Crypto World

Australia passes crypto regulation requiring exchanges to obtain financial services licenses

Australia passed legislation on Wednesday, creating its first comprehensive regulatory framework for digital assets that requires crypto exchanges and custody providers to obtain financial services licenses.

The Corporations Amendment (Digital Assets Framework) Bill 2025 cleared both houses on April 1, bringing firms that hold digital assets on behalf of customers into the existing Australian Financial Services Licence regime.

Australia’s bill creates two new regulated categories under the Corporations Act: digital asset platforms, which hold crypto on behalf of users, and tokenized custody platforms, which hold real-world assets and issue a corresponding digital token.

Operators of both must obtain an Australian Financial Services License from ASIC, bringing them under the same core rules as brokers or fund managers, including requirements to safeguard client assets, provide standardized disclosures, avoid misleading conduct, and maintain dispute resolution and compensation systems.

Instead of regulating crypto itself, the law targets the companies in the middle that control customer funds, aiming to reduce risks like commingling, insolvency, and misuse of assets that have caused losses in past crypto failures.

Research from the Digital Finance Cooperative Research Center and industry groups estimates Australia could generate as much as A$24 billion annually from tokenized markets, payments, and digital assets, roughly 1% of GDP. Under the previous regulatory path, the country was on track to capture just A$1 Billion of that by 2030.

A Kraken spokesperson said the law provides a “top-down signal” that Australia is serious about digital assets, adding that clearer rules would give firms confidence to invest and expand locally.

Kate Cooper, CEO of OKX Australia and co-chair of the Digital Economy Council of Australia, called the bill a “pivotal moment,” saying it establishes a foundation for institutional participation and long-term capital allocation.

Ronin Ethereum is migrating to a Layer 2 on May 12 with roughly 10 hours of scheduled downtime.

Summary

- Ronin will hard fork at block 55,577,490 on May 12, transitioning from an independent sidechain to an Ethereum Layer 2 on the OP Stack.

- All transfers, swaps, and smart contract interactions will pause for roughly 10 hours during the migration window.

- RON token inflation will drop from over 20% to below 1%, with 90 million RON redirected to the treasury as marketplace fees rise to 1.25%.

Ronin, the gaming-focused blockchain behind Axie Infinity, is executing a hard fork on May 12 to complete its transition from an independent sidechain to an Ethereum Layer 2. The migration was announced in April and will trigger at block 55,577,490, expected around 15:16 UTC.

All Ronin transactions will pause for roughly 10 hours during the migration window. That covers transfers, swaps, NFT trades, and smart contract interactions. Node operators on Ronin mainnet are required to upgrade to release 1.2.2 before the hard fork.

What changes after the migration

Ronin said the move is about plugging “back into the mothership.” The new structure will link the network directly to Ethereum for settlement and data availability, replacing the older nine-validator sidechain model with OP Stack rollup infrastructure.

RON token inflation will fall sharply from over 20% annually to below 1% under a new Proof of Distribution model. Marketplace fees will also rise from 0.5% to 1.25%, with 90 million RON tokens previously allocated for staking redirected to the Ronin treasury.

Ronin will integrate EigenDA to handle data availability for transactions, storing data off-chain while keeping it verifiable and accessible to Ethereum. The migration brings Ronin into the same OP Stack ecosystem as other chains including Celo and Fraxtal.

Context: the $625 million hack that made this necessary

While operating as an independent sidechain in March 2022, Ronin suffered the largest DeFi bridge exploit in history, with $625 million in ETH and USDC drained from its bridge. The attack exposed the structural risks of the sidechain model, where only a small number of centrally-managed validators were responsible for securing the network.

The Layer 2 transition directly addresses those concerns by inheriting Ethereum’s security rather than relying on Ronin’s own validator set. The Ronin bridge previously migrated to Chainlink’s cross-chain interoperability protocol in April 2025 as an earlier step in securing its infrastructure ahead of the full L2 move.

Crypto.com announced that its Dubai entity has received a Stored Value Facilities (SVF) license from the Central Bank of the United Arab Emirates (CBUAE), authorizing crypto-funded payments for Dubai government fees through its platform. The company said customers can fund payments with digital assets, while settlements are processed in UAE dirhams or in dirham-backed stablecoins approved by the central bank under the SVF framework.

The approval, tied to Crypto.com’s local entity Foris DAX Middle East FZE (operating as Crypto.com), enables the firm to activate its partnership with Dubai’s Department of Finance and offer digital asset payment services for government fees in line with the emirate’s cashless payments strategy. The company indicated that the license could pave the way for future integrations with Emirates Airlines and Dubai Duty Free, though such services would require additional approvals from the UAE central bank.

According to Cointelegraph, Crypto.com’s UAE expansion is part of a broader strategy to strengthen its regulatory footprint in the region while pursuing a multi-jurisdictional compliance framework that includes EU licensing under MiCA and a conditional US OCC approval for a national trust bank charter to support crypto custody and related services.

Key takeaways

- The Central Bank of the UAE granted a Stored Value Facilities license to Crypto.com’s Dubai affiliate, Foris DAX Middle East FZE (Crypto.com).

- Under the SVF license, users can fund government fee payments with digital assets, with settlements settled in UAE dirhams or dirham-backed stablecoins approved by the central bank.

- The authorization supports a digital asset payment workflow with Dubai DoF and aligns with the city’s broader cashless payments initiative.

- Potential future crypto-funded payments with Emirates Airlines and Dubai Duty Free are on the horizon, subject to further regulatory sign-offs.

- Crypto.com’s UAE push complements its existing regulatory footprint (VARA VASP license) and its ongoing global licensing efforts, including MiCA in the EU and a conditional OCC approval for a national trust charter in the United States.

UAE regulatory milestone and the SVF framework

The SVF regime in the UAE is designed to govern facilities that store monetary value electronically and enable its use for payments. By granting the license to Crypto.com’s local entity, the CBUAE authorizes the firm to facilitate crypto-backed payments for government-related fees while maintaining fiat or stablecoin settlement channels approved under the framework. This move deepens Crypto.com’s regulatory standing in the UAE and reinforces the city’s strategy to integrate digital assets into government and public-facing payment rails. The license explicitly covers settlements in dirhams or in dirham-linked stablecoins that the central bank has approved for SVF participants.

