Crypto World

Bitcoin volatility looks cheap as $10 billion options settlement nears: Crypto Daily

“Call spreads remain attractive for anyone wanting recovery exposure into the post-quarterly reset. And now look even better on a relative-vol basis, since call spread longs are buying the cheaper wing of a skew that is leaning the other way,” he said.

There are a number of factors that might drive volatility higher in the near term. Friday’s options expiry, for example, which Péquignot described as “traditionally one of the most significant liquidity events on the annual calendar.”

Moreover, ahead of the expiry, options traders who bought puts, or downside bets, in recent months are sitting in profit. That is, they are in the money, while those who bought calls are set to see their bets expire worthless.

“With spot at 64k, the June 26 book is net long puts in the money and long calls out of the money – the embedded loss is sitting with the call buyers who chased the 80k+ strikes,” Péquignot noted.

The sharp decline in Alphabet (GOOG) and SpaceX (SPCX) stocks, and declines in Asian equity indexes is another factor that could stoke volatility in bitcoin, which often takes its cue from technology stocks.

Not to forget, the Fed’s preferred inflation measure, the core PCE, is scheduled for release Thursday and is expected to show price pressures at their strongest since May 2024. Such a reading may breed volatility across assets, including Treasury notes and cryptocurrencies. Stay alert!

Bitcoin mining difficulty has dropped 19.9% from its peak in the third deepest ASIC era decline on record, as miners sell bitcoin at record rates and redirect power capacity toward artificial intelligence data centers.

Summary

- Bitcoin mining difficulty has fallen 19.9% from its November 2025 peak of approximately 156 trillion to 126.23 trillion, the third deepest decline since dedicated ASIC hardware replaced graphics processors.

- Network hashrate declined roughly 12% from its late 2025 peak above one zettahash per second to approximately 868 exahashes per second by late July 2026, with Bitcoin Magazine Pro tracking 287 consecutive days of downward trend.

- Publicly traded miners sold more than 32,000 BTC in the first quarter of 2026 alone, exceeding their combined sales for all of 2025 and surpassing the 20,000 BTC sold during the 2022 Terra Luna collapse.

- Major mining companies including Hut 8, Core Scientific, and TeraWulf have signed multi billion dollar AI data center agreements, with Hut 8’s total contracted AI portfolio reaching $26.6 billion.

- Mining stocks have diverged from bitcoin’s price, with a basket of mining equities gaining 56% in early 2026 while bitcoin fell 17%, as investors increasingly value miners as energy infrastructure companies.

Bitcoin mining difficulty has dropped 19.9% from its all time peak. That single number captures a transformation that has been building for months but accelerated through the first half of 2026: the economics of mining bitcoin have deteriorated to the point where a meaningful share of the global fleet has shut down, and the operators that remain are increasingly looking beyond bitcoin for revenue.

The decline, tracked by Bitcoin Magazine Pro from the November 2025 peak of roughly 156 trillion to 126.23 trillion as of the July 25 adjustment, ranks as the third deepest drawdown since application specific integrated circuits became the standard mining hardware. Only the aftermath of China’s 2021 mining ban and a 2018 bear market contraction produced deeper declines. But unlike those episodes, this one has no single policy catalyst. It is the compound result of a lower bitcoin price, rising energy costs, post halving revenue compression, and a structural shift in how mining companies view their own business.

The capitulation is visible across every metric: hashrate, difficulty, miner selling, and hashprice. What makes this cycle different is what comes next. The miners who survive are not simply waiting for higher bitcoin prices. They are converting their facilities into AI data centers.

How difficulty measures mining health

Bitcoin’s difficulty adjustment is one of the protocol’s most elegant mechanisms. Every 2,016 blocks, roughly every two weeks, the network recalculates how hard it is to mine a new block. If blocks arrived faster than one every ten minutes during the previous epoch, difficulty increases. If they arrived slower, difficulty decreases. The system exists to keep block production steady regardless of how much computing power is pointed at the network.

When difficulty falls, it means hashrate has left the network. Miners have switched off machines, either because their operating costs exceed their revenue or because they have found more profitable uses for their power capacity. A falling difficulty makes mining easier for the operators who remain, temporarily improving their economics until the incentive draws hashrate back.

The current 19.9% decline from peak is notable for both its depth and duration. Bitcoin Magazine Pro’s data shows the downward trend extending approximately 287 days, making it one of the longest sustained mining contractions in bitcoin’s history. The July 25 adjustment of negative 0.74% was the ninth downward adjustment of 2026. The previous major drop in June was 10.09%, which ranked as bitcoin’s 11th largest single downward adjustment ever, reducing difficulty from 138.96 trillion to 124.93 trillion.

Difficulty has also turned negative on a year over year basis for only the second time in bitcoin’s history. The previous instance followed China’s 2021 mining ban, when authorities forced an estimated 50% of global hashrate offline in a matter of weeks. That comparison is instructive: the current decline has reached similar severity without any government ban, driven entirely by market forces.

The economics behind the shutdown

The fundamental problem is arithmetic. After the April 2024 halving, miners receive 3.125 BTC per block, half what they earned before. That reduction was expected. What was not expected was that bitcoin’s price would fail to compensate.

Bitcoin traded near $63,100 on July 31, down approximately 47% over 12 months and nearly 50% below its October 2025 record. For miners, this price decline arrives on top of the halving’s structural revenue cut. The combined effect has been devastating for operators running older hardware or paying higher electricity rates.

The math is stark. Before the halving, a miner producing one block earned 6.25 BTC. At bitcoin’s October 2025 peak near $120,000, that block was worth $750,000. Today, the same miner earns 3.125 BTC per block at a price near $63,100, yielding approximately $197,000. That is a 74% decline in per block dollar revenue in less than a year. No industry can absorb that kind of revenue compression without significant operational fallout.

Transaction fees, which historically provide a secondary revenue stream for miners, have not offset the decline. Fee revenue as a percentage of total mining revenue has remained in the low single digits through most of 2026, well below the spikes that accompanied the inscription boom in late 2023 and early 2024. The fee market has normalized, removing what had briefly appeared to be a structural supplement to block rewards.

Hashprice, which measures the expected daily revenue from one petahash of computing power, stood near $32 per PH/s per day in late July. That figure sits below the breakeven threshold for many operations. CoinShares estimated in March 2026 that 15% to 20% of the global mining fleet was operating at a loss. Older machines, including models from the Antminer S19 generation, cannot generate positive cash flow at current prices unless operators have electricity costs below approximately five cents per kilowatt hour.

The result is a fleet rationalization. Miners with newer hardware, primarily the Antminer S21 and comparable models, continue to operate profitably at current prices. Miners with older hardware and higher power costs are shutting down, selling their bitcoin reserves, or converting their facilities to other uses. The 12% decline in hashrate from the late 2025 peak of over one zettahash per second to approximately 868 EH/s by late July reflects this ongoing culling.

Record bitcoin sales by miners

The selling pressure from mining companies has been extraordinary. Publicly traded miners sold more than 32,000 BTC in the first quarter of 2026, a single quarter record that exceeded their combined sales for all of 2025. The total also surpassed the roughly 20,000 BTC sold during Q2 2022, when the Terra Luna collapse sent bitcoin below $20,000.

The individual disclosures paint a clear picture of the pressure. Riot Platforms sold 3,778 BTC in Q1 at an average price near $76,626, generating approximately $289.5 million, while producing only 1,473 coins in the same period. Core Scientific liquidated roughly 1,900 BTC worth about $175 million in January alone. Cango sold 2,000 BTC in March for approximately $143 million, using proceeds to retire bitcoin backed loans.

In a single week during Q1, MARA, Genius Group, and Nakamoto Holdings revealed combined sales of more than 15,000 coins. These were not routine sales of freshly mined production to cover electricity bills. They were drawdowns of treasury reserves that companies had previously chosen to hold.

The aggregate miner reserve, the total bitcoin held by mining companies, has been declining since 2023. It fell from more than 1.86 million BTC at the end of that year toward roughly 1.8 million by mid 2026. The sustained drawdown suggests that this is not opportunistic selling but a structural shift in how mining companies manage their balance sheets.

