Crypto World

Roundhill’s Election-Event Contract ETFs Could Be Groundbreaking

Roundhill Investments, a US-based ETF issuer, has moved to bring six exchange-traded funds tied to event contracts that bet on the outcome of the 2028 US presidential election. The filing with the Securities and Exchange Commission describes ETFs that would use a specialized derivative known as event contracts to speculate on political results. If approved, the products could broaden access to prediction-market-style exposure within a traditional exchange-traded wrapper, a development that ETF observers characterized as potentially groundbreaking. The six funds cover presidential, Senate, and House outcomes across both major parties: Roundhill Democratic President ETF, Roundhill Republican President ETF, Roundhill Democratic Senate ETF, Roundhill Republican Senate ETF, Roundhill Democratic House ETF, and Roundhill Republican House ETF. The filing also flags that regulators continue to weigh how such instruments should be classified and regulated.

The prospect of an ETF-based route into event contracts has drawn commentary from industry observers. ETF analyst Eric Balchunas noted in a post that, if the SEC were to approve the lineup, the impact could be “potentially groundbreaking.” He argued that the ETF structure could unlock a broader set of prediction-market applications that are more accessible to a wide range of investors than raw prediction markets on bespoke platforms. The filing itself describes the objective of the fund tied to the winning election outcome as capital-focused, while cautioning that the other five funds face materially higher risk where investors could see substantial losses.

The Roundhill filing explicitly describes the structure as investing in, or gaining exposure to, a class of instruments known as event contracts. The approach would apply to the presidential outcomes as well as to control of the Senate and the House, spanning both major parties. In the filing, Roundhill underscores that while the fund aiming to capture the ultimate election result seeks capital appreciation, the remaining five ETFs could lose “almost all” of their value, depending on how market events unfold and how the contracts converge on settlement. The document warns that a rapid convergence between opposing event outcomes could trigger sharp NAV movements, a phenomenon described as highly atypical for conventional ETFs.

The regulatory dimension is front and center. The filing notes that US rules governing event contracts are evolving, and any future classification changes or “restrictions” could affect the funds. The document also flags the possibility that policymakers may limit, suspend, modify, or even prohibit certain political outcome contracts, should concerns around investor protection or market integrity intensify. Investors who are uncomfortable with regulatory uncertainty are urged to avoid purchasing shares. The discussion highlights the broader tension between liquidity, innovation, and consumer safeguards in the growing ecosystem of prediction-market-style financial products.

The debate around prediction markets has gained momentum alongside regulatory signals from US authorities. In early February, reports indicated the Commodity Futures Trading Commission (CFTC) had moved to withdraw a Biden-administration proposal seeking to ban sports and political prediction markets, a sign that a more permissive stance could be emerging for certain forms of event-driven contracts. The regulatory arc remains a key variable shaping how Roundhill’s six ETFs would perform in practice, particularly if classification or restriction decisions shift in coming months. The evolving framework raises questions about how these funds would be priced, settled, and taxed, and whether they would attract meaningful liquidity given the novel nature of the underlying contracts.

Industry observers note that the intersection of traditional equity markets and prediction markets could mark a broader shift in how investors access political risk and price uncertainty. The Roundhill filing arrives as the so-called prediction-market conversation grows more nuanced, with debates about whether such markets should focus on hedging price-exposure risk or remain oriented toward speculative bets on short-term political outcomes. Ethereum co-founder Vitalik Buterin has weighed in on the topic, arguing that prediction markets, if left to their current trajectory, risk over-convergence on short-horizon bets and price swings that are detached from longer-term value creation. In a widely cited post, he called for shifting toward marketplaces that hedge price exposure for consumers, a stance that aligns with ongoing discussions about consumer protection in digital markets. Ethereum (CRYPTO: ETH) has become a focal point in these debates as developers and investors consider how to align incentives with real-world utility. For context, Buterin’s remarks have been echoed in discussions around hedging mechanisms and risk controls in prediction-market ecosystems.

The broader conversation around event contracts and their perceived suitability for mainstream investors continues to evolve. The Roundhill proposal sits at a moment when traditional asset managers are experimenting with derivative-like structures to capture political risk, while regulators voice caution about liquidity, reliability, and the integrity of price discovery. The SEC’s review process for these six ETFs will hinge on whether event contracts can offer transparent settlement, robust risk disclosures, and a structure that can scale liquidity to support a diversified investor base. The filing’s emphasis on the potential for significant NAV volatility in the five riskier funds underscores the need for clear risk management frameworks and investor education as these products progress through the regulatory pipeline. For readers, the main takeaway is that the integration of event contracts into an ETF wrapper could represent a notable pivot in how political risk is monetized, even as the regulatory environment remains a decisive constraint on immediate execution.

As the market watches for ongoing developments, the Roundhill filing serves as a litmus test for whether prediction-market-style derivatives can be reconciled with the governance and investor protections that underpin traditional ETFs. While the six-fund lineup targets different political outcomes, the core insight for investors is the relative risk asymmetry: one fund may pursue capital appreciation from the ultimate election result, while the other five grapple with convergence events that can push net asset value sharply in either direction. The path to approval remains uncharted, and the regulatory equation—balancing innovation with safeguards—will likely dictate the pace and shape of any eventual launch. In the meantime, the discourse surrounding prediction markets enters a more formal, regulated phase, with the potential to broaden access to politically linked derivatives for a broader cohort of investors while inviting heightened scrutiny from policymakers and market participants alike.

Why it matters

The Roundhill filing matters because it tests whether prediction-market concepts can be packaged into the familiar ETF format. If approved, it could provide a regulated, transparent avenue for investors to engage with political risk using a market-based mechanism that has historically lived outside mainstream asset management. By packaging six distinct event contracts into a single lineup, the fund family aims to offer diversified exposure to different branches of government, potentially enabling portfolios to hedge or express views on the political calendar without stepping outside established exchange-traded infrastructure.

For the broader crypto and digital-asset discourse, the development signals a continuing convergence between traditional finance instruments and more experimental market ideas. The emergence of ETF-based event contracts could feed into ongoing debates about how to design markets that are resilient, accessible, and protective of ordinary investors while still enabling innovative risk transfer. The attention from figures like Balchunas and the ongoing commentary from prominent crypto thinkers, including Ethereum’s Vitalik Buterin, underscores the cross-pollination between traditional ETFs and decentralized finance conversations about hedging, price discovery, and consumer protection. As policymakers refine regulatory guidance, proponents argue that a regulated ETF wrapper could deliver improved transparency, settlement mechanics, and liquidity compared with niche, permissioned prediction platforms.

For participants in the prediction-market space, Roundhill’s approach may set a precedent for how event-driven instruments could be evaluated by mainstream markets. Stakeholders will be watching whether the funds can attract sufficient liquidity, how settlement will be determined, and how sensitive the NAV will be to shifting political narratives and polling trajectories. The tension between potential liquidity gains and risk of rapid NAV swings will be central to any future discussions about the viability of these vehicles in a volatile political landscape.

What to watch next

- SEC decisions on the Roundhill ETF filings and the final product terms, including eligibility criteria and settlement procedures.

- Any regulatory updates or guidance on event contracts, including potential reclassifications or restrictions that could affect the funds.

- Regulatory commentary from the CFTC or other bodies regarding prediction markets and related derivatives.

- Market liquidity and investor demand for election-related ETFs as the 2028 cycle progresses.

Sources & verification

- Roundhill’s filing with the SEC detailing six election-event ETFs, including the six fund names and their objectives: SEC filing.

- Eric Balchunas’s remarks about potential impact if approved: X post.

- Regulatory discussions around prediction markets and CFTC coverage, including referenced coverage on the Biden-era proposal status: CFTC stance.

- Vitalik Buterin’s comments on prediction markets and hedging, including his X post: X post, and a related piece on hedging: Buterin hedging discussion.

Bitcoin briefly touched a fresh intra-day high near $68,589 as markets absorbed a mix of geopolitics and macro signals. The move came alongside a broad risk-on rally in U.S. equities, with the Dow Jones Industrial Average climbing more than 1,125 points, the S&P 500 rising around 2.9%, and the Nasdaq advancing about 3.8%. The day’s headlines centered on chatter about ending a war involving the United States, Israel and Iran, buoying sentiment even as traders remained wary of sustaining gains in the crypto market.