Operational model: crypto funding to dirham settlement

In practical terms, residents and businesses could use Crypto.com’s platform to fund government fee payments with digital assets, with the corresponding settlement settled in local currency or in CBUAE-approved stablecoins. The arrangement is anchored to Crypto.com’s Dubai entity and its partnership with the Dubai Department of Finance, enabling a regulated pathway for cryptocurrency-influenced government payments. While the company flagged possible future integrations with Emirates Airlines and Dubai Duty Free, these initiatives remain contingent on additional regulatory clearances. The development signals a broader move toward officially sanctioned crypto-enabled payment channels within the UAE’s financial ecosystem and highlights the attention authorities are giving to digital asset settlement mechanics and AML/KYC controls in public-use cases.

Regulatory footprint and cross-border ambitions

The UAE expansion sits within a broader regulatory narrative for Crypto.com. In the emirate, the company already holds a Virtual Asset Service Provider license from the Dubai-based regulator VARA, underscoring an institutional-grade, compliance-focused posture for its regional operations. Beyond the UAE, Crypto.com has pursued licensing aligned with the EU’s Markets in Crypto Assets (MiCA) framework and has publicly pursued a national trust bank charter in the United States under an OCC program that would enable custody services for digital assets. Separately, the firm has moved into regulated event-based derivatives and prediction markets through a US affiliate, reflecting a strategy to couple enhanced regulatory oversight with a wider suite of trading and payments products tied to cryptocurrencies. This multi-jurisdictional approach is designed to reduce regulatory risk while expanding access to institutional and retail users under clear supervisory regimes.

From a policy perspective, the UAE’s SVF milestone reinforces a pattern of central-bank-backed pathways for digital assets within government services, offering a potential blueprint for other jurisdictions seeking to integrate crypto assets into public payments. It also raises questions for banks, payment processors, and crypto firms about licensing ladders, cross-border interoperability, and the balance between innovation and regulatory compliance. As authorities in different regions adjust to evolving standards around custody, stablecoins, and on/off-ramps, the UAE example illustrates how centralized oversight can enable cryptocurrency-enabled services while maintaining financial-system safeguards.

Looking ahead, observers will be watching how the DoF and central bank calibrate further integrations, especially in larger commercial payments beyond government fees. The ongoing convergence of crypto payments with mainstream financial rails depends on continued clarity around eligible stablecoins, reserve standards, and risk-management expectations for participants operating within SVF frameworks.

Closing perspective: the UAE’s SVF license for Crypto.com marks a notable step in codifying crypto-enabled payments within a sovereign cashless agenda, yet the broader regulatory journey—spanning cross-border licensing, custody standards, and government-linked deployments—will unfold as approvals are granted and new use cases are evaluated against evolving policy and enforcement considerations.

The U.S. Senate Banking Committee is poised to take up a markup on the Digital Asset Market Clarity Act (CLARITY) this week, with Democratic lawmakers signaling they may withhold support if ethics provisions remain unresolved. The bill, which the House passed in July 2025, has faced months of delay as negotiators work through language on stablecoin yields, tokenized equities, and other industry-specific concerns. According to Cointelegraph, the committee’s action comes as policymakers seek a clearer framework for crypto markets without compromising ethical standards for public officials.

Although the Senate Agriculture Committee moved its own version of CLARITY forward in January, the legislation still must clear both panels to align securities and commodities authorities and to address jurisdictional differences. “Negotiations continue to be positive, and I remain confident we can get a bipartisan bill over the finish line this Congress,” Senate Democrat Kirsten Gillibrand told Cointelegraph. “Americans deserve a well-regulated market with strong consumer protections and real ethics reforms so politicians can’t cash in on their insider status for personal gain.”

Key takeaways

- House-passed CLARITY Act dates back to July 2025, setting a bipartisan framework for a regulated crypto market.

- Senate Agriculture Committee advanced its version in January, signaling continued momentum across chambers.

- The Banking Committee markup is scheduled this week, with ethics provisions and stablecoin yield language identified as critical sticking points.

- Political dynamics show divergent views on ethics and conflicts of interest, potentially shaping whether the bill can reach the floor for a full vote.

- Any path to law requires reconciliation between House and Senate outputs and presidential action; timing remains uncertain.

Policy dynamics and the path forward

From a regulatory architecture standpoint, CLARITY represents a concerted effort to codify a market structure for digital assets that aligns with existing securities and commodities regimes. The contrast between committee positions underscores ongoing tensions between innovation, investor protection, and public accountability. As negotiations unfold, many lawmakers view ethics provisions as the gatekeeper that could determine the bill’s ultimate fate, even if other provisions enjoy broad bipartisan support. In this context, the intersection of crypto policy with congressional ethics rules is increasingly in focus, with industry stakeholders watching closely for any precedent-setting language that could influence future oversight and enforcement actions.

Democrats have pressed for robust ethics safeguards to curb conflicts of interest among members of Congress and top executive branch officials. Gillibrand’s remarks reflect a broader aim to ensure that policy debates on digital assets are insulated from personal financial considerations. Republicans, including Senate Banking Chair Tim Scott, have emphasized the need for a timely, bipartisan deal but indicate that ethics language must ultimately be resolved on the floor rather than within committee confines. Wyoming Senator Cynthia Lummis, a leading advocate for CLARITY in the Senate, has encouraged colleagues to move forward, signaling continued support for a functional regulatory framework while acknowledging the ethics concerns that lawmakers have raised.

Industry voices have framed the ethics debate as a practical hurdle that could stall otherwise constructive policy progress. Cody Carbone, CEO of the Digital Chamber, argued that while ethics matters, it should be tackled on the Senate floor and not become a fatal obstruction to markup. “Ethics has to be tackled on the floor; it’s not within the jurisdiction of the Senate Banking Committee, so I don’t expect it to hold up the markup,” he told Cointelegraph.

