Business

Bauducco launches biggest US manufacturing facility

I’m an individual investor looking to grow my wealth over the long term. I’ve tried many different styles of investing over the last 25 years and have found that buying dividend growth stocks and reinvesting the dividends is one of the easiest ways to grow wealth over the long term. Over the years, I’ve owned stocks, options, ETFs, treasury notes, and mutual funds. I operate a blog, HarvestingDividends.com, that provides information on the S&P Dividend Aristocrats and other dividend growth stocks.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

I may take a position in any of the stocks mentioned in this article in the near future.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Why Roblox Had Its Worst Day Ever After Earnings

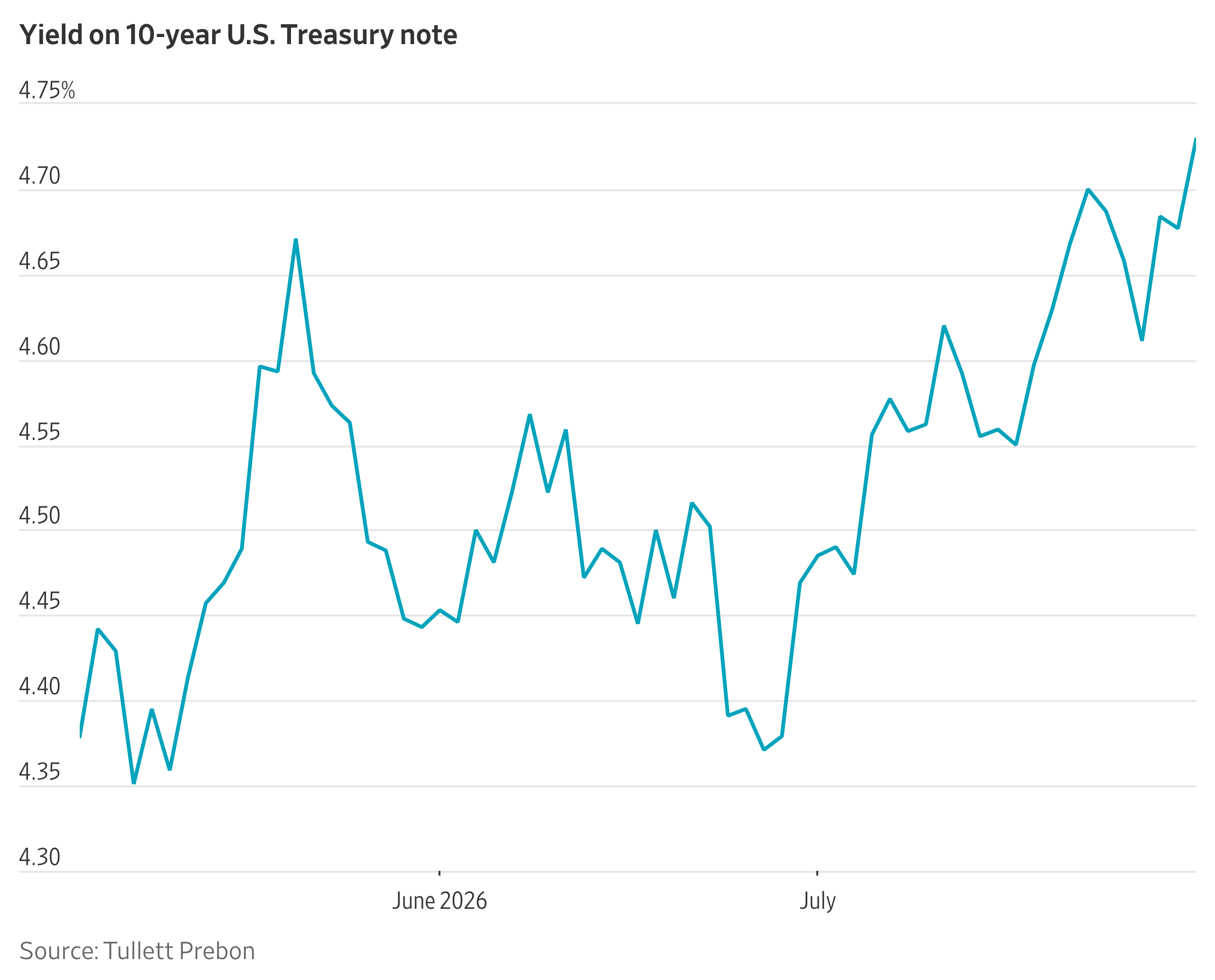

Treasury yields extended their recent gains Friday after three Federal Reserve officials explained why they cast dissenting votes in favor of raising interest rate this week.

