Crypto World

BeInCrypto Institutional Research: 10 Enterprise Blockchain Implementations Powering Production-Scale Finance

Best Institutional Enterprise Blockchain Implementation recognises named deployments that move real money or assets on distributed-ledger infrastructure, rather than the broader company or the underlying blockchain.

This category is a part of the BeInCrypto Institutional 100 awards. It sits under Pillar 6: Tokenization & Enterprise Blockchain. The 10 implementations below are listed alphabetically and are not ranked. A shortlist will be named in May 2026, with the winner announced at Proof of Talk in Paris on June 2–3, 2026.

Key Facts

- Long list: 10 production deployments across settlement, tokenized deposits, digital bonds, regulated stablecoins, capital markets infrastructure, cross-border interoperability, and institutional custody

- Initial pool: More than 25 enterprise blockchain deployments screened; 10 advanced to the long list

- Order: Listed alphabetically, not ranked

- Scoring: 30% quantitative data · 50% Expert Council · 20% disclosed company data

- Criteria assessed: Business impact and ROI, deployment scale, technical sophistication, innovation, replicability, stakeholder breadth, sustainability

- Boundary scope: This category evaluates the implementation itself, not the underlying chain, DLT framework, or parent company’s broader digital asset strategy

| Implementation / Firm | HQ & Listing | Reach | Representative Work |

|---|---|---|---|

| BNY Mellon Digital Asset Platform | New York, USA NYSE: BK |

Institutional digital asset stack within BNY Mellon’s $55.8T AUC/A platform BTC and ETH custody live since 2022 with Fireblocks integration |

IBIT primary cash custodian and administrator since spot Bitcoin ETF launch in Jan 2024 Co-custodian for Morgan Stanley Bitcoin Trust; tokenized MMF platform with Goldman Sachs live since Sep 2025 |

| Broadridge Distributed Ledger Repo (DLR) | New York, USA NYSE: BR |

More than $1T per month in tokenized repo transactions Production since 2018; built on Canton Network with DAML smart contracts |

UBS, Société Générale, HSBC, and BNY Mellon participate Privacy-preserving sponsored repo platform with JP Morgan Kinexys interoperability for collateral movement |

| Citi Token Services | New York, USA NYSE: C |

Citi tokenized deposit and trade finance platform Production since Sep 2023 across the US, Singapore, and the UK |

Tokenized deposit cross-border platform for institutional clients Smart-contract trade finance covering reverse factoring, automated FX, and programmable corporate liquidity |

| Goldman Sachs Digital Asset Platform (GS DAP) | New York, USA NYSE: GS |

Institutional digital bond platform built on Daml and Canton Spin-out as standalone industry utility announced with partners including BNY, BNP Paribas, Barclays, Microsoft, Tradeweb, Standard Chartered, and EquiLend |

European Investment Bank €100M digital bond issued in Nov 2022 HKMA Project Ensemble tokenized deposit pilots; interoperability alignment with Broadridge DLR through Daml and Canton |

| HSBC Orion | London / Hong Kong LSE / HKEX: HSBA |

HSBC permissioned blockchain digital bond issuance and tokenization platform Integrated with Hong Kong Central Moneymarkets Unit and active in multi-bank interoperability pilots |

Hong Kong government HK$6B digital green bond issued in Feb 2024 Digital bond platform connects Hong Kong CMU infrastructure with tokenized issuance rails |

| Kinexys by J.P. Morgan | New York, USA NYSE: JPM |

More than $5B daily transaction value as of Apr 2026 More than $3T cumulative volume since 2020; hundreds of institutional clients across five continents |

Kinexys Digital Payments processes tokenized deposits at production scale Kinexys Digital Assets includes intraday repo and Tokenized Collateral Network; Trimont settlement compressed from two days to near real time |

| Mastercard Multi-Token Network (MTN) | Purchase, New York / UK NYSE: MA |

$4.5B in stablecoin card spending in 2025 Crypto Partner Program launched in Mar 2026 with 85 participating companies |

Definitive agreement to acquire BVNK for up to $1.8B announced in Mar 2026 Integrated with JP Morgan Kinexys, Ondo OUSG, Fiserv Digital Asset Platform, USDG, PYUSD, USDC, and FIUSD |

| Société Générale FORGE (EURCV / USDCV) | Paris, France EPA: GLE |

EURCV about €105M circulating USDCV 26.3M tokens; multi-chain on Ethereum, Solana, and XRP Ledger |

First MiCA-compliant EUR stablecoin from a tier-one bank First US tokenized bond issuance on Canton Network; MetaMask integration via Consensys |

| SWIFT + Chainlink CCIP Cross-Border Interop | La Hulpe, Belgium Chainlink Labs: multi-location |

SWIFT network reaches 11,000+ banks Production interoperability launched in 2024 with partners including UBS, BNY Mellon, ANZ, Citi, and Lloyds |

UBS Asset Management Singapore tokenized fund cross-chain pilot MAS Project Guardian integration and Australia–EU interbank tokenized asset transfer corridor |

| Visa Tokenized Asset Platform (VTAP) | San Francisco, USA NYSE: V |

API-based bank-grade tokenization platform on Visa Developer Platform $7B annualized stablecoin settlement run rate; 15,000+ Visa-network banks accessible globally |

BBVA fiat-backed euro and dollar token on public Ethereum live in 2025 USDC settlement live in the US; Visa Direct stablecoin pilot; Circle Arc design role; Visa-Bridge card API program |

About This List

The BeInCrypto Institutional 100 — Best Institutional Enterprise Blockchain Implementation identifies production blockchain deployments in which regulated banks, payment networks, asset managers, and corporates have moved real money or real assets onto distributed ledger infrastructure.

Coverage includes tokenized deposit settlement, regulated bank stablecoins, B2B tokenization networks, institutional digital bond issuance, cross-border interoperability, DLT-based capital markets infrastructure, and institutional digital asset custody.

The category does not score the underlying chain or DLT framework. It also does not evaluate the parent institution’s broader digital asset adoption strategy. Pilots and proofs of concept are not eligible.

Methodology

This category is evaluated under Track B of the BeInCrypto Institutional 100 methodology: 30% quantitative metrics, 50% Expert Council scoring, and 20% disclosed company data.

Assessment spans seven criteria: business impact and ROI, deployment scale, technical sophistication, innovation, replicability, stakeholder breadth, and sustainability.

The disclosed data weighting reflects the limited public visibility into bank-operated tokenized deposit volumes, intra-platform settlement flows, permissioned network integrations, and named-counterparty programs.

Data was verified using regulatory registers, company annual reports, SEC EDGAR filings, audited platform disclosures, Chainlink CCIP and Canton Network transaction logs, RWA.xyz, DefiLlama, third-party rating agencies, private-market sources including PitchBook, Tracxn, and Crunchbase, and mainstream financial press.

The post BeInCrypto Institutional Research: 10 Enterprise Blockchain Implementations Powering Production-Scale Finance appeared first on BeInCrypto.

Kraken leads MiCA-regulated crypto exchanges in liquidity, according to DefiLlama’s MiCA exchange dashboard. The data cited by Wu Blockchain showed Kraken with $399.71 million in spot liquidity and $206.90 million in perpetual liquidity, placing it first in both categories.

Summary

- Kraken leads MiCA exchanges in liquidity, giving larger traders deeper order books across regulated European markets.

- Coinbase remains the closest rival, but DefiLlama data shows Kraken ahead across core liquidity metrics.

- MiCA licensing has changed Europe’s exchange race, making liquidity and market coverage key user factors.

DefiLlama’s live MiCA-regulated exchanges dashboard later showed Kraken still ahead, with more than $400 million in spot liquidity and more than $220 million in perpetual liquidity. The live figures may change because liquidity data moves with market depth, prices and exchange activity.

Coinbase ranked second in the figures cited by Wu Blockchain, with $305.23 million in spot liquidity and $167.39 million in perpetual liquidity. DefiLlama’s live page still placed Coinbase among the top regulated venues, but behind Kraken in the main liquidity table.

The gap matters for traders who need deeper order books. Higher liquidity can help reduce slippage when users place larger orders. It can also make an exchange more useful for active traders, market makers and institutional clients.

Coinbase and Crypto.com remain close rivals

Coinbase remains Kraken’s closest large rival among MiCA-regulated exchanges. The exchange has built its European base in Luxembourg, where it uses a MiCA license to serve users across the bloc.

crypto.news reported that Coinbase opened its Luxembourg MiCA hub as the EU deadline approached. The exchange said Luxembourg became its MiCA home for all 27 EU member states.

Crypto.com also ranked among the larger MiCA exchange venues by spot liquidity. Wu Blockchain cited $130.84 million in spot liquidity for Crypto.com, while DefiLlama’s live dashboard showed a similar range.

Bitstamp, Bybit, OKX, Gate and Backpack showed smaller liquidity pools. Bitstamp and Bybit stood near $50 million in spot liquidity in the cited data. OKX, Gate and Backpack were lower in spot liquidity, though Backpack and OKX had recorded perpetual liquidity.