On Tuesday, The Wall Street Journal reported that President Trump told aides he could consider ending the conflict with Iran, with the Strait of Hormuz partially open but no formal statement issued. Separately, unconfirmed reports attributed to Iranian President Masoud Pezeshkian suggested Tehran might be seeking a path to exit the war, though such remarks have not been independently verified. Whether the statements prove reliable or not, they contributed to a mood shift that encouraged risk-taking across traditional markets, even as crypto traders kept their expectations in check.

Despite the synchronized bounce in risk assets, observers caution that Bitcoin’s ability to sustain the breakout remains uncertain. Analysts cited by Cointelegraph highlighted that a daily close above the 50-day moving average near $68,879 would be a meaningful signal of a potential trend shift. From there, some see room for a liquidity-driven extension toward approximately $82,000, but only if buyers step in with durable, directional commitments rather than headline-driven moves.

Key takeaways

- Bitcoin briefly rose to about $68,589 as geopolitical and macro headlines supported a risk-on backdrop.

- U.S. equities logged a broad rally: the Dow up by more than 1,125 points, the S&P 500 up roughly 2.91%, and the Nasdaq up about 3.83%.

- Analysts say a daily close above the 50-day moving average near $68,879 would mark a potential trend change and could unlock further upside if leveraged players unwind or cover shorts.

- Crypto traders remained skeptical of a durable breakout, with much price action driven by headlines, equities, and perpetual futures rather than sustained buy-side conviction in spot markets.

- Cointelegraph notes point to flat open interest in futures and weak spot demand since the Feb. 6 sell-off below $60,000, alongside short-term traders selling below cost basis around $85,800 and stablecoin inflows near a two-year low.

The market backdrop: what’s really pushing the price action

In the broader market, the relief rally follows a period of heightened attention to policy and conflict dynamics. The weekend and early-week headlines suggested at least a possibility of de-escalation, with Trump’s communications and unconfirmed statements from Iranian leadership contributing to a mood swing that benefited risk assets. However, the cryptocurrency market did not display the same confident impulse that characterized equities, underscoring a divergence between macro optimism and crypto-specific demand.

In a sense, Bitcoin’s price trajectory remains tethered to a mix of headline risk and technical thresholds. The $68,879 level—the approximate 50-day moving average—has emerged as a practical line in the sand. A daily close above that level would be interpreted by many traders as a sign that bullish momentum can persist beyond a few sessions. Conversely, failure to clear that barrier could reinforce a rangebound pattern, leaving BTC prone to whipsaws tied to news flow and broader market sentiment.

Analysts highlighted that the market’s appetite for directional bets remains constrained. The research notes that a lack of durable bid depth—evidenced by flat open interest in Bitcoin futures and tepid spot demand since the February dip below $60,000—suggests most price moves are driven by news and correlated markets rather than a broad base of new buyers. This posture makes BTC more vulnerable to abrupt reversals if headlines turn sour or if macro conditions deteriorate again.

What traders are watching next

Beyond the immediate friction at the $68,879 threshold, traders are watching for clearer signals from both the spot and futures markets. A sustained move past that line could invite a liquidity-driven push higher if liquidations and stop-orders align to reinforce the breakout. In practice, that would require a broad shift in investor posture—from cautious footing to active accumulation among spot buyers and ETF-like vehicles, if applicable in the current market environment.

On the technical front, the next real milestones are shaped by volatility regimes and risk tolerance. If Bitcoin can establish a daily close above the 50-day moving average, buyers may gain confidence to press toward higher targets. If not, the picture could tilt back toward consolidation, with traders awaiting a fresh catalyst to re-ignite momentum. This dynamic underscores a larger question facing the crypto market: will the current price action translate into durable demand, or will it remain a series of episodic rallies tethered to headlines?

On-chain signals add nuance to the story. Cointelegraph highlighted that stablecoin inflows to exchanges are near a two-year low, which generally signals a cautious stance among traders. Simultaneously, open interest in Bitcoin futures and spot demand have remained flat since the Feb. 6 decline, reinforcing the impression that the market is not currently laying down strong directional bets. These indicators suggest that even as price moves translate into headlines-based enthusiasm, the fundamental bid for Bitcoin remains restrained—a critical factor for readers weighing whether this rally has legs or is likely to falter.

For investors and builders, the unfolding scenario offers a key lesson: headlines can temporarily lift risk assets, but the path to sustained upside in BTC depends on a credible, durable bid from market participants across the full spectrum of the ecosystem. In this context, the potential for a broader move will hinge not just on geopolitical optics but on the crypto market’s ability to attract real spot demand and to overcome the structural restraint that has characterized the current cycle.

Looking ahead: uncertainty and the path forward

While the Wall Street Journal’s report on possible de-escalation added a narrative tailwind, the absence of official confirmation means markets remain in a wait-and-see posture. For Bitcoin, the critical test remains whether buyers can sustain a move beyond the near-term technical ceiling and ignite a longer-lasting uptrend. Until then, the price action could continue to reflect a tug-of-war between headline-driven optimism and the more cautious posture seen in on-chain metrics and spot-market activity.

Readers should watch for any tangible policy developments that could shape risk appetite and for evidence of improving spot demand, not just speculative leverage. In the near term, the absence of a clear bid from the spot market and muted open interest imply that BTC could continue to drift within a familiar range until a decisive catalyst emerges.

As markets digest these signals, the next few sessions may reveal whether the current optimism has a durable basis or if crypto markets will revert to a more cautious stance as the macro and geopolitical backdrop evolves. The balance between headlines, technical levels, and real demand will determine whether BTC can translate short-term enthusiasm into a sustained move higher or retreat to the lower end of its recent trading band.

Key takeaways

- Binance’s BNB is down 4.5% in the last 24 hours and now trades below $590.

- The bearish performance comes as President Trump threatens to attack Iran’s power plants.

BNB (formerly Binance Coin) is currently trading below $585 as of Thursday, continuing its three-week decline.

The correction has deepened following US President Donald Trump’s statement that the ongoing US-Iran conflict could last until late April, which has dampened investor sentiment towards riskier assets.

From a technical standpoint, momentum indicators are signaling a potential for further downside in BNB.

Trump’s remarks weigh on market sentiment

Bitcoin, Ether, BNB, and XRP are in the red after President Trump warned on Wednesday that the US-Iran war could extend until late April. He also threatened to target Iranian power plants and stated that Iran would be sent back to the “Stone Age” if an agreement is not reached.

These statements have tempered hopes for de-escalation, further reducing investor appetite for riskier assets. As a result, the US Dollar (USD) and oil prices have strengthened, while US equities and other high-risk assets have come under pressure.

Retail interest in BNB has also declined in recent days. According to CoinGlass, BNB’s long-to-short ratio reads 0.80 on Thursday, its lowest point in a month.

A ratio below one indicates bearish market sentiment, with traders betting on a further decline in BNB’s price.

BNB could dip to February’s low

The BNB/USD 4-hour chart is bearish and inefficient as BNB has underperformed in recent days.

Currently, BNB is trading well below the 50-day, 100-day, and 200-day Exponential Moving Averages, which all trend higher above the current price and frame a broader bearish backdrop.

The Relative Strength Index (RSI) on the 4-hour chart reads 42, below the neutral 50, indicating a bearish bias. The Moving Average Convergence Divergence (MACD) is also drifting deeper below the zero, signaling persistent selling pressure rather than a completed downside exhaustion.

If the bearish trend persists, BNB will retest the initial support at $570.16 (February’s low). A break below this level would open the way toward lower daily lows and deepen the corrective phase toward the key psychological level at $500.

However, if the bulls regain control of the market, they would encounter immediate resistance at $697, in line with the descending EMAs.

A sustained recovery above this barrier would be needed to ease the current bearish tone and expose the next resistance at $790.79.

