Crypto World

10% Bounce Hope Rise As Whales Buy

Ethereum is trying to stabilize after weeks of heavy selling. The price is holding near the $1,950 zone, up around 6% from its recent low. At the same time, the biggest Ethereum whales have started accumulating aggressively.

But short-term sellers and derivatives traders remain cautious, creating a growing tug-of-war around the next move.

Biggest Ethereum Whales Accumulate as Bullish Divergence Stays Intact

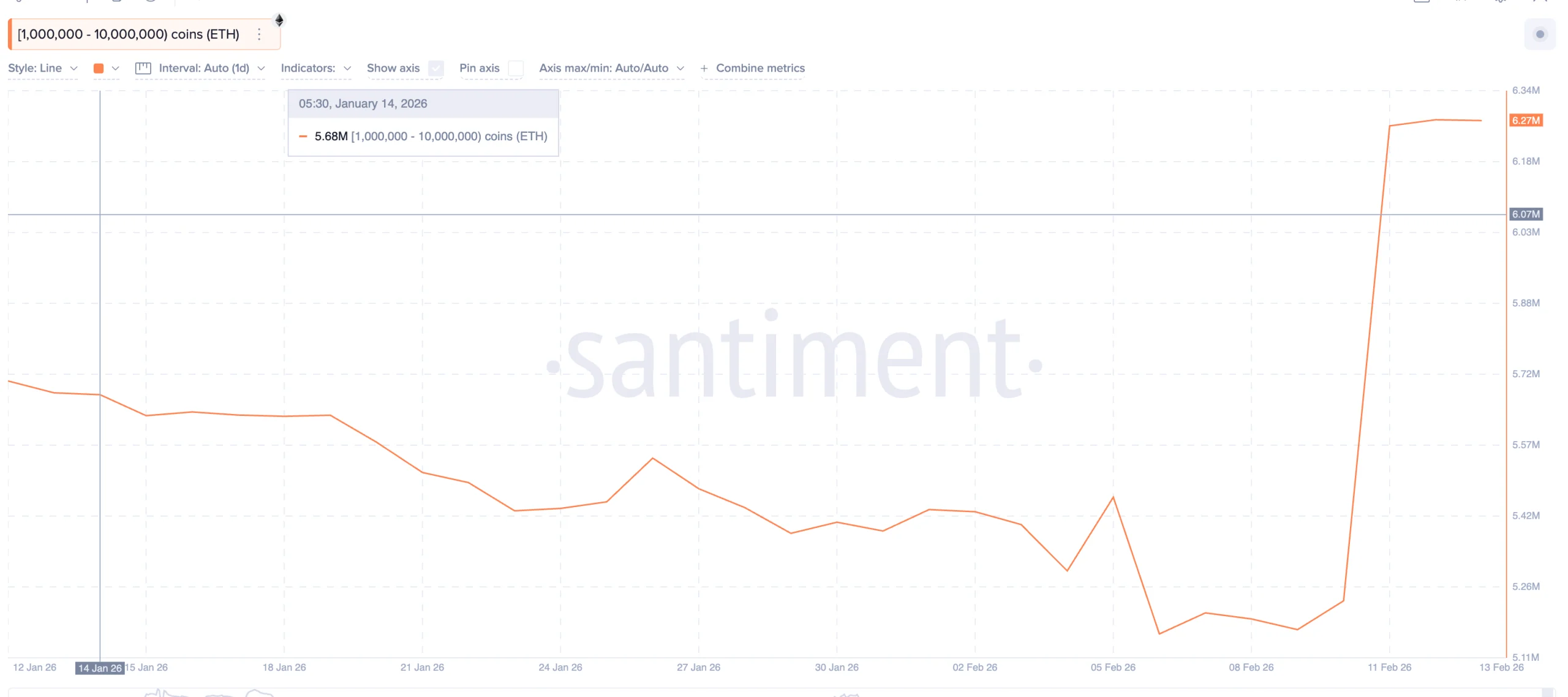

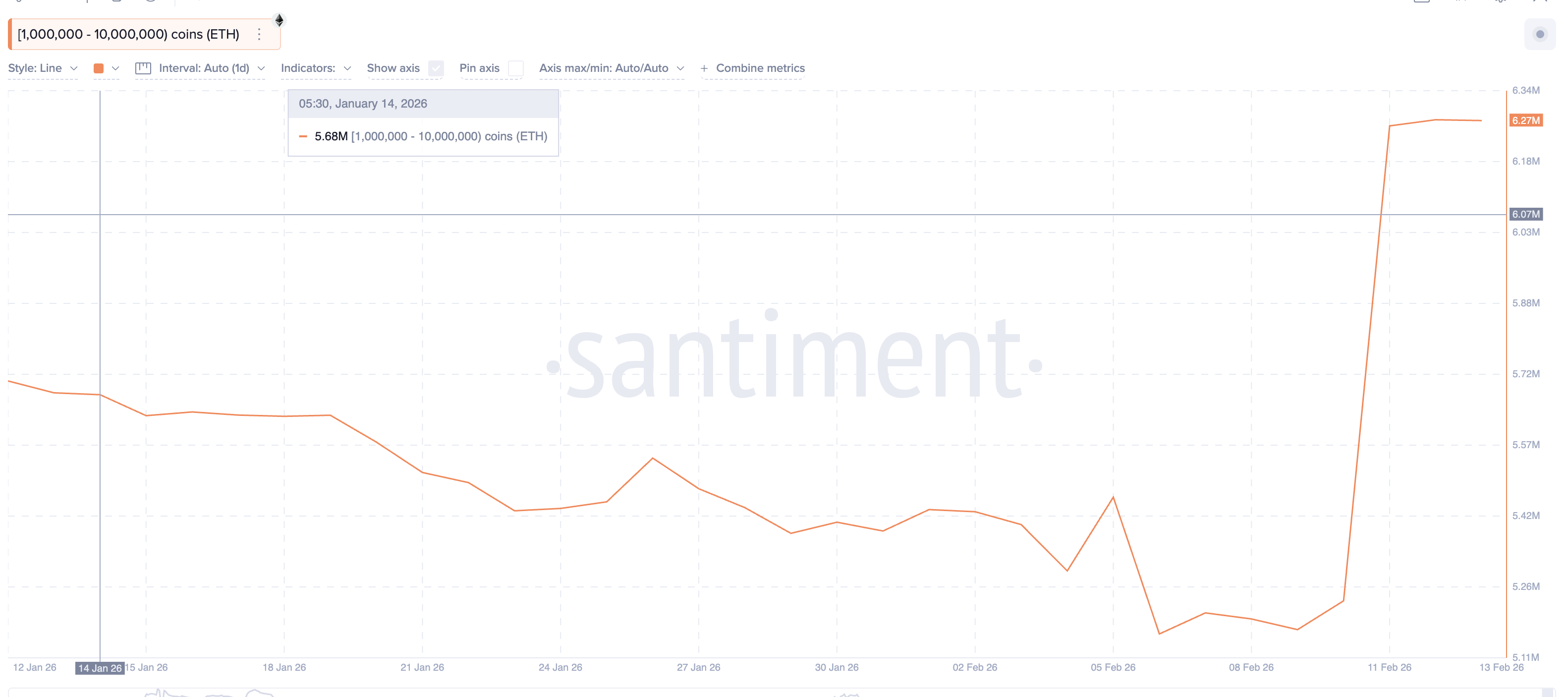

On-chain data shows that the largest Ethereum holders are positioning for a rebound. Since February 9, addresses holding between 1 million and 10 million ETH have increased their holdings from around 5.17 million ETH to nearly 6.27 million ETH. That is an addition of more than 1.1 million ETH, worth roughly $2 billion at current prices.

Sponsored

Sponsored

Want more token insights like this? Sign up for Editor Harsh Notariya’s Daily Crypto Newsletter here.

This accumulation aligns with a bullish technical signal on the 12-hour chart.

Between January 25 and February 12, Ethereum’s price made a lower low, while the Relative Strength Index, or RSI, formed a higher low. RSI measures momentum by comparing recent gains and losses. When price falls, but RSI rises, it often signals weakening selling pressure.

This bullish divergence suggests downside momentum is fading.

The structure remains valid as long as Ethereum holds above $1,890, as the same signal flashed even on February 11 and still seems to be holding. A breakdown below this level would invalidate the divergence for now and weaken the rebound case.

For now, whales appear to be betting that this support will hold.

Sponsored

Sponsored

Short-Term Holders Are Selling?

While large investors are accumulating, short-term holders are behaving very differently.

