Crypto World

Banks Take Hard Line on Stablecoin Yields as White House Talks Stall

Crypto and banks clashed over stablecoin rewards, with no agreement reached ahead of the March 1 deadline.

Banks and crypto executives met again at the White House this week to settle a dispute over stablecoin rewards, but the talks ended without agreement ahead of a March 1 deadline set by the administration.

The standoff centers on whether crypto firms can offer yield on dollar-pegged tokens without draining deposits from traditional banks.

White House Talks Narrow Gaps But Yield Ban Remains Sticking Point

Details from the closed-door meeting were first shared on X by journalist Eleanor Terrett, who cited banking and crypto sources present in the room. According to her, participants described the session as “productive,” though no compromise was reached.

She added that banking groups arrived with a written set of “yield and interest prohibition principles.” The document argued that payment stablecoins, as outlined in the GENIUS Act, were designed strictly as payment instruments, not interest-bearing products. It also called for a broad ban on “any form of financial or non-financial consideration” tied to holding or using a payment stablecoin.

The handout allows for only extremely limited exemptions and warns against deposit flight that could reduce credit availability for communities. It also proposed civil penalties for violations and strict rules against marketing stablecoins as deposits or FDIC-insured products.

One banking concession, according to Terrett’s sources, was the inclusion of language allowing for “any proposed exemption,” a shift from earlier refusals to discuss carve-outs at all.

Still, the scope of permissible activities remains disputed, with crypto firms pushing for broader definitions that would let platforms reward users under certain conditions, while banks want those definitions drawn more narrowly.

You may also like:

The meeting was led by Patrick Witt, executive director of the President’s Crypto Council. Attendees included Coinbase Chief Legal Officer Paul Grewal, Ripple’s Stuart Alderoty, a16z’s Miles Jennings, and representatives from Paxos and the Blockchain Association.

Major banks present included JPMorgan, Goldman Sachs, Bank of America, Citi, Wells Fargo, PNC, and U.S. Bank, along with trade groups such as the American Bankers Association.

Alderoty later wrote on X that “compromise is in the air,” though others described the outcome as unresolved. Further discussions are expected in the coming days, although it is unclear whether another White House meeting will occur before the deadline.

Deposit Fears Shaping the Broader Legislative Fight

The yield debate is unfolding against a wider push to pass a long-delayed crypto market structure bill. Last week, crypto firms floated concessions, including sharing stablecoin reserves with community banks or allowing them to issue their own tokens, in an effort to ease opposition.

However, banks argue that yield-bearing stablecoins could pull funds from checking and savings accounts, weakening a primary source of lending capital. Analyst Geoff Kendrick warned that stablecoins could draw up to $500 billion in deposits from banks in industrialized nations by 2028.

SECRET PARTNERSHIP BONUS for CryptoPotato readers: Use this link to register and unlock $1,500 in exclusive BingX Exchange rewards (limited time offer).

