Crypto World

Bitcoin Trader Sees Coinbase, Kimchi Premium Sparking New BTC Price Uptrend

Bitcoin (BTC) has fulfilled two of three key conditions to spark the next BTC price “rally,” new analysis says.

Key points:

- Bitcoin whales on Hyperliquid and Bitfinex are already pointing to the beginning of a BTC price uptrend, according to the latest findings.

- Bitcoin markets now need demand to return in the form of the Coinbase and Kimchi Premium.

- Other preconditions for a bear market bottom are also in the process of forming.

Bitcoin price comeback hinges on US, Korea demand

Bitcoin whale traders are laying the foundations for BTC price relief, even as BTC/USD plumbs four-month lows.

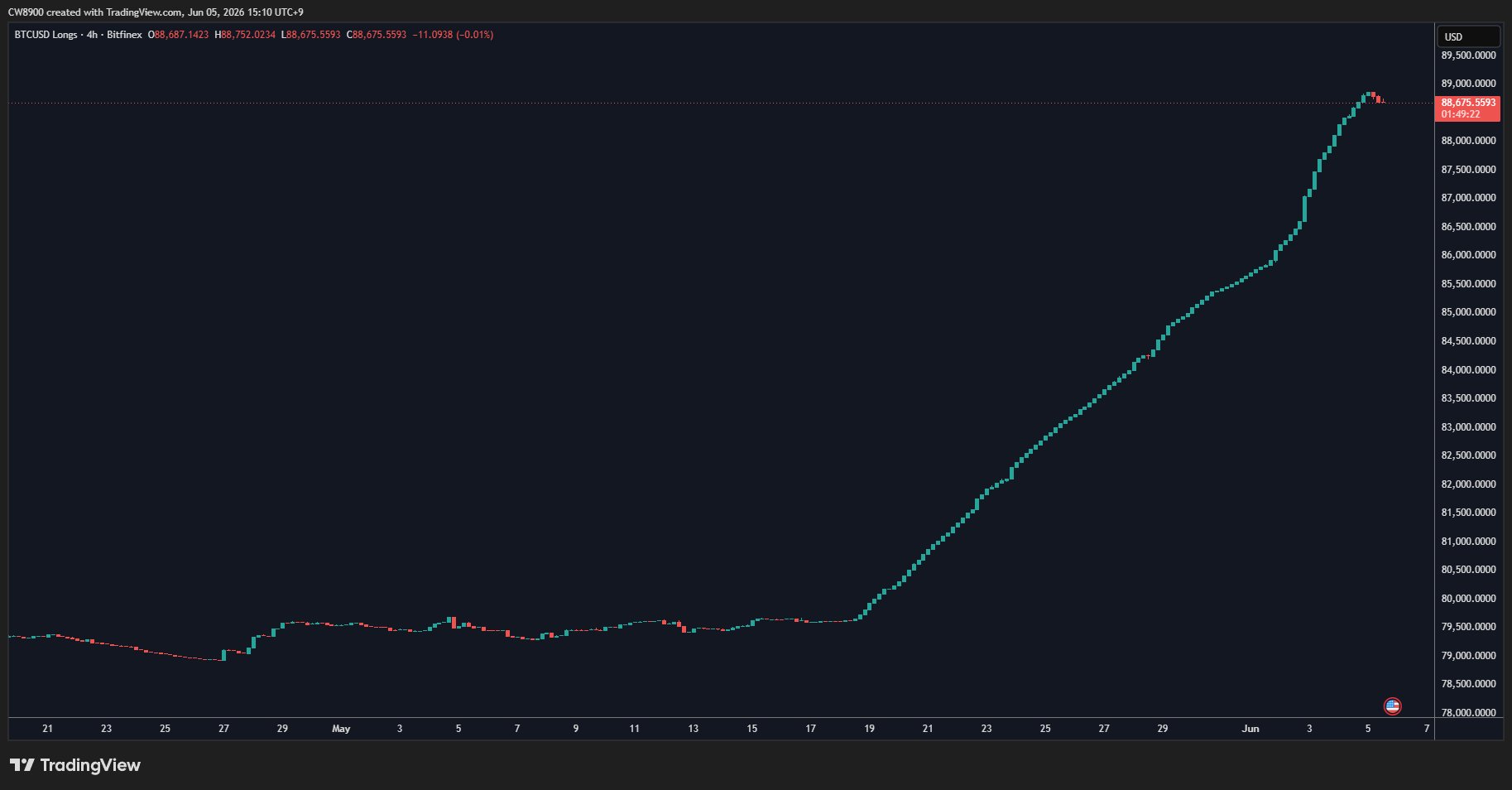

In an X post on Friday, trader CW confirmed that Bitcoin whales on both Hyperliquid and Bitfinex are signaling a market rebound.

BTC/USD long positions on Bitfinex. Source: CW/X

CW notes that Hyperliquid whales have adopted a “bullish stance” on the market, while on Bitfinex, long positions have tailed off. The latter is a classic sign that an uptrend is due next.

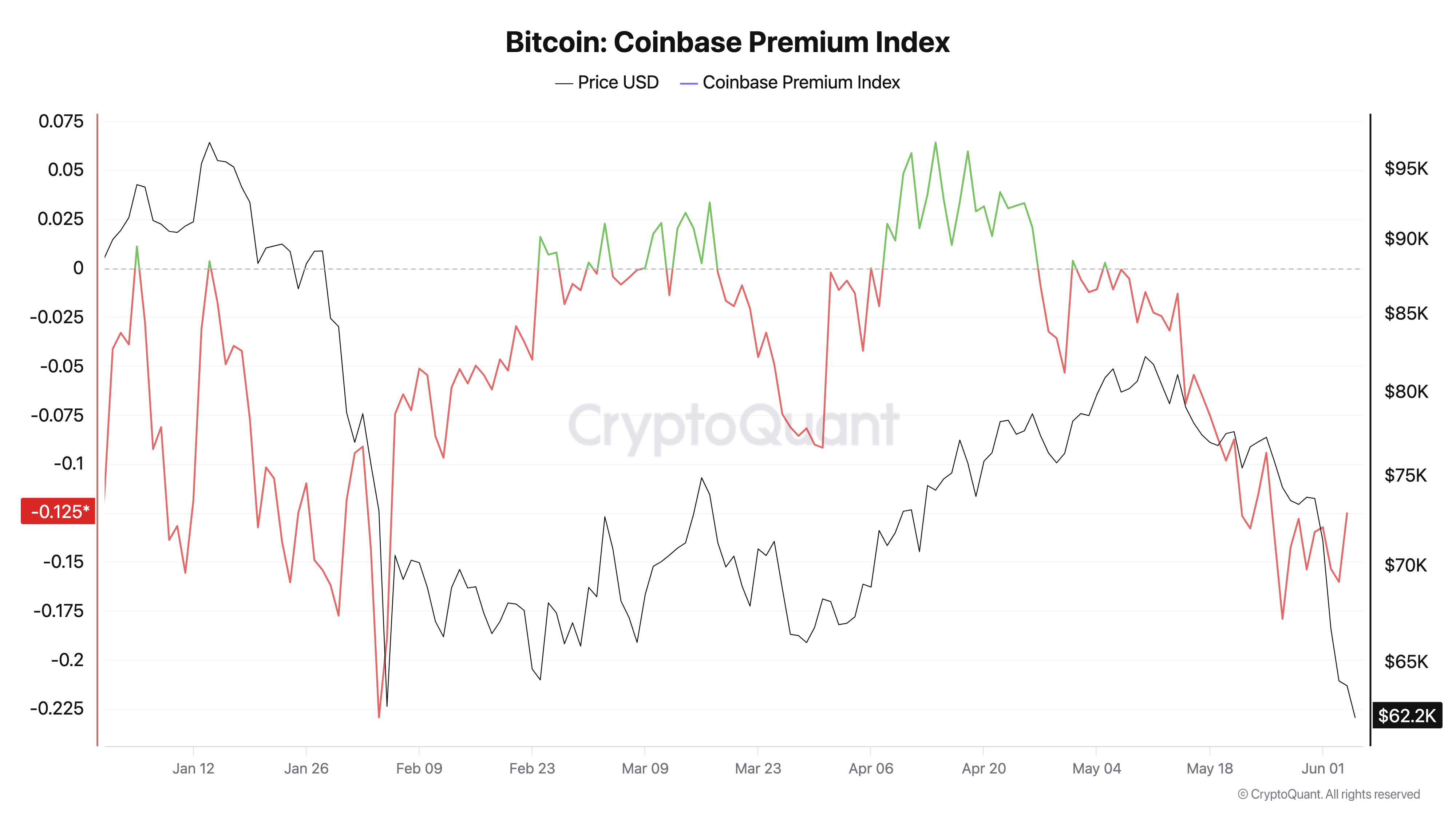

“What remains is for the Kimchi Premium and Coinbase Premium to turn positive,” he commented.

The Coinbase Premium is the difference in price between Coinbase’s and Binance’s BTC/USDT pairs and has been mostly negative in 2026.

Bitcoin Coinbase Premium Index. Source: CryptoQuant

A negative premium reflects weak US demand, while the Kimchi Premium monitors the South Korean exchange sector.

Once demand returns across the board, Bitcoin has a better chance of reentering a sustainable uptrend.

CW acknowledged that the Kimchi Premium has already “decreased significantly” versus earlier in the week.

Bitcoin starts its latest “bottoming out” phase

As Cointelegraph reported, consensus overall favors a macro bottoming phase playing out for BTC/USD next.

Related: Trump says Iran will ‘work out well’: Five things to know in Bitcoin this week

The week has seen the pair touch a key bear-market trend line in the form of its 200-week simple moving average (SMA) — another essential ingredient in a bottom formation.

“Bitcoin has only just started deviating below the 200-week SMA,” trader and analyst Rekt Capital emphasized to X followers on Friday.

“The significance of this is that historical Bear Market Bottoming out formations have started to develop via such deviations.”

BTC/USD one-week chart with 200SMA. Source: Rekt Capital/X

Earlier, trader Leviathan described BTC price action as copying the 2022 bear market “almost perfectly.”

Bitcoin and Ethereum trading activity has fallen to multi-quarter lows on Hyperliquid, while volume in equity-linked and pre-IPO perpetual contracts has climbed sharply.

