Crypto World

Arthur Hayes Says Bitcoin Price at $750,000 by 2027 Because Of Money Printing

Arthur Hayes is not backing down on his Bitcoin price predictions.

The BitMEX co-founder is sticking to his bold call: $250,000 Bitcoin in 2026, then $750,000 in 2027. In his view, this cycle is not about charts. It is about liquidity.

Hayes argues the Trump administration will eventually flood the system with money to stabilize growth and keep voters calm. That wave of liquidity, he says, is rocket fuel for hard assets like Bitcoin.

While retail panics through corrections, Hayes is betting on fiscal dominance. His thesis is simple. Governments spend. Currencies weaken. Scarce assets go vertical.

- Arthur Hayes projects $250,000 BTC in 2026 and $750,000 in 2027.

- The forecast relies on the Liquidity Cycle driven by U.S. fiscal spending.

- Institutional flows remain strong with $458.2M entering ETFs Monday.

Arthur Hayes: Why Trump’s Money Printing Could Send Bitcoin Price to $750,000

Governments facing voter pressure will spend aggressively, even if inflation lingers. More spending means more debt. More debt eventually means more money creation. And that is bullish for scarce assets.

Hayes is framing this around one thing: liquidity.

Crypto billionaire Arthur Hayes is predicting a $500k – $750k Bitcoin by end of 2026??? — Altcoin Daily (@AltcoinDaily) March 2, 2026

Trump admin + Iran conflict + Fed easing =

He explains: pic.twitter.com/AU23sd216a

He also ties it to geopolitics. A prolonged U.S.-Iran conflict, in his view, gives the Federal Reserve cover to ease policy again. History shows that during major wars, liquidity tends to expand, not contract. If conflict is financed through debt, the system absorbs it through monetary expansion.

At around $65,000 today, a move to $250,000 by 2026 would mean nearly a 4x return. The 2027 forecast of $500,000 to $750,000 is where the thesis goes exponential. That implies double-digit multiples from current levels.

Is This the Setup for Bitcoin Supercycle Run?

Institutional flows are not matching retail panic.

U.S. spot Bitcoin ETFs just pulled in $458.2 million in one session, with BlackRock’s IBIT alone accounting for $263.2 million. It fits the pattern we have seen before, where extreme fear brings fresh institutional capital back into crypto.

On the chart, $63,000 remains the key support. As long as that holds, the structure stays intact. The real breakout trigger is $72,000. Clear that level and momentum likely shifts toward previous highs.

If $60,000 breaks, though, the correction could extend before any major liquidity wave arrives. For now, $72,000 is the confirmation level that decides whether the next leg up begins.

Discover: The best new crypto in the world

The post Arthur Hayes Says Bitcoin Price at $750,000 by 2027 Because Of Money Printing appeared first on Cryptonews.

Bermuda’s disciplined path to an onchain economy

When Bermuda announces its ambition to become the world’s first fully onchain national economy with support from Circle and Coinbase, you could picture a dramatic, quick overhaul. However, that is not the case.

To be a fully onchain economy, Bermuda has not taken a hard route, which might involve instantly building government services and pushing merchants to accept digital payments. Instead, the island is following a cautious path of well-thought-out, regulated innovation in finance.

The island intends to begin with carefully designed pilots. It will work through licensed and supervised institutions, share the results with transparency and only expand when the systems prove reliable and effective. The goal is to position “onchain” as dependable, everyday infrastructure rather than a radical, quick shift.

What fully onchain means (and what it doesn’t) in this context

As outlined in the announcement at the World Economic Forum, Bermuda is focusing on rolling out digital asset infrastructure across government departments, local banks, insurers, businesses and everyday consumers.

The early emphasis appears to be on stablecoin-powered payments and expanded financial tools rather than abruptly replacing traditional systems.

Here’s what “fully onchain” does not include:

-

No legislation making crypto or stablecoins legal tender

-

No prohibition on cards, bank wires, cash or other conventional payment methods

-

No immediate push for the population to switch to self-custody wallets.

Bermuda’s approach is pragmatic; it focuses on establishing the efficacy of the infrastructure before broadening its reach.

Did you know? Bermuda was among the first jurisdictions to allow insurers and reinsurers to experiment with blockchain record-keeping, long before “onchain economy” became a buzzword.

Credentials of Bermuda for running this experiment

The Bermuda Monetary Authority has built a framework that encourages innovation. This enables Bermuda to execute complex experiments with speed, transparency and accountability.

Bermuda’s regulatory container for crypto

Bermuda has spent years building a robust, supervised framework for digital asset activities. The cornerstone of this system is the Digital Asset Business Act (2018), which empowers the Bermuda Monetary Authority (BMA) to license and oversee firms in this space. This matters because turning an economy “fully onchain” is not just a technical endeavor; it is a holistic effort involving consumers, compliance, risk management and operations.

The BMA’s tiered licensing system — Class T (for pilot/beta testing), Class M (modified requirements for a limited period) and Class F (full operations) — is designed for staged progression.

Firms can start small, test concepts under supervision, demonstrate safety and viability, and scale when ready. This structure supports controlled pilots rather than blanket mandates, allowing regulators to contain risks, gather data and refine rules iteratively.

Smaller systems can iterate faster

Unlike large economies with cumbersome legacy payment systems, deeply ingrained consumer habits and fragmented political interests around money, a compact jurisdiction like Bermuda can move faster. Coordinating across government agencies, key merchants, regulated financial institutions and local stakeholders becomes simpler when the initial focus is narrow.

Rather than overhauling the entire economy, this approach focuses on stablecoin-based flows for things like government fees, permits or targeted disbursements. This combination of strong regulation and agility positions Bermuda to run a structured, evidence-based experiment.

Did you know? Bermuda’s economy relies heavily on cross-border transactions, from insurance premiums to reinsurance settlements, making it unusually sensitive to payment delays. This is one of the reasons blockchain rails appeal more for efficiency than ideology.

Why testing beats mandates for an onchain transition in Bermuda

While Bermuda’s aim is a long-lasting, widely accepted integration of digital assets into its national financial system, “mandates” could risk slowing or complicating the effort.

Mandates invite swift resistance

Pushing widespread use of crypto could lead to immediate pushback over privacy concerns and create an impression of government overreach. People may feel as if changes are being forced on them.

Bermuda’s public statements emphasize a measured, step-by-step approach, and its leadership intends to build confidence first and then broaden access.

