Crypto World

Visa & Stripe’s Bridge Plan Expands Stablecoin Cards to 100+ Countries

Visa is expanding its stablecoin-linked card program with Bridge, broadening its geographic reach and pushing toward onchain settlement. The latest move lifts the program from its initial Latin American rollout to 18 countries, with a plan to surpass 100 countries across Europe, Asia-Pacific, Africa and the Middle East by year-end. The expansion builds on the program’s April 2025 debut in markets including Argentina, Colombia, Ecuador, Mexico, Peru and Chile, and comes as the two companies test settlement directly in stablecoins through a pilot tied to Visa’s rails and Bridge’s banking partner. The broader industry context features heightened activity around stablecoins in payments, with rival initiatives in the space highlighting a competitive push toward real-time, programmable settlement.

Key takeaways

- Visa and Bridge are extending the stablecoin-linked card program to 18 countries, with a target of more than 100 countries by year-end across Europe, Asia-Pacific, Africa and the Middle East.

- The program’s initial launch in 2025 covered Latin American markets, including Argentina, Colombia, Ecuador, Mexico, Peru and Chile.

- Settlement is moving toward onchain processing, enabled by Bridge’s collaboration with Lead Bank, allowing transactions to be settled in stablecoins instead of fiat.

- Visa is evaluating potential support for Bridge-issued assets, which are created programmatically by businesses rather than by a traditional issuer.

- The move comes amid broader payments-industry activity around stablecoins, including Mastercard’s recent stablecoin card enablement with MetaMask in the United States.

Tickers mentioned: $USDT, $USDC

Market context: The expansion aligns with a wider shift toward crypto-enabled payments and onchain settlement rails, as major incumbents test how tokens can streamline merchant settlements and reduce counterparty risk in everyday purchases.

Market context: Linked to broader USDt and USDC usage in payments, the push also sits against a backdrop of regulatory scrutiny and ongoing experimentation with tokenized settlement in traditional rails.

Why it matters

The enhanced collaboration between Visa and Bridge underscores a strategic bet on programmable, onchain settlement as a means to speed up merchant settlements and improve transparency for card programs built on stablecoins. By enabling issuers and acquirers to settle transactions directly in stablecoins, the network could reduce latency and friction inherent in fiat conversions, especially for cross-border transactions or cross-currency purchases. The approach also signals an appetite to expand the set of tools available to fintechs and brands that want to issue their own digital dollars or stable assets tailored to their customer base, without relying solely on a third-party issuer.

Bridge’s participation remains central to the evolution of these rails. The program leverages Bridge’s infrastructure to enable onchain settlement, with Lead Bank providing the regulatory and banking framework necessary to move transactions from card networks into the onchain ecosystem. In practice, this arrangement allows card issuers to settle in stablecoins rather than converting transactions to local fiat post-authorization, aligning settlement timelines with blockchain realities and potentially improving settlement finality for merchants and consumers alike.

From a competitive standpoint, the Visa-Bridge expansion sits alongside a broader trend in the payments space: the growing willingness of major processors to experiment with crypto rails. Mastercard, for example, has recently enabled stablecoin card spending in the US through a partnership with the MetaMask wallet, illustrating how traditional payment networks are responding to consumer interest in crypto-backed payments and the desire for real-time settlement capabilities. The juxtaposition of these efforts signals a broader industry push toward integrating crypto-native settlement with fiat-backed consumer spending, while navigating the regulatory and risk considerations that come with such a transition.

Visa’s crypto leadership has been clear about meeting businesses where they operate. Cuy Sheffield, Visa’s head of crypto, has framed the expansion as part of a broader strategy to bring the speed, transparency and programmability of stablecoins into the settlement process. The company is exploring how Bridge-issued assets—stablecoins that are created programmatically by businesses on Bridge’s platform—could be supported more broadly within Visa’s network, a path that could unlock new programmable currency options for merchants and brands that want to control settlement terms or tokenized reward structures. Unlike the most widely used stablecoins issued by independent entities, Bridge-issued assets are designed to be created and managed via Bridge’s infrastructure, a model that could appeal to fintechs seeking bespoke token strategies.

Bridge has positioned the expansion as a step toward more seamless, on-chain settlement for digital-asset-enabled card programs. The practical effect is a potential reduction in the time and complexity involved in moving value from a customer’s stablecoin balance to a merchant’s local currency—an outcome that could matter for shoppers who want near-instant payments and for issuers seeking tighter control over settlement economics. The program’s onchain settlement is described as a natural extension of Bridge’s rail, with Lead Bank acting as the bridge between traditional banking and the onchain settlement layer. In a mid-February update, Bridge noted that it had received conditional approval from a regulator to become a national trust bank, a milestone that underscores the regulatory dimensions of this kind of expansion and the careful navigation required to scale such rails.

As part of the broader, ongoing stablecoin race in payments, Visa’s initiative adds to a landscape where banks and fintechs are willing to experiment with programmable money at the point of sale. The expansion’s strategic rationale rests on creating more options for merchants to accept stablecoins without abandoning familiar payment interfaces, and for consumers to transact with tokens that can be settled efficiently. By aligning with Bridge’s architecture and Lead Bank’s regulatory framework, Visa is building a more integrated model where stablecoins do not live only in wallets or exchanges but become a practical settlement instrument for everyday card purchases.

The announcement also highlights a broader industry trend: the move toward enhanced interoperability between card rails and blockchain settlement. If the onchain settlement pilot proves scalable, issuers may gain more flexibility in structuring rewards, fees and settlement terms around stablecoins, potentially broadening the appeal of crypto-enabled cards to a wider audience of merchants and cardholders. While regulatory considerations remain a constant backdrop, the practical demonstrations of speed and transparency in settlement have kept this initiative in the spotlight as a potential blueprint for future integrations across the payments ecosystem.

What to watch next

- Timeline and results of the onchain settlement pilot with Lead Bank and Bridge; potential adjustments to settlement cadence and liquidity requirements.

- Progress toward the goal of reaching 100+ countries by year-end, and which markets will be prioritized in the near term.

- Details on Visa’s potential support for Bridge-issued assets and any regulatory approvals that shape that path.

- Regulatory developments regarding Bridge’s national trust bank status and how they affect cross-border card programs.

Sources & verification

- Visa and Bridge expansion to over 100 countries: official Visa investor relations announcement.

- Original Latin American rollout: Visa and Bridge collaboration announcement outlining the April 2025 launch.

- Onchain settlement pilot and Bridge-Lead Bank collaboration: Visa press materials and Bridge announcements, including regulatory status updates.

- Industry context: Mastercard’s stablecoin card spending in the US via MetaMask—contextual reference in related coverage.

