Business

Recent MSG Shows Highlight Gothic Spectacle

NEW YORK — Lady Gaga continues to dominate the pop landscape in 2026, delivering theatrical highs on her ongoing **Mayhem Ball** tour while teasing future projects that keep fans buzzing. The 14-time Grammy winner’s latest North American dates, including back-to-back performances at Madison Square Garden on March 19 and 20, 2026, drew rapturous reviews for their cinematic staging, emotional depth and vocal prowess.

The March 20 MSG show, part of the expanded leg announced last year, featured Gaga at her gothic best. Reviewers described it as a “gothic opera” with acts titled “And She Fell Into A Gothic Dream” and “The Beautiful Nightmare That Knows Her Name.” Fans wept during poignant moments, as Gaga blended hits from her 2025 album *Mayhem* with catalog staples like “Paparazzi” and “Lovegame.” The production included elaborate costumes, dramatic lighting and narrative arcs that evoked a dark fairy tale, solidifying her reputation as a live performer at her peak.

The tour, supporting *Mayhem* — which earned her Best Pop Vocal Album at the 2026 Grammys — kicked off in 2025 and has spanned Asia, Europe, North America and Oceania. Recent extensions added multiple nights in cities like Atlanta (March 4-5), Austin (March 8-9), Miami (March 13) and Washington, D.C. (March 23-24). Upcoming stops include Boston’s TD Garden on March 29, Montreal’s Bell Centre on April 2, Saint Paul on April 9 and a final New York run concluding April 13 at Madison Square Garden.

Gaga’s Grammy night earlier this year added to the momentum. She performed a rock-infused version of “Abracadabra” — which won Best Dance Pop Recording — despite nearly canceling due to the tight schedule after Japan dates. She also took home Best Pop Vocal Album for *Mayhem*. The performance, featuring archival Alexander McQueen pieces in memory of Lee McQueen, showcased her collaboration with producers Andrew Watt and Cirkut, plus drummer Josh Freese.

A trademark dispute over “Mayhem” resolved in her favor in late 2025, allowing uninterrupted use for the album, tour and merchandise. A federal court denied a preliminary injunction from surf brand Lost International, affirming artistic expression rights.

Beyond the stage, Gaga’s team confirmed development of a “very bombastic” large-scale project slated for 2026 release. Details remain confidential, fueling speculation about new music, a film or multimedia endeavor. Fans also anticipate a concert film from the Mayhem Ball, with reports of professional filming during her February 2026 Los Angeles Kia Forum run. Director Sam Wrench is reportedly involved, following a streaming bidding war. The project could capture the tour’s spectacle for global audiences later this year.

Gaga’s personal style continues to influence trends. She revived her signature hair bow in a coquette twist during Japan prep videos, pulling platinum blonde locks back with a black accessory that echoed her 2010s era while feeling fresh.

The tour’s success builds on her post-pandemic resurgence, including the Chromatica Ball in 2022 and recent awards recognition. With more than 1.3 million fans already served across 87 dates, the Mayhem Ball demonstrates her enduring draw. Upcoming shows promise continued innovation, blending pop anthems with theatrical storytelling.

As Gaga wraps the North American leg in April, attention turns to what follows — potentially a new era hinted at by her team. For now, Little Monsters savor the mayhem, with tickets for remaining dates moving fast via Live Nation and Ticketmaster.

In a career defined by reinvention, 2026 finds Lady Gaga thriving: commanding arenas, collecting Grammys and plotting her next bold move.

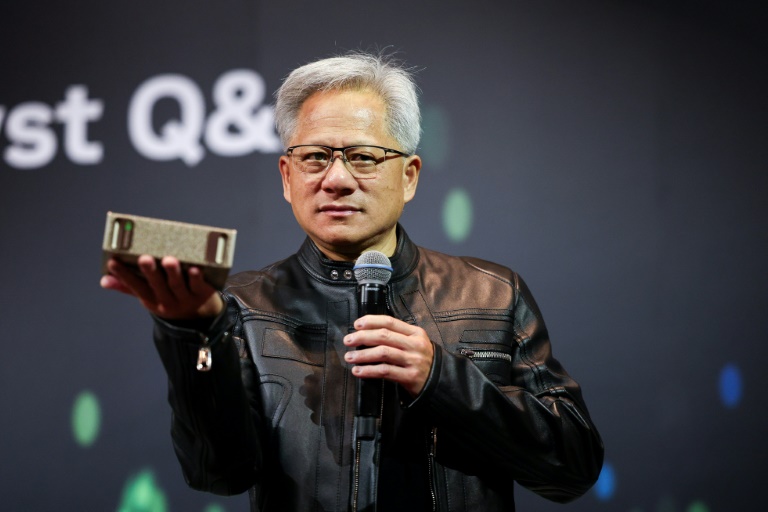

NEW YORK — Nvidia Corp. enters the heart of 2026 as one of the market’s most compelling stories, with Wall Street analysts overwhelmingly recommending investors buy shares amid explosive artificial intelligence demand, robust earnings growth and a dominant position in data center chips that shows few signs of slowing. The semiconductor giant’s stock has delivered extraordinary returns in recent years, but questions linger about valuation sustainability and potential headwinds in a rapidly evolving tech landscape.

