands RLUSD use beyond basic payments

The supply contraction comes as Ripple continues adding new uses for RLUSD. As per report, Ripple joined the x402 Foundation as a Premier Member as the Linux Foundation moved the open payment standard under formal governance.

The initiative focuses partly on machine-to-machine payments. XRP and RLUSD can support payments by AI agents through x402 on the XRP Ledger, giving autonomous software a way to settle transactions using blockchain-based assets.

Ripple also introduced new tools aimed at developers building AI payment applications. As previously reported, the company launched the XRPL AI Starter Kit in June, allowing developers to build software agents that can send and receive payments.

The company is positioning RLUSD as one settlement asset that developers can use for those transactions. The work adds another potential use case for the stablecoin beyond exchange trading and traditional cross-border transfers.

RLUSD remains active across the XRP Ledger

Recent supply reductions also follow a period of growing RLUSD activity on the XRP Ledger. Evernorth said RLUSD pairs had generated more than $2.5 billion in XRP Ledger trading volume since launch.

The figures included about $900 million in volume from the RLUSD/XRP pair over six months. Evernorth also reported that the XRP Ledger held slightly more than half of RLUSD’s circulating supply by late June.

That distribution can change as minting, burning and cross-chain transfers continue. However, the figures show that RLUSD remains active across trading and settlement markets even as its total circulating supply falls from its May peak.

Ripple has also continued expanding RLUSD through institutional and payment partnerships. A coverage showed that the company is increasingly connecting the stablecoin with automated payment infrastructure and emerging machine-to-machine transaction systems.

The latest 10 million RLUSD burn reflects another reduction in outstanding supply while Ripple continues building new payment and settlement uses. The market will now watch whether the current burn cycle continues or whether new minting resumes as demand changes.

At about $1.52 billion in market capitalization, RLUSD remains below its May peak. Future treasury movements could provide a clearer picture of whether the recent contraction represents a temporary redemption cycle or a longer period of lower circulating supply.

Base creator Jesse Pollak says he is stepping back from leading the Base App after admitting he made a “wrong bet” on social, leaving the chain to fall behind on prediction markets and perpetual futures.

In a post to X on Wednesday, Pollak said he had bet that creator, content and messaging apps would drive adoption, but instead the market “disintegrated completely.”

“We realized how our focus on social had meant that base had fallen behind in key areas that were now increasingly critical — we had perps (shoutout avantis!) and prediction markets (shoutout limitless!), but both were well behind scaled competitors.”

Pollak’s comments give further insight into the reversal of Base’s growth strategy earlier this year. While Base initially focused on social products such as Farcaster, Zora and miniapps to bring crypto to “a billion people,” Pollak said financial applications are the way forward for the network, with a focus on trading, payments and AI agents.

Limitless Exchange’s monthly notional volume is only a fraction of its larger competitors. Source: Dune Analytics

Pollak added he will be returning leadership of the Base App to Coinbase, under Jordan Fish, known on X as “Cobie,” while he focuses on the Base blockchain.

Coinbase CEO: “We messed up” on content coins

Pollak’s post came just days after Coinbase CEO Brian Armstrong acknowledged content coins “didn’t work,” prompting the company to pivot earlier this year.

“We messed up, time to turn the page,” Armstrong said on Monday.

In February, Base sunset its Creator Rewards program and Farcaster-powered social feed as part of a strategic shift to tradable assets.

Related: Moonbeam to pivot from Polkadot to Base, unveils AI agent framework

The Creator Rewards program launched in July 2025 and was intended to make the Ethereum layer-2 Base a more social ecosystem, where activity and engagement translate into earnings. Meanwhile, Pollak admitted the Base App was an “imperfect Farcaster client.”

Base’s work on stablecoins, AI agents

Last week, Base activated its B20 token standard on the mainnet, introducing a native framework for stablecoins, tokenized real-world assets (RWAs) and other fungible tokens.

In May, Base launched Base MCP (Model Context Protocol), a tool that lets users manage their crypto directly from an AI model’s chat interface and interact with crypto protocols such as Morpho, Moonwell, Uniswap, Aerodrome, Avantis, Bankr and Virtuals.

In April, Base said it was upgrading key systems in preparation for an AI agent economy as part of its 2026 roadmap. It highlighted real-world asset (RWA) tokenization, stablecoins, and prediction markets as being key growth areas in 2026.

“We’re going to build base into the blockchain for global finance and do everything we can to be the place that the world’s money settles over the next century,” Pollak said on Wednesday.

Magazine: Is Robinhood Chain’s success bullish or bearish for ETH the asset?

Ethereum-backed EthSystems has launched with support from Bitmine, SharpLink and Consensys CEO Joe Lubin, adding another independent organization to Ethereum’s institutional development network after the Foundation cut 54 roles.

Summary

- EthSystems has launched with backing from Bitmine, SharpLink and Consensys CEO Joe Lubin to build confidential infrastructure for institutional Ethereum.

- The company was spun out of the Ethereum Foundation by former members of its Institutional Privacy Task Force.

