Business

Business Daily – Taking Stock: A slower China and a durian glut

Available for over a year

Connecting the timezones this week are Will Bain in London, David Kuo in Singapore and Emily Peck in New York to unpack the week’s biggest business stories. China’s economy has recorded one of its weakest quarterly growth rates on record, raising fresh questions about the country’s outlook and the impact on the global economy. Plus, why prices for durian, the ‘king of fruits’, are tumbling across Asia. And New York’s move to target AI data centres.

Presenter: Will Bain

Producer: David Cann

You can email the team: businessdaily@bbc.co.uk

(Picture: People walk in the Lujiazui financial district, in Shanghai, China, 14 July 2022. Credit: ALEX PLAVEVSKI/EPA-EFE/REX/Shutterstock)

Rosendorff Diamonds has rebutted reports of its administration after the director of its former owner company was involved in a tax dispute in the state’s highest court.

Veradermics: VDPHL01 Looks Promising Enough On Paper

Shares in Jim Beyer-led Regis Resources fell on Friday, following the release of its FY27 annual production guidance.

CEO John Brase says complexity is a barrier to growth.

Concussions may have driven former West Coast Eagles defender Jeremy McGovern to an early retirement, but they didn’t stop him from diving headfirst into his charity.

Robert Nicholas | Ojo Images | Getty Images

A version of this article first appeared in CNBC’s Inside Wealth newsletter with Robert Frank, a weekly guide to the high-net-worth investor and consumer. Sign up to receive future editions, straight to your inbox.

A new estimate for the great wealth transfer has sparked a debate over how many trillions of dollars will pass from baby boomers to their heirs, and how it will be spent and invested.

Last week, Visa Business and Economic Insights released a new projection for the great wealth transfer, estimating that $36 trillion in baby boomer wealth will be passed down to Gen X and millennials over the next 20 years. The figure is a fraction of the widely cited estimate from Cerulli Associates, which says $105 trillion will pass from older generations to heirs by 2048.

The more than $60 trillion gap between the two studies has raised new questions about the size and impact of the great wealth transfer. Some say it will be the largest in history, dramatically reshaping wealth management, charity and the global wealth landscape. Others say its impact will be far more limited and simply marks a continuation of long-term inheritance trends.

The dueling Visa and Cerulli numbers highlight just how important the estimates have become for wealth managers and other companies overhauling their businesses to prepare for the next generation of wealth.

Visa, as a credit card payments company, focuses its study on the amount of inherited wealth that will be spent by everyday American consumers. Cerulli, being a financial research firm, focuses its study on the total wealth being transferred, including the outsized share of fortunes being passed down by the ultra wealthy. While Cerulli focuses on all wealth transfers in coming decades, Visa looked only at transfers from baby boomers.

“We wanted to go through and inspect how much money will actually be spent,” said Wayne Best, chief economist at Visa. “A lot of people think about the $93 trillion or $124 trillion and think ‘All that money’s going to be available for spending; this is going to be incredible.’ That’s why we went through the kind of the step-by-step process.”

Visa’s process started with the total amount of wealth held by today’s baby boomers, which it put at about $93 trillion. The report then stripped out liabilities, which includes mortgage debt, of $5 trillion and subtracted the wealth of the top 1%, estimated at $28 trillion.

Best said the top 1%, or those with wealth of at least $12 million, approach money very differently from the rest of consumers. They spend a much smaller share of their wealth and they tend to buy different things.

“They don’t spend like the rest of us,” Best said. “They’re buying yachts and airplanes. It’s all great for the economy, but that’s not what the average person really thinks of. So we removed that top 1%, to put this more on a normal or level playing field.”

Visa then stripped out the retirement spending of baby boomers, which could be larger than expected. Because boomers are living longer and spending their wealth more than past generations, Visa estimates their retirement spending at $16 trillion. It also subtracted $8 trillion for charity and taxes.

In addition, Visa focused its analysis exclusively on the wealth being transferred from baby boomers over the next 20 years. Cerulli looked at transfers from all generations by 2048, which includes members of the older Silent Generation, as well as the younger Generation Xers, who are now between 46 and 61 years old.