Market coverage gives Kraken another lead

Kraken also leads the listed exchanges in market coverage. Wu Blockchain cited 1,704 markets for Kraken, followed by Coinbase with 1,074 markets and Crypto.com with 883 markets.

Market coverage shows how many trading pairs and products a platform supports. It does not guarantee better prices by itself, but it gives users more routes to trade assets under one regulated platform.

Gate, Bitstamp, Bybit, Backpack and OKX showed smaller market counts. The cited data listed Gate at 303 markets, Bitstamp at 298, Bybit at 133, Backpack at 125 and OKX at 65.

For European users, the mix of liquidity and market coverage may shape where activity moves after MiCA. Exchanges with deeper liquidity and more markets may attract users who left platforms without full authorization.

MiCA changes Europe’s exchange race

MiCA has changed how crypto exchanges operate in Europe. The framework requires crypto asset service providers to hold approval if they want to serve users under the bloc’s unified rules.

crypto.news reported that Kraken secured its MiCA license from the Central Bank of Ireland in June 2025. The license allows Kraken to offer regulated services across the European Economic Area.

Other exchanges also moved before the July 1 deadline. crypto.news reported that OKX expanded services across 28 EEA markets after securing MiCA approval through Malta.

The new data shows that licensing alone does not decide the race. Liquidity, trading products and market coverage now separate regulated exchanges from each other. Kraken currently leads those metrics among the listed MiCA platforms, while Coinbase, Crypto.com and other venues continue to compete for European users.

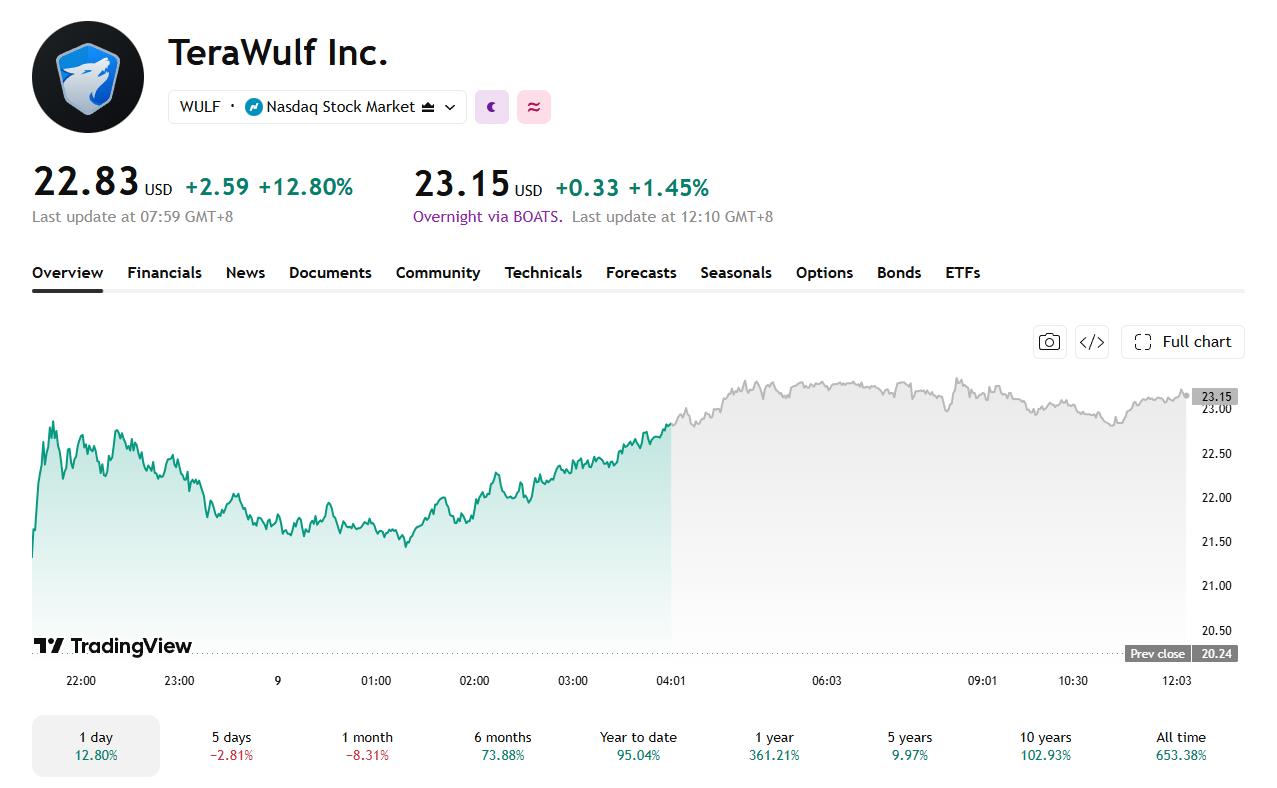

TeraWulf (WULF), IREN, and Hut 8 (HUT) all rallied yesterday, July 8, but Bitcoin’s price had nothing to do with it. Each saw their stock prices continue to rally on separate AI infrastructure news.

All three companies were in the top 16 best performing stocks for Wednesday, July 8 as investors reward their shift no matter what Bitcoin does on the day.

TeraWulf’s Anthropic Deal Set the Tone

TeraWulf stock rose more than 12.8% after signing a 20-year lease with Anthropic for a Kentucky data center. The site will support 401 megawatts of critical IT load, online by early 2028.

Analysts project roughly $19 billion in revenue over the lease’s term. Compass Point raised its price target to $40 from $28 after the deal and kept its buy rating.

CEO Paul Prager said the lease confirms the company’s AI infrastructure pivot and locks in a long-term revenue stream. TeraWulf also sold its stake in a Texas project, freeing cash for AI infrastructure investment elsewhere.

IREN and Hut 8 Caught the Same Bid

IREN climbed 8.01% after Freedom Capital Markets upgraded the stock to buy. The firm argued the recent pullback had created more upside than the market recognized. A Nvidia keynote appearance on July 8 also lifted sentiment around Bitcoin miner stocks.

Hut 8 jumped 9.69% in a single session after joining several Russell growth and small-cap indexes. Index inclusion suggests institutions are noticing the shift toward AI. The stock is up 383% over the past year.

The pattern is clear across the sector, visible in crypto stocks to watch beyond these three names. Miner valuations now track AI leasing headlines more closely than bitcoin mining stocks ever tracked Bitcoin’s price.

Whether that holds once AI capex slows is the question for the second half of 2026.

The post Bitcoin Miners Bet Big on AI Infrastructure and Win. TeraWulf, IREN, Hut 8 Surge appeared first on BeInCrypto.

Over three weeks ago, the Ripple team launched a new software update for the XRP Ledger (XRPL). Although the infrastructure upgrade (v3.2.0) has been running for close to a month now, not all of the network’s validator nodes have adopted it. In fact, more than half of the nodes are still running on the old version (v3.1.3) and are yet to come on board.

Data from XRPScan shows that only 43%, accounting for 357 out of 828 nodes, have upgraded to v3.2.0. On the other hand, 51%, that is 426 of the nodes, are still running on v3.1.3.

XRPL Launches New Upgrade

The latest infrastructure upgrade introduces several new features to the XRPL. One of them is the rebranding of the core server software from rippled to xrpld. The update also optimizes institutional usage by significantly reducing operating costs and implementing 30% to 40% lower memory usage across network nodes.

Additionally, v3.2.0 improves security, developer experience, and network efficiency, adding another confidence layer for builders. These features will add to the bug fixes and improvements to permissioned domains and vaults implemented during the v3.1.3 maintenance rollout in late May.

It is worth mentioning that despite the majority of nodes still operating on v3.1.3, roughly 61% of XRPL validators running on rippled versions have adopted the new upgrade. Also, 89% of the Unique Node List (UNL), which is the ledger’s trusted set of validators, are currently running on the software.

The XRPL needs 80% of the UNL to activate any network upgrades. With 31 out of 35 UNL validators having cleared the threshold, the network treats v3.2.0 as sufficiently updated. So, it is only a matter of time before other nodes jump on the bandwagon.

V3.2.0 Amendment Under Voting

In the meantime, the XRPL is trying to approve and implement security fixes associated with v3.2.0. The fixes, bundled in an amendment titled fixCleanup3_2_0, are yet to be approved, as it is still under voting on the XRPL.

The XRPL needs 28 out of 35 UNL votes to cross the threshold and approve the amendment; however, the network has gotten 17 so far. This means only 48.57% of trusted validators have voted so far.

If approved, fixCleanup3_2_0 will deploy fixes for single-asset vaults, lending protocol, multi-purpose tokens, permissioned domains, and permissioned decentralized exchanges.

The post Ripple Rolls Out New XRPL Upgrade, but Less Than Half of Nodes Have Upgraded appeared first on CryptoPotato.

Federal Reserve officials were split last month on whether to increase interest rates or keep them steady, with many seeing accelerating demand for artificial intelligence as a driver of inflation, according to meeting minutes released on Wednesday.