Stablecoins, yield, and regulatory nuance

A central flashpoint remains the treatment of stablecoins and yield mechanics within the CLARITY framework. Earlier this month, Senators Thom Tillis and Angela Alsobrooks announced a compromise on stablecoin yield that could unlock movement on the bill after months of delay. Nevertheless, Democratic leadership has signaled that even with progress on yield, ethics provisions could derail prospects for a floor vote. Gillibrand’s position underscores a broader condition: any final package must address governance integrity to satisfy lawmakers who have prioritized anti-corruption safeguards alongside market structure clarity.

Beyond ethics and yield language, the bill’s broader aim is to reconcile differences between securities and commodities laws as they apply to digital assets, including questions around tokenized equities and other complex instruments. The Senate Agriculture Committee’s earlier action indicates a willingness to pursue a comprehensive approach, but the Banking Committee’s markup will test whether a unified, bipartisan compromise can be achieved in a manner compatible with the regulatory aspirations of both chambers.

Broader implications for institutions and oversight

For crypto firms, exchanges, and financial institutions, the CLARITY process signals a tightening of regulatory expectations around market structure, disclosures, and governance. A clarified framework could influence licensing trajectories, compliance costs, and the scope of permissible activities within crypto markets. From an enforcement perspective, alignment with established prudential standards—while preserving innovation—would likely intersect with ongoing oversight by the SEC, CFTC, and DOJ, as well as corresponding AML/KYC regimes. Observers also note potential interactions with international standards, such as the European Union’s MiCA, as policymakers compare approaches to cross-border compliance and transfer of risk across jurisdictions.

As the legislative effort unfolds, market participants must remain alert to evolving guidance on tokenized assets, stablecoins, and digital yield strategies. The path to law will depend not only on the content of ethics provisions but also on the administration’s priorities and the ability of lawmakers to secure a reconciled, floor-ready bill that can withstand potential veto or political headwinds.

Closing perspective

With the markup advancing and ethics debates unresolved, CLARITY’s fate rests on a delicate balance between bipartisan agreement and robust governance safeguards. Stakeholders should monitor committee proceedings for signs of a workable compromise and assess how any final text could reshape regulatory expectations for the crypto industry, compliance programs, and cross-border policy alignment.

Crypto World

Senator Moreno Vows to ‘Break the Cartel’ as Banks Panic Over CLARITY Act Stablecoin Yields

Senator Bernie Moreno on Monday accused the U.S. banking lobby of full panic mode over CLARITY Act stablecoin yields. The American Bankers Association is urging bank CEOs to pressure senators against the provisions.

The Ohio Republican sits on the Senate Banking Committee. He published the criticism on X ahead of Thursday’s CLARITY Act markup.

ABA Letter Targets CLARITY Act Stablecoin Yield Language

ABA CEO Rob Nichols sent a Sunday letter to every bank CEO in the country. He called for “immediate engagement” on stablecoin yield policy.

Nichols warned that the current proposal would prompt deposit flight into payment stablecoins, citing risks to growth and stability. His note described what banks call a stablecoin loophole in the committee’s draft.

“we believe committee members may not be fully aware of the risks to the economy by the stablecoin loophole,” read an excerpt in the letter, citing Nicholas.

Moreno rejected that framing, saying the question was already litigated during the GENIUS Act debate led by Senator Bill Hagerty.

What’s at Stake Thursday

The Senate Banking Committee marks up the CLARITY Act on Thursday, May 14, at 10:30 a.m. ET. Polymarket bettors now give the bill a 73% chance of becoming law this year.

Senators Thom Tillis and Angela Alsobrooks brokered the disputed compromise text. It bars yield “economically or functionally equivalent” to deposit interest. The provision still permits rewards from bona fide platform activity.

Patrick Witt of the President’s Council of Advisors for Digital Assets called out the bank lobby. He said the ABA refused White House meetings on the yield issue back in February.

“I specifically requested the attendance of Mr. Nichols and other bank trade CEOs at the meetings we hosted back in February to resolve the stablecoin rewards/yield issue. They refused. I guess the White House was beneath them? In their defense, I wouldn’t want to have to defend their position in public either,” he said.

A successful markup would advance the bill toward a full Senate floor vote. A stall could sideline U.S. crypto legislation for the rest of the session.

Moreno said he plans to vote to break the cartel.

The post Senator Moreno Vows to ‘Break the Cartel’ as Banks Panic Over CLARITY Act Stablecoin Yields appeared first on BeInCrypto.

Crypto World

Crypto Lawyer Warns Anthropic Stock Crackdown Risks Litigation as Claude Launches on AWS

Crypto lawyer Gabriel Shapiro warned that Anthropic’s May 11 stock crackdown could trigger major litigation, with the AI company declaring void all secondary share trades on Forge, Hiive, and similar platforms.

His warning landed the same day Anthropic switched on Claude Platform inside Amazon Web Services (AWS), opening direct enterprise access to its first-party APIs.

Forge, Hiive and SPVs declared void

Anthropic’s transfer restrictions, lodged in its bylaws, now nullify any share movement without explicit board approval. The policy covers beneficial interests, forward contracts, special purpose vehicles, and tokenized securities.

The company’s blocklist names Open Door Partners, Unicorns Exchange, Pachamama, Lionheart Ventures, Sydecar, Upmarket, and new offerings posted on Forge and Hiive. Purported buyers receive no stockholder rights.

“Any sale or transfer of Anthropic stock… that has not been approved by our Board of Directors is void and will not be recognized on our books and records,” read an excerpt in the announcement.

Void Versus Voidable Raises Litigation Stakes

Shapiro, founder of crypto law firm MetaLeX, flagged the wording as the most aggressive stance Anthropic could have taken.

Declaring transfers void rather than voidable forecloses most equitable defenses for downstream buyers under Delaware corporate law.

He raised the prospect of original sellers keeping both the cash and the shares while downstream buyers chase upstream parties for recourse.

The wording also opens questions about whether entire chains of secondary buyers get wiped from the cap table at once.