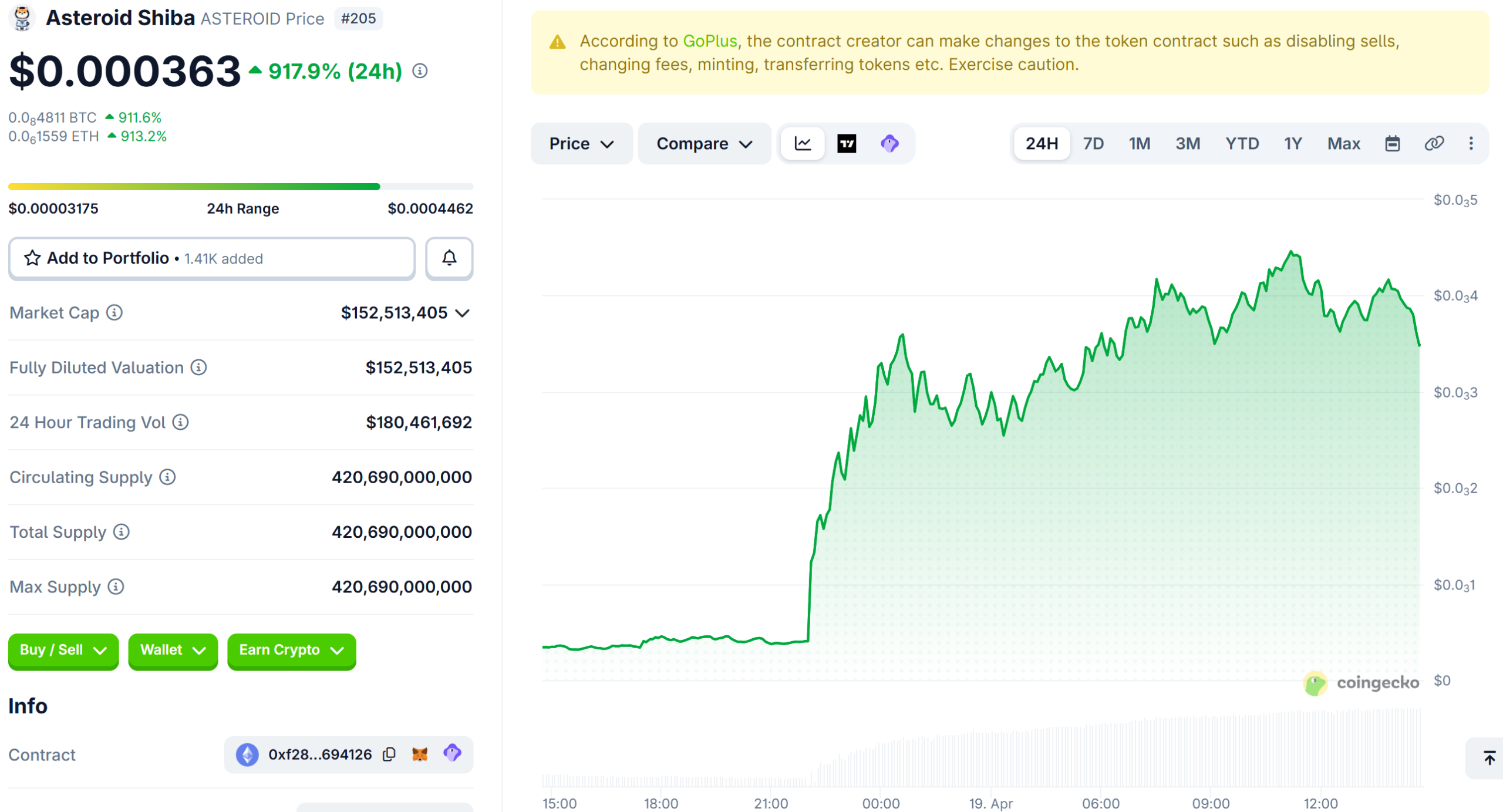

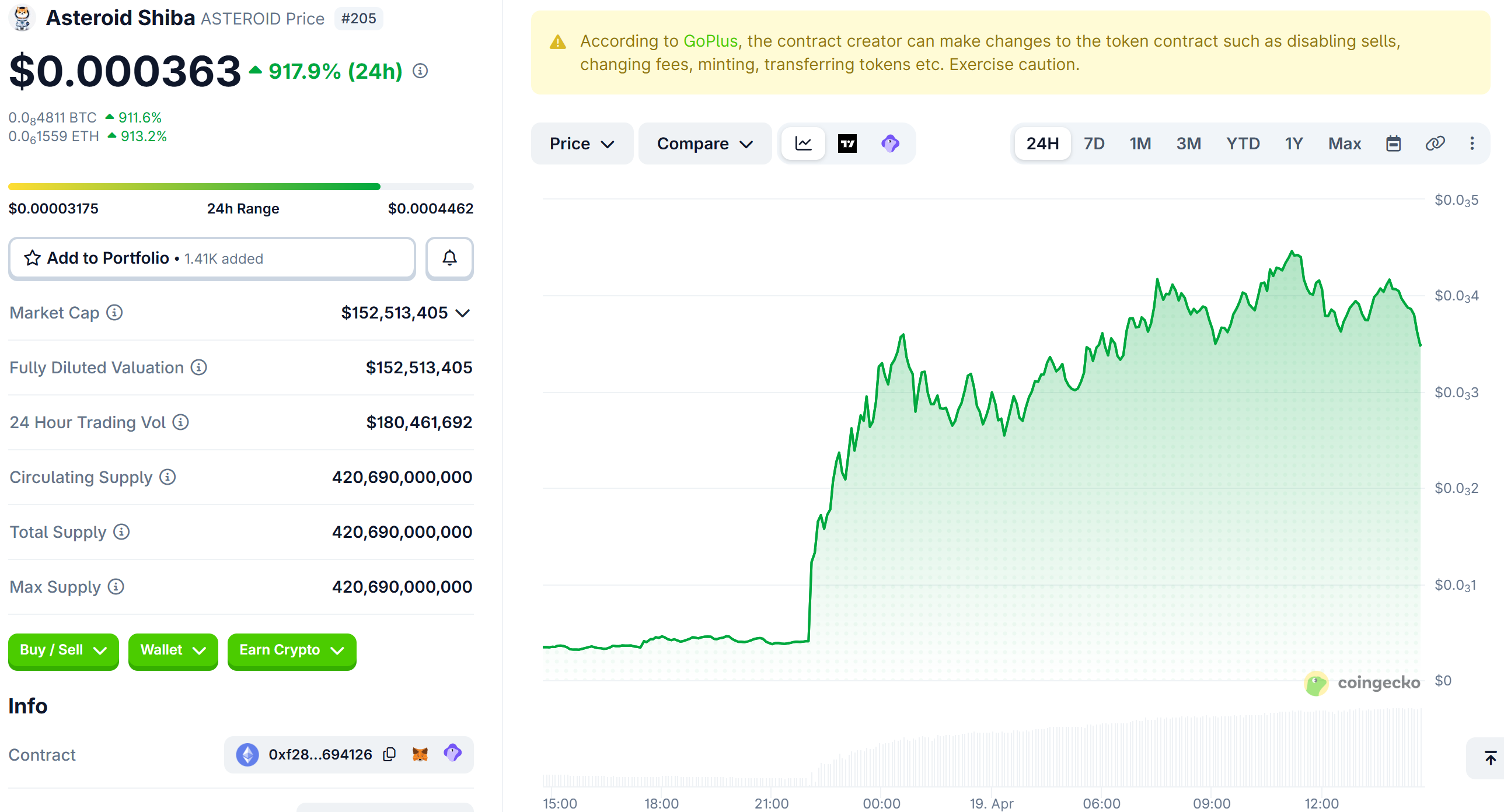

A trader sold 7.43 billion Asteroid Shiba (ASTEROID) tokens for $405 just one day before the meme coin rallied over 920%, turning that same position into a $2.6 million windfall.

On-chain data from Lookonchain revealed that wallet 0x5811 had bought the tokens 80 days earlier for $542. The sale locked in a $137 loss, erasing what would have been a life-changing gain.

What Triggered the Asteroid Shiba Rally

The rally began after Elon Musk replied to eight questions left behind by Liv Perrotto, a 15-year-old who died in January after a five-year battle with cancer.

Perrotto had designed a plush Shiba Inu named Asteroid as the zero-gravity indicator for SpaceX’s Polaris Dawn mission in September 2024.

For her final question, she asked Musk to make Asteroid the official SpaceX mascot. He agreed.

The Asteroid Shiba price is up by almost 920%, and nearly 68,000% in the last week.

Her mother, Rebecca Perrotto, responded on X, thanking him for keeping her daughter’s memory alive.

“You didn’t just honor a young girl’s dream, you are keeping her spirit alive. Liv’s love, her laughter, her unbreakable fight lives on through Asteroid,” she wrote.

Winners, Losers, and Risk

While wallet 0x5811 missed millions, another trader turned roughly $1,800 in ETH into nearly $500,000 within hours of Musk’s post.

However, Musk’s ability to move meme coins has shown signs of fading. Previous Musk-linked rallies in tokens like GORK and KEKIUS were short-lived.