After taking out the debt, the fortunes of the top 1%, retirement spending, taxes and charity, Visa estimates that boomers will pass on only $36 trillion of their $93 trillion in wealth.

Of that $36 trillion, they estimate that $28 trillion will go to savings and investments and $8 trillion will go to spending. The $8 trillion will be spent mainly on cars, homes, travel and retail.

“You know, $8 trillion in spending is nothing to sneeze at,” Best said.” It’s a significant amount of money. And it’s additive. But we wanted to put that in perspective because when you start throwing around trillions of dollars it can get confusing very quickly.”

Cerulli, by contrast, sought to estimate the total wealth being passed down by all wealth groups, of all ages, by 2048.

Chayce Horton, Cerulli’s associate director of wealth management, said the biggest impact of the great wealth transfer will be in wealth management, rather than consumer companies.

Half of the more than $100 trillion being passed down will be from high net worth or ultra-wealthy families, he said. The first transfers in the coming years will be to spouses, mainly women. Cerulli estimates that $4 trillion will go to spouses before being passed down to children and other family members.

“When you look at that demographic, on average, spouses are a couple years younger, and those spouses live a couple years longer,” Horton said.

Cerulli said it does factor in retirement spending, taxes and debt. It also estimates that about $18 trillion of $124 trillion in total transferrable wealth will go to charity — leaving a total of $106 trillion going to heirs and spouses.

Gen Xers will be the first recipients, followed by millennials and then Gen Z. Gen X will inherit $14 trillion in the next 10 years, but millennials will eventually inherit the most, estimated at $46 trillion in the next 25 years.

Horton said it would be a mistake for the wealth management industry or any company serving wealthy clients to discount the impact of the great wealth transfer and the acceleration of inherited wealth. He said that one of every four wealth management clients currently come from inherited wealth — second only to business owners and founders, and ahead of corporate executives.

“The focus of our report when we do this analysis is understanding where the wealth is today, and where that wealth will be moving tomorrow so the wealth and asset management industry can adapt,” Horton said. “Something that we continue to emphasize as an important consideration for the wealth management industry, is making sure that they have those relationships across spousal lines, as well as intergenerational lines.”

Business

Microsoft Patches a Record 570 Security Flaws in July as AI Accelerates the Pace of Vulnerability Discovery

Microsoft Patches a Record 570 Security Flaws in July as AI Accelerates the Pace of Vulnerability Discovery

Microsoft released software updates Tuesday to fix at least 570 security vulnerabilities across Windows and its other products, nearly tripling the number of flaws the company patched in last month’s already record-setting release, as the company points to artificial intelligence as a major driver behind the surging patch counts.

Nearly 60 of the vulnerabilities addressed in this month’s release earned a “critical” severity rating, meaning attackers could potentially exploit them to seize remote control of a Windows device with little or no action required from the user. Microsoft also patched three zero-day vulnerabilities as part of the release, including two flaws that were already being actively exploited before the fix became available.

Two of the zero-day vulnerabilities allow attackers to elevate their level of access on a compromised Windows system, joining roughly 250 other elevation-of-privilege flaws fixed this month. Among them are CVE-2026-56155, a bug affecting Active Directory Federation Services, and CVE-2026-56164, a vulnerability in Microsoft SharePoint. Separately, Microsoft addressed CVE-2026-50661, a security feature bypass affecting Windows BitLocker that could allow an attacker with physical access to a device to gain entry to encrypted data. Microsoft said that flaw had been publicly detailed but that the company was not aware of any active exploitation of it at the time of the patch’s release.

Microsoft has attributed the dramatic rise in disclosed vulnerabilities directly to artificial intelligence tools now being used to hunt for security flaws across its massive codebase. In a blog post published July 9, Microsoft Executive Vice President Pavan Davuluri wrote that users would begin noticing “a higher volume of security updates included in each security release” as AI-assisted discovery methods continue to mature. Davuluri explained that advances in AI are changing how quickly vulnerabilities can be found, allowing researchers to identify more issues across larger volumes of code than was previously possible using traditional manual review methods.

