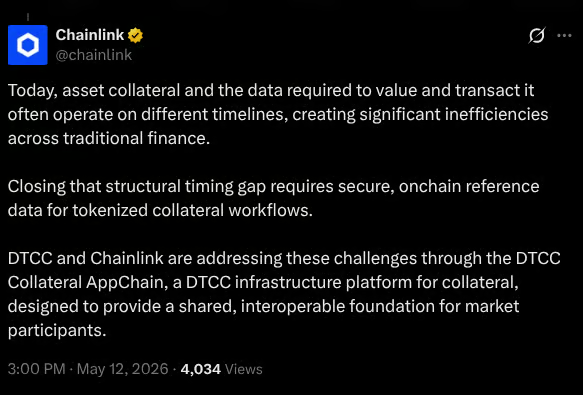

AMSTERDAM — The Netherlands has emerged as one of Europe’s most dynamic AI ecosystems in 2026, boasting the continent’s highest density of AI talent at 10.9 professionals per 10,000 inhabitants. Despite challenges in scaling startups, the country’s deeptech strength, strong university ties and strategic location have fueled growth in hardware, software, data platforms and applied AI solutions. From edge AI chips in Eindhoven to vector databases and medical imaging in Amsterdam, Dutch companies are attracting international investment and addressing global challenges in efficiency, healthcare and sustainability.

Top 10 AI Companies in Netherlands 2026: Leading Innovators Powering Europe’s AI Talent Hub

Here are the 10 best AI companies in the Netherlands in 2026, ranked by a combination of funding, innovation impact, market traction and expert recognition across recent reports and rankings.

1. Axelera AI (Eindhoven) Axelera AI stands out as the Netherlands’ flagship AI hardware player. Founded in 2021, the fabless semiconductor company develops high-efficiency platforms for edge AI inference, including its Metis AI platform that accelerates computer vision and generative AI workloads with low power consumption. The company has raised over $200 million, including significant grants, and focuses on simplifying deployment for industrial and automotive applications. Its technology addresses the growing demand for on-device AI without relying on cloud connectivity, positioning Axelera as a key contributor to Europe’s technological sovereignty.

2. Weaviate (Amsterdam) Weaviate has become a global leader in open-source vector databases optimized for AI applications. The company’s platform enables semantic search, recommendation systems and retrieval-augmented generation for large language models. With strong adoption among developers building generative AI tools, Weaviate continues to expand its ecosystem through integrations and enterprise features. Its open-source roots and focus on scalability have driven rapid growth, making it a cornerstone of the Dutch AI software scene.

3. Innatera (Eindhoven) Specializing in neuromorphic processors, Innatera designs ultra-low-power AI chips inspired by the human brain. The company targets edge devices in IoT, wearables and sensor networks where energy efficiency is critical. Backed by substantial funding, Innatera’s technology promises dramatic reductions in power usage compared to traditional GPUs, appealing to industries seeking sustainable AI solutions. Its progress highlights Eindhoven’s role as a deeptech powerhouse.

Advertisement

4. ScreenPoint Medical (Nijmegen/Amsterdam area) ScreenPoint Medical applies AI to breast cancer detection through its Transpara software, which analyzes mammograms with high accuracy. The company has secured regulatory approvals in multiple markets and demonstrated strong clinical results, helping radiologists improve detection rates while reducing workload. Its success in medical imaging underscores the Netherlands’ strength in healthtech AI and positions ScreenPoint as a leader in life-saving applications.

5. Nebius (Amsterdam) Nebius, formerly part of Yandex, has established itself as a major AI cloud infrastructure provider with headquarters in Amsterdam. The company builds large-scale GPU clusters and data centers across Europe, offering computing power for training and deploying advanced AI models. Its Nasdaq listing and multi-billion-dollar valuation reflect its scale and importance in addressing Europe’s AI infrastructure gap amid growing demand from enterprises and researchers.

6. Toloka (Amsterdam) Toloka delivers high-quality human-labeled data essential for training large language models and generative AI systems. The Amsterdam-based platform connects AI developers with a global workforce for data annotation tasks, emphasizing quality and ethical practices. With significant funding and partnerships, Toloka supports the data-hungry AI boom while maintaining operations that align with European privacy standards.

7. FRISS (Utrecht) FRISS specializes in AI-driven fraud detection and risk management solutions, primarily for the insurance and financial services sectors. Its platform uses machine learning to analyze claims, detect anomalies and automate investigations, helping clients reduce losses and improve efficiency. Established as a mature player, FRISS continues to expand its international footprint with advanced analytics tailored to regulated industries.

Advertisement

8. Pyramid Analytics (Amsterdam) Pyramid Analytics provides an AI-powered decision intelligence platform that combines analytics, business intelligence and machine learning. The company’s tools help enterprises make data-driven decisions across finance, operations and strategy. With over $200 million in funding historically, it serves large organizations seeking to democratize AI insights without requiring deep technical expertise.

