Crypto World

BitGo Lays off 15% of Staff in Stablecoin, AI Focus

Crypto infrastructure company BitGo Holdings laid off about 15% of its staff on Thursday as its CEO pledged to focus the company on areas including trading, stablecoins and artificial intelligence.

“Today I’m sharing a hard decision: we are reducing our workforce by nearly 15%,” BitGo co-founder and CEO Mike Belshe posted to X on Thursday. “The ecosystem has evolved, and the way we build financial services has changed dramatically.”

“We need to be sharper, more focused, and concentrate our people and energy on the areas that matter most: security, trading, stablecoins, settlement, and AI-powered infrastructure,” he added.

The layoffs add to the thousands of jobs lost in the crypto industry so far in 2026, with many companies citing efficiency gains from AI and a wide crypto market slump as the reason for the cuts.

Source: Mike Belshe

BitGo did not confirm the number of staff affected in the layoffs. Its 2025 annual report published in March disclosed it had 603 full-time employees as of Dec. 31, 2025, meaning the layoffs could have impacted about 90 staff.

Belshe said the layoffs were “a one-time action” and BitGo does not “anticipate further reductions.” The company is still hiring for 51 roles across various regions, according to its job board.

BitGo did not immediately respond to a request for comment.

Related: Blockworks acquires Messari in crypto data consolidation push

Shares in BitGo (BTGO) closed Thursday down 4.67% at $4.80, extending a nearly 73% slide from its public debut at $18 on Jan. 22.

Shares in BitGo on Thursday slid more than 4.5% after the company announced it cut 15% of its staff. Source: Google Finance

Crypto companies have so far cut more than 5,000 jobs this year, with Block Inc. undertaking the biggest round of layoffs by cutting 4,000 staff or about half its workforce in February.

Robinhood cut 10% of its workforce on June 16, while in May, crypto exchange Kraken cut 150 staff, data company Dune cut 25% of its workforce and Coinbase cut 700 employees, or about 14% of its workforce.

Earlier this year, Gemini laid off 200 employees and Crypto.com also laid off about 180 staff, with both citing the rising use of AI.

So far this year, the wider US technology sector has seen over 121,500 layoffs from over 200 companies, according to Layoffs.fyi.

