Business

Analysts Urge Buy Amid AI Boom Despite High Valuation Risks

NEW YORK — NVIDIA Corp. shares hover near $200 in mid-April 2026, trading as the world’s most valuable company with a market capitalization topping $4.9 trillion, as Wall Street analysts overwhelmingly recommend buying the stock amid unrelenting demand for its artificial intelligence chips.

The semiconductor giant, whose stock has seen volatile swings this year after a massive multi-year rally, continues to dominate the AI infrastructure market. As of April 17, 2026, NVIDIA closed at approximately $201.68, up about 1.68 percent in the session amid high trading volume exceeding 147 million shares. The 52-week range spans from a low near $95 to a high above $212, reflecting both the explosive growth in AI spending and periodic market concerns over valuations.

Analysts maintain a strong consensus “Buy” or “Strong Buy” rating on NVIDIA. Across more than 50 Wall Street firms, the overwhelming majority — often 90 percent or higher — rate the stock as a purchase. The average 12-month price target sits around $268 to $275, implying roughly 35 percent upside from current levels. Some optimistic forecasts reach as high as $400, while more conservative ones hover near $205.

Recent financial performance underscores the bullish case. In the most recent reported quarters, NVIDIA posted record revenues driven by its data center segment, which accounts for the vast majority of sales. Blackwell architecture chips, the company’s latest flagship for AI training and inference, have seen strong adoption across major cloud providers, hyperscalers and enterprises. CEO Jensen Huang has repeatedly described demand as “insane” or “off the charts,” with supply commitments and visibility extending well into future years.

For investors debating whether to buy or sell NVIDIA stock in 2026, the dominant narrative centers on artificial intelligence as a transformative, multi-year secular trend. Data center revenue has surged year-over-year, fueled by exponential growth in AI model training, inference workloads and the emergence of AI agents. Companies like Meta, Microsoft, Google and others continue pouring billions into GPU clusters to power large language models and next-generation applications.

NVIDIA’s upcoming Rubin platform, expected later in 2026, is already generating excitement as the successor to Blackwell. Analysts anticipate this next architecture will sustain momentum, with some projecting continued high-teens to low-20s percentage revenue growth rates even as the base expands dramatically. Gross margins remain robust, often exceeding 70 percent on a non-GAAP basis, supporting healthy profitability and free cash flow generation that funds share buybacks and innovation.

Yet the “sell” side of the debate highlights legitimate risks that could pressure the stock. NVIDIA trades at an elevated forward price-to-earnings multiple in the mid-20s to low-30s range depending on estimates, far above historical averages for semiconductor firms. Critics argue that much of the AI hype is already priced in, leaving limited room for error if hyperscaler capital expenditure growth decelerates or if economic conditions tighten.

Competition poses another headwind. Tech giants are developing in-house AI chips — such as Google’s TPUs, Amazon’s Trainium and custom silicon from startups — aiming to reduce reliance on NVIDIA hardware. While NVIDIA maintains an estimated 80-90 percent market share in high-end AI accelerators, any meaningful erosion could impact pricing power and growth trajectories.

Geopolitical tensions add uncertainty. U.S. export restrictions to China, a once-significant market, continue to limit sales. Management has guided future quarters assuming no meaningful data center revenue from China, shifting focus entirely to other regions. Any escalation in trade disputes or broader semiconductor supply chain disruptions could affect results.

Valuation concerns have manifested in periodic pullbacks. The stock entered 2026 with some softness amid broader market rotations away from mega-cap tech, though it has stabilized near recent highs. Short-term technical patterns show support levels around $180-190, with resistance near $210-220. Longer-term bulls point to historical resilience: NVIDIA has repeatedly overcome skepticism during previous chip cycles.

Institutional ownership remains high, with mutual funds and hedge funds maintaining significant positions. Retail investors, many of whom rode the post-2022 AI surge, continue monitoring the name closely. Options activity reflects mixed sentiment, with some positioning for volatility around upcoming earnings or product events.