9. Source (Amsterdam area) Source ranks among the top AI companies for its innovative applications in enterprise automation and data processing. The firm develops custom AI solutions that integrate with existing business systems, focusing on efficiency gains in sectors like logistics and manufacturing. Its consistent recognition in startup rankings reflects strong product-market fit and growth potential.

10. Wonderflow (Amsterdam) Wonderflow leverages AI for customer experience and product intelligence, analyzing feedback, reviews and market data to help brands improve offerings. The company’s platform uses natural language processing to extract actionable insights at scale, serving consumer goods and retail clients. Its focus on practical business outcomes has driven steady adoption and international expansion.

The Dutch AI landscape benefits from close collaboration between academia — including strong programs at TU Eindhoven, University of Amsterdam and Delft University of Technology — and industry. Government initiatives and organizations like Techleap.nl support talent development and commercialization, though reports note that scaling remains a hurdle, with many promising startups relying heavily on foreign capital.

Advertisement

Eindhoven’s Brainport region has solidified its reputation as Europe’s “Silicon Valley” for hardware and deeptech AI, while Amsterdam dominates in software, data and applied solutions. Rotterdam and Utrecht also host growing clusters in logistics AI and fintech applications.

Challenges persist. The 2026 State of Dutch Tech report highlights that while AI attracts 27% of venture capital, conversion from startup to scaleup lags behind European peers. Talent density is a major asset, but retaining and commercializing innovations requires more domestic growth capital and supportive policies.

Industry observers expect continued momentum in 2026, driven by European Union AI regulations that favor trustworthy and transparent systems — an area where Dutch companies often excel. Edge AI, sustainable computing and domain-specific applications in healthcare, agriculture and finance are likely to see the strongest growth.

For businesses and investors exploring opportunities, the Netherlands offers a mature ecosystem with English-speaking talent, excellent infrastructure and a business-friendly environment. Companies on this list represent a mix of established players and high-potential innovators, many of which are actively hiring and seeking partnerships.

Advertisement

As AI adoption accelerates globally, these 10 Dutch firms illustrate the country’s ability to punch above its weight. From chips that run AI on tiny devices to platforms that power large-scale models, the Netherlands is carving out a distinctive role in the international AI landscape — one built on precision engineering, ethical considerations and practical innovation.

The coming years will test whether the ecosystem can convert its talent advantage into more homegrown unicorns and global leaders. For now, these companies stand as proof that the Netherlands remains a vital node in Europe’s AI ambitions.

Containers at the Port of Oakland in Oakland, California, US, on Thursday, March 26, 2026.

David Paul Morris | Bloomberg | Getty Images

Months after the Supreme Court ruled some tariffs were unconstitutional, the first round of tariff refunds has begun flowing in.

Advertisement

Oshkosh Corporation CFO Matt Field confirmed to CNBC that the company has started receiving tariff refunds as of Tuesday.

“Following acceptance of our initial filing, we have begun receiving payments on our tariff refund claims, representing an initial portion of our total claims submitted,” Field said.

The company has not yet verified its total refund amount, Field added.

Basic Fun, the company behind Care Bears and Tonka trucks, also told CNBC it began receiving tariff refunds on Tuesday.

Advertisement

CEO Jay Foreman said the refunds so far have only represented 5% of the company’s total claim on its early invoices.

“We will utilize the refund dollars to help support our 2026 cash flow and invest in our team. This is the toughest time of the year for toy companies,” Foreman said in a statement. “We’ll also be announcing to our staff that we will be increasing salaries to help offset cost of living increase, announcing promotions and larger merit increases. We are reinvesting the funds in our business and people.”

Logistics companies UPS, FedEx and DHL have previously said that they will file for tariff refunds on behalf of their customers, requiring no further action from them. The first phase of tariff refunds only covers requests for entries that CBP finalized within the past 80 days, though that process could take months to reach customers.

The U.S. Customs and Border Protection said in a court filing that it anticipated paying refunds of $35.46 billion on 8.3 million shipments, as of Monday morning.

Advertisement

In February, the Supreme Court invalidated President Donald Trump‘s tariffs imposed under the International Emergency Economic Powers Act of 1977. In the months that followed, companies began filing for tariff refunds in a portal, called the Consolidated Administration and Processing of Entries.

In a radio interview with WABC on Tuesday morning, Trump called the tariff refund situation “crazy.”

“In theory, you have to pay the tariffs back. We’ll fight that,” Trump said. “We were taking in fortunes from people that hate us, countries and companies that hate us.”

A United Airlines plane approaches the runway at Denver International Airport on March 23, 2026.

Al Drago | Getty Images

United Airlines flight attendants approved a new five-year labor contract with 31% average raises to base pay by August and other improvements, marking the last of the major carriers with unionized flight crews to reach a deal post-Covid.

