Crypto World

Anyone Can Print Credit Now

The Rise of Permissionless Credit Creation

Introduction

For centuries, the ability to create and extend credit has been tightly controlled by centralized financial institutions. Banks, acting as gatekeepers, determined who could borrow, at what cost, and under what conditions. This structure concentrated power, limited access, and introduced inefficiencies that often excluded large segments of the global population.

Today, a new paradigm is emerging—permissionless credit creation. Built on a decentralized financial infrastructure, this model enables anyone with capital and an internet connection to participate as a lender. It represents a fundamental shift in how credit is created, distributed, and priced.

From Gatekeepers to Open Access

Traditional credit systems rely on intermediaries to assess borrower risk, allocate capital, and enforce repayment. These intermediaries introduce friction, increase costs, and often restrict access based on geography, identity, or credit history.

Permissionless systems remove these barriers. Through blockchain-based protocols, individuals can directly supply capital to lending markets without requiring approval from a central authority. Participation is no longer determined by institutional criteria but by ownership of digital assets and willingness to engage with transparent, open systems.

This shift transforms credit from a controlled resource into a globally accessible financial primitive.

Anyone Can Become a Lender

In a permissionless environment, the role of a lender is no longer exclusive to banks or financial institutions. Individuals can allocate their assets into decentralized liquidity pools, where they are algorithmically matched with borrowers.

This democratization of lending introduces several key dynamics:

- Capital Efficiency: Idle assets can be deployed to generate yield.

- Global Reach: Lenders can serve borrowers across jurisdictions without friction.

- Continuous Liquidity: Markets operate 24/7, unconstrained by traditional banking hours.

The result is a system where capital flows more freely and efficiently, driven by incentives rather than institutional mandates.

Credit Markets Without Banks

At the core of permissionless credit systems are smart contracts—self-executing code that enforces the rules of lending and borrowing. These contracts replace many functions traditionally performed by banks, including:

- Loan issuance

- Collateral management

- Interest rate calculation

- Liquidation processes

Because these mechanisms are encoded and transparent, they reduce reliance on trust and eliminate many operational inefficiencies. Borrowers can access credit instantly, provided they meet the protocol’s requirements, typically in the form of overcollateralization.

While this model differs from traditional unsecured lending, it establishes a foundation for more complex and nuanced credit systems to evolve.

Algorithmic Risk Pricing

One of the most significant innovations in permissionless credit creation is algorithmic risk pricing. Instead of relying on human judgment or opaque credit scoring systems, decentralized protocols use real-time market data to determine interest rates and risk parameters.

These systems dynamically adjust based on:

- Supply and demand for capital

- Volatility of collateral assets

- Utilization rates within lending pools

As a result, interest rates become market-driven signals rather than institutionally imposed figures. This creates a more responsive and adaptive credit environment, where risk is continuously assessed and priced in real time.

Advantages of Permissionless Credit

The emergence of permissionless credit systems introduces several transformative benefits:

- Financial Inclusion: Individuals without access to traditional banking can participate in global credit markets.

- Transparency: All transactions and rules are visible on-chain, reducing information asymmetry.

- Efficiency: Automation reduces administrative overhead and operational delays.

- Resilience: Decentralized systems are less vulnerable to single points of failure.

These advantages position permissionless credit as a powerful alternative to legacy financial systems, particularly in regions underserved by traditional institutions.

Risks and Limitations

Despite its potential, permissionless credit creation is not without challenges:

- Overcollateralization Requirements: Many systems require borrowers to lock more value than they borrow, limiting accessibility.

- Smart Contract Risk: Vulnerabilities in code can lead to significant financial losses.

- Market Volatility: Rapid price fluctuations can trigger liquidations and amplify systemic risk.

- Regulatory Uncertainty: Evolving legal frameworks may impact adoption and operation.

Addressing these limitations will be critical for the long-term sustainability and scalability of permissionless credit systems.

The Future of Credit

Permissionless credit creation represents more than a technological innovation—it is a redefinition of financial power. By removing intermediaries and enabling open participation, it shifts control from centralized institutions to decentralized networks.

As infrastructure matures, we can expect the development of:

- Undercollateralized and reputation-based lending models

- Cross-chain credit markets

- Integration with real-world assets and identities

These advancements will further blur the line between traditional finance and decentralized systems, potentially leading to a hybrid global credit network.

Conclusion

The ability to create credit has long been one of the most powerful tools in finance. With the rise of permissionless systems, that power is no longer confined to banks.

Anyone can now participate in credit creation—allocating capital, pricing risk, and earning yield in a transparent, global marketplace. While challenges remain, the trajectory is clear: credit is becoming open, programmable, and accessible to all.

The question is no longer who is allowed to lend.

It is how this newfound power will reshape the financial world.

REQUEST AN ARTICLE

Crypto World

Bitcoin Price Prediction Faces Strategy Earnings Pause While Whales Buy 270,000 BTC and Pepeto Presale Goes Viral, Here Is What You Need To Know

