STMicroelectronics N.V. (STM) Shareholder/Analyst Call May 4, 2026 9:30 AM EDT

Company Participants

Jerome Ramel – Executive VP of Corporate Development & Integrated External Communication Remi El-Ouazzane – President of Microcontrollers, Digital ICs & RF Products Group

Advertisement

Conference Call Participants

Stephane Houri – ODDO BHF Corporate & Markets, Research Division Sandeep Deshpande – JPMorgan Chase & Co, Research Division Gianmarco Bonacina – Banca Akros S.p.A., Research Division Didier Scemama – BofA Securities, Research Division Joshua Buchalter – TD Cowen, Research Division Jakob Bluestone – BNP Paribas, Research Division Domenico Ghilotti – Equita SIM S.p.A., Research Division

Presentation

Advertisement

Operator

Ladies and gentlemen, welcome to the ST The LEO Opportunity Conference Call and Live Webcast. I am Sandra, the Chorus Call operator. [Operator Instructions] The conference must not be recorded for publication or broadcast. At this time, it is my pleasure to hand over to Jerome Ramel, EVP, Corporate Development and Integrated External Communications. Please go ahead, sir.

Jerome Ramel Executive VP of Corporate Development & Integrated External Communication

Advertisement

Thank you. Thank you, everyone, for joining ST the LEO Opportunity Conference Call. Hosting the call today is Remi El-Ouazzane, President, Microcontrollers, Digital ICs and RF product groups. This live webcast and presentation materials can be accessed on the ST Investor Relations website. A replay will be available shortly after the conclusion of this call. This call will include forward-looking statements that involve risk factors that could cause ST results to differ materially from management expectations and plans. We encourage you to review the safe harbor statement contained in the press release , the financial results this morning and also in ST’s most recent regulatory filings for a full description of these risk factors. [Operator Instructions] I’d like now to turn the call over to Remi El-Ouazzane.

Remi El-Ouazzane President of Microcontrollers, Digital ICs & RF Products Group

Mumbai: Shares of several companies headquartered in West Bengal rose Monday as the BJP emerged victorious in the state assembly polls, defeating the ruling Trinamool Congress (TMC).

Analysts, however, cautioned investors against buying into the sentiment-driven frenzy, instead advising them to wait for clarity on policy implementation by the incoming administration and impact on company earnings.

Shares of CESC, the Kolkata-based flagship company of the RP-Sanjiv Goenka Group, which supplies electricity to the state capital and other parts of West Bengal, rallied over 6.5%. West Bengal-based tea companies McLeod Russel India, and Dhunseri Tea saw their share prices rise 5% and 3%, respectively. Bandhan Bank jumped 3.4%, while Emami climbed 2.6%.

Agencies

“This looks like a classic sentiment-driven rally rather than a structural rerating,” said Gautam Duggad, head of research – institutional equities at Motilal Oswal Financial Services. “The trigger appears to be a sentiment booster which has led to a sharp uptick in West Bengal-headquartered names. However, such moves tend to be transient unless backed by earnings visibility.”

Live Events

Assuming that the BJP will be taking charge of West Bengal, the policy will be pro-growth, which could help industries based out of Kolkata or West Bengal in the medium-tolong-term perspective, said Sunny Agrawal, head of fundamental research at SBI Securities. “The rising stock price today is predominantly on the back of positive sentiment on account of this election outcome,” he said. “The actual impact in terms of changes in the policy and its impact on the businesses will be seen over a medium to long term.”Most analysts say it could take 18–24 months for any policy or structural changes to get fully implemented. Only thereafter, clarity will emerge on whether the policy moves would positively impact earnings of companies that have rallied on expectations tied to the election outcome.

In terms of outlook, Agrawal believes that for the new government, the low-hanging fruit in terms of policy changes can be in sectors like aquaculture, fisheries and ports as West Bengal is a coastal belt.

Advertisement

“BJP is known for creating state of-art infrastructure in any state, so infrastructure like roads, bridges and railways can be another focus area for a new incoming government,” said Agrawal. In addition, companies can benefit from a pro-industrial and pro-growth policy in existing businesses across sectors.

