Crypto World

Charles Schwab, Citadel Both Mull Prediction Market Play

Traditional finance giants Charles Schwab and Citadel Securities are both considering entering prediction markets, with each separately weighing up how they wish to get involved in the fast-growing sector.

“I think at some point we likely will have prediction markets,” Rick Wurster, the CEO of the banking and investing titan Schwab, told investors during a call on Thursday.

He added that prediction markets weren’t “of tremendous interest” when he recently asked a group of Schwab clients about them, but it was an area the company would “take a hard look at, and it would be quite straightforward for us to offer.”

Prediction markets such as the popular Kalshi and Polymarket have exploded in use over the past few months, with both platforms seeing a record combined total monthly trading volume of $23.6 billion in March, according to Token Terminal.

However, Kalshi, Polymarket and other prediction market platforms have also caught the ire of some US state regulators, who have accused them in court of offering unlicensed sports betting.

Some federal lawmakers have also vowed to crack down on prediction markets, claiming the platforms weren’t doing enough to stamp out insider trading.

Wurster said Schwab’s potential offering would steer away from allowing bets on areas such as sports, politics and pop culture as it looks to position itself as a partner for building long-term wealth.

“Prediction markets that are not aligned to that are not something that we want to pursue,” he said. “If you look at the stats on the success of gamblers, they’re not strong, and people generally lose money.”

Citadel “keeping an eye” on prediction markets

Meanwhile, Citadel Securities president Jim Esposito said at a Semafor conference in Washington, DC, on Thursday that the company is “absolutely keeping an eye on developments” in prediction markets.

“We’re not there yet, there’s not that much liquidity,” he added, but said that the market is likely to “ramp and scale,” and it was “certainly possible” that the market-making firm would potentially look to get involved.

Related: Democrats question CFTC chair on insider trading in prediction markets

Esposito said Citadel was “not looking at sports at the moment at all, I don’t see us entering that market,” but did signal an interest in some event contracts.

He added that Citadel could see its retail and institutional clients use some event contracts as a hedge for risks to their investments, such as contracts for elections, which have been known to move markets.

“That’s going to be some of the biggest risks to investors’ portfolios that they’re going to have to grapple with,” Esposito said. “Having a clean and distinct way to hedge certain risks, I think there’s a good use case and industrial logic to it.”

Magazine: Should users be allowed to bet on war and death in prediction markets?

Key Takeaways

- A Saturday attack on Kelp DAO’s LayerZero bridge resulted in the theft of 116,500 rsETH tokens valued at approximately $292 million

- The exploit manipulated LayerZero’s cross-chain messaging system to authorize fraudulent fund withdrawals

- Approximately $250 million in stolen assets were swapped for ETH using an address funded through Tornado Cash

- Nine or more DeFi protocols implemented emergency rsETH market freezes, including major platforms Aave, SparkLend, and Fluid

- The incident represents 2026’s most significant DeFi security breach, exceeding April’s Drift Protocol compromise

On Saturday at 17:35 UTC, malicious actors successfully extracted 116,500 rsETH tokens from Kelp DAO’s LayerZero-integrated bridge infrastructure, absconding with cryptocurrency assets valued at approximately $292 million.

The compromised volume accounts for roughly 18% of rsETH’s entire circulating token supply, which totals 630,000 units based on CoinGecko analytics.

Kelp DAO operates as a liquid restaking platform that accepts ETH deposits, channels them through EigenLayer for enhanced yield generation, and distributes rsETH as transferable receipt tokens to depositors.

The perpetrators exploited vulnerabilities in LayerZero’s cross-chain communication infrastructure, deceiving the system into processing what appeared to be legitimate cross-network instructions. This manipulation prompted Kelp’s bridge contract to transfer substantial funds to wallets under attacker control.

Kelp’s emergency response team activated protocol pause mechanisms across core smart contracts at 18:21 UTC, exactly 46 minutes following the initial breach. Two subsequent withdrawal attempts targeting an additional 40,000 rsETH — approximately $100 million in value — were successfully prevented.

Blockchain forensics from security firm Cyvers revealed that stolen assets were routed through addresses previously funded via Tornado Cash. Roughly $250 million of the compromised rsETH had already undergone conversion to ETH at the time of analysis.

Widespread Impact Across DeFi Ecosystem

The compromised bridge contract served as the collateral reserve supporting wrapped rsETH deployments across over 20 blockchain networks, including Base, Arbitrum, Linea, Blast, and Scroll.

With reserve backing eliminated, rsETH holders on layer 2 platforms now confront significant questions regarding token collateralization and redemption capabilities.

Aave implemented immediate rsETH market suspensions across both V3 and V4 platforms within hours of breach detection. [[LINK_START_0]]Aave’s token[[LINK_END_0]] experienced approximately 10% depreciation as traders factored in potential bad debt exposure risks.

SparkLend and Fluid similarly enacted rsETH market freezes. Lido Finance suspended deposits to its earnETH product due to rsETH holdings while emphasizing that its primary staking infrastructure remained unaffected.

Ethena implemented precautionary LayerZero OFT bridge suspensions from Ethereum mainnet for approximately six hours, though the protocol confirmed zero rsETH exposure.

Kelp’s initial public statement arrived at 20:10 UTC — nearly three hours post-attack. The protocol confirmed active collaboration with LayerZero, Unichain, audit partners, and external security consultants.

2026’s Challenging DeFi Security Landscape

Cyvers CEO Deddy Lavid characterized the breach as demonstrating inherent vulnerabilities within DeFi’s interconnected composability architecture.

The Drift Protocol, operating on Solana, sustained approximately $285 million in losses on April 1 through an attack attributed to North Korean threat actors.

Additional protocols including CoW Swap, Zerion, Rhea Finance, and Silo Finance have experienced security compromises throughout recent weeks.

According to Cyvers data, combined cryptocurrency losses from exploits and fraudulent schemes reached approximately $482 million during Q1 2026.

The Kelp DAO incident now holds the position as 2026’s most substantial DeFi security breach, marginally exceeding the Drift Protocol compromise.

As of publication, Kelp has not provided technical details explaining how attackers circumvented the bridge’s validation architecture.

Traditional finance giants are signaling a renewed interest in prediction markets, a sector that has surged in public attention as retail and institutional players explore hedging tools tied to real-world events. Charles Schwab and Citadel Securities each indicated they are weighing how to participate, signaling a potential shift from curiosity to concrete product ideas in the near term.

During an investor call, Schwab CEO Rick Wurster said the firm “likely will have prediction markets” at some point, though they are not currently of primary interest among Schwab clients. He added that if the firm does pursue such offerings, it would be “quite straightforward” to roll them out as part of a broader wealth-building platform. Wurster also stressed one caveat: Schwab’s approach would intentionally sidestep markets tied to sports, politics or pop culture, aiming instead to align with long-term financial planning for clients. He noted that, in his view, the typical gambler’s edge in prediction markets is not favorable over time, and Schwab would pursue a model focused on prudent investing rather than speculative betting.

