Crypto World

BlackRock Places $5 Billion Order for SpaceX IPO Ahead of Historic Nasdaq Debut

BlackRock placed an order for at least $5 billion in SpaceX IPO shares ahead of the historic Nasdaq debut, according to Bloomberg. The move adds heavyweight institutional backing to what could be the largest IPO ever recorded.

The reported bid from the world’s largest asset manager intensifies the spotlight on the listing.

What BlackRock’s Bet on the SpaceX IPO Reveals

An IPO marks the moment a private firm begins trading on an exchange, opening its capital to a broader base of shareholders. SpaceX combines a high-impact technology narrative with a growth track record that has drawn strong demand from both institutional funds and retail investors, making this listing one of the most anticipated of the decade.

The scale of the deal is unprecedented, with SpaceX aiming to raise roughly $75 billion at a valuation near $1.8 trillion, a figure that would not only set a global IPO record but also place the company among the most valuable in the world.

BlackRock, the world’s largest asset manager, is reportedly seeking at least $5 billion in shares, a level of conviction that, according to Bloomberg, reflects either deep confidence in SpaceX’s long-term growth potential or the strategic value of securing exposure to a company of this caliber from day one of trading.

Read More: How to Buy the SpaceX IPO Stock? Crypto Users Have an Inside Lane

The order book reportedly closed on Wednesday, and lead banks are now finalizing the allocations ahead of the Nasdaq listing, a delicate process given that large funds, institutional clients, and a sizable retail segment are all competing for a limited number of shares.

A $5 billion order, however, does not necessarily translate into the final allocation, as oversubscribed IPOs typically see large investors request far more shares than they ultimately receive, particularly when demand outpaces supply by a wide margin.

Why Elon Musk’s IPO Style Is Different

Elon Musk has rewritten the traditional IPO rules for SpaceX, designing a process that gives retail investors a stronger role, pushes for early index inclusion, and embeds a governance structure built to preserve firm founder control in the years ahead.

BeInCrypto previously reported that SpaceX is considering allocating up to 30% of the offering to individual investors, a share that clearly breaks with traditional practice, where the most attractive tranches usually concentrate in the hands of institutions with close ties to the placement banks.

That detail matters far beyond the equity market, since a larger retail allocation could intensify FOMO buying around the debut and pull liquidity away from other risk assets, including Bitcoin and Ethereum, during the trading days surrounding the Friday listing.

The expectations extend beyond traditional finance, since traders on the prediction market platform Polymarket see a strong likelihood that SpaceX will rise on its public market debut, with high odds of closing with a market capitalization above $2 trillion.

Follow us on X to get the latest news as it happens

For BlackRock, the strategic logic looks straightforward, as SpaceX brings together Starship, Starlink, and a growing set of AI projects, including the recent xAI acquisition, a bundle that fits perfectly into a market that keeps rewarding growth stories tied to technology, defense, connectivity, and strong founder leadership.

The reported $1.8 trillion valuation also places SpaceX inside a tier reserved for the most dominant global companies, reflecting the confidence parts of the market assign to its competitive position and long-term business vision.

For now, all eyes are on the official Friday debut, where BlackRock’s reported $5 billion interest already signals the financial weight surrounding this listing, and the final allocations will reveal just how much each investor group ultimately receives.

The post BlackRock Places $5 Billion Order for SpaceX IPO Ahead of Historic Nasdaq Debut appeared first on BeInCrypto.

U.S. Senate Minority Leader Chuck Schumer introduced the Anti-Corruption Bureau Creation Act on July 30, proposing a federal agency with authority to investigate and pursue executive-branch corruption.

Summary

- Seven Senate-confirmed members would lead the proposed bureau, with subpoena, enforcement and reporting powers nationwide.

- Trump’s certified disclosure entries totaled over $1.4 billion across crypto-related ventures during calendar year 2025.

- Four Democratic senators sponsor the bill; its launch materials named no Republican cosponsor on Friday.

Senators Andy Kim, Alex Padilla and Jeff Merkley joined Schumer as original cosponsors.The bill cites President Donald Trump’s 2025 financial disclosure and says he received at least $2 billion from investments and business interests, including more than $1.4 billion connected to crypto ventures. The proposal does not itself establish that any disclosed income resulted from illegal conduct.

The crypto figure represents an aggregation of entries in the disclosure, rather than a single total calculated by the Office of Government Ethics. The filing reports income and transaction amounts, not the net profit that would appear on a tax return.

Anti-Corruption Bureau would combine three watchdogs

Schumer’s proposal would place the Federal Election Commission, Office of Government Ethics and Office of Special Counsel inside one independent bureau. A seven-member board confirmed by the Senate would oversee investigations, subpoenas, enforcement actions and public reporting.

The legislation would also allow state attorneys general and private plaintiffs to seek recovery of funds allegedly obtained through corruption. Its official summary describes disgorgement, treble damages and awards for successful plaintiffs. It also proposes a self-financing Freedom From Influence Fund.

A three-judge division of the U.S. Court of Appeals for the D.C. Circuit could appoint temporary board members when vacancies threaten the bureau’s operation. The provision is intended to prevent a president or Senate from disabling the agency by leaving seats vacant.

Trump’s crypto income came from several ventures

Trump’s certified disclosure lists $635.1 million in royalties from Celebration Coins. It also records hundreds of millions of dollars from World Liberty Financial token sales, equity transactions and crypto wallets, plus $196.9 million tied to a stablecoin-related holding company. Together, the listed crypto-related entries exceed $1.4 billion.

Those figures describe disclosed revenue and proceeds, not necessarily Trump’s personal after-tax earnings. As previously reported, the filing showed that crypto generated more income than Trump’s resorts and other property businesses during 2025.

The bill separately states that Trump’s family held more than $1 billion in a crypto fund connected to foreign governments. It references a reported United Arab Emirates-backed investment in World Liberty Financial. These are legislative findings and allegations, not a court judgment that corruption occurred.

