Crypto World

Bitcoin 2026 ETF Sell-Off Purifies the BTC Bull Case, Analysis

Bitcoin (CRYPTO: BTC) stands at a turning point as institutional participation deepens and exchange-traded products reshape the trajectory of the largest crypto asset. Eric Jackson, founder of EMJ Capital, describes a coming wave of “purification” in which long-horizon capital becomes a more persistent buyer, even as price momentum remains tethered to ETF flows. Recent weeks have featured persistent net outflows from U.S. spot BTC ETFs, reinforcing a bearish tilt in the near term, yet Jackson argues that the industry is not failing as an asset class so much as redefining its owners and its catalysts. The market’s attention has shifted to the way Bitcoin interacts with broader markets, particularly through the lens of large equity ETFs and the evolving holdings of institutional investors.

Key takeaways

- Bitcoin has evolved into a high-beta tech position driven by ETF structures and institutional participation, with price dynamics increasingly echoing tech equities.

- Despite ongoing net outflows from U.S. spot BTC ETFs, the prevailing view is that the flow pattern may shift as longer-term institutional buyers re-emerge as meaningful holders.

- Stablecoin supply on exchanges needs to recover to counter prevailing bearish momentum and inject fresh liquidity into the market.

- Bitcoin’s price moves are closely tied to the performance of large ETFs like IGV (EXCHANGE: IGV), complicating the narrative that BTC is merely a store of value.

- The next wave of buyers could come from sovereign wealth funds, corporate treasuries, and other patient capital that plans to hold BTC for decades instead of quarters.

Tickers mentioned: $BTC, $IGV, $IBIT

Sentiment: Neutral

Price impact: Negative. BTC dipped below $63,000 amid ETF outflows.

Market context: The story sits at the intersection of ETF-driven liquidity, the risk-on attitude of macro markets, and the pursuit of longer-term capital that could redefine Bitcoin’s role beyond a short-term driver of price action.

Why it matters

The core argument explored by Jackson is that the current ETF environment is not a repudiation of Bitcoin’s thesis but a reconfiguration of who owns BTC and why. He notes that Bitcoin’s recent price action has been highly reactive to the behavior of large tech-focused baskets rather than gold-like stability, underscoring a shift toward a “high-beta tech position.” This is not a condemnation of Bitcoin as an asset; it highlights how ETF architecture can amplify or dampen moves depending on the flow dynamics of large holders.

In a contrast to 2021’s retail-driven exuberance, this cycle has institutions acting as the marginal buyers, with retail money gravitating toward other tech equities. The outcome, Jackson argues, could be a new equilibrium in which long-duration capital, less prone to rapid rebalancing, steps in as a stabilizing influence over time. This shift is underscored by the fact that the largest spot BTC ETF provider, via BlackRock, operates IBIT (EXCHANGE: IBIT), a vehicle that reframes who actually owns BTC and how its supply is interpreted in the broader market. In his words, “IBIT changed who owns Bitcoin.”

“BTC didn’t fail as an asset. It succeeded as an ETF. And that’s the problem.”

The analysis also points to a broader ecosystem dynamic: as exchange-traded products accumulate assets, their flows can become a dominant price driver, even if the asset itself remains in a longer-term growth trajectory. Jackson emphasizes that the true test is not immediate price action but the durability of new ownership patterns—whether sovereign wealth funds, corporate treasuries, and patient capital will embrace BTC as a decades-long holding rather than a quarterly rebalancing instrument. The evolution toward such ownership could act as a counterweight to cyclical pressures and help Bitcoin resist the pull of any single macro narrative.

“IBIT changed who owns Bitcoin.”

Market data cited in the commentary show a continued pattern of ETF outflows in the U.S. spot market, with sector-wide momentum often tied to the fate of the IGV (EXCHANGE: IGV), the BlackRock-run tech software ETF that remains a barometer for Bitcoin’s near-term price direction. Jackson notes a stark relationship: when IGV sells off, BTC tends to slide in tandem. This linkage reinforces the view that Bitcoin, for now, functions more as a risk-on tech proxy than as a pure store of value, a reality that could persist until a broader base of durable, long-horizon buyers emerges.

On the bearish side, data from Farside Investors indicate net outflows from US spot BTC ETFs topping the $200 million mark on a single day, reinforcing the delicate balance between supply and demand in the current environment. This outflow backdrop coincides with BTC/USD trading beneath recent support zones and with the market contemplating a potential macro bottom near the $50,000–$60,000 range. Yet the rhetoric around purification—an upgrade in the quality and durability of BTC ownership—offers a counter-narrative: the next phase could bring steadier demand from capital that does not chase quarterly returns but seeks a multi-year thesis aligned with the future of digital assets in institutional portfolios.

For observers, the key question remains: will the bears be proven right in the near term, or will the emergence of longer-duration capital push BTC toward new, steadier footing? Jackson’s framing suggests the latter, arguing that every cycle clears weak hands and paves the way for a more durable, patient class of buyers that can compress volatility over time. The bear-case focuses on current price behavior and ETF-outflow metrics; the bull-case centers on a structural shift in ownership that could re-anchor Bitcoin to a longer horizon rather than a shorter trading horizon.

As the market absorbs this tension, the role of stablecoins and liquidity in exchange ecosystems will be crucial. Jackson highlights a potential bullish trigger in the stabilization and expansion of stablecoin supply on venues where BTC trades, arguing that liquidity depth and cross-asset flows will better support a longer-duration investment thesis. The broader takeaway is not a single catalyst but a sequence of developments: improved ownership dispersion, more patient capital, and a liquidity backdrop capable of supporting larger, more durable bets on BTC’s future.

Ultimately, the narrative is not about abandoning the Bitcoin thesis but about reframing it in the language of institutions and ETFs. If “purification” proves to be a meaningful transition rather than a temporary lull, BTC could transition from a speculative cycle-driven asset to a more mature component of diversified institutional portfolios. That is the arc Jackson envisions: a gradual reweighting of the BTC thesis as the market benefits from a new class of owners who cross asset boundaries and commit to holdings that endure beyond quarterly reporting cycles.

For readers, the implications extend beyond price action. If the trend toward long-horizon ownership takes hold, Bitcoin could see more predictable demand patterns, reduced reliance on fickle retail speculation, and a broader acceptance within traditional investment portfolios. The coming months will be telling as ETF flows, stablecoin dynamics, and the behavior of IGV and IBIT converge to shape Bitcoin’s role in the institutional narrative.

What to watch next

- Watch for the end of IGV-driven selling pressure and any decoupling of BTC price from tech-equities movements.

- Observe whether stablecoin supply resumes growth on major exchanges, potentially altering liquidity dynamics.

- Track net flows into IBIT and other spot BTC ETFs as a gauge of increasing long-term institutional interest.

- Monitor commentary from sovereign wealth funds and corporate treasuries regarding BTC allocations and long-horizon positioning.

- Pay attention to price levels around the $50k–$63k range and any signals from volume that could precede a new phase of demand.

Sources & verification

- Eric Jackson’s X post discussing BTC price strength and the ongoing institutional exodus.

- Spot Bitcoin ETF net flows coverage detailing five weeks of net outflows.

- BlackRock’s position in BTC via IGV and the role of IBIT, the iShares Bitcoin Trust.

- Farside Investors’ data on netflows for Bitcoin ETFs.

- Historical references to BTC price behavior on macro timelines and timeline-based targets mentioned in market commentary.

Market reaction and the next phase for Bitcoin

Bitcoin (CRYPTO: BTC) is navigating a landscape where ETF mechanics and institutional involvement increasingly dictate price action, even as longer-horizon capital begins to align with a more durable ownership thesis. From Jackson’s perspective, the current environment is not a failure of Bitcoin’s core premise but a maturation of its ownership structure. He points to the fact that Bitcoin’s popularity as an ETF instrument has transformed who holds it and why, a transformation that could ultimately stabilize demand and reduce the volatility that has characterized the asset in previous cycles. In his framing, the “purification” process refines the Bitcoin thesis by pushing it toward a cohort of buyers capable of maintaining positions across a variety of market regimes.

IGV’s behavior—an influential proxy for tech-sector risk appetite—has underscored the degree to which BTC’s macro environment remains tethered to broader equity flows. The relationship is not a perfect one, but it has become a meaningful driver in days of outsized ETF activity. The linked commentary suggests that if IGV ceases its selling pressure, BTC could benefit from a re-tightening correlation and a broader base of liquidity that supports more stable trading ranges. IBIT, as a cornerstone of BTC exposure within a regulated ETF framework, represents a structural shift in ownership that could cement a longer-term, institutional footprint in the Bitcoin ecosystem.

Despite near-term headwinds, the long arc of this narrative remains optimistic for holders who are patient and disciplined. The prospect of sovereign wealth funds and corporate treasuries adopting BTC as a dedicated, multi-year allocation is the biggest potential inflection point described by Jackson. If realized, this shift would move Bitcoin beyond episodic cycles of price strength tied to fundraising or speculative sentiment, toward a steadier, more resilient accumulation that could redefine Bitcoin’s role in the global financial system over the coming decade. In the near term, traders will watch for liquidity signals, ETF flow trends, and the evolving interaction between BTC and large tech-equity benchmarks as the market slowly prices in a longer horizon reality.