Meanwhile, Citadel Securities is watching developments in prediction markets with cautious interest. Citadel Securities president Jim Esposito said at a Semafor conference in Washington, DC, that the firm is “absolutely keeping an eye on developments” but emphasized that liquidity remains a constraint. “We’re not there yet, there’s not that much liquidity,” he noted, though he acknowledged the market is likely to scale in the future and suggested a potential path for involvement if conditions evolve.

Key takeaways

- Major incumbents are considering entry: Schwab publicly signals a future prediction market offering, focusing on wealth-building rather than sports or politics.

- Liquidity and maturity are gating factors for market makers: Citadel notes low current liquidity but envisions a ramp in participation as volumes grow.

- Event contracts as hedging tools: Both parties see potential use cases for event-driven products (e.g., elections) as hedges against portfolio risks, distinguishing them from pure betting markets.

- Regulatory backdrop remains unsettled: Courts have scrutinized platforms like Kalshi and Polymarket for unlicensed activity, while lawmakers debate how to address insider trading and consumer protections.

- Market growth persists alongside conflicts: Data from market trackers show brisk growth in prediction-market activity, even as regulators push back on certain offerings.

Growth, scrutiny and the evolving landscape of prediction markets

Prediction markets have surged in visibility over the past year, driven by platforms such as Kalshi and Polymarket that allow users to trade contracts tied to real-world events. These markets have captured broad interest from traders seeking hedges or alternative risk exposures outside traditional financial instruments. In resounding numbers, Token Terminal reported that Kalshi, Polymarket and similar platforms together posted a record combined monthly trading volume of 23.6 billion dollars in March, highlighting a trajectory of rapid adoption and liquidity growth for event-driven markets.

Yet the expansion of these markets has not come without friction. Regulators in several U.S. states have pursued actions against prediction-platform operators, accusing them of offering unlicensed forms of betting disguised as markets for predictions. The intensity of scrutiny is underscored by ongoing litigation and regulatory scrutiny in multiple jurisdictions, complicating the path to broader adoption. Lawmakers in Congress have also signaled a willingness to tighten oversight, arguing that existing frameworks do not adequately deter insider trading or protect consumers in these newer trading venues.

Against this backdrop, Schwab’s cautious posture reflects a broader tension in the market: mainstream financial institutions want to participate in the potential utility of prediction markets, but they gravitate toward use cases aligned with risk management and long-horizon investing, rather than pure entertainment or speculative bets. Wurster’s comment that prediction markets must be aligned with “building long-term wealth” indicates a preferred framing: markets that help investors hedge or calibrate exposure to macro- or event-driven risk, rather than markets centered on volatile narratives or sensational outcomes.

Esposito’s remarks at Semafor likewise underscore a pragmatic view from a market-making perspective. While indicating interest in event contracts as hedges—such as those tied to elections or other geopolitical developments—Citadel remains attentive to liquidity conditions. If and when volumes and counterparties converge to support reliable price discovery, the economics of market-making in prediction markets could become more compelling for large liquidity providers and institutions with diversified risk profiles.

The regulatory environment adds another layer of complexity. The record-level activity reported by market trackers contrasts with the legal challenges faced by platforms that have been accused of running unlicensed betting markets. The tension is not simply about whether such products exist, but how they’re structured, who can access them, and what protections are in place for participants. In parallel, the debate over insider trading and market manipulation in prediction markets has intensified, with policymakers weighing appropriate compliance standards for both operators and participants.

From a market perspective, the current maturity gap—significant interest and use by both retail and institutional segments, but limited high-liquidity participation—creates a classic “build vs. wait” scenario for incumbents. Schwab’s stance implies a potential, measured integration into mainstream financial services with a focus on wealth management workflows, risk planning, and portfolio hedging. Citadel’s position suggests caution, but a readiness to scale into the right niches if liquidity improves and regulatory clarity advances.

For traders and investors, the evolving picture suggests several near-term watchpoints. First, the regulatory timeline is crucial: any new framework or enforcement direction could alter product design, accessibility and pricing dynamics across prediction markets. Second, liquidity signals from current market-makers and new entrants will shape price discovery and the feasibility of sophisticated hedging strategies that rely on event-driven outcomes. Third, investor education and risk disclosures will determine how a broader audience uses these instruments—whether as speculative vehicles or as practical hedges against uncertain but foreseeable events.

In parallel, the broader crypto and traditional markets will be watching how these developments influence risk-sharing tools and derivative-like instruments. Event-based contracts share some characteristics with traditional options, yet they operate in a space where real-world outcomes can rapidly reshape pricing and exposure. If large financial institutions begin to offer or partner on such products, it could lend more legitimacy and stability to the sector, while also inviting intensified regulatory scrutiny and a reevaluation of risk controls for participants.

Notably, Schwab’s recent foray into crypto-lite exposure—specifically the launch of Bitcoin and Ether trading on Thursday—frames how traditional players are diversifying beyond conventional equities and fixed income. While that launch is separate from prediction markets, it signals an overarching trend: incumbents are testing digital-asset and event-driven product suites in parallel, seeking to blend familiar wealth-management paradigms with newer forms of risk transfer and exposure.

As the market evolves, observers should watch how liquidity, regulatory clarity and user demand interact to shape the viability of prediction-market offerings from large financial institutions. The next several quarters could reveal whether these strategies remain experimental or begin to form a core component of the mainstream financial toolkit.

For readers seeking deeper context, the ongoing coverage of prediction markets’ legal status and regulatory developments remains essential. Related reporting has highlighted debates around insider trading and the appropriate scope of oversight, with lawmakers and enforcement agencies weighing how to balance innovation with guardrails. Meanwhile, industry data continues to illustrate a fast-growing user base and notable volume, reinforcing the idea that prediction markets occupy a pivotal niche at the intersection of finance, technology and public events.

As Schwab and Citadel monitor the landscape, the broader market will be watching closely to see which model gains traction: a carefully framed, wealth-focused product by traditional finance players, or more modular, liquidity-driven solutions that attract a broader base of traders and institutions.

What unfolds next may hinge on regulatory clarity and the ability of market makers to build durable liquidity. If those elements align, prediction markets could slip from curiosity to cornerstone tools for portfolio hedging and risk assessment in a more mainstream financial ecosystem.

Sources and context: The discussion around Schwab and Citadel’s potential entry into prediction markets was reported alongside coverage of growth in prediction-market activity. Token Terminal data indicate a record 23.6 billion dollars in combined monthly trading volume for Kalshi, Polymarket and related platforms in March. Industry observers have noted regulatory actions against prediction-market operators in several states, as well as congressional scrutiny over insider trading concerns. Citadel’s comments were reported during a Semafor World Economy conference in Washington, DC, and Schwab’s remarks followed remarks linked to client discussions, with Schwab also recently launching cryptocurrency trading on its platform, as reported by CNBC.

