Crypto World

Bitcoin Teeters Between CME Gaps and New Macro Lows: Analysis

Bitcoin failed to sustain a move above $69,000 as markets opened the weekend with caution, mirroring a broader hesitancy among traders about chasing new highs amid an uncertain macro backdrop. Fresh downside risk was baked into price action as BTC slipped more than $4,000 from the daily open, signaling that the rebound into the weekend may have been a relief rally rather than a durable trend reversal. Analysts point to resistance just below or at the old 2021 all-time high, around $69,000, which is seen as a formidable barrier. Meanwhile, two CME futures gaps loom on the horizon, offering potential magnets for price if demand accelerates again.

Key points:

-

Bitcoin faces a lack of acceptance above $69,000, while traders see new lows to come.

-

Analysis says that the rebound into the weekend was nothing more than a “relief rally.”

-

Two CME futures gaps provide potential targets for BTC price upside.

BTC price bottom “not in,” analysis warns

Data from TradingView showed BTC price action dropping more than $4,000 versus the daily open. With the old 2021 all-time high increasingly turning to resistance, cautious traders rejected the notion of a quick revival. The immediate takeaway among several market observers was that the weekend rally looked more like a relief bounce than a sustainable bottom formation.

“TLDR: The bottom for BTC is not in. My priority right now is capital preservation,” said Keith Alan, cofounder of trading resource Material Indicators, in a post on X the day before the latest price action. His warning captured a broader mood among traders who view the market as exposed to further downside risk before any durable upward momentum could reassert itself. A separate blockquote captured his sentiment: “If you’re thinking, ‘We’re so back,’ we’re not. There is literally no evidence of that yet.”

Alan also highlighted the significance of the 2021 peak around $69,000, describing it as an “important” level within what he characterized as an ongoing relief rally. He added that the recent move was “a gift yesterday,” but warned that lower prices may come before a renewed bull-market cycle could take hold.

Zooming out, market analyst Rekt Capital also argued that the most pronounced downside pressure may still be ahead. In a post on X, he likened BTC/USD’s behavior to the late-2022 bear market, suggesting that a recurring historical pattern—where a fourth consecutive cycle echoes a familiar base formation—points to further weakness before a potential bottom is established. “This is the 4th consecutive cycle that this historical tendency has continued. And history suggests there’s more downside to come,” he wrote, underscoring the stubborn risk that BTC could test lower support before a broader recovery materializes.

Bitcoin bulls bet on CME gap fills

Saturday’s retracement, meanwhile, left a new potential “gap” in CME Group’s Bitcoin futures market. This development has kept a subset of traders focused on classic short-term price magnets, with the market watching two CME gaps that could act as catalysts if prices rally in the near term.

Related: Bitcoin beats FTX, COVID-19 crash with record dive below 200-day trend line

A short-term magnet narrative has re-emerged, centered on a gap near $84,000 and a separate level that could pull prices higher if demand re-emerges. Traders argued that such gaps often attract price action as liquidity cycles through the market, even if the longer-term trend remains uncertain. The chatter around CME gaps aligns with a broader view that a relief rally could redraw price trajectories in the near term, though it is not a guarantee of a lasting bounce.

Will we see this #Bitcoin CME Gap filled next week?

$84,215 🎯 pic.twitter.com/ZHaKynuR3F

— Elja (@Eljaboom) February 7, 2026

In parallel, traders like Michaël van de Poppe, a veteran analyst and founder of various crypto ventures, voiced a more constructive near-term view. He forecast a continuation pattern where a correction gives way to a move toward the CME gap and beyond, suggesting that the next week could carry BTC toward the $75,000-and-higher zone if momentum reasserts. “Today: correction day. Tomorrow: back up again towards the CME gap. Next week: continuation to $75k+,” he wrote in a post on X, signaling that the possibility of a rebound is not dismissed by some observers.

Notably, Samson Mow, CEO of Bitcoin-adoption firm JAN3, framed the event as a test of whether large-scale corporate buyers will step in to buy BTC at the new price levels. He described the higher CME gap as one of two questions every financial analyst should be asking: whether institutional demand can absorb the selling pressure given the 15-month low in BTC prices, and whether corporate treasury activity will pick up as prices drift lower. “I believe the answers are not for long and very soon,” he concluded in a post on X, signaling that the near term could reveal significant shifts in demand just as price action wobbles around key levels.

//platform.twitter.com/widgets.js

Why it matters

The present price action matters because it tests the resilience of BTC’s uptrend hypothesis at a time when macro uncertainties linger. A failure to sustain moves beyond critical resistance around $69,000 reinforces the notion that the market is wrestling with a structural pivot rather than a short-lived surge. The CME gaps add a practical, price-target dimension to the debate: if price finds buyers near those gaps, it could spur a corrective rally that lasts into the following week; if not, the risk-off mood may extend and push BTC toward the lower end of recent ranges.

Moreover, the discourse around corporate treasury demand—an ongoing theme in crypto markets—could shape the supply/demand balance in the months ahead. If large buyers re-enter at these levels, they could provide a floor that mitigates downside risk and sets the stage for a broader recovery. Conversely, persistent macro weak spots or a fresh risk-off impulse could keep BTC mired in a corrective phase, testing support levels that traders have watched since late 2025.

Taken together, the footage from trading desks shows a market that remains finely poised between a cautious, risk-averse stance and a renewed appetite for risk-taking when specific technical benchmarks align with liquidity drivers. The result is a price story that is less about a single breakout and more about the tug of war between macro-impacted liquidity and market structure signals like CME gaps and key resistance levels.

What to watch next

- Watch how BTC trades around the CME gap near $84,000 in the coming days and whether price action tests that area again.

- Monitor whether buyers reappear near the mid-to-upper $70k region, potentially signaling a shift in the short-term trend.

- Look for any signs of renewed institutional or corporate BTC treasury activity as prices approach critical levels.

- Assess macro cues and liquidity conditions, since they likely will continue shaping volatility and the pace of any potential relief rallies.

Sources & verification

- TradingView BTCUSD price data referenced in the price action discussion.

- Comments from Keith Alan (Material Indicators) on BTC’s bottom and capital preservation, shared on X.

- Analysis from Rekt Capital regarding cycle patterns and potential downside in BTC/USD.

- Forecasts from Michaël van de Poppe on CME gaps and near-term targets.

- Remarks from Samson Mow on corporate BTC treasury activity and near-term demand dynamics.

What the market is watching next

The coming days will be telling for BTC’s near-term orientation. If the price can reclaim and sustain a move above the $75,000–$80,000 range and, more broadly, approach the CME gap around $84,000, bulls may gain a foothold that could catalyze a more substantive rebound. Conversely, if selling pressure intensifies and price breaks back toward the mid-$60,000s, the market could extend the current corrective phase while traders reassess whether a longer bear-market cycle has run its course. As always, liquidity, macro risk sentiment, and institutional participation will remain the key variables shaping outcomes in the weeks ahead.

On Tuesday, March 19, the SEC issued joint guidance with the CFTC to “finally” provide clarity about how the securities laws apply to digital assets. On many issues, including staking and meme coins, the SEC’s new guidance is a welcome development and a marked improvement from the Gensler days. It also rightly acknowledges that the agency’s “regulation by enforcement” campaign under Chair Gensler had muddied compliance obligations and stifled the industry. But in important ways, the guidance stops short of the full course correction the crypto industry needs.

The biggest shortcoming is the SEC’s articulation of the Howey test for “investment contract” securities. All agree that most digital assets are not, on their own, investment contracts. Even the Gensler SEC (eventually) admitted as much, and the SEC’s new guidance reiterates that position. The key question, though, is when a digital asset is sold as part of an investment contract such that the sale becomes subject to the securities laws.

