Crypto World

Broadcom (AVGO) Stock Climbs as AI Chip Sales More Than Double in First Quarter

Key Takeaways

- First quarter revenue reached $19.3 billion, representing 29% annual growth and setting a company record

- Artificial intelligence revenue more than doubled, climbing 106% to $8.4 billion and exceeding internal projections

- Second quarter outlook calls for $22 billion in total revenue, including $14.8 billion from AI operations

- Morgan Stanley upgraded its price objective to $470 from $462 while maintaining an Overweight stance

- Wall Street analysts forecast potential AI revenue reaching $120 billion by fiscal year 2027

Shares of Broadcom (AVGO) finished March 5 trading at $322.77, marking a 4.8% gain following the chipmaker’s fiscal first quarter 2026 earnings release. The stock has experienced modest declines since that session and continues trading below its year-to-date starting point.

The company delivered quarterly revenue of $19.31 billion, surpassing Wall Street’s $19.18 billion projection and establishing a new high-water mark. Earnings per share on an adjusted basis reached $2.05, topping the Street’s $2.03 estimate.

The headline figure came from artificial intelligence operations — $8.4 billion in revenue representing 106% year-over-year expansion and exceeding the company’s own internal forecasts.

Custom AI accelerator chip revenue drove much of this performance, skyrocketing 140% from the prior-year period. Revenue from AI networking products increased 60%, with management indicating that networking growth should accelerate significantly in the current quarter thanks to Tomahawk Ethernet switching technology and SerDes product lines.

Adjusted EBITDA expanded 30% annually to $13.1 billion, translating to margins of 68% relative to revenue. Gross profit margins settled at 77%, down from 79.1% in the year-ago quarter but showing sequential stability.

Focus Shifts to Custom AI Chip Performance

Semiconductor solutions revenue climbed 52% year-over-year to $12.5 billion overall. Traditional non-AI chip revenue, by contrast, expanded just 4% — highlighting where the company’s growth engine truly resides.

Infrastructure software revenue increased modestly by 1% to $6.8 billion. Within that category, VMware-related revenue posted 13% growth.

During the earnings conference call, CEO Hock Tan pushed back against concerns that hyperscale AI developers might bypass chip partners like Broadcom by developing proprietary silicon. His counterargument was direct: “You need the best silicon design team around. You need cutting-edge SerDes, very advanced packaging. We’ve been doing this for more than 20 years. I would say we are by far way out there, and we will not see competition in customer-owned tooling for many years to come.”

CFO Kirsten Spears highlighted that the company distributed $10.9 billion to shareholders during the quarter — $3.1 billion through dividends and $7.8 billion via stock repurchases. Management also authorized an additional $10 billion buyback program extending through calendar year 2026.

Wall Street Analyst Lifts Valuation Target

Morgan Stanley’s Joseph Moore increased his valuation target on AVGO to $470 from a previous $462, reaffirming an Overweight recommendation. Moore characterized the quarterly performance as “strong,” citing AI-fueled upside momentum and enhanced long-term revenue visibility.

He observed that margin worries have diminished, networking segments exceeded expectations, and the fiscal 2027 AI opportunity remains attractive as custom accelerator programs continue expanding.

For the current quarter, Broadcom projected approximately $22 billion in revenue, suggesting 47% year-over-year expansion. AI segment revenue for the second quarter is anticipated to reach $14.8 billion — reflecting 76% annual growth.

Management has communicated to the analyst community that its five primary custom AI chip clients are advancing according to plan, and that the company can generate over $100 billion in AI chip revenue during fiscal 2027 alone. Morgan Stanley’s team places that estimate even higher at approximately $120 billion, with potential for further upward adjustments.

AVGO shares currently trade at approximately 32 times fiscal 2026 earnings projections and roughly 22.5 times the fiscal 2027 consensus estimate.

Latest Acquisitions Drive Overall Holdings To Greater Heights

The recent purchase comes after a huge one announced last week. Bitmain has already accumulated more than 71,000 ETH, boosting total holdings to more than 4.7 million ETH. It now holds nearly 4 percent of the total Ethereum supply. The company still aims to own five percent of Ethereum’s supply in the market. In addition, the strategy signals a long-term accumulation plan that targets market positioning. The aggressive buying has, however, exposed it to price volatility.

Statistics indicate that Bitmain has a large unrealized loss on its Ethereum investment at present. The average purchase price is above current market rates, which has impacted portfolio value. This puts the firm under pressure as market conditions remain uncertain. Since the beginning of the year, Bitmain’s stock has fallen more than 30 percent. Nonetheless, it posted a small profit in the last week along with a slight uptick in Ethereum’s price. Moreover, this movement suggests a more favorable mood even amid ongoing geopolitical threats.

According to Tom Lee, the company will continue purchasing at current levels despite the unstable markets. He explained that the plan rests on optimism about the broader economic outlook. Therefore, current pricing is seen as an opportunity rather than a risk for the firm. Lee noted that present oil prices are lower than historical highs when adjusted for inflation. He compared current levels with those observed in previous market cycles. He added that this analogy supports the belief that the economy can sustain higher energy prices.

Notably, the leading cryptocurrencies have remained relatively stable even amid geopolitical tension. Both Bitcoin and Ethereum have avoided further losses during the recent conflict period. Consequently, Bitmain is still consolidating its assets in line with the long-term plan.

Bitcoin price now reflects capital inflows over halving cycles. Institutional adoption reshapes Bitcoin’s long-term market behavior. Credit systems and banks now influence Bitcoin growth trajectory. Bitcoin traded near $68,000 as market structure signals a major shift in price drivers. Michael Saylor said the four-year cycle no longer defines market behavior. He added that capital flows now guide Bitcoin’s direction across global financial systems.

For years, traders linked price growth to halving events that reduced mining rewards. Saylor now rejects that model and points to structural market evolution. As a result, Bitcoin’s role continues to expand beyond its early speculative phase.

