Crypto World

Banks vs crypto over stablecoin yield

The biggest fight in American finance right now is over a single clause: whether digital dollars can pay their holders interest. Banks say yield-bearing stablecoins would drain trillions in deposits and break the lending machine. Crypto says the banks are defending a monopoly on other people’s money. The CLARITY Act is hostage to the answer, and this week the standoff escalated on every front.

Summary

- A battle over whether stablecoins should pay interest has become the biggest obstacle to advancing the CLARITY Act in the US Senate.

- Banks warn that yield bearing stablecoins could pull trillions of dollars from deposits while the crypto industry argues savers should receive the returns generated by reserve assets.

- As lawmakers remain divided, banks are also preparing for a future with stablecoins by investing in digital dollar infrastructure and settlement networks.

The week of June 29, 2026, was supposed to move the CLARITY Act toward the Senate floor. Instead, Coinbase publicly pulled its support for the bill it had spent two years championing, Senate Banking Committee chairman Tim Scott postponed the markup, and President Trump posted that the banks lobbying against stablecoin yield were threatening and undermining his own signature crypto law. The proximate cause of all three events was the same unresolved question: can a stablecoin pay interest?

The question sounds technical. It is not. It is a fight over roughly $6 trillion, which is the amount of deposit money that Bank of America chief executive Brian Moynihan has warned could migrate out of the banking system if digital dollars are allowed to pass their reserve earnings to holders. Behind the number sits the basic architecture of American credit: banks fund loans with deposits that pay savers little, and anything that gives savers a better default option attacks the cheapest funding source in finance.

Both sides understand the stakes with total clarity, which is why neither will yield. The banks have the oldest lobby in Washington and a century of regulatory capture to draw on. Crypto has the GENIUS Act already signed, a president publicly on its side, and products that customers demonstrably want. Between them sits a Congress trying to pass a market structure bill that both industries claim to support and each is willing to kill over this clause.

This is the anatomy of the standoff: where the yield actually comes from, what each side’s studies really say, how the fight broke into the open at Davos, why the CLARITY Act is stalled, and what the banks are quietly building in case they lose.

Where stablecoin yield comes from

A dollar stablecoin is a bearer claim on a reserve. The issuer takes a customer dollar, parks it in Treasury bills and repo and cash equivalents, and gives back a token redeemable at par. At 2026 short-term rates, that reserve portfolio throws off meaningful income: roughly four cents per year on every dollar, paid by the United States government to the issuer.

Under the GENIUS Act, the stablecoin framework signed in 2025, issuers keep that income. The law prohibits payment stablecoins from paying interest or yield to holders, a clause the banking lobby fought for and won. The result is one of the stranger economic arrangements in modern finance: tens of millions of stablecoin holders collectively finance a float measured in hundreds of billions of dollars, and the entire risk-free return on that float accrues to issuers and their distribution partners.

Tether’s profits, Circle’s revenue-sharing arrangement with Coinbase, and the business case for every new entrant described in the consortium stablecoin model behind Open USD all rest on that captured spread.

Crypto’s position is that the arrangement is indefensible on its own terms. If the token holder supplies the dollar, the token holder should be able to receive the yield, the same way a money market fund passes through its portfolio income. Exchanges already approximate this with rewards programs that pay users for holding certain stablecoins, a workaround the banks call interest by another name and want closed.

The banks’ position is that the arrangement is the only thing standing between the deposit system and a slow-motion run. A stablecoin that pays four percent, holds only Treasuries, settles instantly, and lives in a phone app is not a payment instrument, in their telling. It is a narrow bank, the exact institution American regulators have refused to charter for a century, because a narrow bank collects deposits and funds nothing.

Both descriptions are accurate. That is what makes the fight so hard to resolve. A product can be, simultaneously, a long-overdue transfer of interest income to the people who supply the money and a structural threat to the funding model of every lender in the country. The legislative machinery now stuck in the Senate exists precisely because Congress must pick which description governs, and there is no compromise text that makes both true halves false.

The dueling studies: $6.6 trillion or $2.1 billion

In early 2026 the American Bankers Association put a number on the threat. Its analysis warned that permitting interest-bearing stablecoins could trigger as much as $6.6 trillion in deposit flight from the banking system, a figure that would represent a structural repricing of bank funding. Moynihan carried the message personally, telling audiences that 30 to 35 percent of transactional deposits could leave banks if yield-bearing digital dollars became legal, and putting the Bank of America estimate in the $6 trillion range.

The mechanism behind the number is credit contraction. Deposits fund loans. A dollar that leaves a checking account for a stablecoin backed by T-bills stops funding a mortgage or a small business line and starts funding the federal government. Multiply by trillions and the banks’ model produces higher loan rates, reduced credit availability, and concentrated stress on community banks whose entire funding base is retail deposits. The ABA’s framing is not that banks would earn less, though they would; it is that the economy would lend less.

The White House Council of Economic Advisers looked at the same question and produced a number three orders of magnitude smaller. Its assessment put plausible deposit displacement in the low billions, around $2.1 billion in the scenario most cited, arguing that stablecoin demand comes overwhelmingly from crypto trading, cross-border flows, and dollar demand abroad, none of which is money sitting in a Kansas checking account today. In the CEA’s telling, the banks are counting every deposit that could theoretically move as a deposit that would move, ignoring deposit insurance, banking relationships, and the fact that money market funds have offered better rates than checking accounts for fifty years without ending bank lending.

The three-orders-of-magnitude gap is not really an empirical dispute. The two studies answer different questions. The ABA models the ceiling of a mature, frictionless, fully legal yield-bearing stablecoin market; the CEA models the floor of the current one. The honest answer, that displacement would start small and compound as the products improved, satisfies neither side, because the banks need the threat to be immediate and crypto needs it to be imaginary.

Davos, and the fight goes personal

The clearest public glimpse of how raw the conflict has become came at Davos in January, in an exchange between the two most powerful executives on either side.

JPMorgan chief executive Jamie Dimon, discussing stablecoin yield with Coinbase chief executive Brian Armstrong on a panel, dismissed Armstrong’s framing of deposit competition with a phrase that escaped the room within minutes: he told him he was full of s—, a vulgarity from the most measured banker of his generation that did more to reveal the temperature of the fight than any comment letter.

Armstrong’s argument, the one that drew the response, is the consumer-surplus case. American savers hold trillions in accounts paying a fraction of a percent while banks earn multiples of that on the float. Stablecoin yield, in his telling, is simply technology forcing banks to pay depositors something closer to the market rate for their money, and the deposit-flight studies are incumbents pricing their own margin as a systemic necessity. Coinbase has the most direct commercial stake of anyone in the room: its revenue share on USDC reserves is one of its largest income lines, and a world of legal yield pass-through is a world where its stablecoin business attacks bank deposits head-on.

Dimon’s counter is that payments and banking are different businesses with different risk, and that crypto wants banking economics without banking obligations: no lending mandate, no Community Reinvestment Act, no branch network, no discount window responsibilities, just the float. JPMorgan has hedged its own position, running deposit tokens and blockchain settlement internally while its chief executive argues against the retail version, a posture crypto reads as monopoly defense and banks read as prudence.