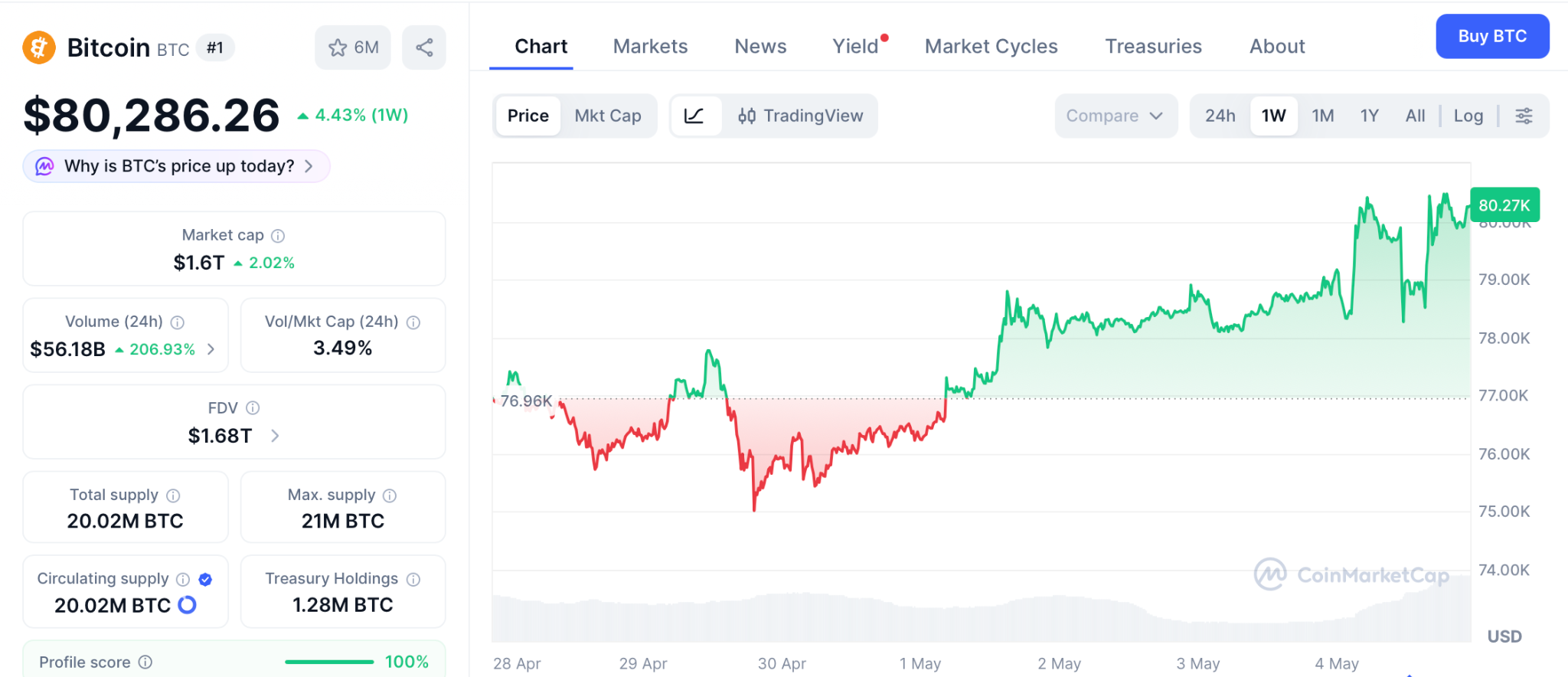

The bitcoin price prediction for May 2026 depends on what happens after Strategy reports Q1 earnings on May 5, according to CoinDesk. Michael Saylor paused weekly Bitcoin buys for only the second time this year, but told followers on X that purchases resume next week.

The bitcoin price prediction sits at a turning point because BTC trades near $80,286 after touching $80,393, its highest since January. The market is consolidating before the breakout every cycle produces after the halving. April 2024 halving, twelve months of sideways, then the move that reprices everything. The traders who position during the pause capture the full return.

While Strategy holds 818,334 BTC at $75,537 cost basis, Pepeto raised $9.89M from wallets not waiting for any earnings report. The presale fills because exchange tools are built, the Binance listing is approaching, and the bitcoin price prediction debate is exactly the distraction that lets early buyers enter.

CoinDesk reported Strategy paused its weekly Bitcoin buys ahead of Tuesday Q1 earnings, stopping a pattern that moved $5.5 billion into BTC last quarter alone. But whale wallets bought 270,000 BTC over the past 30 days and exchange reserves dropped to a seven year low not seen since December 2017, right before BTC broke $20,000 for the first time.

When the largest corporate buyer pauses but whales speed up buying and exchange supply hits multi year lows, the bitcoin price prediction signals the breakout is forming, and presale entries positioned with exchange tools capture the move before charts confirm it.

The Consolidation Before the Breakout Is Where the Biggest Returns Get Built

Pepeto: The Presale Filling Faster Than the Bitcoin Price Prediction Can Move BTC From $80,286

Every Bitcoin cycle follows the same sequence, and every time it happens, the majority miss the best entry because they wait for confirmation that arrives after the move started. April 2024 was the halving. May 2026 is month thirteen. The bitcoin price prediction is entering the phase where the chart breaks higher, and the wallets positioned before that move keep the return late arrivals pay for.

Pepeto raised $9.89M during this consolidation window because the exchange already runs. The cross chain bridge connects Ethereum, BNB Chain, and Solana so traders stop paying triple fees, PepetoSwap removes trading costs so every position keeps full value, and before your capital touches anything the risk scoring system reads every contract for hidden drains. Every line of code passed the SolidProof audit, and the cofounder who built the original Pepe token to $7 billion leads the team.

Tracking the bitcoin price prediction means watching BTC go from $80,286 toward $150,000, a decent return over months on an asset that needs hundreds of billions to move 90%. One Binance listing event is where presale wallets collect the return the BTC target takes all year to deliver.

At $0.0000001868 with 175% APY compounding daily, the math favors wallets inside. The entry disappears after the listing, and the gap between entering now and entering after the breakout is the gap between making the return and paying for it.

Bitcoin (BTC) Price at $80,286 as Halving Cycle Points to Breakout

BTC hit $80,393 on May 4 before pulling back to $80,286, its highest since January, according to CoinMarketCap. Strategy holds 818,334 BTC at $75,537 cost basis, whales bought 270,000 BTC in 30 days, and exchange reserves sit at a seven year low.

The all time high of $126,198 from October 2025 sits 58% above, Standard Chartered targets $150,000, and BTC needs to close above the 200 day moving average at $82,228 to confirm the bitcoin price prediction breakout.

Conclusion

Strategy paused its buys, but whales bought 270,000 BTC in a single month and exchange reserves hit a seven year low. The bitcoin price prediction signals the breakout is forming, and the consolidation window where the biggest entries get built is closing fast.

Pepeto crossed $9.89M while the market debated earnings, the Binance listing is approaching, 175% APY compounds daily, and stages fill faster each round. The wallets entering right now are buying at a number the market will never see again after the listing. Visit Pepeto and enter the presale before the breakout arrives and the entry you see today becomes the most expensive hesitation of this cycle.

Click To Visit Pepeto Website To Enter The Presale

FAQs

What is the bitcoin price prediction after Strategy pauses buys ahead of earnings?

The bitcoin price prediction targets $150,000 by year end as BTC trades near $80,286 with whales buying 270,000 BTC in 30 days and exchange reserves at a seven year low. Pepeto at $9.89M raised with a Binance listing approaching offers the returns BTC at $1.33 trillion cannot match, visit Pepeto.

Why is Pepeto filling during Bitcoin consolidation?

Pepeto is filling because the exchange tools are built, the SolidProof audit cleared every contract, and the Binance listing is approaching. At $9.89M raised and 175% APY staking, early wallets compound returns daily before the listing reprices the token permanently.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

Crypto World

How SHRMiner AI cloud mining is reshaping how to easily earn $9,997 in passive income in 2026

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

AI cloud mining expands access as SHRMiner lowers barriers to crypto mining participation in 2026.

