Crypto World

Bitcoin is trading like a tech stock, not gold

Bitcoin was sold as digital gold, an uncorrelated hedge that would hold up when markets broke. In 2026 it fell roughly 50% alongside the Nasdaq while gold hit record highs. So what is Bitcoin now, and did the hedge thesis ever survive contact with Wall Street?

Summary

- Bitcoin has spent 2026 moving with the Nasdaq rather than against it, with rolling correlations to U.S. tech indices reaching as high as 0.80 early in the year while its link to gold fell toward zero.

- The change traces to the spot ETF era: once institutions could hold Bitcoin inside the same portfolios as tech stocks, the same capital flows began driving both, tying Bitcoin to equity risk appetite.

- Analysts describe the current setup as the worst of both worlds, with Bitcoin taking the downside when stocks fall but not the full upside when they rally, behaving as a high-beta tail of macro risk instead of a standalone store of value.

- The counter-case is that Bitcoin is not a clean tech proxy either, since it fell on crypto-specific shocks even when tech rose, and that long-term holders kept accumulating, pointing toward an independent asset class instead of a tech clone.

- Whether the correlation is structural or a feature of the current tight-liquidity regime is the open question, and it decides whether the digital gold thesis is dead or merely dormant.

Bitcoin was supposed to be the asset that zigged when everything else zagged. For years it was sold as digital gold, an uncorrelated hedge that would protect a portfolio when stocks fell and uncertainty rose. In 2026, it has done close to the opposite. Bitcoin is down roughly 50% from its October 2025 record near $126,200, and it fell in near lockstep with technology stocks while gold climbed to record highs above $5,000 an ounce.

The asset marketed as a crisis hedge behaved like a leveraged bet on the same risk appetite that drives the Nasdaq. This piece works through the evidence that Bitcoin now trades like a tech stock, why that happened, and the serious counter-argument that the story is more complicated than a simple correlation chart suggests. The answer matters because it changes how investors should size Bitcoin, how they should compare it with gold, and whether the ETF era strengthened the asset or quietly rewired it into the same macro trade it was supposed to diversify away from.

The evidence: Bitcoin moves with the Nasdaq now

The correlation data is the starting point, and it is stark. Rolling 30-day correlations between Bitcoin and the Nasdaq 100 reached about 0.80 early in 2026, the highest level in close to four years, and Bitcoin’s longer-run five-year correlation with the tech-heavy index sits near 0.54. Standard Chartered analysts have pegged the Bitcoin-Nasdaq correlation around 0.5 with peaks near 0.8, while short-term readings against U.S. tech indices have ranged between roughly 0.55 and 0.68 through the year. However you measure it, Bitcoin and the Nasdaq have been moving together.

The relationship with gold has gone the other way. As Bitcoin’s tie to tech strengthened, its correlation with gold fell toward zero, at points reaching just 0.2. And the price paths made the divergence impossible to ignore. While Bitcoin dropped through 2026, gold surged to record highs above $5,000 and briefly toward $5,600 an ounce, outperforming Bitcoin by a wide margin over the same stretch.

The clearest test came under real stress. When conflict in the Middle East pushed oil higher and rattled markets, gold did what a safe haven does and climbed, while Bitcoin fell alongside risk assets. A hedge is supposed to prove itself precisely in those moments, and Bitcoin did not. The pattern that defined 2026 is simple to state: when the tech trade got hit, Bitcoin got hit, and when investors fled to safety, they chose gold.

Why the digital gold thesis mattered

To understand what has been lost, it helps to recall what the digital gold pitch actually claimed. Bitcoin’s founding appeal to institutions was not only its potential for gains but its supposed independence from everything else. It had a fixed supply capped at 21 million coins, no central issuer, and no cash flows tied to the economy, which in theory made it a store of value that would not move with stocks, bonds, or the business cycle. In its early years, Bitcoin was not just uncorrelated with equities; it was uncorrelated with nearly every major asset class, which made it look like the ultimate portfolio diversifier.

That property was the entire institutional case. A diversifier that zigs when the rest of a portfolio zags reduces overall risk, and that is worth paying for. Wall Street bought into the idea that Bitcoin could serve as a hedge against monetary debasement, market volatility, and economic uncertainty, a role gold has played for centuries. The digital gold narrative underpinned much of the adoption story, from corporate treasuries to the campaign for spot ETFs, because it promised something distinct from a simple speculative growth bet.

The trouble is that an asset’s identity depends not only on its design but on who owns it and how it is traded. Bitcoin’s code did not change in 2026. What changed is the profile of the people holding it and the machinery through which they buy and sell. That shift, more than anything about the protocol, is what turned the hedge into a high-beta risk asset.

What changed: the ETF made Bitcoin a portfolio asset

The pivotal event was the arrival of spot Bitcoin ETFs in January 2024, and the irony is sharp. The ETFs were celebrated as the moment Bitcoin was legitimized, folded into the regulated financial system at last. That same integration is what tied it to the equity market. Research published in late 2025 found robust evidence that ETF approval structurally altered Bitcoin’s role, marking a shift from an independent, idiosyncratic asset toward a conventional risk asset whose correlation with the S&P 500 rose sharply after the launch.

The mechanism is straightforward once you follow the money. Before ETFs, much of Bitcoin sat with crypto-native holders who traded it on its own logic. After ETFs, large institutions could hold Bitcoin exposure inside the same portfolios as their technology stocks, managed by the same risk desks using the same tools. When those desks adjust risk, they buy or sell Bitcoin and tech at the same time, for the same reasons, which welds the two together.

The marginal dollar in Bitcoin became, increasingly, the same dollar chasing artificial intelligence and growth equities, so when that dollar turned cautious, it sold both at once. This is the deeper story behind capital rotating into AI stocks that has drained crypto momentum all year. It is not only that money left Bitcoin for semiconductors; it is that the money still in Bitcoin now behaves like the money in tech, responding to the same Federal Reserve signals, the same liquidity conditions, and the same growth expectations. Bitcoin did not choose to become a tech stock. Its new owners made it one.

The worst of both worlds: downside without the upside

If Bitcoin simply tracked the Nasdaq one for one, that would be a clean story. The reality analysts have flagged is worse for holders. Trading firm Wintermute has argued that while Bitcoin’s directional correlation with the Nasdaq stayed high, the quality of that correlation deteriorated into what it called a bearish skew. In plain terms, Bitcoin has kept the downside beta, falling hard when equities fall, while losing much of the upside participation, failing to rally proportionally when equities recover.