Magazine: Guide to the top and emerging global crypto hubs: Mid-2026

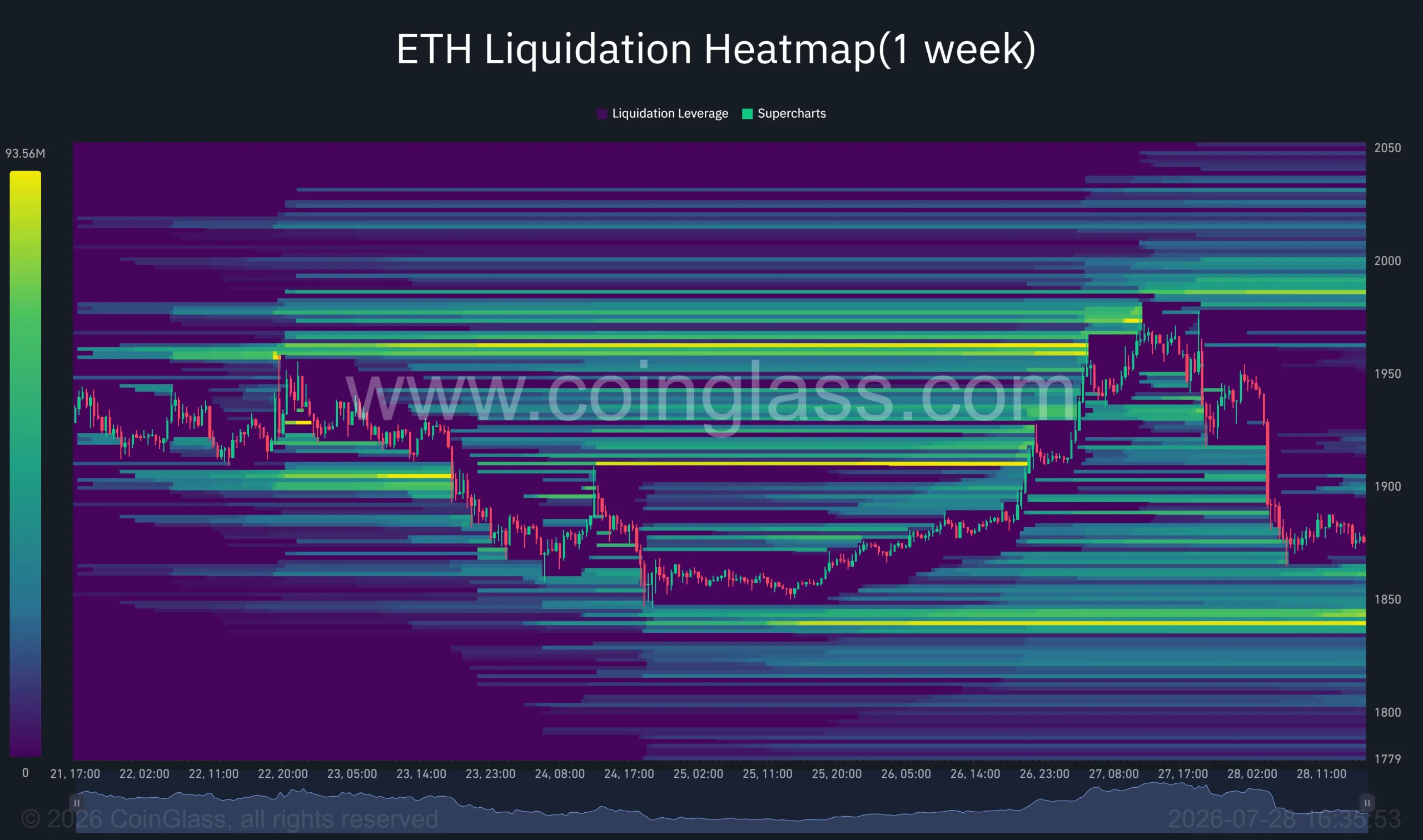

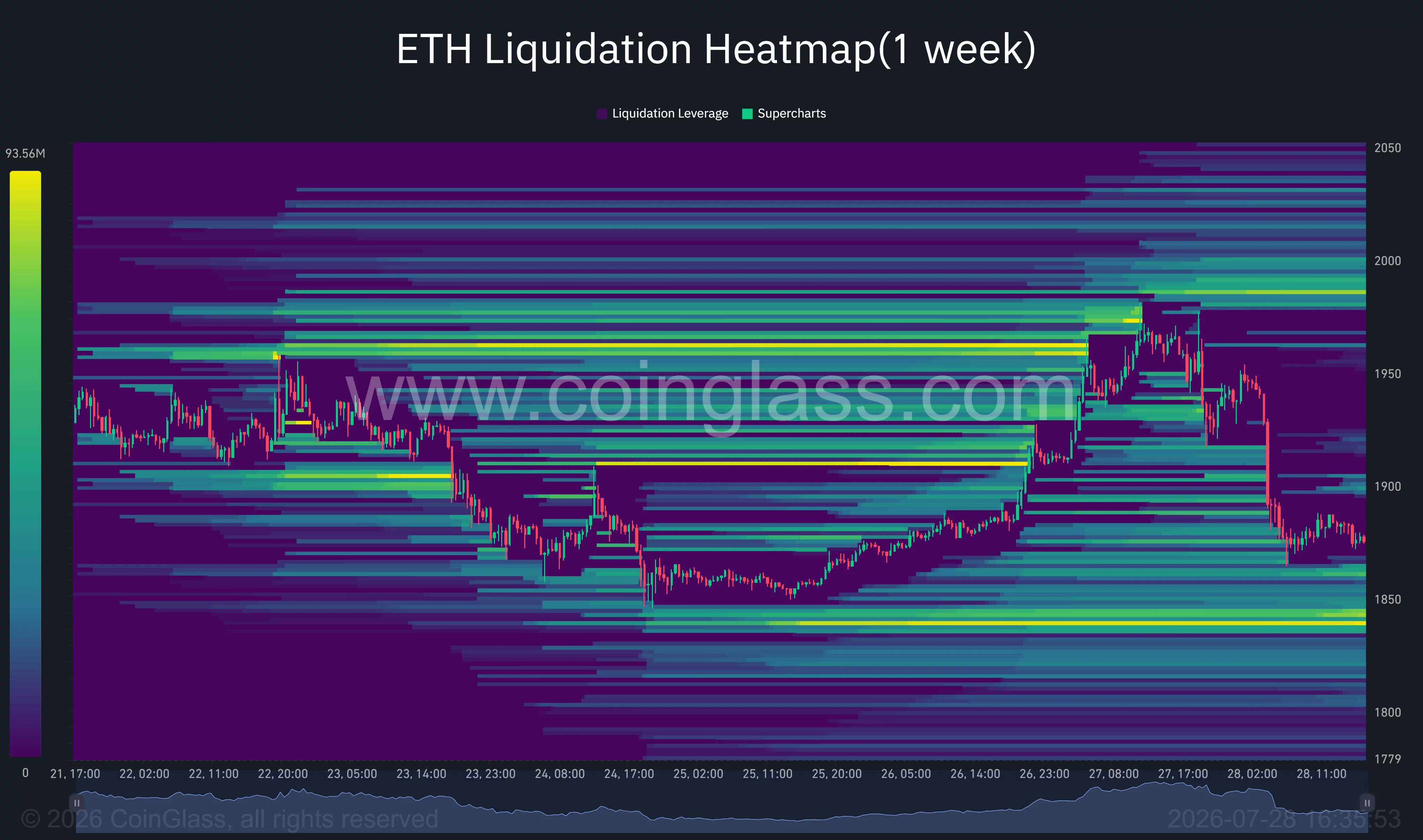

Ethereum price fell 5% from $1,973 to $1,873 on July 28 after another rejection below $2,000 triggered forced selling and pushed ETH into a key technical support zone.

- Ethereum price dropped below $1,900 after buyers failed to break the $1,975–$2,000 resistance zone.

- Leveraged positions accelerated the decline as ETH moved through several long-liquidation clusters.

- ETH is testing the lower boundary of a rising wedge near $1,870 on the 4-hour chart.

- The next large concentration of downside liquidity sits around $1,840–$1,850.

Ethereum price falls below $1,900 after $2,000 rejection

According to data from crypto.news, Ethereum (ETH) price traded near $1,875 at the time of writing, down from an intraday high close to $1,973. The decline erased most of the gains from the previous session, when ETH reached its highest level since early June.

Selling intensified after buyers failed to push the price through the $1,975–$2,000 resistance range. The rejection trapped traders who had opened leveraged long positions in anticipation of a breakout above the psychological threshold.

ETH subsequently moved below $1,900, activating stop-loss orders and forcing position closures. The price reached approximately $1,873 before stabilizing around the lower end of the daily range.

Despite the decline, Ethereum remains above its early July low near $1,560. The token has gained roughly 20% from that level, meaning the wider recovery has weakened but has not yet been invalidated.

Leveraged longs accelerate the ETH sell-off

Derivatives positioning appears to have increased the speed of the decline. Bullish traders had built exposure as Ethereum approached $2,000, leaving the market vulnerable when spot demand failed to sustain the move.

The one-week ETH liquidation heatmap shows that the price passed through multiple areas of leveraged exposure between $1,950 and $1,890. Forced closures likely added sell orders as Ethereum broke through those levels.

The heatmap now shows a larger concentration of liquidity around $1,840–$1,850. Price can gravitate toward such areas because liquidations produce additional trading activity, although the data does not guarantee that ETH will reach the zone.

Transfers from large wallets to centralized exchanges may also have added to the pressure. Exchange deposits increase the amount of ETH available for sale, but they do not confirm that the holders have liquidated their assets.

Broader weakness across technology stocks contributed another source of pressure. Concerns about the financial returns from heavy artificial intelligence spending have increased volatility across global equities, encouraging investors to reduce exposure to risk assets, including cryptocurrencies.

ETH tests rising support near $1,870

Ethereum’s 4-hour chart shows the price testing the lower boundary of a rising wedge near $1,870. The trendline has supported the recovery since the middle of July, making the current area important for the token’s next move.

A decisive close below the trendline would weaken the rebound and could send ETH toward the $1,850–$1,840 liquidity zone. Failure to hold that area would expose the 100-day simple moving average near $1,758.

Momentum indicators support a cautious short-term outlook. The 4-hour relative strength index has fallen to 42.22, below its moving average of 57.68. The reading shows weakening demand but remains above the oversold threshold of 30.

The moving average convergence divergence indicator has also turned bearish. The MACD line has fallen below its signal line, while the histogram has moved into negative territory, showing that sellers retain short-term control.

On the daily chart, Ethereum price remains above its 20-day SMA, currently near $1,864, offering immediate support around the present price. The 50-day SMA stands lower at approximately $1,759.

On the upside, ETH must first recover $1,900. Further resistance sits between $1,950 and $1,975, where the recent high and the 200-day SMA near $1,954 create a stronger supply zone.

A daily close above $1,975 would weaken the bearish setup and give buyers another chance to test $2,000. Until that happens, rebounds into the resistance zone may continue to attract selling.

Analysts identify $1,840 as the decisive support

Crypto analyst Ted Pillows described the current trading area as a key support zone for Ethereum.

“ETH is back into its key support zone. As long as this holds, Ethereum will continue to outperform Bitcoin.”

