Crypto World

Article explains Vitalik’s ETH plan to cut proving costs via binary state tree and RISC-V VM.

ETH tackles 80% proving bottleneck as Vitalik proposes binary state tree and long-term RISC-V VM swap.

Summary

- EIP-7864 replaces the hexary keccak Merkle Patricia Tree with a unified binary state tree using BLAKE3 (or a future Poseidon2), cutting Merkle proof size by about 75% and branches by 3–4x.

- Page-based storage groups 64–256 adjacent slots so early-slot dapps can save over 10k gas per transaction, while simpler, more uniform depth improves auditing and sets up future state expiry.

- Long-term, Vitalik proposes replacing the EVM with a RISC-V VM, arguing state tree plus VM drive over 80% of proving cost and that a RISC-V stack would align with existing ZK provers, reduce precompiles, and keep old contracts via staged migration.

Ethereum (ETH) co-founder Vitalik Buterin has proposed two technical changes aimed at addressing proof-efficiency challenges in the blockchain network, according to a proposal outlined in EIP-7864 and related documentation.

The near-term proposal, designated as EIP-7864, would replace Ethereum’s current hexary keccak Merkle Patricia Tree with a binary tree structure utilizing a more efficient hash function. The existing hexary structure was designed for priorities that differ from the proving-heavy architecture Ethereum developers are currently pursuing, according to the proposal.

The binary tree structure would produce Merkle branches that are four times shorter than the current system, as binary operations require 32 times log(n) compared to hexary’s 512 times log(n) divided by 4, according to technical specifications in the proposal.

The reduction would decrease costs for client-side branch verification and reduce data bandwidth requirements for tools including Helios and private information retrieval systems by the same factor, the proposal states.

Proving efficiency gains would extend beyond branch length improvements. The proposal indicates that shorter branches would deliver a three to four times improvement, separate from hash function optimization. Implementing blake3 instead of keccak could provide an additional three times improvement, while a Poseidon variant could potentially deliver 100 times improvement, though additional security analysis is required before Poseidon deployment, according to the document.

The binary tree design includes a page-based storage system that groups adjacent storage slots into pages of 64 to 256 slots, approximately 2 to 8 kilobytes. The block header and the first 1 to 4 kilobytes of code and storage would share the same page, allowing contracts that read from initial storage slots to benefit from batch efficiency rather than individual access costs. The proposal estimates this could save more than 10,000 gas per transaction for decentralized applications that load data from initial storage slots, which represents a substantial portion of active deployed contracts.

Binary trees offer simpler implementation and auditing processes, according to the proposal. The structure provides more predictable access depth across contracts of varying sizes, reducing variance in execution costs, and creates space for embedding metadata required for future state expiry development.

The longer-term proposal involves replacing the Ethereum Virtual Machine with a more efficient virtual machine such as RISC-V. The proposal argues that the EVM’s architecture is not optimized for a proving-heavy blockchain and that replacing it would address fundamental inefficiencies rather than managing them through accumulated precompiles and workarounds.

Buterin’s proposal cites four advantages of RISC-V over the EVM. First, raw execution efficiency: RISC-V outperforms the EVM to a degree that would eliminate the need for many precompiles, as underlying computations could run efficiently within the VM itself. Second, prover efficiency: zero-knowledge provers are currently written in RISC-V, creating natural alignment with existing proving infrastructure. Third, client-side proving: a RISC-V VM would enable users to generate zero-knowledge proofs locally about account interactions with specific data, enabling privacy and verification applications not currently supported by the EVM without external tools. Fourth, simplicity: a RISC-V interpreter can be implemented in several hundred lines of code, according to the proposal.

The deployment roadmap outlined in the proposal includes three stages. In the first stage, a new virtual machine, potentially RISC-V, would handle precompiles only, with current and new precompiles becoming code blobs in the new VM. In the second stage, users could deploy contracts directly in the new VM. In the third stage, the EVM would be retired and reimplemented as a smart contract written in the new VM, preserving backwards compatibility for existing contracts with the primary change being gas cost adjustments, which are expected to be overshadowed by concurrent scaling developments.

Buterin characterizes both changes as addressing the same fundamental challenge from different angles. The state tree and the VM together account for more than 80 percent of the bottleneck in efficient proving, according to the proposal. Addressing either component without the other leaves the larger problem partially unresolved, while addressing both would produce a protocol structurally aligned with the zero-knowledge-proof-heavy architecture Ethereum has been developing, rather than retrofitting that architecture onto infrastructure designed for different requirements.

The proposal acknowledges that the VM replacement does not currently represent consensus within the Ethereum development community, describing it as a change that will become more apparent once state tree modifications are completed. The proposal presents the changes as sequential: binary trees first, followed by VM replacement once proving infrastructure matures around the new state structure. The EVM has accumulated complexity through years of incremental additions, and the proposal states that meeting Ethereum’s functionality requirements necessitates addressing the VM rather than continuously implementing workarounds.

Si vous cherchez un site de pari sportif fiable et sécurisé, vous êtes au bon endroit. Dans cet article, nous allons vous présenter les avantages de l’application Melbet APK Maroc et les mesures de sécurité mises en place pour protéger vos informations personnelles.

Télécharger Melbet est un choix populaire parmi les fans de sport et les passionnés de jeu. Cependant, il est important de choisir une version APK fiable et sécurisée pour éviter les problèmes de sécurité. Dans ce contexte, l’application Melbet APK Maroc est une excellente option.

La sécurité est un des principaux objectifs de Melbet. L’application utilise des protocoles de sécurité de pointe pour protéger vos informations personnelles et vos transactions. De plus, Melbet dispose d’une équipe de sécurité expérimentée qui travaille en permanence pour détecter et prévenir les menaces potentielles.

En téléchargeant Melbet APK Maroc, vous bénéficiez d’une expérience de jeu sécurisée et fiable. L’application est disponible pour téléchargement sur le site officiel de Melbet et peut être installée sur votre appareil mobile ou ordinateur.

En résumé, l’application Melbet melbet app APK Maroc est une excellente option pour les fans de sport et les passionnés de jeu qui cherchent une expérience de jeu sécurisée et fiable. Avec ses mesures de sécurité mises en place et son équipe de sécurité expérimentée, Melbet est un choix sûr pour vos paris sportifs.

Il est important de noter que la sécurité est un effort continu et que Melbet travaille en permanence pour améliorer ses mesures de sécurité.

Melbet APK Maroc est disponible pour téléchargement sur le site officiel de Melbet.

Melbet APK Maroc : Sécurité et protection des utilisateurs

Pour garantir une expérience de jeu sécurisée et protégée, il est essentiel de télécharger l’application Melbet APK Maroc. Cette application offre une variété de fonctionnalités pour protéger vos informations personnelles et votre argent.

En téléchargeant l’application Melbet APK Maroc, vous pouvez être sûr que vos données sont cryptées et protégées par des mesures de sécurité robustes. De plus, l’application offre une fonction de verrouillage pour empêcher les accès non autorisés à votre compte.

Il est également important de noter que l’application Melbet APK Maroc est régulièrement mise à jour pour garantir la sécurité et la stabilité de l’application. Cela signifie que vous pouvez être sûr que vous bénéficiez de la dernière version de l’application, avec les meilleures fonctionnalités de sécurité et de protection.

En outre, l’application Melbet APK Maroc offre une fonction de réinitialisation de mot de passe pour vous aider à récupérer votre compte en cas de problème. Cela signifie que vous pouvez être sûr de récupérer votre compte rapidement et facilement, sans avoir à vous soucier de la sécurité de vos informations.

En résumé, télécharger l’application Melbet APK Maroc est la meilleure façon de garantir une expérience de jeu sécurisée et protégée. Avec ses fonctionnalités de sécurité et de protection, vous pouvez être sûr de jouer en toute sécurité et de protéger vos informations personnelles.