Musk himself has previously compared meme coins to gambling. ASTEROID has no product, roadmap, or team behind it. The token carries significant risk for anyone buying after the initial move.

“If you expect to win at meme coins, you’re being foolish. You’re not going to win with meme coins. Don’t sink your life savings into a meme coin,” he said in an interview with The Joe Rogan Experience podcast.

The post Asteroid Shiba Gains 920% After Musk Names SpaceX Mascot, But One Trader Misses Big appeared first on BeInCrypto.

Crypto World

Arbitrum (ARB) Breaks Descending Trendline After 96% Crash: Analyst Eyes 7400% Return to $5+

TLDR:

- ARB has dropped 96.36% from its all-time high, now trading at $0.12 after a prolonged descending channel.

- A liquidity sweep below dynamic support confirmed capitulation, triggering a 57% rally from the $0.07–$0.095 demand zone.

- Bullish structure remains valid only if ARB reclaims and holds above $0.27; a breach of $0.065 invalidates the setup.

- Analyst bull cycle targets for ARB range from $0.27 to $5+, representing a potential upside of over 7400% from lows.

Arbitrum (ARB) has broken out of a multi-year descending trendline following a 96% drawdown from its all-time high. The token, currently trading at $0.12, is drawing fresh attention after printing a 57% rally from its cycle lows.

Analysts are now pointing to a potential 7400% return from current levels, with targets stretching to $5 and beyond.

The breakout comes after a prolonged accumulation phase that appears to have absorbed the final wave of selling pressure.

Trendline Break Follows Months of Capitulation and Liquidity Sweeps

ARB spent the better part of its post-2024 cycle trapped inside a brutal descending channel. Every bounce within that structure attracted retail buyers, only to be met with another wave of distribution. The repeated pattern of fake reversals kept bearish pressure firmly in control throughout the decline.

Crypto analyst Crypto Patel flagged a high-risk accumulation zone between $0.095 and $0.07 well before the recent move.

According to the analyst, price completed a full liquidation phase inside that zone before reversing. That sweep of stops below dynamic support confirmed what technicians call a liquidity grab or SSL sweep.

Following that sweep, ARB rallied 57% from its lows, breaking above the descending trendline that had capped price for over a year.

Crypto Patel noted that traders who entered from the previous accumulation call are now sitting on approximately 50% gains. That kind of follow-through after a capitulation event carries more weight than a typical relief rally.

The trendline break, combined with the liquidity sweep below dynamic support, sets up a textbook post-accumulation structure.

However, traders should note that a single breakout candle does not guarantee continuation. Price action in the coming weeks will determine whether this move holds or fades back into the prior range.

Analyst Maps Out Targets as ARB Eyes Structural Recovery

For the bullish case to remain intact, ARB must reclaim and hold above $0.27 on higher timeframes. That level serves as the primary support-resistance flip zone and the first gate for confirming trend recovery. A failure to reclaim $0.27 keeps the structure vulnerable to another distribution leg.

Crypto Patel outlined a full ladder of bull cycle targets starting at $0.27, followed by $0.50, $1.20, $2.50, and $5 or higher.

The previous cycle high of $2.425 is marked as an exit liquidity zone, meaning price could push through it before facing heavier resistance. A move to $5 from current levels would represent a gain of over 7400%.

The invalidation level sits at a two-week close below $0.065. A confirmed close at that level would signal that the accumulation thesis has failed. Until that line breaks, the broader setup remains active for traders who entered near the demand zone.

ARB’s 96.36% macro correction places it among the hardest-hit assets in the current altcoin cycle. Whether the trendline break marks a genuine turning point depends entirely on how price behaves around the $0.27 reclaim in the sessions ahead.

Bitcoin paused its recent ascent as geopolitical tensions resurfaced over the weekend, keeping markets wary of a broader conflict between the United States and Iran. With renewed talk of the Strait of Hormuz facing disruption, traders weighed the potential for an oil-price shock against the appetite for risk assets, including cryptocurrencies. Bitcoin traded near the mid-$70,000s, attempting to defend key levels ahead of Sunday’s weekly close after briefly brushing higher late in the week.

Data and market chatter pointed to a fresh sense of tension. Bitcoin climbed to around $78,400 on Friday, a ten-week high, before retreating as headlines shifted and risk appetite tempered. By Sunday, the price was hovering near $75,000, signaling a pullback after the prior surge. The backdrop remained fluid as market participants gauged whether a ceasefire or renewed hostilities would take hold, and how such developments would interact with oil and broader macro moves.

Key takeaways

- Bitcoin faced renewed resistance near the 21-week exponential moving average, a level around $78,900, as it retraced from intraday highs.

- The geopolitical context intensified oil-market risk: reports of renewed disruptions to the Strait of Hormuz heightened concerns about a potential supply shock and its spillover to risk assets, including crypto assets.

- Oil prices showed sensitivity to headlines, with WTI crude trading below $80 per barrel on some signals of a possible ceasefire, highlighting the link between macro risk and crypto sentiment.

- Market mood remained bullish but vulnerable to sudden news or social-media sparks, with traders cautioning that a single headline or tweet could shift momentum.

- Liquidation data pointed to notable risk-off liquidity pressures, with aggregate crypto liquidations around $260 million over a 24-hour window, underscoring the fragility of near-term positions.

Oil, war fears and the price backdrop

Oil markets became a focal point again as the weekend’s headlines revived fears of a renewed US-Iran confrontation. Reports of renewed activity around the Strait of Hormuz amplified concerns about supply disruptions and renewed price volatility for crude futures. In tandem, traders watched how oil moves might influence appetite across crypto markets, where liquidity often shifts with macro headlines rather than purely idiosyncratic crypto catalysts.

Communication around a possible ceasefire or de-escalation did little to steady the longer-term risk calculus, and oil traders noted that even partial headlines could trigger quick reactions in prices. The up-and-down dynamic in oil underscored a broader market logic: when macro risk rises, risk assets can be pressured, even those like Bitcoin that some participants view as a hedge or diversifier in times of macro uncertainty.

