Crypto World

Bitcoin rebounds towards $65K as cooling CPI slashes July Fed hike odds

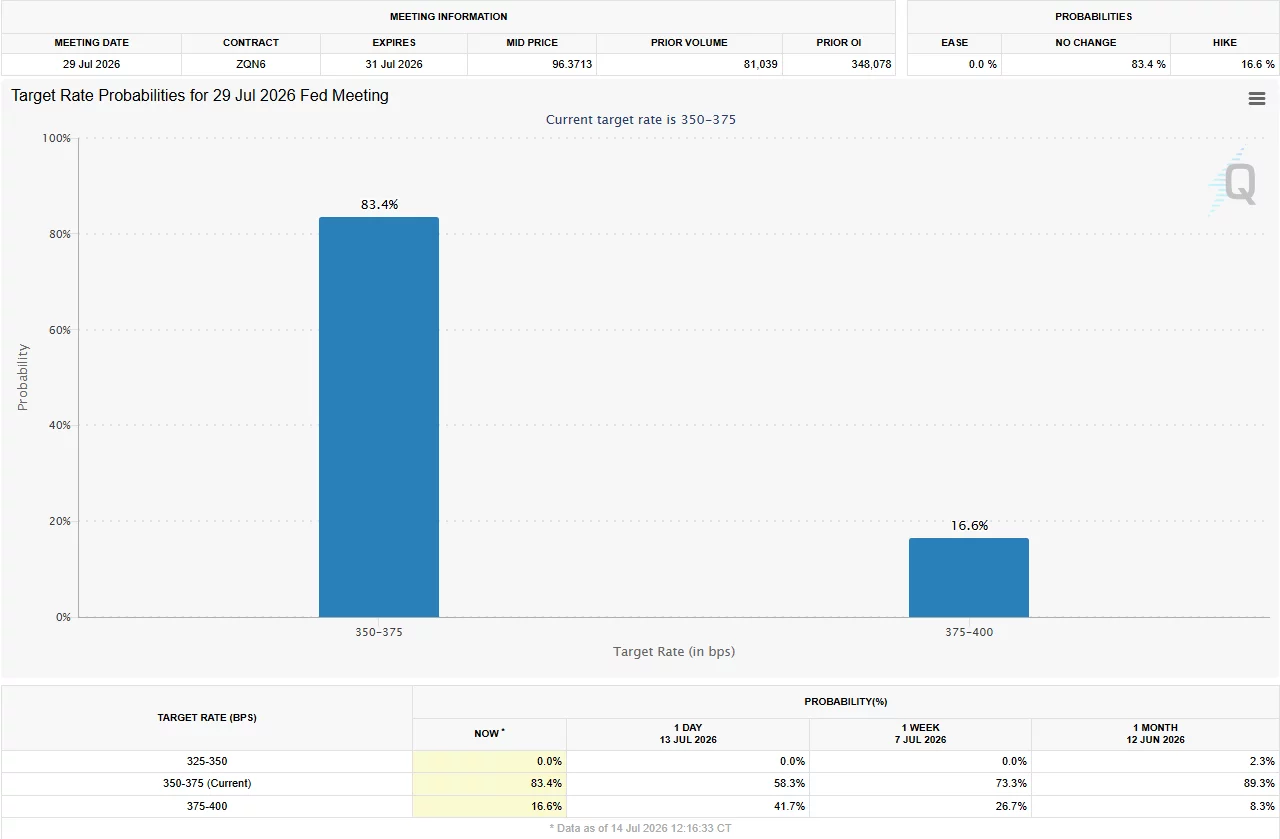

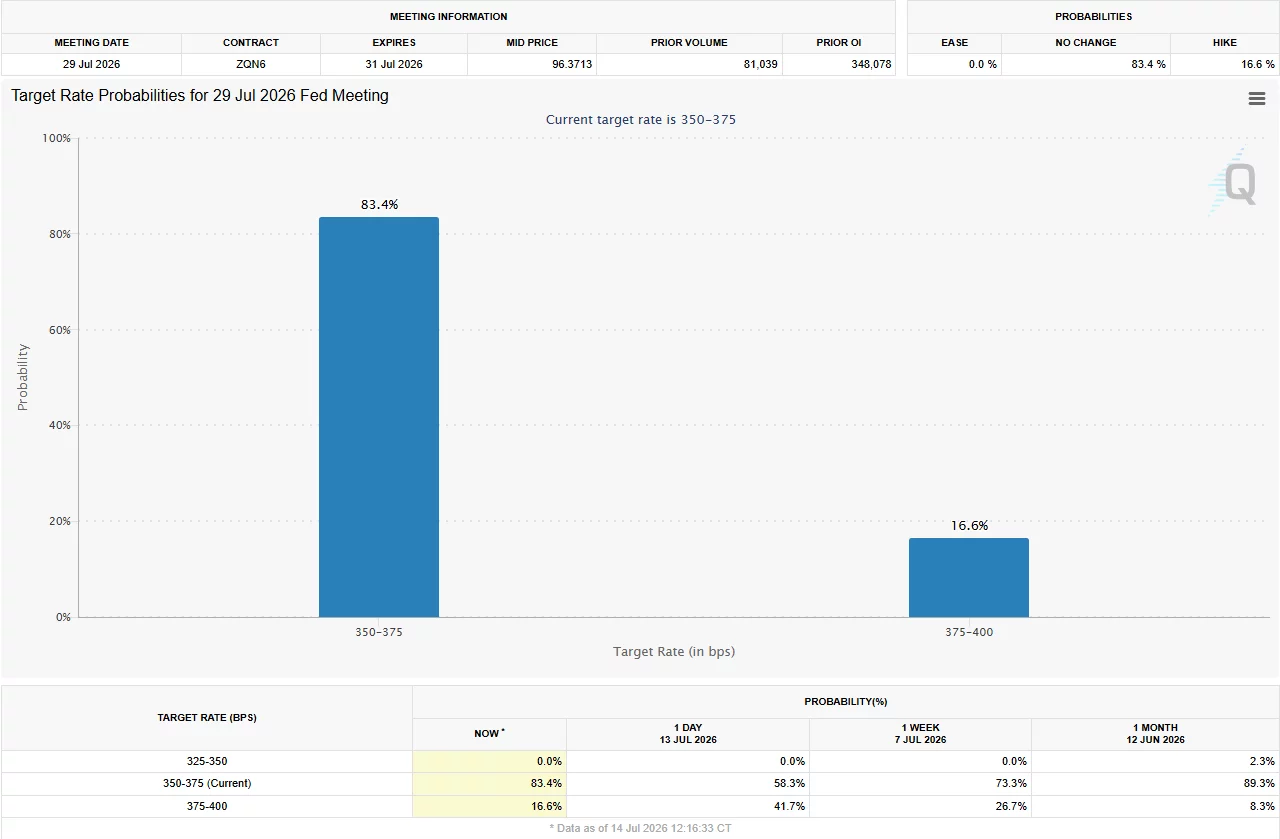

Bitcoin has climbed back toward the $65,000 level after softer-than-expected U.S. inflation data sharply reduced market expectations of a Federal Reserve rate hike at the July policy meeting.

Summary

- Bitcoin climbed toward $65K after June U.S. inflation came in below expectations.

- Cooling CPI data pushed July Fed rate hike odds sharply lower across major markets.

- Investors now await Kevin Warsh’s testimony and PPI data as geopolitical risks persist.

According to the U.S. Bureau of Labor Statistics, the consumer price index (CPI) slowed to 3.5% year over year in June, below the 3.8% economists had expected. Monthly CPI fell 0.4%, compared with forecasts for a 0.1% decline. The inflation report triggered a fresh move higher in risk assets, helping Bitcoin recover from losses linked to renewed geopolitical tensions.

Bitcoin (BTC) rose nearly 5% to an intraday high of $64,830 on July 14 before easing to around $64,560 at press time. The recovery followed a drop below $62,000 during the previous session, when escalating conflict between the United States and Iran weighed on market sentiment.

Core inflation data also came in below forecasts. The Bureau of Labor Statistics reported core CPI at 2.6% year over year and flat on a monthly basis, compared with expectations of 2.8% and 0.2%, respectively.

The latest figures improved from May, when headline CPI stood at 4.2% year over year, and core CPI reached 2.9%, adding to expectations that inflation pressures may be easing despite the ongoing conflict in the Middle East.

Cooling inflation has lowered expectations for a July rate hike

Interest-rate expectations changed quickly after the inflation release. According to CME FedWatch data, traders now assign only a 16.6% probability to a Federal Reserve rate hike at the July Federal Open Market Committee meeting.

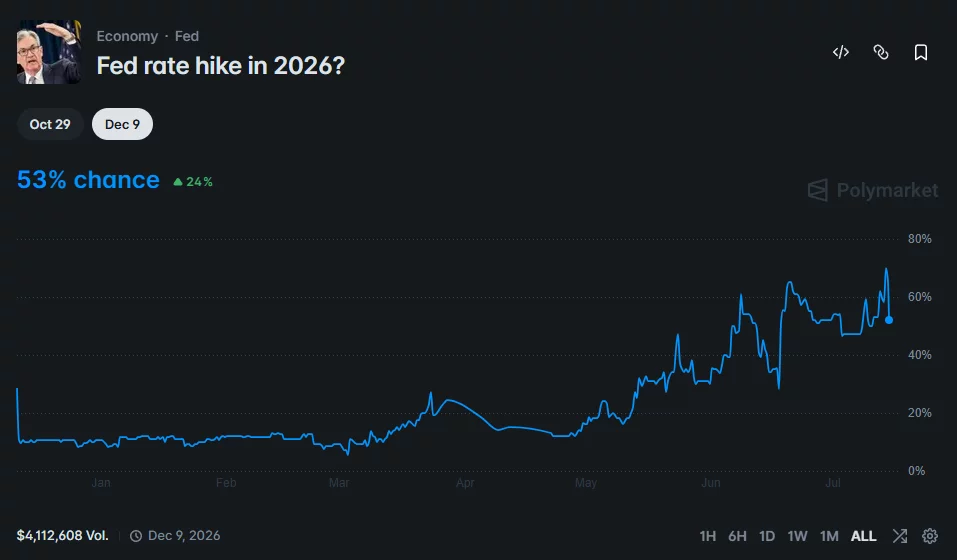

Prediction markets also adjusted their outlook. Data from Polymarket showed the perceived probability of a July rate hike falling to 9%, down from as high as 34% previously. The platform also showed the chance of at least one rate hike during 2026 declining to 53%, compared with a recent peak of 71%.

The inflation report arrived only days after Federal Reserve Governor Chris Waller indicated he could support higher interest rates if inflation remained elevated. Against that backdrop, the weaker-than-expected CPI figures reduced expectations that policymakers would tighten policy this month, providing support for Bitcoin and other risk-sensitive assets.

Attention has now turned to Federal Reserve Chair Kevin Warsh, who is scheduled to testify before Congress over two days. Investors are also preparing for the producer price index (PPI) report, which could influence expectations for future monetary policy and lead to fresh volatility across cryptocurrency markets.

Geopolitical risks continue to limit upside

Even with inflation easing, macro risks remain in focus. Recent weakness in Bitcoin followed renewed fighting involving the United States and Iran, while President Donald Trump’s decision to reinstate the Iranian blockade added pressure to global markets before the CPI-driven rebound.

Another source of uncertainty comes from Trump’s proposal to impose a 20% cargo fee on ships that receive U.S. assistance while transiting the Strait of Hormuz. Market participants have warned that any disruption to shipping through the waterway could tighten global oil supplies and complicate the inflation outlook in the months ahead.

As a result, softer inflation has improved the immediate outlook for cryptocurrencies by reducing expectations of a July rate increase, but upcoming Federal Reserve commentary, fresh inflation data and developments in the Middle East remain key factors that could determine whether Bitcoin can extend its recovery toward the $65,000 level.

MemeCore price has surged more than 20% to an intraday high of $1.46 on July 14, breaking out of a two-week consolidation range after buyers defended support near $1.20.

Summary

- MemeCore surged over 20% to $1.46 after breaking above a two-week consolidation range.

