Crypto World

Bitcoin Open Interest Falls $3B as BTC Deleveraging Exposes Fragile Market Structure

TLDR:

- Bitcoin Open Interest fell from $27B to $24B, reflecting broad long position closures across the derivatives market.

- Funding rates stayed slightly positive, confirming shorts are not leading BTC’s current price correction phase.

- One-hour heatmap data showed no major liquidity zones, pointing to capital outflows rather than liquidity hunting moves.

- Analyst Carmelo Alemán noted BTC’s price decline is a consequence of prior structural weakness, not a fresh bearish trigger.

Bitcoin Open Interest has declined sharply, drawing attention to the market’s weak structural foundation. On-chain analyst Carmelo Alemán noted that BTC’s recent price pullback aligns with a notable drop in derivatives exposure.

Open Interest fell from roughly $27 billion to $24 billion. This pattern reflects long position closures and progressive deleveraging rather than aggressive selling. The data confirms that the earlier rally lacked real spot demand and was largely built on leveraged positions.

BTC Price Decline Tied to Derivatives Deleveraging

Bitcoin’s recent correction is directly connected to a derivatives-heavy market structure. Alemán had previously raised concerns that the bullish move lacked structural consistency.

The rally was fueled by futures activity rather than genuine demand in the spot market. Recent market behavior has since confirmed that earlier assessment clearly.

Open Interest dropping from $27 billion to $24 billion captures the full scope of the unwind. Long positions have been closing at a steady pace, pulling down overall derivatives exposure.

This process does not point to aggressive bearish pressure from short sellers. Instead, it reflects a gradual, market-wide effort to reduce leveraged exposure.

Heatmap analysis on the one-hour timeframe adds further context to the price movement. Based on TradingDifferent visual data, no major contiguous liquidity zones were identified in the area.

This rules out liquidity hunting or stop-loss sweeps as the primary driver behind the move. The price action therefore reflects capital outflows rather than directional pressure from either side.

Alemán, a verified contributor on CryptoQuant, noted that this outcome was foreseeable. A move built on derivatives tends to lose consistency once leverage begins coming off.

The price decline is not the root of the problem but a consequence of earlier fragility. The weak structural base was already present before the correction started materializing.

Positive Funding Rates Signal Risk Reduction, Not Bearish Control

Funding rates have remained slightly positive even as Bitcoin’s price continues to pull back. This is an important data point when assessing who is leading the current market move.

Positive funding rates show that long traders are still paying short traders a small periodic fee. Shorts are not the dominant force pushing prices lower at this stage.

Alemán noted that the market is not attacking the downside. Rather, participants are collectively choosing to reduce their derivatives exposure in an orderly way.

There is no evidence of coordinated short-side aggression driving the current phase. The correction aligns more with disciplined deleveraging than with a fresh bearish trend forming.

The one-hour heatmap data also supports this more neutral reading of market structure. Without major liquidity clusters nearby, price tends to drift lower in a measured, methodical manner.

The sharp, reactive moves typical of liquidity-driven markets are largely absent here. This reinforces the view that capital outflows, not targeted selling, are steering the current phase.

Bitcoin Open Interest contraction is clearing the excess leverage that accumulated during the earlier rally. Once this process runs its course, the market may find a more stable structural base.

Alemán’s analysis ties the current correction directly to the previously identified weakness in market structure. The price decline reflects the consequence of that fragility rather than a fresh bearish catalyst.

TLDR:

- Vitalik Buterin said the Ethereum Foundation will reduce its influence across the broader ecosystem.

- Ethereum leadership placed stronger focus on decentralization, privacy, and censorship resistance goals.

- Buterin rejected speed-focused blockchain competition while defending Ethereum’s long-term technical roadmap.

- Michaël van de Poppe linked weak Ethereum sentiment with potential long-term accumulation opportunities.

Ethereum co-founder Vitalik Buterin shared a detailed update on the future direction of the Ethereum Foundation and its long-term priorities. He said the organization plans to reduce its central role while focusing more heavily on decentralization, privacy, and censorship resistance.

The comments appeared as Ethereum continued facing weak price performance against several major crypto assets. The discussion also resurfaced broader debates around Ethereum’s technical roadmap and institutional role inside the crypto market.

Ethereum Foundation Shifts Toward Decentralization and Privacy

Buterin said the Ethereum Foundation does not serve as the center of Ethereum. Instead, he described it as one participant among many across the ecosystem.

He explained that the foundation plans to become smaller and more selective over time. According to his post, the board is also expanding while his own influence inside the organization decreases.

Buterin credited Aya Miyaguchi for executing much of the organizational transition. He also noted that most of his recent involvement focused on technical questions.

The Ethereum co-founder said earlier operational problems inside the foundation had already improved during 2025. He added that the remaining concern involved whether the foundation’s actions matched Ethereum’s stated principles.

His comments focused heavily on decentralization, privacy, and resistance to censorship or external control. He argued Ethereum should avoid becoming another blockchain optimized only for speed and transaction throughput.

Buterin also discussed Ethereum’s long-term technical direction. He pointed to AI-assisted formal verification as a path toward bug-free blockchain infrastructure and stronger network security.

The post further highlighted efforts around public mempools, intermediary minimization, and lean consensus systems. He described those areas as central to Ethereum’s identity and technical differentiation.

According to Buterin, the Ethereum Foundation currently holds roughly 0.16% of total ETH supply. He contrasted that figure with other blockchain foundations that reportedly control much larger allocations.

Ethereum Market Debate Grows as $ETH Underperforms

The Ethereum discussion spread quickly across crypto social media following Buterin’s statement. Many traders linked the comments to Ethereum’s recent market performance.

Crypto trader Michaël van de Poppe argued that weak sentiment around Ethereum could create accumulation opportunities. His comments focused on capital rotation away from short-term outperforming assets.

Van de Poppe said many traders were moving away from Ethereum after months of weaker price action. He suggested some investors now viewed current ETH valuations differently from high-momentum tokens.

