Crypto World

BTC erases post-election gains during ‘sell at any price’ rout

Bitcoin has recovered from a low near $60,000 to now stand around $69,000, having effectively given back the gains it made after Donald Trump’s election in November 2024 this week.

The cryptocurrency’s drop was accompanied by a broader market sell-off that saw the CoinDesk 20 (CD20) index lose more than 17% of its value in a week.

While bitcoin dropped around 16.5% in the last 7-day period, other cryptocurrencies fared worse. Ether lost 22.4% of its value, BNB dropped 23.4%, and solana 25.2%. Shares of crypto-linked firms registered significant declines despite a Friday rebound, as the price of BTC briefly retook $70,000.

The move followed a violent drop a day earlier that Wintermute described as the worst single-day drawdown in bitcoin since the FTX collapse.

The sell-off was driven by market-wide liquidations and what “felt like a ‘sell at any price’ working order,” said Jasper De Maere, desk strategist and OTC trader at Wintermute in an emailed statement.

De Maere said institutional desks reported “small but manageable liquidation,” which did not fully explain the size of the move, fueling debate over where the stress sat in the system.

De Maere added that the cascade came alongside a wider cross-asset deleveraging. The Nasdaq 100 tracker QQQ fell about 500 basis points over three sessions, while silver and gold dropped roughly 38% and 12% below their cycle highs, respectively.

In crypto options, implied volatility jumped into the 99th percentile, with skew tilting toward unusually expensive puts, he said.

De Maere flagged ether as the “epicenter of the pain,” saying many traders rushed to buy protection against further losses using put options, which can pay out if prices fall and give the holder the right to sell at a set price. In bitcoin, he said positioning pointed to expectations of continued turbulence, with traders focused on a wide range that could run from about $55,000 to $75,000.

Further hitting sentiment, this week crypto exchange Gemini said it plans to shutter operations in the U.K., European Union and Australia, and cut about 25% of staff as part of a restructuring.The firm will enter withdrawal-only mode for users in affected regions and partner with brokerage platform eToro for users to transfer their assets.

Meanwhile, Bitfarms (BITF) saw its shares rise after ditching its “bitcoin company” identity to instead focus on artificial intelligence (AI) infrastructure.

Market structure has added to the turbulence. Bitcoin’s average 1% market depth, a measure of how much can be traded near the current price without moving the market, has fallen to around $5 million from more than $8 million in 2025, Kaiko research analyst Thomas Probst told Reuters. Lower depth can make price moves more abrupt.

Flows in spot bitcoin ETFs have also turned negative. Data from SoSoValue shows about $1.25 billion of net outflows over the past three days. Jim Bianco of Bianco Research estimated on social media that the average ETF cost basis is near $90,000, leaving holders with about $15 billion in unrealized losses.

“It has been said that crypto is ‘programmable money.’ If so, BTC should trade like a software stock,” Bianco said in an X post, adding that the recent decline shows it is trading alongside software stocks.

Software stocks tumbled this week after Anthropic released a new automation tool for its AI models targeting legal and other knowledge-focused workflows. Shares of Salesforce (CRM), Adobe (ADBE), and ServiceNow (NOW) lost 8%, 9%, and 13% respectively over the week, to name a few.

BTIG chief market technician Jonathan Krinsky also said bitcoin has been correlated with software stocks lately. “There’s some pretty compelling evidence both of those [bitcoin and software stocks] have put in tactical lows,” Krinsky said during an interview with CNBC. “[Bitcoin] bottomed last night right around $60,000 so I think that’s a pretty good level to trade against.”

“On the upside you really need to see it back above $73,000, that was the key breakdown level, that would kind of confirm a tradable low is certainly in,” he added.

The Trump administration has maintained a pro-crypto stance, which helped the price of bitcoin hit a new all-time high above $125,000 last year, before a correction kicked in.

Crypto World

Nearly half of all circulating bitcoin is underwater as long-term holders sell at a loss

Nearly half of all bitcoin in circulation is now worth less than it was bought for, according to data from the Bitcoin Impact Index, which jumped sharply last week as stress returned across all segments of the market.

The index, which measures financial stress for bitcoin user cohorts based on onchain behavior, ETF and derivatives activity and liquidity flows, surged 13 points to 57.4 during the week ended March 28, its steepest climb since January, CEX.IO noted in a recent report.

That level, from a range of up to 100, lands it squarely in what’s seen as the “high impact” zone that historically signals the kinds of broad selloffs that led to double-digit price drops in 2018, 2022 and earlier this year.

Long-term holders, wallets that have held BTC for more than six months, were selling at a profit just a week ago, when the cryptocurrency was trading above $70,000. Now, over 4.6 million BTC from these wallets, or roughly 30% of their total holdings, are underwater, the report notes. Their realized losses last week were the worst since 2023.

“This kind of divergence between price action and on-chain conviction has historically been a warning sign,” the firm wrote. “For instance, similar moves occurred in mid-2018 and mid-2022 before price drops by over 25%.”

Short-term holders aren’t faring any better. The report found that 47% of the total bitcoin supply is currently held at a loss, levels not seen since the market’s most stressed stretch in February.

At the same time, capital flows that had supported the market earlier this month have pulled back. Daily stablecoin net flows, which had averaged inflows of $250 million, flipped to outflows of $292 million. ETFs and miners also moved from accumulation to selling, the firm wrote.

So far, one key support remains intact: Onchain data shows holders are not rushing to deposit BTC on exchanges en masse, a behavior often seen in full capitulations.

The US-Israeli war on Iran has rattled energy markets, with many countries taking measures to conserve fuel.