- Bullish MACD momentum and a recovering RSI supported the move, though resistance remains near $1.50.

- Thin liquidity and concentrated token ownership could amplify both further gains and renewed selling.

As per data from crypto.news, MemeCore (M) opened near $1.21 before climbing to $1.468, placing it among the day’s strongest-performing large-cap crypto assets. The move has occurred despite weakness across Bitcoin and Ethereum, indicating that token-specific trading flows, rather than a market-wide rally, are driving the advance.

Buyers appear to have entered after MemeCore spent much of July trading between approximately $1.15 and $1.45. Repeated failures to push the token below the lower end of that range reduced immediate selling pressure, while the latest move through its recent highs likely triggered momentum orders and forced some bearish traders to reduce their exposure.

Alongside the technical breakout, traders have continued to monitor MemeCore’s ecosystem developments, including its Layer-1 blockchain, MemeX launchpad and planned on-chain project releases. Although no specific catalyst has been identified for Tuesday’s rally, continued attention on the project’s roadmap may have supported sentiment

The timing may have renewed attention around M one day before its breakout, although the update did not identify a specific announcement responsible for the rally.

Technical momentum has improved

On the daily chart, MemeCore’s moving average convergence divergence indicator has produced a bullish crossover, while its histogram has moved into positive territory. The pattern indicates that downside momentum from June’s collapse is fading, even though both MACD lines remain below zero and have not confirmed a complete trend reversal.

MemeCore’s relative strength index has risen to approximately 45.5 from deeply oversold levels recorded after the June crash. Because the RSI remains below the neutral reading of 50, the chart points to recovering demand rather than an established bullish trend.

Price structure offers a similar signal. M rebounded from a late-June low near $0.50 and reached approximately $1.80 before pulling back. It then formed a base above $1.10, and the July 14 candle has pushed it back toward the upper edge of that structure.

A daily close above $1.45-$1.50 would strengthen the breakout and leave the $1.70-$1.80 region as the next visible resistance zone on the supplied chart. Failure to hold above $1.45, however, could show that the move was another brief liquidity-driven spike, with support remaining around $1.20 and $1.10.

June’s collapse still clouds the recovery

The rally follows an unusually violent correction that erased more than 70% of MemeCore’s value within hours on June 25. MarketWatch reported that M fell from roughly $2.62 to $0.82, cutting its market capitalization below $1 billion and reducing its fully diluted valuation from about $14 billion to $3.8 billion.

During the sell-off, on-chain investigator ZachXBT renewed allegations that MemeCore’s supply was heavily concentrated among insiders and questioned how the token had passed listing reviews at several major exchanges.

In an earlier post, he had challenged the project to explain its multibillion-dollar valuation and his claim that insiders controlled more than 90% of the supply. MemeCore had not publicly answered requests for comment cited by MarketWatch at the time.

Such concentration concerns help explain both sides of M’s price action. Limited freely traded supply can deepen losses when large holders sell, but shallow order books can also magnify rebounds when demand suddenly increases. Research into meme-token markets has similarly found that concentrated ownership and thin liquidity can make prices unusually sensitive to sentiment and relatively small trading flows.

MemeCore’s breakout therefore signals a meaningful improvement in short-term momentum, but confirmation depends on whether buyers can sustain trading above $1.45 and eventually reclaim $1.80. Until then, the rebound remains exposed to the same liquidity, ownership and transparency risks that intensified June’s crash.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Every few weeks, a token that has done nothing wrong falls ten percent in a day, and the explanation turns out to have been sitting in public view for years. A tranche of supply, promised to early investors back when the project raised money, hit its scheduled release date.

Insiders who bought at a fraction of the market price suddenly held tokens they could sell, and enough of them did. Traders call these events unlocks, and they are among the most predictable forces in crypto markets, which makes it strange how many investors get blindsided by them.

A token unlock is the moment previously locked supply becomes transferable and enters circulation under rules the project set in advance. The rules themselves are called a vesting schedule, and together they answer a question every serious investor should ask before buying any token: who is going to be allowed to sell, how much, and when. This guide explains what unlocks and vesting are, why projects lock tokens in the first place, the difference between cliffs and linear releases, who actually receives unlocked supply and how differently each group behaves, how unlocks move prices, the low float trap that defined the current market cycle, how to read an unlock calendar like a professional, and the honest limits of unlock analysis.

What a token unlock actually is

When a crypto project creates its token, it almost never releases the full supply into the market on day one. Instead, the total supply is divided into allocations: a slice for the founding team, a slice for the venture investors who funded development, a slice for advisors, a slice for the community, a slice for an ecosystem fund or treasury. Most of these allocations start locked, meaning the tokens exist on paper, and often on chain, but cannot be transferred or sold.

An unlock is the scheduled event that releases some of that locked supply. On the appointed date, or continuously according to a formula, tokens move from the locked state to the liquid state, and their owners can finally do what owners do: hold, stake, or sell. Nothing about an unlock is secret. The schedule is typically published in the project’s tokenomics documentation before the token ever trades, and modern vesting is usually enforced by smart contracts that release tokens automatically, with the whole timetable verifiable on chain.

The distinction between vesting and unlocking trips up newcomers. Vesting is the rulebook, the full timetable governing how allocations are earned and released over months or years. An unlock is a single event within that timetable, the moment a specific batch becomes tradable. A project has one vesting schedule and many unlocks. When traders say a token has an unlock next week, they mean one identifiable batch is crossing from locked to liquid, and the size, recipient, and context of that batch are what analysis is about.

Why projects lock tokens at all

Locking is a credibility device. Imagine a project that raised money by selling thirty percent of its supply to venture funds at an early stage price, then listed the token publicly at twenty times that price. If the investors could sell immediately, the rational move would be to dump everything into the listing hype, crush the price, and move on. Everyone who bought at listing would be exit liquidity. Projects that allowed this quickly found that nobody wanted to buy their tokens at all.

Vesting schedules exist to make the promise of long term alignment enforceable. A team whose tokens unlock over four years has four years of reasons to keep building. An investor with a one year cliff cannot flip the token at listing no matter how tempting the price. The lock converts a verbal commitment into a mechanical one, and because the schedule is public, the market can price the commitment instead of guessing at it.

Locking finally serves a signaling function that has nothing to do with mechanics. When a team accepts a four year schedule and investors accept a one year cliff, they are publishing their own confidence interval. Short schedules whisper that insiders want optionality. Long schedules, especially ones the team imposed on itself beyond what any exchange required, tell the market that the people with the most information expect the token to be worth holding. Markets read these signals imperfectly, but they read them.

Locking also manages the physics of supply. A token’s price is set at the margin, by the balance of buying and selling in liquid markets. Releasing supply gradually gives demand time to grow into it. Releasing it all at once is a flood, and floods move prices the way floods move everything else. The entire discipline of tokenomics, the economic design of a token’s supply, distribution, and incentives, treats the release schedule as one of its central levers.

Cliffs, linear vesting, and the shapes of release

Vesting schedules come in a small number of recognizable shapes, and the shape matters as much as the size. A cliff is a period, commonly six to twelve months after the token generation event, during which nothing unlocks at all. When the cliff ends, a large batch releases at once. Cliffs concentrate sell pressure into a single known date, which is why cliff expiries are the unlock events traders circle on calendars.

Linear vesting releases tokens continuously or in small regular steps, daily, weekly, or monthly, over a defined period. The drip is gentler on price because no single day carries a large release, but it creates persistent background pressure, a steady trickle of new supply that demand must absorb month after month.

Most real schedules are hybrids: a cliff followed by linear release. A typical structure for team tokens might be a one year cliff, then monthly unlocks over the following two or three years. Investor allocations often vest faster than team allocations, and community or ecosystem allocations sometimes have no lock at all, or unlock based on milestones instead of dates. Some projects add non linear schedules, with releases that accelerate or step up at intervals, and a few tie unlocks to performance conditions such as product launches. The token generation event, usually shortened to TGE, marks day zero for most schedules, and many tokens release a small percentage at TGE so that a market can exist at all.

Reading a vesting chart is mostly about learning to see these shapes. A wall of supply at a single future date is a cliff. A smooth ramp is linear release. The steeper the ramp and the taller the walls, the more supply the market will be asked to digest, and the more the token’s future depends on demand showing up on schedule.

Who receives unlocked tokens, and why it matters

The same unlock size can produce completely different market outcomes depending on whose tokens are being released, because different holders face different incentives. Venture investors are the most reliable sellers. Funds have limited lifespans and partners to repay, and a position bought at an early stage price that now trades far higher represents a return that fund managers are professionally obligated to realize. When a large investor tranche unlocks, systematic selling is the base case, not the exception.

Team allocations behave less predictably. Founders and employees have reputational reasons to avoid visible dumping, and many hold for belief or for optics, but personal diversification is a powerful force, and team selling after long cliffs is common enough that markets price it in. Ecosystem and treasury unlocks are different again: those tokens usually flow to grants, market making, or incentives instead of directly to exchanges, though grant recipients frequently sell what they receive, so the pressure arrives second hand and on a lag. Advisors sit somewhere in between, small in size but often quick to exit. Community allocations, including airdrops, scatter supply across thousands of small holders whose behavior varies from instant selling to permanent holding.

Sophisticated unlock analysis therefore never stops at the headline number. The question is not how many tokens unlock, but how many unlock into hands that are likely to sell, at what cost basis, and into how much liquidity.

How unlocks actually move prices

The mechanical story is simple: unlocks increase liquid supply, and if demand does not rise to meet it, price falls. But the mechanism deserves one more sentence of precision. Price is set by transactions, not by existence, so an unlock only moves the market to the degree that unlocked tokens are sold or that traders act on the expectation of selling. Supply that unlocks into wallets and stays there changes the risk picture without changing the order book. The market story is more interesting, because unlocks are public information, and public information gets traded in advance.

Ahead of a large unlock, traders who expect selling pressure sell first, or open short positions in perpetual futures to profit from the anticipated decline. This front running spreads the price impact across the weeks before the event, and it occasionally produces the counterintuitive pattern traders call sell the rumor, buy the news, where a token falls into an unlock and bounces after it, because the sellers finished selling early. Empirically, the price damage from major unlocks tends to arrive before and during the event, with the days after determined by how much of the released supply actually hits exchanges.

Context decides magnitude. The ratio of the unlock to average daily trading volume matters more than the ratio to market capitalization, because volume measures the market’s absorption capacity. An unlock worth three days of trading volume is a problem; an unlock worth an hour of volume is noise. Market regime matters just as much. Bull markets swallow unlocks that would crater the same token in a bear market, because absorption is a function of demand, and demand is cyclical. And holder cost basis sets the temptation: supply unlocking at a hundred times its purchase price wants to sell far more than supply unlocking underwater.

The clearest evidence that unlocks bind projects came during the 2024 and 2025 cycle, when several teams paused or restructured their own vesting schedules mid stream after watching unlock pressure grind their tokens down. A project that has to renegotiate its own tokenomics to defend its price is admitting that the original schedule asked the market to absorb more than it could.

From ICO free for all to institutional vesting

Vesting was not always standard. During the initial coin offering boom of 2017 and 2018, projects routinely sold tokens with no lockups at all: a whitepaper, a wallet address, and a promise. Teams and early buyers could sell the moment tokens listed, and many did, with predictable results. The wreckage of that era, thousands of tokens that listed, dumped, and died, is the reason vesting became a market requirement instead of a courtesy. Exchanges began expecting lockup disclosures before listing. Venture funds began accepting, and then demanding, multi year schedules as evidence of seriousness. By the early 2020s a token launching without published vesting for insiders read as a warning label.

The professionalization cut both ways. Structured vesting made token launches more credible, but it also standardized the low float playbook, in which a polished schedule defers the supply problem instead of solving it. A four year lockup does not remove twenty five times the float from the future; it just puts the future on a calendar. The modern unlock calendar industry, with dashboards, alerts, and analytics products tracking every scheduled release across the market, exists precisely because vesting became universal. What was once a question of whether insiders were locked at all became a question of exactly when the locks expire, and an entire analytical discipline grew in the gap.