Government payments require reliability

Trustworthy execution of government payments requires a series of processes:

-

Secure onboarding and identity verification

-

Processing refunds, disputes or clear non-reversible rules

-

Accurate reconciliation, auditing and reporting

-

Robust fraud monitoring and responsive customer support

-

Controlled vendor onboarding and procurement safeguards.

Pilots allow agencies to trial these processes under strict controls that include limited volumes, vetted providers and specific use cases. This ensures all factors related to transactions function seamlessly before integrating critical public services.

Financial stability and consumer safeguards remain central considerations

Stablecoin-based systems face some specific real-world challenges. These include expectations around redemptions and liquidity, risks from overreliance on one issuer or platform, potential outages, regulatory lapses and user exposure to scams or errors.

Controlled testing enables the government to isolate and manage these risks and gather hard evidence on what fails. It can determine what users find confusing, where vulnerabilities emerge and which protections truly work.

Banking partners prefer predictability over disruption

Modern financial systems rely heavily on established banking networks and correspondent relationships, particularly for international transactions. A sudden mandate could signal regulatory uncertainty or an attempt to bypass traditional rails.

Bermuda’s strategy demonstrates alignment with existing compliance standards rather than a radical break from them. It leverages supervised intermediaries, tiered licensing under the Digital Asset Business Act and infrastructure from players like Circle and Coinbase.

Did you know? Unlike countries experimenting with crypto as legal tender, Bermuda’s population already has near-universal banking access, so onchain pilots are aimed at optimization and not financial inclusion emergencies.

What problem an onchain pilot in Bermuda aims to solve

Bermuda’s initiative positions onchain infrastructure as adequate for everyday uses. It is designed to cut friction, reduce costs and streamline value transfer in areas where traditional systems are slow and expensive.

Official announcements and reporting focus initially on stablecoin payments and merchant enablement. The policy targets real transactional and operational improvements rather than speculative or investment-driven use cases.

When stablecoins enable fast, low-cost settlements that integrate seamlessly into existing merchant systems and reduce payment overhead, onchain may function as a practical utility. People and businesses adopt it because it performs better, not because of regulation or hype.

How a pilot could work in practice in Bermuda

Public details describe initial pilots in government agencies, alongside broader private-sector enablement. Here is a scenario of how a phased pilot might unfold:

-

A specific government department selects a limited use case, such as a permit or refund process.

-

Approved, licensed providers handle payment acceptance, built-in compliance checks and integration.

-

Residents and merchants join voluntarily through user-friendly interfaces, with straightforward fiat off-ramps and dedicated support.

-

The program measures clear objectives such as settlement speed, cost per transaction, fraud incidence, customer support volume, merchant participation rates and user feedback.

-

Data from the pilot guides the next steps: Scale up successful elements, refine pain points or adjust or pause as needed.

This methodical, evidence-driven rollout stands in sharp contrast to broad mandates. It prioritizes controlled experimentation to build reliability and trust before wider adoption.

Partners in Bermuda’s initiative, not a mandate

Bermuda’s initiative is built around active collaboration with Circle and Coinbase. These companies are providing the underlying stablecoin infrastructure, enterprise-grade tools and support for education and user onboarding.

This partnership serves two practical purposes:

-

Execution capability: Running reliable, national-scale digital payments and onboarding flows demands sophisticated engineering, security architecture and operational capacity that most governments do not maintain internally.

-

Trust and integration: Working with well-known, regulated firms lowers friction for local banks, insurers and larger merchants who already recognize and trust these names, making adoption smoother.

Relying on major partners also introduces a significant risk: concentration around one or two providers. This issue can be addressed early through a thoughtful pilot, contingency planning and interoperability considerations.

Frameworks for adoption: Balancing innovation with institutional integrity

To ensure an onchain economy is welcome and not resisted, the supporting rules and transparency matter as much as the technology itself. Key elements include:

-

Optionality: Conventional payment methods (cards, bank transfers, cash) must remain fully available at every stage.

-

Transparency: Clearly communicate the pilot’s scope, any associated fees and regular, public reporting on performance metrics.

-

User protections: Provide straightforward risk disclosures, scam-awareness education, accessible support channels and simple complaint/escalation paths.

-

Privacy and compliance clarity: Explain exactly what data is collected, who can access it, under what legal basis and how it is protected.

-

Resilience measures: Build in provider redundancy, documented incident-response procedures and timely communication during any outages or disruptions.

Bermuda’s emphasis on education and onboarding in its public statements signals that sustainable adoption is earned through usefulness and trust.

Most exchange tokens don’t get talked about until they’ve already made their move. WBT, the native coin of European crypto exchange WhiteBIT, is a textbook example. It spent the better part of 2023 trading under $6 with almost zero mainstream attention. Now it sits above $50, ranks inside the top 15 by market cap, and has quietly outperformed some of the most hyped tokens in the market over the past three years.

So what changed? And more importantly, is there still room to run?

A Slow Build, Then an Explosion

WBT launched in August 2022 and immediately landed in the middle of a brutal bear market. It’s all-time low hit around $1.90 in late 2022, and for most of 2023, it barely moved, closing the year near $5.78. Not exactly the kind of chart that gets people excited.

But things began to change in 2024, when WBT began steadily climbing from $6 to $24 by the year’s end, a quiet 4x that most of Crypto Twitter completely missed. Then, in 2025, the token accelerated, blowing past $30, $40, and $50, eventually touching $65.30 on November 18, 2025. From its lowest point to its highest, that’s over 3,000% in roughly three years.

As of February 2026, WBT is consolidating around $50 with a market cap above $10 billion. On-chain data from earlier this month shows 99.52% of the circulating supply is in profit, which is a rare position for any crypto asset.

Adding to the institutional credibility, WBT was included in the S&P Crypto Indices at the end of 2025, a milestone that puts it on the radar of fund managers and institutional allocators who rely on index inclusion as a baseline for asset legitimacy.

The Engine Behind the Price

Price doesn’t move in a vacuum. Behind WBT’s chart is a business that’s been scaling aggressively.

WhiteBIT is the largest European cryptocurrency exchange by web traffic. It was founded in 2018, and by the end of 2025 its parent entity W Group reported serving over 35 million customers globally with a total capitalization of $38.9 billion. The exchange now operates across multiple regions, recently launching WhiteBIT US as a New York-based entity and entering Saudi Arabia through a cooperation agreement focused on blockchain infrastructure and CBDC development.

WBT isn’t just a token to trade, but is woven into everything on the platform. Holding it unlocks up to 90% off taker fees, 100% off maker fees, free daily ERC 20 withdrawals, boosted referral rates, and staking rewards. That kind of utility creates a natural demand: more users on the platform means more people with a reason to hold WBT.