Summary

- Bitcoin and Ethereum perpetual futures volumes on Hyperliquid have fallen to multi-quarter lows as traders increasingly turn to equity and commodity-linked contracts, according to Block Scholes.

- Pre IPO perpetual trading volume has climbed above $50 million per day from less than $5 million, with SpaceX-linked contracts leading activity.

- Block Scholes analyst Thahbib Rahman said speculative interest remains strong in markets such as stock index perps, commodities, and HYPE despite weaker sentiment around Bitcoin and Ethereum.

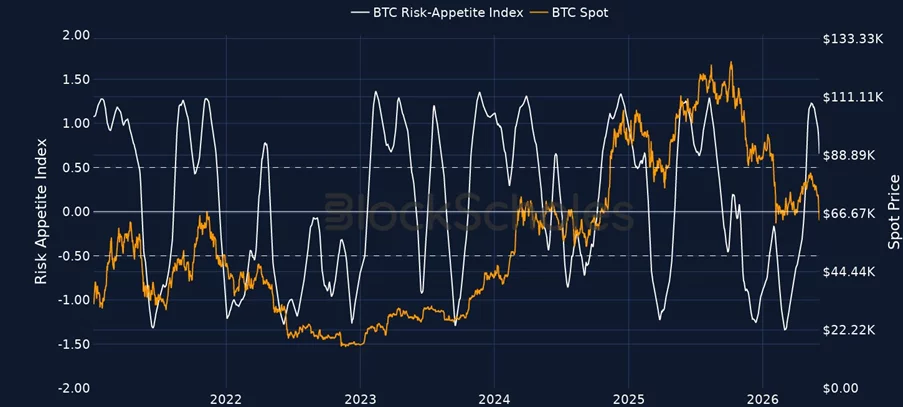

According to a June 5 report from Block Scholes shared with crypto.news, risk sentiment around the two largest cryptocurrencies has continued to weaken, even as speculative demand remains active in other parts of the market.

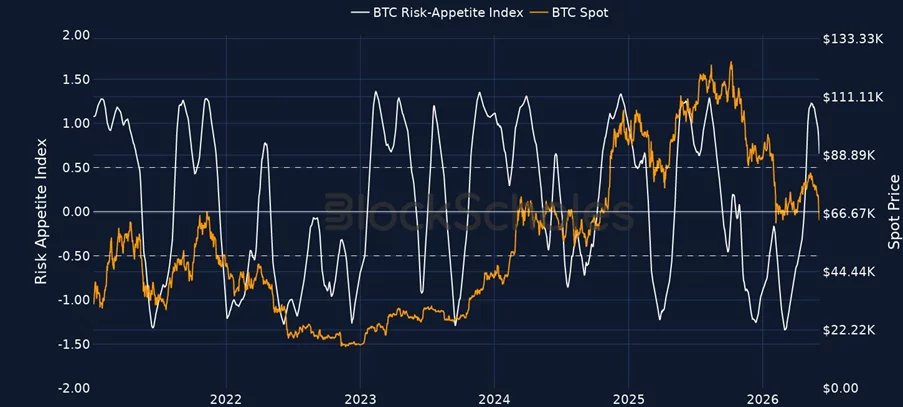

The research firm pointed to its in-house Bitcoin and Ethereum Risk Appetite Indexes, which have moved lower over the past week alongside declines in both assets.

Recent weakness in crypto majors has coincided with several market developments. Block Scholes noted that Strategy sold $2.5 million worth of Bitcoin from its holdings, a move that came after years of public commitment from Executive Chairman Michael Saylor to continue accumulating the asset.

The report also highlighted the longest streak of outflows from U.S. spot Bitcoin ETFs since their launch.

Rather than viewing Bitcoin’s drop toward the low $60,000 region as a sign of fading interest across the entire digital asset market, Block Scholes argued that trading activity has become concentrated in a different set of instruments.

Traders turn to stock and commodity-linked perpetuals

Data from Hyperliquid shows that daily Bitcoin perpetual futures volume has remained near $2 billion, while Ethereum volumes have stayed around $600 million to $700 million, levels Block Scholes described as multi-quarter lows.

At the same time, activity tied to equity and commodity markets has expanded rapidly on the platform. According to Block Scholes, the three most actively traded non-crypto perpetual contracts on Hyperliquid are XYZ100, which tracks the Nasdaq-100, SP500, an S&P 500-linked product, and CL, a contract tied to WTI crude oil.

Combined daily volume across those three markets has reached approximately $1.3 billion, generating $27.1 billion in notional trading volume over the past month. Block Scholes said that total equals about 112% of Ethereum perpetual volume and roughly 38% of Bitcoin perpetual volume on the exchange during the same period.

The report said the development does not necessarily represent a dollar-for-dollar migration of capital from Bitcoin and Ethereum. Instead, the report argued that trader attention and speculative activity that previously supported crypto majors are increasingly being directed toward alternative markets available through the same trading venue.

Pre-IPO contracts draw growing interest

Beyond stock index and commodity products, Block Scholes identified pre-IPO perpetual contracts as another area attracting crypto-native traders.

According to the report, the ratio of pre-IPO perpetual volume relative to Ethereum perpetual volume increased from roughly 0.1% to a peak near 3.0% in recent weeks. Daily trading volume in the segment has climbed from less than $5 million to more than $50 million, with contracts linked to SpaceX accounting for much of the increase.

Block Scholes said the rise has been abrupt and concentrated, with activity accelerating into late May and early June while Bitcoin and Ethereum volumes remained subdued.

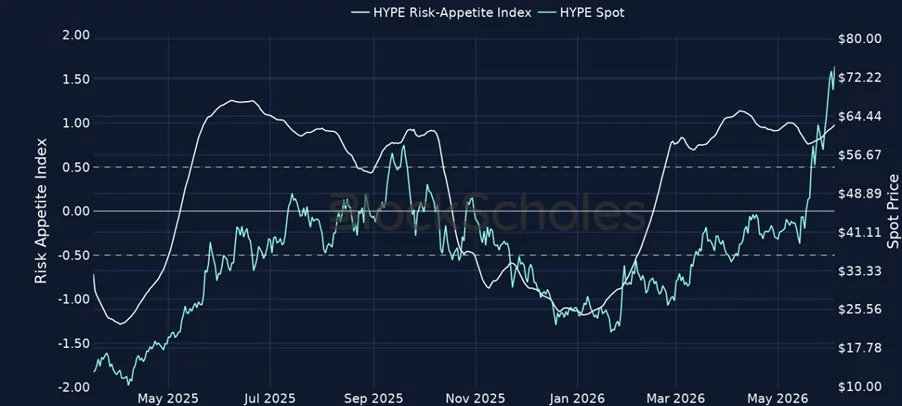

The firm’s risk appetite data also showed a divergence among digital assets. While sentiment tied to Bitcoin and Ethereum has weakened, Block Scholes reported that Hyperliquid’s HYPE token is one of the few major crypto assets where its risk appetite indicator continues to move higher.

HYPE risk appetite index. Source: block Scholes.

As previously reported by crypto.news, Binance Research recently published a report noting that capital has been flowing toward a concentrated group of U.S. equity sectors, including artificial intelligence infrastructure, semiconductor companies, defense contractors, energy firms, and commodities.

According to the report, strong performance in those sectors has historically reduced liquidity available to Bitcoin and other alternative assets.

Using the CBOE Dispersion Index as a measure of market concentration, Binance Research noted that the indicator recently reached 42, its third-highest reading on record. The firm argued that periods of concentrated equity leadership have often coincided with weakness in Bitcoin as investors direct funds toward a smaller group of high-performing themes.

On-chain investigator ZachXBT warned traders to avoid Rain Protocol after claiming that the prediction market project shows weak user traction, questionable wallet links, and possible on-chain price manipulation.

Summary

- ZachXBT warned traders to avoid Rain Protocol, citing low users, weak traction, and team concerns.

- His on-chain claims linked RAIN wallets to DOP, TOMI, Gems, and exchange deposits.

- ZachXBT cut Kraken’s rating over alleged listing failures tied to manipulated low-quality token markets.

ZachXBT questions Rain Protocol traction

ZachXBT described Rain Protocol as an $8.8 billion project and a top-15 crypto asset by market value. He said the prediction market has few users, limited product traction, no major backers, and a team with little public history in crypto.

The investigator told traders to avoid the project “at all costs.” His warning focused on the gap between RAIN’s reported valuation and its visible product activity.

Rain Protocol had already drawn market attention before the latest alert. Earlier reports said traders had questioned RAIN’s supply structure, liquidity setup, and project links after its fast rise toward a multibillion-dollar valuation.

Wallet trails point to DOP and TOMI

ZachXBT said his on-chain review found wallet links between RAIN team addresses and failed crypto projects, including Data Ownership Protocol and TOMI. He pointed to funding trails involving the Gems hot wallet and several centralized exchange deposit addresses.

He cited two dust transfers sent to the same address on Oct. 14, 2025. One came from a wallet he linked to the RAIN deployer. Another came from a wallet he connected to the TOMI team multisig and a centralized exchange deposit address.

ZachXBT also said the recipient wallet later received funds from another address funded by a DOP multisig. In a separate trail, he said another wallet moved funds to an address that later used the same exchange deposit address as the DOP deployer.

The claims remain allegations unless the project, exchanges, or regulators confirm them. Rain Protocol had not issued a public response in the material reviewed.

Price activity and valuation draw scrutiny

ZachXBT also alleged that RAIN’s price appears manipulated on-chain. He said addresses linked to the deployer used Uniswap V3 liquidity pools while routing spot transfers through the Gems hot wallet.

He also questioned Enlivex, the Nasdaq-listed company tied to RAIN’s digital asset treasury plan. Enlivex announced a $212 million treasury strategy in November 2025, but ZachXBT argued that RAIN does not compare with prediction market platforms such as Kalshi or Polymarket.

DefiLlama data cited in his post showed Rain Protocol with $27.2 million locked on Arbitrum. ZachXBT said the full amount was held in RAIN’s own illiquid token, while the protocol generated about $1 million in annual fees.

Kraken rating cut adds exchange angle

ZachXBT also lowered Kraken from S-tier to B-tier. He cited what he called a “lack of due diligence” before listing tokens he described as low quality or manipulated, including M, RAIN, RIVER, and RAVE.