Then the President entered. In a late June post, Trump accused the banks of threatening and undermining the GENIUS Act, his own signed legislation, by lobbying to extend the yield ban and hobble stablecoin competition. A Republican president publicly siding against the banking lobby on a financial regulation fight is a genuinely new configuration in Washington, and it reshuffled assumptions on both sides about who holds the political high ground.

How the yield clause took CLARITY hostage

The CLARITY Act is a market structure bill. It assigns jurisdiction between the SEC and CFTC, defines when a digital asset is a security or a commodity, and creates the registration framework the industry has demanded for a decade. It is not, on its face, a stablecoin bill; the complete stablecoin framework already passed in GENIUS. But Washington does not respect bill boundaries, and the yield war has annexed it.

The banking lobby’s ask is straightforward: use CLARITY to close the loopholes GENIUS left open. That means extending the interest prohibition from issuers to exchanges and affiliates, killing the rewards programs that pay stablecoin holders today, and blocking any structure that passes reserve income to users. Bank trade groups have made support conditional on those provisions, and enough senators from both parties bank with them, figuratively and literally, to make the demand real.

Crypto’s response arrived the last week of June, when Coinbase announced it could no longer support CLARITY in its current trajectory, precisely because the yield restrictions being negotiated into it would, in the company’s view, entrench the ban permanently. The industry’s most important lobbying force turning against the industry’s most important bill was the loudest possible signal that the yield clause now outweighs the rest of the legislation for the companies whose business models depend on it.

Chairman Scott’s postponement of the markup followed within days. The delay was procedural on its face and structural in substance: there is no current text that both the banks and the crypto industry will accept, and members have little appetite to vote on a bill that one of the two richest lobbies in the country has promised to remember.

The market structure everyone claims to want is now collateral in a fight over a clause most voters have never heard of.

The political calendar sharpens everything. The window before the midterm campaign consumes Congress is measured in weeks, and both lobbies know that a bill that slips past the summer likely slips past the election, into a Congress nobody can predict.

The Regulation Q rhyme

The yield war has a nearly perfect historical precedent, and both sides quote it selectively.

From 1933 until its final repeal in 2011, Regulation Q capped or prohibited the interest American banks could pay on various deposits, a Depression-era rule justified in language strikingly close to today’s: unrestrained competition for deposits would push banks into risky lending and destabilize the system. For four decades the cap was mostly invisible, because market rates sat near the ceiling. Then came the inflation of the 1970s. Market rates ran far above what banks were legally allowed to pay, and savers found themselves holding accounts that lost purchasing power by regulatory design.

The market’s answer was the money market mutual fund, an instrument that did precisely what yield-bearing stablecoins propose to do now: pool customer cash, buy short-term government paper, and pass the interest through. Money funds grew from nothing in 1971 to hundreds of billions by the early 1980s, deposit flight became a named phenomenon, disintermediation, and the banking industry warned in congressional testimony that the funds would destroy community banking and starve the economy of credit. Congress ultimately responded not by banning money funds but by deregulating deposits, phasing out the caps and letting banks compete for money at market rates.

Both sides of the 2026 fight live inside this story. Crypto cites it as proof that yield restrictions always fall, that savers eventually get paid, and that the catastrophic credit predictions never arrived; the banking system that emerged from deregulation was different, and more expensive to fund, but intact. The banks cite the sequel: the savings and loan industry, built entirely on cheap capped deposits, could not survive paying market rates for money, and its collapse consumed a decade and roughly $124 billion of public funds. Deposit competition did not end banking, but it did end the banks whose models required the subsidy.

The rhyme suggests the real question is not whether stablecoin yield eventually becomes legal in some form; the historical base rate says restrictions on paying savers erode. The question is which institutions are the savings and loans of this cycle, funded so completely by the interest-free float that they cannot survive its repricing, and whether they are banks, or the stablecoin issuers whose entire margin is the yield they currently keep.

The banks’ quiet hedge

While the trade associations fight the public war, the banks themselves are behaving like institutions that expect to lose it.

Barclays made the most explicit move, taking a stake in Ubyx, the stablecoin clearing network built to let banks and fintechs redeem stablecoins at par across issuers, the plumbing a bank needs on the day it decides to issue or distribute digital dollars itself. It was the first direct stablecoin infrastructure investment by a major bank since the yield fight broke into the open, and it was not framed as an experiment. Bank executives have begun saying the quiet part in public: if Congress makes yield-bearing digital dollars legal, the banks will go into that business, at scale, the day the ink dries.

The logic is the same one that has played out in every disruption cycle in finance. Banks did not want money market funds in 1975 or online brokerages in 1995, and once each became inevitable, banks became the largest providers of both. A legal yield-bearing stablecoin issued by a money center bank, with deposit-adjacent branding, existing customer relationships, and a balance sheet behind it, is a formidable product, and arguably a more dangerous one to Tether and Circle than to the banks themselves. Consortium efforts like Open USD, whose members built a shared issuance model precisely so no single firm owns the float, exist in part because everyone can see the banks coming.

The infrastructure is converging from the other direction too. Payment-first blockchains designed for regulated issuers, the category examined in the rise of dedicated stablechains, are being built with bank compliance requirements as first-order design constraints, not afterthoughts. The technical gap between a bank deposit and a stablecoin narrows every quarter; the yield clause is the last load-bearing wall between the two products.

That is the tell in this fight. Institutions do not invest in the rails of a product category they expect to strangle. The banks are lobbying to delay the future and provisioning to own it.

What each side gets wrong

The banks’ deposit-flight case has a real weakness at its center: it treats the current deposit franchise as an entitlement. The spread between what banks earn on customer money and what they pay for it is not a law of nature; it is a price maintained by friction, and every prior technology that reduced the friction, from money funds to high-yield online savings, transferred some of that spread to savers without collapsing credit. The system adapted, banks paid more for funding, lending got marginally more expensive, and the economy survived. Framing the next step in that fifty-year process as a $6.6 trillion cliff requires assuming, without much evidence, that this time adaptation is impossible.

Crypto’s consumer-surplus case has a mirror-image weakness: it waves away the run problem. Bank deposits are sticky in a crisis partly because they are insured and partly because moving them is slow. A yield-bearing stablecoin is uninsured and moves at the speed of a tap. In a March 2023-style panic, the same properties that make stablecoins efficient make them the fastest exit door in the system, and a world where a meaningful share of transactional money can flee to tokenized T-bills in an afternoon is a world with a new, untested amplifier under every banking stress. The honest crypto answer is that this risk is manageable with reserve rules and redemption gates; the marketing answer, that it does not exist, is the one that gets said out loud.