Yields, which rise when bond prices fall, were also driven higher by economic data, including a stronger-than-expected reading on Chicago-area economic activity.

The yield on the 10-year U.S. Treasury note settled at 4.743%, according to Tradeweb, its highest closing level since January 2025. The 30-year yield closed at 5.274%, its highest since July 2007.

South Korean stocks surged on Friday, with the KOSPI index rising nearly 18%.

Despite the dramatic gains, the index was still down for the week and the month, a testament to how volatile Korean equities have been as of late.

Not counting today, the KOSPI has gained more than 10% in a single day in only six instances, according to Dow Jones Market Data. History shows that in the week following those six times, the S&P 500 traded lower two-thirds of the time, with an average decline of 1.6%.

1539 ET – Oil futures end July with hefty gains as the month saw renewed Iranian attacks on shipping in a dispute with the U.S. over control of the Strait of Hormuz. Concerns that a return to negotiations could quickly reduce risk premium and lead to oversupply have kept prices from reaching the lofty levels seen in March and April. “Traders are essentially betting on two very different geopolitical outcomes, and neither one is a safe assumption right now,” says Baron Lamarre, co-founder of Index Litro and former head of trading at Petronas. “My base view is we won’t end up with either a massive glut or a full-blown supply crisis by the end of the year,” he adds. “Instead, we’re in for a period of stubbornly tight, volatile conditions that will stick around longer than the optimists are hoping.” WTI settles up 1.3% at $84.67 a barrel for a 22% monthly gain. Brent for September delivery goes off the board at $90.12 a barrel, up 1.2% on the day and up 24% from the end of June.(anthony.harrup@wsj.com)

Oil Futures on Track for Big Monthly Gains

0951 ET – Oil futures turn higher in early U.S. trading and are on track for hefty gains for July, which saw the U.S.-Iran Memorandum of Understanding fall apart and Iran resume attacks on shipping in the Strait of Hormuz. “All things held equal, the market should go a lot higher and led by diesel and gasoline as refinery run rates arejust too low on a lack of crude,” Scott Shelton of TP ICAP says in a note. “The reality is that we are back to a very small amount of crude versus what is needed.” WTI is up 2.2% at $85.42 a barrel. September Brent is 1.5% higher at $90.36 ahead of today’s expiry, while the October contract gains 1.8% to $88.47.(anthony.harrup@wsj.com)

Copyright ©2026 Dow Jones & Company, Inc. All Rights Reserved. 87990cbe856818d5eddac44c7b1cdeb8