He also criticized Kraken’s handling of its recent security breach disclosure. He said the exchange did not mention compensation for affected users, while rivals such as Coinbase and Bybit had prioritized customer repayment after past incidents.

ZachXBT said he raised his bounty to as much as $100,000 for insiders who can provide documents or chat logs tied to alleged centralized exchange market manipulation schemes.

The latest Rain Protocol alert now sits within a broader debate over token listings, thin liquidity, market-maker activity, and retail risk. For now, traders are watching whether RAIN or Kraken respond to the claims with verifiable on-chain or operational details.

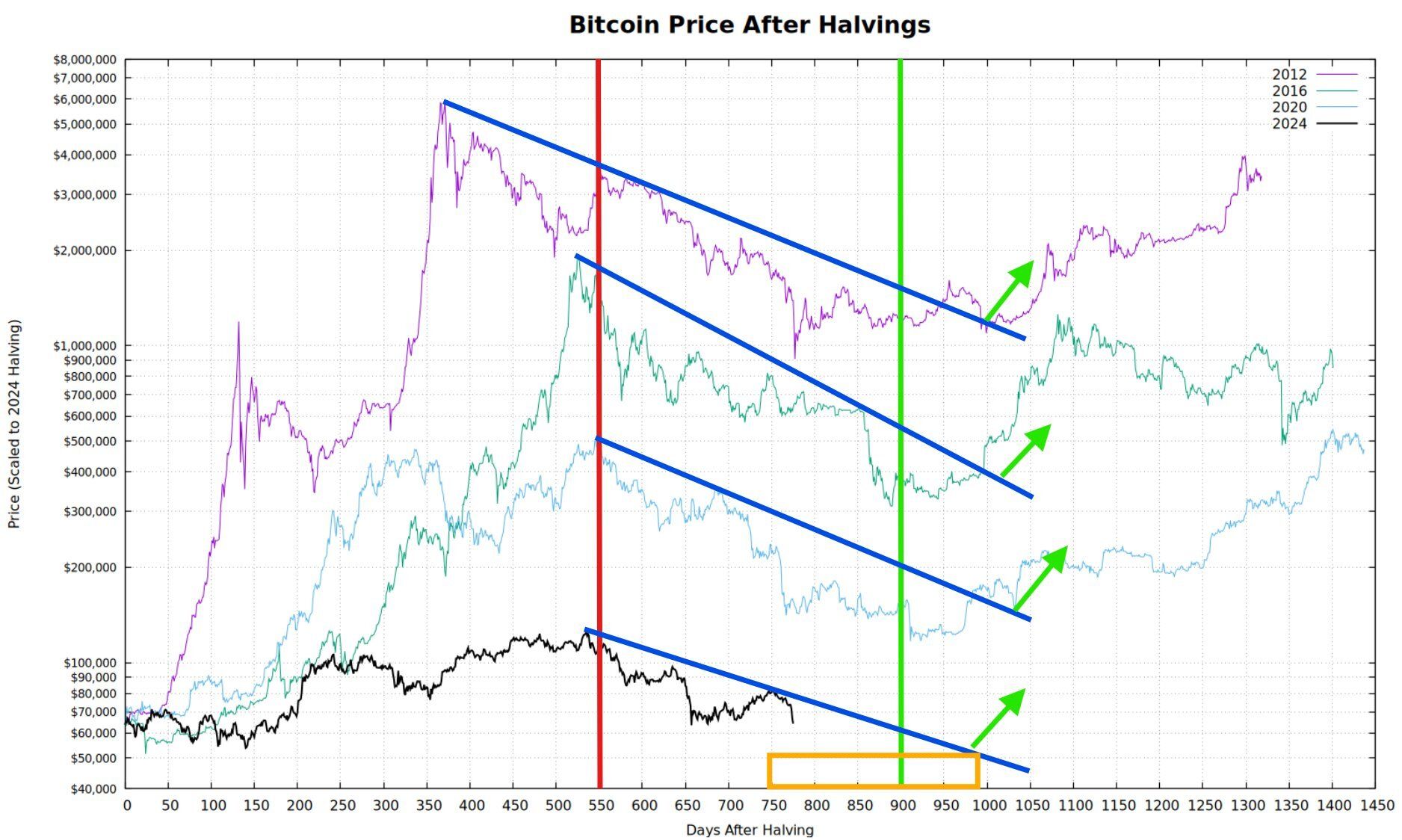

Bitcoin (BTC) trades near $60,000 after a 5% daily drop, leaving it about 50% below its record high. Three widely shared charts argue that the four-year cycle is intact and that the deeper cycle bottom still lies ahead.

The setup echoes recent BeInCrypto analysis, placing the cycle low in the fourth quarter of 2026. The new charts put a rough date and a price on that thesis.

Bitcoin’s Halving Clock Points to Day 900

The first chart, from analyst Jesse Olson, scales all four cycles since 2012 to the 2024 halving. Every prior cycle bottomed near day 900 after its halving.

The current cycle reached day 775 this week. That leaves about 125 days, or roughly four months, before the historical bottom window opens.

An orange band on the chart marks the projected low in the $40,000s. The black 2024 line has already rolled over, mirroring the post-top declines of 2012, 2016, and 2020. A prior BeInCrypto analysis reached the same read on the halving rhythm.

The Bitcoin Spiral Shows This Time Is Not Different

The second chart plots price on a spiral. Each loop represents one four-year cycle. The angle marks the position in the cycle, while the distance from the center marks the price.

Tops cluster in one arc, bottoms in another, and halvings in a third. The 2026 and 2027 markers fall inside the same arc that has framed every previous low.

The analyst captioned the chart “This time is different,” a nod to the institutional narratives. Its self-similar shape makes the opposite case.

Moving Averages Have Flipped to Resistance

The third chart stacks the levels Bitcoin must reclaim. The 21-week simple moving average sits at $75,100, the short-term holder cost basis at $77,000, and the 200-day average at $78,900.

Each acted as support during the bull phase. All three now sit overhead as resistance. Price below short-term holder cost basis means recent buyers, the holders most likely to sell, are underwater.

BTC has since slid toward the 50% drawdown line near $63,000. The newsletter behind the chart framed the grind as a slow, time-based capitulation rather than one violent flush.

The Cycle Timing Lines Up With October

The charts match a recent BeInCrypto report on analyst Benjamin Cowen. He notes Bitcoin topped on day 1,162 of the cycle, within a week of the prior two peaks at day 1,059 and day 1,168.

“Bitcoin topped within one week of when it historically tops, despite the narratives for calling the four-year cycle dead.”

Cowen places his base case at low in October 2026. That date sits about 125 days out, the same window Olson’s day 900 count produces.

Where the Bull Case Could Break the Pattern

The thesis is not guaranteed. Spot ETFs, corporate treasury demand, and a sovereign reserve narrative have pulled new money into Bitcoin at a scale earlier cycles never saw.

Some analysts argue this institutional bid could stretch or flatten the cycle rather than repeat it. A weekly close back above the $78,900 average would weaken the bearish read.

For now, the burden of proof sits with the bulls. Until Bitcoin reclaims those overhead levels, the path of least resistance points lower.

Bitcoin Price Outlook

Three independent methods, a halving day count, a cyclical spiral, and price structure, point to the same place. Each suggests Bitcoin has not yet found its cycle bottom.

A drop into the $40,000s would align with the orange target band and the on-chain floor. The 50% drawdown near $63,000 is the first marker; deeper levels are open if it breaks.

The likely window centers on the fourth quarter of 2026, near October. A weekly reclaim of $79,000 would be the first real signal that the pattern has finally broken.

The post Bitcoin Has 125 Days Until the Real Bottom, Charts Warn appeared first on BeInCrypto.

Kraken is broadening access to SpaceX’s upcoming IPO by enabling participation through its tokenized equities platform, xStocks. The exchange announced that SpaceX will be the first public offering available via IPO Access, a feature that lets eligible users acquire tokenized shares before the actual market open.

Under the program, investors can apply for IPO access through the Kraken mobile app. The offering is not accessible via Kraken Pro or the desktop platform, and eligibility is limited by region and regulatory constraints. Kraken notes that IPO Access is available across the European Economic Area and more than 110 international markets, but participation is unavailable in the United States, Canada, Australia, and the United Kingdom due to local rules.

Investors who receive an allocation will be issued SPCXx, a tokenized representation of SpaceX equity that is backed 1:1 by the underlying shares. The tokens are tradable 24/7 on Kraken and other participating xStocks platforms, enabling around-the-clock liquidity for a portion of the traditional equity lifecycle.

Kraken’s move underscores a broader push to bridge crypto infrastructure with traditional capital markets, offering a familiar stock-like instrument in a programmable, on-chain format. The company has previously highlighted that tokenized equities can give a wider audience access to high-profile listings and provide new trading modalities that operate beyond regular stock market hours.

In related context, prior coverage has highlighted that xStocks has already seen significant on-chain activity, with volumes and wallet activity illustrating growing interest in tokenized equities. This latest SpaceX IPO access case adds another high-profile asset to the roster of tokenized offerings on crypto-native platforms.

SpaceX targets a historic IPO debut

SpaceX is widely expected to begin public trading on June 12, marking a milestone for a privately held company that has grown into a major force in aerospace and satellite communications. Bloomberg, citing demand dynamics around the offering, reports that demand has already outstripped the number of shares available, with SpaceX seeking roughly $75 billion in proceeds and a valuation of at least $1.8 trillion. If reached, that would position SpaceX’s IPO as the largest ever, surpassing the previous record set by Saudi Aramco in 2019.

The growth story driving SpaceX’s valuation remains closely tied to Starlink, its satellite internet business, which has become a meaningful revenue stream and profitability driver for the company. At the same time, SpaceX’s launch and exploration ventures are capital-intensive and continue to entail substantial costs, raising questions about how early investors will appraise the business in a public market setting.

News of the anticipated mega-IPO has drawn attention to how investors value private companies as they transition to public markets, and how tokenized representations might influence price discovery, liquidity, and access. The SpaceX filing and the ensuing market reaction will be watched closely by practitioners and policymakers alike as they assess the implications for tokenized equity formats and cross-border trading.

For readers tracking the broader space, SpaceX’s on-chain disclosures and asset mix have already been a focal point of discussions about crypto-enabled capital markets. The trajectory of this IPO, and the way tokenized instruments perform in the weeks after listing, could shape how exchanges approach future cross-asset tokenization and whether similar models gain traction among other high-profile offerings.

