Business

Auxier Spring 2026 Market Commentary (Mutual Fund:AUXFX)

Donny DBM/iStock via Getty Images

After a strong start in January the market corrected largely due to the Strait of Hormuz crisis. Technology was the quarter’s worst-performing S&P 500 sector, especially software-related companies which suffered from AI disruption fears, excessive stock-based compensation and high valuations. Adding to that were monetization concerns over a sizable increase in “hyperscaler” capital expenditures in excess of $660 billion. The conflict in Iran and resulting Strait of Hormuz shutdown effectively halted shipping of 20.5-21 million barrels per day of crude oil and refined products that pass through what is one of the world’s most critical commodity corridors. This boosted energy, the best performing sector. Value outperformed growth with the Russell 1000 Value Index advancing 2.10% compared to a decline of 9.78% for the Russell 1000 Growth Index.

Defense Spending on the Rise

Geopolitical uncertainties over the last several years have brought about steadily increasing defense budgets, particularly in the United States which saw an increase from $715 billion in 2020 to just under $850 billion in 2025. For the first time ever, the 2026 budget exceeds $1 trillion. These increases have been driven by events like the Russia-Ukraine conflict as well as the war in Israel. Most recently, the US proposed a $1.5 trillion defense budget for 2027, citing factors like increasing global threats and the need for more domestic defense infrastructure. Lockheed Martin (LMT), Northrop Grumman (NOC) and RTX (RTX) stand to be among the largest beneficiaries of rising defense budgets, as all three are prime contractors for the US’s proposed $185 billion “Golden Dome” nationwide missile defense system. General Dynamics (GD), meanwhile, serves as the prime contractor for the nation’s $65.8 billion naval modernization effort. Boeing (BA) should see consistent revenue following their award of the F-47 next-generation aircraft contract, which is particularly attractive as aircraft programs typically run for decades. The previous generation F-35 first delivered in 2011 is still in production. Outside of traditional defense companies, we also see some tech names as beneficiaries of higher military spending with Nvidia (NVDA), Intel (INTC) and Qualcomm (QCOM) providing processing and compute for current and future autonomous vehicle and drone programs.

Growing Risk in Private Equity and Private Capital

The private equity and credit markets have exploded in growth over the last decade and are among the fastest-growing alternative asset classes. S&P Global estimated that private market assets under management totaled $15 trillion in 2024, up from $10.89 trillion in 2022. They project that those markets could reach more than $18 trillion by 2027. Private equity investments account for over half of the market. This lightly regulated industry is now facing headwinds. Payment-in-Kind loans have flourished as borrowers struggle to meet cash interest payments. Private equity funds are unable to exit their mid-market companies and investors are questioning valuation parameters. The opaque nature of these funds has further damaged investor confidence.

AI Disruption Fears Hit Software Companies Hard

The Software as a Service (SaaS) industry was one of the hardest hit areas of the market during the first quarter as investors have increasingly become uncertain over AI’s potential for disruption that could commoditize the industry and compress profit margins. Forbes reported that the software sector’s price-to-earnings ratio fell to 20 times during the first quarter compared to around 35 at the end of 2025, the lowest level since 2014. Companies like Intuit (INTU), Adobe (ADBE), Salesforce (CRM) and FICO (FICO) saw their shares fall 30%-37% during the first quarter despite reporting strong earnings. Investors fear that AI agents could replace much of the work currently performed by software companies for a fraction of the cost. Intuit has been working to counter the fears by heavily investing in their AI agent platform, bringing it to all their existing products. Adobe has been doing the same and both companies have seen strong support for AI features with around 90% of users taking advantage of the new capabilities. On the commodity risk side, these companies possess an advantage over popular general purpose AI models as they have access to specialized proprietary data they can use to train their own models. Adobe owns hundreds of licensed images they use for training and provides protection from litigation. Intuit instills confidence that taxes and business operations will comply with laws and regulations. AI models training only on public general data have a history of hallucinating false information and presenting it as fact which could be incredibly costly when dealing with important financial information. Proprietary data and the promise of security is something that we see as an advantage for long-standing SaaS companies that could help them better compete with growing AI players. It is amazing to see the P/E compression of these stocks since Covid. Fiserv (FI)—an unglamorous back-office processor for banks—was valued at over 100x earnings four years ago and now trades at just 7x, despite delivering 39 consecutive years of double-digit earnings-per-share growth.