The Spent Coins Age Band for the 7-day to 30-day cohort has surged sharply. Since February 9 (the same time when the whale pickup started), this metric has risen from around 14,000 to nearly 107,000, an increase of more than 660%. This indicator tracks how many recently acquired coins are being moved. Rising values usually signal possible profit-taking and distribution.

In simple terms, short-term traders are exiting positions. This pattern appeared earlier in February as well. On February 5, a spike in short-term coin activity occurred near $2,140. Within one day, Ethereum dropped by around 13%.

That history shows how aggressive selling from this group can quickly reverse moves. As long as short-term holders remain active sellers, upside moves are likely to face resistance.

Sponsored

Sponsored

Derivatives Data Shows Heavy Bearish Positioning

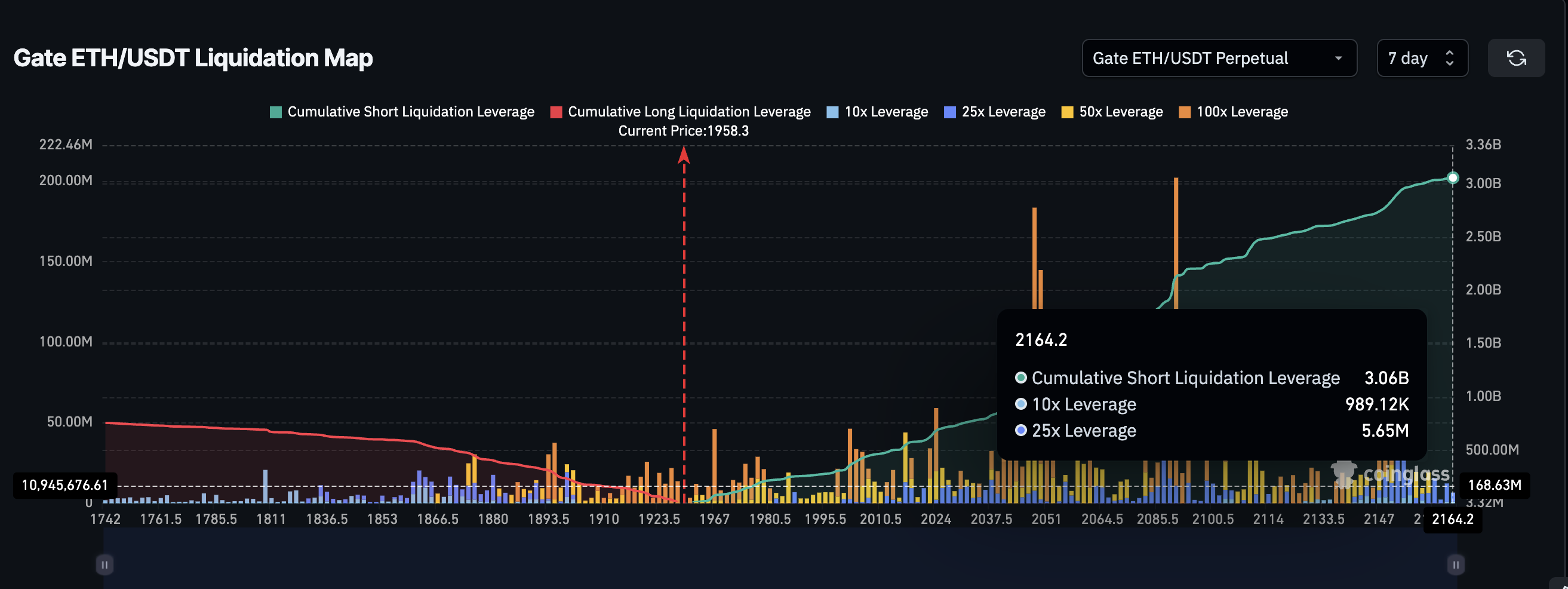

Derivatives markets are reinforcing this cautious outlook. Current liquidation data shows nearly $3.06 billion in short positions stacked against only about $755 million in long leverage. This creates a heavily bearish imbalance with almost 80% of the market betting on the short side.

On one hand, this setup creates fuel for a potential short squeeze if prices rise. On the other hand, it shows that most traders still expect further weakness. This keeps momentum muted but keeps the bounce hope alive if the whale buying pushes the prices up, even a little bit, crossing past key clusters.

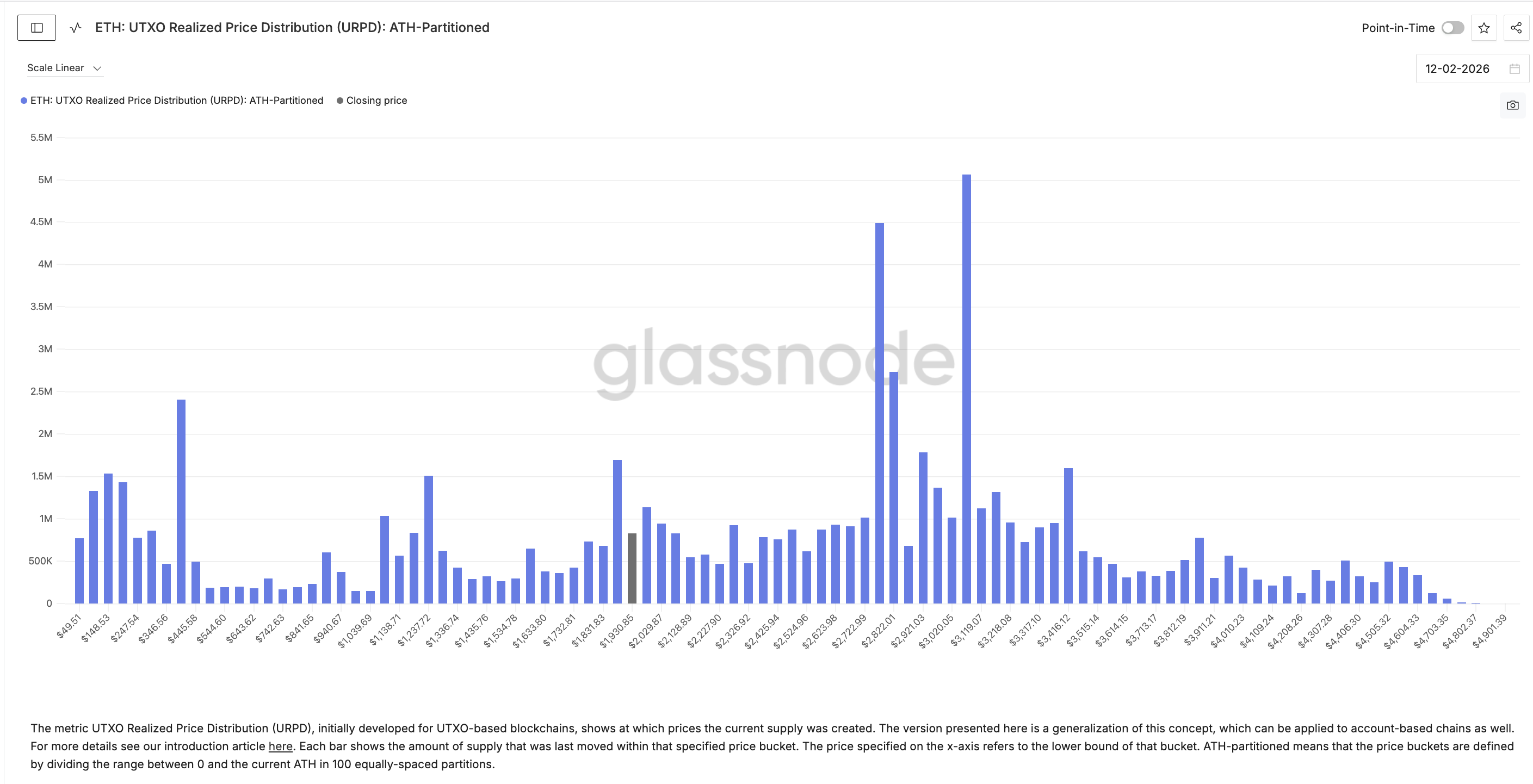

On-chain cost basis data helps explain why Ethereum struggles to break higher. Around $1,980, roughly 1.58% of the circulating supply, was acquired. Near $2,020, another 1.23% of supply sits at breakeven. These zones represent large groups of holders waiting to exit without losses.

Sponsored

Sponsored

When price approaches these levels, selling pressure increases as investors try to recover capital. This has repeatedly capped recent bounces. Only a strong leverage-driven move or short squeeze would likely be powerful enough to push through these supply clusters.

Until then, these zones remain major barriers.

Key Ethereum Price Levels To Track Now

With whales buying and sellers resisting, Ethereum price levels now matter more than narratives.