Summary

- Cloud mining platforms like SHRMiner lower barriers, enabling easy entry into crypto mining.

- SHRMiner uses AI and smart contracts to simplify mining with real-time tracking.

- With low entry and flexible contracts, SHRMiner offers accessible, automated crypto earning options.

As the global technological landscape continues to evolve in 2026, more and more people are exploring passive income opportunities in the digital economy. Technologies such as smart contracts, cloud mining, and cross-chain asset deployment are gradually reshaping how individuals interact with cryptocurrencies.

Blockchain-based cloud mining platforms are rapidly emerging, providing users with a more user-friendly and convenient alternative. Compared to traditional mining, which requires high hardware investment, complex maintenance, and a high technical barrier, cloud mining lowers the barrier to entry, allowing ordinary users to easily enter the crypto ecosystem. The deep integration of the blockchain ecosystem is opening up new and sustainable passive income avenues for the public.

One of the most notable developments is the rise of the SHRMiner AI-driven cloud mining platform. This platform streamlines the mining process by leveraging automation, smart contracts, and AI-driven resource allocation. These eliminate physical barriers, enabling users to participate in mining activities with extremely low barriers to entry.

Why investing in SHRMiner is worthwhile

Zero entry barrier: Register to receive a free $15 computing power reward, earning $0.60 daily.

Access all miner information in real-time via the mobile app control panel.

Fully own your hardware: No third-party risk.

Mining, tracking earnings, and reinvesting: All operations are handled by the same platform.

A new landscape in the mining industry: Secure, flexible, and profitable.

With SHRMiner, users don’t need to be a technical expert or pay exorbitant electricity bills. You can directly invest in high-performance mining: completely transparent, with stable daily earnings.

SHRMiner offers a variety of high-yield cloud mining contract options to meet the investment preferences and financial goals of different users. Whether seeking flexible short-term returns or valuing stable long-term returns, users can find a suitable option on the platform.

Intelligently allocated, high-yield mining contracts allow wealth growth to begin today.

Contract profit example:

| Contract Name | Price | Profit | Days | Principal + Total Return |

| New User Experience Agreement | $100 | $4 | 2 | $100+$8 |

| Bitdeer Sealminer A2 Pro | $500 | $6.25 | 5 | $500.00 + $31.25 |

| Litecoin Miner L9 | $1000.00 | $13.00 | 10 | $1000.00 + $130 |

| Bitcoin Miner S21 XP Imm | $5000.00 | $70.00 | 25 | $5000.00 + $1750 |

| Bitcoin Miner S21e XP Hyd | $10000.00 | $150.00 | 35 | $10000.00 + $5250 |

| ANTSPACE HW5 | $50000.00 | $900.00 | 45 | $50000.00 + $40500 |

For example, by leasing the hash power of an ANTSPACE HW5 mining rig, users can earn $900 in Bitcoin rewards daily. They can track earnings in real time through the control panel.

Click here for more contract details.

Easy mining: Located in an affordable location with modern infrastructure

SHRMiner is a service provider that allows users to easily get started with cryptocurrency mining. The company operates 150 highly specialized data centers in regions with extremely low electricity costs, such as the US, Europe, and the UAE. It allows you to profit from mining Bitcoin or altcoins without any technical knowledge.

Is SHRMiner legal? What about its transparency, security, and trustworthiness?

Given the skepticism surrounding cryptocurrency mining websites, it’s natural to ask: Is SHRMiner legitimate?

- The company is registered in the UK and holds a UK operating license, ensuring compliance and transparency.

- There are no extra service fees or hidden charges.

- Supports mining in multiple currencies: Earn XRP, BTC, ETH, DOGE, USDC, USDT, SOL, LTC, BCH and other mainstream cryptocurrencies.

- 100% remote access; track earnings in real time via the SHRMiner application or platform website without hardware requirements.

- Protected by McAfee® and Cloudflare® security, ensuring the safety of user account funds.

- We offer 100% uptime guarantee and 24/7 online technical support.

Conclusion: Is SHR Miner a good passive income tool?

The answer is yes — its advantage lies precisely in its AI-driven cloud mining. It offers a sustainable, transparent, and minimally invasive way to generate passive income through legitimate Bitcoin mining infrastructure, setting it apart from other Bitcoin mining applications.

For those wondering if Bitcoin mining will be profitable in 2026, SHR Miner would be a wise choice for earning passive income.

For more details, please visit the official platform or download the mobile application.

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

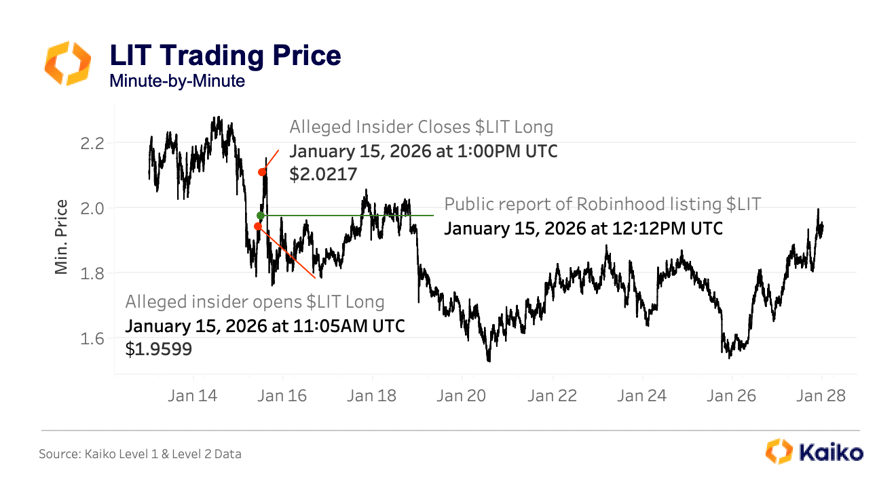

Open interest in perpetual futures markets and onchain trading patterns suggest some traders may have positioned ahead of Robinhood crypto listing announcements, according to a Monday report from analytics provider Kaiko.

One of the clearest examples was wallet address ‘0xa1E,’ which Kaiko said opened a long position on Lighter (LIT) on decentralized exchange Hyperliquid at 11:05 am UTC on Jan. 15, about an hour before Robinhood announced the token’s listing at 12:12 pm The wallet closed the position at 1:00 pm, shortly after the announcement.