Key figures and next steps

Market reaction and key details

Why it matters

The Visa-Bridge collaboration represents a deliberate push to embed stablecoins deeper into everyday payments while testing the viability of onchain settlement for consumer card programs. If the pilot demonstrates efficiency gains and regulatory viability, issuers and merchants could gain access to more flexible settlement terms and new token-based monetization options. For users, the prospect of faster settlement and more predictable funds availability could enhance the appeal of stablecoins as a practical payments tool, particularly for cross-border purchases and commerce that spans multiple currencies.

Beyond Visa, the broader payments ecosystem is watching how these rails will coexist with existing fiat-based settlement, risk controls, and compliance regimes. The tension between innovation and regulation remains a key driver, but the ongoing experiments with stablecoins at the point of sale reflect a maturing phase in crypto-enabled payments where real-world usage and governance concerns are increasingly aligned. As more institutions participate, the competence and reliability of onchain settlement in consumer contexts will be tested under a variety of market conditions, from everyday retail transactions to cross-border remittances.

What to watch next

- End-of-year milestones for country expansion and the potential scaling of onchain settlement.

- Regulatory updates on Bridge’s national trust bank status and related compliance requirements.

- Adoption metrics from merchants and issuers participating in the program, including any changes in settlement times and cost structures.

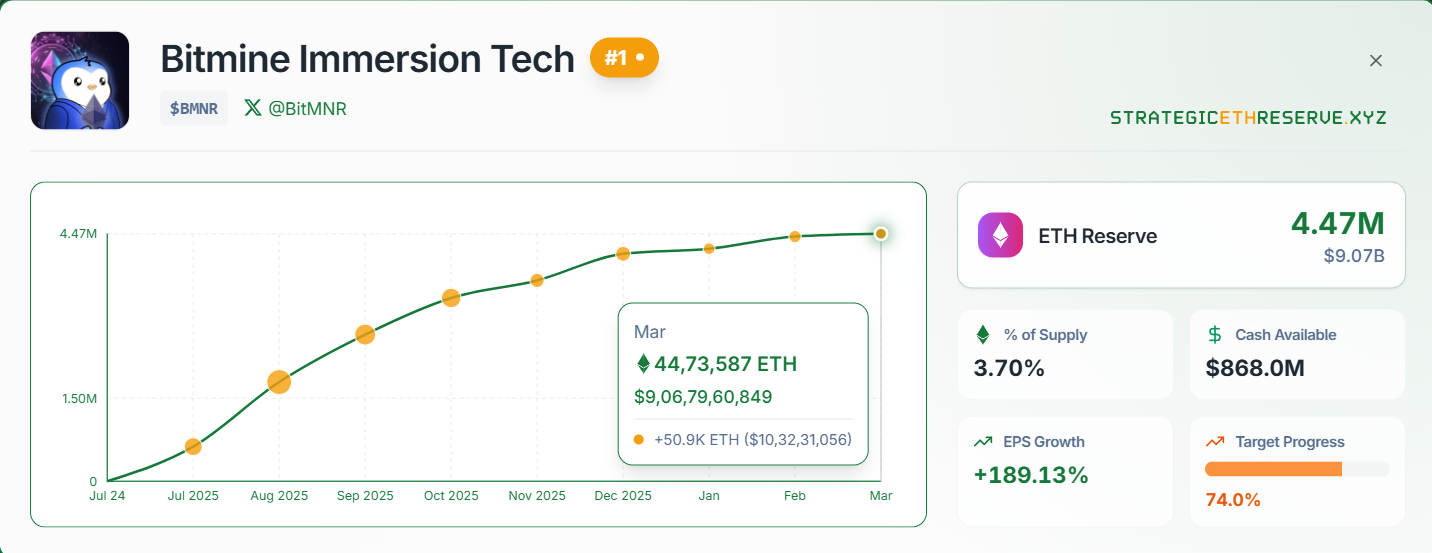

BitMine Immersion Technologies (BMNR) has been experiencing sideways movement in its price for nearly a month. However, recent developments hint that this could be a turning point for the company.

A notable purchase of over 50,900 ETH has sparked new interest, potentially signaling a shift in BMNR’s price and Ethereum’s (ETH) future.

BitMine’s Bold ETH Purchase: A Strategic Move for March

On March 2, BitMine made a significant acquisition, purchasing 50,9928 ETH, bringing its total holdings to 3.71% of all Ethereum supply. This is just 1.29% short of the company’s target of holding 5% of Ethereum’s supply.

Despite Ethereum’s price being in the red at the time of the purchase, BitMine’s Chairman Tom Lee believes that March will be a pivotal month for Ethereum and the broader crypto market.

“We understand war headlines make investors nervous, but we expect stocks to be up in March: – led by MAG7, software IGV and crypto $BTC $ETH (sic),” Lee stated.