Secondary platforms had priced Anthropic at implied valuations well above the roughly $350 billion struck in its most recent employee tender, fueling demand for indirect exposure vehicles the company now considers invalid.

Claude Platform Launches Inside AWS

The AWS rollout reached general availability hours later. Enterprise customers can authenticate through AWS Identity and Access Management, consolidate billing, and access the full Anthropic API surface without a separate contract.

The launch follows an April agreement covering up to 5 gigawatts of Trainium compute over a decade, paired with a fresh Amazon investment exceeding $5 billion. Anthropic recently joined the pre-IPO trillion-dollar club alongside OpenAI and SpaceX.

The two moves point in opposite directions yet share one logic. Anthropic wants tighter control over who owns its equity while widening the funnel for who consumes its models.

The post Crypto Lawyer Warns Anthropic Stock Crackdown Risks Litigation as Claude Launches on AWS appeared first on BeInCrypto.

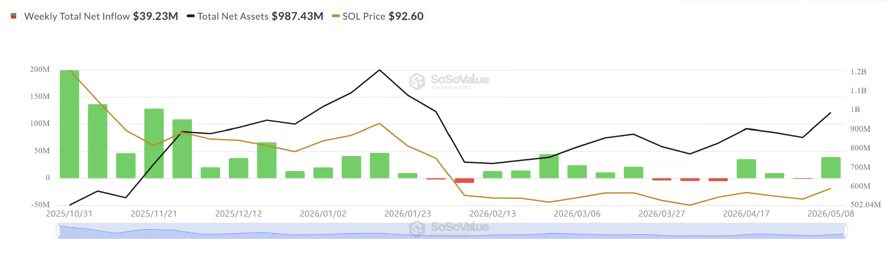

The spot Solana (SOL) exchange-traded funds (ETFs) recorded their strongest weekly performance since February, attracting $39.23 million in total net flows. The surge in capital inflows coincided with SOL futures open interest rising by $1.5 billion in May, signaling a sharp increase in trader positioning across the derivatives markets.

The rise in market activity comes alongside Solana’s 15% rally to $97 in the past seven days, with traders targeting the next major resistance level at $120.

SOL ETF demand rises with futures interest

Bitwise’s BSOL ETF led the latest inflow wave with $36 million in weekly net inflows last week, while Fidelity’s FSOL added over $1.8 million. Since its launch, BSOL has attracted $861 million, accounting for nearly 81% of cumulative inflows across all spot SOL ETFs, which now total about $1.06 billion.

Spot SOL ETF netflows. Source: SoSoValue

Futures activity rose alongside the ETF demand. Solana open interest (OI) climbed to $6.4 billion from $4.94 billion on May 1, marking a 29.5% increase in less than two weeks.

Aggregated spot cumulative volume delta (CVD), which measures the net difference between market buy and sell orders, climbed to nearly $250 million from $163 million in five days, during SOL’s push toward $96.

The futures CVD expanded to about $593.6 million after rising steadily from May 5 onward, as buyers absorbed sell-side liquidity in both the spot and futures markets.

SOL price, aggregated open interest, spot, and futures CVD and funding rate. Source: velo.chart

The funding rate held near 0.065%, indicating traders continued to pay to maintain long exposure. The buying activity has started to flatten near the $95-$96 range as spot and volume deltas have cooled over the past 24-hours.

Related: South Korea crypto holdings halve in a year as investors turn to stock market

Solana eyes a breakout: Is $120 next?

Solana is forming an Adam and Eve pattern near the $95 resistance level, with the setup’s neckline directly at the current breakout zone. A confirmed move above that level places the technical target near $120.

An Adam and Eve pattern on the higher time frame chart could signal a bottom for SOL if price successfully turns the $95 resistance level into support.

SOL/USDT, one-day chart. Source: Cointelegraph/TradingView

SOL also pushed above its 100-day exponential moving average for the first time since October 2025, adding another technical shift to the mix alongside ETF inflows and rising futures positioning.

A confirmed daily close and consolidation above $95 could open the path toward the pattern’s projected target near $120, due to a lack of resistance sitting between the two levels after the 42% dip in February.

Crypto analyst BATMAN noted that Solana recently broke above a 231-day downtrend on the SOL/BTC daily chart, signaling improving relative strength against Bitcoin. According to the analyst, the $89-$91 zone now acts as the nearest support cluster and a likely retest region if SOL holds above the breakout area.