Token Terminal data cited the March volume milestone for Kalshi and Polymarket, illustrating the sector’s rapid momentum.

Further reading and related coverage have highlighted ongoing debates about the legality and ethics of prediction markets, including questions about the role of sports and politics Betting and how regulators respond to new products, as described in coverage of court cases and regulatory proposals.

As the conversation around prediction markets continues to unfold, investors should monitor regulatory developments, liquidity dynamics and product design choices that will determine whether these markets become a staple of mainstream financial risk management or remain a niche instrument for specialized traders.

TLDR

- BTC climbed to $78,000 following Iran’s temporary reopening of the Strait of Hormuz, before retreating to $76,000 when the passage was shut down again less than a day later.

- The upward move sparked $762 million in cryptocurrency liquidations, with short positions accounting for $593 million of the total.

- Spot Bitcoin ETFs recorded approximately $1 billion in weekly inflows — marking their strongest performance since January.

- Morgan Stanley introduced a Bitcoin Trust fund that has accumulated $120 million in assets within its first six days of trading.

- Major altcoins including Ether, XRP, BNB, and Solana registered weekly gains despite experiencing weekend declines.

Bitcoin experienced significant volatility this week as geopolitical developments in the Middle East dominated market sentiment. The digital asset’s price fluctuated dramatically as circumstances surrounding the Strait of Hormuz evolved rapidly.

Iran’s foreign minister declared on Friday that the Strait of Hormuz would be accessible to commercial vessels throughout the duration of a ceasefire agreement. President Donald Trump corroborated the announcement, stating that Iran had committed to an “unlimited” halt of its nuclear activities.

The cryptocurrency market reacted swiftly, pushing Bitcoin beyond the $78,000 threshold. Conversely, energy markets moved in the opposite direction as Brent crude plummeted nearly 10% to approximately $85 per barrel.

This breakout catalyzed one of 2026’s most substantial short squeezes. According to CoinGlass analytics, the market witnessed $762 million in aggregate liquidations affecting 168,336 traders. Short positions comprised $593 million of these liquidations, with bitcoin shorts specifically representing $381 million.

Funding rates for bitcoin perpetual contracts had remained in negative territory for several weeks, indicating that short sellers were compensating longs to maintain their bearish positions. The Hormuz announcement served as the catalyst that reversed this dynamic.

ETF Inflows Reach Three-Month Peak

While price movements captured market attention, Bitcoin ETFs silently achieved their most impressive week since January. SoSoValue data reveals that spot Bitcoin ETFs attracted $996 million in net inflows throughout the week.

Friday recorded the week’s largest single-day influx with $663.9 million entering the funds. Combined net assets across all spot Bitcoin ETFs surpassed $101 billion, accompanied by daily trading volumes approaching $4.8 billion.

Ethereum-focused ETFs similarly demonstrated strength, accumulating nearly $276 million over the week, per Farside Investors data.

Morgan Stanley’s recently unveiled Bitcoin Trust contributed to this trend. The financial product has already amassed $120 million in assets despite having only six trading days under its belt, surpassing WisdomTree during this brief period.

Iran Policy Reversal Triggers Bitcoin Decline

Fewer than 24 hours following the Hormuz reopening announcement, Iranian authorities reversed their position. The Nour state news outlet reported that the strait had returned to “strict management and control by the armed forces,” attributing the change to a U.S. blockade targeting Iranian ports.

Multiple tanker operators informed Bloomberg that their ships received Iranian radio communications instructing them to halt passage. One supertanker captain reported hearing gunfire and subsequently reversed direction.

Bitcoin declined to $76,091 by Saturday evening in Asian trading hours, maintaining just a 0.8% daily increase. Ethereum decreased 3% to approximately $2,365, while Solana slipped 1.3% and Dogecoin fell 2.1%.

Examining weekly performance, XRP outperformed all major cryptocurrencies with a 6.4% advance. BNB gained 4.6%, Ether climbed 5.2%, and Bitcoin preserved a 4.7% weekly increase despite the weekend pullback.

Market analysts at Bitunix observed that Bitcoin continues trading within an established range, encountering resistance above $75,000 and finding support near $72,000 according to their most recent assessment.

TLDR:

- MegaETH processes over 100,000 TPS with sub-10ms block times, settling all activity directly on Ethereum mainnet.

- iTRY, a Turkish Lira stablecoin backed by money market funds, launches with a real-time 45% APY yield loop strategy.

- Kumbaya XYZ holds $51M of MegaETH’s $89M TVL, with USDM capturing 74% of the network’s $84M stablecoin market cap.

- 53% of $MEGA token supply unlocks only after hard KPIs are met, with USDM revenue funding active protocol buybacks now.

MegaETH ($MEGA) is gaining attention as the first real-time Ethereum Layer 2 in history. The network delivers sub-10-millisecond block times and over 100,000 transactions per second.

All activity settles directly on Ethereum. The protocol currently holds approximately $89 million in total value locked.

With 2.26 million transactions in 24 hours and zero artificial incentives, MegaETH is building momentum. The network positions itself as a high-throughput onchain settlement layer for real applications.

iTRY Launch and Live DeFi Protocols Drive Activity on MegaETH

One of the most anticipated developments is the launch of iTRY, a Turkish Lira stablecoin. As noted by researcher Nick Research on X, iTRY is backed by money market funds and offers around 45% APY.

The yield strategy works through a real-time loop: lock iTRY, mint wiTRY, borrow USDm, and compound yield. This carry loop removes traditional lock-up barriers for yield seekers.

The broader stablecoin market on MegaETH is already well-established. USDM, issued through Ethena, captures over 74% of the $84 million stablecoin market cap on the network.

Kumbaya XYZ contributes $51 million of the $89 million total TVL on its own. That concentration shows real capital deployment rather than distributed incentive farming.

Bluechip DeFi protocols went live on the network from day one. Aave V3, GMX, and World Markets launched alongside a Chainlink Scale integration.

That integration provides access to nearly $14 billion in flagship assets, including wstETH and LBTC. This confirms that major DeFi infrastructure views MegaETH as production-ready.

Perpetuals trading activity is rising sharply on the network as well. Weekly perps volume climbed 900% to reach $45 million over seven days.

The sequencer operates at cost, which keeps transaction fees among the lowest in crypto. These factors together are drawing active traders to the platform.

$MEGA Tokenomics Link Supply Unlocks to Hard Performance Milestones

The $MEGA token structure stands out for its milestone-based unlock mechanism. There are no points programs, no emissions, and no manufactured TVL incentives in the design.

Instead, 53% of total supply unlocks only after the network hits hard KPIs. Token release is directly tied to real, measurable growth.

Foundation revenue from USDM activity flows into direct $MEGA buybacks, which are already active. This buyback mechanism provides consistent demand without depending on market speculation.

