Crypto World

Did the WBTC DAO approve Justin Sun’s HTX as a merchant?

Wrapped Bitcoin (WBTC) spent years marketing itself as being governed by decentralized autonomous organizations (DAOs) that would have oversight over many parts of the product, including “the addition and removal of merchants and custodians.”

Its whitepaper claimed that “signatures are required from DAO members in order to add/remove members.”

Even as recently as a few months ago, WBTC has continued to emphasize that it “operates through a DAO.”

However, this supposed role of the WBTC DAO hasn’t always been respected.

HTX, formerly Huobi, was added as a merchant, the product’s term for an entity who can initiate mints and burns of WBTC, however, it was not approved by the DAO members listed on the Github, but a different set of signers from a different multisignature wallet.

A review of the smart contract reveals that 0xbE6d2444a717767544a8b0Ba77833AA6519D81cD is one of the merchants returned by the “getMerchants” function.

Read more: Is HTX redeeming 80% of TrueUSD?

This address was listed as HTX on the WBTC dashboard in late 2024 when Protos reported on it being used to redeem approximately half a billion dollars worth of WBTC.

However, this address isn’t listed as one of the merchants on the WBTC DAO GitHub page.

HTX is listed as one of the merchants on the WBTC website.

The entities that are still listed on GitHub include defunct and fraudulent entities such as Alameda Research and Three Arrows Capital, both of which are also still listed on the smart contract.

By further reviewing blockchain transactions on Ethereum, we can identify that this address was added as a merchant in November 2024, approximately two months after BiT Global and Justin Sun got involved in WBTC.

Read more: WBTC relaunches on TRON, but abandoned version is bigger

At the time, this transaction came from 0x4dbbbFb0e68bE9D8F5a377A4654604a62E851e80.

Strangely, this address isn’t listed as one of the multisignature wallets for WBTC on GitHub.

The listed multisignature wallet doesn’t include any transactions for the day when HTX was added as a merchant.

The inclusion of HTX as a merchant becomes increasingly important in light of some of the problematic behaviors that the exchange is engaged in.

Read more: Justin Sun defends HTX while it lends 92% of its USDT on Aave

It appears the publicly disclosed multisignature wallet, 0xB33f8879d4608711cEBb623F293F8Da13B8A37c5, appears to have been quietly replaced with a brand new multisignature wallet.

The wallet that was used lists several owners, many of whom differ from the WBTC DAO Github:

- 0xFDF28Bf25779ED4cA74e958d54653260af604C20 — Listed as Kyber on the Merchants list on the GitHub, isn’t listed as a DAO member.

- 0xb0F42D187145911C2aD1755831aDeD125619bd27 — Listed as BitGo on the custodian part of the GitHub, isn’t listed as a DAO member on the current GitHub commit, is listed as a small DAO member on a pull request.

- 0xd5d4aB76e8F22a0FdCeF8F483cC794a74A1a928e — Not listed on the current GitHub commit, is mentioned in a pull request as Maker.

- 0xB9062896ec3A615a4e4444DF183F0531a77218AE — Listed as Aave on the Merchants list on the GitHub, is not listed as a DAO member on the current commit, and is mentioned as a small DAO member on a pull request.

- 0xddD5105b94A647eEa6776B5A63e37D81eAE3566F — Not listed on the current GitHub commit, is listed on a pull request as Tom Bean and is listed as a small DAO member there, multisignature wallet that includes:

- 0x97788A242B6A9B1C4Cb103e8947df03801829BE4 — Not listed on the GitHub at all.

- 0x59150a3d034B435327C1A95A116C80F3bE2e4B5E — Not listed on the GitHub at all.

- 0x926314B7c2d36871eaf60Afa3D7E8ffc0f4F9A80 — Not listed on the current GitHub commit, appears to be a multisignature wallet created using BitGo’s technology, and is listed as BitGo 2 on a pull request describing it as a member of the small DAO.

- 0x51c44979eA04256f678552BE65FAf67f808b3EC0 — Not listed on the current GitHub commit, appears to be another multisignature wallet created using BitGo’s technology, is listed as BitGo 3 on a pull request describing it as a member of the small DAO.

- 0x0940c5bcAAe6e9Fbd22e869c2a3cD7A21604ED8D — Not listed on the GitHub at all.

- 0x5DCb2Cc68F4b975E1E2b77E723126a9f560F08E8 — Not listed on the GitHub at all.

It is not clear why these changes aren’t reflected on the current version of the GitHub repository. Protos reached out to WBTC for some clarification, but it didn’t respond before publication.

By further reviewing the smart contract at 0x4dbbbFb0e68bE9D8F5a377A4654604a62E851e80, we can identify the five addresses that approved the listing of HTX:

- 0xFDF28Bf25779ED4cA74e958d54653260af604C20 — Kyber

- 0xb0F42D187145911C2aD1755831aDeD125619bd27 — BitGo

- 0xddD5105b94A647eEa6776B5A63e37D81eAE3566F — Tom Bean

- 0x926314B7c2d36871eaf60Afa3D7E8ffc0f4F9A80 — BitGo

- 0x51c44979eA04256f678552BE65FAf67f808b3EC0 — BitGo

This means that although this multisignature wallet requires five signatures, three of them came from the same entity.

Only two non-custodian entities approved the addition of HTX as a merchant and those aren’t currently listed as DAO members on GitHub.

Adding to the intrigue, Tom Bean’s project, bZx, was built on Kyber.

It’s also worth highlighting the fact that this multisignature wallet requires five signatures, BitGo controls three, and there are two addresses that aren’t listed at all on GitHub.

If those are controlled by BitGo or BiT Global, then it would be possible for the custodians to make changes without approval from a single additional WBTC DAO member.

Protos reached out to WBTC to determine the identity of those two addresses, but again, didn’t get a response before publication.

BiT Global was added without WBTC DAO approval

This isn’t the first time that WBTC has appeared to ignore the advertised role of its DAO.

The whitepaper for WBTC claimed that “addition/removal of custodians” would be controlled by this DAO.

This used to be echoed on the website, which claimed, “The addition and removal of merchants and custodians will be an open process controlled by a multi-signature contract.”

Read more: Coinbase to delist WBTC months after Justin Sun controversy

Mike Belshe, the chief executive of BitGo, also claimed when BiT Global was being installed that there was a large DAO that “owns the smart contract” and “picks, you know, how we do custody of this thing.”

Strangely, despite that claim, the WBTC DAO didn’t seem to be consulted on the addition of Sun-affiliated BiT Global as a custodian for WBTC.

The Github for the WBTC DAO still doesn’t list BiT Global as a custodian.

The website for WBTC does list BiT Global as one of the custodians, alongside BitGo and BitGo Singapore.

The “members” smart contract still only lists a single custodian, 0xb0F42D187145911C2aD1755831aDeD125619bd27, a BitGo address.

This address is a multi-signature, so it’s possible that BiT Global was added as a signer to this wallet, meaning that the smart contract did not need to be updated with a new custodian address.

Broadly, despite the fact that WBTC manages over $8 billion in value, it seems to have neglected and ignored the DAO that has frequently been an important part of its marketing.

It’s replaced the multisignature wallet that governs it, without updates, with members whose identity we do not know.

This replacement made it possible, or convenient, for HTX to be added as a merchant, but other problems have been ignored, such as the fact that both Alameda Research and Three Arrows Capital are included as merchants.

The large DAO was apparently bypassed regarding the addition of BiT Global.

However it is that WBTC operates, it’s not principally through its DAO.