For now, the day-to-day energy-relevant headlines remain a meaningful driver for traders looking for directional cues in crypto. The oscillation between hawkish rhetoric and quiet moments of diplomatic negotiation has the potential to tilt sentiment on short timeframes, particularly if the Strait of Hormuz scenario tightens again or if oil futures react decisively to any fresh geopolitical signals.

Bitcoin price action and key technical themes

Beyond the headlines, Bitcoin’s price action in the near term has been tethered to a critical technical juncture. A close near the weekly low around $75,000 would keep the market within a range defined by a rising but tested resistance near the 21-week EMA. The EMA, a broad gauge of medium-term momentum, sits close to $78,900 and has repeatedly acted as a cap on advances in recent sessions. Rejection at this level could set up a retest of nearby support zones and, depending on weekly closes, potentially expose traders to a retest of the lower boundary of a prior consolidation pattern around the mid-$70k area.

Analysts have flagged the possibility that the market could undergo a short-term pullback even amid a broader bullish backdrop. The sense that sentiment is “overwhelmingly bullish” at present notwithstanding, some observers warned that a sudden shift—whether from a social-media post, a geopolitical headline, or a shift in macro data—could reframe risk appetite quickly. As one market watcher cautioned, “sentiment is bullish, but that could change with one Tweet in the coming days.”

On the micro front, leveraged long positions and other speculative bets faced pressure as Bitcoin retraced from intraday highs. Data aggregators tracked a flurry of liquidations across the broader crypto complex, with total crypto liquidations estimated at about $260 million over a 24-hour window as traders recalibrated exposures in light of the move lower. The quick swing underscored the sensitivity of near-term price action to changes in market mood, even as longer-run fundamentals remained a topic of ongoing debate among investors and builders alike.

From a futures perspective, some traders looked to a potential gap opening in CME Group’s Bitcoin futures market at the start of the week. Historical precedents show gaps can act as magnets for price action after a weekend or holiday backdrop, drawing participants to monitor the opening prints for signs of momentum. As the weekend downward drift fed into talk of a fresh gap, observers anticipated whether the “week opening magnet” effect might pull BTC higher or contribute to further consolidation near a key level.

Looking further ahead, prominent technical analysts emphasized the importance of a weekly close near critical support and resistance zones. For instance, commentary highlighted a potential post-breakout retest of the upper boundary of a former double-bottom pattern if the weekly candle closes show structural resilience. In practical terms, a weekly close that preserves the bullish structure could set the stage for renewed attempts to challenge the $80k barrier and beyond, provided macro and crypto-specific catalysts line up.

Market dynamics, signals and what to watch next

Beyond the price tape, several threads are shaping the near-term narrative. Traders are watching sentiment drivers that could tip the balance from cautious optimism to renewed risk appetite or vice versa. The presence of a volatile macro backdrop—where geopolitical headlines, oil-price moves and policy signals intersect—means crypto markets could quickly flip direction if a major headline emerges.

In addition to macro factors, liquidity dynamics remain a critical determinant of short-term price action. The recent wave of liquidations is a reminder that the crypto market can exhibit sharp, disorderly moves when positions are unwound rapidly. For traders, it’s a reminder to manage risk and to avoid overreliance on a single data point or indicator, especially in an environment where headlines can outrun technical signals.

On the technological and adoption side, observers continue to monitor how broader macro volatility may influence demand for decentralized finance, layer-1 ecosystems, or crypto-native hedging strategies. While Bitcoin and the wider market have shown resilience at times, the path forward will likely hinge on how the geopolitical situation evolves, how oil markets respond to headlines, and whether risk appetite returns with a stronger, more durable macro backdrop.

Industry voices have offered a cautious note: the current setup could breed both opportunity and risk. If the market can digest the latest headlines without triggering a self-sustaining downside, Bitcoin could attempt to extend gains toward the high-$70k region and perhaps test the previous swing highs. Conversely, a renewed spike in energy prices or an escalation in tensions could reassert downside pressure, prompting a reversion toward key support near the mid-$70k zone.

Notably, the weekend’s developments—and the ensuing discussions about possible gaps in CME futures—illustrate how crypto markets are increasingly intertwined with macro narratives. For investors and builders, the takeaway is clear: macro headlines remain a primary channel of influence, and the next few sessions could be decisive in establishing the next directional bias for Bitcoin and the broader crypto complex.

As the week opens, traders will be scanning a constellation of inputs: oil-price movements, any shifts in geopolitical talk, and the technical signals from Bitcoin’s chart, particularly the interplay with the 21-week EMA and the possibility of a retest of critical support. The coming days will reveal whether current bullish undertones harden into a sustained up-leg or whether the market cools and consolidates as macro uncertainties persist.

Meanwhile, observers will continue to monitor the macro backdrop for signs of a lasting shift in risk sentiment. If the Strait of Hormuz remains stable or oil prices stabilize despite headlines, there could be a constructive setup for Bitcoin and altcoins. If not, the market could test previously broken levels and reassert risk-off dynamics across digital assets.

What remains uncertain is how quickly macro news translates into crypto price action and whether any single event can set a new baseline for risk appetite. Readers should keep a close eye on the weekly close, the trajectory of oil futures, and the dynamics of CME futures gaps, all of which will shape the near-term path for Bitcoin and the wider market in the days ahead.

Crypto World

Caitlyn Jenner Wins $JENNER Memecoin Lawsuit as Federal Court Rules Token Is Not a Security

TLDR:

- A California federal court dismissed all Securities Act claims against Caitlyn Jenner over the $JENNER memecoin on April 16, 2026.

- The court ruled the $JENNER Ethereum token failed the Howey test due to lack of horizontal and vertical commonality among investors.

- Jenner’s 3% transaction tax gave her independent income regardless of investor losses, defeating vertical commonality claims in court.

- State law claims for fraud and quasi contract were dismissed without prejudice, leaving Greenfield the option to refile in California state court.

Caitlyn Jenner wins lawsuit after a California federal court dismissed all securities claims tied to the $JENNER cryptocurrency token.

Lead plaintiff Lee Greenfield had sued Jenner and her manager Sophia Hutchins, alleging the token was an unregistered security.