Source: Kraken

Related: Kraken’s xStocks tops $25B in tokenized-equities volume with thousands on-chain holders

What tokenized equity means for crypto markets

The SpaceX IPO through xStocks illustrates a notable convergence: established public offerings can be mirrored as on-chain tokens that are tradable around the clock. For traders and investors, the arrangement potentially unlocks new avenues for liquidity, hedging strategies, and exposure to marquee names without traditional stock-market hours constraints. For issuers, tokenized access expands the potential investor base beyond geographic and logistical boundaries that often constrain classic IPOs.

From a risk-management perspective, tokenized equities introduce considerations around custody, settlement, and regulatory alignment across jurisdictions. While the SPCXx token is anchored 1:1 to SpaceX shares, the on-chain environment introduces new layers of operational risk and governance that market participants will watch closely as more companies explore tokenized offerings. The ongoing regulatory dialogue around tokenized assets will also influence how quickly and broadly these products scale in traditional markets.

For investors, the SpaceX case offers a practical glimpse into how crypto-native platforms are integrating with real-world capital markets. The use of a tokenized instrument tied to a well-known private company as it transitions to the public market could serve as a blueprint for future tie-ins between crypto infrastructure and mainstream equity markets. As with any IPO, due diligence remains essential: investors should assess not only the company’s business trajectory but also how much bandwidth tokenized formats have to deliver reliable, timely access to allocations and post-listing trading liquidity.

As the IPO unfolds and more details emerge about allocations, pricing, and secondary-market activity for SPCXx, market participants will be weighing how tokenized formats compare with traditional post-IPO liquidity and whether the added accessibility translates into meaningful long-term value capture for investors.

Investors should monitor the next steps for SpaceX’s public debut, including allocation outcomes and how the tokenized structure performs in live trading. The evolving regulatory framework around tokenized assets will likewise shape how quickly such offerings expand and how broadly they are accepted by retail and institutional participants alike.

What remains uncertain is how pricing will align between the on-chain representation and the actual SpaceX equity on public markets, once trading begins. If demand remains robust and the tokenized vehicle gains deeper adoption, SpaceX’s IPO could become a defining moment for tokenized equity infrastructure and the broader integration of crypto platforms with traditional capital markets.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Investors assess early-stage crypto opportunities as DOGEBALL gains attention alongside lessons from past launches.

Summary

- Investors continue searching for early-stage blockchain projects, hoping to capture growth before major exchange listings and broader market adoption.

- DOGEBALL positions itself as a Layer-2 ecosystem combining gaming and payments, with a focus on low-cost transactions and crypto-to-fiat settlement tools.

- Supporters argue the project’s DOGEPAY infrastructure and cross-border payment capabilities help differentiate it from purely speculative crypto offerings.

Missing out on early-stage blockchain opportunities is one of the most common regrets in the digital asset space. The investors who achieve life-changing returns are rarely the ones buying assets after major exchange listings. Instead, they are the analytical buyers who secure allocations when utility projects are still in their infancy.

This article analyzes a massive market shift where transactional utility is intersecting with high-growth community-driven ecosystems. This guide evaluates the performance dynamics of historic launches like Internet Computer (ICP) and provides an evidence-based breakdown of why the ongoing DOGEBALL allocation is emerging as a top crypto presale candidate for strategic portfolios in 2026.

With multiple projects competing for market share, investors are actively searching for concrete tech stacks that go beyond empty speculation. To make informed decisions, market participants are looking closely at how structural token mechanics and deflationary designs influence long-term asset value. By comparing structural performance across different network frameworks, this analysis breaks down the true financial utility behind the scenes. This direct review covers everything from historical multipliers to the modern mechanics driving the current DOGEBALL crypto presale 2026 window.

The History of Internet Computer (ICP): A Lesson in timing and resilience

The launch of Internet Computer (ICP) remains one of the most discussed events in tokenomic history. During its initial coin offering (ICO) phase, the project was met with widespread skepticism. Critics doubted its ambitious architecture, which aimed to replace the traditional centralized web with a decentralized global compute platform. However, early evaluators who looked past the noise and understood the underlying infrastructure secured allocations at an ICO price of approximately $0.03 per token.

When the network officially launched and mainstream trading commenced, the asset experienced an astronomical surge, briefly scaling heights above $700. For those early buyers, this multiplied their initial capital by over 20,000x at peak valuation, turning modest allocations into multi-million-dollar positions. The dramatic growth of ICP serves as an emotional and psychological case study for missing major market cycles. It highlights how initial market doubt often creates the most profitable entry points.

The core reason behind this historic trajectory lies in the project’s institutional-grade tokenomics and aggressive early developer-grant marketing. While missing that specific window left many buyers behind, the cyclical nature of decentralized finance continuously introduces new technical frameworks. For investors looking to capture similar early-stage upside, identifying structural value through a top crypto presale before the broader market catches on is the key to minimizing future portfolio regret.

Unpacking the DOGEBALL ecosystem and architectural utility

The ongoing DOGEBALL project represents a structural shift in how high-throughput ecosystems combine consumer gaming with global liquidity channels. Built on a custom, EVM-compatible Ethereum Layer 2 blockchain called DOGECHAIN, the platform establishes a hybrid model integrating GameFi and PayFi frameworks. The primary architecture solves two of the largest pain points in the current web3 landscape: high transaction friction and complex fiat offramping. Rather than forcing users to navigate multiple decentralized exchanges and centralized intermediaries to cash out, the native ecosystem enables instant crypto-to-fiat conversion directly into global bank accounts.

Smart money is increasingly leaning toward the DOGEBALL crypto presale 2026 due to its distinct structural advantages over legacy utility tokens. The core engine, known as DOGEPAY, supports over 30 fiat currencies with zero foreign exchange (FX) fees, completely bypassing traditional remittance networks like PayPal or Wise. Furthermore, the underlying DOGECHAIN Layer 2 infrastructure achieves sub-second transaction finality with near-zero gas fees. This technical setup provides developers, esports organizations, and casual gamers with a seamless micropayment network. By providing immediate, real-world transactional value alongside an audited, 100% secure smart contract infrastructure, the asset differentiates itself through tangible, cross-border settlement mechanics.

Analyzing the financial mechanics and presale growth potential

To truly understand why this asset is gaining traction as a top crypto presale, we must look at the hard tokenomic numbers, deflationary mechanics, and structural pricing schedule currently in play.

Metric

Details & Figures

Current Presale Stage

Stage 6

Current Token Price

$0.000741

Total Capital Raised

$298K+

Total Active Participants

1,000+ Investors

Projected Exchange Launch Price

$0.015

Recent Supply Deflation

4 Billion Tokens Burnt (20% of Presale Supply)

The project has transitioned away from static funding rounds to a highly disciplined, timed crypto presale structure consisting of 22 total stages. Each stage lasts a maximum of 7 days. However, the current pricing stage is expiring this weekend. At 21:00 UTC, the current stage closes permanently, and the next sequential stage begins with an automatic, mandatory price increase. Any unsold tokens from a completed stage’s allocation are immediately and permanently burnt, accelerating supply scarcity. This means this weekend represents the last opportunity to secure the asset at this exact low entry point before the acquisition cost increases.

Let us calculate the mathematical return on investment (ROI) for an investor acquiring tokens at the current Stage 6 valuation in plain text:

- Current Stage 6 Acquisition Price: $0.000741

- Fixed Exchange Launch Price: $0.015

- ROI Calculation Formula: (0.015 – 0.000741) / 0.000741 is approximately equal to 19.2429

- Percentage Growth Profile: ~1,924.29% baseline to launch

This means a capital allocation of $1,000 at the active presale price of $0.000741 is mathematically projected to scale to a gross value of $20,242.91 upon exchange listing, representing an approximate 19.24x multiplier before the token even hits mainstream trading platforms (not including the extra tokens unlocked by utilizing the DB30 30% bonus code).

Exclusive 30% Bonus Activated: Also, the Bonus code DB30 can be used for 30% BONUS tokens, so hurry up! Inputting code DB30 at checkout immediately grants an extra 30% token allocation on top of the order, allowing investors to maximize their portfolio depth before the tier rolls over this weekend.

Because the price climbs automatically at the upcoming phase deadline, securing an allocation this weekend minimizes cost basis and maximizes the mathematically locked-in launch premium.

Step-by-step guide: How to acquire DOGEBALL

Securing an allocation in this top crypto presale requires a few simple, secure steps before the looming pricing escalation occurs:

- Step 1: Set up a secure, EVM-compatible web3 wallet such as MetaMask, Trust Wallet, or Coinbase Wallet, ensuring it is properly funded with ETH, USDT, or MATIC.

- Step 2: Navigate to the official project website to access the secure, updated Timed Presale Widget.

- Step 3: Connect a web3 wallet to the widget, select a preferred network (Ethereum or BNB Chain), and input the exact amount of crypto to exchange.

- Step 4: Apply the active bonus code DB30 in the promotional field to claim a 30% bonus multiplier.

- Step 5: Authorize and confirm the smart contract transaction within the wallet interface at the current $0.000741 rate, ensuring the process is completed this weekend before the stage cut-off.

Conclusion: Strategic positioning in early-stage utility markets

Navigating the decentralized market requires looking past short-term speculation to identify assets with robust, underlying infrastructure. Historical assets like Internet Computer proved that investors who absorb early-stage volatility can capture exponential rewards. As the broader blockchain landscape evolves, ecosystems that merge low-cost Layer 2 rollups with global fiat settlement networks are positioned to lead the next major adoption cycle.

The structural setup of the DOGEBALL presale offers an asymmetric risk-to-reward opportunity. By combining an audited Ethereum Layer 2 framework with a zero-fee fiat offramp app, the platform positions itself far ahead of standard speculative assets. With a fixed launch target of $0.015 and an aggressive deflationary burning schedule that permanently eliminates unsold tokens, early participants have a transparent path to calculated capital growth. Given that the current pricing tier expires this weekend and moves upward across the remaining timed stages, securing an entry at the current Stage 6 pricing represents the most efficient risk-mitigated entry point for portfolios before mainstream exchange trading begins.

For more information, visit the official website, Telegram, and X.

FAQs for top crypto presale

Which presale crypto is best?