Contributors

Bank of New York Mellon (BK) reached all-time highs following their first quarter earnings report of a 42% increase in year-over-year earnings per share along with an 18% increase in interest income resulting from higher yields. Assets under management grew 12% to a record $59.4 trillion. AI initiatives have been paying off as AI agents led to 20% faster client onboarding and 80% faster settlement inquiry investigation; agents are now writing 40% of all code. They returned $1.4 billion through repurchases and dividends and authorized a new $10 billion share repurchase program. CEO Robin Vince has done an exceptional job since taking over four years ago. Major US banks as a whole are aggressively retiring stock in 2026 due to recent deregulation, with a record $33 billion bought back in the first quarter alone—up 35% from the prior year quarter. This is the type of “double play” return we seek; an undervalued, vital, dull business with inspired management improving operating results leading to a sixfold return on our investment.

Industrials were the best performing sector during the quarter relative to the overall Fund, due in part from strong reshoring thanks to low domestic natural gas prices, legislation like the CHIPS and Inflation Reduction Acts as well as geopolitical risks that incentivize companies to return manufacturing to the US. Last year’s massive increase in hyperscaler capital expenditures continues, projected to be over $650 billion this year and may account for up to half of US GDP growth. Strong performers in the Fund included Gates (GTES), Caterpillar (CAT), Corning (GLW), and FedEx (FDX). Corning has seen strong demand for their optical connectivity products used in AI-focused data centers. Corning CEO Wendell Weeks is impressive in his ability to execute.

Defense and aerospace companies Boeing, Parker-Hannifin (PH), General Dynamics and RTX have reaped the benefits of a massive increase in global defense spending in response to rising conflicts.

Skilled labor educators Lincoln Educational (LINC) and Universal Technical Institute (UTI) have reported strong growth in student starts as demand for trades continues to rise. The expansion of data centers has led to high demand for electricians, HVAC technicians, welders and CNC machining engineers. AI automation is expected to impact many professional industries, driving interest in trades that are viewed as more resistant to disruption. Reshoring trends in the US specifically in the semiconductor and defense industries are also contributing to strong student starts.

Energy refiners Valero (VLO) and Phillips 66 (PSX) outperformed with diesel and Jet A fuel prices soaring. The crack spread hit a record $88.25 per barrel of oil in March. Chevron (CVX) has been a major beneficiary of years of diligent investments in oil and gas production.

Detractors

UnitedHealth (UNH) has been a major laggard for the past quarter and year. However, since CEO Stephen Hemsley’s return last May operating performance has been improving. We made over a fivefold return under his previous tenure from 2006-2017 and are confident that he can navigate a successful turnaround going forward. The recent medical cost ratio (MCR) of 83.9% is the lowest in two years and combined with a 2.48% CMS rate increase this spring has been a big boost. The lower amount spent on patient medical claims follows the company’s late 2025 shift to focus on higher margin patients over aggressive membership growth. Total membership has fallen by about 700,000 since the end of 2025. Management cited their higher margins as the reason for raising their full year adjusted earnings per share guidance to over $18.25, up from their previous guidance of $17.75 in January and consensus estimates of $17.86. Going forward, management also announced at least $1.5 billion in spending on artificial intelligence technology in 2026. This technology will be focused on areas like helping members understand their coverage and automating some administrative tasks and claims processing.

Software-related stocks in the portfolio have been hit hard due to the threat of margin compression from artificial intelligence. Microsoft (MSFT)’s 21.9% drop in the quarter was the worst decline since the 2008 financial crisis. They are spending $190 billion on AI-related capital expenditures in 2026 yet their AI Copilot product has failed to scale, with less than 15 million total paid seats. Google Gemini has successfully integrated their AI and captured the largest share of casual AI users with 2 billion people interacting with “Gemini-powered AI overviews” in Google Search every month. Microsoft has a large installed base with Fortune 500 companies. They have over $88 billion in cash on the balance sheet which is a huge competitive advantage. It is hard to bet against CEO Satya Nadella who took over in February 2014 and has a great record with the stock up over elevenfold.