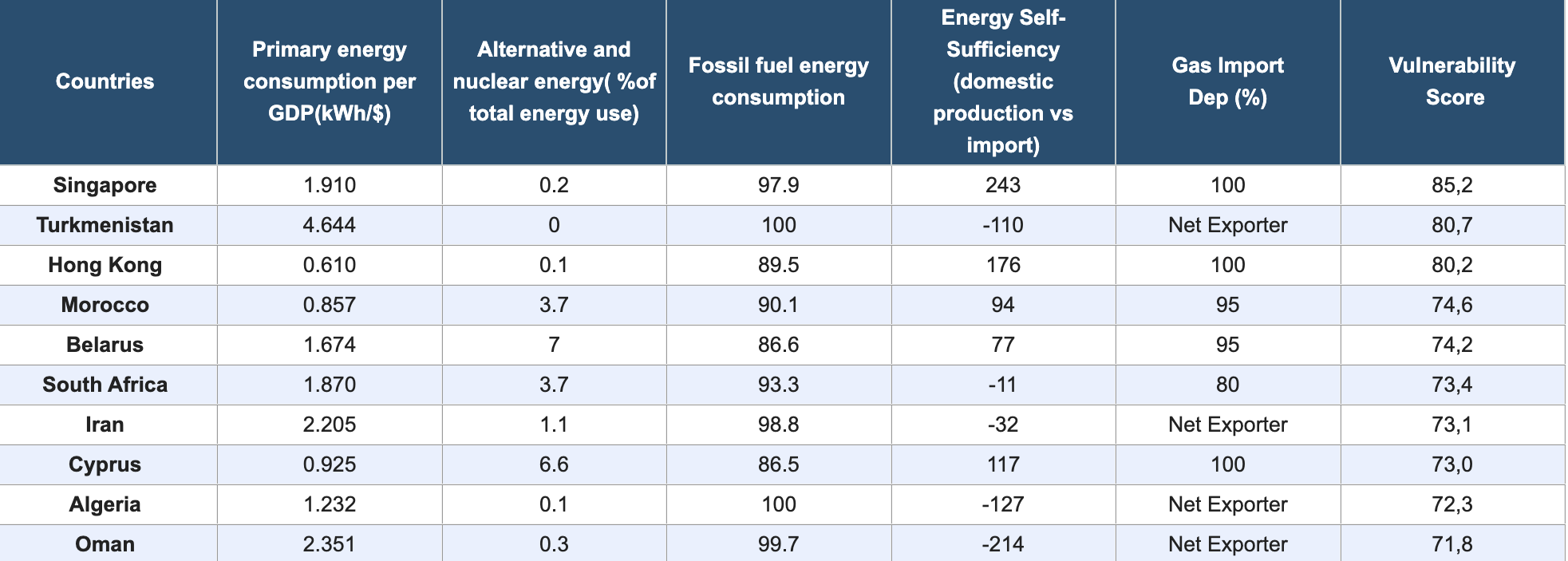

Amid this, a March 2026 study by Energy World Mag examined 75 countries across seven factors to determine which nations would struggle most during global energy disruptions.

The study scored each country on a 0-100 scale, with higher scores indicating greater risk if energy supplies are disrupted. The factors included fossil fuel dependency, energy self-sufficiency, reliance on fuel imports, and more.

Singapore Leads Energy Vulnerability Ranking

Singapore topped the list. The city-state earned the highest vulnerability score of 85.2. Nearly 98% of its energy comes from fossil fuels.

Moreover, Singapore imports 100% of its natural gas. Its energy imports exceed domestic production by 243%.

Turkmenistan placed second with a score of 80.7. The country derives 100% of its power from fossil fuels, with zero alternative capacity. Average incomes of roughly $9,000 also limit the population’s ability to absorb price spikes.

Follow us on X to get the latest news as it happens

Hong Kong followed at 80.2. The city imports 176% more energy than it produces and relies on overseas sources for all of its natural gas.

Morocco (74.6) and Belarus (74.2) round out the top five, both importing the vast majority of their energy. At the same time, low average incomes ($4,000 and $8,000, respectively) leave their populations with limited capacity to handle price shocks.

An energy market analyst from World Energy Mag warned that even wealthy economies like Germany and Italy faced energy rationing during the 2022 crisis. Smaller import-dependent markets like Singapore and Hong Kong have even less capacity to cope with disruptions.

“Germany and Italy had to ration energy despite being among the world’s largest economies. The difference is that places like Singapore or Hong Kong have even less room to maneuver because they produce almost no domestic energy. When supplies get disrupted, they can’t just switch to local coal or increase their own gas production,” the analyst said.

Nonetheless, Singapore’s Minister for Manpower Tan See Leng noted that about half of the country’s gas arrives via piped natural gas, unaffected by the Middle East conflict. The government also maintains a fuel stockpile.

Still, with Brent crude exceeding $116 per barrel and supply disruptions expected to continue, concerns are rising. Whether current emergency reserves can absorb a prolonged disruption remains an open question for policymakers and markets alike.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Which Countries Would Suffer Most in a Global Energy Shutdown? This Study Has Answers appeared first on BeInCrypto.

Crypto World

Will XRP price drop to $1.12 as it remains capped under a descending trendline resistance?

XRP price fell 15% over the past two weeks as its price action remained below a descending trendline that has been acting as key dynamic resistance.

Summary

- XRP price has dropped over 15% in two weeks and remains capped below a long-term descending trendline acting as key resistance.

- Macro pressures, including geopolitical tensions and reduced rate-cut expectations, have weighed on sentiment, contributing to over 40% decline from yearly highs.

- Bearish indicators signal further downside risk toward $1.12 and potentially $1.00, while a breakout above $1.40 could trigger a short-term recovery.

According to data from crypto.news, XRP (XRP) price has fallen 15.6% from its monthly high of $1.60 reached on March 17 to $1.35 at press time. Zooming out the charts, the losses mount up to over 40% from its year-to-date high of $2.39.

XRP price fell amid geopolitical and macroeconomic concerns that have plagued the entire crypto market since the beginning of this year. These include U.S. tariff hikes on the EU and Canada and the subsequent war between the U.S. and Iran in the Middle East that has led crude oil prices to soar to multi-year highs, sparking concerns of rising inflation and driving investors away from risk assets.