There is also a shared blind spot. Both sides model the fight as domestic, and the stablecoin market is not. The majority of dollar stablecoin demand originates outside the United States, from savers and businesses in weak-currency economies for whom the yield question is secondary to the dollar itself. Whatever Congress decides about interest, the offshore float will keep growing, and the deposits it drains first are not in Kansas; they are in Buenos Aires and Lagos and Istanbul. The American fight over yield is, in part, a fight over who gets to monetize a global phenomenon neither side created.

The endgame scenarios

Three broad resolutions are visible from here, and each has a coalition behind it.

The first is the status quo hardened: CLARITY passes with the extended yield ban, rewards programs die, and issuers keep the float. This is the banks’ victory condition. Its weakness is that it is probably temporary, an attempt to legislate against a spread that technology keeps making easier to deliver, enforced against an industry with a sitting president publicly on its side. Prohibitions that fight both technology and the White House have a poor record.

The second is the pass-through world: yield becomes legal, the banks execute their hedge, and within a few years the largest stablecoin issuers in America are the same institutions that spent 2026 warning about them. Deposits reprice, weaker banks consolidate, and the credit system adjusts to more expensive funding, the way it adjusted to money market funds. This is where the investment behavior of the banks themselves suggests the smart money already sits.

The third is stalemate: CLARITY dies this Congress, GENIUS remains the only law, and the yield question migrates to regulators and courts, fought product by product through rewards programs, tokenized money funds, and offshore issuers that Congress never manages to reach. This is the default outcome if the next few weeks produce no text, and default outcomes in a midterm year are heavy favorites.

The watch list for the next few weeks is short and concrete. First, whether Scott reschedules the markup before the August recess, because a markup date means a text exists that leadership believes can survive both lobbies, and no date means the third scenario is winning. Second, the behavior of the pro-crypto Senate bloc, which has to decide whether a CLARITY with a hardened yield ban is worth passing over the industry’s objection, or whether half the coalition walks. Third, the regulatory perimeter fights already underway: how the Treasury implements the GENIUS provisions on affiliates, whether the rewards programs survive their first supervisory challenges, and how aggressively tokenized money market funds, which pay yield legally because they are securities, get marketed as the stablecoin alternative the ban cannot touch. Every one of those is a proxy battle in the same war, and each can move independent of Congress.

It is also worth naming the quiet incentive nobody in the fight advertises: the federal government is a beneficiary of the stablecoin boom regardless of who keeps the yield, because every reserve dollar is demand for Treasury bills at the exact moment deficits need buyers. A Washington that quietly likes the float’s growth has reasons to resolve the fight in whatever way grows it fastest, and that logic, unspoken, may ultimately weigh more than either lobby’s studies.

The $6 trillion number that anchors the fight will keep being quoted whichever path unfolds, and it is worth remembering what it actually is: not a measurement, but a boundary claim, the banks’ estimate of everything they could lose in the world their opponents want. The real number will be discovered the way these numbers always are, one repriced deposit at a time. The only certainty is the direction. Money has spent fifty years migrating toward whoever pays for it, and no clause has ever held that line forever.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Digital asset markets are volatile and you can lose your entire investment. Always do your own research. Information current as of July 6, 2026.

The wallet behind BonkDAO's $20 million governance attack has parked most of the stolen BONK in a multisig controlled by a newly created shadow DAO, Chainalysis said in a post on its official X account Tuesday. The blockchain analytics firm calls the structure "BONK 2.0." The multisig is governed… Read the full story at The Defiant

Tether has invested $20 million in a strategic growth financing round for Mercado Bitcoin, Brazil's largest crypto exchange, the stablecoin issuer announced Tuesday. The deal backs Mercado Bitcoin's push into tokenization, payments, credit and capital markets across Latin America. Mercado Bitcoin,… Read the full story at The Defiant

The U.S. Securities and Exchange Commission has added three major crypto-related rule proposals to its 2026 regulatory agenda, expanding its work on digital asset regulation while Congress continues to debate the CLARITY Act.

Summary

- The SEC has added three crypto-related rule proposals to its 2026 regulatory agenda covering assets, broker-dealers, and market structure.

- The proposals include possible crypto asset exemptions, broker-dealer rule changes, and new trading rules for exchanges and ATSs.

- Meanwhile, the CLARITY Act awaits a Senate vote as lawmakers work to reconcile competing versions before the Aug. 7 deadline.

According to the SEC’s Agency Rule List, the commission is considering separate rulemaking projects covering crypto assets, crypto broker-dealers, and crypto market structure. Together, the proposals would address how digital assets are issued, traded, and handled by regulated financial firms, while providing new guidance in areas that have long lacked clear federal rules.

The proposal covering crypto assets would explore regulations for the offer and sale of digital assets, including potential exemptions and safe harbors. The SEC said these measures could clarify the regulatory framework for crypto assets and provide more certainty for market participants.

The initiative follows the commission’s recently proposed innovation exemption, which would allow eligible firms to issue and trade tokenized U.S. stocks under specific conditions.

New rules extend across crypto trading and broker-dealers

Another proposal focuses on broker-dealers that deal with crypto assets. The SEC’s Division is considering recommending amendments to Rules 15c3-1 and 15c3-3, along with other broker-dealer financial responsibility rules and Rules 17a-3 and 17a-4, to address how existing requirements apply to digital assets.

Earlier this year, the SEC also outlined conditions under which certain decentralized finance platforms could operate without registering as broker-dealers. At the same time, the commission is separately seeking public comments on several novel exchange-traded fund proposals, including prediction market ETFs.

A third proposal listed in the regulatory agenda concerns crypto market structure. Under the plan, the Division is considering recommending amendments to Exchange Act rules governing the trading of crypto assets on alternative trading systems (ATSs) and national securities exchanges.

Speaking previously about the agency’s regulatory direction, SEC Chair Paul Atkins said the commission is embracing innovation by bringing more financial products onshore, creating clearer capital-raising rules for crypto businesses, and providing regulatory clarity for tokenized securities.

Atkins linked those efforts to President Donald Trump’s stated objective of making the United States the world’s crypto capital.

Congress continues work on the CLARITY Act

While the SEC advances its own rulemaking process, lawmakers are still negotiating the CLARITY Act, one of the most significant crypto market structure bills under consideration in Congress.

The legislation did not become law before the previously discussed July 4 timeline, despite earlier optimism expressed by White House crypto adviser Patrick Witt. Attention has now turned to Aug. 7, the Senate’s final scheduled session day before lawmakers leave for the summer recess.

Crypto.news previously reported that the CLARITY Act has already passed the House of Representatives, cleared the Senate Banking Committee, and remains on the Senate calendar awaiting a full Senate vote.

Before floor consideration can proceed, Senate staff are still reconciling separate versions produced by the Agriculture and Banking Committees because both panels oversee different parts of digital asset policy.

More recently, crypto.news reported that Senator Bill Hagerty outlined a revised Senate roadmap that could see final legislative text released before lawmakers return from recess. Bloomberg Intelligence has estimated the bill has roughly a 60% chance of passing this month.

Still, crypto.news has also reported that the legislation will likely require 60 Senate votes, meaning Republican lawmakers will need Democratic support before the proposal can move closer to President Trump’s desk.

