Crypto World

Bitcoin (BTC) isn’t broken, says Strategy’s (MSTR) Saylor

Bitcoin has tanked over 14% in one week and 22.7% in four weeks. Strategy Chairman Michael Saylor has a simple explanation for the decline: It’s capital rotation, not impairment.

In a post on X, Saylor pointed to the historic pace of AI infrastructure funding to the tune of approximately $400 billion deployed over the past six months while noting the $4 billion in outflows from the U.S.-listed spot ETFs since mid-May.

In essence, he argued that institutions are pulling money out of bitcoin and deploying into AI, leading to weakness in the top cryptocurrency. This matters because rotation implies temporary weakness, driven by capital chasing a hot theme before it eventually finds its way back.

“Volatility creates opportunity,” Saylor said, a characteristically bullish framing from the most prominent corporate bitcoin holder on the planet.

Saylor’s Strategy recently sold 32 BTC, a move, analysts say, added to the bearish sentiment in the market, deepening the price selloff. The publicly listed firm still holds 843,706 BTC.

While some analysts have flagged the AI boom as a headwind for bitcoin, most bears have drawn a darker conclusion from the recent selloff: that crypto is simply broken.

“Bitcoin just looks broken at this point Even Saylor is selling now,” pseudonymous trader QE Infinity said on X.

Their case probably rests on a confluence of concerning signals: Saylor’s surprise sale of 32 BTC, weeks of heavy ETF outflows, and the striking fact that almost every major asset class, from equities to commodities, is trading at or near record highs while bitcoin languishes.

Ripple built its identity on replacing SWIFT, the bank-messaging network that moves roughly $150 trillion a year, with XRP as the bridge that would kill slow correspondent banking. A decade on, the banks kept SWIFT, adopted Ripple as a fast lane beside it, and the disruptor is learning to integrate. What that pivot means for XRP is the real question.

Summary

- Ripple built its identity on replacing SWIFT, the messaging network linking roughly 11,000 banks and about $150 trillion in annual flows, with XRP cast as the bridge that would end slow correspondent banking.

- A decade later, banks have kept SWIFT and adopted Ripple as a fast lane alongside it, not a replacement, and Ripple’s posture has shifted from disruption toward integration.

- Signals now point to Ripple working with SWIFT-connected infrastructure rather than purely against it, a pragmatic maturation of its original pitch.

- Rival Chainlink has already connected SWIFT to blockchains through its cross-chain messaging layer, showing that integration, not replacement, is where the institutional money is flowing.

- For XRP, the open question is whether it ends up as a settlement layer beneath SWIFT messaging or gets sidelined as banks keep messaging on SWIFT and settle in stablecoins.

For most of its existence, Ripple defined itself by a single enemy: SWIFT, the global messaging network that connects roughly 11,000 banks and underpins the movement of something like $150 trillion a year.

Ripple’s founding pitch was that SWIFT was slow, antiquated plumbing, that moving money across borders through it took days and trapped capital in pre-funded accounts around the world, and that XRP could replace all of that by acting as a neutral bridge asset that settled value in seconds.

The company’s executives spent years framing the contest in exactly those terms, as a young, fast technology coming to take the lunch of an aging incumbent.

A decade later, the scoreboard tells a more complicated story. SWIFT is still standing, still carrying the world’s bank messaging, and the banks that adopted Ripple mostly did so as a fast lane running alongside SWIFT rather than as a replacement for it.

And now, in a quiet but telling shift, Ripple appears to be moving from trying to replace SWIFT to looking for ways to plug into the world it once vowed to dismantle.

This piece examines that reversal, why it happened, and the question it raises for XRP holders, which is whether the token has a place in an integrated future or gets left out of it.

The arc matters because it is really a story about how disruption meets entrenched infrastructure, and how the ambitious narratives that sell a token in its early years collide with the slower reality of how global finance actually changes.

Ripple’s evolution from would-be SWIFT killer to prospective SWIFT partner is not a humiliation; it is a maturation, and arguably a smart one. But it scrambles the original thesis that many XRP holders bought into, the one in which the token replaces a $150 trillion network and captures the value of doing so.

This guide traces the original pitch, what SWIFT actually is and why it survived, what really happened when banks adopted Ripple, the pivot toward integration, how a rival already executed that integration, and what the whole shift means for the token at the center of it.

The original pitch: replace SWIFT

To appreciate the reversal, you have to remember how absolute the original ambition was.

Ripple was sold, for years, as the technology that would render SWIFT obsolete. The argument was concrete and, on its own terms, compelling.

When money moves across borders through the traditional system, it does not actually travel. Instead, banks send messages to one another through SWIFT and settle through a chain of correspondent banking relationships, in which each bank holds pre-funded accounts in foreign currencies at other banks.

This system is slow, taking days for some transfers, and it is capital-intensive, because trillions of dollars sit idle in those pre-funded accounts around the world. That money cannot be used for anything else.

Ripple’s pitch was that XRP could eliminate all of it by serving as a bridge asset: a bank could convert its currency into XRP, move the XRP across the world in seconds, and convert it into the destination currency on the other end, with no need for pre-funded accounts and no multi-day delay.

In that vision, XRP was not a speculative token but the grease in a new global settlement machine, and its value would rise with the volume of cross-border payments it bridged.

Ripple’s leadership leaned into the rivalry, repeatedly casting SWIFT as the slow, outdated incumbent and Ripple as the disruptor coming to replace it.

For holders, this was the heart of the bull case, and it was intoxicating precisely because the prize was so vast. If XRP became the bridge for even a meaningful slice of global cross-border value, the implications for its price were enormous.

The entire thesis rested on replacement, on XRP supplanting the old rails rather than complementing them. That framing shaped how a generation of holders understood what they owned.

It is also the framing that reality has spent the past decade quietly dismantling.

What SWIFT is, and why it did not die

The flaw in the replacement thesis was an underestimation of what SWIFT actually is and how hard it is to displace.

SWIFT is not a settlement system that moves money. It is a messaging standard, a secure, standardized language that banks use to instruct one another to move funds.

Its power comes not from technology but from its network: roughly 11,000 institutions all speaking the same language, with decades of trust, integration, and regulatory acceptance built around it.

Replacing a network like that is categorically harder than building a faster alternative, because the value of SWIFT to any one bank is that every other bank is already on it.

A faster technology does not automatically overcome that. A bank cannot unilaterally switch to a system the rest of the world is not using.

SWIFT also did not stand still. Faced with the threat from blockchain-based challengers, it modernized, rolling out faster services and adopting new global messaging standards designed to carry richer data and move more quickly, narrowing the speed advantage that challengers like Ripple had built their pitch around.

The combination, an entrenched network effect plus a modernizing incumbent, proved far more durable than the disruptor narrative allowed.

