Crypto World

Bankers rebuff White House claim that stablecoin yield doesn’t threaten deposits

The crypto industry’s chief effort in U.S. policy — the Digital Asset Market Clarity Act — has remained held up on a point about stablecoin yield that has little to do with the bill’s central aim to regulate U.S. crypto markets. It’s still a sticking point as bankers fired the latest volley to claim the industry’s reward programs are a danger to bank deposits.

In response to a recent White House economists report that the banks have little to fear from the rise of stablecoins, the American Bankers Association contends that the Council of Economic Advisers was analyzing the wrong scenario. Instead of looking at what would happen if Congress were to institute a ban on stablecoin yield now, it should have looked at what would happen if such returns from stablecoins were allowed.

“The CEA paper minimizes the core risk by starting from the wrong question,” according to ABA economists. “There is already ample evidence and analysis showing that a prohibition on yield for payment stablecoins is a prudent safeguard. Such a policy will allow stablecoins to mature as a payments innovation rather than as an economically risky substitute for insured bank deposits.”

This conflict over a topic already partially dealt with in last year’s Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act effectively derailed the Senate legislation for months. Though the Clarity Act’s lawmaker advocates have predicted it could get its necessary hearing in the Senate Banking Committee before the end of this month, that session hasn’t yet been scheduled.

Senators from both parties had been moved by the bankers’ arguments that their depositors (who fund their lending) would leave them in droves to chase stablecoin yield that outpaces what the banks offer in interest. So the lawmakers hashed out a compromise that would ban yield on stablecoin holdings that look like deposit accounts and only allow rewards programs for activity, akin to credit-card rewards. But the banks haven’t come out cheering it.

Senator Cynthia Lummis, the Wyoming Republican who chairs the Banking Committee’s digital assets subcommittee, posted Monday on social media site X, “America needs Clarity.” She’s kept a steady stream of posts going on the topic, saying over the weekend that it’s “now or never” for the bill.

The longer this debate stretches out, the more difficult it’ll be to get Clarity through the Senate process that can lead to a floor vote. While crypto insiders have been relatively vocal about the clash, bank representatives have been more reserved.

The bankers’ latest arguments suggest that the absence of intervention on stablecoin yield now would let stablecoin markets scale rapidly from $300 million to as much as $2 trillion.

“In a larger market, yield is not a minor product feature; it is the mechanism that would accelerate migration out of bank deposits,” they contend.

And though leading stablecoin issuers would deposit reserves in banks, they’re likely to go to larger institutions and not community banks, according to the ABA’s thinking.

Read More: Clarity Act returns to U.S. Senate, bank earnings: Crypto Week Ahead

Scope of Interfaces to Be Covered

The Commission outlined covered user interfaces as websites, browser extensions, or applications associated with crypto wallets. These applications assist users to plan and start transactions on blockchain platforms or smart contracts. Also in the guidelines, there are platforms that provide routing information, pricing and cost estimates of transactions. Such interfaces provide support to users that make use of self-custodial wallets to conduct crypto asset securities trades. They might also contain aggregators and swap platforms that show execution paths. As a result, the SEC acknowledges their functions in operations but does not differentiate them from the traditional intermediaries.

The SEC, however, added that it will not object to some platforms functioning without registration of a broker-dealer in some circumstances. The platforms should enable users to customise the parameters of transactions and offer educational aids to make informed choices. In addition, they should not give instructions to the users on certain securities transactions. The Commission highlighted that platforms should be neutral when offering trading options. The interface providers can provide default execution facilities, but they are not able to rank or favor specific trades. Therefore, it requires compliance by ensuring that the user is in control and restricting access to the results of transactions.

Section 15 of the Exchange Act that regulates the registration of brokers is referred to as the guidance. Though certain interfaces might fit the definition of brokers, the SEC made it clear that there are situations in which the enforcement might not be applicable. Moreover, such a strategy is an indication of a loose reading of the law on securities. The research head of Galaxy Digital Alex Thorn claimed that the SEC is moving forward with market structure without legislation. He observed that the agency is developing rules that resemble the ones suggested in the CLARITY Act. Furthermore, he emphasised the fact that the guidance provided to the staff might change with time.

Also, the guidance can facilitate future exemption of innovation covered by the SEC leadership. This may go as far as tokenised securities trading via automated systems and decentralised applications. The agency therefore keeps on demarcating operational limits of new crypto services. The crypto regulation debate in the U.S. Senate is set to be reintroduced in the near future. The legislators can proceed with official reviews and amendments of the suggested bill. The schedule indicates that there will be ongoing liaison between regulatory and legislative action.

The U.S. Securities and Exchange Commission said that software that sets up user interfaces allowing crypto securities to be transacted through individuals’ wallets won’t need to be registered and regulated as a broker.

In the latest of the agency’s staff statements on crypto — now a wide-ranging list of views meant to allow the crypto industry to move forward in the absence of permanent rules — the SEC staff said on Monday that the websites or software used by people pursuing securities transactions with their self-hosted wallets won’t itself be considered as belonging to the broker-dealer category. That tracks with the agency’s recent stance that developers should be able to write software without triggering such regulations.

The agency provided a checklist of measures the creators of these interfaces can take to keep them out of the regulatory box, including that it “does not solicit investors to engage in any specific crypto asset securities transactions” and “does not provide commentary on any potential execution route(s) displayed to a user.”