The selling also reflects the debt burden that many miners accumulated during the 2024 and early 2025 expansion cycle. Companies borrowed against their bitcoin holdings and future production to finance fleet upgrades and facility construction. As bitcoin’s price fell and revenue declined, those loans required either refinancing at unfavorable terms or liquidation of the bitcoin collateral. Cango’s March sale of 2,000 BTC was explicitly used to retire bitcoin backed loans, a pattern that has repeated across the industry.

The irony is that miner selling itself contributes to the price pressure that makes mining less profitable. When miners sell tens of thousands of bitcoin into the market over a single quarter, they add supply at a time when demand is already weakened by broader market conditions. The selling becomes self reinforcing: lower prices lead to more selling, which pushes prices lower, which forces more machines offline, which triggers more selling of treasury reserves to cover fixed costs.

The AI pivot

The most significant development in the mining industry is not about bitcoin at all. It is about artificial intelligence.

Mining companies operate large scale power infrastructure in locations with grid access, cooling capacity, and favorable energy contracts. Those same characteristics are exactly what AI data center operators need. The realization has transformed the investment thesis for publicly traded miners, turning them from pure bitcoin proxies into energy infrastructure companies.

Hut 8 provides the most dramatic example. The company signed a second 15 year lease on July 20 for 352 megawatts at its Beacon Point campus in Texas. The agreement raised the campus’s base term contract value to $19.6 billion and Hut 8’s total contracted AI portfolio to $26.6 billion. Initial delivery for the second phase is scheduled for Q2 2028. Hut 8’s shares more than quadrupled over the preceding 12 months and rose 11% after the announcement.

Core Scientific followed on July 28 with an AMD partnership anchored by 15 year agreements covering approximately 530 MW. The company said its total leased customer capacity had reached roughly 1.1 GW, representing more than $24 billion in potential contracted revenue.

TeraWulf’s transition is already generating revenue. The company reported $21 million in AI and high performance computing hosting revenue in Q1 2026, surpassing its bitcoin mining revenue of less than $13 million for the first time. HIVE Digital announced a $2.55 billion AI super factory project near Toronto designed to host more than 100,000 GPUs.

The scale of these AI commitments dwarfs the bitcoin mining operations they are displacing. Hut 8’s $26.6 billion in contracted AI revenue over 15 years exceeds what the company could plausibly earn from bitcoin mining over the same period at current prices and difficulty levels.

The pivot is not limited to North America. Mining operators in the Nordics, the Middle East, and parts of Central Asia are exploring similar conversions, attracted by the same logic: AI workloads pay more per megawatt hour than bitcoin mining and provide contractual revenue certainty that bitcoin mining cannot offer. A 15 year lease agreement with a hyperscaler eliminates the price volatility, halving risk, and difficulty uncertainty that define the bitcoin mining business.

The infrastructure requirements are different, however. AI data centers need higher power density, better cooling, more reliable uptime guarantees, and enterprise grade networking that most mining facilities were not built to provide. The conversion from mining to AI hosting requires significant capital expenditure, which is part of why miners are selling bitcoin reserves and issuing equity. The transition is not free, and companies that underestimate the engineering and capital requirements may find themselves stuck between a declining mining business and an AI hosting business that is not yet ready to generate revenue.

Why mining stocks diverged from bitcoin

The AI pivot has broken the historical relationship between mining stocks and bitcoin’s price. A basket of bitcoin mining equities gained 56% during the early months of 2026 while bitcoin fell 17%, according to research cited by industry analysts. That divergence would have been unthinkable two years ago, when mining stocks moved in lockstep with bitcoin’s price, only with greater amplitude.

Investors are now valuing these companies on their power contracts, real estate, and AI revenue potential, not on their bitcoin production. The market is pricing in a future where bitcoin mining is a secondary revenue stream for companies whose primary business is providing power and infrastructure for artificial intelligence workloads.

This creates an ironic dynamic for bitcoin’s network security. The same companies that built the infrastructure securing the bitcoin network are now economically incentivized to redirect that infrastructure toward AI. Every megawatt that moves from mining to AI hosting reduces the hashrate protecting bitcoin’s blockchain. The difficulty adjustment compensates for the loss automatically, but the trend raises questions about the long term security implications if mining becomes a marginal activity for what were once dedicated mining companies.

The counterargument is that the AI revenue stream makes these companies more financially resilient, which ultimately benefits the bitcoin network. A mining company with $26 billion in contracted AI revenue can afford to keep mining bitcoin through price downturns that would force a pure play miner to shut down entirely. The AI business subsidizes the mining operation.

The historical parallel is not perfect, but it is instructive. After the 2021 China ban, difficulty dropped more than 50% before recovering within months as displaced miners relocated and reconnected. That episode proved that bitcoin’s difficulty adjustment mechanism works as designed: when enough hashrate leaves, difficulty falls until mining becomes profitable again for the remaining operators, creating an economic incentive for hashrate to return. The current episode tests whether the same self correcting mechanism applies when the departure of hashrate is driven not by a ban but by a better economic opportunity. Miners who leave for AI may not return even if bitcoin prices recover, because the AI revenue exceeds what bitcoin mining can offer.

What capitulation historically signals

Miner capitulation has historically preceded bitcoin price recoveries. The logic is straightforward: when the weakest miners shut down and sell their reserves, the selling pressure eventually exhausts itself. Difficulty falls, making mining cheaper for survivors. The supply of newly mined bitcoin continues at a fixed rate regardless of hashrate, but the forced selling from distressed operators slows as those operators exit the market.

The 2022 capitulation followed this pattern. Miners sold aggressively through Q2 and Q3, difficulty fell, and by early 2023, bitcoin had begun a sustained recovery that eventually carried prices to new all time highs. Proponents of the capitulation thesis argue that the current period will resolve similarly: the pain is intense but temporary, and the difficulty adjustment ensures that mining always returns to profitability for the marginal operator.

The structural difference this time is the AI alternative. In previous cycles, sidelined mining capacity had no productive alternative use. It simply sat idle until bitcoin prices made mining profitable again. Today, that capacity has a buyer willing to pay more, which means the recovery mechanism may not function as cleanly as it has in the past.

What to watch

- The next difficulty adjustment. Whether difficulty continues to fall or stabilizes will signal whether the current round of miner shutdowns has run its course. A sustained difficulty increase would indicate that surviving miners are expanding or that sidelined operators are reconnecting.

- Q2 miner selling data. The 32,000 BTC sold in Q1 set a record. Whether Q2 selling accelerated, stabilized, or declined will indicate the severity of the remaining financial pressure on listed operators.

- Bitcoin price relative to production cost. Some analysts estimate the average production cost for the global mining fleet near $80,000. Bitcoin trading at approximately $63,100 means a significant portion of miners are operating below cost. A price recovery above $80,000 would alleviate much of the current pressure.

- AI data center construction timelines. The announced deals from Hut 8, Core Scientific, and others involve multi year construction timelines. Whether these projects proceed on schedule and begin generating revenue will determine whether the AI pivot delivers on its promise.

- Regulatory treatment of dual use facilities. Mining companies that operate both bitcoin mining and AI hosting from the same campuses may face different regulatory frameworks for each activity. How jurisdictions classify and regulate these hybrid operations could affect the economics of the pivot.

Frequently asked questions

How much has bitcoin mining difficulty dropped?

Bitcoin mining difficulty has fallen 19.9% from its all time peak of approximately 156 trillion set in November 2025 to 126.23 trillion as of the July 25, 2026 adjustment. This is the third deepest decline since dedicated ASIC mining hardware became standard.

Why is bitcoin mining difficulty falling?

Difficulty falls when miners switch off their machines, which slows block production. The current decline results from lower bitcoin prices, post halving revenue cuts, high electricity costs, and mining companies redirecting power capacity toward AI data centers.

How much bitcoin have miners sold in 2026?

Publicly traded miners sold more than 32,000 BTC in the first quarter of 2026 alone, a single quarter record. This exceeded their combined sales for all of 2025 and surpassed the roughly 20,000 BTC sold during the 2022 bear market.

What is hashprice and why does it matter?

Hashprice measures the expected daily revenue a miner earns per unit of computing power (per petahash per second). It stood near $32 per PH/s per day in late July 2026, below the breakeven threshold for many operators with older hardware.