Buterin also addressed Ethereum’s scaling direction during the post. He said Ethereum should not compete purely on maximum throughput or extremely low latency.

Instead, he emphasized security, censorship resistance, and open infrastructure. He described those goals as more important than matching the fastest blockchain networks.

The post additionally referenced Ethereum layer-2 systems and specialized scaling networks. Buterin said properly designed L2s could still support higher transaction capacity without weakening Ethereum’s core principles.

He also noted that most of his personal net worth remains allocated to ETH. According to the statement, the rest mainly supports open-source biotech, software, and hardware initiatives.

Vitalik Buterin, Ethereum’s co-founder, has pushed back against criticisms that the Ethereum Foundation should play a more aggressive, market-facing role in supporting token prices or marketing efforts. In a public note and subsequent remarks, Buterin outlined a recalibrated view of the Foundation’s remit, stressing that its mandate is to advance censorship resistance, open-source software, long-range research, cybersecurity, and the decentralization of the Ethereum protocol.

In a reframing of the Foundation’s position, Buterin emphasized that the EF is “not a centre of Ethereum,” but rather “one node, with a defined purpose, alongside other nodes.” He added that the Foundation has always advocated for the latter role, even as some in the ecosystem — and within the EF itself — urged a shift toward a more centralized, marketing-driven function. “Now, we are taking action to ensure that we will be the latter,” he said, signaling a deliberate move away from any perception that the EF is the ecosystem’s controlling hub.

“EF is not a ‘center of Ethereum’, rather EF is ‘one node, with a defined purpose, alongside other nodes’. We have always said that the EF should be the latter, but many in the Ethereum ecosystem, and even within the EF, wanted us to be the former.”

The Ethereum Foundation’s mandate, published in March 2026, frames its activities around long-term governance and core protocol resilience. Buterin signaled that the Foundation’s future focus would be on strengthening Ethereum’s cybersecurity, maintaining a robust codebase, and supporting research that underpins long-range, decentralized growth — rather than competing with high-throughput networks or chasing rapid user growth through promotional campaigns.

These comments come amid ongoing market pressure on Ethereum and heightened scrutiny of the Foundation’s role. A number of large ETH holders have liquidated portions of their positions, underscoring the tension between tokenomics and market sentiment. At the same time, leadership changes within the EF — including high-profile departures — have intensified questions about the organization’s capacity to influence the ecosystem’s trajectory.

Buterin acknowledged that the Ethereum Foundation possesses a relatively small stake in ETH, noting that it holds roughly 0.16% of the total supply. He contrasted this with other foundations in the crypto space, which in some cases hold much larger percentages of their native tokens. The point, he argued, is that a token’s health is not built on the Foundation’s balance sheet alone but on the broader, long-horizon work it funds.

Meanwhile, the industry has been weighing tokenomics as a central factor in Ethereum’s post-Dencun landscape. The Dencun upgrade — a major protocol update released in March 2024 — significantly reduced layer-1 fees for layer-2 transaction activity, a shift that coincided with a notable drop in base-layer revenue. As Laura Shin, a veteran crypto journalist, observed, many market participants have struggled to reconcile Ethereum’s high development ambitions with the immediate measures that impact token economics.

“I think Ethereum’s original sin was not considering tokenomics with every move it made from Dencun on,” Shin remarked, highlighting the persistent tension between on-chain efficiency gains and the market’s appetite for tangible, price-related signals.

In the near term, the price environment has remained challenging. At the time of reporting, Ethereum traded around $2,094, still more than 50% below its all-time high of nearly $5,000 reached in August 2025. The price backdrop has fed a narrative among some investors that the ecosystem’s structural improvements will take time to translate into broader market enthusiasm.

Against this backdrop, the Ethereum Foundation has signaled a shift in its treasury strategy. Buterin stated that the EF plans to “focus on longevity” and stretch its funds to finance research, implying a potential reduction in the pace of ETH sales in the future. This comes after months of treasury moves designed to balance research funding with the realities of a bear-leaning cycle.

In May, the Foundation unstaked 21,270 ETH from the Lido liquid staking platform as part of its treasury management. Unstaking such a portion of ETH could affect yield generation for the Foundation, though a direct sale of those tokens had not been confirmed at press time. The unstaking decision aligns with a broader effort to optimize funds for long-term research and protocol work rather than short-term liquidity events.

The evolving stance from the EF — coupled with ongoing debates about tokenomics, governance, and the role of large holders — continues to shape investor expectations. The market is watching not only how the Foundation deploys resources but how its actions intersect with the broader dynamics of Ethereum’s scaling roadmap and security posture, including ongoing research into censorship resistance and decentralization.

Several industry observers have framed the Foundation’s role as a stabilizing force in a rapidly evolving ecosystem. A core question remains: will the EF’s emphasis on longevity and openness translate into measurable gains for developers, users, and long-horizon holders, or will market dynamics continue to demand more immediate signals from institutions within the Ethereum ecosystem?

Under pressure amid shifting tokenomics and leadership changes

The timing of these remarks coincides with broader investor sentiment shifts. The market has seen a number of high-profile departures from the Ethereum Foundation, and questions persist about whether such moves reflect a broader recalibration of influence within the ecosystem. In parallel, major holders’ selling activity — including reports of large-scale exits from long-standing ETH positions — has kept price action in check and heightened scrutiny of the EF’s treasury strategy.

Critics have argued that a token’s value should be anchored not only in protocol upgrades and research outputs but also in transparent, policy-driven actions that align with investors’ expectations. Buterin’s response emphasizes governance and resilience over marketing and market-making. He reiterated that the EF’s core mission remains focused on enabling a robust, decentralized Ethereum via open-source software, robust security, and long-term research, rather than acting as a cash-generating, brand-building entity.