Polymarket, the prediction-market platform, rolled out a broadened fee model on March 30, expanding taker fees beyond crypto and sports to a wider array of categories. In the days that followed, metrics tracked by DefiLlama show a sharp rise in on-platform activity monetized through fees, with daily trading fees crossing the $1 million mark on Wednesday and Thursday. Revenue after incentives climbed to as high as $995,000 on Wednesday before easing to roughly $899,000 on Thursday. The shift underscores how Polymarket is recalibrating its economics to lock in ongoing investor interest amid intensifying regulatory scrutiny.

The broadening of the fee schedule coincides with a deliberate push to monetize activity more aggressively. Polymarket expanded taker fees to categories such as finance, politics, economics, culture, weather and tech, while keeping geopolitical and world events free of fees. The core idea appears to be extracting more value from routine trading activity, a move that aims to sustain liquidity and growth even as jurisdictions around the world tighten oversight of prediction markets. Data from DefiLlama illustrates the immediate impact: daily fees surged from about $363,000 on Monday to more than $1 million on midweek days, with revenue after incentives peaking at near $1 million on Wednesday before settling lower on Thursday.

Key takeaways

- DefiLlama data show Polymarket’s daily fees jumped from roughly $363,000 to over $1 million in the days after the March 30 fee overhaul, signaling a dramatic monetization shift.

- Revenue after incentives rose to as high as about $995,000 on one day, then moderated to around $899,000 on the following day, reflecting how the new fees translate into platform economics.

- The fee expansion added taker charges across more categories—finance, politics, economics, culture, weather and tech—while keeping geopolitical and world-events fees free.

- Regulatory pressure remains a core driver of strategy, with ongoing limits on access in multiple jurisdictions and actions by U.S. states, even as investor interest persists.

Regulatory pressure tightens across borders

The surge in Polymarket’s fees arrives amid a broader regulatory crackdown on prediction markets across Europe, North America and beyond. In Europe, the platform has faced mounting restrictions as regulators argue that it operates as an unlicensed gambling venue in several jurisdictions. Hungary and Portugal, for example, moved to block or limit access in January over licensing concerns and, in Portugal’s case, questions around political betting. These frictions complicate user acquisition and liquidity, even as demand for event-based markets remains visible among certain trader cohorts.

Other notable developments illustrate the global regulatory tension. In Argentina, a court order issued on March 17 ordered a nationwide ban on Polymarket, contending that the platform allowed users to place bets without sufficient identity and age verification, raising concerns about accessibility for underage users. Polymarket’s own geoblock information indicates the platform is currently blocked in 33 countries, a figure that underscores the cross-border compliance challenges faced by the operator. Kalshi, a competing prediction market, reports even broader restrictions, stating it is banned in 52 jurisdictions.

Across the United States, the regulatory environment remains unsettled. At least 11 states have taken legal action against prediction markets such as Polymarket and Kalshi, with cease-and-desist orders or new legislative proposals under consideration in several states. Despite these crackdowns, both platforms have signaled an ability to pursue expansion, with reports of potential large-scale fundraising rounds that could value each platform around $20 billion. The tension between growth ambitions and regulatory risk continues to shape the trajectory of the sector.

In late March, Polymarket and Kalshi introduced new trading restrictions aimed at curbing insider trading after criticism about well-timed bets and concerns about market integrity. The reform push signals a desire to bolster trust in event markets while navigating a landscape where regulators are increasingly vigilant about preemptive positions and information asymmetries.

Investor interest persists amid a risk-laden backdrop

The interplay between monetization, regulatory risk and investor sentiment remains delicate. The private investment narrative around Polymarket received a high-profile boost when Intercontinental Exchange, the parent of the New York Stock Exchange, reportedly invested about $600 million in Polymarket last week. The move underscores a sustained interest from large financial players in the potential of structured prediction markets, even as the sector contends with licensing, anti-gambling, and consumer-protection concerns in key markets.

On the funding side, both Polymarket and Kalshi are rumored to be exploring new rounds that could push their valuations into the tens of billions of dollars, highlighting a long-term belief among some investors that event-based markets can scale beyond their current regulatory envelopes. The ongoing push for expansion, paired with legal scrutiny, creates a dynamic where monetization levers, compliance, and user protection must co-evolve to maintain liquidity and participation.

As a matter of policy and practicality, March 24 saw explicit steps to address market integrity concerns through tightened trading rules, setting a precedent for how similar platforms might balance rapid growth with stronger oversight. The broader market will continue to watch how regulators respond to these shifts, whether geoblocking efforts intensify, and how exchanges balance revenue opportunities with responsible operator practices that protect users and maintain fair markets.

Readers should stay attentive to regulatory updates, particularly in Europe and the United States, where the legal status of prediction markets remains unsettled in several jurisdictions. The evolution of Polymarket’s fee model, alongside liquidity dynamics and enforcement actions, will likely shape how users engage with event-based markets in the coming months and whether investor appetite for large-scale funding rounds sustains the sector’s momentum.

What to watch next: regulatory clarity in key jurisdictions, the sustainability of elevated fee-driven revenue, and whether the ongoing confluence of large-cap investment and stricter market rules will redefine how forecast markets operate at scale.

Prediction market Polymarket’s recent fee expansion has started to affect its numbers, with daily fees and revenue climbing sharply in the days following a March 30 price overhaul.

According to DefiLlama data, daily fees rose from about $363,000 on Monday to over $1 million on both Wednesday and Thursday, while revenue (the portion retained after incentives) reached as high as $995,000 on Wednesday before easing to about $899,000 on Thursday.

The jump follows the rollout of a broader fee model on Monday, when the platform expanded taker fees beyond crypto and sports to categories including finance, politics, economics, culture, weather and tech, while keeping geopolitical and world events fee-free.

The spike shows how aggressively Polymarket is monetizing trading activity to maintain continued investor interest amid regulatory scrutiny in the US, Europe and other countries worldwide. Last week, Intercontinental Exchange, the parent company of the New York Stock Exchange, invested $600 million in Polymarket.

Prediction markets face growing regulatory scrutiny

The fee and revenue spike comes as prediction markets, including Polymarket, face growing regulatory scrutiny across multiple jurisdictions.

In Europe, Polymarket has faced mounting restrictions, with Hungary and Portugal moving to block or limit access in January over concerns that the platform operates as unlicensed gambling. Regulators in both countries cited licensing issues and, in Portugal’s case, concerns around political betting.

Related: Peter Brandt, Polymarket traders don’t see new Bitcoin highs this year

On March 17, a court in Argentina ordered a nationwide ban on Polymarket, arguing that the platform allowed users to place bets without sufficient identity and age verification. The court said this meant that even children and adolescents could access the platform and place bets without any control.

According to Polymarket’s website, the platform is currently blocked in 33 countries. Kalshi, on the other hand, reports that it’s banned in 52 jurisdictions.

In the United States, at least 11 states have taken legal action against prediction markets such as Polymarket and Kalshi, with several issuing cease-and-desist orders or considering new legislation.

Despite regulatory crackdowns, Polymarket and Kalshi are looking to expand, with both reportedly exploring new funding rounds that could value each platform at around $20 billion.

On March 24, Polymarket and Kalshi introduced new trading restrictions to curb insider trading following criticism over well-timed bets and growing concerns around market integrity.

Magazine: Are DeFi devs liable for the illegal activity of others on their platforms?

Key takeaways

- BTC is down 2%, erasing the recovery earlier this week,

- US-listed spot ETF recorded an outflow of $173.73 million on Wednesday, breaking its two days of inflow this week.

Bitcoin faces continued losses amid weaker institutional demand

Bitcoin (BTC) prices continued to decline on Thursday, trading below $67,000, almost completely erasing the recovery from earlier in the week. Institutional demand also appears to be faltering, as spot Exchange Traded Funds (ETFs) experienced a significant outflow of over $173 million on Wednesday, ending a two-day streak of inflows.

This decline in demand coincides with a growing sense of bearish sentiment in the market, which is further amplified by US President Donald Trump’s recent remarks suggesting an escalation of the ongoing conflict.

On Wednesday, President Trump addressed the nation, warning that the ongoing conflict could drag on until late April. He stated that the US would take extreme measures over the next two to three weeks, including threats to attack Iranian power plants and send Iran back to the “stone age” if no agreement is reached.