Lower expectations of any interest rate cuts from the Federal Reserve have also dampened the mood for speculative assets.

Now, XRP price stands at risk of more downside, especially as the broader crypto market remains under pressure.

On the weekly chart, XRP price has respected a descending trendline that had been acting as a key dynamic resistance since mid July 2025. Every time the bulls managed to push XRP price towards the resistance level, it experienced a sharp drop as bears regained control of the market.

A look at technical indicators also seems to suggest a similar bearish outlook for its price. Notably, the Supertrend has flipped red while the Aroon Down at 42.86% remains far above the Aroon Up at 14.29%. Both indicators point toward a continuation of the current downward trend.

Hence, XRP price may visit the February 2 low of $1.12, a sharp drop below which could extend losses to the $1 mark. On the contrary, if XRP price manages a breakout above $1.40, it could pave the way for a recovery toward $1.50.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Crypto World

Bitcoin price outlook as Bernstein signals potential bottom for crypto stocks this quarter

Bitcoin price has fallen over 30% from its yearly high, largely impacted by geopolitical and economic concerns that deteriorated investor appetite for risk assets.

Summary

- Bitcoin price has dropped over 30% from its yearly high amid geopolitical tensions and persistent macroeconomic pressure weighing on risk assets.

- Bernstein analysts expect market weakness to persist until Q1 earnings, with crypto-linked stocks down sharply but potentially nearing a bottom.

- Bearish technical indicators point to further downside risk toward $60,000, while a move above $69,000 could signal a shift in momentum.

After rallying nearly 12% to a yearly high of $97,538 on Jan. 15, the bellwether crypto has fallen by nearly 31% to $67,525 at the time of writing. This came amid several geopolitical and macroeconomic concerns that have largely risen due to U.S. President Donald Trump’s tariff drama that has extended into the beginning of this year, followed by the start of a war in the Middle East against Iran that has led to repercussions in energy and financial markets across the globe.

The hawkish stance the Federal Reserve has maintained as a result has also not helped the situation.

According to analysts at Bernstein, the resulting volatility has left stocks tied to crypto markets, including exchanges, brokerages, and tokenization platforms such as Coinbase, Robinhood, and Figure, down nearly 60% from their recent highs. This represents a big discount considering that these businesses have continued to expand their operations despite the turbulence.

In their Monday note to clients, they predicted that the current market weakness will extend until the release of first-quarter earnings reports, at which point a market bottom could potentially form. Such a prediction suggests that Bitcoin could likely continue to see more downside at least until April ends.

On the daily chart, Bitcoin (BTC) price has lost the support of a key descending trendline where bulls have often previously found footing.

Technical indicators such as the MACD and RSI show that bears still have the advantage in the current setup. The MACD lines have formed a bearish crossover and were trending downwards while the RSI line was moving within a descending channel, both signs that selling pressure remains dominant.

For now, $65,000 could serve as the key psychological support which bulls would seek to defend. If Bitcoin falls sharply below this key level, bears could aim to drag it all the way down to its yearly low around $60,000 once again.

On the contrary, if BTC price rebounds above $69,000, which aligns with the 23.6% Fibonacci retracement level, it could signal a shift in momentum.

Bullish outlook on crypto-linked stocks despite downturn

While the recent report projected trimmed price targets for crypto-linked stocks, Bernstein analysts maintained “outperform” ratings for Coinbase, Robinhood, and Figure as they attributed the recent weakness to macro pressure and deteriorating market sentiment rather than fundamental business failures.

This means that following the expected weak quarter, they expect these companies to come out stronger in the long term, likely as Bitcoin retraces back to its former highs once all the drama from the ongoing U.S.-Iran war settles down.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