Among the vulnerabilities drawing particular attention from security researchers is CVE-2026-48561, a remote code execution flaw in Microsoft Copilot carrying a severity score of 9.6 out of a possible 10 on the Common Vulnerability Scoring System. Jack Bicer, director of vulnerability research at the cybersecurity firm Action1, flagged the bug as especially serious, noting that Microsoft has said an attacker could exploit it simply by hosting a malicious website capable of automatically sending crafted prompts to Copilot when a victim visits the site using Microsoft Edge on an Android device.

The same forces accelerating Microsoft’s ability to find and patch vulnerabilities are also making it easier for attackers to develop working exploits for known flaws more quickly. Microsoft has traditionally used an internal measure called the “exploitability index” to estimate how likely it is that a given vulnerability will be reliably exploited by attackers. But Satnam Narang, a senior staff research engineer at the cybersecurity firm Tenable, argued that Microsoft’s current approach to rating exploitability has not kept pace with how quickly AI tools can now generate working exploits. Narang pointed to this month’s SharePoint zero-day as an example, noting that Microsoft had initially rated it as “less likely” to be exploited, even though the flaw had already been added to the Cybersecurity and Infrastructure Security Agency’s Known Exploited Vulnerabilities list by July 1.

Narang cited internal research from Anthropic’s red team as evidence of how quickly the landscape has shifted, noting that the company’s Mythos Preview model was able to independently produce proof-of-concept exploits for 13 of 14 known vulnerabilities that Microsoft had rated as unlikely to be exploited. “What this means is that our way of looking at Patch Tuesday has changed, because the exploitability index is centered around humans, not AI tools, and as these tools continue to improve, defense needs to improve alongside it,” Narang said.

Microsoft is not alone in scaling up its patch cadence in response to AI-assisted vulnerability discovery. Chris Goettl, a security researcher at the IT management firm Ivanti, noted that several other major software makers have similarly increased how frequently they release security fixes. Adobe announced this week that it is shifting to a twice-monthly security bulletin schedule, publishing updates on the second and fourth Tuesday of each month, and specifically cited AI as a factor accelerating its own patch cycles. Goettl added that Cisco, Mozilla and Oracle have also increased the frequency of their security updates recently, while Google’s cumulative patch releases in June 2026 alone totaled more than 900 individual security fixes.

Security professionals recommend that organizations and individual users back up their systems and data before applying large batches of operating system updates. Given the unusually high volume of patches included in this month’s release, some experts suggested users consider waiting a few days before installing the updates, since large patch releases can occasionally introduce system stability issues alongside the security fixes they deliver. That risk appears to have grown alongside the dramatic increase in patch volume seen in recent months, as Microsoft and other vendors race to keep pace with AI-accelerated vulnerability discovery on both the defensive and offensive sides of the security landscape.

The record patch count adds to a broader industry conversation about how artificial intelligence is reshaping both cybersecurity research and the software development practices that produce the underlying code in the first place. While AI tools have proven effective at surfacing previously undiscovered flaws in massive, decades-old codebases that would be impossible for any single researcher to fully review manually, the same technology is simultaneously lowering the barrier for attackers to weaponize newly disclosed vulnerabilities, a dynamic that security researchers say is forcing companies like Microsoft to rethink how they prioritize and communicate risk to their customers going forward.

Nyoongar businessman Gerry Matera is bringing in the legal big guns as he investigates an attack on his Indigenous Business Integrity Register.