The best presale option is DOGEBALL (DOGEBALL). It combines a custom Ethereum Layer 2 blockchain with DOGEPAY, a utility engine offering zero FX fees, instant bank offramping across 30+ currencies, and a mathematically sound 1,924.29% launch growth profile.

Which crypto has 1000x potential?

Assets with custom Layer 2 technical foundations like DOGEBALL hold major long-term scaling potential. Its built-in utility requires the token for all ecosystem transaction fees, generating persistent market demand alongside an aggressive weekly token burning mechanism that continuously shrinks circulating supply.

Is it good to buy presale crypto?

Yes, purchasing presales like DOGEBALL provides a distinct liquidity advantage. Buying early locks in a lower cost basis relative to the fixed $0.015 exchange listing price, guaranteeing automated value increases as the project moves through its timed stages.

What is the biggest crypto presale in history?

While EOS and Ethereum hold historical fundraising records, the ongoing DOGEBALL campaign is setting new structural benchmarks. It utilizes a highly strategic timed mechanism where all unsold stage tokens are permanently burnt to aggressively preserve early investor value.

Which meme coin will reach $1 in 2026?

While traditional meme assets lack utility, DOGEBALL is uniquely architected to reach long-term milestones. Its dual integration of a $1M Play-to-Earn gaming prize pool and real-world PayFi global remittance channels builds sustainable capital inflows to drive asset valuation, especially when supercharging early stakes with bonus code DB30.

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

On June 4, 2026, JPMorgan delivered a warning the crypto industry did not want to hear. In a report led by managing director Nikolaos Panigirtzoglou, the bank said the window for Congress to pass the CLARITY Act this year is narrowing fast, squeezed by the approaching midterm elections and an unresolved fight over whether stablecoins can pay yield.

Summary

- JPMorgan has warned the window to pass the CLARITY Act this year is narrowing as lawmakers face election season and unresolved stablecoin yield disputes.

- Bank lobbying groups and major financial institutions continue to oppose provisions that could allow stablecoins to compete with traditional bank deposits.

- Failure to pass the bill in 2026 could leave the crypto industry facing continued regulatory uncertainty and enforcement-driven oversight.

This matters because the CLARITY Act is widely viewed as the crypto industry’s single most important legislative priority, the bill that would finally establish a comprehensive federal framework for digital assets and end years of regulation-by-enforcement. JPMorgan had previously expected the bill to pass and act as a positive catalyst for crypto in the second half of 2026.

Now its own analysts are flagging that the path has become “high-friction,” and the crypto investment firm Galaxy puts the odds of passage this year at “roughly 50-50, and possibly lower.” The bill that was supposed to be crypto’s big regulatory win is running into a wall of calendar math and bank lobbying.

This piece explains what CLARITY would do, why it is stalling, and what is actually at stake if the window closes.

What the CLARITY Act would do

To understand why JPMorgan’s warning matters, you have to understand what the bill is supposed to fix.

For years, US crypto regulation has been a mess of ambiguity. The central unresolved question is whether any given cryptocurrency is a security, regulated by the Securities and Exchange Commission, or a commodity, regulated by the Commodity Futures Trading Commission. That distinction determines almost everything about how a token can be issued, traded, and custodied, and for most of crypto’s history it has been settled not by clear law but by enforcement actions, with the SEC suing companies and letting courts sort out the boundaries case by case. The industry calls this “regulation by enforcement,” and it has been a persistent complaint that the rules are unknowable until you are already being sued for breaking them.

The CLARITY Act is designed to end that. It would establish the first comprehensive federal framework governing digital assets, drawing clear lines between which tokens fall under the SEC and which under the CFTC, and setting rules for issuers, exchanges, and investors. Supporters argue this regulatory certainty would unlock institutional participation that has been sitting on the sidelines, encourage investment and innovation, and most importantly keep crypto businesses and capital in the US rather than driving them to overseas jurisdictions with clearer regimes. It is, in the industry’s telling, the foundational piece of legislation that everything else depends on.

That is why the stakes around its timing are so high. This is not a minor regulatory tweak. It is the bill that would define the legal status of an entire asset class in the world’s largest financial market, and its passage or failure this year shapes the regulatory environment crypto operates in for years to come.

Why it’s stalling: the stablecoin yield fight

The single biggest obstacle, by JPMorgan’s account and everyone else’s, is a fight over stablecoin yield. It sounds technical. It is actually a war between the banking industry and crypto over deposits.

The question is whether stablecoin issuers should be allowed to pay yield, effectively interest, to people who hold their tokens. Crypto-native firms want this: a yield-bearing stablecoin is a powerful product that could attract enormous balances. The banking industry is fiercely opposed, and the reason is self-interested and obvious. If stablecoins can pay interest, they become direct competitors to bank deposits, and money could flood out of regulated banks and into crypto-issued dollar tokens. Banks see that as an existential threat to their deposit base, which is the cheap funding their entire business model runs on.

The CLARITY Act, as currently drafted, tries to thread this needle by prohibiting “passive” yield, plain interest paid on balances, while allowing rewards tied to specific activity. JPMorgan’s analysts note the text is ambiguous because it does not explicitly ban interest on balances, leaving room for interpretation. That ambiguity has satisfied no one. A compromise between Senators Thom Tillis and Angela Alsobrooks reached a tentative deal on stablecoin yield, but bank lobbying groups immediately attacked it as too friendly to crypto, with members of the American Bankers Association reportedly sending more than 8,000 letters to Senate offices criticizing the compromise.

The most striking sign of the deadlock came from JPMorgan’s own chief executive. Jamie Dimon said publicly that he is not satisfied with the CLARITY Act as written, citing the stablecoin yield compromise and what he called insufficient consumer protections, and warned that banks “will not accept it that way.” When the CEO of America’s largest bank is openly opposing the bill while his own analysts warn it is running out of time, you have a clear picture of the forces working against it. The bank lobby is one of the most powerful in Washington, and it has decided this fight is worth having.

The calendar math is brutal

Even if the stablecoin fight were settled tomorrow, the CLARITY Act faces a problem no amount of negotiation can fix: there is almost no time left on the legislative clock.

Here is the sequence the bill still has to clear. It passed the Senate Banking Committee on May 14, which sounds like progress but is only one step of many. From there it must secure 60 votes in the full Senate, a high bar that requires bipartisan support. Then it must be reconciled with the House version of the legislation, since the two chambers have passed different texts that have to be merged into one. Then it needs the president’s signature.

JPMorgan’s analysts called these “several high-friction steps outstanding,” which is analyst-speak for a gauntlet.

Now overlay the calendar. The Senate all but leaves Washington for the month of August, and once members return, they shift into campaign mode for the November midterm elections, which consumes legislative attention and makes controversial votes harder to whip. That leaves a narrow handful of working weeks, by some counts only about eight, before the August recess to get floor time scheduled and the remaining steps done.

Crypto advocates had hoped to get the bill to the Senate floor before July 4. Treasury Secretary Scott Bessent has pressed lawmakers to pass it this summer. But the bill has not moved into June with much momentum, and floor time is precious, competing with all the other non-crypto business the Senate must handle.

This is why JPMorgan’s framing shifted from “positive catalyst” to “narrowing window.” The bank had expected passage to lift crypto in the second half of 2026. Now the realistic paths are: a narrow summer passage if everything breaks right, a long-shot September window, or punting to the post-election “lame duck” session, where the odds drop further.

Galaxy’s “50-50, and possibly lower” estimate captures the uncertainty, and as Galaxy noted, the risk is not any single issue but “the sheer number of unresolved questions that must be settled in sequence under severe time pressure.” Any one blowup among the negotiators could be a fatal delay.

What’s actually at stake

It is worth being clear-eyed about what passage or failure would mean, because the consequences cut in both directions and the stablecoin fight has a twist worth understanding.

If CLARITY passes, the industry gets the regulatory certainty it has wanted for years. Institutional capital that has stayed on the sidelines due to legal ambiguity would have clearer rules to operate under, which could unlock a wave of participation and, as JPMorgan originally expected, act as a positive catalyst for crypto markets. The SEC-versus-CFTC question gets settled, exchanges and issuers get defined rules, and the US positions itself as a jurisdiction where crypto businesses can operate with legal confidence rather than fleeing offshore.

If it fails or slips to 2027, the status quo of regulation-by-enforcement persists, the uncertainty that has constrained institutional adoption continues, and the momentum behind US crypto-friendly policy loses a major win. In a year when the market is already weak, the failure of the industry’s top legislative priority would be a sentiment blow on top of the price weakness.

But the stablecoin yield twist complicates the simple “passage is bullish” story. JPMorgan’s analysts point out that if the final bill does restrict passive stablecoin yield, as the current draft intends, the effect would be to push idle crypto cash toward alternatives: tokenized Treasuries, digital money market funds, and tokenized deposits.

In other words, even a successful bill might not be the clean victory crypto-native firms wanted, because the yield restriction would channel capital into bank-friendly and Treasury-backed products rather than yield-bearing stablecoins.

The banks, in that scenario, win the substance even if the bill passes. So the real question is not just whether CLARITY passes, but what it looks like if it does, and who actually benefits from the compromise that gets it across the line.

The honest read is that crypto’s most important bill is caught between a hostile bank lobby and a closing legislative window, and even the optimistic outcome may hand the banking industry a quiet victory on the issue it cares about most. JPMorgan’s warning is not that CLARITY is dead. It is that the easy path is gone, the clock is loud, and the version that survives may look very different from what the industry set out to pass.

This article is for informational purposes and does not constitute financial or investment advice. Cryptocurrency markets are highly volatile. The figures and analysis described reflect data available as of June 5, 2026. Always do your own research and consult with qualified financial professionals before making investment decisions.

This is the uncomfortable truth at the center of the XRP investment case in 2026.

Summary

- XRP Ledger adoption is real, but ledger usage does not automatically create XRP token demand.

- XRP value capture depends on fee burn, reserves, and bridge-currency demand, but each channel has limits.

- RLUSD helps Ripple serve banks, yet it may also let institutions use Ripple infrastructure without buying XRP.

- The real test is whether XRP lending, RWA trading pairs, and ODL volume scale enough to require the token.