Wintermute’s Jasper De Maere tied this to a shift in investor attention. As mindshare and risk-on capital crowded into mega-cap tech, Bitcoin remained correlated when global sentiment turned negative but stopped benefiting fully when optimism returned. He described Bitcoin as reacting like a high-beta tail of macro risk rather than a standalone narrative, keeping the downside beta while shedding the upside premium. The Kobeissi Letter put the same idea more bluntly, noting that Bitcoin was increasingly behaving like a leveraged technology stock.

That combination, all of the downside and only part of the upside, is the least attractive profile an asset can have. It means Bitcoin has been amplifying the pain of equity selloffs without delivering the diversification that justified holding it, and without matching the gains of the tech names it now mirrors. For a portfolio manager, an asset that adds volatility without adding either diversification or reliable upside is hard to defend, which is part of why some funds have re-labeled Bitcoin from a long-term hedge to a tactical growth position sized like any other speculative bet.

The counter-case: Bitcoin is decoupling, just not how bulls hoped

Here the story turns, because the simple tech-proxy narrative has a serious flaw. If Bitcoin were purely a leveraged Nasdaq, it would have risen when tech rose. Instead, for stretches since the October 2025 peak, Bitcoin fell while the Nasdaq strengthened, a divergence that some analysts said had rarely been so wide. Tech stocks climbed on strong earnings while Bitcoin dropped more than 30% from its high, driven by forces that had nothing to do with corporate profits.

Those forces were crypto-specific. The October 10 flash crash triggered a cascade of leveraged liquidations that hit Bitcoin while barely touching equities. Spot ETF outflows accelerated, pulling out the marginal buyer. The reflexive feedback loop around Bitcoin treasury companies like Strategy, most visibly Strategy, threatened to reverse from a buyer of last resort into a source of supply. And post-halving mining economics added their own pressure through miner selling pressure. None of that is in a Nasdaq chart.

So the honest reading is that Bitcoin is not a clean tech proxy: it takes the downside when tech falls, but it also falls on its own crypto-native shocks when tech rises. That is a worse outcome than pure correlation, but it also means Bitcoin is not simply a technology stock in disguise. The distinction matters for anyone trying to model the asset. A pure tech proxy would at least be predictable, rising and falling with the Nasdaq. What Bitcoin actually did in 2026 was absorb equity-market downside through the ETF-era ownership channel while simultaneously generating its own downside through leverage unwinds, ETF redemptions, treasury-company stress, and miner selling. It behaved less like gold, less like a clean tech stock, and more like a uniquely fragile hybrid during a bad year.

The maturation argument: a third asset class

There is a more optimistic frame that some analysts and long-term holders favor, which is that Bitcoin is becoming its own asset class instead of a copy of gold or tech. On this view, the correlation to equities is a phase driven by who happens to hold the marginal coin today, not a permanent identity. Bitcoin still has properties neither gold nor a tech stock shares: a hard-capped supply that cannot be expanded by decision, no cash flows or earnings to miss, and no management team or governance structure that can fail. Those features do not disappear because a correlation chart spikes.

The behavior of long-term holders supports the maturation read. During the same 2026 window when the ETF complex bled, the supply held by long-term holders moved in the opposite direction, with those flows running far larger in magnitude than ETF flows and skewing toward net accumulation. In other words, the traders treating Bitcoin as a high-beta risk asset were selling through ETFs, while conviction holders who treat it as a long-term store of value were buying. Two different populations, two different theses, playing out in the same asset at the same time.

Which group defines Bitcoin’s identity depends on which one is setting the marginal price, and that can change. Standard Chartered, for its part, has kept multiyear price targets well above current levels even while acknowledging the rotation into AI, framing the moment as a question of timing and competition for capital rather than a verdict on what Bitcoin fundamentally is. The maturation argument does not deny that Bitcoin trades like a risk asset right now. It argues that the current correlation is a snapshot of a particular ownership mix and liquidity regime, not the final word on an asset that is still only in its second decade.

Is this structural or cyclical?

The whole debate reduces to one question: is Bitcoin’s correlation with tech a permanent feature of the ETF era, or a temporary product of the current environment? The case for structural is that the ownership change is not reversing. ETFs are here to stay, institutions will keep managing Bitcoin alongside equities, and as long as they do, the flows that link the two assets will persist. If that is right, the digital gold thesis is effectively dead for as long as this ownership base dominates, and Bitcoin is a growth allocation that happens to be more volatile than most.

The case for cyclical rests on how correlations behave over time. Cross-asset correlations tend to spike during tight-liquidity, risk-off regimes and to loosen when liquidity returns and assets trade more on their own fundamentals. Bitcoin’s correlation with the Nasdaq has swung dramatically before, from deeply negative to strongly positive within weeks, which is not the signature of a fixed relationship. A shift in Federal Reserve policy, a change in the liquidity backdrop, or a rotation of capital away from the crowded AI trade could all loosen the tie and give Bitcoin room to trade on its own narrative again.

Some analysts even argue the correlation has already begun to break, though so far in the unhelpful direction of falling while tech rose. What would restore the digital gold thesis is a period where Bitcoin holds up while equities fall, proving the hedge in the only way that counts. That has not happened in 2026, which is why the thesis is on the ropes. But a single bad year in which a leverage-driven crypto drawdown collided with an AI-fueled equity rally is not a controlled experiment, and reading a permanent identity change off it may be as premature as the original digital gold claim was.

What it means for how to hold Bitcoin

For anyone actually holding Bitcoin, the practical takeaway is to match the thesis to the timeframe. Over the horizon that matters in 2026, Bitcoin has behaved as a high-beta risk asset, so treating it as a crisis hedge or a portfolio insulator has not worked and is not supported by the data. An allocation sized as if Bitcoin will hold up when stocks crash is mis-sized, because this year it fell harder than the stocks it was meant to hedge. The more defensible approach in the current regime is to treat Bitcoin as a volatile growth position, size it to risk tolerance, and watch the Nasdaq and AI-stock sentiment as closely as the crypto charts, because that is where much of the near-term direction is being set.

Over a longer horizon, the store-of-value case does not depend on short-term correlation. The fixed supply, the absence of governance and cash-flow risk, and the accumulation behavior of long-term holders are the pillars of that argument, and they survive a year of trading like a tech stock. The honest conclusion is that Bitcoin is currently being priced as a leveraged expression of risk appetite, not as digital gold, and that this reflects who owns it in the ETF era more than any change in what it is. Whether it grows into the independent, hedge-like asset its supporters imagine, or stays a high-beta satellite of the tech trade, will be settled by the next regime, not this one.

For now, the market has given its answer, and it is not gold. The strongest near-term read is not ideological; it is practical. In a world of a hawkish Fed and tight liquidity, Bitcoin behaves like a risk asset, and risk-off market sentiment matters as much as on-chain conviction. The digital gold thesis is not dead by definition, but in 2026 it has not been the trade.