First Quarter 2026 Performance Update

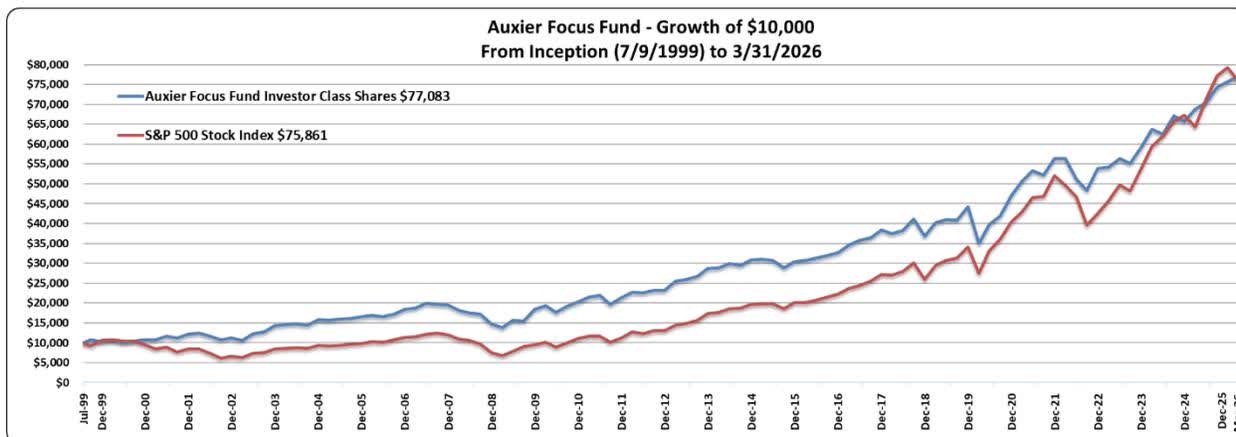

Auxier Focus Fund’s Investor Class gained 1.73% in the first quarter of 2026 with stocks up 2.00%. For the same period the S&P 500 cap-weighted index declined 4.33% and the equal weight returned 0.67%. The Russell 1000 Value was up 2.10%. For the quarter, fixed income investments as measured by the S&P US Aggregate Bond Index returned 0.04% and the longer-dated ICE US Treasury 20+ Year Index was up 0.11%. Stocks in the Fund comprised 92% of the portfolio. The breakdown was 82.5% domestic and 9.5% foreign, with 8.0% in short-term debt instruments. A hypothetical $10,000 investment in the Fund from inception on July 9, 1999 to March 31, 2026 is now worth $77,083 vs $75,861 for the S&P 500 and $65,542.76 for the Russell 1000 Value Index. During the same period, equities in the Fund (entire portfolio, not share class specific) have had a gross cumulative return of 1,323.34% vs 658.61% for the S&P. The Fund had an average exposure to the market of 82% over the entire period. Our results are unleveraged.

In Closing

We continue to seek businesses and managements displaying a strong culture with a heart and soul. Great leadership combined with enduring business models purchased in periods of fear and uncertainty have generated most of our returns over the past three decades. We have had good luck

with gritty founder CEOs who love their business. There is however a shortage of great operators. The key is to identify these managers and businesses ahead of time and do vigorous daily research to determine the sustainable earnings power of each entity. While we are aggressively monitoring the risks of a continued Strait of Hormuz shutdown, we remain mindful that many opportunities can be missed by focusing too much on macro headlines and not enough on micro details of improving operating fundamentals with exceptional leaders. Program trading dominates the investment landscape, but we firmly believe that investing is still the craft of the specific and knowing what you own is crucial to mitigating risk and improving investment odds.

Finally, during this time of global turmoil Warren Buffett said it best: “What we learn from history is that people do not learn from history. You can count on fear, greed and folly to be ever present in the marketplace. Their sequence is unpredictable; their duration is unpredictable; and their effects are unpredictable. But their presence is certain. ” Emotional and psychological responses to money often lead to substantial misappraisals in auction markets, creating new opportunities.

We appreciate your trust.

Jeff Auxier

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

St John of God Health Care’s new private hospital in Midland has reached practical completion, paving the way for the state government to take over St John’s existing private hospital.

Private port proponent Crestlink has struck a deal to buy the Koolan Island iron ore mine for $20.2 million from MGX Resources.

Uber sues New York City over ’reckless’ driver protection law

STEW: Deep Discount Gets Deeper (Rating Upgrade)

Peter Kyle’s comments come as the government sets out how it would back British technology companies.