The statute provides the answer. As a matter of text, history and common sense, an “investment contract” means a contract – an express or implied agreement between the issuer and investor under which the issuer will deliver ongoing profits in return for the purchaser’s investment. Most digital assets are not investment contracts because they are not contracts. A digital asset can be the subject of an investment contract (like any other asset), but it can still be sold separately from the investment contract without implicating the securities laws. In the suits brought by Gensler, crypto companies vigorously defended that proper interpretation of the law.

Yet the SEC’s new guidance is silent about whether an investment contract requires contractual obligations. Instead, it says an investment contract travels with a digital asset (at least temporarily) when the “facts and circumstances” show the digital-asset developer “induc[ed] an investment of money in a common enterprise with representations or promises to undertake essential managerial efforts,” leading purchasers to “reasonably expect to derive profits.” That does not clearly confirm a clean break from the SEC’s former view that Howey eschews “contract law” and demands “a flexible application of the economic reality surrounding the offer, sale and entire scheme at issue, which may include a variety of promises, undertakings and corresponding expectations.”

The Gensler SEC’s know-it-when-I-see-it approach to Howey was deeply problematic. It allowed the agency to piece together an “investment contract” from various public statements by digital-asset developers — tweets, white papers, and other marketing materials — even absent concrete promises by the issuers. And it failed to distinguish securities from collectibles like Beanie Babies and trading cards, the value of which depends heavily on their maker’s marketing and attempts to create scarcity. The SEC missed an important opportunity to clearly reject that approach and restore a key statutory dividing line between assets and securities — a contract.

The SEC can still fix this problem, but to do so, it will need to further clarify how the agency intends to apply Howey going forward — and to finally make a clean break with Gensler’s overbroad interpretation of the securities laws. For example, the Gensler SEC repeatedly cited various “widely distributed promotional statements” as a basis for pushing a digital asset into the realm of investment contracts. The SEC’s new guidance puts some guardrails on that approach by requiring a developer’s representations or promises to be “explicit and unambiguous,” to “contain sufficient details,” and to occur before the purchase of the digital asset. But even that improved approach leaves too much room for interpretation. It could be expansively applied by private plaintiffs, the courts or a future SEC. Rather than continue down the path Gensler trod, the SEC should make clear that mere public statements affecting value are insufficient and that promises and representations must be made in the context of the specific sale at issue — not strung together from whitepapers or social-media posts that many purchasers likely never considered.

The SEC also should clarify its approach to secondary-market trading. Helpfully, the agency now recognizes that digital assets are not investment contracts “in perpetuity” just because they once were “subject to” investment contracts. But the agency also says that digital assets remain “subject to” investment contracts traded on secondary markets (like exchanges) so long as purchasers “reasonably expect” issuers’ “representations and promises to remain connected” to the asset. The SEC says little about how to assess those reasonable expectations, providing only two “non-exclusive” examples of when an investment contract “separates” from a digital asset. And it says nothing about whether a secondary-market purchaser must have a contractual relationship with the token issuer. That leaves it unclear whether the SEC has really moved on from the Gensler-era view that investment contracts “travel with” or are “embodied” by crypto tokens.

Instead of those mixed messages, the SEC should impose meaningful restraints on the application of the securities laws to secondary-market transactions by adopting Judge Analisa Torres’s approach in Ripple. Judge Torres recognized that it is unreasonable to infer an investment contract in the context of “blind bid-ask” transactions — that is, transactions where the counterparties do not know each other’s identities (as is common in secondary-market trading). Because buyers have no idea whether their money goes to a token’s issuer or to some unknown third party, they can’t reasonably expect that the seller will use the buyers’ money to generate and deliver profits. The SEC should endorse Judge Torres’s analysis expressly.

These are not academic quibbles. The current SEC might not read or enforce its new guidance in a manner that threatens the viability of the crypto industry in the United States. But by failing to clearly reject the excesses of the Gensler era, the SEC’s new guidance leaves the industry exposed to a future SEC that could leverage ambiguities in the SEC’s current guidance to resume regulation by enforcement. Private plaintiffs could try to do the same in lawsuits against key industry players (such as the leading exchanges). And in the meantime, the SEC’s interpretations could distort the securities-law baseline during negotiations over market-structure litigation.

The SEC invited comments on its guidance, and the industry should oblige. The SEC should get credit where credit is due. But the industry should not hesitate to highlight the lingering flaws and ambiguities in the agency’s approach and advocate for clear, meaningful, and permanent restraints to ensure regulatory clarity and stability. Simply giving the legal architecture of the last enforcement campaign a facelift is not enough.

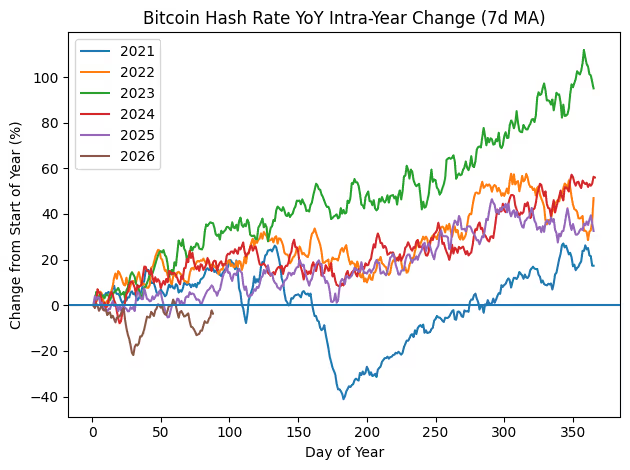

For the first time in six years, the bitcoin hashrate, the total computational power securing the network, fell during the first quarter. It is currently down around 4% year to date, hovering around 1 zettahash per second (ZH/s).

Over the past five years, the rate has surged from roughly 100 exahashes per second (EH/s), a 10-fold increase, according to Glassnode data. Each year, the metric rose during the first quarter and ended with strong full-year growth in excess of 10%. In 2022, the figure almost doubled.

The AI Pivot

The shift in 2026 reflects changing economics across the bitcoin mining sector. With production costs near $90,000 per bitcoin and the spot price closer to $67,000, margins are negative. In response, many publicly listed miners are switching to artificial intelligence and high-performance computing infrastructure, where returns are higher and more predictable.

This transition is being funded through debt issuance and bitcoin sales, reducing reinvestment into bitcoin mining. As a result, hashrate growth is becoming more sensitive to the cryptocurrency’s price, with weaker prices likely to trigger further declines as smaller operators exit.

While a falling hashrate may raise concerns about network security, decentralization may matter more than absolute size. Publicly listed U.S. miners have accounted for over 40% of the global hash rate, and a reduction in their influence could lead to a more geographically distributed network. In that sense, the current shift may ultimately support decentralization.

Despite the slowdown, CoinShares still forecasts hashrate growth to around 1.8 ZH/s by the end of 2026, conditional on bitcoin recovering toward $100,000.

Read More: End of bitcoin ‘HODL’: public miners going all-in on AI, signaling more BTC selling

DeFi risk curator Steakhouse Financial has been hacked and its website and app are now being used to host a phishing scam.

Steakhouse disclosed the breach Monday morning and warned that any new users interacting with the website or app are likely interacting with a malicious version implemented by the hackers.

The attack appears to have affected just the front-end of operations, as Steakhouse assured users, “No deposits are at risk. No contracts are affected. All Steakhouse depositors are safe.”

Read more: Fake Uniswap phishing ad on Google steals trader’s life savings

“We are working to restore the frontend as soon as possible,” the firm said.

