Crypto World

Bipartisan Senators Ask CFTC Chair Whether Agency Is Investigating Polymarket's Fake-Bet Campaign

— title: Bipartisan Senators Ask CFTC Chair Whether Agency Is Investigating Polymarket's Fake-Bet Campaign excerpt: Senators Adam Schiff and John Curtis sent a letter to CFTC Chair Michael Selig Thursday asking whether the agency is investigating Polymarket's paid influencer scheme, putting the… Read the full story at The Defiant

Research from the National Cryptocurrency Association (NCA), an organization backed by Ripple Labs, broke down the economic impact of the entire crypto industry on the United States, estimating that salaries, worker spending and output will have contributed $55 billion this year.

According to a report released Wednesday by the Pragmatic Policy Group on behalf of the NCA, the total economic contribution was based on direct, indirect and induced employment. Of the sectors to benefit from crypto’s economic contributions, the NCA said that investments in securities and commodity contracts were among the highest at $9.7 billion, while housing and real estate were a combined $4.8 billion.

The research found that about 34,000 people in the US were directly employed by crypto companies, accounting for just a fraction of the 232,000 jobs supported by the industry across the entire economy. This would mean crypto companies directly employ more Americans than the coffee and tea manufacturing and aerospace industries, according to data from the US Bureau of Labor Statistics.

The crypto industry’s growing employment footprint in the US. Source: NCA

Related: Goldman Sachs CEO backs ‘not perfect’ CLARITY Act as vote expected soon

Among the individual US states, Texas, Washington, North Carolina, California and New York employed the most people involved in the industry, but Colorado was a “growing blockchain hub” based on friendly regulatory policies, according to the economic report. The NCA added that North Dakota was “becoming an energy-integrated digital infrastructure hub” due to the state’s tax laws favoring crypto mining and favorable flare gas policies.

The NCA launched in March 2025 as a non-profit organization focused on consumer crypto education, with $50 million in backing from Ripple. Stuart Alderoty, Ripple’s chief legal officer, heads the group.

The industry experienced multiple shutdowns in 2026

Several projects tied to digital assets announced they would be shuttering operations this year for various reasons, including difficulty with scaling and market conditions.

Entropy, a crypto start-up based in New York, said in January that it would shut down after four years in operation. Dmail, a decentralized email platform based in Singapore, began ceasing operations in May, citing expenses on bandwidth, storage and computing. Decentralized autonomous organization governance platform Tally and Balancer Labs also shuttered in March.

Magazine: Will the US get CLARITY this week? Bitcoin’s new $80K target: Hodler’s Digest, July 19