Il est donc recommandé de télécharger l’application Melbet APK Maroc pour bénéficier de ces fonctionnalités de sécurité et de protection. Vous pouvez télécharger l’application en cliquant sur le lien suivant : [télécharger l’application Melbet APK Maroc](https://www.melbet.com/maroc/download).

En résumé, l’application Melbet APK Maroc est la meilleure façon de garantir une expérience de jeu sécurisée et protégée. Avec ses fonctionnalités de sécurité et de protection, vous pouvez être sûr de jouer en toute sécurité et de protéger vos informations personnelles.

La nécessité d’une application sécurisé

Il est essentiel de disposer d’une application sécurisée pour protéger vos informations personnelles et vos transactions en ligne. La mélbet app est une application sécurisée qui garantit la confidentialité de vos informations et la protection de vos transactions.

En téléchargeant la mélbet app, vous pouvez être sûr que vos informations sont protégées et que vos transactions sont sécurisées. La mélbet app utilise des méthodes de cryptage avancées pour protéger vos informations et vos transactions.

Il est important de noter que la mélbet app est disponible pour téléchargement sur les appareils mobiles et les ordinateurs de bureau. Vous pouvez télécharger la mélbet app sur votre appareil mobile ou votre ordinateur de bureau pour accéder à vos informations et vos transactions en ligne.

En utilisant la mélbet app, vous pouvez être sûr que vos informations sont protégées et que vos transactions sont sécurisées. La mélbet app est une application sécurisée qui garantit la confidentialité de vos informations et la protection de vos transactions.

Il est important de noter que la mélbet app est disponible en plusieurs langues, y compris le français. Vous pouvez télécharger la mélbet app sur votre appareil mobile ou votre ordinateur de bureau pour accéder à vos informations et vos transactions en ligne.

En résumé, la mélbet app est une application sécurisée qui garantit la confidentialité de vos informations et la protection de vos transactions. Il est essentiel de disposer d’une application sécurisée pour protéger vos informations personnelles et vos transactions en ligne.

A Blue Origin New Glenn rocket carrying an AST SpaceMobile Bluebird 7 satellite launches from pad 36 at Cape Canaveral Space Force Station on April 19, 2026 in Cape Canaveral, Florida.

Paul Hennesy | Anadolu | Getty Images

A failed satellite launch sent of AST SpaceMobile down sharply on Monday.

The stock fell nearly 12% in premarket trading after a rocket designed by Jeff Bezos’ space technology company Blue Origin placed the satellite in a lower-than-planned orbit on Sunday.

AST SpaceMobile’s BlueBird 7 satellite would have been the company’s eighth launched into low-earth orbit, the company said in a Sunday press release. It was launched on Blue Origin’s third New Glenn rocket.

Blue Origin acknowledged in a post on X that the satellite was placed into the wrong orbit, but only added it was assessing the situation and would provide further updates. The company hasn’t made a statement since the satellite was officially deemed lost.

The cost of the satellite loss is expected to be covered by an insurance policy, AST said in the release. It also still expects to launch a satellite on average once every one to two months in 2026, and said BlueBird satellites 8, 9 and 10 should be ready to ship in 30 days.

ASTS year-to-date chart.

William Blair analyst Louie DiPalma thinks that AST’s goal of 45 satellites in orbit by year-end will likely be hard to hit now. However, he didn’t see Sunday’s events as a total loss for the company.

“AST gained experience integrating its satellite with New Glenn and working with the Blue Origin team,” DiPalma wrote in a Monday note. “This experience will be integral for future missions. The silver lining is that there was only one satellite on board, whereas future New Glenn launches may have as many as eight of AST’s BlueBirds.”

While Clear Street analyst Greg Pendy was still bullish on the stock, reiterating a buy rating after the news, he cut his price target to $115 from $137. That’s still a 34% gain from Friday’s close, but much less than his previously forecasted 60% jump in shares.

UBS analyst Christopher Schoell said in a note the financial impact on AST will be limited, but added that AST and its share price performance are now linked with Bezos’ Blue Origin.

“We believe the success of Blue Origin’s New Glenn vehicle … is key to meeting year-end deployment targets/ management’s 2027 revenue goal, and expect the uncertainty to weigh on investor sentiment initially pending greater clarity,” Schoell wrote.

Markets shift and headlines fade, but the core principles of building long-term wealth remain constant. Join us for our third CNBC Pro LIVE, where investors of all backgrounds – from financial professionals to everyday individuals – come together to cut through the noise and gain actionable strategies for smarter, more disciplined investing. No matter where you’re starting from, you’ll leave with clearer thinking, stronger strategies. Enter your email here to get a discount code

Key Takeaways

- Fermi (FRMI) shares plummeted 20% to $5.27 during premarket hours Monday following executive departures

- CEO Toby Neugebauer resigned; CFO Miles Everson simultaneously exited his role

- Board members had been evaluating potential CEO replacement for a minimum of three months

- Company unveiled “Fermi 2.0” initiative, representing a comprehensive overhaul of governance and strategy

- Evercore analysts reaffirmed Outperform rating with $20 price target for FRMI

Shares of Fermi (FRMI) tumbled 20% on Monday following the data-center company’s announcement that both its chief executive and chief financial officer would be exiting, prompting a comprehensive leadership transformation the firm has branded “Fermi 2.0.”

Co-founder and CEO Toby Neugebauer, who established the company with former Texas Governor and U.S. Energy Secretary Rick Perry, resigned with immediate effect. Neugebauer will continue serving as a board member.

According to reports, the board had been deliberating a potential CEO replacement for no less than three months. Several sell-side analysts verified this timeline after participating in a management conference call that followed the public disclosure.

CFO Miles Everson similarly departed from his executive position. Following his resignation, Everson was appointed to the board after a trust controlled by the Neugebauer family executed its board nomination privileges.

The board has initiated an active search for Neugebauer’s successor. Leadership recruitment firm Heidrick & Struggles has been retained, with a committee composed of independent board members overseeing the selection process.

Fermi has additionally established an Office of the CEO to maintain business continuity throughout the transition period. Jacobo Ortiz Blanes, the former COO, and Anna Bofa, previously serving as a Board Advisor, have been promoted to Co-Presidents and will answer to newly designated Chairman Marius Haas.

Haas, who formerly held the position of Lead Independent Board Director, assumed the role of Executive Chairman immediately.

Jeffrey S. Stein, co-founder of Breakpoint Advisory Partners, joined the board as a new member, increasing the board size from five to seven seats.

Executive Transition Linked to Tenant Acquisition Struggles

The management upheaval arrives as Fermi has encountered difficulties securing a major anchor tenant for its Project Matador development in Amarillo, Texas. The massive 7,570-acre property is designed to become the world’s largest data center facility.

Company officials emphasized that the transition would not impair its capacity to deliver electrical infrastructure or execute tenant agreements. Management noted that prospective lease negotiations had actually intensified, with potential clients resuming engagement within 48 hours following the announcement.

Evercore analyst Nicholas Amicucci characterized the transformation as a shift in leadership philosophy while maintaining operational momentum. Evercore maintained its Outperform rating and $20 price target on the stock.

FRMI shares had already declined 18% year-to-date before Monday’s trading session, with the premarket selloff driving the price down to $5.27.

Corporate Headquarters Relocation and Expansion Strategy

As a component of the Fermi 2.0 initiative, company leadership revealed plans to relocate corporate headquarters to Dallas. Additionally, Fermi intends to develop a dedicated corporate office facility at the Project Matador location in Amarillo.

Management stated these strategic moves represent the company’s evolution from startup phase to large-scale enterprise operations.

Texas Tech University System Chancellor Brandon Creighton reaffirmed the university’s ongoing commitment to its collaboration with Fermi America. Negotiations continue regarding potential extensions to certain milestone deadlines contained in the lease agreement as Project Matador progresses.

The company indicated it would name an Interim CFO within the current week.