Duggad said from the medium to long-term perspective, sustainability of share prices will hinge on core fundamentals and earnings. “Investors should be careful not to extrapolate this momentum blindly, as stock-specific performance will ultimately converge with earnings delivery rather than sentiment alone.”

SBI Securities recommended investors to focus on fundamentals of West Bengal-based company stocks in the coming 12 to 36 months. “We continue to maintain apositive stance on few large established businesses like Emami, Britannia, ITC or CESC, which is more of a power-related sector and constructive on Bandhan Bank.”

Hancock Prospecting has referred an $850 million gas plant to regulators, outlining a Perth Basin gas vision beyond the assets it acquired from Mineral Resources in 2024.

Fund investors can thank the big tech stocks for getting the second quarter off to a better start than the first.

Powered by gains in Nvidia and Google parent Alphabet, the stock market in April logged its best month since 2020, shaking off declines in the first quarter when the war in Iran started. That in turn, powered the average U.S.-stock mutual fund or exchange-traded fund to a total return of 10.3% for April, according to statistics from LSEG. (See Mutual-Fund Yardsticks table.)

Oil prices edged lower on Tuesday after surging as much as 6% in the previous session, as signs emerged that the U.S. Navy is easing Iran’s blockade of the Strait of Hormuz, raising hopes of some supply returning from the Middle East.

The United States on Monday began a fresh operation to reopen the key waterway. Shipping group Maersk later confirmed that its U.S.-flagged vehicle carrier, Alliance Fairfax, had successfully exited the Gulf through the strait under U.S. military escort, calming immediate concerns over supply disruptions.

Crude oil price on May 5

Brent crude for July delivery slipped 68 cents, or 0.6%, to $113.76 a barrel after rising 5.8% on Monday. U.S. West Texas Intermediate (WTI) crude dropped $1.59, or 1.5%, to $104.83, following a 4.4% gain in the prior session.Tensions, however, remain elevated. Iran launched attacks in the Gulf on Monday in response to the U.S. move, as both sides vie for control of the Strait of Hormuz, a crucial route that typically carries around 20% of global oil and gas supply each day.

Advertisement

Live Events

Reports indicated that several commercial ships were hit in the area, while an important oil port in the United Arab Emirates caught fire following an Iranian strike. The U.S. effort to secure the waterway marks the most significant escalation since a ceasefire was declared four weeks ago. In a separate post on Truth Social, he said a South Korean cargo ship had come under fire and suggested that South Korea should consider joining the mission. In an interview with Fox News, U.S. President Donald Trump warned that Iran would be “blown off the face of the earth” if it attacked U.S. ships protecting commercial traffic. The U.S. push to reopen Hormuz comes after Iran largely shut the passage following the outbreak of war with the U.S. and Israel on February 28, triggering a major disruption to global energy supplies. On the outlook, Haitong Futures, as cited by Reuters, noted that the current ceasefire could be temporary. A lack of progress in U.S.-Iran talks by the end of April may lead to renewed escalation, potentially pushing oil prices higher.

Macquarie expects crude to remain supported in the $85 to $90 range in the near term, gradually moving toward $110 as supply conditions improve. However, it cautioned that prolonged disruptions through April could drive Brent as high as $150 per barrel.

Nuvama Institutional Equities echoed a similar view, stating that an extended shutdown of the Strait of Hormuz, which carries around 20 million barrels per day, could lift crude prices into the $110 to $150 range.

(Disclaimer: Recommendations, suggestions, views and opinions given by the experts are their own. These do not represent the views of The Economic Times)

NEW YORK — John Sterling, the unmistakable voice of the New York Yankees for 36 seasons and one of the most beloved broadcasters in Major League Baseball history, died Monday at the age of 87. The Yankees confirmed the news, saying Sterling passed peacefully at his home in New Jersey surrounded by family. Known for his theatrical home run calls, unwavering optimism and deep connection with generations of fans, Sterling became synonymous with Yankees baseball through more than three decades behind the microphone.

Sterling joined the Yankees radio booth in 1989 and remained the team’s primary play-by-play voice until his retirement in 2024. His signature home run call — “It is gone!” followed by the player’s name stretched dramatically — became part of Yankees lore, heard on car radios, in living rooms and at backyard barbecues across the tri-state area for more than three decades. From Don Mattingly to Derek Jeter, Mariano Rivera to Aaron Judge, Sterling narrated the franchise’s modern golden era with passion and consistency.