Protocol revenue-backed buybacks at this stage of development remain uncommon. It adds a self-sustaining element to the overall token economy.

The token generation event remains tied to milestones rather than a fixed calendar date. This approach shifts builder incentives toward long-term throughput growth.

The network currently runs at 10 gigagas per second, supporting complex smart contracts at scale. That throughput level makes MegaETH suitable for applications requiring fast, reliable execution.

The MegaMafia ecosystem is expanding into DeFi, gaming, and culture. Brix recently secured $5.5 million from Turkish institutional investors ahead of the iTRY launch. Active addresses reached 3,230 in 24 hours, reflecting genuine user engagement on the network.

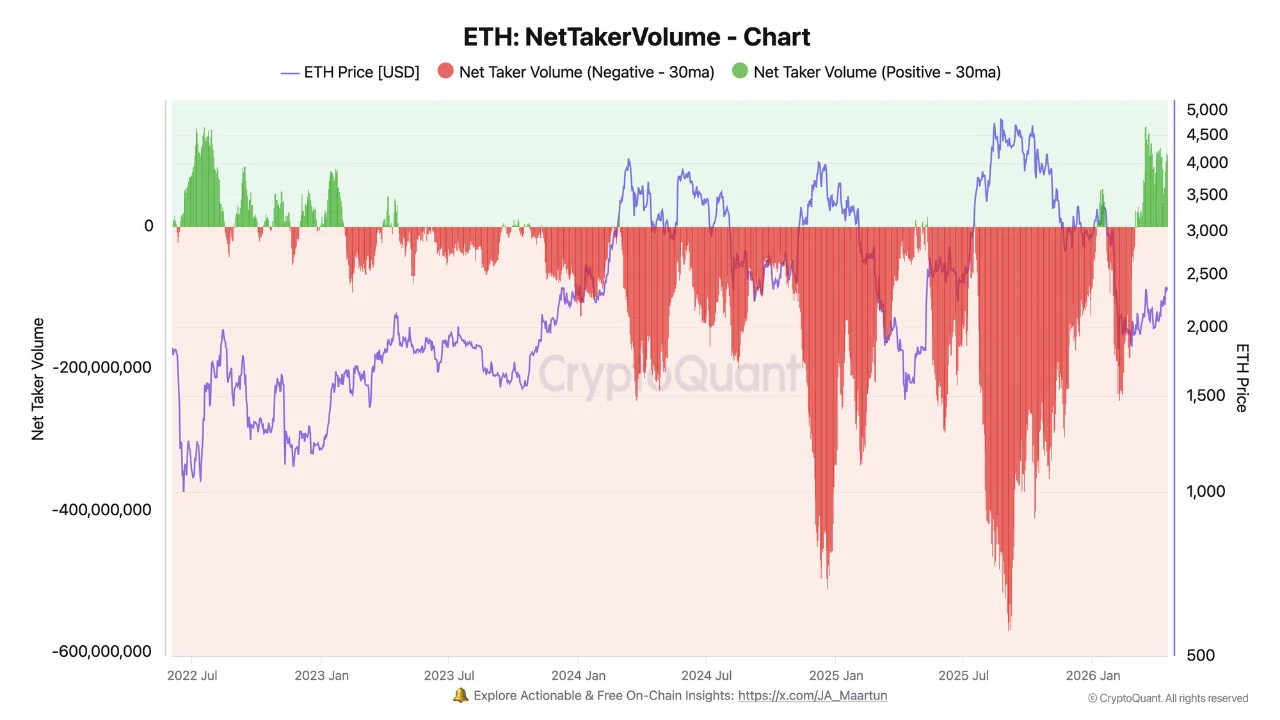

TLDR:

- ETH net taker volume turned positive at +$102M, snapping months of consistent sell-side dominance.

- Sell pressure peaked at -$568M when Ethereum set its all-time high just below $5,000 this cycle.

- Comparable buying pressure was last recorded in 2022 when ETH traded near the $1,000 price level.

- Since March, buy-side volumes have steadily grown, pointing to a possible shift in market positioning.

ETH derivatives sentiment has undergone a notable change in recent weeks. After prolonged and consistent selling pressure throughout this market cycle, buy-side volumes are finally gaining ground.

Data from derivatives exchanges shows that net taker volume has turned positive, recording +$102 million in a single day.

This marks a clear departure from the heavy sell-side dominance seen at previous ETH price peaks. Analysts are now watching whether this shift holds and supports a broader recovery for Ethereum.

Heavy Sell Pressure Shaped ETH Derivatives Throughout This Cycle

For most of this cycle, Ethereum has faced unusual and persistent selling pressure in derivatives markets. Net taker volume, which tracks the difference between buy and sell market orders on derivatives exchanges, remained almost consistently negative. This pattern became particularly visible during key price events in late 2024.

When ETH attempted to break above $4,000 in December 2024, net taker volume fell sharply to -$511 million. The sell pressure became even more extreme when Ethereum later reached an all-time high just below $5,000. At that point, sell-side dominance hit a cycle high of -$568 million in net taker volume.

Source: Cryptoquant

On-chain analyst Darkfost drew attention to this persistent trend in a recent post on Cryptoquant. The data showed that buyers repeatedly failed to absorb supply at key price levels throughout this cycle.

Sellers consistently overpowered buying activity, pushing net taker volume deep into negative territory during each rally.

That ongoing imbalance prevented Ethereum from sustaining breakouts, even during brief moments of upside price action.

Buy-Side Volume Climbs to Levels Not Seen Since the 2022 Bear Market

Since March, the dynamic in ETH derivatives markets has changed considerably. This change followed months of negative readings that characterized Ethereum’s derivatives activity.

Buy-side volumes have taken control, with net taker volume recording +$102 million in a single day. The last time Ethereum recorded comparable buying pressure was back in the 2022 bear market.

At that time, ETH was trading near the $1,000 area when similar buy-side activity appeared in the market. Market observers note this comparison carries weight given the scale of the current buying activity.

The return of strong buying interest at current price points to a change in how derivatives traders are positioned.

Darkfost noted in the post: “Since March, buy-side volumes have finally taken control, with +$102 million recorded today.”

The analyst added that buyers absorbing supply and chasing upside could signal the early stages of a recovery for Ethereum. The data stands in sharp contrast to the aggressive sell-side behavior that defined much of this cycle.

Crypto World

Tokenized Treasuries Cross $13.74B as Institutions Shift Focus From Issuance to Utility

TLDR:

- Tokenized U.S. Treasuries have reached $13.74B onchain, marking a shift from proof of concept to real utility.

- Standard Chartered and OKX launched a collateral mirroring programme using tokenized money market funds for trading.

- BounceBit’s Prime platform connects regulated custody with onchain execution through off-exchange settlement flows.

- Circle acquired Hashnote to position USYC as yield-bearing collateral within its expanding digital asset platform.