The next stage of that evolution is already visible: on chain vesting contracts that anyone can audit, third party verification services, and standardized disclosure formats. The direction of travel is toward supply schedules as verifiable public infrastructure, which raises the analytical bar. When everyone can see the calendar, seeing it is no longer an edge. Interpreting it is.

The low float, high FDV trap

The defining supply structure of the recent cycle was the low float, high FDV launch. A project lists with a small fraction of total supply circulating, sometimes under ten percent, while the fully diluted valuation, the price of all tokens that will ever exist, implies a number many multiples higher. The small float makes the price easy to support at listing. The enormous locked overhang means years of scheduled unlocks stand between the listing price and the day the token’s market cap honestly reflects its supply.

The arithmetic is unforgiving. If a token trades at a two billion dollar fully diluted valuation with eight percent circulating, then over the coming years roughly twenty five times the current float will be released. For the price simply to stay flat, new demand must absorb all of it. Buyers of such tokens are, whether they realize it or not, betting that demand will grow faster than a supply schedule designed years earlier by people who bought at a fraction of the current price. The bet occasionally pays. The base rate does not favor it.

Markets learned this lesson expensively. Token after token from the low float era spent months in structural decline as unlocks arrived on schedule and demand did not, and by the middle of the cycle, unlock calendars had become one of the most watched datasets in DeFi and beyond. Aggregate unlock volume across the market now runs into billions of dollars in heavy months, and traders treat clusters of large unlocks as a marketwide supply headwind, particularly for assets far down the liquidity curve.

What big unlocks look like in practice

A few well known episodes show the full range of outcomes. Arbitrum’s ARB, one of the largest airdropped tokens of its generation, spent much of its first two years grinding lower as investor and team tranches unlocked month after month into demand that never matched the schedule, becoming the reference example of structural unlock pressure on a fundamentally serious project. The token’s technology kept shipping; the supply kept arriving; the price reflected the arithmetic.

AltLayer provided the reference example of a project blinking. After its first major unlock in mid 2024 hit the price hard, the team announced a six month vesting pause covering investors, team, advisors, and treasury. The pause relieved the calendar but not the market, and the token’s struggles afterward became a case study in why rescheduling supply does not manufacture demand.

Pump.fun’s PUMP token compressed the entire lifecycle into months. The July 2025 sale raised over a billion dollars at a valuation the open market immediately began stress testing, and every subsequent tranche movement from team and treasury wallets was tracked by thousands of traders in real time, a reminder that for high profile tokens, unlock analysis now happens wallet by wallet, not just date by date.

And Pi Network became the retail era’s unlock story: roughly 1.21 billion tokens scheduled to release across 2026 against thin exchange liquidity, an overhang so large relative to volume that the unlock calendar itself became the primary narrative around the asset. Whatever one thinks of the project, the episode taught millions of retail holders the vocabulary of cliffs, floats, and absorption for the first time.

The pattern across all four is consistent. Unlocks did not decide whether these projects mattered. They decided when the market was forced to render a verdict on how much demand actually existed at the prevailing price.

Reading an unlock calendar like a professional

Several platforms track unlock schedules across the market, including Tokenomist, CryptoRank, DropsTab, and CoinGecko, and they present broadly the same data: upcoming unlock dates, sizes in tokens and dollars, percentages of circulating supply, and the allocation buckets involved. The skill is in the interpretation, and it reduces to five questions.

First, how large is the unlock relative to circulating supply? Below one percent is usually noise; above five percent deserves attention. Second, how large is it relative to daily trading volume? This is the absorption test, and it is the single most predictive ratio. A useful rule of thumb: if the unlocked value exceeds three to five days of average volume, absorption will be slow and the price will likely do the absorbing. Third, who receives the tokens? Investor and team tranches carry the highest sell risk; ecosystem and treasury tranches are slower burning. Fourth, what is the recipients’ cost basis? Deeply profitable supply sells harder. Fifth, what happened at this token’s previous unlocks? Past behavior around identical events is the closest thing unlock analysis has to a controlled experiment.

Two practical refinements separate careful traders from calendar tourists. Cliff events deserve more respect than equivalent linear amounts, because concentration in time is what overwhelms order books. And exchange flow data, where available, tells you whether unlocked tokens are actually moving toward venues where they can be sold, or sitting in the same wallets that received them. Tokens that unlock and do not move are potential supply; tokens that unlock and flow to exchanges are incoming supply. On chain analytics platforms make this distinction observable in near real time, and the gap between the two is often where the actual trade lives.

What unlock analysis cannot tell you

Unlock data describes supply mechanics, and supply is only half of any price. A token with a brutal unlock schedule and explosive demand growth can rise through every release date, which is exactly what the strongest projects of every cycle have done. A token with a clean, fully vested supply and no demand will still go to zero, just without a schedule announcing it. Unlocks set the height of the wall; they say nothing about whether the buyers on the other side can climb it.

The data also cannot capture private arrangements. Locked tokens are routinely hedged through over the counter deals and derivatives, meaning the economic selling may have happened long before the unlock date, with the on chain release a mere formality. Conversely, some unlocked supply is contractually committed to market makers or custody and cannot hit the market as fast as the calendar implies. On chain vesting contracts have also occasionally diverged from published schedules, in both directions, which is why serious analysts verify the contract instead of trusting the documentation.

Treat unlocks the way professionals treat them: as one high quality, freely available input among several. In a market where edges are scarce and expensive, a public calendar of exactly when supply arrives, from Solana majors to the long tail of meme coins, is a gift. It is not a trading system. It is a schedule of when the questions get asked; demand still writes the answers.

Frequently asked questions

What is a token unlock in crypto?

A token unlock is a scheduled event in which previously locked tokens become transferable and enter circulating supply. Unlocks follow a vesting schedule the project defined in advance, and they typically release tokens to teams, early investors, advisors, or ecosystem funds.

What is the difference between vesting and unlocking?

Vesting is the overall timetable that governs how locked allocations are released over time. An unlock is a single event within that timetable. A project has one vesting schedule but many individual unlock events.

What is a cliff in a vesting schedule?

A cliff is an initial period, often six to twelve months, during which no tokens from an allocation are released. When the cliff ends, a large batch unlocks at once, which concentrates potential sell pressure into a single date.

Are token unlocks always bearish?

No. Unlocks add supply, but the price outcome depends on demand, on how much of the released supply actually gets sold, and on how much was priced in beforehand. Some tokens fall into an unlock and recover afterward once the anticipated selling clears.

How do I check when a token unlocks?

Unlock schedules appear in project tokenomics documentation and on tracking platforms such as Tokenomist, CryptoRank, DropsTab, and CoinGecko. These tools show upcoming dates, sizes, percentages of supply, and which allocation groups receive the tokens.

What is a low float, high FDV token?

It is a token that lists with a small share of total supply circulating while its fully diluted valuation implies a much larger market value. The structure supports the listing price but leaves years of scheduled unlocks that future demand must absorb.

Why do venture capital unlocks cause more selling?

Venture funds have finite lifespans and obligations to return capital to their partners, and their tokens were typically bought at prices far below market. Realizing those gains when tokens unlock is standard practice, so investor tranches carry the highest sell risk.

Can a project change its vesting schedule?

Sometimes, if governance or the token contract allows it. Several projects have paused or extended vesting to relieve price pressure. Any change should be publicly disclosed, and unexplained deviations between the published schedule and on chain behavior are a warning sign.

This article is for educational purposes only and does not constitute financial or investment advice. Vesting structures and unlock data vary by project and change over time. Details are accurate as of July 14, 2026.

The most important legal test in crypto was written in 1946 to settle a dispute about orange groves. That single sentence explains most of the past decade of American crypto regulation: the confusion, the lawsuits, the exodus of projects to friendlier jurisdictions, and the legislative fight now playing out in the United States Senate.

\Every argument about whether a token is a security eventually arrives at the same four questions, and those questions come from a Supreme Court case decided before the transistor was invented.

The Howey test is the legal standard American courts and regulators use to decide whether an arrangement counts as an investment contract, one of the categories of security defined in federal law. If a crypto token sale meets the test, the full weight of securities regulation applies: registration, disclosure, liability, and the jurisdiction of the Securities and Exchange Commission. If it does not, the token falls outside the SEC’s core authority and, increasingly, into the hands of the Commodity Futures Trading Commission. Billions of dollars, entire business models, and the architecture of pending legislation turn on which side of the line an asset lands.

This guide explains where the test came from, what its four prongs actually require, how the SEC applied it to crypto through a decade of enforcement, what the landmark cases decided and left undecided, how the March 2026 joint SEC and CFTC interpretation reshaped the analysis, and how the CLARITY Act now moving through Congress would change the rules again.

The orange groves that defined a security

In the 1940s, the W. J. Howey Company owned large citrus groves in Florida. To raise money, it sold small tracts of the groves to visitors, mostly tourists with no farming experience, and offered each buyer a service contract under which Howey’s own company would cultivate the land, harvest the oranges, pool the fruit, and remit a share of the profits. Buyers owned land on paper, but in substance they were handing money to a business and waiting for returns.

The Securities and Exchange Commission sued, arguing that these land sales were unregistered securities. The case, SEC v. W. J. Howey Co., reached the Supreme Court in 1946, and the Court agreed with the regulator. It held that an investment contract exists when there is an investment of money in a common enterprise with an expectation of profits derived from the efforts of others. The Court stressed that substance beats form: it does not matter what a scheme is called, what asset is nominally being sold, or how the paperwork is dressed. If the economic reality matches the definition, it is a security.

That flexibility was the point. Congress wrote the securities laws of 1933 and 1934 broadly, after a crash fueled by opaque investment schemes, and the Howey test gave courts a tool that could reach any new packaging of the same old arrangement: money in, promises made, profits expected from someone else’s work. Eighty years later, that packaging includes tokens, and the same interpretive flexibility that let the test reach franchise schemes, whiskey warehouse receipts, and payphone leaseback programs across the twentieth century is what let regulators reach token sales in the twenty first.

The four prongs, one at a time

The test has four elements, and all four must be satisfied. The first is an investment of money. Courts read this liberally: cash qualifies, but so do other crypto assets, property, services, or anything else of value given up in exchange. Buying a token with ether is an investment of money. Even effort, in some framings, can qualify, which is why free distributions raise their own questions, discussed below.

The second prong is a common enterprise. The investor’s money must be pooled with others, or the investor’s fortunes must be tied to those of the promoter, such that everyone rises and falls together. Courts have developed competing doctrines here, horizontal commonality focusing on pooled funds and shared outcomes, vertical commonality focusing on the link between investor and promoter, and the disagreement matters in crypto cases because token buyers do not always have any formal relationship with each other or with the issuer.

The prongs interact, which is why the test resists mechanical application. A strong showing on reliance can compensate for a fuzzy common enterprise; a purely consumptive purchase can defeat the whole analysis even where a promoter exists. Courts weigh the total mix of facts, and small factual differences flip outcomes, which is exactly what makes the test flexible for regulators and maddening for anyone trying to comply in advance.

The third prong is an expectation of profits. The buyer must be motivated primarily by the prospect of financial return, capital appreciation, dividends, yield, instead of by consumption or use. Someone who buys a token to pay for computation on a network looks like a customer; someone who buys the same token because they expect the price to rise looks like an investor. The same asset can be both things to different buyers, which is one of the deep awkwardnesses of applying Howey to tokens.

The fourth prong is that profits must come from the efforts of others. If returns depend predominantly on the managerial or entrepreneurial work of a promoter, a founding team, a company, the arrangement points toward a security. If value arises from broad market forces or the holder’s own activity, it points away. This prong carries most of the weight in crypto disputes: the more a token’s value story depends on a specific team shipping a roadmap, the more it resembles the orange grove.

Why crypto and Howey collided

For its first decade, crypto mostly sold itself as something new, and the law mostly did not care. That ended with the initial coin offering boom of 2017, when thousands of projects raised money by selling tokens to the public on the strength of whitepapers and roadmaps. Functionally, many of these sales were indistinguishable from Howey’s service contracts: money in, a team promising to build, buyers expecting the token to appreciate through that team’s efforts.