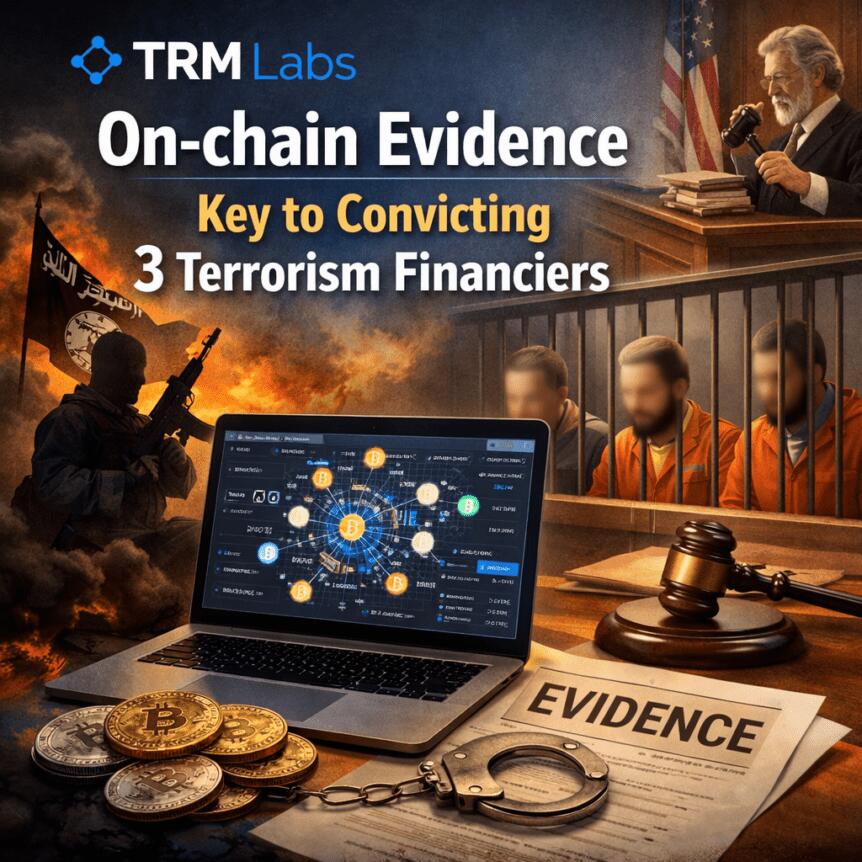

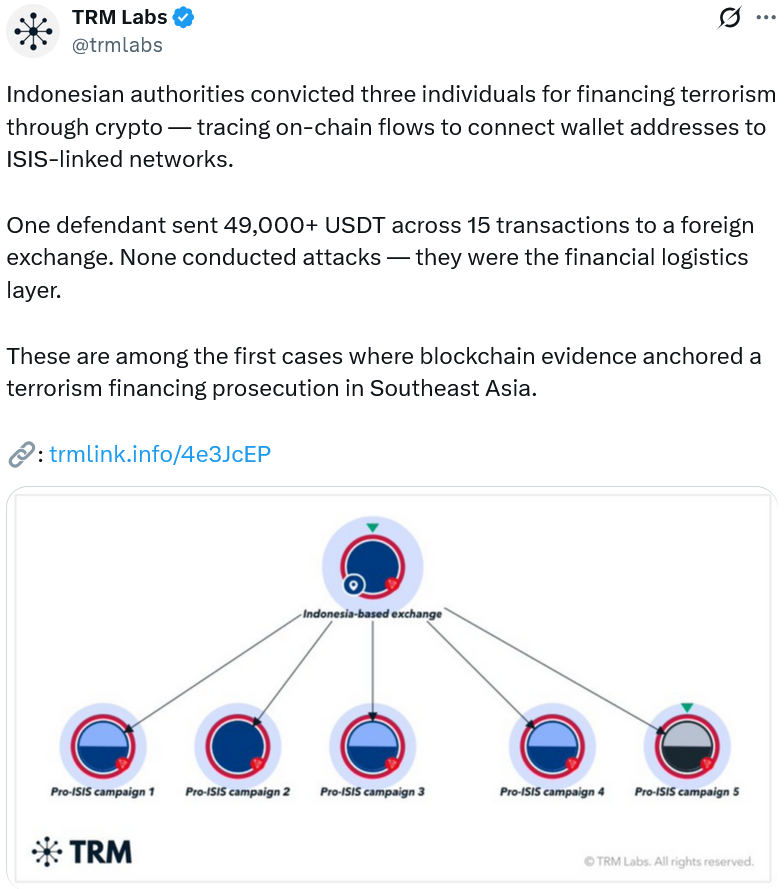

Indonesia’s courts are increasingly accepting on-chain evidence as a legitimate basis for terrorism-financing prosecutions, marking a notable shift in how blockchain data is treated in legal proceedings. In cases resolved in 2024 and 2025, authorities relied on wallet addresses, transaction histories, and on-chain flows to build the narrative of illicit funding, a development highlighted by TRM Labs as a sign that crypto traces are becoming a cornerstone of prosecutorial work.

“Indonesian courts have demonstrated that cryptocurrency evidence — wallet addresses, transaction histories, on-chain flows — is not only admissible but can anchor a terrorism financing prosecution,” said TRM Labs in a statement. The firm adds that these cases reflect a broader trend in which regulators and law-enforcement agencies are nearing parity with traditional financial channels when pursuing illicit financing.

TRM noted that terrorism-financing networks have increasingly used cryptocurrency as a movement mechanism, partially because authorities have historically scrutinized fiat channels more intensively. However, the framework is evolving, with courts and investigators reportedly closing the gap between digital traces and real-world consequences.

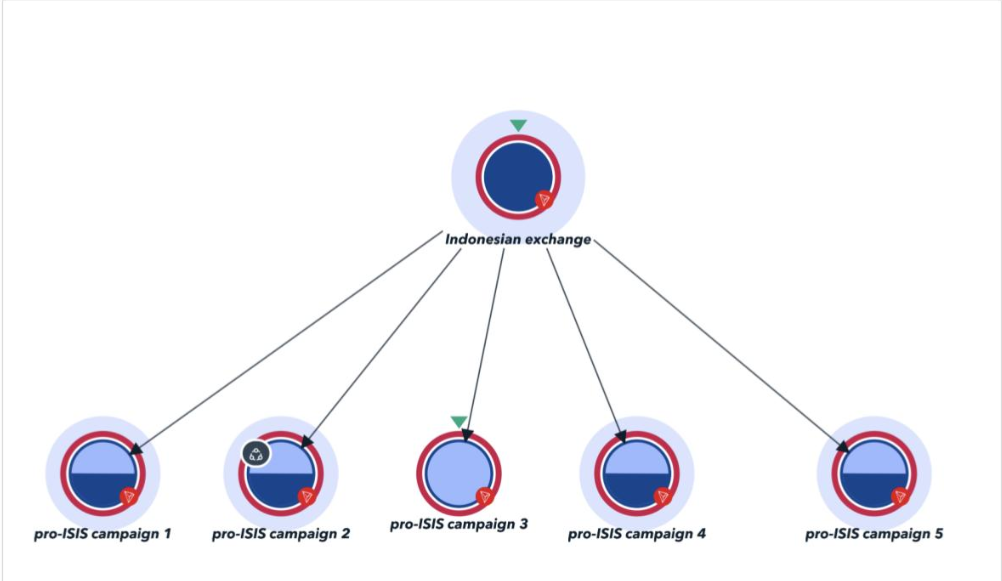

In Indonesia, one defendant allegedly sent more than $49,000 in USDt across 15 transactions from a domestic exchange to a foreign platform, with funds later routed to an ISIS-linked fundraising campaign in Syria, according to blockchain analytics cited by TRM Labs. The tracing work was conducted by Indonesia’s financial intelligence unit and the counterterrorism police unit, Densus 88, who presented the findings to the courts. The blockchain data was deemed a pivotal piece of evidence in each of the three cases.

TRM Labs emphasized that the Indonesian case underscores a broader Southeast Asian push to harness blockchain intelligence in criminal investigations, as authorities increasingly view crypto-forensics as a critical enforcement tool.

“Similar patterns are emerging across Southeast Asia, where governments are investing in blockchain intelligence capabilities and enhancing collaboration between public and private sectors to address illicit finance risks.”

Beyond Indonesia, regional authorities are building capacity to trace cryptocurrency flows. TRM noted that Singapore and Malaysia’s financial-intelligence units and law-enforcement agencies are expanding technical capabilities to follow crypto activity across borders, reflecting a growing regional emphasis on digital-forensics as part of anti-financial-crime strategies.