Why are mining stocks going up while bitcoin is falling?

Mining stocks have diverged from bitcoin because investors are valuing these companies as AI and energy infrastructure operators. A basket of mining equities gained 56% in early 2026 while bitcoin fell 17%, driven by multi billion dollar AI data center contracts.

Which mining companies are pivoting to AI?

Hut 8 has $26.6 billion in contracted AI portfolio value. Core Scientific has roughly 1.1 GW in leased AI capacity worth over $24 billion. TeraWulf’s AI hosting revenue surpassed its mining revenue in Q1 2026. HIVE Digital announced a $2.55 billion AI super factory near Toronto.

What is the bitcoin mining difficulty adjustment?

The difficulty adjustment is an automatic mechanism that recalibrates how hard it is to mine a bitcoin block every 2,016 blocks, roughly every two weeks. It keeps block production steady at approximately one block every ten minutes regardless of total network hashrate.

Is bitcoin mining still profitable in 2026?

For miners with the newest hardware and low electricity costs, mining remains profitable. CoinShares estimated in March 2026 that 15% to 20% of the fleet was operating at a loss. The breakeven threshold for older machines sits near $35 per PH/s per day, above the current hashprice.

Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice. The information presented reflects publicly available data as of August 1, 2026. Readers should conduct their own research and consult qualified professionals before making financial decisions.

The United States has sanctioned Iranian exchanges, frozen nearly $1 billion in cryptocurrency, and traced $3.84 billion in Iran-linked flows through a single offshore exchange, exposing the scale of sanctions evasion through digital assets.

Summary

- The US Treasury has sanctioned four Iranian cryptocurrency exchanges, including Nobitex, which handles approximately 50% of Iran’s crypto trading volume, as part of Operation Economic Fury launched in April 2026.

- Treasury has seized or frozen nearly $1 billion in cryptocurrency from Iranian exchanges and wallets since the US-Israeli strikes on Tehran in February, including a $344 million USDT freeze in April and a $131 million freeze in July.

- The Wall Street Journal reported that Iran-linked entities moved more than $3.84 billion through crypto exchange CoinEx since 2019, with investigators tracing flows from Central Bank of Iran wallets that connected to the North Korean Bybit hack.

- Chainalysis estimated that Iranian crypto outflows reached $4.18 billion in 2025, a 70% year over year increase, as the rial collapsed and citizens sought alternatives to the sanctioned banking system.

- The enforcement campaign reveals both the capabilities and limitations of crypto sanctions: centralized stablecoins like USDT can be frozen by issuers, but decentralized protocols and cross chain transactions continue to provide routes for moving value beyond government control.

The numbers tell the story before the analysis begins. Nearly $1 billion in Iranian cryptocurrency seized by the US Treasury. More than $3.84 billion in Iran-linked flows traced through a single offshore exchange. Iranian crypto outflows of $4.18 billion in a single year. Four domestic Iranian exchanges sanctioned. Executives added to the OFAC list. Central Bank of Iran wallets frozen on the Tron network.

These figures, accumulated over the first half of 2026, describe the largest and most technically sophisticated sanctions enforcement campaign ever conducted through blockchain infrastructure. The US government is not merely identifying Iranian crypto activity. It is actively seizing, freezing, and blocking it at multiple points in the financial chain. The question is whether the campaign is working or whether it is simply documenting the scale of a problem it cannot contain.

The answer is probably both. The United States has developed meaningful new tools for sanctions enforcement on public blockchains, and it is deploying them at unprecedented scale. At the same time, the gap between what investigators can see and what they can stop is wide and growing. Iranian crypto activity grew 70% year over year in 2025 even as US surveillance capabilities expanded. Every enforcement action generates a public record of Iranian evasion methods, which Iranian operators then adapt against. The cat-and-mouse dynamic is running faster than the enforcement side can respond.

Operation Economic Fury

The enforcement campaign has a name: Economic Fury. Treasury Secretary Scott Bessent introduced it on April 14, 2026, as the financial arm of the US response to the military conflict that began with joint US and Israeli strikes on Tehran in February. The campaign targets Iran’s use of cryptocurrency exchanges, wallets, and traditional financial networks that officials accuse of supporting sanctions evasion and military financing.

The campaign followed months of intelligence gathering that began before the military strikes. Treasury officials had been tracking Iranian crypto networks since at least 2024, when Chainalysis and TRM Labs began publishing research on the scale of Iranian stablecoin adoption. The strikes accelerated the timeline from monitoring to action.

The first major crypto action came in April, when Tether froze approximately $344 million in USDT across two Tron wallets after US authorities linked the addresses to Iranian networks. One wallet held about $213 million; the other contained roughly $131 million. Blockchain analysis found transaction patterns associated with wallets linked to Iran’s Islamic Revolutionary Guard Corps and intermediaries connected to the Central Bank of Iran.

In June, Treasury escalated by sanctioning four Iranian cryptocurrency exchanges: Nobitex, Wallex, Bitpin, and Ramzinex. Nobitex, the largest, handles approximately 50% of Iran’s cryptocurrency trading volume according to Chainalysis and claims to serve 11 million users. Treasury also added Nobitex CEO Seyed Ali Khoee and chairman Amir Hossein Rad to the OFAC sanctions list, making them personally subject to asset freezes and travel restrictions.

In July, Treasury froze an additional $131 million in USDT held in four Tron wallets tied to the Central Bank of Iran. Bessent said on X that Treasury remained “committed to disrupting and degrading Iran’s illicit financial activities, including its abuse of digital assets.”

By late July, Bessent disclosed that the cumulative total of cryptocurrency seized or frozen from Iranian sources since the conflict began had approached $1 billion. The figure, while significant, represents assets identified by investigators and does not include Iranian-linked cryptocurrency that moved through compliant exchanges and was not captured in enforcement actions.

The CoinEx connection

While Treasury focused on domestic Iranian exchanges, a parallel investigation exposed the offshore dimension of Iran’s crypto network. On June 24, the Wall Street Journal reported that Iran-linked entities had moved more than $3.84 billion through crypto exchange CoinEx since 2019.

The investigation, citing TRM Labs and public on-chain data, found that CoinEx had become one of the primary routes for moving funds outside US sanctions. More alarmingly, investigators traced activity from two wallets controlled by the Central Bank of Iran and found links to assets stolen from Bybit by North Korean hackers in what was one of the largest thefts in crypto history, involving approximately $1.5 billion in virtual assets.

CoinEx denied any knowledge of Iran-linked activity. The exchange said that on-chain fund flows through a platform do not prove knowledge, support, or participation. It also said it had strengthened Iran-related risk reviews, geo-fencing, sanctions screening, and transaction monitoring. CoinEx has not been subject to new US sanctions as of this writing, but the WSJ report placed it under heightened regulatory scrutiny.

The $3.84 billion figure is notable not just for its size but for its duration. The flows spanned seven years, from 2019 through 2026, covering periods when international attention to Iranian crypto activity was already high. The Financial Action Task Force had placed Iran on its blacklist for most of that period. The fact that billions in Iranian linked flows continued through a single exchange for seven years without triggering enforcement action until journalists reported it raises questions about the gap between blockchain transparency and operational enforcement.

TRM Labs data cited in the WSJ report also showed that CoinEx was not the only offshore exchange processing Iranian flows. Several smaller platforms with limited compliance infrastructure handled significant volumes. The concentration at CoinEx reflects the exchange’s combination of low fees, minimal identity verification requirements during the relevant period, and availability in jurisdictions where Iranian users could access the platform without VPN restrictions.

The CoinEx case illustrates a fundamental challenge in crypto sanctions enforcement. Centralized exchanges operate as choke points where authorities can intervene, but only if the exchange cooperates or is within jurisdictional reach. CoinEx is based outside US jurisdiction. Its compliance response, strengthening internal controls after public reporting, is the kind of reactive posture that allows billions in flows before any intervention occurs.

