Crypto World

Bank of Canada issues Canada’s first tokenized bond in a pilot

Canada has wrapped up a formal test of distributed ledger technology in its debt markets, marking a milestone with the issuance of the country’s first tokenized bond. The Bank of Canada announced on a recent Friday that Project Samara brought together the central bank, Export Development Canada, Royal Bank of Canada, and TD Bank Group to explore whether a blockchain-inspired infrastructure could streamline the lifecycle of bonds—from issuance to settlement. The pilot involved a CAD 100 million instrument maturing in under three months, issued to a closed group of investors, and settled using wholesale central bank deposits rather than traditional commercial bank money. The platform, built on Hyperledger Fabric, linked separate cash and bond ledgers to enable near-instant settlement and end-to-end lifecycle management, including issuance, bidding, coupon payments, redemption, and secondary trading.

Key takeaways

- The pilot issued a CAD 100 million tokenized bond with a maturity of less than three months to a select group of investors, representing a tangible step toward tokenized government-like debt in Canada.

- Settlement relied on wholesale central bank deposits rather than conventional bank money, underscoring a shift in how payment rails could interact with tokenized securities.

- Hyperledger Fabric served as the core platform, integrating separate ledgers for cash and bonds to support a full lifecycle from issuance to trading with near-instant settlement.

- Participants tested a comprehensive workflow—issuance, bidding, coupon payments, redemption, and secondary trading—highlighting both operational gains and governance or regulatory hurdles.

- Early results point to improved data integrity and operational efficiency, while signaling that broader uptake will hinge on governance, regulatory alignment, and integration with existing financial infrastructures.

Sentiment: Neutral

Market context: The Canadian pilot sits within a growing global wave of experiments where governments and financial institutions explore tokenized and blockchain-enabled bonds. Notable precedents include the World Bank’s Bond-i issuance in 2018, which is widely cited as the first bond whose lifecycle was managed on a blockchain, and Singapore’s 2022 introduction of Project Guardian to study digital-asset use in wholesale markets. Hong Kong’s tokenized green bond program launched in 2023, with subsequent expansions in 2024 and 2025, and the World Bank’s 2024 collaboration with Swiss National Bank and SIX Digital Exchange illustrate a broader push toward digital settlement rails for traditional assets.

Why it matters

The Canadian experiment adds momentum to the concept that distributed ledger technology can streamline bond issuance, trading, and settlement by harmonizing disparate ledgers and enabling faster, more transparent post-trade processing. In theory, tokenized bonds promise reduced counterparty risk and improved data integrity, because the lifecycle—issuance, auction, coupon payments, and redemption—can be captured on an auditable, shared ledger with restricted access controls. The use of wholesale central bank deposits for payments further signals a potential evolution of settlement rails that aligns with central bank objectives for digital currency and streamlined settlement finality.

Yet the pilot also exposes real-world frictions. Governance structures and regulatory regimes must adapt to tokenized asset workflows, encompassing disclosure, investor protection, and cross-ledger interoperability. The need to integrate a distributed system with established financial infrastructures—clearing, custodial practices, and risk management frameworks—presents a non-trivial hurdle for scale. In addition, the transition from pilot to live, broad-based issuance requires careful calibration of operational risk, access rights, and oversight to ensure that security, privacy, and settlement finality meet both market and regulatory expectations.

Beyond Canada, the trend toward tokenized debt is not simply a technology story; it reflects evolving market architecture preferences. The World Bank’s historic Bond-i project demonstrated the feasibility of recording bond lifecycles on a blockchain platform, while MAS’s Project Guardian has driven industry exploration into digital-asset tokenization in wholesale markets. The Hong Kong Monetary Authority’s tokenized-bond initiatives show strategic regulatory support for digitalized debt, and Switzerland’s engagement with SIX Digital Exchange to settle a Swiss-franc digital bond highlights a growing ecosystem of cross-border experimentation. Taken together, these efforts illustrate how tokenization and distributed ledgers could eventually broaden access to capital markets, reduce settlement risk, and enable more granular post-trade data analytics—though each jurisdiction faces its own governance and technical integration challenges.

In this context, Canada’s test represents a proof-of-concept that a traditional debt instrument can be issued, traded, and settled on a ledger that mirrors wholesale central-bank-ready infrastructures. It also demonstrates a collaborative model among a government authority, a crown corporation, and large domestic banks, which could serve as a blueprint for future pilots or potential live deployments in other markets. The emphasis on end-to-end lifecycle management—issuance through secondary trading—addresses a longstanding pain point in bond markets: friction and latency in post-trade processes. While the initiative does not imply immediate disruption to conventional bond markets, it signals a path toward more efficient settlement, tighter data governance, and potentially new forms of investor access, should scale and regulatory support align in the coming years.

For participants and observers, the key takeaway is not that a single tokenized bond will disrupt the market but that a working, production-grade, distributed-ledger environment validated by major financial institutions can execute a bond’s lifecycle with high degrees of automation and near-instant settlement. The learnings—benefits in operational clarity and data integrity, paired with governance and integration challenges—will inform both policy considerations and private-sector decisions about the role of blockchain-inspired architectures in the capital markets ecosystem. As central banks and regulators monitor live pilots, the Canadian example reinforces the proposition that tokenized assets can be more than a speculative concept; they can be engineered into functional components of a broader, digitized financial infrastructure.

The Bank of Canada’s announcement and accompanying materials provide a window into how pilots like Project Samara are shaping practical experimentation. The release notes that the bond issuance and settlement occurred on a distributed ledger platform, with payments routed through wholesale central bank deposits. For more granular details on the official pilot, see the Bank of Canada’s announcement here: Bank of Canada, Export Development Canada, RBC, TD successfully complete bond issuance experiment using distributed ledger technology.

As the data set from this pilot becomes more concrete, observers will be watching for how governance structures evolve, how regulators respond to cross-jurisdictional interoperability considerations, and whether subsequent pilots scale to larger debt issues or longer maturities. The path from a single trial to a broader adoption hinges not only on technical feasibility but on the alignment of risk controls, settlement finality guarantees, and fiscal-technical harmonization across institutions and regulatory bodies. In that sense, Project Samara is less about the immediate utility of the CAD 100 million note and more about demonstrating that a coordinated, ledger-based approach can support end-to-end bond management in a way that resonates with evolving central-bank digital currency and digital-asset policy discussions.

What to watch next

- whether Canada expands the pilot to include larger issues or longer tenors within the same framework

- regulatory guidance or updates that address governance and interoperability for tokenized fixed income in Canada

- additional participants from the private sector or other Canadian provinces contemplating similar experiments

- technical refinements to the ledger architecture that improve scalability and cross-ledger reconciliation

- potential live deployments or cross-border pilots tied to wholesale settlement rails

Sources & verification

- Bank of Canada, Export Development Canada, Royal Bank of Canada, and TD Bank announce successful bond-issuance experiment using distributed ledger technology (March 2026): https://www.bankofcanada.ca/2026/03/bank-canada-export-development-canada-rbc-td-successfully-complete-bond-issuance-experiment-distributed-ledger-technology/

- World Bank: Bond-i—the first global blockchain bond issuance (2018): https://www.worldbank.org/en/news/press-release/2018/08/23/world-bank-prices-first-global-blockchain-bond-raising-a110-million

- Monetary Authority of Singapore: Project Guardian and wholesale digital-asset initiatives (2022): https://www.mas.gov.sg/news/media-releases/2022/mas-partners-the-industry-to-pilot-use-cases-in-digital-assets

- Hong Kong Monetary Authority: tokenized green bond issuance and program updates (2023–2025): https://www.hkma.gov.hk/eng/news-and-media/press-releases/2023/02/20230216-3, https://www.hkma.gov.hk/eng/news-and-media/press-releases/2024/02/20240207-6

- World Bank: partnership with Swiss National Bank and SIX Digital Exchange to advance digitalization in capital markets (2024): https://www.worldbank.org/en/news/press-release/2024/05/15/world-bank-partners-with-swiss-national-bank-and-six-digital-exchange-to-advance-digitalization-in-capital-markets

Tokenized bonds in Canada: outcomes, mechanics, and implications

Canada’s tokenized-bond pilot under Project Samara represents a deliberate, methodical step toward reimagining debt markets through distributed ledger technology. The collaboration among the Bank of Canada, Export Development Canada, and two of the country’s largest banks demonstrates a practical, governance-conscious approach to testing a full lifecycle on a shared ledger. The CAD 100 million instrument with a sub-three-month maturity illustrates how tokenization can be deployed for relatively short-duration debt in a controlled setting, providing a limited but meaningful data point for how such assets might behave in real markets.

The mechanics of the Pilot Samara platform—built on Hyperledger Fabric and featuring integrated cash and bond ledgers—address a core challenge in traditional bond markets: the latency and risk associated with post-trade processing. By enabling issuance, bidding, coupon settlement, redemption, and secondary trading on a single ledger, and by processing payments through wholesale central bank deposits, the pilot pushes the envelope on settlement efficiency and inter-ledger coherence. The approach also offers a blueprint for potential future interoperability with central bank digital currencies and wholesale payment rails, a topic of growing interest among policymakers around the world.