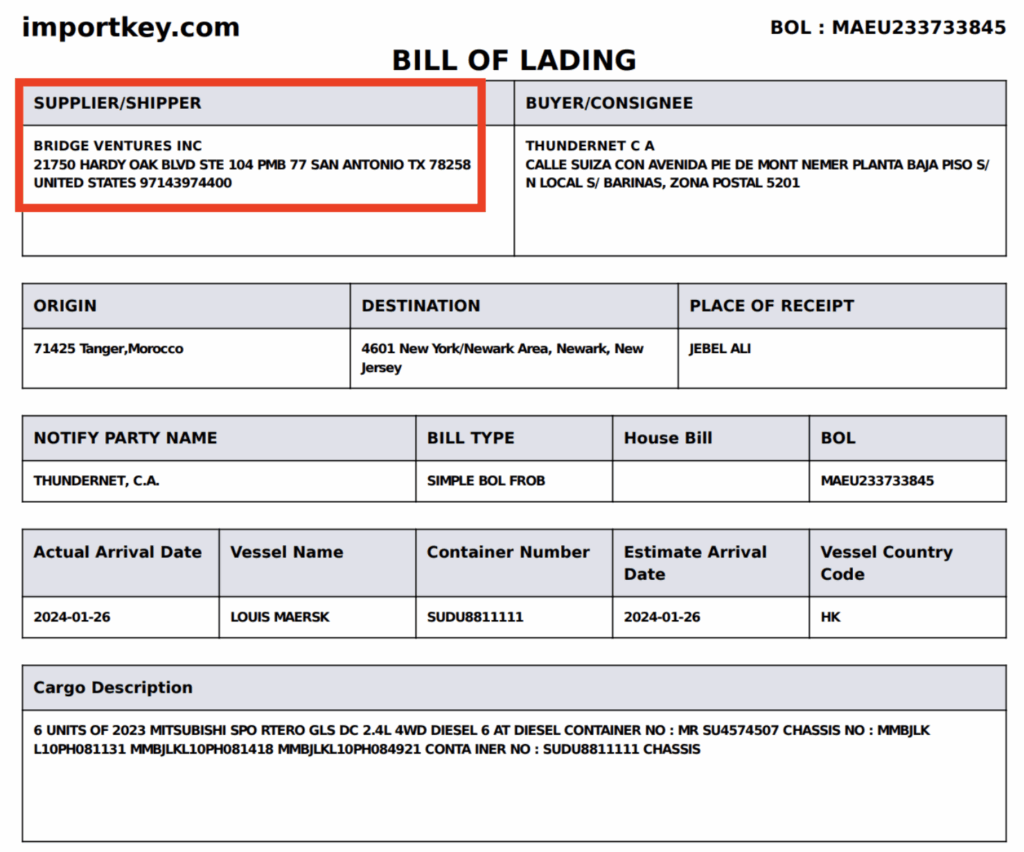

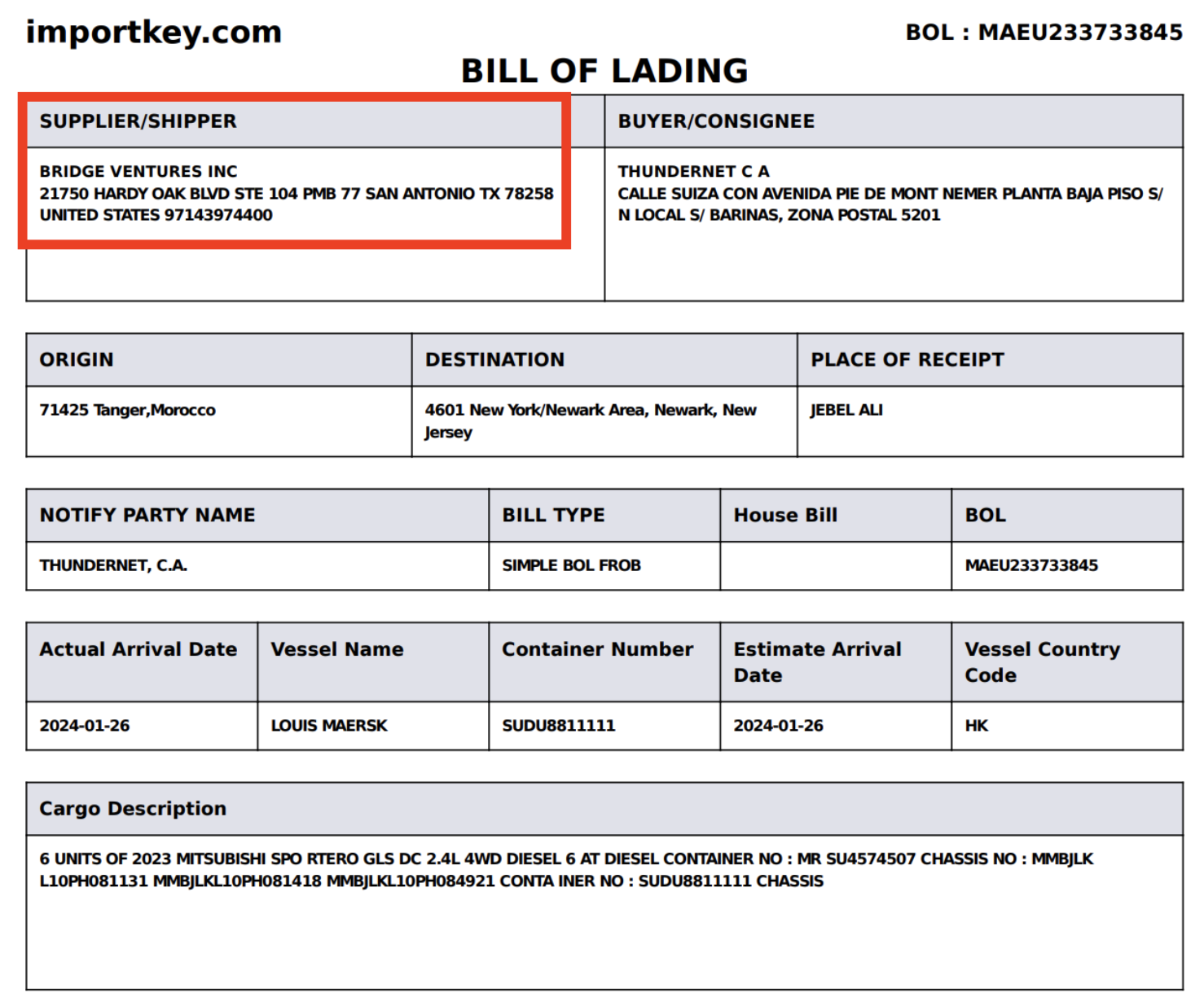

Stripe’s billion-dollar stablecoin subsidiary Bridge Ventures Inc. has apparently been listed on documents as having sold 12 Mitsubishi trucks to a company in Venezuela with ties to the family of former president Hugo Chávez.

The stablecoin company, which Stripe acquired for $1.1 billion, appears, along with its exact street address, suite number, city, state, and zip code, on a shipment slip that sent trucks through a New Jersey port to a company in Venezuela.

At the time of the shipment, Venezuela was under broad US sanctions that covered many companies connected to the Chávez regime’s state-owned oil company PdVSA, and entities acting on its behalf.

Bridge categorically denies any involvement with the shipment. “Whatever this is about, it has nothing to do with us: Bridge had no involvement in this shipment or any associated payment activity,” a spokesperson told reporter Jason Mikula.

“The only explanation we can think of is some clerical error or confusion around a common name like Bridge.”

However, the platform’s character-by-character name isn’t particularly common, while the address on both bills of lading match US Patent and Trademark Office filings and third-party business registries like Bloomberg.

Mikula tweeted and published an article about his skepticism that a third party used Bridge’s name without its authorization.

Thundernet, a Hugo Chávez family connection

The buyer on both truck shipments from “Bridge Ventures Inc.” was Thundernet, C.A., an internet provider based in Barinas, Venezuela.