Kraken has secured a $22 million arbitration award against its former auditor Mazars USA, with co-CEO Arjun Sethi linking the dispute to what he described as Operation Chokepoint 2.0.

Summary

- Kraken secured a $22 million arbitration award against former auditor Mazars over its withdrawn 2022 audit.

- Co-CEO Arjun Sethi linked the dispute to Operation Chokepoint 2.0 and called for passage of the CLARITY Act.

- The exchange continues expanding its product suite with tokenized stock collateral and institutional lending services.

According to a letter published Tuesday by Kraken co-CEO Arjun Sethi, parent company Payward has asked the Delaware Court of Chancery to enter judgment on the arbitration award after prevailing against Mazars USA. The dispute centers on the firm’s withdrawal from Kraken’s nearly completed 2022 audit, which Sethi said caused financial damage to the exchange.

Sethi wrote that Mazars ended the engagement despite finding no fraud, raising no concerns about Kraken’s management and reporting no disagreements with the company. He argued that the decision disrupted access to banking relationships, licensing processes and other essential business services that rely on completed independent audits.

Describing audits as critical infrastructure for financial companies, Sethi wrote that “an audit is not a favor. It is oxygen,” while arguing that lawful crypto firms were denied access to basic financial services during the period.

Sethi ties audit dispute to regulatory pressure

In the letter, Sethi attributed Mazars’ withdrawal to Operation Chokepoint 2.0, a term used by parts of the crypto industry to describe alleged coordinated pressure on banks, auditors and service providers to distance themselves from digital asset companies.

To support that argument, the letter pointed to several regulatory developments during 2023. These included joint guidance issued by U.S. banking regulators, the Securities and Exchange Commission’s since-rescinded Staff Accounting Bulletin No. 121, and the collapse of crypto-focused banking networks Silvergate SEN and Signature Bank’s Signet payment system.

Sethi also urged Congress to pass the CLARITY Act, saying a dedicated crypto market structure law would provide clearer operating rules for digital asset companies instead of relying on enforcement actions.

Offering his own reaction on X, Kraken co-CEO Dave Ripley said the arbitration case represented only part of what happened during that period. Ripley described the $22 million award as compensation for financial harm that he said resulted from a coordinated campaign against the crypto industry.

Meanwhile, U.S. regulators have continued reviewing banking oversight tied to digital assets. In February, the Federal Reserve requested public feedback on a proposal to remove “reputation risk” from bank supervision after its 2025 directive instructing supervisors to stop pressuring banks to close customer accounts over reputational concerns. Critics of the previous framework argued the proposal could help end practices associated with Operation Chokepoint 2.0.

Kraken expands products while IPO plans continue

Even as the legal dispute moves through the Delaware court, Kraken has continued adding new institutional and trading products.

As previously reported by crypto.news, the exchange recently began allowing eligible users outside the United States to use selected tokenized stocks and exchange-traded funds as collateral for futures and margin trading on Kraken Pro.

The launch covers 10 xStocks assets, including SPYx, QQQx, AAPLx, GOOGLx, TSLAx, NVDAx, HOODx, MSTRx, GLDx and CRCLx, allowing traders to back leveraged crypto positions without selling those holdings.

The collateral initiative follows other recent product launches. In May, Payward partnered with Franklin Templeton to introduce tokenized money market products for collateral and cash management on Kraken. A month later, Kraken and Maple launched an institutional crypto lending structure using a bankruptcy-remote vehicle for crypto-backed loans.

Founded in 2011, Kraken has also been preparing for a public listing. The company disclosed in November 2025 that it had confidentially submitted a draft Form S-1 registration statement to the U.S. Securities and Exchange Commission.

However, reports published in May said the IPO may be delayed until 2027 because of weaker crypto market conditions and ongoing cost-cutting efforts.

Nigel Farage has resigned as a Member of Parliament after confirming he will seek re-election in a by-election while facing scrutiny over multimillion-dollar gifts from figures linked to the crypto industry.

Summary

- Nigel Farage has resigned as MP and will contest a Clacton by-election while parliamentary investigations continue.

- Farage denies wrongdoing over multimillion-dollar gifts linked to crypto figures Christopher Harborne and George Cottrell.

- The controversy comes as crypto-related political funding faces growing scrutiny in both the UK and the US.

According to statements Farage made during an X livestream on Tuesday, the Reform UK leader stepped down as the MP for Clacton so local voters could decide whether he should continue representing the constituency while parliamentary investigations into his financial declarations continue.

Farage said he had “done nothing wrong” and insisted he had not broken any laws or misused public money. He also confirmed that the UK’s parliamentary standards commissioner is investigating two separate matters related to gifts he received from crypto billionaire Christopher Harborne and George Cottrell, who has a previous fraud conviction and has been linked to a crypto casino.

Describing the donations as unconditional gifts, Farage said funds provided by Harborne would be used to cover his personal security costs, citing threats and attacks against him. He added that standing again in a by-election would allow Clacton voters to judge his actions directly rather than leaving the matter to political opponents.

Why has Nigel Farage resigned?

Speaking during the livestream, Farage accused established politicians of using what he described as “foul means” against him, saying the investigations had prompted his decision to resign and contest the seat again.

The controversy follows media reports that Farage personally received millions of dollars in donations and gifts from Harborne and Cottrell. Earlier reports in May stated that Harborne had given Farage a gift valued at about $6.7 million.

At the time, Farage described the payment as a reward for his role in campaigning for Brexit, the 2016 referendum that led to the United Kingdom leaving the European Union.

The London Standard reported that the timetable for the Clacton by-election remains uncertain because several procedural steps must be completed before voters return to the polls. According to the publication, the process could take weeks or even months. Farage originally won the Clacton seat in the July 2024 general election with 46.2% of the vote, defeating both Conservative and Labour candidates.

Long before the latest controversy emerged, Farage had built relationships within the crypto sector. He appeared as a speaker at the Bitcoin 2025 conference in Las Vegas and has disclosed that he is an investor in Stack, a London-listed Bitcoin treasury company.

Crypto money remains under political scrutiny

While the UK investigations continue, political funding tied to the crypto industry has also remained under scrutiny in the United States ahead of the November 2026 midterm elections.

According to a June report from consumer advocacy group Public Citizen, crypto companies and industry figures had spent roughly $189 million during the 2026 election cycle to support candidates viewed as favorable to digital asset policies.

Separately, U.S. President Donald Trump has continued to face criticism from several lawmakers over his 2025 financial disclosures. Those filings reported approximately $1.4 billion in earnings connected to crypto-related ventures, adding to ongoing debate over the industry’s growing financial influence in politics on both sides of the Atlantic.

New Hampshire’s Executive Council is holding a public hearing this Wednesday on $100 million in bonds financing private Bitcoin (BTC) purchases. Approval would clear the last governmental hurdle for the first municipal bond collateralized by Bitcoin.

However, Bitcoin’s winter drawdown cut its price by more than half. This deal enters mandatory liquidation after a roughly 12.5% slide. That gap, rather than the vote, may decide how the experiment ends.

