Business

Will Sensex, Nifty extend gains or turn volatile? Q1 updates, F&O expiry among 8 factors set to steer stock market this week

Market participants will closely monitor the beginning of the June-quarter earnings season, monthly auto sales, the June F&O expiry, foreign fund flows, crude oil prices, monsoon progress, global bond yields, and key macroeconomic data for cues on the market’s next direction. Here are eight factors that could dictate Dalal Street this week.

1) Q1 business updates in focus

Investor attention will gradually shift from macro factors to corporate earnings as the June-quarter reporting season approaches. The first set of Q1 business updates and quarterly results will be watched closely for indications on demand trends, margins and management commentary.

According to Mayuresh Joshi, Head of Equity at Marketsmith India, markets have rebounded strongly in recent weeks and attention will now shift to earnings.

“The expectation is largely getting built out for Q1 that it is going to be a washout quarter because of supply chain issues, input cost inflation and some element of demand probably coming off,” he said.

2) June F&O expiry, portfolio rebalancing

Traders are bracing for a volatile week as the NSE’s June monthly derivatives expiry falls on Tuesday, accompanied by quarterly portfolio rebalancing by institutional investors.

According to Santosh Meena, Head of Research at Swastika Investmart, derivatives positioning has improved marginally, but expiry-related adjustments could lead to heightened volatility.3) Auto sales data

Monthly automobile sales for June, scheduled to be released on July 1, will be another major domestic trigger.

Investors will track dispatch trends across passenger vehicles, two-wheelers, commercial vehicles and tractors to gauge demand momentum after the onset of the monsoon. Strong numbers could reinforce optimism around consumption-led sectors, while any disappointment may weigh on auto stocks.

4) Monsoon progress

The progress and distribution of the southwest monsoon will remain on investors’ radar, given its implications for rural demand, inflation and agricultural output.

A healthy monsoon is expected to support farm incomes and consumption, benefiting sectors such as FMCG, automobiles and rural-focused businesses.

5) FII flows

Foreign institutional investor activity will continue to be a key determinant of market direction after selling pressure showed signs of easing in recent sessions.

Dr VK Vijayakumar, Chief Investment Strategist at Geojit Investments, said relentless foreign selling appears to be over.

“A significant trend in FPI activity in the second half of this month is the tapering of FPI selling. The big relentless FPI selling appears to be over,” he said.

According to Vijayakumar, the appreciation in the rupee and volatility in other Asian markets have made India relatively more attractive for overseas investors despite weak earnings expectations.

“The crash in crude to below $73 is a huge positive for India. Therefore, it can be safely concluded that the period of relentless FPI selling is over. But it may take some time for FPIs to become sustained buyers in India,” he added.

6) Oil prices

Crude oil prices will remain a closely watched global variable after retreating sharply from recent highs.

Lower crude prices are positive for India as they ease inflationary pressures, improve the current account position and reduce input costs for several sectors. Any fresh geopolitical developments that trigger volatility in oil could quickly influence market sentiment.

7) US bond yields

Global investors will also monitor movements in US Treasury yields and the dollar index for signals on capital flows into emerging markets.

Persistently elevated bond yields or renewed strength in the dollar could limit risk appetite, while softer yields may support foreign inflows into equities.

8) Macro data

A host of macroeconomic releases will keep global markets on edge during the week.

Investors will track manufacturing PMI data and employment numbers from the US, along with key economic indicators from China, for fresh clues on global growth and the outlook for interest rates.

Technical setup

According to Santosh Meena of Swastika Investmart, the Nifty continues to face a strong hurdle around the 24,200 mark.

A sustained breakout above 24,200 could open the door for a rally towards the 24,450-24,600 zone. On the downside, 24,000 and 23,770 remain immediate support levels.

Bank Nifty continues to outperform and is trading above its key moving averages. The index faces resistance in the 59,000-59,300 zone, while 57,500 and 57,000 are expected to provide strong support.

