Crypto World

Coinbase (COIN) Stock Rises as Bitcoin-Backed Home Loans Get Fannie Mae Approval

Key Highlights

- A groundbreaking partnership between Coinbase (COIN) and Better Home & Finance (BETR) introduces cryptocurrency-collateralized home loans with Fannie Mae’s backing.

- Homebuyers can use bitcoin or USDC as down payment collateral without liquidating their digital assets.

- The financing structure eliminates capital gains tax liabilities and margin call risks — crypto price fluctuations won’t trigger additional collateral requirements.

- Borrowers will pay rates that are 0.5 to 1.5 percentage points above conventional 30-year mortgage rates.

- Fannie Mae’s acceptance of crypto-collateralized mortgages represents a watershed moment for digital asset integration into traditional finance.

Coinbase (COIN) has partnered with digital mortgage provider Better Home & Finance (BETR) to introduce a cryptocurrency-collateralized mortgage offering that enables prospective homeowners to leverage bitcoin or USDC as down payment security, now supported by Fannie Mae.

This represents an unprecedented milestone for Fannie Mae, which has never previously endorsed such financial products. As a government-sponsored enterprise regulated by the Federal Housing Finance Agency, Fannie Mae’s participation in U.S. housing finance is pivotal. This endorsement could catalyze broader institutional acceptance.

The financing solution targets ordinary homebuyers rather than exclusively serving wealthy individuals. Coinbase characterized the offering as quintessentially accessible to all Americans.

According to Better’s CEO Vishal Garg, approximately 41% of American households cannot purchase homes due to insufficient down payment funds. Many prospective buyers possess substantial assets in alternative forms, including cryptocurrency holdings.

The mechanics are straightforward: purchasers secure a conventional 15- or 30-year Fannie-backed home loan through Better. Rather than providing cash upfront, a secondary loan is collateralized by bitcoin or USDC stored with Coinbase.

The digital assets move into a custodial wallet managed by Better, though borrowers maintain ownership privileges. USDC holders continue receiving staking returns on their pledged collateral.

Rates for these cryptocurrency-backed products will exceed standard 30-year mortgage rates by 0.5 to 1.5 percentage points, varying based on individual borrower qualifications. Prospective buyers must factor this premium into their financial calculations.

Protection From Market Volatility and Forced Sales

Among the product’s most attractive characteristics is built-in protection against cryptocurrency price volatility. Bitcoin value declines don’t alter mortgage conditions or trigger additional collateral demands.

Liquidation occurs exclusively after 60 days of payment default — identical to conventional mortgage standards. Market volatility alone cannot result in collateral forfeiture.

Mark Troianovski, Coinbase’s head of consumer and platform business development, drew parallels to private banking for affluent clients. “They leverage assets rather than liquidating them for purchases; they secure loans against their holdings,” he explained.

Previous Crypto Mortgage Products Existed, But With Limited Scope

Cryptocurrency-backed home financing isn’t entirely novel. Miami-based Milo has provided such products since 2022, serving more than 100 clients. However, earlier offerings primarily served specialized markets — frequently foreign buyers or luxury property transactions.

Fannie Mae’s participation fundamentally alters the landscape. As the institution that purchases, securitizes, and guarantees mortgages on a massive scale, its underwriting criteria influence industry-wide lending standards.

Better had already pioneered similar territory in February 2023, permitting Amazon employees to pledge company stock for down payment collateral. The cryptocurrency variant employs comparable frameworks while expanding accessibility to Coinbase’s substantial user base.

Gallup data indicates that 14% of American adults held cryptocurrency in 2025. A Redfin survey from 2025 revealed nearly 13% of millennial and Gen Z purchasers liquidated crypto holdings to finance down payments — creating taxable consequences this product is specifically designed to circumvent.

The Trump administration previously instructed Fannie and Freddie Mac to establish protocols for recognizing cryptocurrency as qualifying mortgage application assets last June, demonstrating governmental support for digital asset industry growth.

TLDR:

- ONDO has rallied over 100% from its local lows and is now testing major Fibonacci resistance.

- Elliott Wave structure suggests the current move may still be a corrective rally within a bearish trend.

- A breakout above $0.598 could invalidate the bearish setup and support further upside momentum.

- Ondo’s RWA narrative gains traction through ties with JPMorgan, Mastercard, and Ripple pilots.

The ONDO price is shifting toward whether ONDO can sustain momentum or face renewed selling pressure at overhead resistance.

ONDO Price Analysis Signals Caution Near Major Resistance

ONDO has posted an aggressive recovery since bouncing from the February capitulation zone near $0.19. The move delivered a strong upside reaction after months of sustained downside pressure across the broader altcoin market.

The current rally has now pushed the price directly into the $0.486 to $0.598 region. This zone represents the 50% to 61.8% Fibonacci retracement of the prior decline, making it a critical technical barrier.

In Elliott Wave analysis, this area often acts as the termination point for wave 4 recoveries before the broader downtrend resumes.

Although price action has remained constructive, the structure of the rally continues to raise caution. The advance shows overlapping internal moves rather than the clean breakout behavior usually associated with a fresh bullish impulse. This suggests the recent recovery may still be corrective.

The bearish structure remains valid while ONDO trades below $0.598. If price fails to clear this resistance cluster, downside pressure could return quickly. The first major downside trigger remains a break below $0.35, which would suggest the rally has likely topped.

In that scenario, ONDO could revisit the $0.24 support zone initially. Additional weakness may expose the prior capitulation floor near $0.19 once again.