Cryptocurrency investment products logged another week of strong inflows on ceasefire optimism and a Bitcoin price breakout driving investor sentiment.

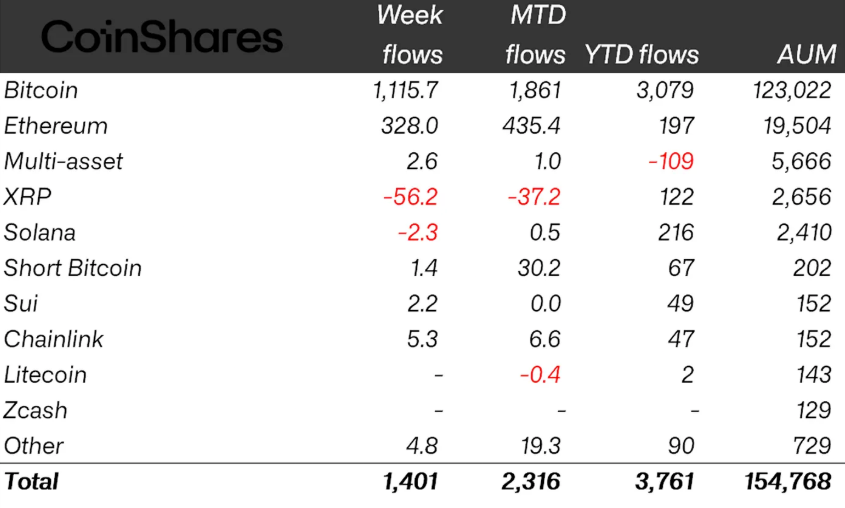

Crypto exchange-traded products (ETPs) posted $1.4 billion in inflows last week, beating the prior week’s $1.1 billion and marking the second-largest weekly inflows since January, CoinShares reported on Monday.

Following the three-week inflow streak totaling $2.7 billion, crypto ETPs now have net year-to-date inflows of around $3.8 billion, with assets under management (AUM) at $154.8 billion — the highest level since early February after dipping to as low as $128 billion in March.

The uptick in crypto funds has likely been driven by a recovery in risk appetite on US-Iran ceasefire extension talks, CoinShares head of research James Butterfill said.

The sentiment was further reinforced by Bitcoin (BTC) nearly touching $78,000 on Friday, according to CoinGecko.

Ether funds turn positive year to date

Bitcoin led last week’s ETP gains by a significant margin, with inflows totaling $1.12 billion. The gains brought year-to-date inflows to $3 billion, with AUM at $123 billion.

The majority of gains were contributed by US spot Bitcoin exchange-traded funds (ETFs), which posted $1 billion in inflows last week.

Ether (ETH) investment products also picked up with $328 million inflows in its strongest week since January, finally lifting the ETPs into green year-to-date with $197 million inflows.

Still, altcoin ETPs, including XRP (XRP) and Solana (SOL), recorded negative flows, with XRP leading the outflows at $56 million. Solana recorded minor outflows of $2.3 million.

Short-Bitcoin products saw a modest $1.4 million of inflows, suggesting residual but limited hedging demand.

Regionally, the US dominated the surge with $1.5 billion of inflows, while Germany ranked second with just $28 million of inflows. Switzerland saw the largest redemptions last week, with outflows totaling $138 million.

Addressing the implications of recent economic data, CoinShares’ Butterfill suggested that March’s Consumer Price Index (CPI) increase of 3.3% appears to have been largely looked through by markets, with core CPI at 2.6% seen as relatively contained, pointing to inflation pressures that remain more supply-driven than broad-based.

Related: Bitcoin erases weekend gains as US-Iran ceasefire faces pressure

Nomura’s Laser Digital echoed that view, telling Cointelegraph that backward-looking macro indicators currently offer only limited insight while conflicts continue to affect supply chains and spending patterns.

“Delayed indicators like CPI and PMIs mostly reflect past conditions rather than the current situation,” Laser Digital said, adding that the outlook remains “cautiously optimistic.”

Sentiment improvement was also reflected in the Crypto Fear & Greed Index, which moved from “extreme fear” to “fear,” with the score rising above 29 on Monday for the first time since Jan. 29.

Magazine: Bitcoin ‘on track’ for $90K, ETFs pull in nearly $1B: Hodler’s Digest, April 12 – 18

Si vous cherchez un moyen sûr et fiable de télécharger l’application Melbet, vous êtes au bon endroit. Dans cet article, nous allons vous présenter les avantages de l’application Melbet APK Maroc et les moyens de la télécharger de manière sécurisée.

La sécurité est un sujet très important pour les utilisateurs de l’application Melbet. C’est pourquoi nous allons vous donner quelques conseils pour télécharger l’application de manière sécurisée.

La première chose à faire est de télécharger l’application Melbet APK Maroc à partir d’un site web fiable. Il est important de vérifier que le site web est sécurisé et que l’application est téléchargée de manière sécurisée.

Ensuite, il est important de vérifier les permissions demandées par l’application. Vous devez vous assurer que l’application ne demande pas plus de permissions que nécessaire pour fonctionner correctement.

Enfin, il est important de surveiller vos transactions et de vérifier vos comptes régulièrement pour vous assurer que tout est en ordre.

En résumé, la sécurité est un sujet très important pour les utilisateurs de l’application Melbet. Il est important de télécharger l’application de manière sécurisée, de vérifier les permissions demandées et de surveiller vos transactions pour vous assurer que tout est en ordre.

Comment télécharger l’application Melbet APK Maroc ?

Pour télécharger l’application Melbet APK Maroc, vous pouvez suivre les étapes suivantes :

1. Ouvrez votre navigateur web et allez sur le site web de téléchargement de l’application Melbet.

2. Cliquez sur le bouton “Télécharger” pour télécharger l’application.

3. Une fois le téléchargement terminé, installez l’application sur votre appareil.

4. L’application est maintenant prête à être utilisée.

Il est important de noter que l’application Melbet APK Maroc est disponible uniquement pour les utilisateurs résidant dans le Maroc.

Conclusion télécharger melbet

En résumé, l’application Melbet APK Maroc est une application de jeu en ligne qui offre une expérience de jeu sécurisée et fiable. Pour télécharger l’application, vous pouvez suivre les étapes précédemment mentionnées. Il est important de noter que l’application est disponible uniquement pour les utilisateurs résidant dans le Maroc.

Melbet APK Maroc : Sécurité et protection des utilisateurs

Il est essentiel de garantir la sécurité et la protection des utilisateurs lors de la téléchargement et de l’utilisation de l’application Melbet APK Maroc. Pour cela, il est recommandé de télécharger l’application directement de la page officielle de Melbet, plutôt que de la télécharger à partir de sources non officielles.

En téléchargeant l’application Melbet APK Maroc, vous pouvez être sûr que vous obtiendrez une version sécurisée et vérifiée de l’application. De plus, vous pourrez bénéficier d’une protection renforcée contre les virus et les malwares, ce qui vous permettra de vous concentrer sur votre jeu et non sur la sécurité de votre appareil.

Comment télécharger l’application Melbet APK Maroc de manière sécurisée

Pour télécharger l’application Melbet APK Maroc de manière sécurisée, suivez les étapes suivantes :

1. Allez sur le site web officiel de Melbet et cliquez sur le bouton “Télécharger” pour télécharger l’application.

2. Assurez-vous de télécharger l’application directement de la page officielle de Melbet, plutôt que de la télécharger à partir de sources non officielles.

3. Une fois l’application téléchargée, assurez-vous de la vérifier et de la scanner pour détecter les virus et les malwares.

En suivant ces étapes, vous pourrez être sûr de télécharger l’application Melbet APK Maroc de manière sécurisée et de bénéficier d’une protection renforcée contre les virus et les malwares.

Il est important de noter que la sécurité est une priorité pour Melbet, et que l’application est conçue pour offrir une expérience de jeu sécurisée et amusante.