If the interface offers financing, provides investment recommendations, handles user assets, takes orders or executes transactions, it’s no longer outside the agency’s regulatory reach.

“The staff is providing its views as an interim step while the commission continues to consider various regulatory issues relating to crypto asset securities activities and the feedback it has received,” the document said.

Under the administration of President Donald Trump, who has demanded that his executive branch clear an easier path for the rise of friendly crypto regulation, the leadership of the SEC has reversed previous resistance and embraced the technology. Even before the arrival of SEC Chairman Paul Atkins, a series of pro-crypto statements began emerging, clarifying the regulator’s new view that various assets wouldn’t be considered securities or wouldn’t trigger oversight requirements. But these statements don’t carry the weight and greater permanence of full-fledged rules.

In the meantime, Atkins’ agency is working on such rules. Wide-ranging SEC rules are close to the proposal stage at the agency, he’s said. Even as the Senate continues to work on the Clarity Act that would cement crypto regulations into law, the agency is working on interim measures to give the agency great certainty.

Read More: SEC makes quiet shift to brokers’ stablecoin holdings that may pack big results

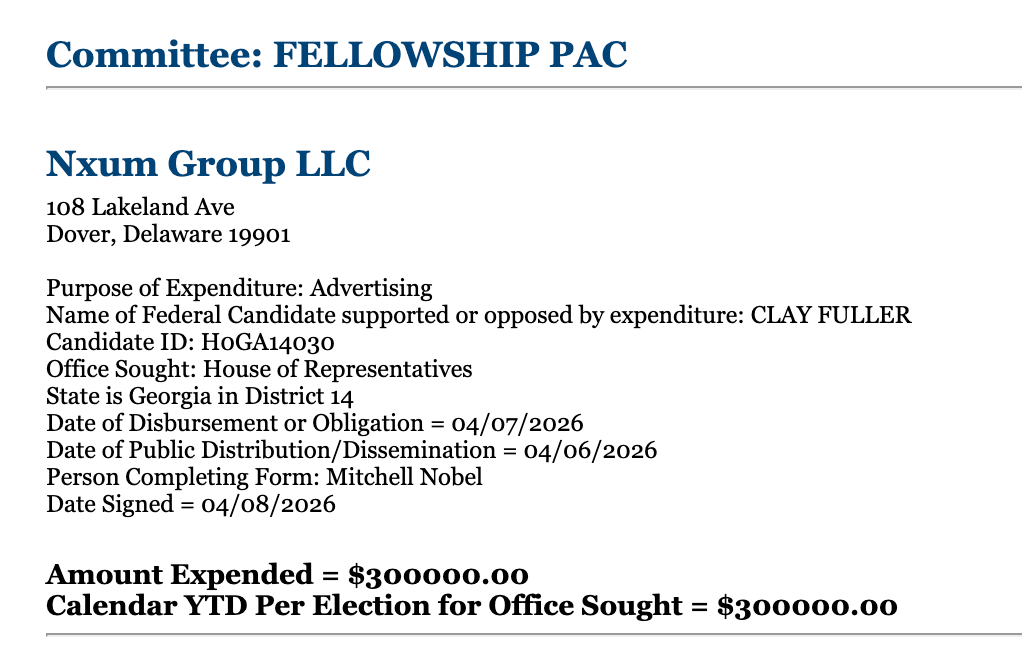

Fellowship, a super political action committee (PAC) that claims to have $100 million in its war chest from crypto-aligned parties ahead of the 2026 US midterms, has begun reporting spending and endorsements for the next election.

According to a filing with the Federal Election Commission (FEC), the Fellowship PAC reported spending $300,000 on advertising for Clay Fuller, a Republican who won a special election for Georgia’s 14th Congressional District to replace resigning congresswoman Marjorie Taylor Greene. The spending, reported disbursed on Tuesday, comes about a month before Georgia’s Republican primary on May 19.

Fellowship is just one of several crypto-backed or aligned PACs expected to pour money to support or oppose candidates in another critical US election season. In 2024, the Fairshake PAC spent more than $130 million in media buys in congressional races, possibly influencing the outcomes in key battlegrounds like the US Senate seat for Ohio.

According to the FEC, super PACs may “receive unlimited contributions from individuals, corporations, labor unions and other PACs for the purpose of financing independent expenditures and other independent political activity.”

In addition to its only reported expenditure since the Fellowship PAC’s statement of organization filed in 2025, Fellowship posted endorsements for candidates to its X account on Thursday, signaling support for Republicans in races across five states. The candidates included Alan Wilson for South Carolina governor, Blake Miguez for Louisiana’s 5th Congressional District, Mike Collins for the US Senate in Georgia, Julia Letlow for the US Senate in Louisiana, Pete Ricketts for the US Senate in Nebraska and Nate Morris for the US Senate in Kentucky.

Related: Chainlink and Anchorage Digital back launch of crypto-aligned PAC

Fellowship announced its launch in September, claiming to have “over $100 million” from undisclosed backers aligned with the crypto industry. On April 1, it said that Tether’s head of government affairs, Jesse Spiro, would chair the PAC, signaling support for candidates with pro-crypto views.

US lawmakers are still stalled on crypto market structure bill as midterms approach

The CLARITY Act, legislation passed by the US House of Representatives in July, has faced several delays in the Senate with no clear path forward on passing the legislation as of Monday.

