Business

Perth Racing teams up with SEN

The UAE leaving Opec is seen as a major blow and potential death knell for the oil cartel.

Business

Varun Beverages shares jump 9% in 3 days. Why Jefferies, Motilal, and others are bullish after Q4 results?

The recent rally follows the company’s Q1 CY2026 earnings announced on Monday. Varun Beverages reported a 20.1% rise in consolidated net profit to Rs 878.71 crore for the quarter, compared with Rs 731 crore in the same period last year.

For the quarter under review, the company’s revenue from operations rose 18.1% to Rs 6,574 crore, compared to Rs 5,567 crore in the same period last year.

EBITDA rose 21% to Rs 1,528.93 crore in Q1 CY2026 from Rs 1,263.96 crore in Q1 CY2025. EBITDA margin improved by 55 basis points to 23.3% during the quarter. In India, EBITDA margin expanded by 112 basis points, supported by operational efficiencies from strong volume growth and better gross margins.

Consolidated sales volume grew 16.3% to 363.4 million cases in Q1 CY2026 from 312.4 million cases in Q1 CY2025, driven by strong volume growth of 14.4% in India and 21.4% in international markets.

Jefferies on Varun Beverages

With a Buy rating and target price of Rs 615, the global brokerage said Varun Beverages delivered a strong quarter, with volume growth of more than 14% in India and stable margins, a positive outcome amid concerns over rising competition from Campa. The international business also posted a broad-based and healthy performance.

The brokerage added that the summer season has begun on a strong note and will be a key driver for growth going forward, while a favourable base is also supporting momentum. Management remains unfazed by increasing competition, particularly from Campa.

Lower discounts and efficiency gains, including benefits from new plants, are expected to support margins ahead. On international margins, Varun Beverages holds raw material inventory for six months, providing good visibility. In India, the company has sufficient inventory for the second quarter and is partly covered for the third quarter. Any additional cost impact is likely to be offset through lower discounts and cost-control measures.

Motilal Oswal on Varun Beverages stock

The domestic brokerage has maintained its Buy rating on Varun Beverages with a target price of Rs 600, implying a potential upside of 16%. Analysts expect the company to see stronger earnings momentum, supported by an extreme heatwave this year due to El Niño, which could boost peak summer demand.

It also sees growth driven by a scale-up in international operations, led by South Africa and a recovery in the Zimbabwe market. In India, improving on-ground execution is expected to further support performance.

Motilal Oswal also highlighted the scale-up of the snacking business, backed by the operationalisation of the Morocco and Zimbabwe markets in the second half of CY2025. In addition, the company’s expanding product portfolio, including the recent launch of the energy drink ‘Adrenaline Rush’, is expected to aid future growth.

JM Financial on Varun Beverages shares

With a target of Rs 600, JM forecasts 16% upside. Management is optimistic about India’s volume trajectory and margin resilience. VBL management remained upbeat about the outlook for the coming quarters, too. It expects India’s volume momentum to sustain, given the favourable summer season this time (a healthy consumption trend visible in April).

In terms of raw materials, the company is well covered for the upcoming season. As a result, it does not expect any material impact on overall margins and can offset likely pressure on India margins through lower discounts and cost efficiencies. Hence, margin resilience is likely to continue, which is quite commendable, it added.

(Disclaimer: Recommendations, suggestions, views and opinions given by the experts are their own. These do not represent the views of The Economic Times)

Experts says Claire’s suffered from a perfect storm of issues which has spelled the end for the accessories chain.