Banks, it turned out, had little appetite to rip out the messaging standard that connects them to every other bank on earth in favor of a system built around a volatile cryptocurrency, however fast it settled.

The result was not the replacement Ripple had promised but something the original pitch did not really contemplate: coexistence. SWIFT kept doing what it does, and Ripple’s technology found a narrower role beside it.

What actually happened: banks kept both

The reality that emerged is that banks adopted Ripple’s technology selectively, as a fast lane for specific corridors and use cases, while keeping SWIFT for the vast bulk of their messaging.

Hundreds of financial institutions came to have some relationship with Ripple’s network, and its on-demand liquidity service, which uses XRP as a bridge to avoid pre-funded accounts, found genuine adoption in particular remittance corridors where it offered real advantages.

But this was adoption as a complement, not a conquest. A bank might route certain payments to certain countries through Ripple while continuing to handle the rest of its global business through SWIFT, treating Ripple as one specialized tool in a kit instead of as the new foundation of cross-border payments.

This coexistence is the crucial fact that the replacement narrative obscured. XRP did not become the bridge for global finance; it became a useful option for slices of it, valuable in specific corridors but nowhere near the universal settlement asset the original pitch envisioned.

And even within Ripple’s own growing business, the company increasingly leaned on its dollar stablecoin instead of XRP for the cash leg of institutional settlement, because a stable, dollar-denominated instrument suits banks and treasurers better than a volatile token.

As previously reported, that is the coexistence reality now defining Ripple’s 2026: bank partnerships can deepen while XRP still waits for direct demand.

So the decade did not deliver the dramatic replacement of SWIFT by XRP. It delivered a more modest reality in which SWIFT remained the backbone, Ripple’s technology served as a fast lane for particular needs, and even Ripple’s own institutional ambitions came to rest as much on its stablecoin as on its token.

That is the landscape into which Ripple’s strategic pivot arrived, and it is why the pivot makes sense.

The quiet pivot from replacement to integration

Against that backdrop, Ripple’s posture has shifted in a way that would have been hard to imagine in the company’s combative early years.

Instead of positioning itself purely as SWIFT’s replacement, Ripple has increasingly built itself into the institutional financial system as it actually exists: adopting the new global messaging standards that SWIFT uses, pursuing banking charters and regulated custody, expanding a dollar stablecoin designed to fit institutional settlement, and signaling interest in connecting to, instead of only competing with, the SWIFT-based infrastructure that banks already run.

That is Ripple’s integration-ready stack: banking access, custody, stablecoin rails, and the XRP Ledger sitting beside the traditional system rather than outside it.

The disruptor that once vowed to dismantle the old rails is learning to plug into them.

This pivot is pragmatic, and it reflects a hard-won recognition. If you cannot persuade 11,000 banks to abandon the messaging standard that connects them, the smarter play is to become the layer that their existing messaging can trigger, the settlement and tokenization infrastructure that sits beneath SWIFT instead of in opposition to it.

In that model, a bank does not stop using SWIFT. It keeps sending SWIFT messages, and those messages reach into a faster settlement or tokenization layer where companies like Ripple operate.

Ripple’s whole banking and stablecoin build, its charter, its custody business, its regulated rails, positions it to be exactly that kind of layer.

That is also why Ripple USD becoming available in Japan through SBI after JFSA approval matters. It shows Ripple building a regulated settlement asset inside one of the markets most important to XRP’s history and liquidity.

The shift from replacement to integration is not an admission of defeat so much as a recalibration toward how global finance actually adopts new technology, which is by addition and connection, not by wholesale demolition.

It is a more realistic strategy. The question it raises is what role the token plays in it.

Chainlink already did it

The integration path is not hypothetical, because a rival has already walked it, and watching that rival clarifies where the institutional money is flowing.

Chainlink, the oracle and interoperability network, built its institutional strategy around connecting SWIFT to blockchains instead of replacing SWIFT. It advanced that integration to a pre-production stage in which banks can send their familiar SWIFT messages to trigger smart-contract actions across blockchains, without tearing out their legacy systems.

That is the rival that integrated first. The model is precisely the integration thesis made concrete: SWIFT stays, the banks keep their existing messaging, and a crypto-native infrastructure layer connects that messaging to the on-chain world.

The banks do not have to choose between the old system and the new one, because the new one plugs into the old.

That a major competitor reached this integration first is instructive for Ripple and for XRP holders, because it shows both the viability and the competitiveness of the integration approach.

The institutions tokenizing assets and modernizing settlement are not looking for a single technology to replace their entire stack. They are looking for connective infrastructure that links what they already use to the blockchain rails they are starting to explore.

That is the opportunity, and it is a crowded one, with Chainlink, Ripple, and others all positioning to be the layer that bridges traditional messaging and on-chain settlement.

The race is no longer about who can replace SWIFT, because the market has decided SWIFT is not going anywhere. It is about who becomes the indispensable connector between SWIFT’s world and the tokenized future, and that is a fundamentally different competition than the one Ripple originally framed.

Why integration beats replacement

It is worth dwelling on why the integration strategy is the right one, because understanding that explains both Ripple’s pivot and the constraints on XRP.

Global finance does not adopt new infrastructure by abandoning the old. It adopts by layering the new on top of the existing, connecting them, and migrating gradually as trust and standards develop.

A bank evaluating blockchain settlement is not going to disconnect from the network linking it to every other bank on earth. It is going to look for a way to use blockchain capabilities while keeping that connection intact.

Any strategy that demands wholesale replacement is fighting the fundamental way the system changes, which is why the SWIFT-killer pitch, however exciting, was always going to struggle against the slower reality.

Integration, by contrast, works with that reality. By becoming the settlement and tokenization layer that existing messaging can reach, a crypto-native firm makes itself useful without asking banks to take the impossible step of abandoning their core infrastructure.

This is why Ripple’s evolution toward regulated banking, institutional custody, a fitting stablecoin, and connection to existing standards is a more credible path to relevance than the original replacement dream ever was.

It positions Ripple to capture real institutional business in the way institutions actually adopt technology. The strategy makes sense, and the pivot is wise.

But the very logic that makes integration the right move for Ripple the company also reshapes the role available to XRP. In an integrated world, the cash leg, the part that actually settles value, can be filled by a stable instrument.

That is precisely where the token’s place becomes uncertain.

What it means for XRP

Here is the question the whole reversal forces, and it is uncomfortable for the original thesis.

In the replacement vision, XRP was indispensable: it was the bridge asset that would carry global value across borders, and its necessity was the entire point.

In the integration vision, that necessity is far less clear. If the model is that banks keep using SWIFT for messaging and connect to a settlement layer beneath it, then the critical question becomes what does the settling, and there are two candidates.

One is XRP, used as a neutral bridge asset to move value between currencies in seconds. The other is a stablecoin, used as a steady dollar instrument that banks and treasurers find easier to work with because it does not swing in value.