Steakhouse co-founder, Sébastien Derivaux, warned crypto users to avoid the website until further notice.

Various crypto firms offered alternative services and safety assurances for customers with funds at Steakhouse.

Others found humor in the incident, with one user asking, “Does phishing on Steakhouse make this a surf and turf attack?”

At the time of writing, neither Steakhouse Financial or its CEO have shared any further updates on the incident.

Steakhouse Financial housing a crypto drainer

Crypto security firm Blockaid claims that the Steakhouse attackers are utilizing code from one of the “largest active wallet drainer operations onchain” known as Angelferno, or Angel Drainer.

Read more: Fears of $27M Venus Protocol hack turn out to be phishing attack on power user

Earlier this month, AI crypto firm GAIB fell victim to a social engineering scheme that gave hackers access to its domain, where they implemented a copycat website kitted with Angelferno.

Drainers work by stealing a user’s crypto after they sign a malicious transaction that gives hackers full access to withdraw their funds.

Blockaid was able to help GAIB detect the malware, and the malicious site was gone in roughly seven hours, with no apparent user losses.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

This month, Bitcoin’s hashrate fell 6% after the US and Israel attacked Iran, highlighting Iran’s significant crypto mining activity.

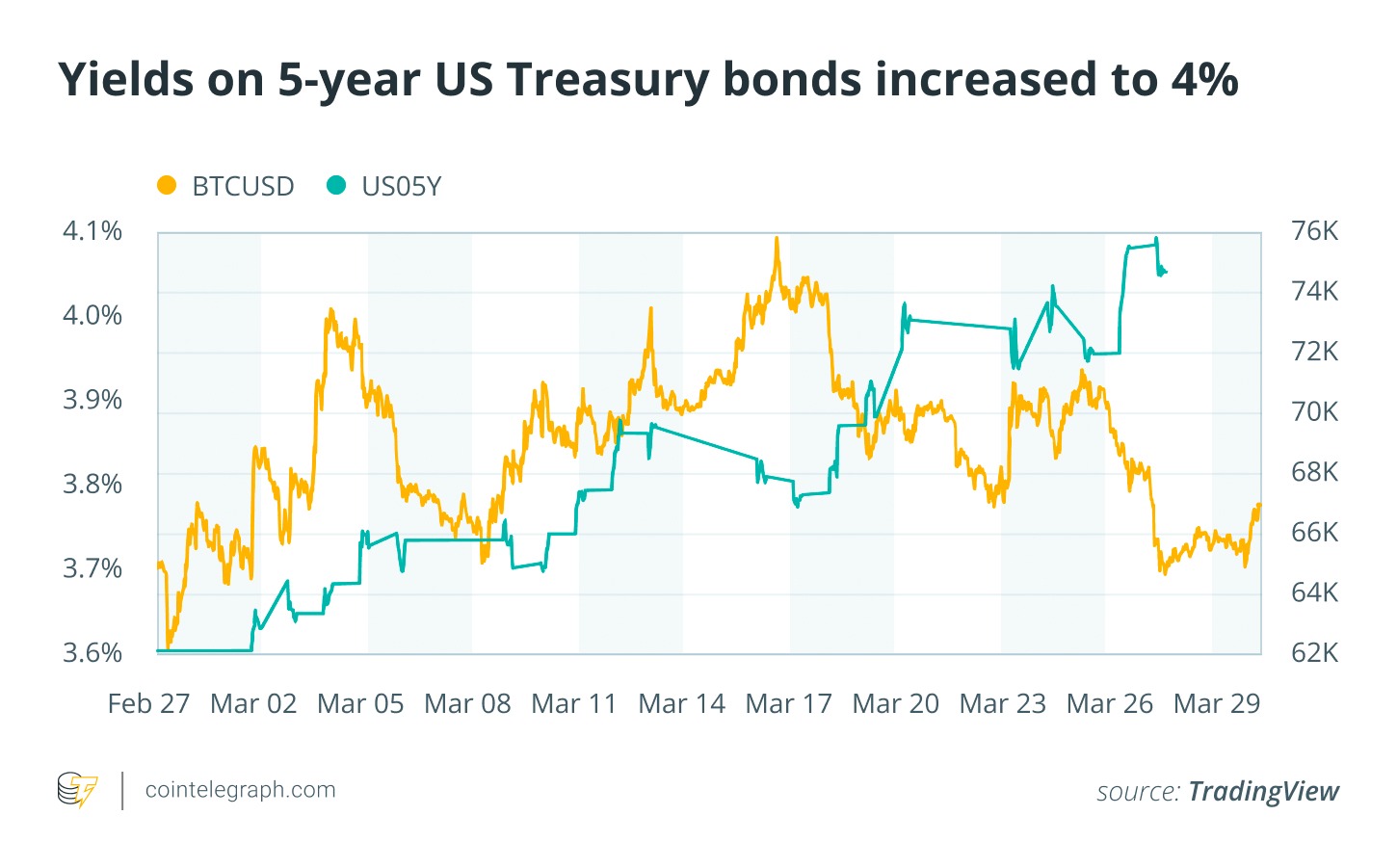

Bitcoin price, meanwhile, remains lackluster. Higher 4% yields on US Treasury bonds have added pressure, and investors are seeking less risky prospects amid geopolitical tension.

Less appetite for crypto trading has proven problematic for Robinhood. The trading platform’s stock is down 16% on the month, and leadership has announced a stock buyback program.

Prediction markets marked a record number of transactions, representing a more than 2,800% increase since this time last year.

Here’s March by the numbers:

Bitcoin lacks momentum as 4% US Treasury bond yields put pressure on price

Yields on five-year US Treasury bonds are up 4% in March, putting pressure on Bitcoin price. While showing some gains in mid March, the asset ended the month much where it started, around $67,000.

As per an analysis from Cointelegraph, fears of a drawn-out conflict between the US and Israel against Iran have led investors to cut out risk. A sell-off in bonds, along with a nine-month high of 4% in yields, suggests that traders are building cash positions.

Bitcoin hashrate falls nearly 6% after US and Israel attack Iran

On Feb. 28, the United States and Israel launched a joint special military operation in Iran called “Operation Epic Fury.” One month later, the Bitcoin (BTC) hashrate is down almost 6%.

Bloomberg crypto and digital assets strategist Dushyant Shahrawat said in a recent interview that Iran is one of the world’s largest Bitcoin miners, accounting for some 6-8% of global hashrate, and 70% of mining activities are conducted by the military.

Disruptions to the country’s energy infrastructure and diversion of military priorities to defense have thus hit Iran’s ability to mine Bitcoin.

Prediction market transaction top 192 million

Transactions on prediction markets like Polymarket and Kalshi topped 192 million in March. That represents a 24% increase from last month and a 2,880% increase compared to the same time last year, according to Dune analytics.

Related: Lawmakers push another bill to curb prediction market insider trading

Prediction markets are growing in popularity, but in the United States, they face state regulators who say they facilitate a form of gambling. At least 11 states have taken legal action against them.

On March 20, Carson City District Court Judge Jason Woodbury upheld a regulator’s move to temporarily ban prediction market Kalshi in Nevada.

Arizona has brought criminal charges against Kalshi for allegedly “running an illegal gambling operation and taking bets on Arizona elections, both of which violate Arizona law.”

Other states like Utah and Pennsylvania are currently considering legislation that would bring prediction markets under state gambling or gaming laws. Kalshi says that it answers only to federal regulation under the Commodity Futures Exchange Commission (CFTC).

Euro-denominated stablecoins account for 85% of non-dollar volume

Stablecoins backed by the euro have emerged as a favorite alternative to assets backed by US dollars. Some 85% of non-dollar stablecoin volumes occur in euros, according to a March report from Dune.