These statements have dampened hopes for de-escalation, which in turn has reduced investor appetite for riskier assets. The US Dollar (USD) and Oil prices have risen as a result, while US equities and other risk assets have suffered, effectively erasing the gains Bitcoin saw earlier this week.

Data from CoinGlass indicates that institutional interest in Bitcoin remains uncertain. Spot Bitcoin ETFs saw a significant outflow of $173.73 million on Wednesday, following two days of positive inflows earlier this week. This suggests indecisiveness among institutional investors, who appear hesitant to increase exposure to risk assets amid ongoing market uncertainty.

According to Glassnode’s weekly report on Wednesday, Bitcoin remains trapped within a broad trading range of $60,000 to $70,000. While the market shows early signs of stabilization, it has not yet shown enough momentum to break decisively in either direction.

The report indicates that Bitcoin’s on-chain conditions reflect a continued period of repair, with elevated supply in loss and long-term holder capitulation still not fully resolved. However, spot demand has shown some improvement, signaling that sellers are not entirely in control of the market anymore.

Bitcoin Price Forecast: BTC could record further losses

The BTC/USD 4-hour chart is bearish and efficient as Bitcoin is trading below $66,400 on Thursday, erasing the recovery from earlier this week. The near-term bias is mildly bearish.

Bitcoin remains capped well below the clustered 50-day, 100-day, and 200-day Exponential Moving Averages (EMAs) between roughly $70,800 and $84,800, which reinforces downside pressure despite the recent bounce attempts.

Currently, the technical indicators are bearish. The Relative Strength Index (RSI) on H4 sits at 51, just above the midline.

The Moving Average Convergence Divergence (MACD) remains below the signal line, indicating persistent selling pressure.

If the market continues its decline, sellers would meet immediate support at $65,900. Breaking this level would expose the key psychological level at $60,000.

On the flipside, if the bulls regain control of the market, they would encounter resistance at the $69,200 level, with the major resistance around $72,600.

A daily close above $72,600 would signal a bullish break from the sideways structure and open the door toward the 100-day EMA near $76,400.

Metaplanet (3350) continued to scale its accumulation strategy through the first quarter of 2026, acquiring 5,075 BTC for approximately $398 million, implying an average purchase price of about $78,000 per coin.

The Tokyo-based firm has has generated a BTC yield of 2.8% year-to-date.

As of March 31, Metaplanet holds a total of 40,177 BTC, acquired for roughly $3.9 billion, with an average cost basis of approximately $97,000 per BTC.

Metaplanet is now the third largest bitcoin treasury company worldwide, overtaking MARA Holdings after the miner reduced its bitcoin stack significantly.

Twenty One Capital (XXI) holds second place with 43,514 BTC, according to Bitcoin Treasuries, while Strategy (MSTR) is by far and away the largest with over 762,000.

Shares of Metaplanet were down 2%, trading at 302 yen ($1.89).

Crypto World

Audit admin keys, not just code, expert says after $200 million Drift exploit: Crypto Daybook Americas

By Omkar Godbole (All times ET unless indicated otherwise)

Programmable blockchain Solana’s SOL token has hit five-week lows after an exploit at one of its largest perpetual decentralized exchange, Drift, underscored that security risks go beyond just smart contracts.

“If you’re building in DeFi, audit the surface area of your admin key. Not only the smart contracts,” Omer Goldberg, founder of Chaos Labs, said, explaining what went wrong.

Goldberg explained in his X thread that the attacker compromised Drift’s admin key. This single key gave the attacker god-like control — like handing someone the master password to the entire bank vault with no limits or alarms.

Using this power, the attacker created a fake collateral market for a worthless token called CVT. They maxed out the risk parameters so the system treated hundreds of millions of this junk token as safe, high-value collateral. In the same transaction, they switched the CVT price oracle to one they fully controlled, artificially pumped its value to sky-high levels, lifted the circuit breakers on major assets (removing withdrawal limits) such as USDC, eETH and others, and drained over $250 million worth of tokens.

This also worked because Drift features a single shared liquidity pool that holds everyone’s collateral and trading funds, providing a seamless trading experience. (Imagine putting all your money in a single bank account and losing everything in a signature hack).

The real issue wasn’t a bug in the code. It was the enormous “surface area” of that admin key, or the massive damage one compromised signer could cause by rewriting protocol-wide risk rules, assigning oracles, and disabling safety guards.

This isn’t the first time a compromised privileged key has led to big losses. Just 10 days earlier, Resolv was drained for $25 million in tokens after attackers compromised a SERVICE_ROLE key.

So, the message is clear: protocol safety now depends as much on strong governance and key controls as it does on smart contract audits.

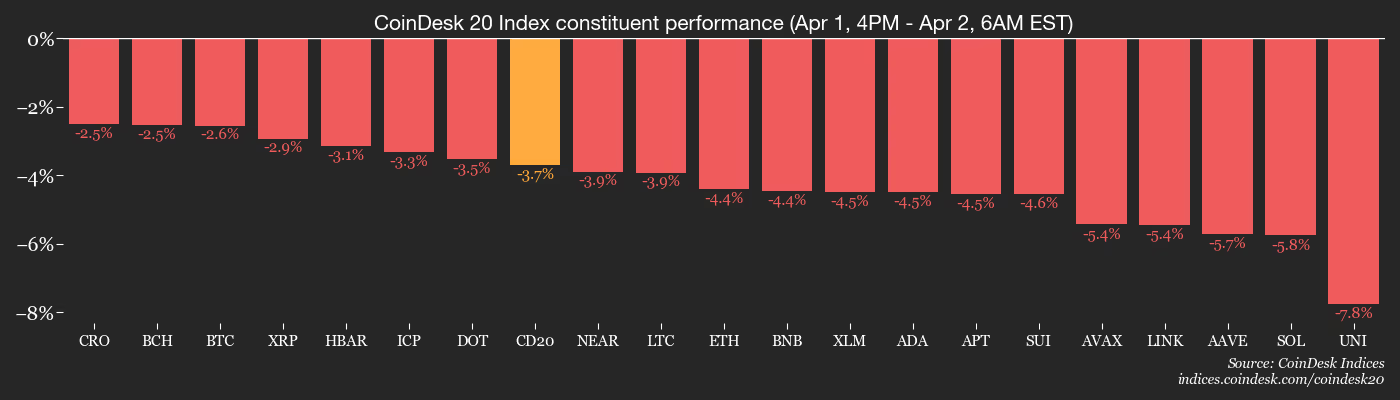

As for markets, SOL’s near 3% drop to $78.30, the lowest since late February, is consistent with the weakness in bitcoin , ether (ETH), XRP (XRP) and the wider market, as represented by the CoinDesk 20 Index.

The culprit once again is President Donald Trump’s renewed threat to Iran, which has sent oil prices higher. In the short term, these headlines could continue to lead movements in both traditional and crypto markets. Stay alert!

Read more: For analysis of today’s activity in altcoins and derivatives, see Crypto Markets Today

What to Watch

For a more comprehensive list of events this week, see CoinDesk’s “Crypto Week Ahead“.

- Crypto

- Macro

- April 2, 8:30 a.m.: U.S. Initial Jobless Claims for week ending March 28 (Prev. 210K)

- Earnings (Estimates based on FactSet data)

Token Events

For a more comprehensive list of events this week, see CoinDesk’s “Crypto Week Ahead“.

- Governance votes & calls

- Unlock DAO is voting to transfer 3 ETH to its Base multisig to swap for USDC to cover current and future operational expenses. Voting ends April 2.

- Aavegotchi DAO is voting to elect nine multi-sig signers, maintain a 5-of-9 signature threshold, and set their quarterly compensation at $1,000 paid in GHST. Voting ends April 2.

- Arbitrum DAO is voting across two proposals to transition its Code of Conduct and Procedures into living documents managed by OpCo, and to upgrade to ArbOS 60 Elara. Voting ends April 2.

- Unlocks

- April 2: Ethena (ENA) to unlock 2.18% of its circulating supply worth $16.05 million.