On the upside, the first major resistance sits near $2,010. A clean 12-hour close above this level would increase the probability of short liquidations. And it sits near the key supply cluster.

If that happens, Ethereum could target $2,140 next, a strong resistance zone with multiple touchpoints. It also sits around 10% from the current levels. On the downside, $1,890 remains the critical support. A break below this level would invalidate the bullish divergence and signal renewed downside pressure. Below that, the next major support sits near $1,740.

As long as Ethereum holds above $1,890 and continues testing $2,010, the rebound structure remains intact. A sustained breakdown below support would cancel the current recovery attempt.

Australia has passed legislation that will bring many digital asset platforms and tokenised custody platforms under the country’s financial services licensing regime.

The Corporations Amendment (Digital Assets Framework) Bill 2025 has now cleared both houses of the Australian Parliament, according to parliamentary records, marking the biggest step yet in Canberra’s push to create a dedicated regulatory framework for digital assets.

Introduced in November 2025, the bill amends the Corporations Act and ASIC Act to regulate digital asset platforms and tokenised custody platforms, with the stated aim of improving consumer protection, market integrity and regulatory certainty.

The bill now awaits royal assent, the final step before becoming law. It is set to take effect 12 months after assent, with an additional transition period for businesses to comply.

The bill requires crypto operators, including exchanges and custody platforms, to obtain an Australian Financial Services Licence (AFSL) from the Australian Securities and Investments Commission (ASIC), the country’s financial regulator.

The Digital Economy Council of Australia (DECA), an industry group representing Australia’s digital economy, praised the development in a statement on LinkedIn.

“For the first time, we have a legislative framework that directly addresses digital asset platforms and it provides long-awaited clarity for businesses, investors and regulators, and marks a shift from uncertainty toward implementation,” DECA said.

Related: Australia fines local Binance unit $6.9M over client onboarding failures

Addendum clarifies treatment of MPC and crypto custody under new law

Jazz Ozvald, former assistant director of digital asset policy at the Commonwealth Treasury, took to LinkedIn to express delight at the milestone in passing the bill.

He noted that the government also tabled an Addendum to the Explanatory Memorandum, which includes additional detail about how the bill is intended to apply where digital tokens are factually controlled through multi-party computation (MPC).

MPC is a cryptographic technology used to secure crypto wallets by splitting control between multiple parties, so no single person has full control. Transactions can only be approved when enough parties work together, making it harder for funds to be stolen or misused.

Related: Google targets 2029 post-quantum migration as threats draw nearer

The addendum says that the law only applies to platforms that actually hold crypto for customers, rather than just providing technology that helps control it, even in shared-control setups like MPC.

Magazine: Nobody knows if quantum secure cryptography will even work

SpaceX, Elon Musk’s aerospace powerhouse, has reportedly filed confidentially for an initial public offering with the U.S. Securities and Exchange Commission. The move, described by Bloomberg as citing people familiar with the matter, positions the company for what could be one of the largest public listings in U.S. history and signals a potential shift in how a private space and AI conglomerate marshals capital for its next phase.

According to Bloomberg’s reporting, the IPO could be timed for a June close, should the process move forward as planned. While details remain shielded behind confidentiality, insiders told Bloomberg that the offering could value SpaceX well above $1.75 trillion and could raise as much as $75 billion, a scale that would dwarf many prior debutings and reimagine the company’s public-market footprint.

The listing could feature a dual-class share structure designed to preserve control for insiders, including SpaceX founder Elon Musk, even as public investors participate. In line with such structures, the offering is expected to allocate up to 30% of shares for individual investors, according to the coverage.

On the banking and advisory front, the process is anticipated to involve a cadre of Wall Street firms, with Bank of America, Goldman Sachs, JPMorgan Chase, Morgan Stanley and Citigroup commonly cited as likely participants in steering SpaceX through its transition to a public company.

Beyond the IPO chatter, SpaceX’s crypto footprint remains a recurring point of interest. The company is widely reported to hold a substantial Bitcoin position—8,285 BTC on its balance sheet, valued at more than $565 million at current prices. Notably, SpaceX moved its Bitcoin to a new wallet address in October, fueling speculation about whether the company intends to maintain a long-term crypto strategy or adjust holdings in response to market conditions.

Market structure and access to private holdings are also on the radar as SpaceX eyes broader investor participation. Trading venues and tokenization platforms have been examining opportunities to offer tokenized shares or similar vehicles for high-profile private companies, including SpaceX and other AI leaders. Robinhood and Kraken, among others, have discussed how retail investors might gain access to nonpublic companies through blockchain-based tokenized instruments, a development Robinhood’s CEO has described as potentially widening participation even as high-profile private tech firms pursue public-market exits.

Key takeaways

- SpaceX reportedly filed confidentially for an SEC IPO, with a possible June timeline and a valuation above $1.75 trillion; potential raise up to $75 billion.

- The deal could use a dual-class structure preserving insider voting control, with up to 30% of shares reserved for individual investors.

- Major banks—Bank of America, Goldman Sachs, JPMorgan Chase, Morgan Stanley and Citigroup—expected to advise on the transition to a public company.

- SpaceX reportedly maintains 8,285 BTC (worth over $565 million) on its balance sheet, with a October wallet move prompting questions about long-term crypto strategy.

- Tokenized private-share concepts are circulating in crypto markets, with Robinhood and Kraken cited as exploring access to SpaceX, OpenAI and other nonpublic firms for retail investors.

- In the AI space, SpaceX’s acquisition of xAI places it in a broader race with OpenAI and other private AI labs; OpenAI recently closed a funding round with about $122 billion in committed capital, lifting its implied valuation toward the hundreds of billions, and Bloomberg notes potential IPO activity for both OpenAI (as early as 2026) and Anthropic (potentially as soon as October).

Context: SpaceX’s AI ambitions and the public market timing

The reported IPO comes on the heels of SpaceX’s February move to acquire xAI, Elon Musk’s AI venture, signaling a ramp-up in the company’s participation in the fast-evolving AI ecosystem. The combination of aerospace prowess and AI development positions SpaceX to leverage a broader technology and capital-market narrative as investors assess how private companies transition to public ownership.

OpenAI, the creator of ChatGPT, has been central to the AI funding landscape. Bloomberg notes that OpenAI concluded its latest funding round with about $122 billion in committed capital, driving its estimated value higher—a point underscoring the growing parallel between AI capital intensity and public-market appetites. The firm has been widely discussed as a potential IPO candidate in 2026, a signal to market participants that large AI players could become regulars on public exchanges in the coming years. Anthropic, another important name in the field, is also reported to be weighing a public listing, with Bloomberg indicating a possible listing as soon as October of this year.

As SpaceX contemplates a potential public listing, retail and institutional investors alike are watching how the company would balance the demands of a public-filed governance framework with its private-market strategies and multi-vertical ambitions. The prospect of a dual-class structure remains a point of contention for some market observers, given how it concentrates voting power among insiders even as it enables faster strategic execution and longer-term investment horizons.

For crypto-market observers, the overlap between SPAC-like tokenization concepts and traditional IPOs adds another layer of consideration. Tokenized shares and blockchain-based participation could, in theory, broaden access to a private giant like SpaceX for retail buyers who traditionally have had limited entry points. While these products are still gaining regulatory clarity and market traction, the ongoing interest from platforms such as Robinhood and Kraken indicates a broader industry push to bridge private-market participation with public-market liquidity via tokenization tools.

What this means for investors and the AI ecosystem

If SpaceX proceeds with an IPO in the proposed size and structure, it would be among the largest listings in U.S. history and would place the company at a valuation tier previously seen with mega-cap tech and consumer platforms. For investors, the potential blend of aerospace breadth and AI stakes could create a diversified exposure within a single name, while the dual-class voting framework could shape how quickly and how decisively SpaceX can execute long-term strategy in a volatile market environment.

From a broader market perspective, the convergence of SpaceX’s public-market ambitions with the AI arms race highlights a trend where tech giants are building vertical integrations across space, transportation, and artificial intelligence. OpenAI’s and Anthropic’s public-market trajectories, while not guaranteed, add a tailwind to this narrative, suggesting that the next wave of big listings could include private AI labs alongside more diversified technology conglomerates. Investors should watch regulatory developments, the timing and terms of any anchor shareholders, and how SpaceX plans to balance public reporting requirements with its rapid, multi-domain execution plan.

Whether or not the SpaceX IPO materializes on schedule, the reporting underscores a larger dynamic: the market’s willingness to value private, highly strategic technology entities at multi-trillion-dollar levels and to explore new models of ownership and participation, including tokenized access to private-equity-like positions. For crypto markets, the ongoing dialogue around tokenization, crypto holdings, and public-market access remains a live space to watch as these conversations intersect with traditional capital-raising mechanisms.