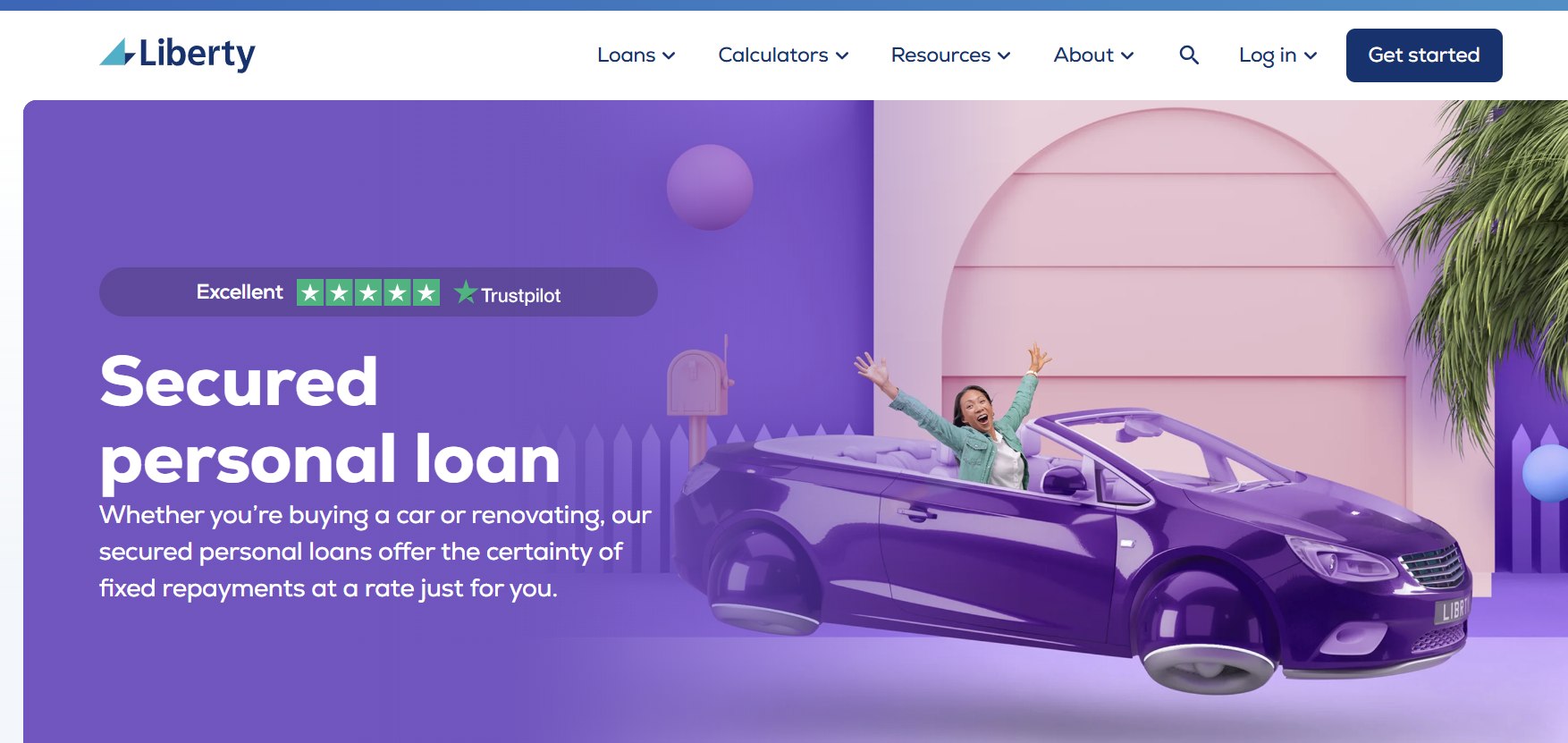

SYDNEY — Australians seeking personal loans in 2026 have more competitive options than ever, with leading lenders offering rates as low as 5.67% p.a. as the Reserve Bank of Australia’s easing cycle and strong competition drive down borrowing costs amid ongoing cost-of-living pressures.

As of late April 2026, comparison websites show unsecured personal loan rates starting from 5.76% p.a., while secured and green loans dip even lower. Borrowers can access funds for debt consolidation, home renovations, vehicles, weddings or travel, with many lenders offering fast online approvals and flexible terms of one to seven years.

Here are the 10 best personal loan options currently available in Australia, ranked primarily by starting comparison rates for excellent credit profiles (rates are indicative and subject to individual assessment):

- Liberty Financial Secured Personal Loan — Starting from 5.67% p.a. (comparison rate around 6.10% p.a.). This secured option offers competitive rates for borrowers using assets as collateral, with loan amounts up to significant limits and terms suited for larger purchases.

- Harmoney Unsecured Personal Loan — From 5.76% p.a. (comparison rate 5.76% p.a. for excellent credit). A fully online lender with personalised rates, no ongoing fees for many customers and quick funding. Popular for its transparency and borrower-friendly features.