The SEC responded first with the DAO Report of 2017, concluding that tokens sold by a decentralized fundraising vehicle were securities, then with a 2019 staff framework listing dozens of factors relevant to applying Howey to digital assets, and then with years of enforcement. The commission’s central position hardened into a slogan associated with its then chairman: nearly every token except Bitcoin looked to the agency like a security, because nearly every token had a team whose efforts buyers relied on. The industry’s counterargument was equally simple: a token is just an asset, like a commodity or a collectible, and an asset is not a contract. The sale of a token might create an investment contract in some circumstances, but the token itself, trading hands years later between strangers on an exchange, carries no promises with it.

Courts spent years sorting between these views, one enforcement action at a time, in what the industry came to call regulation by enforcement. The commission brought actions against issuers over unregistered sales, against exchanges over listing alleged securities, against staking services over yield programs, and against promoters over undisclosed paid touting, naming along the way dozens of specific tokens it considered securities in complaint after complaint. The pattern imposed enormous costs: projects could not know their legal status without being sued, exchanges could not know which listings were lawful, and the question of who regulates crypto, the SEC or the CFTC, stayed unresolved because the answer depended on an asset by asset legal test from 1946.

The cases that drew the map

A handful of decisions define the current terrain. The fundraising cases came first and went badly for issuers. Telegram raised 1.7 billion dollars selling contracts for future tokens and was enjoined in 2020; Kik lost on summary judgment the same year over its token sale; LBRY lost in 2022 despite arguing its token had genuine utility. Together they settled the easy half of the question: selling tokens to fund development, with buyers expecting profit from that development, satisfies Howey.

The hard half arrived with the Ripple litigation. In 2023, a federal judge split the difference in a way that reorganized the entire debate: Ripple’s direct sales of XRP to institutional buyers were securities transactions, because those buyers knew they were funding Ripple’s efforts, but programmatic sales on exchanges to anonymous buyers were not, because a purchaser on an exchange has no idea whether their money goes to Ripple at all and relies on no specific promises. The decision was contested and other judges pushed back on parts of its reasoning, but the core distinction, between a primary sale that creates an investment contract and a secondary trade in the bare asset, became the intellectual center of the reform argument. The token is not the security; the transaction might be. Readers following the XRP saga watched this distinction move billions of dollars in market value in a single afternoon.

The later enforcement wave against exchanges, targeting the listing of dozens of alleged securities, raised the stakes further, because it put the secondary market question directly in play. If tokens themselves were securities, most of the American crypto market was operating illegally. If only certain sales were, most of it was fine. That was the unstable equilibrium the current reform era inherited. Notably, the courtroom record itself stayed mixed: judges in different districts reached different conclusions about secondary sales, some rejecting the Ripple court’s programmatic sales reasoning outright, which guaranteed that without either a definitive appellate ruling or a statute, the question would stay open indefinitely. Uncertainty, not hostility, became the binding constraint on the American market.

The March 2026 interpretation: Howey, narrowed

On March 17, 2026, the SEC issued a formal interpretation of how Howey applies to crypto assets, with the CFTC issuing companion guidance the same day, and it marked the most significant regulatory repositioning since the enforcement era began. The interpretation runs in the industry’s direction on almost every contested point, and although it is not legislation and not binding rulemaking, a Commission level interpretation carries real weight with courts and total weight with the agency’s own staff.

Three moves matter most. First, the interpretation centers the analysis on the issuer’s own representations and promises. A buyer’s expectation of profit counts only if it rests on what the issuer said and did, not on hype from third parties, influencers, or the market at large. Second, it reaffirms that a common enterprise is a genuine, independent requirement, narrowing a prong the agency had previously treated as nearly automatic, and making it harder for secondary market transactions between strangers to satisfy the test. Third, and most consequentially, it describes a pathway for separation: a token born inside an investment contract can shed that status once the issuer’s original promises have been fulfilled or abandoned and no reasonable buyer still relies on them. The asset and the contract can come apart over time, which is exactly what the industry had argued since the Ripple decision.

The interpretation also addressed activities. Protocol mining, protocol staking without discretionary management or guaranteed returns, wrapping of assets, and airdrops generally do not involve the offer or sale of securities when conducted as described. Alongside the interpretation, the agencies jointly classified a first group of sixteen assets, including Bitcoin, Ethereum, and XRP, as digital commodities falling under CFTC jurisdiction. The classification was a watershed and also a warning: what an interpretation gives, a future commission can take back. Only statute is permanent, which is why the legislative fight matters more than any agency document.

What Howey does not cover

Understanding the test also means understanding its limits, because three misconceptions do most of the damage in public debate. The first is that Howey is the whole definition of a security. It is not. Federal law lists dozens of instruments that are securities on their face, stocks, bonds, notes, options, and the investment contract category that Howey defines is the catch all at the end of the list. Tokenized stocks are securities because they are stocks, no Howey analysis required. The test matters for crypto because most tokens resemble nothing on the enumerated list, so everything turns on the catch all.

The second misconception is that failing the Howey test makes an asset unregulated. A digital commodity escapes SEC registration requirements, but it lands in CFTC territory, where fraud and manipulation rules still apply, and it remains subject to tax law, sanctions law, and money transmission rules regardless. The Howey question decides which regulator and which rulebook, not whether rules exist.

The third is that passing or failing is permanent. Because the analysis attaches to transactions, an asset’s status can change as facts change. A network that decentralizes can grow out of its investment contract origins, which the 2026 interpretation now recognizes explicitly, and a dormant project that resumes making promises can walk back into securities territory. Lawyers describe tokens as existing on a spectrum with a direction of travel, not in fixed categories.

One more boundary matters in practice: the test only reaches offers and sales. Simply holding a token, building software, or validating a network is not a securities transaction. This is why so much legal engineering in crypto concentrates on the moment of distribution, the single point where the securities laws attach or do not.

The CLARITY Act: replacing the test with a statute

The Digital Asset Market Clarity Act is Congress’s attempt to answer by statute the question Howey answers by litigation. The bill passed the House in July 2025 by a bipartisan 294 to 134 vote and cleared the Senate Banking Committee in May 2026, and as of mid July 2026 it awaits a Senate floor vote that must clear a sixty vote threshold. Its core mechanism is a formal division of the asset universe: digital commodities, defined largely by reference to decentralization and function, fall to the CFTC, while tokens sold as part of capital raising remain with the SEC, with defined pathways for assets to migrate from one category to the other as networks mature.

In effect, the bill writes the Ripple distinction and the 2026 interpretation into law: primary fundraising is securities territory, sufficiently decentralized assets trading in secondary markets are commodities territory, and the boundary is defined by criteria a project can evaluate in advance instead of a four part test applied after the fact by a court. Supporters call this the end of regulation by enforcement. Opponents, including state securities regulators, argue it weakens investor protection by letting issuers structure their way out of disclosure obligations. Prediction markets currently price passage this session as roughly a coin flip, and the market’s live odds, which fell sharply through early July as the Senate calendar tightened, have become the industry’s real time barometer of whether the Howey era is actually ending, a story crypto.news has tracked closely in its coverage of the CLARITY Act’s odds and what they mean for major assets.

Until a statute passes, Howey remains the operative standard. Committee votes do not reclassify tokens, and interpretations do not bind future commissions. The 1946 test is still the law of the land, which is precisely why it is still worth understanding.

Why free tokens still raise Howey questions

Airdrops look like the easy case, no money changes hands, so the first prong fails, but the analysis proved more tangled than that. The SEC argued in several matters that free distributions can still involve an investment of value, because recipients often provide something, promotional activity, network usage, personal data, or because the issuer benefits by creating a trading market for the remainder of its supply. Courts entertained versions of this theory as far back as internet stock giveaways in the 1990s, and the uncertainty was severe enough that some projects excluded American users from airdrops entirely for years, a self imposed geofence that became a running symbol of the enforcement era.

The 2026 interpretation defused most of this. Airdrops conducted as genuine distributions, without payment and without the issuer soliciting value in return, generally do not involve the offer or sale of securities under the interpretation, and the same logic extends to network rewards from protocol mining and staking. The reasoning follows the interpretation’s core move: securities law attaches to the issuer’s representations and the exchange of value, and a distribution lacking both sits outside the perimeter.

The practical consequence arrived quickly. Projects that had walled off American users began including them again, and airdrop design shifted from legal risk management back toward marketing mechanics. The episode stands as a compact illustration of how much economic behavior a single legal test can shape: for half a decade, the geography of free token distribution on the internet was drawn by a 1946 precedent about oranges.

How to think about any token under Howey

For a practical read on any asset, walk the prongs in order and be honest about the facts. Was there a sale in which buyers handed over value? Almost always yes. Were funds pooled toward a shared venture whose success buyers share? Usually yes for fundraising sales, murkier for secondary trades. Did buyers primarily expect profit? Marketing tells you: materials emphasizing price potential, scarcity, and listings point one way, materials emphasizing use point the other. And do those profits depend on a specific team’s ongoing efforts? This is where decentralization matters legally, not aesthetically: a network that would keep functioning and accruing value if its founding team vanished makes a weak Howey case, and a token whose entire value story is a company’s roadmap makes a strong one.

Two cautions complete the picture. First, labels are irrelevant. Calling something a utility token, a governance token, or a meme changes nothing; courts look at economic reality, and the regulatory history is littered with projects that discovered this in court. Second, the analysis is transaction by transaction, not asset by asset. The same token can be sold as a security in a fundraising round, trade as a non security on an exchange years later, and be offered as a security again if the issuer restarts making promises. The question is never what is this token. The question is always what was this transaction, and that is the insight the orange groves have been teaching for eighty years.

Frequently asked questions

What is the Howey test in simple terms?

It is the four part legal standard American courts use to decide whether an arrangement is an investment contract, and therefore a security. The four elements are an investment of money, in a common enterprise, with an expectation of profits, derived from the efforts of others. All four must be met.

Where does the name Howey come from?

From SEC v. W. J. Howey Co., a 1946 Supreme Court case about a Florida company that sold citrus grove plots along with service contracts to manage them. The Court ruled the packages were investment contracts, creating the test that still applies today.

Is Bitcoin a security under the Howey test?

No. Regulators have consistently treated Bitcoin as a commodity, because there is no central issuer or promoter whose efforts drive returns. The March 2026 joint SEC and CFTC action formally listed Bitcoin among the first group of digital commodities.

Why did the SEC treat most other tokens as securities?

Because most tokens were originally sold by identifiable teams to raise money, with buyers expecting the token to appreciate through those teams’ work, a fact pattern that maps closely onto the Howey prongs. That view drove years of enforcement actions against issuers and exchanges.

What did the Ripple ruling actually decide?

A federal court held in 2023 that Ripple’s direct institutional sales of XRP were securities transactions while its anonymous exchange based sales were not. The decision popularized the distinction between a token sale that creates an investment contract and the token itself trading later.

What changed in March 2026?

The SEC issued a formal interpretation narrowing how Howey applies to crypto: profit expectations must rest on the issuer’s own representations, common enterprise is a real requirement, and tokens can separate from their original investment contracts over time. Mining, staking, wrapping, and airdrops conducted as described generally fall outside securities offerings.

Would the CLARITY Act replace the Howey test?

For crypto assets, largely yes. The bill creates statutory categories, digital commodities under CFTC oversight and capital raising tokens under SEC oversight, with defined criteria replacing case by case Howey analysis. Until it becomes law, Howey remains the operative standard.

Does the Howey test apply outside the United States?

No. It is a doctrine of American federal law. Other jurisdictions use their own frameworks, such as the European Union’s MiCA regulation, though the underlying question of whether a token functions as an investment product appears in some form almost everywhere.

This article is for educational purposes only and does not constitute legal or investment advice. Securities law is fact specific, and regulatory positions change. Details are accurate as of July 14, 2026.