New Hampshire Bitcoin Bond Takes the Conduit Route

The New Hampshire Business Finance Authority (BFA) requested the hearing under state statute RSA 162-I. Executive Director James Key-Wallace asked Governor Kelly Ayotte and the five-member council to determine whether the project is feasible and beneficial.

If approved, the BFA will issue taxable conduit revenue bonds, meaning the state will facilitate the loan but never borrow. It will lend the proceeds to NH CleanSpark Borrower Trust 2026-1, tied to CleanSpark, the Nevada-based miner still absorbing steep first-quarter losses. Jefferies will underwrite the deal, which Wave Digital Assets designed.

Repayment falls entirely on the borrower, so taxpayers carry no direct exposure. Meanwhile, the BFA earns its fee in Bitcoin, seeding a planned Bitcoin Economic Development Fund.

House Bill 302, signed in May 2025, made New Hampshire the first state to let its treasurer hold digital assets. In contrast, the federal Strategic Bitcoin Reserve remains tangled in legal questions.

Why the 140% Liquidation Trigger Worries Researchers

Moody’s assigned the bonds a provisional Ba2 rating on March 31. That mark sits two notches below investment grade, in the tier commonly called junk bonds. The three-year notes rely on BitGo Trust Company to custody the collateral in cold storage and execute any liquidation.

CleanSpark must post $160 million in Bitcoin against $100 million of obligations, a 160% coverage cushion. If that ratio falls to 140%, mandatory liquidation and early redemption follow. All else equal, a 12.5% price drop erases that buffer.

Recent history clears that bar easily. Bitcoin peaked above $126,000 in October 2025, then slid to just above $60,000 by February. Meanwhile, record miner BTC sales showed how fast the industry converts coins to cash under stress.

David Krause, an emeritus finance professor at Marquette University, modeled the structure. He found that historical Bitcoin swings were highly likely to trigger the trigger, the Boston Globe reported.

“While the bond may serve as a proof of concept for integrating digital assets into structured finance, it is not well suited as a general-purpose public finance tool.”

Wednesday’s outcome appears predictable, since the BFA board approved the framework on November 18.

New York City rejected a similar pitch over tax law concerns, per law professor Tonya Evans.

Therefore, the harder test comes in the market, where investors must price junk-rated bonds against Bitcoin’s near-term price outlook.

The post New Hampshire Bitcoin Bond Nears Final Vote, But There is a Catch appeared first on BeInCrypto.

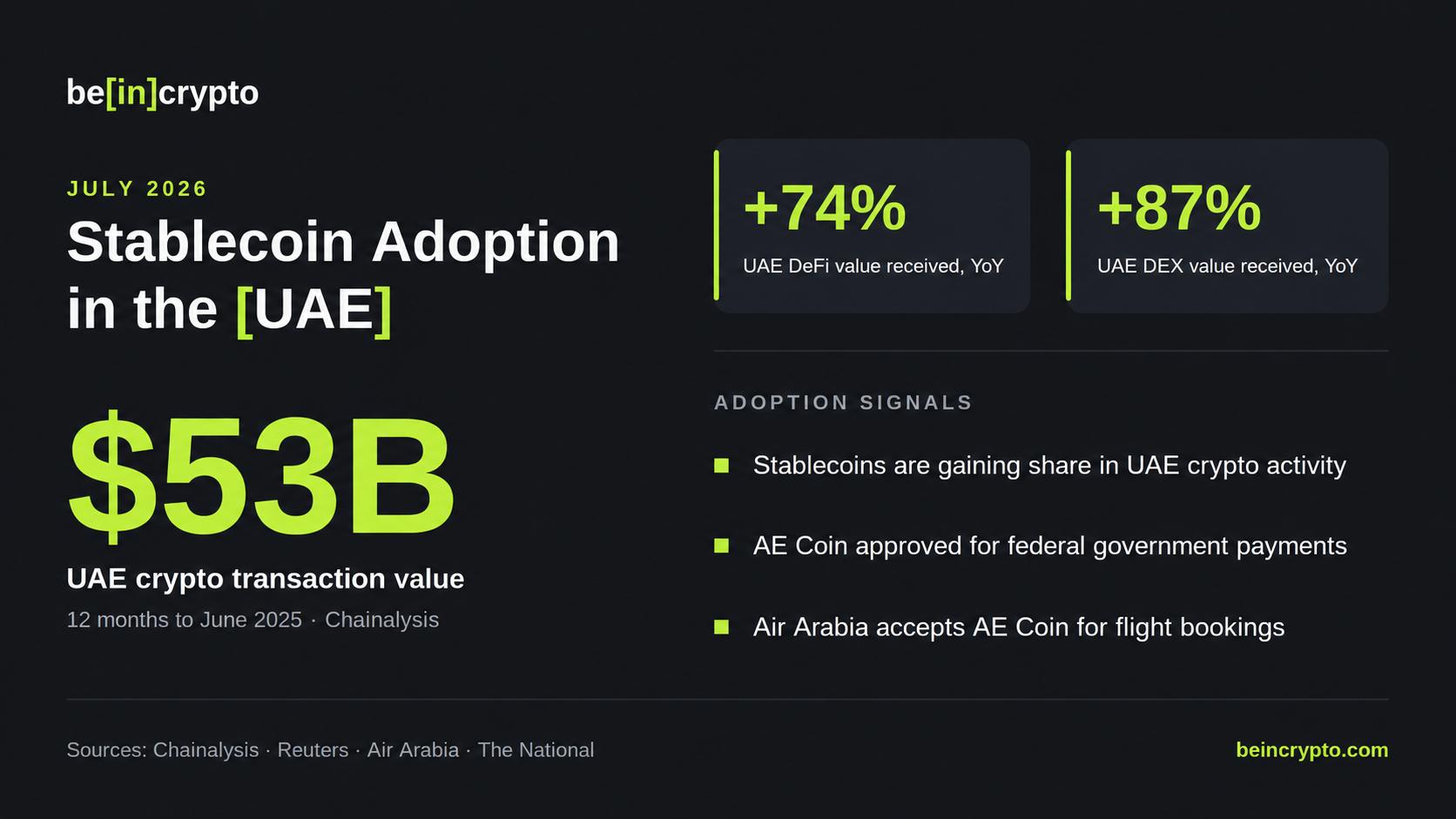

Stablecoins are, undoubtedly, the main operating assets in digital finance. Visa’s stablecoin analytics dashboard showed more than $51 trillion in total transaction volume over the past 12 months.

Meanwhile, TRM Labs estimated stablecoins at 30% of all on-chain crypto transaction volume in 2025. This one asset category carried almost one-third of tracked crypto value movement, while Bitcoin and all other altcoins together accounted for the remaining share.

Almost every blockchain activity today runs through these dollar-pegged assets, whether it’s trading, treasury movement, or cross-border settlement.