The minutes covered the first monetary policy meeting under Fed Chair Kevin Warsh. Many Federal Open Market Committee members said that “ongoing strong demand for AI infrastructure would likely sustain upward pressure on prices for technology products and electricity,” according to the minutes.

AI-related inflationary pressure, colloquially known as “chipflation,” stems from the rising cost of semiconductors used by data centers. This surge in demand, along with data center competition for energy, has pushed up consumer prices for a wide range of electronic goods, devices and power, and may continue as AI demand increases.

Higher inflation is generally bad news for risk assets such as crypto, as it results in lower liquidity and spending power and higher interest rates, making borrowing more expensive and cash investments more attractive.

Inflation will remain elevated in the near term

Participants anticipated that inflation would “remain elevated in the near term” but may decline as the Middle East conflict eases. However, they judged that the “risks to the inflation outlook were still tilted to the upside.”

AI growth remained a strong theme, both boosting economic growth and contributing to inflation at the same time.

“Most participants remarked that growth in economic activity that exceeded that of potential output, owing in part to strong AI business investment, could contribute to more persistent inflationary pressures.”

Related: Central bankers sound alarms over agentic AI finance risks

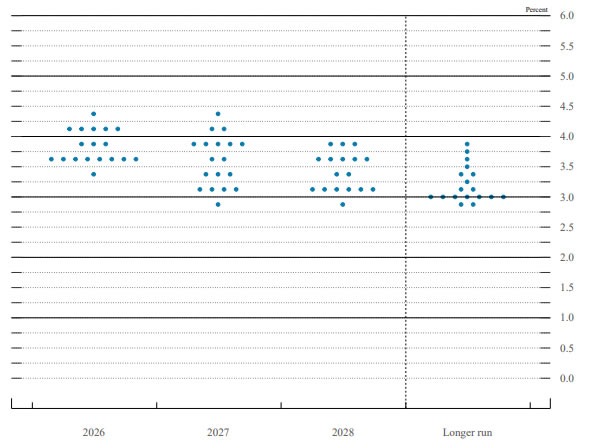

The Fed’s “dot plot” signals hikes, not cuts, with nine of 18 voting members projecting at least one rate hike before the end of 2026 and six expecting two 25-basis-point increases. The central bank’s PCE inflation projection for year-end also jumped from 2.7% to 3.6%.

A hawkish dot plot signals that interest rates are likely to stay higher for longer this year. Source: Federal Reserve

The Fed kept rates steady at 3.5% to 3.75% at its June meeting, while CME futures markets currently show a 70% probability that they will remain unchanged at the next meeting on July 29.

AI infra buildout driving higher inflation

Nick Ruck, director of LVRG Research, told Cointelegraph that the Fed’s recent meeting highlights how the massive AI infrastructure buildout is “driving higher inflation through surging demand for semiconductors, energy and data centers, even as it promises future productivity gains.”

“While this short-term pressure complicates monetary policy, it also underscores the need for innovative solutions in decentralized technologies to optimize resource allocation and ease bottlenecks in the digital economy,” he said.

Analysts said this week that crypto markets could benefit from any Fed intervention to backstop the booming US equity market in a downturn.

Features: The biggest blockchain upgrades still to come in 2026

XRP has slipped below a key short-term support near $1.10, with sellers regaining control as traders lock in profits after Ripple’s latest European regulatory win and macro risk sentiment weakens across global markets.

Summary

- XRP has dropped below key support near $1.10 as profit-taking and long liquidations push the token toward $1.

- A descending channel, weakening RSI, bearish MACD setup, and dense liquidation zones reinforce downside risks.

- Ripple’s MiCA license and $4 billion in XRPL tokenized RWAs highlight long-term adoption despite near-term weakness.

The token traded around $1.08 on Tuesday after falling from an intraday high near $1.18. The decline came shortly after Ripple secured a full Crypto-Asset Service Provider license from Luxembourg’s Commission de Surveillance du Secteur Financier under the European Union’s Markets in Crypto-Assets framework. Instead of extending the rally, the announcement triggered a classic sell-the-news reaction as traders booked gains following the regulatory milestone.

Fresh geopolitical tensions added pressure across risk assets. Reports of a tanker attack in the Strait of Hormuz, U.S. airstrikes on Iran, and the removal of Iranian oil sales waivers pushed crude oil prices more than 2.5% higher.

The move lifted Treasury yields and weighed on equities, particularly technology stocks, dragging major cryptocurrencies lower alongside traditional markets.

At the same time, derivatives positioning amplified the decline. CoinGlass liquidation data shows dense leverage clusters above $1.10 and another major concentration near $1.14, while the latest three-day liquidation heatmap now reveals comparatively thinner liquidity below the market.

As long positions were forced out during Tuesday’s decline, XRP quickly slid toward the next support zone around $1.08, leaving the psychological $1.00 level as the next major downside magnet if sellers remain in control.

A separate on-chain development has highlighted continued institutional interest in the XRP Ledger despite the token’s weak price action. According to crypto commentator Whale Factor, tokenized real-world assets on the network have surpassed $4 billion after standing near $150 million a year ago.

“The crypto as a toy narrative is dead. Tokenized RWAs on the XRP Ledger just smashed through the $4 BILLION mark,” Whale Factor wrote on X.

The growth underscores expanding enterprise adoption of the network, although investors have largely treated it as a long-term fundamental story rather than a catalyst for immediate token demand.

Technical breakdown has exposed the $1 psychological support

The daily chart shows XRP trading inside a descending channel that has capped every recovery attempt since May. The latest rejection occurred after the token failed to hold above the channel’s upper boundary before falling back toward the lower half of the pattern.

Momentum indicators have also weakened. The daily Relative Strength Index has slipped to around 42 after failing to reclaim the neutral 50 level, while the MACD histogram has begun printing smaller positive bars as the MACD line curls toward a bearish crossover. Together, those indicators suggest buying momentum has faded after last week’s rebound.

The Fibonacci retracement drawn from the May high to the June low also places XRP below the 78.6% retracement level near $1.13. Immediate support sits around $1.01-$1.02 near the channel floor, with a decisive break opening the door to a test of the psychological $1.00 level.

On the upside, bulls would first need to reclaim $1.13 before challenging resistance around $1.21, where the 61.8% Fibonacci level and previous supply zone converge.

The 4-hour chart presents a similar picture. Aroon Down has climbed to 100 while Aroon Up has retreated sharply, showing sellers currently dominate the short-term trend. Meanwhile, Chaikin Money Flow has remained only marginally above zero, suggesting capital inflows have weakened despite avoiding outright distribution.

Macro risks could extend losses while a recovery requires reclaiming $1.13

Muted institutional participation has added another headwind. Spot XRP ETF flows have remained largely flat over recent sessions, while uncertainty surrounding the timing of the U.S. CLARITY Act continues to delay a key regulatory catalyst that many investors view as important for broader institutional adoption.

Further weakness in global equity markets or another spike in energy prices could accelerate risk aversion and increase pressure on altcoins. A daily close below the $1.01-$1.02 support area would strengthen the bearish case for a move toward $1.00 and potentially below it.

The downside outlook would weaken if buyers reclaim the $1.13 resistance zone and push XRP back above the descending channel’s upper trendline. Such a move would force short sellers to reassess positions and could shift attention toward the $1.21 resistance area, where the next major supply cluster remains concentrated.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

DeFi analytics and portfolio tooling provider Zapper says it will shut down its website, mobile app, and API services on Aug. 3, bringing an end to a seven-year run as broader crypto activity cools and venture funding tightens.

In a post on X on Wednesday, Zapper CEO Seb Audet said the company concluded that an “orderly wind down is the best course of action.” Audet did not provide detailed reasoning, but in a follow-up response hinted that falling demand played a role, adding that “the market decides.”

Key takeaways

- Zapper will discontinue its website, mobile app, and API on Aug. 3, ending support for wallet tracking and DeFi analytics from that date.

- The shutdown joins several other crypto platforms that have paused operations this year as sentiment weakens and funding becomes harder to obtain.

- Zapper previously scaled to over 2 million monthly active users and processed more than $13 billion in transactions at its peak, according to Audet.

- VC capital appears to be concentrating even as total funding rises, with RootData data cited in the report showing deal counts declining over recent quarters.

- Zapper says it has faced setbacks, including a social engineering attack in April 2025 that briefly redirected users via a hijacked domain.

Zapper sets an Aug. 3 shutdown date

Zapper’s announcement makes it the latest DeFi-focused platform to exit amid a period of reduced activity across the sector. According to Audet, the company will close its public services—including its website, app, and API—on Aug. 3. The CEO framed the move as the result of evaluating multiple options before deciding on an orderly wind-down process.

In an additional comment, Audet pointed to market conditions without spelling out specific metrics or internal causes. “At the end of the day, the market decides,” he wrote, suggesting that revenue potential and usage demand were no longer sufficient to justify continued operation.