In practical terms, readers should watch how the EF allocates funding for critical research programs, cybersecurity initiatives, and codebase improvements. The impact on developer activity, network reliability, and ecosystem incentives may take time to materialize in price signals, but could influence Ethereum’s long-run trajectory as a decentralized platform.

For investors and builders, the episode underscores a broader market truth: token prices respond to a complex mix of tokenomics, on-chain efficiency, governance credibility, and the visibility of foundational research. As Ethereum continues to evolve, the balance between accelerator programs and foundational stability will shape how the ecosystem translates technical progress into real-world adoption.

Meanwhile, observers will closely monitor any further treasury actions by the Foundation. The question remains whether the EF will maintain a lean, long-horizon funding model or adjust its holdings in response to market conditions, regulatory developments, and the pace of protocol upgrades. In any case, the emphasis on longevity and decentralization signals a deliberate attempt to preserve Ethereum’s core values even as market dynamics push for quicker, price-driven outcomes.

With the mandate now clearly articulated, market participants will want to see how these principles translate into concrete outcomes: deeper security auditing, more robust layer-2 compatibility, and continued open-source growth that can withstand scrutiny from regulators and competitors alike. The coming months will reveal whether the Ethereum Foundation’s refined role can coexist with the ecosystem’s broader ambitions and the market’s appetite for visible progress.

Readers should remain attentive to updates on the EF’s funding priorities and any further shifts in treasury policy, as well as to how major holders and developers react to a framework that prioritizes longevity and resilience over short-term market signaling.

Related coverage: blockchain researchers defend the Ethereum Foundation’s exact role in the ecosystem, arguing that it is performing its job as defined.

What comes next for Ethereum’s governance and tokenomics?

As Ethereum navigates a post-Dencun world and a market that remains sensitive to tokenomics, the question for many investors is whether a more restrained, longevity-focused Foundation will foster sustainable long-term value. The roadmap remains significant: continued improvements to security, scalability where appropriate, and governance practices that align with decentralized principles. If the EF’s actions translate into stronger code quality, fewer security incidents, and clearer funding for long-range research, the ecosystem could gradually gain the stability that price rallies alone cannot deliver.

In sum, Vitalik Buterin’s reaffirmation of the Ethereum Foundation’s role reflects a broader shift toward governance that prioritizes resilience and open development over marketing-driven market signaling. The market’s reaction over the coming months will hinge on tangible outcomes from funded research, code improvements, and the Foundation’s ability to sustain innovative work without drift toward centralized gatekeeping.

What to watch next: any updates on the EF’s treasury strategy, further treasury movements, and new research initiatives that address core protocol challenges. As Ethereum continues to mature, investors and developers will gauge whether the Foundation’s clarified mandate translates into a healthier, more decentralized ecosystem that can weather price volatility and regulatory scrutiny alike.

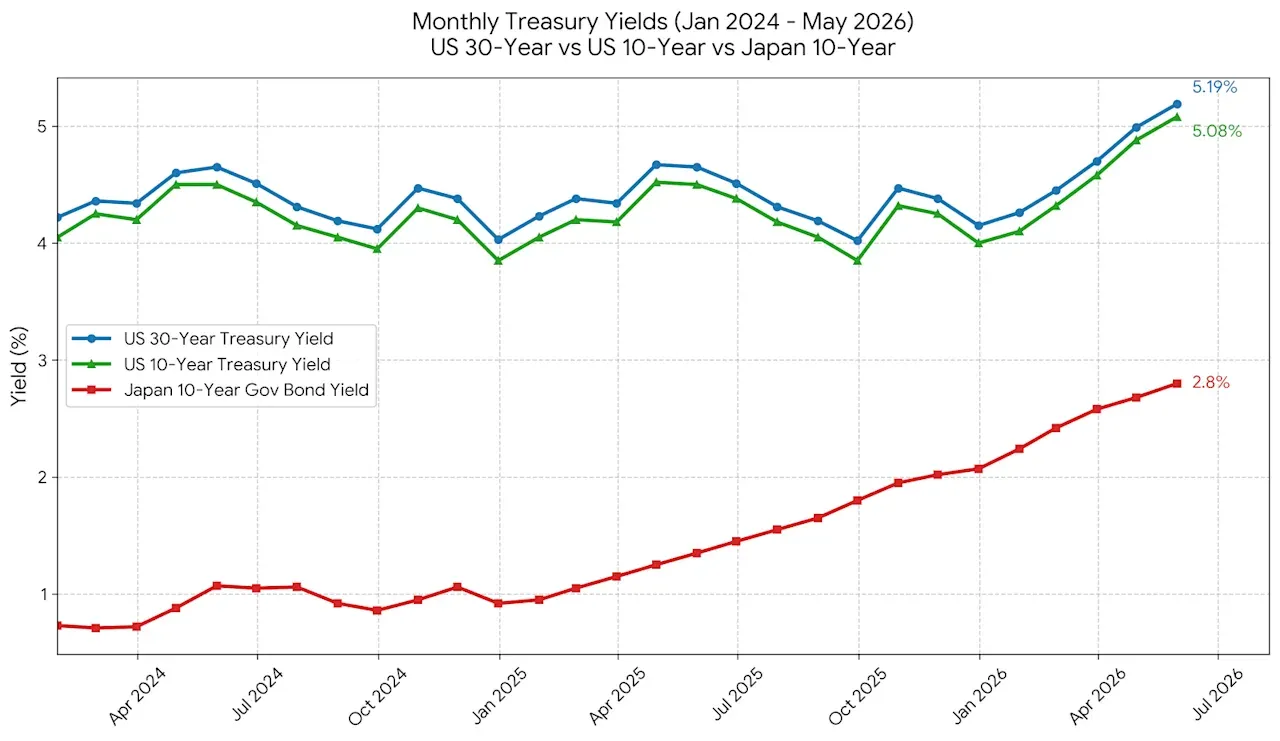

Rising government bond yields signal a coming “structural” shift that will create a Bitcoin “supercycle” of rising prices, as investors flee debasing assets for one that cannot be inflated, according to Shang Wu, a senior research analyst at crypto exchange BitMEX.