These developments sit against a broader backdrop of regional enforcement and cases that illustrate the expanding role of crypto-tracing tools in Southeast Asia. In April, Cambodian and Chinese authorities extradited Li Xiong, a leader of the Huione Group, to China to face fraud and money-laundering charges connected to the organization’s scam operations. The move followed the earlier arrest of Chen Zhi, the head of Prince Group, which operates the Huione network. Separately, TRM’s data from 2025 showed a surge in illicit stablecoin activity, with about $141 billion worth of stablecoins flowing to illicit entities, marking a five-year high in this space.

Key takeaways

- Indonesian courts are increasingly accepting on-chain data — including wallet addresses and transaction histories — as admissible and pivotal evidence in terrorism-financing prosecutions.

- A concrete case linked more than $49,000 in USDt moved across 15 transactions from a local exchange to a foreign platform, with funds ultimately directed to ISIS-linked fundraising in Syria.

- Regional significance is growing: Southeast Asian authorities are expanding blockchain-forensics capabilities and fostering cross-sector collaboration to tackle illicit crypto activity.

- TRM data points to a broader scale of illicit crypto use in 2025, including a substantial surge in illicit stablecoin activity, underscoring why forensics capacity matters for regulators and law enforcement.

Courts and crypto traces: what changed in Indonesia

Central to the Indonesian cases was the application of blockchain analytics by the country’s financial intelligence unit in tandem with Densus 88, the national counterterrorism police unit. By correlating on-chain activity with exchange flows and cross-border transfers, investigators constructed a continuous chain of custody from a domestic source to an international donor and ultimately to a fundraising operation tied to ISIS. The courts’ acceptance of these traces signals a shift in evidentiary standards, aligning digital footprints with traditional investigative records.

TRM’s analysis frames this development as part of a wider trend in which prosecutors are learning to treat crypto evidence not as an adjunct but as a core element of financial-crime cases. The implications for investors and operators are nuanced: while the cases demonstrate that crypto-era enforcement is moving toward greater scrutiny, they also underscore the increasing value of transparent, auditable on-chain activity as a legal tool.

Regional momentum and what it means for the market

The Indonesian trajectory is occurring amid a regional mobilization to fortify crypto-forensics. Southeast Asia is seeing a push to scale capabilities that can trace crypto flows across borders, with Singapore and Malaysia cited as examples of jurisdictions expanding their analytical arsenals and public-private collaboration. For market participants, the trend translates into a more predictable regulatory environment around digital-asset tracing, even as enforcement remains vigilant against abuse.

From an investor perspective, the trend raises several practical considerations. First, the integrity of on-chain evidence can influence case outcomes, potentially elevating the risk-reward calculus for illicit actors and increasing the likelihood of sanctions or asset seizures in connected networks. Second, as authorities invest in blockchain intelligence tools, exchanges and custodians may be called upon to provide faster or more granular data, which could affect due-diligence timelines and compliance costs. Third, the regional emphasis on cross-border cooperation could help standardize some investigative approaches, reducing ambiguity for global firms operating in multiple markets.

Broader enforcement context and ongoing developments

The Southeast Asian enforcement narrative extends beyond Indonesia. In a related development, Li Xiong, a leader of the Huione Group, was captured in Cambodia and China and extradited to China to face fraud and money-laundering charges tied to scam operations. This came three months after the arrest of Chen Zhi, head of the Prince Group, which operates Huione. In parallel, TRM reported that illicit stablecoins activity reached about $141 billion in 2025, signaling a five-year high and reinforcing the importance of robust tracing capabilities for regulators and financial institutions alike.

Taken together, these pieces illustrate a broader pattern: as crypto tracing tools mature and cross-border cooperation intensifies, authorities appear increasingly confident in leveraging on-chain data to pursue financial crime, including terrorism financing. For market participants, that means continuing attention to compliance, transparent corporate disclosures, and readiness to respond to regulatory expectations around crypto-asset flows.

Readers should monitor ongoing capacity-building efforts among Southeast Asian FIUs and law-enforcement agencies, as well as any new court rulings that further define the role of on-chain evidence in criminal cases. The evolving landscape will shape both risk and opportunity for exchanges, wallets, and institutional actors operating in the region.

Bitcoin price struggled to maintain footing above the $70,000 level as traders waited for clearer direction from ongoing geopolitical negotiations between the United States and Iran.

Summary

- Bitcoin remains capped below $70K as traders await clarity on US Iran ceasefire talks.

- Institutional demand continues to absorb supply, with accumulation trends outpacing miner issuance.

Bitcoin briefly climbed past $70,200 earlier in the week after reports suggested both sides were exploring terms for a temporary ceasefire that could ease pressure on global energy markets.

Discussions appear to be advancing behind the scenes, with multiple regional intermediaries involved in shaping a framework that could pause hostilities for several days before moving into wider negotiations.

People familiar with the situation have indicated that both Washington and Tehran have received a proposal that could initiate talks around reopening the Strait of Hormuz.

At the same time, United States President Donald Trump repeated his warning that Iran would face severe consequences if it failed to comply with the outlined conditions.

“I won’t go further because there are other things that are worse than those two,” he said, reinforcing earlier threats targeting infrastructure.

Trup has set a deadline for 8 pm Eastern time on Tuesday, and market participants are closely tracking any signal of progress or breakdown in negotiations.

As a result, price action has remained hesitant near the key psychological support at $70,000. Traders have become reluctant to commit in either direction before the geopolitical outcome becomes clearer.

A confirmed agreement could open the door for a move toward the $75,000 region, as easing tensions would likely support risk appetite across financial markets.

Failure to reach a deal could shift sentiment in a different direction, with Bitcoin once again attracting attention as an alternative store of value during periods of uncertainty.

Iranian officials, however, have yet to signal acceptance of the proposed terms and continue to insist that shipping routes will remain restricted until compensation and sanctions relief are addressed.

That stance has kept upside moves in check, with repeated attempts to break higher running into resistance as sellers step in near recent highs.

Institutions continue buying

Underneath the surface, demand has remained firm, with accumulation continuing to absorb a significant portion of newly issued supply.

Bitcoin treasury firm Strategy has continued to accumulate Bitcoin at a pace that exceeds the supply produced by miners.

Since early March, Strategy has acquired 46,233 BTC. During the same time, miners have produced only about 16,200 BTC. This means Strategy has acquired nearly three times the fresh supply.

At the same time, inflows into spot Bitcoin ETFs have also turned positive.

Such conditions have limited the depth of pullbacks, even as technical setups point toward potential weakness.

However, on the macro side, rising bond yields are introducing a competing force for capital.

Yields on the United States 5-year Treasury have climbed to around 4% from 3.55%, signaling that investors are seeking higher returns from government debt amid ongoing uncertainty.

Elevated energy prices and increased fiscal spending tied to military activity have contributed to inflation concerns, which in turn are influencing bond markets.

A successful ceasefire could reinforce confidence in Treasuries, encouraging some investors to rotate away from alternative assets, including Bitcoin.

For now, price remains caught between steady accumulation and external pressures, with the next move likely to hinge on developments in the geopolitical backdrop.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Indonesian courts convicted three individuals for terrorism financing in 2024 and 2025, using onchain evidence as the backbone of each prosecution.

The cases mark a clear shift in how Southeast Asian courts treat blockchain data, with wallet addresses and transaction histories now serving as admissible, case-anchoring evidence.

How Blockchain Data Built the Case

Indonesia’s financial intelligence unit, PPATK, worked alongside the country’s elite counterterrorism police unit, Densus 88, to trace crypto transactions tied to all three defendants.

None of the individuals carried out attacks directly. Instead, they collected, transferred, and converted funds into crypto to move money to terror networks.

One defendant sent more than $49,000 worth of Tether (USDT) across 15 transactions from a local Indonesian exchange to a foreign platform.

Those funds were later routed to an ISIS-linked fundraising campaign in Syria, according to TRM Labs.

“Indonesian courts have demonstrated that cryptocurrency evidence… is not only admissible but can anchor a terrorism financing prosecution,” read an excerpt in the TRM Labs report.

A Regional Trend Takes Shape

Indonesia is not acting alone. TRM Labs noted that Singapore, Malaysia, and other Southeast Asian jurisdictions are all investing in blockchain intelligence capabilities.

The firm described a broader regional pattern in which terror cells have turned to cryptocurrency precisely because regulators were slow to apply the same scrutiny they give traditional fiat channels.

On April 1, Cambodian and Chinese officials captured Li Xiong, the former chairman of Huione Group. The organization allegedly served as a hub for scam centers that carried out “pig butchering” frauds and other crypto theft schemes.

Xiong was extradited to China, where he faces fraud and money-laundering charges. His arrest came three months after the capture of Chen Zhi, the head of Prince Group, which operates Huione Group.

TRM reported separately in February that illicit entities received roughly $141 billion worth of stablecoins in 2025, a five-year high. Sanctions-related activity accounted for 86% of all illicit crypto flows that year.

These Indonesian convictions signal that the window for using crypto to quietly finance terrorism is closing, particularly as courts across the region accept blockchain data as prosecution-ready evidence.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post $49,000 in Stablecoins Leads Investigators Straight to ISIS appeared first on BeInCrypto.