- OurMoneyMarket (OMM) Low Rate Personal Loan — From 5.95% p.a. (comparison rate 5.95% p.a.). Strong option for exceptional credit, with flexible terms up to seven years and no application or monthly fees in many cases. Good for home improvements or vehicle loans.

- NOW Finance No Fee Personal Loan — From 5.95% p.a. (comparison rate 5.95% p.a.). Zero fees on many secured and unsecured products, making it attractive for cost-conscious borrowers seeking simplicity.

- Plenti Personal Loan — From 6.17% p.a. Competitive rates with a focus on responsible lending and green finance options. Strong customer service ratings.

- ING Fixed Rate Personal Loan — From around 6.19% p.a. A well-regarded bank option with fixed rates for payment certainty and solid digital application process.

- G&C Mutual Bank or Unity Bank Green Upgrades Loan — From as low as 4.59%–5.55% p.a. for eligible energy-efficient projects when secured against a home loan. Excellent for sustainability-focused borrowers.

- Latitude Personal Loan — Variable and fixed options with competitive mid-tier rates. Good for those seeking additional features like repayment flexibility.

- Westpac or CommBank Personal Loans — Starting from around 5.99%–7.25% p.a. for strong credit customers. Big-bank security with branch support, though often higher comparison rates due to fees.

- NAB or ANZ Personal Loans — Competitive tiered rates from major banks, suitable for existing customers who can access discounts and integrated banking benefits.

Key Considerations for Borrowers in 2026Comparison rates are crucial as they include fees and give a truer picture of total cost. Always check your personalised rate, as offers vary significantly based on credit score, income and loan purpose. Unsecured loans generally carry higher rates than secured ones but require no collateral.

Application processes have become faster, with many lenders offering same-day or next-day funding via fully digital platforms. However, approval depends on responsible lending assessments, including income verification and debt-to-income ratios. Borrowers with excellent credit (typically 700+ scores) secure the lowest advertised rates.

Current economic conditions favour borrowers. With the cash rate stabilised or easing, lenders compete aggressively for market share. Green loans and EV-related financing often qualify for discounts, aligning with Australia’s sustainability push. Debt consolidation remains a popular use case as households manage higher living costs.

Expert Advice Financial comparison sites such as Canstar, Finder, InfoChoice and Money.com.au recommend shopping around and using pre-approval tools that perform soft credit checks. Consider total loan cost over the full term rather than just the headline rate. Early repayment without penalties is a valuable feature offered by most non-bank lenders.

Experts also stress budgeting: calculate repayments carefully using online calculators and avoid borrowing more than necessary. Government resources and financial counsellors can help if debt is already an issue. Always read the product disclosure statement and understand exit fees, redraw options and insurance add-ons.

Risks and Responsible Lending While low rates are attractive, personal loans add to household debt. The average unsecured personal loan rate sits around 10.3% p.a., so advertised low rates are reserved for top-tier borrowers. Missed payments can damage credit scores and lead to higher future borrowing costs.

The Australian Securities and Investments Commission and lenders follow strict responsible lending rules. Borrow only what you can comfortably repay. Tools like the National Consumer Credit Protection Act safeguards help protect consumers.

Looking Ahead Personal loan rates in Australia are expected to remain competitive through 2026 if inflation stays controlled. New digital lenders and fintech innovations may further drive down costs and improve customer experience. Green and purpose-specific loans are likely to expand as environmental priorities grow.

For many Australians, a well-chosen personal loan offers a smarter alternative to credit cards with their higher interest rates. By comparing options thoroughly and matching the product to individual needs, borrowers can secure favourable terms in today’s market. Always consult a licensed financial adviser for personalised guidance.

With rates starting in the low 5% range for strong applicants, 2026 presents solid opportunities for those needing flexible financing. Research, compare and apply responsibly to make the most of current conditions.

The lurid purple shopfronts that ushered a generation of British teenagers into their first ear piercing have, quite literally, gone dark.

Claire’s Accessories has confirmed the closure of all 154 of its standalone stores in the UK and Ireland, with more than 1,300 staff handed redundancy notices in one of the most emphatic high-street collapses of the year so far.