While euro-denominated coins initially only represented some 50-70% of the non-dollar market, they began expanding significantly in 2024. Now they represent 85% of total transferred volume. Euro stablecoins are also dominant in regard to participation, with user share rising to over 78%.

Dune attributes this increase to more confidence in stablecoins among institutions, thanks in large part to the Markets in Crypto-Assets regulatory package (MiCA).

Robinhood stock down 16% on month

Robinhood stock has decreased over 16% in March, from nearly $80 to $66 as of publishing time.

The stock and crypto trading company’s share price has been struggling in recent months. Over the last six months, it dropped over 50%. Uncertainty over the regulation of new verticals like prediction markets and social trading, along with a collapse in crypto trading revenues are creating structural obstacles for the company.

Revenue from crypto transactions reportedly dropped 38% year-over-year as of Q4 2025. Crypto app volumes dropped 58%.

To address the problem, Robinhood has approved a $1.5 billion share buyback program in March, which will execute over the next three years.

Strategy’s Bitcoin holdings are 11% in the red

Amid a lackluster price action on the month, Strategy’s Bitcoin portfolio is at an 11% loss. The average cost of Bitcoin in its portfolio is $75,669. Bitcoin is trading around $67,800 at publishing time.

Still, the company has continued its regular Bitcoin purchases. It made two this month: one for 17,994 Bitcoin on March 9 and another for 22,337 Bitcoin on March 16, amounting to roughly $2.7 billion at publishing time.

The software company has financed most of its Bitcoin purchases through high-yield stock offerings, like Stretch (STRC). This allows the company to buy Bitcoin without diluting its MSTR common shares.

The company’s chair, Bitcoin bull Michael Saylor, said recently that 80% of STRC buyers are retail investors. “Retail investors prefer low-volatility, high-yield digital credit,” he said.

Magazine: XRP yet to ‘price in’ 3 bullish catalysts, Bitcoin to $80K? Trade Secrets

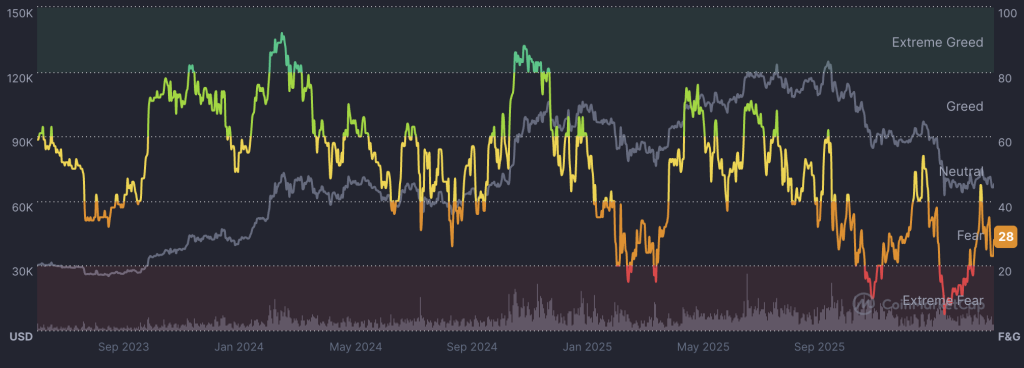

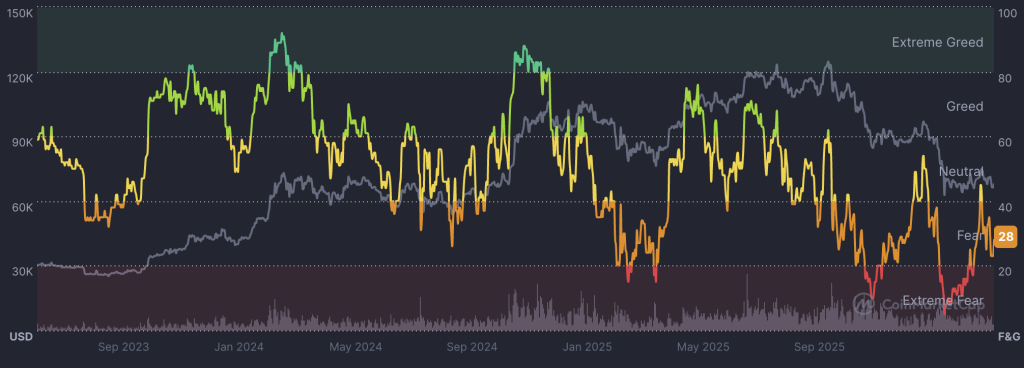

Brent crude punched through $116 a barrel on March 30, 2026 – a 60% monthly surge driven by escalating US-Iran tensions after Tehran accused Washington of preparing an invasion, compounding Houthi strike disruptions, and Bitcoin is now sitting in the crosshairs of the resulting institutional risk-off rotation.

The oil price spike is not hitting crypto directly; it’s hitting it through three compounding channels: inflation re-acceleration, delayed Fed rate cuts, and a geopolitical risk premium that is draining leveraged long exposure across every risk asset class.

Bitcoin dropped to weekly lows between $63,000 and $65,700, over $500 million in derivatives liquidations hit the tape, and 84% of that came from long positions.

The Fear & Greed Index collapsed to 28 – Extreme Fear – while a record $14 billion options expiry amplified the volatility.

Discover: The best crypto to diversify your portfolio with

Bitcoin Faces Structural Deleveraging as Oil-Driven Inflation Rewrites the Fed Playbook

$63,000 is the line Bitcoin cannot afford to lose.

That level has capped the downside through the prior 2 macro shock episodes. The 200-day moving average sits just below at $62,400.

A close beneath it would be the first since the October 2025 rally began and would likely trigger a second wave of systematic deleveraging from quant funds running momentum strategies. Resistance above is layered at $67,500 and $71,000, both former support zones that flipped during the February selloff.

The oil correlation matters more than usual right now. Binance Research puts the Bitcoin-WTI correlation near zero across most market regimes.

The 30-day rolling correlation currently sits at just 0.15. But that changes during extreme disruption events. The Strait of Hormuz is flowing at roughly 4 million barrels per day against a normal 20 million. That is not a tail risk. That is an active structural supply shock, exactly the kind that produces temporary correlation spikes.

If US-Iran tensions de-escalate and Hormuz flows normalize, Brent retreats below $100 and the Fed signals patience at its April 1 to 2 meeting. Bitcoin reclaims $67,500, BlackRock’s IBIT builds on its $225.2 million inflow during the dip, and institutional rotation flips back into accumulation mode.

If tensions persist without full escalation, Brent holds $110 to $116 and the Fed stays hawkish through Q2. Bitcoin grinds between $63,000 and $68,000 with elevated volatility, ETF flows stay choppy, and mining costs for operators like Marathon Digital rise 15 to 25%.

“The United States of America is in serious discussions with A NEW, AND MORE REASONABLE, REGIME to end our Military Operations in Iran.” – President Donald J. Trump

pic.twitter.com/0MWL2hSNmK

— The White House (@WhiteHouse) March 30, 2026

A full Hormuz blockade is the scenario nobody wants to price. Oil above $130, 10-year Treasury yields breaking above 5%, and the Fed forced to choose between fighting inflation and supporting growth.

That combination could send Bitcoin to $55,000 to $57,000 in a full risk-off liquidation wave, mirroring February 2022 when WTI hit $115 and BTC fell from $45,000 to $39,000 in days.

The inflation channel is what most traders are underweighting. Sustained oil above $100 does not just pressure sentiment. It mechanically delays rate cuts.