Reports over the weekend signaled that the Senate Banking Committee, one of the two bodies needed to approve the bill in the chamber before a vote, was planning to hold a markup on the legislation, but the event was not on the committee’s calendar at the time of publication.

The bill, expected to be one of the most comprehensive pieces of legislation affecting the crypto and banking industries, has faced pushback from lawmakers to address ethics, stablecoin yield, tokenized equities and other potential issues.

Magazine: Should users be allowed to bet on war and death in prediction markets?

The European Central Bank is charting a cautious path toward tokenizing Europe’s capital markets, arguing that the gains from distributed ledger technology (DLT) hinge on anchoring transactions in central bank money, ensuring interoperable infrastructures, and maintaining a robust regulatory framework.

In its latest Macroprudential Bulletin, the ECB notes that tokenization could deepen the EU’s savings and investments union, but warns gains depend on policy action keeping pace with evolving risks. The stance signals a measured push to modernize market plumbing without compromising financial stability or monetary control.

Key takeaways

- Tokenization could streamline the issuance-to-settlement chain and boost liquidity, but true gains require interoperable platforms and central bank money for settlement, not just private or commercial instruments.

- Early evidence from tokenized bonds points to lower borrowing costs and tighter bid-ask spreads, yet these improvements depend on scale, risk controls, and market adoption.

- Tokenized money market funds and euro-denominated stablecoins are analyzed as experiments in on-chain cash-like instruments, bringing new operational vulnerabilities alongside familiar liquidity risks.

- MiCA-compliant euro stablecoins could influence sovereign-bond demand and market resilience, depending on how issuers meet deposit and reserve requirements.

- Across five Bulletin pieces, the ECB stresses that tokenization can support a more integrated capital market only if policy, prudential rules, and central-bank infrastructure evolve in tandem.

Tokenized capital markets: Conditions and expected benefits

The ECB’s analysis outlines how tokenized assets could rewire the issuance-to-settlement chain by moving both securities and cash onto compatible ledgers and by automating corporate actions. By doing so, the authors argue, operational frictions tied to multiple intermediaries and legacy systems could be reduced, potentially unlocking improved secondary liquidity. Yet the potential gains hinge on avoiding a patchwork of incompatible platforms and ensuring that central bank money—not merely commercial bank money or privately issued tokens—can be used for settlement in tokenized markets.

One article in the Bulletin highlights that tokenization and DLT are moving from concept to early-scale deployment, but the benefits will be realized safely only if European policy action keeps pace. This framing underscores the balance policymakers are seeking: enabling innovation while preserving financial stability and monetary integrity. For market participants, that means pilots and gradually expanded use cases rather than rapid, broad-based deployment.

The Bulletin also flags the need for robust interoperability standards and risk governance to prevent fragmentation as tokenized infrastructure expands. In practical terms, that could mean common settlement rails, standardized corporate-action workflows, and clear rules on settlement finality and collateral management across platforms.

Tokenized MMFs and euro stablecoins under the lens

The bulletin treats tokenized money market funds (MMFs) as a parallel set of experiments that largely mirror the liquidity and run-risk profile of traditional MMFs, but with added operational vulnerabilities inherent to on-chain structures. The analysis invites scrutiny of how such funds would behave under stress and how they interact with on-chain cash-like instruments during adverse conditions.

A separate piece examines euro-denominated, MiCA-compliant stablecoins and their potential impact on sovereign debt markets. Depending on whether issuers meet deposit and reserve requirements, these on-chain tokens could act as a liquidity buffer in turbulent times or, conversely, become a channel for bank contagion. The report emphasizes the regulatory hinge: the way deposits, reserves, and governance are structured will shape how these stablecoins influence demand for government bonds and overall market stability.

Broader implications and what to watch

Together, the five pieces in the Bulletin lay out a clear, conditional path for tokenization: it can support Europe’s goal of a more integrated and efficient capital market, but only if policy direction, prudential oversight, and central-bank infrastructure evolve in lockstep. The ECB’s nuanced stance reflects an intention to reap potential benefits while keeping a tight line on risk management, liquidity resilience, and monetary integrity as tokenized formats scale beyond flagship deals and select issuers.

For investors and market builders, the early signals are instructive. Tokenized bonds showing lower borrowing costs in initial deployments suggest real efficiency gains from streamlined settlement and enhanced transparency. Yet those advantages are not guaranteed to persist once activity broadens: scale, legal clarity, and robust liquidity mechanisms will determine whether the benefits are durable or merely episodic. The same tension applies to tokenized MMFs and stablecoins, where innovation can improve access to liquidity but must not outpace safeguards around reserve adequacy and systemic risk.

Policymakers appear determined to preserve a centralized architectural logic—anchoring settlements in central bank money and ensuring regulatory clarity—while allowing the market to experiment with tokenized formats. The coming months could bring pilot programs, shared standards, and possible adjustments to settlement infrastructures, as Europe weighs how best to harmonize technology, law, and prudential rules.

Readers should watch how the ECB formalizes these concepts in concrete policy and industry guidance, and how market participants respond to any push toward standardized cross-platform settlement rails. The balancing act between innovation and stability will continue to shape the pace and scope of tokenized instruments across Europe.

The ECB did not respond to Cointelegraph for comment by publication.