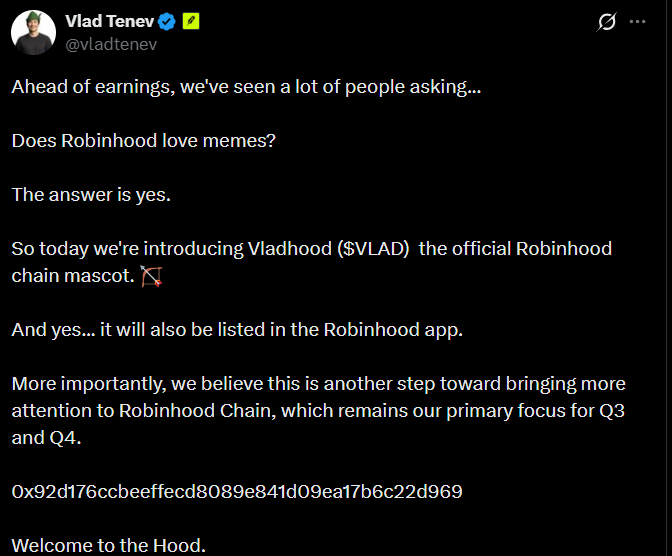

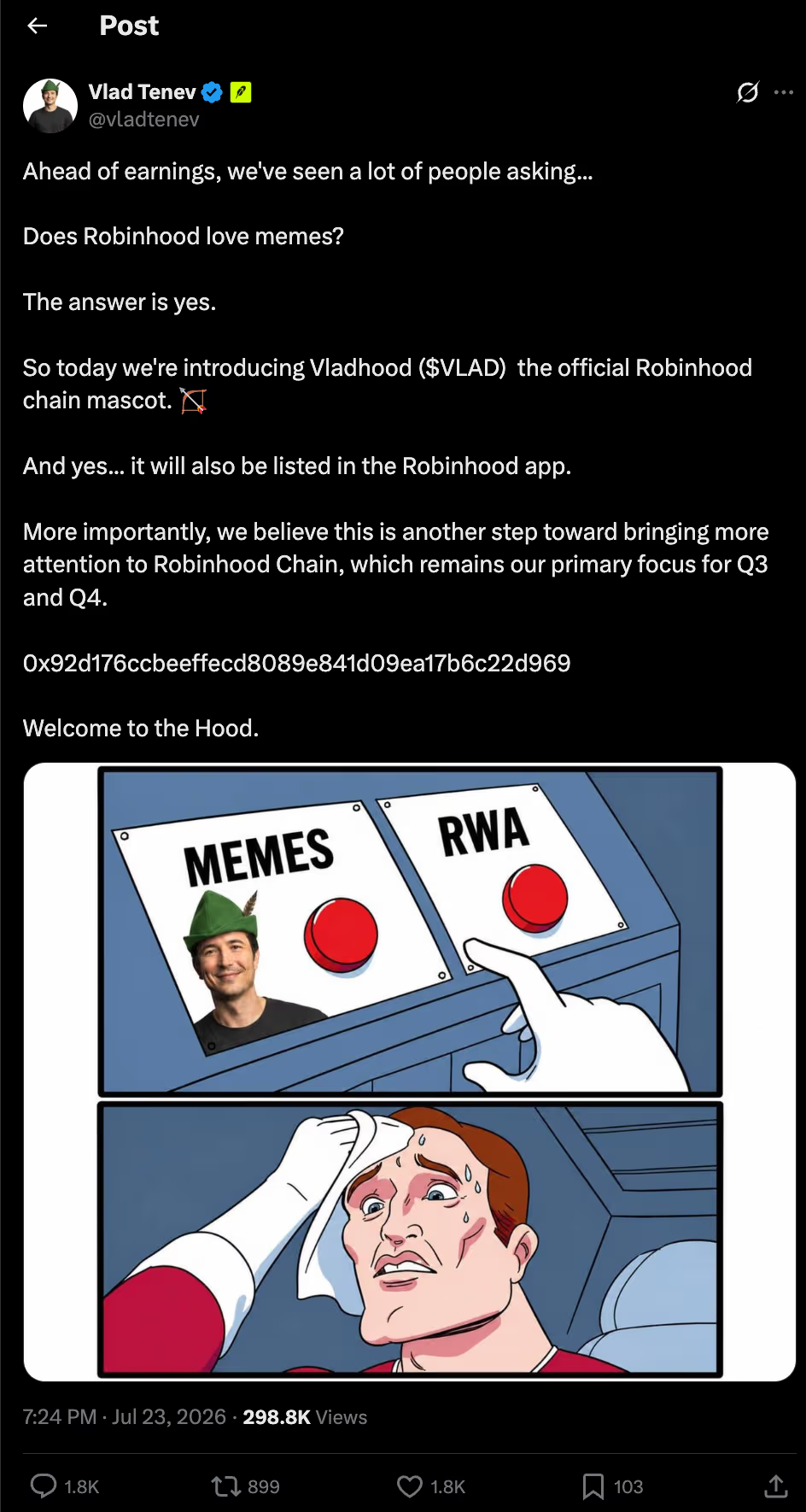

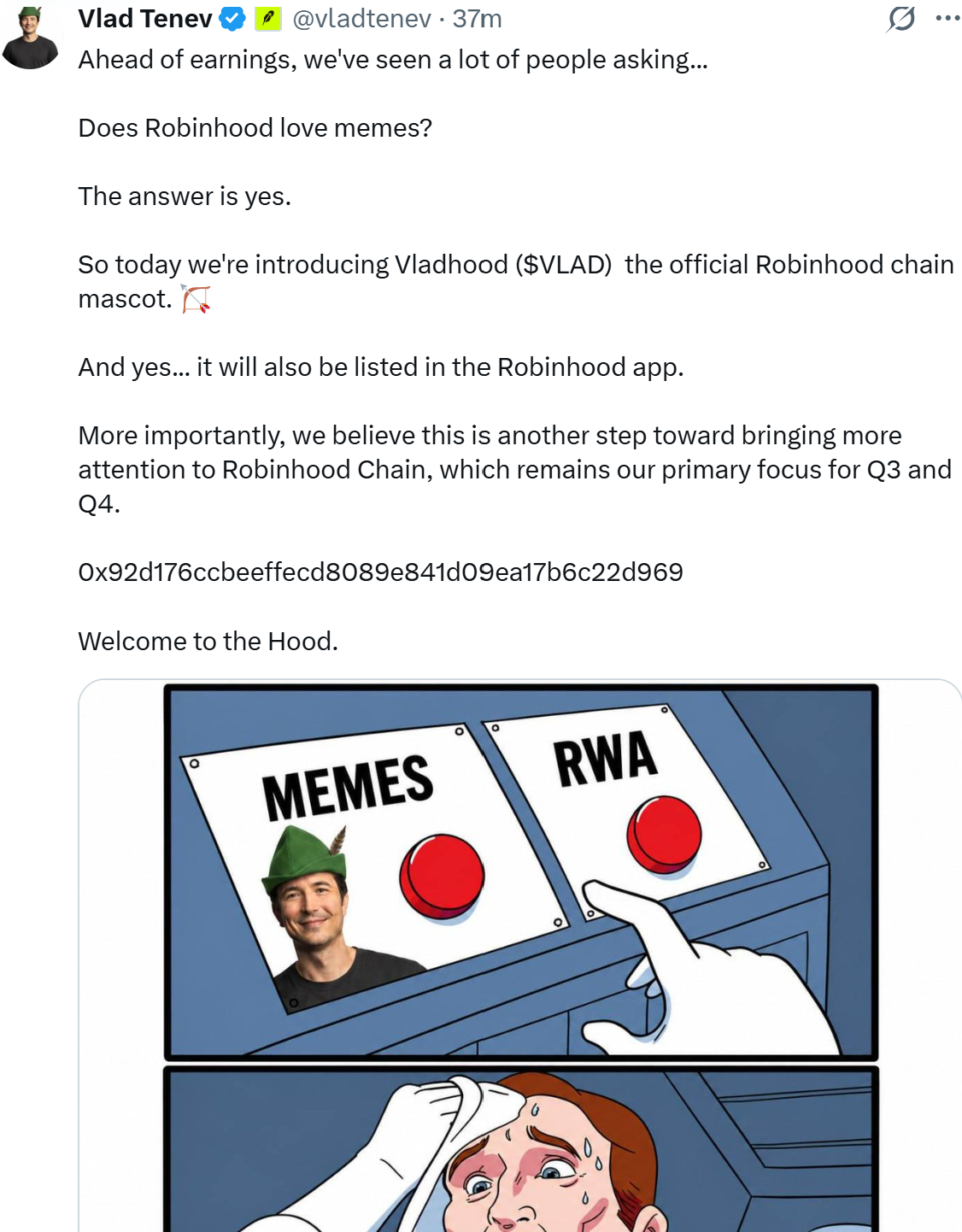

Robinhood CEO Vlad Tenev’s X account has been hacked to promote a fake company-linked memecoin that briefly reached a market capitalization of about $10 million.

Summary

- Hackers used Vlad Tenev’s X account to promote the fake Vladhood memecoin.

- Vladhood briefly reached a $10 million market cap before Robinhood confirmed the breach.

- The attack follows similar memecoin scams targeting CZ, BNB Chain and Yi He.

Robinhood confirmed the breach through its official X account, telling users that Tenev’s profile had been compromised and that the company was working with X to restore access. The brokerage added that the unauthorized post had been removed.

Posted at about 17:24 UTC on July 23, the message introduced Vladhood under the ticker VLAD and described it as the “official Robinhood Chain mascot.” The hackers also claimed that Robinhood would list the token on its trading app.

Seeking to connect the token with Robinhood’s business plans, the deleted post claimed Vladhood would bring attention to Robinhood Chain during the third and fourth quarters. Neither Robinhood’s main X account nor the company’s crypto account published a matching announcement.

The post included a contract address beginning with 0x92d, directing Tenev’s followers to a token deployed only minutes earlier through a contract named PonsLaunchFactory. Robinhood Chain’s block explorer subsequently attached a “potential scam” warning to the asset after recording more than 1,800 transactions.

Vladhood surges before Robinhood confirms the hack

Trading activity accelerated soon after the contract appeared on Tenev’s profile, pushing Vladhood’s market capitalization to roughly $10 million at its peak. The token later fell below $5 million after Robinhood confirmed the breach and the promotional message disappeared.

Onchain data shows that wallets identified as insiders realized more than $1 million in profits during the rapid price increase. At press time, the wallet owners had not been identified, and there was no evidence linking them directly to the compromise of Tenev’s account.