Tokenized U.S. Treasuries have reached $13.74 billion in onchain value, according to RWA.xyz. This milestone marks a turning point for digital asset markets.

The category has moved past proving tokenization is feasible. Now, the focus shifts toward making those assets functional within real financial infrastructure.

Major institutions are already responding to that shift with concrete programmes and integrations.

From Passive Holdings to Active Collateral Use

The first phase of tokenization centered on bringing familiar assets onto blockchain networks. That work is largely done. The next phase is about putting those assets to work once they are onchain.

Faster-moving collateral, productive capital deployment, and treasury-backed assets that serve active roles are now the priorities.

Franklin Templeton captured this thinking directly in its framing of tokenized money market funds. The firm noted that tokenization creates new utility and use cases, not simply a digital version of an existing instrument.

Its Franklin OnChain U.S. Government Money Fund invests at least 99.5% of assets in U.S. government securities, cash, and related repos.

Standard Chartered and OKX announced a collateral mirroring programme with Franklin Templeton. The programme allows institutional clients to use crypto and tokenized money market funds as off-exchange collateral for live trading. That development moves the market clearly beyond passive holding toward active capital markets use.

BlackRock’s BUIDL and Ondo’s USDY have also helped define the institutional profile of tokenized Treasuries onchain.

Together, these products combine recognizable underlying assets, short-duration government yield, and compatibility with digital asset workflows.

Those three qualities make tokenized Treasuries one of the most relevant real-world asset categories for crypto-native markets today.

Infrastructure Built Around Capital Efficiency

BounceBit has positioned its RWA stack around the idea that tokenized cash equivalents should not stop at issuance. The platform integrated Ondo’s USDY as its first tokenized RWA.

It later expanded to source tokenized cash equivalents from Franklin Templeton’s Benji and BlackRock’s BUIDL through Securitize.

BounceBit’s Prime platform connects regulated custody with onchain execution. Client assets are custodied at Standard Chartered and mirrored to trading venues through an off-exchange settlement flow. That structure allows capital to remain controlled while being deployed more efficiently across strategies.

The platform targets yield above the risk-free rate through structured strategies built on tokenized cash equivalents and market-neutral trading.

Rather than passive exposure, Prime is designed to turn tokenized collateral into a working part of institutional treasury and trading operations.

Circle’s acquisition of Hashnote brought USYC into Circle’s platform, with Circle positioning it as yield-bearing collateral for digital asset markets.

That move, alongside the growth of BUIDL and Benji integrations, shows a consistent direction. Stablecoins built the base layer for onchain dollars. Tokenized Treasuries are now building the next layer for onchain yield-bearing capital.

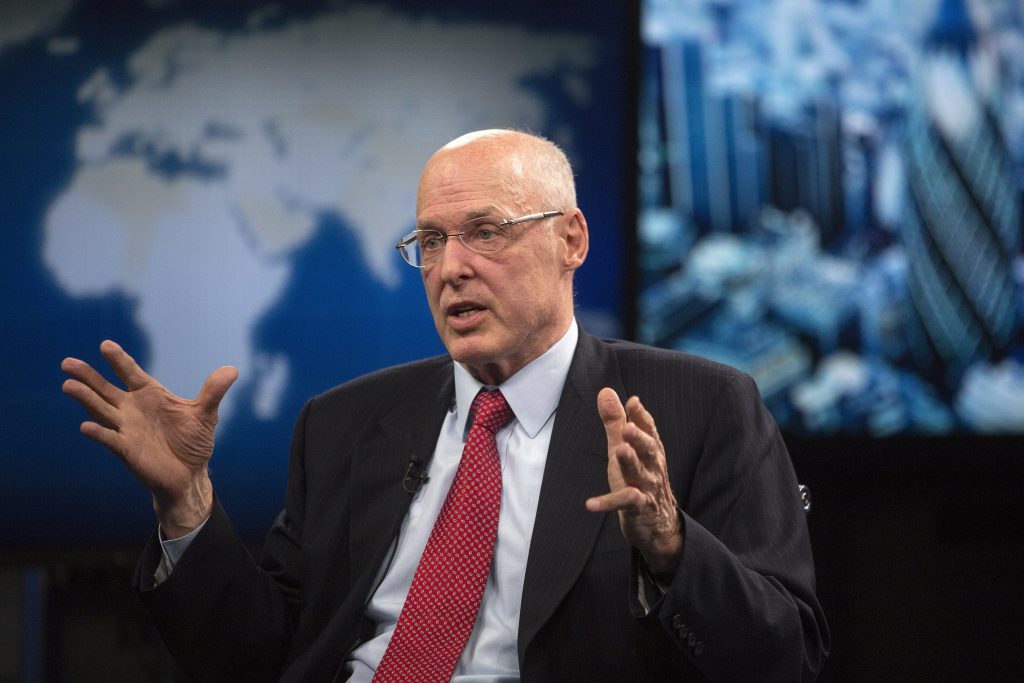

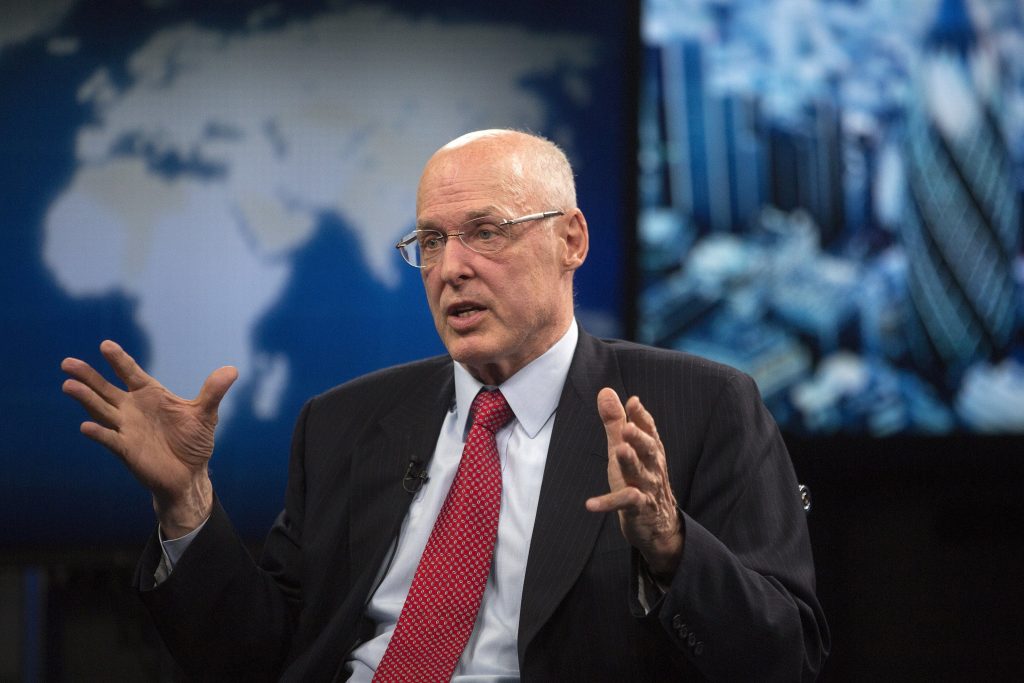

In the latest bond news, Henry Paulson, who steered the U.S. financial system through the 2008 collapse as Treasury Secretary, is warning that the $35 trillion U.S. debt load could trigger a Treasury bond market crash, and calling for an emergency “break-glass” contingency plan to be ready before it hits.