Its claims of transparency and decentralization have been dashed against the difficulty of coordinating a variety of actors around the world.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

In today’s newsletter, Claudia Marcela Hernández analyzes how stablecoins have evolved past volatility-fixers to become the foundational settlement asset for global tokenized markets and cross-border payments, following the clarity provided by the GENIUS Act.

Then, in Ask an Expert, Morva Rohani breaks down how stablecoin regulation serves as a foundation for tokenized capital markets, why some jurisdictions see U.S. stablecoin policy as a risk, and the key factors advisors must use to assess a stablecoin’s credibility.

Learn about the latest advancements in the Clarity Act in Keep Reading.

Happy Reading.

Are stablecoins the infrastructure reshaping global finance?

Stablecoins were originally designed to solve one of crypto’s earliest problems: volatility. By pegging their value to fiat currencies such as the U.S. dollar, stablecoins gave traders a reliable unit of account that could move across blockchains without the price swings associated with assets like bitcoin. For years, they functioned primarily as liquidity tools inside crypto markets. But that role is rapidly changing.

Stablecoins are evolving from niche trading instruments into a foundational layer of global financial infrastructure. They now serve as settlement assets in decentralized finance (DeFi), payment rails for cross-border transfers and the preferred settlement currency for tokenized financial markets.

Institutions that once approached crypto cautiously are beginning to acknowledge the technology’s potential. The International Monetary Fund (IMF) has noted that stablecoins could improve the efficiency of cross-border payments by reducing the number of intermediaries involved in global transactions. Meanwhile, policymakers in the United States are moving to integrate stablecoins into the regulated financial system.

Because most of these tokens are pegged to the U.S. dollar, they may also be doing something far more consequential: quietly extending the reach of the dollar across the blockchain-based global economy.

How a Stablecoin Is Issued and why they matter?

A user provides fiat currency, typically U.S. dollars, to a licensed issuer. In return, the issuer mints an equivalent amount of stablecoins on a blockchain, maintaining a 1:1 peg. The fiat received is placed into reserve accounts, usually held in cash or short-term U.S. Treasuries, which back the value of the tokens in circulation.

When a user wants to exit, the process works in reverse: the stablecoins are redeemed, and the user receives fiat from the reserves. This issuance-redemption mechanism is what anchors the stablecoin’s price to its reference asset.

Stablecoins enable near-instant, 24/7 settlement, independent of banking hours. They allow for programmable transactions, where payments can be automated and embedded into digital systems. And they provide access to dollar-denominated value, often without requiring a traditional bank account.

The World Economic Forum established that stablecoins transaction volumes have reached tens of trillions of dollars annually, underscoring their growing role as a core component of digital financial activity.

For policymakers, this presents both an opportunity and a challenge. The U.S. Treasury has noted that digital payment innovations, including stablecoins, can enhance efficiency, reduce costs and promote financial inclusion, provided that appropriate safeguards are in place.

Use cases and applications

· Cross-border payments: Stablecoins enable near-instant international transfers at a fraction of the cost of traditional correspondent banking systems.

· Remittances: In many emerging markets, stablecoins offer faster and cheaper alternatives to traditional remittance providers, which often charge significant fees.

· Decentralized finance (DeFi): Stablecoins serve as collateral, liquidity pools and settlement assets across lending protocols, decentralized exchanges and derivatives markets.

· Tokenized real-world assets: As tokenization expands to include bonds, real estate and commodities, stablecoins increasingly function as the settlement currency for digital financial markets.

· Corporate treasury and global settlement: Fintech companies and multinational firms are experimenting with stablecoins to facilitate cross-border treasury operations and instant settlement of international transactions.

In short, stablecoins are gradually becoming the base layer of digital financial activity.

The Regulatory Turning Point: The GENIUS Act

The transition of stablecoins from niche crypto instruments to recognized financial infrastructure accelerated significantly in 2025 with the passage of the GENIUS Act (the Guiding and Establishing National Innovation for U.S. Stablecoins Act in the United States).

The legislation created the first comprehensive federal framework governing the issuance of payment stablecoins. Under the law, regulated entities, including banks and approved non-bank financial institutions, are allowed to issue stablecoins backed by high-quality liquid assets and subject to strict requirements including reserve transparency, regular audits, anti-money laundering and counter-terrorism financing (AML/CTF) under the Bank Secrecy Act.

One of the most important aspects of the GENIUS Act was regulatory clarity. For years, uncertainty around whether stablecoins should be treated as securities, commodities or banking products created hesitation among institutional players. The law addressed this ambiguity by establishing stablecoins as a distinct category of digital payment instruments.

Stablecoins and monetary power

Dollar-denominated stablecoins dominate the market by a wide margin compared with those linked to other currencies. That dominance has an important implication because stablecoins may extend the reach of the U.S. dollar beyond the traditional banking system.

Other jurisdictions are responding with their own regulatory strategies. For example, the European Union, through its Markets in Crypto-Assets (MiCA) framework, has introduced strict requirements for stablecoin issuers operating within the EU, including reserve requirements and limits designed to protect monetary sovereignty — but is also exploring the creation of a Central Bank Digital Currency (CBDC)

In Asia, financial hubs such as Hong Kong and Singapore are developing licensing regimes aimed at supervising stablecoin issuance and integrating the technology into regulated financial markets. China, meanwhile, has taken a different path by prioritizing the development of a central bank digital currency and exploring digital yuan settlement systems that could expand its monetary influence internationally.

The future of stablecoins will depend on trust in their reserves, in their governance and in the systems that oversee them. And ultimately, their long-term value will not be defined by how fast they scale, but by how safely and sustainably they become part of the global financial system.

– Claudia Marcela Hernández, digital assets specialist

Ask an Expert

Q. How important is stablecoin regulation to tokenized capital markets?

Stablecoin regulation is important because tokenized capital markets need a credible on-chain settlement asset. But regulation alone is not enough. For stablecoins to support institutional tokenized markets, there must also be legal certainty around settlement finality, redemption at par, issuer credit risk and how stablecoin-based settlement fits within payment system and securities laws.

In that sense, stablecoin regulation is a necessary foundation for tokenized capital markets, but not the whole framework. What institutions ultimately need is confidence that the settlement asset is reliable, that obligations are legally discharged when transactions settle on-chain and that the broader market structure can operate with clear, coordinated oversight.

Q. Are some jurisdictions starting to see U.S. stablecoin policy as a risk?

Yes, there is growing recognition that stablecoins carry geopolitical and monetary implications. Because the vast majority of fiat-backed stablecoins are denominated in U.S. dollars, their adoption could extend the reach of the dollar into blockchain-based financial systems. As U.S. policy frameworks formalize regulated dollar-backed stablecoins, this dynamic becomes more entrenched, positioning the U.S. to shape both the currency and standards of digital financial infrastructure.

In Canada, for example, proximity to the U.S., deep financial integration and broader geopolitical uncertainty have sharpened this focus. The concern is less about direct competition and more about dependency. Without a domestic framework, Canadian users and institutions could default to foreign-issued, USD-based stablecoins.

Canada’s approach has been to create a framework that enables innovation and competition while ensuring safety, consumer protection, and interoperability with global regimes. The objective is to allow both domestic and foreign stablecoins to operate under Canadian oversight, while preserving monetary relevance and ensuring Canadians have trusted, regulated options in a digital financial system.