Despite Robinhood’s warning, Vladhood continued trading after the post was deleted, showing how onchain tokens can remain available even when the social-media promotion behind them has been discredited. Robinhood had not announced any plan to list Vladhood or recognize it as the chain’s mascot at the time of reporting.

The episode follows a method that Binance co-founder and former CEO Changpeng Zhao warned traders about in October 2025. With memecoin activity increasing at the time, Zhao wrote that hackers were targeting social-media profiles because such accounts often had weaker safeguards than crypto platforms.

“With the rise of meme coins, hackers are targeting social media accounts (as they usually have lower security measures) to post CAs [contract addresses].”

Zhao also cautioned users that official accounts did not endorse particular memecoins, urging traders to treat sudden contract-address posts with suspicion. His warning followed the compromise of BNB Chain’s X account, which attackers used to promote a fake BNB-themed token presented as part of an airdrop.

A similar scheme targeted Binance co-CEO Yi He in December 2025. Hackers seized an unused WeChat account connected to her old phone number and used it to promote MUBARA, also known as Mubarakah, shortly after she joined Richard Teng in Binance’s dual leadership structure.

Notably, posts from Yi He’s compromised profile encouraged contacts to buy the token, creating enough demand for a coordinated pump-and-dump. Zhao confirmed the breach and urged traders to ignore the messages, while reported onchain estimates placed the attackers’ profit at about $55,000.

Robinhood Chain keeps attracting speculative trading

Tenev’s account was compromised as Robinhood Chain recorded a sharp increase in activity following its July 1 mainnet launch. Built as an Ethereum layer-2 network using Arbitrum technology, the chain was introduced to support tokenized assets, decentralized finance and round-the-clock trading.

Memecoins, however, supplied much of its early decentralized exchange activity. Entropy Advisors estimated that Robinhood Chain had processed about $9 billion in cumulative DEX volume by July 23, with high-risk memecoin trading responsible for much of that amount.

CashCat became one of the network’s first major tokens, reaching a market capitalization of about $150 million during the chain’s opening weeks. Fortune reported that Robinhood Chain’s daily trading volume rose from slightly above $200,000 on July 1 to more than $500 million nine days later, driven largely by speculative tokens rather than real-world assets.

Although Robinhood designed the network around tokenized finance, Tenev previously acknowledged its early memecoin activity. Fortune quoted him as saying that while the company was building Robinhood Chain for real-world assets, the network also “works great for memes.”

Revenue has risen alongside the trading surge. DeFiLlama data showed that Robinhood Chain generated about $1.1 million in revenue over seven days and $2.11 million since launch, placing it among the highest-earning chains during the measured period.

DeFiLlama also recorded hundreds of millions of dollars in bridged value and substantial daily DEX volume on the network. Those figures explain why a false endorsement tied to Tenev and Robinhood Chain could attract traders within minutes, while Robinhood’s confirmation established that Vladhood had no authorized connection to the company.

Andrew Tate’s DADDY memecoin has shed half its value and is currently trading 97% below its 2024 peak — a plunge that’s coincided with Tate’s latest arrest and his incarceration in Miami’s Federal Detention Center.

US Marshals arrested Tate, 39, and his brother Tristan, 38, on Saturday on a sealed warrant pursuant to UK extradition proceedings outside Miami’s James L. Knight Center. The pair were en route to a boxing event that Andrew was slated to co-host.

It is not the pair’s first time in government detention and they continue to use these experiences to attract media attention.

Indeed, Tate spent some time on Thursday tweeting about jail life, including being housed next door to an alleged cannibal who “screams through the night.”

Whether personally or through a proxy with internet access, Andrew posted to X, “I am being held in SHU,” referring to the Special Housing Unit at the Federal Detention Center of Miami, a US Bureau of Prisons facility.

He inaccurately claimed that it’s “the highest level of security which exists” and continued to embellish his tale, “No commissary. No visits. No contact with the outside world.”

This “no-contact” experience includes over three million impressions on a single post and a dozen posts or retweets over the past 48 hours, not to mention exposure from his other social media channels and countless media stories about the incident.

UK seeks criminal proceedings against Andrew Tate

Britain’s Crown Prosecution Service has authorized 38 further charges against the Tate brothers, involving four more alleged victims and bringing the total to seven.

Andrew personally faces seven fresh counts of rape, trafficking, and assault, and charges over child sex-abuse images and extreme pornography.

Tristan faces two rape counts, one sexual assault count, and three trafficking counts.

Malcolm McHaffie, head of the CPS special crime division, spoke on the matter, saying, “We have decided to prosecute Andrew and Tristan Tate for further offences including rape, arranging or facilitating trafficking for sexual exploitation and offences relating to indecent images of a child.”

The brothers appeared before Judge Lauren Louis on Monday, with another hearing set for Monday, July 27.

For now, they remain at the Federal Detention Center in downtown Miami.

Justice Department filings this week asked the court to keep the pair secured throughout extradition proceedings, alleging that both brothers strangled women unconscious before raping them.

Their lawyer, Joseph McBride, told reporters, “This feels political.”

Read more: Andrew Tate liquidated again amid fresh trafficking charges

DADDY the Tate brothers’ memecoin wreckage

Tate adopted DADDY, a Solana memecoin, as his personal token in June 2024. On Thursday afternoon it traded around $0.008, 97% below its all-time high of $0.29.

Its market capitalization now hovers below $5 million. The token shed more than a quarter of its value in the two days after the arrest, and is down 50% over the past seven days.

None of this should surprise anyone. Bubblemaps found that DADDY’s deployer sent 40% of the entire token supply straight into Tate’s own wallet.

The Tate brothers endorsed more than 10 Solana memecoins during 2024’s celebrity token frenzy, and most soon collapsed by around 99%.

TOPG, another Tate-themed and possibly unauthorized memecoin, now trades 99.8% below its June 2024 peak on less than $200 of daily volume. Another, Tate Terminal, sits more than 99% below its October 2024 high.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