The transmission channel to crypto is direct: a disorderly bond sell-off tightens dollar liquidity fast, and tight dollar liquidity historically punishes risk assets before any safe-haven Bitcoin narrative has time to develop.

30-year Treasury yields have already crossed 5%, a threshold last breached in October 2023 during the inflation-driven spike and essentially unseen before that since the pre-Great Recession era. That’s not a warning sign in isolation. It’s a warning sign with Paulson’s voice behind it.

Key Takeaways:

- Who warned: Henry Paulson, U.S. Treasury Secretary 2006–2009 and architect of the 2008 TARP bailout, issued the alert.

- What he said: Paulson described a potential Treasury demand collapse as having “vicious” effects – likening the timing to hitting “the wall” unpredictably due to the “law of economic gravity.”

- What he wants: An emergency “break-glass” or “emergency brake” debt plan ready on the shelf before a crisis materializes.

- Bond market context: 30-year Treasury yields crossed 5% recently; U.S. debt has grown from $10 trillion in 2008 to over $35 trillion by 2025.

- April 2025 precedent: Treasury yields surged sharply amid Trump tariff escalation, defying safe-haven expectations and coinciding with equity sell-offs – a preview of correlated risk-off pressure.

- Crypto transmission channels: Dollar liquidity tightening, risk-off rotation away from speculative assets, and potential cascading liquidations in leveraged crypto positions.

- Pushback: Treasury Secretary Scott Bessent dismissed comparable warnings from JPMorgan CEO Jamie Dimon on June 1, 2025, calling his track record on such predictions poor.

- Watch: 10-year Treasury yield level relative to 4.8% resistance, upcoming Fed communications, and BTC’s correlation to the DXY during any yield spike.

Discover: The best crypto to diversify your portfolio with

Bond News: How a Bond Market Shock Actually Reaches Crypto, and Which Assets Get Hit First

The question isn’t whether Paulson is right about Treasury market fragility. It’s whether crypto trades as a safe haven or a risk asset when it is proven right, and history gives a clear answer, at least in the short run.

A disorderly Treasury sell-off forces dollar liquidity higher as investors dump bonds and demand cash. That dynamic hits leveraged positions first. Crypto markets, where open interest across derivatives venues has been climbing sharply, carry exactly that leverage profile, elevated exposure that becomes a liability the moment dollar funding costs spike.

The April 2025 episode clearly illustrated the mechanism. When Treasury yields surged amid tariff-escalation fears, crypto did not decouple toward safety. It sold alongside equities, in defiance of the digital-gold narrative. Correlation to risk assets held. That’s the bear case in one data point.

Paulson’s specific concern, that demand for Treasuries could collapse suddenly and without obvious warning, governed by what he calls the “law of economic gravity”, implies a non-linear shock rather than a gradual yield drift.

Non-linear shocks are what liquidation cascades are built from. A 10-year yield breaking decisively above 5% with accelerating momentum would be the confirmation threshold worth watching.

Bitcoin Safe Haven or Risk-Off Casualty: What the Bond Stress Means for Crypto Prices

The idea sounds clean. If bonds start losing credibility, capital has to go somewhere, and Bitcoin, with its fixed supply and non-sovereign nature, becomes an obvious alternative, which is why big players keep that thesis in the background.

But the timing is where people get caught.

In a real bond market shock, the first move is not rotation; it is panic, and in that phase, everything gets sold, including Bitcoin, just like what happened in March 2020 when BTC dropped hard before turning higher.

Ethereum and major altcoins are currently at technical inflection points, making them particularly vulnerable to a macro liquidity shock, which could be the deciding factor. ETH does not carry the same hard-money narrative as BTC and would likely underperform in a genuine risk-off episode driven by sovereign debt stress.

Jamie Dimon’s parallel warning, that investor demands for higher Treasury yields could spike mortgage rates independently of Fed policy, reinforces Paulson’s thesis from a different angle. Bessent’s public dismissal of Dimon on June 1 suggests official Washington is not in crisis mode. But bond markets are already pricing something the Treasury Secretary isn’t fully acknowledging.

Discover: The best pre-launch token sales

The post Former Treasury Chief Warns Bond Market Crash Could Hit Crypto Outlook appeared first on Cryptonews.

A California federal judge has cleared Caitlyn Jenner of a class-action push stemming from her JENNER memecoin, ruling that the token does not meet the basic securities requirements under U.S. law. In a Thursday order, U.S. District Judge Stanley Blumenfeld Jr. said the plaintiffs failed to plausibly plead that JENNER tokens were investment contracts because the venture did not pool investor money or use funds to develop a related product or technology.

Defendants stated that “the $JENNER token is a memecoin on the Ethereum blockchain intended solely for entertainment purposes,” and that its value would increase because Jenner would use her fame and influence to promote it, increasing demand. Promotion alone, however, does not establish a common enterprise absent pooling or a structure linking investor fortunes.

The case traces back to November 2024, when a group of JENNER memecoin buyers filed suit against Jenner and her late manager, Sophia Hutchins, alleging an unregistered securities offering and that investors lost thousands as the token’s price collapsed. The plaintiffs claimed that Jenner’s campaign-promised activities and fee mechanics would drive a return for investors. In May 2025, Blumenfeld had already tossed the suit for failure to state a claim, and an amended complaint was filed later that month, led by Lee Greenfield, a UK citizen who said he had invested more than $40,000.

In the amended filing, plaintiffs argued that investors pooled their assets as Jenner promised that once the token reached a market value of $50 million, a 3% transaction fee would fund token buybacks, marketing, donations to a political campaign, and a separate token representing ownership in Jenner’s Olympic gold medal. Blumenfeld pointed out that the amended complaint heavily focused on donations to Donald Trump’s campaign but did not clearly explain how such donations would deliver a financial return to investors. He also noted that the plan to distribute fractional ownership in the gold medal was announced after most purchases and was never executed.

The judge declined to give the class another chance to amend the complaint and indicated that claims tied to contracts and common-law fraud under California law would be more appropriate in state court. The decision leaves the securities-related claims resolved in federal court, while signaling that related state-law claims may proceed separately on different grounds.