The scale of Iranian crypto adoption

The enforcement actions unfold against a backdrop of massive and growing cryptocurrency adoption within Iran. Chainalysis estimated that Iranian crypto outflows reached $4.18 billion in 2025, a 70% increase over the previous year. The surge coincided with the collapse of the Iranian rial, which lost approximately 40% of its value against the dollar during the same period, and intensifying sanctions that cut Iran further from the global banking system.

For ordinary Iranians, cryptocurrency serves the same function it serves in other countries experiencing currency devaluation and capital controls: a way to preserve savings and move value across borders. The distinction between legitimate civilian use and sanctions evasion is difficult to draw at scale, and US enforcement actions have not attempted to make the distinction. When Treasury sanctions an exchange like Nobitex that serves 11 million users, the action affects both the IRGC operative moving military funds and the shopkeeper converting rials to USDT to protect against inflation.

Reuters reported that Nobitex was founded in 2018 by brothers Ali and Mohammad Kharrazi, who used the surname Aghamir, and that the pair belong to a politically connected Iranian family. Nobitex rejected the characterization, describing itself as a private and independent company with no relationship to the IRGC, Iran’s central bank, or other state institutions.

The platform’s scale suggests that Iranian crypto activity is not a marginal phenomenon. If Nobitex alone handles 50% of Iran’s crypto trading and processes volumes proportional to the $4.18 billion in outflows that Chainalysis tracked, the total Iranian crypto economy is likely larger than what any single data provider captures.

Tron is the dominant blockchain for Iranian USDT activity, but on-chain analysis shows significant use of Ethereum-based assets and bitcoin for larger transactions. Iran’s geographic position as a major energy producer gives it access to cheap electricity that has long sustained domestic bitcoin mining. Even under US pressure, Iran’s mining industry continues to produce bitcoin that is then sold through non-compliant channels, mixing mined coins with purchased ones in ways designed to obscure provenance.

What the $4.18 billion Chainalysis figure captures is primarily exchange-mediated activity. Peer-to-peer crypto transactions, informal hawala-style networks that use crypto as a settlement layer, and government-level transactions that go through diplomatic channels are not fully reflected in the data. The total Iranian crypto economy, combining formal exchange activity with informal flows, is likely substantially larger than the $4 billion headline figure cited by US officials.

How stablecoin controls enable enforcement

The most effective tool in Treasury’s crypto sanctions arsenal is not blockchain analysis or traditional intelligence. It is the freeze function built into centralized stablecoins. USDT, issued by Tether on various blockchains including Tron, contains issuer level controls that allow Tether to freeze specific addresses, preventing the stablecoins from being transferred regardless of who holds the private keys.

Every major freeze in the Iran campaign has involved USDT on Tron. The $344 million April action and the $131 million July action both targeted Tron wallets holding USDT. The pattern is not coincidental. Tron’s low transaction fees and fast settlement have made it the preferred blockchain for USDT transfers in emerging markets, including Iran. That same preference concentrates Iranian stablecoin holdings in a token that the issuer can freeze on demand.

This creates an asymmetry that favors enforcement. Iranian entities using USDT accept a counterparty risk that bitcoin users do not face: Tether can render their holdings inaccessible with a single transaction. The $475 million in USDT freezes during the Economic Fury campaign shows that this risk is not theoretical.

Tether’s cooperation with US authorities is not legally required in the traditional sense. Tether is incorporated offshore and is not subject to direct US regulatory jurisdiction. But the company has consistently complied with US law enforcement freeze requests, a pattern that reflects both the practical reality of wanting US banking relationships and the risks of being designated as a sanctions violator under OFAC regulations. Tether’s voluntary compliance with freeze requests is one reason why USDT on Tron became the enforcement mechanism of choice in the Iran campaign.

The limitation is that the freeze mechanism only works for centralized stablecoins. Iran has also adopted bitcoin and other decentralized assets for cross border transactions, including accepting cryptocurrency for weapons sales. Bitcoin cannot be frozen by any issuer. Decentralized exchanges and cross chain bridges provide routes that do not pass through compliant intermediaries. The freeze function addresses the largest and most visible flows but not the entire ecosystem.

The Bybit hack connection

The WSJ’s discovery that Central Bank of Iran wallets were linked to assets from the North Korean Bybit hack adds a dimension that extends beyond Iran sanctions. It suggests that the networks facilitating Iranian sanctions evasion overlap with the infrastructure used for state sponsored cybercrime.

The FBI attributed the Bybit hack to North Korean actors who stole approximately $1.5 billion in virtual assets. The hackers converted stolen funds into bitcoin and other tokens across many wallets, using decentralized protocols including THORChain to obfuscate the trail. THORChain processed almost $3 billion in trading volume from swaps tied to stolen Bybit assets, according to on-chain tracking.

The intersection of Iranian sanctions evasion and North Korean cybercrime through a common exchange infrastructure raises questions about whether these networks are coordinated or simply convergent. Two sanctioned states using similar crypto channels to evade financial restrictions could reflect shared operational methods, shared intermediaries, or merely the natural tendency of illicit actors to gravitate toward the same low compliance venues.

For regulators, the connection strengthens the argument for applying comprehensive sanctions screening and transaction monitoring requirements to all centralized exchanges, regardless of jurisdiction. For the crypto industry, it highlights the reputational and regulatory risk of operating exchanges that attract illicit flows through weak compliance.

The Bybit connection also matters for how crypto exchanges frame their role in global financial crime. For years, exchanges in non-US jurisdictions argued that sanctions compliance was a US issue, not a global one. The discovery that the same wallets connected both Iranian government funds and North Korean cybercrime proceeds changes the argument. State-sponsored actors from multiple sanctioned countries are using the same infrastructure, which pushes exchanges into a position where choosing not to comply with US sanctions implicitly means becoming a service provider for state-level threat actors.

FinCEN and OFAC have signaled in recent regulatory correspondence that they intend to pursue secondary sanctions against offshore exchanges that knowingly or negligently process flows from sanctioned jurisdictions. Whether CoinEx, which handled $3.84 billion in Iran-linked flows, faces secondary sanctions action will be a test case for how aggressively that posture is applied in practice.

The enforcement paradox

The Iran crypto sanctions campaign reveals a paradox at the heart of blockchain based enforcement. The same transparency that allows investigators to trace $3.84 billion in flows through CoinEx or identify Central Bank of Iran wallets on Tron also shows the scale of activity that proceeded without intervention for years.

Treasury’s ability to freeze USDT, sanction exchanges, and trace on chain activity represents a significant expansion of sanctions enforcement capabilities compared to the traditional banking system. But the $4.18 billion in Iranian crypto outflows in 2025 alone suggests that enforcement is capturing a fraction of total activity. The actions are significant in dollar terms but may represent less than 25% of annual Iranian crypto flows based on available estimates.

Critics of the campaign argue that sanctioning exchanges like Nobitex primarily harms ordinary Iranians who have no alternative to crypto for preserving savings. Proponents argue that the distinction between civilian and military use cannot be drawn cleanly when the Iranian government uses the same financial networks as the civilian population, and that targeting the infrastructure is the only viable method at scale.

The campaign also faces a structural limitation: as enforcement increases on centralized platforms, activity migrates to decentralized alternatives. Each successful USDT freeze teaches Iranian operators to diversify into bitcoin, privacy coins, or decentralized stablecoins that cannot be frozen. The enforcement action itself accelerates the adaptation that makes future enforcement harder.

What to watch

- Additional exchange sanctions. CoinEx has not been sanctioned despite the WSJ report. Whether Treasury acts against offshore exchanges that process Iranian flows will test the limits of US jurisdictional reach.

- The total seized figure. Treasury’s $1 billion in seized crypto is a running total. Whether it continues to grow at the current pace or plateaus will indicate whether enforcement is keeping up with the flow.

- Migration to decentralized platforms. If Iranian entities shift from USDT on Tron to bitcoin, decentralized stablecoins, or privacy focused protocols, the freeze mechanism that has powered most seizures will become less effective.

- Regulatory response to the Bybit-Iran link. The connection between Iranian sanctions evasion and North Korean cybercrime through shared exchange infrastructure may drive new compliance requirements for exchanges globally.

- Impact on Iranian civilians. The sanctions affect both government entities and ordinary citizens who use crypto as an inflation hedge. How the humanitarian dimension is addressed, or not addressed, will influence the political sustainability of the campaign.

