Business

Apple Stock Holds Steady Near $252 as Geopolitical Tensions and Oil Surge Test Tech Resilience

Apple Inc. (NASDAQ: AAPL) shares closed at $252.89 on Thursday, up modestly by 0.27 or 0.11% from the prior session, demonstrating relative stability in a turbulent market rocked by escalating uncertainties in the U.S.-Iran conflict and sharply higher oil prices that stoked inflation fears across Wall Street.

![]()

The iPhone maker’s performance stood out amid broader selling pressure. While the Dow Jones Industrial Average plunged 469.38 points, or 1.01%, to close at 45,960.11, and the Nasdaq Composite dropped more than 2%, Apple managed a narrow gain on volume exceeding 41 million shares. The stock traded in a range between $250.77 and $257.00 during the session.

Apple’s market capitalization remained around $3.71 trillion to $3.75 trillion, underscoring its status as one of the world’s most valuable companies despite shares sitting roughly 12% below the 52-week high near $288.62. The stock continues to trade well above its 52-week low of about $169.21, supported by strong brand loyalty and a diversified business model.

Analysts maintain a predominantly bullish outlook. The consensus 12-month price target hovers near $297 to $304, suggesting potential upside of 17% to 20% from current levels. Optimistic calls, including from Wedbush Securities, point as high as $350, with analysts highlighting 2026 as a pivotal year for Apple’s artificial intelligence ambitions.

Market Volatility Tied to Middle East Developments

Thursday’s trading reflected Wall Street’s heightened sensitivity to geopolitical headlines. The U.S.-Iran conflict, now in its fourth week, has driven oil prices sharply higher, with Brent crude climbing toward or above $104-$108 per barrel in recent sessions amid fears of prolonged supply disruptions through the Strait of Hormuz. U.S. West Texas Intermediate crude also rose significantly.

Conflicting signals from Washington and Tehran have fueled uncertainty. Reports of a U.S. 15-point proposal for de-escalation met with Iranian denials or cautious reviews, dimming hopes for a swift resolution. Higher energy costs risk acting as a drag on consumer spending and corporate margins, potentially delaying Federal Reserve rate cuts and pressuring growth-sensitive sectors like technology.

Apple’s modest advance came even as high-valuation tech peers faced steeper declines. The company’s massive cash reserves, recurring services revenue and premium product positioning appeared to offer some buffer against the day’s macro headwinds.

Supply Chain Diversification Gains Momentum

Apple has accelerated efforts to reduce reliance on China for manufacturing. The company now assembles approximately 25% of its iPhones in India, producing around 55 million units there in 2025 — a 53% increase from the previous year. This shift helps mitigate risks from tariffs and geopolitical tensions.

Plans call for India to produce the majority — or potentially most — of iPhones sold in the United States by the end of 2026. This would require roughly doubling output in the country and represents a major step in Apple’s long-term supply chain strategy. The move comes as the company navigates potential trade policy changes and seeks greater geographic resilience.

Apple has also expanded its roster of U.S.-based suppliers and invested in domestic component production, further diversifying its global footprint while maintaining focus on quality and innovation.

AI Initiatives and Siri Overhaul in the Spotlight

Investors continue to eye Apple’s progress in artificial intelligence. The company is working on a significantly enhanced version of its Siri voice assistant, with expectations that a major upgrade could feature prominently at WWDC 2026 alongside iOS 27 and macOS 27 releases. Internal testing challenges have reportedly pushed some advanced capabilities beyond an earlier March target, with features potentially rolling out in phases through iOS 26.5 or later in the year.

Apple has explored partnerships, including potential integration of third-party models such as Google’s Gemini, to bolster Siri’s capabilities. While the company has adopted a more measured approach to generative AI spending compared with some rivals, executives and analysts believe these enhancements could drive meaningful growth as Apple Intelligence features expand across the ecosystem.

Upcoming software updates are expected to bring deeper on-device intelligence, better context awareness and improved handling of complex user requests. These developments could help Apple close perceived gaps with competitors in the rapidly evolving AI landscape.

iPhone Demand and Services Growth Provide Foundation

The iPhone remains Apple’s core revenue driver, supported by loyal customers, trade-in programs and enterprise adoption. Steady demand has persisted despite macroeconomic pressures, though sustained high oil prices could eventually weigh on global consumer spending for premium devices.

Services — including the App Store, Apple Music, iCloud, AppleCare and emerging advertising initiatives — continue to deliver high-margin, recurring revenue that provides stability. Plans to introduce ads in Apple Maps in the U.S. and Canada this summer represent one avenue for further expansion.

Valuation remains a point of discussion, with shares trading around 32 times trailing earnings. Bulls argue that Apple’s ecosystem strength, innovation pipeline and capital return programs (dividends and buybacks) justify the multiple, while bears point to risks from trade policies, competition and any prolonged economic slowdown.