The XRP Ledger is winning. Banks and payment firms are adopting it, tokenized funds are settling on it, stablecoins are moving across it, and Ripple has built an end-to-end institutional infrastructure that traditional finance can plug into without changing how it operates. By almost every measure of adoption, the thesis XRP holders have believed for years is finally coming true.

And yet the XRP token has spent 2026 stuck in a narrow band around $1.30, far below where its believers expected adoption to take it. The reason is a problem most bullish coverage glosses over: a thriving XRP Ledger does not automatically create demand for the XRP token. Banks can use the rails without ever buying the asset.

This piece works through exactly how XRP is supposed to capture value, why those mechanisms are not firing the way holders hoped, what would have to change for the disconnect to close, and how to tell the difference between a transitory lag and a structural flaw. It is the honest version of the XRP story.

The disconnect, stated plainly

Start with the two facts that do not fit together, because holding them side by side is the whole point.

Fact one: the XRP Ledger is being adopted by serious institutions. Ripple Payments and On-Demand Liquidity are live across more than 40 corridors with named partners processing real cross-border flows. UnionBank in the Philippines, the first fully licensed virtual asset bank there, uses ODL for remittances. Travelex Bank Brazil, Yes Bank and Axis Bank in India, and dozens of other institutions have moved past pilots into production. Cumulative Ripple Payments volume crossed $95 billion as of January 2026. Tokenized funds sit on the ledger, stablecoins move across it, and Ripple has assembled a full stack, prime brokerage through Ripple Prime, treasury services through Ripple Treasury, and a bundled product combining stablecoin issuance, custody, and digital identity. This is real institutional adoption, not vaporware.

Fact two: the XRP token has gone nowhere. It trades around $1.30, pinned below its moving averages, locked in a range that has held since early in the year. The adoption keeps growing and the price keeps not responding. After reaching above $3.50 in the prior summer, XRP entered a long decline of lower highs and lower lows that the adoption news has not reversed.

The gap between these two facts is the most important thing to understand about XRP right now, and it has a name worth using: value capture. A blockchain can be wildly successful as infrastructure while its native token captures almost none of that success in price. That is not a contradiction or a market error. It is a question of plumbing, specifically whether the token is mechanically required, in meaningful quantities, by the activity flowing across the network. For XRP, the honest answer in 2026 is: not as much as you would think.

How XRP is supposed to capture value

XRP has three plausible channels through which network usage could translate into token demand. Walking through each one shows why the disconnect exists, because each channel turns out to be weaker than the bull case assumes.

The first channel is fee burn. Every transaction on the XRP Ledger destroys a tiny amount of XRP as a fee, which is mildly deflationary and, in theory, links usage to scarcity. The problem is scale. The amount of XRP burned daily has collapsed 95 percent since December 2024, from around 15,000 XRP per day to a current range of roughly 163 to 750 XRP per day. Over the entire history of the ledger, only about 14 million XRP have ever been burned, equal to 0.014 percent of the total supply. To put that in perspective, even if tokenized-asset activity drove a burn rate one hundred times higher than today, it would still take decades to create meaningful scarcity. And there is a catch that makes fee burn self-defeating as a value driver: fees only climb materially when the network is congested, and congestion is the opposite of what a payment network wants. So XRP is consumed every time the ledger is used, but fee burn alone cannot move the valuation in any macro-relevant way.

The second channel is the reserve mechanism, and it is the most direct and measurable of the three. The XRP Ledger requires users to lock up small amounts of XRP to open an account and to own certain ledger objects. Current mainnet requirements are 1 XRP per account plus 0.2 XRP per owned item, and the items that consume reserves include trust lines, which are needed to hold most issued assets such as stablecoins and tokenized instruments. This means that as more accounts and more tokenized assets live on the ledger, more XRP gets locked into reserves, creating genuine structural demand. This is the strongest part of the bull case. But notice its limit: the demand is tied to the number of accounts and objects, not to the dollar value being settled. A bank moving a billion dollars across the ledger locks up the same trivial reserve as a bank moving a thousand. The reserve mechanism scales with the count of things, not the value of flows, which caps how much demand it can generate even under heavy institutional use.

The third channel is the bridge-currency function, the original thesis, and the one in the most trouble. In Ripple’s On-Demand Liquidity model, a payment firm converts local currency into XRP, sends it across the ledger in seconds, and converts it to the destination currency on arrival, eliminating the need to park cash in foreign accounts. Every such transaction does generate real buy demand for XRP, because the token is actually purchased as the bridge. This is the mechanism that directly ties usage to token demand. The problem is twofold: ODL volume, while real, is not large enough to move the price on its own, and Ripple has introduced something that may cannibalize it.

The RLUSD problem the bulls underplay

The thing most likely to weaken XRP’s strongest value-capture channel is a Ripple product: its own stablecoin, RLUSD.

RLUSD launched as a dollar-backed stablecoin and crossed a $1.26 billion market cap in under a year. Ripple now runs a hybrid model where RLUSD operates alongside XRP in Ripple Payments. The official framing is elegant: RLUSD provides price stability for banks that do not want crypto volatility, while XRP acts as the bridge that swaps between different currencies. In this telling, the two are complementary, with XRP as the settlement layer moving value between stablecoin systems.

But look at it from a bank’s perspective and the tension becomes obvious. Many financial institutions prefer stablecoin settlement precisely because it avoids holding a volatile asset like XRP, even for the few seconds of a bridge transaction. If a bank can settle a corridor using RLUSD end to end, it has no need to touch XRP at all. By offering RLUSD, Ripple meets banks where they are, which is good for Ripple the company, but it also hands those banks a way to use Ripple’s infrastructure without generating XRP demand. The hybrid model that bulls cite as proof of XRP’s central role may, in practice, route around the token in exactly the corridors where stablecoins work well.

This connects to a broader competitive reality. In dollar-denominated corridors, stablecoins like USDC and USDT are genuine competitors to XRP, settling cross-border payments almost as fast while holding their value in transit. XRP’s structural advantage is real but specific: it shines in fiat-to-fiat corridors where neither party wants dollar exposure, particularly emerging-market routes where a direct local-currency-to-local-currency bridge beats routing through a dollar stablecoin. That is a meaningful niche, but it is a niche, and the rise of regulated stablecoins under frameworks like the GENIUS Act puts a ceiling on XRP’s addressable market even where it does not eliminate the use case.

The starkest illustration came when Société Générale tokenized its euro stablecoin on a ledger: the operation could be carried out without any party needing to hold XRP beyond the fraction of a cent required to pay the transaction fee. That is the disconnect in a single example. The ledger gets the business. The token gets a fraction of a cent.

Why this isn’t necessarily fatal

Having made the bear case honestly, it is worth giving the bull case its strongest form, because the disconnect is not proof that XRP is doomed. It is proof that XRP’s value capture depends on specific things happening that have not happened yet.

The reserve mechanism genuinely does scale with adoption, and if the XRP Ledger becomes the settlement layer for a large fraction of tokenized real-world assets, the cumulative reserve demand from millions of accounts and tens of millions of ledger objects could become substantial. The bull case is not that any single mechanism is huge, but that account growth, trust-line proliferation, and tokenized-asset issuance compound over time into structural demand that the current depressed price does not reflect.

There is also genuine optionality in the roadmap. The XRP Ledger is adding lending protocols and a native decentralized exchange, and if those achieve real adoption, they create new contexts in which XRP could be required as a base trading pair or collateral. Garlinghouse has made aggressive predictions, including that the XRP Ledger could eventually capture 14 percent of the volume currently running through SWIFT, which if even partially realized would represent a transformation in ODL scale that does move the token. The regulatory unlock matters too: the CLARITY Act writing XRP’s commodity status into law would green-light US banks for ODL adoption and open the door to spot ETFs, both of which create demand channels that regulatory uncertainty has kept closed.

The honest framing is that the bull case is conditional, not broken. XRP captures value if specific conditions are met: if the new protocols achieve real adoption, if tokenized-asset issuers choose to use XRP as a medium of exchange rather than operating purely in stablecoins, and if ODL volume scales into truly transformative territory rather than growing incrementally. Those are real possibilities. They are just not guarantees, and the current price reflects a market that has stopped paying for the promise and started waiting for the proof.

How to tell a lag from a flaw

The most useful thing an XRP holder or analyst can do is define, in advance, what evidence would distinguish a temporary disconnect from a permanent structural feature. Vague faith that “adoption will eventually flow to the token” is not analysis. Specific, falsifiable thresholds are.

One sharp framework, laid out by analysts watching the value-capture question, proposes three concrete tests over a six-month horizon. First, lending volumes denominated in XRP exceeding $500 million, which would show the new DeFi protocols creating real token demand. Second, at least three major real-world-asset issuers incorporating XRP as a trading pair in their products, which would show tokenized-asset activity actually requiring the token rather than routing around it in stablecoins. Third, ODL volume consistently exceeding $500 million per day, which would show the bridge-currency function scaling to a level that generates sustained buy pressure. If those three things happen, the current disconnect is a transitory phase and the bull case is vindicated. If they do not, the disconnect is structural, and XRP is an infrastructure token whose infrastructure simply does not need much of it.

The remittance math gives a sense of the distance involved. The global remittance market is roughly $685 billion annually. XRP processed around $15 billion through ODL in 2024, about 2.2 percent penetration. That is meaningful progress, but it is also a reminder of how far the network is from the dominance its more ambitious price targets imply. For XRP to reach the $5-plus targets that bulls cite, ODL adoption would need to scale into transformative territory, doubling and redoubling rather than growing 30 to 50 percent a year.

So the practical guidance is to ignore the adoption headlines that do not specify token demand and watch the three thresholds instead. “Bank X is using the XRP Ledger” tells you nothing about whether bank X is buying XRP. “ODL volume hit $500 million a day” tells you everything. The disconnect closes when the metrics that actually require the token start moving, and not before.

The bottom line on the disconnect

XRP in 2026 is the cleanest example in crypto of a successful network whose token has not yet been invited to the party. The XRP Ledger has achieved something rare: it has become financial infrastructure that institutions adopt because it is efficient, compliant, and cheap. That is a genuine accomplishment, and the adoption is not fake. But the three mechanisms that are supposed to turn that adoption into XRP demand, fee burn, reserves, and the bridge-currency function, are each weaker than the bull narrative assumes. Fee burn is negligible and self-defeating. Reserves scale with object count, not settled value. And the bridge function, the strongest channel, is being partially routed around by Ripple’s own RLUSD stablecoin and squeezed by the broader rise of regulated dollar stablecoins.