The yield on the 30-year US Treasury broke past 5.14% on Tuesday, while the Bank of Japan’s 10-year government bond yield touched 2.8%, Wu said.

These yields are unsustainable in the long-term and will force governments to choose between debasing their currencies and a “sovereign debt collapse,” Wu said.

Bond yields for US and Japanese government debt from April 2024 to May 2026. Source: BitMEX

“Central banks are backed into a corner. They must choose between a sovereign debt collapse and debasing their currencies,” Wu said. According to the analyst:

“For Bitcoin, the upcoming volatility will be chaotic in the short term, but it serves as the ultimate structural tailwind for a long-term supercycle.”

The analysis comes as the US national debt crosses $39 trillion, and growing geopolitical tensions threaten to boost government spending, while the ongoing war in Iran causes a surge in energy prices and a corresponding inflationary spike.

Related: Bitcoin bounces as Trump prepares to announce ‘negotiated’ Iran deal

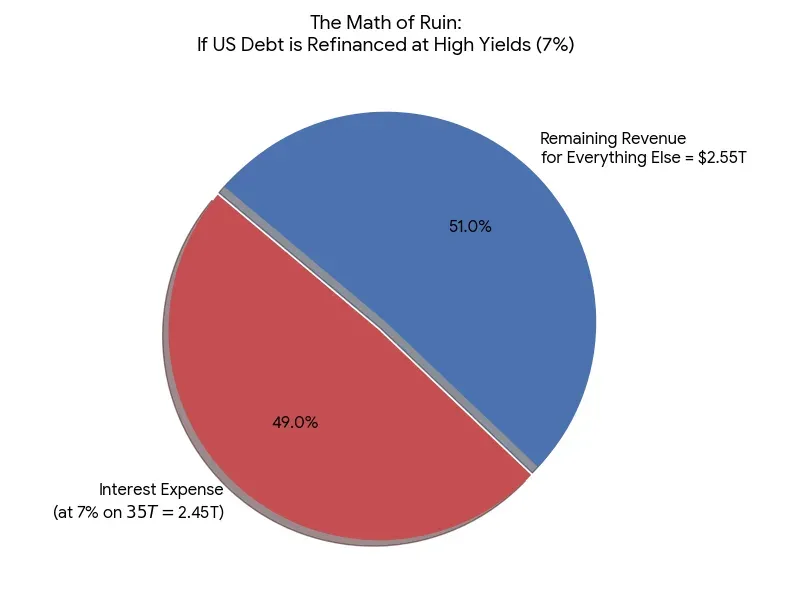

Rate hike won’t solve problem, it will simply bankrupt the government

Central banks typically use higher yields to tamp down inflation by restricting access to credit; when borrowing costs are high, consumers and investors borrow less, and asset prices fall.

However, the $39 trillion US national debt, which continues to grow due to deficit spending, makes it impossible to control inflation by raising interest rates, as the higher rates would also increase the government’s debt servicing costs, Wu said.

A forecast of what the annual US budget would look like if bond yields spike to 7%. Source: BitMEX

“With the national debt at $39 trillion, keeping rates at these levels means the annualized interest expense of the government will soon consume the entire federal tax base,” according to the analyst.

Wu and others, including macroeconomist Lyn Alden, say that the government and central banks will attempt to disguise quantitative easing by adding liquidity through other methods like yield curve control and unannounced buybacks of US government debt.

Magazine: Big Questions: Can Bitcoin save you from the dreaded Cantillon Effect?

TLDR:

- ZEC’s MVRV ratio climbed to 1.59 as the asset traded above its realized price level

- Rising open interest and short liquidations continue supporting the latest ZEC price expansion

- Alphractal warned declining active addresses may weaken the sustainability of the current rally

- Trader Ardi identified the $700 region as the next major resistance zone for ZEC price action

ZEC has extended its sharp recovery as traders monitor rising derivatives activity and improving profitability metrics.

Data shared by Alphractal showed the privacy-focused cryptocurrency trading in aggregate profit territory after its MVRV ratio climbed above 1.0.

The token also posted strong daily gains while reclaiming levels above its 200-day moving average. However, weakening network activity has raised questions about the sustainability of the latest move.

ZEC Price Rally Accelerates as MVRV Turns Bullish

Alphractal said ZEC’s MVRV ratio reached 1.59 while the asset traded near $632.88. The realized price stood around $367.50 according to the firm’s shared metrics.

The platform described the current MVRV structure as constructive rather than euphoric. Historical ZEC cycle tops reportedly formed above 3.5 on the same metric.

Alphractal also tracked ZEC’s Net Unrealized Profit and Loss indicator, known as NUPL. The metric currently sits inside the “Optimism” zone according to the report.

The firm stated previous entries into that phase aligned with continued upside before reaching stronger euphoria conditions. ZEC also gained 7.19% during the latest 24-hour trading period.

Price action continued trading well above the 200-day moving average. Alphractal described the broader trend structure as clearly bullish on higher timeframes.

Derivatives data also showed rising participation across futures markets. Open interest increased on both daily and weekly measurements according to the report.

The platform additionally highlighted a 0.56 long-to-short ratio alongside increased short liquidations. That combination often appears during short squeeze-driven market moves.

ZEC Trading Activity Diverges From Network Usage Metrics

Despite the strong price recovery, Alphractal identified weakening on-chain activity as a risk factor. Active addresses and transaction counts reportedly declined sharply over the past week.

The report suggested the rally currently relies more on derivatives positioning than organic network growth. Alphractal described the move as real but structurally fragile.

According to the framework shared in the post, continued upside depends on either stronger usage metrics or sustained leverage flows. The firm said active address trends remain the key confirmation signal.

Crypto trader Ardi also discussed ZEC’s broader technical structure in a separate post. He described the chart as one of the stronger macro recovery setups currently visible across the market.

