“Singapore’s 2026 economic focus shifts from growth to stability, emphasizing reliable regulation, strategic positioning, and dependability for investors in a changing global trade environment.”

Overview of Singapore’s Economic Outlook

The “Introduction to Doing Business in Singapore 2026” report from Dezan Shira & Associates highlights Singapore’s economic resilience. While growth has slowed, with GDP expected to expand between 0 and 2 percent, this reflects softer external demand and a decline in manufacturing output. Trade-sensitive sectors, including non-oil domestic exports, have experienced about a 3.5 percent decrease year-on-year, emphasizing Singapore’s economy reliance on global demand conditions.

Strategic Investment Environment

Despite slower growth, Singapore remains attractive for foreign investors due to its stable regulatory environment, advanced financial markets, and institutional capacity. The shift in investment strategy focuses less on short-term growth and more on leveraging Singapore’s reliability as a strategic platform. In today’s uncertain trade landscape and restructuring of global supply chains, Singapore’s consistent regulatory framework offers a competitive advantage.

About the Publication

This comprehensive guide, prepared in June 2023, provides essential insights into investing in Singapore. Dezan Shira & Associates, experts in foreign direct investment services, compiled it to assist multinationals and SMEs in understanding Singapore’s business environment, covering aspects such as corporate setup, compliance, tax, and financial management.

Cocaine and cannabis are among drugs being readily offered for sale in High Street mini-marts, a BBC investigation has revealed.

Undercover researchers secretly filmed in towns across the West Midlands, including one shop called Cradley Market. One of those researchers met Akwa, who works behind the counter there.

It took just seconds for Akwa to supply him with 3.5g of cannabis for £30. “I’ve got weed, coke, everything. Whatever you want, I can sort you out,” Akwa told the researcher, later supplying him with cocaine.

Akwa denied any wrongdoing when the BBC’s UK Editor Ed Thomas later confronted him. When asked about selling drugs, he said he did not know what he was talking about, before asking Ed and his team to leave.

Advertisement

The government is working with police, the National Crime Agency (NCA) and Trading Standards to “take the strongest possible action against these criminal businesses”, a spokesperson for the Home Office said. West Midlands Police said it would always work with partners “to act on complaints about illegal drugs sales, anti-social behaviour, and crime and disorder”.

Business to open sites in Cardiff, Brighton and Chester

The Padel Club secured investment from NPIF II – PXN Equity Finance(Image: NPIF)

A Cheshire business focused on fast-growing racket sport padel has secured eight sites across the UK and plans to open more after securing investment through the Northern Powerhouse Investment Fund.

The Padel Club was founded in 2020 by Kris Ball after he played padel overseas and realised it would soon take off in the UK too. Its first site opened in Wilmslow in 2022 and it soon grew to four sites.

Since then it has secured eight new sites in the UK and plans to grow further. Upcoming openings will include venues in Brighton, Cardiff, Chester and Handforth Dean.

Advertisement

Kris Ball, CEO of The Padel Club, said: “We saw an opportunity to bring padel to the UK at a time when the sport was still relatively unknown. Starting with just a couple of courts in Wilmslow, our ambition has always been to build a network of clubs that could introduce more people to the game and create a real sense of community around it. The support from NPIF II and PXN has given us the platform to accelerate that vision, helping us scale at pace, invest in new sites and continue growing this much-loved sport across the UK.”

Louise Chapman at PXN Ventures, said: “The Padel Club is a standout example of an ambitious, fast-scaling business bringing a relatively new sport to communities across the UK. From a single site in Wilmslow, Kris has built a strong platform for growth with a clear pipeline of locations and a differentiated, community-led offer. We’re pleased to be supporting their next stage of expansion as they continue to introduce more people to padel.”

Sue Barnard, senior investment manager at the British Business Bank, said: “Through the Northern Powerhouse Investment Fund II, we’re backing ambitious, fast-growing and community-focused businesses that are delivering real impact across the North. Just two years on from its launch, we’re already seeing tangible results, with businesses creating jobs and unlocking new opportunities to support local economies and The Padel Club is a great example of this.”