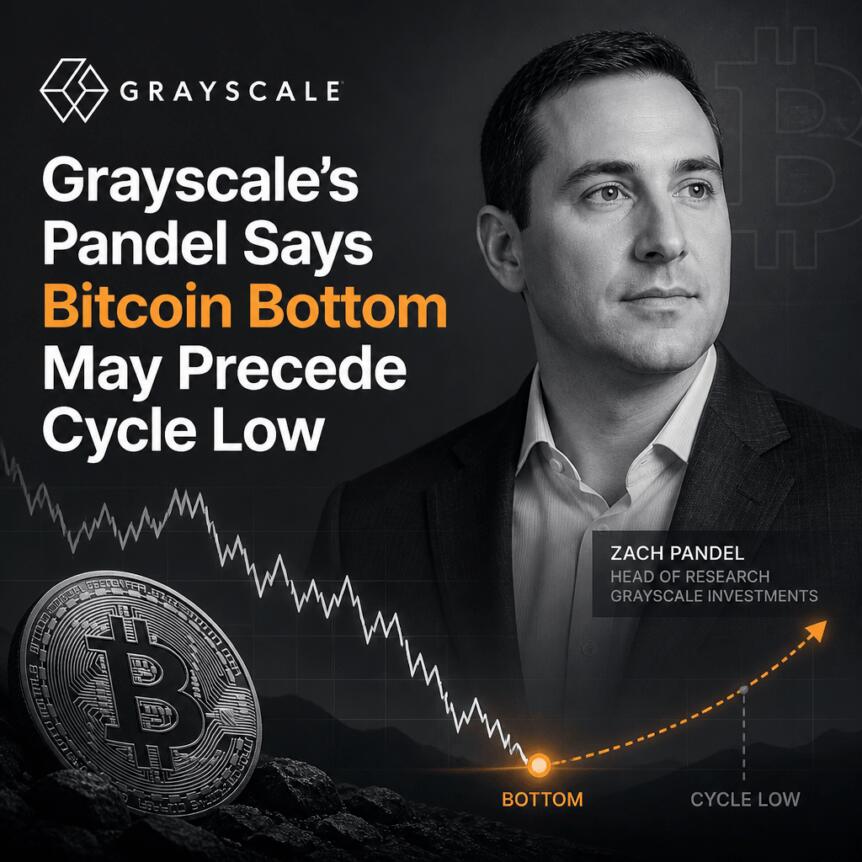

Grayscale is challenging a key assumption many traders use to frame Bitcoin’s price cycle: the idea that bottoms reliably line up with the traditional four-year, halving-driven rhythm. In a Wednesday research note, the firm’s head of research, Zach Pandl, suggested that Bitcoin may have already found a floor—potentially pointing to a cycle low as early as September or October—if upcoming macro conditions remain supportive.

Pandl’s argument centers on Bitcoin’s increasing sensitivity to broader economic variables. Rather than treating the halving cycle as the dominant force, Grayscale says macro factors—especially Federal Reserve policy—may be doing the heavy lifting for price direction right now.

Key takeaways

- Grayscale says Bitcoin’s cycle low could arrive earlier than the historical four-year pattern, with September or October cited as a potential window.

- Zach Pandl argues Bitcoin is increasingly “macro-driven,” implying that rate expectations may determine when price bottoms.

- CME FedWatch data at the time of Grayscale’s note showed markets pricing about a 66% chance the Fed holds rates on July 29, down from 88% a week earlier.

- Despite the macro thesis, Grayscale warns regulation could still cap recovery momentum, particularly if the CLARITY Act fails to pass this year.

- Other analysts still expect a later bottom, including a view that a trough may not appear until October–December 2026.

Why Grayscale thinks the cycle floor may be sooner

Grayscale’s framing departs from the more rigid “four-year cycle” approach. In the firm’s report, Pandl wrote that if the Federal Reserve “forgoes rate hikes” and economic growth remains resilient, Bitcoin “may already have bottomed.” That would imply the cycle low could come earlier than some models anticipate, potentially in September or October.

This matters for investors because it changes how risk is likely to be assessed around typical cycle milestones. If macro conditions are now the primary driver, historical calendar-based expectations may be less reliable—making forward-looking indicators (like real rates and central bank guidance) more important than fixed cycle timing.

The Fed’s meeting and shifting rate odds

A central element of Grayscale’s view is that the Fed remains the most actionable near-term variable for Bitcoin. Pandl said macro factors place Bitcoin in the “driver’s seat,” adding that Bitcoin could “bottom when these macro factors turn around.”

The next scheduled rate decision cited in Grayscale’s discussion is due on July 29. According to CME Group’s FedWatch tool referenced by Grayscale, market participants were pricing in a 66% chance the Fed will hold interest rates unchanged—down from 88% a week earlier. The change highlights how quickly expectations for policy path can evolve, and why Grayscale sees macro shifts as central to the timing of a market bottom.

Grayscale also connected prior Bitcoin bear markets to periods of slowing economic growth alongside rising real interest rates. In that framework, the direction of real rates—more than nominal liquidity narratives—has historically aligned with whether downside pressure persisted or eased.

Regulatory uncertainty remains a drag on upside

Even if macro conditions improve, Grayscale cautioned that policy risk could still limit how far Bitcoin can recover. In a June 26 Grayscale report titled “Two scenarios for the Bitcoin bear market,” Pandl argued that regulatory uncertainty may force continued “deleverage” among certain crypto treasury-related entities.

Specifically, Grayscale suggested that if the CLARITY Act does not pass this year, Strategy and other treasury companies may continue to reduce leverage, a process that could lead Bitcoin to “fall moderately further.”

This point is important because it introduces a potential mismatch: macro might be stabilizing, but balance-sheet pressure within parts of the crypto market could still weigh on prices. For market participants, the takeaway is that “macro-driven” doesn’t automatically mean “macro-only”—regulatory outcomes can influence liquidity and forced selling dynamics even when economic data looks better.

Competing views on how late the bottom could be

Grayscale’s earlier-bottom thesis is not universally shared. Earlier this year, crypto analysts pointed to market structure and long-term investor behavior as signals that a bottom could be approaching sooner rather than later. For example, K33 had argued that Bitcoin’s supply held at a loss could signal cycle timing, noting that historically Bitcoin has tended to bottom weeks after more than half of supply moved underwater. Separately, Swan Bitcoin CEO Cory Klippsten told Cointelegraph in a June interview that record long-term holdings—reaching an all-time high of 14.7 million Bitcoin—could indicate an imminent bottom.

Still, other analysts have suggested that the trough may not arrive until later. Lebit Mining Pool founder Jiang Zhuoer predicted that Bitcoin’s bottom could fall between October and December 2026—roughly six months after Strategy’s Multiple to Net Asset Value (mNAV) indicated its cycle low.

That contrast underscores a broader uncertainty for traders and portfolio managers: different approaches—cycle timing, macro signals, supply-at-loss statistics, or balance-sheet metrics—can point to different windows. The question for readers is not only whether Bitcoin bottoms, but whether the market is responding to the same underlying regime shift that each model assumes.

What to watch next

With the Fed decision on July 29 in focus and regulatory developments still capable of influencing deleveraging pressure, investors should track both macro indicators (especially real-rate expectations) and any signs that the CLARITY Act timeline or related market balance-sheet activity is changing. Grayscale’s thesis hinges on “macro turning around,” but whether that translates into a durable cycle low may depend on policy risk and crypto-specific liquidity conditions as much as on economics.