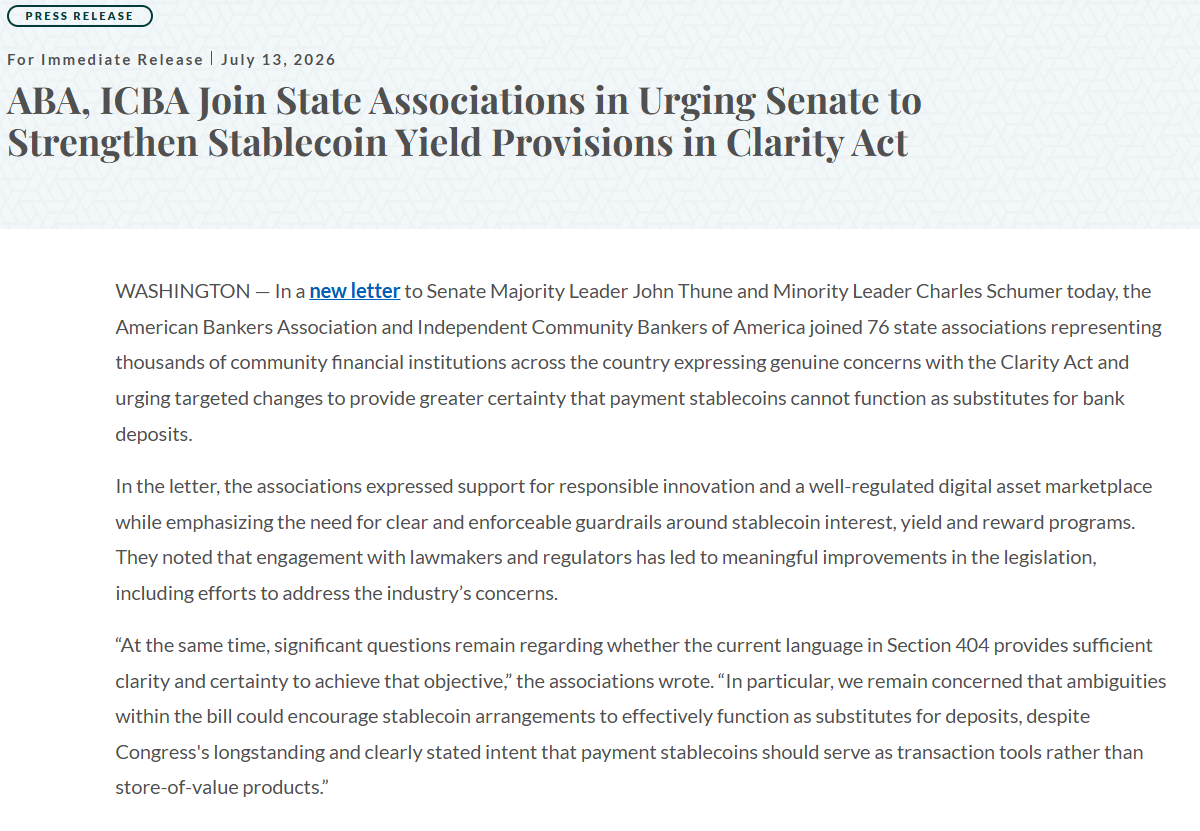

A wide swath of the US banking industry is urging Senate leaders to amend the stablecoin yield provisions of the Digital Asset Market Clarity Act (CLARITY) now under consideration.

The American Bankers Association (ABA), the Independent Community Bankers of America (ICBA) and 76 other state banking associations sent a joint letter to Senate leaders that claimed that the current language on stablecoin interest, yield and rewards is too ambiguous and argued that new amendments need to prevent payment stablecoins from acting as deposit substitutes rather than pure transaction tools.

The joint letter, which showed support for the broader bill, said the ABA is concerned that ambiguities within the bill “could encourage stablecoin arrangements to effectively function as substitutes for deposits, despite Congress’ longstanding and clearly stated intent that payment stablecoins should serve as transaction tools rather than store-of-value products,” according to a press release published on Monday.

This marks the latest pushback from the US banking industry against the act’s stablecoin yield provisions and comes just days ahead of the bill’s scheduled House of Representatives hearing on Friday. The bill aims to establish the first regulatory framework for digital assets in the US.

The banking groups said that the current draft poses the risk of a “deposit flight,” urging lawmakers to revise section 404 to “clarify the prohibition on interest and yield and help ensure that the prohibition cannot be circumvented through alternative incentive structures.”

The pushback reinforces Galaxy Digital’s prediction that the Senate is running out of time to pass the bill before the end of the year, due to a looming Senate recess and other congressional priorities. Galaxy Digital cut its odds of the CLARITY Act becoming law in 2026 to 50% on June 26, citing the lack of a unified Senate Banking-Agriculture text, no firm floor schedule and a narrowing legislative window before lawmakers leave Washington.

ABA, ICBA join state associations in urging Senate to strengthen stablecoin yield provisions in Clarity Act. Source: ABA.com

Bankers, Dems push back against stablecoin yield elements

The CLARITY Act cleared the Senate Banking Committee in May, but met pushback from Democrats and the banking industry, who argued that it would allow crypto firms to offer yields on stablecoins without facing the same requirements as traditional banks.

In a May interview, JPMorgan CEO Jamie Dimon said that the banking industry would continue to “fight” against the current version of the CLARITY Act and said that crypto companies wanting to pay yield on stablecoins should apply for banking charters.

Related: A16z’s Andreessen lands Federal Reserve role as AI reshapes policy debate

Meanwhile, the CLARITY Act secured its second public endorsement from a major US law enforcement organization on Friday, when the Federal Law Enforcement Officers Association (FLEOA) said it submitted a letter to the US Senate Banking Committee endorsing the CLARITY Act, while calling for strengthening accountability in decentralized finance (DeFi) and for preserving the investigators’ existing powers.

At the beginning of June, more than 200 crypto companies and related organizations urged the US Senate to pass the CLARITY Act in a letter shared by crypto lobby group Stand With Crypto.

Magazine: From Bitcoin critics to blockchain believers: The 5 biggest crypto backflips

Bitmine Immersion Technologies says its Ethereum staking operation is now the dominant driver of its business, with $45.7 million in revenue generated from Ether staking and validation in the most recent quarter. The figure underscores how the company’s earlier focus has shifted toward institutional-grade Ethereum participation, following the launch of its staking platform in March.

In its latest 10-Q filing, Bitmine reports that staking revenue represented 98% of total revenue for the three months ended May 31. By comparison, it recorded $624,000 from self-mining Bitcoin (BTC) and $168,000 from consulting services during the same period.

Key takeaways

- Bitmine recorded $45.7 million in quarterly revenue tied to Ether staking and validation, making staking its overwhelming revenue source.

- Staking contributed 98% of Bitmine’s total revenue for the three months ended May 31, far ahead of BTC self-mining and consulting.

- Bitmine said it has staked 85% of its Ether holdings—about 4.9 million ETH—after its March institutional staking platform launch.

- The company’s staking strategy is linked to MAVAN, an institutional validator infrastructure offering that expanded beyond Bitmine’s own treasury.

Quarterly results highlight the staking-driven shift

The latest numbers show a stark transformation in Bitmine’s revenue profile. According to the company’s filing, Ether staking and validation drove $45.7 million during the three months ended May 31. In the same quarter, non-staking lines—BTC self-mining and consulting—remained comparatively small, at $624,000 and $168,000 respectively.

Bitmine also frames this as evidence that its strategy pivot is working at scale. The results follow a year earlier when the company reported just $2 million in total revenue for the quarter ended May 31, 2025, and the largest contributor at that time was machine leasing.

For investors and market participants, the key question is sustainability: staking revenues tend to depend on the size of assets actively deployed and the evolving economics of Ethereum network activity. While Bitmine’s filing provides a snapshot of recent performance, readers will likely look for how the company’s staked percentage and validator operations translate into future quarterly results.

Bitmine says 85% of its ETH is staked

Alongside the financial disclosure, Bitmine said on Monday that it has staked 85% of its ETH holdings. The company linked that figure to approximately 4.9 million ETH.

Bitmine’s announcement also pointed to the scale of its holdings, including an update that ETH holdings reached 5.77 million tokens and total crypto and cash holdings of $11.3 billion. (The company’s statement was carried in a release from PR Newswire.)

In the same context, Tom Lee, Bitmine’s chairman, said that at full deployment—when the company’s ETH is “fully staked by MAVAN and its staking partners”—projected annualized staking rewards would be $284 million. His remarks suggest the company sees significant upside if it continues to increase the portion of its Ether actively earning staking returns.

Still, investors should separate projections from realized results. The $45.7 million quarterly revenue already reflects current operations, while the $284 million annualized statement is conditional on full staking at scale. The next signal to watch is whether Bitmine maintains the staked level and how it evolves with network conditions and validator capacity.

MAVAN expands validator infrastructure beyond Bitmine’s treasury

Central to Bitmine’s staking push is MAVAN, an institutional-grade Ethereum staking platform. Bitmine’s financial performance is explicitly connected to the March launch of MAVAN, which the company describes as operating validator infrastructure for its own holdings and for external clients.

MAVAN—short for “Made in America VAlidator Network”—was developed initially to support Bitmine’s Ethereum treasury. Its mission later broadened after Bitmine acquired Australia-based non-custodial validator operator Pier Two Holdings. According to the reporting in earlier coverage from Cointelegraph, the platform’s reach expanded to support institutional investors, custodians, and partners across the ecosystem.

That expansion matters because validator infrastructure can generate recurring fee streams, but it also increases operational exposure—such as dependence on client demand, service performance, and the ability to manage validator operations reliably at scale. Bitmine’s latest quarter suggests its staking model is generating substantial revenue today, but the longer-term test will be whether MAVAN can keep attracting and retaining external staking and validation business.

Tom Lee also points to Robinhood Chain’s ETH-denominated activity

Outside Bitmine’s own staking results, Tom Lee discussed another development: Robinhood Chain, which he described as a “breakaway success.” In his remarks, Lee highlighted that dollar volumes exceeded $1 billion since Robinhood Chain’s July 1 launch, and he compared that activity to other decentralized exchanges.

He argued that the chain’s structure ties user behavior to Ethereum because Robinhood Chain uses ETH as the native gas token, with transaction fees denominated in ETH and finality settled on Ethereum. Lee also referenced Robinhood’s 27 million users paying crypto fees denominated in ETH, framing it as evidence that everyday users increasingly interact with ETH as money.

While this is not directly tied to Bitmine’s quarterly financials, it adds color to the broader narrative Lee is promoting: Ethereum’s role as a settlement layer and fee asset may drive more real-world usage. For readers, the practical takeaway is to consider how L2s and DEX ecosystems using ETH-denominated fees could affect sentiment around demand for staking and on-chain utility—though the causal link to staking revenue would still need to be demonstrated through future reporting.

As Bitmine heads into subsequent quarters, the most important items to monitor are whether its ETH staked percentage continues rising toward full deployment, how MAVAN performs with external clients, and whether staking revenue remains the clear majority of total earnings under changing network conditions.