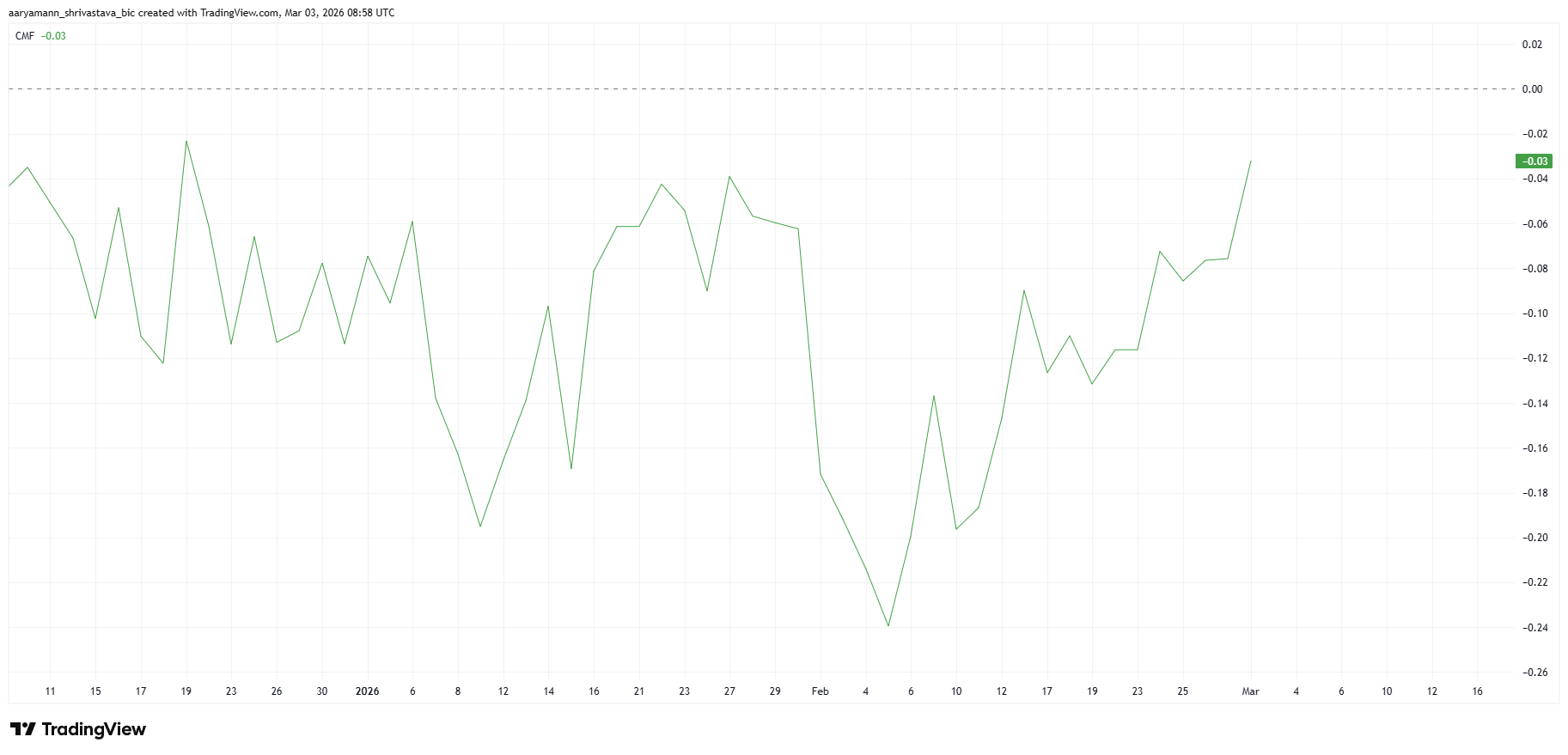

CMF Indicator Shows Potential Bullish Momentum

The Chaikin Money Flow (CMF) has shown an uptick, signaling that investor support for BMNR may be growing. While the CMF is still below zero, the rising trend indicates that outflows are declining, which is a positive sign for the company. A move into the positive territory by the CMF could confirm that BMNR holders are supporting the price, further fueling optimism about a potential price reversal.

This uptick suggests that investor confidence is strengthening and could signal an incoming period of inflows. If the CMF crosses into the positive zone, it would provide confirmation that the market sentiment is shifting in favor of BMNR.

Want more token insights like this? Sign up for Editor Harsh Notariya’s Daily Crypto Newsletter here.

Bullish Divergence Amidst Geopolitical Challenges

The Money Flow Index (MFI) is showing a bullish divergence since the beginning of the year. The indicator has been forming lower highs, while BMNR’s price has seen lower lows, signaling a decrease in selling pressure. Despite the ongoing geopolitical instability in 2026, which has added volatility to global markets, the MFI suggests that BMNR is on track for a potential recovery.

Although external factors like geopolitical unrest have impacted BMNR’s price, the bullish divergence in the MFI suggests that the selling pressure is waning. This reduction in selling pressure could lead to a price rebound for BMNR in the near future.

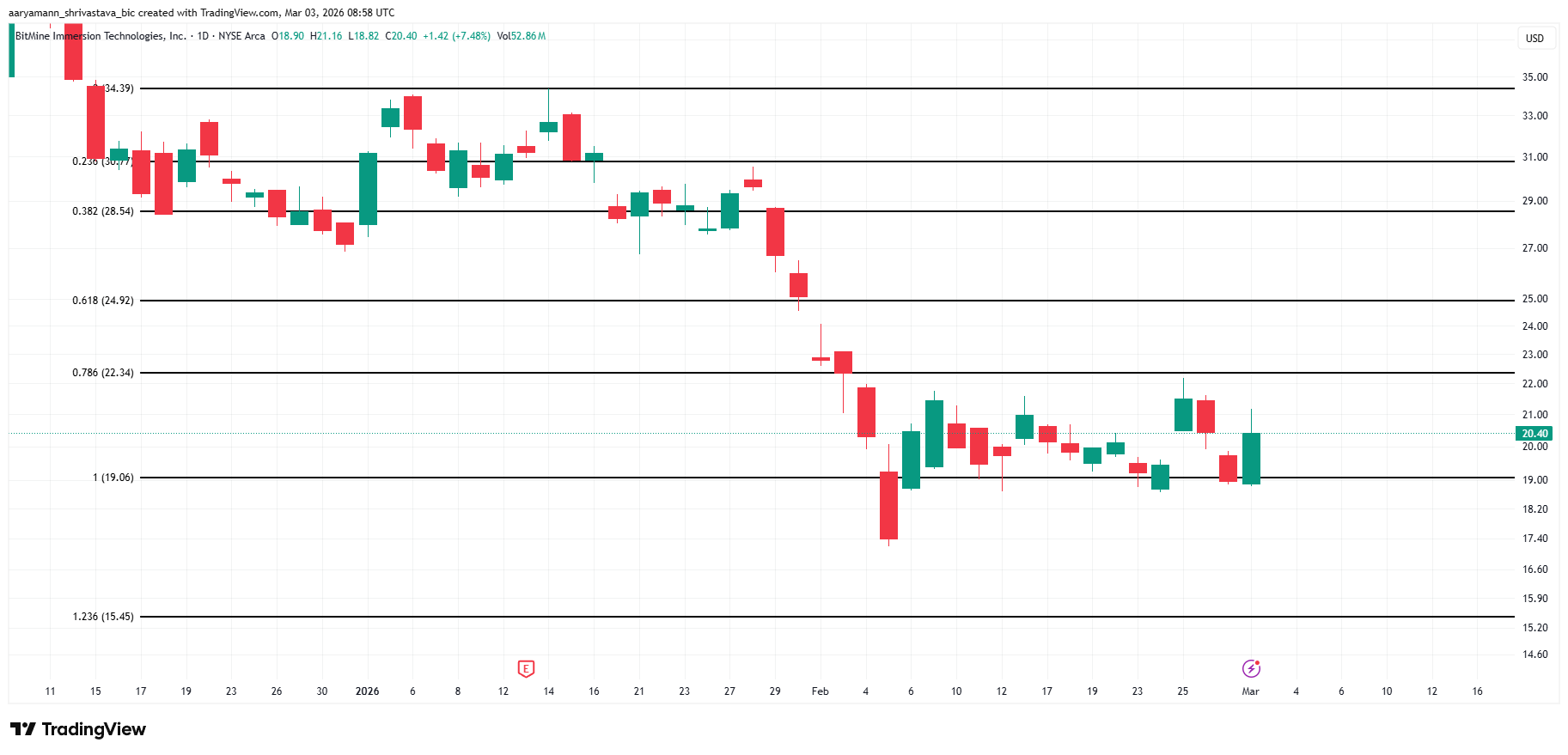

Is BMNR Price Breaking Up With ETH?