Operator

Good day, and welcome to the Aethlon Medical Fiscal Year-end March 31, 2026, Financial Results and Corporate Update Conference Call. [Operator Instructions]

Please note this event is being recorded. I would now like to turn the conference over to Jim Frakes, CEO and CFO of Aethlon Medical. Please go ahead.

James Frakes

CEO, CFO, Chief Accounting Officer, Secretary & Director

Thank you, operator, and good afternoon, everyone. Welcome to Aethlon Medical’s Fiscal Year-end March 31, 2026, Earnings Conference Call. My name is Jim Frakes, and I’m the Chief Executive Officer and Chief Financial Officer of Aethlon Medical. At 4:15 p.m. Eastern Time today, Aethlon Medical released financial results for its fiscal year ended March 31, 2026. If you have not seen or received Aethlon Medical’s earnings release, please visit the Investors page at www.aethlonmedical.com to view it.

Following this introduction and the reading of the company’s forward-looking statement disclaimer, Dr. Steven LaRosa, our Chief Medical Officer, and I will provide an overview of Aethlon’s strategy and recent developments. I will then make some brief remarks on Aethlon’s financials. We will then open up the call for the Q&A session.

Before we start the business portion of the call, please note that the news release today and this call contain forward-looking statements within the meaning of the Securities Act of 1933, as amended, and the Securities Exchange Act of 1934 as amended. The company cautions you that any statement that is not a statement of

Check out what’s clicking on FoxBusiness.com.

Soccer fans hoping to watch the World Cup in person may need a housing-sized budget.

The tournament kicks off Thursday in Mexico City, launching a six-week event expected to draw between 5 million and 6 million fans across 16 North American host cities. But for many U.S. fans, getting inside the stadium has become a major financial hurdle, according to Realtor.com.

In five of the 11 U.S. host cities, the cheapest available World Cup tickets for late-stage tournament matches cost more than the average monthly mortgage payment in that market, Realtor.com reported, citing real estate research firm PropertyShark.

A general view outside MetLife Stadium on June 9, 2026, in East Rutherford, New Jersey. (Catherine Ivill – AMA/Getty Images)

That means fans in Miami, Dallas, Atlanta, Kansas City and the New York area could spend the equivalent of a mortgage payment — or more — for a single seat. The figure does not include airfare, hotel stays, food, parking or merchandise.

The steepest prices are for the July 19 final at MetLife Stadium in East Rutherford, New Jersey. The least expensive seats are listed at $7,256, far above New York’s average monthly mortgage payment of $4,096 and average rent of $4,872, according to Realtor.com.

In Dallas, the cheapest tickets for the July 14 semifinal are listed at $2,391, slightly above the city’s average mortgage payment of $2,351. In Atlanta, the lowest-priced semifinal tickets are $2,208, above the average mortgage payment of $2,149, the outlet reported.

10 HOTTEST RENTAL HOUSING MARKETS IN THE US THIS SUMMER

A general view of FIFA World Cup 2026 signage at Kansas City Stadium on June 8, 2026, in Kansas City, Missouri. (Jay Biggerstaff/Getty Images / Getty Images)

Kansas City’s cheapest seats for a July 11 match are $1,567, compared with an average mortgage payment of $1,477. In Miami, the lowest-priced tickets for Colombia versus Portugal on June 27 are $2,700, nearly matching the city’s average mortgage payment and rent, according to Realtor.com.

Some consumers have already been priced out. A LiveSportsonTV survey of 1,008 U.S. soccer fans found that 52% had given up on buying World Cup tickets because of high prices.

“We’re seeing unprecedented prices for events like the World Cup because of supply and demand, to put it simply,” Mark Sanaiha of Macallan Capital said in a statement. “For years, the experience economy has outpaced wage growth, and younger generations aren’t planning to change that trajectory.”

AMERICANS OPTIMISTIC ABOUT INNOVATION ADDRESSING MAJOR CHALLENGES, SURVEY FINDS

A detailed view of a FIFA World Cup 2026 sign inside Dallas Stadium on April 13, 2026, in Arlington, Texas. (Stacy Revere/Getty Images / Getty Images)

The pricing has also drawn scrutiny from state officials. Attorneys general in Texas, New York, New Jersey and California have launched probes into World Cup ticket pricing and packaging policies, Realtor.com reported.