Ripple has built a capable stablecoin precisely because institutions want that stability, and across its own business the stablecoin has increasingly taken the settlement role.

That is the settlement asset competing with XRP. RLUSD may be good for Ripple’s institutional strategy while making XRP’s direct role less automatic.

This is the heart of the matter for holders. The integration strategy that makes Ripple more relevant as a company does not automatically make XRP more relevant as a token, because the settlement function XRP was meant to perform can be performed by the stablecoin instead, and often is.

XRP retains a genuine potential role as a bridge asset in cross-currency flows where converting through a neutral token is more efficient than holding many stablecoins, and that role is real and not negligible.

But it is no longer the indispensable, central role the replacement pitch promised. It is a contested role, competing for relevance with the stablecoin inside Ripple’s own integrated infrastructure.

The regulatory backdrop still matters here. If the CLARITY Act codifies digital-commodity treatment for XRP, it could make institutions more comfortable using the token where it actually has settlement utility.

But legal clarity alone does not decide the routing question. Banks still have to choose XRP over a stablecoin for actual value transfer, and that is a use-case decision, not just a regulatory one.

So the pivot from fighting SWIFT to plugging into it is good strategy for Ripple and ambiguous news for XRP. It improves the company’s odds of institutional relevance while leaving genuinely open whether the token shares in that relevance or watches the stablecoin capture the settlement role it was built to fill.

The decade in perspective

Stepping back, the arc from SWIFT killer to SWIFT partner is best understood not as a failure but as a lesson in how technological change actually unfolds in finance, and it carries a clear-eyed conclusion for anyone holding the token.

Ripple set out to replace the world’s bank-messaging network and learned, as most disruptors of deeply entrenched infrastructure do, that the incumbent’s network effects are more durable than any speed advantage. It also learned that the path to relevance runs through integration instead of demolition.

The company adapted intelligently, building the regulated, institutional, integration-ready business that actually fits how banks adopt new technology. That adaptation is a strength, and it positions Ripple far better for real institutional adoption than the original confrontational pitch ever did.

For XRP, though, the maturation is double-edged, and honesty requires holding both sides. The good news is that Ripple is becoming a more serious, more credible institutional player, which strengthens the ecosystem the token lives in.

The hard news is that the integrated future Ripple is building does not obviously need XRP the way the replacement future did, because the settlement role the token was created to fill can be, and increasingly is, filled by a stablecoin instead.

The decade did not deliver the dramatic story holders were sold, in which XRP supplants a $150 trillion network and captures the value of doing so.

It delivered a more modest and more realistic story, in which Ripple earns a place inside the existing system and XRP fights for a role within it.

For that role to matter, value still has to enter and exit the rails. That is why how value enters and exits the rails remains central to any serious XRP thesis.

Whether plugging into SWIFT eventually means real demand for the token, or simply real relevance for the company that issues it, is the question the next decade will answer.

The disruptor grew up. Whether its token grows with it remains to be seen.

Frequently asked questions

Did Ripple really try to replace SWIFT?

Yes. For years Ripple’s defining pitch was that SWIFT, the messaging network connecting roughly 11,000 banks, was slow, outdated plumbing, and that XRP could replace it by acting as a bridge asset that settled cross-border value in seconds without the pre-funded accounts that correspondent banking requires. The company’s leadership repeatedly framed the contest as a fast disruptor coming to take the incumbent’s business. That replacement vision, in which XRP became the bridge for global payments, was the heart of the bull case many holders bought into.

Why did Ripple not replace SWIFT?

Because SWIFT’s power is its network, not its technology. Roughly 11,000 banks all use the same messaging standard, and the value to any one bank is that every other bank is already on it, which makes replacement far harder than building a faster alternative. SWIFT also modernized, adopting faster services and new messaging standards that narrowed the speed gap. Banks proved unwilling to abandon the standard connecting them to every other bank in favor of a system built on a volatile token, so instead of replacement, the result was coexistence, with Ripple used as a fast lane alongside SWIFT.

What does it mean that Ripple wants to plug into SWIFT?

It reflects a strategic pivot from replacement to integration. Instead of trying to dismantle SWIFT, Ripple is building itself into the existing financial system, adopting the messaging standards banks use, pursuing banking charters and custody, expanding a stablecoin suited to institutional settlement, and signaling interest in connecting to SWIFT-based infrastructure instead of only competing with it. The idea is to become the settlement and tokenization layer that existing bank messaging can trigger, so banks keep SWIFT while reaching into faster on-chain settlement. It is a more realistic strategy than the original replacement dream.

How did Chainlink connect SWIFT to crypto?

Chainlink built its institutional strategy around connecting SWIFT to blockchains instead of replacing it, advancing to a pre-production stage where banks can send their familiar SWIFT messages to trigger smart-contract actions across blockchains without rewriting their legacy systems. SWIFT stays in place, the banks keep their existing messaging, and Chainlink’s infrastructure connects that messaging to the on-chain world. It is the integration thesis made concrete, and that a major competitor reached it first shows both the viability of the integration approach and how competitive the race to be the connecting layer has become.

Is the pivot bad news for XRP?

It is ambiguous instead of simply bad. In the replacement vision, XRP was indispensable as the bridge asset. In the integration vision, the settlement role XRP was meant to fill can also be filled by a stablecoin, which banks often prefer because it holds a steady value. XRP retains a real potential role as a bridge asset in cross-currency flows, but it is no longer the central, indispensable role the original pitch promised. It now competes with the stablecoin inside Ripple’s own infrastructure. So the pivot strengthens Ripple the company while leaving open whether XRP shares in that relevance.

Does XRP still have a role in cross-border payments?

Yes, but a more contested one than the original pitch suggested. XRP can serve as a neutral bridge asset in cross-currency settlement, where converting through a single token can be more efficient than holding many different stablecoins, and that role is genuine. But within Ripple’s own integrated, institutional business, the stablecoin has increasingly taken the settlement role because its stable value suits banks better. So XRP has a real but no longer indispensable role, competing for relevance with the stablecoin instead of serving as the sole bridge the replacement vision envisioned. Whether it captures meaningful settlement volume is the open question.

This article is information, not investment advice. Cryptocurrency is volatile, and corporate strategies, partnerships, and figures reflect reporting available as of June 26, 2026, which can change quickly. Verify current data from primary sources before making any decision.

Polymarket has confirmed that attackers compromised a third party vendor and used the access to inject malicious code into the platform’s frontend, leading to a phishing attack that drained an estimated $2.94 million from users.

Summary

- Polymarket said a third party vendor compromise enabled a phishing attack that stole about $2.94 million from at least 11 user wallets.

- The platform removed the malicious dependency, contained the incident and said all affected users will receive full refunds.

- DefiLlama recorded the attack as the 89th crypto security breach of the second quarter, the highest quarterly total by incident count on its records.