Readers should monitor upcoming disclosures and investor briefings, which Bloomberg notes SpaceX has signaled will occur later this month. How the market perceives SpaceX’s balance between leadership in aerospace and AI, and how the company navigates governance, capital structure, and crypto exposure, will likely shape the scope of future public-market activity among technology-first, asset-light conglomerates.

As the IPO discourse unfolds, investors and builders will need to weigh not only the size of the offering but also the governance implications, the strategic roadmap for AI initiatives, and the evolving role of crypto in corporate treasury strategies. The next steps—from regulatory filings to investor roadshows—will reveal how SpaceX intends to translate its private-market momentum into a lasting public-market narrative.

Stay tuned for updates on next steps, regulatory milestones, and any refinements to SpaceX’s proposed capital structure as the market awaits a potential landmark listing that could redefine the contours of big-tech and AI investing.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

AI crypto trading bots reshape investing as automation replaces manual execution and emotional decision-making.

Summary

- AI crypto trading bots simplify investing by automating strategies and removing the need for constant monitoring.

- SaintQuant targets beginners with pre-configured strategies and no coding or complex setup required.

- Its fully automated system offers a hands-off approach for users seeking simple, consistent crypto trading.

The rise of AI trading bot crypto solutions has transformed how people approach cryptocurrency trading. What once required deep technical knowledge, constant monitoring, and emotional discipline can now be handled by intelligent automation.

Today, both beginners and experienced traders are exploring automated crypto trading platforms to improve efficiency and reduce manual effort. But key questions remain:

- Do AI trading bots work?

- Can you build one without coding?

- Is there a free crypto trading bot worth trying?

In this guide, we’ll break down everything that is needed to know — from how these bots work to how to choose the best platform — while sharing practical insights to help anyone get started.

What is an AI trading bot in crypto?

An AI trading bot is a software program that uses artificial intelligence to analyze market data and execute trades automatically. Unlike traditional bots that follow fixed rules, AI-powered bots adapt to changing market conditions using:

- Machine learning algorithms

- Predictive analytics

- Real-time data processing

These bots are widely used in:

- Crypto trading online for automated execution

- Portfolio management

- Arbitrage opportunities across exchanges

In essence, an AI-powered Bitcoin bot acts as a 24/7 trading assistant, capable of making decisions faster than any human trader.

Do AI trading bots work? (Realistic expectations)

The short answer: Yes — but with limitations.

Advantages

- 24/7 trading without downtime

- Emotion-free decisions, reducing impulsive trades

- Fast execution in volatile markets

Limitations

- No guarantee of profits

- Performance depends on strategy quality

- Vulnerable to extreme market conditions

AI trading bots work best when used as tools to enhance strategy, not as “set-and-forget money machines.”

How to build an AI Crypto trading bot without coding, and are there free options?

One of the biggest myths in crypto trading is that there’s no need for programming skills to use automation. Fortunately, that’s no longer true.

Simple no-code setup process

For those wondering how to build an AI crypto trading bot without coding, here’s a simplified path:

- Choose a platform

- Select pre-built AI strategies

- Configure risk settings

- Backtest strategies

- Deploy live trading

Modern platforms now provide intuitive dashboards, making the process accessible even to complete beginners.

Tools that make it easy

- Plug-and-play platforms

- Strategy marketplaces

- Managed cryptocurrency trading services

These tools eliminate complexity and allow users to focus on outcomes rather than technical setup.

Is there a free crypto trading bot?

Yes — but most “free” options come with trade-offs.

What “Free” Usually Means:

- Limited features

- Trial-based access

- Restricted performance tools

Hidden Costs to Consider:

- Exchange fees

- Spread and slippage

- Paid upgrades for full functionality

Real example: Try before committing

Some platforms offer a better alternative through trial-based access to premium features.

For instance, SaintQuant provides a beginner-friendly experience with:

This allows users to experience a real automated crypto trading platform — not just a limited demo.

When free bots make sense

Free or trial bots are ideal for:

- Beginners exploring AI trading bots

- Testing strategies safely

- Learning how automation works in real markets

Key takeaway

There is no need for coding skills or a large upfront investment to start using an AI trading bot crypto solution. With no-code tools and trial offers, entry barriers are lower than ever.

Best AI trading bot crypto platforms (expert insights)

Choosing the right platform is critical. Based on usability, features, and accessibility, here are some top options:

1. SaintQuant – Simplified AI Trading for passive income

SaintQuant stands out as a beginner-focused platform designed for simplicity and efficiency.

Key Features:

- Pre-configured AI trading strategies

- No coding or complex setup required

- Fully automated trading system

Advantages:

- Ideal for beginners and passive investors

- Quick onboarding process

- Focus on consistent, automated performance

If you’re looking for a hands-off automated bitcoin trading platform, SaintQuant offers one of the easiest entry points.

2. Cryptohopper – Advanced customization

Cryptohopper is a well-known platform offering:

- Strategy customization

- Signal marketplace

- Advanced trading tools

Pros:

Cons:

- Steeper learning curve for beginners

3. Other AI trading bots worth considering

There are also various:

- Bots for sale in strategy marketplaces

- Hybrid platforms combining AI and manual controls

When evaluating options, always prioritize:

- Security

- Exchange integration

- Transparency

Key features to look for in the best AI trading bot

When choosing the best AI trading bot crypto, consider:

- Automation quality

- Backtesting capabilities

- Risk management tools

- Exchange compatibility

- Performance transparency

These features determine whether a bot is truly effective or just hype.

Risks and best practices

Even the best bots require responsible usage.

Best Practices:

- Start with a small capital

- Diversify strategies

- Monitor performance regularly

- Use secure API configurations

Avoid relying entirely on automation—human oversight still matters.

AI trading bots vs manual trading

| Factor | AI Trading Bots | Manual Trading |

| Speed | Instant execution | Slower |

| Emotion | Emotion-free | Emotion-driven |

| Control | Less direct control | Full control |

Best approach: combine both for optimal results.

Future of AI in crypto trading

The future of AI trading bots is promising, with trends including:

- Integration with DeFi ecosystems

- More advanced predictive models

- Increased adoption among retail investors

As technology evolves, automation will likely become a standard part of crypto trading online.

Conclusion

AI trading bots are reshaping the crypto landscape by making trading more accessible, efficient, and data-driven.

- They work — but require smart usage

- They can be built and deployed without coding

- Free and trial options make it easy to start

Platforms like SaintQuant are helping bridge the gap for beginners, offering a streamlined way to enter the world of automated trading.

If you’re new, start small, experiment with strategies, and gradually scale your involvement. With the right approach, AI-powered cryptocurrency trading services can become a valuable part of your investment toolkit.

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

Art on Tezos is no longer a niche experiment; at TezDev 2026 in Cannes, it felt like a working model of where digital culture is going next.

Summary

- At TezDev 2026 in Cannes, “Art on Tezos” staged an immersive, projection-mapped environment that framed on-chain work as a living model for digital culture.

- Speakers highlighted how Tezos lowers costs and barriers so artists from Kurdistan, Africa and South America can build sustainable practices and even escape repression.

- Trilitech’s planned Tezos-powered exhibition at HEK Basel signals that on-chain art is moving deeper into museum ecosystems, compressing photography’s century-long legitimation curve.

TezDev 2026 in Cannes shows how Tezos art has evolved from NFTs into global, politically charged and increasingly institutional grade digital culture and infrastructure.

Hosted at the Hôtel Martinez on March 30, “Art on Tezos: The future of digital creativity” unfolded as an immersive environment rather than a standard panel. Projection‑mapped works wrapped the room in moving images while a conversation between artists, curators, and ecosystem builders traced how on‑chain art has evolved from early NFTs into complex generative systems and responsive installations.

For curator and art advisor Brian Beccafico, Tezos’ real innovation is who it brings into the conversation. Drawing on his work with marketplaces like Objkt, he stressed that on Tezos “you get to meet a lot of artists coming from places that usually just don’t have access to the broader art markets… artists from Africa… South East Asia, South America,” a sharp contrast with a global art economy where “pretty much 70 percent of global value auctioned… is auctioned in New York.” Lower costs and open tooling translate into economic reality: “even if you’re selling artwork for 100 bucks a piece… in a country where the average income is 300 bucks a month, that’s… sustainable for an artist.”