White House rejects conflict-of-interest claims

White House Principal Deputy Press Secretary Anna Kelly said Trump’s investments were held in fully discretionary accounts managed by independent third-party financial institutions. She maintained there were “no conflicts of interest.” Trump has also said he does not manage his personal finances while serving as president.

Schumer described the existing federal oversight system as a “broken patchwork” and argued that its agencies were not designed to address current executive-branch conduct. The White House disputes the premise that Trump’s business income creates an unlawful conflict.

The bill faces a difficult path through Congress

The publicly released full bill text still displayed a placeholder instead of a Senate bill number on July 31. The launch announcement listed four Democratic sponsors and no Republican cosponsor. The measure must clear both chambers before reaching Trump, who could veto it.

The proposal also enters a wider debate over the Digital Asset Market Clarity Act. Senator Cynthia Lummis released updated Senate text on July 22 after the bill passed the Banking Committee by a 15–9 vote. Senator Elizabeth Warren argued that its current ethics provisions would not adequately restrict presidential crypto interests, while supporters continued to seek a bipartisan agreement.

Crypto.news reported that the CLARITY Act still faced disputes over ethics and banking provisions as supporters pressed for a vote. The Senate is scheduled to reconvene on Aug. 3, but no timetable has been announced for Schumer’s anti-corruption bill. Its next steps could include formal numbering, committee referral and hearings before any floor consideration.

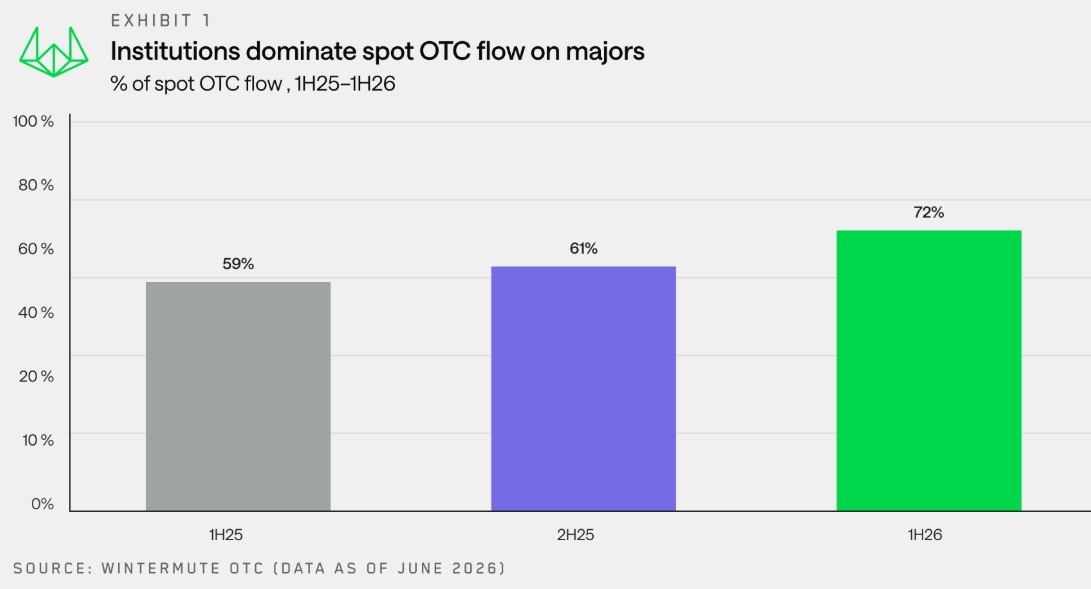

Wintermute says the next phase of altcoin momentum may look different from past cycles: fewer tokens could attract sustained inflows as institutional desks concentrate their activity into a narrower basket of assets. In a first-half 2026 OTC flow report, the market maker found that institutional counterparties accounted for the vast majority of spot trading activity on its desk—an outcome that, if mirrored across the broader market, would likely make “altseason” less broad and more selective.

The shift also appears to include a timing mismatch. Wintermute reports that institutional participation tends to fade quickly after a token’s price and volume spike, while retail activity typically stays elevated for longer—suggesting any future rallies could be more short-lived and restricted to the tokens institutions already favor.

Key takeaways

- Wintermute’s first-half 2026 OTC data shows institutional counterparties generated 72% of spot flow across all tokens on its desk—the highest share recorded—up from 61% in H2 2025 and 59% in H1 2025.

- Liquidity and attention are concentrating in the “short list” of assets institutions choose, while activity in the market’s smaller “long tail” weakens.

- The number of unique tokens traded by institutional counterparties rose only 24% from H1 2024 to H1 2026, versus 76% growth for retail clients.

- Institutional activity after a price-and-volume surge typically cools within about one day, while retail activity remains elevated for around three days.

Institutional desks are pulling OTC liquidity toward a smaller set of tokens

Wintermute’s OTC flow report points to a structural change in how capital is deployed across the altcoin market. According to Wintermute, institutional counterparties drove 72% of spot flow across all tokens handled on its OTC desk in the first half of 2026—its highest recorded level. That compares with 61% in the second half of 2025 and 59% in the first half of the previous year.

While institutional participation has been rising, Wintermute’s interpretation matters for traders and investors: when the majority of activity is concentrated among a smaller group of counterparties and assets, rallies can become narrower. The firm said liquidity is increasingly clustering in tokens institutions favor, while the broader “long tail” of smaller tokens sees less consistent engagement.

That concentration effect is reinforced by the growth rates in token participation. Wintermute found that from H1 2024 to H1 2026, the number of unique tokens traded by institutional counterparties increased by 24%, whereas retail clients increased their number of unique traded tokens by 76% over the same span. In practical terms, the data suggests that retail participants explore a wider range of assets, while institutional flow remains comparatively disciplined.

Faster institutional pullbacks after spikes could reshape altcoin rally dynamics

Another detail in Wintermute’s report relates to how quickly activity cools after a token experiences a surge. The firm found that institutional activity following spikes in a token’s price and volume faded after roughly one day. Retail behavior differed: Wintermute says retail activity typically stays elevated for about three days after similar surges.