Kaiko said the same address later opened a short position on a HOOD-linked perpetual contract on April 28, hours before Robinhood reported first-quarter revenue that missed analyst expectations. The trader closed the short later that day after HOOD moved lower.

The trading patterns raise questions about whether some market participants had access to non-public listing information or had developed a reliable method for detecting public signals before announcements. Kaiko also said sophisticated traders may have been reacting to funding-rate spikes, volume increases and open-interest changes rather than inside information.

Multiple other wallets made similar moves just before a listing was made public, raising the question of whether “more than one participant had access to the same information ahead of the announcement,” wrote Laurens Fraussen, a research analyst at Kaiko.

LIT trading price, listing time, minute-by-minute. Source: Kaiko

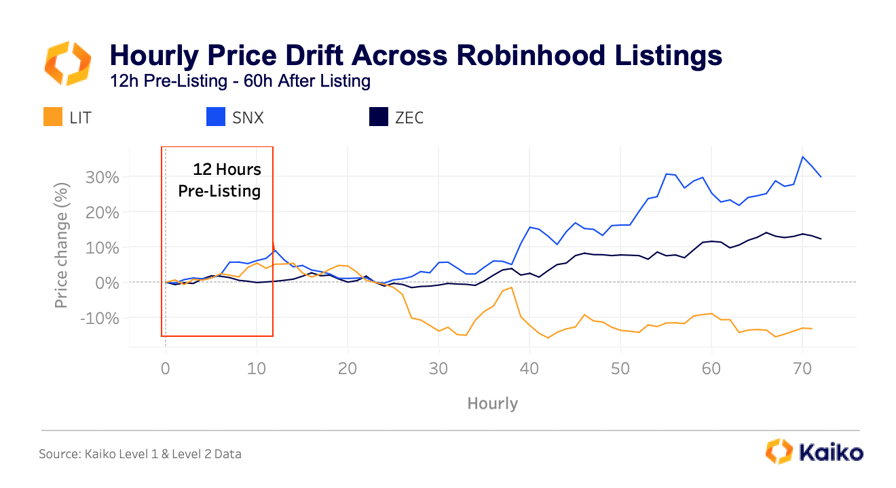

Hyperliquid data points to unusual pre-listing trades

Kaiko pointed to multiple cryptocurrency listings that led to a surge in open interest and funding rates just ahead of Robinhood’s public listing announcements, including Zcash (ZEC), Synthetix (SNX) and the Near Protocol (NEAR) tokens, among other assets.

Hourly price drift ahead of Robinhood listing announcements for LIT, SNX and ZEC. Source: Kaiko

All three tokens recorded a pre-announcement price drift, with each coin averaging abnormal returns in the hours leading up to and following the listing announcement, explained the report.

Related: Crypto VC funding plunges to $659M in April, hits near two-year low

While the data raises concerning signs of potential insider activity, it may also indicate that some of the smartest traders are positioning based on funding or volume increases, Kaiko’s Fraussen told Cointelegraph.

“Traders that know how microstructure works could have noticed the funding spikes, increase in volumes and open interest spikes, and position based on that.”

Still, derivatives metrics show that this type of positioning was statistically consistent and repeated across multiple asset listings, reflecting either “privileged access to Robinhood’s listing pipeline” or an “exceptionally reliable front-running methodology built on public signals.”

Magazine: Bitcoiners eye ‘sell in May,’ SBF’s bid for new trial shut down: Hodler’s Digest, April 26 – May 2

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

AJC Mining’s free cloud mining service gives global users an easy way to join the crypto market and explore higher earning opportunities amid Bitcoin’s latest rally.

Summary

- AJC Mining offers a simple, hardware-free way to explore Bitcoin and crypto mining online.

- With no setup or technical skills needed, AJC Mining makes mining accessible to beginners.

- AJC Mining enables 24/7 cloud mining with an easy dashboard and daily tracking.

The global cryptocurrency market is entering a new wave of momentum as Bitcoin recently climbed above the $80,000 level, supported by strong Bitcoin ETF inflows and renewed optimism around U.S. crypto legislation. Market reports showed that Bitcoin ETFs recorded approximately $629.37 million in inflows, while crypto-related stocks also rallied after progress on a bipartisan U.S. digital asset market structure bill.

As Bitcoin returns to the center of global investor attention, more users are looking for simple ways to participate in the digital asset economy. One of the fastest-growing search trends is cloud mining, especially among users searching for Bitcoin cloud mining, crypto cloud mining, cloud miner, free cloud mining, Bitcoin cloud mining free, and free cloud mining site without deposit.

Against this positive market backdrop, AJC Mining is introducing a smart, automated cloud mining platform designed for users who want easy access to crypto mining without purchasing equipment, managing technical systems, or operating mining machines.

AJC Mining brings cloud mining to everyday users

AJC Mining is a cloud mining platform built for simplicity, accessibility, and automated participation. The platform allows users to explore cryptocurrency mining through an online account system, making it easier for beginners to access mining opportunities without traditional hardware barriers.

Traditional mining often requires expensive mining machines, electricity management, cooling systems, technical configuration, and daily maintenance. AJC Mining simplifies the entire process by offering a cloud-based model where users can participate through digital mining plans and monitor account activity online.

For users searching for a reliable cloud miner experience, AJC Mining provides a streamlined way to explore Bitcoin cloud mining and crypto cloud mining from anywhere.

Why cloud mining is gaining momentum after Bitcoin’s latest rally

Bitcoin’s recent move above $80,000 has created renewed excitement across the crypto sector. Barron’s reported that Bitcoin moved back above $80,000 for the first time since late January 2026, while broader crypto stocks also gained as market confidence improved.

This market strength is helping drive interest in easier crypto participation models. Cloud mining gives users a simple way to join the mining economy without owning physical mining hardware.

Instead of buying ASIC miners or building technical mining systems, users can access mining services through platforms like AJC Mining. This makes cloud mining attractive to beginners, mobile users, and global crypto participants who want a convenient entry point.

Key advantages of AJC Mining

1. No mining equipment required

One of the biggest advantages of AJC Mining is that users do not need to buy mining hardware.

With AJC Mining, users can participate in Bitcoin cloud mining and crypto cloud mining through the platform’s online system. There is no need to purchase ASIC miners, graphics cards, power supplies, cooling devices, or mining accessories.

This makes AJC Mining especially attractive for users who want a lower-barrier way to enter the mining market.

2. No technical experience needed

AJC Mining is designed for users with no mining background.