Institutional RWA Narrative Keeps ONDO in Spotlight

Despite technical caution, ONDO continues attracting strong attention due to its expanding role in tokenized finance.

The recent collaboration involving JPMorgan Chase, Mastercard, Ripple, and Ondo Finance has strengthened market confidence in the project’s long-term narrative.

The pilot reportedly demonstrated tokenized US Treasury settlement across institutions in under five seconds. This development addresses one of traditional finance’s major inefficiencies by improving settlement speed and cross-border liquidity movement.

As tokenized Treasuries gain traction, ONDO is increasingly being positioned within the infrastructure layer of the Real World Asset market.

Analysts view this as a strong narrative catalyst, especially as institutions continue exploring blockchain settlement solutions.

From a technical perspective, maintaining support above $0.35 to $0.40 keeps the medium-term bullish structure intact. However, a confirmed breakout above $0.598 remains the most important trigger for trend continuation.

If bulls secure that move, ONDO could open a path toward $0.70, with momentum potentially extending toward the $0.85 region in the next expansion phase.

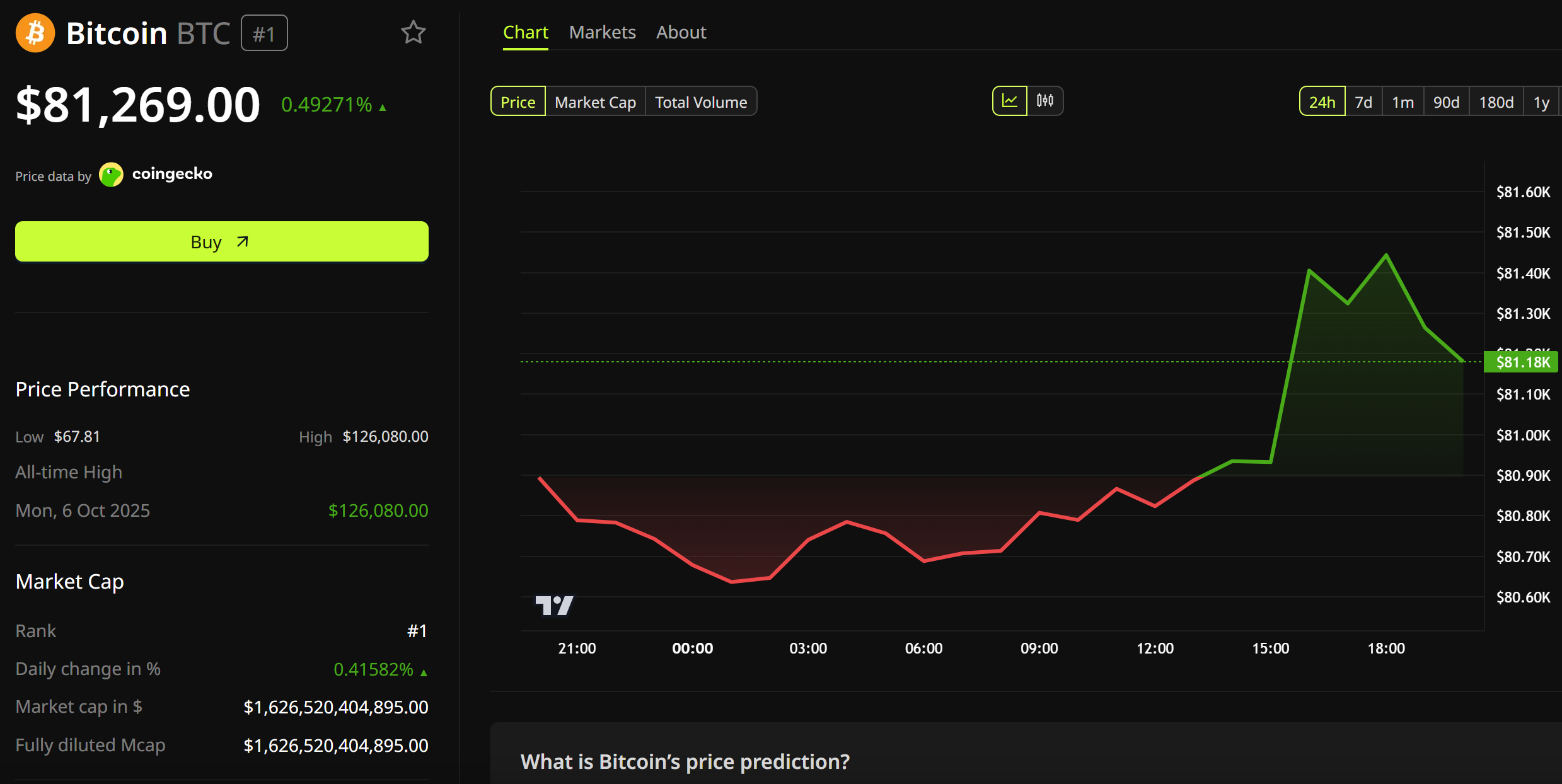

Bitcoin (BTC) climbed above $81,000 over the weekend, drawing trader caution as inflation data and political tension collide this week. The next technical target sits at $83,400 based on Fibonacci projections, with a rising RSI suggesting momentum continues to build.

Investors now face Tuesday’s Consumer Price Index (CPI) print, Wednesday’s Producer Price Index (PPI), and Thursday’s retail sales reading. OPEC’s monthly report also lands midweek. Friday marks Jerome Powell’s final day as Federal Reserve Chair.