If these patterns extend beyond Wintermute’s OTC venue, they can influence how traders structure exposure during altcoin moves. Short-lived institutional participation can mean that order flow—and therefore liquidity—does not remain supportive for as long as it may have in earlier cycles when broader rotation into many assets sustained momentum.

For market participants, the implication is straightforward: rallies may require faster decision-making and more asset-selective positioning, because the “institutional bid” may not persist the way it once did across a wide swath of tokens.

Other data points suggest “altseason” rotation is narrowing across venues

Wintermute’s proprietary OTC findings add to a growing set of signals that capital is clustering around fewer altcoins. On June 20, CryptoQuant CEO Ki Young Ju said the “traditional rotation of Bitcoin profits” into smaller assets had “basically disappeared.” CryptoQuant data referenced by Young Ju suggested that trading volume in Bitcoin-denominated altcoin pairs was near its weakest level since 2021.

Meanwhile, CryptoQuant’s CEO also pointed to market cap concentration. The 10 largest non-stablecoin altcoins accounted for about 80.5% of the non-Bitcoin, non-stablecoin market’s capitalization—another indicator that the market’s center of gravity is increasingly tilted toward the biggest names in the category.

Exchange-level data has also suggested a similar pattern. In July 2025, Kaiko reported that the ten largest altcoins made up 63% of altcoin trading volume, up from roughly 50% several months earlier as activity in smaller tokens weakened. Together with Wintermute’s OTC numbers, the message across different datasets is consistent: liquidity and trading interest are drifting toward the same smaller group of assets.

Market debate: broad rallies vs. selective sector moves

The question now facing investors is whether this concentration will permanently reduce the breadth of future altcoin runs—or simply change their shape. DWF Labs managing partner Andrei Grachev has argued that broad altcoin rallies are giving way to more selective sector activity. In March 2025, Grachev said too many tokens were competing for limited capital, while institutional investors remained focused on Bitcoin, Ether, and tokenized real-world assets.

This framing aligns with the mechanics Wintermute describes: if institutions are more concentrated, and their participation fades quickly after price and volume spikes, “rotation” may become less of a market-wide wave and more of a series of targeted moves. In such an environment, tokens outside the institutional comfort zone may struggle to attract sustained liquidity, even if retail interest remains visible for a brief period.

It also highlights a potential tension between retail and institutional behavior. Retail participation appears to spread across more tokens and remain elevated longer after bursts. But if institutional desks dominate overall spot flow on major venues and OTC desks, retail-led excitement may not be enough to maintain broad-based momentum without follow-through from larger pools of capital.

For readers, the key watch items are whether institutional concentration continues to increase beyond H1 2026, and whether the “one-day” institutional fade and “three-day” retail persistence become stable patterns across more tokens and more trading conditions. If they do, the definition of “altseason” may shift from a widespread rotation into many names to a narrower, faster-moving set of trades that reflect where liquidity is actually concentrated.

Roughly 594 bitcoin, worth about $38 million, was swept out of around 500 separate wallets between 01:31 and 01:56 UTC on Friday in an attack traced to a flaw in how Coldcard hardware wallets generated their keys.

The theft moved 1,324 chunks of bitcoin across 500 transactions inside a three-block window, with 562 BTC then consolidated into a single address that has not moved.

Every drained wallet was single-signature and each held more than 0.15 BTC. Many had been dormant for years and the coins spanned 2021 to 2026, matching the flaw’s age almost exactly.

Coldcard is a hardware wallet built by Canadian firm Coinkite, a small standalone device that stores bitcoin keys offline, away from internet-connected computers. Mk2, Mk3, Mk4, Q and Mk5 are successive generations of that product, released over several years the way a phone maker ships numbered models.

Exposure depends on the firmware the device was running at the moment the wallet was first created, not on when the hardware was bought.

A wallet’s seed, the secret phrase controlling the funds, is meant to be drawn at random from a pool so vast that guessing is hopeless.

Canary Capital renewed its marketing push for the Canary HBAR ETF on July 30, describing HBR as the first U.S. spot exchange-traded product holding Hedera’s native token.

Summary

- 704.3 million HBAR backed Canary’s fund, with net assets near $47.8 million on July 30.

- 5.18 million HBR shares were outstanding after Canary added fifty thousand shares in latest update.

- HBR’s 0.95% sponsor fee accompanied a 37.32% year-to-date market-price decline recorded through July 29, 2026.

The post was not a new launch announcement. HBR began trading on Nasdaq on Oct. 28, 2025, after its registration became effective with the U.S. Securities and Exchange Commission.

The latest fund data gives a clearer view of its current scale. HBR held 704.35 million HBAR and reported about $47.8 million in net assets on July 30. The product had 5.18 million shares outstanding and charged a 0.95% sponsor fee.

Canary HBAR ETF now holds 704 million HBAR

Canary’s official fund page shows that HBAR represented effectively all the trust’s assets, apart from about $30 in cash and other items. The 704.35 million-token position was valued at approximately $47.8 million using the administrator’s stated price. HBR provides price exposure through brokerage accounts without requiring investors to manage private keys.

Shares outstanding increased from 5.13 million on July 28 to 5.18 million on July 29. That 50,000-share increase was the latest reported expansion in the fund’s share count. It does not, by itself, establish the identity or strategy of the investors behind the creation.

Additionally, HBR recorded $989,000 in net inflows on July 2, its largest single-day inflow since May 15. The fund then listed roughly $49.14 million in net assets, showing that its asset value can move even when new shares enter because HBAR’s market price also changes.

Latest filing shows losses despite share growth

HBR’s first-quarter SEC filing showed 4.2 million shares outstanding and $50.34 million in net assets on March 31. The trust created 740,000 shares and recorded no redemptions during the quarter. However, HBAR depreciated 17.8% during the period, and the fund reported a $10.58 million decrease in net assets from operations.

More recent performance data remained weak. Canary listed HBR’s market-price return at negative 37.32% for 2026 through July 29 and negative 63.32% since inception. Its net asset value return was negative 36.48% year-to-date.