Institutional adoption continues to reshape demand patterns across regulated financial platforms. Large firms now integrate Bitcoin into treasury strategies and financial products. Consequently, the asset reflects broader economic forces instead of isolated supply shocks.

Capital Flows Replace Halving Cycles

Saylor emphasized that capital movement now determines Bitcoin price trends in modern markets. He linked this shift to increased access through banks and digital credit systems. Liquidity conditions now influence price behavior more than programmed supply changes.

Financial institutions have expanded Bitcoin access through structured investment products. These platforms allow broader participation from corporate and traditional finance sectors. As a result, capital inflows and outflows now drive short-term and long-term price movements.

Analysts now focus on fund allocation trends rather than historical halving timelines. This shift reflects a deeper connection between Bitcoin and global financial systems. Consequently, Bitcoin responds more directly to macroeconomic conditions and liquidity cycles.

Institutional Adoption Redefines Market Structure

Traditional finance has increased its involvement in Bitcoin through custody, trading, and reserve strategies. This participation has improved liquidity while stabilizing extreme price swings over time. Institutional demand now plays a central role in shaping market direction.

Companies continue to build services that integrate Bitcoin into regulated financial ecosystems. These developments expand access and improve trust among large-scale participants. Bitcoin gains recognition as a global digital capital asset across multiple sectors.

The asset now appears in portfolios alongside traditional financial instruments. This integration reflects growing acceptance across banking and corporate environments. Consequently, Bitcoin’s valuation aligns more closely with broader capital market dynamics.

MicroStrategy Strategy Fuels Ongoing Debate

MicroStrategy remains a focal point in discussions about institutional Bitcoin accumulation strategies. The company built a large Bitcoin position through consistent and aggressive purchases. Therefore, it holds a unique position within the evolving digital asset landscape.

Market commentator Adam Livingston noted that early accumulation created a strong competitive advantage. He suggested that replicating such a strategy now requires significantly higher capital. As a result, few firms can match the company’s scale and timing.

At the same time, this approach continues to influence corporate treasury strategies worldwide. Firms now evaluate Bitcoin as a reserve asset within diversified portfolios. Consequently, MicroStrategy’s model remains central to discussions about institutional adoption.

Michael Saylor, Executive Chairman of Strategy (MicroStrategy), hit back at Peter Schiff after the goldbug posted data suggesting Bitcoin (BTC) had lagged gold, silver, and equities over five years.

The exchange reignited a long-running public feud between two of the loudest voices on opposite sides of the Bitcoin-versus-gold divide.

Schiff’s Five-Year Window and Why It Matters

Schiff highlighted Bitcoin’s measly 12% gain over the past five years, comparing that figure to the NASDAQ’s 57.4% gain, the S&P 500’s 59.4% rise, gold’s 163% surge, and silver’s 181% rally.

“If the appeal of Bitcoin is its superior long-term performance, why should anyone keep HODLing it?” posed Schiff.

The five-year window he cited begins near April 2021, when BTC traded close to its then all-time high of approximately $69,000.

That starting point captures both the 2022 crypto crash and the slower 2024-2026 recovery. As of this writing, BTC trades for $66,847.

Gold, meanwhile, has surged above $4,700 per ounce. That represents a gain of over 160% from its April 2021 level near $1,780, confirming Schiff’s figures.

The precious metal hit an all-time high of $5,602 in late January 2026 before pulling back amid broader macro volatility tied to the Iran conflict and rising inflation expectations.

Schiff followed up with a separate post targeting Strategy directly. He noted that MSTR stock had outperformed the NASDAQ, gaining 68.5% over five years, but argued the rally had nothing to do with BTC’s performance.

“It’s due to investors’ willingness to overpay for MSTR so Saylor could keep overpaying for Bitcoin. Sell MSTR before it crashes,” warned Schiff