Currently, BMNR is trading at $20.40, sitting just above the $19.06 support level. Maintaining this support is vital for BMNR to eventually break out above the $22.34 resistance. If BMNR stays above the $19.06 support, it may have the potential to rally in the coming weeks.

Interestingly, the correlation between BMNR and Ethereum has been decreasing, with the correlation currently at 0.36. This suggests that BMNR is less likely to follow Ethereum’s price movements, which is a positive sign. Ethereum has been in a period of consolidation, allowing BMNR more room to move independently and potentially rally.

However, there is a risk if BMNR holders panic due to ongoing geopolitical events. If the $19.06 support is lost, BMNR could see a drop toward the next major support at $15.45. This would invalidate the current bullish outlook and require careful monitoring of market conditions.

TLDR

- Ripple expanded its payments platform to support a full stablecoin workflow for banks and fintechs.

- The upgraded Ripple Payments platform now enables collection, custody, conversion, and payout using stablecoins.

- Ripple Payments operates in more than 60 markets and has processed over $100 billion in transaction volume.

- Ripple integrated its dollar-pegged stablecoin RLUSD into the expanded payments stack.

- RLUSD has reached a circulating supply of about $1.5 billion in the global stablecoin market.

Ripple has expanded its global payments platform to support a broader stablecoin workflow for banks and fintechs. The company aims to reduce reliance on pre-funded overseas accounts and speed up cross-border transactions. It announced the upgrade on Tuesday and confirmed expanded capabilities across its network.

Ripple upgrades payments platform with stablecoin workflow

Ripple upgraded Ripple Payments to support collection, custody, conversion, and payout through stablecoins. The company said the update connects financial institutions directly to blockchain-based settlement rails. As a result, clients can manage funds without parking capital in foreign accounts.

The platform operates in more than 60 markets and has processed over $100 billion in volume. Ripple stated that Switzerland’s AMINA Bank, Brazil’s Banco Genial, Malaysia’s ECIB, and Philippines-based AltPayNet participate in the network. The company said the expanded stack allows institutions to move funds faster while maintaining operational control.

Ripple is valued at $17.7 billion, according to Forge Global, which tracks pre-IPO shares. The company remains privately held while expanding its enterprise offerings. It said the new features position Ripple Payments to compete directly with legacy providers.

RLUSD stablecoin gains traction as supply reaches $1.5 billion

Ripple continues to integrate its dollar-pegged token, RLUSD, into its payments infrastructure. RLUSD trades at $1 and holds a circulating supply of about $1.5 billion. The company said the token supports real-time settlement across supported markets.

Ripple stated that RLUSD accounts for a small but growing share of the global stablecoin market. It said clients can hold, exchange, and settle transactions using fiat or stablecoins. The company completed its acquisition of Rail last August for $200 million to support these services.

Ripple also acquired custody and treasury automation firm Palisade to strengthen asset management. It said these acquisitions expand its custody and treasury capabilities within the payments stack. The company confirmed that these tools integrate with Ripple Payments.

In December, the US Office of the Comptroller of the Currency conditionally approved national trust bank charters for Ripple National Trust Bank. The regulator also granted conditional approvals to Circle, BitGo, Paxos Trust Company, and Fidelity Digital Assets. If finalized, the charters would allow asset and stablecoin reserve management under federal oversight.

Ripple chief legal officer Stuart Alderoty attended a February White House meeting on crypto legislation. He joined other crypto and banking representatives to discuss stablecoin provisions. Lawmakers continue negotiations in Washington, DC, over a proposed US crypto market structure bill.

Usual’s introduction of a direct EUR ↔ EUR0 rail leverages SEPA Instant and virtual IBAN technology to streamline fiat transactions, enhancing euro transfers for users across Europe.

Decentralized stablecoin protocol Usual has rolled out direct EUR0-to-EUR conversions, marking a significant milestone in simplifying fiat on- and off-ramps for European users. The service utilizes SEPA and SEPA Instant transfers, providing seamless euro transactions across the continent.

The EUR0 token represents a digital euro balance backed by European sovereign bonds, integrated into Usual’s platform to facilitate efficient euro transfers. This integration aims to enhance the ease of transactions by eliminating the need for exchange accounts, intermediate tokens, or third-party trading platforms, according to a blog post.

SEPA Instant, a key component of this service, allows real-time euro transactions across 36 countries, including the UK and Switzerland. This rapid settlement feature is complemented by virtual IBANs, which provide unique digital account numbers linked to a primary bank account, facilitating international payments without requiring multiple accounts.

Usual’s platform offers an efficient on-ramp for users, who can deposit euros to a virtual IBAN, automatically updating their EUR0 balance. Off-ramping is equally streamlined, allowing users to convert EUR0 back to euros and receive them via SEPA transfer. Identity verification is conducted within the Usual app.

Usual has around $114 million in total value locked (TVL), according to DeFiLlama.

This article was generated with the assistance of AI workflows.

The White House set a March 1st deadline for the banking industry and crypto firms to reach a deal on stablecoin yield, clearing the way for the Clarity Act, the market structure legislation meant to put the industry on a solid legal foundation in the U.S.

Clarity was passed by the House seven months ago. The Senate has set many deadlines to move it, and they have all gone unmet. The latest deadline also blew by with no deal.

The crypto industry has been fixated on legislation as the next catalyst, as if it is the only path toward the long-needed regulatory clarity in the world’s largest economy.

But legislation is not the only path.

The existing laws that provide authority to the market regulators at the Securities and Exchange Commission and the Commodity Futures Trading Commission are broad and flexible. Those agencies are acting now.

Fresh legislation would ensure against future Gary Genslers, but Gary Gensler’s era is done. President Donald Trump appointed a friendly chair to bless the industry just as Gensler had appointed a hostile one to bedevil it.

And while everything else that Trump has done vis-à-vis crypto has created political headwinds, it could be that all he really needed to do was pick the right chief for the SEC, and I suspect he has.

Trump appointed a veteran, Paul Atkins, who knows how to write regulations that will withstand legal challenges. Trump then appointed one of Atkins’ deputies to lead the other investment agency, the CFTC, ensuring rulemaking harmonizes across markets. All the industry has to do in order not to screw this up is avoid another FTX-like implosion.

It’s crypto’s game to lose.

Not his first rodeo

Paul Atkins served for six years at the SEC in the 2000s, serving under three different chairs. Since then, he has served as an advisor to the Chamber of Digital Commerce and to Securitize.

He was sworn in April 2025. A few weeks later, he spoke at an event at the SEC office, saying the agency has the authority to grant the crypto industry the rulemaking it needs to operate.

Later, before a dozen or so reporters, he was asked whether he needed to wait for Congress to write market-structure legislation before he could act. He repeated that his staff can and would act with or without new legislation.