Trump’s Iran Warning Adds Geopolitical Risk

Donald Trump accused Iran of stringing along the United States for 47 years. The post singled out former President Barack Obama. Trump claimed Obama’s administration handed Tehran billions, including $1.7 billion in physical cash.

Trump described the transfer as a windfall the regime “had no idea what to do with.” He argued it gave Iranian officials a financial lifeline. The president did not announce new sanctions or military steps.

The remarks landed as Bitcoin’s weekend rally tested resistance near $81,000, sharpening focus on geopolitical risk across crypto markets.

Macro Calendar Tests Bitcoin’s Momentum

Tuesday’s CPI release remains the most consequential print for Federal Reserve policy expectations. Cooler-than-expected readings typically support risk appetite, while hot inflation tends to push out rate-cut timing. April data could reshape pricing for the next two FOMC meetings.

Wednesday adds PPI alongside OPEC’s monthly oil outlook, with Thursday’s retail sales and Friday’s industrial production rounding out the calendar. Each release could shift Fed rate-cut bets within minutes.

Whether Bitcoin reaches $83,400 or retreats depends on how Trump’s Iran rhetoric collides with US data this week. Powell’s final session as Fed Chair adds another wildcard.

“Never trust a $BTC weekend pump,” remarked Trader Killa in a post.

Bitcoin Channel Pattern Targets $83,400 if BTC Clears 200-Day EMA

Meanwhile, Bitcoin traded at $81,269 as of this writing, holding within a month-long ascending channel as price approached the 200-day exponential moving average (EMA) resistance at $82,036.

The token recovered roughly 35% from February lows near $60,000, supported by renewed spot Bitcoin ETF inflows. However, momentum indicators show mixed signals as BTC stalls just below a long-term trend line that has capped every rally attempt since late January.

Bitcoin RSI Climbs Above 65 as Overbought Risk Builds

The Relative Strength Index (RSI) on the daily chart sits at 65.56, with its moving average trailing at 61.89. Both readings remain firmly above the neutral 50 line, confirming that buyers control short-term price direction.

This momentum reading tracks Bitcoin’s steady recovery from the February capitulation. RSI has climbed without interruption since the indicator briefly pierced oversold conditions three months ago, mirroring the parallel rebound visible across BeInCrypto’s bear market analysis coverage.

Yet the current strength carries a warning. The 70 threshold marks entry into overbought territory, and the indicator now prints its highest reading since the breakdown began in January. Historical precedent shows that daily RSI pushes above 70 typically precede short-term cooling phases for BTC.

A clean breakout still needs volume confirmation. If buyers fail to drive the RSI through 70 while price holds below the 200-day EMA, bearish divergence could form between price highs and momentum highs. A daily close that drops the RSI back below 50 would flip the signal and validate sellers regaining control of the trend.

Bitcoin Price Prediction Eyes $83,400 if Channel Holds

Bitcoin trades inside a clean ascending channel that began in early April near the $60,000 floor. Price action has respected the channel midline as dynamic support throughout the rally, with each pullback finding buyers within the structure.

The 200-day EMA at $82,036 currently caps the upside. This level coincides with a heavy supply zone that rejected price multiple times during the January through February breakdown. A daily close above $82,036 would mark Bitcoin’s first reclaim of this trend line in nearly four months, validating the May outlook projected by several analysts.

Should BTC clear that hurdle, the 61.8% Fibonacci retracement at $83,399 becomes the next logical target. This level sits at the upper boundary of the channel, creating a confluence zone that could trigger profit-taking.

A measured move from the channel projects toward roughly $86,500 over subsequent weeks if buyers absorb supply at $83,400.

The bearish invalidation sits at the 50% Fibonacci level of $78,915. A daily close below this support would break the channel structure and open the door to a retest of the 38.2% Fibonacci retracement at $74,431.

Below that, the 23.6% retracement at $68,884 marks the final support before the recovery thesis breaks, in line with the broader long-term forecast for BTC in 2026.

Continued spot ETF demand remains the primary catalyst. Net inflows totaled roughly $2.7 billion across nine consecutive sessions in late April, with BlackRock’s IBIT and Fidelity’s FBTC capturing the majority share.

Total assets across U.S. spot Bitcoin products have now passed $100 billion, providing a steady bid that has held the lower channel boundary intact despite bearish risk factors flagged earlier in 2026.

Whether Bitcoin clears the 200-day EMA or rejects from it within the next two weeks will set the directional tone for the trend heading into June.

The post Bitcoin Eyes $83,400 But Trump’s Iran Warning and CPI Week Spark Trader Caution appeared first on BeInCrypto.

TLDR:

- Pompliano declared confidence that Bitcoin’s cycle bottom was established at the $60K price level.

- Institutional accumulation by buyers like MicroStrategy created consistent demand against Bitcoin’s fixed supply.

- Pomp argues volatility compression has broken Bitcoin out of its traditional four-year market cycle.

- Bitcoin, stablecoins, and tokenization are the assets Pompliano sees surviving and leading crypto’s next phase.

Bitcoin’s recent price action has renewed debate over whether the market has already seen its cycle low. Anthony Pompliano, widely known as “Pomp,” made a bold claim, stating, “I’m pretty confident that was the bottom at $60K.”

His comments came during a broader discussion on Bitcoin’s fundamentals, institutional adoption, and long-term outlook. The statement has since drawn significant attention from investors watching Bitcoin’s next move closely.