Trading recently around $200 per share after earlier volatility, Nvidia commands a market capitalization exceeding $4 trillion, reflecting its pivotal role in powering the AI revolution. Analysts tracking the company issue predominantly “Buy” ratings, with consensus price targets clustering near $270, suggesting meaningful upside potential through year-end and beyond. Strong Buy recommendations from over half of covering firms underscore confidence in continued leadership.

Earnings Momentum and AI Tailwinds Drive Bull Case

Nvidia’s fiscal results highlight why optimism prevails. Recent quarterly reports showed revenue and earnings growth far outpacing broader markets, fueled by insatiable demand for its GPUs used in training and inference for large language models. Data center revenue has surged, offsetting any softness in gaming or automotive segments.

Chief Executive Jensen Huang has positioned the company at the forefront of accelerated computing, with new architectures like Blackwell generating excitement. Partnerships with major cloud providers and hyperscalers ensure a robust order backlog, while software ecosystems such as CUDA create significant switching costs for competitors.

Projections for 2026 call for revenue exceeding $100 billion, with earnings per share growth supporting premium valuations. Analysts forecast continued expansion in AI infrastructure spending, even as some question the pace of adoption. Energy demands and infrastructure constraints represent risks, but Nvidia’s diversification into networking, software and potentially sovereign AI initiatives provides buffers.

Valuation Debate Centers on Growth Sustainability

At current multiples, Nvidia trades at a premium reflecting its growth profile. Bulls argue the valuation remains reasonable given earnings trajectory and market dominance. Forward price-to-earnings ratios, while elevated, align with historical tech leaders during transformative periods.

Skeptics point to concentration risks, potential AI spending slowdowns and geopolitical tensions affecting supply chains. China restrictions and export controls have already impacted results, though domestic demand and alternative markets mitigate effects. Competition from AMD, Intel and custom chip efforts by hyperscalers could erode margins over time.

Despite these concerns, the consensus leans bullish. Average price targets imply 30-35% upside, with optimistic forecasts reaching higher on successful product cycles. Long-term models project substantial growth if AI permeates enterprises, autonomous systems and scientific computing.

Investor Strategies for Nvidia Exposure

For those considering buying Nvidia stock in 2026, a long-term horizon suits best. Dollar-cost averaging helps navigate volatility while capturing compounding gains from innovation. Portfolio allocation should remain disciplined, perhaps limiting single-stock exposure given sector concentration.

Growth-oriented investors view Nvidia as a core holding in technology and AI themes. Dividend initiation, though modest, signals maturing capital return policies. Technical analysis shows support levels during pullbacks, offering entry points for opportunistic buyers.

Sellers or those on the sidelines cite rich valuations and mean-reversion risks. Profit-taking after multi-year runs makes sense for some, particularly if broader market corrections loom. Short-term traders monitor earnings beats, guidance and macroeconomic data closely.

Diversification across semiconductors, cloud computing or broader tech ETFs provides balanced AI exposure without single-company risk. Options strategies or leveraged vehicles suit sophisticated investors comfortable with amplified volatility.

Competitive Landscape and Innovation Pipeline

Nvidia maintains clear leadership in high-performance GPUs, but the field evolves quickly. AMD’s MI series chips gain traction, while custom silicon from Google, Amazon and others targets specific workloads. Open-source alternatives and software optimizations could democratize access, pressuring pricing power.

Nvidia counters with full-stack solutions encompassing hardware, software and services. CUDA’s ecosystem lock-in, combined with rapid iteration on new architectures, sustains moats. Ventures into robotics, autonomous vehicles and enterprise software broaden the addressable market.

Geopolitical factors add complexity. U.S.-China tensions influence export policies, prompting Nvidia to develop compliant products while expanding in friendly markets. Supply chain resilience and manufacturing partnerships with TSMC remain critical.

Macroeconomic and Sector Influences

Broader economic conditions shape Nvidia’s prospects. Interest rates, inflation and corporate spending on technology influence AI investment appetite. Recession fears could delay projects, while robust growth accelerates adoption.