JENNER first surfaced on the Solana blockchain via the memecoin creatorPump.fun in May 2024. The project quickly found itself embroiled in controversy after Jenner and other celebrities behind memecoin launches claimed they were allegedly scammed by Sahil Arora, a figure linked to the project’s early promotion efforts. Jenner subsequently relaunched JENNER on Ethereum, a move that investors said diluted the value of the original Solana token, which had peaked at nearly $7.5 million in June 2024 before retreating sharply.

The court’s ruling highlights a central challenge in memecoin litigation: promotional activity alone does not automatically create a securities partnership or an investment contract unless funds are pooled and a plausible path to investor returns can be demonstrated. The decision does not provide a broad endorsement of memecoins as safe investments, but it narrows the legal route for investors who relied primarily on celebrity promotion to claim securities violations.

For investors and builders in the memecoin ecosystem, the ruling reinforces the importance of transparent token mechanics and verifiable fundraising structures. It also underscores that, even in high-profile celebrity launches, the line between entertainment-focused tokens and regulated securities remains a contested frontier—one that regulators continue to scrutinize, particularly as new token categories emerge and promotional campaigns accelerate.

Key takeaways

- The court dismissed the federal securities claims against Caitlyn Jenner in the JENNER memecoin case, ruling the token did not plausibly constitute an investment contract because funds were not pooled and no related product or technology was developed with investor money.

- The decision preserves the possibility that related California-law claims could proceed in state court, though the federal securities case is resolved on the merits for now.

- The amended complaint failed to convincingly connect promised uses of a 3% fee and public donations to tangible financial returns for investors, according to the judge’s order.

- JENNER originated on Solana in May 2024, later migrated to Ethereum after controversies and claims of misrepresentation, with the token peaking at about $7.5 million in mid-2024 before collapsing.

- The ruling underscores that promotional activity alone is insufficient to show a common enterprise or an investment contract; structure and fund flows matter significantly in securities analyses of memecoins.

Context and implications for the memecoin landscape

The ruling arrives at a time of heightened regulatory attention toward memecoins and celebrity-led token launches. While it narrows the scope for investors to pursue federal securities claims in similar cases, it does not absolve promoters from potential liability on other legal grounds. The case illustrates that courts will closely examine whether investor money was actually pooled and whether a credible pathway exists for investors to obtain a financial return, beyond hype and promotional activity.

Looking ahead, observers will watch whether California state courts continue to pursue related contract or fraud theories and how parties might frame future campaigns to balance promotional potential with clear, investor-centric tokenomics. As the ecosystem evolves, the balance between creative branding and legally compliant fundraising remains a central concern for issuers, platforms, and legal counsel navigating a rapidly shifting regulatory environment.

Readers should monitor developments around memecoin regulation, enforcement actions, and any new guidance from U.S. authorities as they analyze cases where celebrity-led launches intersect with traditional securities law principles. The outcome in this case serves as a notable data point in the broader discourse on what constitutes a security in the fast-moving world of blockchain-enabled hype tokens.

US media personality and former Olympian Caitlyn Jenner has escaped a class-action lawsuit after a federal judge ruled her memecoin was not a security under US law.

California federal judge Stanley Blumenfeld Jr. wrote in an order on Thursday that the lawsuit failed to plausibly plead that Caitlyn Jenner (JENNER) tokens were investment contracts, as they didn’t pool investor money or use funds to develop “any related product or technology.”

“Defendants stated that ‘[t]he $JENNER token is a memecoin on the Ethereum blockchain intended solely for entertainment purposes,’ and that its value would increase because Jenner would use her fame and influence to promote it, increasing demand,” the order said.

“Promotion alone, however, does not establish a common enterprise absent pooling or a structure linking investor fortunes,” it added.

A group of JENNER memecoin buyers first sued Jenner and her late manager, Sophia Hutchins, in November 2024, claiming they lost thousands of dollars as the token’s price collapsed and that JENNER was an unregistered securities offering.

Blumenfeld tossed the suit in May 2025 for failure to state a claim, and the group filed an amended complaint later that same month, led by Lee Greenfield, a UK citizen who claimed he lost more than $40,000 investing in JENNER.

The amended complaint had argued that investors had pooled their assets as Jenner promised that once the token reached a market value of $50 million, a 3% transaction fee would fund token buybacks, marketing, donations to Donald Trump’s presidential campaign and a token for ownership in Jenner’s Olympic gold medal.

Blumenfeld wrote that the amended complaint heavily focused on planned donations to Trump, but didn’t explain how investors believed that doing so would provide a financial return to them.

“Nor is it clear that the alleged plan to distribute fractionalized ownership interests in Jenner’s gold medal has any bearing on Greenfield’s claim, since the plan was not announced until August 2024—after the last of his purchases—and was never executed,” he added.

Related: TRUMP whales load up as Mar-a-Lago luncheon approaches

Blumenfeld denied allowing the class group another chance to amend the lawsuit and added that claims regarding contracts and common law fraud under California law were best sent to state court.

JENNER was first launched on the Solana blockchain via the memecoin creator Pump.fun in May 2024. It was soon embroiled in controversy after Jenner and other memecoin launching celebrities claimed they were scammed by Sahil Arora, a claimed collaborator on the tokens.

Jenner relaunched the token on Ethereum, which investors claimed diminished the value of the original Solana token. The token has since essentially lost all of its value after hitting a peak value of nearly $7.5 million in June 2024.

Magazine: Memecoins: Betrayal of crypto’s ideals… or its true purpose?

Crypto World

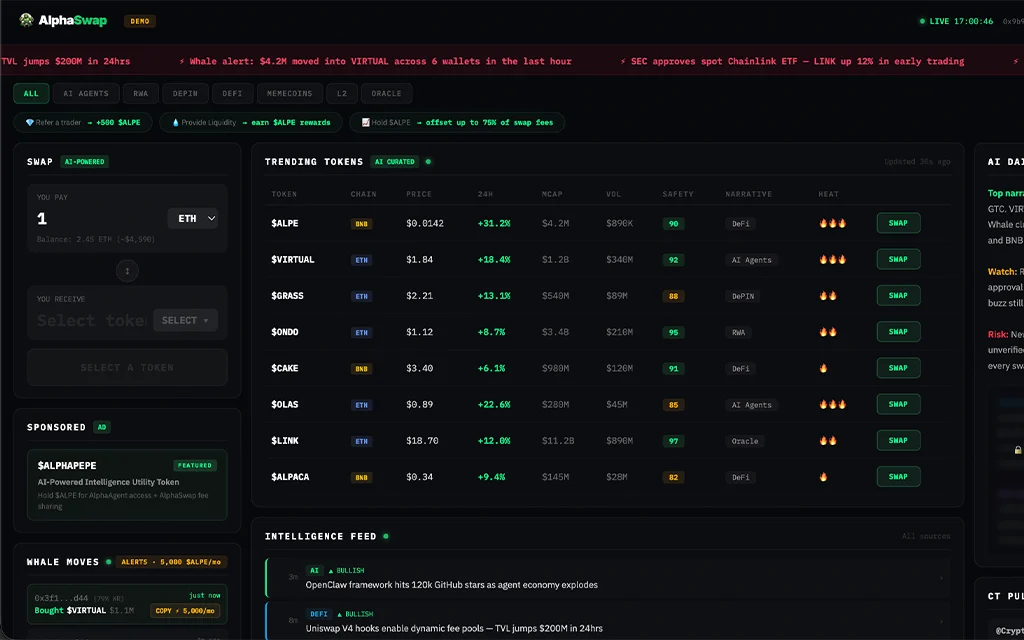

Solana Price Prediction: SOL Is a Legacy Trap at $79 While AlphaPepe AI DEX Generates Real Traction for Early 1,000x Gains