Advertisement

The labor deal would give United’s roughly 30,000 flight attendants their first raises in close to six years. The company and the flight attendants’ union reached a preliminary deal in March. Crews had rejected a contract last year.

The union said the contract won 82% approval from the flight attendants, with close to 90% of them voting.

“The contract will immediately change the lives of United Flight Attendants, especially our thousands of new hires who have been hired since the pandemic,” said Ken Diaz, president of the United chapter of the Association of Flight Attendants.

The contract also includes boarding pay, or pay for when the aircraft’s door is open and travelers are getting on. Airlines had for years started flight attendants’ pay clock once the boarding door was closed.

Advertisement

The contract comes with a roughly 7% to 8% increase in compensation and $741 million in back pay, as well as quality-of-life improvements like restrictions on red-eye flights and “sit pay” during disruptions of more than 2½ hours.

Many employers assume that withdrawing a job offer before someone starts work is a low-risk decision.

A recent Employment Appeal Tribunal ruling suggests otherwise. It held that the withdrawal of a conditional job offer amounted to a breach of contract, even though the employee had not actually started work, and that the financial consequences can be significant.

The case of Kankanalapalli v Loesche Energy Systems Ltd is a timely reminder that a job offer, even one labelled “conditional”, can amount to a binding contract the moment a candidate accepts it.

What happened?

A candidate was offered a role as a project manager, subject to satisfactory references, a right to work check, and successful completion of a six-month probationary period. The offer letter referred to key terms such as salary and a start date, but it did not mention a notice period. The employer also agreed to contribute towards relocation costs.

The candidate accepted the offer by email and completed the new-starter paperwork, including providing referee details and the required right to work documents.

Advertisement

A few weeks later, the employer withdrew the job offer because of delays in the project. The candidate brought a claim for breach of contract, citing the withdrawal of the offer and failure to pay any notice pay.

What did the Employment Tribunal and EAT decide?

The Employment Tribunal dismissed the claim. It held that the job offer was conditional and that the employer had not yet received references or completed the right to work checks (which required original documents). The contract had therefore not been formed.

The EAT disagreed. The key question was the nature of the conditions attached to the offer and whether they were:

“Conditions precedent”, that is, conditions that must be satisfied before any contract is formed) or

“Conditions subsequent”: whereby acceptance of an offer gives rise to a binding contract, but if the conditions are not satisfied, the contract terminates.

The conditions were grouped together in the offer letter, and one (passing the probationary period) could only be satisfied after employment began. As there had been no attempt to differentiate between the different conditions, this prevented the EAT from finding that they could be conditions precedent.

The offer letter included the key terms, both parties had treated the contract as binding, and the employer had started the onboarding process. Consequently, the employer did not have an unrestricted right to withdraw the offer for reasons unrelated to the conditions subsequent.

Advertisement

Finally, as the offer letter was silent on notice, the EAT had to imply a reasonable notice period. Taking into account the role’s seniority, the relocation requirement, and the lengthy interview process, it was concluded that three months’ notice would be a reasonable period, which the employer was required to pay.

What does this mean for your business?

The case highlights several practical steps employers should take when making job offers:

Labelling an offer “conditional” is not enough on its own and will not prevent a binding contract from forming or a breach of contract if the job offer is withdrawn. If you intend certain conditions to be met before a contract exists, those conditions need to be clearly spelled out, with pre-contract conditions listed separately from post-start conditions, such as probation.

Always include a notice period in the offer letter, covering both the probationary period and the post-probation standard notice period after probation has been successfully completed. If you don’t, the Employment Tribunal will imply one, and it may be longer than you’d expect.

Before withdrawing any offer, take legal advice to ascertain whether the job offer was conditional or unconditional. Depending on the seniority of the role and the implied or stated notice period, a successful breach of contract claim can mean significant compensation as well as considerable management time.

Finally, it’s worth reviewing your current offer letter templates to ensure key terms are included and that the conditional nature of any offer is clearly and correctly expressed.

A little extra care at the offer stage is far less costly than defending a claim if a job offer is withdrawn.

Hannah Waterworth

Hannah Waterworth is an employment solicitor in Blake Morgan’s Employment, Pensions, Benefits and Immigration team.

NEW YORK — Meta Platforms Inc. shares rose modestly to $600.22 in midday trading Tuesday, up 0.23% or $1.36, as investors continued digesting the social media giant’s aggressive artificial intelligence investments and robust advertising performance following its strong first-quarter 2026 earnings report. The modest gain comes amid broader market caution but underscores ongoing confidence in Meta’s ability to monetize AI across its family of apps despite significantly higher capital spending forecasts.

The stock has traded in a wide range this year, pulling back from 2025 highs near $796 after the company raised its 2026 capital expenditure guidance to $125 billion-$145 billion to fuel AI infrastructure buildout. Yet Meta’s core advertising business remains exceptionally resilient, with Q1 revenue hitting a record $56.31 billion, up 33% year-over-year and beating analyst expectations.