Why this matters to DeFi users and builders

Zapper’s tooling has served a practical niche in the DeFi stack: traders and liquidity providers used it to track token performance, monitor DeFi positions, and manage activity such as liquidity pools and yield farms. The platform also enabled wallet connections for position visibility and for discovering ecosystem updates, including information tied to upcoming token events like airdrops.

For users who rely on analytics and wallet-linked monitoring, a full service shutdown typically means losing an interface that consolidates balances, positions, and activity across protocols. Even if users can still access blockchain data directly, platforms like Zapper help translate those data into actionable dashboards. With the Aug. 3 cutoff, customers will need to migrate workflows to alternative analytics options or rebuild their own monitoring routines.

The impact may be broader for developers as well: Zapper’s API offering indicates it was used not only as a consumer product but also as an integration point for applications wanting to surface token and DeFi position information. When the API ends, integrators will need to adjust quickly to avoid broken data pipelines or dashboards.

A pattern of exits as sentiment and funding tighten

The Zapper shutdown comes alongside other crypto platform closures that have been linked, directly or indirectly, to softer demand and a tougher market for fundraising.

The report notes that Cardano-based analytics platform TapTools made a similar decision to shut down in June, while Bitcoin-focused DeFi platform Botanix followed about a week later, citing weak demand for Bitcoin DeFi.

Beyond DeFi analytics, several other categories have seen exits too. The article references SBI’s crypto unit, decentralized email service Dmail, and NFT marketplaces including Nifty Gateway and Rodeo as having sunset operations in 2026 amid a broader downturn in NFT activity. Separately, Cointelegraph also previously covered a wave of closures tied to reduced engagement and changing investor appetite.

The broader backdrop described in the report is that crypto sentiment has sunk toward near all-time lows, and that venture capital funding has become harder to secure. While the piece does not provide marketwide adoption numbers, it frames the exits as part of a larger contraction in both user appetite and the financing environment.

From seed funding to scaling—then setbacks and a funding squeeze

Zapper was founded in 2019 and built early momentum through success in Kyber’s DeFi Hackathon later that year, which helped it raise a $1.5 million seed round, according to the article. It later raised $15 million in a Series A funding round in May 2021 led by Framework Ventures, with participation from Mark Cuban and Coinbase Ventures, as well as Sound Ventures, which is associated with Ashton Kutcher.

At its peak, Audet said the team scaled the product to over 2 million monthly active users and processed more than $13 billion in transactions. The same figures underline why the shutdown is notable: Zapper was not a niche experiment but a widely used piece of DeFi infrastructure for tracking and management.

Still, Zapper’s journey included operational disruption. In April 2025, the platform suffered a social engineering attack in which attackers temporarily hijacked its domain and redirected users to a malicious page containing phishing traps. The incident would have raised ongoing risk management and user trust challenges even after any remediation.

On the financing side, the report cites RootData’s VC dashboard to argue that capital has become more concentrated despite an increase in aggregate funding. It states that crypto VC funding rose 57.6% year-on-year to $4.21 billion in the second quarter, while the number of deals has fallen nine times over the last 10 quarters, according to RootData.

That combination—more total dollars but fewer deals—can make it difficult for mid-stage companies to bridge the gap between growth and profitability, especially when usage depends on an overall market cycle. For platforms like Zapper that serve users whose behavior is often correlated with market activity, weaker demand can reduce subscription and integration leverage precisely when fundraising terms are less flexible.

What to watch after Zapper’s exit

With Aug. 3 as the shutdown date, users and integrators should focus on migrating wallet tracking, DeFi analytics, and any API-dependent workflows to alternatives before services go offline. The key remaining uncertainty is whether Zapper’s team will offer any transition support—such as data exports, migration guidance, or replacement guidance—and whether similar analytics and tooling providers will face accelerated consolidation as the funding environment continues to concentrate.

Palantir Technologies (PLTR) shares fell 1.6% to $132.22 on Wednesday, July 08 snapping a seven-day winning streak that had pushed the stock up 25%.

The stock surge hit the brakes after a report raised the prospect of Democratic lawmakers targeting the company’s government contracts.

A Rally Interrupted

The drop halted one of Palantir’s strongest short-term runs of the year. Shares had climbed from a June 25 low of $107.27 back above $134, before Wednesday’s reversal.

Even after the bounce, Palantir remains down 27% for 2026 and 37% below its November 2025 record close of $207.18, as investors continue to weigh AI valuations across software stocks.

The company’s record Q1 revenue surge earlier this year had briefly quieted some of those valuation concerns.

What Triggered the Selloff

D.A. Davidson analyst Gil Luria told Barron’s the reversal tracked a Financial Times report describing internal concern at Palantir over how Democratic lawmakers might respond to the company’s expanding role in government work, potentially threatening contracts that make up a large share of its revenue.

The scrutiny echoes broader questions raised in government contracts scrutiny tied to defense and data firms with deep Washington ties.

Palantir pushed back on the framing in a statement to Barron’s:

“For over twenty years, and across five administrations, Palantir has been proud to work with the U.S. government and its allies to strengthen national security and deliver public services effectively and efficiently. We will continue to work with Democrats and Republicans alike to support all Americans.”

A Bullish Backdrop Complicates the Picture

The political overhang lands just as Palantir’s near-term narrative had turned more favorable. Days earlier, the company unveiled a partnership with Nvidia to build sovereign AI models for government agencies, and D.A. Davidson upgraded the stock to Buy.

That contrast, a growing business facing fresh political risk, is likely to keep volatility elevated as Palantir’s next earnings report approaches.

The post Palantir Shares Slide on Fears Democrats Could Target Government Contracts appeared first on BeInCrypto.

Two projects have verified roughly 18 million humans each, by completely different methods, for the same prize: becoming the identity layer of an internet overrun by AI. Worldcoin scans irises with orbs and has Vercel, Zoom, and Tinder integrating its ID. Pi Network verified its users with documents and social trust and just opened the system for business. Both tokens are down catastrophically. Here is the honest comparison of who is positioned to win, and why the market believes neither.

Summary

- Pi Network and Worldcoin have each verified around 18 million users using different approaches to build proof of human identity for the AI era.

- Worldcoin leads in enterprise integrations while Pi Network is betting on its new PiVerify service to create real demand for its token.

- Both projects face the same challenge of turning verified users into sustainable revenue as their tokens remain far below previous highs.

The internet is filling up with things that are not people. By one widely circulated Fundstrat compilation, non-human accounts now generate about 75% of trading volume on Polymarket, 53% of web traffic, 47% of email, and 44% of US equity buy-side execution, and the AI agents behind those numbers are getting more convincing every quarter. In that world, the ability to cryptographically attest that an online actor is a real, unique human stops being a niche crypto experiment and becomes basic infrastructure, the kind of primitive that login systems, exchanges, dating apps, and payment rails all eventually need.

Two crypto projects have spent years and enormous resources building exactly that attestation, and by a strange coincidence they arrive in mid-2026 with almost identical headline numbers and opposite methods. Worldcoin, the Sam Altman-founded project now called World, has verified about 18 million humans by scanning their irises with a chrome device called the Orb, inside an app ecosystem claiming over 40 million users across 160 countries. Pi Network has verified more than 18 million of its users across 200-plus countries using a hybrid of document KYC, machine automation, and human validators drawn from its own community, and on June 28 it opened that system to outside businesses as a paid product called PiVerify. Both projects call the same trend their reason to exist. Both tokens have been demolished, WLD down roughly 80% over seven months at its trough and PI down about 96% from its peak to an all-time low this month.

That combination, identical scale, opposite architectures, shared narrative, mutual price collapse, makes the comparison worth doing properly. This piece sets the two systems side by side: how each verifies a human and what that method costs, who is actually integrating each ID today, how each converts verification into token demand, the privacy and regulatory exposure each carries, and the shared, unsolved problem that explains why the market currently prices both near despair.

Two answers to one question

The technical question both projects answer is called proof of personhood: how do you prove that an online account belongs to a real, unique, living human, without a central authority vouching for everyone? The two answers could not be more different.

Worldcoin’s answer is biometric. A user visits an Orb, a purpose-built imaging device that scans the iris and converts it into a cryptographic code confirming uniqueness, the premise being that irises cannot be duplicated or mass-produced the way documents, phone numbers, or social accounts can. The resulting World ID lives in the World App and can be presented to any integrated service as a zero-knowledge attestation, proving humanity and uniqueness without revealing identity. The strengths are real: biometric uniqueness is the hardest possible Sybil defense, one person physically cannot enroll twice, and the zero-knowledge design means integrating services learn nothing about who the user is. The weaknesses are equally structural. Orbs are hardware that must be manufactured, distributed, and staffed, making enrollment slow and geographically lumpy; iris collection has drawn regulatory bans and investigations in multiple jurisdictions; and the whole scheme depends on trusting the device and the entity that built it.