SOL/USDT, one-chart analysis by BATMAN. Source: X

Related: XRP metrics line up bull signals for ‘full-scale rally’ to $2

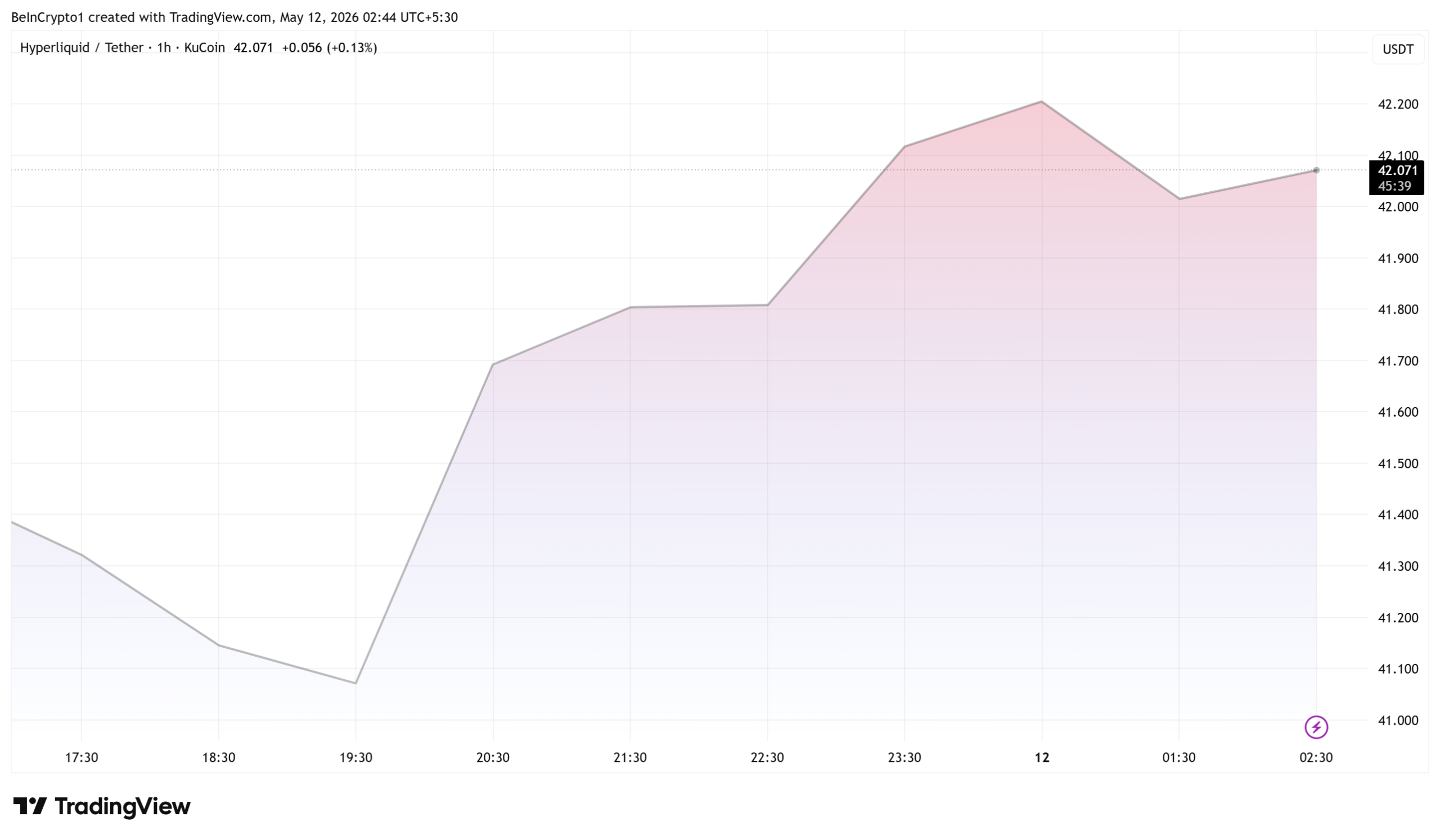

21Shares said it will list its spot Hyperliquid ETF, THYP, on Nasdaq on May 12. The product gives brokerage clients regulated exposure to the native token of the Hyperliquid perpetuals trading network.

The fund is structured as a grantor trust, not a 1940 Act fund. That setup lets the sponsor stake held HYPE for yield while keeping passive price exposure.

21Shares To Launch Spot Hyperliquid ETF on Nasdaq With Built-In Staking

21Shares charges a 0.30% annual sponsor fee, paid in HYPE. Custody sits with Anchorage Digital Bank and BitGo Bank & Trust. Both providers use cold storage backed by up to $350 million in joint theft and fraud insurance.

The trust may stake between 30% and 70% of its HYPE holdings through Figment Inc. The sponsor has discretion to push that share as high as 100%.

Staking rewards are split roughly 70% to the trust and 30% to the provider.

In-kind creation and redemption baskets run in lots of 10,000 shares and are limited to authorized participants. The fund tracks the FTSE Hyperliquid Index as its pricing benchmark.

Hyperliquid’s HYPE token surged on the news, and was trading for $42.071 as of this writing.

Risks and the Spot HYPE ETF Race

The prospectus carries strong risk language. It warns that THYP is unsuitable for investors who cannot afford a total loss, citing HYPE’s annualized volatility above 126%.

Validator jailing penalties, staking lockups of one to seven days, and redemption delays are also flagged in the filing.

21Shares already runs a 2x leveraged HYPE product, TXXH, which began trading on April 30. Rivals Bitwise and Grayscale have filed competing spot HYPE ETFs under the tickers BHYP and GHYP.

The launch follows months of growth in Hyperliquid’s perpetuals volume. Early flows into THYP will signal how traditional investors price the venue.

The post HYPE Price Rises As 21Shares Unveils Groundbreaking Hyperliquid ETF appeared first on BeInCrypto.

Crypto investment products extended their streak of inflows for a sixth consecutive week, reaching $4.9 billion in total. Exchange-traded products (ETPs) gathered roughly $858 million, up sharply from the prior week’s $118 million, as improving sentiment around US crypto legislation helped push Bitcoin above $80,000 and lift assets under management to their highest level since February. The development comes as investors weigh the potential impact of regulatory clarity on the sector’s capital flows.

Key takeaways

- Six straight weeks of inflows into crypto investment products, totaling $4.9 billion year-to-date, with ETPs contributing about $858 million in the latest week.

- Bitcoin led the charge, drawing $706 million in new exposure and pushing year-to-date inflows for Bitcoin-related products to $4.9 billion; total crypto ETP assets exceeded $160 billion, the highest since February.

- Short-Bitcoin funds recorded the week’s largest outflows, totaling $14 million, signaling a cautious shift as investors reduce bets against BTC amid a rising price backdrop.

- Ether ETFs added $77 million in inflows after last week’s outflows; Solana and XRP also drew notable investor interest with inflows around $48 million and $40 million, respectively.

- Late-week profit-taking capped the rally: spot Bitcoin ETFs posted about $423 million in outflows on Thursday and Friday, leaving net weekly inflows around $623 million, per SoSoValue.

Bitcoin drives the flow as sentiment improves

Bitcoin remains the primary catalyst for the renewed wave of investor interest, with total Bitcoin-related inflows for the week lifting the year-to-date total to roughly $4.9 billion. The crypto market’s broader asset base also swelled, taking crypto ETP assets under management to more than $160 billion — a level not seen since February. The improvement in appetite appears linked to evolving policy chatter in the United States, particularly around legislative efforts that could clarify certain regulatory aspects of crypto markets.