Pillows’ chart places support around $1,840, followed by possible recovery levels near $1,956, $2,030, and $2,195. A breakdown below the current zone, however, could shift attention toward approximately $1,700 and $1,530.

Market commentator Rain pointed to corporate accumulation as a potential source of longer-term demand. Rain noted that BitMine added nearly 10,000 ETH during the previous week, taking its reported holdings to approximately 5.79 million ETH.

Rain also said ETH had gained about 2.4% over the week while Bitcoin declined roughly 0.7%, pushing the ETH/BTC ratio to a three-month high. The relative strength suggests some investors continue to favor Ethereum despite the latest intraday correction.

Corporate buying may support ETH over longer periods, but it cannot prevent short-term volatility when leveraged positioning becomes crowded. The immediate outlook still depends on whether buyers can defend the $1,840–$1,870 region.

Fed expectations add pressure for US traders

US investors are also monitoring Treasury yields and expectations surrounding Federal Reserve policy. Higher risk-free yields can reduce demand for speculative assets and make Ethereum’s staking yield less attractive relative to government bonds.

Demand for US-listed spot Ethereum exchange-traded funds represents another key variable. Continued institutional inflows could help absorb exchange-based selling, while sustained outflows would remove a source of demand that supported the July recovery.

Regulatory uncertainty around staking services and liquid staking products remains relevant for US holders. Changes to the treatment or availability of those services could affect institutional demand and the way investors value Ethereum’s yield.

For now, $1,840 remains the principal downside level, while $1,950–$1,975 is the range bulls must reclaim. Holding support would preserve Ethereum’s July recovery structure, but a daily close beneath it could expose the 100-day SMA near $1,758.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Lido, the major liquid staking protocol for Ethereum, has announced an upgrade to its staking infrastructure aimed at improving validator efficiency while keeping decentralization on the roadmap. The change is introduced through a new component called Curated Module v2, which Lido says brings broader support for Ethereum’s newer withdrawal credential format.

According to a Lido update published on Monday, the upgrade adds support for Ethereum’s 0x02 withdrawal credentials. The practical upshot is that validators operating through Lido infrastructure can raise their effective balance from 32 ETH to as much as 2,048 ETH, while still being orchestrated within the protocol’s staking framework.

Key takeaways

- Curated Module v2 adds support for Ethereum’s 0x02 withdrawal credentials within Lido’s staking setup.

- Lido projects validator counts could fall from about 880,000 to roughly 628,000, a drop of around one-third, based on its internal assumptions.

- Lido says the migration has not started yet; the numbers reflect projections rather than realized outcomes.

- The upgrade is expected to reduce messaging and participation needs on the consensus layer, while not targeting changes to the execution layer fee and gas activity.

- New accountability measures for node operators include bonding and penalty mechanisms, with future stake allocation potentially influenced by performance and ecosystem contribution.

What Lido’s Curated Module v2 changes

Lido’s model relies on smart contract coordination and a network of node operators that run Ethereum validators. The protocol’s announced upgrade centers on expanding how those validators are configured, specifically through withdrawal credentials that Ethereum supports via the 0x02 format.

Lido states that this credential support enables validators to operate with a larger effective balance—up to 2,048 ETH. In systems like Ethereum’s staking architecture, larger effective balances can translate into fewer independent validator instances needed to steward a given amount of stake.

Importantly for stakers, Lido emphasized that users do not need to take action. Since Lido is a liquid staking protocol, stakers hold stETH, and Lido said the migration will be handled at the protocol level.

Projected impact on Ethereum validator counts

Lido’s update includes a quantification of what the migration could look like. The protocol said the shift could reduce Ethereum’s validator count from approximately 880,000 to about 628,000, implying a roughly 33% reduction.

Lido also stressed that the migration is not underway yet. The figures are based on the protocol’s projections rather than results that have already been observed on-chain.

From an investor and market-structure standpoint, validator-count changes matter less for token price mechanics and more for how efficiently the network runs under load. If fewer validators and fewer validator messages are required to maintain consensus, it can lower certain overhead costs and complexity—particularly during periods when validator participation is highly dynamic.

Consensus layer efficiency—without changing execution-layer fees

Beyond the raw validator count, Lido expects the upgrade to affect Ethereum’s consensus layer by reducing the number of validators and validator messages required for the network to operate.

Lido also drew an explicit boundary around what the upgrade does not intend to change: it is not designed to alter execution-layer activity. The execution layer is where transaction fees and gas costs arise, so the protocol’s stated aim is to improve consensus-side operational characteristics rather than influence fee markets directly.

For users watching network performance, this distinction is crucial. Upgrades that affect validator messaging and participation typically influence consensus efficiency, while execution-layer changes are the ones most directly tied to the user experience around gas and transaction inclusion.

New operator accountability: bonds, penalties, and weighting performance

Lido’s announcement also goes beyond infrastructure configuration by outlining additional accountability measures for its node operators. The protocol said the upgrade introduces bonding and penalty mechanisms, intended to increase alignment between operator behavior and protocol expectations.

According to Lido, operator incentives will evolve as part of this framework. Lido further suggested that future stake distribution could place more weight on a broader set of factors—potentially including operator performance, fees, and contributions to the broader Ethereum ecosystem.

In other words, the upgrade is not only about reducing how many validator entities are used; it is also about changing how operators are evaluated and economically constrained. That matters for decentralization, since more robust accountability mechanisms can help ensure that operator quality and reliability are not treated as afterthoughts when scaling staking infrastructure.

Lido described Curated Module v2 as a “next major step” in the evolution of its architecture, citing new operator incentives, bond-based security mechanisms, and governance improvements.

What stakers and observers should monitor next

As Curated Module v2 moves from announcement to migration execution, the main things to watch are how quickly Lido completes the change and whether the projected reduction in validator count and messaging levels comes close to the protocol’s stated estimates. Since Lido says the migration is handled at the protocol level, the practical signal for stakers will likely be tracking network-level behavior during and after the rollout—especially consensus-layer efficiency metrics—while keeping in mind Lido’s assertion that execution-layer fee dynamics are not the target of this upgrade.

Decentralized exchange (DEX) aggregator 1inch opened Aqua, its shared liquidity protocol, to users across 13 Ethereum Virtual Machine-compatible chains.

Aqua lets liquidity providers use the same wallet balance across multiple positions instead of splitting their assets among separate pools, with tokens remaining in the provider’s wallet until a matching swap executes.

The protocol allows “tokens to stay in your wallet, under your control, while one balance backs multiple positions across different strategies rather than being split between smart contract deposits,” 1inch co-founder Sergej Kunz told CoinDesk.

A $100,000 balance could support three positions quoting a combined $300,000, according to 1inch. That is quoted liquidity rather than additional capital, and orders can only execute against assets held in the wallet, and a swap fails if the balance cannot cover it.