Pi’s answer is social and documentary. Its 18 million verifications come from an in-house KYC pipeline combining automated document checks with human validators recruited from the network itself, validators who have processed over 526 million verification tasks, layered on top of the trust graph produced by Security Circles, the small groups of three to five personally known people every user vouches for, the mechanism at the heart of Pi’s consensus design. The strengths mirror Worldcoin’s weaknesses: no hardware, near-zero marginal cost, enormous geographic reach including regions no Orb will visit for years, and a verification that carries actual identity, which is what regulated businesses performing KYC legally need. The weaknesses mirror back: documents can be forged and purchased at scale in ways irises cannot, human validators are themselves a trust assumption, and a social graph is only as Sybil-resistant as its weakest circles. Where World proves you are a unique human while hiding who you are, Pi proves who you are, which makes the two products less interchangeable than the shared narrative suggests: one is anonymous personhood, the other is identity.

The adoption scoreboard

Verification counts are inputs. The scoreboard that matters is who integrates each ID, because integrations are what convert a verified-human database into a business, and here the two projects are at visibly different stages.

Worldcoin’s integrations are live, external, and increasingly mainstream. World ID is being wired into Vercel’s agentic infrastructure, where the developer platform’s chief product officer frames verified digital identity as the way humans become first-class citizens of the internet again, and companies including Zoom, Tinder, Coinbase, Razer, Okta, Exa, and Browserbase are implementing proof-of-human standards using the World network. The strategic pivot announced by the World Foundation, providing identity checks for AI-agent platforms so that human verification gates agent execution, targets exactly the demand trend the Fundstrat numbers describe. None of this has rescued the token, but as evidence that external, non-crypto businesses will adopt a crypto-native identity layer, Worldcoin’s roster is the strongest that exists.

Pi’s integrations are, as of this month, an opening bid. PiVerify launched on June 28 as a KYC-and-identity service external businesses can buy, alongside Pi Sign-in, which lets third-party sites offer Pi accounts as a login, and SoloHost, which points the network’s 420,000-plus nodes at distributed AI compute. The commercially crucial detail is the billing model: third-party clients pay for PiVerify in PI tokens, making it the most direct token-demand mechanism the project has ever shipped. What Pi does not yet have is a disclosed roster of paying clients; the products are weeks old, the integrations prospective, and the market’s cold reception of the pivot reflected exactly that gap between shipped infrastructure and proven demand. Pi’s founders have also been explicit that they are entering a race with named competitors, telling the community at the mainnet anniversary that KYC-as-a-service would compete with Worldcoin and with Humanity Protocol, the palm-recognition entrant that rounds out the field.

Scored honestly: Worldcoin leads decisively on external adoption and brand-name integrations; Pi leads on reach, verification depth, and, arguably, on having a billing model that routes revenue to the token at all. Neither has disclosed revenue that would register on any income statement.

Tokenomics: two different ways to disappoint holders

Both tokens have collapsed, and the mechanics of the collapses differ in instructive ways.

PI’s problem is supply. The token carries a 100 billion maximum supply against roughly 11 billion circulating, and the migration of users to mainnet plus daily unlocks continuously converts locked balances into sellable ones, over 127 million tokens in the current thirty-day window alone, with roughly 100 million entering circulation monthly on some projections into 2029. The community’s own most-wanted milestones, faster migration, bigger exchange listings, mechanically enlarge the sellable float, a supply treadmill this publication has quantified. Demand from PiVerify, priced and paid in PI, is the first mechanism that could in principle run the treadmill backward, and it starts from zero against roughly $30 million a month of new supply at current prices.

WLD’s problem has been emission against sentiment. The token spent seven consecutive months falling for a cumulative 80% before a modest recovery, and the foundation has responded on the supply side with a tokenomics revamp cutting daily token release by 43% to slow inflation. Worldcoin also carries a listed-company subplot: Eightco Holdings holds one of the largest private WLD stakes, and the token trades in the gravitational field of Sam Altman’s other ventures, with WLD watchers openly tracking the OpenAI IPO as a sentiment catalyst. Neither dynamic depends on the identity product succeeding; both illustrate that WLD’s price is, for now, a bet on narrative and scarcity engineering rather than on verification revenue.

The shared truth is uncomfortable for both: no proof-of-personhood project has yet proven that verifying humans generates token demand at a scale visible against its own supply. Worldcoin has adoption without a strong token sink; Pi has a token sink without adoption. The winner of the category, if there is one, is whichever closes its missing half first.

Privacy, regulation, and the trust question

Identity infrastructure lives or dies on trust, and each architecture concentrates its trust problem in a different place.

Worldcoin’s exposure is biometric and regulatory. Collecting iris scans from millions of people, disproportionately in lower-income countries during the bootstrapping phase, has produced suspensions, investigations, and bans across multiple jurisdictions, and the objection is not hypothetical: a database of biometric uniqueness, however cleverly hashed, is a honeypot whose breach cannot be remediated, because irises cannot be reissued. The zero-knowledge presentation layer genuinely protects users from integrating services; it does not protect them from the system itself, and regulators have consistently focused on exactly that gap. Every jurisdiction that restricts Orb operations also caps enrollment, which is why World’s verified count, for all its integration momentum, sits at 18 million rather than the hundreds of millions its ambitions require.

Pi’s exposure is the mirror image: it holds conventional identity documents for 18 million people, processed partly by community validators, under the data-protection laws of 200-plus countries, and its verification depends on the honesty of both the documents and the humans checking them. Document KYC is a mature, regulated industry precisely because it fails in known ways, and Pi entering it as a vendor means competing not only with Worldcoin but with the incumbent compliance providers that exchanges and fintechs already use, firms with audit trails, insurance, and enterprise sales teams. Pi’s countervailing asset is that its verification is the legally useful kind: a business that must perform KYC cannot satisfy the requirement with an anonymous personhood proof, which walls off a segment of the market from Worldcoin entirely and gives Pi a lane where its main competitors are not crypto projects at all.

The deepest shared risk is architectural: both systems are, in practice, operated by their founding organizations, and an identity layer for the open internet run by a single company is a contradiction the crypto industry has not resolved. Whichever project first makes its verification genuinely decentralized, auditable, and portable will have an argument the other cannot copy quickly.

The third contenders, and the decentralization question

Framing the race as a duel flatters both duelists, because the proof-of-personhood field is wider than two projects and the strongest long-term objection applies to the whole crypto side of it.

Humanity Protocol is the most direct third entrant, attacking the same problem with palm-recognition biometrics converted into zero-knowledge proofs, a design that tries to keep Worldcoin’s uniqueness guarantee while shedding the iris scan’s visceral regulatory baggage; palms feel less dystopian than eyes, and the hardware is cheaper. The project earned a top-tier valuation on exactly that pitch before a major hack earlier this year damaged both its token and its credibility, a reminder that identity infrastructure carries security stakes ordinary DeFi does not: a lending protocol that gets exploited loses money, while an identity protocol that gets exploited loses the only thing it sells. Beyond Humanity sit the non-token approaches that may matter more than any of the coins: government digital-identity schemes advancing across the EU, India, and elsewhere; device-level attestation from Apple and Google that can silently prove a real human holds real hardware; and the incumbent KYC industry, which processes more verifications in a quarter than all crypto identity projects have performed in their lifetimes and which will integrate whatever standard wins instead of losing its enterprise contracts.

Against that field, the crypto projects’ shared pitch is portability and user ownership: a credential the user controls, presentable anywhere, revocable by no platform, and that pitch collides with an awkward fact about how both leaders are actually built. World ID issuance depends on hardware manufactured, distributed, and updated by one foundation; Pi’s verification depends on a pipeline operated by one core team, with validator rewards, KYC rules, and the trust graph’s parameters all set centrally. Neither credential is meaningfully portable outside its issuer’s ecosystem today, neither verification process is independently auditable end to end, and both projects therefore ask users and integrators to trust a company in exactly the way decentralized identity was supposed to make unnecessary. The objection is not fatal, every young network centralizes before it decentralizes, if it ever does, but it defines the endgame: the durable version of proof-of-personhood is a standard, not a product, and standards historically get captured by consortia, regulators, or platform owners rather than by the startup that shipped first. The scenario in which one of these tokens captures the category’s full value requires its issuer to decentralize the credential before a consortium standardizes around something else, and neither team has published a credible roadmap for doing so.

There is also a quieter question about what the tokens are for at all. World ID could function identically if WLD did not exist; PiVerify’s pay-in-PI model is the exception that proves how rare a genuine token sink is in this category. Identity is infrastructure, infrastructure gets paid for in dollars, and every integrator that would rather invoice in fiat than hold a volatile token is a small vote against the thesis that verification demand must flow through a coin. The projects’ answer, that tokens bootstrap distribution no dollar-denominated startup could match, is historically respectable; forty million app downloads and a fifty-million-strong mining community are things marketing budgets cannot buy. Whether bootstrapped distribution converts into token value is the open question this entire market has spent 2026 answering in the negative, and it is the question the next disclosed PiVerify client or World ID enterprise deal will begin to answer properly.

The demand curve both are racing

Step back from the two projects and look at the market they are racing toward, because the size and shape of proof-of-human demand is what determines whether either token’s collapse is a terminal verdict or a mispricing.