In the latest market data available early July 31, HBR traded near $9.33, while HBAR changed hands around $0.0727. Those figures show current pricing only and do not prove that Canary’s July 30 post caused any market move.

Enterprise and tokenization claims need context

Canary said HBR gives registered access to a network governed by organizations including Google and IBM. The Hedera Council says its members run network nodes, vote on governance matters and approve technology updates. Its structure uses equal voting rights and term limits.

The asset manager also called HBR “built for the next wave of real-world asset tokenization.” That is a forward-looking marketing claim rather than a verified forecast. One related development has already occurred: Archax tokenized the HBR ETF on Hedera and completed an after-hours transaction on Nov. 27, 2025, according to a Hedera case study.

That blockchain transaction did not change how ordinary Nasdaq investors buy and sell HBR shares. It instead demonstrated a separate tokenized representation handled through regulated market infrastructure.

What investors should watch next

HBR is structured as a single-asset trust, not an investment company registered under the Investment Company Act of 1940. Canary warns that the product is not diversified and that investors could lose their entire principal. The trust currently lists BitGo Trust Company and Coinbase Custody Trust Company as its digital-asset custodians.

Investors will next look for the quarterly SEC filing covering the period ended June 30. That report will provide fuller figures for share creations, redemptions, expenses and changes in the trust’s HBAR position. Until then, daily holdings, share counts and net assets provide the most current official measures of fund activity.

HBR’s history also matters when assessing Canary’s new promotion. In related coverage, crypto.news reported on the fund’s path to launch in October 2025. The July post therefore renews attention around an existing product rather than introducing a new U.S. HBAR ETF.

Binance Research said on July 30 that the first half of 2026 produced a “broad on-chain contraction, not a rotation.”

Summary

- 38% DeFi TVL decline erased $43.4 billion as six major Layer 1 valuations fell 42%.

- 77% fewer Layer 2 user operations contrasted with Ethereum’s smaller 9% decline through June 2026.

- 207 security incidents caused $972 million in losses, while prediction markets reached $51.6 billion monthly.

Its 52-page report found that DeFi total value locked fell by $43.4 billion, or 38%, while the combined market capitalization of Ethereum, BNB, Solana, Tron, Sui and NEAR declined by $246.5 billion, or 42%.

Crypto market contraction hit DeFi and major L1s

The decline spread across capital, lending and network valuations rather than moving money cleanly from one blockchain sector into another. DeFi TVL dropped 38.7% during the half, nine percentage points more than the broader crypto market. Active loans fell 38%. April brought the steepest deterioration as large exploits reduced confidence in supplying onchain liquidity.

Current data shows a limited rebound rather than a full reversal. DefiLlama listed total DeFi TVL at about $74.9 billion on July 31. Based on Binance Research’s reported decline, the end-June level was roughly $70.8 billion. That calculation suggests some value returned in July, although token prices and differences in measurement can change TVL figures.

Security losses added to the pressure. TRM Labs independently recorded 207 hacks and $972 million stolen during H1, more than double the 83 incidents a year earlier. Smart-contract exploits accounted for 125 incidents. Infrastructure and operational failures represented about 76% of stolen value. As crypto.news previously reported, April attacks erased billions of dollars from DeFi TVL.

Ethereum treasuries overtook ETFs as L2 usage fell

Ethereum’s holder mix changed during the downturn. Binance Research said spot ETF balances declined from more than 6 million ETH to 5.2 million ETH. Digital asset treasury companies moved in the other direction, increasing their holdings from 6 million to 7.7 million ETH. The report sourced those figures from SoSoValue and Blockworks as of July 1.

Higher throughput did not create stronger base-layer revenue. Average gas prices fell 75% from 2025 after Ethereum raised its gas limit to about 60 million, while transaction count rose roughly 50%. Binance Research said chain revenue is “projected to fall 53% by year end if conditions persist.” That figure is a forecast, not a confirmed full-year result.

Layer 2 networks recorded a sharper usage decline than Ethereum mainnet. Total L2 user operations fell about 77% between January and June, compared with 9% on Ethereum. In June, L2s collected around $15 million in fees but paid Ethereum only $66,397 for data availability. In related coverage, crypto.news examined how Ethereum retained deeper TVL while Solana led several activity and revenue measures.

Solana revenue weakened while BNB remained deflationary

Solana’s network real economic value, which includes transaction fees and out-of-protocol tips, fell from $40 million in January to $14 million in June. Binance Research linked much of the 64.5% decline to weaker memecoin trading. Pump.fun volume fell from $30 billion to $17 billion over the same period, although memecoins still represented 25% of Solana DEX volume in June.

BNB moved differently on supply. The report identified BNB as the only deflationary major L1, with a 5.05% annualized burn rate. Its tokenized RWA market value also rose 107% to $3.8 billion in H1. However, that growth did not offset the broader decline across DeFi and major L1 valuations.

Prediction markets and tokenized assets resisted the slump

Tokenized real-world assets were among the clearest growth areas. Their distributed value increased from about $22 billion in January to roughly $34 billion by mid-July. BNB Chain led tokenized equity DEX volume, while tokenized equities reached 4% of Solana DEX activity in June. As crypto.news reported, tokenized stock products recently reached 752,000 holders across several networks.

Prediction markets also expanded during the 2026 FIFA World Cup. Monthly notional volume rose 86% from January to $51.6 billion in June. Kalshi recorded about $33 billion and Polymarket about $14.5 billion, giving the pair 92% of the month’s volume. Non-sports activity across both platforms rose 136%, indicating that growth was not limited to football markets.

In addition, the World Cup pushed Polymarket past $5 billion in tournament volume. Binance Research cautioned that H2 “will test” whether tournament-driven users remain active and whether regulation and settlement systems can support continued growth.

Network upgrades now provide measurable milestones. BNB Chain has scheduled its Pasteur hard fork for Aug. 25 at 02:30 UTC. Ethereum lists Glamsterdam for H2 2026 without a firm mainnet date. Meanwhile, Solana’s latest official release information points to Alpenglow activation with Agave 4.3 in October, later than the Binance report’s Q3 target.