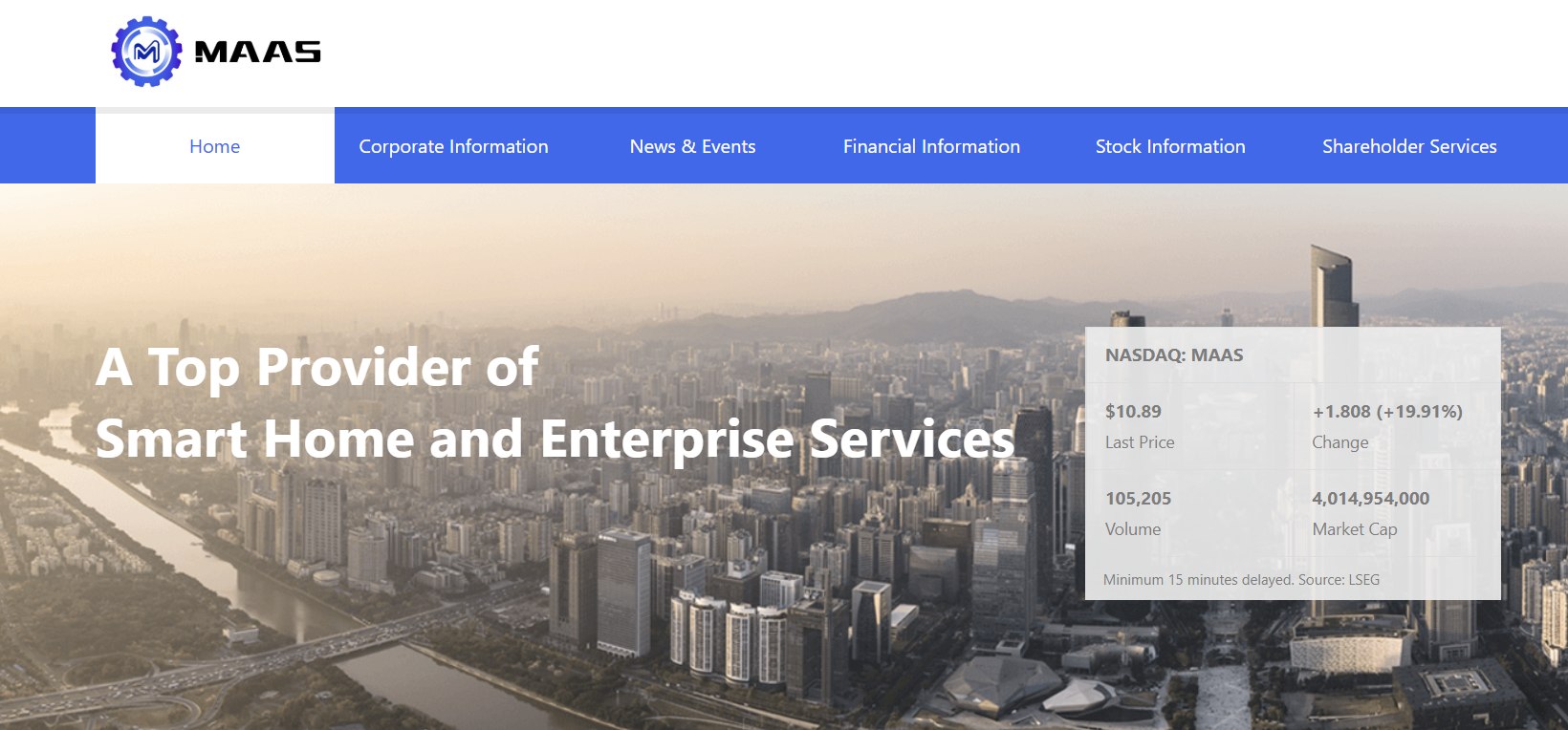

NEW YORK — Maase Inc. shares skyrocketed more than 21 percent in early trading Wednesday, reaching $11.01 as speculative enthusiasm returned to the China-based financial technology and emerging AI player following a period of sharp volatility and heavy trading volume.

Maase Inc Stock Explodes 21% on Renewed AI Acquisition Momentum and Speculative Buying

The Nasdaq-listed stock (MAAS) gained $1.93, or 21.31 percent, by 10:10 a.m. EDT, reversing much of Tuesday’s steep decline and highlighting the highly volatile nature of the name amid its aggressive pivot toward artificial intelligence infrastructure. Trading volume surged well above recent averages, reflecting continued retail and momentum-driven interest in the company’s transformation narrative.