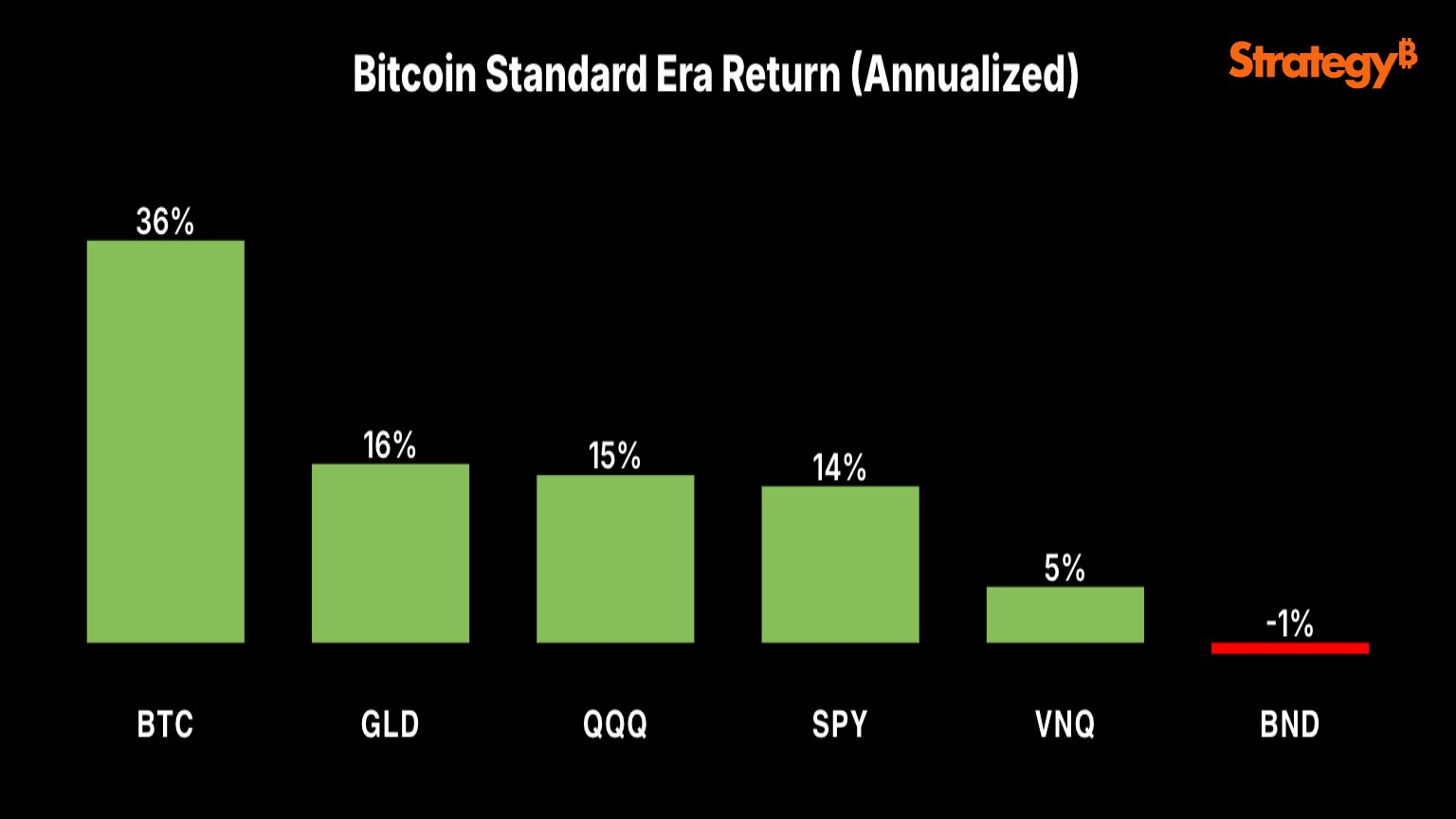

Saylor Responds With Annualized Returns

However, according to Michael Saylor, Schiff’s analogy is flawed. Saylor measured Bitcoin’s performance from August 2020, the month Strategy began its corporate BTC treasury strategy.

With this, the Bitcoin believer highlighted BTC annualizing at 36%, compared to 16% for gold (GLD), 15% for the Nasdaq-100 (QQQ), 14% for the S&P 500 (SPY), 5% for real estate (VNQ), and negative 1% for bonds (BND).

“Timeframes matter. Since Aug 2020, Bitcoin has been the top-performing major asset, and it’s not even close. Zoom out further, and the gap only widens,” Saylor challenged.

Strategy held 762,099 BTC as of this writing, making it the largest corporate holder of the cryptocurrency. The company acquired its holdings at an average price of roughly $75,699 per coin, putting its position below break-even at current spot prices.

A Familiar Feud With Higher Stakes

The Schiff-Saylor rivalry has become a recurring feature of crypto commentary. Schiff has called Strategy’s business model a “fraud” and predicted the company would eventually go bankrupt.

In December 2025, he challenged Saylor to a public debate at Binance Blockchain Week in Dubai. Saylor did not accept.

However, Schiff and CZ, the founder and former CEO of Binance, recently debated on the same topic, Bitcoin versus gold, with the outcome exposing a core divide between gold-backed stability and crypto innovation.

The post Michael Saylor Exposes the Fatal Flaw in Peter Schiff’s Anti-Bitcoin Argument appeared first on BeInCrypto.

Crypto World

Bitcoin Price Prediction: OCC Grants Crypto Bank Charter as Pepeto Targets 100x While ETH and XRP Hold

Bitcoin price prediction shifted this week after the OCC granted conditional approval for the biggest US crypto exchange to become a federally regulated trust bank, pulling digital assets deeper into the traditional banking system.

While the wider market has cooled with major coins pulling back, Pepeto stands out as the top presale entry with its Binance listing getting closer every day.

With a working exchange already live and $8.68 million raised, Pepeto combines real technology with a presale that analysts see running 100x once the listing opens, making it the play that the next rally is about to reward.

The OCC gave Coinbase conditional approval for a national trust bank charter on April 2, placing the largest US crypto exchange under direct federal oversight, according to CoinDesk.

The charter lets Coinbase handle custody services across all 50 states under one set of rules instead of juggling separate state licenses, according to Bitcoin Magazine. Pension funds and sovereign wealth funds often need bank-grade oversight before moving capital into crypto, and this approval knocks down one of the last walls.

The biggest stamp of trust in crypto history just dropped, and the presale entries set to ride that wave are where the real gains live.

Pepeto: The Presale Where 100x Lines Up as the Bitcoin Price Prediction Turns Bullish on Federal Backing

While the CLARITY Act sits stuck in committee, the direction is obvious, and sharp traders are hunting for the best entries to catch the recovery forming underneath.

Pepeto ranks near the top because a live exchange with $8.68 million committed and a Binance listing closing in gives it everything needed to stand as one of the best plays of 2026.

The math speaks for itself. At $0.0000001862, analysts see 100x once the Binance listing opens. The person who created the original Pepe token, which hit $11 billion on hype alone, built this exchange with a veteran from Binance’s listing team. Every swap runs through PepetoSwap at zero cost, every cross-chain move between ETH, BNB, and Solana lands at full value, and every token gets flagged for scam patterns before your capital touches it, all verified clean by SolidProof.

What drives Pepeto daily is real utility, and 188% APY staking grows every position while the listing window gets tighter. The entries that turned early believers into millionaires in past cycles all shared one trait: they found a working project before the crowd showed up, and Pepeto at presale pricing is that exact setup right now.