Users do not need to install mining software, configure mining pools, update firmware, or monitor physical mining machines. The platform provides a simple account dashboard where users can view mining activity, track estimated output, and manage participation options.

This beginner-friendly structure makes AJC Mining suitable for users searching for cloud mining, crypto cloud mining, and a simple cloud miner platform.

3. 24/7 automated cloud mining system

AJC Mining promotes a fully automated cloud mining system that operates 24/7.

The platform is designed to support continuous mining activity and daily account settlement. Users can participate without manually running equipment or managing technical operations.

This automated model helps make cloud mining more convenient for global users who want a simple, online-first mining experience.

4. Free cloud mining for new users

Free cloud mining is one of AJC Mining’s most attractive entry points.

New users may receive a $15 welcome bonus after registration. Eligible users can also participate in daily free cloud mining activity with an estimated daily output of $0.60.

Click to register now and claim a $15 new user bonus.

This makes AJC Mining highly relevant for users searching for:

- free cloud mining

- Bitcoin cloud mining free

- free cloud mining site without deposit

For beginners, the free mining option provides an easy way to experience the platform before choosing additional mining plans.

AJC Mining cloud mining plans and estimated output

AJC Mining offers multiple cloud mining participation options designed for users with different goals and account sizes. The platform’s example plans highlight flexible participation and daily estimated output.

| Contract Name | price | Daily Profit | Contract Term | Principal + Total Returns |

|---|---|---|---|---|

| Daily Check-in Contract | $15 free | $0.6 | 1 jours | Once daily |

| New User Experience Contract | $100 | $4 | 2 jours | $100 + $8 |

| Avalon Miner A15 | $500 | $6.25 | 5 jours | $500 + $31.25 |

| Litecoin Miner L9 | $1000 | $13 | 10 jours | $1000 + $130 |

| Bitcoin Miner S21 XP Imm | $5000 | $70 | 25 jours | $5000 + $1750 |

| Bitcoin Miner S21e XP Hyd | $10000 | $150 | 35 jours | $10000 + $5250 |

| ANTSPACE HW5 | $50000 | $900 | 45 jours | $50000 + $40500 |

These sample scenarios are designed to help users understand AJC Mining’s participation structure and estimated daily output options.

Click to view all cloud mining contracts.

Referral rewards create additional user benefits

AJC Mining also offers referral rewards to users who invite others to join the platform. Click to view affiliate rewards.

The referral mechanism includes:

- Level 1 reward: 3%

- Level 2 reward: 1.5%

This gives users additional participation opportunities within the AJC Mining ecosystem. Users who share the platform with friends, crypto communities, or online networks may access extra rewards based on eligible referral activity.

The combination of cloud mining output and referral rewards makes AJC Mining appealing to users who want a more active role in the platform’s growth.

Daily settlement and withdrawal convenience

AJC Mining highlights daily account settlement, allowing users to view mining activity and estimated output on a regular basis.

The platform also promotes withdrawal options for eligible users, creating a more flexible cloud mining experience. For users who value convenience, daily tracking and account visibility are important features that make the platform easier to use.

This is one reason AJC Mining is positioned as a user-friendly cloud miner platform for global crypto participants.

Why AJC Mining fits the current crypto market trend

The crypto market is becoming more accessible. Bitcoin ETFs have brought institutional capital into the market, while progress around U.S. crypto regulation is helping improve confidence across the digital asset industry. Recent reports showed crypto companies and Bitcoin-related stocks gaining after positive developments around stablecoin and market structure legislation.

At the same time, Bitcoin’s move above $80,000 has renewed public interest in digital assets. As more users search for simple crypto participation methods, cloud mining is becoming a natural entry point.

AJC Mining fits this trend by offering:

- Simple registration

- Free cloud mining opportunities

- No hardware requirements

- No technical setup

- 24/7 automated mining system

- Daily account settlement

- Flexible mining plans

- Referral reward opportunities

For users searching Google for cloud mining, Bitcoin cloud mining, crypto cloud mining, cloud miner, free cloud mining, Bitcoin cloud mining free, and free cloud mining site without deposit, AJC Mining provides a clear and beginner-friendly solution.

AJC Mining and the future of cloud mining

Cloud mining is becoming an important part of the next stage of crypto adoption. As digital assets become more mainstream, users want platforms that are easier to access, simpler to understand, and more convenient to use.

AJC Mining is designed to meet this demand by giving users access to cloud-based mining participation without the complexity of traditional mining.

With Bitcoin gaining renewed market momentum and institutional demand continuing to grow, cloud mining platforms like AJC Mining are positioned to attract users who want a simple way to explore crypto mining online.

Conclusion

Bitcoin’s latest rally above $80,000, strong ETF inflows, and improving crypto market confidence have created a positive environment for cloud mining platforms. As more users search for accessible ways to participate in the digital asset economy, AJC Mining is gaining attention as a smart and beginner-friendly cloud mining platform.

With no mining hardware required, no technical skills needed, 24/7 automated operation, free cloud mining opportunities, daily settlement, flexible plans, and referral rewards, AJC Mining offers a simple path for users exploring Bitcoin cloud mining and crypto cloud mining.

For users looking for cloud mining, cloud miner, free cloud mining, Bitcoin cloud mining free, or a free cloud mining site without a deposit, AJC Mining provides a convenient entry point into the cloud mining market.

For more information, visit the official website and download the mining app.

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

Bitcoin miners are turning to AI infrastructure to ramp up revenues, and some treasury firms are joining in on the rotation too.

K Wave Media (KWM), a Nasdaq-listed Korean media and entertainment firm, told the U.S. Securities and Exchange Commission on Monday that it is redirecting up to $485 million in remaining financing capacity away from a planned bitcoin treasury push and into AI infrastructure.

The money will flow into data centers, GPU compute operations and acquisitions across the AI value chain, under an amended agreement with structured equity financier Anson Funds.

The original $500 million facility was set up in June 2025 explicitly to buy bitcoin, part of K Wave’s effort to reposition itself in capital markets at a time when bitcoin treasury announcements were doing more for share prices than the underlying businesses were.

Less than a year later, that thesis has been retired in favor of a sector with newer momentum.

Investors did not love the pivot. K Wave shares closed down 24% on Monday, and are down 4% in premarket trading on Tuesday.

Chief executive Ted Kim termed the redirection as an ambition to become “a meaningful participant in the rapidly growing AI infrastructure sector,” with plans to build a scalable platform across compute and related technologies.