Pompliano Points to $60K as the Cycle Bottom

Pompliano’s confidence in the $60K bottom is rooted in Bitcoin’s core fundamentals. He described Bitcoin as offering “certainty” that traditional assets simply cannot provide.

Unlike gold or U.S. Treasuries, Bitcoin’s fixed supply and transparent monetary policy give investors a clear picture of what they own. That clarity, he argues, is what separates Bitcoin from every other asset class available today.

He also noted that the shift from fear to confidence among investors played a major role in establishing that floor. When prices hovered around $60K, many retail and institutional participants were still hesitant.

Pompliano described this period as one where the market needed to move from “fear to confidence” before a sustained recovery could take hold. That transition, in his view, defined the bottom.

Institutional activity also supported the case for $60K as a turning point. Buyers like Michael Saylor and MicroStrategy were accumulating during that period, adding consistent demand against a fixed supply.

However, Pompliano was careful not to overstate any single buyer’s role, calling the recovery a “confluence of events” rather than the result of one catalyst. Each factor reinforced the other, creating a durable floor.

Pompliano also challenged the traditional four-year Bitcoin cycle, arguing that “volatility compression” has changed how the market behaves entirely. Price movements now happen faster and with less dramatic drawdowns than in previous cycles.

If that pattern holds, the $60K level may represent the deepest pullback of this cycle. Investors waiting for lower prices, he suggested, may have already missed their entry point.

Bitcoin’s Fundamentals Back the Bullish Case

Beyond the price call, Pompliano laid out the structural reasons Bitcoin is well-positioned from here. He described Bitcoin as “the only asset” offering digital scarcity, decentralization, and a predictable monetary policy at the same time.

In periods of geopolitical tension and economic volatility, those qualities attract serious capital. Investors seeking certainty are finding fewer alternatives outside of Bitcoin.

He also addressed the growing intersection of artificial intelligence and crypto. Pompliano argued that AI systems will increasingly require assets like Bitcoin and stablecoins to operate, framing both industries under the broader theme of “automation.”

Crypto infrastructure, therefore, becomes a foundational layer for the emerging automation economy. Venture firm a16z has already raised a dedicated fund targeting exactly this convergence.

On surviving assets within crypto, Pompliano was direct and unambiguous. He expressed strong conviction in Bitcoin, stablecoins, equity infrastructure, and tokenization as the areas that will endure.

Most altcoins and meme coins, he argued, are unlikely to recover meaningfully. The smarter approach, in his words, is to “provide the venue” for speculation rather than being the one speculating.

While acknowledging that Bitcoin’s days of delivering 100x returns are behind it, Pompliano remains firmly bullish on its long-term performance. He expects Bitcoin to outperform equities over a sustained period.

For investors who missed the $60K entry, his message is straightforward — “the bottom,” by his assessment, is already in.

TLDR:

- Digital Asset is targeting $300M at a $2B valuation, with a16z crypto set to lead the funding round.

- Canton Network has processed over $6 trillion in tokenized assets, drawing major institutional backers globally.

- A16z crypto raised $2.2B for its fifth fund, bringing total dedicated crypto capital to roughly $10 billion.

- Crypto venture deal counts dropped sharply to 97 in Q1 2026, down from 427 in the same quarter last year.

Digital Asset Holdings, the company behind the Canton Network blockchain, is in talks to raise approximately $300 million at a valuation of around $2 billion.

Bloomberg reported the round on Sunday, citing sources familiar with the matter. The financing, led by a16z crypto, is expected to close within weeks. Final figures could still shift before the deal is sealed.

a16z Crypto Takes the Lead in Major Institutional Blockchain Bet

The raise marks a sharp jump from Digital Asset’s earlier funding rounds. In June 2025, the company secured $135 million led by DRW Venture Capital and Tradeweb Markets. Goldman Sachs, Citadel Securities, and DTCC also participated in that round.

A follow-on raise of $50 million came in December 2025 from BNY Mellon, Nasdaq, S&P Global, and iCapital. The new $300 million round would therefore represent a substantial step up in both size and valuation.

For a16z crypto, the investment follows the firm raising $2.2 billion for its fifth dedicated crypto fund. That brings the firm’s total crypto capital to roughly $10 billion across five vehicles.

A16z general partner Ali Yahya addressed the privacy question directly in January, writing that privacy is “the critical missing feature preventing global finance from fully moving onchain.”

That view aligns directly with what Canton Network offers. Unlike Ethereum or Solana, Canton is built with protocol-level privacy and confidentiality guarantees. Those features are central to its pitch for institutional adoption.

Canton Network Gains Traction Across Institutional Finance

Canton is a public, permissionless Layer 1 blockchain with configurable privacy tools. It supports smart contracts written in Digital Asset’s open-source language, Daml.

The network is designed to handle tokenized asset workflows while keeping transaction data confidential between parties.

Institutional momentum has been building steadily. More than $6 trillion in tokenized assets have been issued or processed on the network. In March, Visa became a Canton Super Validator, marking the payments company’s first blockchain governance role.

Visa later added Canton to its stablecoin settlement pilot in April, alongside Base, Polygon, Arc, and Tempo. Also in March, a project called Zenith completed atomic swaps between Canton and an EVM-compatible environment, opening a potential bridge to Ethereum developers.

In November, Canton Strategic Holdings raised $540 million to build a Canton Coin treasury. Backers included DRW, ARK Invest, and Kraken. The broader venture picture, however, remains uneven.