The U.S. District Court for the Central District of California ruled on April 16, 2026, that the Ethereum-based token did not meet the legal definition of a security. Greenfield had lost over $40,000 in the investment.

Judge Rules $JENNER Token Fails the Howey Test for Securities

The court applied the longstanding Howey test to determine whether the $JENNER token qualified as an investment contract.

That test requires proof of a common enterprise and an expectation of profits from others’ efforts. Greenfield could not satisfy either requirement, and the court dismissed the Securities Act claim with prejudice.

Greenfield argued that all token holders experienced identical percentage gains and losses, proving horizontal commonality.

The court disagreed, stating that parallel price movement does not substitute for pooling of investor funds. The SAC itself acknowledged that cryptocurrencies like the $JENNER token “lack utility other than as a store and transfer of value.”

Jenner and Hutchins made no development commitments behind the $JENNER token. Defendants described it plainly as “a memecoin on the Ethereum blockchain intended solely for entertainment purposes.” No funds were raised to build any product, software, or ecosystem connected to the token.

Jenner’s promotion included an AI-generated tweet image of her in a “JENNER ETH” T-shirt carrying an American flag.

A crowd member in the image held a sign reading, “LETS MAKE EVERYONE RICH!” Hutchins further promoted the project by touting Jenner’s ability to “bring attention and investors into the project,” citing her awards, fame, and powerful connections.

The court ruled that promotional activity alone could not replace the pooling structure that securities law requires.

Jenner’s Transaction Tax Seals Vertical Commonality Argument Against Plaintiff

Greenfield also pursued vertical commonality, pointing to Jenner’s holdings of over 20 million $JENNER tokens. He argued her financial stake linked her fortunes directly to those of investors. The court found otherwise, citing her 3% transaction tax as a decisive factor working in Jenner’s favor.

During a Twitter Spaces chat, Jenner said tax proceeds would fund Trump campaign donations, buybacks, and marketing.

When an X user pushed back, writing, “Use half of the taxes for buybacks. The community doesn’t like to just fund Trump. It would be fair to do half and half,” Jenner responded, “Not all taxes going for Trump.

The first distribution would be made when we hit 50m MC. And never said it would be ALL of them. Some have been used for buybacks, marketing, etc.” The court treated these statements as too vague to constitute meaningful managerial commitments.

Critically, the tax paid Jenner on every transaction whether investors profited or not. Under the Ninth Circuit’s ruling in Brodt v. Bache & Co., a promoter must share in investor losses for vertical commonality to exist.

The court noted that Jenner “kept hundreds of thousands of dollars in tax revenues for herself even as the investments of Greenfield and others became nearly worthless.” Because Jenner faced no downside risk tied to investor outcomes, the vertical commonality standard was not met.

With no viable federal claim remaining, the court declined jurisdiction over Greenfield’s state law claims for fraud and quasi contract. Those claims were dismissed without prejudice, allowing him to refile in California state court.

The court also denied any further attempt to amend the Securities Act claim, finding such an amendment would be futile. Jenner’s legal victory draws a clear legal boundary between celebrity-promoted memecoins and regulated securities.

Crypto World

Nomura survey shows rising institutional crypto adoption driven by regulation and diversification

Institutional investors are warming to digital assets, with improving sentiment and broader use cases emerging as key drivers of adoption, according to a new survey from Tokyo-based bank Nomura and its crypto unit Laser Digital.

The study, based on responses from more than 500 investment professionals in Japan, found that 31% of respondents now hold a positive outlook on crypto over the next year, up from 25% in 2024. Meanwhile, negative sentiment has declined, pointing to a gradual shift in perception as the asset class matures.

A central theme is diversification. Some 65% of respondents said they view crypto as a portfolio diversifier, while 79% of those considering exposure plan to invest within three years. Most expect relatively modest allocations — typically between 2% and 5% — suggesting institutions are still in the early stages of adoption.

That shift is being supported by a changing regulatory and policy backdrop. In Japan, policymakers have spent the past year refining crypto frameworks, including discussions around classification, taxation and investor protections. Globally, clearer rules in major markets — alongside the approval and expansion of crypto investment products such as exchange-traded funds (ETFs) and tokenized assets — have reduced some of the uncertainty that previously kept institutions on the sidelines.

As a result, interest is expanding beyond simple price exposure. More than 60% of respondents expressed interest in staking, lending, derivatives and tokenized assets, reflecting growing demand for yield-generating strategies and more sophisticated portfolio construction.

Stablecoins are also gaining traction, with 63% of respondents identifying potential use cases ranging from treasury management to cross-border payments and investment in tokenized securities.

Still, barriers remain. Concerns around volatility, counterparty risk and the lack of established valuation frameworks continue to weigh on adoption. Regulatory uncertainty, while improving, has not fully disappeared.

Even so, the survey suggests the conversation is shifting. Rather than debating whether to invest in crypto, institutions are increasingly focused on how to do so — a sign that digital assets are moving closer to becoming a standard component of institutional portfolios.

Peter Schiff, a well-known Bitcoin critic and gold advocate, has raised concerns about MicroStrategy’s ongoing Bitcoin acquisition strategy.

Summary

- Peter Schiff says MicroStrategy Bitcoin funding model may increase shareholder dilution through repeated share issuance.

- Company shifts toward 11.5% yield preferred shares as earlier funding methods become less effective.

- Debate continues as analysts disagree whether MicroStrategy faces risk or retains financial flexibility.

The company has continued to expand its holdings through a mix of debt and equity issuance.

Schiff stated that MicroStrategy’s approach is becoming harder to sustain under current market conditions. He said “the company is shifting toward more expensive capital” while referencing recent financing changes linked to preferred shares.

He added that earlier funding methods, which included issuing shares at higher valuations, are becoming less effective in the present environment.

MicroStrategy has recently relied more on preferred share offerings with higher yield obligations. Schiff noted that the company is now issuing instruments with yields around 11.5 percent.

He said ”these obligations cannot be covered by software earnings alone” when describing the firm’s financial position. The company’s core software business has limited profit contribution compared to its Bitcoin exposure.