On the supply side, the tokenomics include a hard cap of 400 million tokens with no future minting. The exchange also runs weekly token burns, gradually compressing the circulating supply, which currently sits around 214 million. Deflationary pressure plus growing demand is a combination that tends to push price in one direction.

Big Brand, Bigger Ambitions

WhiteBIT has made moves that most exchanges in its tier haven’t even attempted. A three-season partnership with FC Barcelona started in 2022. In 2025, they added a global partnership with Juventus FC, complete with kit sleeve branding and a dedicated Crypto Fan Zone for supporters.

These aren’t just marketing stunts but signal the kind of institutional credibility that attracts larger players. WhiteBIT now serves over 1,300 institutional clients with solutions spanning OTC trading, liquidity provision, custody, and Crypto-as-a-Service. The WhiteBIT Nova debit card processed over $50 million in its first year. WhitePool, their mining operation, climbed into the top 15 globally.

Each of these developments feeds back into WBT demand.

What to Watch From Here

WBT is currently sitting about 25% below its all-time high. The consolidation around $50 after a massive run is healthy, but the next move depends on a few key factors.

On the bullish side: the US launch is still in its early stages, the Saudi expansion opens a massive new market, weekly burns continue to tighten supply, and a broader crypto bull cycle could lift all boats. As of today, Kraken has also added WhiteBIT Coin (WBT) to its Tokens Launching Soon roadmap on its official listings page, signaling upcoming support on one of the world’s largest exchanges, a potential catalyst for fresh demand.

On the cautious side: exchange tokens are directly tied to platform performance. Increased competition, regulatory shifts, or a prolonged market downturn could slow things down.

Either way, the data makes one thing clear. WBT’s move from $3 to $65 wasn’t luck. It was built on real users, real utility, and real growth. Whether you’re watching it or holding it, this is a token worth understanding.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Always do your own research before making investment decisions.

The post WBT Did a Quiet 15X While Everyone Was Watching Meme Coins appeared first on Cryptonews.

TLDR

- Unified platform from Crypto.com enables tax-advantaged growth of both equities and cryptocurrencies.

- Staking capabilities and integrated portfolio management available through Crypto.com IRAs.

- Both Traditional and Roth retirement accounts offered with contribution matching up to 5%.

- Access to stocks, ETFs, and 400+ digital tokens within a single user interface.

- Multi-asset retirement accounts signal evolving convergence of digital and conventional investments.

Crypto.com has unveiled a groundbreaking retirement solution for U.S. investors that merges equities and digital currencies within a unified platform. This innovative service enables account holders to maintain stocks, exchange-traded funds, and crypto assets under tax-advantaged retirement vehicles. Both Traditional and Roth IRA variants are now directly available through Crypto.com’s ecosystem.

The platform delivers an opportunity for investors to diversify across multiple asset categories while maximizing tax efficiency. Traditional IRAs offer tax-deferred accumulation, while Roth accounts provide tax-free growth potential. Account holders can execute contributions, transfer existing accounts, and complete rollovers without incurring fees.

Crypto.com provides incentives including up to 5% matching on contributions and up to 2% on transfers and rollovers. These benefits are designed to drive user adoption and accelerate retirement savings growth. Integrated portfolio management capabilities are embedded within the application.

IRA Features Include Crypto Holdings and Staking Rewards

The Crypto.com IRA platform accommodates bitcoin, ethereum, and over 400 additional digital currencies. Multiple tokens are eligible for staking and lockup mechanisms, allowing account holders to generate supplemental yields within their retirement accounts. According to IRS guidelines, staking income is subject to taxation in the year received.

The service also facilitates trading of equities, ETFs, and cryptocurrencies through a consolidated interface. Advanced features like Recurring Buys and Whale Baskets provide enhanced flexibility and automation for portfolio construction. Users can track performance and rebalance holdings directly within the Crypto.com application.

Crypto.com facilitates enhanced yield generation by enabling compounding of crypto staking income. Earned rewards are systematically deposited into retirement accounts, fostering long-term asset accumulation. This framework establishes an integrated approach to blending digital and traditional investment vehicles.

Market Context and Regulatory Environment

This product launch aligns with expanding mainstream adoption of cryptocurrency within U.S. retirement planning. Policy initiatives have promoted greater accessibility, with executive directives and legislative measures endorsing crypto participation. Major financial institutions like Morgan Stanley have similarly expanded digital asset options for their clientele.

Unlike employer-provided 401(k) programs, these Crypto.com retirement accounts function as individual vehicles. Investors retain full authority over asset selection and account administration. Custodial arrangements for stocks and ETFs were not specified, while cryptocurrency custody operates through the platform infrastructure.

Crypto.com is positioning itself within an emerging sector of multi-asset retirement products that bridge conventional securities and blockchain-based assets. This development mirrors widespread momentum toward portfolio diversification and digital asset adoption. The platform consolidates access to equities, ETFs, cryptocurrencies, and yield opportunities, streamlining comprehensive retirement preparation.

A confidential blockchain advisory agreement between Libra co-creator Hayden Davis and Argentinian president, Javier Milei, has been discovered on a suspect’s phone during the country’s ongoing investigation into the collapse of the LIBRA token.

That’s according to La Nación and sources familiar with the results of a January 9 report led by the Public Prosecutor’s Office (MPF).

The department’s computer experts reportedly recovered multiple copies of the agreement from Mauricio Novelli’s seized phone. The document appeared in exchanges between himself and Davis as various drafted iterations before the final version was signed by Milei.

The Argentinian president reportedly still denies the existence of the “confidential agreement” that cemented Davis’ role as the country’s blockchain advisor and, in turn, his association with LIBRA’s launch on February 14, 2025.

Novelli is part of a group of lobbyists, alongside Manuel Terrones Godoy and Sergio Morales, who allegedly helped launch and profited from LIBRA’s collapse.

Read more: Javier Milei disbands crypto unit he set up to investigate himself

Prosecutor Eduardo Taiano said that the MPF’s findings mean that the undersecretary of presidential affairs, who reports to Milei’s sister, General Secretary Karina Milei, will now have to confirm whether or not she has copies of the secret agreement.

The report also found Novelli played a key role in organizing the LIBRA launch and maintained contact with both Milei and his sister, Davis, Terrones Godoy, Morales, and Julian Peh, the CEO of the KIP protocol, which helped launch the token.

Multiple messages between Novelli and other parties were also found to have been deleted, but some messages were recovered after forensic extraction.