Atkins confidently promised action, like a regulator who understands the scope of his existing authority.

Harmonization

And Atkins will be aligned with the chief of the SEC’s sister agency, the CFTC.

Gensler was never aligned with Rostin Benham, the CFTC’s prior chief. Benham kept asking Congress to take action, which Gensler kept saying wasn’t necessary.

Benham clearly did not believe every coin was a security, but Gensler believed that only Bitcoin was clear of his scrutiny. They were not harmonized.

But to effectively regulate and give founders confidence, it’s key that the agencies don’t fight about when and if a digital asset can move from SEC jurisdiction to the CFTC’s.

So I believe one of the key reasons that Atkins hasn’t already posted draft rules for public comment is that he wanted to do so in concert with the CFTC. However, Trump switched gears on appointing a chair for that agency, and the new helmsman, Michael Selig, didn’t get sworn in till the end of December.

It would not be surprising if, one day, we learn that Atkins convinced the president to change course on CFTC chair appointments to ensure the two agencies work well together.

Expect an official memorandum of understanding between the two agencies delineating responsibilities soon. This arrangement will be reminiscent of the historic Shadd-Johnson accord of 1981.

The new sheriff

By this fall, I suspect, Project Crypto will have submitted draft rules — each written in consultation with the other — before their respective commissions.

By next Spring, those rules will have been amended based on public comments and, most likely, finalized.

This will be the first administration to actually write rules with decentralized financial networks in mind.

Under new rules, it should be possible, for example, for exchanges like Kraken, Coinbase, and Crypto.com to finally say that all their operations are registered with an agency and under state supervision.

It should also be possible for new enterprises to raise funds with token sales. Some of those tokens will likely enjoy rights that entrepreneurs avoided during the regulation-by-enforcement era, such as the ability to distribute revenue.

Provided the rules are written conservatively enough to survive court challenges, the industry is likely to have two or three years to grow before it’s even possible to roll back the work of Atkins and Selig (because doing so will require both a Senate appointment process and a fresh rulemaking process).

Fait accompli

While we all know that crypto has always been an industry that welcomes new participants, the president’s family didn’t do digital assets any favors by launching memecoins, a stablecoin, and bitcoin miners. Those activities might have been enough to torpedo any hope of satisfying the crypto lobby’s ambitions for this session of Congress.

But while Congress dithers, agency staff are writing rules.

If the SEC and CFTC collaborate effectively–both agency leaders announced today that several crypto polices are coming–whatever arrangement they devise may eventually become law anyway. After all, Congress codified the Shadd-Johnson accord in the early 80s.

So the lobbyists may ultimately get the legislation they want, but only after crypto has gone mainstream anyway — without Congress, which is why Trump’s decision to appoint Paul Atkins may already have been sufficient to give the industry enough legal whitespace to reach its potential.

The United States (U.S.) Senate has taken a major bipartisan step by advancing the 21st Century ROAD to Housing Act. The bill combines housing reforms with a ban on central bank digital currencies (CBDC).

According to Burgess Everett, congressional bureau chief at Semafor, the legislation passed a key procedural vote of 84–6. The result signals broad support for changes affecting both housing policy and digital money rules.

Housing Supply Push Comes With Crypto Conditions

Beyond its digital currency provisions, the bill targets America’s housing challenges by cutting bureaucratic delays and expanding home supply. It also seeks to curb the dominance of large institutional players in single-family rentals while simplifying financing and development processes nationwide.

Highlighting the scale of bipartisan backing, Everett described the vote margin as one not seen every day. Supporters argue the reforms could make housing more accessible and affordable for ordinary Americans.

Despite the focus on housing, a notable feature of the legislation is its ban on central bank digital currencies. The provision bars the Federal Reserve from issuing or creating a digital currency through 2030. It also covers any similar assets issued directly or through financial intermediaries.

The restriction emerged after House conservatives pushed for tighter crypto-related limits as part of broader legislative compromises. Lawmakers opted to fold the provision into the housing bill rather than advance standalone digital asset legislation.

Federal Reserve officials have said any CBDC initiative remains exploratory and would require congressional approval. Even so, the ban has prompted renewed debate over the future of digital currency in the U.S., particularly around privacy, payments, and financial oversight.

White House Signals Support Despite CBDC Controversy

The White House has endorsed the bill, noting that President Trump’s advisers would recommend signing it if it reaches his desk. The backing underscores the legislation’s unusual cross-party appeal, even as Democrats have always opposed limits on Federal Reserve digital currency research.

Despite the endorsement, the bill still faces several procedural hurdles before becoming law, including reconciliation with the House version. It remains unclear whether the CBDC restriction will survive final negotiations, leaving the digital currency community closely watching.

The post U.S. Senate Pushes Housing Reform Bill With Surprise CBDC Ban appeared first on CryptoPotato.