Frequently asked questions

Is Bitcoin still considered digital gold?

Less and less in practice. Through 2026, Bitcoin behaved like a high-beta risk asset instead of a safe haven, falling alongside technology stocks while gold climbed to record highs. Its correlation with the Nasdaq reached as high as 0.80 while its link to gold fell toward zero. The digital gold label describes Bitcoin’s design and long-term thesis, but its 2026 trading behavior did not match it.

Why does Bitcoin move with tech stocks now?

The main driver is the spot ETF era that began in January 2024. Once institutions could hold Bitcoin inside the same portfolios as technology stocks, managed by the same risk desks, the same capital flows started moving both. When those desks adjust risk exposure, they buy or sell Bitcoin and tech together, which ties Bitcoin to equity market sentiment and Federal Reserve policy the same way growth stocks are.

How correlated is Bitcoin with the Nasdaq?

Correlation varies with the time window, but it has been high in 2026. Rolling 30-day correlations with the Nasdaq 100 reached about 0.80 early in the year, the highest in nearly four years, and the five-year correlation sits near 0.54. Short-term readings against U.S. tech indices have ranged roughly between 0.55 and 0.68. Correlations shift over time and have swung from negative to strongly positive within weeks.

Did the Bitcoin ETFs cause this?

They appear to be the central cause. Research from late 2025 found that spot ETF approval structurally raised Bitcoin’s correlation with the S&P 500, marking a shift from an independent asset to a conventional risk asset. The ETFs legitimized Bitcoin by integrating it into traditional finance, and that same integration tied its price to equity flows and institutional risk management.

What is the bearish skew analysts mention?

It refers to Bitcoin keeping the downside of its tech correlation while losing much of the upside. Trading firm Wintermute described Bitcoin as falling hard when equities fall but failing to rally proportionally when they recover, behaving as a high-beta tail of macro risk. That combination, full downside and partial upside, is a poor profile because it adds volatility without reliable gains or diversification.

Is Bitcoin just a leveraged tech stock then?

Not cleanly. If Bitcoin were purely a leveraged Nasdaq, it would have risen when tech rose, but for stretches in 2026 it fell while tech strengthened, driven by crypto-specific shocks: the October flash crash, ETF outflows, treasury-company stress, and miner selling. So Bitcoin took equity downside while also generating its own downside, which is a fragile hybrid instead of a simple tech proxy.

Could Bitcoin become a hedge again?

It is possible, and it hinges on whether the correlation is structural or cyclical. Cross-asset correlations tend to spike in tight-liquidity, risk-off regimes and loosen when liquidity returns. A shift in Federal Reserve policy or a rotation away from the crowded AI trade could let Bitcoin trade on its own narrative again. Restoring the hedge thesis would require Bitcoin to hold up while equities fall, which has not happened in 2026.

How should investors treat Bitcoin given this?

Match the thesis to the timeframe. In the current regime, Bitcoin trades as a volatile growth asset, so sizing it as a crisis hedge is not supported by the data, and investors may watch the Nasdaq and AI sentiment as closely as crypto charts. Over a longer horizon, the store-of-value case rests on fixed supply, no governance risk, and long-term holder accumulation, which do not depend on short-term correlation.

Disclaimer: This article is for information and educational purposes only and does not constitute financial, investment, or trading advice. Cryptocurrency prices are highly volatile, and correlations between assets change over time and may not persist. Nothing here is a recommendation to buy or sell any asset. Always do your own research and consider consulting a licensed financial professional before making investment decisions. Information is accurate as of July 2, 2026, and may change.

Meta CEO Mark Zuckerberg said AI agent development at the firm is progressing more slowly than expected, even as technology and crypto firms continue pouring resources into the nascent technology.

In a company meeting on Thursday, Zuckerberg said the “trajectory of the agentic development over at least the last four months hasn’t really accelerated in the way that we expected,” according to Reuters, which reviewed a recording of the call.

The bet on agent adoption hasn’t “come to fruition yet,” Zuckerberg said, adding that executives made an aggressive push into agentic infrastructure in January in part because of fears they weren’t moving “fast enough.”

Despite the slower progress, Zuckerberg said he expects the firm’s AI investments to start paying off within the next three to six months.

Zuckerberg’s comments offer a reality check for technology and crypto firms betting that autonomous agents will soon become major users of blockchain payments. Meta, along with several crypto firms, has bet big on agentic AI, with many pivoting their business models to cater to autonomous AI agents.

In May, Meta cut roughly 10% of its workforce and reassigned about 7,000 employees to AI-focused teams — a restructuring Zuckerberg acknowledged was not as clean as it could have been, with executives miscalculating the timing.

Meta expands AI agent feature on three platforms

Zuckerberg’s concerns come as Meta expanded its Meta Business Agent globally for businesses on Instagram, Messenger and WhatsApp on Thursday.

The Business Agent can respond to customer inquiries, make product recommendations and close sales without human intervention, Meta said.

Zuckerberg also revealed in March that he was building a personal AI agent designed to support his decision-making as CEO.

The crypto industry has been a keen adopter of the technology, with Coinbase CEO Brian Armstrong and Circle CEO Jeremy Allaire among the executives predicting that AI agents will become the dominant users of blockchain-based payments in the coming years.

Several notable integrations advancing AI agent-driven stablecoin spending have emerged in recent months, including one by Amazon Web Services in May, when it integrated Coinbase’s x402 payments protocol into Amazon Bedrock AgentCore, allowing agents to transact in the USDC (USDC) stablecoin.

Related: OKX launches AI marketplace for autonomous agent economy

In April, crypto wallet startup Oobit launched a Visa-supported virtual card for AI agents to make online purchases in USDt (USDT) on behalf of businesses.