Thundernet belongs to Grupo Nemer, a conglomerate of dozens of companies across Venezuela, Panama, and the US with close ties to Chávez’s regime.

For example, Hugo Chávez’s youngest brother, Adelis, previously owned the Barinas-based Zamora Futbol Club. The club is now run by Omar Jose Nemer Irched, the eldest son of Grupo Nemer head, Syrian-born Atef Salami Nemer Hirchedd.

That soccer club’s sponsor switched from PdVSA to Thundernet.

In addition, investigative outlet Armando.info reported in 2021 that Nemer Hirchedd maintained a close relationship with another Chávez sibling, Adan Chávez Frías.

Adan served as governor of Barinas and Venezuela’s ambassador to Cuba, a relationship that allegedly helped Grupo Nemer take over operations of a bankrupt state agriculture company.

An exact name match and a denial from Bridge

According to Mikula, the shipping documents compound an already dubious compliance record.

In January 2026, he revealed Stripe’s connection via the Bridge stablecoin platform to Venezuelan crypto exchange Kontigo, rumored to have links to ousted President Nicolas Maduro’s son.

Maduro served as president of Venezuela since 2013, succeeding Chávez.

Moreover, as recently as November 2025, Bridge and Stripe executives were praising Venezuela as a stablecoin showcase.

Bridge subsequently reclassified Venezuela from “controlled” to “prohibited” in its sanctions compliance document.

The timing aligned neatly with the Kontigo fallout and Bridge’s pursuit of a national trust bank charter from the US Office of the Comptroller of the Currency, which conditionally approved its application, after Bridge’s downward revision of Venezuela, in February 2026.

Read more: Venezuela had crypto for buying jet fuel, now its president has lost his plane

The entities on the bills of lading don’t appear on OFAC’s Specially Designated Nationals list. However, Venezuela’s broad program-level sanctions arguably cover persons acting on behalf of the government.

Grupo Nemer’s opaque, multi-jurisdictional corporate structure makes verifying beneficial ownership extraordinarily difficult.

Both shipments originated from Jebel Ali port in Dubai, transited Morocco, and passed through Newark, New Jersey. The same Gmail address appeared for both seller/shipper and buyer/consignee on the documents.

Got a tip? Send us an email securely via Protos Leaks. For more informed news, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

Crypto World

Lido DAO proposes $20 million LDO buyback as token trades at 70% discount to two-year median

Lido DAO proposed spending up to 10,000 stETH to buy its own governance token at what it calls a historically depressed valuation. That works out to roughly $20 million at current ether prices near $2,000.

The problem is where to spend it.

Onchain LDO liquidity sits at about $90,000 of depth at plus-or-minus 2%, according to the proposal posted by the Lido Ecosystem Operations team over the weekend. The market depth measure means a transaction of that value could move the token’s price by as much as 2%.

A single 1,000 stETH batch executed onchain would blow through available liquidity multiple times over, meaning Ethereum’s largest liquid staking protocol has to go offchain to buy its own token at scale.

The proposal authorizes the Lido Growth Committee to route trades through centralized exchanges including Binance, OKX, Bybit, Gate and Bitget, each of which currently offers more than $100,000 in depth. It also permits the committee to engage market-maker partners on behalf of the Lido Ecosystem Foundation to facilitate execution.

Valuing governance

LDO hit an all-time low of $0.27 on March 7 and currently trades near $0.30, according to CoinGecko data, with a market capitalization of roughly $258 million.

The token is down more than 95% from its 2021 peak of $7.30. At current prices, the proposed buyback could use up roughly 65 million tokens, or about 8% of the circulating supply.

The DAO’s case rests on a gap between token performance and protocol fundamentals. The LDO-to-ETH ratio sits at approximately 0.00016, a 70% discount to levels that held for most of the past two years.

Net protocol rewards, in contrast, have dropped only about 20% over the same period, while costs improved 13% year-over-year and the protocol’s effective take rate rose to 6.11% from 5%. Lido still holds the largest share of staked ether at around 23%, per DefiLlama.

“This is not a routine fluctuation,” the proposal states. “It represents one of the most significant dislocations between LDO’s market price and its underlying protocol fundamentals in the token’s history.”

Execution would proceed in 1,000 stETH batches, each requiring a separate Easy Track motion — a governance mechanism for routine or approved operations — with a three-day objection period. The Growth Committee retains discretion over timing and pace to avoid signaling exact moves to the market, a necessary precaution given that the proposal is public. Slippage is capped at 3% below the reference price.

The deeper question the proposal surfaces is one facing DeFi governance tokens broadly. LDO’s 95% drawdown from peak is extreme, but it is not an outlier in the category. A protocol that dominates its sector, generates consistent fees, and holds billions in TVL is trading at a $258 million market cap because the market has broadly repriced what a governance token is worth when it controls a fee switch but distributes nothing.

Lido’s answer is to treat the dislocation as a buying opportunity. Whether that works depends on whether the market ever decides governance tokens deserve to trade on fundamentals at all.

Opinion by: Ashna Vaghela, chief customer officer at Mercuryo, and Vi Powils, CEO at World of Women.

For decades, the financial industry has treated creativity as a high-risk hobby. If you’re a woman building a global brand from a laptop, there is a risk that your bank doesn’t see a CEO. Rather, it sees someone with a non-standard income stream, without collateral, who might have to stop or pause working, to have children. Our global economy champions the middleman while the actual source of value can be treated as an afterthought.

For many women, particularly in emerging markets, creating online is not supplemental income; it is primary income and often the most borderless economic opportunity available to them.

That barrier runs deeper in emerging markets. A creator in Lagos can build a following of millions, only to find that the banking systems turn cross-border payments into a months-long exercise in fees and delays. When you control the flow of capital, you control who gets to stay in business. Women have spent years asking for a seat at the table where the legs were already broken.

The intersection of the creator economy and crypto payment infrastructure offers the first genuine path to financial freedom that doesn’t require anyone’s permission. As we move toward a world where code does the work that banks used to gatekeep, and that shift matters more for women than almost anyone else.