Frequently asked questions

How much Iranian cryptocurrency has the US seized?

The US Treasury has seized or frozen nearly $1 billion in cryptocurrency from Iranian exchanges and wallets since the military conflict began in February 2026. Major actions include a $344 million USDT freeze in April and a $131 million freeze in July, both involving wallets on the Tron network.

What is Operation Economic Fury?

Operation Economic Fury is a US Treasury campaign launched on April 14, 2026, targeting Iran’s financial networks including cryptocurrency exchanges, wallets, and traditional banking channels. The campaign is the financial arm of the US response to the military conflict with Iran.

Which Iranian crypto exchanges were sanctioned?

Treasury sanctioned four Iranian exchanges in June 2026: Nobitex, Wallex, Bitpin, and Ramzinex. Nobitex, the largest, handles approximately 50% of Iran’s crypto trading volume and claims 11 million users. Two Nobitex executives were also added to the OFAC sanctions list.

How much money flowed through CoinEx from Iran?

The Wall Street Journal reported that Iran-linked entities moved more than $3.84 billion through crypto exchange CoinEx since 2019, based on TRM Labs data and public on chain analysis. CoinEx denied knowledge of Iran-linked activity and said it strengthened compliance controls.

How does the US freeze cryptocurrency?

The US leverages the freeze function built into centralized stablecoins like USDT. Tether can freeze specific wallet addresses, preventing tokens from being transferred. This mechanism does not work for decentralized assets like bitcoin, which cannot be frozen by any issuer.

What is the connection between Iran and the Bybit hack?

Investigators traced activity from Central Bank of Iran wallets to assets stolen from Bybit by North Korean hackers, who took approximately $1.5 billion in virtual assets. The connection suggests that Iranian sanctions evasion networks and North Korean cybercrime infrastructure may share common exchange intermediaries.

How much crypto do Iranians use?

Chainalysis estimated that Iranian crypto outflows reached $4.18 billion in 2025, a 70% increase year over year. The surge coincided with the collapse of the Iranian rial and intensifying sanctions that cut Iran from the global banking system.

Can Iran avoid crypto sanctions?

Centralized stablecoins can be frozen, but decentralized assets like bitcoin cannot. As enforcement increases on centralized platforms, Iranian entities are expected to migrate toward decentralized protocols, privacy coins, and cross chain bridges that operate beyond the reach of issuer level controls.

Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice. The information presented reflects publicly available data as of August 1, 2026. Readers should conduct their own research and consult qualified professionals before making financial or legal decisions.

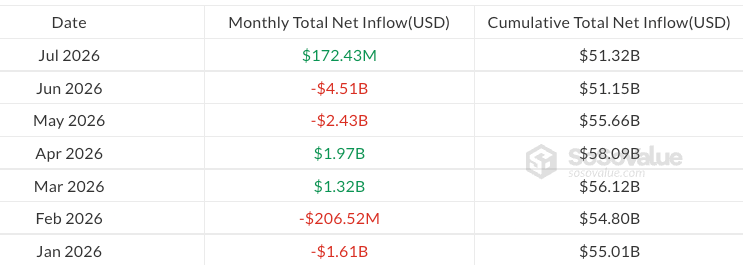

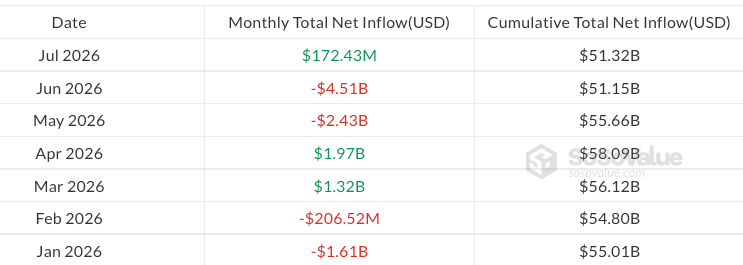

US-listed spot Bitcoin exchange-traded funds (ETFs) finished July with net inflows, even after a late-month pullback that underscored how cautious investors remained going into August. According to SoSoValue, the funds brought in $172.4 million in net inflows during July—enough to reverse two straight months of outflows.

The month’s positive result was tempered by volatility in the final stretch. On the final Friday of July, spot Bitcoin ETFs logged a $265.4 million net outflow, the largest single-day withdrawal since July 13, suggesting the rebound in demand was not fully sustained.

Key takeaways

- Spot Bitcoin ETFs took in $172.4 million in net inflows in July, reversing two consecutive months of outflows, according to SoSoValue.

- Despite the monthly gain, the last Friday of July saw a $265.4 million net outflow—Bitcoin ETFs’ biggest daily withdrawal since July 13.

- Year-to-date flows remain negative: US spot Bitcoin ETFs have recorded about $5.29 billion in net outflows in 2026.

- Ether ETFs were steadier, ending July with $365.2 million in net inflows and a four-week inflow run, per SoSoValue.

- XRP ETFs also posted continued demand, adding $27.3 million in net inflows in July while recording their fifth positive month of 2026.

Bitcoin ETFs return to inflows—weak finish signals caution

SoSoValue data indicates July’s net inflow improved the outlook for spot Bitcoin ETF investors after a difficult stretch. The article notes that investors pulled nearly $7 billion in aggregate outflows over the previous two months, including what earlier reporting described as the largest monthly outflow of 2026 in June, totaling $4.5 billion (coverage referenced in the original piece: Cointelegraph).

Still, the late-month selling pressure matters for how traders may read positioning. The $265.4 million outflow on the final Friday of July not only flipped daily flows negative, but also marked the largest daily withdrawal since mid-July. In practical terms, that pattern suggests July’s inflows were vulnerable to sudden risk-off behavior—important for anyone tracking ETF flow-driven momentum.

On a broader time frame, weekly flows also turned negative at the end of the month. For the week ending July 31, Bitcoin ETFs recorded a $61.53 million outflow after three consecutive weeks of inflows. That shift reinforces the message that demand improved during parts of July, but participation thinned as the month closed.

Where 2026 stands: cumulative outflows stay elevated

Even with a positive July, the year-to-date picture for US-listed spot Bitcoin ETFs remains firmly in the red. Based on the figures cited from SoSoValue, Bitcoin ETFs have accumulated roughly $5.29 billion in net outflows in 2026.

The monthly distribution shows a market that has not found consistent footing. March, April, and July are the only months reported as positive so far this year, bringing total inflows of $3.46 billion. Meanwhile, the remaining months—January, February, May, and June—accounted for outflows totaling about $8.75 billion.

Despite that imbalance, the products have still attracted meaningful long-term net capital since launch. The article states that US spot Bitcoin ETFs have drawn $51.32 billion in cumulative net inflows, and that total net assets reached $76.29 billion at the end of July.

Ether ETFs keep the momentum going

While Bitcoin ETFs faced renewed selling pressure at the end of July, Ether-related products showed comparatively steadier demand. According to SoSoValue, US spot Ether ETFs ended July with $365.2 million in net inflows and maintained four consecutive weeks of inflows.

That marks a second month of positive flows for Ether ETFs in 2026 after April’s $356 million inflow. Yet, the recovery is not enough to fully erase earlier weakness: despite this improvement, the article notes Ether ETFs are still around $1.1 billion in net outflows year to date.

For investors, the contrast between Bitcoin and Ether flows can be informative. It suggests that even if market-wide sentiment is cautious, some capital has been willing to rotate into Ether exposure—at least at the ETF level—rather than staying entirely risk-off.

XRP ETFs post another positive month

Other altcoin ETF categories also appear to have avoided the same late-month stress seen in Bitcoin. XRP ETFs, in particular, maintained steadier activity. The article reports that XRP ETFs recorded $27.3 million in inflows during July and marked their fifth positive month of 2026.

Year-to-date, XRP ETFs have generated about $343 million in net inflows, positioning them as one of the stronger-performing crypto ETF segments in the market this year, at least based on the net flow figures cited.

In a market where ETF flows can swing quickly with broader macro conditions and crypto price action, continued positive monthly demand for XRP products can serve as a signal that some investors are still finding specific altcoin exposure compelling—even when Bitcoin faces repeated episodes of volatility.