Quarterly crypto deal counts fell to 97 in Q1 2026, down from 427 in the same period a year earlier, per The Block. Some historically active crypto funds are increasingly shifting focus toward AI and robotics.

Michael Saylor, co-founder of Strategy, signaled that the Bitcoin treasury company will resume its BTC purchases this week, following an earnings call on Tuesday, during which he said the company may periodically sell portions of its treasury.

“Back to work, BTC,” Saylor said in an X post on Sunday, messaging that has previously preceded a BTC purchase, which typically the day after his posts.

The company last purchased BTC on April 27, buying 3,273 coins for about $255 million, which brought its total holdings to 818,334 BTC. Those holdings were worth about $61.8 billion, according to Strategy’s website at the time of publication.

Strategy’s history of Bitcoin purchases since 2020. Source: SaylorTracker.com

The company paused its BTC buying streak for one week ahead of Tuesday’s first quarter 2026 earnings call, in which Saylor said that the company could sell portions of its Bitcoin holdings periodically to pay dividends to holders of its credit instruments.

The announcement appeared to contradict the company’s previous stance of never selling BTC, and the sales could weigh on Bitcoin’s market price by introducing new selling pressure, critics of the move say.

Related: Bitcoin’s recent rally is largely fueled by Strategy purchases: Bitwise’s Hougan

Strategy CEO says dividend-funding sale could “inoculate” the market

“We’ll probably sell some Bitcoin to fund a dividend, just to inoculate the market, just to send the message that we did it,” Saylor said during Strategy’s Q1 earnings call.

The announcement drew mixed reactions from the Bitcoin community, with some, like Strategy investor Adam Livingston, arguing that periodic sales will be accretive for the company’s treasury, allowing it to finance the purchase of more BTC in the future.

Strategy’s Bitcoin per share since 2020, measured in sats, the base unit of Bitcoin. Source: SaylorTracker.com

Bitcoin advocate Samson Mow said Strategy’s ability to sell BTC gives it optionality and greater room to maneuver in the financial markets.

Others social media sentiment posited that Strategy’s Bitcoin sales and credit instruments will create a “doom loop” that suppresses the spot market price of BTC.

Strategy CEO Phong Le clarified that the company would only sell BTC in specific instances, including paying dividend yields and deferring taxes, and that neither its sales nor purchases should affect Bitcoin’s market price.

Bitcoin’s average daily trading volume of more than $60 billion could easily absorb Strategy’s $1.5 billion in annual dividend payments owed to holders of its corporate credit products, he said.

“I don’t think we’re driving the price up or down,” Le told CNBC, adding that the company owns about 4% of the total BTC supply.

Magazine: Big Questions: Can Bitcoin save you from the dreaded Cantillon Effect?

Crypto World

Bitcoin’s Realized Cap Turns Positive, Signaling Fresh Capital Inflows After February Slump

TLDR:

-

- Bitcoin’s realized cap monthly growth has returned to +0.25%, ending a steep -2.6% decline recorded in February 2025.

- The February correction triggered realized losses as investors who bought BTC at higher prices exited their positions.

- The downturn reflected a weak-to-strong hands transfer, with patient buyers absorbing supply from loss-realizing sellers.

- Analysts now watch whether rising profit-taking will slow recovery or if fresh demand will sustain the positive cap trend.

- Bitcoin’s realized cap monthly growth has returned to +0.25%, ending a steep -2.6% decline recorded in February 2025.

Bitcoin’s realized cap has moved back into positive monthly growth, posting a gain of +0.25% after a steep decline.

This shift follows a difficult correction period that pushed the metric to -2.6% in February. The realized cap tracks the difference between realized profits and realized losses in the market.

It is considered one of the clearest measures of capital movement. Analysts are now watching closely to see whether the trend can hold as market conditions improve.

Realized Cap Drop Reflected Investor Losses During Correction

The February decline in Bitcoin’s realized cap came as investors sold holdings at a loss. Many of those investors had purchased BTC at higher price levels earlier in the cycle. As selling pressure grew, the realized cap pulled back sharply, reflecting capital destruction in the market.

Crypto analyst Darkfost explained the pattern on X, noting that the realized cap measures “the difference between realized profits and realized losses.” During the downturn, this balance tilted heavily toward losses. That shift dragged the monthly growth rate deep into negative territory.

The correction phase also produced a shift in ownership. Investors unwilling to absorb further losses exited their positions and transferred holdings to buyers at lower prices.

This process is commonly referred to as a transfer from weak hands to strong hands. It is a pattern that has appeared in previous Bitcoin market cycles.

Even so, overall sentiment during the correction remained cautious. New capital did not immediately return to the market after prices fell. Buyers waited for valuations to reach levels they considered attractive before committing fresh funds to Bitcoin.

Positive Shift Suggests New Capital Is Returning to Bitcoin

Now that the realized cap has turned positive again, the market dynamic appears to be changing. According to Darkfost, “investor sentiment is improving as capital begins flowing back into the market.”

That change is reflected in the monthly growth figure moving above zero for the first time since the downturn.

The +0.25% reading is modest on its own. However, coming directly after a -2.6% monthly decline, it carries weight as a directional shift. Analysts tend to look at this kind of recovery as an early sign that buyers are returning with confidence.

Capital inflows at this stage often reflect improved sentiment among both retail and institutional participants. When new money enters the market, it tends to push realized profits higher. That, in turn, supports further growth in the realized cap over subsequent months.