AI agent payments adoption lagging

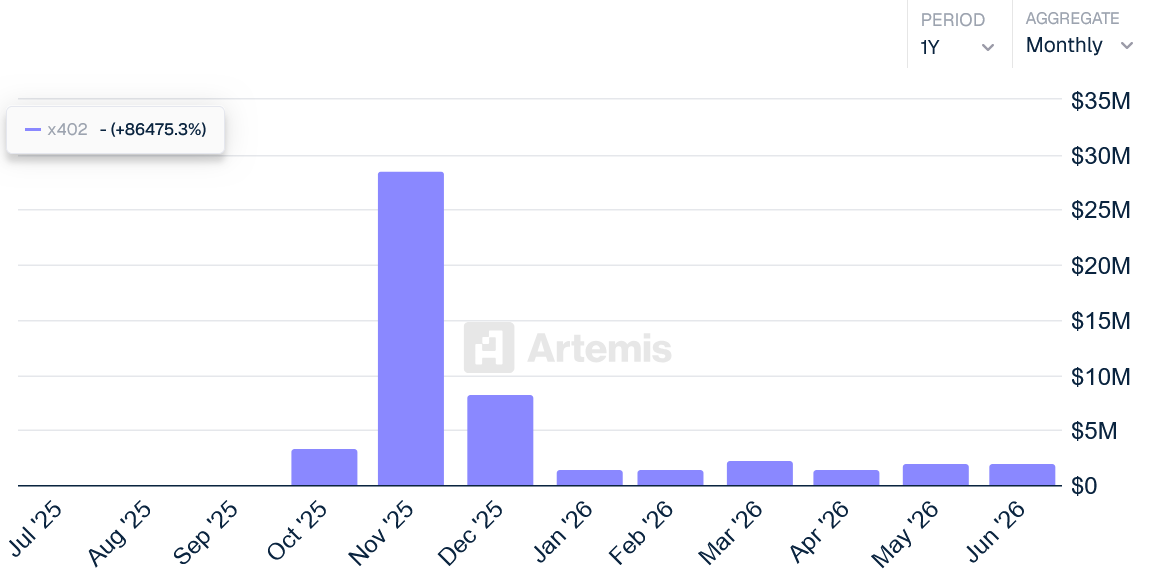

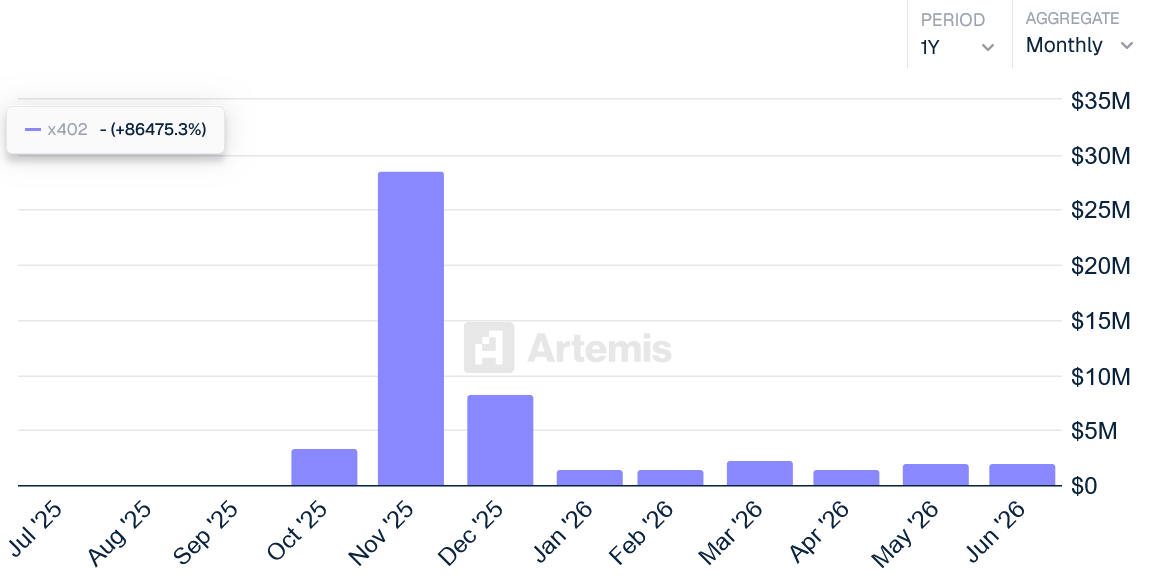

Despite the integrations, data shows that AI-agent transaction activity on the blockchain remains relatively small, with Artemis data showing that only $2 million in trading volume has been facilitated through the AI agent-supported x402 protocol over the past 30 days.

Monthly change in x402 transaction volume over the past 12 months. Source: Artemis

Magazine: The end of anonymity? AI could unmask crypto’s hidden identities

A teenager suspected of involvement with the “Scattered Spider” hacking group has been extradited to the US over his alleged role in an $8 million crypto ransom.

The US Justice Department said on Wednesday that Peter Stokes, a 19-year-old dual US-Estonian national, was arrested in Finland in April on an Interpol Red Notice and extradited to the US last week to appear in a Chicago federal court on Tuesday.

A criminal complaint unsealed in court accused Stokes and others of breaching a luxury jewelry retailer’s computer system in May 2025 to steal data and demand a ransom payment of $8 million in crypto. The retailer managed to evict them from the network and did not pay the ransom, but suffered $2 million in disruption damages, according to the complaint.

Stokes is one of the few arrests that authorities have tied to Scattered Spider, which often uses crypto ransoms. Ransomware actors received more than $820 million in payments last year, an 8% decline from 2024, even as attacks rose by 50%.

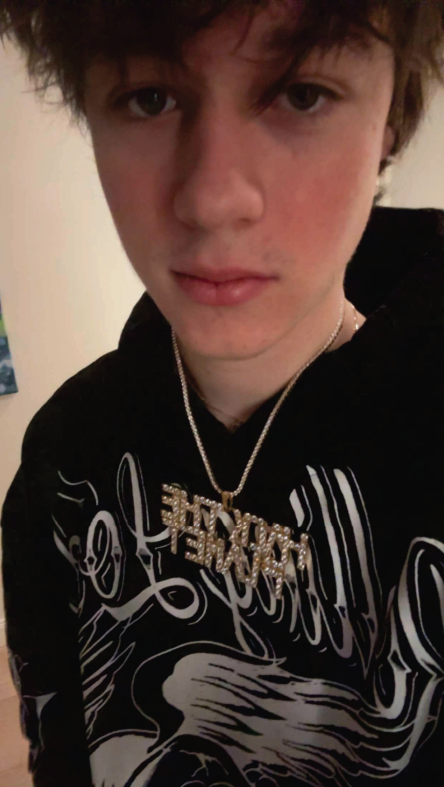

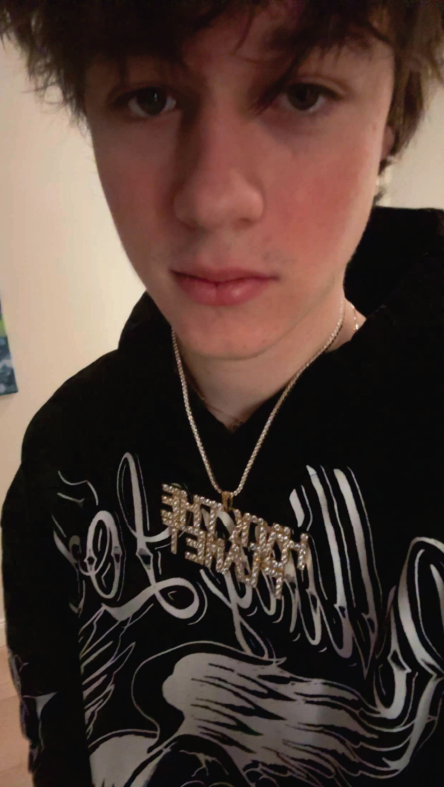

An image the FBI took from Stokes’ Snapchat account shows him wearing a necklace that says “Hack the Planet,” a quote from the 1995 cult film “Hackers.” Source: US Department of Justice

Alleged hack started with phishing call

According to the complaint, the hack against the jewelry retailer started with several phishing calls to the company’s technology help desk, with Stokes and others allegedly pretending to be employees requesting a reset of login credentials.