None of this means XRP cannot appreciate. It means XRP’s appreciation depends on conditions that are identifiable and not yet met: real adoption of the ledger’s new lending and DEX protocols, tokenized-asset issuers actively choosing XRP as a medium of exchange, and ODL volume scaling past the levels where it generates real buy pressure. The CLARITY Act and a wave of post-legislation bank partnerships could accelerate all of this, which is why the regulatory calendar matters so much to XRP specifically.

For holders, the discipline is to stop treating ledger adoption and token demand as the same thing, because they are not. The ledger is thriving and the token is waiting, and the gap between them will close only when the specific value-capture mechanisms start firing at scale. Watch the lending volumes, the RWA trading pairs, and the daily ODL figures. Those numbers, not the partnership press releases, will tell you whether the banks using the XRP Ledger ever actually start buying XRP. Until they do, the most accurate description of XRP is the one the bulls least like to hear: great infrastructure, waiting for its token to matter.

This article is for informational purposes and does not constitute financial or investment advice. Cryptocurrency markets are highly volatile. The figures and analysis described reflect data available as of June 5, 2026. Always do your own research and consult with qualified financial professionals before making investment decisions.

Ethereum price remained under heavy selling pressure for a fourth straight day on Friday as liquidations, sustained ETF outflows, and a major technical breakdown pushed ETH to its lowest level this year.

Summary

- Ethereum price dropped to a new yearly low near $1,680 as liquidations and ETF outflows weighed on sentiment.

- Spot Ethereum ETFs posted $19.3 million in inflows, ending a 17-day outflow streak.

- Analysts see $1,600 and $1,500 as the next key support levels after ETH lost $1,825.

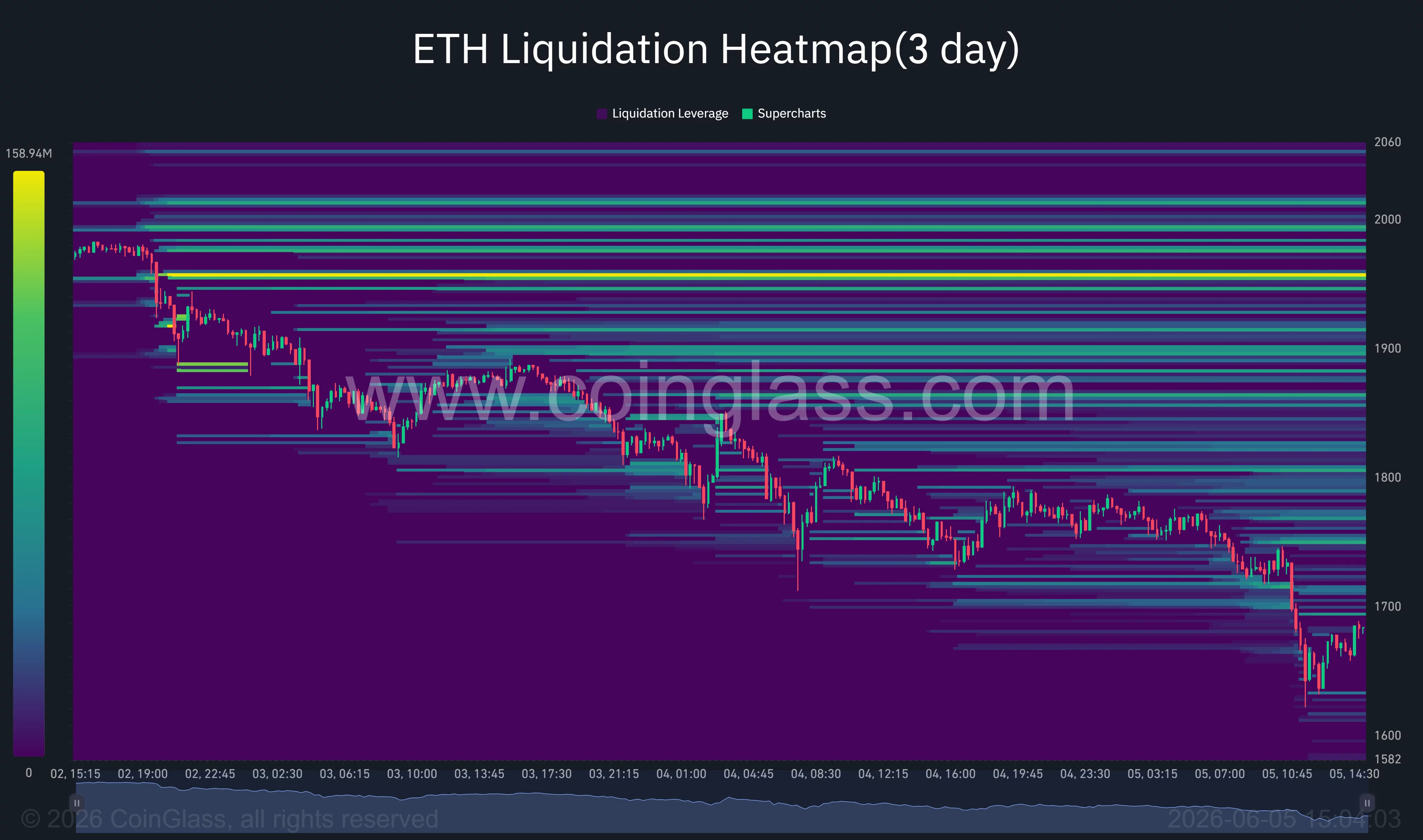

According to data from crypto.news, Ethereum (ETH) price traded near $1,680 on June 5 after falling almost 5% on the day. The decline followed a sharp move below $1,825, a level traders had watched as one of the last major supports before the $1,600 and $1,500 zones.

Ethereum’s selloff accelerated after a crowded long trade unwound across crypto futures markets. CoinGlass data showed more than $1.2 billion in crypto positions were liquidated in a single day, with forced selling adding pressure to Ethereum as automated liquidation engines cut leveraged exposure.

Market sentiment also weakened after on-chain trackers flagged a movement of 10,422 Bitcoin, worth about $739 million, linked to the legacy Mt. Gox estate. The coins did not move directly to exchanges, but the transfer raised supply concerns across crypto markets.

At the same time, Strategy’s rare Bitcoin sale to fund preferred stock dividends added another psychological blow for traders already dealing with falling prices and thin liquidity.

ETF inflows offer limited relief

Spot Ethereum ETFs snapped their longest outflow streak on Thursday, recording $19.3 million in net inflows after 17 straight trading days of withdrawals, data from SoSoValue shows.

The inflow does not show a strong return of institutional demand, but it suggests the heavy bearish stance among professional investors may be starting to ease. Earlier in the week, Ethereum ETFs had suffered steep redemptions, including more than $519 million in outflows on June 2 alone.

Macro pressure remains another drag. WTI crude futures held near $93 per barrel on Friday, leaving oil up more than 6% for the week despite a 3% pullback in the previous session.

As reported by crypto.news earlier, the U.S. and Iran could still pursue a diplomatic solution, have helped calm oil markets, but talks have yet to produce clear progress. Israel’s military operations in Lebanon and Hezbollah’s rejection of a U.S.-mediated ceasefire proposal have kept geopolitical risk elevated.

Higher oil prices have revived inflation concerns at a time when the Federal Reserve is already maintaining a higher-for-longer stance. With the 10-year U.S. Treasury yield near 4.43%, investors have continued to move capital away from risk assets and into safer yield-bearing markets.

Ethereum chart keeps $1,500 in focus

Ethereum’s daily chart shows an inverse Adam and Eve structure that broke below neckline support near $1,975. The measured move from the pattern projects a possible decline toward roughly $1,412, placing the $1,500 area directly inside the next major downside zone.

The breakdown also pushed ETH below its 200-day exponential moving average and local ascending support, turning the $2,030 to $2,245 area into a heavy resistance zone. A recovery into that band would be needed before bulls can challenge the bearish structure.

Momentum remains weak. The daily MACD sits below its signal line, while the histogram remains in negative territory. The 14-day RSI has fallen into deeply oversold territory, with the chart showing a reading near 15 and the RSI average near 30.

According to crypto analyst Ali Charts, Ethereum’s break below $1,825 has opened the next downside levels.

“Ethereum $ETH broke past the $1,825 support level! Now the path to $1,600 and $1,400 is open.”

CoinGlass’ three-day liquidation heatmap shows heavy liquidation clusters above spot price, especially between $1,900 and $2,060. Below current levels, liquidity appears thinner until the $1,600 area, meaning a failure to hold the current rebound zone could leave ETH exposed to another sharp move lower.

Commenting on the latest price action, crypto trader Ted Pillows noted that Ethereum had dropped to a new yearly low and argued that the $1,500 level could become an accumulation zone for larger buyers.

Michael van de Poppe offered a more contrarian view, noting that Ethereum had reached its lowest daily RSI ever recorded. He described the extreme RSI reading as “close to the end of the bear market,” though price has not yet confirmed a reversal.

Downside risk would deepen if ETH loses $1,600 on strong volume. Such a move would place $1,500 and the measured target near $1,412 into focus, especially if liquidation pressure returns and ETF inflows fail to continue.

The bearish setup would begin to weaken only if Ethereum reclaims $1,825 and then closes above $1,975. Until then, $1,500 remains the key level traders are watching as the next major test of buyer demand.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Michael Saylor has outlined four Bitcoin ideologies in a new paper, framing the debate over how Bitcoin should grow, connect with markets, improve technically, and protect its core principles.

Summary

- Saylor separates Bitcoin believers into maximalists, capitalists, technologists, and fundamentalists as adoption debates widen globally.

- Capitalists favor market integration, while fundamentalists warn against custody, leverage, regulation, and protocol compromise risks.

- The paper lands as Strategy faces scrutiny after Strategy’s rare Bitcoin sale and price pressure.

Saylor said Bitcoin has moved beyond its early role as a niche technology or monetary protest. He described it as a global monetary network that now matters to individuals, companies, banks, capital markets, and governments.

In the paper, Saylor identified four groups: Bitcoin Maximalists, Bitcoin Capitalists, Bitcoin Technologists, and Bitcoin Fundamentalists. He said these groups all see Bitcoin as important, but they differ on adoption, upgrades, market access, and preservation.