For long-term holders, the bull thesis rests on AI’s expanding total addressable market. Estimates for the AI infrastructure opportunity range into the trillions over the coming decade, with NVIDIA positioned as the pick-and-shovel provider. Inference — running trained models in real-world applications — is seen as the next growth leg, potentially dwarfing training spending. Software advancements, including CUDA ecosystem lock-in, further entrench the company’s moat.

Short-term considerations for 2026 include the pacing of Blackwell ramp-up and early signals on Rubin adoption. Positive updates could catalyze fresh rallies, while any signs of softening demand or inventory buildup might trigger selloffs. Broader economic factors, including interest rates, corporate spending and potential recession risks, will also influence sentiment.

Diversification remains key advice from financial planners. While NVIDIA has delivered extraordinary returns for early believers, concentrated bets in any single stock carry risk, especially one as volatile as a high-growth technology leader. Investors considering new positions may dollar-cost average or wait for dips below key moving averages.

NVIDIA’s financial strength provides a buffer. The company generates tens of billions in free cash flow annually, maintains a fortress balance sheet with low debt relative to cash reserves, and consistently returns capital through dividends and aggressive buybacks. These factors support resilience during market corrections.

Looking further into 2026 and beyond, some optimistic models project NVIDIA shares could reach $250-$300 by year-end if AI spending trajectories hold. More cautious scenarios see the stock trading sideways or modestly higher if growth moderates to mid-30s percentages. A handful of bearish voices warn of potential 20-30 percent corrections if multiple compression coincides with any earnings miss.

Ultimately, the decision to buy or sell NVIDIA in 2026 hinges on an investor’s time horizon, risk tolerance and conviction in artificial intelligence as a once-in-a-generation platform shift. For growth-oriented portfolios, the consensus leans heavily toward accumulation on weakness. Value-conscious or defensive investors may prefer waiting for clearer evidence of sustainable margins or multiple contraction.

As the company prepares for its next earnings cycle and major technology conferences, all eyes remain on execution. NVIDIA has historically underpromised and overdelivered during AI’s ascent, building credibility that sustains premium valuations.

Market participants in Seoul and global financial centers continue tracking the stock closely, given its influence on broader technology indices and semiconductor supply chains. Exchange-traded funds heavy in NVIDIA, such as those tracking the Nasdaq-100, amplify its impact on retail portfolios worldwide.

In summary, while risks of competition, valuation and cyclical slowdown exist, the prevailing analyst view supports buying NVIDIA shares for those with a multi-year horizon. The AI tailwinds appear durable, powered by massive infrastructure buildouts that few other companies can match in scale or sophistication.

Investors should consult personal financial advisors and conduct thorough due diligence, as past performance does not guarantee future results. Stock prices can fluctuate sharply, and no single name should dominate any portfolio.

With AI adoption accelerating across industries — from healthcare and automotive to finance and entertainment — NVIDIA’s central role suggests the story has further chapters. Whether 2026 brings new highs or testing periods, the company remains at the epicenter of one of the most profound technological transformations in modern history.

In final moments before truce, Israeli strike kills Lebanese man’s family

Brazil’s Lula calls on permanent members of UN Security Council to change behaviour

The company reported a net loss of 29.09 crore in the January-March quarter a year ago, according to a regulatory filing by Network18 Media, a subsidiary of billionaire Mukesh Ambani-led Reliance Industries Ltd.

Its consolidated revenue from operations rose by 9.7 per cent to Rs 615.78 crore in the March quarter compared to Rs 561.32 crore in the corresponding quarter in the last fiscal.

Consolidated operating revenue for the quarter increased by 9.7 per cent “despite the multiple headwinds in the macro environment. On a QoQ basis, the revenue grew 14.2 per cent,” said Network18 Media & Investments in its earnings statement.

Advertising inventory demand for the TV news industry declined by 10 per cent YoY, but Network18’s inventory grew 4.5 per cent, helping the company perform better than the industry.