However, the pilot also makes clear that technology alone is not a panacea. Governance structures, cross-border data agreements, and regulatory requirements remain critical to the viability of broader adoption. The institutions involved acknowledged that while operational improvements were evident, so too were governance and integration hurdles—issues that would need to be resolved before any large-scale rollout. As the market grows more comfortable with the idea of tokenized assets and as central banks continue to refine their digital-currency frameworks, pilots like Samara provide a concrete, observable test of how tokenized debt could function within a regulated, institutionally trusted ecosystem.

In the broader context, Canada’s experiment sits at the intersection of technological capability and policy design. It reflects a systematic, risk-conscious approach to exploring new settlement paradigms while preserving market integrity and investor protection. The results contribute to a landscape in which tokenized bonds are no longer a speculative curiosity but a potential instrument for more efficient settlement and improved data governance. Investors, financial institutions, and policymakers will be watching closely for how Canada translates pilot insights into scalable solutions that could reshape the structure and speed of debt markets in the years ahead.

The path from Stake.com to ZunaBet is becoming one of the most well-traveled routes in crypto gambling. It starts with a question that more players are asking in 2026 than at any point before: is there a better option? That question leads to a search. That search leads to comparisons. And those comparisons increasingly lead to the same destination. ZunaBet launched in 2026 and has quickly established itself as the platform that crypto gamblers discover when they decide to look beyond what they already know. Stake.com continues to operate at scale — its brand and traffic remain significant. But a growing number of its users are no longer content with what the platform provides, and ZunaBet has built exactly what those users are looking for. Here is why the path keeps leading to the same place.

Stake.com: The Platform That Opened the Door

Stake.com deserves its place in the history of crypto gambling. Launching in 2017 under a Curaçao license, it was among the first platforms to demonstrate that a full-scale gambling operation could function entirely on cryptocurrency. Bitcoin, Ethereum, Litecoin, Dogecoin, and other major coins were accepted from the beginning, which gave crypto holders something the rest of the gambling industry was not yet willing to offer — a native place to play.

Original games gave Stake a soul. Crash, Plinko, Mines, and Dice became iconic within the crypto gambling community, building a player base that was loyal not just to the platform but to the specific experience those games created. Provably fair mechanics and clean design made them endlessly replayable. Third-party content from providers including Pragmatic Play, Evolution, and Hacksaw Gaming eventually expanded the casino with slots and live dealer options.

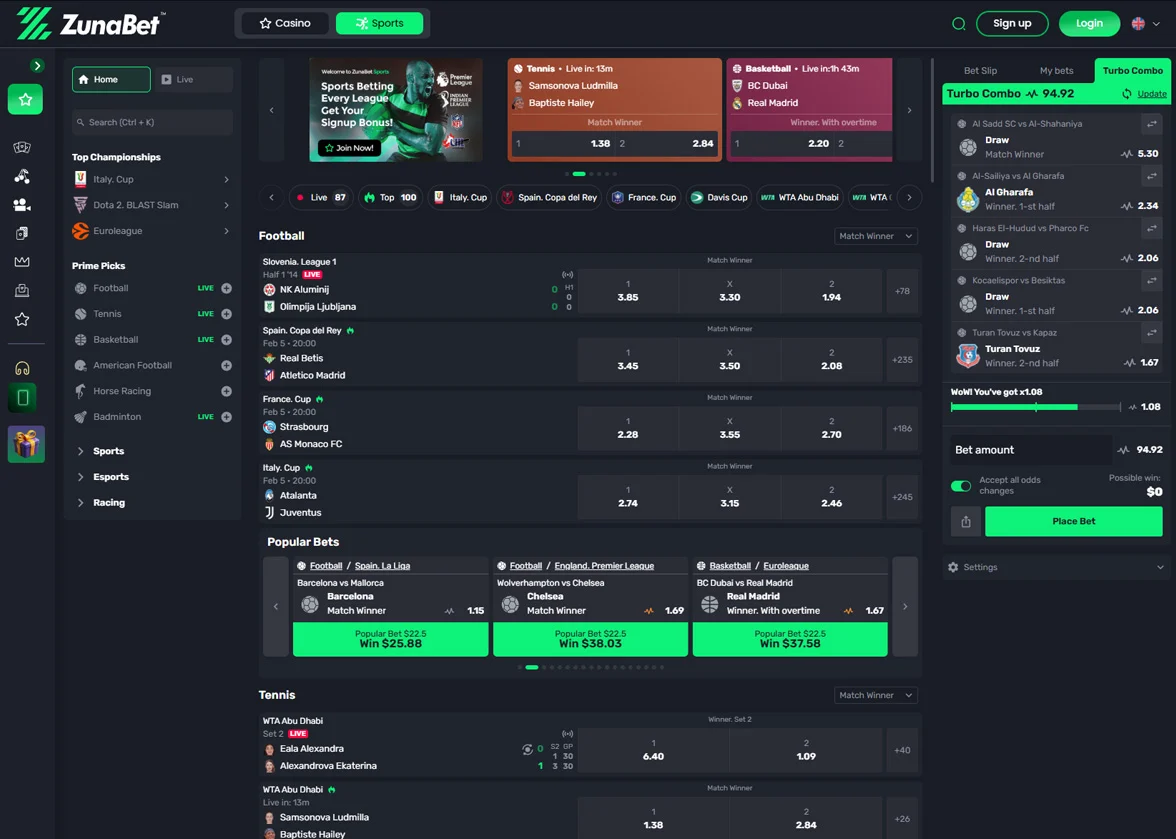

A sportsbook covering football, basketball, tennis, MMA, esports, and additional markets rounded out the product with competitive odds and an interface that kept things simple for experienced bettors.

Stake opened a door that the entire crypto gambling industry walked through. The complication is that some of the platforms that followed walked through it with better offerings.

What Sends Players Looking

The search for alternatives always starts with something specific. In Stake’s case, three recurring frustrations have created enough collective momentum to turn individual dissatisfaction into a visible market trend.

The absence of a welcome bonus is the trigger that initiates most searches. Stake has never offered deposit matching, free spins, or sign-up promotions of any kind. In the platform’s earlier years, this was a minor inconvenience because few crypto casinos were doing things differently. In 2026, with competitors extending welcome packages worth thousands of dollars, the inconvenience has matured into a genuine competitive weakness. Every player who learns about a multi-thousand dollar bonus on another platform while holding a bonusless Stake account faces a question that gets harder to ignore each time it comes up.

The concealed VIP program transforms mild frustration into active disengagement. Stake rewards its most valuable players through an invitation-only system that includes rakeback, recurring bonuses, and dedicated account management. For that small group, the program works well. For everyone else — which is the overwhelming majority — the program does not visibly exist. No tiers are published. No requirements are disclosed. No progress is shown. Playing regularly on Stake while receiving no structured recognition for that regularity creates a slow-building sense that the platform does not value your presence unless you are already in the top tier of spenders.

Game catalog size has become an increasingly common point of comparison. Platforms entering the market in 2025 and 2026 have arrived with game libraries that are dramatically larger than what Stake maintains. Players who enjoy exploring new games, testing different providers, and accessing a wide range of styles find themselves constrained on Stake in ways they no longer need to tolerate.

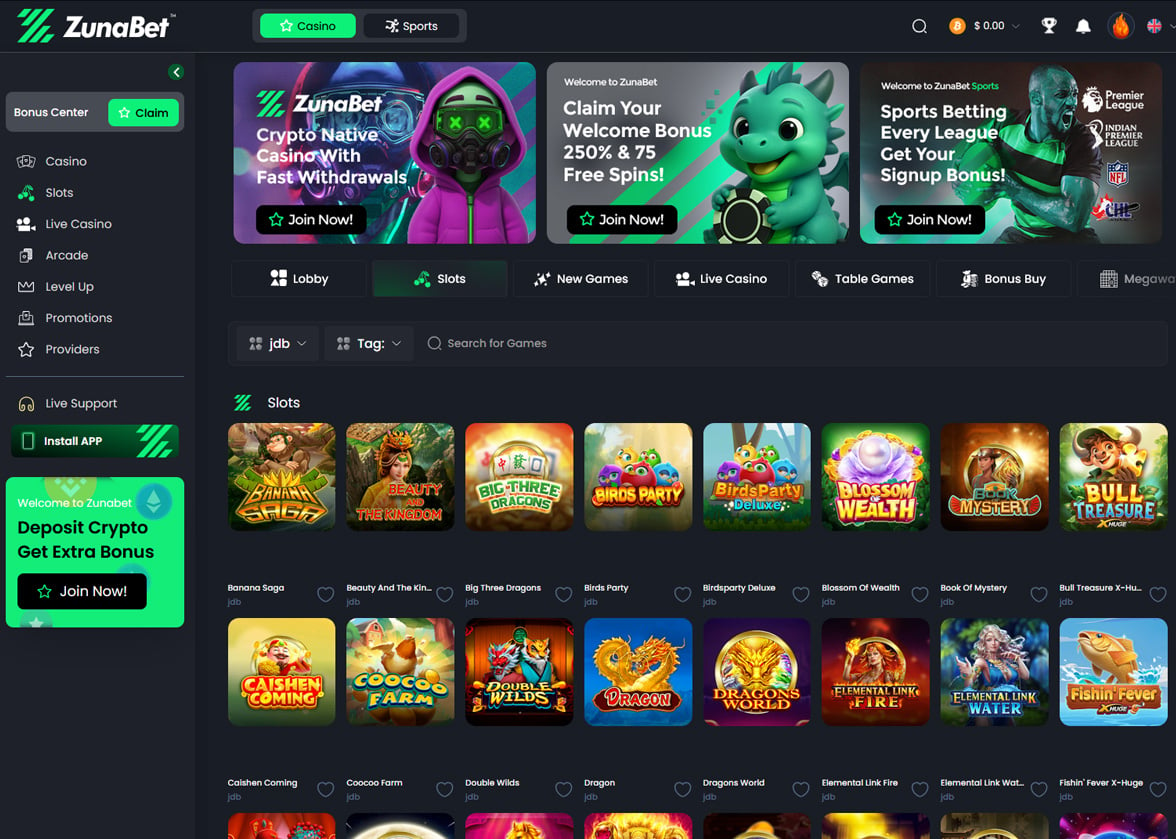

What Players Find When They Arrive at ZunaBet

ZunaBet went live in 2026 under Strathvale Group Ltd with an Anjouan gaming license. The founding team has more than 20 years of combined experience in online gambling. The platform was not bolted onto existing fiat infrastructure — it was designed natively around cryptocurrency, making digital assets the default for every function.