“All individual conversations and those related to WhatsApp groups made up of Novelli, Terrones Godoy and Sergio Morales were found to be empty or had been deleted,” analysts claimed.

One exchange involved Cardano founder Charles Hoskinson who accused Terrones Godoy of demanding a five-figure sum of money to meet Milei.

Hoskinson was promised “magical things will happen,” but refused the offer.

Hayden Davis-linked wallets sent $1M USDC after signing deal

Argentinian outlet Clarín revealed that Milei had signed a “confidential agreement” with Davis 15 days before the launch of LIBRA. It was subject to a non-disclosure agreement and required Davis to provide unpaid blockchain advice “ad honorem.”

Davis would “provide professional support, in line with global trends in decentralization and technological modernization, ensuring the highest quality and confidentiality at every stage of the advisory process.”

On the day it was signed, two payments of USDC worth roughly $1 million, were sent from Davis-linked wallets to the wallet of 75-year-old Orlando Rodolfo Mellino, a retiree with no real address, who then sent the funds to a wallet linked to Novelli.

Read more: LIBRA case judge orders full disclosure of Javier Milei bank accounts

La Nación reports that after a year, the investigation into LIBRA has been carried out at varying speeds, and has witnessed delays in key areas, such as the disclosure of the report into Novelli’s devices. It adds that Milei is yet to hire a lawyer to represent himself.

Meanwhile, Davis appeared to be walking free as of December 2025. Crypto analytics firm Bubblemaps recently claimed that Davis had made $15 million from Pump Fun’s private token sale just six months after LIBRA’s launch.

However, Bubblemaps then deleted its findings after Pump Fun’s pseudonymous CEO, Alon Cohen, called it defamatory “misinformation.” He said, “No one from the team ever spoke to the guy, I didn’t even know he existed until after the scandal.”

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

Visa is expanding its stablecoin-linked card program with Bridge, broadening its geographic reach and pushing toward onchain settlement. The latest move lifts the program from its initial Latin American rollout to 18 countries, with a plan to surpass 100 countries across Europe, Asia-Pacific, Africa and the Middle East by year-end. The expansion builds on the program’s April 2025 debut in markets including Argentina, Colombia, Ecuador, Mexico, Peru and Chile, and comes as the two companies test settlement directly in stablecoins through a pilot tied to Visa’s rails and Bridge’s banking partner. The broader industry context features heightened activity around stablecoins in payments, with rival initiatives in the space highlighting a competitive push toward real-time, programmable settlement.

Key takeaways

- Visa and Bridge are extending the stablecoin-linked card program to 18 countries, with a target of more than 100 countries by year-end across Europe, Asia-Pacific, Africa and the Middle East.

- The program’s initial launch in 2025 covered Latin American markets, including Argentina, Colombia, Ecuador, Mexico, Peru and Chile.

- Settlement is moving toward onchain processing, enabled by Bridge’s collaboration with Lead Bank, allowing transactions to be settled in stablecoins instead of fiat.

- Visa is evaluating potential support for Bridge-issued assets, which are created programmatically by businesses rather than by a traditional issuer.

- The move comes amid broader payments-industry activity around stablecoins, including Mastercard’s recent stablecoin card enablement with MetaMask in the United States.

Tickers mentioned: $USDT, $USDC

Market context: The expansion aligns with a wider shift toward crypto-enabled payments and onchain settlement rails, as major incumbents test how tokens can streamline merchant settlements and reduce counterparty risk in everyday purchases.

Market context: Linked to broader USDt and USDC usage in payments, the push also sits against a backdrop of regulatory scrutiny and ongoing experimentation with tokenized settlement in traditional rails.

Why it matters

The enhanced collaboration between Visa and Bridge underscores a strategic bet on programmable, onchain settlement as a means to speed up merchant settlements and improve transparency for card programs built on stablecoins. By enabling issuers and acquirers to settle transactions directly in stablecoins, the network could reduce latency and friction inherent in fiat conversions, especially for cross-border transactions or cross-currency purchases. The approach also signals an appetite to expand the set of tools available to fintechs and brands that want to issue their own digital dollars or stable assets tailored to their customer base, without relying solely on a third-party issuer.

Bridge’s participation remains central to the evolution of these rails. The program leverages Bridge’s infrastructure to enable onchain settlement, with Lead Bank providing the regulatory and banking framework necessary to move transactions from card networks into the onchain ecosystem. In practice, this arrangement allows card issuers to settle in stablecoins rather than converting transactions to local fiat post-authorization, aligning settlement timelines with blockchain realities and potentially improving settlement finality for merchants and consumers alike.

From a competitive standpoint, the Visa-Bridge expansion sits alongside a broader trend in the payments space: the growing willingness of major processors to experiment with crypto rails. Mastercard, for example, has recently enabled stablecoin card spending in the US through a partnership with the MetaMask wallet, illustrating how traditional payment networks are responding to consumer interest in crypto-backed payments and the desire for real-time settlement capabilities. The juxtaposition of these efforts signals a broader industry push toward integrating crypto-native settlement with fiat-backed consumer spending, while navigating the regulatory and risk considerations that come with such a transition.

Visa’s crypto leadership has been clear about meeting businesses where they operate. Cuy Sheffield, Visa’s head of crypto, has framed the expansion as part of a broader strategy to bring the speed, transparency and programmability of stablecoins into the settlement process. The company is exploring how Bridge-issued assets—stablecoins that are created programmatically by businesses on Bridge’s platform—could be supported more broadly within Visa’s network, a path that could unlock new programmable currency options for merchants and brands that want to control settlement terms or tokenized reward structures. Unlike the most widely used stablecoins issued by independent entities, Bridge-issued assets are designed to be created and managed via Bridge’s infrastructure, a model that could appeal to fintechs seeking bespoke token strategies.

Bridge has positioned the expansion as a step toward more seamless, on-chain settlement for digital-asset-enabled card programs. The practical effect is a potential reduction in the time and complexity involved in moving value from a customer’s stablecoin balance to a merchant’s local currency—an outcome that could matter for shoppers who want near-instant payments and for issuers seeking tighter control over settlement economics. The program’s onchain settlement is described as a natural extension of Bridge’s rail, with Lead Bank acting as the bridge between traditional banking and the onchain settlement layer. In a mid-February update, Bridge noted that it had received conditional approval from a regulator to become a national trust bank, a milestone that underscores the regulatory dimensions of this kind of expansion and the careful navigation required to scale such rails.