Q. How can advisors assess whether a stablecoin is credible?

As stablecoins integrate into regulated systems, credibility comes down to a few core factors. First, reserve quality and transparency: assets should be fully backed by high-quality liquid instruments with regular disclosure or audits. Second, redemption: holders must have a clear, enforceable right to redeem at par. Third, regulatory oversight: credible issuers operate within defined legal and compliance frameworks. Governance also matters, including issuer structure, jurisdiction and custody of reserves. Ultimately, the key question is not just whether a stablecoin trades at $1, but whether its structure ensures it can consistently meet redemptions and retain user confidence during periods of stress.

– Morva Rohani, executive director, Canadian Web3 Council

Keep Reading

Bitcoin lost its grip on $70,000 amid inflation and recession talk as analysis suggested that BTC price action lacked “outright stress.”

Bitcoin (BTC) daily losses approached 3% at Thursday’s Wall Street open as markets stayed on edge over fresh Iran tensions.

Key points:

-

Bitcoin slips from $70,000 as markets continue to observe Iran developments.

-

Inflation and recession worries grow louder with no clear end to the conflict in sight.

-

Bitcoin analysis avoids an outright bearish appraisal of BTC price action.

Bitcoin wobbles as US inflation fears increase

Data from TradingView showed BTC/USD nearing $69,000 for the first time since Monday.

Volatility picked up as the US session began, with traders reacting to the latest developments in the US-Iran war.

A reported lack of mutual understanding over a peace proposal followed pressure from US President Donald Trump.

In a post on Truth Social, Trump called Iranian negotiators “very different and ‘strange.’”

“They better get serious soon, before it is too late, because once that happens, there is NO TURNING BACK, and it won’t be pretty!” he wrote.

US stocks turned red at the open, while attention also focused on the longer-term impact of the conflict on inflation.

As reported by trading resource The Kobeissi Letter and others, the Organization for Economic Co-operation and Development (OECD) put US inflation at 4.2% in 2026 — the highest among G7 countries.

“Potential rate HIKES in the US and EU are now back on the table,” it responded on X, referring to central banks raising interest rates — a key headwind for crypto.

Earlier, Cointelegraph reported on increasing expectations that the US would enter a recession within the next 12 months.

Analysis: BTC price action “not obviously bearish”

With Bitcoin still wedged in a narrow range, trading company QCP Capital stressed its “resilience” within the overall macro landscape.

Related: Bitcoin ‘compression’ outcome may send BTC to $80K: Analyst

“BTC is hovering around $70k, and the price action still feels more like quiet consolidation than outright stress,” it summarized in its latest “Market Color” analysis on the day.

“The broader macro backdrop remains fragile, with risk sentiment weighed by renewed Middle East headlines and oil still carrying a meaningful geopolitical premium, even after pulling back from the week’s highs.”

QCP described Bitcoin’s price activity as “not obviously bearish.”

“For now, BTC is trading like an asset being accumulated on dips but not yet chased. The range is holding, the surface is defensive but orderly, and macro remains firmly in the driver’s seat,” it added.

As Cointelegraph continues to report, many traders remain highly risk-averse to BTC, expecting new macro lows to result from an eventual range breakdown.

This article does not contain investment advice or recommendations. Every investment and trading move involves risk, and readers should conduct their own research when making a decision. While we strive to provide accurate and timely information, Cointelegraph does not guarantee the accuracy, completeness, or reliability of any information in this article. This article may contain forward-looking statements that are subject to risks and uncertainties. Cointelegraph will not be liable for any loss or damage arising from your reliance on this information.

Key Takeaways

- Adobe (ADBE) lost its Outperform rating from William Blair, downgraded to Market Perform this Thursday

- Analyst Arjun Bhatia pointed to “intense competition” pressuring Adobe’s flagship Creative Cloud offerings

- Competitors like Canva (achieving $4B ARR with +30% growth) and Figma (hitting $1.2B ARR with +40% expansion) are encroaching on Adobe’s $19B Digital Media business

- Artificial intelligence has rapidly “democratized” creative capabilities, putting Adobe’s professional user segment at risk

- While not labeling Adobe an “AI loser,” William Blair expects the stock to remain range-bound near term

On Thursday, William Blair stripped Adobe of its Outperform designation, lowering the rating to Market Perform. Analyst Arjun Bhatia’s rationale revolves around a singular anxiety: the protective moat surrounding Adobe’s Creative Cloud franchise appears to be eroding.

Bhatia recognized that Adobe’s valuation appears attractive at merely nine times free cash flow. Yet an inexpensive price tag doesn’t guarantee security. His apprehension isn’t rooted in valuation metrics — it’s about whether Adobe can defend its territory.

The analyst’s report stated it directly: “intense competition” represents the central challenge. And the threats are emerging from every angle.

Artificial intelligence platforms have advanced rapidly. In Bhatia’s assessment, they have “overnight, democratized the highly technical skills creative professionals had built.” This represents a direct assault on Adobe’s primary customer segment — the professionals whose livelihoods depend on mastering its complex software suite.

Canva has reached $4 billion in annual recurring revenue, expanding beyond 30% year-over-year. Figma — Adobe’s failed acquisition target — currently generates $1.2 billion in ARR while posting 40% growth. Adobe’s Digital Media division operates at a $19 billion annual run rate, yet these rivals are narrowing the gap considerably.

Canva has systematically captured market share at the entry level. Figma has dominated the UI/UX design category. Both companies are advancing from the periphery, and those boundaries are dissolving.

New AI-First Competitors Intensify Challenges

The competitive pressure extends further. Midjourney, Runway, Synthesia, and StabilityAI represent a generation of AI-first entrants transforming the creative software landscape. These aren’t traditional software vendors adapting to AI — they were architected around artificial intelligence from inception.

Beyond these startups, Google, OpenAI, and Apple are each advancing into creative tooling through distinct strategies. The competitive environment Adobe confronts today bears little resemblance to what existed just 24 months ago.

Bhatia deliberately avoided hyperbole. “We are not calling Adobe an ‘AI loser,’” his report stated. However, too many uncertainties remain to maintain an Outperform stance at present.

Profitability Metrics Draw Scrutiny

Adobe maintains operating margins in the mid-40 percent range — an exceptional figure that has historically strengthened the investment thesis. William Blair identified this as potentially problematic. Such robust margins may invite additional competition rather than deter it.

The firm emphasized that margin trajectories and Adobe’s success in monetizing emerging AI-driven opportunities deserve intensive monitoring ahead.

Bhatia’s conclusion noted that outstanding questions surrounding pricing authority, competitive differentiation, and sustainable economics “are unlikely to be resolved in the near term,” suggesting the stock will trade sideways until greater certainty emerges.

Adobe’s most recent quarterly results demonstrated ongoing expansion within its Digital Media division, though forward guidance for the current period fell short of certain analyst projections — a disappointment investors hadn’t completely digested before this downgrade arrived.

The Reserve Bank of Australia has put a hard number on tokenization: $16.7 billion in annual economic gains, with upside beyond that if new markets emerge.

RBA Assistant Governor Brad Jones cited those findings Wednesday, drawn from Project Acacia, a structured pilot that tested tokenized assets across Australia’s wholesale financial markets, not a whitepaper projection or a consultancy estimate.

This is a central bank quantifying economic value from a live experiment. That distinction matters.

Jones stated plainly that the question is no longer whether tokenization has a future, but how. That framing signals a policy posture shift, from exploratory to infrastructure-building — with the RBA now moving toward a formal digital financial market infrastructure sandbox.

- Pilot Scope: Project Acacia tested 20 tokenization use cases across asset classes including government bonds, repos, bank term deposits, and trade payables, settled via stablecoins, deposit tokens, and wholesale CBDC.

- Economic Quantification: RBA projects AUD 24 billion ($16.7 billion) in annual gains from RWA tokenization, with higher potential if new tokenized markets develop.