Polymarket disclosed on X that it has removed the affected dependency, contained the incident, and will fully reimburse affected users.

Blockchain analyst Specter estimated that the attack drained funds from at least 11 wallets after the malicious script appeared on the platform’s frontend.

Frontend compromise targets user wallets

Specter identified the attack as a phishing campaign rather than a protocol exploit. The analyst said the injected script enabled attackers to steal funds from connected wallets after users interacted with the compromised interface.

DefiLlama recorded the incident as the 89th reported crypto security breach of the second quarter, making it the highest quarterly total by incident count in the platform’s records.

DefiLlama also reported $74.9 million in losses across 29 crypto exploits during June. That total exceeded May’s $60.5 million but remained well below April’s $644 million.

The platform listed the $36 million Humanity Protocol exploit as June’s largest attack. Other major incidents included a $4.7 million exploit involving the Secret Network bridge, two separate $2.1 million exploits affecting Aztec, and a $1.7 million bridge exploit on Taiko.

DefiLlama reported that private key compromises accounted for 43% of exploit losses over the past 30 days. Fake proof exploits represented 10% of losses, while reverse MEV honeypots accounted for 8%.

Previous exploit traced to compromised private key

Polymarket disclosed a separate security incident about a month earlier after attackers exploited a six year old private key used for internal top up operations and stole about $600,000.

Security researchers, including ZachXBT, PeckShield, and Bubblemaps, initially flagged suspicious activity involving Polymarket’s UMA CTF Adapter contract on Polygon. Bubblemaps reported that attackers withdrew 5,000 POL every 30 seconds before estimating total losses at roughly $600,000.

Polymarket protocol contributor Shantikiran Chanal later attributed that incident to a compromised wallet used for internal operations rather than a vulnerability in the platform’s contracts or core infrastructure.

Josh Stevens, the company’s vice president of engineering, stated at the time that user funds and smart contracts remained secure and that all permissions linked to the compromised key had been revoked.

Grant Cardone, CEO of Cardone Capital, used this week’s crypto slide to restate the case for his bitcoin-and-property model, saying the structure is designed to keep buying as prices fall.

“We work to improve the cash flow of the real estate and buy more bitcoin as it falls,” Cardone said in a post on X.

Cardone Capital, which has about $5.3 billion under management, uses the income generated from its real estate assets to buy bitcoin at regular intervals regardless of its price, smoothing out the expenditure in a process known as dollar-cost averaging. The largest cryptocurrency has lost 4.7% this week.

Cardone said the model was “inspired by treasury companies but with real assets and real cash flow,” and called his firm the largest real estate-bitcoin hybrid in the world, with no institutional investors shaping its strategy.

I’ve consistently promoted combining BTC to real assets and using cash flow from the real asset to dollar cost average into BTC through its volatility. We work to improve the cash flow of the Real Estate and buy more BTC as it falls.

Cardone Capital BTC hybrid was inspired by…

— Grant Cardone (@GrantCardone) June 26, 2026

His comment draws a distinction with the corporate bitcoin treasury model popularized by Strategy (MSTR), in which companies raise money by issuing stock or debt to buy bitcoin.

That approach has come under pressure this week, with Strategy’s stock trading below the value of the bitcoin it holds and analysts at CryptoQuant arguing the firm has overextended itself.

Bitcoin briefly fell below $59,000 late Thursday as selling pressure spread across the crypto market.

Summary

- Bitcoin’s break below $59K came as ETF outflows and long liquidations deepened pressure across markets.

- Short-term holders are sending BTC to exchanges at a loss, raising capitulation and seller-exhaustion questions.

- Technical indicators remain fragile, with RSI near oversold and $59K-$60K still the key support zone.

The move pushed BTC to an intraday low near $58,189 before a small rebound toward the $60,000 area.

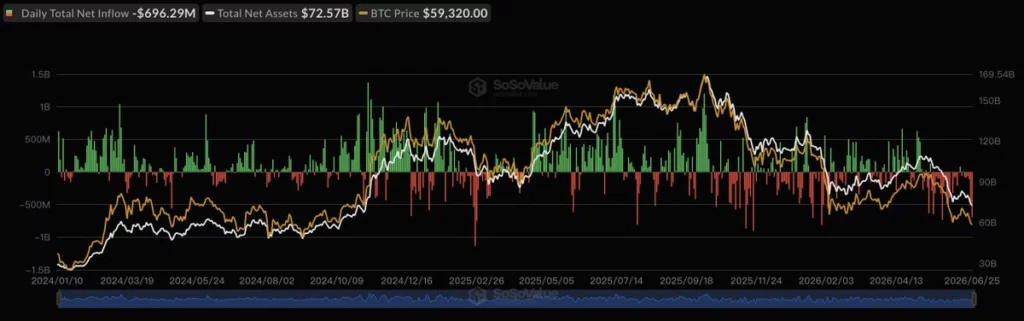

According to crypto.news market data, Bitcoin remains under pressure after losing the $60,000 level during the latest selloff. The move kept traders focused on whether the $59,000-$60,000 area can turn back into support.

The selloff also came as major tokens weakened. Ether fell near $1,500, while altcoins saw larger losses as leveraged positions were forced out. The drop followed several days of weak ETF demand and poor risk appetite across crypto markets.

As previously reported, Bitcoin had already rebounded toward $62,000 after a $459m ETF exodus, but sellers kept control. That rebound has now faded, leaving BTC back near the same support zone that traders have watched through June.

Bitcoin ETF outflows and liquidations add pressure

U.S. spot Bitcoin ETFs lost $696m on Thursday, according to SoSoValue ETF data. The outflow extended the run to six straight trading days of net redemptions. U.S. spot Ether ETFs also lost $81.9m, marking their sixth straight day of outflows.

The Bitcoin ETF selling was broad. BlackRock’s IBIT, the largest fund, accounted for about $63m of the outflows. Fidelity’s FBTC lost $3.5m, while Grayscale’s funds saw about $23m leave. No fund posted strong inflows during the session.

Leveraged traders also faced a sharp wipeout. According to CoinGlass data, more than $1b in crypto positions were liquidated over 24 hours. Long traders took most of the damage, with about $842m in long positions closed.

Bitcoin led the liquidation wave with about $489m in forced closures. Ether followed with about $295m. The largest single liquidation was a $38.05m BTC-USD position on Hyperliquid, showing how quickly large leveraged bets were removed.

Bitcoin traders watch $59K-$60K range

Crypto trader Daan Crypto Trades said Bitcoin had taken much of the liquidity around the $60,000 region. In a post on X, he said the biggest liquidity cluster now sits near $67,000, around the June high.

He added that the $59,000-$60,000 area remains key. If Bitcoin forms a range and buyers defend that area, the market could stabilize. If BTC slowly returns to the same support again, he warned that it may prepare for another higher-timeframe leg lower.