Bitcoin’s slide below $67,000 alongside rising Treasury yields already showed how directly that linkage bites. BTC’s 0.9 correlation to the IGV tech index means it trades like a rate-sensitive growth asset in the short run, not an inflation hedge.

Watch the Fed’s April 1 to 2 meeting. Any language signaling a longer hold is the catalyst for the next leg down. Congressional votes on Iran sanctions expected mid-April carry equal weight. Further Hormuz disruption sends another shock through energy markets and straight into institutional risk appetite.

Discover: The best pre-launch token sales

The post Oil at $116: Why This Macro Shock Could Trigger a Bitcoin Risk-Off Deleveraging appeared first on Cryptonews.

BitMine Immersion Technologies (BMNR) made its largest weekly purchase of either (ETH) this year, adding 71,179 ETH and extending a month-long ramp-up in buying even as crypto prices remain under pressure.

The purchase, worth roughly $143 million at current prices, lifted the company’s total holdings to over 4.73 million ETH, about 3.92% of the token’s supply, according to a Monday update. BitMine has now increased its buying pace for four straight weeks, stepping up from a prior average of 45,000 to 50,000 ETH.

The move stands out as most other large digital asset treasuries (DAT) halted crypto accumulation or even sold tokens during the crypto market downturn. Strategy (MSTR), the largest corporate bitcoin owner, was the only other major buyer in the recent months, and even the Michael Sayler-led company refrained, breaking a 13-week buying streak.

Bitmine Chairman Thomas “Tom” Lee said the firm continues to see the current market as the final phase of a downturn as rising oil prices and geopolitical tensions keep risk assets under pressure.

The company’s total crypto and cash holdings stood at $10.7 billion. In addition to its ETH treasury, BitMine held 197 bitcoin, and $961 million in cash and equity stakes, including $102 million in Eightco Holdings.

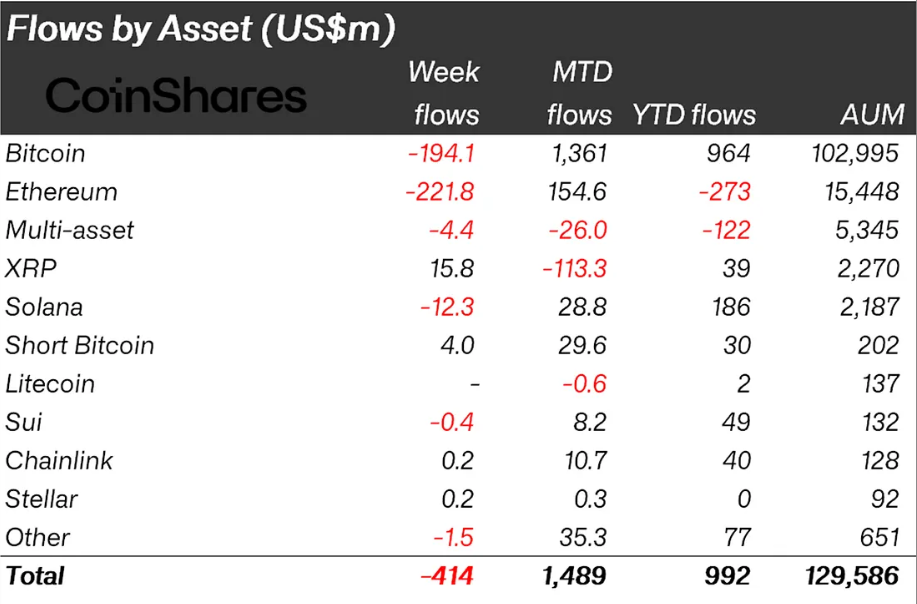

Digital asset investment products posted their first weekly outflows in over a month, as a mix of geopolitical tensions and shifting monetary policy expectations rattled investor confidence.

According to the latest data, crypto funds saw $414 million in net outflows, marking a sharp reversal after five consecutive weeks of inflows.

Crypto Funds Lost $414 Million Last Week

The pullback coincided with rising tensions tied to the Iran conflict and a notable shift in expectations around the Federal Reserve, as markets pivot from anticipating rate cuts to pricing in potential hikes.

The US accounted for the bulk of the outflows, with $445 million exiting digital asset funds, highlighting a decisive risk-off stance among American investors.

In contrast, European markets showed signs of opportunistic buying. Investors in Germany and Canada added $21.2 million and $15.9 million, respectively, suggesting confidence in long-term valuations despite short-term volatility.

Among individual assets, Ethereum was hit hardest, recording $222 million in outflows. The move pushed its year-to-date flows into negative territory, reflecting sustained pressure that analysts link in part to regulatory uncertainty surrounding the Clarity Act.

Bitcoin also faced headwinds, shedding $194 million during the week. However, it continues to show resilience, maintaining a strong $964 million in net inflows for the year so far.

This suggests that while short-term sentiment has weakened, institutional conviction in Bitcoin remains intact.

In contrast, XRP stood out as a rare gainer, attracting $15.8 million in inflows. Its performance positions it as a relatively safe haven within the digital asset space during periods of broader market stress.

The latest fund flow data shows how quickly sentiment in crypto markets can shift when macroeconomic and geopolitical risks converge, leaving investors to reassess their exposure in an increasingly uncertain environment.

The post Geopolitics and the Fed Flush $414 Million From Crypto Funds in a Week appeared first on BeInCrypto.

Key takeaways

-

Hong Kong’s 2026-27 budget marks a shift from experimental digital bond projects to the direct integration of tokenized issuance and settlement into the city’s regulated financial market infrastructure.

-

CMU OmniClear, a subsidiary of the Hong Kong Monetary Authority, will build a digital asset platform to support tokenized bond issuance and settlement. This embeds digital securities within Hong Kong’s established clearing and post-trade framework.

-

Hong Kong has issued multiple tokenized government bonds, including a HK$10 billion digital bond in 2025. Authorities plan to make such offerings a regular feature to deepen market participation and improve liquidity.

-

Hong Kong is introducing stablecoin licensing, digital asset dealer and custodian regulations and compliance rules aligned with global tax transparency standards to support a fully regulated digital asset market.

For years, tokenized bonds were discussed as a future upgrade to capital markets. In Hong Kong, that transition is now moving into practice.

The city’s 2026-27 budget marks a pivotal turning point. Tokenization is no longer confined to isolated experiments but is being integrated into the heart of Hong Kong’s financial ecosystem. By embedding issuance and settlement directly into its post-trade systems, the city is moving beyond one-off digital deals to create a standardized, regulated environment.

This article explores how Hong Kong is integrating tokenized bonds into its financial infrastructure through a new digital platform developed by CMU OmniClear, a subsidiary of the Hong Kong Monetary Authority (HKMA), regular government issuances and supportive regulations. This development reflects a shift from experimental pilots to scalable, institutional-grade digital capital market systems.

Hong Kong’s advancing tokenized bond program

Hong Kong has already completed several rounds of tokenized government bond issuances. In Q4 2025, the government launched its third series, valued at HK$10 billion, approximately US$1.28 billion. Authorities have since confirmed that these tokenized bond offerings will continue on a regular basis.

The 2026-27 budget, however, marked a significant escalation.

Financial Secretary Paul Chan stated that CMU OmniClear Holdings, a wholly owned subsidiary of the HKMA, will develop a dedicated digital asset platform. The platform is designed to handle both the issuance and settlement of tokenized bonds.