Going forward, traders and long-term holders will likely watch whether Bitcoin ETF demand can withstand similar end-of-month selling pressure, especially since weekly flows flipped negative as July closed. At the same time, the relative stability in Ether and XRP inflows may keep comparing as a useful read on whether the next wave of capital concentrates in Bitcoin or broadens across the rest of the crypto ETF complex.

Trading volume across South Korea’s five major won-based crypto exchanges fell 54.6% year over year in the first half of 2026 as liquidity became increasingly concentrated on market leader Upbit.

Summary

- Five major exchanges recorded $366.58 billion in first-half trading volume.

- Combined volume fell 54.6% year over year, according to NexBlock.

- Upbit expanded its July market share to 67.4% despite lower trading activity.

- South Korea will introduce a 22% crypto gains tax on Jan. 1, 2027.

South Korea crypto volume drops below $367B

Upbit, Bithumb, Coinone, Korbit and Gopax generated about $366.58 billion in combined trading volume during the first six months of the year, NexBlock reported. That represented a 54.6% decline from the corresponding period in 2025.

The contraction continued in July. From July 1 through July 27, the five exchanges recorded cumulative trading volume of approximately 17.34 trillion won, down 16.9% from the same period in June.

The figures point to weaker activity across South Korea, one of Asia’s most active retail crypto markets. They also show that lower overall volume has not affected all exchanges equally.

Upbit processed about 11.69 trillion won during the July period. Its trading volume fell 10%, but its market share increased from 62.3% to 67.4% as competing platforms suffered steeper declines.

Bithumb recorded approximately 4.71 trillion won in volume. Its share of the five-exchange market dropped from 30.7% to 27.1%, widening the gap between Upbit and Bithumb to 40.3 percentage points.

Upbit gains as liquidity becomes concentrated

NexBlock attributed the changing competitive landscape to liquidity moving toward the largest platforms during the broader market slowdown.

Deep liquidity can attract more traders by supporting larger orders with less price slippage. That advantage can reinforce the position of leading exchanges when overall activity declines, leaving smaller platforms with fewer trades and thinner order books.

Coinone, Korbit and Gopax now face growing pressure to differentiate themselves beyond retail spot trading. According to NexBlock, smaller exchanges are exploring partnerships with securities firms, institutional services and internal restructuring.

Future competition could therefore depend less on headline trading volume and more on stablecoin liquidity, regulatory compliance, institutional access and cooperation with traditional financial companies.

For US investors, South Korean exchange data can provide insight into retail demand in a major Asian market, although the won-based platforms primarily serve domestic users. Reduced Korean volume may weaken one source of global altcoin liquidity and price discovery, particularly for tokens that historically attracted strong local trading interest.

Crypto tax could reshape trading activity in 2027

The volume decline comes as South Korea prepares to implement its long-delayed cryptocurrency tax.

Finance Minister Koo Yun-cheol confirmed on July 29 that the government will begin taxing crypto gains on Jan. 1, 2027, as previously scheduled.

“We are pushing forward with the plan to tax cryptocurrency starting next year as scheduled,” Koo said.

Income generated by transferring or lending virtual assets will be classified as other income. Annual gains exceeding 2.5 million won, or about $1,740, will face a 20% national tax, while a local income tax will raise the combined rate to 22%.

Investors who remain below the annual threshold will not owe tax under the framework. Taxpayers are expected to file their first returns in May 2028 for gains earned during 2027.

The policy creates an additional consideration for domestic traders after three previous delays. Its effect on exchange volume will depend partly on how platforms implement transaction reporting and cost-basis calculations before the rules take effect.

Smaller exchanges seek new sources of growth

South Korea is simultaneously expanding state-backed investment in strategic industries, though the initiative is separate from its crypto tax and exchange policies.

The government approved plans for a new account under the Korea Investment Corporation, the country’s sovereign wealth fund. The account will begin with at least 20 trillion won, or approximately $13.7 billion, and may invest domestically in artificial intelligence, data centers and other strategic sectors.

KIC has historically focused on overseas assets. The expanded mandate reflects a wider effort to direct institutional capital toward domestic industries while seeking long-term returns.

For crypto exchanges, the immediate challenge remains rebuilding activity while complying with tighter rules. Upbit’s rising market share suggests smaller platforms may need institutional partnerships, stablecoin services, or structural changes to compete in a market where total trading volume continues to fall.

Crypto World

New York Attorney General Sues Kalshi for Violating State Laws Against Illegal Gambling

New York Attorney General Letitia James has sued prediction markets platform Kalshi for violating state laws against illegal gambling by offering users event contracts on elections, sporting events, and other outcomes.

Kalshi has called the lawsuit “political theater,” while the Commodity Futures Trading Commission (CFTC) has accused the state of trying to “annihilate prediction markets.”

New York Files Lawsuit Against Kalshi

The lawsuit alleges Kalshi operates an illegal gambling operation in New York and asks Kalshi to stop operating in the state, forfeit its illegal gains, pay restitution to users, and pay civil penalties up to three times its gains. James alleges that Kalshi has not obtained a New York State Gaming Commission license to operate in the state.

New York had filed similar lawsuits against Coinbase and Gemini’s prediction market platforms. James said in a statement released Friday:

“New York’s gambling laws protect children from underage betting and help combat gambling addiction. No matter what they call themselves, prediction markets like Kalshi are gambling platforms, plain and simple. We are taking them to court to uphold our laws and protect New Yorkers.”

The latest action comes after the New York State Gaming Commission issued a cease-and-desist order against Kalshi in October 2025. Kalshi responded by suing the regulator in court. However, a judge rejected Kalshi’s request for a preliminary injunction, and the appeals court rejected a subsequent bid to block enforcement action during the appeals process.

Elisabeth Diana, Kalshi’s head of communications, called the action “political theater,” saying:

“It’s sad to see this type of political theater from the leadership in our own state. States can’t just shut down a federally licensed exchange. This would also hurt New Yorkers, who would be driven offshore. We love New York, we love New Yorkers, and New Yorkers love our product.”

The prediction market platform wants to move the lawsuit to Manhattan federal court, stating that it is based in New York. According to court filings, damages and costs could amount to $36 billion, significantly higher than Kalshi’s $22 billion valuation.

CFTC Files Emergency Motion

Prediction markets have gained immense popularity since the 2024 US Presidential elections, and the Commodity Futures Trading Commission (CFTC) has claimed exclusive regulatory oversight over them. The commission has also challenged regulatory attempts by other agencies in nine jurisdictions, including New York.

The regulator filed an emergency motion to block any enforcement action by New York, arguing that it oversteps authority and infringes upon the CFTC’s exclusive authority to regulate contract markets like Kalshi and other prediction market platforms, and threatens to annihilate the industry nationwide.

Kalshi added that by attempting to shut down the platform, New York was subverting the CFTC’s exclusive jurisdiction to regulate prediction market platforms:

“New York seeks to place itself in the position of a nationwide derivatives regulator. Through this action, which seeks to shut Kalshi down nationwide, New York seeks to fundamentally subvert the exclusive jurisdiction of the CFTC.”

Why Does New York See Prediction Markets As Gambling

New York equates Kalshi’s prediction markets with gambling because it allows people to wager on events whose outcomes they do not control. This includes wagering on outcomes like “who wins the Super Bowl” and even reality TV shows.

The state also highlighted that the minimum age under state law for mobile sports betting was 21 and opposed Kalshi allowing 18- to 20-year-olds on its prediction market platform.

New York Governor Kathy Hochul stated:

“Kalshi has chosen to ignore New York’s gaming laws, which exist to protect consumers, prevent problematic gambling, deliver funding for critical public services, and ensure that every company plays by the same rules. This choice has consequences.”

Prediction Markets Gaining Popularity

Despite regulatory scrutiny, prediction markets like Kalshi and Polymarket are gaining significant traction. Kalshi has expanded its blockchain-based infrastructure and launched tokenized prediction markets on Solana. It subsequently added support for multiple blockchain networks.

Prediction markets have also grown beyond sports, allowing users to trade event contracts on real-world outcomes like elections, inflation, interest rate cuts or hikes, entertainment, and even daily temperatures.