Ethereum (ETH)

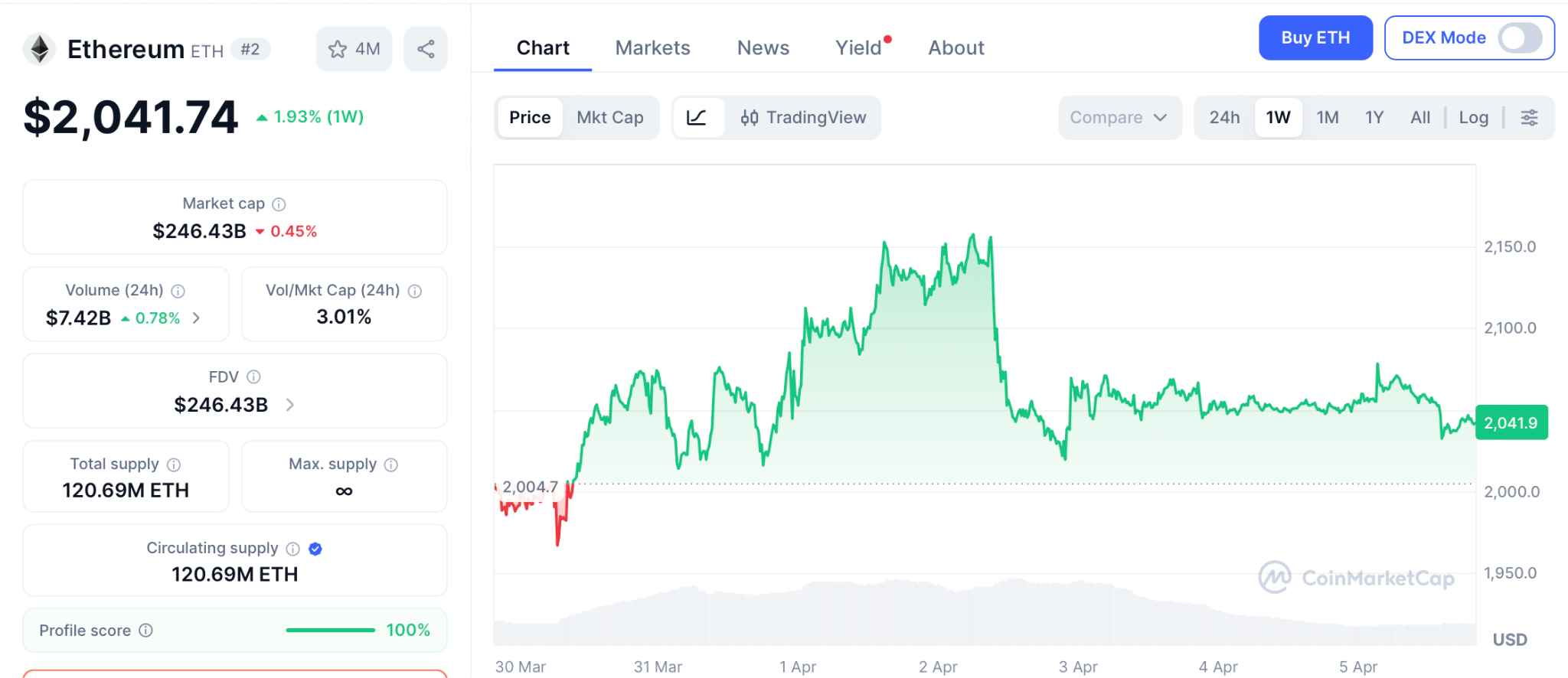

ETH trades at $2,041 per CoinMarketCap, holding just above the $2,000 floor as the broader rally has not yet carried altcoins higher.

Standard Chartered keeps a $7,500 year-end target, but from here that is a 3.6x over nine months, decent for big portfolios, while Pepeto at presale pricing targets 100x from a single listing event the Binance debut is set to kick off.

XRP

XRP trades at $1.29 per CoinMarketCap, drifting below key moving averages as sellers stay in control.

Standard Chartered recently cut its year-end call to $2.80, roughly a 2x that takes patience, but presale entries grab the multiples that XRP at an $81 billion cap can no longer produce.

Conclusion

The picture is forming fast and the math is simple. The OCC handing a federal bank charter to the largest US exchange means the bitcoin price prediction just got backed by the same system that watches over Wall Street. ETH at $2,041 targets $7,500 over nine months, a 3.6x that pays patience, and the investors who grabbed ETH at $0.30 turned $1,000 into $16,000 because they spotted a working platform at early pricing and moved.

The bitcoin price prediction shows early bull signals building while the presale window gets tighter by the day. Visit the Pepeto official website and secure your spot before this chance turns into a headline you read about instead of a gain you earned, because projects with real products, viral buzz, and a Binance listing on deck do not sit at presale prices for long.

Click To Visit Pepeto Website To Enter The Presale

FAQs

What is the Coinbase OCC charter and how does it change the bitcoin price prediction?

The OCC gave Coinbase a federal trust bank charter, pulling crypto under Wall Street-grade rules. The bitcoin price prediction turns structurally bullish.

What are ETH and XRP targets next to the bitcoin price prediction?

ETH targets $7,500 by year end, XRP targets $2.80, and Pepeto targets 100x from the Binance listing. The Pepeto official website still takes entries.

Why is Pepeto the top pick as the bitcoin price prediction shifts bullish?

Pepeto has a live exchange, a SolidProof audit, $8.68 million raised, and 100x projected from the coming Binance listing.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

MicroStrategy, the largest publicly traded corporate holder of Bitcoin, appears set to resume BTC purchases this week. This comes after a brief pause that interrupted one of the longest buying runs in its treasury strategy.

On Sunday, Executive Chairman Michael Saylor resurrected his customary “Orange Dot” tracker on the social media platform X, posting the phrase, “Back to work.”

STRC Rebound Raises Odds of Another MicroStrategy Bitcoin Purchase

Notably, similar phrases have served as a highly reliable leading indicator for multi-million-dollar Bitcoin buy orders over the past several months.

MicroStrategy currently holds 762,099 Bitcoin, valued at more than $50 billion. Another purchase this week would extend that lead and further separate the company from every other listed firm holding the token on its balance sheet.

Meanwhile, the size of any new purchase has not been disclosed.

Still, market watchers following the company’s financing activity say the latest issuance tied to its STRC preferred stock may have restored enough buying capacity. That would be enough to fund the acquisition of at least 1,500 Bitcoin.