In a note to clients, CoinShares head of research James Butterfill pointed to the final compromise proposal surrounding stablecoin yields as a supportive factor for the renewed inflows. The proposal, released on May 1, has been cited by market participants as a potential milestone toward more predictable regulatory treatment, which in turn could bolster institutional participation in crypto markets.

Broader momentum: ETH, SOL, and XRP pick up steam

Ethereum investment products posted $77 million in inflows, reversing the prior week’s outflows and underscoring sustained interest in the network’s upgrade cycle and activity. Solana and XRP complemented the broader trend with inflows of roughly $48 million and $40 million, respectively, illustrating a diversified appetite beyond Bitcoin for those exploring multi-chain exposure and liquidity profiles.

Despite the positive momentum, some segments of the market remained sensitive to the pace of gains and macro news flow. The week’s data show buyers stepping in for high-conviction assets while more tactical positions were pared back as prices fluctuated near key levels.

Profit-taking and market mechanics temper the rally

Profit-taking emerged as a notable feature toward the end of the week. After Bitcoin briefly dipped below the $80,000 mark on Thursday, US-listed spot Bitcoin ETFs recorded about $423 million in outflows on Thursday and Friday. SoSoValue estimated that this late-week selling trimmed net weekly inflows to roughly $623 million. The oscillation underscores how traders balanced the outlook for further upside with the realization of gains accumulated in the run-up.

On-chain analytics added another layer to the narrative. CryptoQuant highlighted a surge in realized profits on Monday, quantified at 14,600 BTC — about $1.1 billion at the time — marking the largest single-day profit-taking since December 10, when Bitcoin traded near $90,000. The firm noted that rising realized profits could prompt further profit-taking as BTC tests multimonth highs, especially if the market continues to rally on improving sentiment.

Industry participants offered their take on the price dynamics. Laser Digital’s derivatives desk observed that the rally began to stall midweek as traders booked profits from long positions. The desk suggested that the pace and scale of buying from institutional or large-scale participants could influence the trajectory of the move, with some investors reportedly pre-positioned ahead of anticipated bids from major players such as MicroStrategy this week. Such positioning, the note implied, can trigger additional take-profit flow if the market moves faster than anticipated.

Regulatory backdrop, adoption implications, and what to watch next

The week’s flows arrive amid a broader regulatory backdrop that could shape how investors price risk and allocate capital. The May 1 release of a compromise proposal on stablecoin yields is widely viewed as a potential signal of bipartisan movement toward clearer rules for digital assets and related products. While not a complete policy framework, the document has been cited by market participants as a sign that policymakers are closer to laying out concrete guardrails, which could unlock further institutional engagement if implemented.

Investors will be watching several development threads in the coming weeks: filings and approvals for additional ETPs and ETFs, the trajectory of the CLARITY Act conversations and its potential impact on stablecoins and custody, and any further guidance on how regulated markets will treat on-chain activity and cross-border flows. The balance between appetite for risk-on exposure and the need for regulatory clarity will likely dictate whether inflows sustain their momentum or wobble in the face of new headlines.

What this means for investors, traders, and builders

For investors, the sixth straight week of inflows signals growing confidence in crypto investment products and the potential for continued diversification beyond Bitcoin. The breadth of inflows across Bitcoin, Ether, Solana, and XRP suggests a maturing market where participants are evaluating multiple narratives — from layer-1 and smart contract platform growth to cross-chain liquidity and appeal to traditional asset allocators.

Traders will likely monitor the near-term dynamics around price levels and the rate of profit-taking. The observed outflows from spot Bitcoin ETFs late in the week highlight the importance of timing and risk management in a market characterized by volatile swings even as macro catalysts align with a constructive sentiment backdrop.

For builders and ecosystem participants, the regulatory trajectory matters. A clearer framework around stablecoins and crypto products could reduce uncertainty for custodial and fund-structure providers, potentially enabling more sophisticated product offerings and improved investor protection. The market’s next phase will hinge on how quickly policy moves translate into durable, rules-based market access and whether the optimism surrounding regulatory clarity translates into sustained capital inflows.

Looking ahead, readers should watch the progress of the CLARITY Act-related discussions and any concrete steps toward standardizing yields, as well as the continued delivery of new investment products that blend on-chain innovation with traditional fund structures. As always, the liquidity picture will adapt to both price action and policy signals, and traders should stay attentive to evolving flows data and on-chain activity that could foreshadow the next leg of the cycle.

Readers should remain attentive to the evolving regulatory landscape and the cadence of new product approvals, as these factors will shape liquidity and investor participation in the months ahead. The market seems to be moving toward greater clarity, but how and when that translates into durable inflows remains an open question worth watching closely.

Bitcoin (BTC) climbed to an intraday high of $82,450 on Sunday after President Donald Trump knocked back Iran’s latest proposal during negotiations to end the ongoing conflict. The rejection triggered wild swings across the market, and the flagship cryptocurrency tumbled towards $80,000 on Monday as volatility returned to the crypto market.

According to data from CoinGecko, BTC fell from around $81,500 to $80,500 minutes after President Trump called Iran’s counteroffer “totally unacceptable.” However, buyers defended the $80,000 level as the rebound wiped out over $400 million in short positions.

Strategy To Replenish Bitcoin Reserves After Every Sale

Strategy co-founder Michael Saylor has said the company plans to buy far more Bitcoin than it will sell. Saylor’s comments come as the company contemplates selling some of its Bitcoin reserves to fund dividend payments for its STRC perpetual preferred stock. Saylor stated in multiple interviews that while Strategy could sell some of its Bitcoin holdings, it would offset these sales with new purchases, adding that companies should be net accumulators of Bitcoin, not net sellers.

“In these periods, even if we were to sell one bitcoin, we’d be buying 10 to 20 more bitcoins. You should be a net accumulator of Bitcoin. You don’t want to be a net seller of bitcoin because bitcoin is capital.”

Morgan Stanley Bitcoin ETF Sees $194M In Inflows

Morgan Stanley’s spot Bitcoin ETF, the Morgan Stanley Bitcoin Trust (MSBT), has recorded $194 million in inflows since its debut, without a single day of outflows. Between its launch and May 7, the ETF recorded 17 days of inflows, 5 sessions with relatively little movement, and 0 days of net outflows. The fund’s stability is remarkable given the current market conditions, and the bank also offers Bitcoin, Ethereum, and Solana through E*TRADE, its retail brokerage platform.