The CEO of StarkWare, the once-$8 billion Israeli company behind Ethereum-based blockchain Starknet, announced layoffs and a full corporate restructuring today. Monthly revenue on its flagship network has collapsed more than 98% from its peak.

In November 2023, Starknet’s on-chain revenue peaked near $5.8 million within a single month. This month, it is on track for approximately $100,000.

In other words, the network that once generated $187,000 in daily fees now generates about $3,500 per day. StarkWare declined to disclose the number of layoffs.

StarkWare, founded in Israel in 2018, develops Starknet, an Ethereum layer 2. For disambiguation, there is no StarkWave entity, a common misnomer that circulates online.

Starknet’s STRK token launched via airdrop in February 2024 and briefly traded to $4.41. It’s since fallen to $0.033, giving it a market capitalization of $187 million. That’s a 91% decline from its $2 billion market cap in March 2024.

StarkWare CEO: We are downsizing

CEO Eli Ben-Sasson posted his internal memo to X, telling staff the company had grown too large.

“Very sadly, as part of this process, we are downsizing,” he said as he fired staff. “Our new strategy requires that we move fast, and we’re too big and too inefficient for that.”

StarkWare raised $100 million at an $8 billion valuation in May 2022, quadrupling its size from $2 billion in a round six months prior. Although the company hasn’t updated its valuation in today’s downsizing announcement, it would probably be embarrassing relative to those 2022 figures.

GreenOaks Capital and Coatue were lead investors in the company. Earlier backers included Sequoia Capital, Paradigm, Founders Fund, as well as crypto dumpster fires Three Arrows Capital and Sam Bankman-Fried’s Alameda Research.

StarkWare raised more than $260 million over its lifetime — more than the current market cap of STRK.

COO Oren Katz has submitted his resignation and departs at the end of this month.

A split and a sunset

The restructuring splits StarkWare into two independent business units. An applications division, led by Chief Product Officer Avihu Levy, will chase revenue directly. A Starknet development unit, led by Product Head Tom Brand, will continue core protocol work.

Read more: Crypto Twitter upset by Starknet STRK airdrop

The revenue decline is mostly due to Starknet’s failure to attract usage of its blockchain as well as limited revenue across layer 2 blockchains.

Ethereum’s Dencun upgrade in March 2024 slashed data costs for all layer 2 networks, compressing fee revenue across the board. Layer 2 governance tokens like STRK posted average returns of negative 40% in 2025 in their second consecutive unprofitable year.

Starknet fared worse than most. Its total value locked sits around $241 million per DefiLlama, far behind Coinbase’s Base at roughly $4.3 billion and Arbitrum at $1.9 billion. Starknet’s all-time cumulative fees total just $45 million.

Ben-Sasson acknowledged as much. “Infrastructure alone does not win the game.”

Got a tip? Send us an email securely via Protos Leaks. For more informed news, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