Gibraltar has long been a hub for online gambling, and the rise of crypto casinos has added an exciting new dimension. If you’re looking for the best crypto casinos available in Gibraltar, you’ve come to the right place.

We’ve spent countless hours researching and testing crypto gambling sites that cater to players in Gibraltar. Our goal is to help you find a safe, fun, and rewarding experience.

We have personally tested and reviewed each site on the list, you can read our in depth reviews below.

Let’s dig in…

Top Gibraltar Casinos

- Massive game library with 11,294 titles from 63 providers

- Accepts 20 different cryptocurrencies with multiple network options

- Generous welcome bonus package worth up to $5,000 plus 75 free spins

- Unique dragon-themed loyalty program with rakeback up to 20%

- Comprehensive sports betting covering traditional sports and esports

- Fast crypto withdrawals processed within 24 hours

- Low minimum deposit of $1

- Provably fair games with verifiable outcomes

- User-friendly interface with intuitive navigation

- Massive selection of games

- Quality live dealer offering

- Crypto and fiat payment options

- Varied welcome offers and bonuses

- Up to 70% Rakeback + 10% Cashback

- Unlimited deposits and withdrawals

- Exclusive Thrill Original games

- 1500+ Casino Games from the Top Providers

- Truly anonymous and private gambling – no personal details or accounts required

- Innovative blockchain competitions with big ETH prize pools and NFT rewards

- Instant, fee-free deposits and withdrawals directly to/from your crypto wallet

- Instant Web3 withdrawals up to 100K USD

- Simple, user-friendly platform design with great mobile compatibility

- No KYC & VPN Friendly anonymous casino

- Zero fees, instant deposits & withdrawals

- 5,000+ casino games & sports betting without limits

- 10% Weekly Cashback

- Generous welcome bonus up to 1 BTC

- 8,000+ games including slots, casino, sports betting, crypto betting

- 470% Welcome Bonus & 400 Free Spins

- Supports 18+ major cryptocurrencies for deposits and withdrawals

- Smooth and user-friendly interface

- Massive game library with 11,294 titles from 63 providers

- Accepts 20 different cryptocurrencies with multiple network options

- Generous welcome bonus package worth up to $5,000 plus 75 free spins

- Unique dragon-themed loyalty program with rakeback up to 20%

- Comprehensive sports betting covering traditional sports and esports

- Up to 70% Rakeback + 10% Cashback

- Unlimited deposits and withdrawals

- Exclusive Thrill Original games

- 1500+ Casino Games from the Top Providers

- Fast crypto withdrawals processed within 24 hours

- Low minimum deposit of $1

- Provably fair games with verifiable outcomes

- User-friendly interface with intuitive navigation

- Massive game variety with over 6,000 slots, tables, specialty and live titles

- Huge sportsbook covering 40+ leagues including niche options

- Instant withdrawals to crypto wallets for fast access to funds

- Generous recurring sports betting promotional offers

- 8,000+ games including slots, casino, sports betting, crypto betting

- 470% Welcome Bonus & 400 Free Spins

- Supports 18+ major cryptocurrencies for deposits and withdrawals

- Smooth and user-friendly interface

- Truly anonymous and private gambling – no personal details or accounts required

- Innovative blockchain competitions with big ETH prize pools and NFT rewards

- Instant, fee-free deposits and withdrawals directly to/from your crypto wallet

- Instant Web3 withdrawals up to 100K USD

- Simple, user-friendly platform design with great mobile compatibility

- Wide range of cryptocurrencies accepted

- Large selection of games (7,000+), including slots, table games, and live casino options

- Sports betting platform integrated

- Fast deposit and withdrawal processing times

- Attractive welcome bonus and ongoing promotions

- Instant withdrawals processed on the blockchain

- Generous welcome bonus of 200% up to 1 BTC + 50 free spins

- Wide selection of games from top providers like Evolution, Pragmatic Play, Hacksaw

- Offers a sportsbook in addition to casino games

- Innovative features like Telegram integration and WalletConnect

- Huge selection of over 2,700 games from top providers

- Lucrative 200% deposit bonus up to €25,000

- Wide variety of cryptos supported

- Instant withdrawals

- Cutting-edge Telegram & WalletConnect integration

- No KYC & VPN Friendly anonymous casino

- Zero fees, instant deposits & withdrawals

- 5,000+ casino games & sports betting without limits

- 10% Weekly Cashback

- Generous welcome bonus up to 1 BTC

- Large game selection with over 6,000 titles from top providers

- Generous crypto welcome bonus up to 50 mBTC

- Fast withdrawals through cryptocurrency support

- Slick, intuitive site design optimized for mobile

- Live chat provides quick customer support

- Instant withdrawals for crypto currencies

- Huge selection of slots and table games

- Instant play site needs no downloading

- VIP program rewards loyal players

- Huge selection of over 9408 casino games from top providers

- Extremely generous 100% match welcome bonus up to 999 BTC

- Supports all major cryptocurrencies for payments

- Smooth and fast site with flawless mobile optimization

- 24/7 live chat and email customer support

- Lucrative 300% welcome bonus for new players

- Supports over 15 popular cryptocurrencies

- Huge selection of over 2,000 casino games

- Competitive odds and props available on 25+ sports leagues

- Highly Recommended by Blockonomi

- Massive selection of over 7000 games from leading providers

- Quick withdrawals, especially for cryptocurrencies

- Multi-tier VIP program with escalating rewards

- Generous ongoing promotions like free spins and reload bonuses

- Huge selection of betting markets across dozens of sports

- Extensive casino game portfolio with hundreds of slots and table games

- Ongoing promotions, prize drops, cashback, and VIP program

- Responsive 24/7 customer support via live chat and email

- Massive selection of games

- Quality live dealer offering

- Crypto and fiat payment options

- Varied welcome offers and bonuses

- Telegram integration for seamless gambling within the messaging app

- No KYC required for completely anonymous play

- Impressive selection of 5,000+ games from top providers

- Native TGC token offering 25% cashback and profitable staking options

- Fast cryptocurrency transactions with instant deposits and quick withdrawals

- Huge selection of over 5000 games from top providers

- Instant withdrawals for cryptocurrencies

- Regular promotions like free spins and reload bonuses

- 8-tier VIP program with escalating rewards

- Huge selection of over 8,000 casino games and sports betting options

- Generous welcome bonuses up to $3,500 in value plus free spins

- Lucrative loyalty program with escalating cashback rewards

- Quick crypto deposits & withdrawals in over 40 coins/tokens

- Staking system to earn native BFG tokens as you play

Gibraltar Casino Reviews

Zunabet

Zunabet

Welcome Bonus of 250% up to $5000 + 75 Free Spins

ZunaBet is a crypto casino offering over 11,000 games from 63 providers, extensive sports betting options across traditional and eSports, and a generous welcome package of 250% up to $5000 with 75 free spins

- Massive game library with 11,294 titles from 63 providers

- Accepts 20 different cryptocurrencies with multiple network options

- Generous welcome bonus package worth up to $5,000 plus 75 free spins

- Unique dragon-themed loyalty program with rakeback up to 20%

- Comprehensive sports betting covering traditional sports and esports

ZunaBet is a brand new crypto casino and sportsbook that launched in 2026. The site has over 11,000 games from 63 providers and accepts 20 different cryptocurrencies for deposits and withdrawals.

Key Features

- Massive Game Selection – ZunaBet offers 11,294 casino games including slots, table games, and live dealer options. Players can choose from titles by top providers like Pragmatic Play, Hacksaw Gaming, and Playtech.

- Crypto Payment Options – The casino accepts 20 cryptocurrencies including Bitcoin, Ethereum, Dogecoin, and multiple stablecoin options on different networks. Transactions process quickly, with most deposits confirming within minutes.

- Dragon Loyalty Program – Players progress through six tiers from Squire to Ultimate by wagering on games. Higher tiers unlock better rewards including up to 20% rakeback, 1,000 free spins, and VIP club access.

- Complete Sportsbook – The platform covers traditional sports like football, basketball, and tennis plus esports titles like CS2, Dota 2, and League of Legends. Live betting lets players wager as games unfold in real time.

- Mobile-Friendly Design – ZunaBet works on all devices through its responsive website and downloadable apps for iOS, Android, Windows, and MacOS. Players can access nearly all games and features from their phones or tablets.

ZunaBet delivers a solid gambling experience with its huge game library and modern cryptocurrency focus. The unique dragon loyalty program and generous welcome bonus make it worth checking out for both new and experienced players.

Thrill

Thrill

Welcome Bonus of Up to 70% Rakeback + 10% Cashback

Thrill Casino has emerged as an exciting new player in the crypto gambling space. With its sleek design, provably fair games, and cryptocurrency focus, it’s positioning itself as a forward-thinking option for modern gamblers.

- Up to 70% Rakeback + 10% Cashback

- Unlimited deposits and withdrawals

- Exclusive Thrill Original games

- 1500+ Casino Games from the Top Providers

Thrill Casino is a crypto-focused gambling platform launched in 2025, operating under Curaçao licensing. It offers a modern, sleek interface with 1,850+ slots, 80+ live dealer tables, and proprietary provably fair games.