Analyst Views and Technical Considerations

Wall Street’s consensus rating for Apple is Moderate Buy to Buy, with dozens of analysts covering the stock. Price targets range from conservative levels near $205-$248 to bullish forecasts up to $350. Many see the current consolidation as a potential entry point for long-term investors betting on AI-driven growth and supply chain improvements.

Technically, support levels are watched near $250, with resistance around $257-$260 in the near term. A decisive move above recent highs could signal renewed momentum, while broader market weakness tied to energy prices or conflict escalation might test lower supports.

For individual investors, Apple often serves as a core holding in diversified portfolios due to its track record of adaptation and shareholder returns. However, near-term volatility linked to oil markets and geopolitics warrants caution and disciplined risk management.

Broader Context and Outlook

Apple’s relative resilience Thursday highlights the differing dynamics within the technology sector. While some names tied closely to cyclical spending or speculative AI plays faced heavier pressure, Apple’s blend of hardware, services and brand power has helped it weather uncertainty.

Looking ahead, investors will monitor any fresh developments from the Middle East, movements in oil futures and upcoming U.S. economic data on inflation and employment. Apple’s next earnings report will be scrutinized for commentary on demand trends, supply chain progress and AI monetization.

Longer term, many strategists view 2026 as potentially transformative for Apple as it rolls out more advanced AI features and completes key manufacturing shifts. Yet the path may include continued swings as external risks evolve.

Founded in 1976, Apple has grown from a garage startup into a global leader in consumer electronics and services. Its stock, while not immune to macroeconomic shocks, reflects ongoing confidence in management’s ability to innovate and adapt amid challenges.

As markets open Friday, attention will remain on oil prices, diplomatic signals regarding Iran and how these factors influence broader risk sentiment. For Apple specifically, execution on diversification, software advancements and sustained iPhone strength will likely shape its trajectory through the remainder of 2026 and beyond.

NEW YORK — As the global package delivery market continues its rapid expansion in 2026, investors are weighing UPS against FedEx to determine which logistics giant offers the stronger long-term opportunity. Both companies have posted solid year-to-date gains, but differing business models, cost structures and growth strategies are creating a clear divergence that could shape portfolio decisions for the remainder of the year and into 2027.

United Parcel Service Inc., the world’s largest package delivery company, has seen its shares rise about 14% so far this year, driven by resilient e-commerce volume, successful cost-cutting initiatives and steady progress in automation. FedEx Corp. has advanced roughly 11%, supported by strong international express growth and efficiency gains under its “FedEx 2.0” transformation plan. With both trading near multi-year highs, the choice between them hinges on an investor’s preference for scale and stability versus higher-margin international exposure.

UPS reported robust fiscal first-quarter 2026 results, with revenue climbing 6% to $24.8 billion and adjusted earnings per share beating estimates by 8%. The company’s ground network, which handles the majority of U.S. e-commerce packages, continues to benefit from diversified revenue streams including healthcare logistics and supply chain services. CEO Carol Tomé highlighted ongoing efficiency improvements, noting that automation investments have already reduced labor costs by more than $1 billion annually.

FedEx, meanwhile, posted first-quarter revenue of $22.1 billion, up 4%, with particularly strong performance in its international priority segment. The company’s focus on premium express services has delivered higher margins, though domestic ground volumes have faced pressure from intense competition. CEO Raj Subramaniam emphasized the success of network optimization efforts, which have improved on-time performance and reduced reliance on third-party capacity.

Analysts at firms like Goldman Sachs and JPMorgan have issued nuanced outlooks. Goldman Sachs maintains a Buy rating on UPS, citing its superior scale and diversified portfolio as advantages in a maturing e-commerce market. JPMorgan favors FedEx for its higher-margin international business and potential for margin expansion as cost savings materialize. Consensus price targets suggest modest upside for both, but UPS carries a slightly lower forward price-to-earnings multiple of around 18 times compared with FedEx’s 20 times.

Key Differences in Business Models

UPS operates the largest ground delivery network in the United States, giving it unmatched density and cost advantages on domestic routes. The company’s strategy emphasizes volume growth through e-commerce partnerships while expanding into higher-margin segments like healthcare and industrial logistics. Its massive scale also provides bargaining power with suppliers and labor unions, though recent contract negotiations have increased wage costs.

FedEx relies more heavily on its air express network, which commands premium pricing but is more sensitive to fuel costs and global economic conditions. The company has made significant strides in integrating its FedEx Express and FedEx Ground networks, reducing overlap and improving efficiency. International operations, particularly in Asia and Europe, represent a larger portion of FedEx’s business and offer higher growth potential as global trade recovers.

Both companies face common headwinds, including rising labor expenses, volatile fuel prices and intensifying competition from Amazon’s expanding logistics arm. Amazon now handles a growing share of its own deliveries, putting pressure on traditional carriers. Additionally, slowing e-commerce growth rates after the pandemic boom have forced both firms to focus on pricing discipline and operational efficiency.