The game library hits first. Over 11,000 titles from 63 content providers fill the platform. Pragmatic Play, Hacksaw Gaming, Yggdrasil, BGaming, and Evolution sit among 60+ studios that contribute slots, RNG table games, and live dealer content. The catalog is not inflated with filler — the range of mechanics, visual styles, volatility profiles, and themes provides genuine variety that sustains interest over months of regular play.

Sports betting is a built-in feature rather than an add-on. The sportsbook handles football, basketball, tennis, NHL, combat sports, virtual sports, and esports markets covering CS2, Dota 2, League of Legends, and Valorant. A single account with a shared balance keeps everything connected, so moving between a slot session and a live match bet takes seconds.

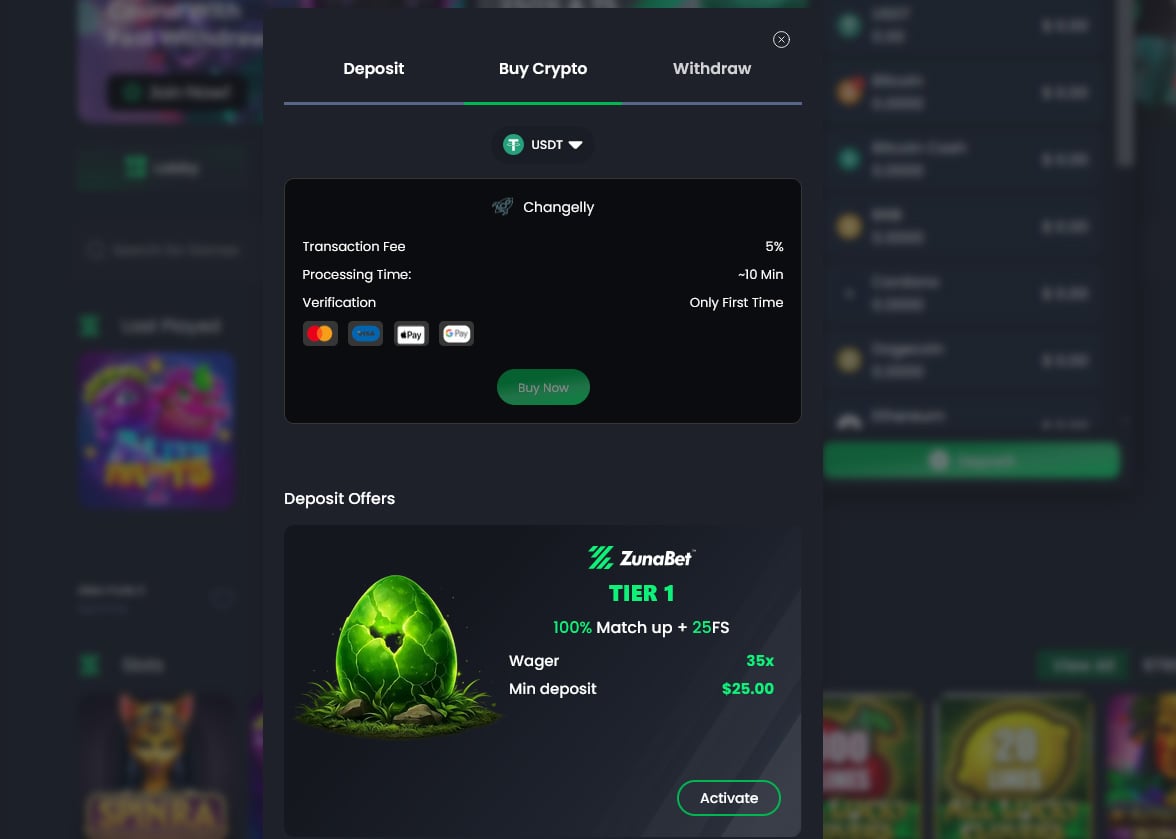

More than 20 cryptocurrencies are accepted: BTC, ETH, USDT on multiple blockchain networks, SOL, DOGE, ADA, XRP, and others. No processing fees are charged. Withdrawals are engineered to settle quickly. Native apps for iOS, Android, Windows, and MacOS provide consistent access, and live chat operates around the clock.

The First Thing That Changes Their Mind

The welcome bonus is typically the moment a browsing Stake player becomes a depositing ZunaBet player.

On Stake, there is no bonus. Your deposit equals your balance and nothing is added. Every session from your first bet onward is funded entirely by your own money.

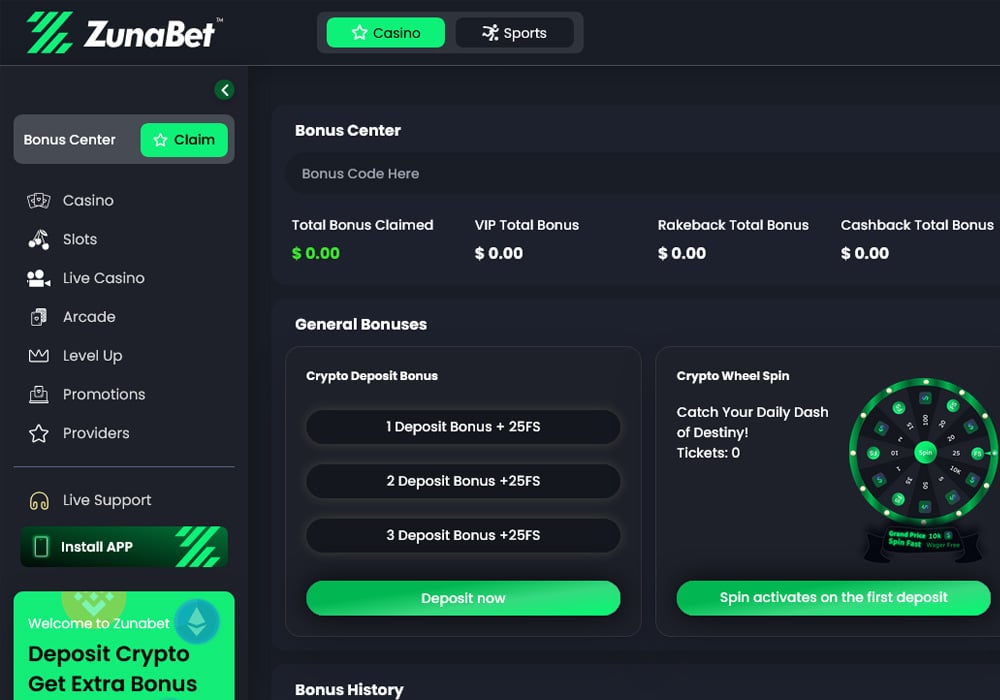

On ZunaBet, new players receive up to $5,000 in matched deposits plus 75 free spins across three transactions. First deposit: 100% match up to $2,000 with 25 free spins. Second: 50% match up to $1,500 with 25 spins. Third: 100% match up to $1,500 with 25 spins. The three-deposit format means the welcome period extends across multiple sessions, building engagement gradually rather than exhausting the bonus in one shot.

For someone who has never received a bonus on any platform, the impact goes beyond the financial. Seeing a deposit doubled communicates something about how the platform views the player relationship. It says your business is worth competing for. That message alone is enough to shift a player’s mindset from casually browsing to genuinely considering a permanent switch.

The Thing That Makes Them Stay

Welcome bonuses attract attention. Loyalty programs earn commitment. The gap between how Stake and ZunaBet handle ongoing rewards is what turns a ZunaBet trial into a ZunaBet home.

Stake keeps its loyalty system behind a barrier that most players will never cross. The VIP program is by invitation only, governed by criteria nobody can see. Those inside it benefit from rakeback, regular bonuses, and personal account management. Those outside it — the vast majority of the player base — receive nothing beyond the standard gambling experience. No tiers to track. No milestones to chase. No feedback that their play is generating any return beyond what the games themselves provide.

ZunaBet shows you everything before you place your first bet. The dragon evolution loyalty program has six tiers published in full: Squire at 1% rakeback, Warden at 2%, Champion at 4%, Divine at 5%, Knight at 10%, and Ultimate at 20%. Free spins increase with each tier up to 1,000. VIP club access and double wheel spins add additional layers. A dragon mascot called Zuno gives the progression personality and makes climbing tiers feel like part of the fun rather than background accounting.