La nécessité d’une application sécurisée

Il est essentiel de télécharger l’application Melbet pour garantir une expérience de jeu sécurisée et protégée. En effet, la sécurité est un aspect crucial pour les joueurs, car elle garantit la confidentialité de leurs informations personnelles et financières.

En téléchargeant l’application Melbet, vous pouvez être sûr de bénéficier d’une protection renforcée contre les cybermenaces. L’application est conçue pour offrir une expérience de jeu sécurisée et protégée, avec des mesures de sécurité robustes pour protéger vos données.

- La sécurité est un aspect essentiel pour les joueurs, car elle garantit la confidentialité de leurs informations personnelles et financières.

- L’application Melbet est conçue pour offrir une expérience de jeu sécurisée et protégée, avec des mesures de sécurité robustes pour protéger vos données.

- En téléchargeant l’application Melbet, vous pouvez être sûr de bénéficier d’une protection renforcée contre les cybermenaces.

Il est important de noter que la sécurité est un aspect essentiel pour les joueurs, car elle garantit la confidentialité de leurs informations personnelles et financières. En téléchargeant l’application Melbet, vous pouvez être sûr de bénéficier d’une protection renforcée contre les cybermenaces.

En résumé, la sécurité est un aspect essentiel pour les joueurs, car elle garantit la confidentialité de leurs informations personnelles et financières. En téléchargeant l’application Melbet, vous pouvez être sûr de bénéficier d’une protection renforcée contre les cybermenaces.

Il est donc essentiel de télécharger l’application Melbet pour garantir une expérience de jeu sécurisée et protégée. En téléchargeant l’application Melbet, vous pouvez être sûr de bénéficier d’une protection renforcée contre les cybermenaces.

The landscape of the Middle East and North Africa changed dramatically when the United States and Israel joined forces and attacked Iran. The whole world then became involved in the conflict. Some tried to be a mediator and tell both sides to calm down. Others chose sides and expressed their support or disapproval.

While countries try to figure out issues associated with oil prices, sanctions, migration, and the threat of nuclear war, ordinary people (the most vulnerable members of any society) are just trying to live their best lives. Some entrepreneurial spirits have even bet on the end of the war on Polymarkets.

These are tough times for the region, but some nations have been tougher for over 8,000 years, and this column will offer a different perspective on the conflict and explore some of the potential scenarios, as well as the role of crypto in the region.

Three Scenarios, One Certainty

Before we get to the money, let’s be honest about the map. We’ve been tracking this conflict closely, and the trajectories that matter most aren’t the dramatic ones, they’re the structural ones.

As we discussed in “From Oil to On-Chain: The Evolution of Technology, Crypto, and RWA Tokenization in the MENA Region,” we outlined three possible scenarios.

The most realistic path is a War of Attrition: the conflict simply grinds on. The US and Israel continue degrading Iran’s military and nuclear infrastructure; Tehran, battered but not broken, keeps firing back with missile barrages, drone swarms, and tanker harassment. Oil stays above $100 not as a spike but as a floor. Diplomatic channels don’t collapse, but they don’t function either. Nobody wins and nobody stops, many countries around the world suffer.

The darker version is Systematic Collapse (and it doesn’t require malice) just one miscalculation. A single strike on civilians, and Iran stops calibrating its response and uses everything at its disposal. The Strait of Hormuz goes from “threatened” to “closed,” cutting off roughly 20% of the world’s oil supply and triggering an energy crisis that hits China, India, Japan, and Europe hardest.

The least likely but not impossible path is a Fragile Pause. Washington is bleeding political casualties, no endgame, Congress demanding answers. Tehran is absorbing infrastructure damage that the state can no longer sustain. What follows is not peace, but a frozen conflict. No bombing, but no reconstruction either. Both sides rearm. It’s the least bad version of all possible outcomes, which makes it grim to call optimistic.

One truth runs through all three: wars end either when participants get what they want, or when the cost in lives exceeds what anyone is willing to justify. We haven’t reached that line yet.

But while diplomats negotiate, businesses still need to move money.

The “New Normal”: Navigating the Fog of War

In the wake of the strikes, a strange “new normal” has emerged. While most Arab nations have issued stern condemnations of the escalation, life in the regional hubs remains a study in calculated calm.

In the UAE, resilience trumps panic. Students go back to school at the end of March, and the digital economy continues to hum despite the erratic swings in oil prices and frequent market-moving tweets from the White House, backed by decentralized cloud infrastructure.

However, the war has left its mark on the physical world. The crypto community felt the sting of reality with the postponement of TOKEN2049 Dubai, as organizers moved the event to 2027 citing safety and logistics. Some of the international events have been called off for safety reasons. For many firms, physical operations have hit “pause,” shifting entirely into the digital ether.

But infrastructure doesn’t cancel. And that distinction matters enormously.

Saudi Arabia moved with uncharacteristic bureaucratic speed. To stabilize trade routes, the Kingdom’s Transport General Authority (TGA) recently suspended all documentation requirements for marine vessels for 30 days. It’s a pragmatic admission that in 2026, the flow of goods is more important than the flow of paperwork.

Meanwhile, Israeli news portals hint at a growing, if silent, alignment between the UAE, Saudi Arabia, and the West against Tehran, the region finds itself at a crossroads. This isn’t just a military conflict; it is a stress test for the future of decentralized finance and regional unity.

On the other hand, the media and the government of Turkey and Qatar are actively promoting the idea of mutual peace and cease the fires from both sides.

The Digital Bridge: Stablecoins as a War-Time Necessity

The Middle East Council on Global Affairs recently published a framework for navigating this “New Normal,” warning GCC states against falling into a “strategic trap” between competing alliances. Their recommendation is a sophisticated form of differentiated hedging: maintaining diplomatic channels with all sides while building a security architecture capable of standing without external life support.

In the streets of Dubai and the boardrooms of Riyadh, this “Strategic Autonomy” is being built not just with hardware, but with code. If the 20th century was defined by the petrodollar and Western security guarantees, 2026 is becoming the era of Digital and Financial Neutrality.

For the regional business community, being “diplomatic with both sides” means using financial tools that don’t take sides. This is why we are seeing a massive surge in On-Chain Settlement. When traditional banking rails become entangled in the sanctions and counter-sanctions of the US-Israel-Iran triangle, crypto provides the “exit ramp.”

While in more stable regions (Europe or South East Asia) crypto is still largely treated as a speculative asset or an innovation layer. In MENA, it is rapidly evolving into something far more practical: a mechanism for continuity.

For many, crypto has become the “last-mile” solution. When traditional credit lines are frozen due to force majeure, a stablecoin transfer settled in seconds on-chain allows a merchant to secure a cargo flight or a rerouted shipment through Saudi Arabia’s newly deregulated maritime routes.

By betting on ceasefire odds, local businesses are essentially hedging their real-world losses. If the war continues, their “win” on-chain helps offset the rising cost of fuel and disrupted trade.

By 2026, the blockchain will evolve beyond a mere ledger, becoming the region’s de facto emergency reserve.

RWA: When “Infrastructure” Becomes Urgent

This isn’t happening in a vacuum. The shift toward on-chain settlement in MENA mirrors a broader structural transformation already underway in global finance. Institutions like BlackRock, Franklin Templeton, and J.P. Morgan tokenizes real-world assets because of its atomic settlement, programmable yield, and the elimination of intermediary layers are simply better infrastructure. Moving from slow T+2 settlement cycles to near-instant on-chain finality is an operational upgrade that the world’s largest financial institutions have already begun executing.

When correspondent banking freezes under sanctions pressure, that “better infrastructure” stops being theoretical. The multi-trillion dollar RWA market has its most urgent real-world stress test right now, in the trading desks of Dubai and Riyadh.

War doesn’t slow the adoption of better financial plumbing, it accelerates it.