(Disclaimer: Recommendations, suggestions, views and opinions given by the experts are their own. These do not represent the views of The Economic Times)

The Federal Reserve: A Question Of Credibility

Russia pounds Kyiv with missiles, killing at least nine

This means that only those shareholders who own the shares of the company in their demat accounts as on August 10 (Monday) will be eligible to receive the dividend by the company, subject to shareholders’ approval at its upcoming Annual General Meeting (AGM).

This comes after the company paid a dividend of Rs 0.5 per share to its shareholders last year. The company, which had announced the latest dividend in April this year, has a dividend yield of 0.19%, according to data on Trendlyne.

Earlier this month, Jio Financial Services reported 155% year-on-year (YoY) growth in its consolidated net profit at Rs 830 crore in the first quarter, while revenue from operations in the reporting period increased 227% YoY to Rs 2,004 crore.

Consolidated total income rose 141% YoY to Rs 1,496 crore from Rs 619 crore. It was up 47% from Rs 1,020 crore in the March quarter. Interest income grew 165% YoY to Rs 962 crore, while fees and commission income surged to Rs 325 crore from Rs 54 crore.

Also read | Peter Lynch does not like the AI trade; here’s why he says ‘Know what you own’

Jio Financial Services share price

Jio Financial Services shares jumped nearly 4% to close at Rs 256 apiece on Friday. The stock gained more than 9% in a week and iver 8% in a month. Is it however down over 13% in 2026 so far.

In the longer term, the shares of the company have fallen over 22% in a year. The company currently has a market capitalisation of more than Rs 1.69 lakh crore.Motilal Oswal has a Buy rating on Jio Financial Services with a target price of Rs 315 apiece. The brokerage said the company delivered a healthy quarter, driven by strong growth in Jio Credit, whose assets under management (AUM) crossed Rs 300 billion.

It also highlighted steady progress across the payments, insurance, and asset management businesses, although operating expenses remained elevated due to continued investments in incubating new businesses and expanding existing operations. Motilal Oswal cut its FY27 and FY28 EPS estimates by 4% and 6%, respectively, to account for higher operating costs, but expects consolidated PAT to grow at a 46% CAGR between FY26 and FY28.

Also read | Maharashtra-based SME stock plunges 20% as MD gets shot, director taken in police custody

(Disclaimer: Recommendations, suggestions, views and opinions given by the experts are their own. These do not represent the views of The Economic Times)

Central Banks Hold Steady As Semiconductor Volatility Returns

Business

Invesco Mortgage Capital Inc. 2026 Q2 – Results – Earnings Call Presentation (NYSE:IVR) 2026-08-01

Seeking Alpha’s transcripts team is responsible for the development of all of our transcript-related projects. We currently publish thousands of quarterly earnings calls per quarter on our site and are continuing to grow and expand our coverage. The purpose of this profile is to allow us to share with our readers new transcript-related developments. Thanks, SA Transcripts Team

Alkane Resources: Dirt-Cheap Ounces In Top-Ranked Jurisdictions

Operator

Good day, everyone. Welcome to the TELUS 2026 Q2 Earnings Conference Call. I would like to introduce your speaker, Ian McMillan. Please go ahead.

Ian McMillan

Director of Investor Relations

Thank you, Karl, and hello, everyone. Thank you for joining us. Our second quarter 2026 news release, MD&A, financial statements and detailed supplemental investor information were posted on our website earlier this morning.

Today’s agenda will include opening remarks from Victor Dodig, President — TELUS President and Chief Executive Officer; and Gopi Chande, our Executive Vice President and Chief Financial Officer. After the presentation, there will be a question-and-answer period, followed by brief closing remarks by Victor.

Turning to Slide 2. Prepared remarks, slides and answers to questions contain forward-looking statements. Actual results could vary from these statements. Additionally, please note that all dollar amounts referenced today are in Canadian dollars, unless otherwise stated. The assumptions on which they are based and the material risks that could cause them to differ are outlined in our public filings with securities commissions in Canada and the United States, including our Q2 2026 and 2025 annual MD&A.