Saylor wrote that Bitcoin is “no longer a narrow technical experiment or a niche monetary protest.” His paper presents the split as a natural stage in Bitcoin’s growth, not a simple conflict inside the community.

Maximalists and capitalists see different routes

Saylor said Bitcoin Maximalists view Bitcoin as the dominant digital monetary network. They see it as sound money, a store of value, and a tool for people facing inflation, debasement, or weak financial systems.

He said Maximalists give Bitcoin moral clarity, but they must still answer how the network fits into banks, companies, capital markets, and governments. In his view, Maximalism defines the destination, while other groups debate the route.

Bitcoin Capitalists take a broader market view. Saylor said they want Bitcoin inside portfolios, balance sheets, credit products, securities, custody systems, and global financial infrastructure.

This group sees Bitcoin as digital capital. It supports corporate treasuries, Bitcoin-backed credit, institutional custody, and higher-layer tools that help Bitcoin reach more users.

Technologists and fundamentalists pull in opposite directions

Saylor said Bitcoin Technologists believe the protocol must keep improving. Their focus includes scalability, privacy, security, usability, wallet design, custody models, and future threats such as quantum computing.

He also warned that protocol changes carry risk. Bitcoin’s base layer has value because users trust its stability, so any change must meet a high standard before the network accepts it.

Bitcoin Fundamentalists take the opposite caution further. Saylor said they focus on self-custody, personal nodes, decentralization, immutability, and censorship resistance.

They worry that banks, governments, custodians, leverage, and financial engineering could weaken Bitcoin’s original purpose. Saylor said their role is to protect Bitcoin’s core principles while avoiding a closed view of adoption.

Strategy backdrop adds market context

The paper comes during a tense week for Saylor and Strategy. As previously reported by crypto.news, Strategy sold 32 BTC for about $2.5 million, its first Bitcoin sale since 2022.

The sale was small compared with Strategy’s holdings, but it drew attention because Saylor has long argued for holding Bitcoin. Related reports also said Bitcoin traded near $60,000 as ETF outflows and weak sentiment added pressure.

That backdrop gives Saylor’s paper a timely market angle. Bitcoin is no longer only a technical network or a personal savings tool. It now sits inside public companies, credit structures, ETFs, and policy debates.

Saylor’s final message favored a mixed path. He argued that Bitcoin should protect its base layer while allowing markets, applications, custody tools, and financial products to develop around it. He called that path disciplined expansion.

Pi Network’s PI token fell to a new all-time low near $0.126 on June 5, 2026, capping a slide that has erased more than 30% of its value in a month and confirmed a bearish breakdown traders had been watching for weeks.

Summary

- Pi Network fell to a new all-time low near $0.126 after a month-long decline that erased more than 30% of its value.

- More than 163 million PI tokens are set to enter circulation in June, adding supply pressure as demand remains weak and market liquidity stays thin.

- New ecosystem initiatives, including a developer center and four games from CiDi Games, have yet to generate enough demand to offset the ongoing token unlocks.

At roughly $0.13, the token carries a market cap around $1.36 billion and sits near rank #58, a long way from the excitement that surrounded its Open Mainnet launch and exchange listings.

The immediate triggers are clear and specific. More than 163 million PI (PI) tokens are scheduled to unlock and enter circulation this month, averaging over 5 million per day, with the single largest release of nearly 16 million PI due on June 11. That fresh supply is landing into thin liquidity and a brutal market-wide selloff that has dragged Bitcoin below $62,000 and wiped out over $1.6 billion in leveraged positions.

The question every PI holder is now asking is whether the unlocks push the token below $0.10. This piece breaks down why Pi hit a new low, the supply problem at the heart of it, the one bright spot, and what would have to change.

How Pi got here

The path to a new all-time low was not sudden. It was a steady erosion that accelerated into a breakdown.

Pi Network surged to around $0.296 in March 2026, riding enthusiasm around its exchange listings and the broader attention its unusually large user base attracted. That was the peak. From there the token entered a persistent downtrend, retreating through the spring as the initial excitement faded and selling pressure built. By late May it was trading near $0.15, already its lowest level since February, and below all its major moving averages, a sign that bears had taken firm control of the trend.

The technical structure then broke. For weeks, Pi had been trading inside a falling wedge pattern on the daily chart, with buyers repeatedly failing to reclaim resistance in the $0.18 to $0.20 region. When they failed one final time, sellers forced a decisive breakdown below the lower boundary of the wedge and below the critical support band around $0.129 to $0.131. That breakdown is what pushed PI into price discovery on the downside, opening the door to the fresh record low near $0.126 reached on June 5.

The drop also has to be understood against the backdrop of the broader market. This was not a Pi-specific collapse happening in isolation. Bitcoin briefly fell to an intraday low near $61,550 on June 4, Ethereum dropped below $1,800, and the CoinGlass data showed more than $1.6 billion in leveraged positions liquidated across crypto. That kind of market-wide capitulation crushes appetite for speculative altcoins, and Pi, as one of the more speculative large-cap names, felt it acutely. But the market selloff is only the accelerant. The core problem is structural, and it is about supply.

The supply problem at the heart of it

The single most important factor in Pi’s decline is its token unlock schedule, and the math is unforgiving.

Pi Network has a token release schedule that steadily moves locked tokens into circulation, and June is a heavy month. Data from PiScan shows more than 163 million PI scheduled to enter circulation over the next 30 days, with daily unlocks averaging over 5 million tokens. The largest single-day release, nearly 16 million PI, is expected on June 11. Every one of those tokens is new supply hitting the market, and supply that arrives faster than demand grows pushes price down by simple arithmetic.

This is the deep structural challenge Pi faces, and it is not new, just intensifying. The token’s design front-loads a large amount of supply entering circulation over time, and for that not to crush the price, there has to be commensurate demand: new buyers, real usage, genuine utility pulling tokens out of circulation as fast as the schedule puts them in. Right now, that demand is not there. Liquidity is thin, the broader market is in retreat, and there is no flood of new buyers stepping in to absorb the unlocks. The result is a persistent imbalance where new supply consistently outweighs new demand, and the price grinds lower.

The timing makes it worse. The June unlocks, and especially the June 11 release, are landing precisely when market liquidity is at its weakest and risk appetite at its lowest. In a strong bull market, an ecosystem might absorb 163 million new tokens without much trouble, because demand is rising fast enough to soak them up. In a fearful, illiquid market, the same supply becomes a heavy weight. This is why analysts are openly discussing whether PI breaks below $0.10: it is not a wild bearish fantasy; it is a straightforward read of supply outrunning demand at the worst possible moment.

The one bright spot

It would be incomplete to describe Pi purely as a supply-driven collapse, because there is genuine development activity worth noting, even if it has not yet moved the price.

The most concrete recent positive is on the ecosystem side. CiDi Games launched a Developer Center alongside four new games, explicitly designed to attract builders and users into the Pi ecosystem. The pitch to developers is straightforward: plug into Pi’s large community, access built-in revenue streams, and integrate through a ready software development kit. The ambition, in CiDi’s framing, is to become the infrastructure for games inside Pi. The network also completed a mandatory protocol upgrade, with node operators required to move to the latest version to stay connected, a sign of ongoing technical maintenance.

Why does this matter? Because the only durable fix for Pi’s supply problem is real demand, and real demand comes from actual usage. If the ecosystem develops applications that people use, and those applications create genuine reasons to hold and spend PI, then the network starts generating the organic demand needed to absorb the unlocks. Gaming is a plausible vector for that, since games can drive frequent, real transactions rather than pure speculation. A developer center and new games are exactly the kind of foundational ecosystem-building that, if it succeeds, could eventually change the demand side of the equation.

The honest caveat is the size of the gap between this and what the price needs. Four new games and a developer center are early-stage ecosystem development. They are not, today, generating anywhere near the transaction volume or token demand required to offset 163 million in monthly unlocks. The bright spot is real, but it operates on a timeline of months and years, while the supply pressure is hitting right now. For the ecosystem activity to matter to the price, it has to scale dramatically, and that has not happened yet.

What would have to change

Pi’s near-term path and its longer-term prospects are different questions, and it helps to separate them.

In the near term, the price is caught between the unlock schedule and the broader market, and neither is in Pi’s favor right now. The immediate technical question is whether the $0.126 to $0.131 zone holds or breaks.

A decisive break below it, especially around the June 11 unlock, would put PI firmly in downside price discovery with $0.10 as the obvious psychological target. A broader market stabilization, by contrast, would relieve some of the pressure mechanically, since much of the recent drop came from the market-wide selloff rather than Pi alone.

So in the short run, watching Bitcoin and the overall risk environment tells you a lot about where PI goes, because a fearful market amplifies the unlock damage and a recovering one cushions it.

In the longer term, the question is entirely about whether demand can catch up to supply. This is the structural test Pi has to pass. The unlock schedule will keep putting tokens into circulation regardless of price. For the token to find a durable floor and eventually recover, the ecosystem has to generate enough genuine usage and demand to absorb that supply, ideally pulling tokens out of circulation through real economic activity faster than the schedule adds them.

The CiDi Games developer push is a step in that direction, but it needs to multiply many times over. Tier 1 exchange access, which has been a persistent topic for Pi, would also help by broadening the buyer base, though it is not a substitute for organic demand.

The community itself is split on what comes next, which is honest given the uncertainty. Some traders see the slump as a clear warning and a reason for caution, pointing to $0.10 as a real risk if selling continues. Others frame it as a buy-the-dip opportunity for long-term believers, urging patience and focus on whether the network can build real utility through the downturn. Even Pi’s supporters concede the move is a reality check.

The fairest summary is that Pi is a project with an unusually large user base and a genuine supply problem, and its future depends on whether it can convert that user base into the kind of real, on-chain demand that makes the relentless token unlocks survivable. Until that conversion happens at scale, the supply keeps coming, and the price keeps feeling it.

This article is for informational purposes and does not constitute financial or investment advice. Cryptocurrency markets are highly volatile. The figures and analysis described reflect data available as of June 5, 2026. Always do your own research and consult with qualified financial professionals before making investment decisions.

28 horror movies on HBO Max that deliver thrills and chills

Free outdoor activity day on Redcar seafront this summer

Indonesia central bank, finance minister agree to boost asset yields to aid rupiah

-

Business4 days ago