The platform supports 15 cryptocurrencies including BTC, ETH, USDT, SOL, and DOGE, with no deposit limits and near-instant withdrawals. Instead of traditional welcome bonuses, Thrill offers up to 70% rakeback and 10% lossback, providing ongoing value without complex wagering requirements.

Key Points:

- 15+ supported cryptocurrencies

- No deposit/withdrawal limits

- Instant blockchain-speed withdrawals

- 70% rakeback + 10% lossback

- No mandatory KYC

- Provably fair original games

- Comprehensive sportsbook

- Mobile-optimized platform

- 24/7 live chat support

- Strong security measures

The casino features games from reputable providers like Evolution, Pragmatic Play, and NetEnt, plus exclusive “Thrill Originals.” Sports betting is available through BETBY integration. No KYC is required for most users, appealing to privacy-conscious players.

Cybet

- Fast crypto withdrawals processed within 24 hours

- Low minimum deposit of $1

- Provably fair games with verifiable outcomes

- User-friendly interface with intuitive navigation

Cybet Casino is a fresh addition to the online gambling world, bringing a unique frog-themed crypto platform to players since its launch in 2025. This modern casino caters primarily to cryptocurrency enthusiasts, offering seamless transactions across eight popular digital currencies.

With over 1000 games, including slots, live dealer options, and provably fair originals, Cybet delivers an engaging gambling experience wrapped in a user-friendly interface. The platform stands out for its fast withdrawals, generous bonuses, and commitment to security, making it an appealing choice for both casual players and dedicated gamblers looking for a streamlined crypto casino experience.

Key Points

- Cybet Casino launched in 2025 with an engaging frog theme and modern design.

- The platform supports 8 cryptocurrencies including Bitcoin and Ethereum.

- Players can enjoy over 1000 games with 800+ slots and 30+ live dealer options.

- The casino offers provably fair “Cybet Originals” games like Crash and Dice.

- Withdrawals process within 24 hours, often faster for crypto transactions.

- Low $1 minimum deposits make the casino accessible to all players.

- New players get a 100% match up to $500 plus 50 free spins.

- Regular players earn 20% Rakeback with no wagering requirements.

- The referral program pays 25% commission on friends’ wagers.

- VIP program offers progressive benefits with transfer options available.

Cybet Casino successfully combines innovation with accessibility, delivering a standout crypto gambling experience for players of all levels. With its diverse game selection, rapid payouts, and generous rewards system, this frog-themed platform demonstrates a clear understanding of what modern players want. The thoughtful design, robust security measures, and around-the-clock support further enhance its appeal. For cryptocurrency users seeking a fresh, reliable, and engaging online casino, Cybet offers everything needed for an enjoyable and potentially rewarding gaming journey.

Jackbit

JackBit

100% Welcome Bonus + 100 Free Spins

A crypto gaming hub packing thousands of slots, live dealers, niche sports, and instant withdrawals alongside player anonymity, JackBit Casino delivers versatile entertainment and innovations.

- Massive game variety with over 6,000 slots, tables, specialty and live titles

- Huge sportsbook covering 40+ leagues including niche options

- Instant withdrawals to crypto wallets for fast access to funds

- Generous recurring sports betting promotional offers

JackBit is a premier crypto-based online gambling site that burst onto the scene in 2022, bringing a massive game selection and sportsbook. With intuitive navigation optimized for slots, specialty titles like lottery and arcade offerings, and extensive sports betting markets, JackBit utilizes blockchain protocols to enable instant anonymous payouts.

Players can easily deposit leading cryptocurrencies to access competitive odds and niche brackets across mainstream professional leagues and esports. And with the ability to withdraw winnings in under 10 minutes,

Key Points

- Launched in 2022, licensed in Curacao, over 6,600 games and 40+ sports

- Massive variety including slots, table games, live dealers, virtual sports

- Generous sports promotions like betting insurance and free plays

- Accepts 13 major cryptocurrencies with instant, anonymous payouts

- Overall robust, innovative crypto casino and sportsbook suitable for all

With its vast selection of thousands of games across every major gambling vertical paired with extensive sports betting markets, JackBit has firmly established itself as a premier one-stop entertainment hub since entering the scene in 2022.

Most importantly, by championing player privacy through anonymous accounts and lightning fast crypto payouts, JackBit pushes iGaming forward responsibly.

For these reasons, JackBit represents an exciting new option that both recreational punters and devoted bettors should evaluate to appreciate a refined, innovative destination catering to all play styles.

Bcgame

BC.Game

470% Welcome Bonus & 400 Free Spins

BC.Game is a popular crypto-focused online casino launched in 2017 that offers over 8,000 games, generous bonuses up to 300%, and supports 18+ major cryptocurrencies and various payment methods across its sports betting, slots, table games, and live casino.

- 8,000+ games including slots, casino, sports betting, crypto betting

- 470% Welcome Bonus & 400 Free Spins

- Supports 18+ major cryptocurrencies for deposits and withdrawals

- Smooth and user-friendly interface

BC.Game is a feature-rich crypto gambling platform launched in 2017 that has quickly become a top choice for enthusiasts seeking an exciting and generous online casino.

With over 8,000 games spanning slots, table games, live casino, sportsbook, and more, BC.Game offers a smooth, mobile-friendly gambling experience for players around the world.

Keypoints

- Launched in 2017, BC.Game offers over 8,000 crypto-focused games including slots, table games, sports betting, and live casino

- Generous welcome bonuses up to 300% for new players

- Supports 18+ major cryptocurrencies like Bitcoin, Ethereum, Tether for deposits and withdrawals

- Good selection of sports betting options including football, tennis, esports

- 10,000+ slot games available from top providers like Pragmatic Play and Spinomenal

- Classic table games on offer including roulette, baccarat and blackjack

- Live casino games streamed in HD quality for an immersive experience

- Fun games like crypto price betting, lottery, bingo and horse racing also available

- Fast and helpful 24/7 live chat customer support

- User-friendly interface and mobile apps for iOS and Android

With over 8,000 games, generous bonuses, multiple crypto payment options, and a slick user interface, BC.Game has positioned itself as a top choice for crypto casino gaming since its launch in 2017.

Powered by leading gaming providers like Pragmatic Play and Evolution Gaming, the sheer variety coupled with rapid payouts across 18 cryptocurrencies makes BC.Game a one-stop shop for thrilling, trustworthy online gambling with crypto.

Throw in 24/7 live support, regular promotions, and a rewarding VIP program, and BC.Game checks off all the perks players desire in an online casino.

With so many strengths powering this nascent yet wildly popular platform, crypto gambling fans would be remiss not to give BC.Game a spin.

Metawin

MetaWin

30% Extra Free on Every Deposit! Highest RTP. Instant payouts

MetaWin is a crypto casino that delivers anonymous & provably fair gambling by allowing users to connect a Ethereum wallet to access slots, table games, live dealers & more.

- Truly anonymous and private gambling – no personal details or accounts required

- Innovative blockchain competitions with big ETH prize pools and NFT rewards

- Instant, fee-free deposits and withdrawals directly to/from your crypto wallet

- Instant Web3 withdrawals up to 100K USD

- Simple, user-friendly platform design with great mobile compatibility

MetaWin is an exciting new decentralized online casino that offers a truly innovative and anonymous gambling experience on the Ethereum blockchain.

As the first-of-its-kind web3 cryptocurrency gambling platform, MetaWin allows users to connect their Ethereum wallet to access a great selection of casino games like slots, table games, live dealer tables, and more – all while maintaining complete privacy and security.

The site’s real innovation shines through its blockchain-based competitions where users can win big ETH prize pools and valuable NFTs from popular collections, with the results transparently determined by Ethereum smart contracts to guarantee fairness.

Key Points

- Truly innovative and anonymous online casino operating on the Ethereum blockchain

- Offers complete privacy as no account creation or personal information is required

- Allows players to connect their Ethereum wallet (e.g., MetaMask) to access games

- Hosts exciting blockchain-based competitions with opportunities to win big ETH prizes

- Chance to win valuable NFTs from popular collections like Beanz and Killabears

- Transactions and gaming activity occur on the secure Ethereum blockchain

- Players retain full custody of their funds in their private crypto wallets

MetaWin is truly at the vanguard of blockchain-based online gambling. By harnessing the power of the Ethereum blockchain, it delivers an anonymous, secure, and provably fair gaming experience like no other.

From the seamless wallet integration and instant payouts to the innovative smart contract competitions and opportunities to win big ETH prizes and coveted NFTs, MetaWin represents the future of web3 crypto casinos.

For crypto enthusiasts who have been awaiting a way to enjoy casino games while taking full advantage of the inherent benefits of decentralization, anonymity, and transparency, MetaWin is undoubtedly leading the way into this new frontier.

Rakebit

Rakebit

450% Bonus & 100 Free Spins!