Aleksandra Art, Head of Arts at Trilitech, placed this shift in a longer media history that runs from early photography to Instagram and now blockchain. She reminded the audience that photography itself was once dismissed—“wait, photography is art? What? Like, no, it’s just a picture”—before fairs, critics, and collectors built a new ecosystem around it. The same dynamic is now playing out in digital art: “we had Instagram launch and all of a sudden there are Instagram artists… that don’t need gallery representation,” and blockchains plus marketplaces extend that logic by “creating these networks that congregate people who are passionate about it.” For her, the crucial break is that digital work “doesn’t have to be a confined gallery space… it can be a vertical screen, horizontal screen, HTML, site specific work,” accessible globally “at any point of time” with “similar experiences for different people.”

Beccafico pushed the political edge of this transformation. He recalled exhibitions where artists from Kurdistan “used crypto to flee terrorism, to flee ISIS during the war in Syria,” arguing that cypherpunk ideals still matter: “being able to free yourself from state‑owned currency, state‑owned control, and censorship is still very much a reality in today’s art world.” The result is a scene in which artists from Iraq, Turkey, South America, and beyond are no longer at the margins but, in his words, “the future of both crypto and the future of the art world.”

Alongside Aleksandra and Beccafico, the session’s participants—Vinciane Jones (Art Partner Manager, Trilitech), artists Patrick Tresset and Georg Eckmayr, and others—situated Tezos inside a broader genealogy of systems‑driven practices, from algorithmic drawing to AI‑assisted installations, now made verifiable and tradable on‑chain. Their discussion aligned with the wider TezDev 2026 program, which underscored how protocol upgrades like Tezos X and faster Etherlink confirmations are intended to support richer real‑time art and gaming experiences, not just finance.

Trilitech signaled that TezDev’s immersive exhibition is not a one‑off but part of a longer institutional arc. The team previously announced plans for a forthcoming Tezos‑powered show at HEK (Haus der Elektronischen Künste) in Basel, curated by the established duo Dr. Alfredo Cramerotti and Auronda Scalera, known for pioneering projects at Art Dubai Digital and other major venues that connect blockchain, NFTs, and critical media art. Their involvement points to a future in which on‑chain practices move even further into museum contexts, bringing Beccafico’s emerging‑market artists and Aleksandra’s “fluid,” screen‑native works into dialogue with decades of digital and conceptual experimentation.

If photography’s journey from “just a picture” to museum cornerstone took a century, Tezos (TEZ) artists are compressing that curve into a few intense years, using blockchains not only as markets but as infrastructure for new forms of authorship, community, and survival.

Hedera price has been in a downtrend over the past month as the token continues to be bruised by the geopolitical concerns that have pushed investors away from risk assets.

Summary

- Hedera price dropped to a six-week low of $0.083, down over 12% in a month amid weak market sentiment and geopolitical tensions.

- On-chain activity declined, with DeFi app revenue falling nearly 70% and stablecoin supply dropping 6%, signaling reduced network usage and liquidity.

- Technical indicators remain bearish, with price trading in a descending channel and key support seen at $0.087.

According to data from crypto.news, Hedera (HBAR) price fell to a six-week low of $0.083 on Tuesday, down over 12% in the past month and over 20% from its year-to-date high.

Hedera price fell amid weakness in its underlying ecosystem activity as key performance indicators started to flash red. Data from DeFiLlama shows that revenue generated by DeFi apps on the network had slumped nearly 70% from the previous month’s high.

A drop in app revenue means that a lower number of users are interacting with the Hedera ecosystem, signaling weakening demand for its decentralized applications and reduced overall network usage.

Third-party data also show that the total supply of stablecoins on the network has fallen 6% over the past 7 days to $52.71 million. Declining stablecoin supply typically reflects reduced liquidity and capital inflows on the network, further reinforcing signs of slowing activity.

Hedera price has also remained in a downtrend due to reduced investor appetite for risk assets amid the ongoing U.S.-Iran war that has led to a flight to more traditional safe-haven assets such as gold and U.S. equities.

On the daily chart, Hedera price has been trading within a descending parallel channel pattern, a formation where the asset consistently makes lower highs and lower lows. As long as an asset trades within such a pattern, it will likely continue to face persistent selling pressure as it bounces between the upper and lower boundaries.

Technical indicators also appear to portray a bearish outlook for Hedera price in the upcoming sessions. Notably, the Bollinger Bands have begun to narrow, with the price trading below the middle band, suggesting contracting volatility while the short-term trend remains tilted to the downside.

The Aroon Down is at 92.86% while the Aroon Up remains at 0%, indicating strong downward momentum and that a recent low has likely been established within the current trend.

For now, the immediate support level for Hedera price lies at $0.087, which aligns with the 23.6% Fibonacci retracement level. A drop below this level could increase selling pressure and open the door for a move toward lower support zones.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Coinbase is folding regulated prediction markets into its “everything exchange” vision, using The Clearing Company to clear on‑chain event contracts beside crypto and stocks.

Summary

- Coinbase is moving prediction markets from a Kalshi integration toward an on‑chain, in‑house stack after acquiring The Clearing Company, aiming to keep them inside a regulated perimeter.

- In Europe, financial‑underlying prediction markets fall under MiFID while politics and sports are pushed into fragmented national gambling regimes, leaving most current on‑chain volume in regulatory limbo.

- Coinbase is already experimenting with cross‑margining via perpetual futures and sees long‑term scope to extend collateral efficiency across prediction markets, crypto, and tokenized assets on a single venue.

Coinbase’s push to become an “everything exchange” will increasingly run through regulated prediction markets rather than just spot crypto, according to Côme Prost‑Boucle, the exchange’s head of international listings, speaking with crypto.news at ETHGlobal Cannes on March 31.

For Prost‑Boucle, prediction markets are not a novelty bolt‑on. They sit at the core of Coinbase’s plan to become what he calls an “everything exchange.” “The whole strategy is pretty simple,” he told crypto.news.

“We want to build the everything exchange with Coinbase, meaning that we want to bring under one regulated umbrella all of the asset classes that you can imagine and offer this to both our retail customers and our institutional customers.”

Coinbase leading the way to become an ‘Everything Exchange’

That umbrella now stretches beyond spot crypto into derivatives, options, tokenized stocks and equities, token sales and, crucially, event‑based contracts that let users trade on future outcomes. “We have this whole breadth of different products that we’re bringing into one umbrella, which is Coinbase,” he said. “Our goal is to push this to as many users as possible across the world, and the reaction has been pretty tremendous so far.”

Coinbase’s debut in prediction markets was deliberately conservative. The initial launch in the U.S. leaned on Kalshi, the CFTC‑regulated event‑contract venue, giving the product an immediate regulatory backbone but also clear constraints on geography and design.

“The first iteration of the product is available in the US and in a couple of regions, but for instance, it’s not available in Europe because of lack of regulatory clarity,” Prost‑Boucle said. That version effectively pipes Kalshi’s markets into the Coinbase interface, letting users trade small‑ticket contracts on elections, sports, macro data and other real‑world events while staying inside a U.S. event‑contract framework.

The second phase is more aggressive. In December, Coinbase agreed to acquire The Clearing Company, a specialist prediction‑market clearing startup with roots in the existing event‑contract ecosystem.

Prost‑Boucle referred to it in the interview as “a company called The Clearing House,” but the strategic intent is clear. “The goal is for us to bring these capacities internally so that we can develop this product on chain and we can develop with the DNA that we have to bring all asset classes on chain,” he said. In effect, Coinbase is moving from renting regulated rails to owning the clearing and risk stack, and then pushing more of the lifecycle on‑chain while staying within the event‑contract perimeter. That stands in contrast to crypto‑native venues such as Polymarket, which prioritizes unconstrained on‑chain liquidity first and only later began to grapple with regulatory structure.

Prediction markets dominate conversation at ETHGlobal

If prediction markets are to sit alongside crypto, derivatives and tokenized stocks in a single app, collateral efficiency will determine whether users actually route meaningful size through Coinbase. Here, Prost‑Boucle says institutional desks are already applying pressure. “That’s also something that institutional clients have been pushing for,” he noted when asked about cross‑margining prediction markets with other Coinbase products. “We’re currently doing cross‑margining for our perpetual futures product, and that’s something that our institutional clients have been craving,” he added, pointing to demand for “always‑on exposure possibilities, weekend hedging, all of this that perpetual futures have as internal features.” The logical goal is to have a single collateral pool backing BTC perpetuals, tokenized equity and a portfolio of geopolitical or macro event contracts, rather than trapping capital in isolated silos across venues. “At the moment we’re working on this product,” he said of cross‑margining, “but I think that’s a good vision for us in the longer term—to have cross‑margining across the different asset classes, I guess.”