Valuation and Risk Profiles

UPS currently trades at a more attractive valuation relative to expected earnings growth, making it appealing for value-oriented investors. The company’s consistent dividend increases and strong free cash flow generation provide a safety net during economic slowdowns. FedEx offers potentially higher returns if international trade accelerates, but its higher valuation leaves less margin for error if cost savings fall short of expectations.

Risks for UPS include labor contract renewals and potential union actions, while FedEx faces greater exposure to currency fluctuations and global supply chain disruptions. Both stocks have shown resilience in recent quarters, but analysts caution that near-term volatility could arise from quarterly volume reports and macroeconomic data.

Growth Drivers and Long-Term Outlook

The broader logistics sector is expected to benefit from continued e-commerce expansion, nearshoring trends and increased demand for time-sensitive deliveries. UPS is well-positioned to capture market share in domestic ground delivery, while FedEx’s strength in international express could drive faster revenue growth if global trade rebounds strongly.

Technological investments are playing a key role for both. UPS has rolled out advanced routing algorithms and electric vehicle fleets, aiming for carbon neutrality targets. FedEx has focused on data analytics and artificial intelligence to optimize flight schedules and package sorting. These innovations are expected to deliver meaningful cost savings and service improvements over the next several years.

Wall Street consensus points to mid-single-digit revenue growth for both companies through 2027, with UPS potentially benefiting from greater domestic stability and FedEx from higher-margin international upside. Dividend yields are comparable, around 2.8% for UPS and 2.5% for FedEx, making both attractive for income-focused investors.

Analyst Consensus and Investor Considerations

Most analysts recommend holding both stocks but see UPS as the slightly safer choice for conservative portfolios due to its scale and diversified revenue. FedEx appeals to those seeking higher growth potential and is often favored in growth-oriented accounts. For investors deciding between the two in 2026, the decision ultimately comes down to risk tolerance and view on the global economy.

Those bullish on U.S. consumer spending may lean toward UPS, while those expecting a strong rebound in international trade could prefer FedEx. Portfolio allocation matters too — many advisors suggest owning both for balanced exposure to the logistics sector rather than choosing one over the other.

The competitive landscape is evolving rapidly. Amazon’s continued investment in its own delivery network and the rise of regional carriers add pressure on traditional players. However, both UPS and FedEx have demonstrated adaptability, with strong balance sheets that provide flexibility for strategic acquisitions or share repurchases.

As 2026 progresses, quarterly earnings reports and guidance updates will be critical catalysts. Investors should monitor volume trends, margin performance and any new contract wins as key indicators of which company is gaining ground.

In summary, UPS currently edges out as the more balanced investment for most portfolios in 2026 due to its scale, valuation and domestic stability. FedEx remains a compelling choice for those comfortable with slightly higher risk in exchange for international growth potential. Both companies are fundamentally strong players in an essential industry, and patient investors in either are likely to benefit from long-term sector tailwinds.

The logistics sector’s importance to global commerce ensures both UPS and FedEx will remain relevant for years to come. For now, the choice between them reflects differing bets on domestic versus international growth and the relative value each offers at current prices.

Roberts Berzins has over a decade of experience in the financial management helping top-tier corporates shape their financial strategies and execute large-scale financings. He has also made significant efforts to institutionalize REIT framework in Latvia to boost the liquidity of pan-Baltic capital markets. Other policy-level work includes the development of national SOE financing guidelines and framework for channeling private capital into affordable housing stock. Roberts is a CFA Charterholder, ESG investing certificate holder, has had an internship in Chicago board of trade (albeit, being resident and living in Latvia), and is actively involved in “thought-leadership” activities to support the development of pan-Baltic capital markets.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

CUPERTINO, Calif. — Apple’s iPhone 18 Pro Max is shaping up to be one of the most significant upgrades in recent years, with leaks pointing to a substantially larger battery, a groundbreaking variable aperture camera system, under-display Face ID elements and a powerful new A20 Pro chip manufactured on a 2-nanometer process. The flagship device is expected to launch alongside the iPhone 18 Pro and possibly Apple’s first foldable iPhone in September 2026, according to multiple reliable reports circulating in early May.

While Apple has not commented on any upcoming products, supply chain analysts, leakers and industry publications have painted a consistent picture of meaningful improvements focused on battery life, photography versatility and subtle design refinements rather than a complete overhaul. The iPhone 18 Pro Max is rumored to maintain its 6.9-inch display size but could become slightly thicker to accommodate enhanced internals, making it one of the “chonkiest” Pro Max models in recent memory.