“Company’s diversified portfolio, strong market positions across markets, and revenue from new businesses helped soften the impact of a weak advertising environment,” it said.

EBITDA for the quarter was Rs 30 crore with a margin of 4.9 per cent, it added.Its total expenses were at Rs 670.89 crore, up 6.47 per cent in the March quarter.

Network18 Media’s total consolidated income, which includes other income, was at Rs 616.21 crore, up 9.14 per cent in Q4 of FY26.

On a standalone basis, Network18’s loss widened to Rs 72.51 crore in the March quarter compared to a loss of Rs 69.48 crore in the corresponding quarter of the last fiscal. Revenue from operations rose by 4.85 per cent year-on-year to Rs 547.07 crore in the March quarter.

For the entire FY26, Network18 Media & Investments’ profit was at Rs 155.20 crore. Consolidated income was at Rs 2,148.46 crore for the financial year ended on March 31, 2026.

“Excluding the first quarter, which had a decline in revenue due to a high base of election-linked advertising in the previous fiscal, revenue was up 7 per cent. Operating costs grew in line with revenue, resulting in flat EBITDA,” it said.

According to the company, its “figures for the corresponding previous year are not comparable” as Indiacast Media Distribution and Studio 18 Media(Formerly Viacom 18) ceased to be a subsidiary of the Company on 14th November, 2024 and 30th December, 2024, respectively.

Network18 continues to be India’s leading TV news network, with a portfolio of 20 channels (including 14 regional channels), and the largest in terms of reach and viewership.

“The network reached over 2,305 million people a month, 35 per cent higher than the nearest competitor, and had an all-India viewership share of 13.8 per cent,” it said.

It also leads in the digital segment with its platforms – Moneycontrol, News18, Firstpost and CNBCTV18. It has over 360 million monthly users, representing 65 per cent reach in the segment, Network18 said.

Commenting on the results, Chairman Adil Zainulbhai said: “We ended the year on a positive note despite the geopolitical crisis that the world finds itself immersed in currently. In a year marked by high news flow volumes, our network has taken the lead in delivering news over noise, consistently. We are happy with the progress made on the operating front during the year and the impressive scale-up of new businesses in a short time, which is helping us diversify our revenue base.”

The company is focused on strengthening its core news business even as it expands presence in adjacent categories, he added.