Born in 1938 in New York City, Sterling began his broadcasting career in the minor leagues before moving to television and radio work in Atlanta with the Braves. He returned to New York in the late 1980s and quickly won over Yankees fans with his distinctive style. Unlike many play-by-play announcers who favored restraint, Sterling embraced emotion, turning routine fly balls into dramatic theater and walk-off wins into unforgettable radio moments.

His most famous calls captured the heart of Yankees baseball during championship runs in the 1990s and 2000s. “Bernie Williams, it is gone!” and “A-Rod, there it goes!” echoed through the boroughs and suburbs as the team won five World Series titles during his tenure. Sterling was behind the mic for countless iconic moments, including David Wells’ perfect game in 1998 and Mariano Rivera’s record-breaking 602nd save.

Advertisement

Yankees owner Hal Steinbrenner issued a statement calling Sterling “part of the fabric of this organization and this city.” “John wasn’t just the voice of the Yankees — he was family,” Steinbrenner said. “His passion, humor and dedication to our fans made every summer better. We will miss him dearly.” Current Yankees manager Aaron Boone, who played under Sterling’s broadcasts as a player, described him as “the soundtrack of my childhood and my career.”

Tributes poured in across baseball. Commissioner Rob Manfred called Sterling “a true original whose voice defined an era for one of the game’s great franchises.” Former players including Derek Jeter, Andy Pettitte and Jorge Posada shared personal memories on social media, many recalling late-night conversations on team flights and Sterling’s encyclopedic knowledge of Yankees history.

Sterling’s style was unmistakable. He rarely missed a game, earning a reputation for durability and professionalism. Even through health challenges in recent years, he maintained his enthusiasm and distinctive delivery. His retirement in 2024 was marked by emotional ceremonies at Yankee Stadium, where fans and players honored the man who had narrated so many of their favorite memories.

Beyond the calls, Sterling was known for his warmth and accessibility. He frequently engaged with fans at spring training, signed autographs without hesitation and remembered names of longtime listeners. His pregame and postgame shows became appointment listening for generations of Yankees supporters who couldn’t attend games in person.

Advertisement

Sterling’s influence extended beyond the booth. He was a mentor to younger broadcasters and a champion of baseball’s storytelling tradition in an era increasingly dominated by analytics and visual highlights. Colleagues described him as a consummate professional who prepared meticulously for every broadcast while maintaining a sense of joy and wonder about the game.

The news of his passing prompted an outpouring of memories from fans across social media. Many shared how Sterling’s voice accompanied family road trips, backyard games and quiet evenings. For countless New Yorkers, hearing “The Yankees win!” on the radio meant summer nights and hope, even in losing seasons.

Sterling is survived by his wife, several children and grandchildren. Funeral arrangements are expected to be announced in the coming days, with a public memorial likely at Yankee Stadium later this season. The Yankees will honor his legacy with a moment of silence and special tributes during upcoming home games.

In many ways, Sterling represented the golden age of baseball broadcasting — a time when radio voices created vivid pictures in listeners’ minds and became trusted companions through long seasons. His departure leaves a void that may never be fully filled, as modern broadcasts shift toward more analytical and data-driven approaches.

Advertisement

Yet Sterling’s impact endures. His calls remain embedded in the collective memory of Yankees fans, replayed on social media and in documentaries. Young broadcasters still study his phrasing and energy. For millions, the sound of summer in New York will always include that familiar voice rising with excitement as another ball sailed into the night.

As the Yankees continue their 2026 season, they do so without the man who narrated so many of their greatest moments. But for those who grew up listening to John Sterling, every crack of the bat and roar of the crowd will carry a faint echo of his unmistakable joy and passion for the game he loved so deeply.

Mumbai: Individual participation in Indian equities showed a sharp divergence amid sharp swings in January-March, with their direct equity ownership falling for the third straight quarter, while mutual fund holdings, fuelled by retail flows surging to a fresh record. Foreign ownership fell to a 14-year low of 16.1% in the March quarter, underscoring their risk-off sentiment towards domestic stocks, while domestic institutional holdings rose to another all-time high.