The main structural obstacle to that vision is Europe. “Prediction markets in the EU are pretty difficult to apprehend because there’s no unified regulatory framework,” Prost‑Boucle said. “It all depends on what you have as an underlying asset.” He draws a sharp line that mirrors emerging legal commentary: a contract on the future price of Bitcoin is treated as a financial derivative under MiFID, while a contract on an election or football match is pushed into gambling. “If the contract lies on a financial underlying asset, that would be regulated by MiFID,” he explained. “But all of the other classes, where currently all of the volumes are—on politics, on sports, this would be regulated under gambling laws in Europe.”

That split leaves most of today’s on‑chain volume—heavily skewed toward politics and sports—in regulatory limbo from the perspective of a regulated exchange. Any operator that wants to offer political or sports markets across the bloc has to navigate a patchwork of national gambling regimes, each with its own licensing, consumer rules and, in some cases, state monopolies. “It means you would have to go for every single European gambling law, because there is no unified regulatory framework,” Prost‑Boucle said. “These laws are pretty national, they’re quite country‑specific and they’re quite hard to get.” Despite that, he is not writing off the region. “I guess we’re still hopeful that at some point we’re going to have regulatory clarity on prediction markets and a better structure in Europe that enables this type of contract to flourish as well,” he said.

Beyond trading revenues, Coinbase clearly sees prediction markets as an information layer that competes with polling, research, and even traditional media. Prost‑Boucle points to cases in the U.S. where broadcasters are already embedding live market odds, such as CNBC, CNN, the Dow Jones and other media recently integrating Polymarket odds into the ‘traditional’ newscycle.

That, in turn, brings the problem of truth into focus. Once markets start pricing geopolitics, conflicts, and leadership changes, disputes over what actually happened can become payout disputes. That means oracles used to resolve contracts may be facing increasing scrutiny from not only bettors, but also regulators.

Prost‑Boucle argues that most of the damage begins with poor contract design. “It’s crucial when you enter a contract to look at what the event criteria are,” he said. “Obviously you want to diversify sources of truth and have kind of fixed criteria to make sure there is no ambiguity when an event like this happens,” he added. Asked whether AI agents could help by aggregating across outlets and delivering a consolidated verdict, he is open but cautious. “Potentially, AI could be helping with sorting out across different sources‑of‑truth venues and making sure that we have a consolidated view and a fixed view that is not biased by any specific media or even a group of people,” he said.

For now, Coinbase’s approach is less about chasing the wildest version of prediction markets and more about proving they can live inside the same rule‑set as everything else on the platform: keep them in a regulated perimeter, pull clearing and risk in‑house via The Clearing Company, and wire the whole thing into a broader multi‑asset venue where collateral actually earns its keep across products. As Brian Armstrong has put it in other contexts, Coinbase wants to be “the most trusted bridge” into the crypto economy, and in that frame, everything else—from MiFID hair‑splitting in Brussels to the next generation of AI‑driven oracles—is just another set of constraints to engineer around, not a reason to sit out a market.

CoinShares, a European-based digital asset manager, is slated to make its US public markets debut today following the completion of a special purpose acquisition company (SPAC) merger, highlighting the crypto industry’s deepening ties with public markets.

The company announced Wednesday that it had finalized a previously announced business combination with Vine Hill Capital Investment Corp., resulting in the formation of a new holding entity, CoinShares PLC. The combined company begins trading on the Nasdaq on Wednesday under the ticker symbol CSHR.

The transaction, first unveiled in September, values CoinShares at approximately $1.2 billion and includes a $50 million capital commitment from institutional investors.

Although the Nasdaq debut marks CoinShares’ entry into US public markets, the company was already publicly traded in Europe prior to the listing.

A US listing aims to attract institutional capital, wider analyst coverage and increased visibility, while positioning CoinShares to expand its footprint in the world’s largest financial market. The move also comes as the regulatory backdrop for digital assets in the United States continues to evolve.

CoinShares manages more than $6 billion in assets and is one of Europe’s largest crypto-focused investment firms. It is best known for its crypto exchange-traded products (ETPs), which are listed on European exchanges.

A tougher backdrop for crypto stocks

The backdrop for digital asset companies has shifted dramatically since September, when CoinShares’ SPAC deal was first announced.

The exchange-traded fund issuer’s CoinShares Bitcoin Mining ETF (WGMI) is down more than 22% in the last six months, Yahoo Finance data shows.

The crypto market has since lost more than half its value, following a broad correction in digital asset prices, declining trading volumes and the fallout from the Oct. 10 crypto liquidation event that triggered widespread deleveraging, alongside a more volatile environment for capital raising and investors.

Crypto-linked equities have been among the hardest hit. Companies such as Coinbase, Gemini and Figure Technologies are down sharply this year, while Circle has bucked the trend amid continued growth in stablecoins.

However, analysts at Bernstein don’t expect the downturn to persist. In a recent note, they said crypto-related stocks could be nearing a bottom heading into first-quarter earnings, which are widely expected to reflect weak performance.

Related: Circle plunged on CLARITY Act fears, but fundamentals unchanged — Bernstein

At Kaiko’s Cannes conference, S&P DJI and Kaiko unveiled plans to tokenize the iBoxx U.S. Treasury index on Canton, turning it into programmable on-chain IP.

Summary

- iBoxx U.S. Treasuries is being brought natively on Canton alongside DTCC’s on-chain Treasuries to support index-linked product issuance on the same infrastructure.

- S&P will distribute the index as a smart contract token embedding full index data, IP rights, licensing terms, fees and access controls.

- The model treats index data “like a financial asset,” enabling traceability, automated fee collection and reusable, scalable licensing on-chain.

At the Agora Kaiko conference in Cannes on March 31, S&P Dow Jones Indices’ Chief Product and Operations Officer Cameron Drinkwater and Kaiko CEO Ambre Soubiran unveiled a partnership to tokenize one of S&P’s flagship fixed-income benchmarks, the iBoxx U.S. Treasury index, on the Canton network, turning the index itself into a programmable on-chain IP product rather than a simple price feed.

New Canton, Kaiko and S&P DGI partnership announced

Kaiko CEO Ambre Soubiran announced that “Kaiko and S&P DGI, we’ve been partnering now in tokenizing one of the biggest S&P benchmarks, the iBoxx index, and bringing that onto the Canton Network.” The move follows DTCC’s decision to bring U.S. Treasuries natively onto Canton (CC), which Drinkwater described as “a natural opportunity for us to bring the iBoxx Treasury index also on Canton to give product developers or counterparties a tool to use with the physical underlying also on that chain.”

Soubiran emphasized this is “not just publishing the price of the benchmark on the network.” Instead, S&P is “actually creating a smart contract token that contains all of the index data,” so that clients receive “a smart contract containing the index data but also explicitly having licensing and fees and access control all embedded into a smart contract.” She framed it as “more about a distribution play rather than a data play,” delivering the full index product on-chain.

Drinkwater said choosing iBoxx was a “total no-brainer” because with DTCC putting U.S. Treasuries on Canton, “you have the underlying” and “a very active kind of treasury institutional trade landscape on Canton” plus “real demand for the iBoxx Treasury index to be used as a underlying for product issuance on the Canton chain.”

On-chain IP and data-as-asset

For S&P, tokenizing indices as full IP products changes how licensing and economics work. Drinkwater argued that “one of the great advantages for an IP issuer like ourselves on chain is we actually have better auditability, visibility in how IP is being used, reporting on that use case and… instantaneous reporting and potentially commercial exchange based on that smart contract.” In traditional markets, he noted, S&P is “dependent on delayed reporting on volumes,” often disputed, followed by “multiple months on contract settlement,” whereas on chain “the whole timeline pulls in quite considerably” with “far less opportunity for dispute.”

Soubiran linked this to a broader shift: “the more we bring capital markets applications on chain, the more we bring data on chain, especially private and IP protected data, the more we need to treat data like a financial asset.” Blockchain infrastructure, she said, enables “traceability of data and treat data like a financial asset and trace where that data goes,” which is “great from a IP protection standpoint” and for “programmatically” managing monetization of IP in financial products.

Drawing on Kaiko’s own index business, she noted that many index fee arrangements are tied to AUM and turnover, with end-of-year reconciliations still “quite heavily manual.” Moving indices on-chain allows firms to “on chain verify what is the AUM related to the financial product that is linked to your index or your benchmark” and enable “daily fee collection based on daily turnover.” It is, she said, “not necessarily a novel product, it’s just a novel way of distributing” existing benchmarks.

Composability, evergreen contracts and Canton

Both speakers highlighted composability as a key benefit of this design. “The idea of tokenizing an index is for product issuers… to consume that index product natively on chain and wrap it into a index-linked financial product,” Soubiran explained, calling the application of composability to data products “extremely new and powerful.”