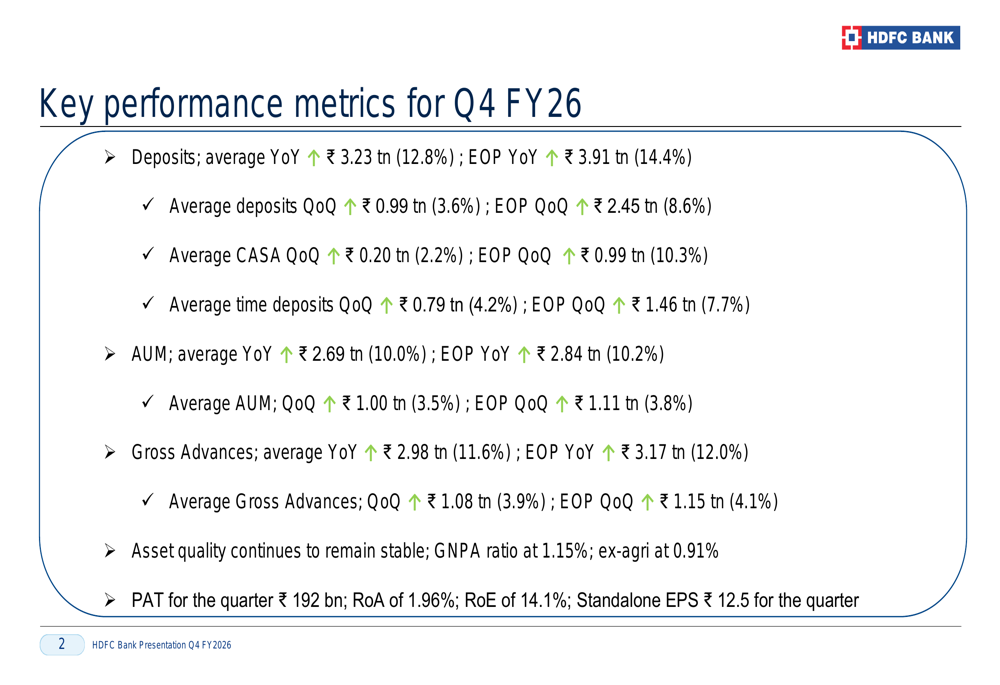

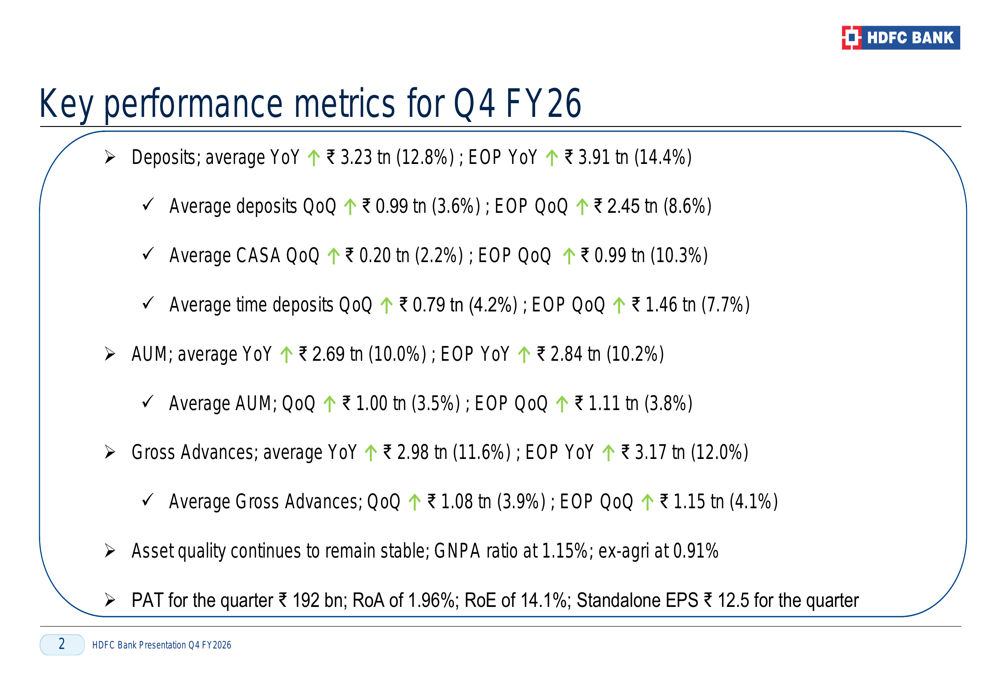

HDFC Bank Q4 FY26 slides: deposit surge drives growth amid stability

Sterling Infrastructure: Impressive Yet Expensive

Earnings call transcript: HDFC Bank Q4 2026 shows strong growth amid challenges

Buying The Fear Before It Shows Up: The PBDC Setup

How InvestingPro’s Fair Value spotted 66% upside in Cimpress stock

ProCap Financial chief market strategist Phil Rosen joins Varney & Co. to discuss brokerage firms introduce investment accounts for teenagers and Allbirds’ pivot to AI on ‘Varney & Co.’

Major brokerages are increasingly targeting younger investors, opening the door for teenagers to begin building portfolios years before they traditionally would.

ProCap Financial chief market strategist Phil Rosen joined FOX Business’ Stuart Varney on “Varney & Co.” to discuss the shift, framing it as part of a broader industry push to capture the next generation of clients amid changing demographics.

New York Stock Exchange on Wall Street. (angeluisma / Getty Images)

Firms like Charles Schwab and Fidelity have long catered to older investors, but the rise of mobile-first platforms such as Robinhood, which counts a large share of millennial and Gen Z users, has intensified competition. Rosen pointed to that dynamic as a key driver behind the push into teen accounts, as legacy firms look to establish relationships earlier in investors’ life cycles.