GET FOX BUSINESS ON THE GO BY CLICKING HERE

“Being honest about ticket sales is not complicated,” New Jersey Attorney General Jennifer Davenport said in a statement. “But FIFA has turned buying a ticket to the World Cup into a gauntlet of confusion, fake scarcity, and impossibly high prices — all at the expense of consumers and hardworking New Jerseyans.”

Consumer Price Index: Inflation At 4.2% In May

US Justice Department subpoenas major banks over alleged ’debanking,’ source says

Thailand is navigating a complex mix of economic pressures, diplomatic tensions, trade disputes, and emerging opportunities across multiple sectors. From regional border conflicts to financial market shifts and digital transformation, the country remains a focal point of activity in Southeast Asia.

Trade Disputes and Economic Pressures

Shrimp Industry Faces Crisis

One of the most pressing economic issues involves Thailand’s seafood sector. Malaysia has imposed a ban on Thai shrimp imports, dealing a significant blow to what was once the world’s largest shrimp industry. Thailand is preparing to challenge the ban through both the World Trade Organization (WTO) and ASEAN frameworks, signaling a deepening trade rift between the two neighbors. The dispute has escalated tensions between Bangkok and Kuala Lumpur, raising broader questions about regional trade relations.

Simultaneously, Thailand is accelerating efforts to finalize a free trade agreement with the European Union, partly to reduce its dependence on US markets amid ongoing tariff uncertainties. Multiple sources confirm this push is gaining momentum, with Thailand viewing the EU deal as a strategic hedge against external economic shocks.

Financial Markets Under Pressure

Thai financial markets are showing signs of strain. Capital is fleeing Thai stocks as the baht continues to decline, reflecting investor concern about the country’s economic trajectory. However, the Bank of Thailand has indicated low risk of a currency crisis, citing robust foreign reserves. Supporting this cautious optimism, Moody’s has upgraded Thailand’s economic outlook to “Stable,” acknowledging improving economic momentum. The JSCIB has also raised its GDP forecast to between 1.6% and 2.0%, offering some positive signals amid broader uncertainty.

Thailand’s automotive sector is also struggling, with car production falling to its lowest level in five years in April, according to Reuters.

Regional Security and Diplomatic Relations

Cambodia-Thailand Border Tensions

Regional security remains fragile. Cambodia has deployed Chinese-built tanks near the Thai border, prompting Thailand’s National Security Council to monitor the situation closely. Former Cambodian Prime Minister Hun Sen has publicly acknowledged that the recent conflict with Thailand was “my fault,” a rare admission that may open the door for diplomatic progress.

Both nations are exploring frameworks for lasting peace, with analysts suggesting UNCLOS-based mechanisms could help rebuild trust and resolve maritime boundary disputes. Thailand has confirmed it will participate in UN-backed conciliation on the maritime dispute, a step seen as constructive by regional observers.

Political Developments

On the domestic political front, former Prime Minister Thaksin Shinawatra is officially free but now faces a new multimillion-dollar tax battle. A Thai criminal court has acquitted a political leader of lèse-majesté charges, a notable development in the country’s ongoing tension between political freedom and royal defamation laws. Separately, a prominent pro-democracy activist, Tiwagorn Withiton, has been convicted and sentenced to prison, drawing criticism from human rights organizations.

Digital Economy and Financial Innovation

Virtual Banking and Crypto Regulation

Thailand is making significant strides in its digital economy ambitions. The country’s newly launched virtual banks are operating within a model that currently offers thin profit margins, raising questions about long-term viability. Meanwhile, Thailand’s crypto regulatory framework has entered a market-building phase, suggesting a more structured and growth-oriented approach to digital assets.

The country is also positioning digital ID infrastructure as the backbone of its emerging digital economy, with biometric systems being developed to streamline services and improve security. True IDC, backed by CP Group and GIP, has won a major award for digital infrastructure{rel=”nofollow” target=”_blank”}, with a large-scale data center project planned for the Eastern Economic Corridor.

Public Health and Environmental Concerns

Air Quality and Health Alerts

Thailand continues to grapple with serious air quality challenges. PM2.5 pollution is costing the country more than 5 billion baht, with structural policy failures prolonging the crisis, according to Kasikorn Research. New regulations are being introduced to mandate emissions monitoring at factories, representing a tightening of environmental standards.