As part of the broader, ongoing stablecoin race in payments, Visa’s initiative adds to a landscape where banks and fintechs are willing to experiment with programmable money at the point of sale. The expansion’s strategic rationale rests on creating more options for merchants to accept stablecoins without abandoning familiar payment interfaces, and for consumers to transact with tokens that can be settled efficiently. By aligning with Bridge’s architecture and Lead Bank’s regulatory framework, Visa is building a more integrated model where stablecoins do not live only in wallets or exchanges but become a practical settlement instrument for everyday card purchases.

The announcement also highlights a broader industry trend: the move toward enhanced interoperability between card rails and blockchain settlement. If the onchain settlement pilot proves scalable, issuers may gain more flexibility in structuring rewards, fees and settlement terms around stablecoins, potentially broadening the appeal of crypto-enabled cards to a wider audience of merchants and cardholders. While regulatory considerations remain a constant backdrop, the practical demonstrations of speed and transparency in settlement have kept this initiative in the spotlight as a potential blueprint for future integrations across the payments ecosystem.

What to watch next

- Timeline and results of the onchain settlement pilot with Lead Bank and Bridge; potential adjustments to settlement cadence and liquidity requirements.

- Progress toward the goal of reaching 100+ countries by year-end, and which markets will be prioritized in the near term.

- Details on Visa’s potential support for Bridge-issued assets and any regulatory approvals that shape that path.

- Regulatory developments regarding Bridge’s national trust bank status and how they affect cross-border card programs.

Sources & verification

- Visa and Bridge expansion to over 100 countries: official Visa investor relations announcement.

- Original Latin American rollout: Visa and Bridge collaboration announcement outlining the April 2025 launch.

- Onchain settlement pilot and Bridge-Lead Bank collaboration: Visa press materials and Bridge announcements, including regulatory status updates.

- Industry context: Mastercard’s stablecoin card spending in the US via MetaMask—contextual reference in related coverage.

Key figures and next steps

Market reaction and key details

Why it matters

The Visa-Bridge collaboration represents a deliberate push to embed stablecoins deeper into everyday payments while testing the viability of onchain settlement for consumer card programs. If the pilot demonstrates efficiency gains and regulatory viability, issuers and merchants could gain access to more flexible settlement terms and new token-based monetization options. For users, the prospect of faster settlement and more predictable funds availability could enhance the appeal of stablecoins as a practical payments tool, particularly for cross-border purchases and commerce that spans multiple currencies.

Beyond Visa, the broader payments ecosystem is watching how these rails will coexist with existing fiat-based settlement, risk controls, and compliance regimes. The tension between innovation and regulation remains a key driver, but the ongoing experiments with stablecoins at the point of sale reflect a maturing phase in crypto-enabled payments where real-world usage and governance concerns are increasingly aligned. As more institutions participate, the competence and reliability of onchain settlement in consumer contexts will be tested under a variety of market conditions, from everyday retail transactions to cross-border remittances.

What to watch next

- End-of-year milestones for country expansion and the potential scaling of onchain settlement.

- Regulatory updates on Bridge’s national trust bank status and related compliance requirements.

- Adoption metrics from merchants and issuers participating in the program, including any changes in settlement times and cost structures.

Bitcoin perpetual open interest posts its largest daily rise since 2025 as BTC stalls below $70k.

Summary

- Perpetual open interest records its biggest daily percentage increase since July 2025 as BTC tests $69.4k resistance.

- Leverage expands sharply into a failed breakout attempt, leaving speculative longs vulnerable to liquidations if price moves away from the $69k–$70k zone.

- BTC trades just under $70k with elevated open interest and hotter funding, signaling higher short-term volatility risk for derivatives markets.studio.

Bitcoin’s (BTC) derivatives market has shifted into a more fragile configuration after a sudden surge in perpetual futures open interest coincided with a stalled breakout attempt just below the psychologically important $70k level. On-chain analytics firm glassnode reported that perpetual open interest saw its largest daily percentage jump since July 2025 as BTC pushed to $69.4k, only for the move to fade without a clean break of resistance. The pattern suggests speculators rushed to add leverage in anticipation of a breakout that did not materialize, leaving a substantial cluster of long positions now exposed to any downside or extended consolidation.

The mechanics are straightforward: when open interest spikes faster than spot prices, it usually signals an influx of leveraged capital rather than organic spot demand. In this case, the new positioning came right as BTC approached the $69.4k–$70k band that several technical analysts identified as a key decision area for the market. If price fails to extend higher, even a modest pullback can push stretched longs toward margin limits, forcing them to reduce risk or face liquidations. The result is a market where short-term moves can become exaggerated as derivatives flows feedback into spot, especially on high-volume venues tracked by platforms such as Coinbase.phemex+4

Leverage and market structure

Several recent analyses have highlighted $69.4k–$70k as a pivotal zone where BTC (BTC) either breaks higher into a new leg up or resolves into a deeper correction. With perpetual open interest now elevated, futures traders are effectively amplifying whichever direction comes next, increasing the probability of a sharp squeeze rather than a calm drift. A clean move above $70k would likely force shorts to cover into strength, while a breakdown below nearby supports in the high-$60k area could trigger a cascade of long liquidations.

The episode underscores how much short-term BTC price action is still dictated by derivatives rather than spot flows, even as regulated products and frameworks like MiCA slowly reshape parts of the market. For traders, the signal is blunt: high leverage near major resistance rarely stays comfortable for long. Watching open interest, funding, and liquidation data in real time—alongside spot metrics from exchanges like Coinbase and aggregated price feeds for BTC—remains essential for managing risk in an environment where a crowded bet on a $70k breakout can quickly turn into a scramble for the exits.