- The launch follows the Ethereum Foundation’s recent restructuring as independent organizations take on more ecosystem development roles.

According to an announcement from EthSystems on Tuesday, the for-profit company will build confidential infrastructure for banks, asset managers, and other regulated institutions using Ethereum.

Bitmine and SharpLink, two major Ethereum treasury companies, have backed the venture alongside Lubin, who co-founded Ethereum and later founded Consensys.

EthSystems was spun out of the Ethereum Foundation and was established by former Foundation employees Mo Jalil, Oskar Thorén, and Aaryamann Challani. The three founders previously worked on the Foundation’s Institutional Privacy Task Force.

EthSystems targets confidential institutional finance

The company said it will help financial institutions use public Ethereum without exposing sensitive information such as trading positions, transaction details, or client identities to the full network.

Its work is expected to include privacy systems based on zero-knowledge cryptography, which can verify transactions without revealing the underlying data.

“The business model is simple: bespoke consulting, focused on solving the hardest blockers for institutional adoption,” the team wrote.

“In practice, this means continuing a lot of the work we have been doing, only charging money for it,” it added. “Commercial engagements often require a commercial counterparty.”

Alongside paid consulting, EthSystems said it will continue publishing protocol specifications and contributing to open-source projects.

While working within the Institutional Privacy Task Force, the founders held hundreds of discussions with central banks, regulators, and financial institutions, according to the company.

Their previous work included private bonds using zero-knowledge proofs, confidential stablecoin transfers, private cross-chain settlements and the Ethereum Privacy Map.

“Our mission: help institutions build confidential systems on public Ethereum without giving up what makes Ethereum worth using,” the team wrote.

EthSystems has emerged during a major reorganization of the Ethereum Foundation and its technical teams.

On June 23, the Foundation cut 54 jobs, equal to about 20% of its workforce, after a months-long review of its spending, staffing and long-term responsibilities.

The organization reorganized its work into five divisions covering protocol, access, users, community, and institutional activity. Separate groups continue to manage operations and administration.

The Foundation said the restructuring would allow it to direct staff and resources towards responsibilities that it believes only the organization can perform.

“These decisions were hard, but they are necessary,” the Foundation said in June. “We must be resourced and organized in a way that allows us to focus on the critical work that only EF can, and therefore must, do in the coming years.”

In July, the Foundation also dissolved its Protocol Support team, which had coordinated All Core Developers meetings, network upgrade tracking, Ethereum Improvement Proposal support, Forkcast, and the Ethereum Protocol Fellowship.

Mario Havel, who worked with Protocol Support for more than five years, said he remained at the Foundation but confirmed that the rest of the team had been dissolved.

“I am still part of EF, continuing my work and figuring out what’s most needed in the future,” Havel wrote on X. “However, all of my team, Protocol Support, that I have been part of for 5+ years, has been dissolved.”

Independent Ethereum groups take on new roles

EthSystems joins Ethereum Institutional and EthLabs, two other independent organizations backed by Bitmine, SharpLink, and Lubin.

EthLabs is expected to take on major Ethereum protocol research and development work, while Ethereum Institutional has been positioned as a neutral contact point for financial companies building on the network.

Lubin previously told The Block that he expected at least three organizations to emerge from the Foundation as it concentrated on censorship resistance, open-source development, privacy, and security under its CROPS framework.

“As EF continues doubling down on cypherpunk fundamentals, especially with a focus on individuals, there’s room for an independent for-profit entity that can make different choices in the trade-off space,” EthSystems wrote.

Despite the restructuring, the Foundation’s protocol division remains responsible for Ethereum’s core technology, including privacy, security, decentralization and censorship resistance.

Ethereum developers are also continuing work on the Glamsterdam upgrade, which includes proposed changes to block construction, data access, and network performance.

Hyperliquid has added a pre-IPO perpetual market linked to ChangXin Memory Technologies, or CXMT, giving traders synthetic exposure to the Chinese chipmaker before its Shanghai debut.

Summary

- Hyperliquid listed a CXMT pre-IPO perpetual as the chipmaker prepares its July 27 Shanghai debut.

- CXMT’s contract price near $8 implied a $535 billion valuation, 526% above its IPO price.

- The market offers synthetic exposure, not ownership of CXMT shares listed on Shanghai’s STAR Market.

The contract, listed as xyz, traded near $8 on July 15, according to on-chain market data cited by Hyperinsight. Applied to CXMT’s expected post-IPO share count of 66.881 billion shares, that price implies a valuation near $535 billion, about 6.3 times its official IPO valuation.

Hyperliquid opens a synthetic route to CXMT

The CXMT contract operates through Hyperliquid’s HIP-3 framework, which allows outside deployers to create perpetual markets linked to assets beyond cryptocurrencies. These markets trade as derivatives rather than spot securities, so the CXMT contract does not provide ownership, dividends or voting rights in the Shanghai-listed company.