1inch first unveiled Aqua last year, including its software development kit, libraries and documentation. The public interface lets users create full-range, concentrated or pegged positions across chains including Ethereum, Base, BNB Chain, Arbitrum and Robinhood Chain.

The rollout follows research commissioned by 1inch that found 85% of $1.84 billion tracked across major concentrated-liquidity exchanges was underutilized in the first half of 2026.

Crypto World

South Korea’s worst market day in years and a stalled Clarity Act put crypto on the back foot

Bitcoin has lost 0.53% since midnight UTC, having shed around 2% during the U.S. session overnight.

Two catalysts are weighing on sentiment.

First, chipmaking stocks tumbled in South Korea, dragging the benchmark Kospi stock index down 11%. The drop, one of its worst single-day declines in years, sent shockwaves across global risk assets.

And on the regulatory front, the U.S. Senate shelved the Crypto Clarity Act for now, opting to prioritize a Russia sanctions bill and federal nominations with just two weeks remaining before the summer recess begins on Aug. 8. The bill’s fate this year is now genuinely uncertain.

Ether (ETH) fell 0.56% to $1,880 having failed to rise through the psychological level of $2,000 on Monday. Both the Fed’s interest-rate decision on Wednesday and the Senate’s remaining floor time loom large over the market this week.

Traditional markets are broadly lower, with Nasdaq 100 index futures down 0.70%, gold shedding 0.93% and silver off 1.50%.

Derivatives positioning

- Taker volume flips bearish: The taker long/short volume in futures has flipped gloomy, with shorts, or bearish plays, now at 51.5%. This marks a complete turnaround from the bullish bias seen in recent days. A taker is a market participant that trades at prevailing prices.

- XRP open interest rises: XRP’s futures open interest has risen to 2.35 billion tokens, up nearly 6% from a day ago. Meanwhile, open interest has held steady in BTC, ETH and SOL futures. That’s been the trend in majors mostly, with participation remaining modest through the price bounce from early June lows.

- Other tokens see outflows: Futures linked to other tokens, such as SHIB, AVAX, LINK and DOGE, have seen open interest decline in a sign of capital outflows.

- CVD turns negative: Other metrics, like the 24-hour open interest-adjusted cumulative volume delta, also paint a bearish picture. For the first time in at least three weeks, the top 25 coins have negative CVDs. That means bears are leading the price action by shorting via market orders rather than passive limit orders.

- Funding rates shift: Funding rates for BTC hover near 0%, a sign of balanced positioning. Meanwhile, those for ETH, SOL, XRP and TRX have flipped negative, a sign of growing bias for bearish plays.

- Volatility remains calm: While key events such as the Fed meeting and the core U.S. PCE inflation figure are due this week, BTC and ETH volatility surfaces do not show any sign of traders pricing genuine stress. BTC and ETH’s 30-day implied volatility indexes remain near recent lows, a sign of market calm.

- Options show put bias: In Deribit-listed options, BTC and ETH put-call skews have climbed slightly, consistent with the overnight losses in the spot price. The bias for puts in ETH options is considerably lower than in BTC. However, volume rankings show puts or downside protection taking the top spot in both BTC and ETH.

Token talk

- Lighter (LIT) is the crypto market’s standout gainer, rising 3.97% to $2.21 as it continues to rebuild after last week’s profit-taking, with the $2.10 support level being defended for the third time this month.

- and ethena (ENA) are among the few other tokens in the green, gaining 1.54% and 1.46%, respectively, and maintaining a run of DeFi resilience even as broader sentiment sours.

- FET led the losses over 24 hours, falling 9.48%, with NEAR, HYPE and WLD all shedding 8%-9%. AI and layer-1 tokens took the brunt of the overnight selloff.

- gave back 3.07% after Monday’s strong session. It is still higher than where it was over the weekend as speculators begin to take profit.

- CoinMarketCap’s “Altcoin Season” indicator is hovering at 53/100, down slightly from Monday but higher than where it has been for the majority of July.

Ethereum withdrawals from BitMart have jumped to their highest level in a year. Users are rushing to pull ETH before the exchange finishes winding down its trading platform.

The exchange had frozen withdrawals briefly, then reopened them within the last day. That reopening triggered an immediate rush for the exits.

BitMart’s move followed a July 26 announcement confirming it would shut down trading entirely over the coming months. Years of declining liquidity had already pushed the exchange out of the top 10 by trading volume. The notice still caught many remaining users off guard.

Ethereum Withdrawals Hit a 2026 High

Data tracked via the blockchain analytics platform CryptoQuant highlights this massive exodus. The metrics reveal Ethereum withdrawal transactions from BitMart climbing past every prior reading since July 2025. That marks a clear signal that holders are moving funds off the exchange while they still can.

The surge tracks closely with BitMart’s own shutdown timeline. Registrations, deposits, and new trading orders paused on July 26. Full trading services end on August 26. Withdrawals stay open through January 2027, giving remaining users a narrow but real window to retrieve their holdings before the final deadline.

BitMart’s exit adds to a run of 2026 shutdowns. Its own token, BitMart Token (BMX), tumbled after the wind-down announcement rattled traders. The closure landed just three days after derivatives exchange BitMEX confirmed its own exit from the market.

Decentralized exchange Dango also halted its blockchain this month. The project shut down entirely after finding no path to lasting success, becoming the third notable platform to close in July alone.

Analysts Call the Wave a Healthy Reset

Historically, exchange failures spark brief panic before conditions settle. Several analysts, meanwhile, are reading these closures as a healthy correction rather than a warning sign for the broader market.

Some traders view the shakeout as clearing out weaker platforms, not as evidence of wider contagion. Smaller exchanges carrying similar liquidity problems could face the same pressure to consolidate or close before the year is out, industry watchers suggest.

Ethereum (ETH) itself has held steady through the turmoil. The token is trading near $1,881, according to the latest BeInCrypto data. Trading volume across the broader market has stayed largely unaffected by the BitMart news, suggesting the impact remains contained to the exchange itself.

Therefore, the withdrawal rush looks like an isolated reaction to one exchange’s closure rather than a market-wide flight from centralized platforms. Ethereum’s price action, in particular, shows little sign of stress spilling beyond BitMart’s own user base.

Still, the pattern raises a question for the rest of 2026. More struggling exchanges could follow BitMart, BitMEX, and Dango toward the exit before the year ends. For now, BitMart users have a shrinking window to move their funds. The CryptoQuant data suggests many are taking it while they still can.

The post Ethereum Withdrawals From BitMart Surge After Wind-Down Notice appeared first on BeInCrypto.

Lido, one of the largest liquid staking platforms on Ethereum, has rolled out an upgrade to its staking infrastructure aimed at improving how validators operate while supporting greater decentralization. The change centers on Curated Module v2, a new component within Lido’s validator system.