The semiconductor cycle historically features booms and busts, but AI represents a structural shift potentially insulating leaders like Nvidia. Energy constraints and regulatory scrutiny around data centers introduce new variables.

Investor sentiment swings with quarterly results and forward guidance. Positive surprises on margins or new verticals tend to catalyze rallies, while any softening in data center demand triggers selloffs.

Risks and Considerations for 2026

Key risks include execution misses on new products, intensified competition or AI hype deflation. Valuation compression could occur if growth moderates. Geopolitical escalation or supply disruptions pose additional threats.

Opportunity lies in sustained AI tailwinds, successful diversification and market share gains. Nvidia’s balance sheet strength and free cash flow generation provide flexibility for acquisitions, R&D and shareholder returns.

Final Thoughts on Investment Decision

Nvidia stock in 2026 presents a compelling case for buyers convinced of AI’s transformative potential. The company’s technological edge and execution track record support optimism, though high expectations leave limited margin for disappointment.

Investors should conduct thorough due diligence, assess personal risk tolerance and consider professional advice. No single stock guarantees success, but Nvidia embodies the innovation driving modern markets. As the year progresses, earnings reports and product announcements will provide fresh data points for buy, hold or sell evaluations.

The semiconductor leader’s journey reflects broader tech evolution, where bold bets on future computing paradigms can yield outsized rewards. For those aligned with its vision, 2026 may offer continued participation in one of the era’s defining investment themes.

GEELONG, Australia — The Geelong Cats delivered a commanding performance against North Melbourne in their Round 8 AFL 2026 encounter at GMHBA Stadium on May 2, showcasing superior skill, physicality and forward pressure to secure a significant victory over the Kangaroos. The Cats’ clinical finishing and midfield dominance proved too much for a North Melbourne side still searching for consistency in the early season.

Geelong controlled proceedings from the opening bounce, utilizing strong contested marking and slick ball movement to generate scoring opportunities. North Melbourne battled valiantly with moments of flair, particularly through their young forward line, but ultimately couldn’t match the Cats’ experience and structural cohesion across four quarters.

Match Summary and Key Stats

Geelong built an early lead through efficient use of the forward 50, converting opportunities with accuracy that North struggled to replicate. The Cats’ midfield brigade, led by standout performers, won the clearance battle and provided constant supply to dangerous marking targets.

By halftime, Geelong held a substantial advantage, forcing North Melbourne into a defensive posture. The third quarter saw the Kangaroos mount a brief challenge with quick transitions and clever play, but Geelong responded with a decisive burst that effectively sealed the result.

Final scores reflected Geelong’s superiority in key metrics: higher disposal counts, better efficiency inside forward 50 and stronger tackling pressure. North Melbourne’s efforts in contested situations showed promise but lacked the polish needed against a top-four contender.

Individual highlights included multiple goal contributions from Geelong’s key forwards and midfielders who accumulated high disposals. North’s young stars showed glimpses of potential with strong marking and creative disposals, offering hope for their campaign despite the loss.

Tactical Battle and Coaching Insights

Geelong coach Chris Scott’s game plan emphasized midfield control and defensive structure, limiting North’s transition game. The Cats’ ability to switch play and exploit space created mismatches that North’s defense couldn’t consistently cover.

North Melbourne coach Alastair Clarkson, in his ongoing rebuild, focused on youth development and contested ball wins. While the Kangaroos competed physically, execution in critical moments let them down. Post-match, Clarkson likely emphasized learning from Geelong’s professionalism while building confidence in his group.

The match highlighted AFL trends toward high-possession football and defensive setups that reward precise kicking. Geelong’s execution in this style proved superior on the day.

Season Context for Both Clubs

For Geelong, the win reinforces their status as premiership contenders in 2026. Consistent performances across the home-and-away season position them well for finals, with key players hitting form at the right time. Depth across the list allows rotation and management of workloads effectively.

North Melbourne continues its development phase. Early season results show improvement in patches but highlight areas needing refinement, particularly in converting opportunities and sustaining pressure. The Kangaroos’ youth movement offers long-term promise, with several emerging talents gaining valuable experience against established sides.

The result impacts ladder standings, with Geelong maintaining pressure on top teams while North seeks to climb from lower rungs through improved consistency.

Fan Atmosphere and Community Impact

GMHBA Stadium buzzed with typical Cats home support, creating an intimidating environment for visitors. Geelong fans celebrated the comprehensive display, while traveling North Melbourne supporters appreciated their side’s fight despite the scoreboard.