The demand is arriving from three directions at once. The first is platform integrity: every consumer service that matches humans to humans, dating apps, marketplaces, social networks, gig platforms, is watching AI-generated accounts erode the assumption its product depends on, and Tinder and Zoom appearing on Worldcoin’s integration roster is early evidence that mainstream platforms will pay for a fix. The second is agentic infrastructure: as AI agents gain wallets and act autonomously, the systems they act through need a way to distinguish an agent operating for a verified human from an agent operating for nobody, which is exactly the gate Vercel is building World ID into and exactly the future in which autonomous agents transacting on-chain stops being a demo and becomes traffic. The third is regulatory: financial services must already verify identity by law, the compliance-KYC market runs to billions of dollars annually, and it is the one segment where demand does not need to be evangelized, only won from incumbents.

Each direction favors a different architecture, which is the subtlest reason the Pi-Worldcoin comparison resists a clean winner. Platform integrity mostly needs uniqueness, favoring the orb’s anonymous personhood. Regulated finance needs identity, favoring Pi’s document-based verification. Agentic infrastructure needs both, plus programmability, plus the neutrality that neither a Sam Altman-adjacent foundation nor a single core team obviously provides. It is entirely coherent to believe the proof-of-human market becomes enormous and that it fragments along these lines, with different providers winning different segments and no single token capturing the category premium the maximalists on each side imagine.

The scale question also deserves sober treatment. Eighteen million verified humans sounds vast until it is set against the systems that would rely on it: the internet has more than five billion users, the largest platforms count billions of accounts each, and a verification layer that covers well under one percent of the online population is a proof of concept, not a standard. Worldcoin’s hardware throttle and Pi’s validator throughput both cap how fast the coverage gap closes, and the gap is the opening through which non-crypto competitors, government digital-ID schemes, Apple and Google device attestation, the incumbent KYC industry, can walk while the two crypto projects fight each other. The bull case for the whole category requires believing that a decentralized, portable, user-owned credential beats those alternatives on trust and reach; the bear case requires only that platforms choose the vendors they already have contracts with.

What the demand curve does settle beyond argument is direction. The Fundstrat-style non-human-share numbers only rise from here, every quarter of AI progress makes synthetic accounts cheaper and detection harder, and the willingness of names like Coinbase, Okta, and Zoom to integrate a crypto-native ID in 2026 would have been unthinkable in 2023. The market both projects are racing toward is real and growing. The race itself, on the evidence of two collapsed token charts, has barely produced a first lap time, and the broader pattern of engagement-first token models struggling to convert attention into demand hangs over both contestants as the thing each must disprove.

Who wins, and what would prove it

The comparison resolves into a clean asymmetry. Worldcoin has solved distribution to businesses and not to humans: its integrations are enviable, its enrollment is hardware-throttled, and its token lacks a demand mechanism tied to usage. Pi has solved distribution to humans and not to businesses: its verified base was built at software speed across geographies Orbs cannot reach, its token has a direct pay-in-PI sink, and its client roster is currently a promise. The projects are, in effect, attacking the same fortress from opposite walls, and the Fundstrat-style demand data suggests the fortress is worth taking: proof-of-human is one of the few crypto narratives whose underlying demand is growing regardless of crypto’s own cycle.

The scoreboard to watch is short and public. For Pi: named external clients paying for PiVerify, PI-denominated revenue visible on-chain, and Pi Sign-in appearing on services outside the Pi ecosystem. For Worldcoin: enrollment growth resuming despite regulatory friction, the emission cut showing up in float math, and World ID integrations converting from announcements into measurable verification volume. For both: any move toward decentralizing the verification layer itself, and any sign that a major platform mandates proof-of-human at scale, the single event that would reprice the entire category overnight.

The market’s current verdict, two tokens near their lows, is not a judgment that the problem is fake. It is a judgment that neither solution has yet earned the problem’s value, and on the evidence assembled here, that verdict is harsh but fair. Eighteen million verified humans, twice over, is a remarkable foundation. It is also, for now, exactly that: a foundation, on which the internet’s identity layer may be built by one of these projects, both, or, as the incumbent compliance industry would quietly insist, neither.

A closing thought on timing. Categories like this one tend to have long quiet periods and then a forcing event, a platform mandating verification at scale, a regulator blessing one credential format, a breach that discredits an architecture overnight, and the forcing event, when it comes, will reprice both tokens in hours on positioning built over years. Worldcoin is positioned for a world that mandates anonymous uniqueness; Pi is positioned for a world that mandates portable identity; the likeliest world mandates both in different places, which is the quiet argument that this war ends not with a winner but with a border. Investors treating either token as a lottery ticket on the whole category should at least know which half of the category their ticket covers.

And for holders of either token, the practical checklist is mercifully short: one disclosed enterprise client with a dollar figure attached, one quarter of verification revenue visible in either ecosystem’s accounts, one integration that a non-crypto user actually encounters in the wild. Until at least one of those exists on either side, every price move in WLD and PI is sentiment trading a story, and the story, for all its genuine promise, remains one that neither project has yet made anyone outside crypto pay for.

The safest forecast in the whole comparison is the boring one: both projects will still be here in two years, because both hold the one resource that does not bleed away with a token chart, a verified human base that took years to assemble and that no competitor can replicate quickly. What their tokens will be worth depends on conversions neither has yet made, but the underlying registries, 18 million identities each, are assets in the plain business sense, and assets of that kind tend to find their buyer, their partner, or their business model eventually, even when their first custodians do not.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Digital asset markets are volatile and you can lose your entire investment. Figures are current as of July 8, 2026, and may change. Always do your own research.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