So, stablecoins are arguably the most explosive asset class in terms of growth. What’s the next phase? As with any financial product, its adoption. And that can only happen through local-currency settlement, regulated access, and payment use cases tied to national economies.

In the UAE, this is already happening.

UAE’s Financial Future is Running on Stablecoins

Chainalysis estimated more than $56 billion in crypto value received by the country during its 2024 to 2025 reporting window, up 33% year over year, with institutional transfers driving a large share of activity and merchant services expanding across smaller retail transaction sizes.

On July 3, 2026, DDSC, the UAE dirham-backed stablecoin developed by International Holding Company, First Abu Dhabi Bank, and Sirius International Holding, received approval from the Central Bank of the UAE to partner with selected exchange platforms regulated by Dubai’s Virtual Assets Regulatory Authority.

The approval gives DDSC a regulated route from institutional settlement into wider market access, allowing users to access, buy, and redeem a dirham-backed stablecoin through compliant exchange channels.

A Dirham Stablecoin for a Dollar-Dominated Market

Most stablecoin liquidity today remains tied to the US dollar. This gives global crypto markets deep liquidity and a familiar settlement currency, while domestic payment use cases still depend on conversion, exchange access, and banking relationships.

DDSC brings a local-currency option into the UAE’s own monetary environment. Pegged 1:1 to the UAE dirham and settled on ADI Chain, the token gives users a digital asset denominated in AED instead of forcing local commerce into dollar units.

This distinction is important for payment adoption because UAE shoppers, merchants, suppliers, and treasury teams all price everyday obligations in dirhams.

A stable asset in AED can keep pricing and settlement aligned while adding blockchain settlement speed, programmable payments, and 24/7 availability.

The UAE has already built much of the regulatory base around this category:

- The Central Bank’s Payment Token Services Regulation created a framework for stablecoin-related services, including issuance, conversion, custody and transfer.

- VARA maintains a public register of licensed Virtual Asset Service Providers in Dubai, including platforms authorized for exchange services.

DDSC connects these two regulatory channels. Central Bank approval covers the payment-token side, while access through selected VARA-regulated platforms gives users a familiar exchange route into the asset.

From Treasury Flows to Everyday Payments

DDSC entered the market with an institutional focus. Since launch, IHC says it has processed more than AED 150 million in transactions. In May 2026, IHC executed an AED 110 million DDSC transaction on ADI Chain, presented as one of the region’s largest disclosed stablecoin transactions.

DDSC is more than able to support high-value settlement. The new approval, therefore, adds distribution, giving individuals, merchants, and businesses a route to acquire and redeem the asset through regulated exchange platforms.

DDSC is left with a more complete adoption path. Large transactions can prove settlement capacity, while exchange availability can bring the asset into daily commercial use. The first phase demonstrated settlement readiness, and the next phase focuses on availability through licensed venues.

VARA-Regulated Platforms and Compliance Control

The approval applies to selected exchange platforms regulated by VARA, giving DDSC a controlled rollout through licensed channels and keeping access aligned with the UAE’s compliance framework.

For context, VARA oversees virtual asset activity in and from Dubai, excluding the Dubai International Financial Centre. Its public register lists licensed Virtual Asset Service Providers and the activities each provider is authorized to offer, including exchange services, broker-dealer services, custody, lending and investment management.

Indeed, stablecoin payments touch redemption confidence, merchant settlement, AML controls, custody, user access, and financial institution requirements. Exchange access through regulated platforms helps combine these requirements within a market structure users already understand.

DDSC’s rollout also shows how the UAE is separating regulated payment tokens from general crypto assets. Bitcoin, Ethereum, and volatile tokens continue to serve trading and investment use cases, while stablecoins such as DDSC are designed around payment value, redemption, and settlement.

This gives businesses a more suitable instrument for pricing, invoices, supplier transfers and customer payments.

A View Toward Merchant and Business Payments

IHC said the stablecoin can support everyday payments once available through selected regulated platforms, including shoppers paying merchants, businesses settling with suppliers and transfers between people.

Retail customers want fast payments, merchants want predictable settlement, and businesses want lower operational friction across invoices, treasury, and cross-border counterparties. There is no doubt that stablecoins can support these flows when they combine price stability, reliable redemption, and regulatory acceptance.

DDSC’s AED designation gives it a local advantage. A UAE merchant accepting a dollar stablecoin still faces accounting and FX conversion work. A dirham-backed token fits local pricing more naturally, while on-chain settlement can reduce delays linked to banking hours and intermediary processing.

A Local Currency Asset for the UAE Digital Economy

The UAE has spent years building a regulated digital asset environment across Abu Dhabi, Dubai and federal authorities. DDSC adds a local-currency payment asset to this environment, backed by major UAE institutions and aligned with the Central Bank’s payment-token framework.

DDSC’s growth ultimately depends on platform availability, merchant acceptance, redemption experience and business integration.

Even so, its Central Bank approval to partner with selected VARA-regulated exchange platforms brings the UAE dirham further into on-chain finance and gives the country’s digital asset market a regulated payment token built for domestic use and future regional settlement.

The post DDSC Brings Regulated Dirham Stablecoin to UAE Exchanges appeared first on BeInCrypto.

Crypto World

Rezolve Ai (RZLV) Stock Dips as Company Unveils Auditable AI for Enhanced Commerce Transparency

Key Highlights

- RZLV declined 1.34% following the introduction of Auditable AI technology.

- The new platform feature provides clear explanations for product recommendations.

- Rezolve targets enhanced enterprise trust in AI-powered commerce systems.

- The solution offers visibility into customer data and operational business logic.

- Company research indicates a 3.7x enhancement in transparency metrics.

Resolve AI PLC (RZLV) closed at $2.7328, declining 1.34% after pulling back from intraday highs to settle near the day’s lower range. The organization unveiled a new AI-driven feature designed to enhance transparency within commerce technology. This development extends its enterprise offerings and seeks to bolster trust in AI-powered product suggestions.

Platform expansion introduces transparent recommendation engine for enterprise users

Rezolve Ai unveiled Auditable AI as an integrated component of its enterprise commerce infrastructure. This innovation clarifies each product suggestion by referencing shopper preferences, transaction histories, product specifications, and operational guidelines. Through this approach, companies gain enhanced understanding of how recommendation algorithms arrive at specific conclusions.

The organization developed this solution to overcome transparency obstacles that have historically hindered enterprise AI implementation. Numerous current AI frameworks produce suggestions without revealing underlying logic. In response, this new functionality delivers human-readable explanations accessible to both businesses and end users.

Rezolve emphasized that this feature bolsters enterprise trust while encouraging wider commercial integration. The system additionally provides organizations with improved visibility throughout recommendation workflows during consumer engagements. As such, merchants can more effectively verify results and strengthen internal governance throughout digital commerce channels.

Enhanced platform capabilities reinforce commitment to reliable AI infrastructure

This recent introduction continues Rezolve’s ongoing platform enhancements centered on enterprise dependability. The organization previously tackled recommendation precision through specialized architecture that minimized erroneous AI outputs. Subsequently, it broadened supervision functionalities by launching monitoring solutions for autonomous AI behaviors.