The match drew strong attendance, underscoring AFL’s community roots in regional Victoria. Local businesses and hospitality venues benefited from the influx, highlighting sport’s economic role in Geelong.

Post-match interactions between players and fans reflected the code’s accessible nature, with autographs and photos boosting morale on both sides.

Injury and Team News Updates

Both teams managed selections carefully. Geelong monitored key personnel for fatigue, while North integrated younger players into the senior setup. Post-match injury reports will influence upcoming preparations, with minor niggles common after physical contests.

Geelong’s medical staff will assess workloads ahead of the next fixture, aiming to keep stars fresh for the demanding middle stretch of the season. North focuses on recovery and tactical review to address defensive lapses.

Looking Ahead in AFL 2026

Geelong eyes continued momentum with favorable matchups on the horizon. Maintaining form away from home will test their credentials as genuine flag hopefuls.

North Melbourne targets winnable games to build belief. Incremental improvements in structure and execution could yield better results against similar opposition.

The round’s other results shape the broader ladder picture, with tight contests defining the competition’s competitiveness. As the season progresses, every point and percentage becomes crucial.

Geelong’s Round 8 victory over North Melbourne exemplifies the blend of talent, strategy and execution required for success in modern AFL. The Cats advance confidently while the Kangaroos regroup, both sides contributing to another memorable chapter in league history. Fans eagerly anticipate the next round as the 2026 premiership race intensifies.

Business

Kuwait International Airport Resumes Operations After Closure as Regional Tensions Ease in 2026

KUWAIT CITY — Kuwait International Airport partially reopened this week following a two-month closure triggered by regional conflicts, marking a significant step toward restoring normal air travel in the Gulf nation as limited commercial flights resumed from Terminals 4 and 5 starting late April. The phased reopening brings relief to travelers and businesses after airspace suspension that disrupted thousands of journeys amid heightened security concerns.

The Directorate General of Civil Aviation announced the gradual return to operations after Kuwait’s airspace reopened on April 23. Kuwait Airways and Jazeera Airways began limited services on April 26 from dedicated terminals, initially operating during specific hours to selected destinations. Authorities emphasize safety and a cautious ramp-up as full capacity restoration continues.

Background of the Closure

The airport shut down commercial passenger flights in late February 2026 due to escalating tensions involving Iran and broader Middle East instability. Missile threats and security risks prompted the precautionary measure, affecting regional connectivity and forcing rerouting through alternative hubs like Dubai and Doha.

The closure impacted Kuwait’s economy, aviation sector and residents reliant on international travel for business, family visits and medical needs. Cargo operations faced delays, while expatriate communities experienced extended separations. Airlines incurred substantial losses from canceled flights and repositioning aircraft.

Phased Reopening Details

Initial operations focus on Terminals 4 and 5, handling a fraction of previous capacity with around 40 daily flights split between arrivals and departures. Kuwait Airways resumed select routes, prioritizing safety protocols and coordination with international partners. Jazeera Airways, the low-cost carrier, transitioned operations back to Terminal 5 for efficiency.

Travelers should expect limited schedules, potential delays and strict security measures during the early phase. Airlines advise checking updates frequently as routes expand gradually. Terminal 1 remains under review for repairs and full reactivation.

Passengers with existing bookings received notifications for rebooking or refunds where necessary. Travel insurance claims surged during the closure period, highlighting the importance of comprehensive coverage for regional trips.

Economic and Regional Impact

Aviation contributes significantly to Kuwait’s diversification efforts beyond oil. The airport serves as a gateway for business, tourism and labor mobility in the Gulf. Reopening supports recovery in hospitality, retail and logistics sectors affected by reduced passenger traffic.

Regionally, the development aligns with stabilizing airspace across neighboring countries. Coordinated efforts among Gulf states aim to restore connectivity while maintaining heightened security. The event underscores aviation’s vulnerability to geopolitical events and the need for resilient infrastructure.

Traveler Advice and Precautions

Authorities recommend confirming flight status directly with airlines before heading to the airport. Arrive earlier than usual due to enhanced screening procedures. Carry essential documents, including visas and health certificates where required for destinations.

For those with upcoming travel, flexible booking options and insurance provide protection against future disruptions. Apps and airline websites offer real-time updates on schedules and terminal information. Ground transportation and hotel transfers may require adjustments during the transition period.

Expatriates and visitors welcomed the news, easing concerns over family reunions and business continuity. Kuwaiti officials expressed commitment to full operational restoration as conditions permit.

Future Outlook for Kuwait Aviation

Long-term plans include modernization of facilities and expansion to handle growing demand. Terminal 2 projects, though delayed, aim to boost capacity significantly in coming years. Investments in technology and sustainability position Kuwait as a potential regional hub.