Authorities alleged the hackers managed to compromise three employee accounts in as little as two hours, two of which belonged to company IT administrators, who had access to higher-privilege accounts that were also breached and used to access the company’s systems,

After a few days, Stokes and others allegedly sent a ransom note from a compromised company email account to demand funds or they would publish credit card and payment information.

However, the complaint said the company repelled the intrusion and that the intruders later contacted the company separately to demand $8 million, which the company did not pay.

Stokes allegedly involved in “numerous intrusions”

The complaint accused Stokes, who uses the online nicknames “Bouquet” and “Jordan,” of being a “Scattered Spider member who has engaged in numerous intrusions, or assisted in them” on multiple unnamed companies.

Authorities claimed that a search of a storage device allegedly linked to Stokes showed it contained downloads from a virtual private server that Microsoft had identified as being used to carry out intrusions on companies.

The complaint alleged that it also “contained exfiltrated records from multiple victim-companies.”

Related: Taiko reopens bridge after $1.7M exploit, says users made whole

The complaint claimed that Stokes’ Snapchat account shows “substantial wealth for a person his age” and alleged that he used the account to boast “about his international travel and wealth, and sent media regarding apprehended Scattered Spider members.”

The Justice Department said that Scattered Spider, also known as “Octo Tempest,” “UNC3944,” and “0ktapus,” has been involved in over 100 network intrusions, resulting in more than $100 million in ransom payments and millions of dollars in damages.

Stokes was charged with six counts related to hacking, cyber extortion, fraud and conspiracy.

Magazine: Crypto scammers face death, Aussie CGT makes Asian hubs attractive: Asia Express

Roughly 10.83 million BTC are currently held at a loss, meaning their holders paid more than today’s price, against 9.22 million still in profit, according to Glassnode data. It is the first time loss-making supply has overtaken profitable supply since the current cycle began and reflects how deep the correction from bitcoin’s $109,000 January peak has cut.

Historically, these crossovers have landed near periods of peak financial stress and capitulation among newer buyers. They have also marked the point at which coins migrate from weaker hands to stronger ones, since only holders with high conviction tend to sit on losses rather than sell. Long-term holder accumulation and rising wallet-cohort balances across several size brackets have run alongside this latest deterioration in profitability.

Bitcoin traded at $61,361 on Thursday, up 0.7% on the day and 2.5% on the week, still roughly 44% below January’s all-time high, per CoinDesk data. Ether added 4.2% to $1,702, and Solana led the majors at 18.6% on the week to $80.44, with volume running above $3.6 billion.

Whether the supply crossover marks a bottom depends on what follows. In 2018-19 and 2022, similar readings preceded months of basing before a sustained recovery. The chart does not resolve on its own. ETF flows returning and macro pressure easing are what convert the accumulation signal into a price signal.

Japanese investment firm Metaplanet continued its corporate Bitcoin buildout in the second quarter, adding 2,823 BTC at an average price of about 12.71 million yen (roughly $78,850 at current exchange rates). The purchase pushed the company’s total holdings above 43,000 Bitcoin, while slightly lowering its average acquisition cost.

Separately, the story also highlights a contrasting trend among some smaller treasury-focused companies. South Korean firm K Wave Media exited its Bitcoin treasury strategy after selling its remaining BTC to address debt, while France-based Sequans Communications previously said it would monetize its remaining holdings over time.

Key takeaways

- Metaplanet bought 2,823 BTC in Q2, bringing its total to more than 43,000 BTC and reducing its average cost per coin.

- The latest tranche was acquired at an average price of about 12.71 million yen per BTC, lowering Metaplanet’s average acquisition cost to roughly $95,117.

- Metaplanet reported about $10.95 million in quarterly revenue linked to Bitcoin income-generation strategies involving options premiums and related yield methods.

- K Wave Media sold its last 88 BTC to repay debt, ending its Bitcoin treasury approach after earlier plans to expand holdings.

- Not every corporate treasury is expanding: Sequans Communications previously signaled that it would monetize its remaining Bitcoin holdings over time.

Metaplanet expands holdings and refines its cost base

According to a Thursday announcement from Metaplanet, the company acquired 2,823 Bitcoin during the second quarter at an average price of about 12.71 million yen per BTC. That figure matters because it was below Metaplanet’s prior average purchase price, enabling the firm to reduce its blended cost basis.

The acquisition lowered Metaplanet’s average acquisition cost to about $95,117 per BTC, down from approximately $96,258 previously. Metaplanet’s total Bitcoin holdings now stand at 43,000 BTC acquired for an aggregate value of about $4.1 billion, based on the figures in the company’s announcement.

Beyond accumulation, Metaplanet also disclosed quarterly performance tied to its Bitcoin income strategy. The company reported around $10.95 million in revenue from Bitcoin-related activities during the quarter. The approach, as described in the announcement, centers on earning premiums by selling cash-secured options and deploying other Bitcoin yield tactics.

For investors, the combination of spot purchases and options-based income generation is a key part of how treasury-style Bitcoin companies attempt to justify their equity valuations. When Bitcoin’s price is volatile, these revenue mechanisms can, in theory, partially offset drawdowns—though the net effect depends on execution, market conditions, and counterparty or strategy risks (none of which are detailed in this particular excerpt).

Shares move, but the broader performance picture remains uneven

Metaplanet’s equity performance reflected modest market optimism around the filing. The company’s shares closed Thursday up 3.5%, though the stock remains down about 48% year-to-date, according to the linked market page cited in the source text.

That underperformance also stands out against Bitcoin itself, which the source notes fell 31% over the same year-to-date period. The contrast underscores a persistent reality for corporate Bitcoin holders: even when a company keeps buying and building a large BTC position, investors may still reprice the stock due to factors like equity dilution risk, funding costs, valuation assumptions, or the market’s perception of how sustainable treasury income is.