Through this latest enhancement, Rezolve now delivers precision, responsibility, and clarity within a consolidated enterprise system. This comprehensive methodology supports organizations pursuing explainable artificial intelligence for business applications. Furthermore, the infrastructure aims to enhance confidence without compromising operational performance.

The organization also engineered the framework to function across various artificial intelligence architectures. Accordingly, enterprises can uphold uniform transparency benchmarks while deploying different AI technologies. This adaptability accommodates businesses managing varied technology ecosystems throughout retail and commerce operations.

Supporting studies demonstrate commercial advantages and wider sector applicability

Rezolve indicated that transparent recommendations can enhance consumer confidence throughout buying journeys. Shoppers can comprehend recommendation rationale through explanations derived from their documented preferences and prior behavior. Subsequently, retailers may deepen customer relationships while minimizing uncertainty during transactions.

The infrastructure also detects ambiguous customer signals before finalizing recommendation workflows. Rather than producing vague suggestions, the framework solicits supplementary information when required. This approach enables businesses to obtain more dependable recommendation results while minimizing unsuitable product pairings.

Based on company-sponsored studies, the technology achieved a 3.7-fold enhancement in transparency relative to traditional large language model frameworks. The supporting investigation also earned acceptance for presentation at the International Conference on Social Robotics 2026 in London. Concurrently, Rezolve intends to incorporate this technology throughout its Brain Suite platform as part of its ongoing enterprise commerce initiative.

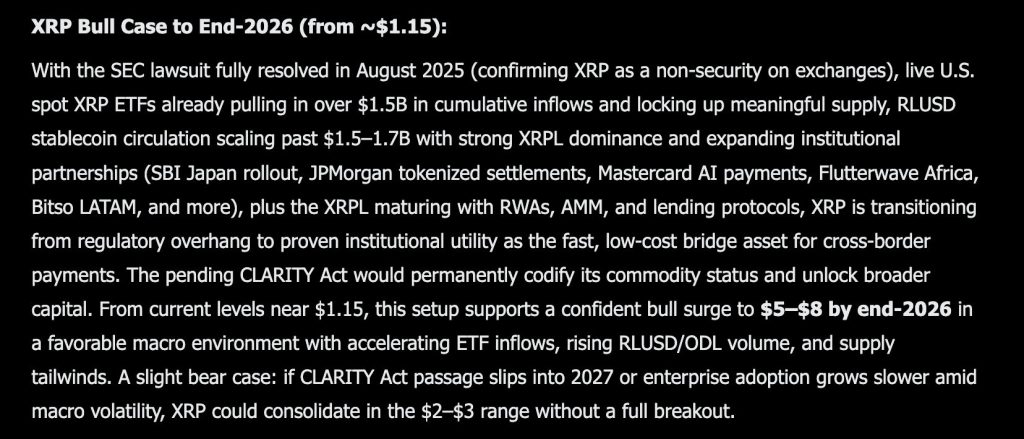

Elon Musk Grok AI just published what might be the most partnership-heavy XRP price prediction in this entire series. The model predicts $5 to $8 by the end of 2026, a 4 to 7 times return from where XRP sits today.

The bull case reads like a who’s who of global finance quietly building on the XRP Ledger while the price stays depressed. XRP trades near $1.15 today, and the thesis rests on the SEC lawsuit being fully resolved in August 2025, formally confirming XRP as a non-security on exchanges and removing the single biggest legal cloud that has held back serious institutional money for years.

Live US spot XRP ETFs have already pulled in over $1.5 billion in cumulative inflows and are actively locking up meaningful supply.

RLUSD stablecoin circulation has scaled past $1.5 to $1.7 billion with strong XRPL dominance. The partnership list is genuinely impressive by any measure.

SBI Japan is rolling out RLUSD, JPMorgan is using the XRPL for tokenized settlements, Mastercard named Ripple a partner in its AI payments network, Flutterwave is covering Africa, and Bitso is handling Latin America.

The XRPL itself keeps maturing with real world assets, automated market makers, and lending protocols all going live. Together the model frames XRP as completing a transition from regulatory overhang to proven institutional utility as the fast, low cost bridge asset for cross border payments.

The pending CLARITY Act would permanently codify its commodity status and unlock even broader institutional capital on top of everything already in motion. In a favorable macro environment with accelerating ETF inflows, rising RLUSD and on demand liquidity volume, and supply tailwinds from ETF accumulation, the model calls that $5 to $8 range a confident bull surge target.

The bear case is relatively contained. If CLARITY Act passage slips into 2027 or enterprise adoption grows slower than expected amid macro volatility, XRP could consolidate between $2 and $3 without achieving a full breakout. That would still represent a meaningful return from current levels, which tells you how skewed the model views the risk reward at $1.15.

XRP Price Prediction: XRP Finally Lifts Off The $1.00 Floor After Months Of Testing It

The daily chart shows XRP at $1.15532 after a long decline from highs above $3.65 set back in early August of last year. That entire move lower has been one extended downtrend, interrupted by a brief bounce toward $2.40 in November before sellers resumed complete control.

The most recent leg of this decline pushed XRP below $1.00 multiple times in June before buyers finally stepped in with enough conviction to push price back above that level and hold it.

That recovery off the $1.00 floor is the most meaningful chart development in months, given how many times that level was tested and how significant it is psychologically for an asset that spent years trying to sustain above $1.00 during the pre ETF era.

Resistance sits first near $1.20, the level price approached on today’s candle high of $1.16 and has not yet cleanly cleared, then a heavier ceiling near $1.60 where multiple rejections accumulated earlier this year.

Support now holds at $1.00, the exact floor that just got defended after several tests. The broader structure still shows a series of lower highs stretching back to August, so no confirmed reversal has appeared on this chart yet despite the encouraging bounce.

Momentum on the daily candles looks more constructive than at any point in the past several months, with larger green candles showing up more frequently and the $1.00 level holding on multiple tests rather than giving way.

If XRP can close convincingly above $1.20 and sustain that level through the coming sessions, the institutional accumulation story Grok is describing finally starts to show up in the price action rather than just the fundamentals.

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

Discover: The best crypto to diversify your portfolio with

Here is What Grok AI Predicts For LiquidChain Near Future, Very Bullish

Sitting at resistance waiting for a breakout is not positioning. It is standing in line.

Bitcoin, Ethereum, and XRP have been pressing against the same ceilings for weeks. The catalyst that unlocks the next leg is perpetually one data print away.

The institutional inflows are perpetually next quarter. Every large-cap trader waiting for a breakout is waiting on a decision that belongs to someone else’s balance sheet.

Early-stage infrastructure plays by completely different rules, Copilot AI predicts. Capital that would vanish as statistical noise at Bitcoin’s scale moves a small undiscovered project by multiples.

The asymmetric return lives in one place only: the gap between what something is genuinely worth and what the market currently thinks it is worth. That gap exists because the project has not been found yet. The moment it gets found, the gap is gone.