- Next Phase: RBA and the Digital Finance Cooperative Research Centre will launch a digital financial market infrastructure (DFMI) sandbox, moving from pilots toward commercialization-stage testing.

Discover: The best crypto presales gaining institutional momentum right now

The Mechanics: What Project Acacia Actually Tested

Project Acacia was not a simulation. It ran 20 discrete use cases across live asset classes, government bonds, repurchase agreements, bank term deposits, investment funds, trade payables, and mining royalties — settled through multiple instrument types: stablecoins, bank deposit tokens, wholesale CBDC, and exchange settlement accounts.

Participants included banks, custodians, fintechs, fund managers, stablecoin issuers, and infrastructure operators, testing settlement on both private and public distributed ledger technology platforms.

BREAKING:

Australia's Reserve Bank says asset tokenization could generate $16.7 billion in annual efficiency gains. pic.twitter.com/KODoCbP0OF— Crypto Rover (@cryptorover) March 25, 2026

The $16.7 billion figure is anchored specifically to efficiency gains from automating asset lifecycle management, reducing manual settlement errors, compressing counterparty risk windows, and unlocking liquidity in fixed income markets.

Fixed income was a focal point because of its scale and its dependence on foreign investor capital, U.S. investors are currently Australia’s largest source of fixed income funding, and tokenized infrastructure could lower capital costs while improving secondary market liquidity.

The pilot also assessed how wholesale CBDC could be issued onto external ledgers, a technical test of interoperability between central bank settlement layers and commercial tokenization platforms. That is the infrastructure question the sandbox is designed to answer at commercial scale. The full findings from Jones’ address map out a sequenced path from pilot learnings to durable market infrastructure.

Industry showed strong appetite for tokenized private money throughout the process. The RBA noted that U.S. and European banks are already issuing deposit tokens in response to stablecoin competition, a dynamic the RBA expects to replicate domestically, with deposit tokens scaling for larger markets and stablecoins addressing smaller greenfield use cases.

Discover: The best crypto to diversify your portfolio with

The Strategic Signal: Why a Central Bank’s Data Changes the Calculus

Central banks do not publish $16.7 billion economic projections as gestures.

The RBA’s quantification of tokenization upside is an institutional green light. The kind that moves compliance budgets, board-level risk appetites, and infrastructure investment timelines in ways that venture capital endorsements never do.

The precedent is already set. Singapore’s MAS BLOOM sandbox converted tokenized trade finance from concept to live deployment fast. Ripple joined with RLUSD and demonstrated exactly how quickly regulatory sandbox frameworks become production infrastructure. The RBA’s DFMI sandbox follows the same logic. Stage-gated testing designed to de-risk commercialization, not validate what is already known.

McKinsey forecasts tokenized asset value approaching $2 trillion by 2030. The RBA data gives that global trajectory a country-level economic mandate. ASIC head Joe Longo made the binary explicit in November. Seize the opportunity or get left behind. The RBA moving from research to sandbox infrastructure is the institutional answer to that ultimatum.

— BSCN (@BSCNews) March 24, 2026

CRYPTO: AUSTRALIAN PENSION GIANT HOSTPLUS EYES BITCOIN ACCESS FOR 2.2 MILLION MEMBERS

CRYPTO: AUSTRALIAN PENSION GIANT HOSTPLUS EYES BITCOIN ACCESS FOR 2.2 MILLION MEMBERS

$96 billion in assets. 2.2 million members. And now crypto is on the table.

Per Bloomberg, @Hostplus, Australia's third-largest pension fund by member count, is weighing a plan to offer… pic.twitter.com/EiS8annBse

The structural risk is timing. Tokenized fixed income is advancing rapidly in the US. Australia’s dependence on foreign investors means isolated domestic development creates fragmentation risk, a scenario where Australian tokenized assets cannot interface with the global settlement layer already forming elsewhere. The sandbox’s cross-border payment research component addresses that directly but the window for seamless integration narrows as other jurisdictions lock in standards.

The rails are being built. Central banks from Canberra to Singapore to Washington are laying them simultaneously.

The only question that matters for active market participants is which projects are already positioned on those rails before institutional volume arrives.

Discover: The best pre-launch token sales

The post Australia Central Bank Backs Tokenization After $16.7B Pilot Finding appeared first on Cryptonews.

Demand for free Bitcoin cloud mining rises in 2026 as users seek hardware-free ways to earn crypto.

Summary

- Demand for free Bitcoin cloud mining grows in 2026 as users seek passive crypto income without hardware costs.

- Cloud mining platforms simplify crypto earnings with contracts, bonuses, and no need for ASICs or high electricity use.

- AngelBTC offers a $100 free mining bonus, enabling users to start contract-based Bitcoin mining with daily rewards.

The demand for free Bitcoin cloud mining without investment in 2026 continues to rise as more users search for accessible ways to earn cryptocurrency without purchasing expensive mining hardware.

Traditional Bitcoin mining requires ASIC machines, cooling systems, and high electricity costs. Today, cloud mining platforms simplify this process by offering contract-based mining services, allowing users to earn passive crypto income through remote mining infrastructure.

Many platforms now provide free entry incentives, such as welcome bonuses or trial mining contracts, making it easier for beginners to get started with bitcoin mining, crypto mining, and passive income strategies.

Below are five verified cloud mining platforms widely discussed in 2026.

1. AngelBTC – Contract-based cloud mining with $100 free bonus

AngelBTC is a cloud mining platform operated by BTC North Corp in Canada, focusing on renewable energy-powered mining infrastructure and structured mining contracts.

Visit AngelBTC official website

Unlike many platforms that only offer limited demo mining, AngelBTC provides a $100 free mining bonus, allowing users to activate real contracts and start generating daily rewards.

The platform connects users to mining farms across the United States, Canada, Norway, and Iceland, utilizing hydropower, wind, solar, and geothermal energy to maintain stable mining performance.

Key Features

- $100 free cloud mining bonus (no upfront investment)

- Real contract-based mining system (not simulation)

- Daily mining rewards with transparent tracking

- Renewable energy mining infrastructure

- Automated mining management for beginners

AngelBTC mining contracts overview

| Contract Name | Amount | Duration | Daily Rate | Daily Profit | Total Profit |

| Solar 5TH | $100 | 1 Day | 1.00% | $1 | $1 |

| Solar 5TH | $200 | 2 Days | 2.00% | $4 | $8 |

| Wind 10TH | $600 | 5 Days | 2.00% | $12 | $60 |

| Hydropower 15TH | $1100 | 5 Days | 2.20% | $24.2 | $121 |

| Hydropower 25TH | $2350 | 5 Days | 2.50% | $58.75 | $293.75 |

| Wind 40TH | $3950 | 4 Days | 2.70% | $106.65 | $426.6 |

| Hydropower 70TH | $9500 | 3 Days | 3.00% | $285 | $855 |

| Geothermal 120TH | $14500 | 2 Days | 3.30% | $478.5 | $957 |

| Natural Gas 200TH | $23500 | 1 Day | 4.00% | $940 | $940 |

| Hydropower 500TH | $49500 | 1 Day | 5.00% | $2475 | $2475 |

View Full Contract & Claim $100 Free Hash Power!

Additional earning opportunity

Beyond mining contracts, AngelBTC also provides an optional referral-based earning model for users seeking additional passive income.

Users can earn a permanent 4.2% commission on every qualifying investment made by referred users, without complex conditions.

This creates a dual-income structure:

- Daily mining rewards from active contracts

- Long-term passive income through referral commissions

For users exploring crypto passive income strategies in 2026, this model offers additional scalability without requiring extra investment.