Betting on Dubai: Why We Opened Our Office Here Anyway

There is a particular kind of clarity that only comes from turbulence. And in April 2026, the MENA region is offering plenty of it.

Since the outbreak of the conflict, a cascade of high-profile cancellations has followed: TON Gateway Dubai was called off in mid-March and Formula 1 announced the Bahrain and Saudi Arabian Grands Prix would not take place in April. For many observers abroad, these headlines painted a picture of a region in retreat.

At ChangeNOW, we see something different.

The events may have paused, but the infrastructure has not. The regulatory architecture that Dubai spent years building is still standing, and it is precisely this foundation that we bet on when we opened our new office here. In 2026, VARA licensing represents a comprehensive regulatory commitment with crypto businesses expected to treat licensing, governance, and compliance as core operational pillars from the outset.

That kind of seriousness is exactly what the moment demands. When traditional banking rails become entangled in the sanctions and counter-sanctions of a conflict, businesses don’t flee toward chaos, they flee toward clarity. Dubai offers that clarity. While many countries continue to struggle with unclear crypto laws and regulatory uncertainty, Dubai has taken a confident lead by establishing a dedicated legal framework for virtual assets, and in 2026, it has evolved into a global headquarters hub for Web3 companies, blockchain startups, and digital asset businesses.

This is not a blunt optimism. It is the same calculation that merchants, traders, and builders have been making in this region for six thousand years: that geography, infrastructure, and institutional trust matter more than any single crisis. The Silk Road didn’t stop when empires fell. It rerouted.

We opened our Dubai office because we believe the same rerouting is happening now, but in finance, in settlement infrastructure, in the architecture of trust. Stablecoins are becoming the “last-mile” solution for businesses whose traditional credit lines have been frozen.

On-chain settlement is replacing correspondent banking for merchants navigating a world of sanctions and counter-sanctions. And Dubai, with its zero personal income tax, unified VASP register visible federally across emirates, and a stablecoin framework anchored by the dirham-backed AE Coin, is positioned to be the clearing house for all of it.

And we are not naive about the risks, we understand that the path ahead is not smooth (and anyone claiming otherwise is selling something). But the companies that define MENA’s next decade of digital finance will be the ones who showed up when the calculation was still uncomfortable.

We showed up.

The post When Empires Shake, Code Doesn’t: Crypto, Dubai, and the New Financial Silk Road appeared first on BeInCrypto.

The crypto market will welcome tokens worth more than $723 million in the fourth week of April 2025. Major projects, including LayerZero (ZRO), Undeads Games (UDS), and Humanity (H), will release significant new token supplies.

These unlocks could introduce market volatility and influence short-term price movements. So, here’s a breakdown of what to watch.

1. LayerZero (ZRO)

- Unlock Date: April 20

- Number of Tokens to be Unlocked: 25.71 million ZRO

- Released Supply: 481.38 million ZRO

- Total Supply: 1 billion ZRO

LayerZero is an interoperability protocol that connects different blockchains. Its primary goal is to facilitate seamless cross-chain communication. Thus, it enables decentralized applications (dApps) to interact across multiple blockchains without relying on traditional bridging models.

The team will unlock 25.71 million tokens on April 20, representing 5.34% of the released supply. Moreover, the supply is worth approximately $41.39 million.

LayerZero will award 13.42 million altcoins to strategic partners. Core contributors will get 10.63 million ZRO. Lastly, 1.67 million ZRO are for tokens repurchased by the team.

2. Undeads Games (UDS)

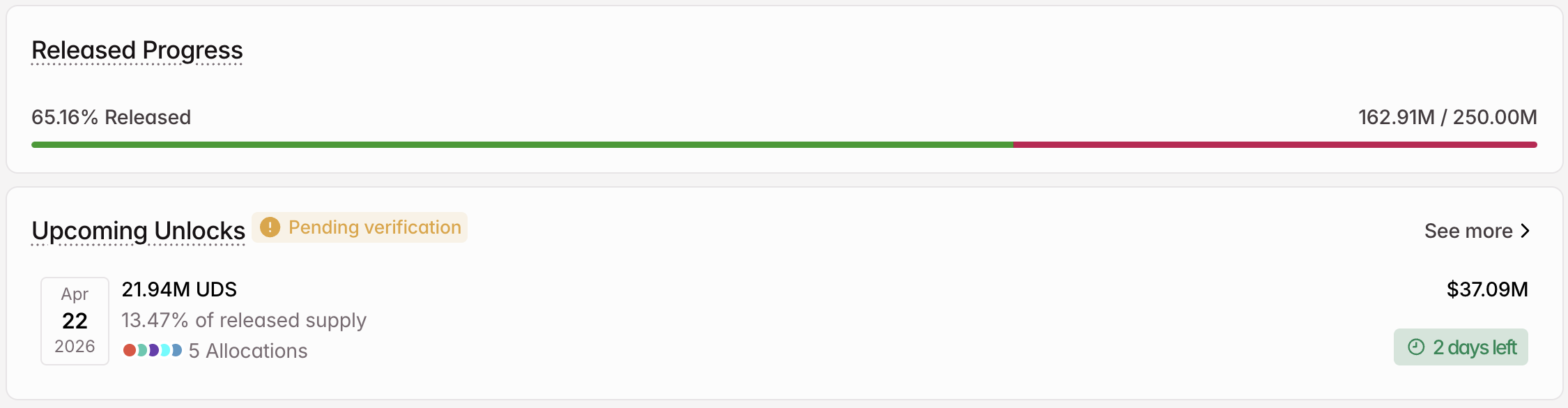

- Unlock Date: April 22

- Number of Tokens to be Unlocked: 21.94 million UDS

- Released Supply: 162.91 million UDS

- Total Supply: 250 million UDS

Undeads Games is a Web3 gaming studio launched in early 2022, building a post-apocalyptic metaverse where humans battle zombies across titles such as Undeads Rush, Viral, and Fighters. UDS is its ERC-20 utility token on Ethereum, powering in-game trading, NFT transactions, staking rewards, and governance

On April 22, Undeads Games will release 21.94 million tokens, valued at $37.09 million. The tokens represent 13.47% of the unlocked supply.

The team fund will receive 9.17 million UDS. Undeads Games will allocate 5.63 million tokens to the seed round and 5 million tokens to airdrop seasons 2-5.

In addition, the ecosystem fund will get 1.74 million tokens. Finally, the marketing fund will gain around 416,670 altcoins.

3. Humanity (H)

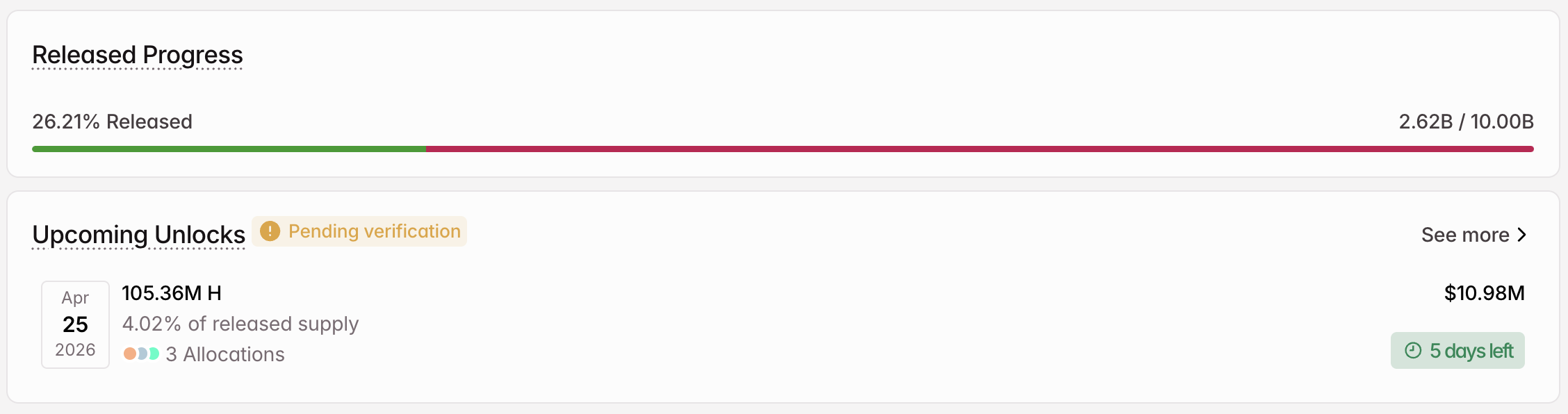

- Unlock Date: April 25

- Number of Tokens to be Unlocked: 105.36 million H

- Released Supply: 2.62 billion H

- Total supply: 10 billion H

Humanity (H) is a decentralized identity protocol that utilizes biometric palm recognition, zero-knowledge proofs, and blockchain to verify the authenticity of real human users without exposing their personal data. It features a native Proof of Humanity (PoH) consensus mechanism.