- Token Launches

Conferences

For a more comprehensive list of events this week, see CoinDesk’s “Crypto Week Ahead“.

Market Movements

- BTC is down 2.53% from 4 p.m. ET Wednesday at $66,459.24 (24hrs: -3.1%)

- ETH is down 4.66% at $2,043.77 (24hrs: -4.16%)

- CoinDesk 20 is down 3.59% at 1,891.30 (24hrs: -3.81%)

- Ether CESR Composite Staking Rate is up 1 bp at 2.77%

- BTC funding rate is at 0.0001% (0.0635% annualized) on Binance

- DXY is up 0.51% at 100.16

- Gold futures are down 3.56% at $4,641.60

- Silver futures are down 6.47% at $71.15

- Nikkei 225 closed down 2.38% at 52,463.27

- Hang Seng closed down 0.7% at 25,116.53

- FTSE is down 0.08% at 10,356.15

- Euro Stoxx 50 is down 1.61% at 5,640.26

- DJIA closed on Wednesday up 0.48% at 46,565.74

- S&P 500 closed up 0.72% at 6,575.32

- Nasdaq Composite closed up 1.16% at 21,840.95

- S&P/TSX Composite closed up 0.58% at 32,957.95

- S&P 40 Latin America closed up 0.95% at 3,658.43

- U.S. 10-Year Treasury rate is up 5.1 bps at 4.372%

- E-mini S&P 500 futures are down 1.17% at 6,540.50

- E-mini Nasdaq-100 futures are down 1.51% at 23,830.00

- E-mini Dow Jones Industrial Average Index futures are down 0.97% at 46,353.00

Bitcoin Stats

- BTC Dominance: 58.58% (+0.04%)

- Ether-bitcoin ratio: 0.03079 (-2.02%)

- Hashrate (seven-day moving average): 1,016 EH/s

- Hashprice (spot): $31.48

- Total fees: 2.55 BTC / $174,507

- CME Futures Open Interest: 107,610 BTC

- BTC priced in gold: 14.4 oz.

- BTC vs gold market cap: 4.44%

Technical Analysis

- The chart shows solana’s daily price swings in candlestick format with the Ichimoku cloud, a trend indicator, identified by the shaded area between green and red lines.

- The token’s price has crossed back below the cloud, indicating continuation of the broader decline. The pattern is similar to what we saw in mid-January, following which prices dropped sharply.

- Ichimoku cloud, invented by a Japanese journalist, is widely used to spot trend changes. Crossovers above and below the cloud are said to represent bullish and bearish shifts in trends.

Crypto Equities

- Coinbase Global (COIN): closed on Monday at $172.99 (-0.93%), -3.17% at $167.50 in pre-market

- Circle Internet (CRCL): closed at $90.74 (-4.89%), -1.59% at $89.30

- Galaxy Digital (GLXY): closed at $17.37 (-5.85%), -2.42% at $16.95

- Bullish (BLSH): closed at $35.07 (-1.85%), -2.79% at $34.09

- MARA Holdings (MARA): closed at $8.04 (-1.47%), -2.74% at $7.82

- Riot Platforms (RIOT): closed at $12.55 (+1.54%), -4.94% at $11.93

- Core Scientific (CORZ): closed at $15.30 (+2.27%), -3.66% at $14.74

- CleanSpark (CLSK): closed at $8.62 (+1.29%), -3.38% at $8.33

- CoinShares Valkyrie Bitcoin Miners ETF (WGMI): closed at $34.86 (+0.11%)

- Exodus Movement (EXOD): closed at $6.68 (+2.77%)

Crypto Treasury Companies

- Strategy (MSTR): closed at $122.78 (-1.62%), -2.09% at $120.21

- Strive (ASST): closed at $10.16 (+1.40%), -3.44% at $9.81

- SharpLink Gaming (SBET): closed at $6.46 (+0.16%), -3.72% at $6.22

- Upexi (UPXI): closed at $0.99 (+0.20%), -5.16% at $0.94

- Lite Strategy (LITS): closed at $1.13 (-2.59%), -5.31% at $1.07

ETF Flows

Spot BTC ETFs

- Daily net flow: -$173.7 million

- Cumulative net flows: $55.92 billion

- Total BTC holdings ~ 1.29 million

Spot ETH ETFs

- Daily net flow: -$7.1 million

- Cumulative net flows: $11.58 billion

- Total ETH holdings ~ 5.71 million

Source: Farside Investors

While You Were Sleeping

Trump stirs market, political angst with vague timeline for Iran (Bloomberg): The $31 trillion U.S. Treasuries market notched its worst monthly performance since late 2024 in March, with bond investors concerned that the war-driven surge in oil prices would ignite inflation.

‘We are going to hit them hard’: Markets disappointed, oil up again after Trump speech (euronews): Oil rose sharply and European stocks fell after Trump said in his first national address since the Iran war began that the U.S. would continue its attacks on Iran.

Gold, silver fall as investors doubt Trump’s exit plan (The Wall Street Journal): Gold and silver prices swung into the red, alongside industrial metals and equities. Spot gold prices were down 3%, at roughly $4,670 a troy ounce. Spot silver fell more than 5%.

The bitcoin treasury boom is unwinding as some companies and governments sell holdings (CoinDesk): Those who rushed into bitcoin over the past two years are now heading for the exits and it’s not a great sign for the market.

United States President Donald Trump has vowed to continue military operations as the country’s Middle East war with Iran enters the third week of intensified hostilities.

Summary

- Trump says U.S. will intensify strikes on Iran’s critical infrastructure over the next two to three weeks as military operations expand.

- Iran warns of “crushing” retaliation and rejects ceasefire talks, claiming US and Israeli strikes have hit only limited targets so far.

- Major cryptocurrencies have fallen in response to the recent escalation.

“We are going to hit them extremely hard over the next two to three weeks. We’re going to bring them back to the Stone Ages, where they belong,” Trump said, adding that the United States would no longer tolerate “state-sponsored provocation” against American assets.

Further, Trump noted that Iran has repeatedly violated the terms of every previous diplomatic deal and confirmed that U.S. forces are going to aggressively target critical infrastructure across the country.

“We are going to hit each and every one of their electric generating plants very hard and probably simultaneously […] We have not hit their oil, even though that’s the easiest target of all, because it would not give them even a small chance of survival or rebuilding,” he added.

The ongoing war in the Persian Gulf has rattled both traditional and emerging markets, and the escalation has led to a massive spike in oil prices immediately after Iran threatened to permanently blockade the Strait of Hormuz.

Since the war began, Bitcoin has dropped nearly 12%; meanwhile, despite its reputation as a safe haven, Gold has also slumped sharply as a surging U.S. Dollar and rising bond yields outweigh geopolitical fears.

Trump says the oil situation will improve

Trump acknowledged concerns over surging gas prices but downplayed the economic impact, saying it was a temporary ”short-term” situation and that he expects global supply routes to open up once Tehran surrenders.

“When this conflict is over, the strait will open up naturally. It’ll just open up naturally. They’re going to want to be able to sell oil because that’s all they have to try and rebuild. It will resume the flowing and the gas prices will rapidly come back down,” he said.

He went on to add that the U.S. Economy is “strong and improving” and the domestic energy sector will be “roaring back like never before.”

“Thanks to the progress we’ve made. I can say tonight that we are on track to complete all of America’s military objectives shortly. Very shortly,” Trump said.

Iran threatens retaliation

Even though Trump said that back-channel discussions for a ceasefire were ongoing, Iranian leaders have vehemently denied that there are any serious talks underway.

After the latest speech, the Iranian Revolutionary Guard has vowed a “devastating” retaliation, adding that so far, the U.S. and Israel have been striking “insignificant” targets.

A spokesperson to the Supreme Leader said the two countries have “incomplete” information about the nation’s underground military capabilities and warned that any further strikes would be met with “crushing, broader and destructive” attacks.

He added that the bulk of Iran’s missile production takes place in ”places that you do not know at all.”

On Wednesday, reports suggested that Iran has blacklisted 18 tech companies, including Silicon Valley giants like Microsoft and Google, stating they would be considered as “legitimate targets” in response to cyber strikes on Iran.