Ardi said ZEC completed a V-shaped recovery into the upper range near $680 after reclaiming its prior corrective structure. However, he noted that a clean break above the $700 resistance zone remained necessary before stronger continuation signals appear.

The trader pointed toward the $740 area as the next upside region if support confirms above resistance. The comments followed one of ZEC’s strongest recovery periods in recent months.

Alphractal maintained that extreme funding conditions without improving address activity could become an exit signal for traders. The firm said leverage-driven rallies often weaken once participation fades.

TLDR:

- Brian Armstrong highlighted tokenization as a major priority for future financial infrastructure

- Coinbase’s CEO linked stablecoins and AI systems to faster and cheaper global financial services

- Armstrong called for risk-based crypto regulation instead of broad industry-wide restrictions

- The post tied blockchain networks to startup funding, open access, and self-custodial finance

Coinbase CEO Brian Armstrong has outlined several areas where he believes the global financial system still requires major upgrades.

His comments focused on tokenization, stablecoins, AI-powered finance, and broader access to capital markets.

The post quickly gained attention across crypto discussions because it tied blockchain infrastructure to long-term financial reform. Armstrong also highlighted regulation and self-custody as central parts of the industry’s next phase.

Brian Armstrong Pushes Tokenization and Global Crypto Trading

Armstrong shared the framework through a post on X outlining eight sectors he believes still need modernization. The list placed tokenization of real-world assets at the center of future financial infrastructure.

According to the post, tokenized assets could include real estate, stocks, bonds, and investment funds. Armstrong said blockchain-based settlement may improve distribution and fractional ownership access.

The Coinbase executive also pointed to round-the-clock global trading as another major gap in traditional finance. He described a system where global liquidity pools allow faster trading access across borders.

Stablecoin payments formed another key part of the discussion. Armstrong referenced near-instant and lower-cost international transfers, including payments tied to AI agents and automated systems.

The comments arrive as tokenization continues gaining traction among crypto firms and traditional financial institutions. Several large firms have recently explored blockchain settlement systems and tokenized treasury products.

Armstrong also linked open blockchain protocols with expanded financial participation. He said self-custodial wallets and smartphone-based access could reduce reliance on traditional intermediaries.

Coinbase CEO Highlights AI, Regulation, and Capital Formation

Armstrong’s post also focused heavily on artificial intelligence within finance. He said AI-powered systems may improve risk analysis, compliance checks, fraud detection, and financial advice.

The comments connected crypto infrastructure with automated financial tools that operate across digital networks. Armstrong described broader access to financial guidance through AI-driven systems.

Regulation also appeared as a central theme throughout the post. Armstrong argued for risk-based regulatory frameworks instead of broad rules that treat all crypto activity equally.

The Coinbase executive said innovation-friendly regulation could increase competition and reduce barriers for startups. He tied those changes to future capital formation across blockchain markets.

Armstrong also described blockchain networks as tools for cheaper fundraising. According to the post, lower issuance costs could help more startups access investment opportunities.

The final section focused on sound money and inflation concerns tied to fiat systems. Armstrong described cryptocurrency as a possible refuge during periods of declining monetary discipline.

His remarks reflected a wider push across the crypto industry toward integrating blockchain systems with traditional finance infrastructure. The post also reinforced how tokenization, stablecoins, and AI remain central themes in current crypto market development.

TLDR:

- Strategy holds about 843,768 Bitcoin with an average acquisition price near $75,700 per BTC

- Michael Saylor’s “BitVac is charging” post sparked fresh speculation about another BTC purchase

- Strategy reportedly added over 171,000 Bitcoin during 2026, exceeding new miner output

- The company continues funding Bitcoin buys through stock sales and preferred share offerings

Michael Saylor has again triggered Bitcoin market speculation with a new social media message tied to Strategy’s treasury activity.

The company executive posted “BitVac is charging” as traders watched for another corporate Bitcoin purchase. Strategy already holds one of the world’s largest Bitcoin reserves among public companies.

The latest signal also arrived as investors tracked the firm’s funding plans, debt restructuring, and comments around possible future Bitcoin sales.

Michael Saylor Bitcoin Signal Revives Strategy Buy Expectations

Saylor shared the “BitVac is charging” message through his X account, drawing immediate attention from Bitcoin traders. Similar posts have often appeared before Strategy disclosed additional Bitcoin purchases.

The company currently holds around 843,768 Bitcoin according to figures cited in the report. Strategy’s average acquisition price stands near $75,700 per Bitcoin.

Bitcoin traded close to $75,958 during the latest market session. That price placed the asset slightly above Strategy’s average cost basis.

Strategy’s Bitcoin purchases this year have reportedly exceeded newly mined Bitcoin supply worldwide. The company added more than 171,000 BTC during 2026 based on the supplied figures.

That accumulation pace has increased Strategy’s influence across Bitcoin markets. Investors now closely monitor both the company’s treasury moves and financing structure.

The firm’s Bitcoin strategy has transformed its market identity over recent years. Many investors now view Strategy primarily as a leveraged Bitcoin holding company rather than a software business.

Strategy Funding Model and Bitcoin Sales Draw Focus

Strategy has financed recent Bitcoin purchases through common stock offerings and preferred shares. The company’s STRC preferred shares reportedly carry an 11.5% dividend.

The company also moved to repurchase approximately $1.50 billion in convertible notes. That decision reflected continued adjustments to its capital structure.

Saylor recently discussed Strategy’s long-term Bitcoin approach during appearances on Coin Stories and The Wolf Of All Streets podcast. He said management remains focused on maximizing Bitcoin per share over time.

The comments marked another example of Strategy linking corporate performance directly to Bitcoin accumulation. That approach has shaped how shareholders evaluate the company.

Saylor also suggested limited Bitcoin sales could occur under certain conditions. The remarks drew attention because Strategy has historically promoted a long-term holding strategy.