The invisible tax on identity

Legacy finance has failed women and creators in tandem. Venture capital still directs a tiny fraction of its capital to female founders with only 2.3% of venture capital funding having gone to female-founded companies in 2024. Credit scoring still penalizes uneven income, which is the reality for most independent artists. These systems were designed for a 9-to-5 world that is no longer the default way of being.

Layered on top of that is the platform toll. Some take up to 50 percent of earnings before a single cent reaches a creator’s wallet. You’re renting your audience from a landlord who can evict you whenever the terms do not suit them.

Programmable revenue and the end of Net-90

In the old world, a creator sells their work and can wait months to get paid. Smart contracts change this entirely. Revenue splits happen at the point of sale. If an artist collaborates with a developer, the payment doesn’t pool in a corporate account, it moves directly to their respective wallets the moment a transaction clears.

Related: Blockchain restores women’s power in AI

The code becomes the escrow. There’s no chasing invoices, no waiting on platforms to release what you’ve already earned. Hardcoded royalties mean creators benefit from the long-term value of their work regardless of where it’s resold.

While an imperfect system, the structure of onchain royalties is intended to help artists capture value over time, rather than relying solely on single transactions. OpenSea made royalty enforcement optional, which most marketplaces have now followed. This is what we mean by participatory capitalism: a model where the growth of the whole, lifts the people who actually built it. For many artists, especially women building global audiences, this shift is more than technical, it enables consistent revenue without depending on a platform’s schedule or policies.

Infrastructure as the foundation of family

Infrastructure sounds dry until you realise it’s the difference between asking for permission and having power. Community is a multiplier, but infrastructure is the engine. For the millions of women entering the creator economy, crypto rails offer a global passport that doesn’t check for borders or bias.

The community talks a lot about community in Web3, but what is really being described is something closer to family. A community is a group you associate with. A family shows up when things get hard. Stablecoins have become that bridge for creators in regions with volatile currencies, letting them hold the value of their work without needing a bank’s approval.

When you lower friction at both ends of a transaction, the creativity in the middle takes off. There is already seeing a generation of entrepreneurs who don’t need an invitation to the boardroom because they own the system it sits on. Reliable payment rails make the difference between being able to monetize globally and being restricted to local, slow, or costly banking systems, a gap that disproportionately affects women creators in emerging markets.

Moving toward ownership

Inclusion is not a gift. Ownership is holding the deed, not being handed a seat. The shift to Web3 payment infrastructure moves us toward that deed. This moment is about refusing to let legacy systems set the value of creative communities. The infrastructure is ready. The only thing left is for the creators to lead.

Let us stop waiting for the system to change. Let us continue to the payment rails that replace it.

Opinion by: Ashna Vaghela, chief customer officer at Mercuryo, and Vi Powils, CEO of World of Women.

This opinion article presents the author’s expert view, and it may not reflect the views of Cointelegraph.com. This content has undergone editorial review to ensure clarity and relevance. Cointelegraph remains committed to transparent reporting and upholding the highest standards of journalism. Readers are encouraged to conduct their own research before taking any actions related to the company.

Dozens of Kash Patel-themed tokens appeared on memecoin launchpad Pump Fun this weekend, after Iranian hackers leaked his personal email along with a burner username that some believe has been used to comment on pornographic videos.

The Iranian government-linked collective published over 300 emails, personal photos, and a resume from Patel’s Gmail account on Friday.

Among the leaked details was an alias, “spiderkash,” that Patel used with a burner email. Researchers searched for exact matches for that handle across the internet and found a profile on XVideos, a pornography website.

Spiderkash created its porn account on January 5, 2020 to review and leave comments on adult videos.

While it’s not been confirmed that the account actually belongs to Patel, crypto promoters believed they had enough evidence with the exact character match.

No official statement has confirmed or denied the connection, and there’s little reason for Patel to clarify.

Nevertheless, screenshots spread across X within hours, racking up millions of views and the profile soon became restricted.

Read more: Research finds less than 0.002% of Pump.fun memecoins succeed

Dozens of Kash Patel porn memecoins, one outcome

Within hours of Patel’s email leak, dozens of promoters created memecoins bearing the Spiderkash username appeared on Pump Fun.

One token named after Patel’s actual leaked email address, [email protected], peaked within one minute of launch before crashing 87% five minutes later and never recovering.

The largest by market cap spiked to a $104,000 value within hours of launch. However, one hour after its peak, it had collapsed 70%.

Within 12 hours it was 87% off its peak and by Saturday night, peak-to-trough losses exceeded 90%.

A third Spiderkash-inspired memecoin called Mayhem reached $5,500 before falling 85% to just $818 within seconds. it never recovered.

One Pump Fun wallet deployed four Spiderkash tokens in the same hour. Each remained at Pump Fun’s starting market cap and, despite illiquid wicks to high prices, never attracted any meaningful trading.

Dozens were trading 90% below their momentary all-time highs.

Iranian hackers previously targeted Patel in December 2024, before his confirmation as FBI director, claiming that the breach was retaliation for the DOJ seizing several of its websites on March 19.