Rakebit Casino offers a comprehensive crypto-gambling platform with a vast game selection, user-friendly interface, and attractive bonuses, catering to both casino enthusiasts and sports bettors while prioritizing fast transactions and user privacy.

- Wide range of cryptocurrencies accepted

- Large selection of games (7,000+), including slots, table games, and live casino options

- Sports betting platform integrated

- Fast deposit and withdrawal processing times

- Attractive welcome bonus and ongoing promotions

Rakebit Casino is a popular online gambling platform that has been making waves in the crypto gaming space.

This innovative casino offers a comprehensive suite of gambling options, including an extensive collection of over 7,000 casino games, a robust sports betting platform, and an immersive live casino experience.

Catering primarily to cryptocurrency enthusiasts, Rakebit supports transactions in 10 different cryptocurrencies, ensuring fast, secure, and private banking for its users.

With attractive bonuses, a rewarding VIP program, and a commitment to fair play evidenced by its provably fair games, Rakebit has quickly established itself as a go-to destination for both casual players and serious gamblers in the world of online crypto casinos.

Key Points

- Specializes in cryptocurrency transactions, supporting 10 popular cryptocurrencies for fast, secure, and private banking

- Features a user-friendly interface with intuitive navigation on both desktop and mobile platforms

- Offers an attractive welcome bonus of up to 200 free spins for new players

- Maintains a comprehensive VIP program with 5 tiers, rewarding loyal players with increasing benefits

Rakebit Casino stands out as a top-tier choice in the world of online crypto gambling. With its vast game selection, user-friendly interface, and commitment to cryptocurrency transactions, it offers a modern and secure gaming experience.

Whether you’re a slots enthusiast, table game aficionado, or sports betting fan, Rakebit provides a diverse and engaging environment for all types of players. Its focus on fast transactions, provably fair games, and mobile accessibility further cements its position as a forward-thinking and player-centric online casino.

Megadice

Mega Dice

200% match up to 1 BTC + 50 free spins

Mega Dice Casino is a legitimate and innovative online crypto gambling platform that offers an extensive game library, generous bonuses, top-notch security features, and seamless integration with popular apps like Telegram.

- Instant withdrawals processed on the blockchain

- Generous welcome bonus of 200% up to 1 BTC + 50 free spins

- Wide selection of games from top providers like Evolution, Pragmatic Play, Hacksaw

- Offers a sportsbook in addition to casino games

- Innovative features like Telegram integration and WalletConnect

Mega Dice is an innovative online cryptocurrency casino and sportsbook that has been operating since 2023. It stands out as the world’s first officially licensed casino platform accessible via the popular Telegram messaging app.

With top-notch security features, generous bonuses, and a user-friendly interface, Mega Dice Casino has quickly established itself as a premier destination for crypto gambling enthusiasts.

Key Points

- Extensive game library with slots, table games, live casino, sportsbook, and unique crypto games

- Generous welcome bonus of 200% match up to 1 BTC + 50 free spins for new players

- Supports a wide range of cryptocurrencies for fast and secure deposits/withdrawals, including Bitcoin, Ethereum, Litecoin, and more

- Instant withdrawals processed on the blockchain for added convenience

- Regular promotions, reload bonuses, and a loyalty program to reward existing players

- Comprehensive sportsbook covering major sports leagues, events, and esports tournaments

Mega Dice Casino is a standout platform in the online cryptocurrency gambling space. With its innovative features like Telegram integration, diverse game offerings from top providers, generous bonuses, robust security measures, and a comprehensive sportsbook, it delivers an exceptional and convenient gaming experience.

The casino’s commitment to providing a secure, transparent, and user-friendly environment, coupled with its focus on cutting-edge technology and instant payouts on the blockchain, solidifies its position as a trailblazer in the industry.

Luckyblock

Lucky Block Casino

Welcome Bonus of 200% match on first deposits up to €25,000

Lucky Block offers a world-class crypto casino and sports betting platform with thousands of games, generous rewards for loyal players, fast payouts, and an overall premium interactive gambling experience.

- Huge selection of over 2,700 games from top providers

- Lucrative 200% deposit bonus up to €25,000

- Wide variety of cryptos supported

- Instant withdrawals

- Cutting-edge Telegram & WalletConnect integration

Lucky Block is a new, feature-rich crypto casino making waves in the online gambling space since its launch in late 2022. Backed by an existing cryptocurrency brand, Lucky Block leverages its solid reputation to offer players a modern casino and sportsbook supporting popular cryptos like Bitcoin, Ethereum, and Tether for deposits and withdrawals.

Slick website design optimized for desktop and mobile coupled with around-the-clock chat support cement Lucky Block’s accessibility for crypto holders worldwide.

Key Points

- Large selection of over 2,700 casino games from 50+ top providers like NetEnt and Pragmatic Play, including slots, table games, jackpots, and live casino

- Generous welcome bonus of 200% match up to €10,000 plus 50 free spins

- Wide variety of 10+ cryptocurrencies supported for fast, anonymous deposits and withdrawals

- Instant crypto withdrawals processed directly to players’ wallets

- Lucrative loyalty program coming soon with cashback, birthday bonuses, and rewards for frequent players

- Innovative features like daily jackpot drops, lottery betting, and native LBLOCK token perks

Lucky Block emerged as one of our top recommendations for crypto gamblers seeking a leading destination supporting both casino games and sports betting with digital currencies

Backed by reputable licensing and a globally-recognized crypto brand, Lucky Block offers players a secure, legal platform to enjoy thousands of slots, jackpots, live table games, and betting markets across sports leagues like the NBA and esports tournaments

Fast and easy account setup via email or Telegram allows new players to claim a generous 200% welcome bonus up to €25,000 and start playing within minutes. Lucrative ongoing promotions and imminent loyalty perks provide recurring value for regular players

It’s a great place for gamblers, sports bettors and crypto enthusiasts – check it out!

Betpanda

- No KYC & VPN Friendly anonymous casino

- Zero fees, instant deposits & withdrawals

- 5,000+ casino games & sports betting without limits

- 10% Weekly Cashback

- Generous welcome bonus up to 1 BTC

BetPanda.io is a modern crypto casino that launched in August 2023 and has quickly made a name for itself in the online gaming space. The platform combines the convenience of cryptocurrency gambling with an extensive gaming library of over 5,500 titles, instant payouts, and a user-friendly interface.

What sets BetPanda apart is its commitment to player privacy with no KYC requirements, coupled with generous bonuses including a 100% welcome bonus up to 1 BTC and weekly cashback rewards.

Key Points

- Over 5,500 games from 76 providers, including slots, live casino, and sports betting

- Ultra-fast withdrawals within 30 seconds and instant deposits with 13+ cryptocurrencies supported

- Generous 100% welcome bonus up to 1 BTC plus 10% weekly cashback with no wagering requirements

- Privacy-focused with no KYC required – only email needed to register

- 6-tier VIP program with increasing rewards and dedicated support

- 24/7 customer service with quick response times

- Clean, mobile-friendly design that works on all devices

- Secure platform with SSL encryption and two-factor authentication

- Regular tournaments and promotions for extra rewards

BetPanda.io has proven itself to be a standout crypto casino despite its relatively recent launch in 2023. With its impressive collection of over 5,500 games, lightning-fast withdrawals, and generous bonus system, it delivers everything that modern crypto gamblers are looking for.

The platform’s commitment to user privacy, combined with its robust security measures and responsive customer support, makes it a trustworthy choice for players seeking a premium crypto gaming experience.

Whether you’re a casual player or a serious gambler, BetPanda’s user-friendly interface, diverse game selection, and attractive rewards program make it a compelling destination in the world of crypto casinos.

Betplay

Betplay

Welcome Bonus Matches 100% up to 50 mBTC

With thousands of high-quality games, lucrative crypto bonuses, sleek mobile compatibility, and excellent customer support, emerging online casino Betplay delivers a polished, feature-rich experience catering to modern player preferences across devices.

- Large game selection with over 6,000 titles from top providers

- Generous crypto welcome bonus up to 50 mBTC

- Fast withdrawals through cryptocurrency support

- Slick, intuitive site design optimized for mobile

- Live chat provides quick customer support

Betplay is an emerging online crypto casino that aims to provide a modern, entertaining gambling experience through its extensive games library, lucrative bonuses, and slick platform design. Established in 2020 and licensed under a Costa Rica-based ownership group, Betplay offers over 6,000 titles across slots, table games, live dealer options and more from leading developers.

The site incentivizes new players with a generous 100% deposit bonus up to 50 mBTC while rewarding loyalty through weekly cashback and daily rakeback programs.

Betplay accepts major cryptocurrencies for fast, secure transactions and implements reasonable security controls around encryption and infrastructure monitoring.

With its expanding features and focus on user experience, Betplay shapes up as an intriguing new contender in the bitcoin casino space.