Amy Oldenburg, Morgan Stanley’s head of digital assets, disclosed that the fund had $239.6 million in assets under management (AUM) as of May 7, adding that the fund recorded $20.6 million in inflows on its first day, along with $34 million in trading volume. The fund also has one of the lowest expense ratios at 0.14%, allowing it to undercut its competitors.

Markets Enter Crucial Week

Meanwhile, global markets are entering a critical week, with CPI, PPI, retail sales, and industrial data lined up. However, geopolitical developments could complicate matters after President Trump rejected Iran’s counteroffer. Geopolitical tensions continue to dictate market reactions this year, with Bitcoin and equities experiencing considerable volatility owing to uncertainty tied to the ongoing US-Iran conflict.

The April CPI inflation data is set to be released on Tuesday, followed by PPI inflation data on Wednesday, and retail sales data and production numbers later in the week. The OPEC monthly report could also influence market expectations.

Bitcoin Price Analysis: BTC Traders Watch For Volatility

Bitcoin (BTC) plunged to a low of $80,504 on Monday but held above the $80,000 mark ahead of a data-heavy week. Despite the market swings, the flagship cryptocurrency held above key short-term support levels. Market analysts are divided on whether data releases this week and the evolving geopolitical situation could push investors towards risk assets or trigger another downturn.

The ongoing US-Iran conflict and the situation around the Strait of Hormuz continue to keep the cryptocurrency market, primarily Bitcoin, jittery. The waterway is crucial to oil and natural gas supply, carrying nearly one-fifth of global flows. Oil rose $4 a barrel, while Brent crude rose 4.5% to $105.85. The dollar gained for a second day due to robust US jobs data and safe-haven demand.

Bitcoin’s recent price action has been linked to US-Iran headlines. The flagship cryptocurrency pushed towards $78,700 on May 1 after Iran sent a revised proposal, easing market pressure and improving sentiment. BTC crossed $80,000 on May 4 after President Trump announced “Project Freedom,” a US-led initiative to secure the Strait of Hormuz.

Analysts are keeping an eye on $80,000 and whether BTC can turn it into support. Crypto Tony, an analyst on X, stated that prediction market Polymarket puts the odds of BTC hitting $85,000 in May at 79%. Analysts have marked $78,000 as the first major support level should BTC slip below $80,000. A decisive move above $82,500 could push the flagship cryptocurrency to test $85,000. However, any adverse developments during the US-Iran negotiations could see prices dip again.

JUST IN: 79% chance Bitcoin hits $85,000 this month. pic.twitter.com/mxvGm4eyqS

— Crypto Tony (@CryptoTony__) May 6, 2026

Disclaimer: This article is provided for informational purposes only. It is not offered or intended to be used as legal, tax, investment, financial, or other advice.

Carl Runefelt remembers a different YouTube. The Swedish creator, known to his 650,000 subscribers as Carl Moon, has been making crypto videos since 2017, and he says this bear market has produced a viewership collapse he could not have predicted.

In an interview with BeInCrypto, Runefelt described the moment plainly.

“Even like back in 2018 bear market, like at the low of the bear market, I had more than double the views that I have right now.”

That single line captures a structural reality that the entire crypto creator economy is now wrestling with. Crypto YouTube, once the dominant retail discovery channel for the asset class, is facing its worst crisis to date.

The numbers, platform behavior, industry layoffs, and search trend data all point in the same direction.

The Platform Turning Hostile

In April 2026, YouTube removed multiple crypto channels in a sweep that the platform justified as targeting “harmful and dangerous” content.

The purge wiped out roughly 35 million combined subscribers across affected creators, including Bitcoin.com’s flagship channel, which had been active since 2015.

For top creators still standing, the platform that built crypto YouTube is no longer a reliable home for it. Runefelt described the broader pattern.

“I’ve checked other channels and it seems to be the same across the board. Like it’s very few YouTube channels that are still actually pulling some good views.”

He emphasized that the squeeze is not isolated to his channel and that he has been making YouTube videos since 2017 across multiple cycles. None of his previous bear markets produced this kind of viewership collapse.

The View Collapse, in Numbers

In a separate appearance on the Matt Haycox Show podcast in late 2025, Runefelt put specific numbers to the decline. During the 2021 cycle peak, his videos routinely pulled 100,000 to 200,000 views each.

By early 2026, with Bitcoin trading near $76,500, that range had collapsed to roughly 15,000-20,000 views per upload.

For perspective, his views during the 2018 bear market low were more than twice what he records today, despite seven additional years of channel growth and subscriber accumulation. The trajectory is not typical for a bear market dip. It is a structural step down.

Carl’s Diversification

Faced with that landscape, Runefelt has been openly redirecting his attention. He told BeInCrypto he is now focusing significant energy on motorsport racing and music.

“I’m also focusing my energy on other things outside of crypto… motorsport racing nowadays. And I’m also focusing on my music because I love making music.”

The framing is not despair. It is adult triage.

“Life is too short to struggle bear markets, you know, 24/7. I’ve done a few of those already, and I want to also have fun before it gets too old.”

Runefelt is not leaving crypto. He still publishes regularly and continues to invest in startups through TheMoon Group, which has backed more than 350 projects. But after seven and a half years of channel growth that has now reversed, his decision to diversify his identity beyond crypto creator is the most honest data point in the entire interview.

Apathy as a Measurement

The view collapse is not just a vibes problem. It is now empirically measurable, and Benjamin Cowen, founder of Into The Cryptoverse, has been the loudest voice arguing the data.

Cowen’s Bitcoin Social Risk chart, published to his X account, color-codes Bitcoin price history by social engagement intensity.

In the 2017 and 2021 cycle tops, the chart prints in bright reds and oranges, signaling extreme retail engagement. The 2025 top, at much higher absolute Bitcoin prices, prints in cold blue, signaling low engagement.