Robinhood (HOOD) CEO Vlad Tenev’s X account was compromised on Thursday and used to promote a fake memecoin as traders have piled into tokens on the brokerage’s recently-launched blockchain network.

The now-deleted post introduced a token called Vladhood ($VLAD) as the “official Robinhood chain mascot” and falsely claimed it would be listed in the Robinhood app. It included a blockchain wallet address and described the token as part of the company’s focus on Robinhood Chain.

“Does Robinhood love memes? The answer is yes,” the post read.

Robinhood later confirmed the account had been hacked.

“Heads up: Our CEO Vlad Tenev’s X account was compromised and posted a fake promotion for a meme coin,” the company said through its communications account on X. “We’re working with X to restore access and the post has been removed.”

The incident came as Robinhood’s newly launched blockchain has become a hotbed of speculative trading.

Empery Digital has committed $20 million to Cardinal Data Power, purchasing an approximately 8% stake in the private developer behind “powered” data center campuses designed for AI and high-performance computing workloads. The capital injection is tied to Cardinal Data Power’s Series A round of roughly $70 million and is intended to help advance a 750-megawatt campus project in West Texas.

While the investment highlights growing demand for large-scale compute infrastructure, it also lands in the middle of Empery’s own strategic shift away from its earlier Bitcoin treasury approach. Over the past two months, the company sold about 1,400 BTC for approximately $87.1 million, leaving it with 1,514 BTC after the transactions.

Key takeaways

- Empery Digital invested $20 million for an ~8% stake in Cardinal Data Power as part of a Series A of about $70 million.

- Cardinal’s West Texas powered data center campus is expected to begin delivering power in 2027, expand to around 1 GW by 2029, and ultimately exceed 5 GW.

- Empery’s Cardinal investment follows a reduction in its Bitcoin holdings, after it sold roughly 1,400 BTC over two months.

- Across the broader market, Bitcoin treasury firms are splitting between continued accumulation and exits or restructurings.

- Investors are watching whether corporate Bitcoin strategies increasingly prioritize operational assets—such as AI infrastructure—over pure balance-sheet accumulation.

Empery backs AI-focused “powered” campus development

Cardinal Data Power builds data center sites that integrate power generation, natural gas supply, and electrical infrastructure into a single development model. According to Empery Digital, the goal is to accelerate the delivery of large-scale computing campuses for artificial intelligence and HPC customers.

The company’s current plan centers on a West Texas campus with an initial scale of 750 MW. Cardinal expects first power in 2027, then scaling to about 1 gigawatt by 2029. The longer-term target is to exceed 5 gigawatts, implying a phased buildout designed to support expanding demand as AI workloads and compute capacity requirements grow.

For investors and data center developers, the appeal of “powered” campus design is that it aims to reduce bottlenecks often associated with securing power capacity and the infrastructure required to deliver electricity at the scale large AI deployments demand. Empery’s decision to place capital into this model suggests it sees AI infrastructure as a near-to-medium term driver of value creation rather than relying solely on financial asset appreciation.

Bitcoin treasury strategy under pressure at Empery

Empery’s investment decision comes during an ongoing adjustment to its treasury posture. Earlier this year, the company moved away from an electric powersports business and adopted a Bitcoin treasury strategy in mid-2025, positioning Bitcoin holdings as a key part of its balance sheet.

However, the company recently reported that it sold about 1,400 BTC over a two-month period for approximately $87.1 million. Empery said it intends to use those proceeds to fund AI infrastructure investments and repay debt.

After the sales, Empery’s Bitcoin holdings dropped to 1,514 BTC. BitcoinTreasuries.NET data indicates Empery previously held as many as 4,081 BTC before beginning to trim its position in March.

The reduction appears to have taken place amid shareholder activism: the filings and coverage referenced in the source say that shareholder Tice P. Brown urged the company to abandon its Bitcoin treasury strategy and called for the resignation of the chief executive officer and the board. The pressure helps explain why Empery’s corporate narrative is shifting from a “hold Bitcoin” approach toward funding operational and infrastructure projects—at least in part using realized value from earlier BTC holdings.

Bitcoin treasury firms diverge: unwind, restructure, or persist

Beyond Empery, the broader Bitcoin treasury landscape continues to show a wide range of strategies and outcomes. Some companies remain committed to accumulation, while others are winding down positions, changing corporate direction, or revising how Bitcoin appears on their balance sheets.

Satsuma Technology is one of the clearest examples of an exit. According to the source, shareholders voted overwhelmingly on July 20 to sell the company’s Bitcoin holdings, return substantially all of its capital to investors, and delist from the London Stock Exchange. More than 90% of votes cast supported both the capital return and delisting.

Meanwhile, a different kind of change played out through attempted consolidation. The proposed merger between Tether-backed Twenty One Capital, Strike, and Bitcoin miner Elektron Energy was scrapped earlier this week. The source notes that Strike will remain a standalone company while discussions between Twenty One and Elektron continue. Even after the abandoned deal, Twenty One remains among the largest publicly tracked corporate Bitcoin holders with 43,514 BTC, ranking behind Strategy.

Taken together, these moves show that the corporate Bitcoin treasury model is not static. Some firms treat BTC accumulation as a long-term thesis; others appear to conclude that capital can be deployed more effectively elsewhere or that shareholder appetite is better aligned with liquidity and balance-sheet simplification.

A new playbook: Bitcoin alongside permanent-capital business ownership

Another strand of development comes from efforts to reframe Bitcoin’s role inside corporate structures. The source says Bitcoin analyst Lyn Alden co-founded Orange Juice HODLINGS, a permanent-capital holding company backed by Mexican billionaire Ricardo Salinas. It reportedly launched with $40 million in initial funding.

Rather than using Bitcoin strictly as an asset to accumulate and hold, the described plan is to acquire and retain profitable businesses indefinitely, while using Bitcoin as a treasury reserve asset. The strategy aims to combine long-term ownership of operating companies with a Bitcoin-backed balance sheet—an approach that differs from both pure accumulation and pure exit.

For readers trying to understand where the market may be headed, this is a meaningful shift in framing. It suggests corporate actors may increasingly treat Bitcoin as one component of a diversified capital stack, rather than the sole centerpiece of a treasury thesis—particularly as institutional narratives around AI infrastructure, compute scaling, and power availability gain traction.

What to watch next

With Empery using realized Bitcoin proceeds to fund AI infrastructure and with Cardinal’s campus ramp targeting multi-year power delivery milestones, investors should watch for how quickly capital commitments translate into construction progress, power milestones, and incremental financial disclosures. At the same time, the broader split in corporate treasury outcomes—unwind versus restructure versus hybrid models—will likely shape how future corporate Bitcoin strategies evolve under shareholder pressure and shifting capital allocation priorities.