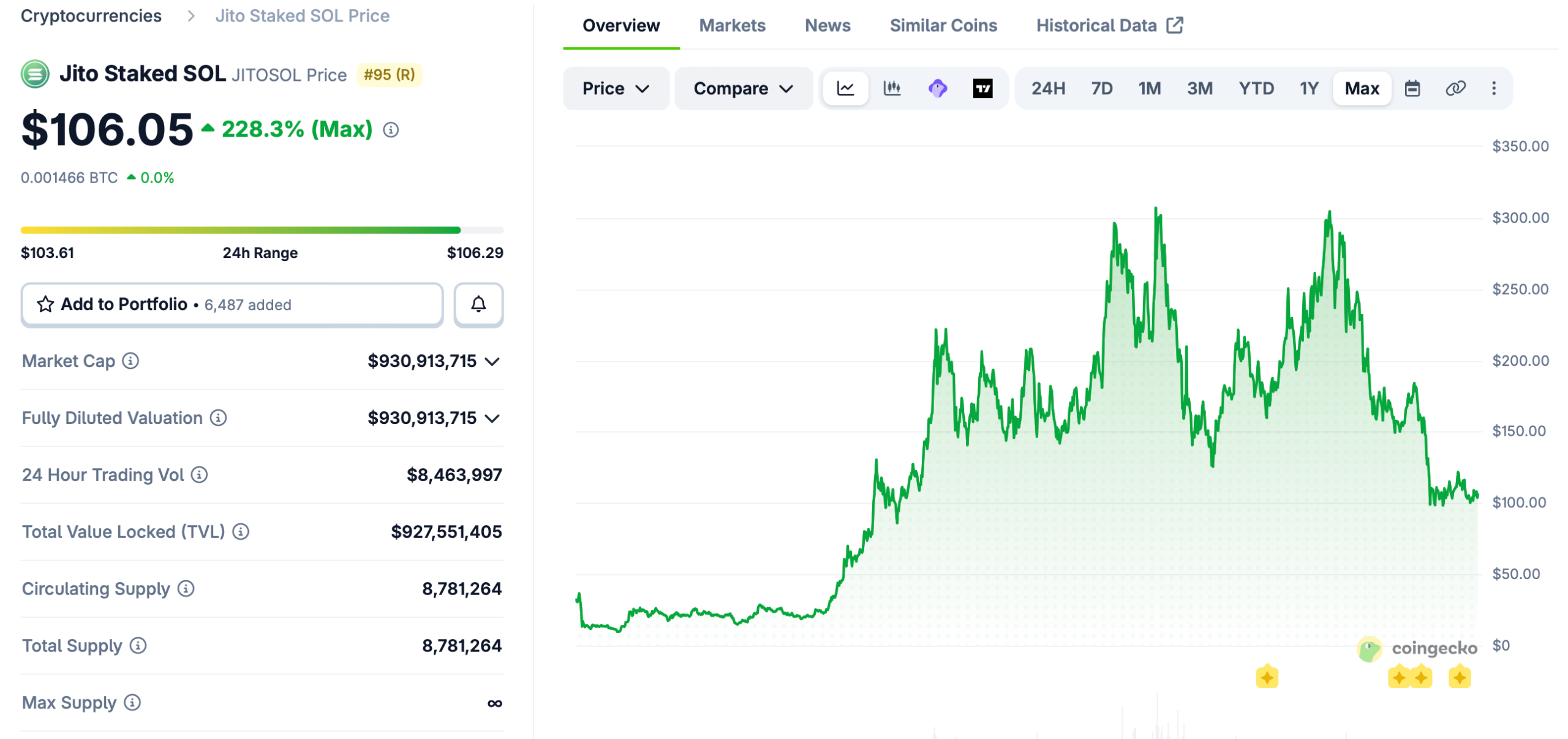

Jito Foundation has signed a memorandum of understanding with Korean digital asset custodian KODA to explore institutional custody and staking support for JitoSOL in the local market.

According to Monday’s announcement, the agreement includes outreach to institutional investors and the development of compliant custody and staking pathways.

It comes as South Korea’s Financial Services Commission is expected to finalize a digital asset regulatory framework later this year.

In February, the foundation said it would work with Hanwha Asset Management to explore a JitoSOL exchange-traded fund in South Korea, pending regulatory approval. Marc Liew, head of APAC at Jito Foundation, told Cointelegraph:

We are seeing significant interest from two main camps: large financial firms looking to build the next generation of wealth management products, and institutional entities that are interested in the yield-bearing nature of JitoSOL for their corporate treasuries.

KODA provides custody infrastructure including cold storage, MPC-based key management and institutional staking, carrying $20 million in digital asset insurance coverage. The company is backed by KB Kookmin Bank and other ininvestors andolds a registered VASP license and ISMS certification.

“Through KODA’s institutional-grade vaulting system, the KODA interface will allow the client to mint JitoSOL directly from their SOL holdings,” Liew said.

Jito is a liquid staking protocol on the Solana (SOL) network where users stake SOL in exchange for JitoSOL, a token usable across decentralized finance applications. The Jito Foundation supports development, partnerships and institutional outreach.

JitoSOL has a market capitalization of about $930 million, according to CoinGecko data. The token already has institutional exposure in Europe through a 21Shares exchange-traded product, while custodians including BitGo and Hex Trust support staking directly from custody accounts.

Related: Grayscale debuts Solana ETF, joining Bitwise in SOL staking ETF race

Seoul tightens crypto market controls

South Korean regulators and policymakers are pushing for tighter controls on the crypto sector as they move toward a more structured regulatory framework.

In January, the country approved changes to its crypto licensing regime, tightening requirements for virtual asset service providers and expanding oversight to include major shareholders. In March, policymakers followed with a proposal to cap ownership stakes in domestic exchanges at 20%, part of wider efforts to impose stricter controls on market structure.

The regulatory push accelerated after a payout error at crypto exchange Bithumb in early February, when users mistakenly received 620,000 Bitcoin (BTC) instead of 620,000 Korean won, triggering a sell-off and exposing weaknesses in exchange oversight.

Following the incident, the country’s Financial Services Commission introduced stricter reconciliation requirements between exchanges’ internal ledgers and onchain balances.

Earlier this month, lawmakers began drafting legislation that would classify stablecoins as foreign exchange payment instruments and require tokenized real-world assets to be backed by assets held in trust.

More recently, the Bank of Korea called for exchange-level “circuit breakers” and stronger internal controls, with the central bank warning that the industry lacks safeguards seen in traditional financial systems.

Magazine: Should users be allowed to bet on war and death in prediction markets?

The bitcoin price is range-bound between $68,000 support and $75,000 resistance heading into the most consequential two-week window of 2026, with three catalysts arriving back to back: the Iran ceasefire expiry on April 22, the CLARITY Act Senate markup targeted for late April, and the FOMC meeting on April 28 and 29.

Summary

- According to 24/7 Wall St. analysis, $68,000 is the key level to watch: bitcoin has held above it through both the Islamabad talks collapse and Monday’s blockade announcement, suggesting the market has already priced in the near-term bad news; if oil climbs past $110, however, analysts project bitcoin could fall to $65,000.

- If the ceasefire extends or new talks are announced before April 22, bitcoin could push back toward $75,000 to $80,000 on the same relief dynamic that drove the original ceasefire rally; a resumption of full hostilities with no diplomatic off-ramp is the scenario that breaks the $68,000 floor.

- The FOMC meeting on April 28 and 29 adds a second layer: with inflation running above 3 percent and oil still elevated above $100, Fed rate cut expectations have been effectively scrubbed from the near-term calendar, removing a key macro tailwind that historically supports bitcoin rallies.