Become an AngelBTC ambassador

AngelBTC also supports a community-driven growth model where users can participate as ambassadors.

There is no investment required to join, and users can start sharing their referral link immediately after registration. This aligns with the broader trend of decentralized promotion and crypto affiliate programs, which are becoming increasingly popular in the blockchain industry.

2. StormGain – Mobile-friendly free mining feature

StormGain offers a mobile-based cloud mining feature that allows users to generate small amounts of Bitcoin without purchasing hardware.

Advantages

- Free mining feature within mobile app

- Beginner-friendly interface

- Integrated crypto trading tools

- Available on Android and iOS

3. NiceHash – Global Hash power marketplace

NiceHash operates as a hash power marketplace, allowing users to buy or sell computing power based on real-time profitability.

Advantages

- Flexible mining model

- Automatic algorithm switching

- Global mining network

- Real-time profit tracking

4. GoMining – Tokenized cloud mining model

GoMining provides a tokenized mining system, where users purchase digital miners backed by real mining hardware.

Advantages

- Tokenized mining ownership

- Passive income generation

- Blockchain-based infrastructure

- Flexible entry levels

5. Hashing24 – Industrial bitcoin mining contracts

Hashing24 focuses on industrial-scale Bitcoin mining contracts, offering stable long-term mining solutions.

Advantages

- Dedicated BTC mining contracts

- Industrial mining farms

- Transparent performance tracking

- Long-term contract options

Why free cloud mining is popular in 2026

The rise of free Bitcoin cloud mining without investment is driven by accessibility and reduced financial risk.

Key Benefits

- No hardware required

- No electricity or maintenance costs

- Beginner-friendly onboarding

- Passive income through mining contracts

- Real-time earnings monitoring

These features make cloud mining one of the most searched topics in crypto, especially for keywords like:

- free bitcoin cloud mining without investment 2026

- Bitcoin mining contracts daily income

- passive crypto income platforms

Conclusion

In 2026, cloud mining has evolved into a contract-driven and scalable ecosystem, offering users multiple ways to participate in cryptocurrency mining.

Platforms like AngelBTC combine:

- real mining infrastructure

- structured contracts

- free entry bonuses

- referral-based income models

At the same time, platforms such as StormGain, NiceHash, GoMining, and Hashing24 provide alternative approaches to mining participation.

For both beginners and experienced users, cloud mining remains one of the most practical methods to access bitcoin mining, crypto mining, and passive income opportunities without managing physical hardware.

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

- Sky is diversifying its revenue streams and yield strategies.

- Securitize and Maple have joined the Sky Ecosystem agent network.

- The SKY token could rally to $0.10

The Sky Ecosystem token is under sell-off pressure as negative sentiment keeps altcoins in the red.

But despite top coins wallowing in bearish territory, Sky is up 13% over the past month, and network fundamentals look bullish.

The latest boost comes from ecosystem platforms joining Sky’s agent network, including Securitize and Maple Finance.

SKY price could benefit as the project taps into diversified revenue streams and yield strategies.

Sky-backed Obex brings 8 new allocators to ecosystem

A lot of the buzz around Sky today stems from an announcement that Sky-backed platform Obex is spearheading the latest onboarding of capital allocators.

Sky Ecosystem has welcomed eight new allocators, marking the largest capital deployment from a decentralized protocol into a coordinated cohort of specialised agents.

These allocators have already borrowed up to $1 billion in USDS from the Sky Protocol, enabling deployment across innovative yield strategies.

The Sky Agent Network operates as the ecosystem’s core revenue engine.

Each agent functions as an independent capital allocator, borrowing USDS and directing it toward high-potential opportunities.

These platforms compete on risk-adjusted returns, with a portion of generated value accruing back to the Sky Protocol.

According to details, the new cohort that is helping broaden the network’s DeFi scope includes Maple Finance, Securitize, Centrifuge, River and TVL Capital.

The projects cut across on-chain lending, tokenization, AI infrastructure plays and structured credit, among others.

By integrating these diverse sources, Sky Protocol is adding potential avenues for untapped revenue pools.

Growth could influence SKY price performance, particularly if DeFi yield optimization takes root.

SKY price outlook

The Sky Ecosystem (SKY) token is trading around $0.071, down about 3% over the past 24 hours, after touching intraday highs of $0.077, according to CoinMarketCap data.

As of March 26, the token remains roughly 13% above its late-February lows, reflecting a modest recovery.

The recent uptick has coincided with rising USDS borrowing volumes, while increased interest around agent onboarding has also supported buying activity.

These trends suggest improving network fundamentals, with the reported $1 billion USDS deployment pointing to notable capital inflows that could enhance SKY’s utility in governance and staking.

Broader tailwinds, including growing adoption of real-world assets (RWAs) and supportive regulatory developments in the US and Europe, may further support sentiment.

However, risks remain. Underperformance in yield strategies or renewed macroeconomic volatility could weigh on prices.

From a technical perspective, SKY appears to be forming a bullish flag pattern on the daily chart.

A move above $0.075 could open the door toward the next major resistance near $0.15.

On the downside, the $0.060 level is seen as key support, while the token’s all-time low stands at $0.03, reached in February.