Wall Street is banking heavily on exchange-traded funds that give investors artificial intelligence exposure, according to J.P. Morgan Asset Management.

The firm’s “Guide to ETFs,” which came out this month, finds it’s a top five theme by assets under management — even as volatility hit the group in the second quarter.

“Many [themes] are morphing towards AI and the ecosystem surrounding AI,” Jon Maier, the firm’s chief ETF strategist, told CNBC’s “ETF Edge” this week.

Maier, who led the insights team that published the report, also highlighted an overlapping relationship between AI-themed ETFs and infrastructure.

“It’s all kind of feeding into the AI story … the applications, the energy [and] the AI models,” he said.

Go with the flow? ETFs vs. mutual funds

JPMorgan’s Guide to ETFs also found that mutual fund overall inflows are meaningfully tapering off while more money is flowing into ETFs.

“That’s only going to continue,” said Maier, who added the report’s data showed negative inflows into mutual funds overall during the past several years.

He also suggests that ETFs have become more attractive to retail investors because of the tax benefits.

“They typically don’t pay a capital gain [tax],” he said.

Maier contends mutual funds are a different story.

“Imagine if you bought a mutual fund in 2022 and you’re down 20%, 30%, 40%, depending on what part of the market you bought, and you still got a capital gain of 6%. You’re not happy,” he said.

Hackers took over the X account of Robinhood CEO Vlad Tenev on Thursday. They used it to push a new crypto coin, Vladhood (VLAD), that has already been flagged as a likely scam.

The fake post called VLAD the official mascot of Robinhood Chain. It even said the coin would be listed in the Robinhood app.

Inside the Robinhood CEO X Account Hack

Robinhood’s own accounts stayed silent. So did Robinhood Crypto. That was the first clue the post was fake.

The message started with a question. Does Robinhood love memes? It answered yes, then shared the coin’s address and signed off, “Welcome to the Hood.”

The post has since been deleted.

A blockchain tracker for Robinhood Chain marks the coin as a likely scam. The token holds no real money. It has changed hands about 1,868 times since launch.

According to on-chain monitoring by MLM, the attacker generated around 650 ETH in proceeds from the VLAD token, worth approximately $1.2 million to $1.3 million.

Scams like this keep hitting the network. Reports of rug pulls have multiplied. The trick is not new. A fake coin named after Coinbase boss Brian Armstrong crashed this month, a lesson about trusting posts from executive accounts.

Meme Coins Keep Testing Robinhood Chain

Robinhood Chain went live on July 1. It is a new blockchain that Robinhood built on Ethereum. The company wants it to power tokenized stocks and other real-world assets.

But memecoins took over fast. The network now handles millions of trades a day. Risky meme coins drive most of it, and recently pushed it to record trading volume. Total trading has topped roughly $9 billion, according to Entropy Advisors.

One coin, the Cash Cat meme coin, has led the pack. Some experts worry this meme coin trading boom could hurt Robinhood’s bigger plans for tokenized stocks.

Tenev has welcomed the fun. He once posted that the chain “works great for memes too.” Now that same hype has been turned against him.

The post Robinhood CEO Vlad Tenev Hacked, Exploiter Makes $1.2 Million Promoting Fake Token appeared first on BeInCrypto.

Bernstein said that it remains overweight on the Bitcoin mining sector, citing the growing partnerships between Bitcoin mining companies that are necessary to address the power constraints of artificial intelligence (AI) data centers.

The investment manager’s Bitcoin mining industry deal tracker registered a new AI-related deal every week in July, with combined deals standing at more than 7.5 gigawatts or the contracted equivalent of $150 billion in multi-year contracts, according to a Thursday research note shared with Cointelegraph.

The analysts said that third-party computing capacity from Bitcoin miners will remain highly valuable as access to power remains the AI industry’s real bottleneck amid growing political pushback against building new US data centers.

Bitcoin mining stocks logged double-digit gains on Monday after Bitcoin mining companies Hut 8 and IREN announced major AI infrastructure deals. Hut 8 announced a 15-year, $9.8 billion lease for its AI data center campus and IREN disclosed $2.8 billion in cloud services contracts with AI developers.

“IREN is beginning to convert that infrastructure advantage into contracted and more predictable revenue,” said Seeking Alpha contributor The Curious Analyst on Thursday. “The biggest risk to my thesis is execution,” they said. The contributor rates IREN a strong buy.

July sees slew of AI-miner tie-ups

Other publicly traded Bitcoin mining companies have also expanded into AI. Earlier in July, MARA Holdings announced plans to acquire a Texas site with up to 2 gigawatts of capacity to expand its AI and digital infrastructure business.

Days earlier, TeraWulf signed a 20-year data center lease with AI startup Anthropic, a deal the company said could generate roughly $19 billion in contract revenue.

Bitcoin mining infrastructure company Bitdeer has also expanded into AI cloud services and high-performance computing.

Most of the miner stocks were poised for gains on Thursday, based on premarket activity. HUT 8’s shares were up 5.23%, IREN was up 1.89% and TeraWulf was up 1.49%. Sector tracking exchange-traded fund CoinShares Bitcoin Mining ETF (WGMI) was up 1.47% ahead of the Nasdaq open. Bernstein has an outperform rating on all of the stocks it named, except for MARA, which it rates as market perform.

Related: Foundry asks Bitcoin miners to vote on BIP-110 support

AI data centers face political pushback

Bernstein’s research note said that Bitcoin miners and third-party computing power providers will remain important for AI companies, as the construction of new data centers is facing growing bipartisan political pushback.

On Wednesday, Texas Democratic Senate candidate James Talarico reportedly shared a proposal to create stronger local approval processes and to repeal tax breaks for AI data centers.

In April, US Senator Ron Wyden shared concerns that AI data centers in his home state of Oregon could worsen water scarcity during persistent droughts. He said that large data centers can consume up to 5 million gallons of water per day and asked large data center operators to explain how they would reduce groundwater withdrawals to protect the local water supply.

In March, President Donald Trump’s administration published a Ratepayer Protection Pledge aiming to expand AI infrastructure without increasing electricity bills for households and small businesses.

In January, several state governors published plans to expand the grid to meet the rapidly growing demand from AI data centers, but stated that new data centers should bear the costs they create, rather than shifting these to existing residential customers and small businesses.

Magazine: Bitcoin’s quantum dilemma: Bigger blocks or STARK proofs?