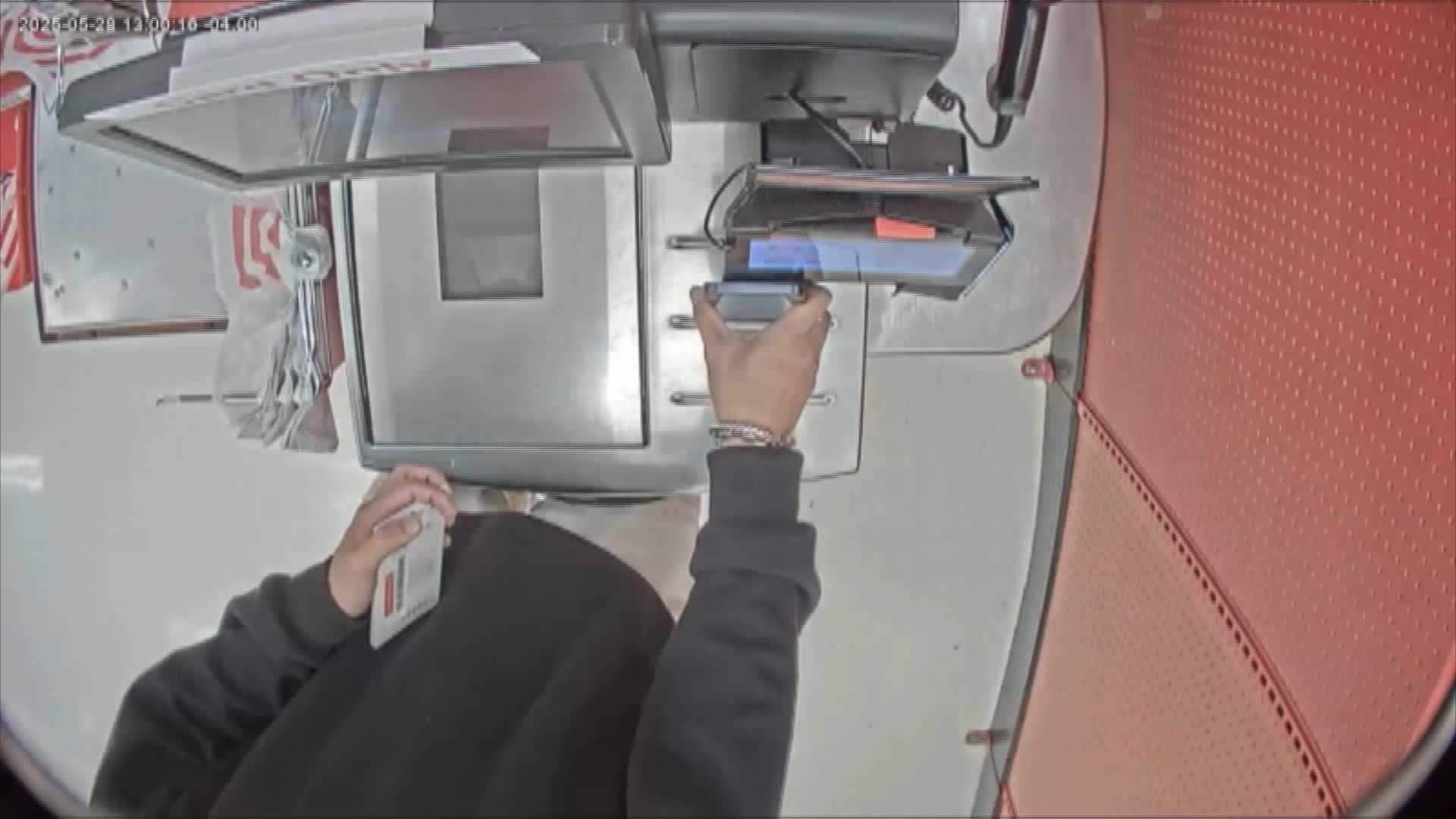

When a man in a black Air Jordan T-shirt walked up to a self-checkout kiosk at a Louisiana Lowe’s last spring, he looked like any other customer.

Over the course of about seven minutes, he methodically rang up different gift cards for $95 each, using his phone to tap-to-pay for each card as a red-vested associate circled nearby, surveillance video showed.

Unknown to the employee, the man was part of a sprawling Chinese crime ring, using stolen credit cards to buy the gift cards while a Southeast Asian scam compound coached him through each transaction through the wireless headphones in his ears, police say.

“We know that there are hundreds of individuals at any one time doing this across the country,” said Adam Parks, an assistant special agent in charge with U.S. Homeland Security Investigations, who investigated the case. “Even though you think that’s $95 every transaction, that adds up to a lot of money.”

A suspect that police said is connected to a Chinese organized crime ring using stolen credit cards to purchae gift cards at a Lowe’s in Hammond, Louisiana.

HSI

After the man left the hardware store, he purchased more gift cards with stolen credit card information at other retailers only to return to the original Lowe’s the same day to repeat the act, Parks said. He was not arrested and is still a suspect, he added. Lowe’s didn’t respond to repeated requests for comment from CNBC.