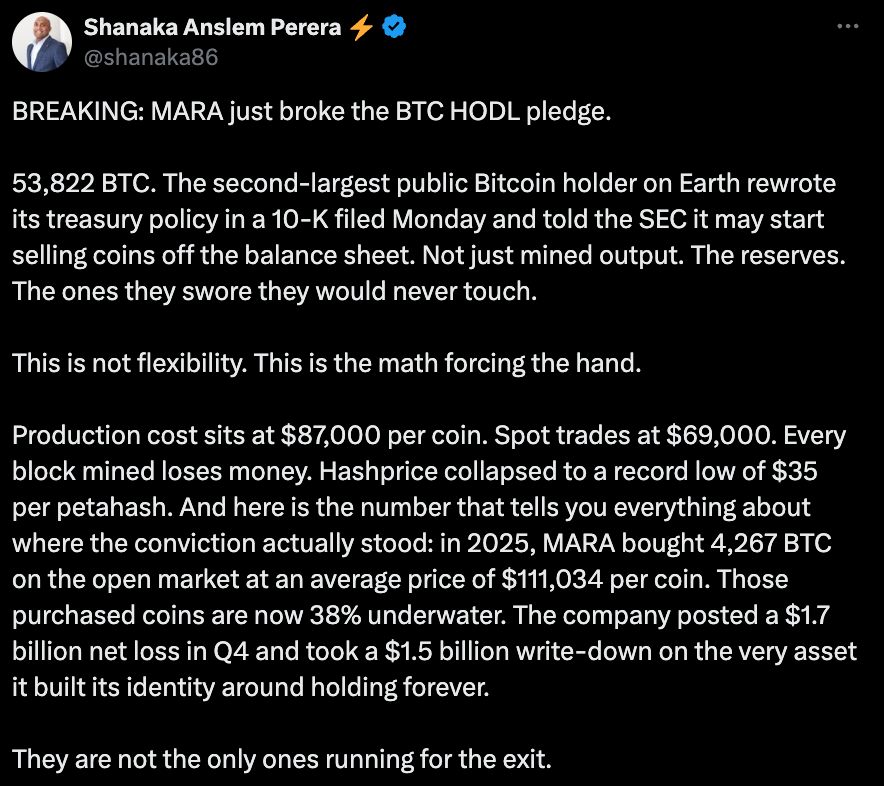

In a Monday SEC filing, the US Bitcoin miner said it would consider selling some of the coins on its balance sheet, depending on market conditions.

US-based cryptocurrency miner MARA Holdings made waves after a regulatory filing signaled that the company could change its HODL strategy.

In a Monday filing with the US Securities and Exchange Commission (SEC), MARA said it was open to selling some of its Bitcoin (BTC) holdings “from time to time” depending on market conditions and its investment priorities. According to the miner, it changed its strategy to allow for BTC sales in 2026, while Bitcoin sales generated from mining at the company have been permitted since 2025.

MARA’s strategy shift comes as many crypto mining companies are pivoting some of their infrastructure into artificial intelligence (AI) and high-performance computing (HPC) amid increasing BTC difficulty and associated costs. On Monday, Riot reported a net loss of $663 million for 2025 in part due to the value of its Bitcoin holdings, while Core Scientific said its Q4 2025 revenue was down 16% from the year-earlier period.

“This is not flexibility,” said analyst Shanaka Anslem Perera in a Tuesday X post on MARA’s SEC filing. “This is the math forcing the hand. Production cost sits at $87,000 per coin. Spot trades at $69,000. Every block mined loses money. Hashprice collapsed to a record low of $35 per petahash.”

He added:

“The entities that mine Bitcoin no longer want to hold it. The entity that holds the most Bitcoin [Michael Saylor’s Strategy] has never mined a single satoshi. Production and accumulation have fully decoupled for the first time in this asset’s sixteen-year history.”

MARA announced last month that it had acquired a 64% stake in computing infrastructure operator Exaion, in a move to strengthen its position through HPC and AI. Similarly, digital infrastructure company Terawulf reported last week that it expects additional growth in 2026 fueled by AI and HPC contracts.

Related: Will Bitcoin crash if oil prices hit $100 per barrel?

At the time of publication, BTC was trading hands for $67,717, off by more than 13% in the past 30 days. MARA reported holding 53,822 BTC as of Dec. 31, then worth about $4.7 billion. At current price levels, that equates to $3.64 billion.

How the US-Iran conflict is affecting Bitcoin

The military actions taken by the United States and Israel against Iran during the weekend spurred concerns over oil supplies and inflation. The price of Bitcoin failed to stay over $70,000 on Tuesday while even assets like gold experienced some volatility amid concerns of a drawn-out conflict.

Magazine: Would Bitcoin really be at $200K if not for Jane Street? Trade Secrets

Harvard University endowment’s decision to trim its bitcoin holdings while adding exposure to ether (ETH) has raised a familiar question: Is the endowment making a bet on Ethereum over Bitcoin, or simply adjusting risk?

The answer may be less dramatic than it appears and potentially bullish for the sector.

Michael Markov, co-founder and chairman of Markov Processes International, who studies university endowments, said crypto is likely the most volatile part of Harvard’s public markets portfolio. In the fourth quarter of 2025, price swings in both bitcoin and ether surged, with both assets losing around 25% of their value.

These sharp price swings have, at least in part, led Harvard to rebalance its portfolio, even if it did not change its long-term view of bitcoin. When an asset becomes more volatile and riskier than intended in a portfolio, cutting back restores balance.

“When volatility rises sharply, the risk contribution of that sleeve can expand disproportionately relative to its capital weight,” Markov said. In that setting, he added, trimming exposure can happen “without implying a strategic shift.”

Simply put, Harvard, which bought BlackRock’s bitcoin ETFs last year, likely didn’t lose its conviction in bitcoin; rather, it moved to rebalance its risk appetite.

In fact, it’s not just a crypto-specific move. Rebalancing capital out of assets that have done well and into underperforming sectors is something most Wall Street portfolio managers do to keep returns fixed. The idea is to rebalance the portfolio ahead of a market rotation, moving outperforming assets into underperforming ones to capture an eventual shift in sentiment.

For example, given sky-high valuations of traditional equities, some of these endowments, which tend to focus on long-term return, have begun looking into other alternative investment ideas, including digital assets-related ETFs. Harvard first bought bitcoin in the third quarter of 2025, allocating roughly 20% of its reported U.S.-listed public equity holdings into the crypto asset. The idea is not to overhaul portfolios but to add measured exposure that could lift returns in years when crypto or underperforming assets perform well, and traditional equities start to lose their higher valuations.

Another possibility is liquidity.

Harvard has increased its allocation to private equity in recent years, Markov noted, pushing more capital into long-term, illiquid investments. At the same time, billions of dollars in unfunded commitments remain on the books. That creates pressure on the smaller slice of the portfolio that can be sold quickly.

“That means the liquid sleeve is relatively small compared to the capital call obligations,” he said. When that happens, and investors such as Harvard need to fund capital investment requests from private equity, they tend to sell more liquid, publicly traded assets to fulfill those commitments.

“Selling some public ETFs – including crypto ETFs – is mechanically the easiest way to manage that pressure,” according to Markov.

Crypto demand

Despite the need to rebalance out of volatile assets or to fund other capital commitments, Harvard didn’t exit crypto.

Instead, it added almost 3.9 million shares of BlackRock’s ether ETF, currently valued at $56.6 million.