The incident highlights broader challenges facing Gulf aviation, from geopolitical risks to infrastructure demands. Collaboration with international bodies ensures compliance with global safety standards during recovery.

As operations normalize, focus shifts to rebuilding passenger confidence and expanding route networks. Successful phased reopening could serve as a model for other nations facing similar disruptions.

Kuwait International Airport’s return to service represents hope amid uncertainty, reconnecting families, facilitating commerce and reaffirming the nation’s role in regional connectivity. Travelers and aviation professionals monitor developments closely as full operations resume in the coming weeks.

Iran offers Strait deal; Trump dissatisfied but prefers non-military path

Americans on a budget mourn loss of low-cost Spirit Airlines

MELBOURNE — Early counting in the Nepean state by-election on May 2, 2026, showed Liberal candidate Anthony Marsh leading independent Tracee Hutchison as voters in the marginal Mornington Peninsula seat chose a successor to resigned MP Sam Groth. Polling stations across the district closed in the afternoon, with results trickling in throughout the evening in a contest that tested local priorities and major party strategies.

The Victorian Electoral Commission reported steady turnout as residents cast ballots at 13 polling places. With preferences still being distributed, officials cautioned that final outcomes could take time, but initial figures pointed to a competitive race in the traditionally Liberal-leaning electorate.

Campaign Focused on Local Concerns

The short by-election campaign centered on peninsula-specific issues, including coastal management, housing affordability and infrastructure demands from population growth. Marsh, the Mornington Peninsula Shire mayor, emphasized community representation and practical governance during his campaign.

Hutchison positioned herself as an independent voice, highlighting environmental protection and decision-making transparency. Candidates from One Nation, Greens and other minor parties added further options, addressing topics from cost of living to cannabis reform.

Labor’s decision not to contest the seat shifted dynamics, potentially directing preferences toward independents or Liberals. The choice drew analysis about opposition tactics in contests where victory appeared challenging.

Preliminary Results and Counting Process

As counting progressed at the main tally room, Marsh held an edge in primary votes, performing strongly in western and eastern booths. Hutchison attracted support in southern areas, appealing to voters seeking alternatives to major parties.

Preference flows from eliminated candidates will determine the two-candidate preferred result. The commission expected clearer indications by late Saturday or early Sunday, though close margins could extend the process.

Officials urged patience as formal verification continued. The by-election, called after Groth’s February resignation, offered an early gauge of sentiment in a key Victorian district.

Historical Background of the Seat

Nepean has changed hands between Liberal and Labor in recent cycles, reflecting its marginal status. The electorate includes affluent coastal communities, expanding suburbs and rural pockets, creating diverse voter bases with varied priorities.

Previous contests featured tight races influenced by broader state trends. The by-election continued the tradition of local issues often taking precedence over partisan narratives.

Voter Priorities Emerge

Cost of living, particularly energy prices and housing, featured prominently in discussions with families and retirees. Infrastructure projects, including road upgrades and public transport, drew attention amid growth pressures.

Environmental concerns around unique ecosystems influenced some voters. Community services and planning decisions also resonated in local forums.

Turnout patterns varied, with higher participation in established areas. Weather and timing as an autumn Saturday influenced accessibility for some residents.

Reactions from Candidates and Parties

Marsh thanked supporters while awaiting fuller counts, stressing commitment to local issues. Hutchison expressed gratitude for backing an independent voice and vowed continued advocacy.

Liberal leader John Pesutto monitored developments, viewing the seat as important for opposition strength. Premier Jacinta Allan focused on government priorities while respecting the democratic process.

Minor parties used the platform to highlight policies, aiming to build profiles for future contests.

Potential Implications for Victorian Politics

Though one seat, the by-election provides insights into voter mood in marginal areas. Results could inform strategic planning for major parties ahead of the next general election.

The independent challenge reflects interest in non-major options in regional Victoria. Preference flows and minor party performances offer data for studying shifting allegiances.

As counting continues, observers watch for clues about broader trends. The outcome, whether a Liberal hold or tighter result, will shape political narratives in coming months.

Smooth Electoral Process

The Victorian Electoral Commission oversaw polling with standard measures for accessibility and safety. Results reporting used modern technology while maintaining verification standards.

Voters received clear candidate information through commission materials. The process upheld Australia’s democratic traditions with high integrity.

Looking Ahead After the By-Election

Attention will turn to how parties interpret the result for future campaigns. Nepean’s voters contributed their voices to Victoria’s political conversation.

Candidates and parties will reflect on effectiveness and voter messages. The by-election adds another chapter to the state’s electoral history.