According to a Lido update published Monday, the upgrade adds support for Ethereum’s 0x02 withdrawal credentials. That support is expected to let validators raise their effective balance from the familiar 32 ETH threshold to sizes of up to 2,048 ETH, depending on how validators are configured.

Key takeaways

- Curated Module v2 is designed to improve validator efficiency by enabling validator effective balances to scale up to 2,048 ETH via Ethereum’s 0x02 withdrawal credentials.

- Lido projects the migration could reduce validator count from about 880,000 to roughly 628,000—a drop of around one-third.

- The upgrade is expected to impact Ethereum’s consensus layer (validator set size and related messages) rather than execution-layer activity like transaction fees.

- Lido is adding bonding and penalty accountability mechanisms for node operators as part of the upgrade.

- Lido says no staker action is needed because the migration is handled at the protocol level.

What Curated Module v2 changes

At the core of the upgrade is the introduction of 0x02 withdrawal credentials support. Lido says this enables validators to increase their effective balance, moving beyond the 32 ETH effective balance commonly associated with how validators are structured.

Lido’s update frames this as a step toward a leaner, more efficient validator footprint. By allowing validators to operate with larger effective balances, Lido expects fewer validators are needed to secure and attest on the network at comparable levels of staked participation.

Importantly, Lido emphasizes that the change is not meant to alter the execution layer—the part of Ethereum responsible for ordering transactions and determining gas costs and fee levels. Instead, Lido says the upgrade should primarily affect how the consensus layer is maintained, including the number of validator messages required to keep the network running.

Projected validator count reduction—based on Lido estimates

Lido said the migration has not started yet and that the figures it shared are projections from its modeling. Under those assumptions, Lido expects the validator count could fall from around 880,000 to about 628,000, representing an approximate 33% decrease.

The practical implication for investors and network participants is that a smaller validator set can change the operational dynamics of staking at scale. Even if overall security assumptions remain grounded in Ethereum’s consensus rules, the structure of who participates and how often messages are produced can differ when fewer validators are responsible for the same underlying economic weight.

Still, because these are Lido’s projections and the migration has not begun, the direction and magnitude of real-world change may depend on how validators and the wider ecosystem adopt and configure the new credentials over time.

Accountability upgrades for node operators

Beyond changing validator sizing, Lido’s update introduces new accountability measures for its node operators. Lido specifically mentioned bonding and penalty mechanisms, indicating that operator security and performance expectations may be enforced more directly through economic incentives and disincentives.

The update also suggests future stake distribution could weigh additional factors. Lido said more emphasis could be placed on operator performance, fees, and contributions to Ethereum’s broader ecosystem—signals intended to reward not just participation, but sustained operational quality and active involvement.

For users who rely on Lido’s liquid staking token—rather than operating validators themselves—the significance is indirect but meaningful. Upgrades that adjust operator incentives and monitoring can influence reliability and service continuity, which in turn can affect user confidence in the system’s robustness.

However, Lido’s message does not specify exact parameter thresholds or the detailed mechanics of how the bonding and penalties will be applied over time. Readers should watch for subsequent technical documentation or governance updates that clarify those operational details as the migration approaches.

Protocol-level migration: no staker action required

Lido said Curated Module v2 represents the “next major step” in its evolution toward operator incentives, bond-based security, and governance improvements. In its update, Lido also stated that no action is required from stakers, because the upgrade will be handled at the protocol level.

That matters for the practical day-to-day of stETH holders. If the change is fully protocol-managed, users should not need to redeploy wallets, move assets, or change validator relationships during the transition—reducing the operational risk that often accompanies large staking infrastructure shifts.

At the same time, the migration timing is a key unknown in the near term. Lido has not indicated that the upgrade is already underway, and it noted the validator count changes are based on projections. Once execution begins, the market will likely look for evidence that real validator set changes align with the expectations Lido has laid out.

For now, the most important things to monitor are whether the consensus-layer effects match Lido’s estimated validator reduction, and how the new operator accountability mechanisms perform once validators begin migrating to the configuration enabled by 0x02 withdrawal credentials.

Lido has introduced a major upgrade to its Ethereum staking infrastructure that supports higher validator balances and projects a one-third reduction in validator count through its new Curated Module v2.

Summary

- Lido has launched Curated Module v2, allowing Ethereum validators to increase their effective balance from 32 ETH to as much as 2,048 ETH.

- The protocol estimates the upgrade could reduce Ethereum’s validator count by about one third while improving consensus layer efficiency.

- New bonding and penalty mechanisms have been introduced to strengthen accountability for Lido’s node operators.

According to a Monday update from Lido, the latest version of its Curated Module adds support for Ethereum’s 0x02 withdrawal credentials, allowing validators to raise their effective balance from 32 ETH to as much as 2,048 ETH.

The protocol said the change is designed to improve validator operations while continuing its push toward a more decentralized staking network.

Lido projects fewer Ethereum validators

Under the proposed migration, Lido estimates Ethereum’s validator count could decline from roughly 880,000 to about 628,000. The protocol said the migration has not yet started and stressed that the figures are projections based on its current modeling rather than live network data.

Lido said reducing the number of validators would lower the volume of validator messages processed on Ethereum’s consensus layer, making validator management more efficient.

According to the protocol, the change does not alter activity on Ethereum’s execution layer, meaning transaction processing, gas fees, and user-facing network costs are not expected to change as a result of the upgrade.

No action is required from stETH holders because the migration will be handled at the protocol level, Lido said.

Curated Module v2 adds new rules for node operators

Alongside the infrastructure update, Lido has introduced new accountability measures for node operators participating in its curated staking module.

According to the protocol, Curated Module v2 includes bond requirements and penalty mechanisms intended to strengthen operator responsibility. Future stake allocation may also consider factors including operator performance, fee structures, and contributions to Ethereum’s ecosystem rather than relying solely on existing allocation methods.

Describing the release as the next stage in the protocol’s development, Lido said the upgrade combines new operator incentives with bond-backed security mechanisms and governance improvements that are intended to improve the operation of its validator set over time.

While validator balances can now grow well beyond Ethereum’s original 32 ETH limit through the updated withdrawal credentials, the protocol said the changes remain focused on validator management and do not modify Ethereum’s core staking rules.

Institutional use of Lido has continued to expand

The infrastructure upgrade follows several initiatives by Lido this year to strengthen its position across both retail and institutional staking markets.

Earlier this month, Anchorage Digital integrated Lido into its institutional platform, allowing clients to mint and burn wrapped staked Ether (wstETH) without moving assets outside the firm’s regulated custody environment.

According to Anchorage Digital, the integration allows institutions to gain Ethereum staking exposure while continuing to use the custody, reporting, governance, and settlement systems already available on its platform.