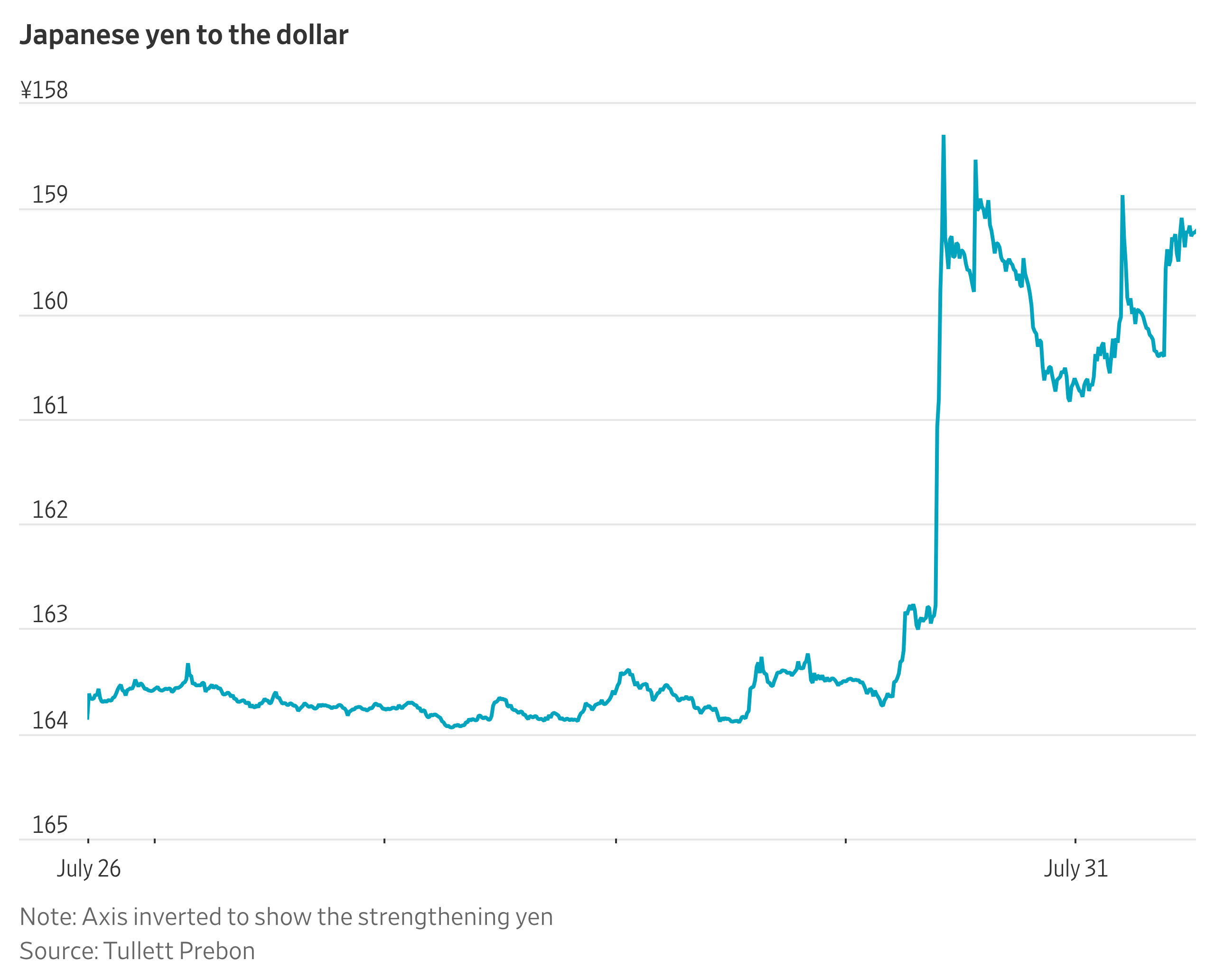

Currency traders broadly believe that the yen’s recent strengthening reflected yen purchases by Japanese authorities, as well as speculation of a possible U.S. intervention. The U.S. Treasury Department meanwhile has informed banks that it might make currency trades on Friday to support the Japanese yen and strengthen its exchange rate against the dollar, the Wall Street Journal reported today.

Global reforms emphasize control and decision-making authority over legal forms, shifting regional headquarters evaluation to governance, risk management, and value creation, impacted by tax rates and regulatory expectations.

Evolving Evaluation of Regional Headquarters

Global minimum tax, stricter substance enforcement, and geopolitical fragmentation have reshaped how regional headquarters are assessed. Singapore, Hong Kong, and Dubai now serve distinct roles, each aligned with different strategies for controlling operations and managing risks. They are no longer interchangeable hubs competing on similar benefits, but rather centers tailored to specific business models and regulatory environments.

Authority and Control Define a Headquarters

The focus has shifted from a legal entity’s structure to the authority it exercises within an organization. Regulators and counterparties increasingly scrutinize where key decisions—related to capital allocation, pricing, treasury, and risk management—are made. An entity exercising discretion in these areas is viewed as a true control center, influencing regulatory treatment and compliance risk instead of mere administrative support.

Governance and Control in Practice

Beyond reporting functions, the extent of authority impacts governance, documentation, and accountability standards. These factors determine a company’s regulatory exposure and defenses. While corporate tax rates like Singapore’s 17% and Hong Kong’s 16.5% are still relevant, emphasis now also rests on where value creation and control are evidenced within the organization.