Polling day in Nepean passed without major incident, allowing the democratic process to unfold. Victorians await official outcomes as the 2026 calendar advances.

NEW YORK — Intel Corp. stock presents a complex investment case in 2026, with analysts divided on whether to buy or sell shares of the semiconductor giant as it pursues a high-stakes turnaround amid fierce competition and shifting industry dynamics. The company, once a dominant force in chips, faces questions about its ability to regain ground in foundry services and data center markets while navigating significant financial and operational challenges.

AFP

Trading recently near $100 after a notable rally earlier in the year, Intel shares reflect cautious optimism around restructuring efforts and potential AI-related opportunities. However, Wall Street’s consensus “Hold” rating and average price targets around $65 to $80 suggest many see limited upside or even downside from current levels. The wide range of forecasts — from as low as $30 to highs near $120 — highlights deep uncertainty surrounding the company’s path forward.

Recent Performance and Turnaround Efforts

Intel reported encouraging signs in early 2026 quarters, with revenue stabilization and progress on cost-cutting initiatives. Leadership under CEO Pat Gelsinger emphasized foundry ambitions, aiming to compete with TSMC through advanced process technologies and U.S.-based manufacturing investments.

Government support through the CHIPS Act provided billions in funding for domestic fabs, bolstering long-term prospects. Intel’s 18A process node, targeted for 2025 production, generated excitement as a potential game-changer for custom chips and external customers.

Yet execution risks remain high. Delays in process technology historically plagued Intel, eroding market share to AMD and others in CPUs. Foundry losses continued weighing on margins, prompting aggressive cost reductions including layoffs and asset reviews.

Analyst Perspectives Split

Wall Street views range widely. Bulls point to Intel’s engineering talent, diversified portfolio and potential recovery in PC and server markets. Some forecast substantial upside if foundry wins materialize and AI demand spills over.

Bears highlight persistent losses, high capital expenditures and competition from Nvidia in accelerators. Valuation concerns persist despite the stock’s pullback from peaks, with many arguing the company trades at a premium to its current fundamentals.

Consensus among 41 analysts tracked by major services leans “Hold,” with a handful of buy ratings and scattered sells. Average targets imply downside from recent prices, reflecting skepticism about near-term profitability.

Key Factors for 2026 Outlook

Several catalysts could influence Intel’s trajectory. Success with 18A and securing major foundry customers would validate the strategy, potentially boosting revenue and margins. PC market recovery and enterprise spending on AI infrastructure offer tailwinds.

Risks include further process delays, foundry customer acquisition challenges and macroeconomic pressures on semiconductor demand. Geopolitical tensions and supply chain issues add uncertainty.

Intel’s balance sheet strength provides runway for investments, but sustained losses could pressure credit ratings and investor confidence. Dividend sustainability remains a focus for income-oriented shareholders.

Investment Considerations

For buyers, Intel represents a contrarian bet on a storied American tech name executing a complex pivot. Long-term investors comfortable with volatility may see value if turnaround milestones hit. Dollar-cost averaging mitigates timing risks.

Sellers or those avoiding the stock cite better opportunities in peers with stronger moats and clearer growth paths. Nvidia’s AI dominance and AMD’s CPU gains highlight competitive pressures. Diversification across semiconductors reduces single-company exposure.

Short-term traders monitor quarterly results, guidance and industry events closely. Technical levels and sentiment shifts drive near-term moves in a volatile name.

Broader Semiconductor Industry Context

Intel operates within a dynamic sector. AI spending fuels demand for advanced chips, benefiting leaders but pressuring laggards. Foundry competition intensifies as nations invest in domestic manufacturing for security reasons.

U.S. policy support through subsidies aids Intel but invites scrutiny over execution. Global supply chains remain vulnerable to disruptions, affecting all players.

Intel’s challenges mirror industry-wide transitions toward specialized computing and advanced packaging. Success depends on adapting faster than rivals while controlling costs.

Company History and Strategic Shift

Founded in 1968, Intel pioneered microprocessors that powered the PC revolution. Decades of dominance gave way to stumbles in mobile and process technology, allowing competitors to gain ground.

The current strategy under Gelsinger focuses on regaining process leadership and building a major foundry business. IDM 2.0 combines internal manufacturing with external partnerships, aiming for resilience and growth.

Progress remains uneven, with promising technology roadmaps tempered by financial losses. The coming years will test whether Intel can reclaim its former glory or settle into a diminished role.

Final Thoughts on Buy or Sell Decision

Intel stock in 2026 suits risk-tolerant investors betting on successful execution of a complex turnaround. The company’s legacy, talent and policy support provide foundations, but competition and history warrant caution.