The central question, as Darkfost noted, is whether this recovery can continue as more investors take profits. If selling pressure increases alongside rising prices, the growth rate could stall again. However, if demand absorbs that supply, the realized cap is likely to continue its upward trend.

Ethereum’s native token, Ether (ETH), has dropped more than 35% versus Bitcoin (BTC) over the last 12 months, a slide that market observers say could have further to run if technical and on-chain signals play out. The underperformance comes as Bitcoin continues to attract corporate interest and mainstream adoption, while Ethereum faces a mix of liquidity and momentum headwinds that have tempered its rally narratives.

Key takeaways:

- ETH/BTC remains trapped below a multi-year descending trend line that has capped breakouts since 2022, with a potential 40% downside target toward 0.0176 BTC if the weakness persists into 2026.

- Binance ETH reserves climbed to 3.62 million ETH as of May, about 24.6% of all Ether held on exchanges, signaling higher near-term selling risk, according to CryptoQuant data.

- Bitcoin reserves on Binance have fallen, highlighting divergent exchange liquidity trends between the two assets.

- The broader market narrative, including Ethereum’s lingering “ultrasound money” momentum and BTC’s growing institutional interest, continues to shape relative performance and risk sentiment.

ETH-BTC: technical setup points to extended weakness

ETH/BTC has remained entrenched beneath a long-standing descending trend line that has constrained every major breakout since 2022. The pattern mirrors a similar setup that preceded the steep drop from late 2024 into 2025, suggesting the same structural pressure could reassert itself if BTC and ETH fail to find fresh demand.

In August 2025, ETH/BTC briefly retested the trend line, only to be repelled at a convergence zone that included the 0.382 Fibonacci retracement and the 50-month exponential moving average. Since then, the pair slid back below the 20-month moving average, which now acts as a resistance-turned-signal of selling pressure around the 0.034 BTC level.

The chart implies a potential objective around 0.0176 BTC if selling continues, a level that would represent roughly a 40% decline from recent prices and aligns with the 2020 cycle bottom. Traders watching the eth/btc ladder see this as a crucial test of whether Ether can regain tempo or if Bitcoin’s uptrend remains the dominant driver of market risk appetite.

On-chain and exchange signals paint a mixed liquidity picture

On-chain data from CryptoQuant highlights a notable divergence in exchange balances between ETH and BTC. Ether reserves on Binance—the world’s largest crypto exchange by volume—have risen to 3.62 million ETH as of May, accounting for about 24.6% of all Ether held on crypto exchanges. This increase in available ETH suggests more supply could be poised for sale if buyers do not absorb it in the current market environment.

In contrast, Bitcoin reserves on Binance have fallen, signaling tighter exchange-side liquidity for BTC. The opposite dynamics—rising ETH supply versus diminishing BTC supply on exchanges—help explain, at least in part, the ongoing divergences in price action between the two assets.

Higher exchange balances for ETH often translate into greater near-term selling pressure, especially when demand lacks the vigor to match supply. By contrast, shrinking BTC reserves can reflect a combination of hodling behavior and a rotation of liquidity away from centralized venues, which can give BTC a relative edge when risk sentiment shifts.

These reserve patterns add a practical dimension to the broader narrative: Ether appears more exposed to potential supply-driven downside on exchange rails, while Bitcoin benefits from tighter liquidity and, in some cases, a stronger bid from institutional participants stepping into the market.

Narrative tensions and market context: where the momentum sits

Beyond the charts and on-chain metrics, the fundamental backdrop for Ether remains a topic of debate. For years, Ether’s “ultrasound money” narrative — the idea of a deflationary or steadily scarce asset embedded in Ethereum’s monetary dynamics — helped frame ETH as a better long-term store of value relative to fiat or even BTC in some cycles. However, that narrative has cooled in recent periods, contributing to a prolonged period of lag versus Bitcoin on a relative performance basis.

Bitcoin, meanwhile, has benefited from growing corporate engagement and wider adoption into traditional portfolios. Market observers have pointed to evidence of corporate accumulation and strategic participation by institutions as a tailwind for BTC’s price resilience. Notably, retail and institutional access to spot BTC trading, including upcoming offerings and integration into mainstream platforms, continues to shape the adoption trajectory for BTC more than ETH in several market segments.

Recent coverage underscores this asymmetry: corporate players have shown sustained interest in BTC, while Ethereum’s growth narrative has faced headwinds that temper a broad-based upside versus BTC. In parallel, developments such as retail access expansions for spot BTC and ETH trading — including moves from traditional financial firms into crypto markets — remain in focus for readers watching how the market prices risk, liquidity, and opportunity across the digital asset spectrum.

Related commentary has explored how these dynamic shifts could influence capex decisions for developers, liquidity provisioning for exchanges, and the pace of adoption on Layer 2s and decentralized finance ecosystems. As the market absorbs these cross-currents, traders may look for catalysts that could tilt the balance—ranging from further macro normalization to concrete progress on Ethereum’s scaling roadmap and the evolution of centralized exchange liquidity pools.

On balance, the ETH-BTC relationship continues to hinge on a mix of technical barriers, on-chain liquidity signals, and the evolving narrative around what each asset represents to investors and users in different market regimes. While BTC’s path remains susceptible to institutional demand and liquidity dynamics, Ether’s fate will likely be decided by how supply pressure on exchanges interacts with network upgrades, layer-2 maturation, and the broader pace of Ethereum’s ecosystem development.