“From now on, for every assassination, an American company will be destroyed,” The Guard, which the U.S. designates as a terrorist organization, warned on Tuesday.

Crypto markets under pressure

Major cryptocurrencies besides Bitcoin—including Ethereum, XRP, and BNB—have started to drop sharply and have losses between 3-5% as of last check.

If the macro situation continues to deteriorate, it could spell trouble for the liquidity of these volatile high-beta assets, especially as Bitcoin is hovering very close to a major support area around $65,000.

If this support breaks, it could trigger a massive wave of liquidations, potentially sending the broader market into a prolonged crypto winter fueled by geopolitical instability.

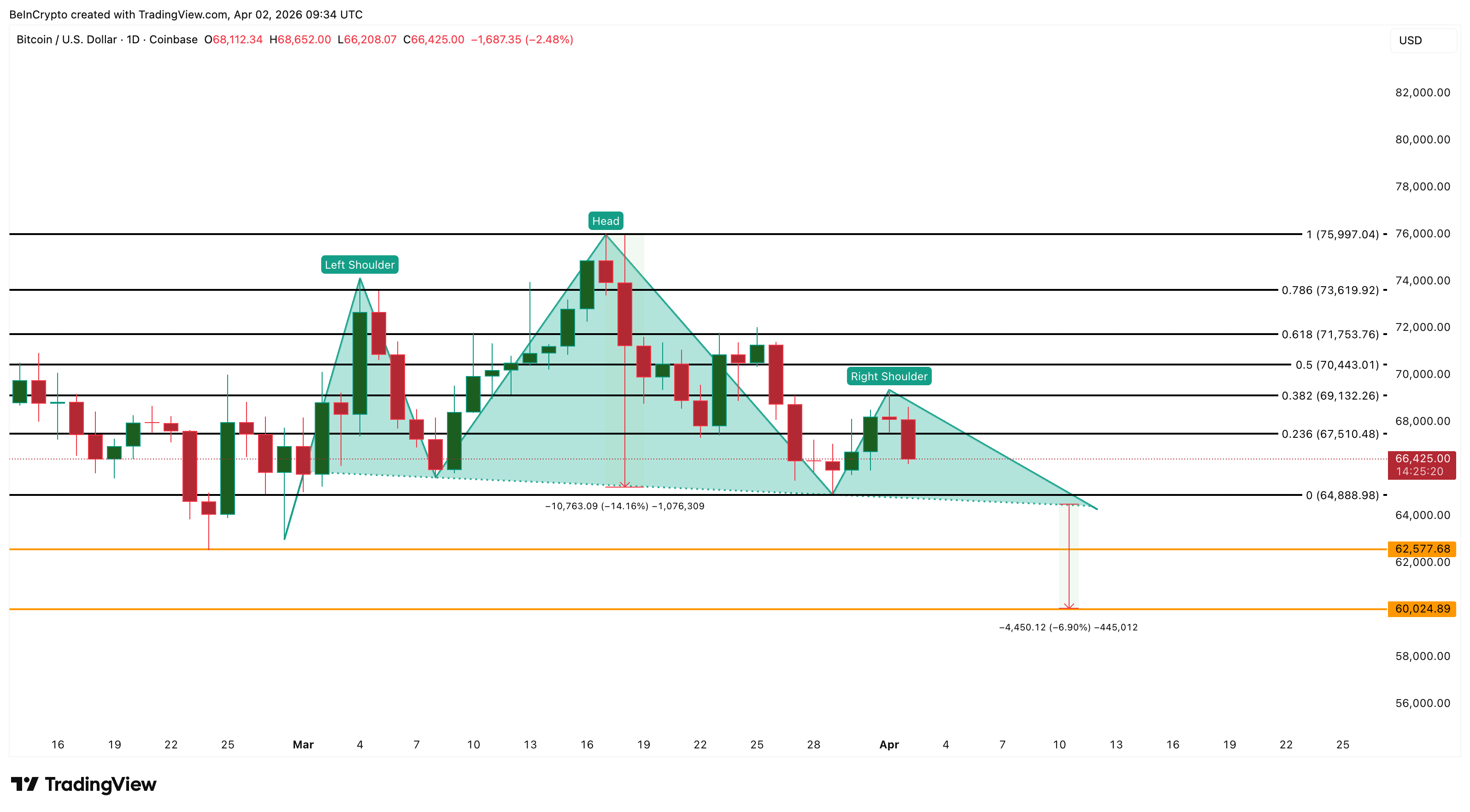

Bitcoin (BTC) price slipped below $67,000 on April 2, falling roughly 2.8% in 24 hours and extending a year-to-date decline that now sits near 23%.

The drop aligns with a pattern forming across on-chain data, chart structure, and derivatives positioning. One cohort of buyers has been steadily exiting since January, and the technical picture now threatens a 14% correction if a key level fails.

The Buyers Who Bought the Dip Are Walking Away

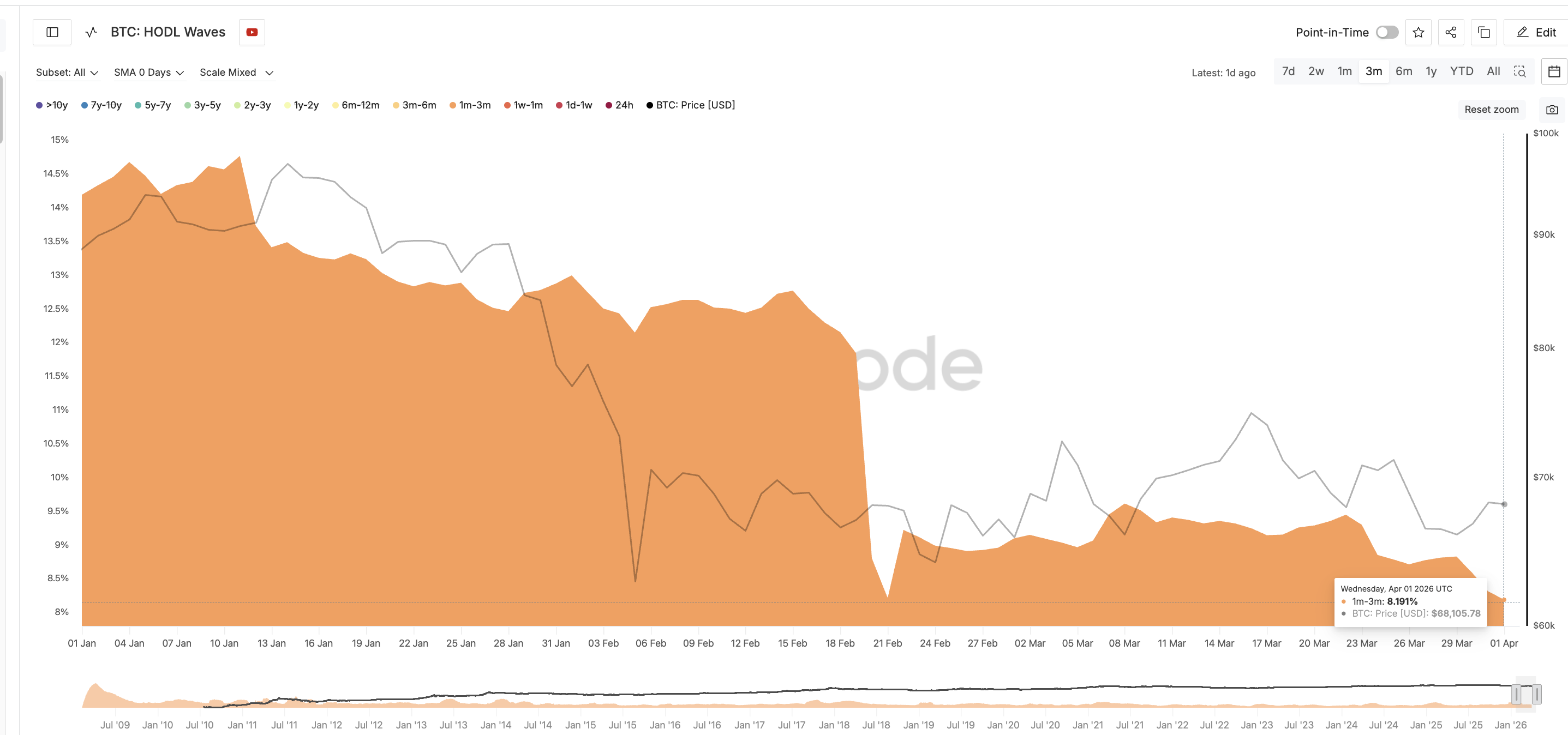

BTC HODL waves, an on-chain metric that tracks the percentage of supply held by different age groups, show a dramatic exit from the 1-month to 3-month cohort. On January 14, this group controlled 14.67% of the total Bitcoin supply. By April 1, that figure had fallen to 8.19%, its lowest reading of the year.

