Crypto World

Ethereum treasury firm Sharplink takes in ether for the first time in eight months

Sharplink (SBET) received 5,000 ether (ETH) worth about $7.85 million on Thursday, its first ether inflow in eight months, according to Arkham data showing the coins arriving from crypto brokerage FalconX.

The inflow is small against the company’s existing pile and lands at an awkward moment. Sharplink held 876,285 ether as of June 21, worth roughly $1.3 billion, making it the second-largest public ether treasury company behind Tom Lee’s Bitmine Immersion (BMNR), which held about 5.67 million ether in mid-June.

Onchain analyst EmberCN put Sharplink’s average purchase price at about $3,609 per coin, which implies an unrealized loss of around $1.79 billion with ether trading near $1,555.

Its last inflow came in October 2025, when it added 19,270 ether for $78.3 million, also now deep underwater.

The ether arrived as the token fell 5% over 24 hours in a broad crypto selloff, dropping below $1,560 as bitcoin slipped under $59,000. Tether’s USDT briefly overtook ether by market value during the rout, at about $186 billion to ether’s $185 billion.

Crypto World

Binance tells EU users it will no longer provide services after failing to secure MiCA license

Binance, the world’s largest crypto exchange by trading volume, told customers in the European Union (EU) it is suspending some services because it will not have a Markets in Crypto-Assets (MiCA) license in place by July 1.

Users were emailed to notify them the exchange was no longer able to accept new registrations and would restrict services, a spokesperson for the Abu Dhabi-based company told CoinDesk. “Your assets remain safe and secure, and will remain accessible at all times,” the email said.

On Thursday, the company said it withdrew its license application in Greece and would seek authorization in another EU country.

“Our ambitions in Europe remain the same, and we are confident we will secure a MiCA licence in the coming months,” Binance said in a statement to CoinDesk.

The exchange intends to approach France instead, the Financial Times reported Friday, citing people familiar with the company’s plans.

The emails to clients in France, Italy, Poland and Spain come days before a June 30 deadline. Crypto firms must have a MiCA license from at least one EU member state by July 1 to provide services across all 27 member states. Unlicensed firms must wind down their EU activities.

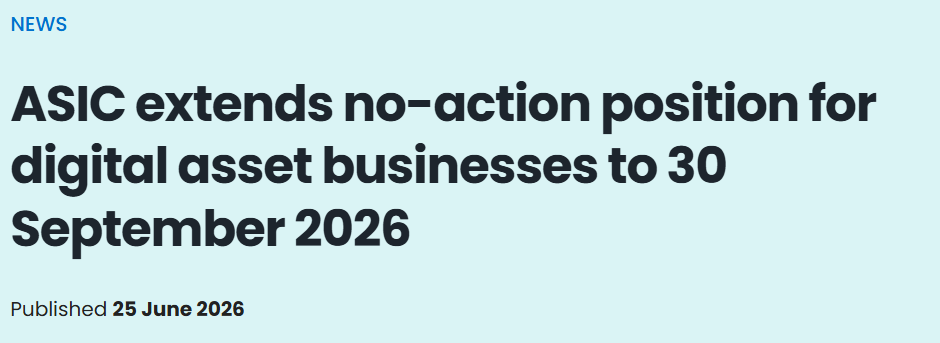

Australia’s corporate regulator has extended a key compliance transition for digital asset businesses, giving firms more time to apply for licenses under updated guidance. The Australian Securities and Investments Commission (ASIC) said the temporary “no-action” position against enforcement will last until September 30, 2026, after being pushed back from an earlier June 30, 2026 deadline.

The extension covers companies seeking an Australian Financial Services (AFS) license, as well as digital asset firms that may require market or clearing and settlement authorizations. ASIC also broadened the relief to include businesses that operate through authorized representatives or via intermediary arrangements with already licensed entities.

Key takeaways

- ASIC extended its digital asset no-action protection to September 30, 2026 for firms applying under updated licensing guidance.

- The relief applies not only to AFS license applicants, but also to companies that may need market and clearing and settlement approvals.

- ASIC widened eligibility to cover digital asset activities carried out through authorized representatives or intermediary arrangements with licensed firms.

- ASIC said it has received around 30 license applications since it updated its digital asset guidance in October 2025.