Readers should watch whether ETH can push through the established trend line, or if the combination of rising ETH supply on major exchanges and continued resistance around key moving averages keeps the pair under pressure. The next price pivot around 0.0176 BTC would not only mark a technical breakpoint but also signal whether Ether can reassert a case for value relative to BTC in the face of shifting liquidity and narrative forces.

The data underpinning these observations draw from CryptoQuant’s exchange-flow analytics, with ETH reserve figures specifically cited for Binance as of May. For anyone tracking the liquidity landscape, these metrics provide a practical lens into where risk might be concentrated in the near term and how institutional and retail behavior could shape the next leg of the crypto cycle.

What unfolds next could hinge on how much buy-side demand returns to ETH in the face of a higher supply ceiling on exchanges and whether BTC’s liquidity backdrop remains supportive as institutional participation continues to expand. Keep an eye on reserve trends, price action around the critical trend line, and any regulatory or product developments that could tilt market sentiment in the coming weeks and months.

Pump.fun traders, after a long stretch of weak performance, are beginning to see a clear turnaround in 2026, according to fresh data from CoinGecko.

Between April 2024 and late 2025, most traders exiting positions on the popular Solana-based meme coin platform ended each month with losses. During this period, the share of profitable wallets rarely crossed the 50% mark and fell as low as 30.1% in June 2025, amid significant underperformance among active participants.

Pump.fun Profitability Improves

The trend began to reverse in early 2026. In February, Pump.fun recorded almost 57% of traders in profit, followed by a sharp rise to 70% in March and 73.3% in April 2026. In April 2026, profits were heavily concentrated at the lower end of the spectrum.

CoinGecko found that the largest cohort, about 2.05 million wallets or 65.1%, earned between $1 and $500. Another 87,000 wallets, or 2.8%, made between $500 and $1,000, while 169,000 wallets, representing 5.4%, booked gains above $1,000.

On the loss side, 793,000 wallets, or around 25%, lost between $1 and $500, while 22,000 wallets (0.7%) lost $500 to $1,000, and 24,000 wallets (0.8%) saw losses of more than $1,000. The data indicated that both gains and losses are largely clustered in small amounts, which “reflects the small-size, high-frequency nature of memecoin trading, where participants typically deploy small amounts of capital.”

The report also noted that the improvement in profitability may be tied to a shakeout of weaker participants, as monthly active wallets fell from a peak of 5.2 million in May 2025 to 1.8 million in December 2025. The subsequent recovery in early 2026 points to a smaller but potentially more experienced trader base returning to the platform.

“This decline can be seen as the exit of the broader retail crowd and subsequent recovery in wallet counts from early 2026 onward implies the return of a more selective, experienced trader base, naturally shifting the profitability distribution in their favour.”

Token Policy Change

Last week, Pump.fun announced it had burned all previously repurchased PUMP tokens and introduced a new buyback-and-burn program funded by 50% of future net revenue. The project said the burned tokens were worth about $370 million and represented 36% of the circulating supply.

It added that, facing trust issues over the longevity of its business, the certainty of buybacks, and how repurchased tokens would be used. According to Pump.fun, the move was meant to address uncertainty through a community-first approach going forward.

The post Solana-Based Meme Coin Launchpad Pump.fun Traders See Turnaround in 2026: CoinGecko appeared first on CryptoPotato.

Bitcoin, Ripple’s token, Solana’s SOL, and several other altcoins made impressive moves over the past few hours, which was rather unexpected given the Sunday market sentiment and lack of major developments.

Interestingly, these recent gains coincided with Donald Trump’s latest message on Iran.

The statement on Truth Social from the POTUS reads that Iran has been “playing games with the United States, and the rest of the World, for 47 years.” He also placed significant blame on former President Barack Obama, saying the situation hit “pay dirt” during his time in office.

“He was not only good to them, he was great, actually going to their side, jettisoning Israel, and all other Allies, and giving Iran a major and very powerful new lease on life. Hundreds of Billions of Dollars, and 1.7 Billion Dollars in green cash, flown into Tehran, was handed to them on a silver platter. Every Bank in D.C., Virginia, and Maryland was emptied out — It was so much money that when it arrived, the Iranian Thugs had no idea what to do with it. They had never seen money like this, and never will again. It was taken off the plane in suitcases and satchels, and the Iranians couldn’t believe their luck.”

After also blaming Joe Biden, Trump said Iran will be laughing no longer at the USA. This statement comes after reports that Iran had sent their response to the US’s latest peace proposal. However, there’s no further information as of press time regarding the actual decision.

As mentioned above, many crypto assets are in the green now. Bitcoin’s gains are among the most modest, but the asset still tapped $81,600. XRP has stolen the show from the larger-cap alts, surging by over 5% daily to a multi-week peak of just over $1.50.

SOL has risen to almost $100 after a 3.5% daily increase, ETH is well above $2,350, and ADA has gained over 5% to sit close to $0.29.

The post BTC, XRP on the Move Amid Trump’s Latest Message on Iran: Details appeared first on CryptoPotato.

XRP is trading in the $1.40 range, as on-chain data paints a picture that looks worse than the news headlines are saying. New daily addresses on the XRP Ledger have collapsed by over 80% from 18,000 in December 2024 to just 2,700. Yet institutions are quietly settling tokenized assets on public blockchains in real time.