Morningstar CEO Kunal Kapoor shares ETFs worthy of long-term investment on ‘The Claman Countdown.’

“I’m very much in the camp that the younger you are to get into investing that’s a good thing, right, because that could be millions of millions of dollars difference by the time you retire if you start at 15 as opposed to 25,” Rosen said.

The trend reflects a broader cultural shift toward financial literacy and early investing, with more young people gaining exposure to markets through apps and social media. At the same time, Rosen cautioned that education remains critical as younger investors navigate increasingly complex and volatile markets.

Sequoia Capital partner Konstantine Buhler discusses Waymo and the companies showcased at the HumanX conference on ‘The Claman Countdown.’

“If we can get them to avoid those things, then I think it’s [a] good thing to get people involved in the markets,” Rosen said, warning against speculative trading behavior like meme stocks and short-term options.

As competition heats up, brokerages appear willing to rethink traditional entry points in an effort to secure long-term growth.

Procter & Gamble: Management Said The Worst Is Over, But Q3 Earnings May Be Key

I’m A Celebrity’s Scarlett Moffatt discusses emotional miscarriage ‘it was awful’

In final moments before truce, Israeli strike kills Lebanese man’s family

Alito and Thomas Stay On

-

NewsBeat6 days ago

NewsBeat6 days agoPep Guardiola and Gary Neville agree over Arsenal title problem that benefits Man City

-

Crypto World5 days ago

Crypto World5 days agoThe SEC Conditionalises DeFi Platforms to Be Avoided for Broker Registration

-

Politics6 days ago

Politics6 days agoWorld Cup exit makes Italy enter crisis mode

-

Crypto World5 days ago

Crypto World5 days agoSEC Signals Exemption for Crypto Interfaces From Broker Registration

-

Fashion19 hours ago

Fashion19 hours agoWeekend Open Thread: Theodora Dress

-

News Videos3 days ago

News Videos3 days agoSecure crypto trading starts with an FIU-registered

-

Sports1 day ago

Sports1 day agoNWFL Suspends Two Players Over Post-Match Clash in Ado-Ekiti

-

Crypto World4 days ago

Crypto World4 days agoSEC Proposes Certain Crypto Interfaces Don’t Need to Register as Brokers

-

Business7 days ago

Business7 days agoIreland Fuel Protests Enter Day 5 as Blockades Spark Shortages and Government Prepares Support Package

-

NewsBeat4 days ago

NewsBeat4 days agoTrump and Pope Leo: Behind their disagreement over Iran war

-

Politics16 hours ago

Politics16 hours agoPalestine barred from entering Canada for FIFA Congress

-

NewsBeat6 days ago

NewsBeat6 days agoJD Vance announces ‘no agreement’ with Iran over nuclear weapons fear

-

Crypto World14 hours ago

Crypto World14 hours agoRussia Pushes Bill to Criminalize Unregistered Crypto Services

-

Sports6 days ago

Dexter Lawrence, Stefon Diggs, Trading for De’Von Achane

-

Crypto World5 days ago

Crypto World5 days agoTrump whales load up ahead of Mar-a-Lago luncheon.

-

Crypto World6 days ago

Crypto World6 days agoSei Network Enters Quiet Reset Phase as On-Chain Metrics Signal a Slowdown in 2026

-

Business2 days ago

Business2 days agoCreo Medical agree sale of its manufacturing operation

-

Sports5 days ago

Sports5 days agoNWFL opens Pathway for new Clubs ahead of 2026 Season

-

Business5 days ago

Kering slides after Morgan Stanley downgrade, Gucci woes loom

-

Entertainment4 days ago

Entertainment4 days agoKarol G’s ‘Ultra Raunchy’ Coachella Set Gave ‘Satanic Vibes’

You must be logged in to post a comment Login