The Metaplanet update comes during an ongoing push by several corporate buyers—yet the story is not purely one-directional, as other firms are trimming exposure.

Treasury strategies: K Wave Media exits after selling remaining BTC

While Metaplanet added Bitcoin, K Wave Media—an Nasdaq-listed company in South Korea—went in the opposite direction. The company sold its remaining 88 BTC to repay $6 million in debt, exiting its Bitcoin treasury strategy, according to a Tuesday filing with the U.S. Securities and Exchange Commission.

The SEC filing indicates a sharper reversal than what the company had previously communicated. Earlier coverage referenced in the source text describes K Wave Media’s July 2025 announcement that it secured $1 billion in capital capacity to drive its Bitcoin treasury strategy and aimed to expand holdings to 10,000 BTC. Exiting after holding only 88 BTC suggests the original plan ran into constraints—whether financial, operational, or strategic—though the excerpted material does not specify the reasons.

This kind of turnaround is important for readers because it highlights a mismatch risk that can exist in treasury models: plans premised on sustained capital access, favorable volatility, and consistent BTC purchase economics may not survive changing market conditions or debt obligations.

Other companies continue to monetize rather than accumulate

The source also points to Sequans Communications, a France-based semiconductor company that said in May it would monetize its remaining Bitcoin holdings over time. At the time of that announcement, Sequans reported holding 658 BTC, and its shares reportedly rose about 14.5% after the disclosure.

Taken together with K Wave Media’s decision to exit, the broader takeaway is that corporate Bitcoin strategies are diverging. Some companies are doubling down through additional spot buying and structured income strategies, while others are winding down exposure, using Bitcoin holdings to address liabilities, or planning to gradually convert BTC into cash.

Even within the same sector, these choices can produce very different investor outcomes depending on each firm’s balance sheet, debt profile, and how its equity market values the “BTC treasury” thesis.

Looking ahead, investors should watch whether Metaplanet can sustain its Bitcoin income-generation revenue while continuing to manage its cost basis, and whether other treasury-focused firms follow K Wave Media and Sequans toward monetization or debt reduction. The key uncertainty across all these cases remains whether corporate models that rely on both holding BTC and generating yield can hold up as market conditions and financing access evolve.

The National Organization of Black Law Enforcement Executives (NOBLE) endorsed the Digital Asset Market Clarity Act (CLARITY Act) in a letter to Senate leaders John Thune and Chuck Schumer.

Notably, NOBLE has become the first major law enforcement group to formally back the bill. The endorsement lands as the bill faces hurdles over ethics and illicit finance concerns.

NOBLE Endorses CLARITY Act

The letter was signed by NOBLE National President Reneé Hall. Hall, a former Dallas police chief, said the bill gives law enforcement new capabilities while preserving longstanding criminal enforcement authorities.

In its letter, the group pointed to expanded regulatory obligations across the digital asset industry, stronger forfeiture authorities, new compliance expectations, and added oversight of crypto kiosks.

“Collectively, these provisions have the potential to improve investigative visibility and provide law enforcement with additional tools to combat financial crime,” the letter reads.

The group also emphasized that the bill does not modify existing federal criminal authorities used to prosecute offenses such as money laundering, unlicensed money transmission, conspiracy, sanctions violations, and related crimes.

Follow us on X to get the latest news as it happens

A Break From Other Law Enforcement Groups

The position sets NOBLE apart from other police and prosecutor organizations. The National District Attorneys Association, the National Association of Assistant US Attorneys, the International Association of Chiefs of Police, and the National Sheriffs’ Association previously raised concerns regarding the bill.

Their objections center on Section 604. A coalition of Catholic sisters also asked Senate leadership to reexamine the lack of provisions on illicit finance, anti-money laundering, and accountability.

Despite the opposition, industry advocates keep pressing for floor time. Stand With Crypto urged supporters this week to lobby their senators.

The bill still needs 60 votes on the Senate floor, meaning seven Democrats must cross over. Whether a law enforcement endorsement softens resistance to Section 604 may become clearer once senators return.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post First Major Law Enforcement Group Endorses CLARITY Act in Letter to Senate appeared first on BeInCrypto.

The HCMC did not immediately respond to a CoinDesk request for comment regarding Binance’s MiCA licensing process.

“As the person who led the license application, there’s nothing that I have been made aware of that there was any issue with the application,” Lynch added. “In fact, I was told the complete opposite.”

Lynch also argued that Europe’s crypto market loses more than just its largest exchange if Binance remains outside the MiCA framework. She said Binance provides liquidity and market infrastructure that benefit the wider crypto ecosystem, adding that regulation should strengthen the industry rather than exclude companies that have invested heavily to meet its standards.

Lynch declined to speculate on reports that political intervention played a role in the delays. Instead, she said the focus is now on helping users through the transition period while preparing a new licensing strategy.

“We’re very committed to being in Europe and very committed to being regulated,” she said.

Despite Binance’s experience, Lynch described MiCA as a positive step for the industry. She said the regulation has helped bring crypto into the financial services system by providing firms with clear rules and consumers with greater protection.

“I fundamentally believe the crypto industry is maturing. Regulation brings maturity,” she said. “The industry is here to stay, and it’s part of the financial services ecosystem.”

Crypto World

Franklin Templeton Executes Tokenized U.S. Treasury Trade With Stablecoins on Canton Network

TLDR:

- Franklin Templeton exchanged a tokenized Treasury security for tokenized cash using on-chain settlement.

- The transaction paired a tokenized U.S. Treasury with USDCx and settled through Canton Network infrastructure.

- Tradeweb executed and priced the trade while several financial firms participated in the transaction.

- The deal occurred after market hours and was later reported to TRACE, according to Christopher Perkins.

Franklin Templeton has completed a tokenized U.S. Treasury transaction using stablecoins and on-chain settlement infrastructure. The trade involved the exchange of a tokenized Treasury security for tokenized cash on the Canton Network.

Tradeweb facilitated execution and price discovery while several financial firms supported the transaction. The deal adds to institutional efforts to move real-world assets onto blockchain-based financial rails.

Tokenized U.S. Treasury Trade Executes on Canton Network

Tradeweb announced the completion of the real-time transaction on July 1. The trade paired an on-chain U.S. Treasury with tokenized cash known as USDCx.

According to the announcement, Franklin Templeton transferred a tokenized Treasury security to Virtu Financial. In return, Virtu delivered USDCx through synchronized settlement on the Canton Network.

Tradeweb supplied the execution venue and pricing services for the transaction. The Canton Network coordinated the simultaneous movement of both assets on-chain.