Nothing is hidden. Nothing is invitation-only. Every player sees the complete structure from day one and can track exactly where they stand within it. At 20% rakeback, the Ultimate tier returns a substantial portion of the house edge on every wager, creating ongoing value that compounds across every session. For a player who spent their Stake tenure with zero structured loyalty recognition, discovering a system that rewards them openly and progressively is usually the deciding factor in making ZunaBet their permanent platform.

Where Both Platforms Sit in the Wider Market

Stake and ZunaBet occupy the crypto-native tier of online gambling, which separates them fundamentally from traditional operators like DraftKings, BetMGM, FanDuel, and Caesars. Fiat platforms carry the overhead of bank processing, card network fees, and withdrawal timelines that can stretch across multiple business days. For players who hold and transact in crypto, those platforms represent a step backward.

Within the crypto tier, ZunaBet extends further. Over 20 supported coins, including USDT across several blockchain networks, reflect how crypto users actually manage their holdings in 2026. Zero platform fees on every transaction and fast withdrawal processing keep the financial experience frictionless. Stake supports fewer coins and offers a narrower payment framework, which increasingly matters to players whose crypto activity spans multiple tokens and chains.

Why the Path Keeps Leading Here

The reason ZunaBet keeps appearing at the end of Stake alternative searches is straightforward — it was built to be found there. Every feature addresses a documented frustration. The $5,000 welcome bonus fills the void Stake leaves empty. The 11,000+ game library from 63 providers replaces a catalog players have outgrown. The transparent six-tier loyalty program with up to 20% rakeback replaces an invisible system that most players never benefit from. The 20+ supported cryptocurrencies with zero fees outpace Stake’s payment infrastructure.

Stake created the foundation for crypto gambling and earned every bit of its reputation. But foundations are meant to be built upon, and ZunaBet represents the next floor. More games, more value at sign-up, more transparency in rewards, and more flexibility in payments — delivered by a platform that treats earning player loyalty as an ongoing responsibility rather than a settled achievement.

The players finding ZunaBet through alternative searches are not leaving crypto gambling. They are upgrading it. And in 2026, ZunaBet is where that upgrade lives.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Web3 careers evolve as professionals adopt new framework to evaluate mature, capital-driven organizations.

Summary

- Web3 matures into regulated global finance, shifting careers from hype to fundamentals and structured growth

- In 2026, crypto firms favor diversified revenue models over token-driven growth and short-term momentum

- Security leads, with firms like WhiteBIT setting standards through audits and top-tier certification

By 2026, web3 will have become the backbone of global finance. The industry has matured into a regulated, capital-heavy, and globally competitive landscape. While many professionals still evaluate web3 employers based on 2020-style hype, this outdated logic no longer works.

To help professionals navigate their next career move, we have outlined the five pillars of a mature web3 organization.

1. Look beyond growth headlines, focus on business structure

Rapid expansion isn’t always a sign of strength. In 2026, a resilient company demonstrates diversified revenue foundations and scalability that withstands market cycles.

- Green Flag: The company has multiple revenue streams (B2B, B2C, RWA integrations).

- Red Flag: Growth depends solely on a single-token model or favorable market conditions.

Candidate Tip: It is worth asking, “How does the company generate value beyond its native token or core trading fees?”

2. Prioritize regulatory and security infrastructure

Compliance and cybersecurity are no longer “optional” — they are the company’s DNA. Today’s leaders operate under evolving frameworks and strict global security standards.

- The Industry Standard: Leading organizations do not just “claim” security; they prove it. WhiteBIT, for instance, was the first crypto exchange to achieve the highest level of CCSS (Cryptocurrency Security Standard) certification, reinforced by regular independent audits.

Interview Question: “What independent security certifications or regulatory licenses does the company currently hold in Tier-1 jurisdictions?”

3. Seek ecosystem thinking, not single-product focus

Standalone products are fragile. Mature companies build ecosystems — interconnected services that reinforce each other.

- Ecosystem Synergy: Evaluation should focus on the integration between a blockchain (e.g., Whitechain), crypto-acquiring (Whitepay), and the core exchange services.

- Global Reach: Serious players form strategic partnerships beyond crypto, proving global credibility and financial stability.

Interview Question: “How does this role interact with other products in the company’s ecosystem, and what are the strategic priorities for cross-product integration this year?”

4. Analyze governance and decision-making discipline

Speed without structure leads to volatility. In a mature web3 industry, disciplined decision-making isn’t bureaucracy; it’s performance-enhancing infrastructure.

The “red flag vs. green flag” checklist:

- Green Flag: Clear ownership, coordinated execution across distributed teams, and transparent leadership communication.

- Red Flag: Using the “move fast and break things” mantra as an excuse for lack of planning and constant team burnout.

Candidate Tip: A professional should ask, “How are strategic pivots communicated to the team, and how is accountability defined in cross-functional projects?”

5. Focus on talent investment, not just role scope

Web3 can offer broad responsibility, but that doesn’t always equal growth. The key in 2026 is whether the company treats talent as long-term capital.

- Development: Are there defined career pathways?

- The Maturity Indicator: Companies like WhiteBIT build internal pipelines and nurture future leaders who can navigate the intersection of finance, law, and AI.

Interview Question: “Can you provide an example of someone who has transitioned between different ecosystem products or moved into a leadership role internally? What did their development path look like?”

Final decision-making checklist

Before signing an offer, professionals should check these four boxes:

- Ecosystem: Is the product part of a larger, stable infrastructure?

- Security: Is there a CCSS Level 3 or equivalent independent validation?

- Sustainability: Does the revenue model work in a “bear” market?

- Growth: Does the company invest in cross-functional skills?

- Compliance: Does the company adhere to legal and regulatory requirements?

Closing perspective

The question in 2026 is no longer “Who is moving fastest?” but rather “Who is built for the long term?” Companies like WhiteBIT have spent years building a global presence focused on security, operational discipline, and ecosystem-driven growth. In a mature market, these factors are the only reliable indicators of a sustainable and rewarding career path.

Explore current career opportunities at WhiteBIT here.