As Cowen has framed it in his BeInCrypto coverage, this cycle topped on apathy rather than euphoria.

The implication for creators is direct. There was never an euphoric audience peak in this cycle, which means the views creators built their business plans around in 2021 may have been a historical anomaly, not a bear-market lull.

Google Trends data supports the same conclusion. Worldwide search interest in “Bitcoin” has trended near one-year lows for much of early 2026, despite spot prices well above $70,000.

The Industry-Wide Pain

Runefelt flagged a broader pattern in the interview that has since hardened into hard news.

“Even the exchanges, usually exchanges are the only ones making money, but I’ve seen even many exchanges are struggling, doing big layoffs and even a couple of them going bankrupt.”

The data quickly caught up to his observation.

In May 2026, Coinbase announced it would cut approximately 700 jobs, or 14% of its workforce, following a $667 million net loss in Q4 2025 and a 21.6% year-over-year revenue decline.

Crypto.com announced its own 12% workforce reduction in March 2026, eliminating roughly 180 positions. The smaller exchange, Bit.com, confirmed a phased shutdown from December 2025 to March 2026.

Beyond the trading platforms, the contraction has spread across the crypto labor market.

Crypto job postings have fallen approximately 80% year-over-year, with major announcements at Gemini, Algorand, Block, MARA Holdings, OKX, MANTRA, Polygon Labs, and Messari layered on top of the exchange cuts. The decline is structural, not seasonal.

David Wulschner’s Counter-View

David Wulschner, the host of the German-language Crypto Familie channel, sees the same conditions through a different lens. He launched his channel in mid-2022, near the bottom of the prior cycle.

“I just founded my channel mid of 2022, when we were really at the bottom of the cycle, and that was a lot of fun.”

The hardest challenge for newer creators in this bear market has not been view drops but community emotional pressure.

“What was really hard for me as a new content creator in that bear market was the emotions, the feedback, and that what you get thrown into your face by the community.”

Wulschner sees the bear market as the work phase, not the marketing phase.

“Profit is not done in the bull market. You set your goals, you set your foundation, you set your anchor positions in your portfolio in the bear market.”

That framing is not contradictory with Runefelt’s. The veteran and the newcomer have arrived at the same conclusion from opposite directions. Both treat the current environment as a reset rather than an ending.

The Shake-Out

In the interview, Runefelt did not present the crypto YouTube collapse as a tragedy. He framed it as a structural cleanse.

“That’s usually what we need to shake out all the bad stuff, all the scams, and all the people that are not here for the vision. They’re only here for the quick money. So getting rid of that before we go back up, it’s just part of the cycle.”

The creators who survive this cycle will likely be the ones who can adapt their business model below the 2018 baseline of views, broaden their content beyond price predictions and pump speculation, or, as Runefelt is doing, diversify their identity beyond the crypto-creator label.

Crypto YouTube is not dying. It is downsizing, and the shape that emerges on the other side will look very different from the cycle creators built businesses around four years ago.

Carl Moon, the man who turned a Stockholm supermarket job into one of the most-watched crypto channels in the world, will probably still be there. He will just be making music and racing cars on the side.

The post Crypto YouTube Crisis: “Even at the 2018 Bear Market, I Had Double the Views” appeared first on BeInCrypto.

SBI sheds over $11 billion in market value in 2 sessions on margin squeeze, disappointing earnings

Ronin Ethereum migration goes live on May 12

Kyle Cooke Claims West Had a ‘Full-Blown’ GF in Reunion Clip

Manchester United reach agreement with Casemiro over contract clause amid transfer speculation

US brings back mandatory military draft registration

Steven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Crypto World4 days ago

Crypto World4 days agoHarrisX Poll Found 52% of Registered Voters Support the CLARITY Act

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Marianne Dress

-

Crypto World5 days ago

Crypto World5 days agoUpbit adds B3 Korean won pair as Base token gains Korea access

-

NewsBeat5 days ago

NewsBeat5 days agoNCP car park operator enters administration putting 340 UK sites at risk of closure

-

Tech2 days ago

Tech2 days agoAuto Enthusiast Carves Functional Two-Stroke Engine from Solid Metal

-

Politics3 days ago

Politics3 days agoPolitics Home Article | Starmer Enters The Danger Zone

-

Business2 days ago

Business2 days agoIgnore market noise, India’s long-term story intact, say D-Street bulls Ramesh Damani and Sunil Singhania

-

Crypto World6 days ago

Crypto World6 days agoUAE Free Zone Deploys Blockchain IDs to Verify Registered Firms

-

Politics47 minutes ago

Politics47 minutes agoWhat to expect when you’re expecting a budget

-

Tech17 hours ago

Tech17 hours agoGM Agrees To Pay $12.75 Million To Settle California Lawsuit Over Misuse Of Customers’ Driving Data

-

Fashion6 hours ago

Fashion6 hours agoCoffee Break: Travel Steam Iron

-

Fashion21 hours ago

Fashion21 hours agoWhat to Know Before Buying a Curling Wand or Curling Iron

-

Crypto World5 days ago

Crypto World5 days agoBlackRock CEO Larry Fink Discusses a New Asset Class

-

Crypto World5 days ago

Crypto World5 days agoRobinhood says Wall Street is building onchain

-

Entertainment5 days ago

Entertainment5 days agoSarah Paulson Called Out For Met Gala ‘Hypocrisy’

-

Tech6 days ago

Tech6 days agoApple and Samsung are dominating smartphone sales so thoroughly that only one other company makes the top 10

-

Entertainment7 days ago

Serena Williams hits Met Gala in metallic dress after GLP-1 reveal

-

Tech6 days ago

Tech6 days agoI tested the Xiaomi 17 Ultra’s camera and I don’t think I’ll ever go back to an iPhone

-

Sports6 days ago

Sports6 days agoNBA playoff winners and losers: Austin Reaves is not loving Lakers vs. Thunder matchup, but Chet Holmgren is

-

Fashion5 days ago

Fashion5 days agoThe Best Work Pants for Women in 2026

You must be logged in to post a comment Login