The company is also punting on a corporate rebrand to “Talivar Technologies,” pending shareholder approval at the annual meeting in early July.

The shift fits a pattern that has been quietly building for months.

CoinDesk reported in March that publicly listed bitcoin miners had collectively zoomed toward AI and high-performance computing, signing more than $70 billion in cumulative contracts and shedding over 15,000 BTC from peak treasury levels to finance the transition. Core Scientific sold roughly 1,900 BTC worth $175 million in January. Bitdeer drained its treasury to zero in February. Riot Platforms sold 1,818 BTC worth $162 million in December.

The miners were forced into it, as the weighted-average cash cost to produce one bitcoin among publicly listed miners hit approximately $79,995 in Q4 2025, while bitcoin spent most of 2026 below that figure.

AI infrastructure contracts, meanwhile, promise margins above 85% with multi-year revenue visibility.

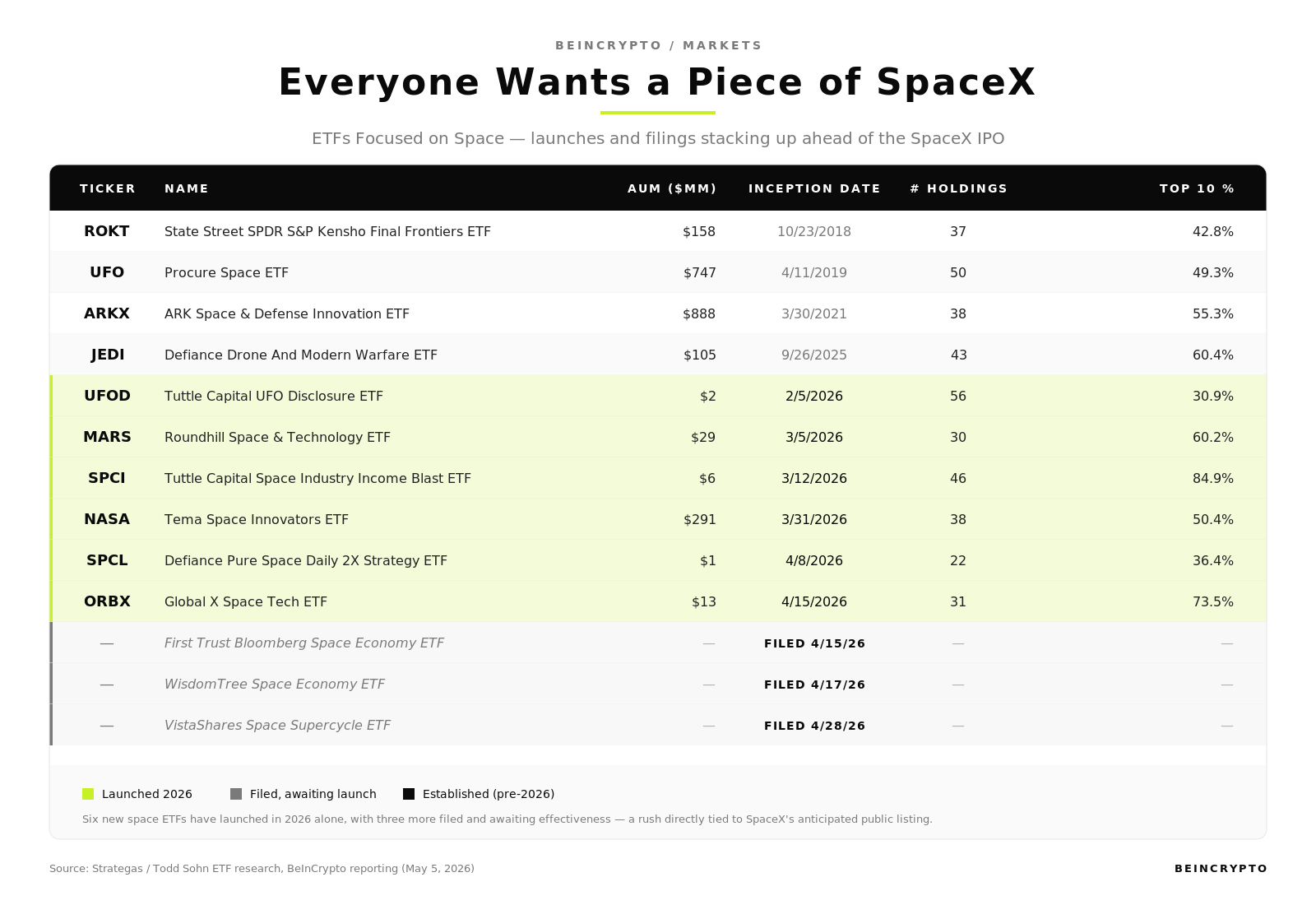

ETF issuers have filed or launched nine space-themed funds in three months, racing to capture flows before SpaceX’s public listing. According to ETF analyst Eric Balchunas, it is a wave bigger than the booms around Facebook or Alibaba.

The buildup ranks among the most aggressive thematic ETF pushes in years. Wall Street is staking branding rights and retail dollars on a single private company expected to set a fundraising record.

Nine New Funds in Three Months

Roundhill Space & Technology ETF (MARS) debuted March 5. Tuttle Capital’s Space Industry Income Blast (SPCI) followed March 12, and Tema’s Space Innovators ETF (NASA) arrived later that month.

April brought Defiance’s Pure Space Daily 2X (SPCL) on April 8 and Global X’s Space Tech ETF (ORBX) in mid-April. First Trust, WisdomTree, and VistaShares filed paperwork for additional space economy products in the same window.

“All this for Space X IPO. Never seen anything like it.. Facebook, Alibaba were big but this is another level,” Balchunas remarked.

A few of these funds offer indirect SpaceX exposure today through private vehicles. Others sit ready to absorb the stock once it lists.

Older entrants are tweaking methodology. The list includes Cathie Wood’s ARK Space & Defense ETF (ARKX), Procure’s UFO, and State Street’s ROKT.

Why Issuers Are Racing

SpaceX confidentially filed its S-1 with the SEC in early April. The company targets a June listing at a valuation potentially exceeding $1.5 trillion.

Elon Musk has floated a retail allocation near 30%, several times the typical IPO carve-out, fueling demand from individual investors.

Existing funds already feel the pull. Procure Space ETF (UFO) drew record inflows of $175 million in the first quarter, its biggest haul since 2019.

Crowding cuts both ways, in the sense that:

- Many new products hold overlapping names, and

- A delayed or weak debut could leave several searching for a thesis.