Administrators at Kroll said trading ceased across the estate on 27 April after the chain tumbled into administration for the second time in barely twelve months. The 350 concession counters that Claire’s operates inside other retailers will continue to trade for now, but the standalone model, for decades a fixture of British shopping centres from Bluewater to Buchanan Galleries, is finished.

For the SME-heavy ecosystem of suppliers, landlords and shopping-centre operators that depend on anchor tenants of this kind, the implications are sobering. Claire’s was not a marginal player: it was, until recently, one of the most reliably trafficked footfall generators on any mid-tier high street, hoovering up pocket money from a demographic that few competitors knew how to reach.

That demographic, it turns out, has moved on. The chain has been outflanked on price by the Chinese-owned ultra-fast-fashion platforms Shein and Temu, whose algorithmically curated trinkets land on teenagers’ doorsteps for a fraction of Claire’s shelf prices. It has been squeezed on the high street itself by Primark and Superdrug, both of which have aggressively expanded their value accessories ranges. And, perhaps most damaging of all, it has been culturally outmanoeuvred.

“We’ve moved away from novelty, colourful jewellery for the most part, which is what Claire’s are best known for,” Priya Raj, a fashion analyst, told the BBC. Today’s teenagers, she noted, take their cues from TikTok and Instagram rather than from a Saturday-afternoon trawl of the local Arndale, and their tastes have shifted to “minimal jewellery, sometimes chunky, sometimes with a more curated look, basically not the cutesy, juvenile look that Claire’s is known for.”

The retail analyst Catherine Shuttleworth was blunter still. Gen Alpha, she argued, has more competing claims on its disposable income than any cohort before it — matcha lattes, bubble tea, gourmet desserts, in-app purchases, and a shop “just selling ‘stuff’ simply doesn’t cut it” any longer.

The collapse will reignite the increasingly fractious debate over the Government’s tax treatment of bricks-and-mortar retail. When Claire’s owner, the private-equity backed Modella Capital, first put the chain into administration in January, it pointed to “alarming” Christmas trading and singled out the rise in employers’ National Insurance Contributions as a material drag on viability. Trade bodies including the British Retail Consortium and the Federation of Small Businesses have warned for months that the cumulative weight of higher NICs, business rates and the National Living Wage uplift is pushing marginal store-by-store economics into the red — a warning that Claire’s now embodies in unusually stark form.

The structural picture is no kinder. Town centre footfall has yet to return convincingly to pre-pandemic levels, the Treasury’s long-promised business rates overhaul has under-delivered, and landlords are still struggling to re-let space vacated by the likes of Wilko, The Body Shop and Ted Baker. A 154-unit hole in the property market is not one that will be filled overnight.

Across the Atlantic, the picture is little better. The American arm of the business filed for Chapter 11 in 2025, its second bankruptcy in seven years, after an earlier failure in 2018 — underlining that Claire’s troubles are global rather than peculiarly British.

What was once a rite of passage has become a case study in how quickly retail brands can be rendered obsolete when consumer culture, cost inflation and online disruption converge on the same balance sheet. The bright purple frontages will be gone within weeks. The questions they leave behind for Britain’s high streets will not.

Seeking Alpha’s transcripts team is responsible for the development of all of our transcript-related projects. We currently publish thousands of quarterly earnings calls per quarter on our site and are continuing to grow and expand our coverage. The purpose of this profile is to allow us to share with our readers new transcript-related developments. Thanks, SA Transcripts Team

Golf WA chief executive Arron Minchin says the state governing body intends to continue working closely with on-course and off-course golf facility owners to maximise participation.

New products include Maíz tortillas and sourdough style tortillas.

OPINION: WA plays a critical role in the national ecosystem of industry, infrastructure and personnel supporting the nation’s defence.

Peak XV sold around 60.8 lakh shares, representing nearly 7.7% equity in the company, at an average price of Rs 214 per share, the source said. The price is at a 4.88% discount to the previous closing price of Rs 225 on the BSE.

Investment firms Florintree Advisors, Viridian Asset Management, Dymon Asia and Karma Capital were among the buyers in the deal, the news report stated. Peak XV had been an early institutional investor in One MobiKwik, and the latest transaction marks its complete exit from the fintech company, the source added.