Importantly, the system is being built with long-term expansion in mind. It will:

-

Be progressively extended to support a wider range of digital assets beyond government bonds

-

Establish interoperability with tokenization platforms in other regional jurisdictions

-

Become fully integrated into Hong Kong’s broader post-trade financial ecosystem

This final aspect, deep integration into core market infrastructure, is what elevates tokenization from experimental pilots to a foundational element of the financial system.

CMU OmniClear: From experiment to core infrastructure

CMU OmniClear is far from a standalone startup or proof-of-concept project. It operates as an integral part of Hong Kong’s established clearing and settlement framework. Regulators have entrusted tokenized bond settlement to an entity directly linked to the HKMA. They have integrated digital securities into the same system that already processes conventional financial instruments.

This strategic move reshapes the tokenization story in three key ways:

-

Standardization replaces experimentation: Rather than relying on custom-built, one-off digital bond structures, issuance and settlement can now follow uniform regulatory rules and proven operational protocols.

-

Clear regulatory oversight: With supervision anchored directly under the central banking authority, legal and compliance uncertainty is significantly reduced.

-

Built-in scalability: Core market infrastructure is designed to handle institutional-scale volumes, not just small-scale trials or limited pilots.

Tokenization is no longer an add-on or side project. It is becoming embedded in the core plumbing of Hong Kong’s financial system.

Did you know? The concept of tokenized bonds builds on the broader idea of tokenizing real-world assets (RWAs). Trillions of dollars’ worth of traditional financial assets, such as bonds, real estate and funds, could eventually move onto blockchain-based infrastructure.

Government issuance: Already scaling

Hong Kong’s tokenized bond program is already demonstrating meaningful scale. Rather than building infrastructure in anticipation of future demand, Hong Kong is responding to existing market interest.

The government’s third tokenized bond issuance, completed in late 2025, reached a record size of HK$10 billion, approximately US$1.28 billion to US$1.3 billion, marking the world’s largest digital bond offering to date. This followed earlier digital bond issuances that also attracted strong investor demand. Authorities have now pledged to make tokenized bond issuance a regular practice rather than relying on occasional pilots.

This steady approach delivers several key benefits:

-

Builds investor comfort and familiarity with tokenized products

-

Draws participation from conventional asset managers

-

Reinforces that tokenization has strong official policy support, moving it beyond experimental status

Consistent and predictable issuance is essential to developing deeper, more liquid markets.

Beyond bonds: Building a digital asset ecosystem

Hong Kong’s ambitions extend well beyond tokenized bonds. The 2026-27 budget outlines additional regulatory steps to foster a broader digital asset ecosystem.

Stablecoin licensing regime

The HKMA is moving toward issuing its inaugural set of licenses for fiat-referenced stablecoins, with the first approvals expected in early 2026.

The licensing assessments emphasize:

-

The strength and quality of asset reserves

-

Robust risk management practices

-

Effective anti-money laundering (AML) and compliance controls

-

Well-defined, legitimate use cases

Stablecoins are not inherently tied to bond settlement. However, the introduction of regulated digital fiat equivalents could enable compliant and efficient settlement mechanisms for tokenized securities and other digital assets.

Did you know? The first blockchain bond issued by a multilateral institution was launched by the World Bank in 2018. Called “Bond-i” (Blockchain Operated New Debt Instrument), it used distributed ledger technology to manage bond issuance and settlement.

Licensing for digital asset dealers and custodians

Hong Kong is advancing its regulatory framework by introducing dedicated licensing regimes for key digital asset service providers.

The government plans to table legislation in 2026 establishing licensing requirements for:

-

digital asset dealing platforms, including over-the-counter (OTC) brokers, block traders, and other intermediaries involved in buying, selling, or exchanging virtual assets

-

custodian service providers focused on safeguarding private keys, segregating client assets, and ensuring strong security and operational controls

These measures will bring a broader range of participants under formal supervision. Dealers will face standards comparable to those applied to conventional securities firms, while custodians will be subject to stringent requirements for asset protection and key management.

By covering issuance, trading, custody, and reporting activities, the regime creates a fully supervised ecosystem for tokenized bond markets and other digital securities, enhancing investor protection and market integrity.

Alignment with global tax transparency standards

To reinforce its commitment to international compliance, Hong Kong is amending the Inland Revenue Ordinance to adopt the Organisation for Economic Co-operation and Development’s (OECD) Crypto-Asset Reporting Framework (CARF).

The implementation will apply to reporting by crypto-asset service providers (CASPs), starting in 2027. Information exchanges would begin in 2028, enabling the automatic exchange of tax-related data on crypto transactions with partner jurisdictions.

The move underscores a clear policy stance. Hong Kong’s tokenized and digital asset markets are being designed to be fully interoperable, transparent, and aligned with global standards. These are essential prerequisites for attracting and retaining institutional capital on a sustainable basis.

Did you know? Traditional bond settlement often takes two business days (T+2) in many markets. Tokenized bonds could potentially enable near-instant settlement, reducing counterparty risk and freeing up capital more quickly.

The liquidity layer: Building deeper regulated crypto markets

In early 2026, the Hong Kong Securities and Futures Commission (SFC) issued new guidance enabling licensed virtual asset brokers to provide margin financing for digital assets. Initially, the framework focused on Bitcoin (BTC) and Ether (ETH) collateral, with safeguards for creditworthy clients. The SFC also published a high-level framework allowing licensed virtual asset trading platforms (VATPs) to offer leveraged perpetual contracts.

These developments significantly enhance market liquidity in a controlled manner while preserving strong investor protections and risk management standards. They form part of a multilayered strategy to:

-

Broaden the scope of regulated digital asset markets

-

Uphold institutional-grade guardrails and compliance

-

More seamlessly bridge digital and traditional finance

Tokenized bonds are not standalone experiments. They sit within a comprehensive, integrated digital financial architecture designed for scale and sustainability.

How tokenized bond infrastructure operates in practice

Tokenized bond infrastructure combines several interconnected layers built on blockchain or distributed ledger technology:

-

Issuance: The issuer originates the bond as a digital token directly on a permissioned or regulated ledger, embedding coupon terms, maturity and covenants into smart contracts or digital records.

-

Primary allocation: Subscriptions and allocations occur through regulated intermediaries, such as banks, brokers or platforms, ensuring Know Your Customer (KYC) and AML compliance and orderly distribution to qualified investors.

-

Settlement and custody: True delivery-versus-payment (DvP) is achieved through integrated systems managed by recognized market infrastructure providers, including central securities depositories or clearing houses adapted for tokenization. Custody is handled by licensed providers with segregated assets and secure key management.

-

Post-trade lifecycle: Ongoing events, such as coupon or interest payments, principal redemptions at maturity, and the handling of corporate actions, are automated through programmable logic. This reduces manual intervention, settlement risk and operational costs.

The critical distinction between early pilots and true infrastructure lies in repeatability, institutional integration, and scale. Mature infrastructure enables frequent, large-volume issuances while interfacing smoothly with existing clearing, settlement, custody and reporting systems. This creates the foundation for liquid, efficient secondary markets.

Why this matters for global markets

Hong Kong’s strategy reflects deliberate, long-term positioning in the changing financial sector.

By integrating tokenized bond issuance and settlement into infrastructure closely aligned with the central bank, and by fostering connectivity with regional platforms and counterparties, Hong Kong is working to:

-

Solidify its status as Asia’s leading regulated digital asset and tokenized securities hub

-

Channel meaningful cross-border institutional capital flows into and through the city

-

Offer institutional investors a compliant, scalable and well-regulated tokenization ecosystem

Hong Kong is competing on regulated reliability, predictable rule-making and institutional-grade infrastructure. These factors matter significantly to large asset managers, banks and sovereign wealth funds.