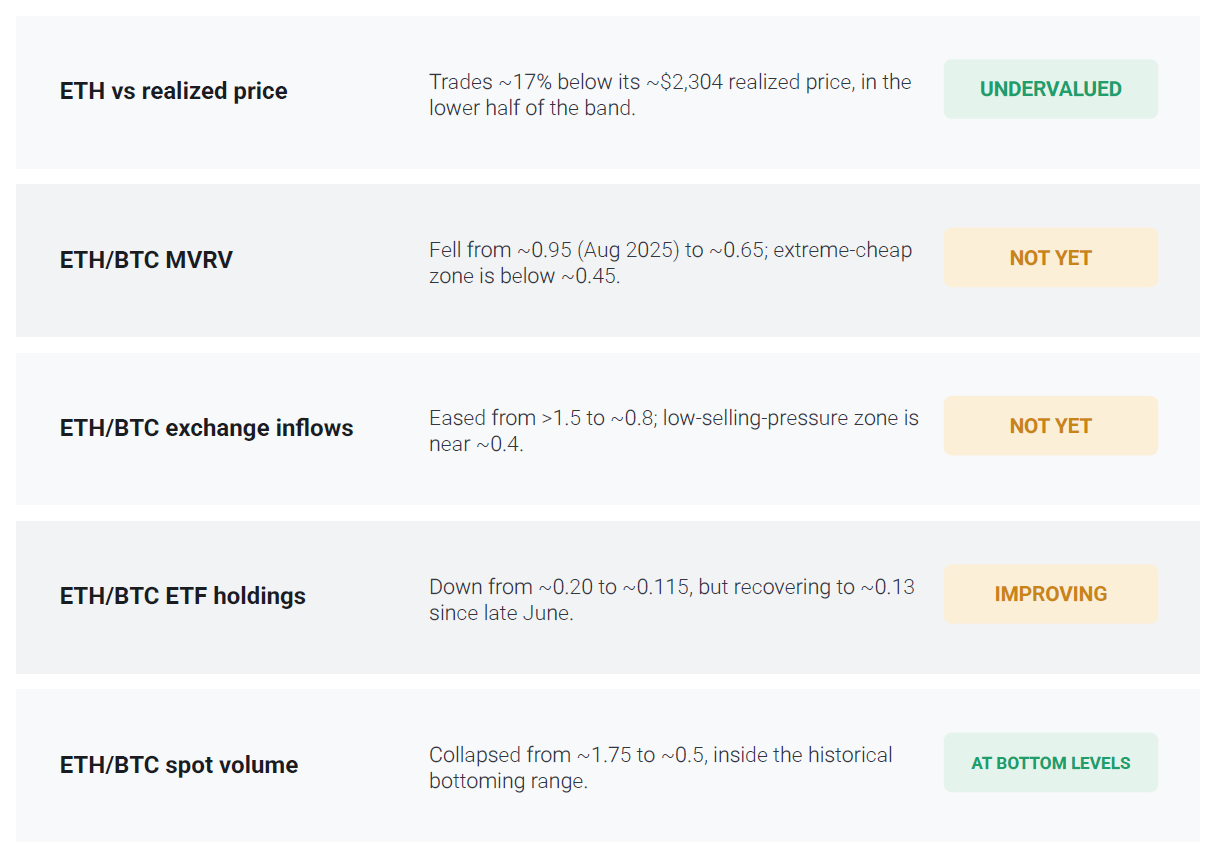

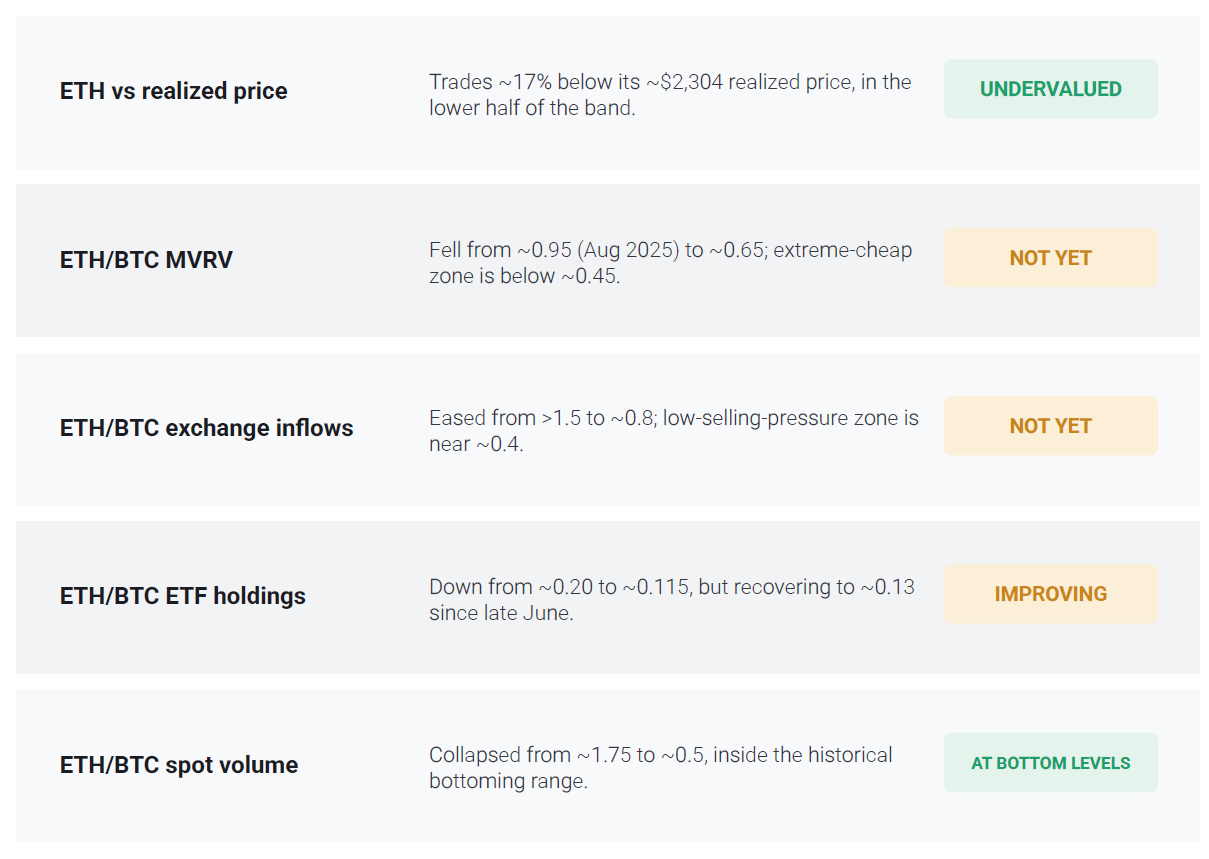

Ether is becoming increasingly attractive from a valuation standpoint, particularly relative to Bitcoin, but onchain data suggests the market has yet to reach a definitive cycle bottom, according to CryptoQuant.