The most exciting rumor centers on the main rear camera. Multiple sources, including MacRumors and The Information, report that the 48-megapixel Fusion camera on both Pro models will feature a variable aperture mechanism. This would allow users to dynamically adjust depth of field and light intake — a first for iPhone — offering greater creative control similar to professional DSLR cameras. The feature is expected to be particularly beneficial for portrait photography and low-light performance.

Battery life is another major highlight. The iPhone 18 Pro Max is rumored to pack a 5,100 to 5,200 mAh cell, a noticeable increase over current models. Combined with more efficient LTPO+ display technology and the power-sipping 2nm A20 Pro chip, the device could deliver significantly better endurance, potentially addressing one of the most common complaints about previous Pro Max models. Some leaks suggest real-world usage could extend well beyond 10 hours of heavy screen time.

Design-wise, the iPhone 18 Pro Max is expected to closely resemble its predecessor with minor refinements. A smaller Dynamic Island is widely anticipated thanks to partial under-display Face ID components. The front camera may shift to the top-left corner, further reducing the notch area. Colors could include a striking new Dark Cherry option alongside Light Blue, Dark Gray and Silver. The titanium frame is likely to return with possible material tweaks for improved durability and feel.

Performance and Hardware Upgrades

The A20 Pro chipset, built on TSMC’s advanced 2-nanometer process, is expected to deliver substantial gains in both raw power and efficiency. Apple’s custom silicon has consistently led the industry, and the new chip should power advanced AI features, smoother multitasking and better thermal management. RAM is rumored to remain at 12GB, while storage options will likely start at 256GB and extend up to 2TB.

Display improvements include LTPO+ technology for better power efficiency at high refresh rates. Peak brightness could exceed 3,000 nits, making the screen even more usable outdoors. The Camera Control button may receive a simplified redesign based on user feedback from the previous generation.

Camera System Enhancements

Beyond the variable aperture main sensor, the iPhone 18 Pro Max is expected to retain a triple-lens setup with upgraded 48-megapixel ultrawide and telephoto lenses. Improved computational photography, enhanced Night mode and better video stabilization are also anticipated. These upgrades position the device as a serious tool for both casual photographers and content creators.

Release Timeline and Pricing

Apple is expected to announce the iPhone 18 Pro and Pro Max in September 2026, potentially alongside its first foldable iPhone. Standard iPhone 18 models may follow in spring 2027 as part of a split launch strategy. Pricing is likely to remain consistent with current Pro Max models, starting around $1,199, though higher storage tiers could push the top configuration well above $1,500.

The foldable device, possibly called iPhone Ultra, is generating significant excitement but is expected to carry a much higher price tag due to its complex hinge and dual-display technology.

Market Context and Competition

The iPhone 18 Pro Max arrives as Apple faces increasing competition from Android flagships offering innovative designs and aggressive pricing. Samsung’s foldables and Google’s Pixel series continue to push boundaries in AI and photography. Apple’s strategy appears focused on refinement and ecosystem integration rather than radical reinvention, maintaining its premium positioning.

Analysts predict strong demand for the new Pro models, particularly among users upgrading from older devices seeking better battery life and camera versatility. The larger battery and efficiency improvements could help Apple close the gap with competitors who have traditionally led in endurance.

What This Means for Consumers

For potential buyers, the iPhone 18 Pro Max rumors suggest a compelling upgrade focused on practical improvements rather than flashy gimmicks. Users frustrated with battery life or limited photographic control may find the new model particularly appealing. Those satisfied with their current Pro Max might wait for more substantial design changes rumored for future generations.

As always with Apple rumors, details could shift as development progresses. Official specifications will be revealed at Apple’s expected September event. Until then, the steady flow of leaks continues to build anticipation for what could be one of Apple’s most refined flagship devices yet.

The iPhone 18 Pro Max appears poised to deliver meaningful upgrades in the areas that matter most to power users — battery endurance, photographic flexibility and everyday performance. With its expected September 2026 launch still several months away, excitement continues to build around Apple’s next flagship.