Read the original article : Singapore vs Hong Kong vs Dubai: Regional HQ Trade-Offs for Investors

Other People are Reading

Are you tired? I’m tired. In addition to four Big Tech companies reporting earnings this past week, the calendar included results for second-quarter gross domestic product and the June personal consumption expenditures price index, along with the Federal Reserve’s interest-rate decision. Unscheduled, there was a meltdown of the artificial-intelligence trade, as highly leveraged bull positions were liquidated. The iShares Semiconductor exchange-traded fund was down 12% across three days, and one of the most successful AI investors—hedge fund Situational Awareness—saw margin calls and forced sales.

Private-equity firm KKR KKR is near a deal to take medical-device outsourcing company Integer Holdings ITGR private, according to people familiar with the matter.

The details

The deal, which could come as soon as next week, would value the Plano, Texas-based company at roughly $127 a share, the people said. There are no guarantees a deal will come together.

Copyright ©2026 Dow Jones & Company, Inc. All Rights Reserved. 87990cbe856818d5eddac44c7b1cdeb8

Exclusive-Japan to announce Tokyo, Washington took joint action on yen, sources say

Recovery Seeds Reportedly Breached for Coldcard Hardware Bitcoin Wallets, $75M Taken

Astonishing first-hand account of the family who SURVIVED Hiroshima… then went on This Is Your Life to meet the desperately repentant US airman who dropped the bomb that killed tens of thousands and changed the world

Altria Among 7 Dividend Kings To Announce Annual Dividend Increases In August

-

Sports6 days ago

Sports6 days agoCommonwealth Games boxing: Jadumani Singh seals dominant 5-0 win over Pakistan’s Sumama Rehman to enter quarter-finals | Commonwealth Games News

-

Business3 days ago

Business3 days agoWhy Trees Belong on the Risk Register

-

Fashion1 day ago

Fashion1 day agoWeekend Open Thread: Wit & Wisdom

-

Tech6 days ago

Tech6 days agoIntel is reversing course and bringing hyper-threading back to its server chips

-

Politics1 day ago

Politics1 day agoMeta enters AI-training agreement with far-right ‘propaganda rag’ Newsmax

-

Politics6 days ago

Politics6 days agoLuke Littler dismantles Gerwyn Price to retain title in Blackpool

-

Crypto World12 hours ago

Crypto World12 hours agoMicroStrategy Post-Earnings CLARITY Act Push Could Add New Catalyst for Its Stock

-

Politics5 days ago

Politics5 days agoThe Part of the Electric Transition Nobody Wants to Discuss

-

News Videos6 days ago

News Videos6 days agoBITCOIN JUST ENTERED THIS CRITICAL ZONE…

-

Entertainment4 days ago

Entertainment4 days ago‘Stargate’ Creator’s New Sci-Fi Series Returns for Season 3 Tomorrow

-

Business4 days ago

Business4 days agoMajor shareholder moves on Canyon

-

Crypto World7 days ago

Crypto World7 days agoXRP Ledger adds $2.6B as RWA inflows rank second

-

Politics7 days ago

Politics7 days agoSpain sweeps the board at 2026 World Cup with individual awards

-

News Videos3 days ago

News Videos3 days agoBitcoin Enters the 3rd Stage of the Bear Market

-

Crypto World21 hours ago

XRP Ledger v3.3.0 brings five institutional features

-

Crypto World4 days ago

Crypto World4 days agoKraken Enables Retail Access to Jersey Mike’s IPO via Tokenized Shares

-

Tech5 days ago

Tech5 days agoNew macOS Sequoia & Sonoma security updates for older Macs

-

News Videos4 days ago

News Videos4 days agoClaude: Build Financial Dashboards in Minutes (2026)

-

Sports2 days ago

Sports2 days agoSeema Kaliramna Wins Discus Throw Bronze, Takes India’s CWG Medals Tally To 17

-

Politics2 days ago

Politics2 days agoLuke Littler’s dominance sparks GOAT debate

You must be logged in to post a comment Login