Adjusted earnings per share reached $10.44 in the quarter, driven partly by a large one-time tax benefit, while core operational performance stayed solid. Daily active users across Meta’s platforms exceeded 3.4 billion, highlighting the company’s unmatched global reach even as it navigates regulatory and competitive pressures.

AI Push Dominates Narrative

CEO Mark Zuckerberg has made clear that 2026 and beyond represent a major acceleration in Meta’s AI ambitions. The company is heavily investing in custom silicon, data centers and foundational models to power everything from ad targeting to content recommendations and new consumer experiences like advanced Meta AI assistants.

Advertisement

Higher capex has weighed on sentiment in recent weeks, with some investors worried about near-term margin pressure and free cash flow. However, analysts largely view the spending as necessary groundwork for long-term leadership in AI-driven advertising and consumer applications. Meta aims to fully automate much of its ad creation process by the end of 2026, allowing businesses to generate campaigns with minimal input while dramatically improving performance.

Google Cloud and other partnerships, along with internal tools like Andromeda ad retrieval and generative models, are already delivering measurable lifts in ad efficiency and relevance. Advertisers using Meta’s latest AI features have reported double-digit improvements in return on ad spend.

Advertising Resilience Remains Key Driver

Despite macroeconomic uncertainty and geopolitical tensions, Meta’s advertising revenue continues to grow strongly. The company benefits from its massive user base across Facebook, Instagram, WhatsApp and Threads, combined with sophisticated AI targeting that helps advertisers reach the right audiences efficiently.

Reels and short-form video continue expanding, while Threads has solidified its position as a viable Twitter/X alternative. Management has expressed confidence in sustained ad market recovery and further gains from AI optimization throughout 2026.

Advertisement

Valuation and Analyst Views

At current levels around $600, Meta trades at a forward price-to-earnings multiple in the mid-20s, which many analysts consider reasonable given projected growth. Consensus price targets cluster between $650 and $750, with several firms maintaining Buy ratings and citing AI as a multi-year tailwind.

Longer-term forecasts remain bullish. Some projections see Meta shares potentially reaching $1,000-$1,250 within five years if AI monetization accelerates and margins stabilize after the current investment cycle.

Risks and Challenges

Investors remain watchful of several headwinds. Regulatory scrutiny in Europe and the U.S. over youth safety and data practices could lead to fines or product changes. Increased competition in AI from OpenAI, Google and others, along with potential moderation in advertiser spending, also pose risks.

Workforce reductions and efficiency efforts continue as Meta balances heavy AI spending with cost discipline. The company has warned of possible material impacts from ongoing legal and regulatory matters.

Advertisement

Technical Outlook

Meta stock has shown resilience after the post-earnings dip in late April. Support levels sit near $570-$580, with resistance around recent highs near $620-$650. Volume on Tuesday remained moderate, suggesting the modest gain reflects steady accumulation rather than aggressive buying.

Broader Context

Meta’s performance fits within the larger AI investment theme dominating technology markets in 2026. While heavy infrastructure costs create short-term pressure, the company’s ability to integrate AI deeply into its core advertising engine and consumer products positions it favorably for sustained growth.

As summer trading approaches, focus will shift to second-quarter results and any updates on AI product launches or ad automation progress. Meta’s diversified revenue streams and massive user engagement give it durability that few peers can match.

For investors, today’s slight uptick reflects continued faith in Meta’s long-term vision despite the elevated spending required to realize it. Whether the stock can sustain momentum will depend on execution in AI and advertising efficiency in the quarters ahead.

Advertisement

With a market capitalization exceeding $1.5 trillion and a proven ability to adapt, Meta remains one of the most important technology companies shaping the future of social media, advertising and artificial intelligence.

NEW YORK — Apple Inc. (NASDAQ: AAPL) shares rose modestly to $293.84 in midday trading Tuesday, up 0.40% or $1.16, as investors continued rewarding the tech giant’s strong fiscal second-quarter 2026 performance and aggressive capital return program. The stock has climbed steadily since its April 30 earnings beat, trading near recent highs and reflecting confidence in Apple’s iPhone momentum, record services growth and accelerating artificial intelligence strategy.

Apple reported fiscal Q2 revenue of $111.2 billion, up 16.6% year-over-year, and earnings per share of $2.01, both surpassing Wall Street forecasts. iPhone sales surged 22% to $57 billion, marking the strongest March quarter in company history. Services revenue reached a record $30.98 billion, while gross margin expanded to an all-time high of 49.3%. The board authorized a massive $100 billion share repurchase program and raised the quarterly dividend to $0.27 per share.

The results triggered a strong post-earnings rally, with shares jumping nearly 4% in early May trading. Tuesday’s modest advance extends that positive momentum, even as broader market caution lingers over geopolitical risks and elevated valuations across big tech. Apple’s market capitalization remains above $4.3 trillion, cementing its position as one of the world’s most valuable companies.