That would mark a reversal from the previous week, when STRC traded mostly below par and appeared to curb the company’s ability to raise fresh capital for additional Bitcoin purchases.

Meanwhile, the focus is shifting beyond the next headline purchase to the mechanics supporting it. STRC, one of the instruments used to finance the company’s Bitcoin strategy, pays a variable annualized dividend of 11.5% as of April 2026.

Since launch, STRC alone has financed the purchase of 50,792 Bitcoin. That has made the preferred stock an important part of the company’s broader funding structure as it continues to build what is already the largest corporate Bitcoin treasury in the market.

The strategy, however, continues to divide opinion.

MSTR supporters view the company’s financing model as a high-conviction way to accumulate Bitcoin at scale and tighten its identity as a proxy for the asset in equity markets.

However, critics argue the growing dividend burden tied to its preferred investors leaves the company more exposed if Bitcoin enters a sharp or prolonged downturn.

The post MicroStrategy May Resume Bitcoin Purchases as Saylor Revives ‘Orange Dot’ appeared first on BeInCrypto.

The Solana Foundation has launched a new developer toolkit aimed at bridging artificial intelligence with its blockchain network.

Last week, the Swiss-based non-profit organization introduced “Agent Skills” to allow AI programs to autonomously execute on-chain transactions.

AI Agents Payments Market Still Small

The open-source toolkit allows developers to install pre-built modules with a single line of code. This enables AI agents to handle automated tasks, process payments, and trade assets across the Solana network.

The foundation provided official modules for security and compatibility, alongside more than 60 community-contributed skills from major Solana ecosystem platforms like Jupiter Exchange, Raydium, and Helius.

However, the foundation noted that community-contributed tools are not officially endorsed. Users are warned that integrating autonomous AI agents with unvetted decentralized finance (DeFi) protocols carries inherent security risks, and inclusion in the toolkit does not imply a warranty.

The launch highlights the cryptocurrency industry’s broader push to capture the emerging market of “agentic payments.” These transactions are initiated and completed by AI without human intervention.

Last year, consulting firm McKinsey & Co. pointed out that more businesses will need to adapt to this AI-driven operating environment. According to the firm, this could create a $5 trillion market by 2030, encompassing retail, logistics, and commerce platforms.

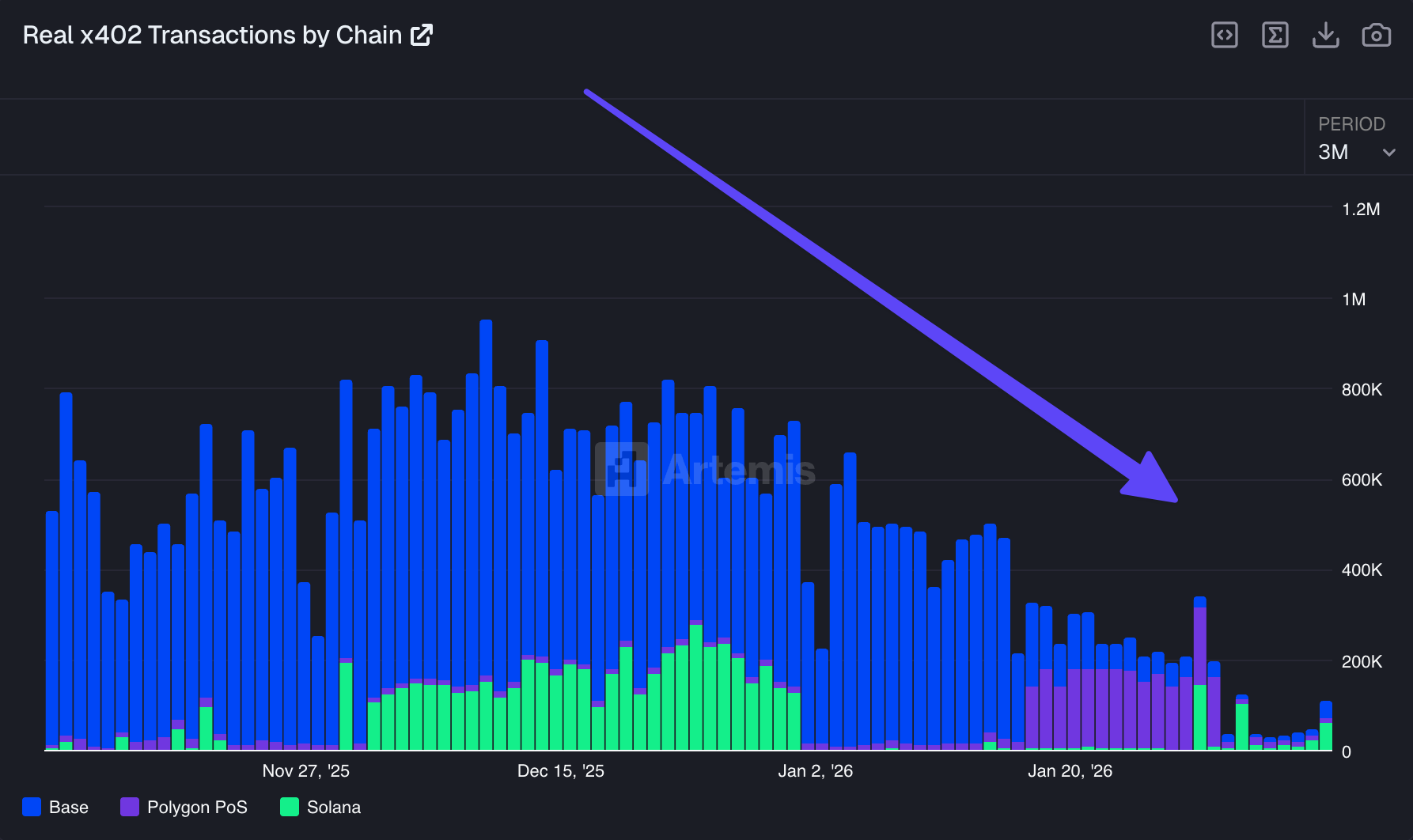

Despite the rapid development of blockchain infrastructure tailored for AI integration, current market demand remains negligible, exposing a significant gap between technological capability and real-world adoption.