With that, let me turn the meeting over to Victor beginning on Slide 3.

Victor Dodig

CEO, President & Director

Thank you, Ian. Hello, everyone, and thank you

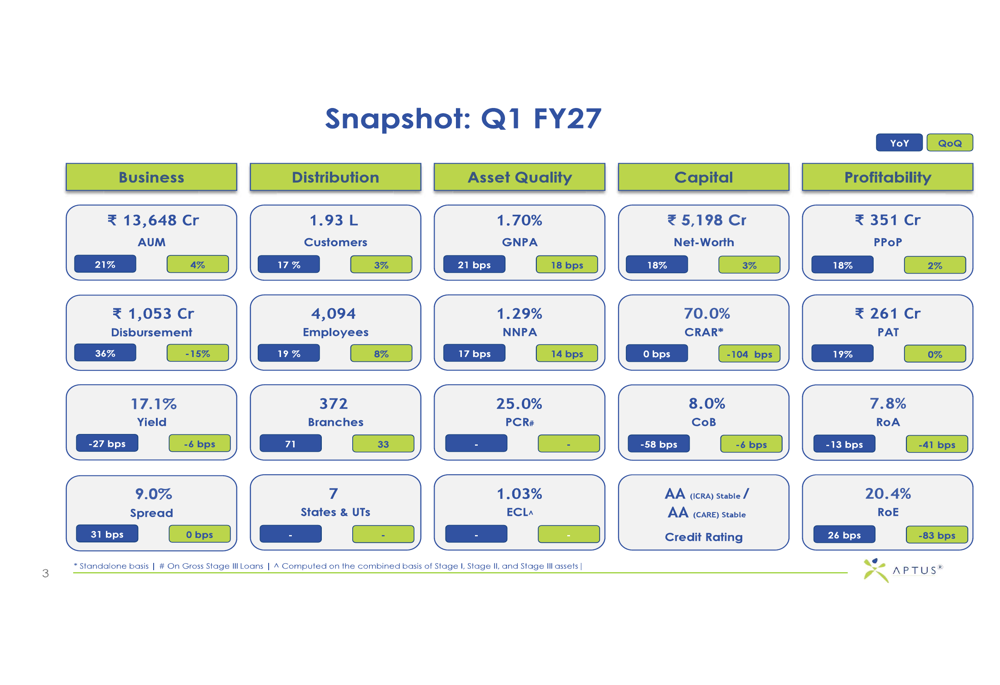

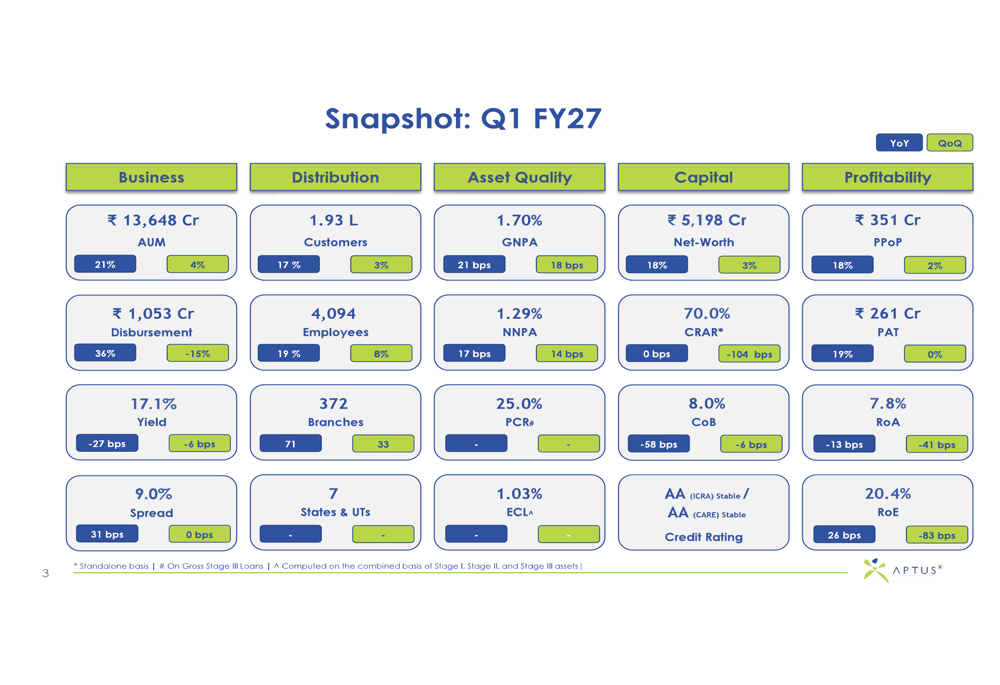

Aptus Value Q1 FY27 slides: profit jumps 19% but NPAs rise

Concurrent Gainers: 15 stocks rally for five straight sessions, surge up to 20%

Business

Higher Yields, Different Risk: How EM Local Currency Bonds Fit Into A Fixed Income Portfolio

Higher Yields, Different Risk: How EM Local Currency Bonds Fit Into A Fixed Income Portfolio

Cambridge South station sees more than 110k journeys in first month

The Federal Reserve: A Question Of Credibility

Bunnie Xo Prepared To Make Surprising Pivot After Jelly Roll Split

-

Sports5 days ago

Sports5 days agoCommonwealth Games boxing: Jadumani Singh seals dominant 5-0 win over Pakistan’s Sumama Rehman to enter quarter-finals | Commonwealth Games News

-

Business2 days ago

Business2 days agoWhy Trees Belong on the Risk Register

-

Fashion14 hours ago

Fashion14 hours agoWeekend Open Thread: Wit & Wisdom

-

Politics10 hours ago

Politics10 hours agoMeta enters AI-training agreement with far-right ‘propaganda rag’ Newsmax

-

Tech5 days ago

Tech5 days agoIntel is reversing course and bringing hyper-threading back to its server chips

-

Crypto World7 days ago

Crypto World7 days agoRipple bought a bank in pieces. The $4 billion audit