CEO Transition and AI Focus

Apple also announced a major leadership change: hardware engineering chief John Ternus will succeed Tim Cook as CEO on September 1, 2026, with Cook transitioning to executive chairman. The smooth succession plan has been well-received by investors, providing continuity while signaling fresh energy as Apple ramps up its artificial intelligence efforts.

Advertisement

R&D spending climbed to a record $11.4 billion in the quarter, representing over 10% of revenue as the company accelerates investments in on-device AI, generative models and new hardware features. Analysts expect AI enhancements in iOS 19, Siri upgrades and future iPhone models to drive the next growth cycle. Wedbush’s Dan Ives has highlighted the “AI opportunity” as a multi-year catalyst, recently raising his price target to a Street-high $400.

iPhone 18 Anticipation Builds

Attention is shifting toward the iPhone 18 lineup expected in September 2026. Supply chain reports suggest Apple is holding pricing steady despite rising memory costs tied to AI demand, while preparing significant camera, display and AI performance upgrades. Stronger-than-expected iPhone 17 demand in the March quarter has fueled optimism that the next generation could sustain double-digit growth.

Services remain a high-margin growth engine, with Apple Music, iCloud, App Store and AppleCare continuing to scale globally. Greater China revenue rebounded strongly, up more than 28% year-over-year, signaling stabilization in a key market.

Analyst Sentiment and Valuation

Wall Street remains overwhelmingly bullish. Consensus price targets cluster between $325 and $400, with recent upgrades from BofA, Goldman Sachs and others citing sustained iPhone strength, services expansion and AI upside. The stock trades at a forward P/E around 33-35, which many view as reasonable given Apple’s consistent execution and massive cash generation.

Advertisement

Technical analysts note Apple has cleared key resistance levels and is forming higher highs. Support sits near $280-$285, with resistance around recent highs near $294-$300. The $100 billion buyback program is expected to provide ongoing tailwinds by reducing share count and supporting the price.

Risks and Challenges

Investors remain attentive to several headwinds. Regulatory scrutiny in the EU and U.S., potential China tensions, and a competitive AI landscape could create volatility. Rising R&D and capex commitments may pressure near-term margins, though management has guided for continued gross margin strength in the mid-to-high 47% range.

Broader market dynamics, including interest rates and geopolitical developments, also influence sentiment. However, Apple’s resilient business model — blending premium hardware with high-margin services and an expanding ecosystem — has historically weathered economic uncertainty well.

Outlook for Remainder of 2026

With the WWDC 2026 developer conference approaching in June, excitement is building around new AI features and software updates. Management has guided for mid-teens revenue growth in the current quarter, setting up a potentially strong back half of the year centered on iPhone 18 momentum.

Advertisement

For long-term investors, today’s modest gain reflects steady accumulation in a fundamentally strong name. Apple’s combination of record profitability, massive capital returns and clear AI roadmap keeps it among the most important holdings in technology portfolios. As the company navigates its leadership transition and invests heavily for the future, Wall Street largely expects continued outperformance.

As midday trading continued Tuesday, AAPL held near session highs with solid volume. The coming weeks will bring more color on AI progress, iPhone demand trends and capital allocation priorities. For now, Apple’s ability to deliver consistent beats and shareholder returns reinforces its status as a blue-chip growth powerhouse even at elevated valuations.

The tech titan remains a core holding for many, with 2026 shaping up as another pivotal year driven by innovation, services expansion and artificial intelligence integration across its ecosystem.

NEW YORK — Microsoft Corp. (NASDAQ: MSFT) shares climbed modestly to $409.01 in midday trading Tuesday, up 0.88%, as investors digested the software giant’s robust fiscal third-quarter 2026 results and continued optimism around its artificial intelligence and cloud leadership despite elevated capital spending. The move comes after a period of consolidation, with the stock rebounding from recent lows amid broader tech sector rotation.

Microsoft reported fiscal Q3 revenue of $82.9 billion, up 18% year-over-year and beating analyst expectations of roughly $81.4 billion. Adjusted earnings per share reached $4.27, exceeding forecasts of $4.06. Intelligent Cloud revenue jumped 30% to $34.7 billion, driven by Azure growth of 40% (39% constant currency). Productivity and Business Processes rose 17%, while More Personal Computing was roughly flat.

CEO Satya Nadella highlighted AI momentum, noting the company’s AI business has surpassed a $37 billion annual revenue run rate. Azure AI services and Copilot adoption continue accelerating across enterprise customers, with strong uptake in both commercial and consumer segments.

Heavy AI Investments Fuel Long-Term Bets

Microsoft guided for full-year capital expenditures around $190 billion in calendar 2026, driven primarily by AI data center buildout and infrastructure needs. While the spending level has raised near-term margin concerns for some investors, analysts largely view it as necessary infrastructure for sustained leadership in cloud and AI.