On the health front, the US Embassy in Thailand has issued an Enhanced Ebola Screening Health Alert, and the WHO is working with Thailand to strengthen risk assessment frameworks for health emergencies.

Tourism, Culture, and Soft Power

Tourism Growth Initiatives

Thailand is actively promoting itself as a premier tourist destination. Initiatives include the Amazing Thailand Grand Sale, participation in tourism expos in Amsterdam, and the promotion of T-POP fandom tourism to attract culturally motivated travelers. The country is also exploring seaplane routes to boost tourism in the Andaman region and eyeing a mysterious eye-shaped island as a potential sustainable travel hotspot.

Vietnam and Thailand have jointly launched a “Two Countries, One Destination” initiative{rel=”nofollow” target=”_blank”} aimed at attracting regional and long-haul visitors through enhanced connectivity and shared tourism products.

Thailand also remains a notable destination for expatriates, with lifestyle publications highlighting its lower cost of living, relaxed pace of life, and family-friendly environment.

Conclusion

Thailand stands at a critical crossroads, balancing economic headwinds, regional security challenges, and ambitious digital and trade agendas. While pressures from currency depreciation, trade disputes, and political tensions persist, positive signals from Moody’s, FTA negotiations, and digital economy investments suggest the country is actively positioning itself for long-term resilience and growth.

Source : Google News – Search

Other People are Reading

Built completes Midland private hospital

Nightrush.com Responds to the AI Personalization Wave Reshaping iGaming And Raises the Bar

Use BetMGM bonus code CBSSPORTS to get $1,500 in bonus bets for Spurs-Knicks NBA Finals Game 4, MLB Wednesday

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Evereve – Corporette.com

-

Crypto World5 days ago

Crypto World5 days agoJensen Huang Approves Samsung, SK Hynix, and Micron for NVIDIA (NVDA) HBM4 Memory Supply

-

Crypto World3 days ago

Crypto World3 days agoAnatomy of the June crypto crash: Fed, Iran, Saylor

-

Entertainment4 days ago

Entertainment4 days agoThe Best Mystery Series of All Time Is Surging on Streaming 30 Years After It Ended

-

NewsBeat3 days ago

NewsBeat3 days agoAlexander Zverev wins the French Open to finally earn a 1st Grand Slam title

-

Tech5 days ago

Tech5 days agoSuspicious Polyfill login prompts pop up on Toshiba, Muji websites

-

Crypto World4 days ago

Crypto World4 days agoSenator Cynthia Lummis Calls CLARITY Act the Most Consequential Financial Legislation of This Generation

-

Tech6 days ago

Tech6 days agoMicrosoft launches MXC, an OS-level sandbox for AI agents, with OpenAI and Nvidia already on board

-

Tech4 days ago

Tech4 days agoMicrosoft unveils seven homegrown AI models in new bid for ‘long term self-sufficiency’

-

Business6 days ago

Business6 days ago(VIDEO) Justin Bieber Delivers Surprise Happy Birthday Serenade to Diners at Los Angeles Mexican Restaurant

-

Business4 days ago

Business4 days agoThe Pain Points Taking a Fragile Tech Rally Down a Notch

-

Crypto World3 days ago

Crypto World3 days agoEli Lilly (LLY) Stock Surges 4% Following Breakthrough Sleep Apnea Trial Results

-

Crypto World6 days ago

LBank Surpasses 25 Million Users Worldwide as AFA Partnership Continues to Drive Global Growth

-

Tech5 days ago

Tech5 days agoVon der Leyen’s AI envoy pick draws conflict-of-interest fire

-

Crypto World3 days ago

Crypto World3 days agoTrump’s AI Ownership Plan Could Benefit Anthropic at OpenAI’s Expense

-

Tech5 days ago

Tech5 days agoMeta steals a tactic from Tesla and builds data centers in tents

-

Sports1 day ago

Sports1 day agoBangladesh beat Australia after 20 years in ODIs, register only their second win over six-time world champions | Cricket News

-

Business3 days ago

Business3 days agoHigh Stakes for Wembanyama as New York Pushes for 3-0 Lead

-

Tech5 days ago

Tech5 days agoHackers now exploit SolarWinds Serv-U flaw to crash servers

-

Tech3 days ago

Tech3 days agoNotion restores access to Anthropic after service disruption

You must be logged in to post a comment Login