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

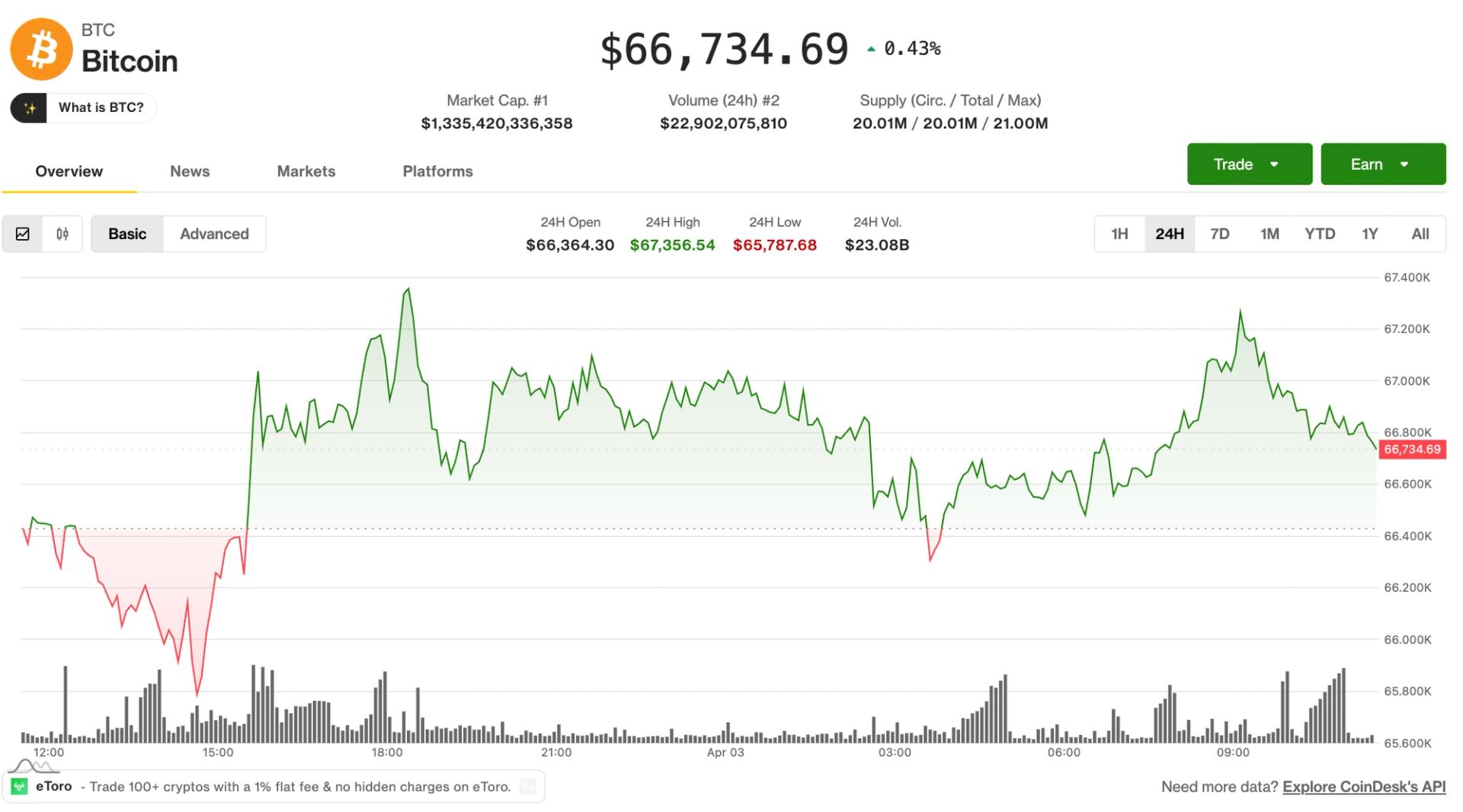

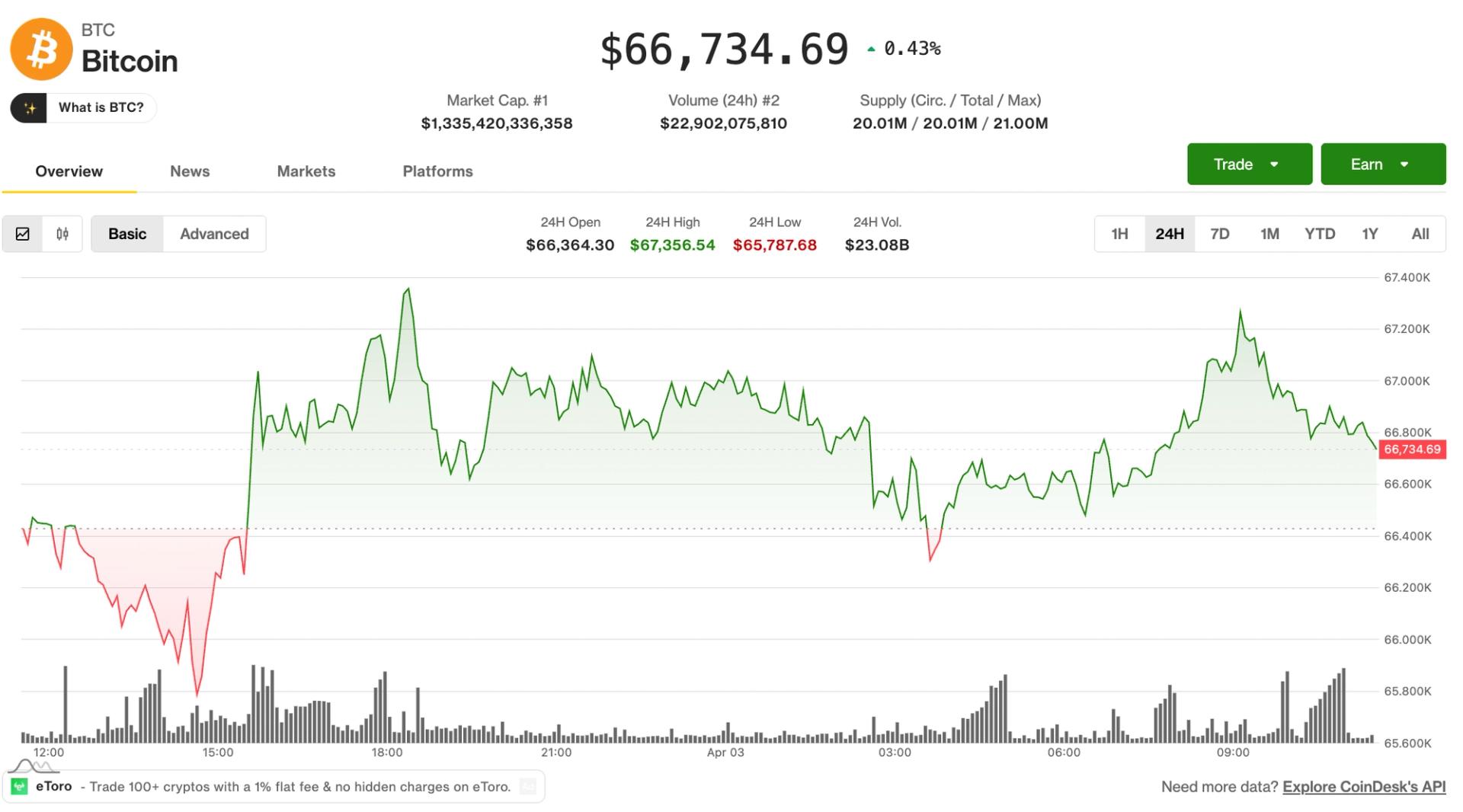

By Francisco Rodrigues (All times ET unless indicated otherwise)

Bitcoin is stuck in a tight range near $66,600 ahead of the Good Friday holiday, as geopolitical tensions and shifting macro expectations keep prices contained.

While the cryptocurrency saw a slight rise in the last 24 hour period it failed to break above $67,000. It’s struggling as U.S. President Donald Trump signaled a harsher stance on Iran, now threatening the country’s infrastructure.

Brent crude hit $120 per barrel on spot markets, levels not seen since 2008, over the ongoing crisis and its effects on the Strait of Hormuz, a key artery for global oil shipping that has effectively been shut down.

That surge in energy prices pushed up inflation expectations and undercut the case for rate cuts, a key support for bitcoin’s recent rally. Inflation in Europe has already risen to 2.5%, driven by energy costs.

The pressure has revealed a divide in market structure. Institutional inflows into bitcoin ETFs remain consistent, with $22 million in net inflows this week. But data from CryptoQuant show total apparent demand has flipped negative, with large holders distributing more than they accumulate.

Wallets holding 1,000 to 10,000 BTC have shed nearly 188,000 BTC since last year’s peak, the data shows. Nearly half of all bitcoin in circulation is, at current prices, trading at a loss.

Heading into the long weekend, liquidity is set to remain thin. That leaves bitcoin exposed to potentially higher volatility based on developments in the Middle East or macro-linked statements. Stay alert!

Read more: For analysis of today’s activity in altcoins and derivatives, see Crypto Markets Today

What to Watch

For a more comprehensive list of events this week, see CoinDesk’s “Crypto Week Ahead“.

- Crypto

- Macro

- April 3, 8:30 a.m.: U.S. Nonfarm Payrolls for March est. 48K (Prev. -92K)

- April 3, 8:30 a.m.: U.S. Unemployment Rate for March est. 4.5% (Prev. 4.4%)

- April 3, 10:00 a.m.: U.S. ISM Services PMI for March (Prev. 56.1)

- Earnings (Estimates based on FactSet data)

Token Events

For a more comprehensive list of events this week, see CoinDesk’s “Crypto Week Ahead“.

- Governance votes & calls

- SSV Network DAO is voting across two proposals to integrate ENS names for core protocol contracts to enhance security against phishing, and to establish a soft fee floor for public operators to ensure economic sustainability. Voting ends April 3.

- Unlocks

- Token Launches

Conferences

For a more comprehensive list of events this week, see CoinDesk’s “Crypto Week Ahead“.

Market Movements

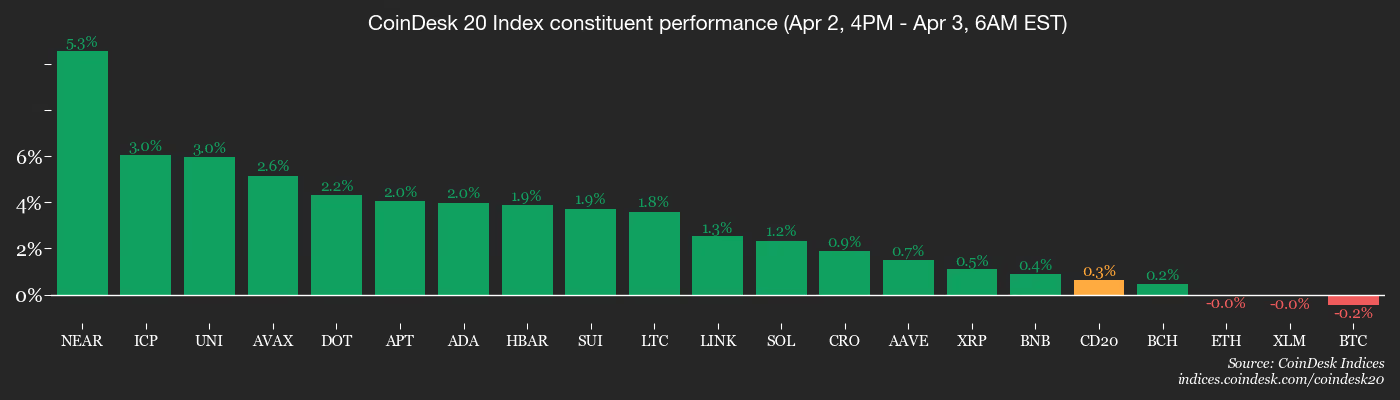

- BTC is down 0.35% from 4 p.m. ET Thursday at $66,785.73 (24hrs: +0.65%)

- ETH is unchanged at $2,058.20 (24hrs: +0.94%)

- CoinDesk 20 is up 0.26% at 1,902.32 (24hrs: +0.80%)

- Ether CESR Composite Staking Rate is up 1 bps at 2.77%

- BTC funding rate is at -0.0007% (-0.7731% annualized) on Binance

- DXY is unchanged at 99.99

- Gold futures are up 1.07% at $4,701.30

- Silver futures are up 0.60% at $73.17

- Nikkei 225 closed up 1.26% at 53,123.49

- Hang Seng closed down 0.70% at 25,116.53

- FTSE 100 is unchanged at 10,436.29

- Euro Stoxx 50 is down 0.26% at 5,678.00

- DJIA closed on Thursday down 0.13% at 46,504.67

- S&P 500 closed up 0.11% at 6,582.69

- Nasdaq Composite closed up 0.18% at 21,879.18

- S&P/TSX Composite closed up 0.46% at 33,108.20

- U.S. 10-Year Treasury rate is down 1 bps at 4.31%

- E-mini S&P 500 futures are up 0.12% at 6,613.00

- E-mini Nasdaq-100 futures are up 0.10% at 24,167.25

- E-mini Dow Jones Industrial Average futures are up 0.10% at 46,678.00

Bitcoin Stats

- BTC Dominance: 58.54% (-0.24%)

- Ether to bitcoin ratio: 0.030821 (0.23%)

- Hashrate (seven-day moving average): 997 EH/s

- Hashprice (spot): $30.68

- Total Fees: 2.54 BTC / $170,134

- CME Futures Open Interest: 106,230 BTC

- BTC priced in gold: 15.9 oz

- BTC vs gold market cap: 4.46%

Technical Analysis

- The chart shows daily swings in tether’s dominance rate in candlestick format. The dominance rate represents the share of stablecoin tether in the total crypto market.