Code is not the weakest point in crypto thefts

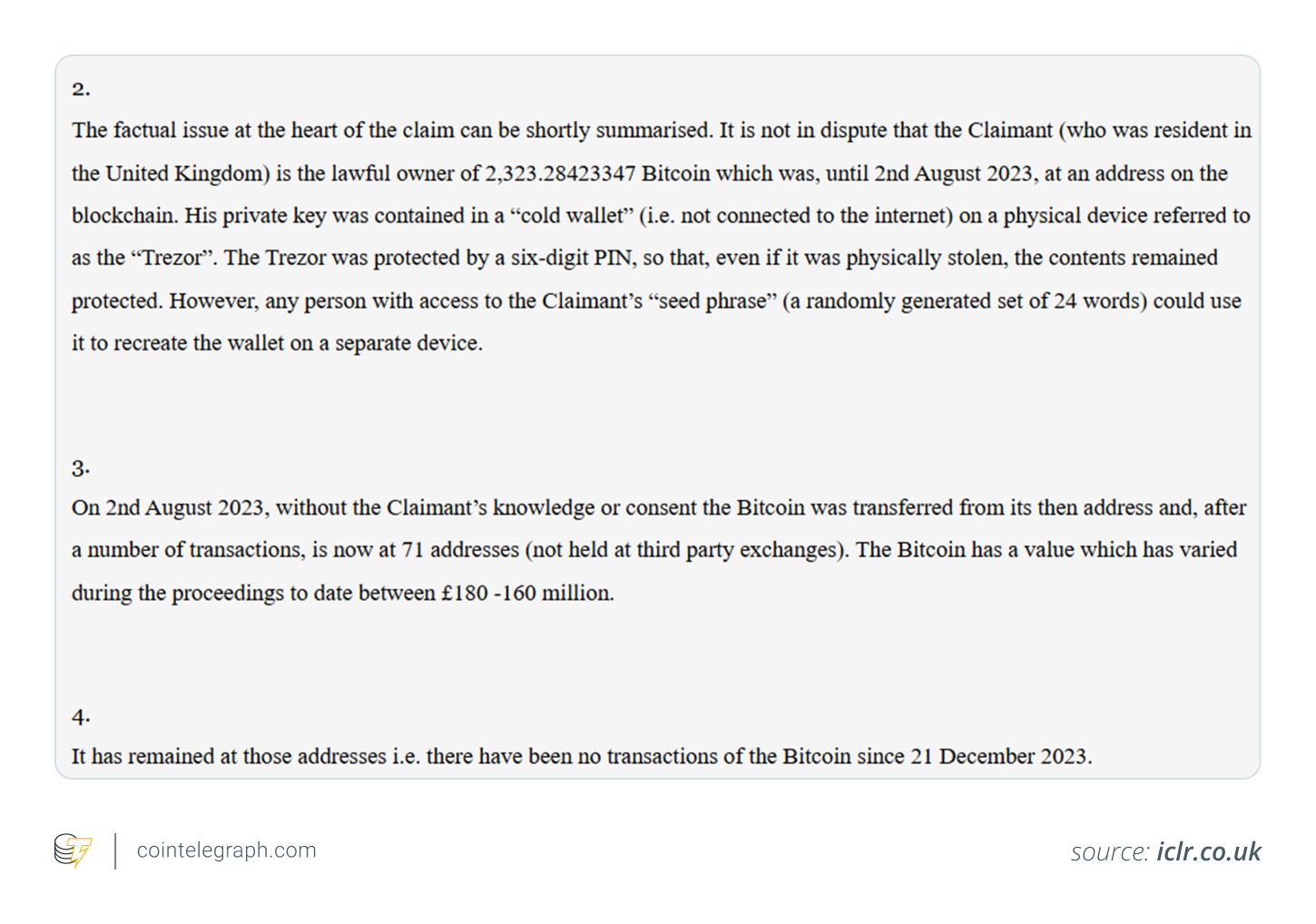

In crypto, security is usually regarded as a technical issue. You are asked to safeguard your private keys, rely on a hardware wallet and steer clear of phishing links. Yet a prominent case in the UK reveals that the real vulnerability in this case might have had nothing to do with code.

The UK High Court is currently reviewing a case involving the alleged theft of 2,323 Bitcoin (BTC), worth about $176 million. The theft did not stem from hacking or malware. Instead, it began with a seed phrase being exposed, which became the single point of failure in self-custody.

The dispute centers on Ping Fai Yuen, who claims that his estranged wife, Fun Yung Li, and her sister gained access to his Bitcoin by secretly recording his wallet’s recovery information.

The assets were held in a hardware wallet, designed to keep private keys completely offline and shielded from remote threats. Yet the theft still happened and it required no breach of encryption.

Court documents suggest the theft only required discovering the seed phrase.

Alleged timeline of the crypto theft

The allegations describe events that suggest surveillance rather than digital intrusion.

-

The individuals in question are accused of using a camera or recording device to capture the seed phrase and related codes.

-

The claimant later learned of the scheme after receiving a warning from his daughter.

-

He then set up audio recording equipment, which he says captured conversations about moving the funds.

-

The Bitcoin was subsequently transferred to 71 separate wallet addresses.

No additional movements have appeared on the blockchain since Dec. 21, 2023, indicating that the assets have remained inactive since the reported transfer.

Authorities are said to have confiscated devices and cold wallets as part of the inquiry, although the proceedings are still ongoing.

Did you know? In several past cases, hidden cameras, not hackers, have been the weakest link in crypto security. Physical surveillance has quietly become one of the most underestimated threats to self-custodied digital assets.

Why the seed phrase mattered in the UK crypto theft

To understand the case, you need to grasp a core principle of crypto: Whoever has access to the seed phrase has full control of the funds.

A hardware wallet shields private keys from online risks. But the seed phrase, typically 12 to 24 words, serves as a full backup of the entire wallet.

Finding the seed phrase allows anyone to:

-

Rebuild the wallet on any other device

-

Access all the associated funds

-

Move the assets without ever touching the original hardware

Put simply, once the seed phrase becomes known, the physical device loses all relevance.

The surveillance element: An uncommon form of compromise

What stands out in this matter is the reported method used to carry out the breach.

Rather than relying on phishing or malicious software, the allegations center on visual or audio capture, possibly through a hidden camera or covert recording.

This brings attention to a seldom-mentioned risk: side-channel exposure.

Seed phrases are frequently written down, spoken or typed during setup. If any of those moments are watched or recorded:

-

The phrase can be pieced together.

-

The wallet can be copied elsewhere.

-

Assets can be relocated without immediate traces.

In environments full of smart devices, cameras and shared spaces, this type of risk continues to rise.

The UK High Court’s early stance

The matter came before the UK High Court, where Justice Cotter examined the evidence presented.

Although this does not constitute a final decision in the case, the judge indicated that the claimant had demonstrated a very high probability of success.

Among the elements considered were:

The court also stressed the need for swift action, citing security concerns and Bitcoin’s price fluctuations.

Did you know? Some wallets now offer decoy wallets that use different PINs. This feature allows users to display a smaller balance under duress, adding a layer of protection against both physical coercion and surveillance-based attacks.

Why the assets were spread across 71 addresses

The claim states that the Bitcoin was distributed across 71 wallet addresses.

This step carries several implications:

-

It makes tracking and recovery more difficult.

-

It avoids drawing attention to a single large transfer.

-

It fragments the holdings, which can delay legal and investigative efforts.

Although the blockchain’s transparency allows movements to be traced, spreading the funds adds layers of complexity and time to any recovery process.

The dusting attack concern

The claimant also expressed concern about a possible dusting attack on the addresses involved.

Dusting refers to sending tiny amounts of crypto to wallets in order to:

-

Monitor subsequent activity

-

Link addresses to real identities

-

Identify valuable targets for future attacks

If wallet addresses become public, they can attract additional scrutiny, even if no further activity occurs.

Why this matter extends beyond a single conflict

On one hand, this case remains a private legal dispute. On the other, it serves as a case study in the broader risks of crypto custody.

It demonstrates that:

-

Hardware wallets limit digital threats, yet leave human factors untouched.

-

Threats from those close to the owner can outweigh those from outside attackers.

-

Exposure of the seed phrase can result in a complete loss of control.

Above all, this shows that crypto security involves far more than just devices; it relies heavily on environment, conduct, trust and relationships.

Security lessons from the case

This example reinforces several straightforward guidelines:

-

Keep the seed phrase completely hidden from cameras, phones and connected devices.

-

Avoid storing recovery information in places that others can access.

-

Separate personal identity from wallet control whenever possible.

-

Use multiple layers of protection for large holdings.

More sophisticated arrangements may include additional passphrases, split backups or multisignature setups. Each of these methods is designed to reduce reliance on a single vulnerable element.