While credit card theft and fraud isn’t new, with the proliferation of tap-to-pay and growing use of retail apps, these digital thefts are shaping the next wave of organized retail crime and earning Chinese gangs as much as $1 billion annually, police said. Unlike typical retail theft operations — where criminals clear out shelves in big box stores and resell merchandise piece by piece on online marketplaces — the crimes can be carried out right under a store employee’s nose or from a computer anywhere in the world.

“It’s very low risk for the bad actors,” said Scott Glenn, vice president of asset protection at The Home Depot. “It’s not the same thing as walking into a Home Depot, filling up a cart full of power tools, and then walking out. It’s just not as visible, it’s not as obvious to what’s happening out there and so it’s become a more preferred method over the last several years.”

Fraudsters have selected retailers as their targets because their platforms carry sensitive information such as stored credit cards and personal data but they do not have the same level of security as banks, according to industry experts and law enforcement.

A man police say participated in a tap-to-pay fraud scheme at a Target store self-

checkout in Tennessee

Source: Knox County Sheriff’s Office

There’s no firm data on how much retailers are losing from digital forms of retail crime, but CNBC found around a dozen criminal cases across the country affecting a wide variety of retailers that police said involve a combination of organized groups and low-level fraudsters.

The cases are complex and often hard for local authorities to handle, said Capt. Matt Lawson of the Knox County Sheriff’s Office in Tennessee, who said he’s been investigating a fraud ring with ties to Chinese organized crime.

Unless the theft hits a certain dollar threshold or rises to the level of a federal crime, “it’s kind of like they get away with it almost,” he said.

Unpaid toll bills and pending criminal judgments

Tap-to-pay fraud, which involves a fraudster adding a stolen credit card to their digital wallet and using it to buy gift cards or merchandise, often starts with a familiar text message and can end with an unwitting consumer’s identity up for sale on platforms such as Telegram.

Fraudsters send out mass text messages warning about unpaid tolls, expiring car registrations or pending arrests that are designed to scare consumers into providing their credit card information, email credentials or other sensitive data. AI has only made the schemes easier, as crime groups can scale the scams more quickly and make the messages appear more legitimate, experts said.

“Once a fraudster has a person’s email password and credit card, they can load that credit card into a device that they control,” said Jeff Otto, the chief marketing officer of Riskified, a tech company that works with retailers including Macy’s, Peloton and Prada to fight fraud.

Jeff Otto, the chief marketing officer of Riskified.

CNBC

“When the bank reaches out to say, ‘Hey, is that you loading the card?’ They’ve already got access to the victim’s email” and can often check it for a one-time passcode before the consumer notices, he said.

Low-level opportunists engaging in tap-to-pay schemes can operate independently, using the practice to either buy merchandise or purchase gift cards and resell them at a discount for cash.

But on the Chinese organized crime level, the practice involves an entire criminal network, Parks said. In order to get profits back to China, crime groups use tap-to-pay fraud to buy gift cards and then use those gift cards to purchase high-value goods that can be resold at a premium in China, such as iPhones with American settings, Parks said. The practice allows gangs to skirt strict banking laws both in the U.S. and China and convert higher amounts of cash into the legitimate economy.

At the heart of the strategy are foot soldiers such as the customer at Lowe’s who police say helped carry out the fraud, which in the years since the Covid-19 pandemic has ramped up along with a surge of Chinese nationals at U.S. land crossings, Parks said.

People looking to enter the country illegally often rely on smugglers and organized crime networks, and they then owe a debt that crime groups require them to pay off once they’re in the U.S.

“So [they’re] going to instruct you on how to go into a store, convert the stolen credit card information into acquiring goods and then now you’re going to ship those goods back to China,” Parks said. “That’s where a lot of times we get our arrests, but that is the lowest level of the organization.”

Adam Parks, an assistant special agent in charge with U.S. Homeland Security

Investigations.

CNBC

Tap-to-pay schemes also can include retail app fraud, which involves stealing someone’s credentials, logging into their account and using stored credit card information to purchase merchandise or gift cards.

Riskified’s Otto showed CNBC how data breaches, phishing and social engineering, which involves piecing together publicly available information about someone to steal their identity, can give fraudsters access to a consumer’s retail account.

CNBC saw that login credentials for Walmart‘s app and website were being sold on various Telegram channels for between $1.50 and $2.50 with information about how long the accounts had been active.