Got a tip? Send us an email securely via Protos Leaks. For more informed news, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

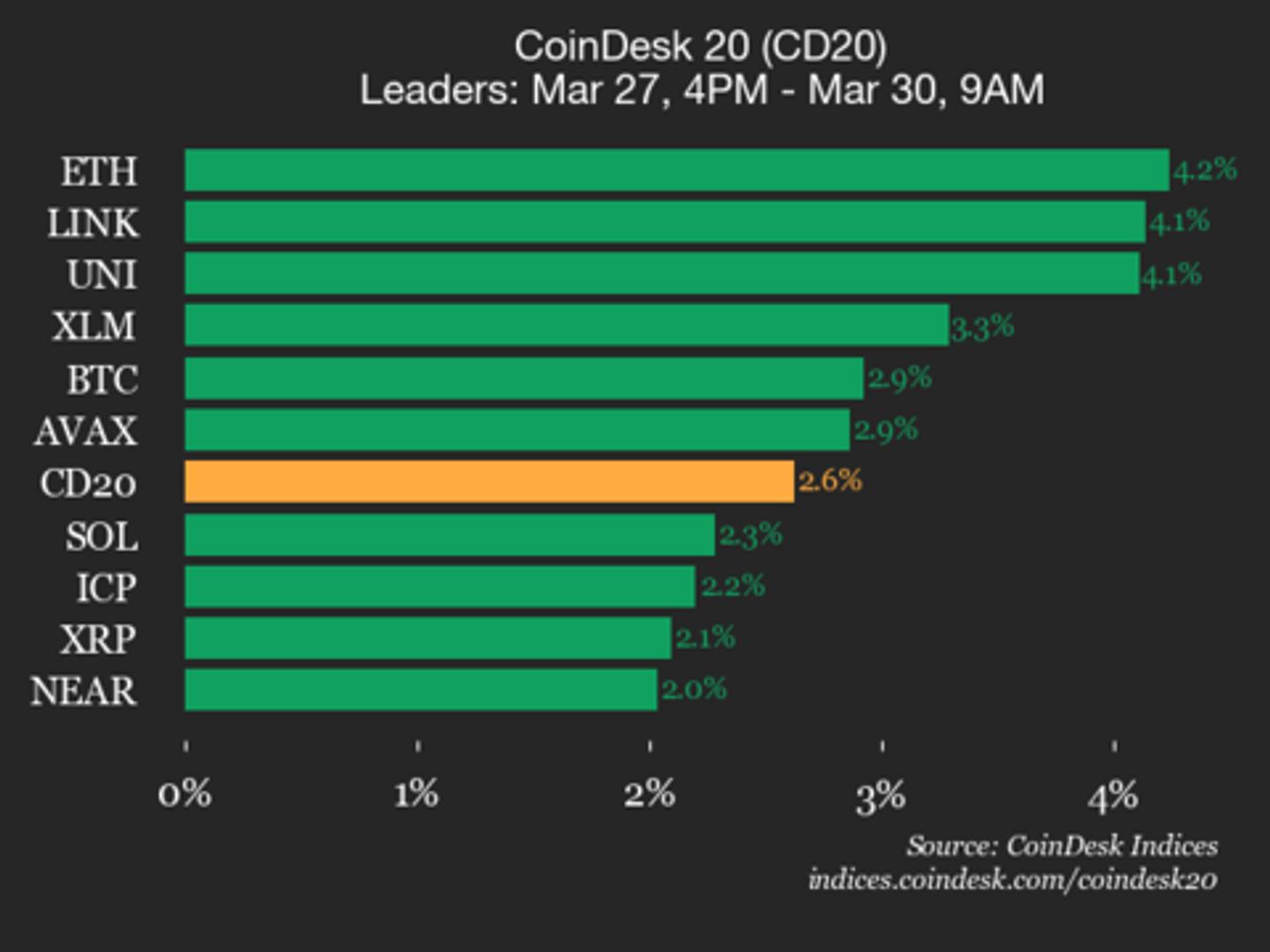

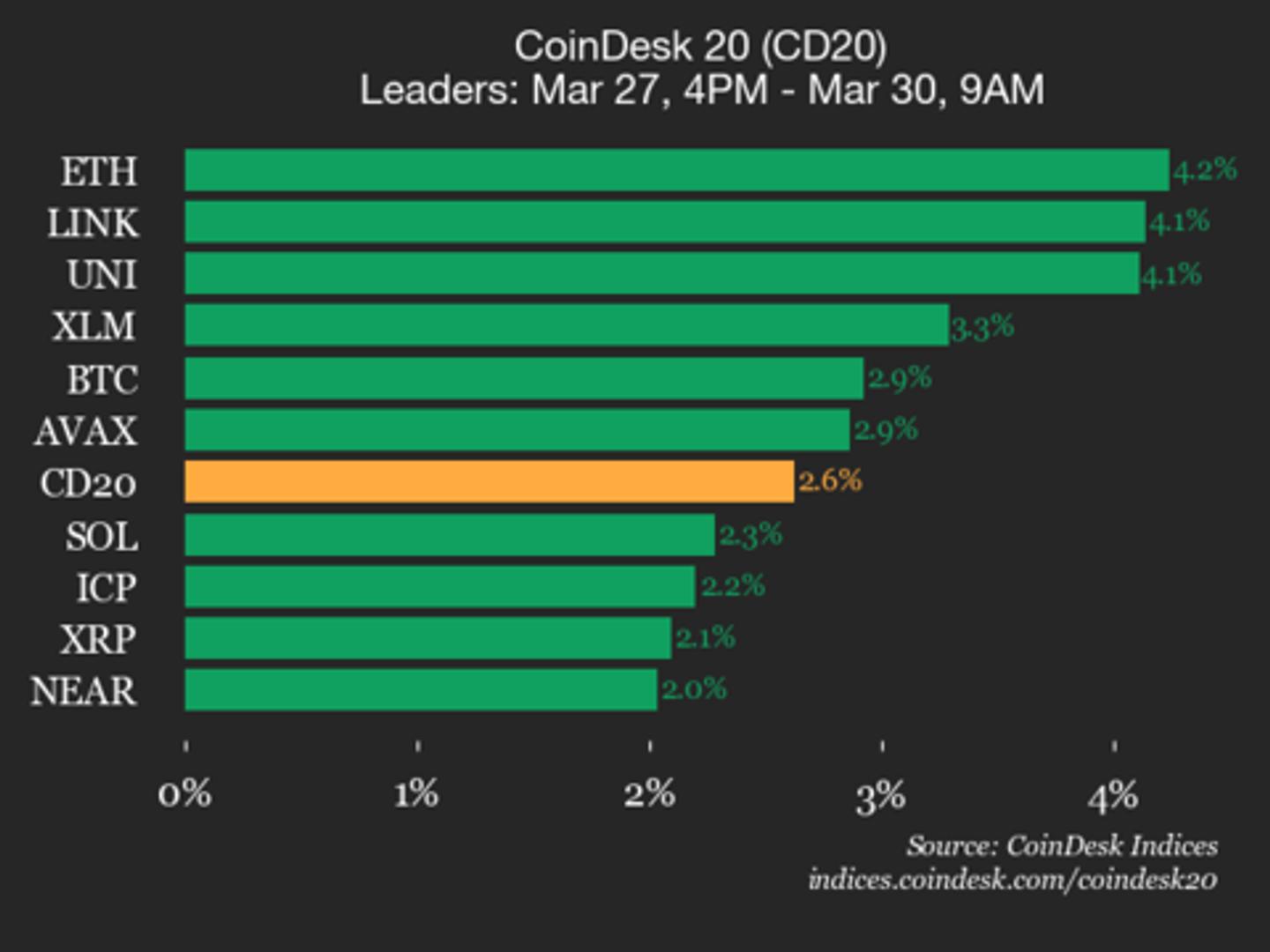

Chainlink (LINK) joined Ethereum (ETH) as a top performer, up 4.1% since Friday.

Aave, one of the largest decentralized lending platforms, debuted its long-awaited v4 upgrade on Ethereum, aiming to push DeFi beyond crypto trading and into broader financial markets.

The upgrade has been in development for about two years and is designed to make it easier to use Aave for a wider range of lending and borrowing activities, including those tied to real-world assets.

The introduction follows months of internal debate over governance and value flow through the protocol. Disputes over interface fees, contributor roles and proposals to redirect product revenue to the decentralized autonomous organization (DAO) have highlighted tensions between decentralization and coordination, even as the work progressed.

At a basic level, v4 changes how Aave organizes its markets. Instead of grouping everything together, the new system allows different types of lending markets to operate separately while still sharing the same pool of funds.

That means users could eventually borrow and lend against more than just crypto tokens.

For Aave Labs founder Stani Kulechov, the shift reflects a broader change in how decentralized finance is evolving. “Lending is based on trust… you need lending conditions that reflect market conditions,” he said in an interview with CoinDesk.

The upgrade is designed to better handle that complexity. By separating different market types while sharing liquidity, Aave aims to support everything from traditional crypto lending to more complex situations like institutional borrowing and real-world assets.

It also opens the door for others to build on top of the protocol more easily.

“It also means that other teams can come and build and expand that infrastructure,” Kulechov said.

Another goal is to make better use of the capital already in the system.

“There’s some technical improvements where the float … can be reinvested,” Kulechov said, referring to idle funds that can now be deployed more efficiently.

The new version went live with a limited set of markets and conservative settings. More features are likely to be added following governance decisions.

“DeFi is stronger than ever,” Kulechov said. “A lot of these opportunities will come from value outside of DeFi.

Read more: Aave labs proposes ‘Aave Will Win’ plan to send 100% of product revenue to DAO