The second half will therefore show whether lower fees and added capacity can rebuild durable demand. It will also test whether tokenized assets gain secondary liquidity and whether prediction-market activity survives after the World Cup. Until those trends appear in sustained usage, revenue and capital data, Binance Research’s contraction thesis remains the clearest reading of H1.

Crypto’s next altcoin season may produce fewer winners as institutional investors concentrate their activity in a narrower group of digital assets, according to crypto market maker Wintermute.

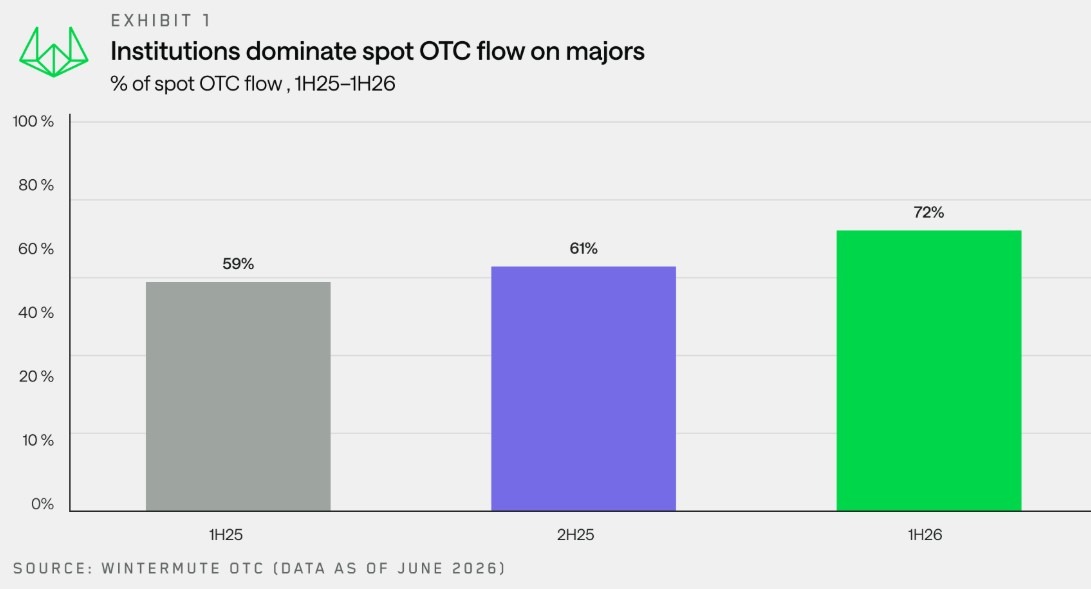

In its over-the-counter (OTC) flow report for the first half of 2026, Wintermute said institutional counterparties generated 72% of spot flow across all tokens on its OTC desk, the highest share on record. That was up from 61% in the second half of 2025 and 59% in the first half of last year.

With institutional activity concentrated in fewer tokens and fading faster after price surges, the findings suggest future altcoin rallies could become narrower and more selective. Wintermute said liquidity was concentrating in the assets institutions favored while activity across the market’s “long tail” weakened.

Between the first half of 2024 and the first half of 2026, the number of unique tokens traded by Wintermute’s institutional counterparties grew by just 24%, compared with 76% among retail clients. The firm also found that institutional activity following a surge in a token’s price and volume faded after roughly one day. In contrast, retail activity typically remained elevated for about three days.

Percentage of institutional spot OTC flow. Source: Wintermute

Altcoin capital was already becoming more concentrated

Wintermute’s findings add proprietary OTC data to signs that capital has been clustering around a smaller group of altcoins across the wider market.

On June 20, CryptoQuant CEO Ki Young Ju said the traditional rotation of Bitcoin profits into smaller crypto assets had “basically disappeared.” CryptoQuant data showed trading volume in Bitcoin-denominated altcoin pairs near its weakest level since 2021.

Meanwhile, the 10 largest non-stablecoin altcoins accounted for about 80.5% of the non-Bitcoin, non-stablecoin market’s capitalization.

Related: Crypto altseason unlikely in 2026 as ‘blue-chip survivors’ to win out: Analyst

Kaiko identified a similar concentration in exchange trading. In July 2025, the data provider said that the ten largest altcoins accounted for 63% of altcoin trading volume, up from about 50% several months earlier, as activity in smaller tokens weakened.

DWF Labs managing partner Andrei Grachev also argued that broad altcoin rallies were giving way to selective sector moves. On March 15, Grachev said too many tokens were competing for limited capital, while institutional investors remained focused on Bitcoin, Ether and tokenized real-world assets.

Magazine: The 100x obsession: Fundamentals grow in importance as crypto matures

Coinkite warned Coldcard Mk3 users on July 30 to move Bitcoin from wallets whose seed phrases were generated on affected firmware.

Summary

- 594 BTC moved across 500 transactions during a coordinated three-block sweep involving single-signature Bitcoin addresses.

- Coldcard Mk3 seeds generated on firmware 4.0.1 through 5.0.3 may face risk, Coinkite warned users.

- No public evidence yet links the Mk3 seed issue directly to the 594 BTC sweep.

The Canadian hardware maker said seeds created on firmware 4.0.1 or any later Mk3 release through version 5.0.3 may put funds at risk.

The notice arrived as security researchers examined a coordinated sweep of 594.48 BTC, worth about $38.2 million at a Bitcoin price near $64,324. However, Coinkite and independent researchers have not established that the Mk3 issue caused those transfers.

Coldcard Mk3 warning covers firmware since 4.0.1

Coinkite’s official advisory said its investigation remains active. The company said the Coldcard Mk4, Q and Mk5 are not affected based on its early analysis. It also said wallets using an affected seed with a BIP-39 passphrase face “minimal risk,” while stressing that a passphrase is different from the device PIN.

The advisory now gives users more detailed migration options. Coinkite recommends generating a new seed on an unaffected device, verifying the backup and receiving address, sending a small test transaction and moving the remaining balance only after the test confirms the setup works.