The combined holdings of retail and high net worth investors in NSE-listed companies declined to a five-year low of 9.1% in the March quarter, down from 9.3% in the December quarter, according to data from primeinfobase.com. Meanwhile, mutual fund holdings rose for the 11th straight quarter to an all-time high of 11.46% from 11.1% in December.

“This indicates individual investors may be preferring to invest through a professional fund manager,” said Pranav Haldea, managing director, PRIME Database Group.

Agencies

SHARP SWINGS IN JAN-MARCH Combined holdings of retail investors & HNIs in NSE-listed cos down to a 5-year low of 9.1% in Q3 l Foreign ownership slips to a 14-year low

Across NSE-listed companies, the retail investors’ direct holdings declined from 7.25% to 7.12% in the March quarter – declining for the third quarter in a row. HNI ownership slipped to 1.9% from 2.03% in the same period. These investors cut their stakes, especially in mid-cap and small-cap companies amid the severe market sell-off in March–marking the worst monthly fall since March 2020, the onset of the Covid-19 wave and the record-breaking rally in precious metals.

Advertisement

Live Events

“HNIs turned discerning and retail investors flocked to other assets such as gold, silver and REITs due to the lethargic equity returns,” said Riddhiman Jain, managing director and head – investment strategy and solutions, Waterfield Advisors. In the quarter ended March 31, Nifty plunged 14.5% while Nifty Midcap 150 and Smallcap 250 dropped 12.7% and 14.4%, respectively.The Nifty 500 index tumbled 14%. Gold rose 6.7%, and Silver gained 6.1%.

But for the purchases by domestic institutions, including mutual funds, pension funds and insurance companies, among others, the equity fall would have been sharper.

“The strong SIP culture prompted investors to allocate money to fund managers through passive investing instead of tracking price movements and reacting to market fluctuations due to fear,” said Siddarth Bhamre, head of research, Asit C Mehta Intermediates. “Retail money through mutual funds will continue to bail out the market. Until their invested corpus doesn’t witness an erosion, SIP money is expected to continue.”

Performance data shown represents past performance. Investment returns and principal value will fluctuate, so that fund shares, when redeemed, may be worth more or less than the original cost. Past performance does not guarantee future results and current performance may be lower or higher than the performance data shown. Visit Madison Funds or call 800.877.6089 to obtain performance data current to the most recent month-end.

Tickers

Portfolio Management

Faraz Farzam, CFAPortfolio Manager, AnalystIndustry since 1999

Advertisement

Aaron Garcia, CFAPortfolio Manager, AnalystIndustry since 2002

Software vs. S&P 500 Index

Although the information in this report has been obtained from sources that the firm believes to be reliable, we do not guarantee its accuracy, and any such information may be incomplete or condensed. All opinions included in the report constitute the authors’ judgment as of the date of this report and are subject to change without notice. This report is for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security and is not investment advice.

Madison Asset Management, LLC does not provide investment advice directly to shareholders of the Madison Funds. Opinions stated are informational only and should not be taken as investment recommendation or advice of any kind whatsoever (whether impartial or otherwise).

Advertisement

Why Madison Small Cap Fund?

High-quality portfolio of quality, durable, and growing small companies

Concentrated portfolio with a flexible mandate ($100M to $15B market cap)

Proprietary Risk Portal and valuation discipline framework help manage downside risk

Advertisement

Average Annual Total Returns ¹,² (%)

3-Months

YTD

1-Year

3-Year

5-Year

10-Year

Since Inception

Class R6

0.10

0.10

2.38

7.75

—

—

2.08

Class I

0.10

0.10

2.29

7.67

1.19

—

1.74

Class Y

0.10

0.10

2.19

7.58

1.07

7.68

11.93

Class A without sales charge

0.00

0.00

1.94

7.31

0.83

—

7.55

Class A with sales charge

-5.76

-5.76

-3.88

5.20

-0.36

—

6.59

Russell 2000

0.89

0.89

25.72

13.05

3.77

9.88

—

Russell 2500

2.04

2.04

23.45

13.25

5.48

10.58

—

Calendar Year Returns ¹,² (%)

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

Class Y

18.04

8.90

-12.09

24.67

23.09

20.52

-24.36

16.05

21.94

-7.12

Russell 2000

21.31

14.65

-11.01

25.52

19.96

14.82

-20.44

16.93

11.54

12.81

Russell 2500

17.59

16.81

-10.00

27.77

19.99

18.18

-18.37

17.42

12.00

11.91

Performance data shown represents past performance. Investment returns and principal value will fluctuate, so that fund shares, when redeemed, may be worth more or less than the original cost. Past performance does not guarantee future results and current performance may be lower or higher than the performance data shown. Visit Madison Funds or call 800.877.6089 to obtain performance data current to the most recent month-end.