Apple Is Quietly Building The Most Profitable AI Toll Booth

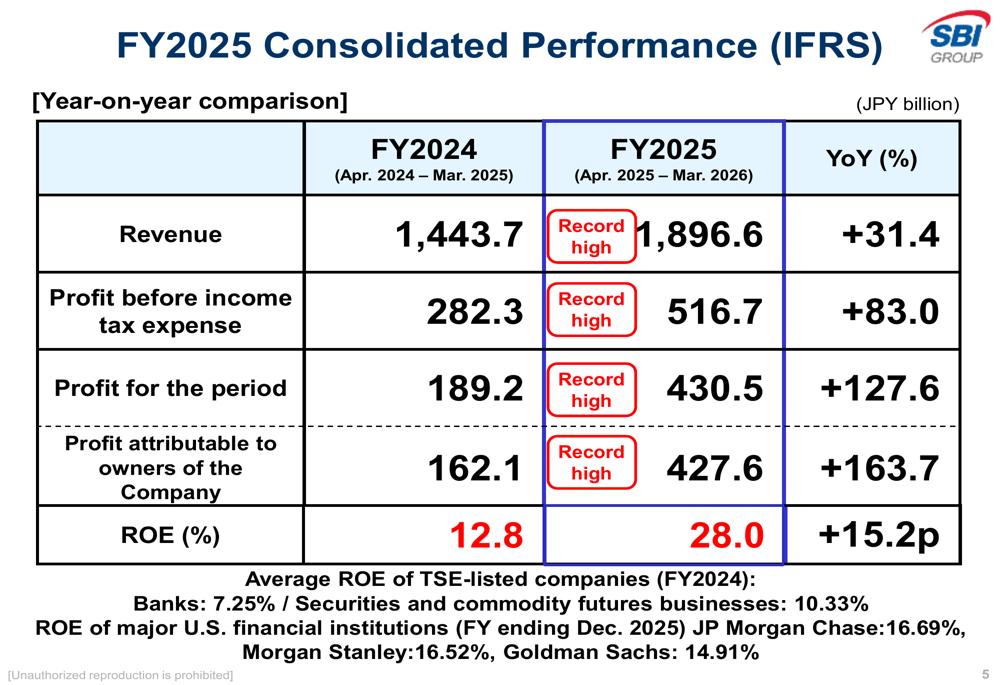

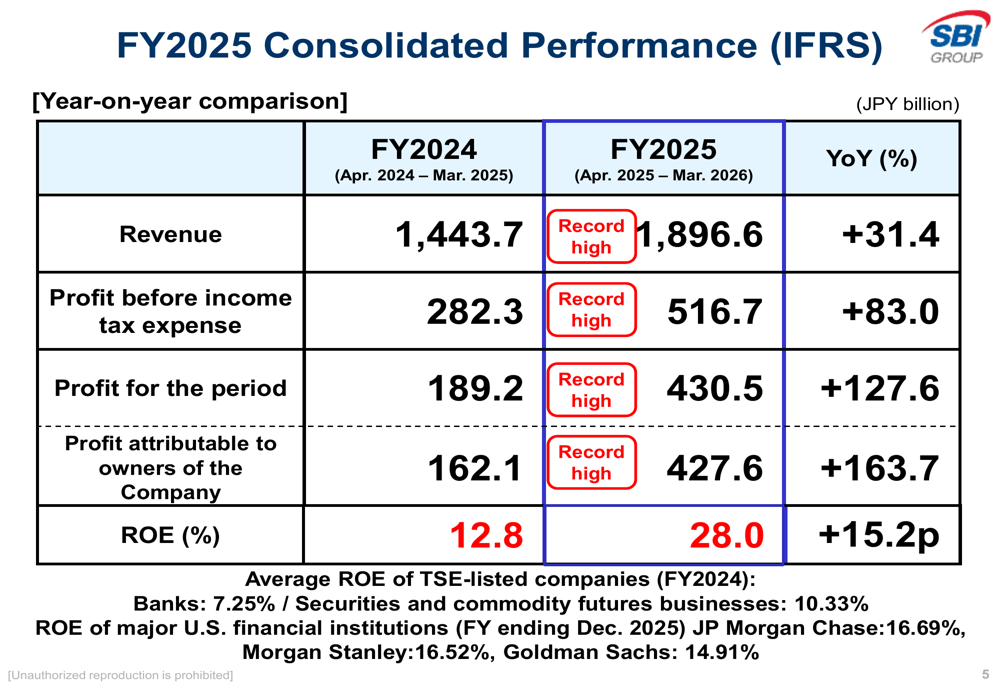

SBI Holdings FY2025 slides: record profit soars 164%, ROE hits 28%

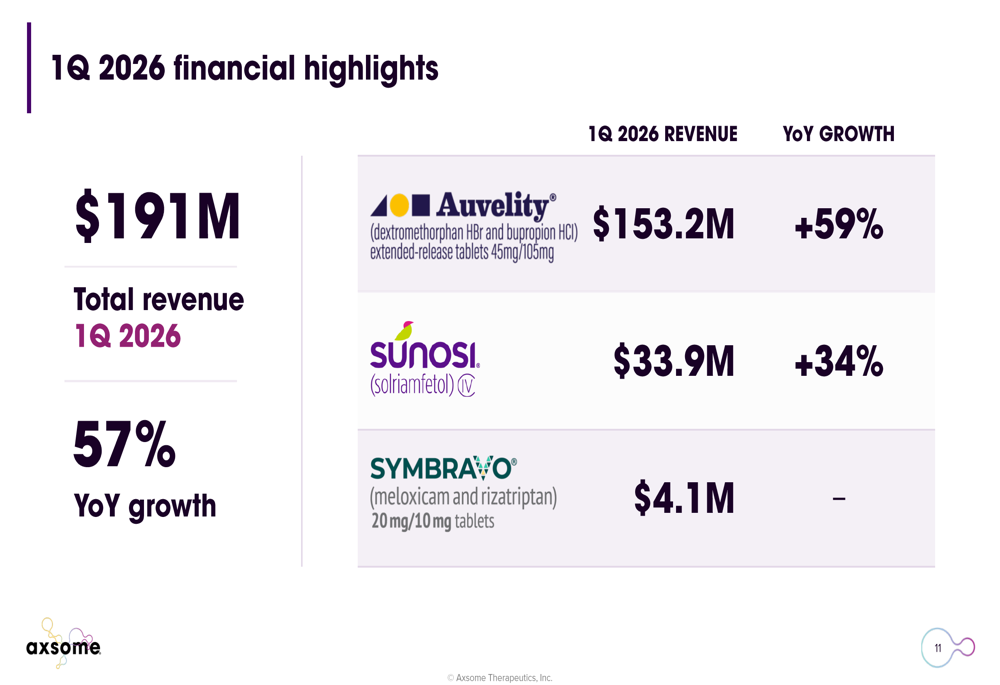

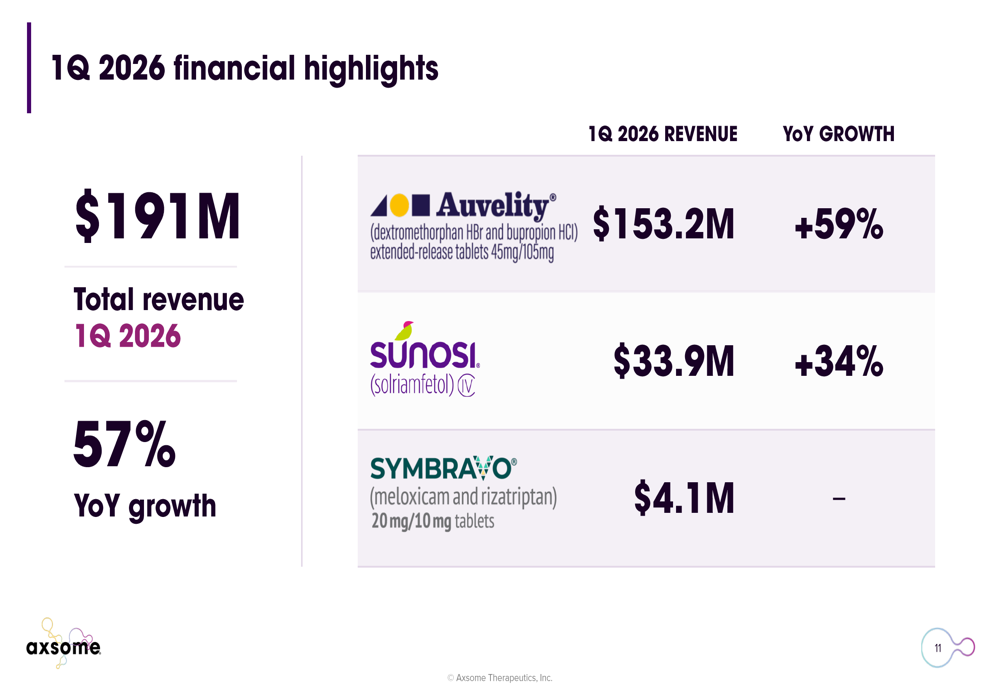

Axsome Q1 2026 slides: 57% revenue surge, $18B peak sales target

Earnings call transcript: Geberit Q1 2026 sees revenue beat, stock dips

TUCSON, Ariz. — Investigators in the Nancy Guthrie abduction case have obtained a significant DNA breakthrough that has narrowed the pool of potential suspects, Pima County Sheriff Chris Nanos announced Saturday, offering the most encouraging update yet as the search for the 84-year-old mother of NBC “Today” show co-anchor Savannah Guthrie entered its 110th day.

Forensic experts at the FBI laboratory in Quantico completed advanced genetic genealogy analysis on a rootless hair sample and partial glove DNA recovered from Guthrie’s Catalina Foothills home. The results have generated several strong investigative leads, including matches to distant relatives of individuals with prior connections to the Tucson area, sources familiar with the probe told local media.

“We are making real, measurable progress,” Nanos said during a brief update. “The genetic genealogy work has opened doors that simply weren’t available in the first weeks of this investigation. We are closer today than we have been at any point.” He declined to provide specifics, citing the active nature of the case, but confirmed that multiple persons of interest are now under closer scrutiny.

Nancy Guthrie disappeared from her secure residence on February 1, 2026. Security footage captured a masked individual near her door in broad daylight. Blood evidence, a disabled Ring camera, propped-open doors and clear signs of a struggle led authorities to classify the incident as an abduction. No ransom demand has ever been received, and no arrests have been announced despite an intensive multi-agency effort involving local police, the FBI and private investigators.