Participants included Blockdaemon, Digital Asset, Franklin Templeton, Societe Generale, Tradeweb, and Virtu Financial. The transaction was also reported to TRACE after execution.

Christopher Perkins, president of CoinFund and former Coinbase executive, said on X that the trade took place after normal market hours. He noted that the transaction settled nearly instantly and represented another step toward continuous on-chain markets.

Tokenized Real-World Assets Gain Institutional Momentum

Tradeweb said the transaction demonstrates how tokenized U.S. Treasuries and tokenized cash can settle in real time. The company noted that traditional timing and settlement limitations did not apply to the process.

The transaction also arrives as the Canton Network prepares for the launch of DTCC’s Tokenization Services later this year. According to the announcement, the initiative aims to support broader access to high-quality liquid assets beyond traditional market hours.

Digital Asset said the transaction marked another milestone in developing always-on and interoperable capital markets infrastructure. The company added that continuous market making can increase asset utility and improve market accessibility.

Franklin Templeton described each tokenized transaction as another step toward a round-the-clock liquidity layer. The asset manager stated that on-chain capabilities can allow high-quality assets to move without the restrictions of standard market schedules.

Virtu Financial said the trade expands its market-making capabilities into tokenized U.S. Treasuries. The company added that blockchain-based settlement can support liquidity provision without conventional settlement constraints.

The Canton Network said active participation from firms including Franklin Templeton, Tradeweb, and Virtu Financial contributes to a unified framework for moving real-world assets across digital financial systems.

Strategy’s long streak as one of Bitcoin’s most consistent institutional buyers may be ending, according to Bitwise chief investment officer Matt Hougan. Speaking Thursday, Hougan suggested the company’s dominance as a “one-way” source of demand is likely to shrink in the next market cycle, after volatility around Strategy’s principal perpetual preferred stock product, Stretch (STRC).

The reassessment comes after STRC broke sharply from its $100 par value to below $75 late last month, a move that undermined investor confidence in the sustainability of Strategy’s dividend-style model. The timing also overlapped with broader market stress, when Bitcoin fell to a 21-month low of $58,190 on June 25.

Key takeaways

- Bitwise CIO Matt Hougan said Strategy’s era as Bitcoin’s dominant buyer may be over, with other institutional allocators expected to play a larger role next cycle.

- STRC’s move away from $100 par value below $75 fueled concerns about whether Strategy’s yield structure can hold up through “end-of-cycle” dynamics.

- Despite the STRC shock, Hougan argued Strategy is not facing near-term liquidity risk based on liquid asset coverage.

- Strive CEO Matt Cole pushed back, calling the STRC episode overblown and noting Strategy’s Bitcoin holdings are about 4% of total supply.

Strategy’s buyer dominance questioned after STRC turmoil

For years, Strategy has been widely viewed as a steady, high-conviction buyer of Bitcoin—helping provide consistent demand even when broader sentiment weakened. Hougan framed Thursday’s comments around a shift in what investors should expect from that demand profile.

“For years, Strategy has been the most dominant Bitcoin buyer in the world and a one-way source of Bitcoin demand. Those days are likely over,” Hougan said in a CIO memo, adding that he expects the company to be “less important” than it was in the previous cycle. In his view, banks, asset managers, pensions, endowments, and sovereign wealth funds may replace Strategy as Bitcoin’s primary demand engine as the next upcycle develops.

Hougan’s concern centers on how STRC behaved during a period when markets were already under pressure. The STRC incident raised fears that the structure underpinning dividend payments could be strained when conditions tighten—particularly in late-cycle environments where risk appetite falls and funding costs rise.

Why Hougan sees STRC as “end-of-cycle dynamics”

Hougan characterized the STRC drop as a pattern he associates with late-cycle stress. He compared the situation to a prior example in 2021: the collapse of Grayscale’s GBTC premium.

His argument is essentially about fit. According to Hougan, “money searching for high yields and low volatility was used to buy Bitcoin, which offers neither.” In that framing, the market eventually needs to “clear out” capital that was attracted by yield characteristics that Bitcoin itself does not reliably provide, before a more durable bottom can form.

This perspective matters for traders and longer-term investors because it reframes Strategy’s recent volatility away from a single-company solvency story and toward a broader liquidity-and-demand composition story—one where the source of marginal demand changes as the cycle matures.

Strategy responds: funding dividends and increasing reserves

In the aftermath of the STRC disruption, Strategy said it would sell Bitcoin when necessary to fund dividends, according to coverage earlier published by Cointelegraph. The company also expanded its US dollar reserve to $2.55 billion, easing some immediate concerns about operational coverage.

Even with those steps, Hougan said Strategy’s role as an aggressive buyer has weakened. The implication for market participants is that reserve moves and occasional Bitcoin sales can stabilize the dividend narrative in the short term, but may also reduce the consistency of net buying during turbulent periods.

Hougan nonetheless said he still expects Strategy to be a “net buyer” in the next bull run—suggesting the firm’s long-term posture may persist, even if its influence on price dynamics is likely to be less dominant than in the last cycle.

Debate over materiality and liquidity risk

While STRC became the focal point, Strategy leadership pushed back on how much attention the incident deserves. Strive CEO Matt Cole argued that the episode has been overemphasized by media and that Bitcoin’s selloff may have been driven more by the broader market than by any single factor.

Speaking with NovaDius Wealth Management president Nate Geraci, Cole noted that Strategy’s 847,363 Bitcoin represents about 4% of total supply. He also referenced US Securities and Exchange Commission standards for materiality, stating that a 4% stake would not be considered material under SEC thresholds, which he described as starting at 5%.

“If one person owned 4%, you don’t even have to report that publicly to the SEC because the SEC deems 4% to be immaterial. They start to view a position to be material at 5%.”

Hougan, meanwhile, addressed liquidity in a more quantitative way. He said Strategy has $52 billion worth of liquid assets marked against $7 billion of debt. In his assessment, Bitcoin would need to fall another 70%—to roughly $18,500—for Strategy to face risk. He also added that if the company began selling Bitcoin immediately, it could cover dividends from STRC and other perpetual preferred stock offerings for the next 28 years.

Taken together, the two positions highlight a tension that investors should watch: one view suggests the STRC mechanism is a late-cycle stress test that affects demand composition and price, while the other emphasizes reserve coverage and argues that the company’s balance sheet prevents an immediate liquidity threat.

For now, the key question is not whether Strategy can operate through the current strain, but whether the market’s next wave of Bitcoin buying will be driven by the same yield-seeking, vehicle-based demand—or by a broader set of long-term allocators that Hougan expects to take a bigger share.