According to comments cited from The Wolf Of All Streets podcast, Saylor said credit rating agencies must recognize Bitcoin as an asset. The statement followed discussion around Strategy’s financing model and balance sheet structure.

Strategy shares closed at $159.89 during the latest trading session based on Google Finance data referenced in the report. The stock declined 10.86% during the previous 30 days.

Market participants continue tracking Strategy’s next Bitcoin move after the “BitVac” signal. Traders are also watching how future purchases could affect funding costs and broader Bitcoin demand.

TLDR:

- Tom Lee warned of a possible bear market while BitMine continued buying Ethereum during the decline

- BitMine recently acquired another 60,000 ETH through wallets linked to Kraken and BitGo

- Ethereum traded near $2,093 while remaining roughly 57% below its reported 2025 peak

- BitMine’s Ethereum treasury now exceeds 5.2 million ETH, equal to 4.37% of supply

Tom Lee’s latest bear market warning has reignited debate across the crypto market. The comments surfaced as BitMine continued expanding its Ethereum treasury despite prolonged ETH weakness.

Blockchain tracking data showed the firm recently acquired another 60,000 ETH through wallets linked to Kraken and BitGo. The move arrived while Ethereum traded more than 50% below its reported 2025 peak.

Tom Lee Bear Market Warning Puts Ethereum Strategy in Focus

Crypto Tony shared Lee’s warning on X, drawing immediate attention from traders monitoring broader market conditions. The discussion intensified because BitMine has remained aggressive with Ethereum accumulation.

BitMine launched its Ethereum treasury strategy in July 2025 following a $250 million private placement. The company later disclosed holdings of 163,142 ETH valued near $500 million at the time.

Since then, the firm has steadily expanded its position during periods of market weakness. Recent blockchain activity tracked by Lookonchain pointed to another 60,000 ETH purchase worth roughly $126 million.

The transactions reportedly moved through newly created wallets connected to Kraken and BitGo infrastructure. Blockchain investigator EmberCN also linked the transfers to BitMine’s treasury activity.

The latest acquisition pushed BitMine’s reported Ethereum holdings above 5.2 million ETH. That figure represents about 4.37% of Ethereum’s circulating supply.

Lee has continued defending the treasury strategy during the decline. According to the report, he viewed Ethereum prices below $2,200 as an attractive accumulation zone.

BitMine ETH Treasury Expands Despite Ethereum Market Weakness

Ethereum traded near $2,093 during the latest market session according to TradingView data. The asset remained roughly 57% below its reported 2025 high.

BitMine previously indicated it would slow future Ethereum purchases during May. However, the company did not signal an end to the treasury plan.

The firm still aims to control 5% of Ethereum’s total supply before December. That target has kept attention fixed on BitMine’s accumulation pace.

Meanwhile, traders continue monitoring Ethereum’s technical structure. Market watchers highlighted a rising wedge formation during the recent recovery attempt.

Some technical setups referenced in the report pointed toward possible downside near $1,600 if support levels fail. A move lower could increase unrealized losses tied to BitMine’s holdings.

Based on reported treasury data, estimated paper losses could approach $10.1 billion depending on Ethereum market prices. The calculation used an average acquisition cost near $3,513 across 5.28 million ETH.

At the same time, rebound scenarios remain active across trading discussions. Analysts tracking the wedge formation identified $2,530 near the 200-day moving average as a resistance level if buyers regain momentum.

Changpeng Zhao (CZ) denied a viral rumor that claimed he went missing in a Dubai surfing accident on Sunday. The fabricated story spread first through Chinese-language WeChat groups.

In his pushback, the Binance founder noted Dubai is not a surfing destination but opportunistic traders had already spun up tiny meme coins on Solana and BNB Chain.

Hoax Triggers Wave Of Low-Cap Meme Coin Launches

The fabricated post claimed CZ had been swept out to sea near Jumeirah beach as rescue teams searched.

“According to eyewitnesses and security personnel at the scene, the sea appeared calm at the time, but the rip current was extremely strong. Zhao was reportedly swept out to sea without warning and disappeared from sight within moments. Local coastal guards and maritime rescue teams quickly deployed speedboats, drones, and rescue helicopters to conduct a large-scale search operation,” the post claimed.