Shares of One MobiKwik Systems rallied as much as 8% to their day’s high of Rs 243 on the BSE on Tuesday, extending gains for a second consecutive session and rallying 20% over the same period.

The sharp surge in One MobiKwik share price comes after the company announced that the Reserve Bank of India (RBI) has approved its application for a Non-Banking Financial Company (NBFC) licence, marking a key milestone in its efforts to strengthen its financial services business.

The licence will allow the launch of a new lending arm, MobiKwik Financial Services Private Limited (MFSPL), a wholly owned subsidiary of the group. Through this entity, the company plans to expand its regulated lending capabilities, introduce innovative credit products, and serve a wider base of consumers and merchants with greater efficiency and control.

The development is in line with the group’s long-term strategy of building a full-stack fintech platform focused on accessible, responsible and technology-driven financial products.The NBFC will build on the group’s existing strengths, including a customer base of more than 186 million users, a trusted brand, and strong technology infrastructure along with risk underwriting and collections capabilities.

MFSPL, the group’s in-house NBFC, is expected to help launch new credit products with faster go-to-market execution, offering both secured and unsecured lending solutions to consumers and MSMEs in underserved geographies. Operations will begin after receipt of the Certificate of Registration (CoR) from the RBI upon fulfilment of certain conditions.

(Disclaimer: Recommendations, suggestions, views and opinions given by the experts are their own. These do not represent the views of The Economic Times)

Supreme Court Hears Case On How To Label Risks of Popular Weed Killer

‘Noise and nuisance’ concerns as former bank could become 24-hour gaming centre

United Arab Emirates to quit oil cartel Opec

Manchester United reach agreement with Casemiro over contract clause amid transfer speculation

US brings back mandatory military draft registration

Steven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread – Corporette.com

-

Tech21 hours ago

Tech21 hours agoRegister Renaming | Hackaday

-

Crypto World3 days ago

Crypto World3 days agoHyperliquid $HYPE Rally Builds Momentum as AI Sector Enters Prove-It Phase

-

Politics6 days ago

Politics6 days agoMaking troops accountable for war crimes threatens US alliance, ex-SAS colonel warns

-

Politics6 days ago

Politics6 days agoDisabled people challenge government SEND proposals over segregation concerns

-

Business5 days ago

Business5 days agoPatterson-UTI Energy, Inc. (PTEN) Q1 2026 Earnings Call Transcript

-

Business6 days ago

Business6 days agoRolls-Royce Voted UK’s Most Iconic Trade Mark as IPO Register Hits 150

-

Sports2 days ago

Sports2 days agoIPL 2026: Ruturaj Gaikwad registers slowest fifty of the season, enters all-time unwanted list | Cricket News

-

Crypto World7 days ago

Crypto World7 days agoNew York sues Coinbase, Gemini over prediction market offerings

-

Politics17 hours ago

Politics17 hours agoDrax board avoid their own AGM, accused of greenwashing & environmental racism

-

Politics6 days ago

Politics6 days agoStarmer handler McSweeney to be dragged from shadows by Foreign Affairs Committee

-

Politics6 days ago

Politics6 days agoZack Polanski responds to home secretary’s taser threat

-

Politics6 days ago

Wings Over Scotland | How To Get Away With Crimes

-

Business6 days ago

Business6 days agoHCL Tech share price tank over 9% after weak Q4. JPMorgan, HSBC & 3 others cut target price

-

Crypto World7 days ago

Crypto World7 days agoCrypto’s great hope in Senate’s Clarity Act still has a path to survive tight calendar

-

Politics6 days ago

Politics6 days ago‘Iran is still a nuclear threat’

-

Sports5 days ago

Sports5 days agoTim Bradley names the current best in the world: “Better than Inoue and Usyk”

-

NewsBeat2 days ago

NewsBeat2 days agoLK Bennett closes all stores after entering administration

-

Crypto World4 days ago

Crypto World4 days agoMichael Saylor says BTC winter is over. Market analyst disagrees, says bitcoin was in a pullback

-

Crypto World7 days ago

Crypto World7 days agoEthereum Price News: ETH Flashes a Bullish Setup No Holder Should Miss While Pepeto Nears Its Binance Listing

You must be logged in to post a comment Login