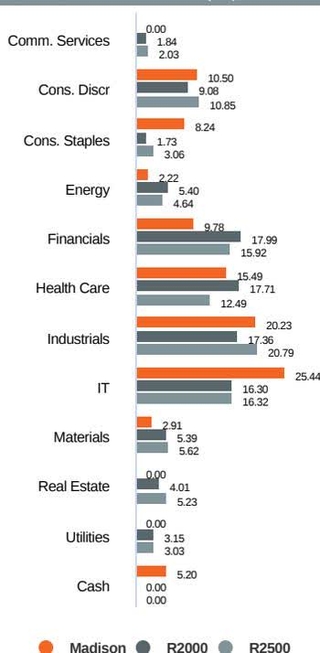

Sector Allocation (%)

Advertisement

5-Year Risk Metrics (%) – Class Y

Madison

R2000

Standard Deviation

17.17

19.98

Up Capture

77.47

100.00

Down Capture

85.10

100.00

Beta

0.80

1.00

5-Year Risk Metrics (%) – Class Y

Advertisement

Madison

R2500

Standard Deviation

17.17

18.67

Up Capture

79.37

100.00

Down Capture

93.18

100.00

Beta

0.88

1.00

Investment Objective

The Madison Small Cap Fund seeks long-term capital appreciation.

Class

Ticker

Inception

Exp. Ratio

R6

MSCRX

02/28/22

0.92%

I

MSCIX

02/26/21

1.00%

Y

BVAOX

12/16/96

1.10%

A

MASMX

08/31/19

1.35%

Expense ratios are based on the fund’s most recent prospectus.

Advertisement

Fund Characteristics

Number of Holdings

49

EPS Growth Rate (Trailing 3-Year, %)

8.14

Price/Earnings Ratio (Trailing 1-Year)

25.20

Price/Earnings Ratio (Forward 1-Year)

17.16

Annual Portfolio Turnover (%)

35.00

Active Share vs. R2000 (%)

97.40

Active Share vs. R2500 (%)

96.83

Wtd. Avg. Market Cap ($ billions)

5.88

Net Assets ($ millions)

146.53

Distribution Frequency

Annual

Portfolio Management

Faraz Farzam, CFAPortfolio Manager, AnalystIndustry since 1999

Advertisement

Aaron Garcia, CFAPortfolio Manager, AnalystIndustry since 2002

Madison FundsP.O. Box 219083Kansas City, MO 64121-9083800.877.6089

Consultant andAdvisor Services

550 Science DriveMadison, WI 53711888.971.7135

This material is authorized for use only when preceded or accompanied by the current prospectus. Before investing, please fully consider the investment objectives, risks, charges and expenses of the fund. This and other important information is contained in the current prospectus, which you should carefully read before investing or sending money. For more complete information about Madison Funds® obtain a prospectus from your financial adviser, by calling 800.877.6089 or by visiting Madison Funds to view or download a copy.

Advertisement

Performance results prior to August 30, 2019 for the Class Y shares are based on the performance of the Predecessor Fund, which was reorganized into the Class Y shares of the Fund on August 30, 2019. Performance for Class A shares was deemed to be new effective August 31, 2019 as a result of the reorganization. Madison waived 0.04% of the Fund’s annual services fee from August 31, 2019 through February 27, 2021. Investment returns reflect this fee waiver, without which returns would have been lower.

Madison lists the performance of the Predecessor Fund and accounting survivor of the Reorganization for the following reasons: Continuity of Fund portfolio managers through the Reorganization; Substantially the same investment objective and investment strategies between the Fund and the Predecessor Fund; Substantially similar investment policies between the Fund and the Predecessor Fund; A similar expense ratio (excluding acquired fund fees and expenses).