Schiff stated that funding future purchases may require additional issuance of preferred shares, discounted equity, or Bitcoin sales. He argued this could increase pressure on shareholders through dilution over time.

Claims of structural risk and market reaction

Schiff described the company’s financing approach as vulnerable if market conditions weaken. He said the structure depends heavily on continued access to capital markets.

Canadian billionaire Frank Giustra also commented on the strategy, calling it ”a giant ponzi that will unravel when the next financial crisis hits” according to remarks cited in reports. He suggested that macroeconomic stress could expose weaknesses in the model.

The comments reflect ongoing debate over corporate treasury strategies that rely on digital assets as a primary reserve.

Additionally, market research group BitMEX Research provided a different view on MicroStrategy’s approach. The firm stated that MicroStrategy is not under forced liquidation pressure and still has financial flexibility.

BitMEX Research said ”nobody is forcing MSTR to do this” and described the strategy as potentially beneficial under current conditions. It noted that the company can adjust financing terms, including coupon rates, instead of selling assets.

The discussion continues as MicroStrategy maintains one of the largest corporate Bitcoin holdings while using structured financial instruments to support its accumulation strategy.

Bitcoin foreshadows fresh market mayhem as it appears that the US-Iran war has returned, including the closure of the Strait of Hormuz oil route.

Bitcoin (BTC) sought to protect $75,000 into Sunday’s weekly close as crypto surfed fresh uncertainty over the US-Iran war.

Key points:

-

Bitcoin price action sinks from ten-week highs amid fears that the US-Iran war has returned in full force.

-

Iran closes the Strait of Hormuz, bringing back the risk of an oil-price surge.

-

BTC price action faces ongoing resistance at a 21-week trend line into the weekly close.

Bitcoin abandons highs as US-Iran war fears return

Data from TradingView showed BTC price pressure reentering after a trip to ten-week highs of $78,400 on Friday.

Mixed signals from US and Iranian sources characterized the weekend, with an assumed ceasefire and mutual agreements between the two sides now seemingly undone.

Among the latest developments was the repeat closure of the Strait of Hormuz, putting the focus on oil futures on the day. News of a ceasefire had sent WTI crude below $80 per barrel for the first time since March 10.

“We expect an eventful Sunday ahead,” trading resource The Kobeissi Letter summarized in ongoing analysis on X.

As BTC/USD circled local highs, and sentiment with it, market participants stayed cautious. Trading resource Material Indicators noted that the entire market mood could flip on relatively little input, such as a social media post.

“Sentiment is overwhelmingly bullish at the moment, but that could change with one Tweet in the coming days. Know your invalidations,” it told X followers.

Data from CoinGlass showed long positions coming under fire during the BTC price retracement, with total crypto liquidations at $260 million over the past 24 hours.

BTC price capped by resistance trend line

Continuing, trader Daan Crypto Trades eyed a potential gap in CME Group’s Bitcoin futures market opening as a result of the weekend comedown.

Related: Bitcoin can grow ‘probably a lot bigger’ than $30T+ gold market — Analysis

As Cointelegraph reported, such gaps often act as short-term price magnets when the new week begins.

“It’s going to be interesting to see the futures open today and how $OIL will react to the recent headlines regarding the strait,” he added.

Looking at the weekly close, trader and analyst Rekt Capital placed importance on Bitcoin’s 21-week exponential moving average (EMA) near $78,900.

“Bitcoin is rejecting from the 21-week EMA (green),” he observed alongside the weekly chart.

“It is this rejection that could force a post-breakout retest of the top of the Double Bottom (~$73k) next week, provided Bitcoin Weekly Closes just like this.”

This article is produced in accordance with Cointelegraph’s Editorial Policy and is intended for informational purposes only. It does not constitute investment advice or recommendations. All investments and trades carry risk; readers are encouraged to conduct independent research before making any decisions. Cointelegraph makes no guarantees regarding the accuracy or completeness of the information presented, including forward-looking statements, and will not be liable for any loss or damage arising from reliance on this content.

World has rolled out upgrades to its World ID protocol, positioning it as a wider digital identity layer for online verification.

Summary

- World ID now serves 18 million users across 160 countries with identity verification tools.

- System uses biometric scanning and cryptography to confirm humans without storing personal data.

- New features aim to block bots, deepfakes, and AI agents in digital platforms.

The system is designed to confirm whether an online user is a real person while keeping personal data private.

The network is currently used by close to 18 million people across around 160 countries. It aims to address growing issues linked to bots, automated accounts, and AI-generated identities in online environments.

World ID uses cryptographic methods to confirm uniqueness without sharing personal data. The system relies on an Orb device that scans biometric features and generates a secure anonymized identifier for each user.

The upgraded system introduces one-time-use nullifiers to prevent tracking across different services. These tools allow users to prove identity without exposing personal information or linking activity between platforms.

World ID also includes multi-key support, session control, and account recovery features. These functions are designed to improve system stability and support enterprise-level use while maintaining user control over identity data.

The company stated ”only cryptographic proofs are utilized, no personal information is stored” when describing how the system handles user data, according to project documentation.

Furthemore, World ID is being integrated into various digital services that require user verification. The system is used in areas such as ticketing platforms, gaming services, and online dating applications.

Examples include identity checks on platforms like Tinder and ticket systems designed to reduce automated resale. Tools such as Concert Kit aim to limit scalping by ensuring ticket buyers are verified individuals.

In enterprise use cases, the system has been linked to digital agreement tools and video verification services. Platforms such as DocuSign and Zoom are cited as potential integration points for human verification features.

Expansion toward AI and automated systems

The protocol also extends to AI agent environments. Developers can require human approval before automated systems complete sensitive actions or transactions.

World ID allows AI agents to be linked to verified human users. This setup is designed to support controlled automation in areas such as digital commerce and workflow systems.

The project stated ”the system enables accountability in automated environments” when describing its approach to AI integration. The focus remains on distinguishing human users from automated agents while maintaining privacy protection across digital platforms.

Former UK Prime Minister Rishi Sunak warned that the United States will recover from the 2026 Iran war far faster than the United Kingdom and Europe, calling America “the indispensable nation.”