At the time, Anchorage Digital co-founder and chief executive Nathan McCauley said liquid staking had become an important part of institutional participation in Ethereum because it reduces operational complexity while keeping assets within regulated custody.

Separately, Kean Gilbert, head of institutional relations at the Lido Ecosystem Foundation, said institutional demand for custody-based staking has increased as staking infrastructure and regulatory frameworks have matured. Gilbert also said Lido has spent more than $4 million on smart contract audits, received an A+ security rating from independent firms including Credora, and has operated without a smart contract exploit since launching in 2020.

According to Gilbert, Lido distributes staked Ether across more than 900 node operators, with no single operator responsible for more than 1% of the network, reducing reliance on individual participants.

Governance changes have accompanied protocol development

The latest infrastructure release follows governance initiatives introduced by the protocol earlier this year.

In March, Lido DAO proposed using up to 10,000 stETH from its treasury to conduct a one-time buyback of LDO tokens after describing the governance token as trading well below what it viewed as the protocol’s underlying fundamentals. The proposal called for purchases to be executed in 1,000 stETH batches, with token holders voting on each tranche before additional buybacks could proceed.

At the time, the DAO said Lido remained the largest liquid staking protocol on Ethereum with approximately 23% market share despite a decline in LDO’s market price. Financial figures released alongside the proposal showed protocol revenue fell 23% to $40.5 million during 2025, while operating costs improved 13% year over year and the protocol’s take rate increased from 5% to 6.11%.

The Curated Module v2 rollout adds another protocol-level update as Lido continues adjusting its staking infrastructure, governance framework, and institutional offerings while preparing for the migration to Ethereum’s updated validator credential system.

Crypto World

Bitcoin Price Prediction: BTC Slides in Asian Hours, Moving in Tandem with Korean KOSPI