Bitcoin (BTC) has spent 46 consecutive days in extreme fear territory, with the Crypto Fear and Greed Index reading between 8 and 12. Despite that, whale wallets accumulated 270,000 BTC over the past 30 days, the largest sustained buying spree since 2013, while exchange reserves hit their lowest level since December 2017 at 2.21 million BTC. Those on-chain signals suggest long-term holders are absorbing the selling from retail and tax-driven exits rather than liquidating.

One analyst described the level plainly: “$68,000: This is the line in the sand.”

The three catalysts between April 22 and April 29 interact with each other in ways that matter. If the ceasefire extends and oil drops toward $90, rate cut expectations improve going into the FOMC meeting and bitcoin gets a macro tailwind at the same time the CLARITY Act markup could add a crypto-specific catalyst. If all three resolve favorably in sequence, analysts at 24/7 Wall St project a move toward $75,000 to $80,000 by the end of April. That scenario requires a lot to go right simultaneously.

Why the Ceasefire Expiry Is the First Domino

The Islamabad talks ran 21 hours and ended without agreement on the two core issues: Iran’s nuclear program and control of the Strait of Hormuz. Iran’s parliament speaker returned home saying Iran would not bow to any threats. With the US Navy now blockading Iranian ports, the conditions for a ceasefire extension look harder to meet than they were before the weekend. 24/7 Wall St noted that “tax selling ahead of April 15 and uncertainty around the war will keep overriding Bitcoin’s rally attempts” in the near term.

What Happens to Bitcoin If $68,000 Breaks

As crypto.news has reported, the Fear and Greed Index has been in extreme fear for 46 consecutive days, and the market is structurally fragile with leveraged positions still present. As crypto.news has noted, a break below $68,000 would likely trigger liquidations from short-term holders who bought the ceasefire rally, with analysts projecting a move toward $65,000 if the war resumes and oil crosses $110.

Hungary’s 16-year Orbán era ended on April 12, 2026, when opposition leader Péter Magyar’s pro-EU Tisza Party secured a commanding parliamentary majority – and with it, a plausible path to unwinding one of the EU’s most aggressive national crypto crackdowns.

The political shift is confirmed. The regulatory reversal is not. That distinction matters, and this article will interrogate exactly what the gap between those two facts means for traders, operators, and the broader MiCA implementation map across Europe.

This story carries a speculative tag for good reason: no legislative rollback has been announced, no enforcement moratorium declared, and no Tisza-led government has yet been formally seated. What exists is a changed political vector – and in crypto policy, that’s often where the real repositioning begins.

- Political event: Péter Magyar’s Tisza Party won a parliamentary majority on April 12, 2026, ending Viktor Orbán’s 16-year rule, with Orbán conceding in early projections.

- Crypto crackdown at stake: Hungary’s amended Crypto Act, effective July 1, 2025, criminalized unauthorized exchange services and imposed a SARA-certificate validation regime on all crypto-to-fiat and crypto-to-crypto transactions.

- MiCA conflict: The European Commission launched infringement proceedings against Hungary’s validation regime, citing incompatibility with the harmonized MiCA framework – proceedings that a new government could resolve swiftly.

- Revolut exposure: The UK-based fintech, serving over 2 million Hungarian clients, halted crypto buying, staking, and deposits post-July 2025 and has given no reinstatement timeline.

- What remains unverified: No confirmed policy reversal, no legislative timeline, and no formal Tisza government position on crypto regulation has been announced as of publication.

Discover: Top Crypto Presales Worth Watching This Month

What Hungary Crypto Crackdown Actually Built – and What Post Election Reversal Would Have to Dismantle

The architecture of Hungary’s crackdown is more surgical than the headlines suggested. Amendments effective July 1, 2025 created two new criminal offenses – “crypto abuse” and “unauthorized crypto exchange services” – carrying penalties of up to 2 years in prison.

But legal analysis clarified the scope: the offenses target large-scale unvalidated exchange operations and unlicensed platforms, not node-running, Bitcoin holding, or personal use of international trading platforms.

The sharper tool was the validation layer. By December 27, 2025, a transaction-level system required SARA-licensed certificates for any crypto-to-fiat or crypto-to-crypto exchange executed through domestic platforms.

The practical effect was a state-controlled regulatory gatekeeper – one that crypto insiders characterized as designed to redirect market power toward licensed incumbents and away from foreign-operated platforms.

The capital flight concern was not hypothetical: Revolut, serving over 2 million Hungarians, has completely banned crypto buying, staking, and deposits, and has offered no reinstatement date.

A rollback under Tisza would not be a single vote to repeal. It would require unwinding the SARA validation regime, amending or nullifying the criminal offense provisions, and coordinating with the European Commission to close the active infringement proceedings.

That’s three separate institutional actions – legislative, regulatory, and diplomatic – that need to move in sequence. Possible within months under a motivated government. Not guaranteed even under a favorable one.

The EU infringement angle is the fastest lever available. The Commission’s proceedings against Hungary’s validation regime rest on a clear argument: MiCA sets a harmonized floor for crypto-asset service regulation across member states, and Hungary’s SARA certificate system creates a parallel national gatekeeping layer that MiCA’s architecture does not permit.

A new government signaling EU alignment – which Tisza’s pro-EU platform explicitly does – could resolve those proceedings through administrative withdrawal rather than full legislative reform. That would remove the validation layer fastest, even before the criminal provisions are revisited.