Sunak argued that structural advantages give the US a larger buffer against geopolitical shocks. As a net energy exporter, America is shielded from the oil price spikes that have hammered import-dependent economies since the conflict began on February 28.

Why Europe Faces Greater Risk

In his column, the former prime minister pointed to a sharp asymmetry between the US and European economies.

Trade accounts for roughly 25% of US GDP, compared to 60-70% for the UK. That gap means disrupted supply chains and higher energy costs hit European economies harder.

Since the Strait of Hormuz was disrupted in early March, Brent crude surged past $119 per barrel, levels last seen in June 2022. A fragile two-week ceasefire brokered in early April brought temporary relief, but oil still trades above $90.

Sunak also warned that post-WWII security arrangements are fraying. NATO allies have long underinvested in defense while relying on US commitments.

A more transactional American foreign policy, regardless of which administration holds power, accelerates that reckoning.

Sunak, who championed the UK’s ambition to become a global crypto hub during his time in office, framed his warning as a call for Europe to invest in energy independence, defense autonomy, and economic resilience rather than hoping the old transatlantic order returns intact.

The coming weeks will test whether the fragile ceasefire holds or whether a fresh escalation deepens Europe’s economic exposure.

The post Rishi Sunak Warns Europe Faces Deeper Iran War Fallout Than the US appeared first on BeInCrypto.

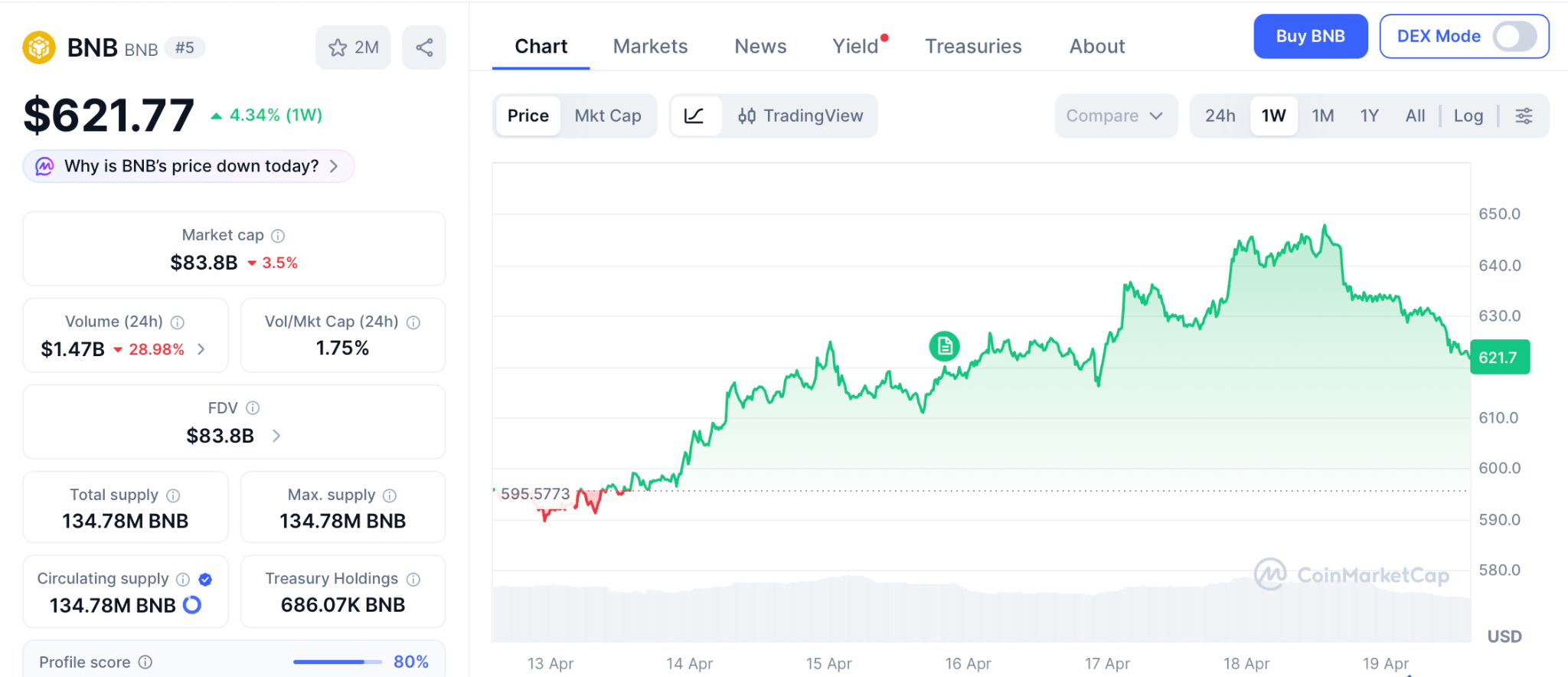

The BNB price prediction got a boost after BNB Chain destroyed 1.57 million tokens worth $1.02 billion in its 35th quarterly burn, dropping total supply to 134.79 million as the network pushes toward its 100 million target. That is real deflationary pressure hitting a token that already leads all Layer 1 networks with 4.5 million daily active users in Q1 2026.

But BNB gives you one way to earn: hope the price goes up. If it trades sideways for three months, your capital sat still. This breaks down where BNB heads next, why the burn matters, and how one presale pays two ways instead of one.

BNB Chain completed its 35th quarterly auto burn on April 15, removing 1,569,307 BNB from supply according to the BNB Chain Blog. The transaction is publicly verified on BSC. Blockchain.news confirmed remaining supply at 134.79 million, meaning 34.79 million more tokens still need to burn before hitting the 100 million target.

The burn follows the Fermi hard fork that cut block time to 0.45 seconds, and the network targets 20,000 TPS with sub second finality by end of 2026. Real usage drives the burns, not just price. And the presale that earns from two directions while BNB earns from one sits where utility meets the kind of entry that listings reprice overnight.