The 594 BTC sweep remains unlinked to Coldcard

AnchorWatch CEO Rob Hamilton reported that 1,324 unspent transaction outputs moved through 500 transactions within a three-block window. The transfers swept 594.48 BTC from single-signature addresses, after which 562 BTC was consolidated into another address.

Hamilton wrote, “At a glance, this looks like there was flawed entropy” during wallet generation. That statement was a preliminary assessment, not a confirmed cause. A Reddit account also described a drained wallet tied to a Mk3-generated seed, but the self-reported account does not prove a wider connection.

Wizardsardine CEO Kevin Loaec described low randomness in a wallet generator as his “current hypothesis.” He said the source could be a software library, secure element, device batch or firmware version. He also proposed that an attacker may have searched a narrow set of BIP-84 paths, which could explain the concentration in native SegWit addresses and partial sweeps.

https://x.com/KLoaec/status/2082926304995762209?s=20

Loaec’s theory remains unverified. No public technical report has identified the faulty component, measured the available entropy or shown how an attacker derived the keys. Coinkite’s advisory still promises a formal technical review, but the company had not published that review at the time of writing.

The case resembles a broader class of weak-randomness failures. In related coverage, crypto.news reported on the Ill Bloom vulnerability, which Coinspect linked to weak recovery-phrase generation across several blockchains.

As previously reported, the older Randstorm vulnerability affected BitcoinJS wallets that did not generate sufficiently random private keys. That case involved wallets created between 2011 and 2016 and is separate from the current Mk3 investigation.

Affected users have two fallback migration paths

Users with an unaffected Coldcard can create a new seed there and migrate carefully. Coinkite advises preserving the old backup until the entire transfer is confirmed. Users should verify every address on the hardware screen and avoid entering seed words or passphrases on websites or untrusted devices.

For users whose Mk3 is their only option, Coinkite suggests a strong, unique BIP-39 passphrase as a temporary measure. Advanced users may instead create a dice-only seed on an empty Mk3 running firmware 4.1.9 by entering at least 99 independent rolls of a fair six-sided die. The company cautioned that this procedure requires careful backup and verification.

What happens next depends on Coinkite’s technical review and continued on-chain analysis. Until investigators publish a confirmed root cause, the 594 BTC sweep and the Mk3 seed-generation warning should be treated as related in timing but not proven to share the same cause.

Canadian hardware wallet vendor Coinkite has issued an urgent security advisory for its Coldcard Mk3 signing device, warning users to move funds away from wallets whose seed phrases were generated on certain Mk3 firmware versions. The company says the issue affects Mk3 firmware 4.0.1 through 5.0.3, and that affected seeds may put funds at risk.

The warning arrives as Bitcoin investigators and security specialists scrutinize an unrelated-looking but highly unusual sweep of 594.48 BTC from single-signature addresses. While commentators have connected the timing to Mk3 devices, Coinkite stresses that no definitive public proof has linked its firmware warning to the broader sweep.

Key takeaways

- Coinkite’s advisory targets Coldcard Mk3 firmware versions 4.0.1 to 5.0.3; Mk4, Q, and Mk5 are stated as not affected.

- The recommended response is to generate a fresh seed on an unaffected device, verify backups and receiving addresses, then send test transactions before moving remaining funds.

- Early internal analysis from Coinkite indicates BIP-39 passphrases (distinct from the device PIN) may face minimal risk.

- Security experts are analyzing a separate event: a sweep of 594.48 BTC across 500 transactions within a narrow three-block window from single-signature addresses.

Coinkite flags an Mk3 firmware window

In a post on its official blog, Coinkite said that seeds created on a Coldcard Mk3 running firmware version 4.0.1 (released in March 2021) or any later Mk3 firmware may expose funds to risk. The company extends the affected range through firmware version 5.0.3, described as the final firmware supporting the Mk3.

Coinkite’s early analysis also draws a boundary around which components of wallet setup are most relevant. It said seeds used with a BIP-39 passphrase face minimal risk, while clarifying that this refers to a passphrase rather than the Coldcard PIN.

Importantly, the company framed its guidance as a precautionary measure. “Out of an abundance of caution,” Coinkite urged users with potentially affected seeds to generate a new seed on an unaffected device, confirm the backup, verify the receiving address, send a small test transaction, and only then transfer the rest of their funds. Coinkite added that its investigation is still ongoing and that it will deliver a formal technical review.

What triggered renewed attention: the 594.48 BTC sweep

Interest in this broader incident intensified after a Reddit user reported that a wallet drained from an account associated with a Coldcard Mk3 purchased in May 2021 had later been restored onto a Coldcard Mk4 in January 2026. That user’s account is self-reported and does not, by itself, establish a direct connection between the Mk3 firmware warning and the sweep activity.

Separately, AnchorWatch CEO and co-founder Rob Hamilton published a preliminary analysis stating that 1,324 unspent transaction outputs were swept across 500 transactions in a three-block window, moving a total of 594.48 BTC. In his write-up, Hamilton noted that all affected addresses were single-signature, and that 562 BTC was later consolidated into another address.

Hamilton described the pattern as consistent with “flawed entropy in wallet generation somewhere along the way,” echoing the possibility that randomness quality during seed creation may have mattered. At the time of writing, the 594.48 BTC was estimated to be worth about $38.3 million based on Bitcoin’s price of $64,364.07, according to CoinGecko.

Experts debate cause: low-entropy seeds and partial drainage

Another security researcher, Wizardsardine CEO Kevin Loaec, offered a hypothesis focused on the randomness source itself rather than the sweep mechanics. In a separate post, Loaec said his current theory is that a low-entropy random-number generator—potentially located in a software library, a secure element, or a specific device batch or firmware version—produced wallet seeds with insufficient randomness.

Loaec further suggested that if attackers were aware of the flaw, they may have used an AI-generated brute-force script. In his account, the search was confined to a limited set of BIP-84 derivation paths, which could help explain why the sweep appears concentrated in native SegWit addresses and why some wallets were only partially drained. He emphasized that the idea remains unconfirmed.