For example, x402, an existing agentic payment protocol, processed only about $24 million in volume during the last 30 days.

Furthermore, blockchain analytics firm Artemis pointed out that “x402 ‘agent payments’ boom is still mostly a mirage.” It noted that x402-related activities had collapsed from a peak of over 731,000 transactions per day in December to around 57,000 transactions per day in February.

This data underscores that while networks like Solana are building the rails for an AI-driven economy, the merchants and users required to sustain it have not yet arrived.

The post Solana Targets $5 Trillion AI Market With New Developer Toolkit appeared first on BeInCrypto.

Bitcoin is hovering near the $67,000 level as weekend liquidity thins and traders weigh the risk of renewed downside. A Bollinger Bands squeeze on shorter timeframes points to a potential burst of volatility, but direction remains uncertain as sellers re-enter into a quiet end of the week.

In a market snapshot on Sunday, a prominent market observer highlighted how the current cycle differs from past Bitcoin bear markets. Pseudonymous trader LP_NXT noted that bottoms in earlier cycles typically formed after several sweeps of the downside, triggering capitulation before a revival. This time, the pattern has tended to sweep the highs, leaving the lows exposed and liquidity building below price action, complicating entries for bears and bulls alike.

“In contrast, this cycle has been sweeping the highs, making it difficult to enter short positions while leaving the lows exposed and building liquidity below.”

Meanwhile, traders are watching for a potential breakdown below key thresholds. LP_NXT suggested that a sweep of sub-$60,000 levels could be a likely signal once selling pressure intensifies, but the eventual breakdown and the way price behaves around consecutive lows will be crucial for identifying a real bottom.

Key takeaways

- Four-hour Bollinger Bands have contracted, signaling a classic volatility squeeze that could precede a sharp move up or down.

- Bottom formation remains uncertain; historical patterns favored repeated low sweeps to trigger capitulation, but this cycle has shown different dynamics by sweeping highs instead.

- Binance order-book data reveals unusual selling activity by a small investor class using a TWAP bot, with a single hour showing about $18 million in sell pressure—far above their typical daily volume.

- Market participants describe a dichotomy in whale behavior: “buying dips and selling rips” even as BTC remains range-bound, amid macro headwinds from stronger dollar pressures.

- Past coverage flagged added risk to bulls from a recovering U.S. dollar; investors should monitor whether price action can sustain above or below critical thresholds as liquidity shifts.

Technical setup: volatility compression and looming decisions

Price action around Sunday kept Bitcoin mired in a relatively tight band near $67k, with intraday volatility showing signs of re-emerging pressure rather than a firm directional breakout. The Bollinger Bands on the four-hour chart narrowed, a familiar prelude to a burst of activity once buyers or sellers step in decisively. Traders often interpret this as a fork in the road: a break above resistance could rekindle upside momentum, while a breakdown might expose the market to fresh liquidity-driven moves.

Among market observers, this has been a focal point because the prior cycles’ patterns around low-volume weekends can set the stage for the next move. The contrast with recent behavior—where repeated sweeps of local highs have dominated—adds an extra layer of complexity to positioning ahead of any potential move.

Whale dynamics and order-book signals

Beyond the price chart, on-chain and order-book activity has drawn attention. Keith Alan, cofounder of trading analytics firm Material Indicators, highlighted unusual selling density in the Binance BTC/USDT book despite muted price action. A time-weighted average price (TWAP) bot was observed distributing BTC, with the smallest order class executing a roughly $18 million sell program in an hour—significantly larger and more rapid than the class’s typical $3 million to $5 million daily volume.

“That’s exponentially more than their normal $3M-$5M daily volume in 1 hr. That ain’t retail!”

A broader portrait emerges of a market where whales are not uniformly aligned with a single directional narrative. Alan summarized the dynamic as “buying dips and selling rips” within a price range that continues to confound shorter-term traders. This pattern aligns with a market waiting for clearer macro cues and a more definitive breakout or breakdown signal.

Earlier reporting noted additional bulls’ headwinds from a recovering U.S. dollar, which can dampen enthusiasm for risk assets like Bitcoin when fiat strength escalates. The current activity in the order book underscores how much of the near-term price action may be driven by large players rather than retail flow, particularly as weekend liquidity dries up and position risks accumulate.

Macro backdrop and what it could mean next

The interplay between Bitcoin’s price trajectory and dollar strength remains a critical backdrop for traders. If the dollar cools or if liquidity shifts back into risk assets, BTC could attempt a sustained push higher. Conversely, renewed dollar strength or renewed selling pressure from large token holders could push the market toward test levels below the February low near $60,000. As with many chart-based narratives, the outcome will likely hinge on whether price can sustain a breakout beyond key resistance and whether further high-low sweeps occur, testing traders’ willingness to commit to new positions.

With Bitcoin hovering near critical junctures, investors are watching for concrete signals: a decisive break above the recent range, a compassionate test of sub-$60,000 lows, or a different pattern of liquidity formation that could indicate a new phase in the market cycle. The next couple of sessions should offer clearer directional clues as macro catalysts and order-book dynamics converge.

Cointelegraph’s prior coverage of dollar strength and its implications for crypto markets remains a useful context for readers assessing risk and potential routes for Bitcoin in the near term.

As the market enters a decision point, traders should monitor both price action and the evolving composition of order-book activity to gauge whether a bottom is forming or if a fresh leg down could materialize.

What remains uncertain is how quickly order-flow dynamics will normalize once weekends end and institutions re-enter the scene. Investors should stay alert to any break of sub-$60k liquidity traps or indicators that reinforce a shift in the prevailing liquidity regime.

Crypto markets faced a mix of structural, market, and policy-related developments on the day.

Summary

- Michael Ippolito said rising token supply diluted returns as average coin values lagged market cap.