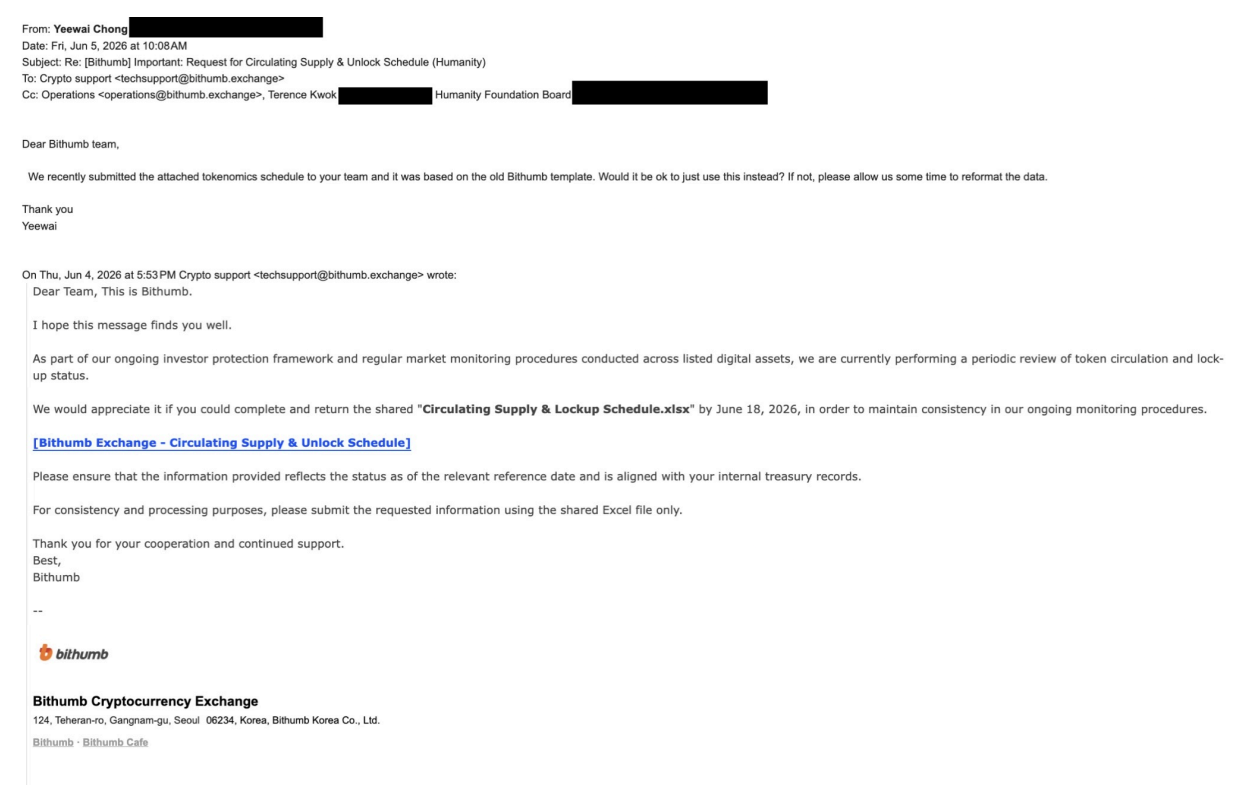

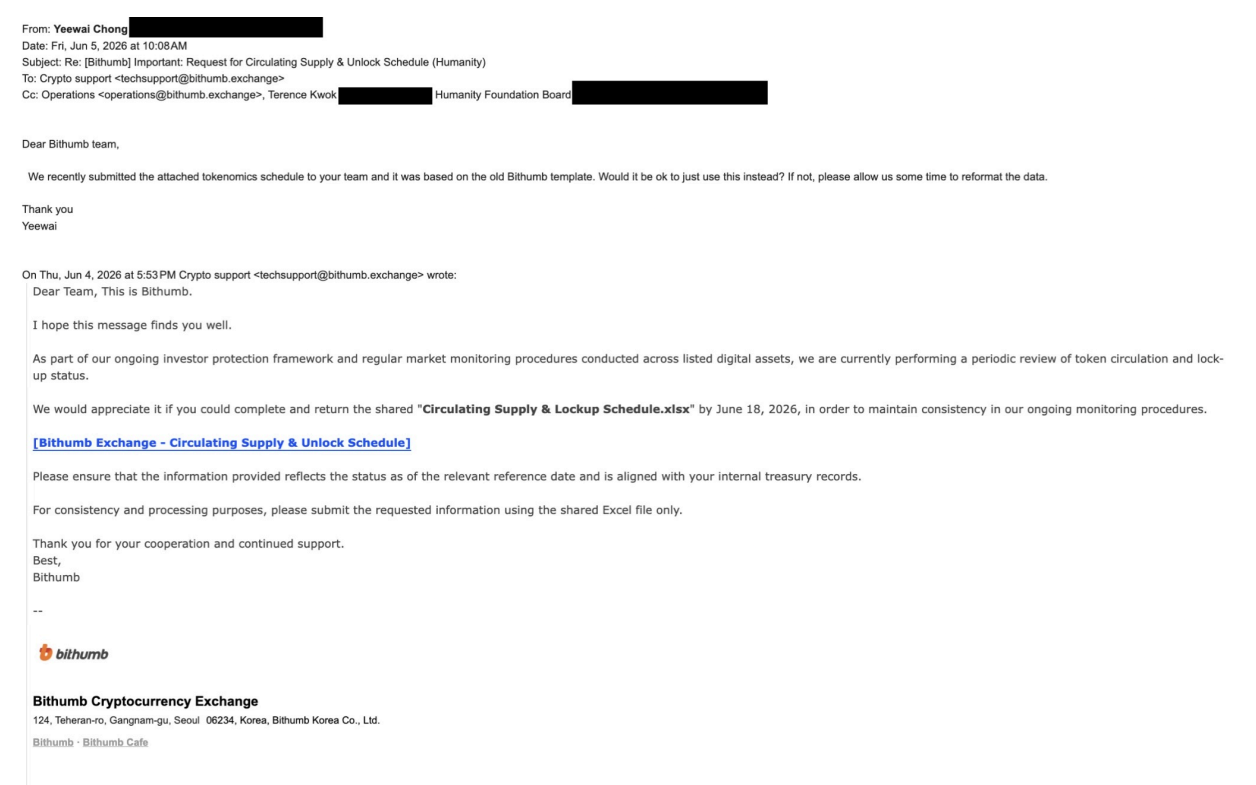

Humanity Protocol will refocus its cybersecurity efforts on operational security following a June $36 million exploit that was traced back to a compromised employee laptop, according to the founder of the decentralized identity company, Terence Kwok.

In an interview with Cointelegraph, Kwok said that the exploit stemmed from last year’s mainnet launch, when several production keys were inadvertently backed up onto the laptop that was compromised, including admin hot wallet keys and a quorum of multisig owner keys across both chains. He said:

“The hard lesson here is that operational security is as critical as smart-contract security, and we’re rebuilding accordingly.”

The exploit and Humanity Protocol’s action highlight an increase in cryptocurrency hackers refocusing their attacks on staff-level vulnerabilities and operational shortcomings, rather than exploiting smart contract code.

Humanity Protocol was exploited last month, when a compromised employee’s laptop enabled attackers to steal $36 million in Humanity (H) tokens. The token’s current market cap is roughly $211 million, according to CoinMarketCap data.

Blockchain security company Quantstamp said that the malicious attachment that was delivered through a phishing email pointed to the involvement of North Korea-linked threat actors. The malicious attachment was disguised as a token lockup schedule update from South Korean cryptocurrency exchange Bithumb and installed malware, giving attackers remote access to the machine.

The phishing email that led to the Humanity Protocol compromise.

Source: Quantstamp

North Korea-linked threat actors were tied to at least $578 million of the $634 million stolen in crypto-related incidents in April alone.

Related: AI has not triggered DeFi ‘hackpocalypse,’ Dragonfly partner says

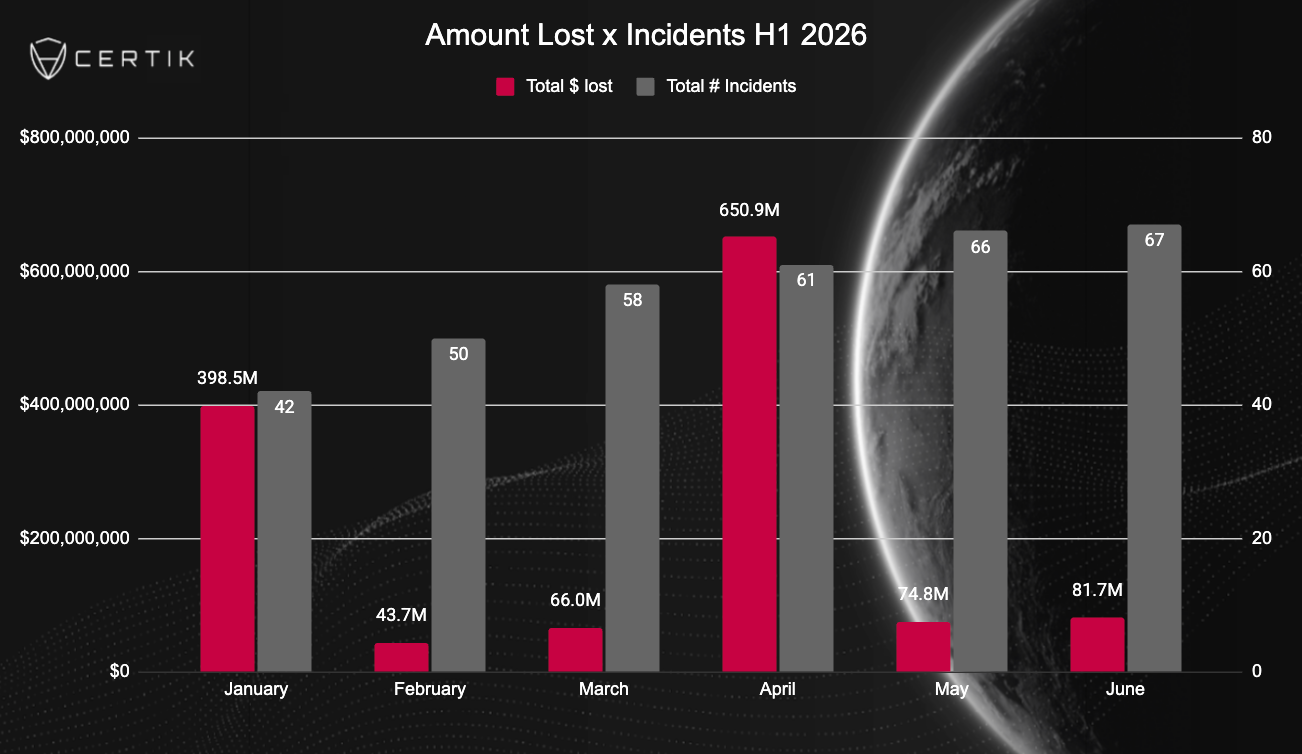

Phishing and wallet compromises lead attack vectors in H1 2026

The Humanity Protocol exploit occurred during a resurgence of cryptocurrency exploits that stemmed from operational failures and social engineering schemes.

Phishing drove the majority of the first quarter losses for a total of $508 million, while wallet compromises emerged as the biggest attack vector in the second quarter, contributing $807 million in losses, according to blockchain security company CertiK.

Monthly change in crypto exploit amounts and number of incidents across H1. Source: CertiK

To be sure, crypto losses to hacks fell 46.8% year-on-year to $1.32 billion in the first half of 2026, but CertiK said that the drop was misleading due to the $1.4 billion Bybit hack in early 2025 and stressed that North Korean malicious actors continue threatening the crypto industry.

During the second quarter of 2026, more than 70% of the losses stemmed from the Drift Protocol and KelpDAO exploits, which were also widely attributed to North Korean state-sponsored hackers.

Magazine: Does Botanix’s failure prove Bitcoiners don’t care about DeFi?