Savannah Guthrie has continued balancing public appeals for information with her anchoring duties on the “Today” show. In recent weeks she has worn yellow — the color of hope — during several broadcasts while expressing quiet gratitude for the public’s ongoing support. The family maintains a $1 million reward for information leading to Nancy’s safe return or the identification and arrest of those responsible.

New Leads Spark Renewed Hope

The genetic genealogy results represent the most tangible advancement since the early days of the case. Law enforcement has been cross-referencing partial DNA profiles against public genealogy databases and private family trees. While officials have not named any suspects, sources indicate that at least two individuals with potential ties to the Tucson metro area are now persons of interest.

The unrelated discovery of ancient human bones near the home several weeks ago briefly raised hopes before forensic analysis confirmed they were decades old. That episode, while disappointing, underscored the exhaustive nature of the search effort across Arizona’s desert terrain.

Criminal behavioral analysts have suggested the perpetrator may have had some degree of familiarity with the neighborhood or the victim. The brazen daytime abduction in an upscale gated community continues to puzzle investigators. Some experts lean toward a burglary gone wrong, while others have not ruled out a targeted act possibly linked to personal grievances.

Community and National Attention

Yellow ribbons remain tied to trees and lampposts throughout Catalina Foothills. Neighbors continue informal vigils and information-sharing through community groups. The case’s visibility, amplified by Savannah Guthrie’s national platform, has kept tips flowing into the dedicated hotline.

Elizabeth Smart, who was abducted as a teenager in 2002, has remained in contact with the Guthrie family. “I still believe Nancy could be found alive,” Smart said in a recent interview. “These cases can stretch on for a long time, but hope is a powerful force.”

The emotional toll on the Guthrie family is evident. Savannah briefly stepped away from the “Today” show earlier this month due to exhaustion but returned after a short break. She and her siblings continue advocating for Nancy while trying to maintain normalcy for the younger children in the extended family.

Investigation Challenges Persist

Despite the DNA progress, significant hurdles remain. Multiple ransom-style notes sent to media outlets have been evaluated as probable hoaxes. No credible proof of life has surfaced in more than 110 days, yet authorities continue operating under the assumption that Nancy may still be alive.

Coordination between local, state and federal agencies has improved after early tensions. FBI Director Kash Patel publicly criticized initial information sharing but now describes the joint effort as “productive and focused.” Hundreds of law enforcement personnel have contributed at various stages, with resources dedicated to surveillance review, extensive canvassing and tip-line management.

The vast desert landscape surrounding Tucson presents unique search challenges. Specialized teams using drones, cadaver dogs and ground-penetrating radar have covered hundreds of acres without success. Officials say they will not scale back efforts even as the case moves deeper into its fourth month.

Sheriff Nanos Under Pressure

Sheriff Chris Nanos, a Democrat elected in 2018 and re-elected in 2024, has faced quiet but growing political pressure as the high-profile case drags on. Some local critics have questioned resource allocation and communication strategies, though no formal calls for resignation have emerged. Nanos has repeatedly vowed that the investigation remains a top priority and that his department will not rest until answers are found.

What Comes Next

Authorities have renewed their public appeal for tips, particularly any information about vehicles or individuals acting suspiciously in the Catalina Foothills area in late January or early February. Forensic testing is expected to continue yielding results in the coming weeks, with additional genetic genealogy work planned.

For the Guthrie family, each new development brings a painful mix of renewed hope and prolonged uncertainty. Friends and colleagues have formed a quiet support network, with “Today” show personalities offering both public encouragement and private assistance.

The disappearance of Nancy Guthrie has highlighted vulnerabilities even in affluent, protected communities and the enduring power of hope amid uncertainty. Whether the case ultimately ends in a joyful reunion or provides answers through other means, it has already left a deep imprint on those following the story — a testament to one family’s resilience and a community’s determination to bring Nancy home.

As the investigation pushes past 110 days, the combination of traditional detective work and cutting-edge forensic science offers the best chance yet for resolution. Sheriff Nanos and his team continue working around the clock, supported by federal partners and the unwavering hope of a family that refuses to give up.