Drinkwater described the structure as layered: “you can think of the token being the index and then the smart contract being wrapped around it and that’s the use case, the use case specific terms and conditions, audit rights, etc.” That wrapper “can be tailored to whatever use case clients come to us for, but then it’s repeatedly usable. It’s evergreen. It’s on chain.” Compared with today’s model, where “clients have to come to us for every use case, it’s a new schedule on their MSA,” he said this offers “a very frictionless process of getting new product issued on chain, massively speeding up timelines,” and a “reusable infrastructure that really benefits all parties.”

On why Canton matters, Drinkwater pointed to its ability to straddle public and private workflows. On fully public chains like Ethereum, “that reporting is going to be public,” which does not fit “a lot of our use cases” such as “private exchange swaps… between institutions and they don’t want that public.” Canton’s setup, he said, lets reporting be “private when it needs to be private, public where it can be public, but back to us nonetheless,” unifying reporting across use cases in a way that “in TradFi is not the case.”

Soubiran framed the broader aim as servicing “almost a new addressable market that is your existing clients moving to an infrastructure that is programmatic and a little bit more disintermediated,” stressing that “a lot of great things exist in our current financial system,” but that the opportunity lies in “making things more automated… more programmatic in the transfer of information, the transfer of data.”

S&P’s broader digital roadmap

Drinkwater placed the Kaiko and Canton partnership within S&P’s longer digital asset strategy. He recalled that SPY “was not SPY for the first decade of its life, but it flag planted,” and said S&P understands “the power of moving first and establishing real use cases in new technology.” With a brand “known and trusted by institutions and retail alike,” S&P wants “to move first and early when we have conviction in new products and new technologies because we need our brand to be firmly planted there as an established entity.”

Over the last year, he said, S&P has “very selectively” chosen “high quality players as partners and putting IP on chain where we saw very discrete and tangible use cases,” citing the on-chain S&P 500 token with Centrifuge and the Digital Markets 50 index with Genari that bundles blockchain-exposed equities and cryptocurrencies in a structure “hard to replicate in TradFi.” Even so, he signaled he is “most excited about the innovation that we’re pushing today” with tokens wrapped in smart contracts that are “tailored to use cases, but extensible and evergreen on chain,” because this “unlocks so many use cases and scalability of our IP.”

The US Senate could soon hear testimony to confirm financier Kevin Warsh as the new chair of the Federal Reserve.

Warsh, who previously served on the Fed’s Board of Governors from 2006 to 2011, has criticized the central bank’s policies under current chair Jerome Powell. Warsh has called for “regime change” and lower interest rates.

Regarding crypto, Warsh has a somewhat nuanced approach. He hails Bitcoin as a sustainable store of value, but claims it doesn’t function as money.

Lower interest rates and a fairly open attitude toward crypto could be good news for digital asset prices, which most investors perceive as risk-on. But even if Warsh passes his nomination, there’s no guarantee he’ll affect the changes expected.

Warsh wants to lower Fed interest rates, but can he?

Warsh, a graduate of Stanford and Harvard, started his career at Morgan Stanley, where he eventually became a VP and executive director. He then served as an executive secretary of the White House National Economic Council under President George W. Bush.

Bush nominated him to the Board of Governors of the Federal Reserve in 2006, where his hawkish views on inflation often differed from his colleagues. He was critical of the aggressive use of its balance sheet, which he said led to a period of “monetary dominance” that artificially depressed rates.

Some of this appears to have changed in recent years. In a November 2025 op-ed for the Wall Street Journal, Warsh criticized Powell’s leadership at the Fed, claiming that “inflation is a choice, and the Fed’s track record under Chairman Jerome Powell is one of unwise choices.”

He said “credit on Main Street is too tight” and that the Fed’s balance sheet, which is “bloated” due to past crisis-management efforts, “can be reduced significantly.”

“That largesse can be redeployed in the form of lower interest rates to support households and small and medium-size businesses,” he said.

Plans for cutting interest rates come at an economically fraught time. The US and Israel’s joint attack on Iran, which could soon escalate into an invasion if US President Donald Trump so decides, has wreaked havoc on oil prices.

Increasing oil prices had a direct effect on the core inflation metrics the Federal Reserve uses when considering rate changes. This could put the damper on any plans for rate cuts, at least certainly under Powell.

Warsh told Barron’s that the “core theory of inflation that the Fed is using” is “mistaken.” He said that “we need to fundamentally rethink macro, which is a fundamental rethink of the core economic models that the Fed is using.”

In his accounting, rising wages and commodity prices are not to blame for inflation. Rather, “at the core, I think inflation comes about when the government spends too much and prints too much.”

Returning to monetarism, as well as dumping some of the debt held by the Federal Reserve, could help address inflation concerns, in his view.

Bankers and former Bush administration officials have congratulated Warsh on the nomination. Former US Secretary of State Condoleezza Rice said the Fed would “benefit from his steady, principled leadership.”

“He understands the central bank’s key role for the United States and our allies around the world,” she said.

Bank of England Governor Andrew Bailey has also welcomed Warsh’s nomination. He said that he knew both Powell and Warsh well, and that “They’re both very qualified.”

Qualifications aside, Warsh may find it difficult to enact his preferred policies.

Roger W. Ferguson Jr., the Steven A. Tananbaum Distinguished Fellow for International Economics at the Council on Foreign Relations (CFR), and Maximilian Hippold, a research associate for international economics at CFR, wrote that Warsh won’t revolutionize the Fed.

They said that the chair alone does not make inflation rate decisions. “They are determined by the Federal Open Market Committee (FOMC), a twelve-member body that includes seven Fed governors and five regional Fed presidents.” The chair can’t change policy without convincing a majority.

Others argue that Warsh’s interest in lowering interest rates is a recent pivot and may not be a core conviction around which he will focus central bank policy. A December 2025 analysis from Deutsche Bank noted Warsh’s response to the global financial crisis in 2008, when he was a Governor at the Fed.

“His views while he was a Governor around the GFC [global financial crisis] at times skewed more hawkish than his colleagues,” the report read. “Although Warsh has argued for lower rates recently, we do not view him as structurally dovish.”

They further questioned Warsh’s plans to lower interest rates and cut assets on the Fed balance sheet. “This trade-off would only be feasible if regulatory changes are made that lower banks’ demand for reserves. While several Fed officials have made this argument recently, including Vice Chair of Supervision Bowman and Governor Miran, it is not obvious these changes are realistic in the near-term.”

“The chair has just one vote amongst a particularly divided committee.”

Warsh’s nomination and Fed independence

Commentators have also drawn attention to Warsh’s connection to the Trump administration. Warsh’s father-in-law, Ronald Lauder, is a classmate of Trump and a major donor to his political campaigns.

His relatively recent opinions on low interest rates also make him uniquely suited to the role, at least in Trump’s eyes. Ferguson and Hippold wrote, “Trump believes he has found a successor who will align with his economic priorities in Warsh.”

The president has long bemoaned Fed officials who supposedly promise rate cuts, but then raise them once in office. “It’s too bad, sort of disloyalty, but they got to do what they think is right,” he said in a speech at Davos last year.

Trump has long pushed for lower interest rates, claiming that they are needed to spur his economic development plans. Powell’s refusal to acquiesce to the White House’s request led to political scandal.

Last year, the Department of Justice (DoJ) opened a criminal investigation into Powell, alleging that he misappropriated billions of dollars for new offices for the Federal Reserve.

A federal judge recently quashed the DoJ’s subpoenas in the case. Judge James Boasberg wrote in a memorandum opinion, “A mountain of evidence suggests that the dominant purpose is to harass Powell to pressure him to lower rates. For years, the President has publicly targeted Powell because the Fed is not delivering the low rates that Trump demands.”

Regarding his pick, Trump said in a January press event in the Oval Office that it would be “inappropriate” to ask Warsh about his stance on interest rates. “I want to keep it nice and pure, but he certainly wants to cut rates, I’ve been watching him for a long time.”

Just a couple of weeks later, in an interview with NBC, Trump said Warsh understands that he wants to lower interest rates. “But I think he wants to anyway. If he came in and said ‘I want to raise them’ […] he would not have gotten the job.”

But Warsh hasn’t “gotten the job,” at least not yet. He will face tough questioning from Democrats on the Senate Banking Committee, possibly as soon as April 13.

In a letter lambasting Warsh’s role in bailing out banks in 2008, Senator Elizabeth Warren, who serves on the committee, said, “I have no doubt that you will serve as a rubber stamp on President Trump’s Wall Street First agenda.”

Warren expected written responses to this, and to Warsh’s opinion about Trump’s “witch hunts” against Powell and Fed Governor Lisa Cook, by April 2.