Another market watcher, BATMAN, said Bitcoin is close to printing a weekly death cross. He argued that the last death cross did not mark the exact bottom. Instead, it led to a long consolidation phase before the final cycle low.

EGRAG CRYPTO also pointed to a bearish cross between the 13-week and 33-week moving averages. He said a two-week close above $74,000 would weaken the bearish setup. Until then, he said the cycle-bottom window remains open, with downside zones around $47,000, $43,000 and $37,000.

Technical indicators remain fragile

Bitcoin’s short-term indicators show weak momentum, even after the small rebound. The MACD shows a mild bullish crossover, with the histogram slightly positive near 16.31. The MACD line sits around -2,269.45, just above the signal line near -2,285.76.

That setup means downside momentum has slowed. Still, both lines remain far below the zero line. This keeps the signal weak and shows that the recovery has not yet shifted the broader trend.

The RSI stands near 32.98, below its moving average around 37.77. This keeps Bitcoin close to oversold territory. Buyers have not regained control because RSI remains well below the neutral 50 mark.

Volume is near 12K, with heavier selling volume during the June decline. The latest candle shows a small rebound, but the market still lacks strong confirmation. Bitcoin needs to reclaim $62,800-$65,000 to show that buyers are taking back short-term control.

Short-term holders show stress

CryptoQuant analyst Amr Taha said Bitcoin’s short-term holder market cap fell to $237.7b on June 26. That was its lowest level since Oct. 2, 2024, when the figure was near $239.7b. The drop shows that many recent buyers are now holding unrealized losses.

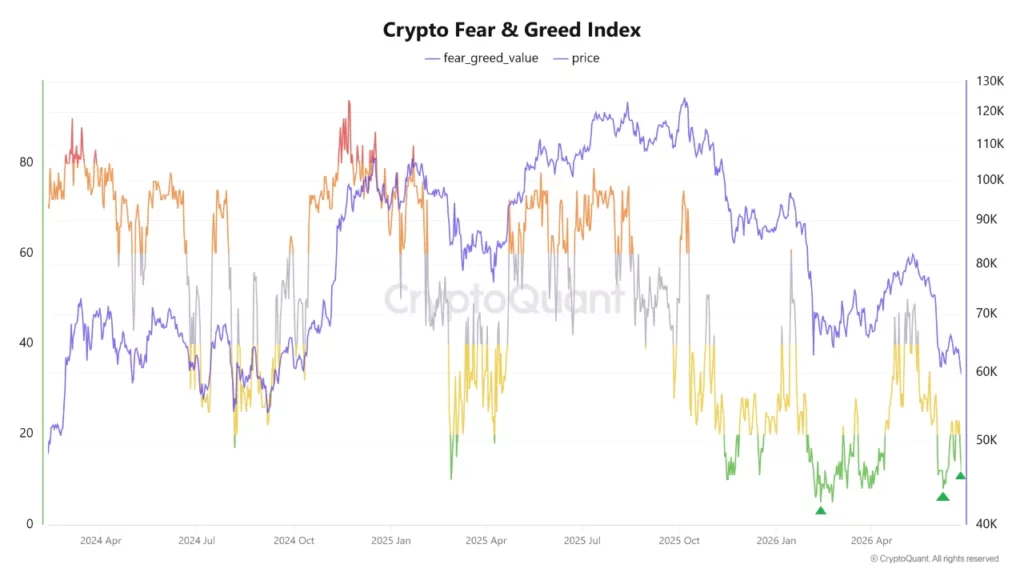

He also noted that the Crypto Fear & Greed Index fell to 12 on June 25, placing the market in Extreme Fear as Bitcoin traded near $59,700. The reading is not the lowest of the year, but it comes at a lower BTC price, showing deeper stress among recent buyers.

Taha also said short-term holders sent about 50,000 BTC to exchanges at a loss over 24 hours. Binance received about 9,500 BTC from that group, its highest reading since early June. Exchange transfers do not prove that all coins were sold, but they show that more BTC has moved to venues where it can be traded.

As crypto.news reported, Bitcoin triggered a large liquidation wave after falling below $60,000. Previously, crypto.news explored how the $60,000 support zone came under pressure after a bearish chart breakdown.

Macro news may help limit panic, but it has not yet changed the chart. An interim U.S.-Iran peace accord gives UN nuclear inspectors access to Iran, although details remain disputed.

For Bitcoin, the near-term test is simpler: hold $59,000-$60,000, or risk another move lower.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