Thorough due diligence, including review of quarterly updates and industry trends, is essential. Professional advice helps align decisions with individual goals and risk profiles.

No outcome is guaranteed in the fast-moving semiconductor sector. Intel’s journey reflects broader challenges and opportunities in American technology manufacturing. For those convinced of its potential, current levels may offer entry into a storied name’s next chapter.

As 2026 progresses, Intel’s ability to deliver on promises will determine whether bulls or bears prevail in one of the market’s most closely watched recoveries.

NEW YORK — Investors weighing Samsung Electronics against Taiwan Semiconductor Manufacturing Co. (TSMC) in 2026 face a classic semiconductor showdown: TSMC’s ironclad dominance in advanced foundry services fueled by insatiable AI demand versus Samsung’s aggressive multibillion-dollar gamble to close the gap through massive capital spending and memory leadership. While most Wall Street analysts favor TSMC as the clearer buy for its technological moat and consistent growth, Samsung’s $73 billion semiconductor investment plan offers higher-risk, higher-reward upside for those betting on a foundry turnaround.

TSMC extended its market-share lead in 2025, capturing nearly 70 percent of the global foundry business with $122.5 billion in revenue, up 36 percent year-over-year. Samsung trailed far behind at 7.2 percent with $12.6 billion, a 3.9 percent sales decline that widened the gap to 62.7 percentage points. The disparity underscores TSMC’s stranglehold on cutting-edge nodes demanded by Nvidia, Apple and other AI heavyweights.

TSMC’s AI Tailwinds Drive Analyst Optimism

Analysts overwhelmingly rate TSMC a Buy, with consensus price targets clustering around $400–$450 and projections calling for 20–30 percent revenue growth in 2026. Strong demand for 3-nanometer and 2-nanometer processes, coupled with advanced packaging like CoWoS, positions the Taiwanese giant as the indispensable enabler of the AI boom. Bernstein named TSMC its top pick, forecasting sustained double-digit expansion through 2027.

TSMC’s focused business model—pure-play foundry without competing against customers—delivers superior margins and predictability. Its $45 billion-plus capital-expenditure plan for 2026 targets capacity expansion in high-margin AI chips, insulating it from broader memory cycles that plague diversified players. Geopolitical risks tied to Taiwan remain a concern, yet U.S. subsidies and global diversification efforts mitigate some exposure.

Valuation reflects quality: TSMC trades at a premium yet remains attractive relative to growth prospects. Dividend yield hovers around 1.5–2 percent with a sustainable payout, appealing to long-term holders seeking stability in a volatile sector.

Samsung’s Massive Bet Seeks to Narrow the Gap

Samsung counters with the industry’s largest single-year semiconductor outlay: more than $73 billion in 2026 targeting memory, foundry and R&D. The South Korean giant aims to ramp HBM4 production, accelerate its SF2 and SF4 processes and bring its Texas fab online for risk production later this year. Executives expressed confidence in winning more advanced-logic customers as yields improve.

Samsung’s memory business—especially high-bandwidth memory—provides a buffer TSMC lacks, with recent HBM4 customer approvals sparking share gains. Yet its foundry division remains a distant second, struggling with yield consistency and customer acquisition. Analysts see 2026 as a pivotal year for profitability targets in the contract-manufacturing arm.

Samsung stock carries a Buy consensus from limited coverage, with price targets suggesting 20–30 percent upside from recent levels. Shares trade at lower multiples than TSMC, reflecting cyclical exposure and execution risks. The conglomerate structure, spanning consumer electronics and appliances, adds diversification but dilutes focus compared with TSMC’s laser-sharp foundry strategy.

Key Comparison Factors for Investors

Market Position and Technology: TSMC leads at the bleeding edge with proven 3nm and upcoming 2nm yields. Samsung undercuts on pricing but lags in advanced-node reliability, though heavy investment could narrow that deficit by 2027.

Growth Drivers: TSMC rides pure AI demand from hyperscalers. Samsung benefits from AI memory tailwinds plus potential foundry share gains if hyperscalers diversify away from Taiwan-centric risk.

Risk Profile: TSMC offers lower volatility and stronger moats. Samsung faces greater cyclical swings in memory pricing and geopolitical diversification pressure on both firms.

Valuation and Returns: TSMC commands a premium justified by execution track record and visibility. Samsung appears cheaper but demands patience on turnaround milestones.

Broader Industry Context

The foundry market is projected to exceed $360 billion in 2026, driven by AI chips and advanced packaging. TSMC and Samsung together control over 75 percent of pure-play capacity, leaving Intel and smaller players fighting for scraps. Global chip demand remains robust despite macroeconomic uncertainty, with AI spending providing structural support.