Key Points

- Offers over 6,000 casino games including slots, table games, live dealer games, and more from top providers like Microgaming and Evolution Gaming

- Lucrative welcome bonus of 100% deposit match up to 50 mBTC

- 10% weekly cashback on losses and daily rakeback rewards for loyal players

- Quick deposits and fast withdrawals through support of major cryptocurrencies

- 24/7 customer support via live chat and email with knowledgeable agents

- Allows play in free demo modes to try games risk-free before betting real money

For players seeking a modern, cryptocurrency-focused online casino, Betplay shapes up as an appealing option worth exploring.

Betplay makes a strong initial impression by getting the fundamentals right – offering a smooth, easily navigable platform across devices, expanding games library with titles from top studios, and reliable customer support response times.

The generous 100% welcome bonus matches competitors while daily rakeback and weekly cashback promotions cater to loyalty long-term.

Betplay has all the makings of a rising star worth betting on for crypto gamblers seeking quality gameplay and modern convenience.

Wild.io

Wild.io

400% Welcome Bonus up to $10,000 + 300 Free Spins

With generous crypto bonuses, instant payouts, and a smooth cross-device gameplay experience, Wild.io provides a compelling new option for cryptocurrency gamblers

- Instant withdrawals for crypto currencies

- Huge selection of slots and table games

- Instant play site needs no downloading

- VIP program rewards loyal players

Bringing innovation to the expanding galaxy of crypto gambling sites, Wild.io has offered premium entertainment since 2022. Obtaining credentials from the reputable Curacao egaming authorities and enlisting talented developers, Wild.io furnishes an abundant game selection spanning over 1,600 titles presently.

Slots steal the spotlight, but blackjack devotees, roulette fans and live stream enthusiasts find tailored action through variants and dedicated studios.

Lucrative matched deposits give way to ongoing cashback incentives, surprise bonus drops and contest entries across desktop and mobile. While constraints exist around eligibility in several countries presently, Wild.io focuses on usability, security and entertainment for crypto gamblers looking to explore modern iGaming frontiers.

Key Points

- Lucrative welcome bonus up to $5,000 + 300 free spins

- Instant withdrawals with no limits for cryptocurrencies

- Generous ongoing promotions like 77% reload matches

- Smooth, contemporary site design for desktop and mobile

- Exclusive focus on major cryptocurrencies only

- Innovative games like Crash, Plinko, Mines

- eSports and sports betting planned for the future

In an increasingly crowded crypto gambling landscape, Wild.io has carved out a distinctive niche since its 2022 founding by merging innovation with entertainment.

Lucrative sign-up rewards in the form of matched deposits and free spins continue through passive cashback, surprise bonus drops and contest entries incentivizing gameplay daily.

Swift verifications and rapid payouts cement convenience while robust cryptography and responsible gambling protocols safeguard activities for customers globally.

For those seeking a contemporary online casino experience, Wild.io makes an appealing choice to wager at your own pace.

Coinkings

CoinKings

100% Unlimited Welcome Bonus + 100 Free Spins

With a gigantic games selection, enormous 999 BTC welcome bonus, smooth performance on all devices, fast payouts, and 24/7 support, emerging crypto casino CoinKings emerges as a top destination.

- Huge selection of over 9408 casino games from top providers

- Extremely generous 100% match welcome bonus up to 999 BTC

- Supports all major cryptocurrencies for payments

- Smooth and fast site with flawless mobile optimization

- 24/7 live chat and email customer support

CoinKings is an exciting new cryptocurrency-focused online casino that aims to offer players a premium gaming experience.

Established in late 2023 by industry veterans, CoinKings brings together an enormous selection of over 9,408 casino games, generous bonus offers, smooth banking, and responsive performance across desktop and mobile.

With games delivered by major studios like NetEnt, Evolution Gaming, Pragmatic Play and more, enthusiasts of classic table games, poker, slots, live dealer tables, and other online gambling options will find top-quality entertainment catered at CoinKings.

Key Points

- Offers over 9,408 games from leading providers like NetEnt and Evolution

- Generous welcome bonus up to 999 BTC match + 150 free spins

- Accepts major cryptos for fast, anonymous payments

- Fiat currency deposits supported through integrated gateways

- Website and mobile apps optimized for all devices

- Lucrative loyalty program with 10 VIP levels

- Progressive jackpot games with big prize pools

After thoroughly testing and reviewing CoinKings’ offerings, there is no doubt this fresh new crypto gambling site establishes itself as a leading player in the market.

With its gigantic game selection from renowned studios, enormously generous 999 BTC welcome bonus and reasonable wagering terms, fast and smooth performance across all devices, and dedication to customer satisfaction through 24/7 support – CoinKings checks all the boxes.

For a fun, rewarding and polished crypto gaming environment with everything you expect from a top-rated operator, CoinKings belongs on the shortlist of casinos to join. With new titles, promotions and innovations surely on the horizon, savvy bettors would do well to secure their lucrative welcome bonus early at this rising star in crypto gambling.

Coinsgame

Coins.Game

Welcome Bonus of 300% Deposit Match Up To $1,500

Coins.Game is a feature-rich crypto gambling site with a huge casino game selection, competitive sportsbook odds, lucrative welcome bonus, fast payouts, and excellent customer support, making it an appealing option for players globally.

- Lucrative 300% welcome bonus for new players

- Supports over 15 popular cryptocurrencies

- Huge selection of over 2,000 casino games

- Competitive odds and props available on 25+ sports leagues

- Highly Recommended by Blockonomi

Coins.Game is a new online gambling site making waves in the crypto space since its launch in 2022. This platform allows players worldwide to enjoy a feature-packed casino, sportsbook, and more using popular cryptocurrencies like Bitcoin, Ethereum, and Tether for deposits and withdrawals.

The site boasts an intuitive interface optimized for desktop and mobile, multiple crypto banking options with fast payouts, and dedicated 24/7 customer support.

Key Points

- Offers over 2,000 casino games including slots, table games, and live dealer

- Comprehensive sportsbook covering 25+ leagues with competitive odds

- Accepts 15+ popular cryptocurrencies for fast, anonymous payments

- Lucrative 300% first deposit welcome bonus up to $1,500

- Regular promotions like free spins, cashback, and reload bonuses

- VIP program unlocks cashback, prizes, and other perks

With over 2,000 total casino games, a full sportsbook and esports betting options, and support for a dozen cryptocurrencies – Coins.Game aims to be a one-stop shop for crypto gamblers.

The 300% first deposit bonus up to $1,500 provides new players with a lucrative head start. Regular promotional offers like free spins, cashback deals, and prizes give you plenty of reasons to stay active in the long run. For security, Coins.Game leverages encryption, firewalls, and fraud monitoring to protect your funds and data.

So if you’re looking for a full-featured Bitcoin and altcoin casino with leading slots, tables games, live dealers, virtual sports, and sportsbook betting under one roof – give this new gambling site serious consideration.

Mirax

Mirax Casino

Welcome Bonus Totalling up to5 BTC and 300 Free Spins.

Mirax is a contemporary licensed crypto casino with a space-age theme, 7000+ games, and instant payouts across digital coins and fiat currencies.

- Massive selection of over 7000 games from leading providers

- Quick withdrawals, especially for cryptocurrencies

- Multi-tier VIP program with escalating rewards

- Generous ongoing promotions like free spins and reload bonuses

Mirax Casino is an innovative and engaging online cryptocurrency casino launched in 2022 that brings a modern space-age aesthetic to its platform.

Players can explore endless slots, classic table games, live dealers and more while taking advantage of generous sign-up bonuses, ongoing promos, instant crypto payouts and around-the-clock customer support.

Key Points

- Extensive games library with over 7,000 slots, table games, live casino titles

- Powered by leading providers like Evolution Gaming and BetSoft for high-quality gameplay

- Lucrative sign-up bonus up to 5 BTC plus 300 free spins

- Generous ongoing promotions like cashback, tournaments, and holiday specials

- Instant withdrawals for cryptocurrencies like BTC and ETH

- Multi-tier VIP program provides escalating rewards for loyal players

Overall, Mirax Casino provides a compelling and entertaining online gambling destination for both crypto and fiat players. With its cosmic aesthetics, massive 7,000+ games library, lucrative bonuses up to 5 BTC, and innovative space theme, Mirax brings an intergalactic twist to the world of internet gambling.

Fast crypto withdrawals, responsive customer service, and multi-platform compatibility cement it as a secure and reputable option.

For those seeking a contemporary, licensed casino that offers an out-of-this-world experience, Mirax checks all the boxes. Its modern approach to bonuses, banking and gameplay make it a standout in the expanding galaxy of crypto casinos.

Thunderpick

Thunderpick

100% Match Up to 500 EUR/USD.

Thunderpick is a premier online gambling site with extensive sports betting markets, hundreds of casino games, generous welcome bonuses, and a smooth, fully mobile-optimized user experience.

- Huge selection of betting markets across dozens of sports

- Extensive casino game portfolio with hundreds of slots and table games

- Ongoing promotions, prize drops, cashback, and VIP program

- Responsive 24/7 customer support via live chat and email

Boasting oversight from the reputable Curacao Gaming Control Board licensing body, Thunderpick offers an extensive sports wagering menu spanning over 30 categories internationally.