Michael Kramer is the founder of Mott Capital, and is a long-only investor who focuses on macro themes and studies trends and options activities to identify and assess entry and exit points for investments in his long-term focused thematic growth strategy. He is a former buy-side trader, analyst, and portfolio manager with 30 years of experience tracking market technicals, fundamentals, and options.Michael Kramer leads the investing group Reading the Markets, where he helps a devoted following of members to better understand what is driving trading and where the market is likely heading, both the short and long-term. Features of the investing group include: daily written commentary and videos analyzing the driving factors behind price action; general macro trend education to help members make well-informed decisions based on market conditions, interest rates, currency movements and how they all interact; chat for questions and community dialogue; and regular Zoom videos sessions to discuss current ideas and answer questions. The level of access RTM subscribers and the expertise of the source are unprecedented given that the subscription price is a fraction of similar technical coaching and mentoring services. Learn more.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

This report contains independent commentary to be used for informational and educational purposes only. Michael Kramer is a member and investment adviser representative with Mott Capital Management. Mr. Kramer is not affiliated with this company and does not serve on the board of any related company that issued this stock. All opinions and analyses presented by Michael Kramer in this analysis or market report are solely Michael Kramer’s views. Readers should not treat any opinion, viewpoint, or prediction expressed by Michael Kramer as a specific solicitation or recommendation to buy or sell a particular security or follow a particular strategy. Michael Kramer’s analyses are based upon information and independent research that he considers reliable, but neither Michael Kramer nor Mott Capital Management guarantees its completeness or accuracy, and it should not be relied upon as such. Michael Kramer is not under any obligation to update or correct any information presented in his analyses. Mr. Kramer’s statements, guidance, and opinions are subject to change without notice. Past performance is not indicative of future results. Neither Michael Kramer nor Mott Capital Management guarantees any specific outcome or profit. You should be aware of the real risk of loss in following any strategy or investment commentary presented in this analysis. Strategies or investments discussed may fluctuate in price or value. Investments or strategies mentioned in this analysis may not be suitable for you. This material does not consider your particular investment objectives, financial situation, or needs and is not intended as a recommendation appropriate for you. You must make an independent decision regarding investments or strategies in this analysis. Upon request, the advisor will provide a list of all recommendations made during the past twelve months. Before acting on information in this analysis, you should consider whether it is suitable for your circumstances and strongly consider seeking advice from your own financial or investment adviser to determine the suitability of any investment.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

One of repatriated French passengers from hantavirus-hit ship has symptoms, PM says

Yankees recall All-Star LHP Carlos Rodon

Whoop adds licensed clinician consultations as Google launches $99 Fitbit Air with Gemini AI health coach

BRAD JUST LEAKED IT LIVE ON AIR?!?!?

Manchester United reach agreement with Casemiro over contract clause amid transfer speculation

US brings back mandatory military draft registration

Steven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Crypto World2 days ago

Crypto World2 days agoHarrisX Poll Found 52% of Registered Voters Support the CLARITY Act

-

NewsBeat7 days ago

NewsBeat7 days agoChannel 5 – All Creatures Great and Small series 7 new post

-

Crypto World3 days ago

Crypto World3 days agoUpbit adds B3 Korean won pair as Base token gains Korea access

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Marianne Dress

-

Tech6 days ago

Tech6 days agoImage AI models now drive app growth, beating chatbot upgrades

-

NewsBeat3 days ago

NewsBeat3 days agoNCP car park operator enters administration putting 340 UK sites at risk of closure

-

Business1 day ago

Business1 day agoIgnore market noise, India’s long-term story intact, say D-Street bulls Ramesh Damani and Sunil Singhania

-

Politics1 day ago

Politics1 day agoPolitics Home Article | Starmer Enters The Danger Zone

-

Crypto World7 days ago

Crypto World7 days agoBlackRock Buys $284M In Bitcoin On May 1 As The Best Crypto To Invest In For 2026 Sits Below A Pending Binance Listing

-

Entertainment7 days ago

Entertainment7 days agoOlivia Wilde Reacts To Viral ‘Corpse’ Comparison

-

Sports7 days ago

Sports7 days agoInter Milan Win Serie A Title After Victory Over Parma

-

Sports7 days ago

Sports7 days agoLa Liga: Vinicius Jr scores twice as Real Madrid win to keep Barcelona waiting for title

-

Sports7 days ago

Sports7 days agoEvery word of Arne Slot’s heated rant after Manchester United win vs Liverpool

-

Crypto World5 days ago

Crypto World5 days agoUAE Free Zone Deploys Blockchain IDs to Verify Registered Firms

-

Entertainment7 days ago

Entertainment7 days agoOther Bennet Sister Love Triangle Cast: Ella Bruccoleri, Donal Finn

-

Sports7 days ago

Sports7 days agoJoel Embiid urges Sixers fans not to sell playoff tickets to Knicks fans

-

Sports6 days ago

Sports6 days ago2026 NHL playoff picks: Second-round predictions, series odds, Stanley Cup bracket

-

Entertainment7 days ago

Jennifer Lawrence’s Mary Jane Sneakers Are Spring’s It-Girl Shoe

-

Entertainment7 days ago

Entertainment7 days agoMoroccan Reacts To Nick Cannon’s Dating Rules For His Sister

-

Entertainment7 days ago

Kylie Jenner and Timothee Chalamet Hold Hands in NYC Outing

You must be logged in to post a comment Login