Strategic Considerations for 2026 Buyers

Long-term believers in AI infrastructure should lean toward TSMC for its proven ability to capture high-margin growth with minimal competition at the leading edge. Patient investors comfortable with execution risk may favor Samsung for its aggressive spending and potential to reclaim share in a diversifying supply chain.

Portfolio construction matters. Many advisors recommend both names for balanced semiconductor exposure, with TSMC as the core holding and Samsung as a satellite bet on memory and foundry recovery. Dollar-cost averaging mitigates timing risks in a sector prone to sharp swings.

Neither stock is without challenges. TSMC must navigate U.S.-China tensions and capacity constraints, while Samsung must deliver on yield and customer wins to justify its capital binge. Currency fluctuations (won versus dollar) and regional politics add layers for international investors.

Final Outlook

As 2026 unfolds, TSMC enters as the consensus favorite—stable, dominant and directly tied to the AI supercycle. Samsung’s $73 billion war chest creates intriguing optionality for those willing to endure volatility in pursuit of catch-up gains. The choice ultimately hinges on risk tolerance: TSMC for quality growth, Samsung for value and turnaround potential.

Investors should monitor quarterly results closely. TSMC’s March and June reports will detail AI momentum, while Samsung’s updates on HBM4 and Texas fab progress will signal whether its massive bet is paying off. In a market where advanced chips power everything from data centers to smartphones, both giants remain essential—but TSMC currently holds the clearer edge for most portfolios.

Trump rallies seniors in Florida as Republicans face tough elections

Airlines scramble to help stranded Spirit passengers after budget carrier collapses

6 Vikings Camp Battles to Watch This Summer

Space data centers sound like a pipe dream. What if we put them on lamp posts?

Swinney ‘very concerned’ by reports of BP considering leaving North Sea

Manchester United reach agreement with Casemiro over contract clause amid transfer speculation

US brings back mandatory military draft registration

Steven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Tech5 days ago

Tech5 days agoRegister Renaming | Hackaday

-

Crypto World7 days ago

Crypto World7 days agoHyperliquid $HYPE Rally Builds Momentum as AI Sector Enters Prove-It Phase

-

Politics5 days ago

Politics5 days agoDrax board avoid their own AGM, accused of greenwashing & environmental racism

-

Tech5 days ago

Tech5 days agoWhy Blue Badges Disappeared From Toyota Hybrids

-

Tech5 days ago

Tech5 days agoImages of Samsung’s rumored smart glasses have leaked

-

Sports6 days ago

Sports6 days agoIPL 2026: Ruturaj Gaikwad registers slowest fifty of the season, enters all-time unwanted list | Cricket News

-

Tech24 hours ago

Tech24 hours agoTrump’s 25% EU auto tariff breaches Turnberry Agreement that also covers semiconductors and digital trade

-

NewsBeat6 days ago

NewsBeat6 days agoLK Bennett closes all stores after entering administration

-

Fashion4 days ago

Fashion4 days agoKylie Jenner’s KHY Enters a New Era with ‘Born in LA’

-

Business4 days ago

Business4 days agoMost Commercial Energy Audits Miss the Real Losses

-

Crypto World4 days ago

Crypto World4 days agoCFTC’s AI will review U.S. crypto registration applications, chairman tells CoinDesk

-

Business5 days ago

Business5 days ago(VIDEO) Charlize Theron Climbs Times Square Billboard to Promote New Netflix Thriller ‘Apex’

-

Business3 days ago

Business3 days agoBarclay Brothers Avoid Bankruptcy: HSBC Drops High Court Petitions After IVA Deal

-

Tech7 days ago

Tech7 days agoMicrosoft to roll out Entra passkeys on Windows in late April

-

Sports24 hours ago

Sports24 hours agoPaul Scholes issues Marcus Rashford reality check as agreement emerges over Man United star

-

Tech6 days ago

Tech6 days agoOpenAI’s Sam Altman apologizes for not reporting ChatGPT account of Tumbler Ridge suspect to police

-

Business3 days ago

Business3 days agoTesla Officially Registers Elon Musk’s Stock: What Investors Need to Know

-

Tech7 days ago

Tech7 days agoOpenAI CEO apologizes to Tumbler Ridge community

-

Tech4 days ago

Tech4 days agoGet Ready for More Brain-Scanning Consumer Gadgets

-

News Videos7 days ago

News Videos7 days ago16 Cryptos Just Became LEGAL Commodities (Full List)

You must be logged in to post a comment Login