Crucially, Loaec warned that if his model is correct, wallets that saw only partial drainage could remain vulnerable to additional attempts. He also said funds in other address types might be exposed if the attacker expands scanning beyond the initially targeted formats.

Why the guidance matters for users—especially in light of the speculation

Even though Coinkite has not publicly connected the Coldcard Mk3 firmware issue to the 594.48 BTC sweep, the overlap in themes—seed quality, single-signature theft, and concentrated sweep behavior—means the advisory should be treated as a direct action item. Hardware-wallet incidents differ from typical “compromised computer” narratives: if the weakness is in seed generation, reusing the same seed (even on a different device) can keep exposure alive.

That’s why Coinkite’s recommended operational steps are specific and defensive: creating a new seed on an unaffected device, validating backups, confirming the correct receiving address, and using a small test transfer before moving the remainder. This sequence is aimed at reducing the risk of both theft and user error during migration—two failure modes that often show up around recovery events.

For users, the key uncertainty is whether the sweep investigators will eventually find deterministic evidence linking the Mk3 firmware range to the stolen outputs. Until then, Coinkite’s advisory stands independently as a risk-management decision for any Coldcard Mk3 owner who created seeds during the stated firmware window.

Going forward, readers should watch for Coinkite’s promised formal technical review and for any public forensic work that either corroborates or rules out a relationship between the Mk3 seed-generation warning and the 594.48 BTC sweep pattern described by security specialists.

The American Arbitration Association launched a specialist Web3 Panel on July 29, creating a roster of arbitrators for disputes involving blockchain systems, smart contracts, digital assets, tokenization and autonomous transactions.

Summary

- Five initial arbitrators bring legal, academic and technology experience to blockchain and digital asset disputes.

- AAA will handle business and consumer Web3 cases under its existing arbitration and mediation rules.

- Parties still need an arbitration agreement before the specialist panel can hear their particular dispute.

The New York-based organization said the panel is intended for commercial conflicts that combine familiar contract questions with technical evidence and cross-border activity. The official AAA announcement said the organization will continue recruiting specialists as the panel expands.

The launch does not establish a regulator or court. Instead, it adds specialists to the AAA’s existing arbitration and mediation system. Parties must still have an arbitration agreement, or agree after a dispute arises, before the organization can administer a case.

AAA Web3 panel covers code, custody and governance disputes

The AAA said the panel may hear disagreements over contract formation, governance, asset control, cybersecurity, transaction records and cross-border enforcement. Its dedicated Web3 dispute-resolution page also lists smart-contract bugs, exchange restrictions, wallet custody, stolen-asset recovery, DAO voting and tokenized-asset rights.

The scope extends beyond cryptocurrency. Agentic commerce and autonomous transactions are included because software or artificial intelligence systems may negotiate, authorize or execute agreements with limited human involvement.

Eric Dill, the AAA’s head of panel relations, said “Web3 disputes involve familiar commercial questions in a highly technical environment.” That statement describes the organization’s reasoning for creating the panel. It does not establish a new legal standard.

In related coverage, a smart contract explainer described these systems as automated blockchain code rather than legal documents. Code can execute transactions, but it cannot interpret intent or independently enforce real-world remedies.

Five initial members combine legal and technical experience

The initial roster includes Kabir Duggal of Akin Gump, technology disputes lawyer David Evans and University of Pennsylvania law professor David Hoffman. Nelson Mullins partner Paula Pendley and Google Cloud Web3 strategy head Rich Widmann also joined the panel.

Their stated experience covers international arbitration, automated commerce, decentralized finance, Bitcoin mining, artificial intelligence infrastructure and digital-asset businesses.

The AAA said it is continuing to recruit arbitrators as new technologies and business models produce additional disputes. However, it did not announce a fixed panel size, a first assigned case or a timetable for expansion.

Therefore, the launch establishes an available specialist roster rather than a mandatory forum for the crypto industry. Companies and customers will still need a valid contractual basis to bring disputes before the AAA.

Existing arbitration rules will still govern cases

Business-to-business technology disputes will generally proceed under the AAA’s Commercial Arbitration Rules. Disputes between consumers and exchanges, wallet providers or other businesses will usually use its Consumer Arbitration Rules.

A claimant must submit an arbitration demand, describe the claim, provide the relevant arbitration clause and pay the applicable filing fee. The panel itself does not gain enforcement or supervisory authority over exchanges, protocols or token issuers.

Under Section 2 of the Federal Arbitration Act, written agreements to arbitrate commerce-related disputes are generally enforceable, subject to legal grounds that may invalidate other contracts. Courts may still become involved when parties contest whether they agreed to arbitrate or seek enforcement of an award.

That distinction has already mattered in crypto cases. As previously reported, the U.S. Supreme Court ruled against Coinbase in a Dogecoin sweepstakes dispute, finding that a court had to decide which of two conflicting contracts controlled.

What happens next for the AAA Web3 panel

Companies seeking access to the panel can add an AAA arbitration clause to commercial agreements. They can also submit an existing dispute when their contract already names the AAA or its rules.

The organization says blockchain transactions are generally not reversed by arbitration itself. Instead, an award or settlement may require repayment, a new asset transfer or another remedy conducted outside the original transaction.

The AAA plans to expand the roster as disputes develop around automated systems, tokenization and AI-driven transactions. As of July 30, its public announcement did not disclose pending case volumes, expected Web3-specific fees or a deadline for adding new members.

The panel arrives as arbitration is already being used in major digital-asset disputes. Kraken secured a $22 million arbitration award against former auditor Mazars USA before seeking court confirmation of the decision.

The Ethereum Foundation appointed Pascal Caversaccio, known as pcaversaccio, to its board on July 29 for an initial one-year voluntary term.

Summary

- One-year voluntary appointment places Pascal Caversaccio on the Ethereum Foundation’s four-member governing board alongside Buterin.

- SEAL 911 provides round-the-clock incident response and reports protecting more than $180 million in assets.