Individual investors on China’s STAR Market generally face a RMB 500,000 asset threshold and a two-year trading-experience requirement. Hyperliquid offers a separate synthetic market that can give eligible users price exposure without access to the underlying A-share. The distinction also means the contract price can differ sharply from CXMT’s official share price.

CXMT contract trades far above IPO valuation

CXMT priced its IPO at RMB 8.66 per share and expects to raise about RMB 57.9 billion, or $8.55 billion, before any over-allotment option. Reuters reported that the deal will be Asia’s largest IPO of 2026 so far and China’s biggest A-share semiconductor offering, surpassing SMIC’s 2020 share sale.

At the offer price, CXMT’s expected post-listing value is about RMB 579.2 billion, or roughly $85.5 billion. A synthetic price near $8 implies about $535 billion, placing the Hyperliquid contract around 526% above the dollar equivalent of the IPO price. The gap reflects pricing in a separate derivatives market and does not set CXMT’s official equity valuation.

China’s largest DRAM maker prepares for listing

CXMT is China’s largest DRAM producer and ranks fourth globally, behind Samsung Electronics, SK Hynix and Micron. Recent market estimates place its global DRAM share near 8%. The company has expanded as China invests heavily in domestic semiconductor production and demand for memory chips grows alongside artificial intelligence infrastructure.

Reuters also reported that CXMT secured a long-term memory supply agreement with Tencent worth more than RMB 20 billion, or about $2.94 billion. Investor subscriptions for the STAR Market offering begin on July 16, while the shares are scheduled to start trading in Shanghai on July 27. CXMT plans to use the IPO proceeds for production and technology investment.

Hyperliquid widens its real-world asset markets

Hyperliquid’s HIP-3 framework allows builders to launch perpetual markets linked to stocks, commodities and other real-world assets. A pre-IPO SpaceX contract also traded through the framework, showing how on-chain derivatives can create markets around companies before their public shares become available.

Hyperliquid has also expanded its connection to tokenized securities. As reported by crypto.news, Ondo Finance brought 35 tokenized U.S. stocks and ETFs to HyperEVM in June. Those products differ from the CXMT perpetual because tokenized securities can use structures backed by assets held through custodians, while perpetuals provide synthetic price exposure.

The CXMT market gives traders another route to speculate on a major public offering before its debut. Attention will now turn to whether the 526% premium narrows before subscriptions start and after the underlying shares begin trading on the STAR Market.

Fresh photos show upgrades to London Stansted Airport ahead of huge transformation

BMW recalls nearly 30,000 hybrid vehicles over engine starter fire risk

Sky TV research exposes postcode lottery in girls’ sport participation

-

Fashion7 days ago

Fashion7 days agoLoro Piana Fall 2026 Enters Houston’s Art Scene

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Nutriplenish Leave-In Conditioner

-

Sports6 days ago

Sports6 days ago2026 Genesis Scottish Open Thursday TV coverage: Round 1

-

Sports6 days ago

Sports6 days agoSuper Eagles star Moses Simon opens up on Liverpool transfer regret

-

Tech7 days ago

Tech7 days agoCharacter.AI enters the microdrama arena with its own productions, but there’s a twist

-

Politics15 hours ago

Politics15 hours agoYoung campaigners urge incoming PM to act on outdoor junk food ads

-

News Videos1 day ago

News Videos1 day agoXRP BOMBSHELL… XRP OMBOARDED FOR TRANSACTIONS!!!

-

Tech2 days ago

Tech2 days agoGet Your ESP32 Sunny Side Up With This Solar Dev Board

-

Tech1 day ago

Tech1 day agoDark Secrets Emerge When Jailbreaking LLMs

-

Sports5 hours ago

Sports5 hours agoNew Cornerback Enters Vikings Trade Rumor Mill

-

Entertainment10 hours ago

Entertainment10 hours agoDisney’s Most Ambitious Failed Star Wars Attraction Is Coming to SDCC

-

Tech7 days ago

Tech7 days agoLevel Infinite Launches Gangstar Mirage City in India with Pre-Registrations

-

NewsBeat7 days ago

NewsBeat7 days agoMajor update after Huntingdon train attack as man enters plea

-

News Videos2 days ago

News Videos2 days agohow to make coin bank box with cardboard #scienceproject #money #diy #shorts

-

Tech2 days ago

Tech2 days agoCloudflare Precursor Watches Your Mouse and Keyboard To Decide If You Are Human

-

Entertainment8 hours ago

Entertainment8 hours agoVicki Gunvalson Defends Discussing Heather Dubrow’s Money

-

NewsBeat5 hours ago

NewsBeat5 hours agoWatch: Is Donald Trump facing a popular backlash on immigration?

-

Crypto World2 days ago

Ripple, Coinbase, Circle Join Linux x402 Foundation to Help Shape AI Payments

-

Sports3 hours ago

Sports3 hours agoMichigan officials not expected to discuss AD Warde Manuel at Thursday meeting

-

NewsBeat5 hours ago

NewsBeat5 hours agoFirefighters issue update on Dovestone moorland blaze as fire enters fourth day

You must be logged in to post a comment Login