On April 25, the protocol will unlock 105.36 million tokens. The tokens are worth $10.98 million and also account for 4.02% of the released supply.

The team will split the released supply three ways. The ecosystem fund will receive 50 million H. Furthermore, Humanity will allocate 42.86 million altcoins to identity verification rewards and 12.50 million to the foundation operations treasury.

In addition to these, other prominent unlocks investors can look out for in the fourth week of April include Plasma (XPL), Kaito (KAITO), Soon (SOON), and more, which will contribute to the total market-wide releases.

The post 3 Token Unlocks to Watch in the Fourth Week of April 2026 appeared first on BeInCrypto.

“Passive income” is one of the most seductive phrases in crypto. It suggests a world where capital works harder than you do—where tokens quietly multiply while you sleep, and DeFi protocols function like automated ATMs for financial freedom.

That story sells well. It just doesn’t fully survive contact with reality.

In practice, most so-called passive income strategies in crypto are closer to low-intensity active management than true set-and-forget investing. The difference matters—because misunderstanding it leads to unrealistic expectations, poor risk management, and often, avoidable losses.

The Illusion of “Set It and Forget It”

At the surface level, decentralized finance (DeFi) offers compelling yield opportunities: liquidity provision, staking rewards, lending interest, and incentive programs. Many platforms market these as passive income streams.

But beneath the branding, these systems are dynamic, reactive environments. Yields shift constantly. Risk profiles change overnight. Incentives migrate between protocols like heat-seeking capital.

What looks passive is often just out-of-sight responsibility.

What “Passive” Actually Requires in Crypto

Even the most conservative DeFi strategies demand ongoing attention. Not occasionally—continuously.

1. Monitoring Liquidity Pools

Liquidity providers must track:

- fee generation vs. impermanent loss

- volume fluctuations

- incentive emissions

A pool that looked attractive yesterday can become inefficient today. Ignoring it doesn’t make it passive—it just delays the consequences.

2. Rebalancing Positions

Yield strategies often rely on shifting allocations between protocols or pools.

That means:

- moving capital when APYs change

- adjusting exposure across chains

- optimizing for gas fees vs. returns

In traditional finance, this would simply be called portfolio management. In crypto, it’s rebranded as “earning passively.”

3. Reacting to Depegs

Stablecoins are only “stable” until they aren’t.

When depegging events occur, users are forced into rapid decisions:

- exit liquidity positions

- unwind leveraged exposure

- assess contagion risk across protocols

Nothing passive about panic management.

4. Chasing Yield Migrations

Incentives in DeFi are rarely static. Capital flows toward higher yields, and protocols respond by:

- launching new reward programs

- ending old liquidity incentives

- shifting emissions schedules

Participants who don’t adapt get diluted. Those who do essentially become active yield hunters.

The Branding Problem: “Passive” as Marketing Language

Calling these strategies “passive income” is less a technical description and more a psychological one.

It lowers the perceived barrier to entry. It frames participation as effortless wealth accumulation. And it encourages users to underestimate both risk and workload.

A more accurate term might be:

Active income with automation and better UX.

That doesn’t make it bad. It just makes it honest.

Why the Myth Persists

There are three main reasons the “passive income” narrative survives:

1. Early-Stage Excitement

In bull markets, yields are high enough that mistakes feel profitable anyway. Attention to detail seems optional—until it isn’t.

2. Interface Simplicity

DeFi platforms abstract complexity into clean dashboards. When everything is one click away, it feels like nothing important is happening under the hood.

3. Incentive Design

Protocols compete for liquidity. Marketing “passive yield” is more effective than “ongoing portfolio management responsibilities.”

The Real Nature of Crypto Yield

Crypto income isn’t passive—it’s conditionally active.

You can reduce effort with automation, diversified strategies, and long-term positioning. But you cannot eliminate decision-making without also accepting higher risk exposure.

Even “lazy” strategies require:

- periodic review

- risk reassessment

- exit planning

In other words, you’re still in the game—you’re just playing at a slower tempo.

Conclusion: Reframing the Expectation

The idea of passive income in crypto isn’t entirely false—it’s just incomplete.

Yes, capital can be productive without constant manual trading. But productivity does not equal absence of responsibility.

A more grounded framing is this:

Crypto doesn’t eliminate work. It redistributes it into monitoring, adaptation, and risk awareness.

Or put less politely:

You’re not escaping effort—you’re outsourcing it to market conditions.

And the market never really stops working.

REQUEST AN ARTICLE

Key Highlights

- Brady Corporation has agreed to acquire Honeywell’s Productivity Solutions and Services (PSS) division for $1.4 billion in an all-cash transaction

- The PSS business recorded approximately $1.1 billion in annual revenue during 2025 and maintains a workforce of about 3,000 employees worldwide

- The transaction values PSS at around 8x its 2025 EBITDA multiple

- This divestiture represents another step in Honeywell’s strategic portfolio restructuring prior to its anticipated Aerospace business separation in the third quarter of 2026

- Brady anticipates the acquisition will deliver double-digit accretion to adjusted diluted earnings per share in year one, alongside $25 million in yearly cost savings achievable within three years

On April 20, 2026, Honeywell (HON) revealed its decision to divest the Productivity Solutions and Services division to Brady Corporation (BRC) through a $1.4 billion all-cash transaction.

The PSS division specializes in manufacturing mobile computing devices, barcode scanning equipment, and industrial printing technologies, primarily serving warehouse operations and logistics customers. The business unit generated approximately $1.1 billion in annual sales throughout 2025.

The acquisition price of $1.4 billion represents approximately 8 times the PSS division’s 2025 EBITDA performance. Transaction completion is anticipated during the latter half of 2026, contingent upon receiving necessary regulatory clearances.

Honeywell International Inc., HON

Vimal Kapur, Honeywell’s Chief Executive Officer, described the divestiture as an important milestone in executing the organization’s “multi-year portfolio transformation” strategy. The corporation continues advancing plans to separate into two distinct publicly traded entities — one concentrating on Aerospace operations, the other on Automation technologies.

The planned Aerospace business separation remains scheduled for the third quarter of 2026.

This transaction marks another in a series of recent divestitures by Honeywell. The corporation previously sold its Personal Protective Equipment division in 2024 and completed the spinoff of its Advanced Materials business as Solstice Advanced Materials (SOLS) during October 2025.

Additionally, Honeywell continues evaluating strategic alternatives for its Warehouse and Workflow Solutions operations, which encompass the Intelligrated and Transnorm product lines.

Strategic Expansion for Brady Corporation

For Brady, this acquisition represents a substantial strategic expansion. The Milwaukee-headquartered producer of identification solutions, signage, and workplace safety products is leveraging the PSS transaction to enter the data capture, mobile computing, and workflow automation markets.