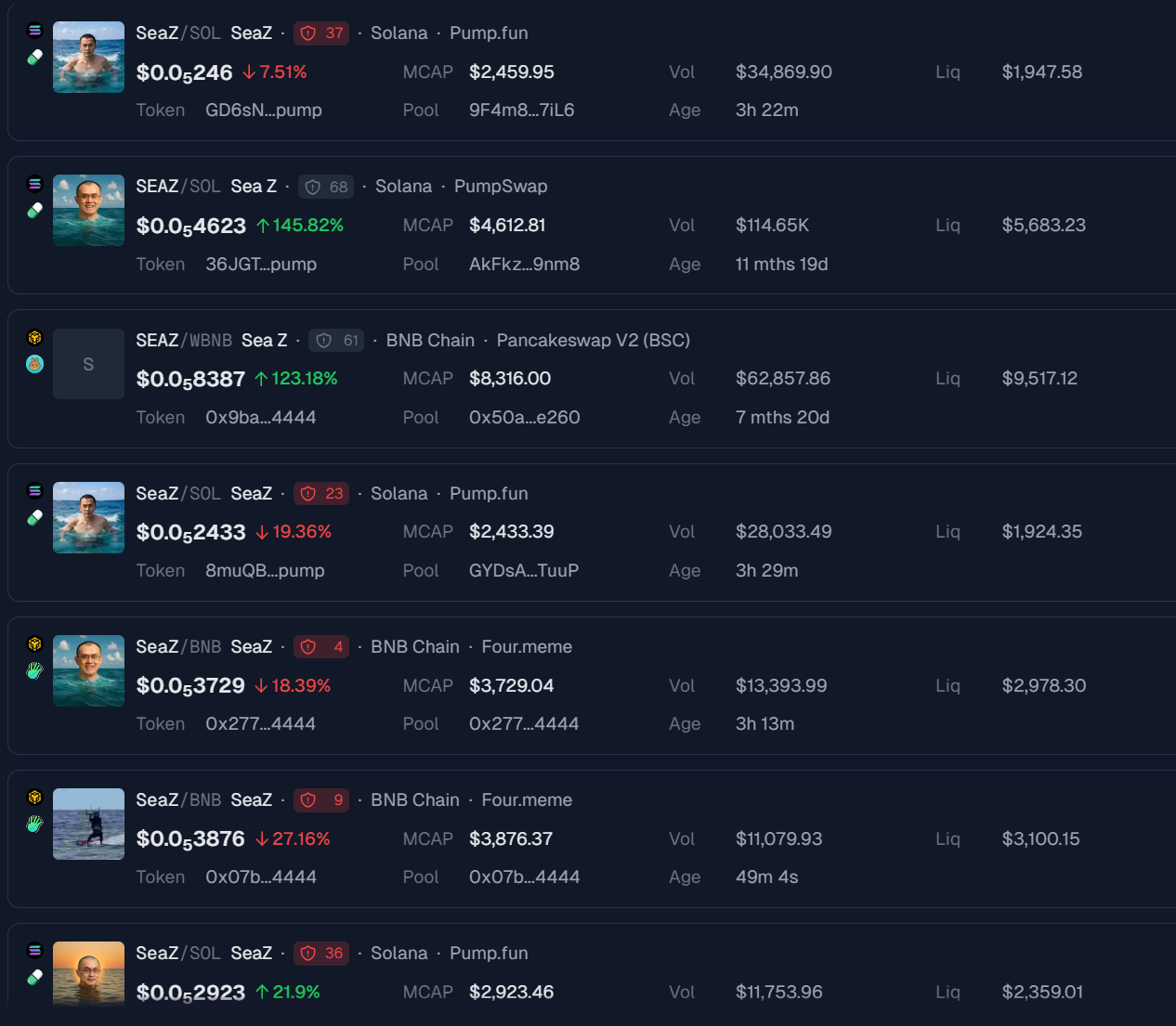

Within hours, traders deployed knockoff tokens on pump.fun and the BNB Chain meme launchpad, most carrying SEAZ and RIPCZ tickers.

GeckoTerminal data shows several SEAZ pools on Solana priced below one-thousandth of a cent. Market caps ranged from roughly $2,400 to $4,600 with liquidity under $6,000.

The BNB Chain version on PancakeSwap V2 traded near $8,300 in market cap on $9,500 of liquidity. One Solana SEAZ pool printed about $114,000 in volume on just $5,683 of liquidity.

Follow us on X to get the latest news as it happens

The setup recalls past Solana meme coin rugs. Most tokens dropped 10% to 40% within hours of launch.

CZ Pushes Back On The Rumor Cycle

CZ addressed the hoax, noting that he kite surfs rather than surfs and invited followers to try Surf Abu Dhabi together.

The Binance founder has criticized meme coin traders before for chasing tokens tied to his name.

“I am not against memes, but meme coins are getting “a little” weird now,” he noted.

The incident mirrors past Binance fake news incidents, including an Interpol red notice rumor that briefly hit BNB.

This pattern also recalls earlier CZ-linked meme frenzy incidents, when traders piled into thin tokens before momentum collapsed.

The post CZ “Surfing Accident” Hoax Sparks Meme Coin Frenzy Across Solana And BNB Chain appeared first on BeInCrypto.

Nakamoto Inc. (NAKA) has defended why a Bitcoin (BTC) treasury company keeps a Chief Medical Officer on payroll. The role went viral as a symbol of what skeptics call Digital Asset Treasury (DAT) excess.

Analysts point to the role alongside NAKA’s 99% share collapse and roughly $200 million debt load. CEO David Bailey responded that the medical position exists for reasons rooted in the company’s reverse merger origin.

Why a Bitcoin Treasury Firm Keeps a Doctor on Staff

NAKA began as KindlyMD, a Utah-based pain management provider. It listed on Nasdaq before merging with Bailey’s private Nakamoto Holdings in 2025.

Tim Pickett, who founded KindlyMD, stayed on as Chief Medical Officer to run the legacy healthcare subsidiary.

“We have a chief medical officer because we merged with a healthcare company and maintaining an operating business is a Nasdaq listing requirement,” explained David Bailey, Nakamoto’s CEO and chairman.

The healthcare arm generates the bulk of Nakamoto’s modest recurring revenue and helps the company avoid shell-company classification.

It is one of several medical firms rebranded into crypto vehicles in 2025.

Follow us on X to get the latest news as it happens

Dilution and Losses Fuel the Backlash

The CMO became a punchline as wider concerns intensified. Analyst Justin Bechler highlighted Nakamoto’s Q1 2026 10-Q, which reported a $238 million net loss.

Operating revenue was $2.3 million while insiders received $7.3 million in compensation.

The company also acquired BTC Inc. and UTXO Management from Bailey and CIO Tyler Evans.

The deal diluted public holders by 58% in one quarter, fueling shareholder dilution concerns across the Bitcoin treasury sector.

Shareholders later authorized a 1-for-40 reverse stock split to restore Nasdaq’s $1 minimum bid compliance. The split took effect May 22, lifting NAKA from around $0.16 to roughly $6.

It also compressed 696 million outstanding shares into 17.4 million.

The first insider lock-up tranche releases August 20, and the Q2 10-Q lands the same month. Both will test whether Bitcoin 2026 conference revenue can justify the goodwill from the BTC Inc. acquisition.

Investors watching ongoing DAT sector losses and Nakamoto’s earlier BTC sale are focused on the operating line.

The 5,058 BTC headline holdings matter less for the next two quarters.

The post A Bitcoin Treasury Company Has a Doctor on Staff, But Why? appeared first on BeInCrypto.