Advertisement

The company’s deepened partnership with OpenAI remains central. Recent updates to the commercial agreement, including revenue share caps, have been interpreted positively as both companies prepare for potential future monetization at scale. Microsoft also continues expanding its own AI models and tools across Azure, Microsoft 365 and GitHub.

Analyst Optimism Remains High

Wall Street consensus on Microsoft stays strongly bullish. Recent price target increases have pushed the average well above $500, with several firms citing 50-60% upside potential over the next 12-18 months. Key drivers include Azure’s market share gains, Copilot monetization progress, and long-term AI infrastructure returns.

The stock trades at a forward price-to-earnings multiple in the mid-20s, which many consider attractive relative to growth projections. Microsoft’s diversified business — spanning cloud, productivity software, gaming, LinkedIn and consumer products — provides resilience that few peers match.

Technical Picture and Market Context

MSFT has shown resilience after pulling back from 2025 highs near $555. Support levels sit near $390-$400, with resistance around recent swing highs near $420-$430. Tuesday’s modest gain occurred on solid volume, reflecting steady institutional buying amid broader market caution tied to geopolitical tensions and oil prices.

Advertisement

Year-to-date performance has lagged some megacap peers due to heavy AI spending, but recent rebound signals renewed investor confidence. Short interest remains manageable, limiting squeeze risk but keeping the name active among retail traders.

Strategic Position in AI Era

Microsoft’s early and substantial investment in OpenAI, combined with its Azure infrastructure, positions it uniquely in the AI value chain. The company is integrating AI deeply across its product portfolio — from Copilot in Office apps to GitHub Copilot for developers and consumer-facing tools. Enterprise adoption metrics remain strong, with commercial bookings and backlog providing multi-year visibility.

Nadella has emphasized “agentic AI” — autonomous systems capable of complex tasks — as the next major wave. Microsoft is investing aggressively to lead in this area while maintaining strong relationships with customers wary of single-vendor dependency.

Risks and Challenges Ahead

Investors remain mindful of execution risks on massive capex plans, potential slowdowns in hyperscaler spending, and intensifying competition in AI from Google, Amazon and emerging players. Regulatory scrutiny in Europe and antitrust matters in the U.S. also represent ongoing overhangs.

Advertisement

However, Microsoft’s balance sheet strength, consistent cash flow generation and history of disciplined capital allocation provide a significant buffer. The company returned over $10 billion to shareholders through dividends and buybacks in the quarter alone.

Outlook for Remainder of 2026

With fiscal Q4 results expected in late July, focus will turn to Azure growth sustainability, Copilot monetization updates and any commentary on 2027 guidance. Analysts project continued double-digit revenue growth, with AI contributing an increasingly visible portion of results.

For long-term investors, today’s modest advance reflects confidence in Microsoft’s foundational role in enterprise AI and cloud computing. While short-term volatility tied to spending concerns or market rotations is likely, the company’s competitive moats and execution track record keep it among the most favored megacap technology names.

As midday trading continued Tuesday, MSFT held near session highs with steady buying interest. The coming weeks will bring more AI conference updates, industry events and economic data that could influence sentiment. For now, Microsoft’s ability to deliver consistent beats while investing for the future reinforces its status as a core holding in growth portfolios.

Advertisement

The tech powerhouse remains at the center of the artificial intelligence transformation, balancing near-term spending pressures with powerful long-term tailwinds in cloud, productivity and AI services.

TUCSON, Ariz. — Pima County Sheriff Chris Nanos vowed Tuesday that the investigation into the suspected abduction of 84-year-old Nancy Guthrie will not go cold, offering the strongest public assurance yet that authorities remain actively pursuing leads as the case reached the painful 100-day milestone without an arrest or confirmed proof of life. The mother of NBC “Today” co-anchor Savannah Guthrie vanished from her Catalina Foothills home north of Tucson on the night of Jan. 31, 2026, in what officials describe as a targeted kidnapping.

“This case will not go cold,” Nanos said firmly in a recent interview. “We will resolve it.” The sheriff reiterated that investigators are making progress and described recent developments as “really great,” though he declined to provide specifics to protect the integrity of the ongoing probe. His comments come amid mounting public frustration, criticism of the investigation’s pace, and growing pressure on his leadership.

Nancy Guthrie was last seen around 9:45 p.m. on Jan. 31 after a family member dropped her off following dinner. She was reported missing the next day around noon. Security footage captured a masked, armed individual tampering with her Ring doorbell camera shortly before she disappeared. Blood confirmed to be hers was found on the doorstep, and her phone, purse and critical medications were left inside the home.

Family’s Heartbreaking Plea on Mother’s Day

On Mother’s Day, Savannah Guthrie shared an emotional Instagram tribute featuring decades of family photos and videos. “Mother, daughter, sister, Nonie — we miss you with our every breath,” she wrote. “We will never stop looking for you. We will never be at peace until we find you.” The post renewed calls for tips and highlighted the $1.2 million reward, including $1 million from the family, for information leading to her mother’s safe return.