Brady management projects the acquisition will generate double-digit accretion to adjusted diluted earnings per share during the first complete fiscal year following transaction closure. The organization has established a target of achieving at least $25 million in annual cost synergies within a three-year timeframe.

Following transaction financing, the deal is expected to elevate Brady’s pro forma net debt to EBITDA leverage ratio to approximately 2.5x — a metric that investors will monitor closely throughout the integration phase.

Transaction Structure and Expected Timing

The agreement is structured as an all-cash acquisition, with Centerview Partners serving as Honeywell’s financial advisor. Legal representation includes Kirkland & Ellis, Baker McKenzie, and Womble Bond Dickinson.

Transaction closure is projected for the second half of 2026, pending customary regulatory approvals and satisfaction of closing conditions.

PSS currently operates within Honeywell’s Industrial Automation business segment. Following deal completion, the unit will function under Brady’s corporate structure as a component of an expanded industrial productivity and safety platform.

Since 2023, Honeywell has disclosed approximately $14 billion in strategic acquisitions while concurrently divesting non-strategic assets. The PSS divestiture represents the most recent action in this comprehensive portfolio repositioning initiative.

Brady’s PSS acquisition incorporates roughly 3,000 employees and an established customer base spanning warehouse operations, logistics providers, and manufacturing facilities.

The transaction remains subject to regulatory examination, with integration execution and talent retention identified as potential challenges to achieving the forecasted synergy benefits.

Key takeaways

-

Mastercard is integrating stablecoins into its payment infrastructure to modernize the back-end settlement process, allowing banks and issuers to settle card transactions using regulated digital dollars such as SoFiUSD.

-

The partnership with SoFi Technologies enables SoFi Bank to settle Mastercard transactions in SoFiUSD, while Galileo’s platform allows other banks and fintech issuers to adopt stablecoin settlement.

-

Stablecoin settlement focuses on the post-transaction clearing stage, meaning consumers will continue using cards normally while the underlying settlement between banks may occur through blockchain-based digital assets.

-

By leveraging its Multi-Token Network (MTN), Mastercard aims to support multiple forms of tokenized money, including stablecoins, tokenized deposits and digital representations of fiat currencies.

Stablecoins are increasingly moving beyond the crypto niche and into mainstream financial discussions. A prime example is Mastercard’s move to integrate stablecoins into its card payment settlement process. Rather than abandoning the traditional card model, Mastercard is simply upgrading the back-end infrastructure by introducing regulated digital dollars into the mix.

By teaming up with SoFi Technologies, the payments giant is testing how these digital assets can streamline transaction settlements across its massive network. This initiative signals that the world’s largest payment rails are preparing for a future in which traditional banking and digital assets exist side by side.

The SoFiUSD partnership

Mastercard’s recent initiative involves a partnership with SoFi Technologies, which has introduced a dollar-backed stablecoin called SoFiUSD.

Under this arrangement, SoFi Bank, N.A. intends to use SoFiUSD to settle its Mastercard credit and debit card transactions. Meanwhile, SoFi’s payments infrastructure platform, Galileo Financial Technologies, will enable banks and fintech issuers on its network to opt for stablecoin settlement through Mastercard’s system.

SoFiUSD is issued by a nationally chartered US bank and is reported to maintain a 1:1 cash reserve structure, positioning it closer to bank-issued digital money than to a typical crypto-native asset.

Did you know? The first credit card to gain wide acceptance across multiple merchants was launched by Diners Club in 1950. Cardholders originally received paper statements and paid their bills monthly, laying the foundation for today’s global card payment networks.

Understanding card settlement

Mastercard’s approach makes more sense once you understand how card payments usually work. When a consumer taps or swipes their card, the following steps take place:

-

The payment is authorized.

-

The transaction is recorded.

-

The merchant receives confirmation.

-

The issuing and acquiring banks complete settlement at a later stage.

This final settlement phase traditionally occurs through conventional banking channels during designated clearing windows.

Mastercard’s stablecoin strategy targets this back-end settlement process specifically. It does not change how users experience or initiate payments. From the shopper’s perspective, the payment process would remain unchanged.

How stablecoin settlement would work

Through stablecoin settlement, Mastercard’s network would enable participating banks and issuers to meet transaction obligations using a digital dollar rather than relying solely on traditional fiat transfers.

In practice, the process could unfold as follows:

-

A customer initiates a card payment in their local currency.

-

Mastercard determines the settlement obligations between the issuing bank and the acquiring bank.

-

Instead of relying only on conventional banking channels, one or both parties may settle using stablecoins such as SoFiUSD.

Because stablecoins operate on blockchain infrastructure, they offer the potential for 24/7 settlement independent of traditional banking hours.

This method could reduce delays in cross-border payments and streamline liquidity management for financial institutions.

Did you know? The term “stablecoin” became popular around 2014, but the concept of digital dollars backed by real-world assets had been explored even earlier through experimental crypto projects that attempted to maintain price stability using collateral and algorithmic mechanisms.

The role of Mastercard’s multi-token network

The foundation of this initiative is Mastercard’s Multi-Token Network (MTN). It is designed to support multiple forms of tokenized money, including:

By bridging conventional banking systems with blockchain-based tokens, Mastercard seeks to create a versatile settlement ecosystem in which regulated digital assets can operate alongside traditional financial infrastructure.

The network would enable financial institutions to transfer value more efficiently while continuing to comply with established regulatory standards.

Why Mastercard is entering the stablecoin space

Stablecoins have become one of the fastest-growing parts of the digital asset market in recent years. They combine the price stability of fiat currency with the speed and efficiency of blockchain technology. As a result, they can support fast transfers, programmable payments and near-instant settlement across global networks.