The popularity of prediction markets surged during the recently concluded FIFA World Cup 2026. According to Chainalysis, prediction markets processed around $20 billion in trading linked to the sporting event.

Disclaimer: This article is provided for informational purposes only. It is not offered or intended to be used as legal, tax, investment, financial, or other advice.

The uncertainty around the highly anticipated regulatory bill continues with new negotiations in Washington. New ethics proposals and political disagreements threaten the legislation’s chances of becoming law this year.

Prediction markets now assign a much lower probability of becoming law this year, around 31%-35%, down from the 70% peaks earlier this year.

Highly Important Weekend

Popular journalist Eleanor Terrett noted on X earlier today that this weekend will be a “high-stakes waiting game” for supporters of the bill as the White House “considers an ethics counteroffer involving a state attorney general.”

The proposal reportedly centers on one of the bill’s biggest remaining sticking points: whether state attorneys general should retain authority in enforcing certain ethics provisions involving federal officials.

Bipartisan negotiations between Senator Thom Tillis (R-NC) and Arizona Democrat Ruben Gallego continue, as both believe the bill has to contain a stronger ethics package than the one proposed by the White House and two Senate Republicans at the end of July. Terrett cited three sources familiar with the matter, indicating that the initial offer did not receive approval from Tillis, Gallego, and other Democrats.

Instead, they believe state attorneys general should be able to sue the Department of Justice if it fails to enforce ethics laws against federal officials.

One of the issues with the White House’s proposal is that the ethics provisions would remain in force through January 2029, and there are few clues on what happens next.

With the Senate scheduled to begin its August recess next week, experts and observers believe the bill has only a narrow window remaining this year, which is why the odds on prediction markets continue to dwindle. If lawmakers fail to move it forward before the break, the prospects are likely to deteriorate significantly as attention shifts toward the midterm elections.

Saylor Supports

Most key figures in the cryptocurrency industry have expressed support for the bill over the past year or so. Michael Saylor, the Chairman of the world’s largest corporate holder of bitcoin, doubled down in the past 24 hours.

He believes that BTC will succeed with or without the bill, but added that “America needs clarity for digital assets.”

I support advancing the CLARITY Act through bipartisan work to establish clear, durable rules, protect property rights, promote innovation, and strengthen American capital markets. Bitcoin will succeed with or without legislation, but America needs clarity for digital assets. https://t.co/LYqpPb5zKL

— Michael Saylor (@saylor) July 31, 2026

The post CLARITY Act Faces Another Critical Weekend as Passage Odds Slide appeared first on CryptoPotato.

US-listed spot Bitcoin exchange-traded funds (ETFs) finished July in the green despite a late-month wave of selling and BTC price volatility.

Bitcoin ETFs attracted a modest $172.4 million in net inflows in July, reversing two consecutive months of outflows, according to SoSoValue data.

The monthly inflows came despite a volatile end to July, as the funds logged a $265.4 million net outflow on Friday, marking their largest daily withdrawal since July 13.

July’s return to positive territory improved Bitcoin ETF flows after nearly $7 billion in combined outflows over the previous two months, including the largest monthly outflow of 2026 in June at $4.5 billion. However, the weak finish showed investors remained cautious heading into August.

Bitcoin ETFs remain negative in 2026 with $5.29 billion in outflows

Despite a modest net inflow in July, US-listed spot Bitcoin ETFs have recorded around $5.3 billion in net outflows year to date.

March, April and July were the only positive months of 2026, bringing in a combined $3.46 billion in inflows, while January, February, May and June posted outflows totaling about $8.75 billion.

Monthly spot Bitcoin ETF flows in 2026. Source: SoSoValue

The products have still attracted $51.32 billion in cumulative net inflows since launch, while total net assets stood at $76.29 billion at the end of July.

Related: Bitcoin price sinks to 2-week lows as US stocks fail to copy Asia rebound

Weekly flows turned negative at the end of the month after three consecutive weeks of inflows, with Bitcoin ETFs recording a $61.53 million outflow for the week ending July 31.

Ether ETFs end July with four-week inflow streak

While Bitcoin ETFs faced renewed selling pressure at the end of July, some altcoin ETFs maintained steadier inflows.

Ether ETFs stood out, posting four consecutive weeks of inflows and ending the month with a $365.2 million net inflow, according to SoSoValue.

The inflows marked the second month of positive flows for Ether ETFs year to date after April’s $356 million inflow. Despite the recovery, the products remained about $1.1 billion in net outflows year to date.

XRP ETFs also maintained steady demand, recording $27.3 million in July inflows and marking their fifth positive month of 2026. The products have recorded about $343 million in net inflows year to date, making them one of the stronger-performing crypto ETF categories this year.

Magazine: A quantum roadmap would push Bitcoin much higher: Charles Edwards

The XRP Ledger wants to let banks pay network costs for their users. If validators agree, people could use the ledger without ever buying XRP.

Jazzi Cooper, head of product at RippleX, said the xrpld 3.3.0 release should arrive next week. It carries five proposed changes. One is called Sponsored Fees and Reserves.

Why Using the XRP Ledger Costs XRP Today

Every account on the ledger locks up 1 XRP. That amount cannot be spent or moved. Each extra item an account holds, such as a trustline, locks another 0.2 XRP.

Every transaction also burns a small fee. So a new user has to buy XRP first. Only then can they do anything else.

The upgrade changes who pays. A bank, issuer, or platform can cover both the fee and the locked amount. Users still hold their own accounts and keys.

Cooper called that requirement one of the biggest barriers for new users, and for institutional tokenization on XRPL.

“Users continue to own their accounts and keys, while removing one of the biggest onboarding hurdles: requiring every participant to acquire and manage XRP before they can interact with the network,” Cooper said.

Follow us on X to get the latest news as it happens

What It Means for XRP Demand

XRP trades near $1.06. It is down 1.3% on the day and about 64% lower than a year ago. Its market cap sits at $66.5 billion.

The locked XRP does not vanish under this plan. It simply moves. Sponsors would hold it instead of millions of small users.

That cuts both ways. Everyday users lose their main reason to buy XRP. But a platform signing up thousands of accounts would need far more of it.

Past upgrades offer little guide. Permissioned Domains went live in February with more than 91% validator support. A smaller update followed in May. Neither moved the price much, and ledger use has grown while XRP fell.

2 of the 5 Changes Failed Before

Confidential MPT hides Multi-Purpose Token (MPT) balances from public view. Auditors can still check them when needed. Dynamic MPT lets issuers decide upfront which token settings they may change later.

The last two are second attempts. Batch groups up to eight transactions so they all succeed or all fail. It was pulled in February. Pranamya Keshkamat and Cantina AI’s tool Apex found a flaw that let attackers spend from other people’s accounts.

Permission Delegation was switched off in September 2025. A developer known as tequ reported that it charged fees before checking signatures. Neither ever reached the live network, so no money was lost.

Validators now decide. Each change needs 80% support for two straight weeks. Batch has been rejected once already.

The post XRP Ledger Upgrade Could Make Owning XRP Optional: Will Demand Fall? appeared first on BeInCrypto.

Moneyflip CEO Marcos Arturo Kleiman Tronllan faces a federal murder-for-hire charge after allegedly paying undercover agents $40,000 to kidnap and kill a businessman over an unpaid debt.

Summary

- Kleiman allegedly agreed to pay $40,000 to kidnap and murder a Mexican businessman.

- Prosecutors said the final payments included $5,000 in cash and about 25,000 USDT.

- Undercover agents previously had Kleiman convert approximately $750,000 into cryptocurrency.

- The federal charge carries up to 10 years in prison and a $250,000 fine.

Moneyflip CEO arrested in Miami

Homeland Security Investigations agents arrested Kleiman in Miami on July 30 in connection with a federal complaint filed in San Diego.

Kleiman, 40, is a Mexican citizen and lawful permanent resident of the United States. He previously lived and worked in San Diego, according to the U.S. Attorney’s Office for the Southern District of California.

Moneyflip is a registered money services business offering cross-border currency exchange services. Kleiman previously operated the company as MXN Financial LLC before it changed its name to Moneyflip LLC in 2025.