Advertisement

A mysterious note left at a makeshift memorial near the home added another layer of intrigue. It read in part, “Your Mom would be ashamed if she knew what you did… TAKE NANCY HOME.” Authorities have not confirmed any connection to the case.

DNA Evidence and Forensic Focus

Investigators continue processing DNA from gloves recovered near the home, with advanced testing underway at both local and FBI laboratories. Officials have described the evidence as promising but have not publicly identified any suspects or persons of interest. Human remains discovered nearby were confirmed to be prehistoric and unrelated. Purported ransom demands in Bitcoin surfaced early but their authenticity remains unverified.

The sheriff’s task force, working closely with the FBI, has reviewed thousands of tips and hours of footage. Nanos has pushed back against criticism, including comments from FBI Director Kash Patel questioning the initial handling, insisting coordination has been strong and progress is being made behind the scenes.

Expert Analysis and Investigation Challenges

Retired FBI profilers have described the kidnapping as unusually sophisticated for a random crime, citing the targeted disabling of security systems. Some experts believe the lack of frequent public updates is a deliberate strategy to avoid tipping off the perpetrator. Others note that major cases often move methodically, with breakthroughs coming after prolonged quiet work.

Advertisement

The case has captivated national attention, blending celebrity interest with the universal fear of losing an elderly loved one. It has spotlighted vulnerabilities for seniors living alone and prompted renewed discussions about home security in affluent suburbs. Extreme summer heat in Arizona raises additional concerns for any potential search efforts or Nancy Guthrie’s well-being if she remains alive.

Public Appeals and Reward

Authorities urge anyone with information — no matter how small — to contact the FBI at 1-800-CALL-FBI, the Pima County Sheriff’s Department at 520-351-4900, or submit tips anonymously. The reward remains fully available and does not require public identification.

Despite the 100-day mark, Nanos and his team reject any notion that momentum has slowed. “Every day they get closer,” he said, emphasizing continued collaboration with multiple agencies. Local leaders have raised questions about the sheriff’s handling, with some pushing for accountability, but the investigation remains active and ongoing.

For the Guthrie family, every passing day deepens the anguish while strengthening their resolve. Savannah Guthrie’s public pleas underscore a simple message: someone knows something that could bring Nancy home. The abduction has already altered Hollywood’s polished image of swift crime-solving, reminding the public that real investigations can stretch for months or years.

Advertisement

As day 101 begins, Sheriff Nanos’s vow offers a flicker of hope amid uncertainty. Whether recent developments lead to a breakthrough or the case tests the limits of patience and resources remains to be seen. For now, Tucson and the nation continue watching, hoping the next development brings answers rather than another painful milestone.

The sheriff’s determination sends a clear message: Nancy Guthrie’s disappearance has not been forgotten, and law enforcement will not rest until the case is solved.

The £100m plans include a new hydrogen powered furnace at 7 Steel in Cardiff

14:36, 12 May 2026Updated 15:46, 12 May 2026

7 Steel’s Cardiff plant.(Image: Robert Mills Photography Ltd)

Owners of Cardiff-based steel maker 7 Steel have confirmed £100m investment plans.

The investment, up to 2030, includes £30m for a new hydrogen-ready furnace, which would be the first large scale industrial application of hydrogen in steel manufacturing in the UK.

Advertisement

Czech investment company Sev.en Global Investments acquired the business from Spanish firm Celsa last year. The business makes steel from scrap steel through its electric arc furnace mill operation.

The £100m investment also covers plant upgrades, technology improvements and wider operational development.

The new furnace will be operational next year but will not initially be using hydrogen.

The Cardiff plant, which also serves as the firm’s UK headquarters, recycles domestic scrap into low-carbon steel for construction, infrastructure, transport and energy projects. Its products, such as rebar and mesh, have gone into some of the UK’s most recognisable buildings and infrastructure, including The Shard, Wembley Stadium, the Heathrow Terminal 5 extension, Hinkley Point C nuclear power station and rail’s HS2.

Advertisement

The investment arrives at an important moment for British steel. The UK Government, which is nationalising the last remaining heavy steelmaking plant in Scunthorpe, has set out plans to build 1.5 million new homes and upgrade infrastructure, both of which will require significant volumes of steel. Sev.en GI says the new policy direction reinforces its case for long-term investment in the sector.

Alan Svoboda, chief executive of Sev.en Global Investments, said: “As the long-term owners of 7 Steel UK, we recognise the strategic importance of a robust independent British steel sector.”

“Steel is a strategic industrial opportunity which requires continuity and a willingness to invest through the cycle. That is exactly how we invest.”

Beyond capital investment, Sev.en GI has said it is committed to the workforce. 7 Steel UK pays 1.5 times the UK median salary and continues to train the next generation of engineers, helping to keep skilled industrial jobs in Cardiff and across the UK.