- The dominance rate is rising again after a temporary pullback, or counter-trend correction. This breakout suggests that the broader uptrend in dominance has likely resumed.

- This has bearish implications for the broader market, as dollar-pegged assets like Tether typically gain dominance during market-wide sell-offs.

Crypto Equities

- Coinbase Global (COIN): closed on Thursday at $171.46 (–0.88%), unchanged in after-hours

- Galaxy Digital (GLXY): closed at $17.64 (+1.55%), +0.28% at $17.69

- MARA Holdings (MARA): closed at $8.71 (+8.33%), –1.03% at $8.62

- Riot Platforms (RIOT): closed at $12.86 (+2.47%), unchanged at $12.86

- Core Scientific (CORZ): closed at $16.23 (+6.08%), –0.62% at $16.13

- CleanSpark (CLSK): closed at $8.79 (+1.97%), unchanged at $8.80

- Exodus Movement (EXOD): closed at $6.10 (–8.68%), –0.80% at $6.05

- CoinShares Bitcoin Miners ETF (WGMI): closed at $35.76 (+2.58%), –0.17% at $35.70

- Circle Internet Group (CRCL): closed at $90.26 (–0.53%), +0.60% at $90.80

- Bullish (BLSH): closed at $36.37 (+3.71%), –0.19% at $36.30

Crypto Treasury Companies

- Strategy (MSTR): closed at $119.83 (–2.40%), +0.34% at $120.24

- Strive Asset Management (ASST): closed at $9.75 (–4.04%), +0.10% at $9.76

- SharpLink Gaming (SBET): closed at $6.19 (–4.18%), +0.32% at $6.21

- Upexi (UPXI): closed at $0.98 (–1.32%), –2.12% at $0.95

- Lite Strategy (LITS): closed at $1.12 (–0.88%), unchanged at $1.12

ETF Flows

Spot BTC ETFs

- Daily net flow: $9 million

- Cumulative net flows: $55.93 billion

- Total BTC holdings ~ 1.28 million

Spot ETH ETFs

- Daily net flow: -$71.2 million

- Cumulative net flows: $11.51 billion

- Total ETH holdings ~ 5.69 million

Source: Farside Investors

While You Were Sleeping

French ship crosses Strait of Hormuz in first Western European transit during Iran war (euronews): The news could encourage other carriers to resume operations if the corridor proves reliable in the coming days and it follows Iran’s deputy foreign minister Kazem Gharibabadi announcement of a deal with Oman to secure traffic through the Strait of Hormuz.

U.S. repatriates Chinese drug fugitive in a sign of stabilizing ties (The Wall Street Journal): This is the first case of its kind in recent years and is described as a rare move that points to cooperation ahead of the planned Trump-Xi summit next month.

Iran strikes Gulf energy sites as Trump warns of further attacks (Bloomberg): Iran targeted more sites in Arab Gulf states, including in Kuwait Friday morning, hours after Trump issued fresh threats against Iranian infrastructure to pressure Tehran to start peace negotiations.

Japan turns up FX heat as volatility rises, signals readiness to act (Reuters): The yen, trading near the psychologically key 160-per-dollar mark, lingered at levels that stoke concerns of market intervention, highlighting growing unease over the speed and scale of its decline.

Key Highlights

- Google unveiled two additional Gemini API service tiers: Flex and Priority

- Flex provides 50% cost reduction for non-urgent, background processing tasks

- Priority commands 75–100% premium pricing for mission-critical, real-time operations

- Batch API maintains 50% discount with latency extending to 24 hours

- Caching tier uses token volume and retention time for pricing calculations

On April 2, Google rolled out a comprehensive pricing update for its Gemini API, introducing five separate service tiers: Standard, Flex, Priority, Batch, and Caching. This expansion provides developers with greater flexibility to optimize their applications based on cost efficiency, response time, and performance reliability.

The newly introduced Flex tier targets non-time-sensitive background operations that can tolerate delayed responses. By leveraging underutilized computing resources during off-peak periods, it delivers a 50% price reduction compared to standard rates. Response latency varies between 1 and 15 minutes without guaranteed delivery times. Ideal applications include CRM data synchronization, computational research models, and automated agent workflows.

What distinguishes Flex from the pre-existing Batch API is its synchronous endpoint architecture. Developers avoid the complexity of managing file-based inputs/outputs or monitoring job completion status. This streamlined approach maintains identical cost benefits while simplifying implementation.

Conversely, the Priority tier addresses high-stakes, time-critical applications. With pricing 75% to 100% above standard rates, it guarantees rapid response times measured in milliseconds to seconds.

Google positions Priority for use cases like live customer service chatbots, real-time fraud prevention systems, and automated content filtering. When Priority tier usage exceeds allocated quotas, surplus requests gracefully shift to Standard tier processing instead of generating errors.

Complete Tier Structure

The original Batch API continues operating with 50% cost savings and accepts latency windows extending to 24 hours. This option suits intensive offline computations where immediate results aren’t necessary.

The Caching tier employs pricing models based on token quantities and content storage duration. Google recommends this tier for conversational AI with extensive system prompts, recurring analysis of large video datasets, or searches across substantial document collections.

Both Flex and Priority tiers utilize identical service_tier parameters within API calls. Developers can switch between tiers through simple configuration adjustments, with API responses confirming the tier that processed each request.

Flex accessibility extends to all paid tier subscribers using GenerateContent and Interactions API endpoints. Priority remains restricted to Tier 2 and Tier 3 paid accounts accessing identical endpoints.

Developer Benefits

The standardized interface represents the most significant advancement. Previously, managing both background operations and interactive workloads necessitated separate architectural frameworks for synchronous and asynchronous processing. The current update consolidates both through unified synchronous endpoints.

Google positioned this enhancement as integral to supporting AI agent development, which frequently requires simultaneous handling of low-priority background tasks and time-sensitive interactive functions.

Gemini API product manager Lucia Loher and engineering lead Hussein Hassan Harrirou announced the update on April 2, 2026.

Crypto World

Google unveils Gemma 4 as its most advanced open AI model for reasoning and agentic tasks

Google has introduced Gemma 4, its latest open artificial intelligence model family focused on advanced reasoning and agent-style workflows.

Summary

- Google launches Gemma 4, its latest open AI model family focused on advanced reasoning and agent-style workflows.

- The model is available in four sizes, ranging from edge-device variants to high-performance systems, and supports over 140 languages.

- Gemma 4 introduces features such as multi-step reasoning, agent tools, and offline code generation, with models accessible via AI Studio and Edge Gallery.

In an April 2 post on X, Demis Hassabis, chief executive of Google DeepMind, announced the launch of Gemma 4, its latest open artificial intelligence model family focused on advanced reasoning and agentic workflows.

Open models are designed to be modified and adapted by developers, allowing them to tailor systems for specific use cases.

The release comes amid strong uptake of the Gemma ecosystem. Since the first version launched, developers have recorded over 400 million downloads and created more than 100,000 variants, according to Google.

Hassabis said Gemma 4 is available in four sizes, each suited to different workloads and hardware setups, and can be fine-tuned for specialised tasks.

The largest version, 31B, is a dense model built for “great raw performance,” prioritising accuracy and depth of output, though it requires high-end computing resources.

Alongside it is the 26B Mixture of Experts (MoE) model, which is designed for lower latency. It activates fewer parameters during inference, allowing faster responses and improved efficiency, albeit with some trade-offs in output quality.

For lighter use cases, Google has introduced the 2B and 4B models. These are optimised for edge devices such as smartphones and compact systems, enabling on-device execution with lower computational demands.

What can you do with Google Gemma 4?

Gemma 4 introduces improved reasoning capabilities, allowing it to handle tasks that require multi-step logic and structured problem-solving. It has also shown stronger performance in benchmarks tied to mathematics and instruction-following.

The models support agent-style workflows through native function calling, structured JSON outputs, and system-level instructions. These features allow developers to build autonomous systems that can interact with APIs, tools, and external services. Gemma 4 also enables high-quality offline code generation, turning local machines into AI coding assistants.