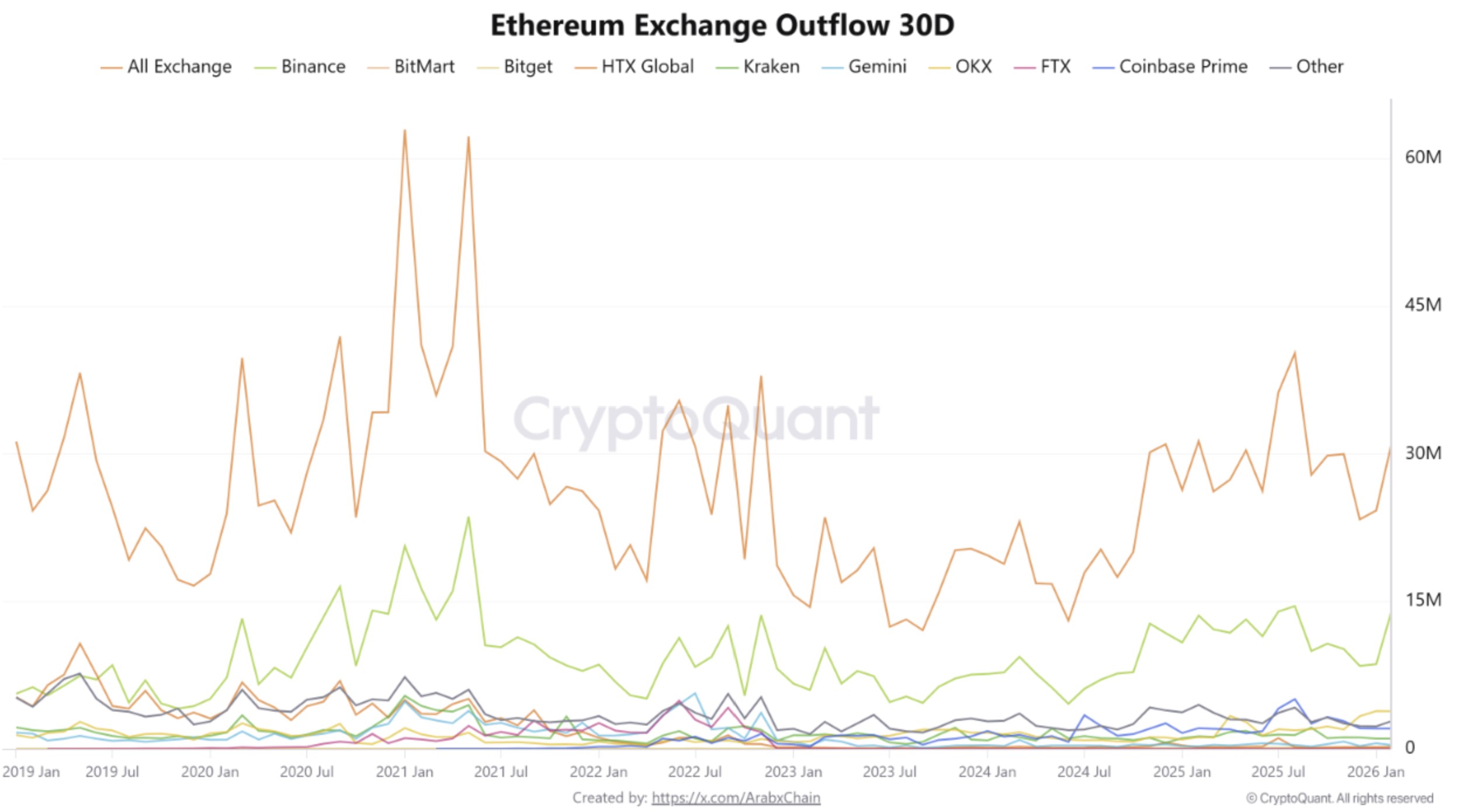

The balance of Ether (ETH) held on exchanges has slid to a multi-year low, with more than 31 million ETH leaving centralized exchanges in February, marking the largest monthly withdrawal since November.

While the ETH price remained near $2,000, derivatives data show a split between small buyers and larger sellers, raising the question of how the price may respond if demand becomes uniform across both retail and whale wallets.

Ether exchange reserves signal supply squeeze

Crypto analyst Arab Chain said that more than 31.6 million ETH left major exchanges in February, the highest monthly outflow since November. Binance led with roughly 14.45 million ETH withdrawn, nearly half of the total. OKX followed with about 3.83 million ETH, and Kraken recorded close to 1.04 million ETH.

Sustained withdrawals reduce the pool of coins readily available for spot trading activity. Coins moving to private wallets or staking platforms are typically less liquid in the short term. As a result, thinner exchange balances can heighten the price volatility when market activity surges.

Likewise, CryptoQuant data also showed that Binance’s Ether reserves have dropped to around 3.46 million ETH, the lowest level since 2020. In previous cycles, reserves peaked above 5 million ETH before entering a gradual downtrend marked by lower highs. The latest reading extends that decline.

With ETH trading below $2,000, the contraction in exchange supply places added focus on future demand. If buying pressure expands while reserves continue to fall, the available liquidity on order books may tighten further around the $2,000 threshold.

Related: Ether price again rejected at $2K: How low can ETH go in March?

Market remains split between retail and whales

Hyblock data highlighted a divergence across trade sizes. The cumulative volume delta (CVD), which tracks net aggressive buying and selling, stands near $95 million for smaller trades (between $0 and $10,000). That shows consistent retail-led buying pressure.

In contrast, the $10,000–100,000 trade bracket records roughly -$162 million in CVD, while the $100,000+ category sits near -$357 million. As observed, the larger participants have leaned towards net selling during the same period.

The bid–ask ratio has turned slightly positive, rising to around 0.2 before dipping to 0.03, indicating marginally stronger buying interest in recent sessions. The move follows a stretch of negative readings and points to short-term stabilization rather than broad conviction.

The aggregated open interest is near $9.41 billion, down from levels close to $10 billion in late February. The reduction signals that leverage has been trimmed as the price consolidates between $1,900 and $2,000.

If retail accumulation persists and large-scale selling slows, bullish positioning may become more aligned. In that case, the reduced exchange supply may amplify the price move once ETH solidifies a position above $2,000-$2,150.

Related: AI ‘vibe coding’ could put Ethereum roadmap ahead of schedule: Vitalik Buterin

This article does not contain investment advice or recommendations. Every investment and trading move involves risk, and readers should conduct their own research when making a decision. While we strive to provide accurate and timely information, Cointelegraph does not guarantee the accuracy, completeness, or reliability of any information in this article. This article may contain forward-looking statements that are subject to risks and uncertainties. Cointelegraph will not be liable for any loss or damage arising from your reliance on this information.

TLDR

- Circle shares rose more than 20% this week following Israeli and U.S. airstrikes on Iran.

- Mizuho linked the rally to higher oil prices and fading expectations for Federal Reserve rate cuts.

- WTI crude climbed about 7 to 8% after tensions in the Middle East escalated.

- Circle earns most of its revenue from interest on U.S. government debt backing its USDC stablecoin.

- Analysts said reduced rate cut expectations add about 1% to Circle’s 2026 and 2027 revenue forecasts.

Circle (CRCL) shares jumped over 20% this week after Israeli and U.S. strikes on Iran lifted oil prices and rate expectations. Mizuho linked the rally to higher crude and fading Federal Reserve rate cut hopes. The bank raised its price target to $100 while keeping a neutral rating.

Circle shares gain as oil surge shifts rate outlook

Circle shares outperformed the broader market as WTI crude rose about 7% to 8% since the weekend strikes. Japanese bank Mizuho said higher oil prices could revive inflation pressures and reduce expectations for Federal Reserve rate cuts.

The bank explained that Circle earns most revenue from interest on U.S. government debt backing its USDC stablecoin. Higher interest rates increase yields on those reserves and support revenue growth. Conversely, lower rates compress that income stream and limit earnings potential.

Mizuho analysts Dan Dolev and Alexander Jenkins adjusted their forecasts after reviewing recent market data. They estimated that reduced expectations for rate cuts add about 1% to their 2026 and 2027 revenue forecasts.

They also cited Chicago Mercantile Exchange FedWatch data to support their outlook. The analysts said the probability of a no-rate-cut scenario in 2026 has doubled in the right tail risk distribution.

Bitcoin rebound supports market sentiment

Crypto markets reacted sharply when the Middle East conflict began over the weekend. Bitcoin fell in early trading during a broad risk-off move but later stabilized.

Bitcoin now trades near $68,100 after rising roughly 5% in the past 24 hours. The recovery has helped improve overall market sentiment around digital assets.

Mizuho increased its Circle price target to $100 from $90 following these developments. The stock traded 6% higher at $101.90 at publication time.