Crypto exchanges have rolled out synthetic SpaceX tokens, adding speculation to an equity story yet to unfold.

Whether the field consolidates or expands may hinge on the listing’s reception.

The post Space-Themed ETFs are Flooding Wall Street Before Elon Musk’s SpaceX IPO appeared first on BeInCrypto.

Jito Labs, a core infrastructure provider on Solana, has unveiled JTX, a new crypto trading platform aimed at bringing more advanced trading tools to the blockchain.

Announced at the Solana Accelerate conference in Miami, Florida, JTX is the company’s first product built specifically for traders. It allows users to trade tokens on Solana while maintaining self-custody, meaning they have full control of their funds unlike other set ups that have to hand assets over to a centralized exchange like Coinbase or Binance.

JTX is designed to feel more like those centralized platforms, the team shared in a press release with CoinDesk. It is supposed to offer faster trade execution and a range of tools typically used by professional traders, including stop-loss orders, preset trade strategies and detailed market charts powered by TradingView.

The launch comes as trading activity on Solana has surged, Jito Labs claimed, with decentralized exchanges on the network processing over $1 trillion in volume last year. Much of the more sophisticated trading still happens on centralized platforms or other blockchains.

Jito is betting that demand for more advanced, onchain trading will keep growing, with JTX expecting to come out with products like perpetual futures and prediction markets. In addition, a large portion of the revenue generated by JTX will go back to the protocol, benefiting holders of its JTO token.

JTX is currently open for sign-ups via a waitlist, with early access expected soon.

“Solana’s infrastructure is the best in the world, processing more daily transactions than every other blockchain combined,” said Lucas Bruder, the CTO at Jito Labs. “JTX is what happens when we point that at traders who’ve outgrown what’s currently being built for them. It beats a CEX on execution. It doesn’t take your keys. That’s the pitch.”

Read more: Jito Foundation acquires and revives SolanaFloor following shutdown over $27 million exploit

The American Innovation Project (AIP), a non-profit advocacy group, has added a crypto policy specialist to its ranks as it expands its work on digital asset legislation.

Jacob Smagula, a 2026 graduate of Claremont McKenna College, will join Democratic Representative Ritchie Torres’ (D-NY) team, AIP said. Smagula brings a background in crypto policy and industry affairs, having worked on the government relations team at publicly traded bitcoin miner MARA and currently serving on the policy team at the DeFi Education Fund.

He has also held roles on Capitol Hill, including internships with Representative Jake Auchincloss and Senator Angus King.

Smagula’s appointment comes as part of AIP’s Policy Innovation Fellowship, a two-part program designed to give congressional staff hands-on exposure to emerging technologies and direct experience in Congress.

AIP also named Hugo Swangstu, a 2025 graduate of the University of Washington, as a fellow. Swangstu previously interned for Representative Adam Smith and Representative Torres and will serve in the Washington office of Representative Shomari Figures (D-AL).

“The next generation of policymakers must understand the technologies reshaping our economy, national security, and daily lives,” Torres said.

Figures added that “as technology continues to advance at a rapid pace, it’s essential that Members of Congress are informed and prepared to craft sound tech policy.”

Allie Page, AIP’s executive director, said the organization is focused on bringing in talent with expertise in emerging technologies as lawmakers make decisions that will shape the U.S. role in AI, crypto and other sectors.

AIP was founded in August 2025 as a digital assets advocacy organization backed by crypto venture capital firm Digital Currency Group and the Cedar Innovation Foundation, a group whose funders are anonymous. Other supporters include Coinbase, Kraken, Andreessen Horowitz, the National Cryptocurrency Association, Paradigm, the Solana Policy Institute, Stand With Crypto and Uniswap Labs, according to the organization.

Quick Overview

- Walt Disney is set to unveil Q2 2026 financial results on Wednesday morning, May 6, with Wall Street projecting roughly $25 billion in revenue and earnings per share of $1.49

- The spotlight falls on streaming unit profitability — Disney+ and Hulu are working toward a 10% operating margin target by fiscal year-end, with approximately $500M in quarterly profit anticipated

- The Parks and Experiences segment confronts near-term headwinds including reduced international tourism and capital expenditures linked to expansion initiatives

- CEO Josh D’Amaro, who assumed leadership on March 18, prepares for his debut earnings conference call after succeeding Bob Iger

- Wall Street analysts maintain a Strong Buy rating on Disney shares with a consensus price target of $132.09, suggesting roughly 30% appreciation potential from present levels

The House of Mouse approaches Wednesday’s quarterly financial disclosure under fresh leadership, with a streaming operation now generating profits and its theme park empire navigating temporary challenges. Here’s what matters most.

Wall Street’s consensus calls for Disney to deliver Q2 2026 revenue near $25 billion alongside earnings per share of $1.49. Shares currently trade around $101.70, reflecting a 5.6% climb over the trailing 30-day period.

Market expectations point toward year-over-year revenue expansion of approximately 5.2% — matching the growth rate from the previous quarter, though trailing the 7% increase recorded during Q2 2025.

Streaming Profitability Commands Attention

The critical metric investors are monitoring isn’t top-line growth — it’s streaming operating margin. Disney’s direct-to-consumer platforms Disney+ and Hulu have established a 10% operating profit margin objective for fiscal year-end, making Wednesday’s figures a crucial progress indicator.

The Street anticipates the streaming segment will generate approximately $500 million in operating income this quarter. Should that materialize, it would represent roughly $200 million in year-over-year improvement.

This trajectory carries significance. Disney invested heavily in building its streaming infrastructure for years while absorbing substantial losses, and financial markets now demand evidence that these investments yield sustainable, recurring returns.

Theme Park Division Encounters Headwinds

The Experiences business unit — Disney’s most profitable segment — faces near-term obstacles. Analysts anticipate softer international visitor counts at U.S.-based parks combined with elevated expenses tied to development initiatives.

A particular pressure point: the forthcoming Disney Adventure cruise ship launch, which accelerates capital spending and compresses margins in the current period.

Despite these challenges, the parks division still generates nearly 68% of total operating earnings. Disney continues investing in new attractions including Toy Story and The Mandalorian-themed areas, and stakeholders await updates on whether these capital deployments are driving guest traffic.

Disney has fallen short of Wall Street’s revenue projections multiple times across the past 24 months. The broader consumer discretionary sector has demonstrated strength recently, with comparable stocks advancing 4.4% on average. Companies like Rush Street Interactive and Monarch exceeded estimates and posted double-digit gains following their reports.