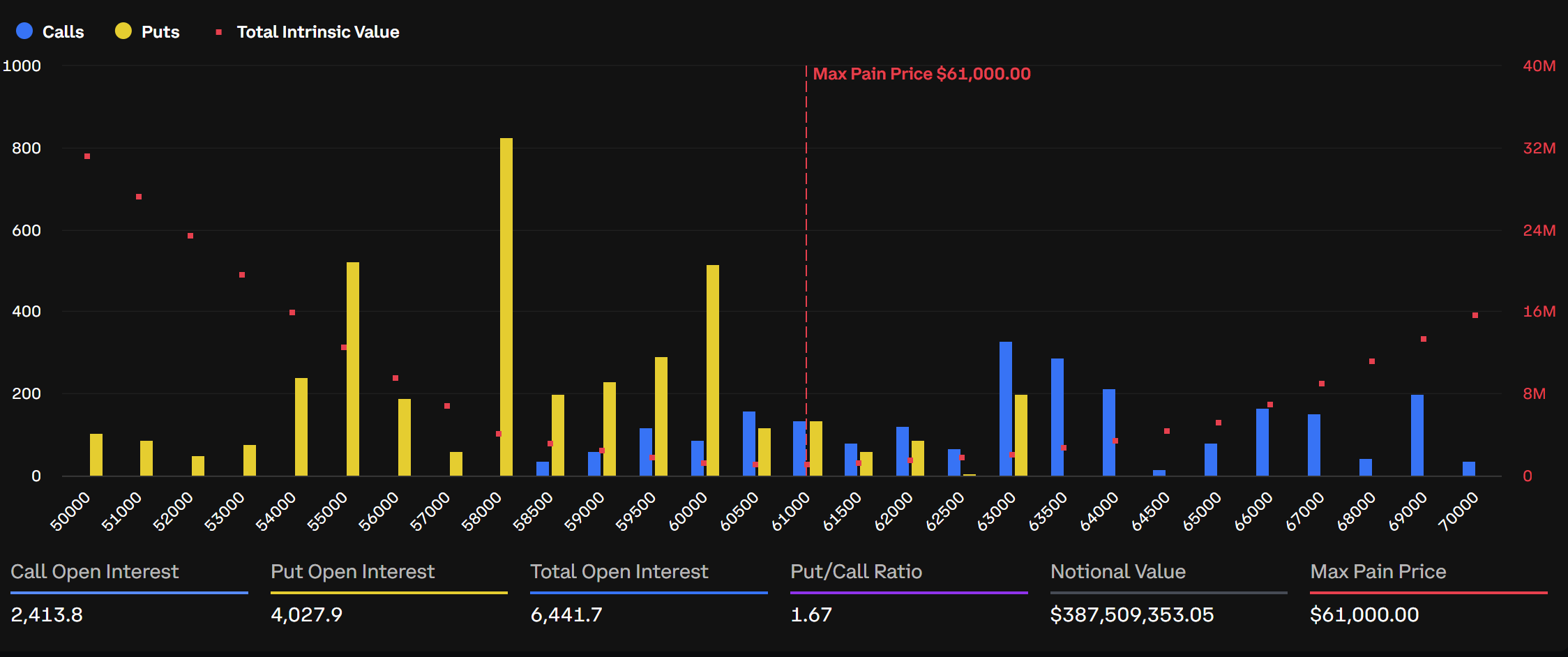

Roughly $10.63 billion in Bitcoin (BTC) and Ethereum (ETH) options expire on Deribit Friday. The settlement drops into a market that keeps sliding lower while traders hunt for a floor.

Bitcoin trades near $60,200 after a 2% daily drop, while ether sits around $1,580 after a steeper 4.43% fall. Both rest far below their options max pain levels.

Puts Command a Premium as Traders Brace for Downside

Friday’s settlement ranks as the quarter’s largest options event on Deribit. The bulk of expiring value sits in Bitcoin, with notional contracts worth about $9.06 billion against ether’s $1.57 billion. Max pain marks the price where the most options expire worthless. Bitcoin’s level sits at $70,000, while ether’s sits at $2,000.

Open interest leans toward calls in raw terms, yet positioning tells a cautious story. Bitcoin’s put-to-call ratio sits at 0.63, with 92,154 calls against 57,652 puts. Ether’s ratio runs lower at 0.50. The heavier call count reflects bullish bets now stranded well above the current price. Bitcoin’s recent options expiry events have followed a similar defensive pattern.

According to Greeks.live, Bitcoin’s 25-delta skew has turned sharply negative on short-dated contracts. The skew reads -10.7% at one day, -11.3% at seven days, and -9.6% at one month. By contrast, longer tenors stay calmer near -6% and -5%.

“Puts continue to command a meaningful premium over calls across all major tenors,” analysts at Greeks.live stated.

That premium reflects steady demand for near-term downside protection. Traders are paying up to hedge a further slide rather than chase upside. Bitcoin’s recent price action has kept that hedging active through the week.

The Bottom Question Hangs Over Settlement

Greeks.live places negative gamma between $60,000 and $64,000, the band where Bitcoin trades now. Positive gamma spreads across $67,000 to $82,000, with clusters near $67,000, $71,000, $75,000, and $80,000. The June, July, and September contracts drive most of that dealer exposure. The firm notes these readings exclude IBIT data.

That structure can keep price action choppy near current levels through expiry. Meanwhile, ether’s steeper price drop has pushed it well below its $2,000 max pain mark.

The expiry also lands during a broad crypto downturn. Both assets have slid to multi-month lows this week, deepening the case for caution into settlement.

Some forecasters expect deeper losses first. Jiang Zhuoer, founder of mining pool BTC.TOP, sees a late-2026 bottom forecast near $42,000 to $44,000. He points to Strategy’s mNAV slipping to 0.72, close to its 2022 low. BitMEX co-founder Arthur Hayes has floated a $40,000 Bitcoin bottom within six months. Even so, his year-end target still runs above $200,000.

Jiang’s broader four-year cycle model points to a bottom around late October. He has mined through several halvings and plans to buy back near the low.

Deribit, however, cautions against reading too much into the max pain pull.

“While max pain remains a widely followed metric, recent quarterly expiries have shown limited evidence of a consistent pinning effect ahead of settlement,” Deribit analysts indicated.

Both assets remain stuck below max pain heading into settlement. The next sessions may show whether sellers extend the search for a bottom or buyers finally step in.

The post $10.63 Billion Bitcoin and Ethereum Options Expire as Markets Search for a Bottom appeared first on BeInCrypto.

Crypto World

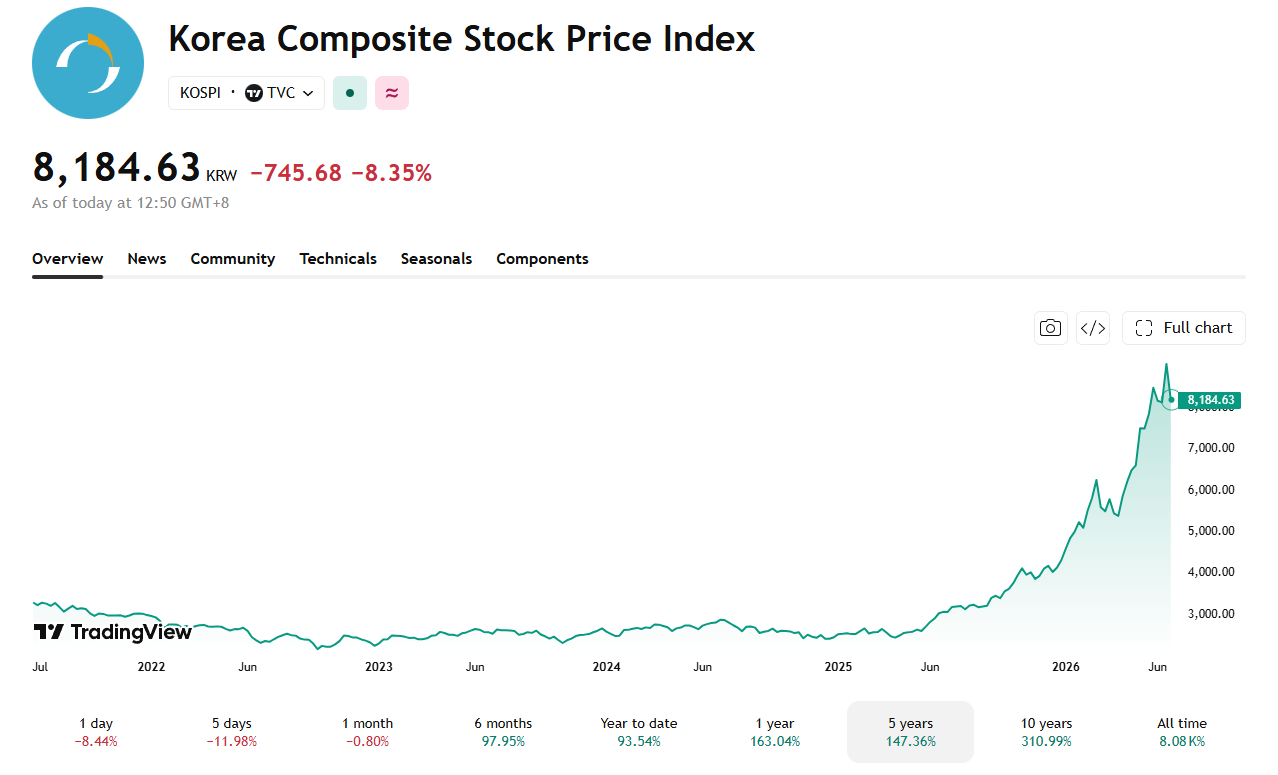

South Korea Has the World’s Hottest Stock Market: Why Does MSCI Still Call It ‘Emerging’?