The decline accelerated in two distinct waves. The first came post mid-February, when the cohort’s share dropped from 12.72% on February 15 to single digits by February 22. A second aggressive leg down arrived around March 22, when the reading slipped from 9.44% and continued falling without recovery.

Want more token insights like this? Sign up for Editor Harsh Notariya’s Daily Crypto Newsletter here.

This group represents participants who accumulated during the Q1 drawdown, expecting a bounce. Their persistent selling over nearly three months signals that short-term conviction has evaporated. When recent buyers distribute at a loss rather than averaging down, it typically reflects capitulation rather than healthy rotation.

That behavioral shift is visible on the Bitcoin price chart as well. Since late February, the daily timeframe has been forming a head and shoulders pattern. The pattern validates the weakness that the HODL wave data already flagged.

However, whether the pattern triggers depends on how the derivatives market is positioned around the breakdown zone.

Leverage Leans the Wrong Way

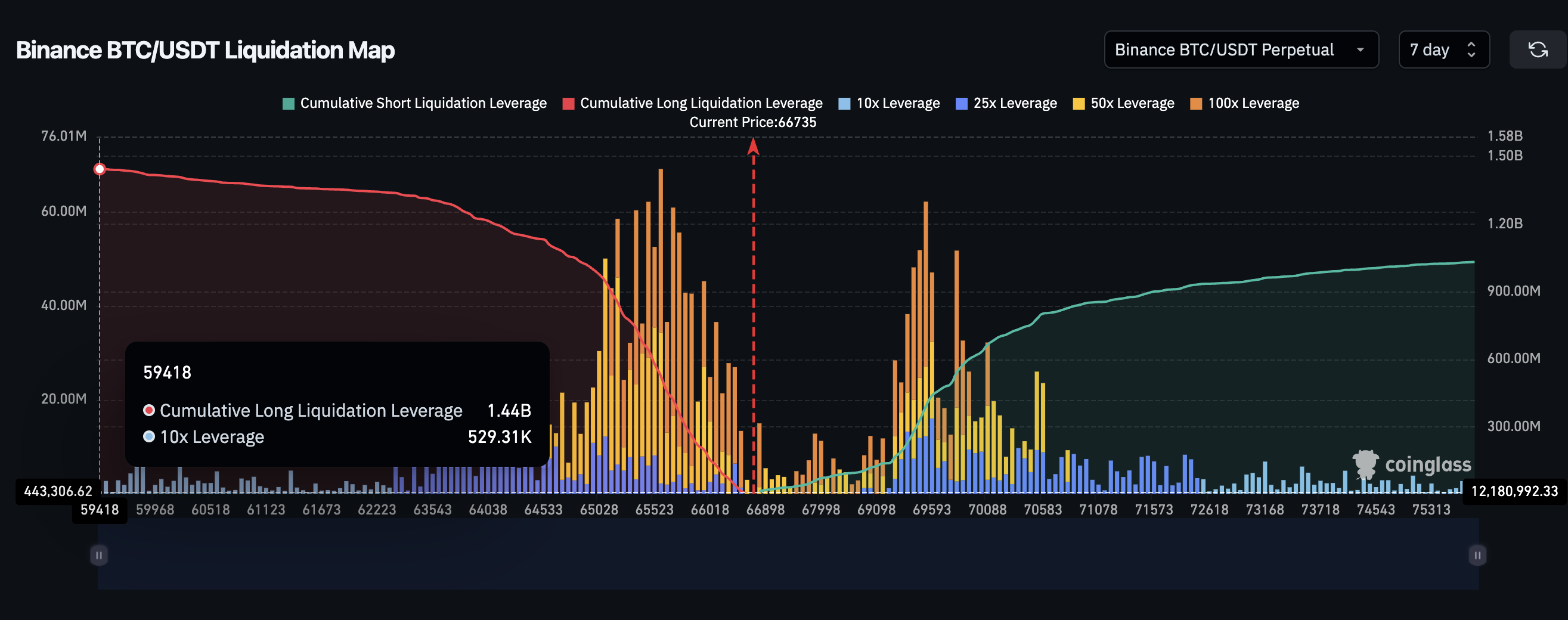

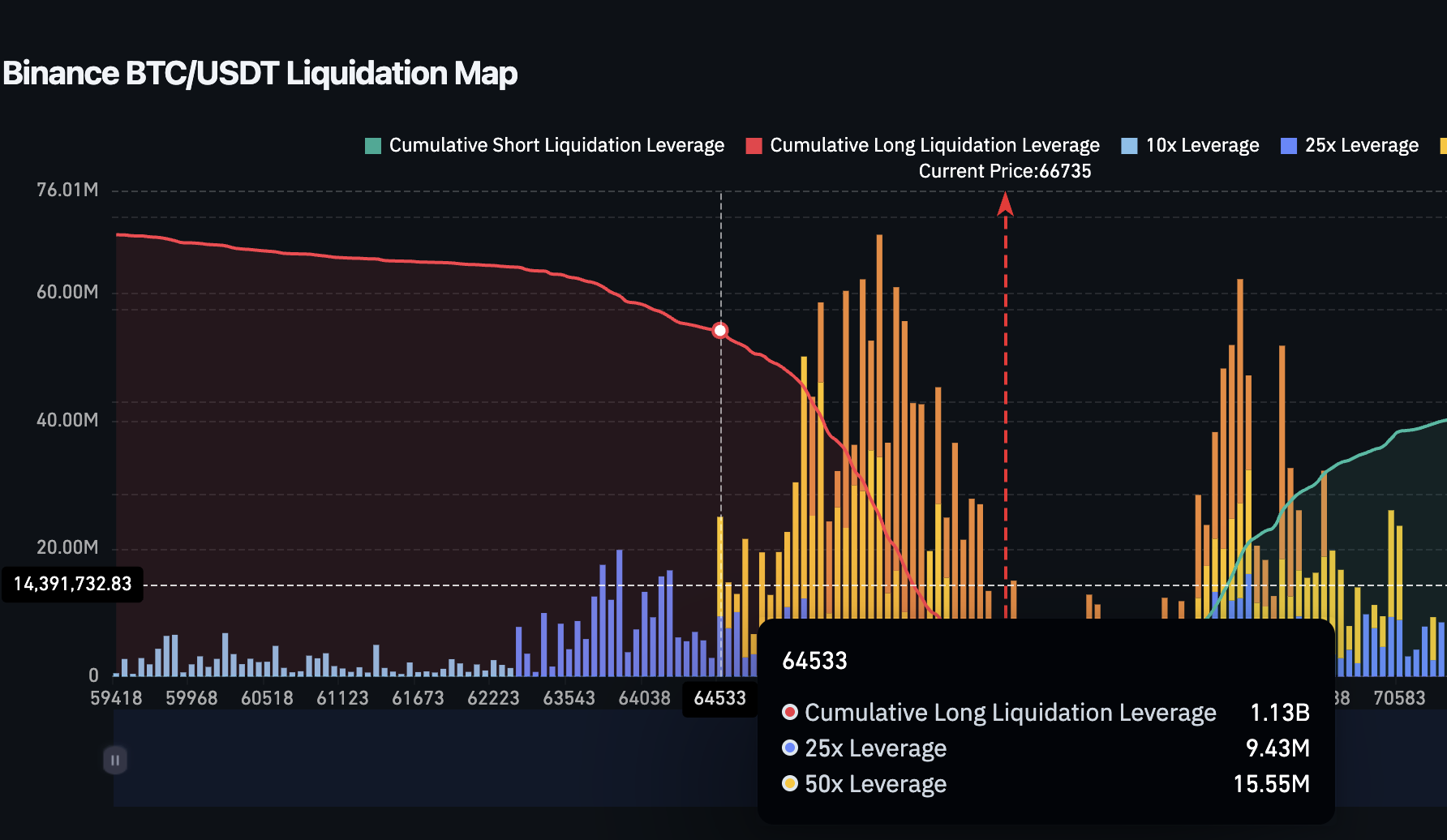

Despite bearish signals from both on-chain behavior and chart structure, the BTC derivatives market has not adjusted defensively. Over the past seven days on the Binance BTC/USDT perpetual pair, cumulative long liquidation leverage totals $1.44 billion in active positions.