Safire W/ Antonio Bibbs Amid Safaree Mom Death

England: Thomas Tuchel not angry with eight withdrawals for Japan friendly

Goldman Sachs Mid Cap Value Fund Q4 2025 Commentary

-

NewsBeat5 days ago

NewsBeat5 days agoManchester United reach agreement with Casemiro over contract clause amid transfer speculation

-

News Videos5 days ago

News Videos5 days agoParliament publishes latest register of MPs’ financial interests

-

NewsBeat3 days ago

NewsBeat3 days agoThe Story hosts event on Durham’s historic registers

-

Business4 days ago

Business4 days agoInstagram, YouTube Found Responsible for Teen’s Mental Health Struggle in Historic Ruling

-

NewsBeat5 days ago

NewsBeat5 days agoTesco is selling new Cadbury Dairy Milk bar and people can’t wait to try it

-

Tech7 days ago

Tech7 days agoSamsung will soon let you control smart home devices from your car’s dashboard

-

Entertainment2 days ago

Entertainment2 days agoLana Del Rey Celebrates Her Husband’s 51st Birthday In New Post

-

Fashion6 days ago

Fashion6 days agoDoes It Matter What You Wear When You’re Laid Off and Looking?

-

Business6 days ago

Business6 days agoMore women enter wealth management, but few in advisory roles: study

-

NewsBeat7 days ago

NewsBeat7 days agoColombian military plane with 110 soldiers onboard crashes following takeoff

-

Politics7 days ago

Politics7 days agoHow Media Platforms Balance Performance and Accessibility in Image Delivery

-

NewsBeat6 days ago

NewsBeat6 days agoEntrepreneurs Forum survey reveals optimism in North East

-

NewsBeat6 days ago

NewsBeat6 days agoNASA Artemis II Astronauts enter 14-Day quarantine as moon rocket reaches launchpad

-

Business6 days ago

Business6 days agoLate-paying firms face multimillion-pound fines under new crackdown

-

Tech4 days ago

Tech4 days agoIntercom’s new post-trained Fin Apex 1.0 beats GPT-5.4 and Claude Sonnet 4.6 at customer service resolutions

-

Crypto World6 days ago

Crypto World6 days agoBTC gives up $70,000 level as markets mull higher interest rates

-

Sports5 days ago

Sports5 days agoFantasy Baseball Week 1 Preview: Top sleeper hitters for both five- and 12-day period led by Munetaka Murakami

-

Tech5 days ago

Tech5 days agoUS FCC Prohibits Approval Of New Foreign-Made Consumer Routers

-

Fashion6 days ago

Fashion6 days agoCoffee Break: Korean Skincare Set

-

Fashion6 days ago

Fashion6 days agoAlthea Mink: Patrice Taylor’s Atlanta Couture Brand Built on Legacy, Resilience, and Architectural Glamour

You must be logged in to post a comment Login