Investigators began examining Kleiman while investigating currency exchange businesses in San Diego and Imperial counties. Authorities suspected that he used cross-border transactions to avoid Bank Secrecy Act reporting requirements and launder proceeds from drug sales.

The complaint contains allegations rather than proven facts. Kleiman is presumed innocent unless convicted.

Undercover agents converted $750K into crypto

Undercover HSI agents approached Kleiman in February and asked him to convert U.S. dollars into cryptocurrency. The agents allegedly told him that the money came from drug sales.

Prosecutors said Kleiman created an email account and shared its password with the agents. The parties allegedly communicated through unsent draft emails to avoid transmitting messages directly.

Kleiman then allegedly converted approximately $750,000 into cryptocurrency and arranged for the assets to be transferred to an undercover agent’s wallet. Authorities said he charged a 10% fee.

“Kleiman converted approximately $750,000 of United States currency into cryptocurrency and caused the transmission of those crypto coins into an undercover federal agent’s wallet,” prosecutors said.

During those discussions, Kleiman allegedly asked whether the agents could recover a debt from a Mexican businessman and kill him. Prosecutors said he agreed to pay $40,000 for the kidnapping and murder, including two $5,000 advance deposits.

Agents staged murder before 25,000 USDT payment

Kleiman allegedly arranged for a third party to deliver the first $5,000 deposit to an undercover agent in San Diego in May. Prosecutors said he later paid another $5,000 deposit after an agent requested money to reserve the purported killers.

On July 28, the undercover agents showed Kleiman three photographs and a video that falsely depicted the businessman as having been captured, tortured and killed. No murder occurred as part of the operation.

Authorities said Kleiman responded that the agents could count on him to complete the payment. On July 29, he allegedly delivered another $5,000 in cash and transferred approximately 25,000 USDT to an undercover cryptocurrency wallet.

USDT is a dollar-pegged stablecoin issued by Tether. Unlike cash, transfers made through public blockchain networks can leave transaction records that investigators may use alongside messages, surveillance, and other financial evidence.

Federal charge carries a 10-year maximum sentence

Kleiman faces one count of murder-for-hire under Title 18, Section 1958(a) of the U.S. Code. The charge carries a maximum sentence of 10 years in federal prison and a fine of up to $250,000.

The case is being prosecuted by Assistant U.S. Attorneys Michael Deshong and Christopher Beeler. HSI led the investigation with support from the U.S. Postal Inspection Service, Drug Enforcement Administration, Customs and Border Protection, IRS Criminal Investigation, and local law enforcement agencies.

Money services businesses that exchange or transmit convertible virtual currencies may fall under federal Bank Secrecy Act requirements. Registration as a money services business does not represent government approval of a company or its activities.

George Santos said he would attend the 2026 State of the Union. He was also betting on Kalshi that he would skip it. Regulators have now fined him $35,000.

He made $17,570 on that bet. He kept the money for about five months. Now he has to give all of it back.

He Bet Against Himself, and Won

Kalshi is a US exchange where people trade contracts on real events. Federal derivatives rules cover it, not state gambling rules.

The contract was simple. It asked who would show up at the State of the Union. Santos traded it between February 12 and February 25.

While he held those bets, he posted about his plans on X. The US Commodity Futures Trading Commission (CFTC) says those posts were misleading. Its order came out Friday.

Prices then moved his way. He walked away with $17,569.98. He now owes that back, plus a $17,500 fine.

He is also banned from trading for three years. He admitted nothing.

This is not his first problem. Congress expelled Santos in 2023. Trump commuted his fraud sentence last year.

Kalshi Caught It in Seconds

No regulator spotted this first. The exchange did, and so did other traders. Kalshi CEO Tarek Mansour described how fast it happened.

“within seconds it was flagged by our system. We opened investigations and within minutes we had like a hundred whistleblower complaints,” Axios reported, citing Tarek Mansour, Kalshi CEO.

That speed is the real story here. On a stock exchange, staff dig through records weeks later. On these markets, the people holding the other side notice immediately.

They have every reason to look. Their own money is at stake. Most Kalshi traders lose as it is, so they watch each other closely.

Regulators are circling too. In February, the CFTC said it would go after insider trading and manipulation on markets like these. Former officials had warned about weak oversight earlier.

Kalshi has since punished three congressional candidates who bet on their own races. A White House teleprompter operator lost his job in July. Reports said he won over $100,000 betting on Trump’s speeches.

Santos Says He Did Nothing Wrong

His lawyer, Joseph W. Murray, says the deal proves nothing.

“Mr. Santos has settled without admitting any of the Commission’s allegations, findings, or conclusions,” Joseph W. Murray, via MS NOW.

Kalshi is running its own case against him as well. If it collects any money, it says it will try to repay the traders he beat.

The timing is awkward, though. New York sued the company on the same day. The state calls it illegal gambling and wants up to $36 billion.

Kalshi says it is a regulated exchange, not a casino. It is fighting that case while chasing a $40 billion valuation.

Catching Santos in seconds may be the best argument it has.

The post George Santos Kalshi Bet Cost Him $35,000: Who Caught Him First? appeared first on BeInCrypto.

Coronation Street star confirms engagement just months after soap wedding

WHY’S IT TAKING SO LONG FOR XRP TO HIT $1000? – XRP INSTITUTIONAL WAVE ALREADY STARTED!

Chris Wood warns AI capex binge may burn billions as markets turn against Big Tech spending

Renter of Home in Anne Heche Crash Denies Settlement With Son

No Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

Weekend Open Thread: Staud – Corporette.com

WHY’S IT TAKING SO LONG FOR XRP TO HIT $1000? – XRP INSTITUTIONAL WAVE ALREADY STARTED!

From Learning to Earning: My MRR Certification, Website- Next..Financial Freedom Online!

#stock #finance #financialeducation #What is share holding pattern #shortvideo

-

Sports5 days ago

Sports5 days agoCommonwealth Games boxing: Jadumani Singh seals dominant 5-0 win over Pakistan’s Sumama Rehman to enter quarter-finals | Commonwealth Games News

-

Business2 days ago

Business2 days agoWhy Trees Belong on the Risk Register

-

Fashion15 hours ago

Fashion15 hours agoWeekend Open Thread: Wit & Wisdom

-

Politics11 hours ago

Politics11 hours agoMeta enters AI-training agreement with far-right ‘propaganda rag’ Newsmax

-

Tech5 days ago

Tech5 days agoIntel is reversing course and bringing hyper-threading back to its server chips

-

Crypto World7 days ago

Crypto World7 days agoRipple bought a bank in pieces. The $4 billion audit

-

Politics5 days ago

Politics5 days agoLuke Littler dismantles Gerwyn Price to retain title in Blackpool

-

Politics4 days ago

Politics4 days agoThe Part of the Electric Transition Nobody Wants to Discuss

-

News Videos5 days ago

News Videos5 days agoBITCOIN JUST ENTERED THIS CRITICAL ZONE…

-

Entertainment4 days ago

Entertainment4 days ago‘Stargate’ Creator’s New Sci-Fi Series Returns for Season 3 Tomorrow

-

Crypto World6 days ago

Crypto World6 days agoXRP Ledger adds $2.6B as RWA inflows rank second

-

Business3 days ago

Business3 days agoMajor shareholder moves on Canyon

-

Politics6 days ago

Politics6 days agoSpain sweeps the board at 2026 World Cup with individual awards

-

News Videos2 days ago

News Videos2 days agoBitcoin Enters the 3rd Stage of the Bear Market

-

Crypto World2 hours ago

XRP Ledger v3.3.0 brings five institutional features

-

Entertainment6 days ago

Entertainment6 days agoSara Gilson Killed By Husband After Viral “Pedophile” TikTok Video

-

Crypto World3 days ago

Crypto World3 days agoKraken Enables Retail Access to Jersey Mike’s IPO via Tokenized Shares

-

Tech4 days ago

Tech4 days agoNew macOS Sequoia & Sonoma security updates for older Macs

-

News Videos4 days ago

News Videos4 days agoClaude: Build Financial Dashboards in Minutes (2026)

-

Politics2 days ago

Politics2 days agoLuke Littler’s dominance sparks GOAT debate

You must be logged in to post a comment Login