Short liquidation leverage sits at $1.03 billion. The roughly 40% skew toward longs means the market remains positioned for upside while the technical picture deteriorates.

The Binance BTC liquidation map sharpens the risk further. Of the $1.44 billion in total long exposure, approximately $1.13 billion clusters at a single level near $64,533. That concentration means nearly 80% of all long positions opened over the past week would be forcibly closed if price reaches that zone.

High-leverage positions using 25x and 50x multipliers dominate the cluster.

Even a modest push into that range could trigger cascading forced selling, turning a controlled decline into a liquidation-driven flush. The mismatch between bearish structure and bullish leverage is where the greatest Bitcoin price risk builds. The BTC price chart now becomes the final arbiter of whether that risk materializes.

Bitcoin Price Prediction and One Critical Line

The daily chart confirms the head and shoulders pattern with Fibonacci (Fib) levels mapping every critical zone. The Fib levels are drawn from the head of the pattern to the completed swing low.

Bitcoin currently trades near $66,425, having already lost the 0.236 Fib level at $67,510.

The measured move from the pattern projects a 14.16% decline, targeting approximately $60,024 on the way down. However, the path runs through $64,888, a level that is slightly above the neckline area for the pattern.

Losing $64,888 would place price directly into the $1.13 billion long liquidation cluster at $64,533 identified in the derivatives section. That overlap transforms the neckline break from a technical event into a leverage-driven cascade. From there the full 14% target, under $60,000 becomes realistic.

For the bearish thesis to fail, Bitcoin price needs a daily close above $69,132 to begin neutralizing the right shoulder. Strength only returns above $71,750, the 0.618 level, and a move past $75,997 would invalidate the head and shoulders entirely.

Head and shoulders patterns do not always resolve in the expected direction. A sudden demand surge or macro catalyst could reverse the structure before the neckline is tested. However, the convergence of capitulating short-term buyers, long-heavy leverage, and declining price structure lowers the probability of that outcome.

A daily close below $64,888 separates a measured pullback from a leveraged flush toward the $60,000 zone, while reclaiming $69,132 would be the first signal that sellers are running out of momentum.

The post One Selling Pattern Reveals the Next Major Bitcoin Price Risk of 2026 appeared first on BeInCrypto.

Key Insights

- GENIUS Act defines state-regulated stablecoin compliance, allowing smaller issuers to operate locally while meeting federal oversight standards.

- OCC guidance establishes federal benchmarks, guiding stablecoin issuers transitioning from state to federal supervision after $10 billion circulation.

- Monthly reserve disclosures and uniform branding rules ensure consistent transparency and regulatory alignment across state and federal stablecoin frameworks.

The U.S. Department of the Treasury has released an 87-page proposal implementing the GENIUS Act. The notice opens a 60-day public comment period and outlines how stablecoin oversight will function across both state and federal systems.

The proposal details how the Treasury will determine whether state-level regulatory frameworks are “substantially similar” to federal standards. Smaller issuers can remain under state supervision if their systems meet the defined benchmarks.

State Stablecoin Oversight Must Meet Federal Standards

Issuers with less than ten billion dollars in circulation may opt for state-level regulation, provided their frameworks align with federal rules. The proposal separates requirements into two categories: uniform rules covering reserves and anti-money laundering and state-calibrated rules where local regulators control supervision, licensing, and risk management.

This approach allows states to maintain flexibility while ensuring all systems comply with the federal baseline, preventing gaps in regulation.

OCC Guidance Shapes Federal Stablecoin Compliance

The Treasury relies on the Office of the Comptroller of the Currency to define the federal benchmark. Nonbank issuers that exceed the $10 billion threshold will transition toward federal supervision guided by OCC standards.

The rule also clarifies that state frameworks may exceed federal requirements, but they cannot conflict with federal law or reduce regulatory comparability.

Stablecoin Disclosure and Branding Rules Enforced

Issuers must publish monthly reserve composition reports to maintain transparency across state and federal systems. This ensures that disclosure practices remain consistent for all regulated stablecoins.

In addition, naming restrictions apply uniformly to prevent misleading branding. These rules align compliance across jurisdictions and maintain public confidence in dollar-backed stablecoins.

GENIUS Act Implementation Drives Regulatory Alignment

The rulemaking represents a key step in turning the GENIUS Act into an operational framework. Passed in July 2025, the law introduced mandatory reserve backing, regular disclosures, and anti-money laundering compliance for payment stablecoins.

Meanwhile, Congress continues advancing complementary measures, including the Clarity Act, to define SEC and CFTC oversight, although disputes over stablecoin yield have slowed broader market reforms.

BITCOIN SUPERCYCLE CONFIRMED BY GOLD

The cheapest petrol and diesel prices in Scotland – check your postcode

Tax changes have rich parents trying to claw back fortunes from kids

-

Business7 days ago

Business7 days agoInstagram, YouTube Found Responsible for Teen’s Mental Health Struggle in Historic Ruling

-

NewsBeat6 days ago

NewsBeat6 days agoThe Story hosts event on Durham’s historic registers

-

Tech7 days ago

Tech7 days agoIntercom’s new post-trained Fin Apex 1.0 beats GPT-5.4 and Claude Sonnet 4.6 at customer service resolutions

-

Sports6 days ago

Sports6 days agoSweet Sixteen Game Thread: Tide vs Michigan

-

Entertainment3 days ago

Fans slam 'heartbreaking' Barbie Dream Fest convention debacle with 'cardboard cutout' experience

-

Entertainment5 days ago

Entertainment5 days agoLana Del Rey Celebrates Her Husband’s 51st Birthday In New Post

-

Crypto World2 days ago

Dems press CFTC, ethics board on prediction-market insider trades

-

Crypto World16 hours ago

Crypto World16 hours agoGold Price Prediction: Worst Month in 17 Years fo Save Haven Rock

-

Tech3 days ago

Tech3 days agoThe Pixel 10a doesn’t have a camera bump, and it’s great

-

Sports2 days ago

Sports2 days agoTallest college basketball player ever, standing at 7-foot-9, entering transfer portal

-

Tech2 days ago

Tech2 days agoEE TV is using AI to help you find something to watch

-

Fashion4 days ago

Fashion4 days agoAmazon Sundays: Soft Spring Layers

-

Tech3 days ago

Tech3 days agoApple will hide your email address from apps and websites, but not cops

-

Tech2 days ago

Tech2 days agoHow to back up your iPhone & iPad to your Mac before something goes wrong

-

Crypto World3 days ago

Crypto World3 days agoU.S. rule change may open trillions in 401(k) funds to crypto

-

Tech2 days ago

Tech2 days agoFlipsnack and the shift toward motion-first business content with living visuals

-

Fashion7 days ago

Fashion7 days agoEn Vogue in Brown Leather and Tailored Neutrals by Atelier Savoir, Styled by J Bolin

-

Politics3 days ago

Politics3 days agoShould Trump Be Scared Strait?

-

Fashion7 days ago

Fashion7 days agoWhat Are Your Favorite T-Shirts for the Weekend?

-

Business6 days ago

Business6 days agoChinese universities with military links bought Super Micro servers with restricted AI chips

You must be logged in to post a comment Login