Discover: Best Crypto Presales Gaining Traction in 2026

The post Hungary Election Political Shake-Up Could Reopen Crypto Policy and Regulation Debate appeared first on Cryptonews.

This editorial introduces a press release describing a rapid market reassessment driven by geopolitical tensions and a rise in oil prices. It notes that talks with Pakistan collapsed and a blockade of the Strait of Hormuz has occurred, shifting sentiment from relief to caution across energy and equity markets. The release links higher crude costs to potential inflationary pressure and central‑bank policy responses, while framing the upcoming earnings season as a gauge for how firms price energy risk. A market analyst is quoted on whether the move signals a short‑term tactic or the start of a longer supply shock, a distinction readers will weigh carefully.

Key points

- Crude prices have risen about 8% on the development, signaling tighter energy markets.

- US equity futures have slipped as markets reassess risk and potential supply disruptions.

- Emergency stockpiles are being drawn down and the IEA warns that supply pressures could intensify.

- S&P 500 earnings are expected to grow about 12.6% this quarter, with major banks set to report; forward guidance will be critical.

Why it matters

The practical effect of geopolitical risk and higher energy costs extends to inflation expectations, borrowing costs, and corporate forecasting. If the disruption proves temporary, markets may adjust; if it persists, inflation and policy responses could become louder market drivers. For readers, traders, and investors, the message is to monitor how energy risk is priced into forecasts and what earnings commentary reveals about resilience or vulnerability in the near term.

What to watch

- The ceasefire deadline of April 22 and any progress toward a resolution.

- How companies adjust guidance on energy costs and demand in earnings reports.

- Oil maintaining levels above $100 per barrel and the implications for inflation and policy.

- Market volatility in response to headlines and headline-driven risk reassessment.

Disclosure: The content below is a press release provided by the company or its PR representative. It is published for informational purposes.

Markets Reprice as Oil Surges and Geopolitical Risks Escalate

Abu Dhabi, UAE -13 April 2026: Markets have rapidly shifted from optimism to uncertainty following the collapse of Pakistan talks and the immediate blockade of the Strait of Hormuz, reversing last week’s relief rally driven by ceasefire hopes. The move has already pushed crude prices higher by around 8%, while US equity futures have slipped, underscoring growing investor concern over potential disruptions to global energy supply.

Josh Gilbert, Market Analyst at eToro, said: “The key question for markets right now is whether this is a short-term negotiating tactic or the start of a more prolonged supply shock. If it’s temporary, markets may look through it. But if this disruption persists, the inflationary consequences will be significant and will quickly move back to the top of the agenda for investors.”

Higher oil prices are already feeding into global inflation expectations, complicating the outlook for central banks that had been edging closer to rate cuts. With oil expected to remain above USD $100, policymakers may be forced to delay easing plans, adding further pressure on consumer sentiment and economic growth.

The impact is being felt globally, with emergency stockpiles being drawn down and limited buffer capacity to absorb further shocks. Warnings from the International Energy Agency suggest supply pressures could intensify in the coming weeks, increasing the risk of sustained volatility across energy markets.

This backdrop coincides with the start of US earnings season, where the S&P 500 is expected to report earnings growth of approximately 12.6%, marking a sixth consecutive quarter of double-digit growth. Major banks including Goldman Sachs, JPMorgan, Wells Fargo, and Citi are set to report, offering early insight into how rising geopolitical tensions are impacting the real economy.

Gilbert added: “Forward guidance will be critical this earnings season. While first-quarter results may not fully reflect the impact of higher oil prices, the real focus will be on whether companies are starting to factor in a prolonged disruption. Any signs of caution around consumer spending, corporate confidence, or deal activity could add another layer of pressure on markets.”

With the ceasefire deadline approaching on April 22 and no clear path to resolution, markets are expected to remain highly sensitive to headlines. Volatility is likely to persist, with investors needing to stay prepared for further downside risks if tensions continue to escalate.

About eToro

eToro is the trading and investing platform that empowers you to invest, share and learn. Founded in 2007 with the vision of a world where everyone can trade and invest in a simple and transparent way, today eToro has 40 million registered users from 75 countries.

eToro believes in the power of shared knowledge and that investors can become more successful by investing together. The platform has built a collaborative investment community designed to provide users with the tools they need to grow their knowledge and wealth. On eToro, users can hold a range of traditional and innovative assets and choose how they invest: trade directly, invest in a portfolio, or copy other investors.

Visit eToro’s media centre for the latest news.

The crypto market entered a new phase of geopolitical stress on Monday morning when the US Navy began enforcing a blockade of Iranian ports at 10 AM ET, sending Brent crude above $103 a barrel and keeping bitcoin pinned near the $70,000 support level that has held since the Islamabad ceasefire talks collapsed over the weekend.

Summary

- Brent crude rose more than 7 percent to top $103 a barrel after CENTCOM confirmed the blockade, while WTI climbed 7.8 percent to $104; the moves came after the US and Iran failed to agree on extended terms during 21 hours of talks in Islamabad on April 11 and 12, with VP Vance announcing the breakdown Saturday night.

- Bitcoin traded around $70,600 to $71,085 on Monday morning, holding above $70,000 through the blockade announcement; the ceasefire technically remains in effect until April 22, though neither side has indicated it will be extended following the Islamabad collapse.