The bank maintained a neutral rating despite the revised target price. Analysts stated that higher-for-longer rates create a near-term revenue benefit for the company.

However, the report warned that long-term growth could slow as stablecoins become more commoditized. Competitive pressures may affect margins over time.

Circle shares also surged more than 45% last week after fourth-quarter earnings triggered a short squeeze. That rally ended an 80% decline from record highs reached last year.

The recent price action reflects shifting macro expectations and crypto market movements. At publication time, Circle shares traded above the revised $100 target set by Mizuho.

Crypto World

Middle East tensions, higher oil boost Circle (CRCL) shares as rate-cut odds fade: Mizuho

Shares of stablecoin issuer Circle (CRCL) have risen over 20% this week, outperforming the broader market following Israeli and U.S. airstrikes on Iran over the weekend.

Japanese bank Mizuho attributed the rally in part to a sharp rise in oil prices, as tensions in the Middle East exploded. Higher crude prices could rekindle inflationary pressures, lowering expectations for Federal Reserve rate cuts.

That dynamic matters for Circle. The company earns the bulk of its revenue from interest income on the U.S. government debt it holds as reserves backing its USDC stablecoin. Higher interest rates translate into greater yield on those reserves, directly supporting revenue. Conversely, rate cuts compress that income stream.

Since U.S. and Israeli strikes on Iran over the weekend, WTI crude has climbed roughly 7%–8% on elevated geopolitical risk and supply disruption concerns.

Crypto markets were jolted at the outbreak of war in the Middle East on Saturday, with bitcoin sliding sharply in early trading amid a broader risk-off move, but prices have since stabilized.

Analysts Dan Dolev and Alexander Jenkins estimated that reduced expectations for rate cuts add about 1% to their Circle 2026 and 2027 revenue forecasts.

More importantly, the analysts pointed to a doubling in the “right tail risk” of a no-rate-cut scenario in 2026, according to Chicago Mercantile Exchange (CME) FedWatch data, a shift that could further support Circle’s valuation multiple.

A roughly 5% rise in bitcoin over the past 24 hours may also be contributing to positive sentiment. The largest cryptocurrency is currently trading around $68,100.

The bank raised its Circle price target to $100 from $90, while maintaining a neutral rating on the shares. The stock was trading 6% higher at $101.90 at publication time.

While higher-for-longer rates are a near-term positive, longer-term revenue growth could face pressure as stablecoins become increasingly commoditized, the report added.

Circle shares gained more than 45% last week in a violent short squeeze following fourth quarter earnings. That move snapped what had been a brutal 80% drawdown from record highs hit last year.

Read more: Circle’s post-earnings surge nears 50% as short squeeze, not strong financials, fuels rally

HBAR price has faced repeated rejection at the value area high, signaling fading upside momentum. With demand weakening, the market now risks rotating toward deeper support near $0.07.

Summary

- Repeated rejection at value area high resistance

- $0.09 support critical for short-term structure

- Breakdown exposes $0.07 high timeframe support

HBAR (HBAR) price remains locked in a corrective phase as price continues to trade within clearly defined value levels. Multiple failed attempts to break above resistance highlight persistent supply overhead, preventing bullish continuation.

As momentum fades near the upper boundary of the range, attention shifts toward whether key support can hold or if further downside rotation will unfold.

HBAR price key technical points

- Resistance Zone: Value Area High continues to cap upside attempts.

- Immediate Support: $0.09 high timeframe demand level.

- Downside Target: Breakdown exposes $0.07 high timeframe support.

HBAR’s recent price action reflects rotational market behavior rather than trending expansion. The asset has repeatedly tested the Value Area High, only to be rejected on multiple occasions. This level acts as a ceiling within the current trading structure, signaling that buyers lack the conviction necessary to sustain a breakout.

The inability to reclaim the Value Area High suggests weakening demand at higher prices. When price repeatedly fails at resistance without strong volume confirmation, markets often rotate lower in search of stronger liquidity zones. In HBAR’s case, price has now reverted back toward the $0.09 high timeframe support, which serves as the next immediate demand area.

The $0.09 region represents a structural pivot within the range. Holding this level would preserve consolidation dynamics and maintain rotational price behavior between the value area boundaries, especially after HBAR recently rebounded from its year-to-date low of $0.0725 to the psychological $0.100 level.

However, a confirmed close below this support would indicate acceptance at lower prices and significantly increase the probability of continuation toward the Point of Control (POC) and ultimately the Value Area Low.

From a volume profile perspective, markets frequently move between the Value Area High, POC, and Value Area Low as liquidity shifts. With the upper boundary firmly rejecting price, the path of least resistance favors a move toward the lower end of the range.

Should $0.09 fail to hold, the next major high timeframe support lies near $0.07, a region that previously acted as a structural demand zone. A move toward this level would represent a deeper corrective rotation within the broader consolidation structure.

Market structure analysis further reinforces caution. HBAR has not established higher highs or sustained bullish momentum above resistance. Instead, the chart reflects ongoing equilibrium conditions where buyers and sellers are battling for control without decisive resolution.

Volume behavior also remains subdued. Without a meaningful influx of buying participation, upside continuation becomes increasingly difficult. For HBAR to invalidate the bearish rotation scenario, price would need to decisively reclaim the Value Area High with strong volume expansion.

Until that occurs, the market remains vulnerable to gradual downside exploration.

What to expect in the coming price action

HBAR is likely to continue rotating within its value range unless a decisive breakout occurs. Loss of $0.09 support would increase the probability of a move toward $0.07. Conversely, reclaiming the Value Area High would signal renewed strength and invalidate the short-term bearish bias.