-

Politics5 days ago

Politics5 days agoLuke Littler dismantles Gerwyn Price to retain title in Blackpool

-

Politics4 days ago

Politics4 days agoThe Part of the Electric Transition Nobody Wants to Discuss

-

News Videos5 days ago

News Videos5 days agoBITCOIN JUST ENTERED THIS CRITICAL ZONE…

-

Entertainment4 days ago

Entertainment4 days ago‘Stargate’ Creator’s New Sci-Fi Series Returns for Season 3 Tomorrow

-

Crypto World6 days ago

Crypto World6 days agoXRP Ledger adds $2.6B as RWA inflows rank second

-

Business3 days ago

Business3 days agoMajor shareholder moves on Canyon

-

Politics6 days ago

Politics6 days agoSpain sweeps the board at 2026 World Cup with individual awards

-

News Videos2 days ago

News Videos2 days agoBitcoin Enters the 3rd Stage of the Bear Market

-

Crypto World1 hour ago

XRP Ledger v3.3.0 brings five institutional features

-

Entertainment6 days ago

Entertainment6 days agoSara Gilson Killed By Husband After Viral “Pedophile” TikTok Video

-

Crypto World3 days ago

Crypto World3 days agoKraken Enables Retail Access to Jersey Mike’s IPO via Tokenized Shares

-

Tech4 days ago

Tech4 days agoNew macOS Sequoia & Sonoma security updates for older Macs

-

News Videos3 days ago

News Videos3 days agoClaude: Build Financial Dashboards in Minutes (2026)

-

Politics2 days ago

Politics2 days agoLuke Littler’s dominance sparks GOAT debate

You must be logged in to post a comment Login