- CENTCOM clarified the blockade targets maritime traffic to and from Iranian ports only and will not impede freedom of navigation for vessels transiting the Strait to non-Iranian ports, a partial scaling back of Trump’s social media announcement which said the Navy would interdict any ship that had paid a toll to Iran.

As CNN Business reported, WTI crude is now more than 50 percent higher than before the war effectively shuttered the Strait in late February. Iran’s oil accounts for roughly 4 percent of world supply, most of it exported to China, and the blockade could cut off a significant source of funding for Tehran’s government and military. Capital Economics chief economist Neil Shearing wrote in a note that the move “risks creating new potential flashpoints,” raising the question of whether the US Navy would seize allied ships that had paid tolls to Iran or target Chinese vessels in the Strait. Only 17 ships passed through the waterway on Saturday, compared with an average of roughly 130 daily crossings before the war.

Bitcoin’s resilience at the $70,000 level through this weekend’s events is meaningful. The asset dropped into the low $60s when Iran first closed the Strait in late February, then rallied to $72,700 when the ceasefire was announced April 7, liquidating $427 million in short positions. The subsequent pullback to the $70,000 to $71,000 range on the Islamabad collapse and Monday’s blockade news shows the market has partially priced in a return to conflict. Holding $70,000 through a formal naval blockade is a structurally different outcome than the early-war behavior.

What the Oil Price Level Means for Bitcoin

The direct transmission between oil and bitcoin runs through inflation expectations and Federal Reserve policy. Every dollar oil climbs above $100 makes a rate cut less likely, keeps liquidity tighter, and suppresses risk appetite across equities and crypto simultaneously. As crypto.news has reported, bitcoin’s behavior as a high-beta risk asset during oil spikes has been consistent across the entire conflict period, with an 85 percent correlation to the Nasdaq-100 during energy price surges.

What Happens Next Before April 22

As crypto.news has noted, three catalysts now define the two weeks ahead: the ceasefire expiry on April 22, the CLARITY Act Senate markup targeted for late April, and the FOMC meeting on April 28 and 29. If the blockade tightens oil supply further and prices push past $110, analysts project bitcoin could fall toward $65,000. A last-minute diplomatic breakthrough before April 22 could reverse that move sharply, as the original ceasefire rally demonstrated.

The SEC Conditionalises DeFi Platforms to Be Avoided for Broker Registration

Alan Ritchson Heads to Netflix With a Brutal New Survival Series

DWP benefit payment changes two child benefit cap scrapped

Why Israel is blocking foreign journalists from entering

Bitcoin: We’re Entering The Most Dangerous Phase

Alan Cumming Brands Baftas Ceremony A ‘Triggering S**tshow’

How much $$ my laundromat made this weekend #shorts

8 Essential Financial Things Everyone Must Know | Smart Money Tips #Finance #Awareness

What’s Business? How to Success in Business? #cryptocurrency #rajatvlogs #cryptopr #propine

-

Politics3 days ago

Politics3 days agoUS brings back mandatory military draft registration

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Veronica Beard

-

Sports3 days ago

Sports3 days agoMan United discover Nico Schlotterbeck transfer fee as defender reaches Dortmund agreement

-

Tech6 days ago

Tech6 days agoHow Long Can You Drive With Expired Registration? What Florida Law Says

-

Politics1 day ago

Politics1 day agoWorld Cup exit makes Italy enter crisis mode

-

Crypto World4 days ago

Crypto World4 days agoCanary Capital Files SEC Registration for PEPE ETF

-

Business3 days ago

Business3 days agoTesla Model Y Tops China Auto Sales in March 2026 With 39,827 Registrations, Beating Cheaper EVs and Gas Cars

-

Crypto World5 days ago

Crypto World5 days agoBitcoin recovers as US and Iran Agree a Ceasefire Deal

-

Politics4 days ago

Politics4 days agoMalcolm In The Middle OG Turned Down ‘Buckets Of Money’ To Appear In Reboot

-

Fashion6 days ago

Fashion6 days agoLet’s Discuss: DEI in 2026

-

NewsBeat20 hours ago

NewsBeat20 hours agoPep Guardiola and Gary Neville agree over Arsenal title problem that benefits Man City

-

Business3 days ago

Business3 days agoOpenAI Halts Stargate UK Data Centre Project Over Energy Costs and Copyright Row

-

Business2 days ago

Business2 days agoIreland Fuel Protests Enter Day 5 as Blockades Spark Shortages and Government Prepares Support Package

-

Politics4 days ago

Politics4 days agoLBC Presenter Mocks Trump Over Iran War Failures

-

Crypto World3 days ago

Crypto World3 days agoFederal judge blocks Arizona from bringing criminal charges against Kalshi

-

Tech4 days ago

Tech4 days agoA version of Windows 10 released a decade ago is now eligible for additional security patches

-

NewsBeat1 day ago

NewsBeat1 day agoJD Vance announces ‘no agreement’ with Iran over nuclear weapons fear

-

Business3 days ago

Business3 days agoIMF retains floor for precautionary balances at SDR 20 billion

-

Entertainment5 days ago

Entertainment5 days agoAlfred Hitchcock’s 10 Most Suspenseful Masterpieces, Ranked

-

Entertainment3 days ago

Entertainment3 days agoA ‘Bridgerton’ Star’s New Survival Thriller Is a Must-Watch on Netflix This Weekend

You must be logged in to post a comment Login