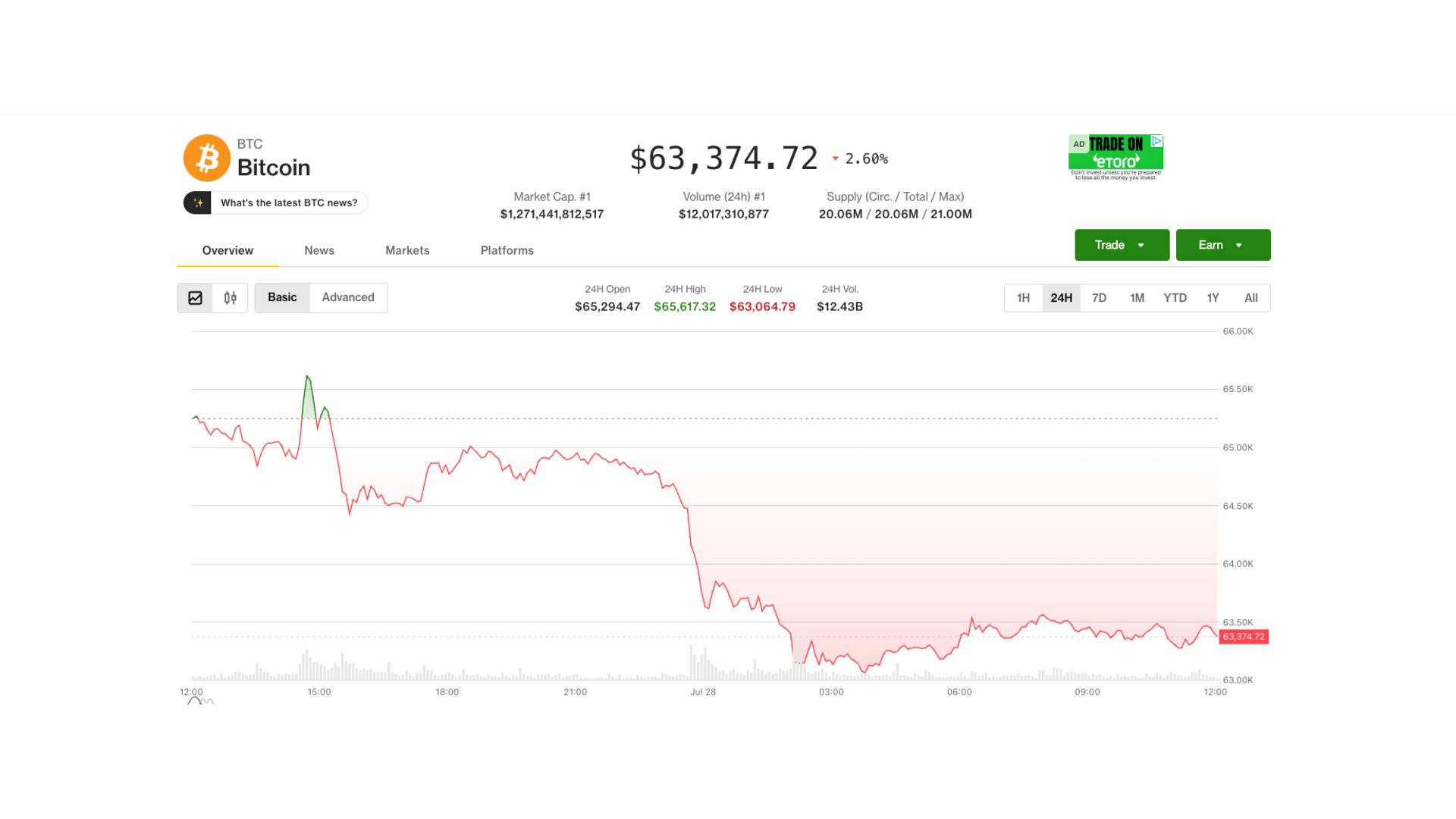

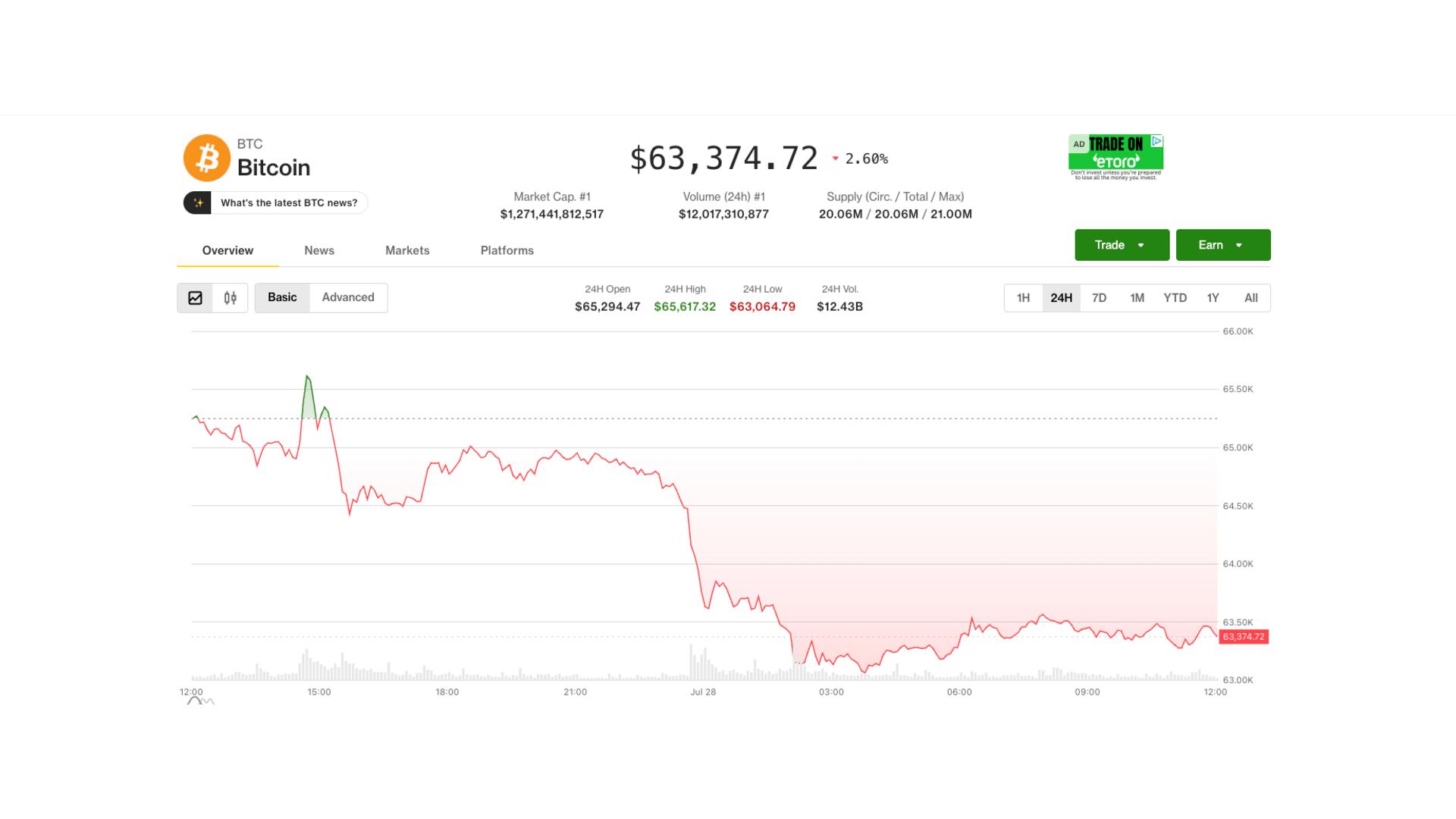

Bitcoin price is trading near $63,480 as selling accelerated during the Asian session, sending BTC prediction slipped into a bearish area. The move reflects rising caution across risk assets rather than a crypto-specific event.

South Korea’s KOSPI fell sharply, pressuring major chipmakers including Samsung and SK Hynix. That sparked another round of risk-off trading across global markets. Bitfinex analysts noted Bitcoin often tracks equities during macro-driven selloffs but can decouple during company-specific events.

Even so, today’s market has kept the correlation intact. Meanwhile, the U.S. Senate has delayed action on the CLARITY Act while prioritizing a Russia sanctions bill, removing a near-term regulatory catalyst for crypto.

Attention now shifts to Wednesday’s Federal Reserve rate decision. Traders will also watch Thursday’s Core PCE inflation report and second-quarter GDP data. Together, those releases are expected to shape expectations for interest rates and likely determine Bitcoin’s next major move.

Discover: The Best Crypto to Diversify Your Portfolio

Bitcoin Price Prediction: Recover to $70,000 Before the Fed Decision Wednesday?

Bitcoin is trading near $63,400, holding just above the key $63,000 support level. The past 24 hours saw a range between $63,038 and $65,598. Sellers continue defending the upper end, while buyers have kept $63,000 intact. A confirmed break below that level could expose $60,000, with stronger support waiting between $54,000 and $57,000.

Technically, BTC remains locked inside a consolidation range between $61,000 and $66,000. Some analysts still see a bear flag that could resolve lower if selling pressure persists. However, a weekly RSI bullish divergence near the 200-week SMA continues to support the longer-term recovery case. Similar setups have previously appeared near major cycle lows.

A bullish outcome would require Bitcoin to reclaim and hold above the $65,600 resistance zone after the Federal Reserve decision. That could open the door to a move toward the low $70,000s, with $79,000 remaining a possible upside target if momentum strengthens.

The base case remains range-bound trading between $61,000 and $66,000 until key macro data arrives. Thursday’s Core PCE inflation report could provide the next directional catalyst. On the downside, a confirmed close below $63,000, combined with continued weakness in Asian equities, would increase the odds of a retest of $60,000.

The CLARITY Act delay remains a meaningful headwind. Some institutional participants had viewed the legislation as a supportive near-term catalyst. With that timeline pushed back, traders are focusing instead on macro events and whether risk appetite returns after this week’s data releases.

Trade Bitcoin on Bybit and Get a Chance to Win Our $1,000 USDT Airdrop

Bitcoin Hyper Targets Early-Mover Upside as Bitcoin Tests Key Levels

When spot BTC is rangebound and regulatory catalysts are delayed, capital looking for asymmetric exposure tends to scan earlier in the risk curve. That’s the context worth understanding here, not as a replacement thesis, but a parallel one.

The macro-driven rotation dynamic is well-established: pressure at the large-cap level historically accelerates attention toward infrastructure plays with structural differentiation.

Bitcoin Hyper ($HYPER) is positioned precisely at that intersection. It is the first Bitcoin Layer 2 with Solana Virtual Machine (SVM) integration, bringing sub-second finality, low-cost smart contract execution, and a decentralized canonical bridge for BTC transfers, all while inheriting Bitcoin’s base-layer security.

The project has raised close to $33 million at a current presale price of $0.0136838, with staking available for presale participants. The USP is genuine infrastructure differentiation: not another EVM fork, but SVM performance on a Bitcoin security layer, faster execution than Solana, while anchored to BTC’s trust model.

Research Bitcoin Hyper and review the presale details here.

The post Bitcoin Price Prediction: BTC Slides in Asian Hours, Moving in Tandem with Korean KOSPI appeared first on Cryptonews.

Hyperliquid’s SK Hynix perpetual contract briefly fell about 17.9% on July 28 after an unusually low pre-market trade in South Korea fed into the contract’s oracle pricing.

Summary

- 17.9% intraday decline followed one anomalous NXT trade involving only a single SK Hynix share.

- Trade.xyz operates the SKHX market and is investigating the oracle-driven move, Hyperliquid representatives said publicly.