Prevailing risks and challenges

Implementing ambitious infrastructure does not automatically eliminate structural challenges. Several significant hurdles remain:

-

Achieving genuine interoperability across different tokenization platforms, protocols and ledgers

-

Securing legal and regulatory harmonization with other major jurisdictions to enable smooth cross-border issuance, trading and settlement

-

Keeping AML, KYC, sanctions and broader compliance frameworks aligned with the rapid pace of technological change

-

Avoiding liquidity fragmentation, where trading volumes are split inefficiently across siloed digital systems, undermining market depth

Building the digital financial rails is only the first phase. Sustained market adoption, active secondary trading, broad institutional participation and organic liquidity growth will determine whether Hong Kong’s vision translates into lasting global relevance.

Cointelegraph maintains full editorial independence. Guides are produced without influence from advertisers, partners or commercial relationships. Content published in Guides does not constitute financial, legal or investment advice. Readers should conduct their own research and consult qualified professionals where appropriate.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Exolix gains traction in 2026 as developers seek fast, reliable crypto exchange API solutions.

As the crypto ecosystem grows, infrastructure is now an essential part of every product, from crypto wallets and exchanges to fintech applications and web3 projects. Most products rely on APIs to support key functionalities such as price feeds, access to liquidity, and transaction execution. As such, finding the best crypto API is no longer a choice but a necessity.

However, the best crypto API remains a concern for many projects and teams. The best crypto API depends on a few key factors: ease of integration, reliability, and the speed at which the product can be deployed without having to build complex infrastructure from scratch.

Exolix is emerging as one of the best crypto exchange API providers in the market in 2026 by addressing the key requirements of the crypto ecosystem. It offers the best crypto API due to its fast deployment capabilities, which provide developers with the best way to integrate crypto swap functionalities into their products. As such, the Exolix crypto exchange API is the best choice for teams seeking the best crypto API for startups.

What Is Exolix API?

Exolix API is a crypto infrastructure product that enables developers to add instant exchange capabilities to their applications. Instead of developing complicated exchange systems or dealing with the intricacies of working with multiple liquidity providers, developers can integrate with Exolix and allow users to exchange cryptocurrencies within the interface.

This makes Exolix API one of the best crypto exchange APIs, especially for projects that wish to add crypto-to-crypto exchange capabilities to their applications.

The API is also lightweight and easy to implement. Some of the key functionalities that can be integrated using the API are as follows:

- execution of crypto swaps across various assets

- real-time calculation of the rate

- tracking of the status of transactions

- cross exchange support

This simplicity also makes Exolix one of the best crypto APIs for startups, as the teams involved in the development of the startups need to launch the projects as soon as possible without having to spend much time and resources on the development of the back end.

Another significant factor related to the API is the non-custodial nature of the API. This means that the users are in full control of the money during the exchange process, which is also in line with the current trend of moving towards more decentralized and user-friendly financial tools.

Why Exolix Is One of the Best Crypto API Providers in 2026

As the number of crypto infrastructure providers grows, the line between an excellent API and the best crypto API comes down to usability, reliability, and performance in the real world. Exolix, in 2026, stands out as an API that focuses on the practical needs of developers, ease of integration, execution, and support.

While some APIs are difficult to set up or require significant technical expertise, Exolix has been created to be simple to use, and this is just one reason it is often considered to be among the best crypto APIs, especially for startups and growing web3 products.

Easy API integration

One of the key advantages of Exolix is the ability of the developers to get started as quickly as possible. This is because the API is quite straightforward.

Developers can explore integration on the developers page.

The key advantages of integrating with Exolix are:

- Simple request and response structure

- Quick onboarding process

- No need to build exchange infrastructure

- Ability to integrate with xisting apps and wallets

This makes Exolix a strong contender for the best crypto exchange API, especially for development purposes.

24/7 Technical Support

Another key aspect in selecting the top API for crypto is reliable support. This is because, in the event of any problems related to swaps, rates, or integration, user experience is affected.

Exolix offers technical support around the clock, enabling teams to quickly address any problems, ensuring optimal performance.

This is especially useful for:

- Startups with small engineering teams

- Platforms with users in different time zones

- Platforms that need to be available 24/7

Integration and Revenue Opportunities

Exolix is constantly improving its API infrastructure to ensure ease of integration for wallets, apps, and crypto platforms to include non-custodial cross-chain swaps in their products. This API is flexible and simple to implement to ensure ease of integration for our partners.

Revenue Share Model

One of the main advantages of integrating with Exolix is our revenue share model. This model ensures our partners receive a share of revenue from swaps done on their platforms. This creates an additional revenue source for our partners.

This means our partners can:

- Monetize their current user base

- Create an additional revenue source

- Improve their products without adding operational overhead

Integration assistance for Developers

Apart from that, Exolix is also offering assistance during the integration process itself. This is going to help teams that may not have the best knowledge of the underlying crypto infrastructure.

The assistance that is going to be available during the integration process is as follows:

- Guidance on implementing the API

- Troubleshooting during the setup process

- Optimization hints for the best performance

- Assistance with edge cases during transactions

This is going to help Exolix become one of the best crypto APIs around.

Key use cases for Exolix API

The flexibility of Exolix makes it perfect for various crypto products. Whether it is developing a crypto wallet, exchange, or any other related application, the right crypto API can help to achieve new heights without adding complexity to the development process.

Exolix is all about simplicity and compatibility, and this is why it is used in various applications that demand timely development and user experience. This is why it is considered one of the best crypto APIs for startups.

Wallet Integration

Crypto wallets are one of the most common applications of the Exolix API. The swap feature is integrated into the user interface of the wallet, allowing the user to swap assets without exiting the application. This is a great way to retain the user and provide a richer experience.

Exchange and trading platforms

For projects that need instant swaps without the hassle of building their own trading engine, Exolix is available as a backend solution. This is the reason Exolix is considered one of the best crypto exchange APIs available today.

Web3 and DeFi applications

Decentralized applications may utilize Exolix, which offers the possibility of cross-chain swaps as well as the moving of assets between different chains.

Startup products and MVPs

For early-stage teams, the key is speed, and Exolix helps teams launch their products quickly by not requiring them to develop from scratch.

This makes Exolix an excellent choice among the best crypto APIs for startups, especially when developing:

- MVPs

- Early product tests

- Quick iteration cycles

With the ability to accommodate multiple use cases with a single integration, Exolix offers a scalable base for various types of crypto products at different stages of development.

FAQ

What is Exolix API?

Exolix API is a product that serves as a solution for building a cryptocurrency infrastructure that can facilitate instant cryptocurrency exchange. The API can be used by developers to add instant cryptocurrency exchange capabilities to their platforms.

Why is Exolix considered one of the best crypto APIs?

Exolix API is regarded as one of the best free crypto APIs because it is simple, has a quick onboarding process, and is reliable. The API has a feature that allows users to make cross-chain swaps, has clear documentation, and is available 24/7. These features make it a feasible choice for both new and old cryptocurrency products.

Is Exolix suitable for startups?

Yes, Exolix is an excellent choice in the list of the top-rated APIs in the cryptocurrency industry. It is an excellent choice for startups that want to launch their project without the need to build their exchange infrastructure. This way, the startup can save time and money while still providing the feature of cryptocurrency swaps.

Does Exolix API require complex integration?

No, one of the biggest advantages of using Exolix is that it is easy to integrate. The API is easy to use and has a simple structure. Moreover, there is support available during the integration process. A developer can easily start using the API with the documentation provided on the official website.

What can you build with Exolix API?

The Exolix API is an excellent choice for developers who want to create different cryptocurrency-related products such as wallets, exchange interfaces, and Web 3 applications. It is also used to add instant swap functionality, which makes it one of the top-rated cryptocurrency exchange API solutions.