Solana trades at $79, down 31% year to date and 73% from its January 2025 high of $293. DEX volume collapsed 62% in three weeks. Active traders fell from 4.4 million to 400,000. Meme coin trading crashed 81%. A whale unlocked 1.82 million SOL worth $163 million in a single transaction. The network has never been healthier. Record TPS, Alpenglow upgrade momentum, SEC commodity classification. None of it has moved the price. SOL at $79 with a $47 billion market cap needs $79,000 per token for 1,000x. That is the legacy trap. While SOL grinds against it, AlphaPepe is generating real traction at $0.01494 with $890,000 raised, a live AI DEX, and 1,000x math that requires $15 billion, not $33 trillion.

Why the Solana Price Prediction Is Trapped

The meme economy that powered SOL’s 2024 rally has broken. New token launches on Pump.fun dropped 80% since January. The TRUMP token wiped $2 billion across 800,000 wallets. Stablecoin transfers fell 80%. The four million traders who left took the revenue model with them.

Standard Chartered revised its target from $310 to $250. Resistance between $95 and $105 has rejected every rally. Even the $250 bull case is a 3.2x requiring ETF inflows, a Fed pivot, and a DEX volume recovery with no current momentum behind it. The Solana price prediction is a macro story wearing a network price tag. The macro is not cooperating.

AlphaPepe AI DEX Generates the Traction SOL Cannot Convert

AlphaSwap is doing what Solana’s collapsed DEX economy stopped doing. The AlphaPepe cross-chain AI DEX screens contracts for exploit patterns before users interact, surfaces whale movements across chains, and collects fee revenue today. Not from meme speculation. From infrastructure utility in a category growing at 22.3% annually toward $120 billion.

The developer proved their engineering across 500 million Shibarium mainnet transactions. A 10/10 BlockSAFU audit verified the contract. Supply fixed at 1 billion. Instant delivery. Zero vesting. Stakers earning 85% APR. Q2 DEX launch approaching. Tier 1 CEX follows.

Over $890,000 from 7,700 wallets. 100 new addresses daily. Stage 13 at $0.01494 with the price climbing every few days and jumping when stages fill. A $2,000 entry secures 133,869 tokens. At $1.50 that reaches $200,803. At $3.50 it crosses $468,541. Buyers at $2,000 or above can apply code ALPHA50 for a 50% bonus. SOL needs $47 billion in new capital for a 2x. AlphaPepe needs Q2 for 1,000x.

The Legacy Trap Has a Floor. The Presale Has a Deadline.

SOL will recover when macro turns. The network deserves a higher price. But the Solana price prediction at $79 is capped by a market cap that makes exponential returns impossible. AlphaPepe at $0.01494 with $890,000 raised and a live AI DEX is not capped by anything except the listing date. Stage 13 is filling.

Click To Visit AlphaPepe Official Website To Enter The Presale

FAQs

Why is SOL a legacy trap at $79?

SOL’s $47 billion market cap needs $79,000 per token for 1,000x. DEX volume collapsed 62%, active traders dropped from 4.4 million to 400,000, and the price is down 31% YTD despite record network performance.

How does AlphaPepe generate real traction?

AlphaSwap is a live AI DEX collecting fee revenue with contract screening and whale tracking. Over $890,000 raised across 7,700 wallets at $0.01494.

Is the AlphaPepe presale still open?

Stage 13 at $0.01494 with over $890,000 raised and 7,700 holders. Instant delivery, no vesting, Q2 DEX launch approaching.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

The Executive’s unity exposes the limits of devolution amidst fuel crisis

Steve Nicol names who he thinks will be next Liverpool manager, and who’d be a solid alternative

The best movies on Amazon Prime Video (April 2026)

-

NewsBeat6 days ago

NewsBeat6 days agoPep Guardiola and Gary Neville agree over Arsenal title problem that benefits Man City

-

Crypto World6 days ago

Crypto World6 days agoThe SEC Conditionalises DeFi Platforms to Be Avoided for Broker Registration

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Theodora Dress

-

Politics7 days ago

Politics7 days agoWorld Cup exit makes Italy enter crisis mode

-

Crypto World5 days ago

Crypto World5 days agoSEC Signals Exemption for Crypto Interfaces From Broker Registration

-

News Videos4 days ago

News Videos4 days agoSecure crypto trading starts with an FIU-registered

-

Sports2 days ago

Sports2 days agoNWFL Suspends Two Players Over Post-Match Clash in Ado-Ekiti

-

Crypto World5 days ago

Crypto World5 days agoSEC Proposes Certain Crypto Interfaces Don’t Need to Register as Brokers

-

NewsBeat5 days ago

NewsBeat5 days agoTrump and Pope Leo: Behind their disagreement over Iran war

-

Politics1 day ago

Politics1 day agoPalestine barred from entering Canada for FIFA Congress

-

Crypto World1 day ago

Crypto World1 day agoRussia Pushes Bill to Criminalize Unregistered Crypto Services

-

Sports6 days ago

Sports6 days agoNWFL opens Pathway for new Clubs ahead of 2026 Season

-

Crypto World6 days ago

Crypto World6 days agoTrump whales load up ahead of Mar-a-Lago luncheon.

-

Business2 days ago

Business2 days agoCreo Medical agree sale of its manufacturing operation

-

Business6 days ago

Kering slides after Morgan Stanley downgrade, Gucci woes loom

-

Crypto World6 days ago

Sei Network Enters Quiet Reset Phase as On-Chain Metrics Signal a Slowdown in 2026

-

Tech6 days ago

Tech6 days agoGoogle adds E2E encryption to Gmail for iOS and Android enterprise users

-

Tech6 days ago

Tech6 days agoApple glasses won’t go brand shopping like Meta did with Ray-Ban and Oakley

-

Entertainment5 days ago

Entertainment5 days agoKarol G’s ‘Ultra Raunchy’ Coachella Set Gave ‘Satanic Vibes’

-

Entertainment5 days ago

Entertainment5 days agoBrand New Day’ Footage Reveals the Devastating Impact of ‘Now Way Home’

You must be logged in to post a comment Login