- Michael Saylor said Bitcoin price now follows capital flows, not the old four-year halving cycle.

- Polymarket removed a market on a missing US service member after backlash over integrity standards.

New comments from industry figures focused on token oversupply, Bitcoin’s changing market cycle, and a backlash that led Polymarket to remove a sensitive prediction market.

Michael Ippolito, co-founder of Blockworks, said the crypto sector faces an “existential” problem as token supply grows faster than value creation. In posts on X, he said total crypto market capitalization has stayed relatively firm, but the average value per token has remained weak.

He wrote that “the average coin is only slightly higher than where it was in 2020” and also down about 50% since 2021. He added that median token returns have fallen sharply, with many tokens down about 80% from their peak levels.

Ippolito said this pattern shows gains have stayed concentrated in a small group of large-cap assets. At the same time, much of the wider market has failed to keep pace. His comments pointed to a growing gap between the number of new tokens and the value generated across the sector.

He also said, “We created a TON of new assets and STILL total market cap is flat.” That view framed token issuance as a dilution problem, where capital spreads across more assets without lifting average returns.

Saylor says capital flows now drive Bitcoin

Michael Saylor said Bitcoin no longer follows the traditional four-year cycle linked to halving events. He stated that the old cycle is “dead” and said price action now depends more on capital flows, credit conditions, and institutional demand.

For years, many traders used halvings as a core part of Bitcoin market analysis. Those events reduced miner rewards and often shaped expectations for future rallies. Saylor now argues that Bitcoin has entered a different stage.

He wrote that “price is now driven by capital flows” and said bank credit and digital credit will play a larger role in Bitcoin’s future path. His comments shifted attention away from supply shocks alone and toward access through funds, banks, and large firms.

That position came as more traditional financial platforms continued to expand Bitcoin-related services. The change has led some market participants to track treasury strategies, regulated products, and large-scale adoption more closely than past cycle models.

Polymarket removes market after criticism

Polymarket removed a market tied to the fate of a missing US service member after public criticism. The listing asked whether US authorities would confirm the rescue of a pilot reportedly shot down over Iran, and it drew sharp backlash online.

US Representative Seth Moulton criticized the market and called it “disgusting.” He said people were betting on the fate of a service member who could be injured, missing, or in danger.

Polymarket said the listing violated its “integrity standards” and removed it. The platform also said the market should not have gone live and that it is reviewing how it passed internal checks.

The company did not give more detail on the exact rule involved. Still, the removal added to the wider debate over what types of real-world events prediction markets should allow, especially when the subject involves war, injury, or loss of life.

Crypto World

ASST Stock Price Forecast: Analyst Projects 53x Surge to $515 by 2034 Using Bitcoin Power Law

TLDR:

- ASST stock price is projected to rise from $9.75 today to $515 by 2034, marking a 53x potential gain.

- Strive’s Bitcoin holdings may grow from 13,628 BTC to 83,299 BTC by 2034 through continuous SATA issuance.

- CEBE per share is forecast to grow 3.2x from 13,193 to 42,028 sats, even after 91% total share dilution.

- Strive currently trades at 73% of NAV with only $10M in debt, offering discounted Bitcoin-amplified exposure.

ASST stock price has drawn growing attention from crypto-focused investors. A financial analyst recently published a detailed multi-year projection for Strive Asset Management’s shares.

The model suggests the stock could climb from $9.75 today to $515 by 2034. The forecast relies on Bitcoin’s historical power law trajectory and a balance sheet leverage model. The analysis has gained traction among those tracking Bitcoin-linked equity vehicles in public markets.

Bitcoin Power Law Forms the Backbone of ASST Stock Price Forecast

Analyst Adam Livingston published the projection via social media. He applied two analytical tools: the Bitcoin Power Law and the CEBE Framework. Bitcoin’s 15-year price trend follows the expression P(t) ~ t⁵·⁶⁹, carrying an R² of 0.961.

The model assumes Strive maintains a 48% amplification ratio throughout the forecast period. This ratio is sustained through continuous SATA preferred share issuance. All proceeds from those issuances are directed toward Bitcoin purchases.

Throughout the model, the enterprise value mNAV remains constant at 1.06×. That figure reflects Strive’s current market valuation. Bitcoin’s price path follows the power law curve across all projected years.

According to the model, Strive’s Bitcoin holdings grow from 13,628 BTC today to 83,299 BTC by 2034. That marks a 6.1× increase in holdings over eight years. The growth stems entirely from maintaining the current amplification strategy.

CEBE Framework Tracks Common Equity Gains Despite Share Dilution

The CEBE framework measures what common shareholders actually own on the balance sheet. It strips out all senior claims before arriving at common equity value. This approach offers a more precise view of shareholder exposure to Bitcoin.

Livingston stated in his post: “CEBE per share grows from 13,193 to 42,028 sats… a 3.2× increase in what common equity actually owns, AFTER subtracting all senior claims, DESPITE 91% total share dilution over 8 years.”

Preferred dividends are set at 12.75% and are paid through common share issuance. This creates roughly 8.4% annual dilution for existing shareholders. Yet Bitcoin’s projected appreciation rate near 35% per year more than offsets that drag.

The spread between Bitcoin’s power law CAGR and the preferred cost sits at approximately 22 percentage points. That gap consistently favors common shareholders over the projection horizon. As Bitcoin’s price rises, dollar-denominated preferred claims become less burdensome in Bitcoin terms.

Strive currently trades at 73% of its net asset value. Its outstanding debt stands at just $10 million, reflecting a 1.1% leverage ratio.

Livingston observed that the market currently assigns no premium to the Bitcoin accumulation engine. He described ASST stock price as a discounted entry point into amplified Bitcoin exposure, with limited debt risk attached.