As conditions evolve, investors should monitor whether STRC stabilizes relative to par and whether Strategy’s net buying pace remains consistent enough to reassert influence—while also tracking if incremental demand truly shifts from Strategy-style products to the wider institutional categories Hougan cited.

Riot Platforms transferred another 500 BTC to NYDIG Custody, according to Arkham data cited by onchain trackers.

Summary

- Riot Platforms moved another 500 BTC to NYDIG Custody, raising fresh sale speculation among traders.

- The miner already sold 3,778 BTC in Q1 while producing only 1,473 BTC total.

- Public Bitcoin miners continue selling reserves as mining costs rise and margins remain under pressure.

The transfer was worth about $30.72 million at the time of the report and was shared through an Onchain Lens post.

The move may signal that Riot is preparing to sell part of its Bitcoin holdings. Transfers to custody or execution partners do not always confirm a sale, but similar Riot transfers this year have often come before reported selling activity.

Another move in a longer sale pattern

The latest transfer follows earlier Riot activity involving NYDIG. As crypto.news reported in April, Riot sent 500 BTC to an NYDIG deposit address in a move worth about $39 million at the time. That report said the transfer added to a series of Bitcoin moves from Riot over the same period.

Riot had also disclosed large Bitcoin sales in its first-quarter 2026 operations update. The company sold 3,778 BTC in Q1 for about $289.5 million. It sold those coins at an average net price of $76,626 per BTC.

Riot produced 1,473 BTC in the first quarter, down 4% from 1,530 BTC in the same period a year earlier. Its BTC holdings fell to 15,680 at quarter-end, down 18% from 19,223 in Q1 2025. The company said 5,802 BTC were restricted at the end of the quarter.

Riot’s Q1 results also showed pressure in its mining business. Bitcoin mining revenue fell to $111.9 million from $142.9 million a year earlier. Riot linked the decline to lower average Bitcoin prices and higher network hash rate.

Miner selling pressure continues

Riot’s latest BTC movement comes as public miners face tighter economics after the Bitcoin halving. Higher mining difficulty, lower hashprice, energy costs, and capital needs have pushed several listed miners to sell reserves.

As crypto.news reported, publicly traded Bitcoin miners sold more than 32,000 BTC in the first quarter of 2026. That was a record quarterly figure and topped the amount sold by the same firms across all of 2025. Riot, MARA, CleanSpark, Cango, Core Scientific, and Bitdeer were among the miners named in that wider trend.

Riot also continues to expand beyond Bitcoin mining. The company has been building a data center business while using its power assets and infrastructure to serve high-performance computing customers. That shift gives the miner another capital need at a time when mining margins remain tight.

The 500 BTC transfer does not confirm an immediate sale on its own. Still, the timing adds to the market’s focus on Riot’s treasury strategy.

Ether and solana led crypto higher on Friday as a squeeze on bearish traders pushed bitcoin toward $62,000, capping the market’s first genuinely strong week since mid June.

Bitcoin traded around $61,360, up 2.5% over seven days, per CoinDesk data. Ether rose 4.2% in 24 hours to about $1,702 and is up 9.7% on the week, while solana held near $80 with a weekly gain of 18.6%, the strongest among the majors. XRP added 5.7% over the week to $1.09 and Hyperliquid’s HYPE rose 5.1% on the day.

Traders betting against crypto lost $281 million to liquidations over the past 24 hours, against $159 million in longs, out of $440 million in total forced closures across 95,690 traders, according to Coinglass data.

When shorts are forced to close, they buy back the asset, and that buying pushes prices into the next tranche of shorts, the loop that turns a modest bounce into a squeeze.

The largest single liquidation was an $18.2 million ether position on Hyperliquid, fitting a day when ether led the damage to bears at $157 million in wiped positions against bitcoin’s $103 million in an unusual flip.

Get these H&M Old Money Finds for your summer wardrobe!

Looking for something to do? Five events happening in Bolton this week

Emerald Resources awards MACA $562m work

No Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

Renter of Home in Anne Heche Crash Denies Settlement With Son

Weekend Open Thread: Staud – Corporette.com

Get these H&M Old Money Finds for your summer wardrobe!

$200K Bitcoin: Michael Saylor Explains the Lagging Price and How We Will Get There

ARE YOU POOR?: Why You’re Broke | ABC of Money #money #finance #aiart #shorts #animation

-

Fashion7 days ago

Fashion7 days agoWeekend Open Thread: Staud – Corporette.com

-

Crypto World3 days ago

Crypto World3 days agoStrategy authorizes up to $1.25B in Bitcoin sales under new capital plan

-

Business7 days ago

Business7 days agoAsia stock markets slide as tech shares slump

-

News Videos5 days ago

News Videos5 days agoMAJOR BITCOIN & MARKET UPDATE!!!! (MUST WATCH ASAP!!!)

-

Tech3 days ago

Tech3 days agoAnonymous researcher drops 0-day ‘exploitarium’ repo

-

Crypto World6 days ago

Crypto World6 days agoCoinbase, Circle Deepen Crypto Stock Losses Despite Resilient S&P 500

-

Business3 days ago

Business3 days agoAustralia treasurer says alleged access of prime minister’s bank data ’incredibly concerning’

-

Crypto World6 days ago

Crypto World6 days agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Sports6 days ago

Sports6 days agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Tech5 days ago

Tech5 days agoBluekit phishing kit adopts browser-in-the-middle for login theft

-

Tech6 days ago

Tech6 days agoRussian hackers now target Signal backup recovery keys

-

Crypto World7 days ago

Crypto World7 days agoTether (USDT) Passes Ether in Market Cap as ETH Drops Toward $1.5K

-

Crypto World7 days ago

Hyperliquid Named on Singapore MAS Investor Alert Register

-

Crypto World7 days ago

Crypto World7 days agoRTX holders must register wallets before token distribution begins

-

Sports2 days ago

Sports2 days agoBroncos roster: OL Ben Powers (No. 74) entering final year of contract

-

Business4 days ago

Business4 days agoThe AI boom won’t burst all at once. It will pop in ‘rolling bubbles’: Macquarie

-

Tech5 days ago

Tech5 days agoClaude Code turned every engineer into three. Now companies need more product thinkers

-

Crypto World7 days ago

Crypto World7 days agoSpaceX Called a Market Top Signal Just 2 Weeks After Its $86 Billion IPO

-

Tech6 days ago

Tech6 days agoSilicon Valley paid to kill AI regulation, now it wants the rules back

-

NewsBeat2 days ago

NewsBeat2 days agoPresenter Caroline Flack’s brother Paul Flack dies aged 55

You must be logged in to post a comment Login