Samir Kerbage, chief investment officer at Hashdex, sees that move as part of a broader institutional shift into digital assets and beyond just investing in bitcoin.

“Harvard’s purchase of Ethereum ETFs is a clear sign of institutional demand for crypto assets beyond bitcoin,” Kerbage said. He pointed to the GENIUS Act — passed into law in July — making it easier for large allocators to navigate the crypto landscape.

As rules around stablecoins and tokenized securities take further shape, investment committees of large institutions may feel more comfortable backing networks that support those applications.

Ethereum sits at the center of much of that activity. Over the past few years, it has become the main network for stablecoins, tokenized funds and other onchain financial applications used by asset managers and fintech firms. Unlike bitcoin, it offers institution-level staking, allowing holders to lock up tokens to help secure the network and earn yield. That feature can make ether look less like a pure directional bet and more like exposure to the underlying infrastructure powering digital financial services.

Kerbage also expects institutions that move beyond bitcoin to favor diversified products, but slowly. While some allocators may consider assets such as ether, XRP or solana (SOL) on their own, he said many will likely choose index-style vehicles instead.

“This ongoing trend is not because it’s the fashionable choice, but because the alternatives are genuinely hard,” Kerbage said, citing questions such as which tokens to hold, how much to allocate and when to rebalance. “These aren’t crypto-specific problems.”

However, for a giant fund like Harvard signaling a desire to expand further into digital assets, even slowly, is likely positive for crypto, as even a few years ago, this was unthinkable.

Taken together, Harvard’s bitcoin trim and ether buy may reflect two things: managing short-term risk and cash needs, while slowly expanding beyond bitcoin as U.S. crypto rules become clearer. Ultimately, it’s likely a broader sign of further institutional confidence in digital assets.

Bitcoin (CRYPTO: BTC) pulled back from its recent tilt toward the $70,000 threshold as geopolitical tensions in the Middle East intensified concerns about oil supply and global inflation. The closure of the Strait of Hormuz sparked a broad risk-off mood, with equities slipping and safe-haven assets showing mixed performance. By midday, BTC hovered near the $66,000 area after retreating from its earlier highs, underscoring how macro headlines continue to drive crypto liquidity and price action. A data point from TradingView highlighted a roughly 3.2% intraday decline, reinforcing traders’ focus on momentum and key technical levels in a volatile environment.

Key takeaways

- Bitcoin (CRYPTO: BTC) failed to sustain a move toward $70,000 as energy-market tensions resurfaced following Hormuz-related disruptions.

- Major equity indices were weaker at the open, with the S&P 500 and Nasdaq each down around 2%, and gold also retreating as risk appetite deteriorated.

- BTC price action remained range-bound and failed to break through critical trend lines, a dynamic traders described as evidence of persistent bearish pressure.

- Analysts linked the session to a broader risk-off cycle driven by oil supply concerns and potential inflationary stress, affecting both crypto and traditional markets.

- While some voices cautioned that BTC could see a rotation opportunity if macro conditions stabilize, the near-term path remained uncertain.

Tickers mentioned: $BTC

Sentiment: Bearish

Price impact: Negative. BTC dropped about 3.2% on the day, returning to the $66,000 region as volatility in oil and cross-asset liquidity weighed on prices.

Market context: The move sits within a broader risk-off backdrop where energy-market shocks, inflation concerns, and geopolitical headlines shape appetite for both traditional assets and digital currencies. The episode underscored how crypto trading remains tethered to macro risk sentiment and liquidity dynamics that can shift quickly in response to geopolitical developments and energy data.

Why it matters

The day’s price action sheds light on Bitcoin’s evolving role in diversified portfolios during periods of geopolitical stress. As oil markets react to potential supply disruptions, the resulting spillovers to equities and currencies can compress risk-on assets, including digital currencies. The observed dynamics imply that BTC is not immune to macro shocks and that its appeal as an inflation hedge or portfolio diversifier may be contingent on broader liquidity conditions and investor risk tolerance.

For market participants, the session highlighted the importance of risk controls and scenario planning. While some analysts had suggested a rotation from gold into BTC as a store of value during periods of stress, the evidence from this single session indicates a more nuanced relationship. The price resilience of BTC in some shorter timeframes contrasts with the larger-timeframe momentum that favored bears, suggesting a wait-and-watch period for a clearer directional signal.

Looking ahead, the interplay between oil-market volatility, inflation expectations, and crypto liquidity will likely calibrate how traders approach BTC in the near term. If macro headwinds ease and risk assets stabilize, BTC could retest upside levels; if not, a continuation of range-bound trading or further downside pressure remains plausible. Investors should monitor whether BTC can reclaim key levels or remain anchored in a consolidative range while macro headlines evolve.

What to watch next

- Oil-price trajectories and official updates on energy supply risks, particularly around chokepoints like Hormuz, over the next several sessions.

- BTC price levels: watch for a decisive move above $70,000 or a clear break below $66,000 to signal a new short- or medium-term direction.

- General risk sentiment: observe moves in the S&P 500 and Nasdaq for continued correlation or decoupling from crypto markets.

- Geopolitical developments: any escalation or de-escalation could rapidly reframe liquidity and volatility in crypto markets.

Sources & verification

Market reaction and key details

Bitcoin (CRYPTO: BTC) traded in a narrow corridor as macro headlines continued to drive prices. The market faced a risk-off tilt after the Strait of Hormuz closed, amplifying concerns about oil-supply interruptions and potential inflationary pressures. In this environment, equities pulled back and safe-haven assets vacillated, with gold not providing the shelter some had anticipated. Data from TradingView captured BTC’s movement, showing a roughly 3.2% decline on the day and a retreat toward the $66,000 mark. The price action followed a broader pattern of cross-asset sensitivity to geopolitical risk and energy-market signals.

“The market is beginning to price-in a longer war,” The Kobeissi Letter wrote on X, reflecting a shift in risk perception as geopolitical tensions persisted.

From a technical standpoint, traders highlighted that BTC once again failed to flip key trend lines that would signal renewed bullish conviction. Keith Alan, cofounder of Material Indicators, observed that “So far $BTC bulls have failed to muster any momentum,” underscoring the lack of a clear breakout above resistance levels. A weekly chart review suggested a memory-like pattern of consolidation spanning 2021 through late 2024, with recent rallies not carrying the DNA of a sustained bull recovery.

“After losing the 2021 Top and the 21-Day SMA again, I’m having flashbacks to March – Nov 2024 when we endured 8 months of consolidation in this range. Nothing about Monday’s rally has the DNA of a bull recovery.”