- Privacy and security now guide protocol work spanning layer-one privacy, post-quantum protection, and safer transactions.

The move expands the governing body to four members as the organization places greater weight on privacy, security and censorship resistance.

Caversaccio joins Ethereum co-founder Vitalik Buterin, Foundation President Aya Miyaguchi and Swiss counsel Patrick Storchenegger. The official board update described him as a longtime Ethereum contributor, a co-founder and lead of SEAL 911, and a member of the Foundation’s Silviculture Society.

Ethereum Foundation adds a security specialist

The Ethereum Foundation said its board sets the organization’s vision and checks whether management’s strategies remain aligned with its values. It also described the body as a “security council” that protects the Foundation’s mission and ensures compliance as a Swiss foundation. That wording reflects the Foundation’s governance model rather than a separate regulatory status.

Caversaccio’s background combines technical security work and privacy advocacy. He wrote The Ethereum Cypherpunk Manifesto in 2024 and Ethereum Privacy: The Road to Self-Sovereignty in 2025. The Foundation also credited him with advancing security practices through technical contributions and community work.

Privacy and security shape the new structure

The appointment follows the Ethereum Foundation’s June reorganization, which reduced its workforce by 54 people, or roughly 20%. The new structure divided work across protocol, access, user, community and institutional layers, alongside operations and management teams.

Within that structure, the protocol cluster treats privacy and security as “non-negotiable protocol guarantees.” Its stated work includes layer-1 privacy, post-quantum security, safer protocol upgrades, reduced technical complexity and defences against harmful maximum extractable value practices.

However, the Foundation’s formal mandate places privacy and censorship resistance at the centre of its work. The mandate does not give the Foundation control over Ethereum. Instead, it describes the organization as one steward among many across the network.

SEAL 911 adds incident-response experience

SEAL 911 is a free, around-the-clock emergency service for active or imminent crypto security incidents. Security Alliance says the initiative has handled more than 3,300 tickets, coordinated over 125 war rooms and helped rescue more than $180 million in assets.

That operational background gives Caversaccio experience with exploits, compromised wallets, protocol failures and fund-recovery efforts. However, the Foundation did not announce any new security programme, budget or incident-response authority tied directly to his appointment.

The two organizations already have a working relationship. The Ethereum Foundation sponsored a SEAL security engineer in February to track and counter crypto drainers targeting Ethereum users.

In related coverage, the Foundation explained how its protocol security team uses coordinated artificial-intelligence agents to identify and verify software flaws. The team reported finding a remotely triggered libp2p flaw that was fixed and disclosed as CVE-2026-34219.

What happens during the one-year term

The board update did not specify committee assignments, voting powers beyond normal board duties or measurable targets for Caversaccio’s first year. It also did not announce compensation, stating only that the role is voluntary and begins with an initial one-year term.

His main formal responsibility will therefore remain board-level oversight. Management will continue to handle execution, while the board reviews whether major strategies and decisions fit the Foundation’s mandate and Swiss legal obligations.

The appointment may place more security and privacy expertise inside those reviews, but the Foundation did not promise specific protocol changes. Work on layer-1 privacy, post-quantum protection and safer transactions will still move through researchers, developers and Ethereum’s broader governance process.

The Foundation has not announced an exact end date for the term or whether Caversaccio may be reappointed. Any continuation beyond the initial year would require a later board decision or public update.

XRP, XLM & HBAR: IT’S FINALLY HAPPENING!

FMC Corporation (FMC) Q2 2026 Earnings Call Transcript

Zendaya Spider-Man Premiere Makeup: How To Get Her Charlotte Tilbury Red Carpet Glow

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Brooks Brothers

-

Sports4 days ago

Sports4 days agoCommonwealth Games boxing: Jadumani Singh seals dominant 5-0 win over Pakistan’s Sumama Rehman to enter quarter-finals | Commonwealth Games News

-

Business1 day ago

Business1 day agoWhy Trees Belong on the Risk Register

-

Tech4 days ago

Tech4 days agoIntel is reversing course and bringing hyper-threading back to its server chips

-

Crypto World5 days ago

Crypto World5 days agoRipple bought a bank in pieces. The $4 billion audit

-

Politics4 days ago

Politics4 days agoLuke Littler dismantles Gerwyn Price to retain title in Blackpool

-

Entertainment7 days ago

Entertainment7 days agoA New Post-Apocalyptic Gundam Anime Series Blasts Into SDCC

-

Politics3 days ago

Politics3 days agoThe Part of the Electric Transition Nobody Wants to Discuss

-

News Videos4 days ago

News Videos4 days agoBITCOIN JUST ENTERED THIS CRITICAL ZONE…

-

Business2 days ago

Business2 days agoMajor shareholder moves on Canyon

-

Crypto World5 days ago

Crypto World5 days agoXRP Ledger adds $2.6B as RWA inflows rank second

-

News Videos18 hours ago

News Videos18 hours agoBitcoin Enters the 3rd Stage of the Bear Market

-

Politics5 days ago

Politics5 days agoSpain sweeps the board at 2026 World Cup with individual awards

-

Entertainment2 days ago

Entertainment2 days ago‘Stargate’ Creator’s New Sci-Fi Series Returns for Season 3 Tomorrow

-

Entertainment5 days ago

Entertainment5 days agoSara Gilson Killed By Husband After Viral “Pedophile” TikTok Video

-

Crypto World2 days ago

Crypto World2 days agoKraken Enables Retail Access to Jersey Mike’s IPO via Tokenized Shares

-

Tech6 days ago

Tech6 days agoAnthropic launches Claude Opus 5, a cheaper AI model for coding, agents and enterprise workflows

-

News Videos2 days ago

News Videos2 days agoClaude: Build Financial Dashboards in Minutes (2026)

-

Politics13 hours ago

Politics13 hours agoLuke Littler’s dominance sparks GOAT debate

-

Tech3 days ago

Tech3 days agoNew macOS Sequoia & Sonoma security updates for older Macs

You must be logged in to post a comment Login