Another key feature is its expanded context window. The edge models support up to 128K tokens, while the larger variants extend this to 256K tokens, allowing the processing of long documents or codebases in a single prompt. The models are trained across more than 140 languages, which allows for global deployment.

Sundar Pichai reposted the announcement, saying Gemma 4 is “packing an incredible amount of intelligence per parameter.”

The models are built to run across a vast range of hardware, from smartphones and laptops to GPUs and developer workstations, with smaller variants capable of running locally without constant internet access.

Developers can start testing Gemma 4 across multiple platforms, with the 31B and 26B MoE models available on Google AI Studio for higher-performance use cases, while the smaller E2B and E4B variants are accessible through Google AI Edge Gallery for on-device and lightweight applications.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

TLDR

-

Google debuts Gemma 4 featuring enhanced reasoning capabilities and autonomous agent frameworks

-

Four distinct model configurations serve mobile devices, edge computing, and enterprise infrastructure

-

Gemma 4 delivers powerful AI performance with reduced computational overhead

-

Supports extended context processing, programming tasks, and multilingual applications

-

Apache 2.0 open licensing encourages widespread developer integration and customization

Google has officially released Gemma 4, advancing its portfolio of open-source AI models with enhanced reasoning abilities and autonomous agent functionality. This latest generation delivers scalable architectures supporting sophisticated workflows and versatile hardware deployment. Gemma 4 emerges as an adaptable platform for developers pursuing robust performance while minimizing computational demands.

Gemma 4 Advances Open-Source AI Innovation

Gemma 4 represents the evolution of Google’s previous open model initiatives, responding to increasing market demand for adaptable AI frameworks. This launch arrives following substantial adoption momentum, with download counts exceeding 400 million worldwide. The developer community has produced over 100,000 customized implementations across the expanding platform.

This model generation comprises four distinct configurations tailored for diverse operational requirements and infrastructure platforms. Options span from compact edge-optimized versions to robust high-capacity architectures for intensive computational workloads. Consequently, Gemma 4 accommodates smartphone implementations alongside large-scale enterprise operations.

Demis Hassabis validated this release as a component of Google’s comprehensive initiative toward democratized AI advancement. The company pursues equilibrium between computational power and operational efficiency across heterogeneous hardware configurations. Gemma 4 reinforces Google’s commitment to transparent AI ecosystem development.

Gemma 4 introduces refined reasoning mechanisms and systematic problem-resolution across numerous evaluation metrics. The system processes sequential analytical tasks with heightened precision and dependable results. These models execute instruction-based operations with superior consistency.

The architecture incorporates autonomous agent frameworks via built-in function invocation and formatted response generation. These capabilities facilitate automated engagement with application programming interfaces and third-party utilities. Developers construct self-directed systems exhibiting more reliable operational patterns.

Gemma 4 additionally enhances programming generation features for disconnected operating environments. This enables standalone computing systems to function as self-contained AI assistants. Developers maintain comprehensive deployment authority independent of cloud-based resources.

Tiered Architecture Addresses Varied Infrastructure Requirements

Gemma 4 features a 31B dense architecture optimized for premium output quality and comprehensive analytical operations. This configuration demands substantial computing infrastructure but produces exceptional results. The version targets research initiatives and corporate-level implementations.

The 26B Mixture of Experts variant emphasizes processing velocity and resource optimization. It engages selective parameter sets during operational cycles to minimize response delays. Consequently, developers obtain accelerated results with streamlined resource allocation.

Gemma 4 additionally delivers compact 2B and 4B configurations designed for edge computing devices. These editions execute effectively on mobile hardware and condensed systems. Users implement AI functionality locally without persistent network connectivity.

The architectures accommodate expanded context processing capabilities for analyzing extensive documentation and software repositories. Compact configurations manage contexts reaching 128K tokens, whereas larger variants process up to 256K tokens. Gemma 4 facilitates comprehensive application scenarios across multiple sectors.

Gemma 4 provides compatibility with more than 140 languages, enabling worldwide implementation across varied geographical markets. This multilingual functionality improves accessibility and practical utility. Developers construct applications serving international user populations.

The models function across platforms encompassing mobile devices, graphics processing units, and development workstations. Google additionally facilitates integration with prominent AI engineering frameworks. Consequently, Gemma 4 delivers versatility for both experimental prototyping and operational deployment.

Open Licensing Framework Accelerates Platform Adoption

Gemma 4 operates under Apache 2.0 licensing, permitting commercial application and research utilization without significant limitations. This framework encourages collaborative advancement and transparent development practices. Developers obtain complete authority over modification and implementation strategies.

The launch corresponds with Google’s strategic vision to broaden its AI ecosystem alongside proprietary platform offerings. It supplements existing infrastructure while enabling local and offline operational modes. Gemma 4 connects open-source and proprietary AI architectures.

Developers acquire access to Gemma 4 through diverse platforms including cloud infrastructure and local computing environments. The models accommodate specialized training for particular applications and industry verticals. Organizations therefore customize AI implementations to precise operational specifications.

Google persistently establishes Gemma 4 as a pragmatic and expandable AI platform. Strategic emphasis centers on efficiency, analytical capabilities, and practical implementation. Gemma 4 elevates the significance of open-source models throughout contemporary AI advancement.

Crypto World

Post-Quantum Cryptography Threat Divides Blockchain Networks as Google Paper Reshapes Timeline

TLDR:

- Google’s latest paper slashes the qubit threshold to break elliptic curve cryptography below 500,000.

- Ethereum targets full post-quantum deployment by 2029 with live testnets and ten active client teams.

- Bitcoin holds an estimated 5–15% quantum-vulnerable supply, including roughly one million Satoshi-era coins.

- Jefferies removed Bitcoin from model portfolios, flagging quantum vulnerability as a material investor risk.

Post-quantum cryptography has become a pressing concern for major blockchain networks worldwide. On March 30, Google Quantum AI published research showing that quantum computers could break Bitcoin and Ethereum’s cryptographic protections with far fewer resources than previously estimated.

A companion paper by Oratomic, a Caltech and Harvard startup, suggested neutral-atom quantum computers could achieve this with just 10,000 qubits. Earlier estimates had placed that threshold at one million qubits or more.

Ethereum Builds the Most Advanced Post-Quantum Cryptography Roadmap Among Major Blockchains

All major blockchains currently rely on elliptic curve cryptography to secure transactions. Shor’s algorithm allows quantum computers to reverse this process and expose private keys quickly. The qubit threshold to break elliptic curve cryptography dropped from 9 million in 2023 to under 500,000 today.

Ethereum Foundation researcher Justin Drake co-authored the Google paper and leads post-quantum research efforts. He estimates at least a 10% chance of a cryptographically relevant quantum computer emerging by 2032.

Google, meanwhile, has set a 2029 internal deadline to migrate its own infrastructure to post-quantum cryptography.

Ethereum’s post-quantum effort stands as the most advanced among major blockchains today. The Foundation began funding hash-based cryptography research in 2018 with a $5 million grant.

The network now has a public roadmap targeting full deployment by 2029, live test networks with around ten client teams, and a $1 million cryptographic bounty program.

Drake described the 2029 target as “realistic/conservative” and pointed to the 2022 Merge as evidence of execution capacity.

That upgrade transitioned Ethereum from proof-of-work to proof-of-stake on a live multi-hundred-billion-dollar network without disruption.

Signature aggregation technology will compress post-quantum signatures into compact proofs, avoiding a throughput penalty.

Ethereum’s quantum-vulnerable supply sits at roughly 2%, compared to Bitcoin’s estimated 5–15%. The network is younger, and better key management practices from launch kept this number lower.

Drake recently remarked: “I’ve stopped thinking about post-quantum as a hurdle that we have to overcome, and I think of it more as an opportunity.”

Bitcoin and High-Throughput Chains Face Greater Post-Quantum Migration Challenges

Bitcoin carries the same elliptic curve vulnerability but operates within a more complex governance environment. BIP-360, a post-quantum migration proposal, has received broad community engagement so far. Even so, over $1.5 trillion in value at stake has not generated the same urgency visible at Ethereum.

Nic Carter, founding partner at Castle Island Ventures, offered a candid comparison between the two networks. He described Ethereum’s approach as “best in class” and Bitcoin’s current posture as “worst in class.” He added: “Elliptic curve cryptography is on the brink of obsolescence. Whether it’s 3 or 10 years; it’s over and we need to accept that.”

Bitcoin’s development culture treats the protocol more as a finished product than an evolving system. That stance benefits monetary credibility but creates friction when cryptographic upgrades are urgently needed. The debate over roughly 1 million BTC in Satoshi-era addresses will also take considerable time to resolve.

Solana and other high-throughput chains face a separate but equally serious challenge. Hash-based signatures are far larger than classical ones, and Solana exposes all public keys by default.

A full migration would narrow the throughput advantage that has served as Solana’s primary competitive differentiator.

Jefferies has already removed Bitcoin from model portfolios, citing quantum vulnerability as a material risk. Carter warned: “ETH people have already figured this out. Unless something changes quickly, ETHBTC will start to reflect the divergence in prioritization.”

Tokenization platforms managing assets with 10- to 30-year durations will increasingly treat post-quantum migration capability as a baseline requirement for institutional deployment.

Key takeaways

- ETH is up by less than 1% and now trades above $2,050.