Despite the bearish tone, some participants sought opportunities in the near term. A widely cited observation from traders noted that, relative to other assets, Bitcoin appeared to hold up better than some precious metals during the crisis, a theme that prompted discussions of potential capital rotation. Yet the prevailing consensus emphasized that volatility remained elevated and that BTC’s intermediate-term direction would hinge on how the oil-market dynamics and inflation outlook evolved in the days ahead.

“Not doing the worst since the escalation in the middle east. Actually outperforming stocks & precious metals for a change,” commented Daan Crypto Trades, highlighting the nuanced performance within a broad risk-off phase.

As the session progressed, gold came under pressure as macro concerns persisted. Nik Bhatia, founder of The Bitcoin Layer, described gold as “absolutely smashed,” while noting it had posted year-to-date gains of around 16%. This juxtaposition—gold weakening even as Bitcoin remains in a tight range—helped illustrate the complexity of risk markets during this period. Some observers, including Michaël van de Poppe, suggested that a rotation of capital from gold to BTC could be underway, a narrative that would require more data to confirm but remains a subject of debate among market watchers.

What’s next in the oil-BTC dynamic

The current episode underscores how energy-market shocks can feed into crypto liquidity, especially when inflation expectations are in flux. As traders reassess macro scenarios, BTC could either test higher resistance levels if risk appetite returns or continue trading within a defined range until new catalysts emerge. The next steps will hinge on how quickly energy markets stabilize, how central banks respond to any escalation in oil prices, and whether risk-on assets regain footing in a global environment of heightened uncertainty.

The cryptocurrency market has rebounded over the past 24 hours, with Bitcoin (BTC), Ethereum (ETH), and many other leading digital assets posting slight increases.

For its part, NEAR Protocol (NEAR) outperformed every competitor in the top 100 club, registering an impressive 12% pump.

What Fueled the Rally and What’s Next?

NEAR has been at the forefront of gains lately, with its valuation rising to a monthly peak of around $1.45 just several hours ago. Currently, it trades at around $1.35 (per CoinGecko’s data), representing a roughly 40% jump on a weekly scale. Its market capitalization has surpassed $1.7 billion, making it the 44th-largest cryptocurrency and flipping popular altcoins like Bittensor (TAO), Pi Network (PI), and others.

The main catalyst for the rally seems to be the latest technical upgrade announced by NEAR Protocol’s team. The project’s official X account revealed that Confidential Intents is live, a feature that lets users make private DeFi transactions without exposing sensitive details.

“DeFi users, developers, and institutions now unlock a wide range of privacy-first use cases without forgoing discretion,” the disclosure reads.

X user Emperor Osmo argued that NEAR is “fundamentally undervalued,” adding that Intents are generating widespread adoption.

“Meanwhile, they continue to increase the rate of adoption under which AI enables privacy-first trading (Iron Claw). Agentic payments are scaling, and Near is positioned to capture a lot of that flow,” they stated.

Michael van de Poppe also spoke highly of NEAR, describing it as “simply the best AI protocol in the ecosystem.” He wondered why investors wouldn’t want to add it to their portfolios, adding that from a technical standpoint, “it’s the best representation of the current status of altcoins.”

Altcoin Sherpa believes NEAR “is insanely strong,” while Sjuul | AltCryptoGems thinks the asset is trying to print “a cup and handle” formation on its price chart. This pattern consists of a rounded bottom (cup) and a small pullback on the right side (handle), and together they usually signal a bullish setup.

Not so Quick

Despite the evident resurgence, NEAR remains far below its all-time high of around $20 witnessed at the start of 2022. Meanwhile, certain technical indicators suggest a correction could be on the way.

The asset’s Relative Strength Index (RSI), which measures the speed and magnitude of recent price changes, has briefly climbed past 70. This means that NEAR has entered overbought territory and could be on the verge of a move south. Conversely, ratios below 30 are considered buying opportunities.

The post NEAR Protocol (NEAR) Soars by Double Digits: Breakout Confirmed or Bull Trap? appeared first on CryptoPotato.

Iran: can the Islamic Republic be toppled?

Badan Pegal Karena Masalah Financial #shortvideo

Trump hits out at Starmer over Iran: ‘This is not Winston Churchill we’re dealing with’

-

Politics5 days ago

Politics5 days agoITV enters Gaza with IDF amid ongoing genocide

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Iris Top

-

Politics9 hours ago

Politics9 hours agoAlan Cumming Brands Baftas Ceremony A ‘Triggering S**tshow’

-

Tech3 days ago

Tech3 days agoUnihertz’s Titan 2 Elite Arrives Just as Physical Keyboards Refuse to Fade Away

-

Business7 days ago

Business7 days agoTrue Citrus debuts functional drink mix collection

-

NewsBeat6 days ago

NewsBeat6 days agoCuba says its forces have killed four on US-registered speedboat | World News

-

Sports4 days ago

The Vikings Need a Duck

-

NewsBeat3 days ago

NewsBeat3 days agoDubai flights cancelled as Brit told airspace closed ’10 minutes after boarding’

-

Tech7 days ago

Tech7 days agoUnsurprisingly, Apple's board gets what it wants in 2026 shareholder meeting

-

NewsBeat6 days ago

NewsBeat6 days agoManchester Central Mosque issues statement as it imposes new measures ‘with immediate effect’ after armed men enter

-

NewsBeat3 days ago

NewsBeat3 days agoThe empty pub on busy Cambridge road that has been boarded up for years

-

NewsBeat2 days ago

NewsBeat2 days ago‘Significant’ damage to boarded-up Horden house after fire

-

NewsBeat3 days ago

NewsBeat3 days agoAbusive parents will now be treated like sex offenders and placed on a ‘child cruelty register’ | News UK

-

NewsBeat7 days ago

NewsBeat7 days agoPolice latest as search for missing woman enters day nine

-

Entertainment1 day ago

Entertainment1 day agoBaby Gear Guide: Strollers, Car Seats

-

Business6 days ago

Business6 days agoDiscord Pushes Implementation of Global Age Checks to Second Half of 2026

-

Business5 days ago

Business5 days agoOnly 4% of women globally reside in countries that offer almost complete legal equality

-

Tech4 days ago

Tech4 days agoNASA Reveals Identity of Astronaut Who Suffered Medical Incident Aboard ISS

-

Politics3 days ago

FIFA hypocrisy after Israel murder over 400 Palestinian footballers

-

Crypto World7 days ago

Crypto World7 days agoEntering new markets without increasing payment costs