In its latest weekly report, the analytics company said Ether (ETH) is trading roughly 17% below its realized price, or the average onchain acquisition cost of all ETH in circulation, of about $2,300. Historically, ETH trading below its realized price has coincided with periods of market undervaluation and long-term bottoms.

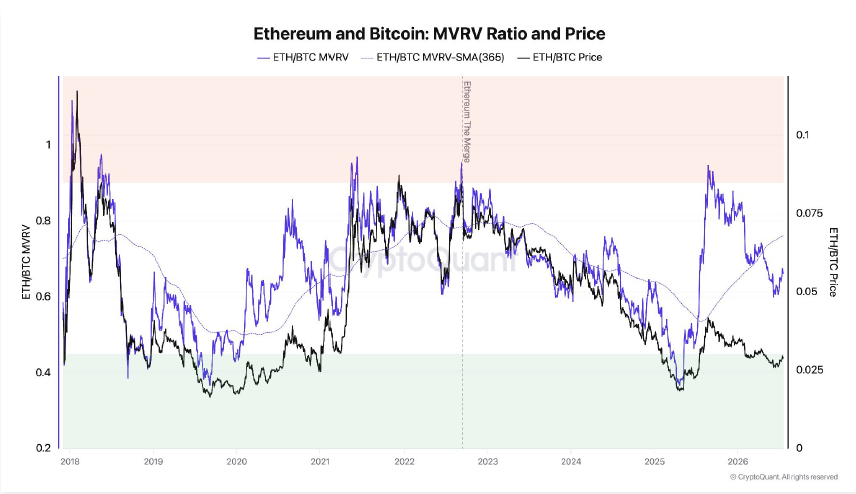

Ether is also showing signs of improving relative to Bitcoin (BTC). CryptoQuant said that ETH’s market value-to-realized value (MVRV) ratio has retreated from extreme overvaluation, exchange inflows have declined, exchange-traded fund (ETF) holdings have begun to recover after months of weakness, and ETH/BTC spot trading volumes have fallen into a range historically associated with market bottoms.

CryptoQuant says two of five key ETH bottoming indicators have been confirmed. Source: CryptoQuant

Even so, only two of CryptoQuant’s five bottoming indicators have reached historical reversal levels. The remaining metrics are improving but have yet to reach the extremes that have marked previous cycle lows, suggesting Ethereum’s bottom may still be forming.

The report comes as Ether briefly climbed above $1,950 this week and Bitcoin topped $67,000, buoyed by optimism surrounding the US CLARITY Act. At the same time, some market analysts have pointed to the potential for capital to rotate out of richly valued AI stocks and back into crypto, a shift that could further support Ether if risk appetite broadens.

The ETH/BTC MVRV ratio has fallen from nearly 0.95 in August 2025 to around 0.65, signaling that Ethereum has become significantly cheaper relative to Bitcoin. Source: CryptoQuant

Related: Grayscale plans regular cash payouts from ETH, SOL staking rewards

Ethereum supply tightens as exchange outflows and staking climb

Ethereum has shown several constructive onchain signals over the past month. During the week beginning June 29, withdrawal activity on Binance, the world’s largest crypto exchange by trading volume, climbed to its highest level in more than three years.

Analysts generally interpret sustained exchange outflows as a sign that investors are moving assets into self-custody or staking rather than keeping them on exchanges for potential sale, although such flows do not guarantee accumulation.

Meanwhile, a record 34% of Ethereum’s circulating supply is now staked, according to Staking Rewards. As Cointelegraph previously reported, higher staking participation reduces the amount of ETH readily available for trading, potentially easing short-term selling pressure if demand remains resilient.

Tom Lee’s Bitmine Immersion Technologies, the biggest corporate ETH holder, continues to accumulate Ether, boosting its holdings by 325,000 ETH over a one-month period, despite sitting on large unrealized losses. It has set a target to hold 5% of the second-biggest crypto.

Related: Will the US get CLARITY this week? Bitcoin’s new $80K target: Hodler’s Digest, July 19

Cabinet on sun loungers? Andy Burnham’s Love Island premiership

Crypto Industry to Contribute $55B to US Economy in 2026: NCA Study

Diokno steers prosecution to major win on Duterte financial records

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread – Corporette.com

-

Politics5 days ago

Politics5 days agoThe House | The City of London can help the new chancellor deliver growth in every postcode

-

Crypto World5 days ago

Crypto World5 days agoRipple Payments Joins MiCA With 14 Firms, Does It Mean Anything For XRP?

-

Crypto World6 days ago

Crypto World6 days agoTwo July Windows Left: The CLARITY Act’s Senate Fight and What Failure Means

-

Politics4 days ago

Politics4 days agoDemocrats look to World Cup watch parties to register thousands of voters

-

Crypto World6 days ago

Crypto World6 days agoRipple wins EU-wide access as ESMA adds it to MiCA register

-

Crypto World2 days ago

Crypto World2 days agoGrayscale Files For Worldcoin ETF, WLD Registers Sharp Rise

-

NewsBeat3 days ago

NewsBeat3 days agoUnregistered fitter used Gas Safe logo on business flyers

-

Tech3 days ago

Tech3 days agoSail Virtually Aboard The “Itanic” With IA-64 Emulator

-

Crypto World7 days ago

Crypto World7 days agoInjective Submits SEC Transfer-Agent Registration to Onchain Ownership Records

-

Tech3 days ago

Tech3 days agoTurtle Beach Command Series KB7 review: a nifty screen-equipped gaming keyboard

-

NewsBeat6 days ago

NewsBeat6 days agoRegistration is now open for March for Men with Kev 2026

-

Business2 days ago

Business2 days agoNew Jersey voter registration controversy explained: How 6,600 noncitizens got on the rolls, and what happens next

-

Crypto World7 days ago

Crypto World7 days agoClaude Fable 5 Slips to Second in AI Coding Leaderboard

-

News Videos7 days ago

News Videos7 days agoMoney | Class 12 Economics | CBSE Board Exam 2026-27

-

Business7 days ago

Business7 days agoBanco Bilbao Vizcaya Argentaria, S.A. (BBVA) Discusses Global Macro Environment and Economic Outlook for Core Markets Transcript

-

Crypto World5 days ago

Crypto World5 days agoKaspersky exposes OkoBot’s 20-module crypto wallet attack

-

News Videos4 days ago

News Videos4 days agoBig Money Is Entering XRP

-

Business6 days ago

Business6 days agoAirlines warn Sunshine Protection Act could disrupt flight scheduling

-

NewsBeat6 days ago

NewsBeat6 days agoDurham County Council to send out electoral registration emails

You must be logged in to post a comment Login