SOL fell 33% in the first quarter of 2026 to close at around $83, but Messari’s Q1 State of Solana report tells a story that’s harder to dismiss than the price chart would suggest.

While dollar-denominated numbers dropped across the board, the network set new records for daily transaction volume, grew its real-world asset market cap to over $2 billion, and barely budged on validator revenue.

Record Activity, Shrinking Prices

The headline figure from the report was the new all-time high for average daily non-vote transactions: 112.6 million, up 50% from the previous quarter and 15% above the previous record set in Q2 2025.

It means that more transactions happened on Solana every day in Q1 than at any point in the network’s history, which clearly sits at odds with the price decline. Meanwhile, Chain GDP, which is Messari’s term for total application revenue, stayed almost flat at $342.2 million, fractionally above Q4 2025’s $341.8 million.

Per the report, Pump.fun is still the largest single revenue source at $124.7 million, an improvement of 17% quarter-over-quarter. In second place was Axiom, a trading app, which recorded a 36% jump, raking in $42.4 million.

However, the most dramatic mover was a launchpad that lets users share trading fees with social media accounts, called Bags. Its revenue went up 1,347% to $11.5 million after meme coins tied to open-source AI projects generated intense trading activity in January.

That momentum didn’t hold, with Bags’ revenue dropping 85% month-over-month into February, making the episode another example of how quickly new activity cycles through Solana’s application layer.

On the other hand, DeFi TVL fell 22% quarter-over-quarter to $6.16 billion, a drop that tracks almost directly with SOL’s price dip rather than with any meaningful outflow of users. Solana’s share of total DeFi TVL moved barely at all, going from 6.9% to 6.7%, while Kamino reclaimed the top protocol spot with $1.72 billion, edging Jupiter at $1.69 billion.

Drift’s performance was affected by a $285 million exploit attributed to a sophisticated social engineering operation linked to North Korean state-affiliated threat actors.

Looking at Real Economic Value, which is basically the fees and MEV tips paid to validators, the report shows it fell just 1% to $89.5 million. That figure placed Solana second among all networks, only behind Hyperliquid’s $156 million.

RWAs Take the Lead

If one story defined Q1 beyond the bear market backdrop, it was real-world assets. On Solana, the market saw its value grow 43% quarter-over-quarter to $2.01 billion.

BlackRock’s BUIDL tokenized money market fund doubled to $525.4 million after Anchorage Digital added custody support, with the latter holding around 81% of the total supply on-network by quarter’s end.

Meanwhile, Ondo Finance launched 200-plus tokenized US stocks and ETFs on Solana, including a same-day tokenization of BitGo stock on the date of the company’s NYSE IPO.

Finally, while the stablecoin market cap on the platform remained at just under $15 billion, the composition changed. USDC fell 21% to $7.83 billion but remains the largest at 53% of the total, while USDT rose 34% to $2.89 billion.

At the same time, World Liberty Financial’s USD1 climbed 473% to $883.5 million, largely on the back of Binance reallocating customer holdings to Solana.

The post Report: Solana Activity Hits Record High Despite SOL’s 33% Q1 Drop appeared first on CryptoPotato.

Inside BRICS’ Secret New Money System

IPL 2026: KL Rahul, Kuldeep Yadav power Delhi Capitals to dominant win over KKR | Cricket News

In a market where Mac has been aspirational, it’s somehow a better deal than windows machines now

-

Crypto World3 days ago

Crypto World3 days agoBlockchain.com files with SEC for U.S. IPO

-

Fashion2 days ago

Fashion2 days agoHoliday Weekend Open Thread – Corporette.com

-

Crypto World3 days ago

Crypto World3 days agoBitcoin Accumulation Weakens as BTC Realized Losses Hit $600M

-

Business2 days ago

Business2 days agoDell Technologies DELL Stock Surges 15% on AI Server Momentum and Analyst Upgrades in 2026

-

Crypto World2 days ago

Crypto World2 days agoSpace X IPO Is ‘Bad News’ for Tech Stocks: But What About Bitcoin?

-

Politics2 days ago

Politics2 days agoMakerfield: a tale of two social-media histories

-

Crypto World3 days ago

Crypto World3 days agoMicroStrategy’s Saylor Says Miners No Longer Set Bitcoin Price, Another Force Has Taken Over

-

Crypto World2 days ago

Crypto World2 days agoRobinhood crypto COO Tanya Denisova exits

-

Business5 hours ago

Business5 hours agoNYT Strands Answers May 24 2026 Revealed for Puzzle No. 812 Theme Summer Essentials

-

Tech3 days ago

Tech3 days agoWhatsApp ads could make Irish debut after discussions with DPC

-

Tech2 days ago

Tech2 days agoA 0.12% parameter add-on gives AI agents the working memory RAG can’t

-

Crypto World2 days ago

Crypto World2 days agoAI infrastructure race heats up as IREN pitches full-stack strategy, WhiteFiber lands $160M deal

-

Business3 days ago

Business3 days agoTrump Invests $1M-$5M in Kura Sushi USA Chain With 27 California Locations

-

Tech3 days ago

Tech3 days agoYou Can Now Add ChatGPT To PowerPoint

-

Crypto World6 days ago

Revolut Launches Dogecoin Debit Card Across UK and EU

-

NewsBeat3 days ago

NewsBeat3 days agoCharity run by Reform leader Malcolm Offord accused of ‘law breaking’ over Scottish registration

-

Sports3 days ago

Sports3 days ago2026 CJ Cup Byron Nelson leaderboard: Brooks Koepka finds putting stroke in Round 1

-

Crypto World3 days ago

Crypto World3 days agoTrump Media’s Bitcoin Stash Shrinks Again as 2,650 BTC Lands on Crypto.com

-

Business3 days ago

Goldman Sachs reinstates Ageas stock coverage with neutral rating

-

Crypto World4 days ago

Crypto World4 days agoExa Labs raises $250 million in funding led by a16z

You must be logged in to post a comment Login