- The bulls defended the $2,000 support level, with further upward movement on the card.

Ethereum is up by less than 1% at the time of writing on Friday, halting the bearish performance that gripped the market on Thursday. The coin could rally higher in the near term as buyers have stepped in over the past few hours.

Onchain data paints a mixed picture for Ether

ETH is trading above $2,050 at press time, but onchain data paint a mixed picture for the top altcoin. Over the past week, investors across different cohorts have cracked under pressure.

According to the onchain data, wallets with a balance of 10K-100K, which have been major buyers throughout the recent downtrend, offloaded 340K ETH between March 24-30.

However, the wallets flipped back to buying on Tuesday, scooping 270K ETH across the past two days.

On the other hand, wallets with 100-1K and 1K-10K ETH continued distribution, scaling down their holdings by roughly 200K ETH over the past week.

In addition to that, US spot ETH exchange-traded funds (ETFs) have also posted a similar trend. The ETFs have recorded only two days of inflows over the past two weeks of trading, indicating a bearish bias.

Ethereum Price Forecast: Bulls defend the $2k psychological level

The ETH/USD 4-hour chart is bullish and efficient as Ether recorded its first monthly gain in six months.

At press time, ETH is trading at $2,062. Its near-term bias remains mildly bullish as ETH is trading below the 20- and 50-day Exponential Moving Averages (EMAs), which cap advances at around $2,080 and $2,160.

The Relative Strength Index (RSI) reads 53, slightly above the neutral level, while the MACD has stabilized around the midline, both indicating a growing bullish momentum.

If the recovery persists, the bulls would face immediate resistance at $2,108, followed by $2,389 and then $2,746. A daily close above $2,108 would be the first step to ease pressure and expose the higher resistance band toward the 100-day EMA and $2,389.

However, if the sellers regain control, ETH would test the initial support at $1,911, followed by $1,741 and $1,524.

If ETH continues to trade below $2,108, it risks drifting back toward the $1,700 area in the near term.

Crypto World

Bitcoin rangebound as altcoins rally while derivatives signal downside risk: Crypto Markets Today

The crypto market continued to exhibit signs of choppiness on Friday, with bitcoin trading at $67,000 in the middle of a trading range that spans back to early February.

A selection of altcoins picked up during the lower liquidity Asia hours, prompting the likes of ALGO and RENDER to post double-digit gains over the past 24 hours.

But the wider picture remains the same; the crypto market is trading in a macro downtrend dating back to October, characterized by a series of lower highs nad lower lows.

U.S. equities trade flat on Friday as volatility continues to cool since Donald Trump’s comments about a potential end to the war in Iran on Monday.

Brent crude oil is trading at $109 a barrel, indicating that an end to the war is perhaps not as close as some analysts are predicting.

Derivatives Positioning

- Futures markets for Bitcoin and Ethereum remained subdued, with the extended holiday weekend keeping trading volumes thin. Open interest in both assets was largely unchanged over the past 24 hours.

- Open interest in Solana futures has climbed to over 65 million SOL, its highest level since Feb. 7. The increase, combined with negative funding rates and an OI-adjusted cumulative volume delta, suggests traders are increasingly positioning for downside, with short sellers showing greater conviction.

- Similar bearish market dynamics are present TRX and BCH.

- OI in Privacy-focused Zcash (ZEC) futures have steadied near 1.70 million ZEC for the third straight day. ZEC’s CVD is also the highest among majors. This combination suggests sustained positioning with strong directional conviction, likely driven by aggressive buying pressure.

- Bitcoin’s 30-day implied volatility index has declined to 51.28%, the lowest since Feb. The market shows no signs of panic whatsoever despite geopolitical concerns and energy market volatility.

- Ether’s volatility index has slipped to 72.55%, the lowest since Feb. 26.

- On Deribit, bitcoin and ether puts continue to trade pricier than calls, indicating a bias for downside protection.

- Glassnode said that the dealer gamma exposure below $68,000, all the way down to $50,000 is negative. This means that dealers could sell in a falling market to hedge their exposure, adding to downside volatility.

Token talk

- The altcoin market has been relatively resilient to crypto’s choppy behavior this week, certain portions of the market have outperformed bitcoin and crypto majors, particularly DeFi and AI tokens.

- The DeFi Select Index (DFX) is up by 1.3% since midnight UTC, while the CoinDesk Computing Select Index (CPUS) rose by 1.5%, beating the bitcoin-heavy benchmarks likes the CoinDesk 20 (CD20), which is up by just 0.16% on Friday.

- The outperformance of certain altcoins is symptomatic of a consolidating market. When bitcoin and the majors trade flat, traders often speculate on lower liquidity altcoins. That speculation typically grinds to a halt when bitcoin is back deciding the next major market move.

Key takeaways

- PYTH is up 9% in the last 24 hours, outperforming other major cryptocurrencies.

- The rally comes following Pyth Network’s integration with Polymarket.

PYTH, the native coin of the Pyth Network, is one of the best performers in the crypto market over the past 24 hours. It could rally higher in the near term as the broader market recovers from Thursday’s slump.

PYTH rallies on Polymarket integration

On Thursday, Pyth Network revealed in a blog post that Polymarket, the world’s largest prediction market platform, has integrated Pyth Pro as its data source for a new suite of traditional asset contracts.

The initial offerings include gold, silver, and major equity index ETFs. Polymarket now relies on Pyth Pro’s data to power its daily up/down and daily close markets, with live price charts updated every second to ensure full transparency.

The integration has seen PYTH rally by 9% in the last 24 hours and now trades at $0.0420 per coin.

Pyth Pro provides real-time price data through WebSocket, which Polymarket samples every second to display as a live “price to beat” chart. This allows traders to monitor the market’s status relative to their position in real-time.

The selected assets span a wide range of traditional finance, including major equity indices, commodities like gold, silver, WTI crude, and natural gas, along with over a dozen high-profile U.S. equities such as TSLA, COIN, and PLTR.

Polymarket has integrated this real-time data as a key component of its perpetual futures trading platform. Pyth Pro delivers institutional-grade market data directly from top firms, ensuring it is accurate, transparent, and affordable across all asset classes and regions.

To enhance this, Pyth has partnered with industry leaders and government agencies like Cboe, Jane Street, Revolut, and the U.S. Department of Commerce. This collaboration has helped establish a new model to make market data more accessible, accurate, and transparent.

PYTH eyes $0.050 as bulls step in

The PYTH/USD 4-hour chart is bearish and efficient despite the coin adding 9% to its value in the last 24 hours.

The technical indicators have flipped bullish, indicating that the bulls are now in control of the market. The RSI of 63 is well above the neutral 50 and would enter the overbought territory if the rally persists.

The MACD lines are also within the positive region, indicating a strong bullish bias. If the rally continues, PYTH could retest the $0.050 psychological level for the first time since March 17.

However, if the bears regain control, PYTH could retest the Thursday low of $0.038 over the next few hours or days.

Trump tariffs fall, but trade war impacts linger

Why More Players Searching for Stake.com Alternatives Are Finding ZunaBet

Melbourne Demons vs Gold Coast SUNS Tips, Odds and Teams – AFL Round 4 2026

-

NewsBeat7 days ago

NewsBeat7 days agoThe Story hosts event on Durham’s historic registers

-

NewsBeat17 hours ago

NewsBeat17 hours agoSteven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Sports7 days ago

Sports7 days agoSweet Sixteen Game Thread: Tide vs Michigan

-

Entertainment4 days ago

Fans slam 'heartbreaking' Barbie Dream Fest convention debacle with 'cardboard cutout' experience

-

Crypto World2 days ago

Crypto World2 days agoGold Price Prediction: Worst Month in 17 Years fo Save Haven Rock

-

Business12 hours ago

Business12 hours agoNo Jackpot Winner and $194 Million Prize Rolls Over

-

Entertainment6 days ago

Entertainment6 days agoLana Del Rey Celebrates Her Husband’s 51st Birthday In New Post

-

Tech4 days ago

Tech4 days agoThe Pixel 10a doesn’t have a camera bump, and it’s great

-

Crypto World3 days ago

Dems press CFTC, ethics board on prediction-market insider trades

-

Sports3 days ago

Sports3 days agoTallest college basketball player ever, standing at 7-foot-9, entering transfer portal

-

Fashion5 days ago

Fashion5 days agoAmazon Sundays: Soft Spring Layers

-

Tech3 days ago

Tech3 days agoEE TV is using AI to help you find something to watch

-

Business1 day ago

Business1 day agoLogin and Checkout Issues Spark Merchant Frustration

-

Tech4 days ago

Tech4 days agoAvatar Legends: The Fighting Game comes out in July and it looks pretty slick

-

Fashion6 days ago

Fashion6 days agoWhen Evening Dressing Gets Colorful for Spring

-

Tech5 days ago

Tech5 days agoElon Musk’s last co-founder reportedly leaves xAI

-

Crypto World4 days ago

Crypto World4 days agoU.S. rule change may open trillions in 401(k) funds to crypto

-

Tech3 days ago

Tech3 days agoHow to back up your iPhone & iPad to your Mac before something goes wrong

-

Tech4 days ago

Tech4 days agoApple will hide your email address from apps and websites, but not cops

-

Politics4 days ago

Politics4 days agoShould Trump Be Scared Strait?

You must be logged in to post a comment Login