“They have Yahoo addresses that are 10 years old, Gmails that are 10 years old,” Otto said. “These are older accounts that often get past some of the more rudimentary fraud checks [because] we tend to trust accounts that have been with us for a long time. And in this case, these can be sold.”

Telegram didn’t return a request for comment.

Compounding the issue is the fact that retail apps and websites don’t always have the same level of security as platforms like banking apps, Otto said. On their face, retail apps are for shopping, places for consumers to buy clothes, household necessities or makeup.

But they also contain stored credit cards, sensitive personal information and sometimes, access to a consumer’s store-branded credit card. For example, Macy’s customers can shop on its app and use the same platform to pay their Macy’s credit card bill.

“It has a lot to do with the fact that they are focused on convenience and they’re focused on conversion, generating the maximum amount of online revenue, and because of that, they do not use bank-grade security,” Otto said. “They don’t want to add additional friction.”

In a statement to CNBC, Walmart said “customer privacy and safety is a top priority.”

“While we won’t disclose specific security measures, Walmart has systems in place to help detect bad actors, prevent, and respond to unauthorized account access and is continuously enhancing these protections,” the company said. “In addition, full payment card information is not stored in an unprotected form.”

Using anime to disguise fraud

In a review of tap-to-pay cases across the country, CNBC found a mix of low-level opportunists and organized crime rings.

In January, Dancliff Labady was arrested in Miami and accused of stealing nearly $95,000 primarily using TJX Companies’ store-branded credit cards for TJ Maxx, Marshall’s and Home Goods, according to a police report. Police allege he obtained access to about 15 different customer accounts by calling Synchrony Bank, the card issuer, and adding a phone number he controlled to the accounts. It’s unclear what customer information Labady needed to provide to Synchrony to make the account changes.

Once Labady added his number to the accounts, he was able to add the cards to his digital wallet and conduct dozens of transactions at TJX stores across the Miami area over the holiday shopping season without having a physical card, police said. He was arrested after TJX’s asset protection team reported the suspicious activity to Synchrony Bank.

Labady has pleaded not guilty and his attorney declined to comment. A spokesperson for Synchrony said it doesn’t comment on ongoing investigations and is “cooperating fully with law enforcement.”

In a statement, a TJX spokesperson said “protecting our customers’ personal information and our technology systems is very important to us.”

“We have measures in place across our systems and stores designed to identify and address potential fraudulent account activity,” the spokesperson said. “We would also encourage our customers to maintain strong online account security practices, including not re-using passwords across websites or apps, and to report any suspected fraudulent activity to their bank or credit card company immediately.”

There have been broader efforts to root out the fraud schemes, as well.

Since spring 2025, the Knox County Sheriff’s Office arrested more than a dozen suspects with alleged ties to Chinese organized crime who officials said were traveling across the country and using stolen credit card information to purchase gift cards and launder money.

In a review of cell phones seized in connection with the cases, investigators found the suspects were using special apps that contained the stolen credit card information but disguised them as games to evade detection.

“They look like anime games. They kind of look like Pokemon characters,” said Lawson, who’s been investigating the fraud ring. “We would just kind of start tapping on them … and we would find the ones that were the actual tap-to-pay apps.”

On a national level, Homeland Security Investigations’ Project Red Hook targets gift card fraud and other forms of digital retail crime. So far, it has led to at least 239 arrests since January 2024 and is targeting some of the largest Chinese organized crime groups operating in the U.S., HSI said.

For several years, the retail industry and law enforcement organizations have been lobbying Congress to pass the Combating Organized Retail Crime Act, which they say would increase information sharing and make these types of complex cases easier to tackle. It passed the House in May and was recently included as part of an amendment to the National Defense Authorization Act in the Senate. It’s expected to be voted on before the end of the year.

Lawson said he’d like to see better sharing of information.

“Law enforcement sometimes likes to hold information and not share everything and kind of compartmentalize it … even the retailers are guilty of this.”

“The more information that we get out when we notice these people are breaking these laws” the easier it will be to catch them, he said.