Maase Inc., formerly known as Puyi Inc. and rebranded to reflect its evolving focus, operates primarily as a technology-driven financial services platform in China. It provides wealth management, insurance agency services and asset allocation solutions for families and enterprises through digital platforms and offline networks. Revenue has historically been dominated by its insurance agency segment, which distributes life and non-life insurance products.

In recent months, however, Maase has executed a series of strategic acquisitions aimed at repositioning itself as a full-stack AI industry player. The most significant move came on March 30, 2026, when the company completed its acquisition of 100 percent equity in Times Good Limited, which controls Huazhi Future (Chongqing) Technology Co., Ltd. and its subsidiaries. The deal, valued in the range of RMB1.1 billion when announced in January, gives Maase access to advanced computing power, algorithms and AI-related assets, marking a shift from traditional financial services toward high-performance computing and intelligent systems.

The Huazhi Future acquisition has been central to the stock’s dramatic price swings. Shares hit a 52-week high of $20.89 on April 20 before pulling back sharply on April 21, closing at $9.08 amid profit-taking and concerns over valuation and integration risks. Wednesday’s rebound suggests some investors view the dip as a buying opportunity, betting on the long-term potential of Maase’s AI ambitions in a market hungry for computing infrastructure tied to artificial intelligence.

Advertisement

Analysts and market observers note that Maase is still in the early stages of its transformation. The company has also pursued deals in new-energy technologies, intelligent unmanned systems, mobile charging robots and wellness sectors, including the acquisition of premium tea producer Oriental Grove and healthcare-related assets. These moves have created a diversified but complex portfolio that blends legacy financial services with forward-looking tech initiatives.

Despite the acquisition-driven narrative, Maase continues to face challenges typical of growth-stage companies executing rapid strategic shifts. The firm has reported ongoing net losses, and its financials reflect the costs of expansion and integration. Recent filings have highlighted risks including goodwill from acquisitions, share-based consideration that has diluted existing shareholders, and the operational complexities of merging Chinese AI assets with its core financial platform.

The stock’s volatility has been extreme. From a 52-week low near $2.41 in mid-2025, MAAS has delivered triple-digit percentage gains at times, fueled by acquisition announcements and broader AI sector enthusiasm. However, the rapid run-ups have also led to sharp reversals, as seen in the April 21 sell-off that erased significant gains from the prior session. Elevated trading volumes — sometimes several times the average — indicate heavy participation from short-term traders and momentum investors.

Maase’s market capitalization has fluctuated wildly with the share price, recently approaching or exceeding $3 billion during peak enthusiasm. The company’s shift toward AI has drawn comparisons to other small-cap names attempting to ride the artificial intelligence wave, though execution risks remain elevated given its relatively modest revenue base and ongoing unprofitability.

Advertisement

Company executives have framed the Huazhi Future deal as establishing “full-stack, self-controlled capabilities” in AI, encompassing computing power, algorithms, hardware and services. This positions Maase to potentially benefit from China’s push for technological self-reliance and global demand for AI infrastructure. Additional initiatives, such as the launch of distributed intelligent computing center projects with planned investments up to RMB5 billion, have further stoked investor interest.

Yet skeptics caution that the valuation appears stretched relative to current fundamentals. With a history rooted in insurance brokerage and wealth management, Maase must successfully integrate its new AI assets while maintaining its core operations. Regulatory considerations in China’s financial and technology sectors, currency fluctuations and geopolitical tensions could also impact progress.

Wednesday’s surge occurred against a broader market backdrop that included modest gains in major indices and continued focus on artificial intelligence themes. The stock’s movement stands out even within the volatile small-cap technology space, where narrative-driven trading often dominates over near-term earnings visibility.

Maase is scheduled to report financial results in coming months, though no specific date has been confirmed in recent disclosures. Investors will look for updates on revenue contribution from newer segments, progress on AI integration, margin trends and any guidance on future acquisitions or capital raises.

Advertisement

The company, headquartered in Chengdu with operations in Guangzhou and other Chinese cities, employs hundreds and continues to expand its digital platforms. Its evolution reflects a common pattern among Chinese-listed firms on U.S. exchanges: leveraging Nasdaq visibility to fund ambitious strategic pivots into high-growth sectors like AI while managing legacy businesses.