Why Holding BNB Alone Is Not Enough in 2026

BNB Gives You One Shot and Pepeto Gives You Two

You hold BNB after it dropped from $1,370 to $621, and the only way you make money is if the price climbs back, so if it trades sideways for three months your wallet shows zero gains because a single bet on direction delivers no yield and earns nothing during the wait.

Pepeto works differently by staking at 181% APY that adds tokens to your wallet daily regardless of market direction, so your holdings expand even during flat weeks as the first layer of returns, while the Binance listing eventually opens the gates and reprices the token to reflect what a working exchange handling real volume across three chains is actually worth, giving you two separate engines paying you instead of one hope and a prayer.

The cofounder who built Pepe to $7 billion designed it this way because one way to earn is not enough when half the market sits below all time highs, and PepetoSwap connects every blockchain with zero fee trading while the cross chain bridge handles Ethereum, BNB Chain, and Solana without gas and an AI scanner filters risky tokens before they appear, with SolidProof auditing every contract before the presale opened and $9.21 million entering during the same drawdown that took BNB from $1,370 to $621.

BNB (Binance Coin) Price at $621 as Quarterly Burn Shrinks Supply

BNB trades at $621 according to CoinMarketCap after rising 2% on the burn news. The token sits inside a $580 to $680 range, with the middle band acting as resistance. BNB Chain leads all Layer 1s with 4.5 million daily active users in Q1 and 322 million total holders, more than Ethereum’s 305 million.

Coinpedia targets $1,000 by Q3 if $600 holds, and Changelly projects a max of $1,121 for 2026. Even the bullish case from an $85 billion market cap cannot deliver the multiples a presale at six decimal zeros creates.

Final Takeaway

Every cycle teaches the same lesson, which is that the people who earned while they waited came out ahead no matter which way the price eventually moved, and the early BNB holders who bought at $0.15 and rode it to $700 did not just sit on price action, they earned exchange rewards along the way, and that same model is exactly what Pepeto offers right now at presale while BNB just burned a billion dollars in tokens and the chart barely flinched because burns alone do not create returns.

Pepeto pays from two directions starting today, with 181% APY compounding in every wallet that already moved and the Binance listing resetting the token permanently the moment the market gets access, and $9.21 million collected during extreme fear proves the conviction is backed by real capital from wallets that ran the math, so once this window closes the entry you see right now will only exist in the portfolios of the people who acted while the rest of the market was still deciding whether to believe it.

Click To Visit Pepeto Website To Enter The Presale

FAQs

What is the BNB price prediction after the $1 billion token burn?

BNB targets $680 to $1,000 in 2026 as quarterly burns shrink supply toward 100 million. Pepeto at presale pricing with 181% APY and a confirmed Binance listing offers higher return potential from a lower base.

What is Pepeto and why is it the best meme coin presale of 2026?

Pepeto is a meme coin presale combining viral energy with real utility through PepetoSwap zero fee exchange, a cross chain bridge, and an AI contract scanner. It has raised $9.21 million with 181% APY and a confirmed Binance listing led by the Pepe cofounder.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

‘I’ll believe it when I see it’: People on street which won Farage’s bills competition say Reform hasn’t paid

Jade Biosciences: Caution Advised Before Clinical Trial Results (NASDAQ:JBIO)

Asteroid Shiba Gains 920% After Musk Names SpaceX Mascot, But One Trader Misses Big

Why Israel is blocking foreign journalists from entering

Bitcoin: We’re Entering The Most Dangerous Phase

Alan Cumming Brands Baftas Ceremony A ‘Triggering S**tshow’

Did you know you can do this with a $100 bill? #cash #money #trick #hundred

When Life Gets Hard, Choose Financial Stability | April 16, 2026

Wallet with no money. #viral #funny #comedy #shortvideos #reaction #viralvideo #viralshorts #prank

-

NewsBeat7 days ago

NewsBeat7 days agoPep Guardiola and Gary Neville agree over Arsenal title problem that benefits Man City

-

Crypto World6 days ago

Crypto World6 days agoThe SEC Conditionalises DeFi Platforms to Be Avoided for Broker Registration

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Theodora Dress

-

Politics7 days ago

Politics7 days agoWorld Cup exit makes Italy enter crisis mode

-

Crypto World6 days ago

Crypto World6 days agoSEC Signals Exemption for Crypto Interfaces From Broker Registration

-

News Videos4 days ago

News Videos4 days agoSecure crypto trading starts with an FIU-registered

-

Sports2 days ago

Sports2 days agoNWFL Suspends Two Players Over Post-Match Clash in Ado-Ekiti

-

Crypto World5 days ago

Crypto World5 days agoSEC Proposes Certain Crypto Interfaces Don’t Need to Register as Brokers

-

NewsBeat5 days ago

NewsBeat5 days agoTrump and Pope Leo: Behind their disagreement over Iran war

-

Politics2 days ago

Politics2 days agoPalestine barred from entering Canada for FIFA Congress

-

Crypto World2 days ago

Crypto World2 days agoRussia Pushes Bill to Criminalize Unregistered Crypto Services

-

Sports6 days ago

Sports6 days agoNWFL opens Pathway for new Clubs ahead of 2026 Season

-

Business3 days ago

Business3 days agoCreo Medical agree sale of its manufacturing operation

-

Crypto World6 days ago

Crypto World6 days agoTrump whales load up ahead of Mar-a-Lago luncheon.

-

Business6 days ago

Kering slides after Morgan Stanley downgrade, Gucci woes loom

-

Entertainment5 days ago

Entertainment5 days agoBrand New Day’ Footage Reveals the Devastating Impact of ‘Now Way Home’

-

Politics4 hours ago

Politics4 hours agoZack Polanski demands ‘council homes not luxury flats for foreign investors’

-

Crypto World7 days ago

Sei Network Enters Quiet Reset Phase as On-Chain Metrics Signal a Slowdown in 2026

-

Tech6 days ago

Tech6 days agoGoogle adds E2E encryption to Gmail for iOS and Android enterprise users

-

Tech6 days ago

Tech6 days agoApple glasses won’t go brand shopping like Meta did with Ray-Ban and Oakley

You must be logged in to post a comment Login