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

The crypto market will welcome tokens worth more than $643 million in the first week of April 2025. Major projects, including Hyperliquid (HYPE), Sui (SUI), and Ethena (ENA) will release significant new token supplies.

These unlocks could introduce market volatility and influence short-term price movements. So, here’s a breakdown of what to watch.

1. Hyperliquid (HYPE)

- Unlock Date: April 6

- Number of Tokens to be Unlocked: 9.92 million HYPE

- Released Supply: 415.33 million HYPE

- Total Supply: 1 billion HYPE

Hyperliquid is a leading decentralized perpetual futures exchange built on its own Layer-1 blockchain. It offers high-performance trading with low latency, on-chain order books, and sub-second transaction finality.

On April 6, the team will unlock 9.92 million HYPE worth $375.84 million. The tokens account for 2.66% of the released supply.

Hyperliquid will direct all unlocked altcoins to core contributors. However, Tokenomist pointed out that HYPE has historically claimed far fewer tokens than its projected unlock amounts.

2. Sui (SUI)

- Unlock Date: April 1

- Number of Tokens to be Unlocked: 42.94 million SUI

- Released Supply: 3.9 billion SUI

- Total Supply: 10 billion SUI

Sui is a high-performance Layer-1 blockchain. It utilizes the Move programming language to enable scalable, secure, and efficient decentralized applications (dApps).

Moreover, the network focuses on parallel execution for high throughput, making it suitable for gaming, decentralized finance (DeFi), and Web3 ecosystems.

On April 1, Sui will unlock 42.94 million altcoins as part of its monthly schedule. This stack represents 1.10% of the released supply. Furthermore, it is worth approximately $36.36 million.

Of the unlocked supply, 19.32 million SUI will go to Series B investors. Community reserve and early contributors will get 12.63 million and 8.93 million SUI, respectively. Lastly, Mysten Labs will receive 2.07 million altcoins.

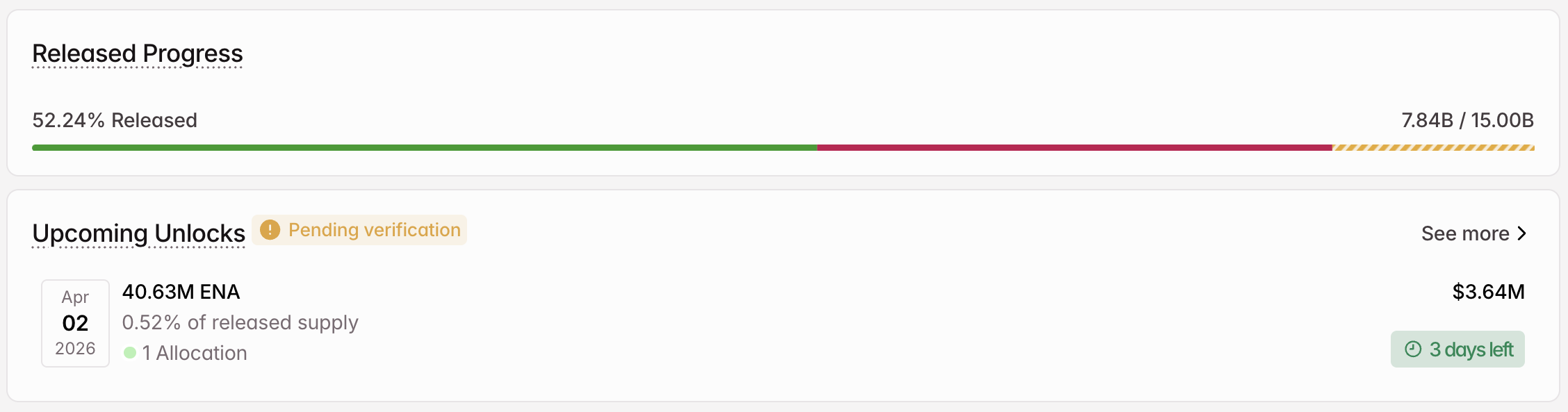

3. Ethena (ENA)

- Unlock Date: April 2

- Number of Tokens to be Unlocked: 40.63 million ENA

- Released Supply: 7.84 billion ENA

- Total Supply: 15 billion ENA

Ethena is a synthetic dollar protocol built on Ethereum (ETH). The protocol’s flagship product is USDe, a synthetic dollar stablecoin. Furthermore, ENA is the protocol’s governance token.

The team will release 40.63 million ENA tokens on April 2. The tokens, worth $3.64 million, account for 0.52% of the released supply.

Ethena will award the entire unlocked supply to the Foundation. In addition to these three, Gunz (GUN), EigenCloud (EIGEN), and Opinion (OPN) will also experience new supply entering the market in the first week of April.

The post 3 Token Unlocks to Watch in the First Week of April 2026 appeared first on BeInCrypto.

17 Floral Spring Tops That Look Boutique-Worthy — All Under $20

Escape Tsunami For BRAINROTS, in Minecraft!

Chopping down areas of tropical rainforest is causing rising temperatures linked to thousands of deaths

-

NewsBeat5 days ago

NewsBeat5 days agoManchester United reach agreement with Casemiro over contract clause amid transfer speculation

-

News Videos5 days ago

News Videos5 days agoParliament publishes latest register of MPs’ financial interests

-

NewsBeat3 days ago

NewsBeat3 days agoThe Story hosts event on Durham’s historic registers

-

Business4 days ago

Business4 days agoInstagram, YouTube Found Responsible for Teen’s Mental Health Struggle in Historic Ruling

-

NewsBeat5 days ago

NewsBeat5 days agoTesco is selling new Cadbury Dairy Milk bar and people can’t wait to try it

-

Tech7 days ago

Tech7 days agoSamsung will soon let you control smart home devices from your car’s dashboard

-

Entertainment2 days ago

Entertainment2 days agoLana Del Rey Celebrates Her Husband’s 51st Birthday In New Post

-

Fashion6 days ago

Fashion6 days agoDoes It Matter What You Wear When You’re Laid Off and Looking?

-

Business6 days ago

Business6 days agoMore women enter wealth management, but few in advisory roles: study

-

NewsBeat7 days ago

NewsBeat7 days agoColombian military plane with 110 soldiers onboard crashes following takeoff

-

Politics7 days ago

Politics7 days agoHow Media Platforms Balance Performance and Accessibility in Image Delivery

-

NewsBeat6 days ago

NewsBeat6 days agoNASA Artemis II Astronauts enter 14-Day quarantine as moon rocket reaches launchpad

-

NewsBeat6 days ago

NewsBeat6 days agoEntrepreneurs Forum survey reveals optimism in North East

-

Business6 days ago

Business6 days agoLate-paying firms face multimillion-pound fines under new crackdown

-

Tech4 days ago

Tech4 days agoIntercom’s new post-trained Fin Apex 1.0 beats GPT-5.4 and Claude Sonnet 4.6 at customer service resolutions

-

Sports5 days ago

Sports5 days agoFantasy Baseball Week 1 Preview: Top sleeper hitters for both five- and 12-day period led by Munetaka Murakami

-

Tech5 days ago

Tech5 days agoUS FCC Prohibits Approval Of New Foreign-Made Consumer Routers

-

Crypto World6 days ago

Crypto World6 days agoBTC gives up $70,000 level as markets mull higher interest rates

-

Tech6 days ago

Tech6 days agoEmbedding compliance in AI adoption

-

Fashion6 days ago

Fashion6 days agoCoffee Break: Korean Skincare Set

You must be logged in to post a comment Login