Crypto World

Ripple (XRP) Aims to Revolutionise Finance, Yet Analysts Say Taurox (TAUX) Might Make it Sooner After Opening Pre-KYA

Ripple trades near $1.32 right now. On April , the International Monetary Fund released a major new note on “Tokenized Finance,” calling tokenization a fundamental shift in how global finance works, not just a small tech upgrade. The IMF highlighted faster settlement, better transparency, and huge potential for real-world assets and cross-border payments. This directly aligns with what Ripple and XRP were built for.

Taurox, an AI-driven trading protocol, is designed to help regular stakers benefit from these big-picture shifts through smart autonomous agents that focus on steady, risk-managed returns.

Even with the IMF validating the exact type of tokenized future Ripple has been pushing, XRP holders often see sharp 20-30% swings due to escrow releases, market sentiment, and short-term noise. It can feel frustrating when the long-term story is strong but the price doesn’t always reflect it. Taurox was created to solve that. It pools deposits of USDT, BTC, or XRP into one shared trading pool and lets a global team of developers, quants, and AI engineers run multiple diversified strategies at once.

Each strategy is strictly limited to 2% of the total pool to keep risk controlled, and smart built-in rules automatically maintain balance. The result is smoother performance, without the constant stress of trying to time every headline or paying high management fees like traditional funds charge.

Taurox has opened the Pre-KYA Registration Table ahead of schedule. This early window lets developers, quants, and AI builders submit their trading agents before the full system launches. The first ones in get priority testing in the Proving Ground, faster access to pool capital, and extra rewards from the Agent Creator Fund (10% of total TAUX supply). If you already have a working trading strategy, this is your opportunity to position yourself early in the Taurox ecosystem.

When you stake, your funds go into one shared trading pool and you receive txTokens that represent your share of the pool’s value, starting at $1.00 each. The protocol keeps 15% in stablecoins as a safety buffer and puts the rest to work through autonomous agents.

These agents only run real strategies after passing strict tests in the Proving Ground. Daily loss limits of 2%, single-trade caps of 5%, and an automatic pause if the pool drops 5% all help protect your capital. Everything is on-chain and fully transparent.

TAUX has a hard-capped supply of 2 billion tokens that can never be increased after launch. Taurox charges zero upfront fees, it only takes 5% of the profits the agents make, buys TAUX on the open market, and permanently burns 30% of it. The rest is shared between stakers, the DAO, and the strategy creators. This design creates real scarcity: the bigger and more successful the pool becomes, the more valuable TAUX can get over time.

The Taurox Presale has entered Phase 4 and has already raised over $950K. TAUX is currently priced at $0.018. Investors joining in this phase are positioned for nearly 4.5x returns when the token lists at $0.08. If Taurox reaches its $1 billion pool target, these early participants could see up to 103x gains as TAUX potentially climbs to $1.85. For example, a $500 investment today would grow to roughly $2,220 at listing and approach $28,000 if TAUX hits the $1 level.

The presale includes a 1-month cliff and 20% monthly unlocks from month 2 to 5, so you can start staking quickly while limiting early selling. Combined with 30% burns and strong reserves, it offers real potential for both short-term and long-term upside.

The IMF just put a global spotlight on tokenized finance, exactly the space Ripple has been building toward for years. While the broader market sorts out the short-term noise, Taurox gives you a practical way to stay exposed without the usual volatility and guesswork. It combines intelligent AI agents with clear risk controls and a token that actually becomes scarcer as the protocol grows. If you believe in Ripple’s long-term role in the tokenized future, Taurox is built for exactly this moment.

Buy TAUX: https://taurox.io

Whitepaper: https://docs.taurox.io/

Official Telegram: https://t.me/tauroxlabs

Official X/Twitter: https://x.com/TauroxProtocol

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

Lola Vice wins NXT Women’s Championship at Stand & Deliver

With One Million Displaced, Lebanon Turns to Digital Wallets for Aid

FA Cup semi-final draw in full: Chelsea and Man City set up huge tests

-

NewsBeat3 days ago

NewsBeat3 days agoSteven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Business3 days ago

Business3 days agoNo Jackpot Winner and $194 Million Prize Rolls Over

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Spanx – Corporette.com

-

Entertainment6 days ago

Fans slam 'heartbreaking' Barbie Dream Fest convention debacle with 'cardboard cutout' experience

-

Crypto World4 days ago

Crypto World4 days agoGold Price Prediction: Worst Month in 17 Years fo Save Haven Rock

-

Tech7 days ago

Tech7 days agoThe Pixel 10a doesn’t have a camera bump, and it’s great

-

Crypto World5 days ago

Dems press CFTC, ethics board on prediction-market insider trades

-

Tech7 days ago

Tech7 days agoAvatar Legends: The Fighting Game comes out in July and it looks pretty slick

-

Sports22 hours ago

Sports22 hours agoIndia men’s 4x400m and mixed 4x100m relay teams register big progress | Other Sports News

-

Business4 days ago

Business4 days agoLogin and Checkout Issues Spark Merchant Frustration

-

Tech6 days ago

Tech6 days agoApple will hide your email address from apps and websites, but not cops

-

Tech5 days ago

Tech5 days agoEE TV is using AI to help you find something to watch

-

Sports5 days ago

Sports5 days agoTallest college basketball player ever, standing at 7-foot-9, entering transfer portal

-

Politics6 days ago

Politics6 days agoShould Trump Be Scared Strait?

-

Tech6 days ago

Tech6 days agoFlipsnack and the shift toward motion-first business content with living visuals

-

Fashion6 days ago

Fashion6 days agoThe Best Spring Trends of 2026

-

Sports6 days ago

Sports6 days agoWomen’s hockey camp eyes fitness boost, tactics ahead of WC 2026 campaign | Other Sports News

-

Tech5 days ago

Tech5 days agoHow to back up your iPhone & iPad to your Mac before something goes wrong

-

Crypto World7 days ago

Bitcoin’s Six-Month Losing Streak: What On-Chain Data Says About the Market’s Next Move

-

Politics6 days ago

Politics6 days agoBBC slammed for ignoring author of The Fraud

You must be logged in to post a comment Login