- HIP-3 deployers control oracle inputs, leverage settings and settlements for markets they independently create themselves.

The market, officially listed as xyz:SKHX, tracks the U.S. dollar value of one common SK Hynix share traded in South Korea. Hyperliquid’s interface displays the contract as SKHYNIX-USDC and permits leverage of up to 10 times.

A Hyperliquid representative said the market was deployed and operated by Trade.xyz under the HIP-3 framework. Trade.xyz is investigating and plans to publish an update after reaching a conclusion, according to a statement reported by ChainThink.

One SK Hynix share triggered the initial price anomaly

The disruption began shortly after South Korea’s alternative exchange, NextTrade, opened its pre-market session. One SK Hynix share changed hands at 1.272 million won, 29.96% below the previous close of 1.816 million won.

The trade briefly placed the stock at its daily lower price limit. Korean reports attributed the print to a possible order error combined with limited liquidity during the early session. The underlying price later moved back above that isolated trade.

On-chain tracker HyperInsight said SKHX dropped from about $1,128.20 to $927 as the external price change moved through the oracle and mark-price system. The contract later recovered above $1,100.

The event occurred during a broader decline in South Korean semiconductor shares. SK Hynix closed the regular Seoul session at 1.55 million won, down 14.65%, although that closing move was less severe than the initial one-share print.Trade.xyz documentation states that the SKHX oracle tracks one SK Hynix common share and converts its Korean won price into U.S. dollars using the prevailing exchange rate.

That design allowed the unusual NXT transaction to affect the on-chain contract even though it involved only one share. Leveraged positions linked to the mark price could then face liquidations or automatic deleveraging as the contract moved lower.

DefiLlama’s later snapshot showed SKHX at approximately $1,067, down 13.7% over 24 hours. Open interest stood near $406 million after falling about 20%, while daily volume exceeded $1 billion. These figures can continue changing as positions are opened and closed.

There is no verified evidence that Hyperliquid’s blockchain or smart contracts were compromised. The available information points to an external market print passing through Trade.xyz’s pricing methodology.

HIP-3 makes Trade.xyz responsible for market operation

HIP-3 allows independent teams to launch perpetual markets on Hyperliquid while using the network’s order books, margin system and liquidation engine. The deployer defines the contract, selects its oracle and controls leverage limits and settlement.

Hyperliquid’s API documentation says deployers supply oracle prices, external perpetual prices and as many as two additional mark-price inputs. The protocol combines those values with a local price based on the best bid, best offer and latest trade. Deployers are expected to consider unusual market conditions when designing price feeds. They must stake 500,000 HYPE and can face slashing for misconduct involving their markets.

As previously reported, Hyperliquid’s HIP-3 framework places oracle selection and market controls with outside deployers. That structure expands the number of tradable assets but makes each deployer’s price methodology central to risk management.

Trade.xyz has not published its conclusion

Trade.xyz had not issued a final incident report when checked. Key unanswered questions include which NXT price inputs entered the oracle, whether filters operated as designed and whether any safeguards will change.

The market remained active after the disruption. Hyperliquid’s documentation allows deployers to halt trading, adjust open-interest limits or settle a contract, but no permanent SKHX suspension had been announced.

Notably, other decentralised exchanges have also introduced perpetual contracts for Korean stocks, increasing the links between thin local trading sessions and continuously operating crypto derivatives.

The next verified update is expected from Trade.xyz. Any final assessment should clarify whether the contract behaved according to its published rules or whether its oracle methodology requires changes.

The IMF said Brazil’s stablecoin market has expanded rapidly since 2017, with cross-border crypto flows growing faster than traditional capital flows.

Ethereum price slips below $1,900 as long liquidations surge

Women’s League Cup: What are changes for 2026-27 season?

Trump Officials Want To Use Human Rights Aid To Advocate For White South Africans And Right-Wing Causes In Europe

Renter of Home in Anne Heche Crash Denies Settlement With Son

No Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

Weekend Open Thread: Staud – Corporette.com

only money is able to pay this bills #billionairemindset #motivation #success #successhabits #money

Financial Audit Guest Steals From Homeless People

6 Smart Financial Habits That Can Make You Wealthy | Money Management Tip #youtubeshorts#motivation

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Brooks Brothers

-

NewsBeat7 days ago

NewsBeat7 days agoHow a former Blue Peter presenter stunned America’s Got Talent judges

-

Tech1 day ago

Tech1 day agoIntel is reversing course and bringing hyper-threading back to its server chips

-

Business6 days ago

Business6 days agoNew Jersey voter registration controversy explained: How 6,600 noncitizens got on the rolls, and what happens next

-

Entertainment7 days ago

Entertainment7 days agoJohnny Depp’s R-Rated Gothic Cult Classic Gets New Release Ahead of Sydney Sweeney Remake

-

Crypto World5 days ago

Crypto World5 days agoEthics, other provisions in crypto Clarity Act to be further discussed

-

Politics1 day ago

Politics1 day agoLuke Littler dismantles Gerwyn Price to retain title in Blackpool

-

Sports2 days ago

Sports2 days agoCommonwealth Games boxing: Jadumani Singh seals dominant 5-0 win over Pakistan’s Sumama Rehman to enter quarter-finals | Commonwealth Games News

-

Sports4 days ago

Sports4 days ago2026 3M Open leaderboard: Scottie Scheffler finds putter in Round 1, sits three back

-

Fashion4 days ago

Fashion4 days ago16 Dresses for the High Summer Event

-

News Videos5 days ago

News Videos5 days agoThe Peugeot Family: How 200 Years of an “Old Money” Dynasty Died in A Boardroom

-

Politics3 hours ago

Politics3 hours agoThe Part of the Electric Transition Nobody Wants to Discuss

-

Politics2 days ago

Politics2 days agoSpain sweeps the board at 2026 World Cup with individual awards

-

News Videos2 days ago

News Videos2 days agoBITCOIN JUST ENTERED THIS CRITICAL ZONE…

-

Entertainment4 days ago

Entertainment4 days agoA New Post-Apocalyptic Gundam Anime Series Blasts Into SDCC

-

Crypto World2 days ago

Crypto World2 days agoXRP Ledger adds $2.6B as RWA inflows rank second

-

Crypto World3 days ago

Crypto World3 days agoRipple bought a bank in pieces. The $4 billion audit

-

Tech3 days ago

Tech3 days agoAnthropic launches Claude Opus 5, a cheaper AI model for coding, agents and enterprise workflows

-

Crypto World5 days ago

Crypto World5 days agoUniswap (UNI) pushes deeper into tokenized RWAs with permissioned trading pools

-

Entertainment2 days ago

Entertainment2 days agoSara Gilson Killed By Husband After Viral “Pedophile” TikTok Video

You must be logged in to post a comment Login