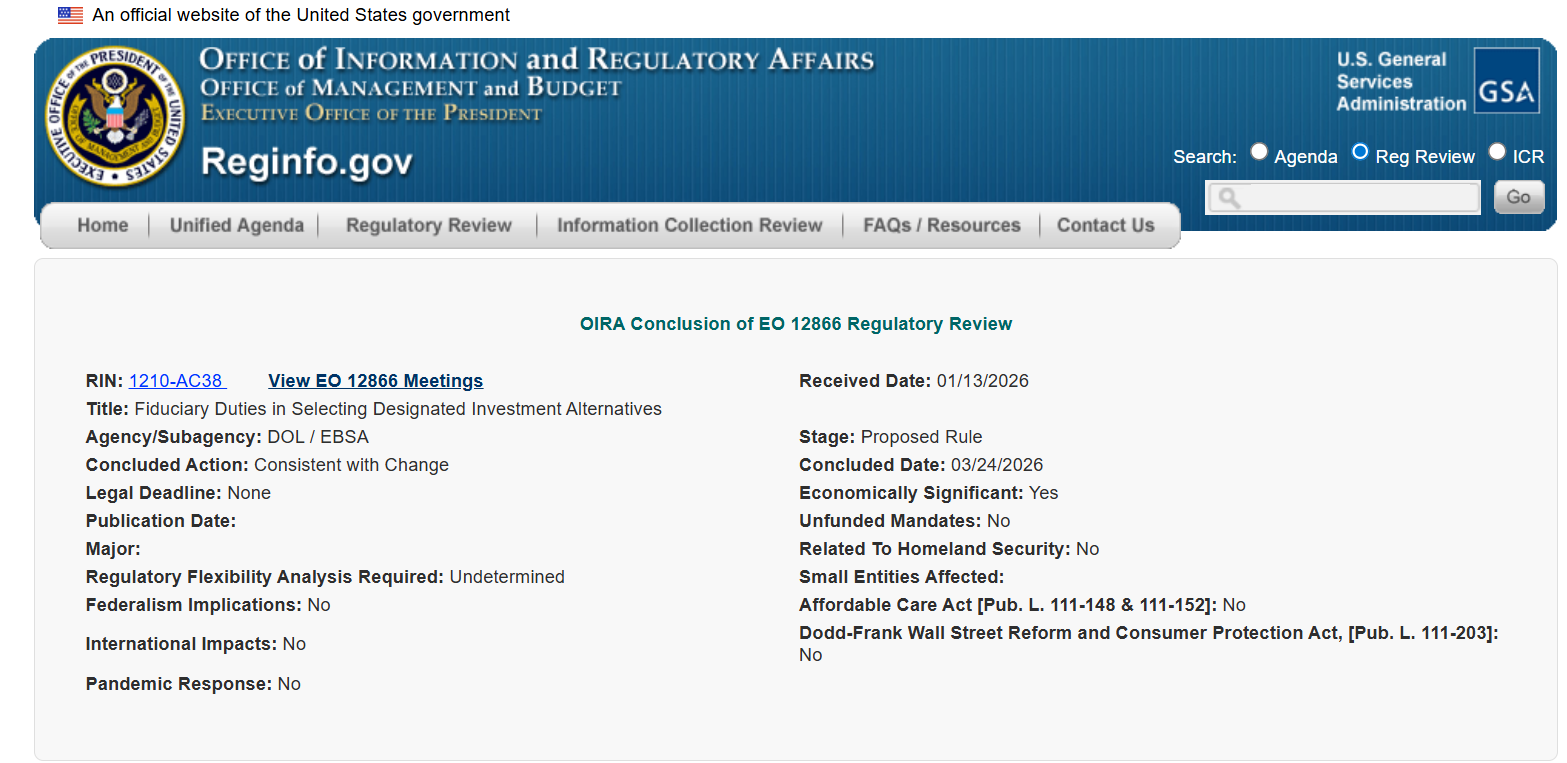

The White House’s Office of Information and Regulatory Affairs (OIRA) has completed its review of a Department of Labor (DOL) proposal that could reshape how 401(k) fiduciaries evaluate alternative assets, including digital-asset exposure.

The OIRA’s website shows the review concluded on March 24, with the action marked “consistent with change” and the proposal classified as “economically significant.” The DOL is now expected to publish the proposed rule for a standard 60-day public comment period, which is usually followed by revisions and the issuing of a final rule.

The proposal follows President Donald Trump’s Aug. 7, 2025, executive order directing federal agencies to expand access to alternative assets in 401(k) plans, including exposure to digital assets through certain investment vehicles.

The order directed the DOL to reevaluate restrictions around alternative assets in defined-contribution plans, including digital assets, private equity and real estate. It also called for inter-agency collaboration between the US Treasury Department and the Securities and Exchange Commission on supporting rule changes.

The completed review clears an interagency hurdle for a proposal that could widen the path for alternative assets in US defined-contribution retirement plans.

Crypto-linked exposure moves closer to 401(k) market

On May 28, 2025, the DOL rescinded a 2022 compliance release that urged fiduciaries to be “extremely cautious” when considering crypto for 401(k) retirement plans, signaling a broader shift in the federal government’s stance toward retirement-plan exposure to digital assets.

The US retirement market reached a record $48.1 trillion in financial assets on September 30, 2025, according to a report by the Investment Company Institute (ICI).

Indiana advances crypto retirement access

Other US states have launched their own legal initiatives to make digital assets a retirement plan asset.

Related: Major Australian pension fund mulls crypto offerings amid growing demand

On Feb. 25, Indiana lawmakers passed a bill that would require certain state retirement and savings plans to offer a self-directed brokerage option with at least one crypto investment option by July 1, 2027.

The bill would allow Indiana citizens to hold Bitcoin (BTC) and digital assets as part of their retirement plans for the first time.

Magazine: Quitting Trump’s top crypto job wasn’t easy: Bo Hines

Wall Street bank Citi says proposed limits on stablecoin rewards in the latest draft of U.S. market structure legislation would be a setback for Circle (CRCL) but not a fundamental threat to the investment case.

“We view this development potentially (but not necessarily) as a scaling setback, but not a thesis killer,” wrote analysts led by Peter Christiansen in the Tuesday report.

The draft bill allows narrowly defined rewards programs as long as they don’t resemble bank deposit interest, the analysts said. A broader ban on third-party rewards would not directly affect Circle’s net revenue, as the firm already passes most of its reserve income to distribution partners like Coinbase (COIN).

Still, the analysts expect weaker incentives to hold USDC, which they characterize as a payment instrument rather than a security, could temporarily reduce circulation and secondary-market liquidity. “We still maintain the view that stablecoin volume is the key indicator of adoption, not circulation.”

Citi has a high risk rating on Circle stock with a $243 price target. The shares were trading around $100 at the time of publication.

Circle shares fell roughly 20% on Tuesday, after a draft of the U.S. Clarity Act raised the prospect of banning yield on passive stablecoin balances, sparking concerns about the attractiveness of yield-bearing crypto products.

The move was compounded by broader investor anxiety around how the rules could impact stablecoin-related revenues and incentives, alongside fresh competitive pressure after Tether signaled plans for a full Big Four audit and potential U.S. expansion.

The Circle selloff on Tuesday reflected a market misread of the draft Clarity Act, according to Wall Street broker Bernstein.

Investors are conflating who earns yield with who distributes it, the broker said in a Wednesday report. Circle earns reserve income from USDC backing assets, while platforms like Coinbase (COIN) pass some of that yield to users, the actual target of the proposed rules.

The draft would ban yield on passive stablecoin balances but allow activity-based rewards tied to trading or payments. Bernstein analysts led by Gautam Chhugani said this pressure on Coinbase’s ~3.5% USDC yield product, likely forcing a restructure. Circle’s model remains unaffected. The firm does not pay yield to holders and generated $2.64 billion in reserve income in FY2025.

The report noted that USDC growth, from ~$30 billion to $80 billion in two years, is driven by trading, payments and collateral demand, not yield.

Bernstein has an outperform rating on Circle shares with a $190 price target.

Coinbase is treading carefully in negotiations over the Clarity Act, privately signaling to Senate staff that it is dissatisfied with the latest compromise while stopping short of publicly opposing the bill, according to people familiar with the matter.

Read more: Circle selloff may be overdone as crypto bill weakens Coinbase edge, say analysts

Crypto World

Fannie Mae Now Accepts Crypto as Mortgage Collateral: But There Is a Catch That Could Cost You Thousands

A $100,000 Crypto bitcoin position now qualifies a borrower for a GSE-backed mortgage, but only $40,000 to $50,000 of it actually counts.