. @Ripple network activity continues slowing down! — CryptoBusy (@CryptoBusy) May 8, 2026

New wallet creation dropped from 18,000 per day in December 2024 to around 2,700 today.

Active $XRP supply also declined sharply during the same period. pic.twitter.com/hkOGsMmUXL

According to Glassnode data, monthly active supply dropped more than 70% from 7.45 billion XRP to roughly 2 billion XRP. Exchange reserves simultaneously hit historic lows at 12.9 billion XRP, suggesting holders are moving coins to self-custody and not to sell.

Whales have also accumulated 110 million tokens through March, even as retail participation faded. “The network is shifting from retail speculation only to institutional rails,” RedStone co-founder Marcin Kazmierczak notes. “That transition rarely looks pretty in the address chart.”

With institutional XRP interest accelerating, the market is sending mixed signals.

Discover: The best crypto to diversify your portfolio with

Can XRP Price Recover to $1.50 With Institutional News?

XRP stabilized between $1.38 and $1.42 over the past 48 hours after a bounce from $1.38 to a high of $1.45. The volume surge is the only genuinely bullish data point on the board right now. Everything else is neutral-to-soft.

RSI, MACD, Stochastic, and CCI are all sitting at neutral readings. Analysts note that “thin participation means rebounds lack follow-through,” which is precisely the problem when network payments risk falling below the 500 million threshold that has historically anchored baseline demand.

Right now, resistance still sits at $1.45; XRP has been grinding against that top without a clean break.

The volume spike is encouraging, but sustained spot demand is what confirms institutional accumulation is absorbing sell pressure.

Discover: The best pre-launch token sales

Bitcoin Hyper Presale With More Upside Potential

XRP’s current setup offers limited asymmetric upside at a $80B+ market cap. For XRP, a clean double requires institutional inflows at scale that may take years, not weeks. Traders hunting for higher-beta exposure are rotating attention toward earlier-stage infrastructure plays where the entry price hasn’t already priced in the thesis.

Bitcoin Hyper ($HYPER) is positioning as the first-ever Bitcoin Layer 2 with Solana Virtual Machine (SVM) integration, delivering sub-second finality and low-cost smart contract execution on top of Bitcoin’s security layer.

The project targets Bitcoin’s core bottlenecks directly: slow transactions, high fees, and zero programmability. Its Decentralized Canonical Bridge enables seamless BTC transfers into the fast-execution environment without sacrificing custody trust.

The presale has raised more than $32.6 million at a current price of just a mere $0.0136, with staking rewards already live for early participants. The presale momentum has been building steadily as Bitcoin infrastructure narratives gain traction.

Research Bitcoin Hyper before the presale phase concludes.

The post XRP News: Institutional Adoption Accelerates, Network Activity At Lowest appeared first on Cryptonews.

26 pictures of classic to modern motor show at Croft Circuit

Artivion, Inc. (AORT) Q1 2026 Earnings Call Transcript

How to watch Round 4

Manchester United reach agreement with Casemiro over contract clause amid transfer speculation

US brings back mandatory military draft registration

Steven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Crypto World2 days ago

Crypto World2 days agoHarrisX Poll Found 52% of Registered Voters Support the CLARITY Act

-

Crypto World3 days ago

Crypto World3 days agoUpbit adds B3 Korean won pair as Base token gains Korea access

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Marianne Dress

-

Tech6 days ago

Tech6 days agoImage AI models now drive app growth, beating chatbot upgrades

-

NewsBeat4 days ago

NewsBeat4 days agoNCP car park operator enters administration putting 340 UK sites at risk of closure

-

Business1 day ago

Business1 day agoIgnore market noise, India’s long-term story intact, say D-Street bulls Ramesh Damani and Sunil Singhania

-

Politics2 days ago

Politics2 days agoPolitics Home Article | Starmer Enters The Danger Zone

-

Entertainment7 days ago

Entertainment7 days agoOlivia Wilde Reacts To Viral ‘Corpse’ Comparison

-

Sports7 days ago

Sports7 days agoInter Milan Win Serie A Title After Victory Over Parma

-

Sports7 days ago

Sports7 days agoLa Liga: Vinicius Jr scores twice as Real Madrid win to keep Barcelona waiting for title

-

Crypto World5 days ago

Crypto World5 days agoUAE Free Zone Deploys Blockchain IDs to Verify Registered Firms

-

Sports7 days ago

Sports7 days agoEvery word of Arne Slot’s heated rant after Manchester United win vs Liverpool

-

Sports7 days ago

Sports7 days agoJoel Embiid urges Sixers fans not to sell playoff tickets to Knicks fans

-

Sports6 days ago

Sports6 days ago2026 NHL playoff picks: Second-round predictions, series odds, Stanley Cup bracket

-

Entertainment7 days ago

Jennifer Lawrence’s Mary Jane Sneakers Are Spring’s It-Girl Shoe

-

Entertainment7 days ago

Entertainment7 days agoMoroccan Reacts To Nick Cannon’s Dating Rules For His Sister

-

Crypto World4 days ago

Crypto World4 days agoBlackRock CEO Larry Fink Discusses a New Asset Class

-

Crypto World4 days ago

Crypto World4 days agoRobinhood says Wall Street is building onchain

-

Entertainment7 days ago

Entertainment7 days agoKylie Jenner and Timothee Chalamet Hold Hands in NYC Outing

-

Entertainment7 days ago

Entertainment7 days agoPost Malone Delays Tour With Jelly Roll Amid Ongoing Backlash

You must be logged in to post a comment Login