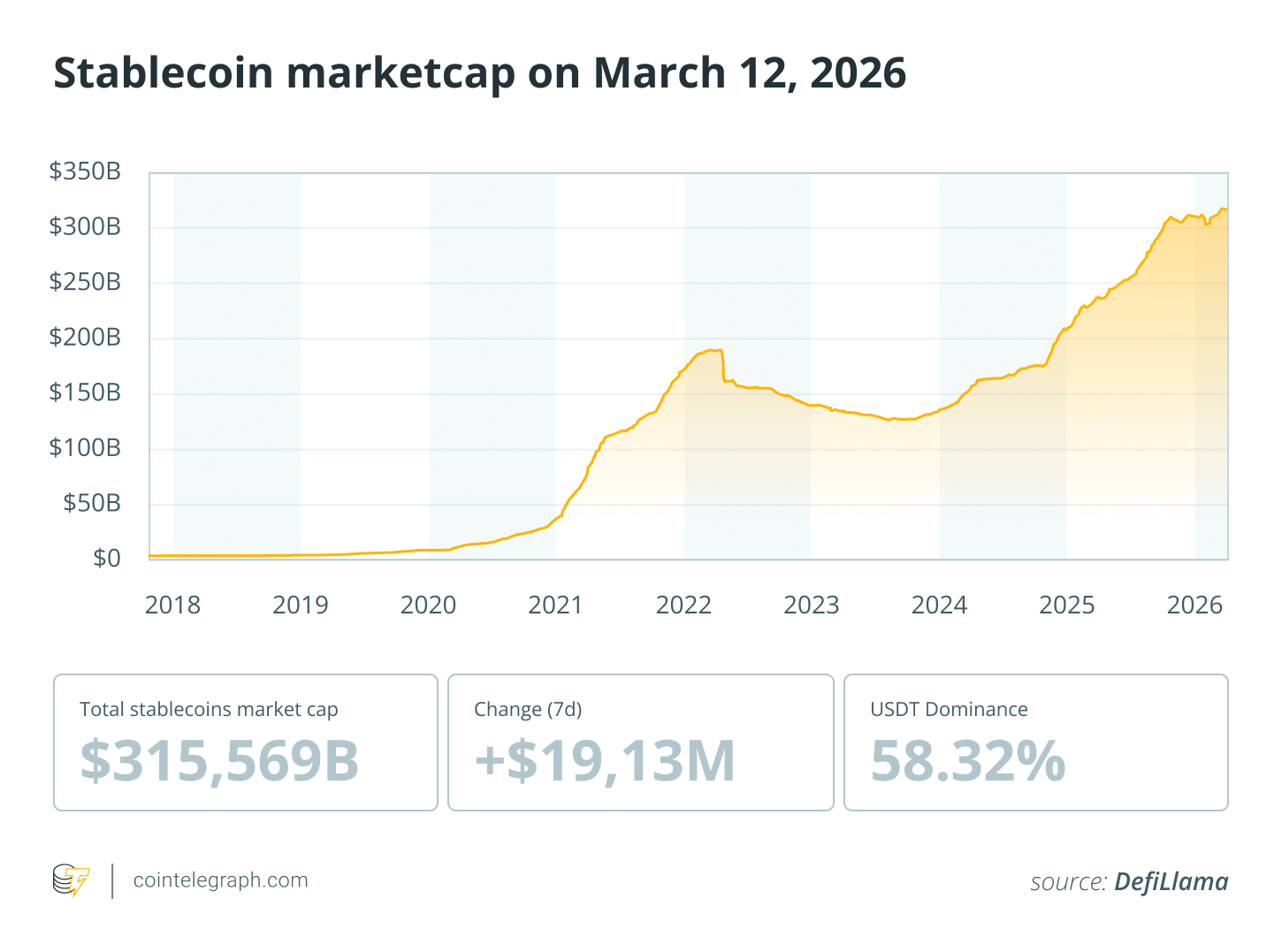

As of March 2026, the stablecoin market had reached a significant milestone, with its total valuation climbing to approximately $314 billion, according to DefiLlama data. This growth followed a breakout year in 2025, during which transaction volumes reached a record $969.9 billion in a single month. Experts now project that monthly volumes are on track to surpass the $1 trillion mark by the end of 2026.

For Mastercard, incorporating stablecoins into its settlement infrastructure helps ensure the company remains central to the changing digital payments ecosystem.

Rather than competing with blockchain systems, Mastercard is positioning itself as a connector between traditional finance and digital asset networks.

Expanding beyond simple payments

The partnership between SoFi and Mastercard also seeks to explore additional financial applications for stablecoins.

Potential uses include:

-

Cross-border remittances

-

Business-to-business payments

-

Treasury management tools

-

Stablecoin-linked card programs

Stablecoins could allow companies to automate complex financial workflows through programmable transactions.

For example, businesses could automatically release payments when contractual conditions are met, reducing manual intervention and operational costs.

Competition from Visa

Mastercard is not alone among global card networks in exploring stablecoin integration. Its main competitor, Visa, has also expanded its use of digital currencies for payment settlement.

Visa has tested cross-border settlement using stablecoins such as USD Coin (USDC), allowing financial institutions to pre-fund international transfers with tokenized dollars. The company has also explored enabling businesses to send payouts directly to stablecoin wallets.

These efforts suggest that stablecoins are becoming a key part of the broader infrastructure competition among leading payment networks.

Why regulation will be crucial

Adoption of stablecoins within mainstream financial systems depends heavily on regulation.

Financial institutions need clear regulatory frameworks that address key concerns, including:

Because SoFiUSD is issued by a regulated US bank, it is likely to inspire greater confidence among regulators and financial institutions than stablecoins that originate in the crypto space.

Payment networks such as Mastercard are therefore prioritizing regulated stablecoins issued by licensed institutions.

Did you know? Global card payment systems process tens of billions of transactions each year, with card networks handling thousands of payments per second during peak shopping periods such as Black Friday and major online retail events.

Challenges to widespread adoption

Despite growing interest, several challenges could limit the wider adoption of stablecoin settlement.

These challenges include:

-

Integration complexity for banks and payment processors

-

Regulatory differences across jurisdictions

-

Liquidity management between fiat and digital assets

-

Interoperability between blockchains and financial networks

Moreover, consumers are unlikely to notice major changes because the technology mainly affects back-end infrastructure rather than the front-end payment experience.

The bigger picture for digital payments

Mastercard’s stablecoin initiative is part of a broader transformation taking place in global finance. Stablecoins were initially used mainly for cryptocurrency trading. Today, they are increasingly viewed as potential tools for payments, remittances and broader financial infrastructure.

If stablecoin settlement proves efficient and reliable, card networks could eventually operate within a hybrid system that combines traditional banking rails with blockchain-based digital assets.

Mastercard is not looking to replace traditional payments. Rather, it is upgrading the under-the-hood infrastructure of global card networks. By integrating regulated stablecoins like SoFiUSD into its Multi-Token Network, the company is preparing its infrastructure for a more digital economy.

The goal is to create a system that is faster, more flexible and available 24/7, while ensuring the average shopper notices no difference at the checkout counter.

Cointelegraph maintains full editorial independence. Guides are produced without influence from advertisers, partners or commercial relationships. Content published in Guides does not constitute financial, legal or investment advice. Readers should conduct their own research and consult qualified professionals where appropriate.

What went right this week: a healthy kickstart for school dinners, plus more

(VIDEO) Japan’s 10 Deadliest and Strongest Earthquakes in History Highlight Nation’s Seismic Vulnerability

Melbet APK Maroc scurit et protection des utilisateurs.94

-

Crypto World7 days ago

Crypto World7 days agoThe SEC Conditionalises DeFi Platforms to Be Avoided for Broker Registration

-

NewsBeat6 days ago

NewsBeat6 days agoTrump and Pope Leo: Behind their disagreement over Iran war

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Theodora Dress

-

Crypto World7 days ago

Crypto World7 days agoSEC Signals Exemption for Crypto Interfaces From Broker Registration

-

News Videos5 days ago

News Videos5 days agoSecure crypto trading starts with an FIU-registered

-

Sports3 days ago

Sports3 days agoNWFL Suspends Two Players Over Post-Match Clash in Ado-Ekiti

-

Crypto World6 days ago

Crypto World6 days agoSEC Proposes Certain Crypto Interfaces Don’t Need to Register as Brokers

-

Business22 hours ago

Business22 hours agoPowerball Result April 18, 2026: No Jackpot Winner in Powerball Draw: $75 Million Rolls Over

-

Crypto World3 days ago

Crypto World3 days agoRussia Pushes Bill to Criminalize Unregistered Crypto Services

-

Politics3 days ago

Politics3 days agoPalestine barred from entering Canada for FIFA Congress

-

Business4 days ago

Business4 days agoCreo Medical agree sale of its manufacturing operation

-

Politics1 day ago

Politics1 day agoZack Polanski demands ‘council homes not luxury flats for foreign investors’

-

Entertainment6 days ago

Entertainment6 days agoBrand New Day’ Footage Reveals the Devastating Impact of ‘Now Way Home’

-

Tech5 days ago

Tech5 days agoMicrosoft adds Windows protections for malicious Remote Desktop files

-

Entertainment6 days ago

Entertainment6 days agoKarol G’s ‘Ultra Raunchy’ Coachella Set Gave ‘Satanic Vibes’

-

Crypto World3 days ago

Crypto World3 days agoRussia Introduces Bill To Criminalize Unregistered Crypto Services

-

Sports7 days ago

Sports7 days agoAaron Judge says Yankees need to ‘simplify’ approach amid offensive slump

-

Entertainment7 days ago

Entertainment7 days agoHow Babylon 5 Turned Brief Side Story Into Emotional Masterpiece

-

Tech7 days ago

Tech7 days agoWhat was the first ransomware attack to demand payment in Bitcoin?

-

Tech5 days ago

Tech5 days ago‘Avatar: Aang, The Last Airbender’ Leaked Online. Some Fans Say Paramount Deserves the Fallout

You must be logged in to post a comment Login