Cross-chain fragmentation has been extracting value from DeFi participants since the first bridge went live and nobody has eliminated it. Bitcoin, Ethereum, and Solana were engineered as independent systems with no shared architecture and no intent to interoperate.

Every transaction that crosses those boundaries pays the price of that design in fees, slippage, and execution failures. Bridges were supposed to be the solution. They became the mechanism through which the problem collects its fee.

LiquidChain eliminates the fee entirely. Three networks inside a single execution layer. One deployment reaches all of them. No cross-chain tax on any interaction anywhere.

Grok AI flagged it as worth watching. The presale is at $0.01454 with just over $860,000 raised.

Execution is unproven. Adoption is unknown. Established assets offer a predictable ride toward a ceiling that is already fully visible. LiquidChain is an entry point that disappears once the market finds it.

The post Elon Musk Grok AI Predicts Incredible XRP Price Target by End of 2026 appeared first on Cryptonews.

An anonymous wallet spent $4.4 million buying BONK tokens over two days, then used that stash to push through a governance vote that allowed it to drain $21.2 million from the BonkDAO treasury.

The incident, which saw the attacker walk away with a $16.8 million profit, has split the crypto community between those calling it a theft and those insisting the DAO did exactly what it was built to do.

How the Vote Went Through

According to blockchain analytics platform Lookonchain, preparations for the theft started on June 30 when the attacker filed a proposal asking BonkDAO to move 4.426 trillion BONK, worth about $21.2 million, to a wallet they controlled. To pass, the proposal had to be supported by at least 1% of the BONK supply, which, per data from CoinGecko, stands at just under 88 trillion tokens.

Then, from around July 4, they bought 882.285 billion BONK on Bybit and Binance, an amount that was just enough to clear the 1% requirement (879.95 billion) to make a quorum that could vote on the proposal they’d made at the end of June. They then proceeded to vote “yes” with all 882.285 billion BONK, passing the proposal, after which 4.426 trillion tokens were transferred to their wallet.

Another company that follows on-chain movements, Chainalysis, corroborated Lookonchain’s account of the incident, saying the attacker acquired their tokens between July 4 and 5, buying some from the mainstream exchanges and borrowing others through DeFi platforms.

About 9 hours after voting their way to the $21 million stash, Chainalysis says the attacker sent $188,000 to OKX (Peckshield puts that figure at $148,000) while putting the rest in a new DAO, “BONK 2.0,” that they created to govern the stolen funds. According to the analytics firm, the new DAO is controlled by the malicious voter, the exploiter wallet, and a third wallet said to have financial ties to the voter wallet.

BonkDAO confirmed the treasury loss in a statement posted on X, saying it had identified the exchange wallets that had been used to acquire the voting tokens before the proposal succeeded and that it had notified law enforcement while also coordinating with exchanges, bridges, and the Solana Foundation to “manage the situation.”

Following news of the theft, the BONK token lost some of its value, with CoinGecko showing it trading around $0.00000438 at the time of writing, a 7.4% drop in 24 hours but still up nearly 5% on the week.

A Working DAO or Fraud?

The event continues a streak reported recently by CryptoRank that has seen DeFi platforms lose nearly $1 billion to bad actors so far this year.

But not everyone agrees that a crime took place, including World Liberty Financial advisor Ogle, who questioned why law enforcement had become involved in what looked like a normal DAO function.

“Someone legitimately bought a lot of tokens, proposed a DAO vote, the vote passed with almost no opposition, and the proposal was executed,” they wrote on X.

The crypto maxi later added that reports claiming the voting website was inaccessible during the voting period, if true, would raise separate concerns but did not necessarily make the on-chain vote illegal.

However, others disagreed. Ripple CTO Emeritus David Schwartz argued that using voting control over a shared treasury for personal gain could amount to fraud because governance participants owe a fiduciary duty to other stakeholders. Further, he stated that BonkDAO’s lack of a formal legal wrapper could expose participants to partnership-style liabilities in some jurisdictions.

The post Was It a Hack or Governance? BONK’s $21M Treasury Vote Divides Crypto appeared first on CryptoPotato.

Charlize Theron Wears Nothing But Diamonds Ahead Of Premiere

REVEALED: Princess of Wales close to the high drama as exhausted hiker was rescued on Ben Nevis

Nasdaq sinks as AI worries hit chipmakers

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: High Hopes

-

NewsBeat3 days ago

NewsBeat3 days agoTaylor Swift and Travis Kelce wedding staffer hilariously struggles to keep her cool while checking in megastars

-

Fashion1 day ago

Fashion1 day agoOpen Thread: What Great Books Have You Read Recently?

-

Politics4 days ago

Politics4 days agoThe House | “Reframing the debate from a binary discussion of winners and losers”: Yuan Yang reviews ‘We Are Not Machines’

-

Crypto World6 days ago

Crypto World6 days agoAirdrop Registration Becomes Key Focus For Remittix As RTX Launch Updates Approach

-

Crypto World4 days ago

Crypto World4 days agoStandard Chartered Secures MiCA License as ESMA Adds 37 New Crypto Firms

-

Business1 day ago

Business1 day agoAXT Shares Jump Nearly 14% as Semiconductor Materials Maker Rebounds on AI-Linked Indium Phosphide Demand

-

Sports6 days ago

Sports6 days agoBroncos roster: OL Ben Powers (No. 74) entering final year of contract

-

Crypto World6 days ago

Crypto World6 days agoBinance stock trading tops $1B in first month after launch

-

NewsBeat7 days ago

NewsBeat7 days agoPresenter Caroline Flack’s brother Paul Flack dies aged 55

-

Crypto World6 days ago

Crypto World6 days agoAlibaba-affiliate Ant Group enters the humanoid robot market with 12 deals

-

Crypto World1 day ago

SK hynix (000660.KS) Stock Dips as $28B Nasdaq ADR Offering Drives AI Memory Expansion

-

Crypto World2 days ago

Crypto World2 days agoSouth Africa proposes crypto tax guidance under existing rules

-

News Videos1 day ago

News Videos1 day agoBest Time to Enter Small Caps Right Now? Another Bull Run? | Financially Free

-

Tech2 days ago

Tech2 days agoLenovo laptops are now shipping with YMTC SSDs, a sign of Chinese NAND entering the mainstream

-

News Videos18 hours ago

News Videos18 hours agoWhats Hidden Inside This Cash Register? #treasure #reselling #money

-

Business6 days ago

Business6 days agoMeta Platforms Stock Jumps 7% Today as Bloomberg Reports Company Plans to Enter the Cloud Business

-

NewsBeat6 days ago

NewsBeat6 days agoNew exhibition reflects five decades of movement between island of Ireland and GB

-

Business5 days ago

Business5 days agoWhat a 10 Percent Drop Means for Buyers, Sellers and Renters

-

Crypto World5 days ago

Crypto World5 days agoBinance Re-Enters Philippines As EU MiCA Rules Restrict Access

You must be logged in to post a comment Login