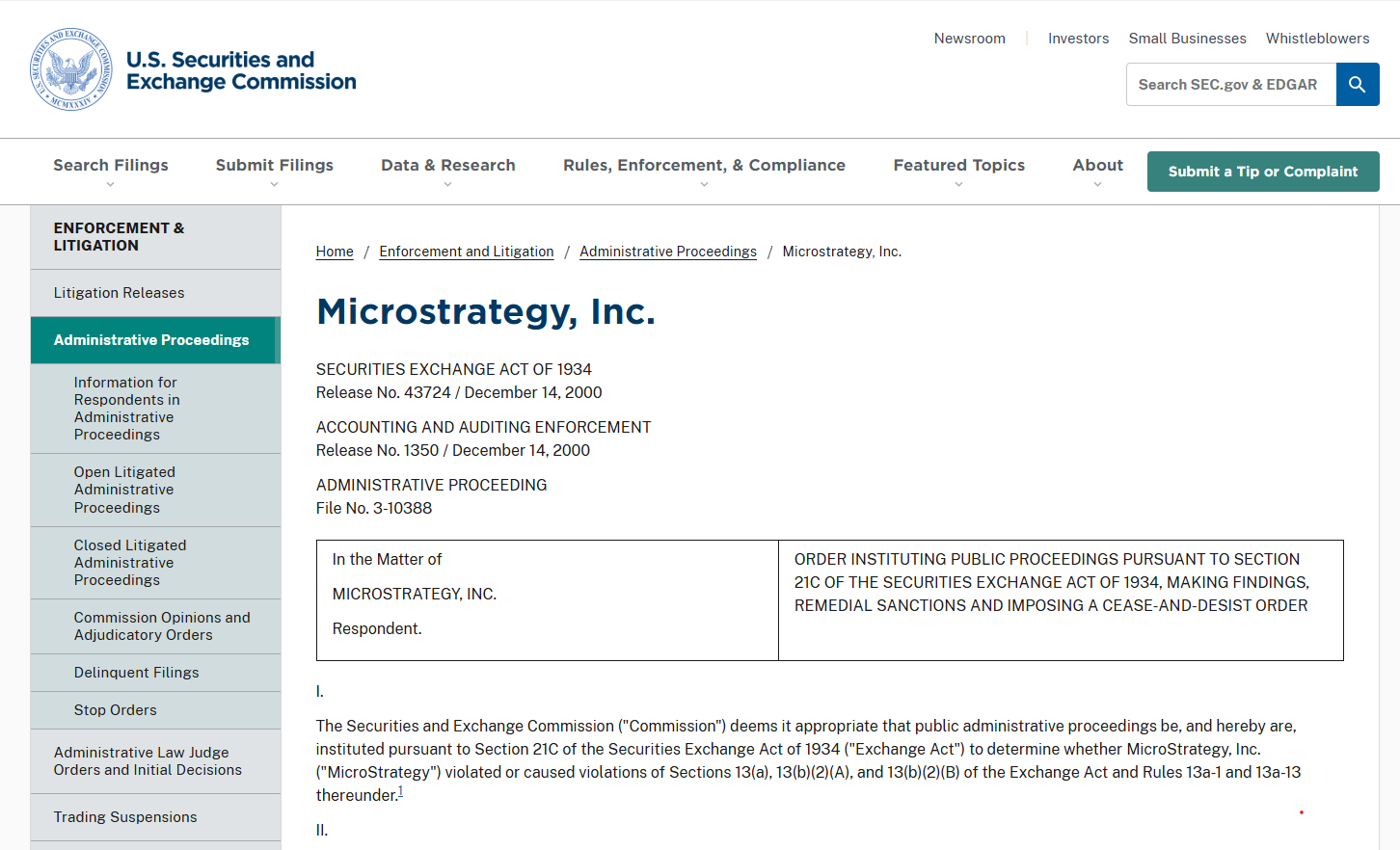

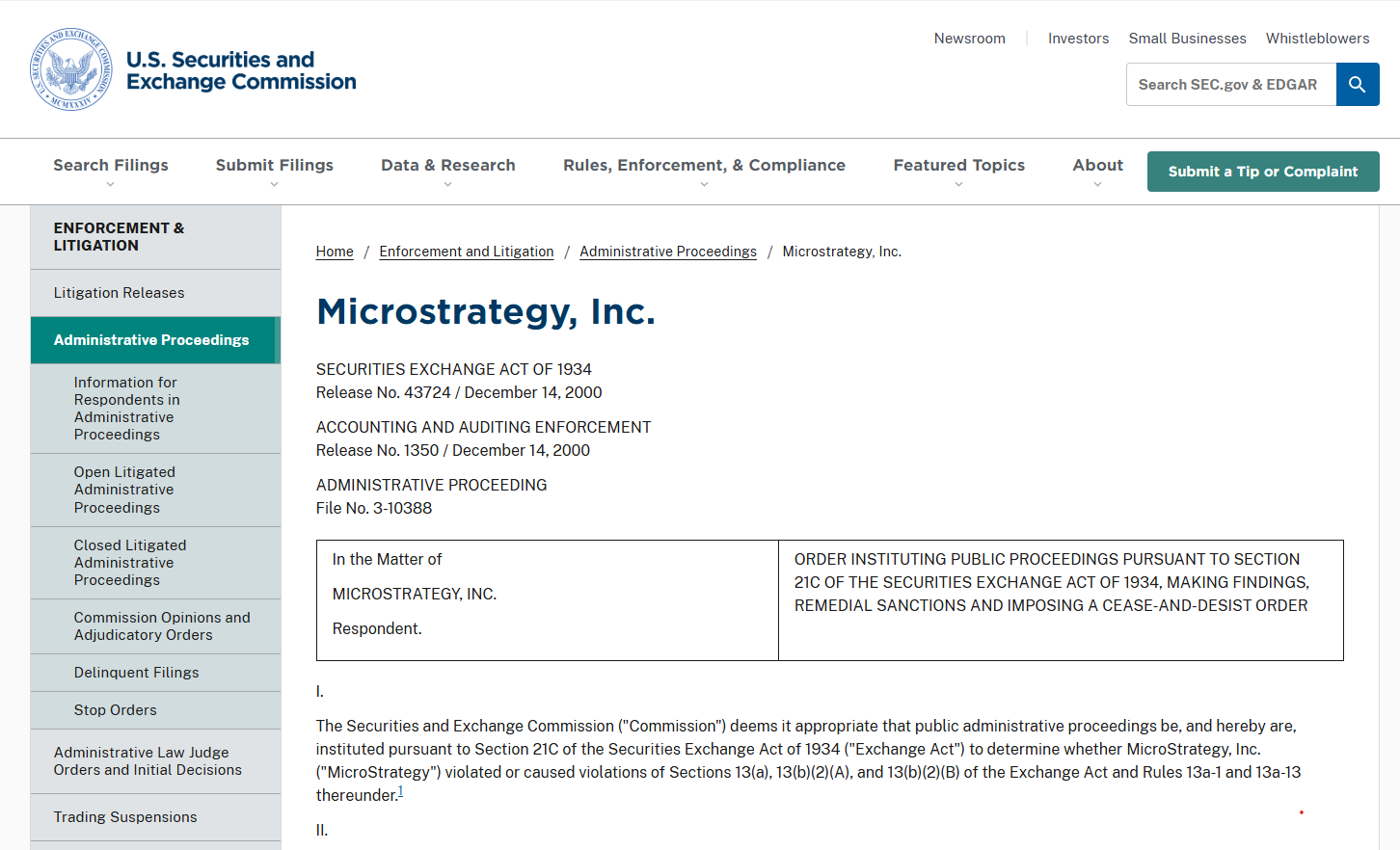

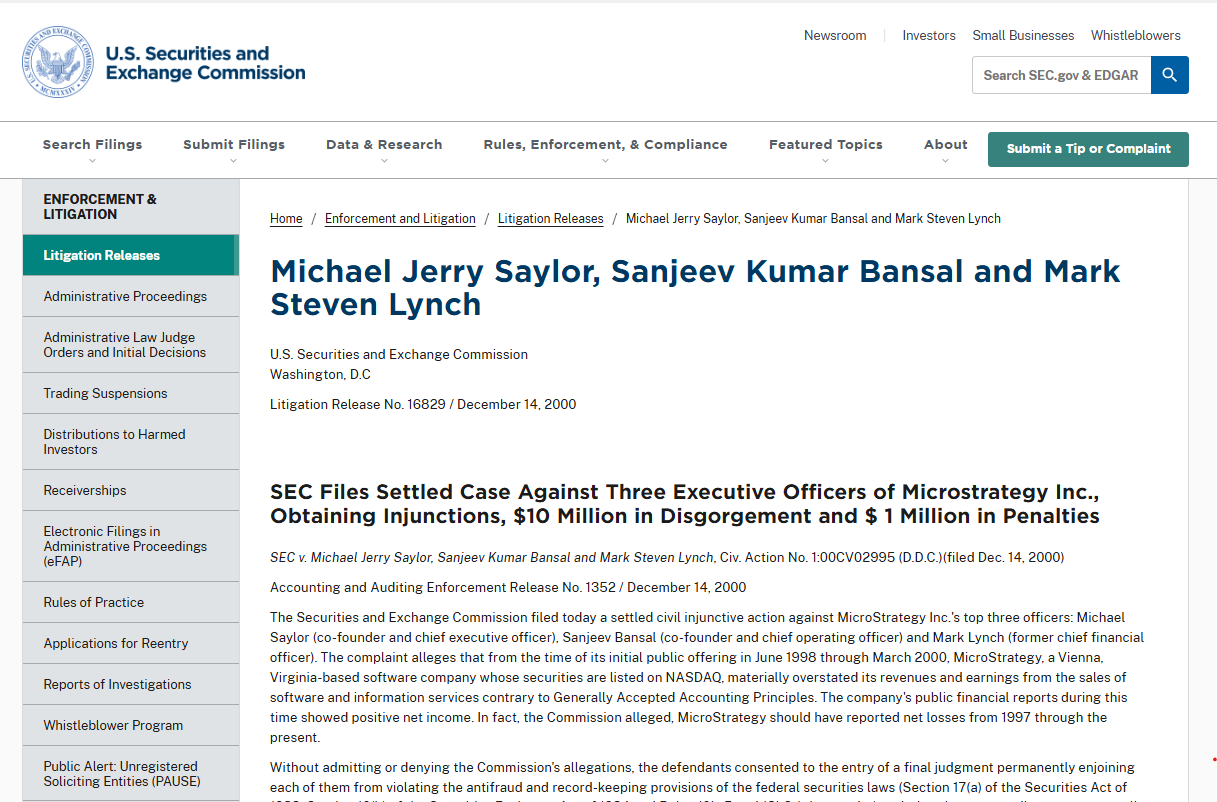

In March 2000, Strategy executive chairman Michael Saylor watched more than $6 billion disappear from his fortune in a single day.

MicroStrategy’s shares had plummeted more than 60%, thrusting the thirty-five year old software entrepreneur into the center of the dot-com crash.

The company later settled civil fraud charges with the US Securities and Exchange Commission over its accounting practices without admitting or denying wrongdoing. MicroStrategy did not cause the dot-com bubble to burst, but the saga was one of the era’s high-profile corporate blowups and the company became a symbol of the periods excesses and risks.

Now, more than 25 years later, the Bitcoin true-believer once again finds himself in the eye of one of Wall Street’s most closely watched financial experiments.

The company, now known simply as Strategy, holds 843,775 Bitcoin, more than any other public company. It has inspired dozens of listed firms to adopt Bitcoin treasury strategies of their own.

But Strategy is no longer simply accumulating Bitcoin, it has developed a series of financial engineering strategies that divide investors and analysts. Some see it as a sophisticated corporate treasury model that can’t lose, while others believe the risks are piling up on top of one another.

“The conversation shifts beyond simply acquiring Bitcoin to how those positions are financed, managed and, when necessary, traded or monetized,” Drew Forman, senior vice president and head of strategy at Talos, told Cointelegraph.

From accumulation to management

On June 29, Strategy unveiled a new capital framework allowing it to sell Bitcoin to fund preferred stock dividends, build its cash reserves and repurchase securities.

The case against MicroStrategy in 2000. Source: SEC

For a company that spent more than half a decade insisting its Bitcoin was to be accumulated rather than sold, the move caused alarm bells to ring.

Related: Lyn Alden says Bitcoin needs no savior as Strategy sells $216M of BTC

Days later, Strategy disclosed the sale of 3,588 Bitcoin, its largest disposal since adopting BTC as its primary treasury reserve asset in 2020.

To Strategy evangelists, these changes reflect the natural evolution of a company managing a multi-billion-dollar Bitcoin treasury, rather than a sharp about-turn.

Yet critics argue that Strategy’s growing reliance on preferred stock, dividend obligations and external financing has made the model more complex and interdependent, rather than more resilient.

MicroStrategy’s road to Bitcoin

MicroStrategy was one of the fastest-growing software companies of the internet boom in the 1990s, selling business intelligence software to blue-chip clients including McDonald’s, Nike and eBay, and making Saylor one of America’s richest entrepreneurs.

But on March 20, 2000, that momentum came to a sudden halt when MicroStrategy announced that it needed to restate its financial results for the fiscal years 1998 and 1999 due to accounting errors.