Their contemporary website design pairs seamlessly with a polished mobile experience to uphold convenience for global audiences. Lucrative matched deposits continue through ongoing reload incentives, free wagers and daily boosts across thousands of betting markets

Key Points

- Extensive sports betting markets across 30+ sports

- Competitive odds comparable to leading sportsbooks

- Hundreds of slots and casino games also offered

- Lucrative welcome bonus package up to €875

- Generous ongoing promotions like 10% weekly cashback

- Smooth, contemporary site design for desktop and mobile

- Live streaming offered for many sporting events

In an increasingly crowded online gambling landscape, Thunderpick has carved out a distinctive niche since its 2017 founding by blending sports betting variety with next-generation convenience.

Lucrative sign-up bonuses continue through ongoing reload matches, free wager tokens and contest entries. For VIPs, an escalating rewards program unlocks higher maximums and personalized support.

For an enjoyable, rewarding online gambling experience, Thunderpick makes an appealing choice to wager at your own pace.

Mbit

mBit Casino

150% Welcome Bonus & 100 Free Spins!

mBit Casino is a feature-rich platform for online casino gaming, especially for Bitcoin players. The expansive games library and robust live dealer offering are definite strengths, while the comprehensive security measures provide peace of mind.

- Massive selection of games

- Quality live dealer offering

- Crypto and fiat payment options

- Varied welcome offers and bonuses

mBit Casino is a popular online gambling site focused on serving Bitcoin players. Established in 2014, this online casino offers over 2,600 slot games, more than 100 progressive jackpots, a large selection of table games and dedicated live dealer options.

mBit Casino accepts deposits and handles lightning-fast withdrawals using top cryptocurrencies like Bitcoin, Ethereum, and Litecoin. Players can also use traditional payment methods if preferred. The site advertises strong security and privacy standards for transactions.

New players are welcomed with a generous 3-part deposit bonus worth up to 5.5 BTC. There’s also a no-deposit bonus on sign-up. Regular players benefit from ongoing promotions, daily races, and an industry-leading 8-tier VIP program.

Key Points

- Huge selection of over 2,600 slot games from top developers like Amatic, Red Tiger Gaming, Play’N GO and Betsoft

- 100+ progressive jackpot slots with lucrative prize pools

- Wide variety of classic table games like blackjack, roulette, baccarat, dice games, etc.

- Immersive live dealer casino powered by Evolution Gaming’s software

- Generous welcome bonus package on first 3 deposits matched up to 110%

- Daily and weekly leaderboard promotions with prizes

- 8-tier VIP program providing bigger rewards for loyal players

- Supports deposits and fast withdrawals with major cryptocurrencies

mBit Casino stands out as a top-tier crypto-centered online casino platform with a lot to offer players. Its biggest strength is undoubtedly its vast games library with over 2,600 high-quality slots, table and live dealer titles from the best providers. This creates almost endless entertainment for every type of player.

Complementing the expansive gaming catalog is strong banking support for major cryptocurrencies like Bitcoin and Ethereum. Deposits and withdrawals are fast thanks to blockchain technology. mBit also provides privacy for players that want to remain anonymous.

With its exceptional game variety, crypto focus, and generous rewards programs, mBit Casino is a winning choice for any fan of online gambling.

Tgcasino

TG Casino

Welcome Bonus of 200% rakeback up to 10 ETH + 50 free spins + $5 sports bet

TG.Casino combines the convenience of Telegram messaging with a massive selection of games and sports betting options, allowing for anonymous crypto gambling without KYC requirements.

- Telegram integration for seamless gambling within the messaging app

- No KYC required for completely anonymous play

- Impressive selection of 5,000+ games from top providers

- Native TGC token offering 25% cashback and profitable staking options

- Fast cryptocurrency transactions with instant deposits and quick withdrawals

TG.Casino has emerged as an innovative player in the online gambling space since 2023, uniquely combining a full-featured casino experience with Telegram integration. This platform allows users to access over 5,000 games and sports betting markets directly through the popular messaging app or via their website.

With anonymous crypto payments across 15+ cryptocurrencies, no KYC requirements, and exclusive benefits through their native TGC token, TG.Casino offers a modern, privacy-focused gambling experience for crypto enthusiasts.

Key Points

- Seamlessly integrates with Telegram for convenient gambling

- 5,000+ games including slots, table games, and live dealer options

- Offers 30+ sports markets with competitive odds

- Supports 15+ cryptocurrencies with no KYC requirements

- TGC token provides 25% automatic cashback on losses

- Generous welcome bonus: 200% rakeback up to 10 ETH

- Fast transactions with 24-hour withdrawal processing

- Available via website or Telegram mini-app

- Licensed by Curacao Gaming Control Board

- 24/7 customer support through multiple channels

TG.Casino stands out as a groundbreaking platform that successfully merges convenient Telegram access with comprehensive crypto gambling options. Its impressive game selection, anonymous play without KYC requirements, and innovative TGC token benefits create exceptional value for players.

For cryptocurrency enthusiasts seeking a secure, feature-rich gambling experience with seamless mobile access, TG.Casino represents one of the most user-friendly and rewarding options available today.

Katsubet

Katsubet

Welcome Bonus of 100% Deposit Match + 100 Free Spins

KatsuBet is a modern, licensed online crypto casino with Japanese-inspired aesthetics, over 5000 games, and fast payouts across cryptos like Bitcoin and fiat currencies.

- Huge selection of over 5000 games from top providers

- Instant withdrawals for cryptocurrencies

- Regular promotions like free spins and reload bonuses

- 8-tier VIP program with escalating rewards

Bringing Japanese inspiration to the world of crypto gambling, KatsuBet has provided an artsy yet contemporary online casino destination since 2020. With licenses cementing legitimacy and leaders like Dama N.V. steering operations, the site offers an abundant game selection numbering over 5,000 titles.

Lucrative deposit matches, free spin bundles and cashback perks incentivize gameplay while swift verifications and cryptography uphold convenience for international users.

Key Points

- Over 5,000 games from leading studios like Evolution Gaming

- Lucrative welcome bonus up to €500 plus 100 free spins

- Cryptocurrency supported for fast, anonymous banking

- 8-tier VIP program with escalating rewards

- Generous promotions like weekly cashback and free spins

- Instant payouts for cryptos like Bitcoin and Ethereum

- Fully optimized for seamless mobile play across devices

In an increasingly crowded online gambling landscape, KatsuBet has carved out a distinctive niche since its 2020 founding by merging vibrant Japanese visuals with varied gaming.

Lucrative sign-up bonuses continue through ongoing reload matches, free spin awards and cashback deals. For VIPs, an escalating rewards program unlocks higher withdrawal limits and personalized support.

For an innovative crypto casino blending culture and convenience, KatsuBet is worth a spin. As additions around live dealers and payment channels continue, this aesthetic-rich gaming portal shows future promise.

Betfury

BetFury

Welcome Bonus Up to $3,500 plus 1,000 free spins

BetFury is the premier one-stop crypto gambling destination for players seeking an enormous selection of fair games, generous bonuses up to $3,500, free token rewards, and robust sports betting options across desktop and mobile.

- Huge selection of over 8,000 casino games and sports betting options

- Generous welcome bonuses up to $3,500 in value plus free spins

- Lucrative loyalty program with escalating cashback rewards

- Quick crypto deposits & withdrawals in over 40 coins/tokens

- Staking system to earn native BFG tokens as you play

BetFury is a premier crypto-based gambling site that has exploded in popularity since launching in 2019. Over 1.6 million members now enjoy the platform’s enormous casino with over 8,000 games, lucrative sportsbook betting markets, innovative social features, and generous bonus programs.

BetFury accepts dozens of major cryptocurrencies for fast and easy gameplay while offering round-the-clock support and full optimization for mobile access.

Key Points

- Features an enormous casino with over 8,000 games including slots, table games, live dealer, and originals

- Accepts 40+ major crypto coins and tokens like BTC, ETH, ADA for deposits and withdrawals

- Generous welcome bonuses up to $3,500 in value plus thousands of free spins

- Operates a full sportsbook with betting on 80+ disciplines including major leagues and esports

- Native BFG token offers profit sharing via daily staking rewards of up to $2M

- Fully optimized mobile web experience enables easy access on any device

- Fast 15 minute withdrawals and responsive 24/7 customer support via live chat

With continual innovation in its products and player experiences, BetFury has swiftly become a trailblazing force demonstrating the full potential of cryptocurrency gambling sites.

Between the expansive game catalog, profitable staking perks, and vibrant social environment – BetFury offers something for all appetite levels.

For an exemplary iGaming hub where entertainment rewards such devotion, search no further than this definitive crypto contender.

Brief Overview of Crypto Casinos

Crypto casinos are online gambling platforms that let you deposit, play, and withdraw using cryptocurrencies like Bitcoin and Ethereum. They work just like regular online casinos, but with the added benefits that come from using digital currencies.

These platforms have exploded in popularity over the past few years. Players love the speed, privacy, and low fees that crypto transactions offer compared to traditional payment methods.

Growing Popularity in Gibraltar