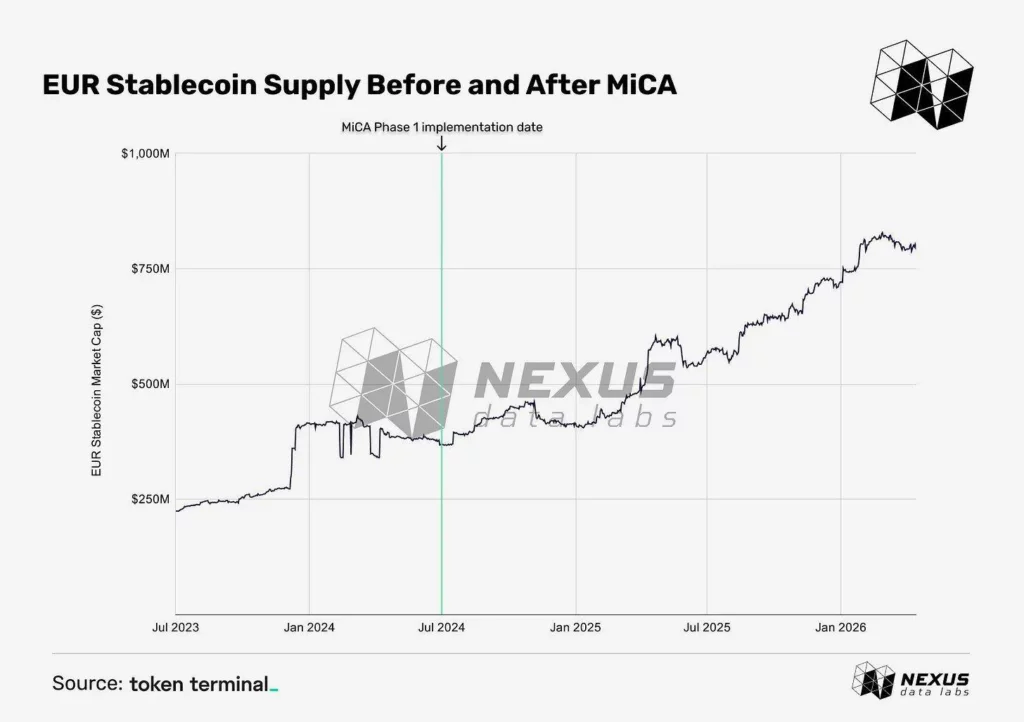

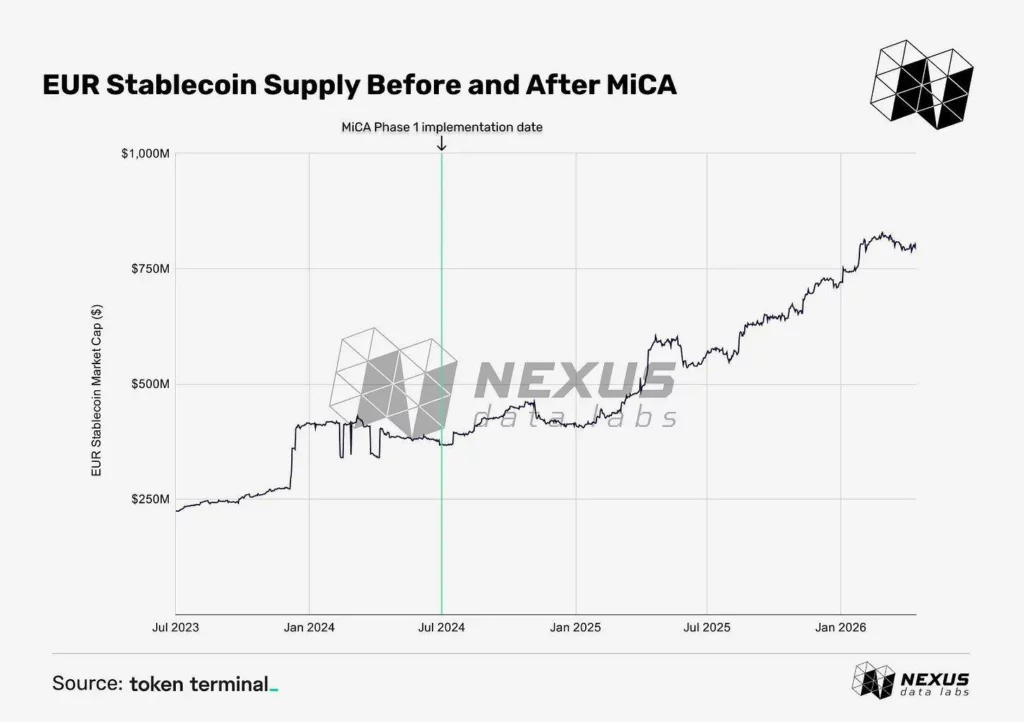

MiCA’s full implementation has reshaped Europe’s crypto market, with hundreds of firms securing CASP licenses while many others exited or restructured.

Summary

- MiCA leaves just 244 licensed crypto firms operating in the EU as thousands exit the market or suspend services after the July deadline.

- Europe’s MiCA rules reshape the crypto industry, with only 244 firms securing CASP licenses as stricter compliance takes effect.

- The EU’s MiCA framework causes a major crypto market shake-up, leaving hundreds licensed while thousands face closures or restructuring.

Overnight, MiCA wiped out 80% of the 3000+ companies with VASP licensing from the European crypto market. Only a handful of companies survived, around 244 as of today. So, what did the rest of 2700+ companies have to do to stay afloat?

MiCA Impact — damage and gains for the market

MiCA has officially entered the market. On the 1st of July, 2026, the transitional period for MiCA in the EU expired. More than 3,000 companies holding VASP licenses were faced with a critical choice: either cease operations or find a viable path forward. Only 244 projects managed to push past MiCA regulatory scrutiny, while the rest 80% of Europe’s crypto market had to make do.

VASP license meant a company was able to operate as a Virtual Assets Service Provider, which is as legal as it gets in crypto.

Even legitimate companies were impacted.Out of 1200+ projects with pre-MiCA registrations, only 17% secured a full CASP legal framework needed to operate under the new ruleset. Binance filed a MiCA application in Greece in January 2026, but failed to comply due to undisclosed reasons. CZ claimed it was a political decision not to license Binance.

Some of the big names have managed to obtain a MiCA license. Coinbase and Kraken registered with the Central Bank of Ireland, OKX and Crypto.com with Malta’s MFSA, Bitstamp picked Luxembourg and Revolut is now in CySEC, Cyprus.

However, the introduction of MiCA was not entirely negative as at least EUR stablecoin use skyrocketed after a phase 1 implementation.

What changed for crypto companies in the EU?

First and foremost, individuals can no longer launch a startup without being subject to regulatory scrutiny. Legally, Crypto in the EU is now treated as traditional finance, which has its own regulatory framework called MiFID II.

The days of garage-based operations are officially over. Europe becomes a tightly regulated space where every move has to be documented, every risk recorded, and AML/KYC checks strictly enforced. For one, it’s harder to innovate in an overly regulated space; on the contrary, it’s much safer to deal with.

It also means that companies can’t operate even if they are getting the license. If a crypto project tries to work with its own users while getting the license, operating under “Pending Application” can now cost a crypto company €15M or $17.1M in fines. As an alternative, they can hand over 12.5% of their annual turnover.

Cooperation rules have changed too. Crypto companies have to report their users to regulatory and financial authorities, not on demand, but on their own. In exchange, survivors of the MiCA slaughter who managed to obtain a CASP license can now access all member states with only one registration.

Targeting rules have also changed heavily. Even 1 EU influencer in the marketing campaign means they must be MiCA compliant now. If the app or project targets the EU specifically, then it has to be regulated.

On July 1st, money had to change hands from 2800 platforms to the surviving 244, which meant an influx of frozen funds. Binance had to freeze spot orders, sign-ups, deposits and staking products for users in France, Italy, Spain, and Poland. DeFi protocols had to pull the plug; Base’s Seamless Protocol and apps like PPL Wallet just physically shut their servers down. The 2800 platforms each had some way of storing or operating user funds, and if users didn’t withdraw their money is now being held because neither company has a legal allowance to actually send user money back.

But being MiCA-compliant costs a small fortune. According to Pharaon Production research, it can cost up to $1M in upfront costs even before you serve the first customer.

How can crypto projects make do after MiCA?

Many are choosing not to play regulatory tug-of-war and simply walk out for Dubai (VARA) or Singapore (MAS). Others are choosing workarounds that provide the same level of regulatory legality while not asking for $1M in upfront costs and dragging the whole company through bureaucratic torturing devices.

Switzerland’s FINMA supervision can be obtained via SRO (Self-Regulatory Organization). Under Swiss law, being a member of SRO is mandatory if a company wants to handle digital assets, which makes it a reason Zurich is so heavily nested with web3 projects, with more than 1749 crypto companies registered in Switzerland’s Crypto Valley alone. Swiss law doesn’t stand still either: in October of 2025 they opened up two new types of FINMA-supervised license categories.

The Swiss solution to MiCA slaughter is simple: come to the country, register with SRO or acquire the SRO-compliant company, and be free to go while being legally sound. One recent example is Neyro, an agentic project that was in the process of obtaining MiCA license but had to pivot to a Swiss SRO in order to sustain operations.

However, acquisition doesn’t mean free pass right from the gate. Companies involved still have to go through the regulatory checkups, but overall, it is the same level of legality without added scrutiny.

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

Tokenized stocks put real equities on blockchains as tradable tokens, and in July 2026 the idea crossed a threshold: the DTCC, the utility that settles nearly every American share, began production trades of tokenized Russell 1000 stocks. This guide explains how stock tokens actually work, the custody chain behind them, what you do and do not get compared to owning shares, how they differ from stock perps, and what the incumbents’ arrival means.

For most of crypto’s history, tokenized stocks were a fringe product with a persistent dream: take the world’s most valuable asset class, equities, and give it blockchain properties, around-the-clock trading, instant settlement, fractional ownership, global access, and composability with DeFi. The early attempts were offshore, legally fragile, and small. The dream, however, kept attracting bigger sponsors, and in 2026 it stopped being fringe: this month the Depository Trust and Clearing Corporation, the post-trade utility that custodies over $100 trillion and settles essentially every US securities transaction, began limited production trades of tokenized Russell 1000 equities, major ETFs, and Treasuries, with a full-service launch scheduled for October and a 50-firm working group of banks and brokers writing the standards.

When the institution whose entire job is recording who owns which share starts issuing those records as tokens, tokenized stocks graduate from crypto experiment to market-infrastructure roadmap. Yet the products a retail user encounters under the name tokenized stocks today are mostly not that; they are a patchwork of offshore wrappers, synthetic trackers, and broker-issued tokens with wildly different claims behind them, and telling them apart is the entire game.

This guide explains the territory properly: what a tokenized stock is and the custody chain that makes it real or fake, the three main models in the wild and what each actually gives you, the rights you do not get, dividends, votes, recourse, and how issuers handle them, the difference between tokenized stocks and the stock perpetuals often confused with them, the regulatory picture as American law catches up, and what the DTCC’s entry means for where all of this lands.

What a tokenized stock is, and the chain of custody that decides everything

A tokenized stock is a blockchain token designed to represent economic exposure to a specific equity, one token tracking one share of Apple, Tesla, or an ETF. The definition is deliberately loose, because the word represent is doing all the work, and what stands behind the token separates a genuine financial instrument from a branded bet.

The gold standard is full backing: for every token in circulation, the issuer holds one real share with a regulated custodian, and the token is a claim on that share, redeemable directly or through authorized participants, with the backing attested by disclosures or audits. This is exactly the architecture of a fiat-backed stablecoin transposed to equities, token supply on-chain, assets in custody off-chain, a redemption mechanism holding the two together, and it inherits the same integrity question: the token is only as good as the custody, the legal claim, and the attestation behind it. The moment you evaluate any tokenized stock, this is the first inquiry: who holds the shares, in what legal structure, under which regulator, and what exactly does the token entitle its holder to?

Everything else about the product flows downstream of that chain. If the shares are real and the claim enforceable, arbitrage keeps the token near the stock’s price, because gaps can be closed by minting or redeeming. If the backing is partial, discretionary, or merely promised, the token is tracking the stock on trust, and history’s failed stock-token experiments cluster precisely there. The blockchain part, which network the token lives on, is comparatively trivial; the custody chain is the product.