The company’s stock nosedived, dropping from $260 per share to just $86 in a single session. It continued to plummet over the following weeks. On April 13, when MicroStrategy announced that it would also need to restate its 1997 financial results, the stock closed at $33 per share.

That episode may have defined many executives’ careers, but Saylor spent the next two decades rebuilding the company largely outside the spotlight until the summer of 2020, when MicroStrategy announced that it would make Bitcoin its primary treasury reserve asset, and Saylor became its most vocal evangelist.

MicroStrategy settled charges with the US Securities and Exchange Commission. Source: SEC

He likened holding cash reserves during a time of unprecedented pandemic-era stimulus to holding “a melting ice cube.” The company bought its first $250 million Bitcoin on August 11.

Few public companies held Bitcoin on their balance sheets at the time, and the move was widely viewed as a high-risk experiment rather than a blueprint for corporate finance.

But Bitcoin’s price soon began to soar, bolstered by the excess liquidity, and Strategy’s valuation ballooned. Suddenly, Saylor’s controversial decision looked more like a stroke of genius and the company quickly became a leveraged proxy for Bitcoin on Wall Street.

Related: Strategy’s MSTR may plunge 80% if it repeats this dot-com-era fractal

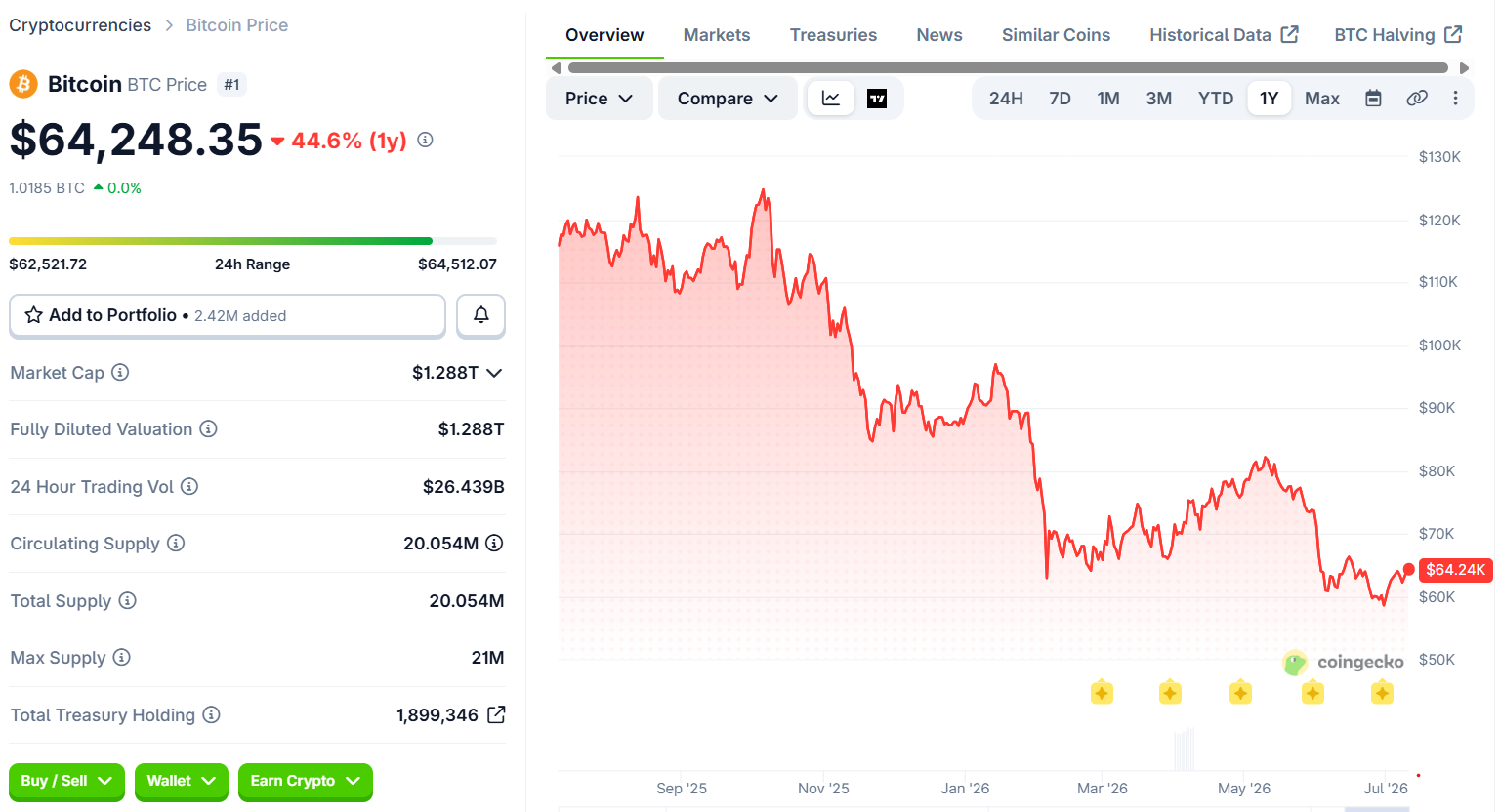

Dozens of listed firms adopted variations of its treasury strategy, and today, Strategy’s Bitcoin stack is worth more than $54 billion. But with BTC languishing far from its all-time high above $126,000 in October 2025, the company’s Bitcoin play has been repeatedly called into question.

Bitcoin price is far from its all-time high. Source: Coingecko

Skeptics argue Strategy’s model only works if Bitcoin keeps appreciating and investors continue providing new capital. Some have even warned that, under prolonged market stress, those dynamics could contribute to a so-called death spiral in Strategy’s financial model.

Different mechanism, same problem

Whether Strategy represents a radical reinvention or history repeating itself depends largely on how investors interpret the risks.

To some critics, the similarities with 2000 are less about accounting than Saylor’s willingness to build his company around a high-risk corporate model that few other chief executives would even contemplate.

“Saylor is insane (not an insult, just a diagnosis) and is either a fool or a knave,” Aswath Damodaran, professor of finance at NYU Stern School of Business, told Cointelegraph in an email.

“It hurts my brain cells just thinking about MSTR and I don’t have enough to waste on it.”

David Trainer, chief executive of investment research firm New Constructs, also holds a hawkish view. He argued that while today’s Strategy looks very different from the company that collapsed during the dot-com era, investors are still being asked to place extraordinary faith in Saylor’s latest corporate experiment.

“Different mechanism, same underlying problem: the equity is a leveraged wrapper around a volatile asset, with no fundamental earnings power supporting the valuation,” he said.

He said that the dot-com blow-up was due to incorrect financial reporting. The SEC claimed in 2000 the company’s financial reports had “showed positive net income” when it should have “should have reported net losses from 1997 through the present.” While Saylor and two executives agreed to pay a $10 million fine to settle the case, they did not admit liability to any of the SEC’s allegations.

“That was a […] mismanagement risk layered on a real (if over-hyped) software business,” he said.

Today, the company’s books are “cleaner,” he argued, with the risks embedded in a capital structure built around financing ever-larger Bitcoin purchases rather than software.

Strategy now runs a “large and growing balance of convertible debt and perpetual preferred stock,” he said, pointing to the $6.7 billion in convertible notes and $15.5 billion in preferred stock outstanding as of late May 2026, used specifically to buy more Bitcoin.

“The software business is now a rounding error next to the balance sheet,” he said.

Related: Grayscale’s Pandl says Strategy should sell $3B Bitcoin to restore confidence

According to Trainer, the bigger concern is not Bitcoin itself, but the premium investors are willing to pay for exposure through Strategy. If that premium disappears, one of the company’s key advantages disappears with it.

“Once you’re structurally reliant on issuance and issuance becomes value-destructive, the company has to either sell Bitcoin, take on more expensive financing or simply stop growing,” Trainer said.

Treasury management, not just HODLing

Forman said that investors should focus on how the company manages its increasingly sophisticated corporate treasury strategy.

“Strategy’s position can’t be understood simply by looking at the size of its Bitcoin holdings,” Forman told Cointelegraph.

He said Strategy’s willingness to sell Bitcoin is less a departure from Saylor’s long-held accumulation strategy than a practical reality of managing a corporate balance sheet. “I see it as a pragmatic evolution of a more complex treasury strategy,” he said.

“The broader takeaway is that Bitcoin is increasingly being treated as an institutional asset class,” he added, stressing that rather than simply deciding whether to buy Bitcoin, companies will increasingly need to think about governance, liquidity management, execution and risk management.

So, has Saylor rewritten his legacy?

26 years after MicroStrategy’s accounting scandal, the questions surrounding Strategy have changed.

Few critics question the integrity of the company’s financial reporting, but whether its increasingly complex Bitcoin strategy can endure prolonged market stress.

Saylor has fundamentally changed the way many public companies think about corporate treasuries, and many have followed his lead.

But whether Saylor has rewritten his legacy won’t be decided by the next bull run, but on how well Strategy performs if the markets continue to turn against it.

Cointelegraph reached out to Strategy but did not receive a response. A spokesperson from the SEC declined to comment on the settlement case.

Magazine: Bitcoin will not hit $1M by 2030, says veteran trader Peter Brandt

Bitcoin pushed above $64,000 during Tuesday’s Wall Street open as US inflation data printed cooler than expected, lifting broader risk sentiment and bringing crypto back toward the top end of its recent trading range. The move came on the heels of a surprise drop in June’s Consumer Price Index (CPI), with energy costs driving much of the decline.

While the CPI release improved the near-term outlook for monetary policy expectations, traders were still cautious about whether Bitcoin can convincingly break above nearby resistance levels and sustain gains. That tension—between relief from macro data and technical hesitation—shaped market action into the early US session.

Key takeaways

- June CPI came in at 3.5% year over year versus 3.8% expected, marking the biggest monthly decline since April 2020, according to the US Bureau of Labor Statistics.

- Energy fell sharply in June, outweighing increases in other categories such as shelter and food, helping risk assets and Bitcoin trade higher.

- Monetary-policy expectations shifted more dovish after the print, even as the CME Group FedWatch Tool still pointed to a 0.25% hike at the September meeting as the baseline.

- Crypto traders remain focused on whether Bitcoin can hold above resistance near $64,000, with some analysis warning of potential rejection if levels aren’t reclaimed and defended.

- Short liquidations in crypto were elevated after the move, but data indicates the market is still range-bound rather than decisively trending.

US CPI’s sharp energy-led drop changes the near-term macro tone

BTC/USD gained more than 2% on the day, according to price tracking on TradingView, as the June CPI release came in below expectations. The key headline was the year-over-year CPI reading at 3.5% against the 3.8% forecast.

More importantly for markets, the CPI report showed a sharp month-to-month decline. The Bureau of Labor Statistics (BLS) said June marked the largest monthly fall in CPI since April 2020. The driver was energy: BLS reported that the energy index fell 5.7% in June after rising 3.9% in May, 3.8% in April, and 10.9% in March.

“The energy index was the largest contributor to the monthly all items decrease, more than offsetting increases in other indexes including those for shelter and food.”

The CPI print landed despite other geopolitical pressures tied to the US-Iran conflict, including concerns around supply routes connected to the Strait of Hormuz referenced in earlier market coverage. However, on this inflation reading, energy prices provided the “shock absorber” that swung the inflation profile downward.

Risk assets rally as markets tilt more dovish—CME still sees September hike

Stocks traded higher following the release, and crypto investors appeared to take the macro relief in stride. The immediate impact was visible in pricing of future Federal Reserve policy: expectations shifted more dovish, with traders reducing the perceived likelihood of additional near-term tightening.

Still, the market’s baseline case did not fully break from the probability framework seen before the release. According to CME Group’s FedWatch Tool, the consensus scenario continued to lean toward a 0.25% increase at the Fed’s September meeting. In other words, the CPI outcome appeared to cool the urgency of hikes rather than eliminate the expectation of one later in the year.

Economist Mohamed El-Erian characterized the release as a counterweight to an overly hawkish tilt in rates pricing, writing that the data should temper what had become “excessively hawkish” market assumptions about monetary policy—an observation he posted in a response on X.

Bitcoin tests the $64,000 ceiling as traders debate breakout odds