As trading progressed Wednesday morning, the rebound to $11.01 demonstrated resilient buying interest despite recent profit-taking. Whether the momentum sustains will depend on fresh catalysts, successful execution of the Huazhi integration and broader market sentiment toward AI-related small caps.

For long-term investors, Maase represents a high-risk, high-reward bet on China’s AI ambitions and the company’s ability to transition from financial services to a broader technology ecosystem. Short-term traders, meanwhile, appear focused on technical levels and news flow around its transformation.

The dramatic price action in Maase Inc. underscores the speculative fervor surrounding artificial intelligence themes in 2026, even as many companies in the space remain pre-profit and face significant operational hurdles. With shares up sharply in early Wednesday trading, all eyes remain on whether Maase can convert acquisition momentum into sustainable growth and profitability.

Thank you for standing by, and welcome to the Regis Resources quarterly briefing. [Operator Instructions] I would now like to hand the conference over to Mr. Jim Beyer, Managing Director and Chief Executive Officer. Please go ahead.

Jim Beyer CEO, MD & Director

Advertisement

Thanks, Darcy. Good morning, everyone, and thanks for joining us for the Regis Resources March FY ’26 quarter results. Joining me on the call today is our CFO, Anthony Rechichi; our COO, Michael Holmes; and our Head of Investor Relations, Matt Collings.

At times, we’ll refer to figures and tables in both the quarterly report, which came out this morning, and also the resource and reserves report, which was released yesterday morning. So you may find it useful to have those documents at hand.

Okay. I’ll start with safety. During the December quarter, our operations continued to perform strongly from a safety perspective. The 12-month moving average lost time injury frequency rate finished the quarter a little bit further down at 0.32, which continues to be well below the Western Australian gold industry average. Our objectives remain unchanged to provide a workplace free from serious injury. We continue to focus on leadership, discipline and continuous improvement to support safe and reliable operations across our business.

Turning now to our enviable production performance. The team has consistently delivered to plan during FY ’26 and the March quarter was no exception. Operationally, the group

ET Intelligence Group: Trent’s revenue growth in the March quarter at 19.2% was better than the 15-16% growth in the previous two quarters, driven by relatively stable consumer sentiment. However, the company’s expansion into Tier-II and Tier-III cities has been putting pressure on its largest business segment, fashion portfolio, which contributes four rupees to every five rupees of revenue. The segment’s like-for-like sales growth reduced for the quarter and for the full fiscal year as well. Though Trent believes underlying demand and market opportunities to be strong, its strategy to win market share through rapid scaling up may restrict the growth momentum in the short term. In addition, the conflict in West Asia may push up input costs though Trent is mitigating the risk through largely India-focused sourcing.

For the fashion portfolio, the same-store-sales-growth (SSSG), which consists of stores operational for over 18 months, slipped to low single digits in the March 2026 quarter and in FY26 from mid-single digit growth in the March 2025 quarter and a double-digit increase in FY25. This could be attributed to most of the stores being opened in Tier II and III cities. It further plans to raise ₹2,500 crore through a rights issue to fund the expansion strategy. It means the growth trend is likely to persist in the medium term as the company has indicated that it takes two-to-three years for newer markets to become more relevant.

Agencies

same-store-sales-growth slips to low single digits For fashion portfolio

Apart from the physical channels, Trent’s online channels – Westside.com and Tata Neu – also showed moderation in sales growth. After rising to 56% in the September 2025 quarter from 35% in the June 2025 quarter, it gradually reduced to 25% in the March 2026 quarter. The share of online channels to Westside revenues remained stable at 6% year-on-year.

On the positive side, Trent’s operating margin (EBIT margin) has gradually increased to 11.5% in the March 2026 quarter from 2.9% in the March 2023 quarter, aided by disciplined pricing, better inventory control, and the benefits of scale in sourcing and supply chain operations.

Advertisement

Trent’s stock has gained nearly 25% since April 06 when it issued an encouraging business update for the March quarter, implying a sustained top line growth. This has taken its one-month gain to 32%, also buoyed by an anticipation of a bonus issue of shares. While the announcement of the bonus issue will support the stock in the near term, its performance over the medium term will depend upon how effectively the company executes its expansion strategy.

You must be logged in to post a comment Login