South Korea’s KOSPI surged 112% in 2026, overtook the UK’s FTSE 100, and ranked as the world’s best-performing major index in 2025. Yet MSCI’s latest annual review left the country in its Emerging Markets category for another year.

MSCI CEO Henry Fernandez says South Korea’s economy is not the problem. Its currency market is.

One Currency Rule Blocks the Upgrade

Fernandez told CNBC that South Korea is “one of the most developed markets on the planet” in economic and technological terms. But MSCI judges countries on how their equity markets function for international investors. On that measure, the Korean won creates a specific barrier.

Fund managers buying South Korean equities must first purchase the won to settle trades. In every other market that MSCI classifies as developed, investors can buy or sell that currency at any hour, from any major financial center. The Korean won trades only during business hours in Seoul.

That constraint matters at scale. Fernandez said a third of all globally managed index assets sit in index funds. Managers running those funds cannot rebalance Korean positions outside Seoul trading hours.

July Reform Is Not Enough to Convince MSCI

South Korea plans to launch 24-hour dollar-won spot trading on July 6. Fernandez acknowledged the reform as real progress. But he raised a direct question: will a Seoul-based night shift generate enough liquidity, with a tight enough bid-ask spread, to satisfy institutional demand? He said he has doubts.

MSCI also cited rigid investor identification requirements, restrictions on in-kind transfers, and limits on exchange data use as additional reasons for keeping the country in emerging markets. The index provider stated that investors reported these issues remain unresolved.

South Korea already holds developed-market status under FTSE Russell’s classification system. The MSCI designation carries greater weight for passive fund flows globally, which is why Seoul has long pursued the upgrade. Earlier this year, the KOSPI overtook London’s FTSE 100 to become the eighth most valuable national equity index in the world. Market performance does not factor into MSCI’s methodology, however.

The July trading launch will be the key test. If it produces deep, liquid markets around the clock, MSCI’s next annual review could look different.

The post South Korea Has the World’s Hottest Stock Market: Why Does MSCI Still Call It ‘Emerging’? appeared first on BeInCrypto.

Key Takeaways

- AAPL shares declined approximately 6% following announcement of widespread hardware price increases — the first major pricing adjustment in years

- Hardware price hikes span from $100 to $300 across most models, with Mac Studio jumping $1,300

- Global memory chip scarcity, fueled by AI infrastructure demand, has driven DRAM costs up roughly 90% in Q1 2026 and an additional 60% in Q2

- Memory chipmaker Micron reported unprecedented 84.9% gross margins on the same day, highlighting the disparity between suppliers and buyers

- iPhone pricing remains unchanged for now, though analysts project the memory supply crisis could add approximately $200 in component expenses per unit

Apple announced sweeping price increases across its hardware portfolio on Thursday, triggering a sharp investor selloff. AAPL shares plummeted roughly 6%, declining $18.78 to close near $274.30, wiping out almost $200 billion in market capitalization during a single trading session.

The pricing adjustments affect Macs, iPads, HomePods, Apple TV devices, and the Vision Pro mixed-reality headset. The M5 MacBook Pro base model now commands $1,999, representing a $300 premium. Mac Studio experienced the steepest adjustment with a $1,300 price escalation. Most mainstream products saw increases between $100 and $300.

Apple CEO Tim Cook offered a stark assessment when speaking with The Wall Street Journal. “This is a hundred-year flood,” Cook stated. “I’ve never seen anything like it in any area in over 40 years.”

The underlying driver is a worldwide memory semiconductor shortage. Explosive AI data center construction has absorbed enormous quantities of DRAM and NAND flash memory, creating severe supply constraints for consumer electronics manufacturers.

DRAM contract pricing surged approximately 90% during Q1 2026, followed by another 60% escalation in Q2, per TrendForce data. NAND flash memory has tracked a comparable trajectory. Memory and storage component expenses now stand at roughly quadruple their levels from three quarters prior.

Cook acknowledged Apple’s efforts to shield consumers from the impact. “We’ve been trying to shield our customers from the increases, but the situation has become unsustainable,” he explained.

Micron’s Record Performance Highlights Industry Dynamics

While Apple shares were declining, Micron experienced a dramatic rally. The memory chip manufacturer reported all-time high revenue and an unprecedented 84.9% gross margin, exceeding analyst forecasts. Micron’s market capitalization expanded by more than $100 billion on Thursday.

This stark divergence illustrates the current market reality. The memory supply crisis has transferred pricing leverage decisively to chip manufacturers. For companies purchasing these components — including Apple — near-term relief appears unlikely. Micron projects its gross margin will expand further to approximately 86% in the coming quarter.

Apple’s Q2 2026 financial results, for the period ending March 28, demonstrated revenue growth of 17% year-over-year reaching $111.2 billion, with EPS advancing 22%. Gross margin reached 49.3%. However, these figures largely preceded the most severe phase of the memory price escalation.

iPhone Pricing Remains Under Scrutiny

Thursday’s pricing revisions notably excluded the iPhone, Apple Watch, and AirPods product lines. This reprieve may prove temporary. Next-generation iPhone models are anticipated this fall, and research firm Counterpoint projects the memory supply crisis could increase component costs by approximately $200 per device. Higher-capacity storage configurations face the most significant impact.

The iPhone generates approximately half of Apple’s consolidated revenue, making any pricing strategy for this product line substantially more consequential than Mac or iPad adjustments.

Apple currently trades at roughly 33 times earnings at the $275 price level. This valuation premium reflects investor confidence in the company’s margin structure and services revenue expansion — the services division achieved record revenue of approximately $31 billion in Q2. Margin compression diminishes the company’s margin for error.

The stock has retreated into its previous consolidation range, with the $275–$280 area emerging as a critical technical support zone for investors to monitor.

Binance will shut off its services for European Union customers from next week, after withdrawing its bid for a licence under the bloc’s crypto rules.

The exchange emailed users in Poland, Italy, Spain, and France this week.

What Binance Told EU Customers

According to Euro News, Binance emailed its French clients. The message said its French unit would stop onboarding new users immediately and would end all crypto asset services in the country from July 1, 2026.

The company confirmed that comparable notices had been sent to affected users in other EU markets.