Magazine: Nobody knows if quantum secure cryptography will even work

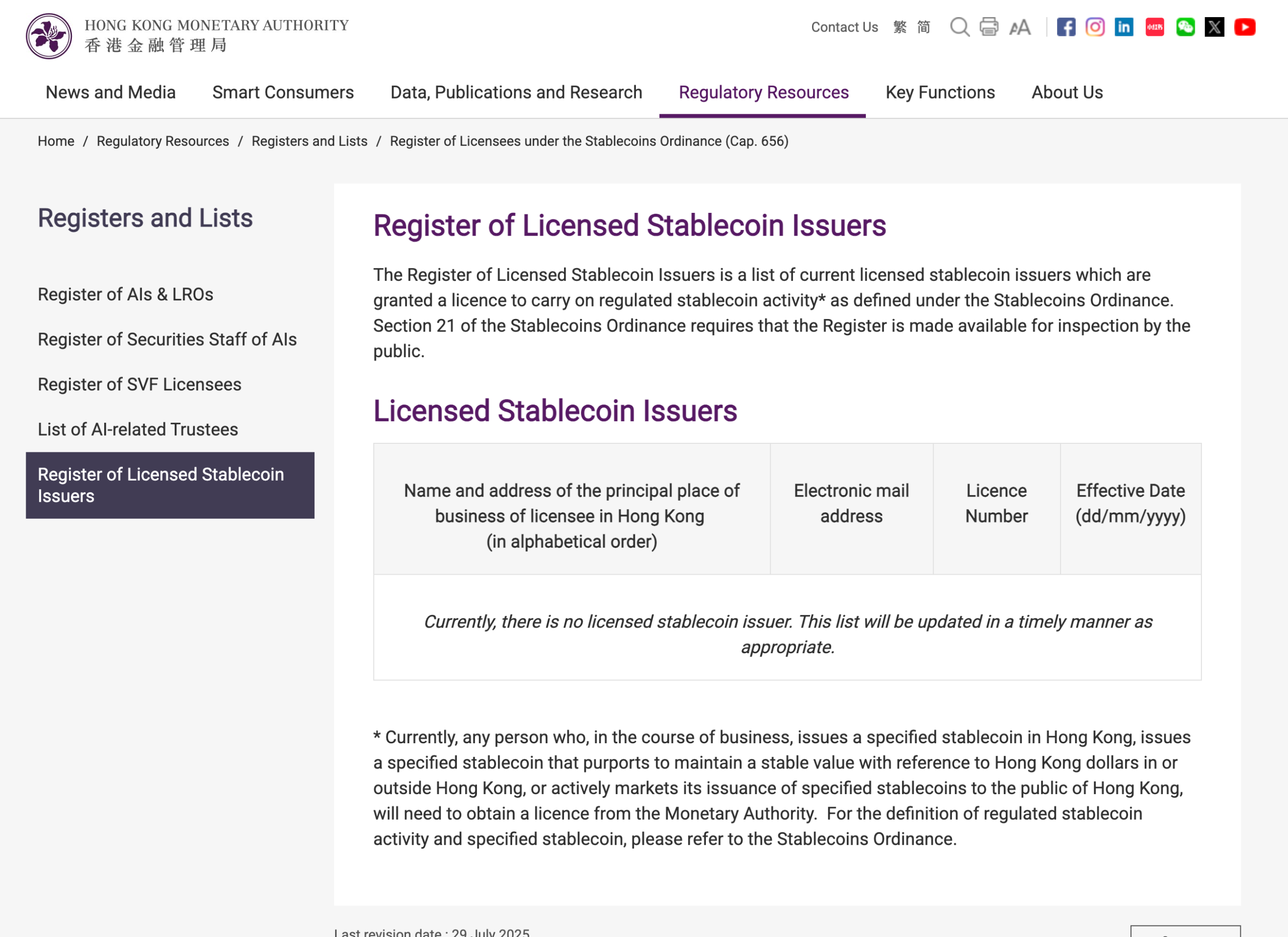

Hong Kong’s first stablecoin licences failed to materialize by the expected end of March target, with the HKMA saying only that it is still advancing the process.

Hong Kong has missed an earlier end of March target for awarding its first stablecoin licences, with the Hong Kong Monetary Authority saying only that the licensing process is advancing and decisions will be announced shortly.

A spokesperson for the Hong Kong Monetary Authority (HKMA) told Cointelegraph that the HKMA is “actively taking forward the licensing matter and will announce further details in due course,” without offering a revised timetable.

The HKMA’s public register still showed no licensed stablecoin issuers at the time of writing.

The March timetable had been set out earlier by HKMA chief executive Eddie Yue, who reportedly told lawmakers in February that only a very small number of issuers would be approved initially and that reviews were focusing on use cases, risk management, anti-money laundering controls and backing assets.

HKMA misses March stablecoin target

Earlier reports indicated that global banking giants HSBC and a Standard Chartered-backed venture were among the frontrunners to receive approvals in the initial cohort, although the HKMA did not confirm the names of any successful applicants.

Hong Kong’s caution is partly a function of how strict the regime is. Cointelegraph previously reported that the city’s stablecoin framework requires issuers to fully back tokens with high-quality liquid reserves, process redemptions within one business day and maintain a physical presence in Hong Kong, alongside broader Know Your Customer and transaction monitoring controls.

The missed deadline comes as Hong Kong places stablecoin regulation at the heart of its strategy to become a global crypto and fintech hub.

China pressure clouds Hong Kong rollout

Cointelegraph previously reported that major fintech players, including Ant International, were preparing to seek Hong Kong stablecoin licenses as the city rolled out its new regime.

Related: How Hong Kong is turning tokenized bonds into real market infrastructure

In October 2025, the FT reported that Ant Group and JD.com had paused their Hong Kong stablecoin plans after regulators in mainland China, including the People’s Bank of China and the Cyberspace Administration of China, raised concerns about privately controlled digital currencies.

Big Questions: Is China hoarding gold so yuan becomes global reserve instead of USD?

Kobbie Mainoo faces clear Man Utd transfer decision after Chelsea complaint

The EU Killed Voluntary CSAM Scanning. West Virginia Is Trying To Compel It. Both Cause Problems.

Swinney calls on PM to recall House of Commons to deal with UK energy ‘crisis’

-

Business6 days ago

Business6 days agoInstagram, YouTube Found Responsible for Teen’s Mental Health Struggle in Historic Ruling

-

Tech6 days ago

Tech6 days agoIntercom’s new post-trained Fin Apex 1.0 beats GPT-5.4 and Claude Sonnet 4.6 at customer service resolutions

-

NewsBeat5 days ago

NewsBeat5 days agoThe Story hosts event on Durham’s historic registers

-

Sports5 days ago

Sports5 days agoSweet Sixteen Game Thread: Tide vs Michigan

-

Entertainment2 days ago

Fans slam 'heartbreaking' Barbie Dream Fest convention debacle with 'cardboard cutout' experience

-

Entertainment4 days ago

Entertainment4 days agoLana Del Rey Celebrates Her Husband’s 51st Birthday In New Post

-

Crypto World2 days ago

Dems press CFTC, ethics board on prediction-market insider trades

-

Tech3 days ago

Tech3 days agoThe Pixel 10a doesn’t have a camera bump, and it’s great

-

Crypto World6 hours ago

Crypto World6 hours agoGold Price Prediction: Worst Month in 17 Years fo Save Haven Rock

-

Sports1 day ago

Sports1 day agoTallest college basketball player ever, standing at 7-foot-9, entering transfer portal

-

Tech2 days ago

Tech2 days agoEE TV is using AI to help you find something to watch

-

Tech2 days ago

Tech2 days agoApple will hide your email address from apps and websites, but not cops

-

Entertainment7 days ago

Entertainment7 days agoHBO’s Harry Potter Series Will Definitely Fail For One Big Reason, And It’s Not J.K. Rowling Or Snape

-

Tech2 days ago

Tech2 days agoFlipsnack and the shift toward motion-first business content with living visuals

-

Tech2 days ago

Tech2 days agoHow to back up your iPhone & iPad to your Mac before something goes wrong

-

Fashion6 days ago

Fashion6 days agoEn Vogue in Brown Leather and Tailored Neutrals by Atelier Savoir, Styled by J Bolin

-

Politics2 days ago

Politics2 days agoShould Trump Be Scared Strait?

-

Crypto World2 days ago

Crypto World2 days agoU.S. rule change may open trillions in 401(k) funds to crypto

-

Fashion6 days ago

Fashion6 days agoWhat Are Your Favorite T-Shirts for the Weekend?

-

Fashion5 days ago

Fashion5 days agoWeekly News Update, 3.27.26 – Corporette.com

You must be logged in to post a comment Login