The three models in the wild

The tokenized stocks a user actually meets come in three broad architectures, and conflating them is the most common mistake in the category.

The first is the fully backed depository-receipt model described above, offered by regulated issuers, typically domiciled in jurisdictions with explicit frameworks, that buy and custody real shares and issue tokens against them. Holders get near-1:1 price tracking, some form of dividend pass-through, usually as additional tokens or cash-equivalent credits, and a redemption path, though often restricted to institutions or accredited users. What they usually do not get is shareholder status: the issuer or its custodian is the shareholder of record, and voting rights almost never pass through.

The second is the synthetic model: no shares anywhere, just a token whose price is maintained by collateral pools and oracle feeds, engineered to track the stock. Synthetics can be fully decentralized and accessible where backed products are not, and they carry categorically different risk: the holder owns exposure to a price feed backed by crypto collateral, with depeg, oracle, and protocol-solvency risks in place of custody risk, and no share exists to redeem under any circumstance.

The third is the broker-integrated model now emerging inside regulated finance: brokerages and infrastructure providers issuing tokenized representations of client holdings, or, in the DTCC’s version, the market’s own settlement layer optionally recording ownership as tokens. Here the token is not a wrapper around the system; it increasingly is the system’s own ledger entry in a new format, which is why the incumbents’ version, when it fully arrives, dissolves most of the category’s historic compromises at once.

What you get, and the rights you do not

Set a tokenized stock beside the share it tracks and the differences are exactly where the fine print lives.

Price exposure transfers well: a properly backed token tracks its stock closely during market hours and trades continuously after them, drifting on expectation while the reference market sleeps, then reconverging at the open. Dividends transfer imperfectly: issuers typically pass economic value through as token top-ups or credits, on the issuer’s schedule and terms, and tax treatment of that pass-through is the holder’s problem in whatever jurisdiction they occupy. Voting essentially does not transfer; the record shareholder votes, and it is not you. Corporate actions, splits, mergers, delistings, are handled by issuer policy, which is worth reading before, not after, the event. Legal recourse is the deepest difference: a shareholder sits inside centuries of securities law, while a token holder sits inside an issuer’s terms of service and the law of wherever that issuer lives, a gap that is invisible daily and decisive in a failure.

Against those losses, the gains are the blockchain properties the dream always promised. Markets that never close, settlement in minutes instead of the T+1 cycle, fractional ownership to arbitrary precision, access for anyone with a wallet in jurisdictions the brokerage system never reached, and, most distinctively, composability: a tokenized Treasury or equity can serve as collateral in lending protocols, sit in automated portfolios, and move across the same bridges and rails as any other token, acquiring uses no brokerage account statement ever had. Whether those properties are worth the surrendered rights is not a general question; it depends entirely on which holder, which jurisdiction, and which issuer.

Before the mechanics, a sizing snapshot situates the category. Tokenized real-world assets on public chains passed the tens of billions of dollars mark across 2025-26, with tokenized Treasuries and money-market funds the dominant slice and the largest asset managers as issuers; tokenized equities remain the smaller, faster-moving frontier of that stack. The Treasuries-first sequence was not accidental: institutions needed a stable, yield-bearing settlement asset on-chain before they needed tradable stock tokens, and the custody, attestation, and redemption plumbing built for Treasuries is precisely what equity tokenization now reuses. The equities wave, in other words, is arriving on rails already laid and already trusted with institutional money, which is the structural reason its 2026 acceleration looks different from the false starts of earlier cycles.

How the peg holds: mint, redeem, and the arbitrage loop

A backed token’s price discipline comes from the same loop that keeps ETF shares near their net asset value, and seeing it once explains why backing quality is everything.

Suppose a tokenized Apple share trades at a 1% premium to the stock. An authorized participant, typically an institution with an agreement with the issuer, buys real Apple shares in the market, delivers them to the issuer’s custodian, mints new tokens against them, and sells the tokens into the premium, pocketing the gap and pushing the token price down toward the share price. At a discount, the loop runs in reverse: buy cheap tokens, redeem them for shares, sell the shares, collapse the discount. As long as minting and redemption are open and frictionless to someone, deviations are profit opportunities that arbitrage erases, and the token tracks.

Every historic failure in this category is a failure of that loop. If redemption is suspended, discretionary, or restricted to a tiny club, discounts can persist indefinitely because no one can close them; if the backing is not verifiably there, the loop’s foundation is a promise; if the issuer’s jurisdiction blocks the flow of underlying shares, the arbitrage dies at the border. This is why the diligence questions are always the same three: who can mint and redeem, how quickly, and against what verified backing. A tokenized stock with an open, audited, fast redemption loop is a different asset class from one without, whatever the marketing says.

A short history of a stubborn idea

Tokenized stocks have been attempted in every crypto cycle, and the failures map the design space as clearly as the successes. The first wave came through offshore derivatives platforms and synthetic protocols around 2020-21: centralized exchanges listed tokenized equities in partnership with offshore issuers, and on-chain systems minted synthetic stocks against crypto collateral. Both halves collapsed instructively, the exchange products died with their venues or were shuttered under regulatory pressure, proving that a token is only as durable as its issuer, and the flagship synthetic protocol was crippled when the collateral backing its stocks imploded, proving that a stock tracker built on volatile collateral is a correlation bet wearing a ticker.

The second wave, from 2023 onward, learned the lessons: regulated issuers in explicit-framework jurisdictions, real custody, attestations, and institutional redemption, with tokenized US Treasuries, not equities, as the beachhead product, because a yield-bearing, stable, dollar-denominated instrument was what on-chain treasuries and funds actually wanted to hold. Tokenized Treasuries grew into a multi-billion-dollar category with the largest asset managers issuing on public chains, normalizing the plumbing that equities could then reuse. The third wave is the one running now: brokerages tokenizing client exposure, exchanges relisting equities under clearer rules, and the settlement layer itself, the DTCC pilot, absorbing the concept into market infrastructure. Each wave moved the custody chain closer to the source of truth, from offshore promise, to regulated wrapper, to the register itself, which is the whole arc of the idea in one sentence.

Tokenized stocks versus stock perps

Because crypto venues now offer both, the confusion between tokenized stocks and equity perpetual futures deserves its own section, and the distinction fits in two sentences. A tokenized stock is a claim: somewhere, in the backed models, a share exists, and the token’s value rests on that ownership chain. A stock perp is a bet: no share exists anywhere, the contract is a leveraged position whose payoff is indexed to the stock’s price through funding-rate machinery against an oracle feed, and holding it means margin, funding payments, and liquidation risk rather than ownership.

The products suit opposite users. Perps offer leverage, easy shorting, and no custody chain, at the cost of liquidation risk and zero ownership economics, a trade-off this publication’s guide to real-world-asset perps details. Tokenized stocks offer unleveraged, holdable, dividend-passing exposure that behaves like an asset rather than a position. A useful heuristic: if the product can liquidate you, it is a perp; if it claims a share stands behind it, it is a tokenized stock, and your next question is where that share is.

The regulatory picture: from offshore workaround to sanctioned rail

Tokenized equities spent years in regulatory exile because the analysis was straightforwardly hard: a token representing a share is, under American law, difficult to distinguish from the share, which makes issuing and trading one a securities activity requiring the full licensing stack. Early products responded by domiciling offshore and geofencing Americans, which capped the category at crypto-native scale.

The thaw has come from both directions. From crypto’s side, the pending market-structure framework, whose classification machinery this publication has mapped, and the year’s stablecoin and custody rulemakings are, piece by piece, defining which agency governs which token, and tokenized securities sit unambiguously with the SEC, a clarity that paradoxically helps: firms can build to a known perimeter, not an enforcement lottery. From finance’s side, the December 2025 SEC no-action letter clearing the DTCC’s tokenization path was the quiet green light for the incumbents, and the pilot now running, Russell 1000 stocks, major ETFs, Treasuries, with October’s full launch letting DTC participants elect tokenized record-keeping as a standard feature, is the loudest possible signal of where the destination lies: not offshore wrappers around the system, but the system itself, token-formatted. The 50-firm working group writing those standards, whose membership and stakes this publication has examined, is in effect deciding the plumbing every future tokenized share will run through.

For a user today, the regulatory takeaway is practical: which tokenized stocks you can legally touch depends on where you are, the products available to you differ enormously in backing and recourse, and the category is converging toward regulated issuance faster than any other corner of crypto, which means today’s product map has a short shelf life.

It also helps to name who the product serves today, because the answer differs by model. The backed offshore tokens serve access: users outside brokerage-served markets holding fractional Apple from a wallet. The synthetic versions serve the permissionless frontier, exposure with no issuer to trust and all the collateral risk that entails. The institutional rail serves the institutions themselves first, faster settlement, collateral mobility, always-on books between firms, with retail benefit arriving later and by policy choice. Tokenized Treasuries, meanwhile, quietly serve everyone in crypto already, as the reserve asset inside stablecoins, funds, and DAO treasuries. One name, four different products, four different users, which is the deepest reason blanket judgments about tokenized stocks are reliably wrong in at least three directions.