The notices stated that Binance will not hold a Markets in Crypto-Assets (MiCA) licence by June 30, 2026. The exchange assured that customer funds remain safe.

Follow us on X to get the latest news as it happens

The MiCA Deadline Behind the Decision

MiCA entered into force in June 2023. Its full licensing regime began in December 2024, opening a window for firms to secure a national licence.

That window closes July 1, 2026, the hard enforcement date across the European Economic Area. After it, operating without a MiCA licence puts a firm in breach of EU law.

Binance applied to the Hellenic Capital Market Commission in Greece but received no formal decision. It withdrew the bid this week. However, Binance said it would instead pursue a licence through another EU member state.

“Europe is an important region for Binance, and our ambition to operate under a clear, fair, and harmonized MiCA framework remains unchanged. We continue to support MiCA’s goal of creating a consistent regulatory framework for crypto assets across the EU, and we are confident we will secure authorization in another EU Member State in the coming months,” the exchange stated.

Two people familiar with the process told Reuters that Binance also approached regulators in Ireland and Latvia but faced resistance. The coming time will reveal which member state Binance targets next.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post MiCA Deadline Forces Binance to Wind Down EU Crypto Services appeared first on BeInCrypto.

Japanese financial services giant SBI Holdings said it agreed to buy cryptocurrency exchange Bitbank for around $289 million.

The Tokyo-based bank first floated the idea at the start of last month, framing it as part of a broader strategy to expand its crypto business ahead of potential regulatory developments in Japan. It bought crypto exchange Bitpoint in 2022.

Japan is in the process of bringing cryptocurrencies under the umbrella of financial products as authorized by the Financial Instruments and Exchange Act, which applies to stocks and other securities. This could take effect from early next fiscal year.

Bitbank is among Japan’s top 10 largest crypto exchanges by trading activity, according to CoinGecko, processing 24-hour volume of just under $50 million. Competitors such as Toobit, CoinW, Kraken and Bitmart all process in excess of $1 billion.

SBI said the acquisition, which is subject to regulatory approval, is set to close in October in a statement on Thursday.

A three-year stress test of Strategy (MSTR) suggests the company could survive an extreme market downturn, although common shareholders would face significant losses, according to Bitcoin-focused author and market commentator Adam Livingston.

The model assumed a severe scenario in which Bitcoin falls 55% from $59,100 to $26,600 within six months, mNAV drops below 0.50x, capital markets remain closed, and the company is forced to sell BTC to meet its obligations.

Brutal MSTR Stress Test

The starting assumptions included MSTR stock at $87.64, total Bitcoin holdings of 847,363 BTC, cash reserves of $1.4 billion, CEBE of 138,161 sats per share, and a claim ratio of 41.5%. As BTC prices decline in the model, fixed-dollar senior claims rise sharply in Bitcoin terms. Senior claims increase from 351,567 BTC to 819,073 BTC, while the claim ratio climbs to 96.7%.

The analysis shows that common equity Bitcoin would fall from 495,796 BTC to 28,290 BTC. CEBE drops from 138,161 sats per share to 7,884 sats per share, while the modeled MSTR share price falls from $87.64 to $1.01. Livingston described this phase of the scenario as the “horror movie.”

The stress test assumes no new Bitcoin purchases, no common share issuance, and monthly obligations of $167.7 million. Cash would be exhausted by the ninth month, after which the company would begin selling Bitcoin to service its obligations. Over the three-year period, Strategy would sell 115,727 BTC.

Despite those losses, the model would end with the company holding 731,636 BTC. The final modeled state places Bitcoin at $48,498, MSTR at $51.86, mNAV at 1.40x, common equity Bitcoin at 274,093 BTC, CEBE at 76,380 sats per share, and the claim ratio at 62.5%.

According to Livingston, the analysis does not point to an “instant bankruptcy” or a “death spiral.” Instead, he said the main risk is CEBE compression as senior claims temporarily consume most of the company’s Bitcoin stack in BTC-equivalent terms.

FUD Around Strategy

Livingston’s analysis comes as the debate surrounding Strategy’s BTC accumulation strategy has intensified in recent months. Some expect the company may need to sell part of its Bitcoin holdings in the coming years. For instance, crypto analyst Kaleo recently warned that the company’s best option now would be to sell 50,000 or more BTC in the next two years.

Meanwhile, others, such as CryptoQuant, have called for a pause in new purchases to strengthen cash reserves.

The post MSTR’s Bitcoin Per Share Gets ‘Annihilated’ in Extreme Bear Case: Analyst appeared first on CryptoPotato.

James Bond Contender’s 10/10 Crime Thriller Is a Major Streaming Hit

The New York-inspired gelato and French toast spot that’s bringing sunshine to Didsbury

Record temperatures drives up home air conditioning inquiries

-

Fashion7 days ago

Fashion7 days agoWeekend Open Thread: Miami – Corporette.com

-

Entertainment5 days ago

Entertainment5 days agoRenter of Home in Anne Heche Crash Denies Settlement With Son

-

Sports3 days ago

Sports3 days agoTwo goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

-

Tech4 days ago

Tech4 days agoMicrosoft accidentally kills epic Outlook email threads

-

Business5 days ago

Business5 days agoSoccer-U.S. defends Iran World Cup travel restrictions, says discussions ongoing

-

Politics7 hours ago

Politics7 hours agoPotential 2028er World Cup attendee leaderboard

-

Politics6 days ago

Politics6 days agoAndy Burnham and the meaning of Makerfield

-

NewsBeat7 days ago

NewsBeat7 days agoKeir Starmer Allies Question His Chances For No 10

-

Tech14 hours ago

Tech14 hours agoA Look At A Gaggle Of Transputer Boards

-

Crypto World2 days ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

Crypto World2 days ago

Crypto World2 days agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Business2 days ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

Politics3 hours ago

Politics3 hours agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Business6 days ago

Business6 days agoWall Street Week Ahead: Investors see Micron earnings as pulse check of AI rally momentum

-

Crypto World6 days ago

Crypto World6 days agoCan Charles Hoskinson Really Rescue Cardano?

-

Crypto World6 days ago

Crypto World6 days agoHIVE shares jump as $220M AI deal speeds Bitcoin mining pivot

-

Entertainment6 days ago

Entertainment6 days agoJose Alvarado Wants Taylor Swift at More Knicks Games

-

Crypto World6 days ago

Crypto World6 days agoJake Chervinsky accuses CME of protecting derivatives monopoly

-

Tech5 days ago

Tech5 days agoSignal’s Meredith Whittaker says AI chatbots ‘are not your friends’ and calls Copilot agents a backdoor

-

Sports20 hours ago

Sports20 hours agoIndia vs Bangladesh LIVE Score, Women’s T20 World Cup: Bangladesh Opt To Bat; India Enter ‘Do-Or-Die’ Stage As Semi-Final Race Heats Up

You must be logged in to post a comment Login