Advertisement

7 Steel employs over 1,600 people across the UK, with 1,050 based in Wales, of which 800 are in Cardiff. It has 14 sites including four fabricator sites in Neath, Newport, Crumlin, and Whiteheads in Newport, which employ 250. The Cardiff site produces more than one million tonnes of steel a year, making it the UK’s third biggest steel producer.

The operation in the Tremorfa area of Cardiff has been owned and operated by some of the biggest names in British industry such as Guest Keen & Nettlefolds (GKN) before becoming British Steel in 1970.

The blast furnace side of the operations closed in 1978 with the remaining works going through a variety of owners. Previous owners Celsa acquired it in 2003.

Key Manchester Airport link could boost links across the North West and Yorkshire

Declan Carey and Local Democracy Reporter

16:00, 12 May 2026

A small piece of HS2 in Greater Manchester is being resurrected – and it could unlock a wave of future transport improvements across the north.

Advertisement

When former Tory Prime Minister Rishi Sunak confirmed that the northern leg of HS2 was all but dead in late 2023, it sparked huge backlash and frustration.

The move, announced during the Conservative Party conference being held in Manchester at the time, killed hopes of a faster train link from Greater Manchester to London.

Mr Sunak told Tory conference in October 2023: “I say to those who backed the project in the first place, the facts have changed and the right thing to do when the facts change is to have the courage to change direction.

“I am ending this long-running saga. I am cancelling the rest of the HS2 project and in its place, we will reinvest every single penny – £36 billion – in hundreds of new transport projects in the North and the Midlands.”

Advertisement

But now one small section of HS2 in the north – which includes a link between Manchester Airport and Manchester Piccadilly station – is being brought back.

It forms part of the High Speed Rail (Crewe – Manchester) Bill, relating to phase 2b of HS2, which is being ‘repurposed’ with a focus on improving rail connections across the north.

The move is expected to feature in the King’s speech on Wednesday, which sets out the new laws being planned by the government.

Creating the new link in Greater Manchester is a crucial part of wider transport plans across the north, insiders say, and would pave the way for a new Manchester to Liverpool line in phase two of the £45 billion Northern Powerhouse Rail programme.

Advertisement

One source described a new Manchester Airport to Piccadilly connection as the ‘key part’ of the future Manchester to Liverpool connection – a piece of the puzzle which is ‘non-negotiable’ and needs to happen to unlock the rest of the project.

So the High Speed Rail (Crewe – Manchester) Bill featuring in the King’s speech on Wednesday could signal a major step forward for a raft of planned railway improvements in northern England.

Henri Murison, chief executive of the Northern Powerhouse Partnership, told the Local Democracy Reporting Service: “We’re expecting there may be good news on Wednesday, this is critical because it will enable not just to be connected to Manchester city centre as part of the wider Manchester-Liverpool scheme, but also will in the end connect Yorkshire better to the airport.”

It’s understood that the government decided to repurpose the current High Speed Rail (Crewe – Manchester) Bill rather than creating a new one to save the time and money that has already been put into the plan.

Advertisement

Transport secretary Heidi Alexander outlined the plan in Parliament in February.

She told MPs that the High Speed Rail (Crewe – Manchester) Bill ‘has been refined’ with a new purpose, and that the Bill itself is the ‘mechanism by which planning consent for the eastern part of the new route between Liverpool and Manchester can be granted.’

She added: “The Bill will have the necessary powers to deliver the section of Northern Powerhouse Rail into Manchester via Manchester airport, including new stations at Manchester Piccadilly and Manchester airport itself.

“We are now seeking to progress the Bill to make the best use of the significant progress it has already made.”

Advertisement

A new Manchester-Liverpool railway line has long been touted as essential to boosting connectivity across the north, as well as keeping the economy in good health.

The plan for a Manchester-Liverpool route could cut journey times between the north west’s two biggest cities to as little as 35 minutes, alongside increasing the number and frequency of trains – something Andy Burnham previously said could turn Piccadilly Station into the ‘King’s Cross of the North’.

Part of the wider project includes plans for an underground Piccadilly station. As Greater Manchester Mayor Andy Burnham said at the start of this year: “Finally, we have a government with an ambitious vision for the North, firm commitment to Northern Powerhouse Rail and an openness to an underground station in Manchester city centre.

Advertisement

“Today marks a significant step forward for Greater Manchester. We’ll now work at pace to prove the case for an underground station and work up detailed designs for the route between Liverpool and Manchester.”

The transport secretary said of the High Speed Rail (Crewe – Manchester) Bill in February that it is ‘important to crack on and get it done’ given the wider ambitions for the north of England.

This small section of HS2 in Greater Manchester set to be resurrected in the King’s speech on Wednesday could be the key to unlock it all.

You must be logged in to post a comment Login