Madison Asset Management, LLC does not provide investment advice directly to shareholders of the Madison Funds.

Madison Funds are distributed by MFD Distributor, LLC, member of FINRA. Portfolio data is as of the date of this piece unless otherwise noted and holdings are subject to change.

Advertisement

“Madison” and/or “Madison Investments” is the unifying tradename of Madison Investment Holdings, Inc., Madison Asset Management, LLC (“MAM”), and Madison Investment Advisors, LLC (“MIA”). MAM and MIA are registered as investment advisers with the U.S. Securities and Exchange Commission. Madison Funds are distributed by MFD Distributor, LLC. MFD Distributor, LLC is registered with the U.S. Securities and Exchange Commission as a broker-dealer and is a member firm of the Financial Industry Regulatory Authority. The home office for each firm listed above is 550 Science Drive, Madison, WI 53711. Madison’s toll-free number is 800-767-0300.

Any performance data shown represents past performance. Past performance is no guarantee of future results.

This report is for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security and is not investment advice.

Non-deposit investment products are not federally insured, involve investment risk, may lose value and are not obligations of, or guaranteed by, any financial institution. Investment returns and principal value will fluctuate.

Advertisement

An investment in the Fund is subject to risk and there can be no assurance the Fund will achieve its investment objective. The risks associated with an investment in the Fund can increase during times of significant market volatility. The principal risks of investing in the Fund include mid cap risk, equity risk, growth and value risks, capital gains realization risks to taxpaying shareholders, foreign security and emerging market risk, depository receipt risk, and market risk. Investing in small, mid-size or emerging companies involves greater risks not associated with investing in more established companies, such as business risk, significant stock price fluctuations and illiquidity. More detailed information regarding these risks can be found in the Fund’s prospectus.

Upon request, Madison may furnish to the client or institution a list of all security recommendations made within the past year.

Indices are unmanaged. An investor cannot invest directly in an index. They are shown for illustrative purposes only, and do not represent the performance of any specific investment. Index returns do not include any expenses, fees or sales charges, which would lower performance.

Russell 2000 Index: small cap market index that measures the performance of the smallest 2,000 companies in the Russell 3000® Index.

Advertisement

Russell 2500 Index: broad index, featuring 2,500 stocks that cover the small and mid-cap market capitalizations of the U.S. equity universe.

Russell Investment Group is the source and owner of the trademarks, service marks and copyrights related to the Russell Indexes. Russell® is a trademark of Russell Investment Group.

EPS Growth (Trailing 3-yr): the annual rate at which a company’s earnings have grown over the past three years.

Price-to-Earnings Ratio: measures how expensive a stock is. It is calculated by the weighted average of a stock’s current price divided by the company’s earnings per share of stock in a portfolio.

Advertisement

Portfolio Turnover: a measure of the trading activity in an investment portfolio—how often securities are bought and sold by a portfolio.

Active Share: the percentage of a portfolio that differs from its benchmark index. It can range from 0% for an index fund that perfectly mirrors its benchmark to 100% for a portfolio with no overlap with an index.

Wtd Avg. Market Cap: the size of the companies in which the fund invests. Market capitalization is calculated by the number of a company’s shares outstanding times its price per share.

Standard Deviation: a statistical measurement of dispersion about an average, which, for a portfolio, depicts how widely the returns varied over a certain period of time. Investors may use the standard deviation of historical performance to understand the range of returns for a portfolio. When a portfolio has a higher standard deviation than its benchmark, it implies higher relative volatility. Standard deviation has been calculated using the trailing monthly total returns for the appropriate time period. The standard deviation values are annualized.

Advertisement

Upside Capture Ratio: a fund’s performance in up markets relative to its benchmark. The security’s upside capture return is divided by the benchmark’s upside capture return over the time period.

Downside Capture Ratio: a fund’s performance in down markets relative to its benchmark. The security’s downside capture return is divided by the benchmark’s downside capture return over the time period.

Beta: a measure of the fund’s sensitivity to market movements. A portfolio with a beta greater than 1 is more volatile than the market, and a portfolio with a beta less than 1 is less volatile than the market.

You must be logged in to post a comment Login