Crypto World

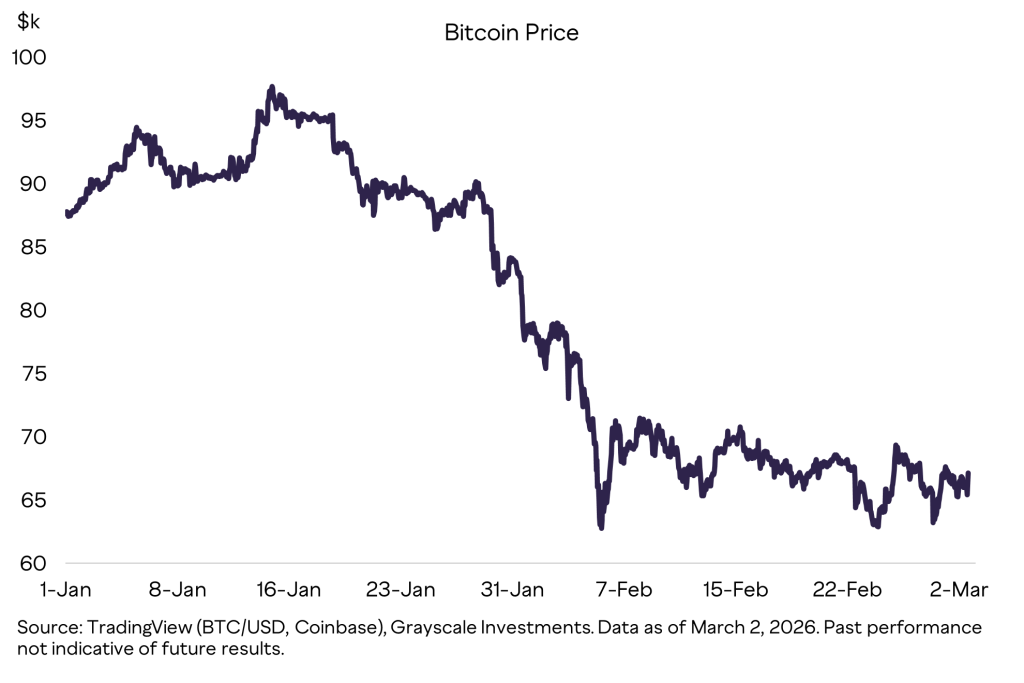

Bitcoin Price Prediction: Billion-Dollar Asset Manager Signals Explosive Opportunity After Market Drop

Crypto has been bleeding. Bitcoin slid toward the $60,000 zone. Altcoins followed. Sentiment at its worst and bearish price prediction everywhere.

Right on cue, a billion dollar asset manager stepped in and said what most retail traders are afraid to think: this might be the opportunity.

In its latest market commentary, Grayscale argued that the recent drawdown does not break the long term thesis. Instead, it may present a strategic entry point for investors willing to zoom out.

The firm pointed to the sharp correction across crypto and tech equities, but stressed that structural drivers remain intact.

One key theme is the growing overlap between AI and blockchain. According to Grayscale, these technologies are complementary, not competitive.

As AI agents become more autonomous, blockchains could serve as their financial rails. That narrative has already shown relative strength compared to other crypto segments during the downturn.

The report also highlighted stablecoins and tokenization as major institutional gateways. Regulatory progress and renewed interest from firms like Meta, Stripe, and BlackRock suggest that traditional finance is not stepping back from crypto. It is building into it.

At the macro level, Grayscale maintains that the broader US economic backdrop remains supportive for risk assets, even with uncertainty around monetary policy leadership. Volatility, in their view, does not equal collapse.

Bitcoin Price Prediction: Is This the Setup for the Next Leg?

Bitcoin price looked ready to break out.

It pushed above the descending trendline of that compressing triangle and started moving toward $72,000. For a moment, it felt like expansion was coming.

But there was no follow-through.

Instead of flipping the breakout level into support, the price stalled and slipped back inside the triangle. That is a classic failed breakout.

Now the focus shifts back to $64,000. If price keeps drifting lower and that support cracks, the structure turns bearish and $60,000 comes into play quickly.

A failed breakout plus support loss is usually a strong downside combo.

That said, the whole setup is not ruined yet. If $64,000 holds and Bitcoin reclaims the upper trendline again, this could still turn into a shakeout.

Can Bitcoin Hyper Presale Grab Everyone’s Attention? One Of The Most Anticipated Projects In 2026

Bitcoin Hyper ($HYPER) is a new presale using Solana tech to make Bitcoin a lot faster and cheaper, without messing with its core security.

It basically turns Bitcoin from something you just watch on a chart into something you can actually use. Payments. Staking. Apps. Real on-chain action.

And this is not just hype. The presale has already raised over $32 million, with $HYPER priced at $0.0136751 before the next increase.

Staking is paying up to 37% right now, which definitely catches attention.

If Bitcoin takes off, Bitcoin Hyper probably moves with it. If Bitcoin keeps moving sideways, Bitcoin Hyper still benefits from actual network usage. It is built around activity, not just waiting for price to pump.

To buy HYPER before it lists on exchanges, simply visit the official Bitcoin Hyper website and connect a wallet (such as Best Wallet).

Visit the Official Bitcoin Hyper Website Here

The post Bitcoin Price Prediction: Billion-Dollar Asset Manager Signals Explosive Opportunity After Market Drop appeared first on Cryptonews.

I Just CHANGED my XRP price prediction for 2026!!!

OpenAI changes deal with US military after backlash

Why Haven’t Oil Prices Surged More?

-

Politics5 days ago

Politics5 days agoITV enters Gaza with IDF amid ongoing genocide

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Iris Top

-

Politics12 hours ago

Politics12 hours agoAlan Cumming Brands Baftas Ceremony A ‘Triggering S**tshow’

-

Tech3 days ago

Tech3 days agoUnihertz’s Titan 2 Elite Arrives Just as Physical Keyboards Refuse to Fade Away

-

NewsBeat6 days ago

NewsBeat6 days agoCuba says its forces have killed four on US-registered speedboat | World News

-

Sports4 days ago

The Vikings Need a Duck

-

NewsBeat3 days ago

NewsBeat3 days agoDubai flights cancelled as Brit told airspace closed ’10 minutes after boarding’

-

NewsBeat6 days ago

NewsBeat6 days agoManchester Central Mosque issues statement as it imposes new measures ‘with immediate effect’ after armed men enter

-

NewsBeat2 days ago

NewsBeat2 days ago‘Significant’ damage to boarded-up Horden house after fire

-

NewsBeat3 days ago

NewsBeat3 days agoThe empty pub on busy Cambridge road that has been boarded up for years

-

NewsBeat3 days ago

NewsBeat3 days agoAbusive parents will now be treated like sex offenders and placed on a ‘child cruelty register’ | News UK

-

NewsBeat7 days ago

NewsBeat7 days agoPolice latest as search for missing woman enters day nine

-

Entertainment2 days ago

Entertainment2 days agoBaby Gear Guide: Strollers, Car Seats

-

Business6 days ago

Business6 days agoDiscord Pushes Implementation of Global Age Checks to Second Half of 2026

-

Business5 days ago

Business5 days agoOnly 4% of women globally reside in countries that offer almost complete legal equality

-

Tech4 days ago

Tech4 days agoNASA Reveals Identity of Astronaut Who Suffered Medical Incident Aboard ISS

-

NewsBeat2 days ago

NewsBeat2 days agoEmirates confirms when flights will resume amid Dubai airport chaos

-

Politics3 days ago

FIFA hypocrisy after Israel murder over 400 Palestinian footballers

-

Crypto World7 days ago

Crypto World7 days agoEntering new markets without increasing payment costs

-

Crypto World5 days ago

Crypto World5 days agoFrom Crypto Treasury to RWA: ETHZilla Retreats and Relaunches as Forum Markets on Nasdaq