— Additional reporting by Paige Tortorelli

I am an individual investor who is now fully focused on managing my own capital. My investing background focuses on value investing with an emphasis and interest in small to mid-cap stocks. I believe history often repeats itself, and investors can gain valuable insights into the future of companies by examining their historical performance and industry peers. By understanding the history of how they got here, meaningful insights can be inferred about where the companies are going in the future. The reason to write on SeekingAlpha is to use this platform as a tracker for my investing ideas, research, performance, and also to connect with like-minded investors who have similar investing interests. I believe clarity of thought can not be obtained without clarity in writing. Putting ideas down on paper helps me refine my thinking and thesis. I tend to write a lot as I look at multiple companies a day and use writing as a tool to track and evaluate my ideas. By writing down all of my ideas it will help me to become a better investor. Although my focus is on small to mid-cap companies, I have an interest in analyzing technology, mining and the retail industry. One area I tend to avoid is biotech, as the industry is highly specialized with technical knowledge requirements and almost impossible for generalists to gain an edge. I hold a degree in accounting, and it has been particularly useful when analyzing companies that are under financial distress (commonly amongst small to mid-cap companies). Evaluating the company’s solvency and ability to continue operations is one of the necessary checks.Disclosure: author is closely associated with Troy Research

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Dutch Court Declares Knaken Crypto Platform Bankrupt

Prime Video’s ‘God of War’ Series Is Officially Recasting Its Lead

Frugal Friday’s Workwear Report: Double-Pleat Wide-Leg Pants

-

Fashion7 days ago

Fashion7 days agoWeekend Open Thread: Nutriplenish Leave-In Conditioner

-

NewsBeat21 hours ago

NewsBeat21 hours agoLondon Mayor Sadiq Khan handed a peerage by Keir Starmer alongside 15 other Labour figures… just days before the PM leaves No10

-

Crypto World1 day ago

Crypto World1 day agoCFTC blocks Kalshi from unwinding Michigan trades after court order

-

Business1 day ago

Business1 day agoNvidia Stock Slips After Big Tuesday Rally as Huang Confirms Vera Rubin Chip Is Now in Production Today

-

Politics2 days ago

Politics2 days agoYoung campaigners urge incoming PM to act on outdoor junk food ads

-

Entertainment2 days ago

Entertainment2 days agoDisney’s Most Ambitious Failed Star Wars Attraction Is Coming to SDCC

-

News Videos3 days ago

News Videos3 days agoXRP BOMBSHELL… XRP OMBOARDED FOR TRANSACTIONS!!!

-

Tech3 days ago

Tech3 days agoGet Your ESP32 Sunny Side Up With This Solar Dev Board

-

Crypto World16 hours ago

Crypto World16 hours agoInjective Submits SEC Transfer-Agent Registration to Onchain Ownership Records

-

Tech3 days ago

Tech3 days agoDark Secrets Emerge When Jailbreaking LLMs

-

Business1 day ago

Business1 day agoPalantir Shares Rise After Expanded Nvidia Partnership and Fresh Analyst Upgrades Ahead of Earnings Day

-

Sports2 days ago

Sports2 days agoNew Cornerback Enters Vikings Trade Rumor Mill

-

News Videos6 hours ago

News Videos6 hours agoMoney | Class 12 Economics | CBSE Board Exam 2026-27

-

Business11 hours ago

Business11 hours agoBanco Bilbao Vizcaya Argentaria, S.A. (BBVA) Discusses Global Macro Environment and Economic Outlook for Core Markets Transcript

-

Tech4 days ago

Tech4 days agoCloudflare Precursor Watches Your Mouse and Keyboard To Decide If You Are Human

-

News Videos4 days ago

News Videos4 days agohow to make coin bank box with cardboard #scienceproject #money #diy #shorts

-

Entertainment2 days ago

Entertainment2 days agoVicki Gunvalson Defends Discussing Heather Dubrow’s Money

-

Crypto World3 days ago

Ripple, Coinbase, Circle Join Linux x402 Foundation to Help Shape AI Payments

-

Crypto World15 hours ago

Crypto World15 hours agoClaude Fable 5 Slips to Second in AI Coding Leaderboard

-

Business12 hours ago

Nephros, Inc. (NEPH) Discusses Evolving Water Safety Strategies and Expansion Beyond Filtration Transcript

You must be logged in to post a comment Login