New CEO Faces Inaugural Earnings Presentation

Wednesday also marks Josh D’Amaro’s first quarterly earnings discussion as Chief Executive Officer. He formally assumed the top position on March 18 following Bob Iger’s exit.

D’Amaro’s initial actions have encompassed workforce reduction of approximately 1,000 positions — roughly 1% of total headcount — alongside authorization of a $7 billion stock repurchase program.

The buyback initiative sends an unmistakable message to market participants that leadership views current share valuations as attractive.

Wall Street sentiment supports this perspective. Disney maintains a Strong Buy consensus rating derived from 11 Buy recommendations and one Hold rating. The mean 12-month price objective stands at $132.09, representing approximately 30% upside from today’s trading levels. Near-term focused analysts project a more conservative target of $128.25.

Disney releases results prior to Wednesday’s opening bell on May 6, 2026.

Miami Beach, FL — A growing group of Wall Street and crypto executives say the financial system is heading toward a breaking point, as markets shift from human-paced processes to machine-driven activity that runs around the clock.

“We’re moving to a world where transactions happen at a speed no human can track,” Sandy Kaul, head of digital assets and innovation at Franklin Templeton, said during a panel on the future of capital markets at Consensus in Miami on Tuesday. At the same time, “almost every process in capital markets today was built for humans, and none of them will stand up to what’s coming,” she added.

The tension between those two ideas — faster, automated markets and legacy systems designed for manual oversight — sat at the center of the conversation.

For decades, financial markets have relied on layered processes to handle trades. Systems batch transactions, reconcile records and settle trades hours or even days later. That structure dates back to a time when physical stock certificates moved across Wall Street by hand.

Now, blockchain infrastructure is starting to remove those constraints. Panelists pointed to tokenization — the process of turning assets like stocks or money market funds into digital tokens — as a key shift. These tokens can move instantly, settle in seconds and operate continuously.

“We are unwinding a system that’s been in place for 50 years and going back to settling one transaction at a time,” Kaul said, describing how real-time settlement could replace today’s batch-based model.

That shift has practical implications. In a tokenized system, an investor’s cash could remain fully invested until the exact moment it is spent. “Every penny of my earnings is fully invested from the moment I earn it to the moment that I spend it,” Christine Moy, partner at Apollo, said, outlining a future where idle cash largely disappears.

The same logic applies to large corporations. Instead of holding cash across multiple accounts worldwide, companies could pool funds into yield-generating assets and convert them only when payments are due.

Still, major hurdles remain. While blockchain networks can already process transactions quickly, some panelists argued that the industry lacks the rules and standards needed for institutions to operate at scale.

“We’ve solved the transaction problem. What’s missing is a standard for governance,” said Tom Zschach, former chief innovation officer at Swift, pointing to the need for clear rules around ownership, compliance and permissions.

That gap matters for large financial firms, where reliability often outweighs speed. “If there’s a chance it might not work, it’s a non-starter. What institutions need is certainty,” he said.

At the same time, competitive pressure is rising. As newer platforms offer faster and more flexible financial services, traditional firms risk losing clients if they fail to adapt.

Taken together, the discussion suggests the next phase of market evolution will not just be about faster trades. It will center on rebuilding the underlying systems so they can support continuous, automated flows of capital—without breaking the trust that global finance depends on.

Antoine Semenyo: Everton fan arrested for alleged racist abuse towards Manchester City forward in Premier League fixture at Hill Dickinson Stadium

Strait of Hormuz tensions rise as Iran accused of ceasefire violations

Bitcoin Price Prediction Faces Strategy Earnings Pause While Whales Buy 270,000 BTC and Pepeto Presale Goes Viral, Here Is What You Need To Know

Manchester United reach agreement with Casemiro over contract clause amid transfer speculation

US brings back mandatory military draft registration

Steven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Business7 days ago

Business7 days agoMost Commercial Energy Audits Miss the Real Losses

-

NewsBeat2 days ago

NewsBeat2 days agoChannel 5 – All Creatures Great and Small series 7 new post

-

Fashion7 days ago

Fashion7 days agoKylie Jenner’s KHY Enters a New Era with ‘Born in LA’

-

Tech4 days ago

Tech4 days agoTrump’s 25% EU auto tariff breaches Turnberry Agreement that also covers semiconductors and digital trade

-

Sports4 days ago

Sports4 days agoPaul Scholes issues Marcus Rashford reality check as agreement emerges over Man United star

-

Business6 days ago

Business6 days agoBarclay Brothers Avoid Bankruptcy: HSBC Drops High Court Petitions After IVA Deal

-

Business6 days ago

Business6 days agoTesla Officially Registers Elon Musk’s Stock: What Investors Need to Know

-

Tech6 days ago

Tech6 days agoTexas Instruments made a new flagship graphing calculator: the TI-84 Evo

-

Business5 days ago

Business5 days agoTwo Powerball Tickets Split $143 Million Jackpot in Indiana and Kansas

-

Entertainment5 days ago

Entertainment5 days agoCelebrities Who Are Attending the 2026 Met Gala Event

-

Business2 days ago

Winning Numbers Drawn as Jackpot Resets to $20 Million

-

Crypto World6 days ago

Crypto World6 days agoSecuritize and Computershare Enable Tokenized Equity Issuance for Over 25,000 U.S.-Listed Stocks

-

Entertainment6 days ago

Entertainment6 days agoInsider Claims Reason Behind Key & Peele Split

-

Crypto World5 days ago

Crypto World5 days agoCoreWeave (CRWV) Stock Climbs 8% Despite $45M Insider Share Dump

-

Entertainment4 days ago

Entertainment4 days agoMet Gala 2026 Rumored Guest List Is Turning Heads

-

Crypto World6 days ago

Crypto World6 days agoMeta (META) starts stablecoin payout to creators in Circle’s USDC on Polygon, Solana via Stripe

-

Crypto World6 days ago

Crypto World6 days agoGibraltar Proposes Tokenized Funds Regulation to Bolster Compliance

-

Business7 days ago

Business7 days agoAlexandria Real Estate Equities, Inc. (ARE) Q1 2026 Earnings Call Transcript

-

Fashion3 days ago

Fashion3 days agoMary J. Blige Vegas Residency Looks: Crystal-Embellished Fjolla Haxhismajli, Todd Fisher, and More!

-

Business6 days ago

Business6 days agoStrait of Hormuz Remains Heavily Restricted on April 29 Amid Iran Conflict

You must be logged in to post a comment Login