FHFA Director William J. Pulte’s June 25, 2025 directive ordered Fannie Mae and Freddie Mac to accept cryptocurrency as financial reserves without requiring conversion to dollars, a direct reversal of Fannie Mae’s longstanding guideline B3-4.1-04 that had blocked digital assets from underwriting since 2022.

The surface headline is historic. The mechanism underneath it is where the real trade-off lives.

Mortgage company Better Home & Finance and Coinbase Global are the first to operationalize the shift, announcing this week a crypto mortgage product that allows borrowers to pledge crypto holdings against a Fannie Mae-backed loan. The institutional adoption signal here is hard to overstate, this is the $12 trillion U.S. residential mortgage market formally recognizing Bitcoin reserves as collateral-adjacent assets.

The analytical question is what the volatility haircut actually costs holders, and whether the math still works for the average BTC or ETH position size.

- FHFA directed Fannie Mae and Freddie Mac on June 25, 2025 to accept crypto as mortgage reserves without forced liquidation.

- A 50–60% volatility haircut applies — $100,000 in BTC counts as $40,000–$50,000 toward reserve requirements.

- Assets must be held on U.S.-regulated exchanges; self-custodied cold wallets are currently excluded.

- Better Home & Finance and Coinbase are the first lender-exchange pair to launch a Fannie-backed crypto mortgage product.

Discover: The best crypto presales gaining institutional momentum right now

The Haircut Mechanism: What FHFA’s Framework Actually Allows

The FHFA framework introduces what it calls a risk-based volatility haircut, a percentage reduction applied to the market value of crypto holdings before they count toward reserve requirements.

Current guidance puts that haircut at 50–60%, meaning a borrower holding $100,000 in BTC can claim between $40,000 and $50,000 in qualifying reserves. The bear case is concrete: a borrower who needs $80,000 in reserves must hold $160,000–$200,000 in crypto to clear the threshold. That’s a steep overcollateralization requirement by any conventional lending standard.

The bull case is equally concrete. Before June 25, those same crypto holders had two options, sell the position and crystallize a taxable event, or disqualify the asset entirely. Now a BTC position held for institutional-grade exposure can anchor a mortgage application while staying on-chain. The preserved market upside during the loan approval window alone is a material benefit for anyone holding meaningful Bitcoin reserves.

Custody rules are non-negotiable under the framework. Assets must be stored on U.S.-regulated centralized exchanges, Coinbase, Kraken, and Gemini qualify; self-custodied cold wallets do not.

Per the FHFA’s July 3, 2025 formalized requirements, lenders will verify holdings via exchange API integrations, and assets must clear AML compliance thresholds.

Staked assets and DeFi-locked positions are excluded from the current automated underwriting systems. That distinction cuts out a significant slice of the sophisticated crypto-holder population who’ve moved assets off exchanges, and it’s the friction point right now.

Pulte framed the directive as enabling GSEs to assess the “full spectrum of asset information” for creditworthy borrowers, per public statements following the announcement. Senator Cynthia Lummis introduced the 21st Century Mortgage Act to codify the policy in statute, explicitly prohibiting forced crypto liquidation.

Discover: The best crypto to diversify your portfolio with

How BTC and ETH Holders Actually Use This: The Practical Workflow

For a borrower holding BTC or ETH on a qualifying exchange, the crypto mortgage workflow starts with documentation: exchange-generated statements showing asset balances, ownership verification, and 60-day holding history consistent with standard reserve seasoning requirements.

The GSE-backed loan covers the property; the crypto remains on the exchange as a verified reserve asset rather than being converted to cash. No liquidation, no taxable event, no forced exit from a position.

The worked math matters here. A borrower purchasing a $500,000 home under a conventional GSE loan typically needs 2–6 months of mortgage payments in reserves, amounting to roughly $15,000–$45,000, depending on the loan product. At a 50% haircut, clearing a $45,000 reserve requirement demands $90,000 in BTC or ETH held on a regulated exchange.

That threshold is accessible for the cohort of crypto-native wealth holders the FHFA is explicitly targeting, but it excludes borrowers with smaller positions who would still need supplemental cash reserves.

Freddie Mac is operating under the same FHFA directive and must submit board-approved proposals for review, watch for finalized approved-asset lists specifying whether altcoins beyond BTC and ETH qualify, and whether haircut percentages differ by asset volatility profile. Regulatory momentum across major economies is accelerating GSE timelines on this front. The implementation is not complete, it’s the opening framework, and the edge cases haven’t been stress-tested by a market drawdown yet.

Discover: The best crypto presales gaining institutional momentum right now

The post Fannie Mae Now Accepts Crypto as Mortgage Collateral: But There Is a Catch That Could Cost You Thousands appeared first on Cryptonews.

Darius Acuff Jr. is dominating March but NBA Draft questions remain

12 Clever Gadgets Under $100 To Upgrade Your Smart Home

William Shatner Recruits Judas Priest’s Rob Halford For New Heavy Metal Album

-

Crypto World6 days ago

Crypto World6 days agoNIO (NIO) Stock Plunges 6.5% as Shelf Registration Sparks Dilution Worries

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Adidas – Corporette.com

-

NewsBeat1 day ago

NewsBeat1 day agoManchester United reach agreement with Casemiro over contract clause amid transfer speculation

-

Politics6 days ago

Politics6 days agoJenni Murray, Long-Serving Woman’s Hour Presenter, Dies Aged 75

-

Crypto World5 days ago

Crypto World5 days agoBest Crypto to Buy Now: Strategy Just Spent $1.57 Billion on Bitcoin During Fear While Early Investors Quietly Enter Pepeto for 150x Potential

-

Crypto World5 days ago

Crypto World5 days agoBitcoin Price News: Bhutan Sells $72 Million in BTC Under Fiscal Pressure, but the Smart Money Entering Pepeto Sees What the Market Does Not

-

Tech6 days ago

Tech6 days agoinKONBINI Lets You Spend Summer Days Behind the Register

-

News Videos13 hours ago

News Videos13 hours agoParliament publishes latest register of MPs’ financial interests

-

Sports3 days ago

Sports3 days agoRemo Stars and Kano Pillars Strengthen Survival Hopes in NPFL

-

Politics7 days ago

Politics7 days agoGender equality discussions at UN face pushbacks and US resistance

-

Business4 days ago

Business4 days agoNo Winner in March 21 Drawing as Prize Rolls to $133 Million for Next

-

Sports3 days ago

Sports3 days agoGary Kirsten Accuses Pakistan Cricket Board Of ‘Interference’, Mohsin Naqvi Responds

-

Tech4 days ago

Tech4 days agoGive Your Phone a Huge (and Free) Upgrade by Switching to Another Keyboard

-

Sports6 days ago

Sports6 days ago2026 Kentucky Derby horses, odds, futures, preview, date: Expert who nailed 12 Derby-Oaks Doubles enters picks

-

Tech4 days ago

Tech4 days agoAI enters the chat: New Seattle dating app relies on tech to facilitate meaningful human connections

-

Politics7 days ago

Politics7 days agoScotland’s rejection of assisted dying is a victory for humanity

-

Business7 days ago

Business7 days agoDLocal: Entering 2026 At Escape Velocity

-

Business6 days ago

Columbia Sportswear enters $500 million credit agreement with JPMorgan Chase

-

NewsBeat7 days ago

NewsBeat7 days agoMissile lands next to presenter during live report

-

Tech5 days ago

Tech5 days agoToday’s NYT Connections Hints, Answers for March 22 #1015

You must be logged in to post a comment Login