ASIC pushes the clock back for licensing applications

ASIC’s update provides additional runway for digital asset businesses working through Australia’s financial services licensing expectations. In a statement, the regulator said the no-action stance that shields eligible firms from enforcement will continue through Sept. 30, 2026, giving applicants more time to prepare submissions and meet licensing requirements tied to ASIC’s approach to digital asset products.

Under the extension, firms that need AFS licensing can remain within the protected period while they apply. ASIC’s scope is also broader than simple trading-platform licensing: it extends to situations where a business may require additional market structure permissions, including market authorizations, and clearing and settlement authorizations.

The regulator said it has also seen activity around the guidance it issued, noting it has received about 30 license applications since the update in October 2025. For industry participants, that figure is a useful signal: demand for formal licensing is moving forward, but the regulator appears to be acknowledging that processing, preparation, and regulatory readiness take longer than the initial timetable.

How INFO 225 shaped the licensing pathway

The latest extension builds on earlier regulatory work. ASIC had previously introduced the no-action position after updating Information Sheet 225 (INFO 225), clarifying how Australia’s existing financial services laws apply to digital asset activities. ASIC’s central point is that many digital asset products can fall within Australia’s definition of financial products, meaning providers may need to hold an AFS license depending on how their offerings are structured.

ASIC has consistently framed its approach as technology-neutral, arguing that the legal definitions are broad enough to cover digital assets. The regulator said its interpretation was recently reinforced by the High Court’s Block Earner ruling, which concluded that the company’s former crypto yield product was a financial product under the Corporations Act.

That High Court outcome matters beyond one case, because it strengthens the legal basis for ASIC’s view that some crypto-linked revenue models—such as yield products—can be regulated under existing securities and financial services frameworks. For businesses, it raises the stakes around product classification: even if a firm believes its activity is “new” or “digital-native,” the legal analysis can still lead back to traditional licensing duties.

What comes after the transition: the Digital Asset Framework

The no-action relief is not the end state. ASIC’s temporary approach runs alongside Australia’s broader legislative track: the Digital Asset Framework, which passed Parliament in April and is currently scheduled to commence on April 9, 2027.

ASIC has warned that the incoming framework will bring digital asset platforms and tokenized custody platforms under the financial services licensing regime in a more formal, dedicated structure. Importantly for existing licensees and applicants, ASIC noted that approvals obtained under the current INFO 225-based route may not fully cover future requirements once the new regime begins.

In a May announcement, ASIC said many digital asset firms that apply for a licence based on INFO 225 will also need to add Digital Asset Platform (DAP) and Tokenized Custody Platform (TCP) authorizations once the new framework commences. That distinction creates a two-stage compliance picture for the industry: first, secure the licensing status that fits current guidance, and then prepare for additional authorizations required under the forthcoming regime.

For investors and customers, the practical implication is straightforward: licensing and oversight for crypto services in Australia may become more granular over time. Firms that focus only on the near-term INFO 225 transition could face additional operational and compliance work after April 2027.

Why the extension matters for builders and market participants

Extending the deadline reduces immediate pressure on applicant pipelines and may allow businesses to align governance, risk controls, and regulatory compliance processes with ASIC’s expectations. It also acknowledges that the licensing journey is broader than submitting paperwork—firms must demonstrate capability across key areas such as client protections, arrangements, and ongoing compliance obligations that regulators typically expect from AFS-licensed entities.

The extension’s inclusion of authorized representative and intermediary arrangements is particularly relevant for distribution models. Digital asset firms often operate through partnerships or regulated intermediaries; by clarifying that no-action relief can extend to those structures, ASIC is signaling that compliance can be achieved through legitimate regulated channels rather than forcing every participant to build an entirely standalone licensing footprint immediately.

Still, the timeline remains tight relative to the next legislative phase. With the Digital Asset Framework scheduled to start in April 2027, the period granted by ASIC now serves as a bridge: enough time to get initial applications in, but not enough to avoid future licensing upgrades if firms will ultimately need DAP and TCP authorizations.

As ASIC continues processing applications and as the April 2027 commencement date approaches, the next items to watch are how many applicants ultimately secure AFS licenses and what proportion need additional DAP/TCP approvals. That will offer the clearest indication of how quickly Australia’s crypto regulatory regime is moving from guidance-based classification to the dedicated structure set out in the new framework.

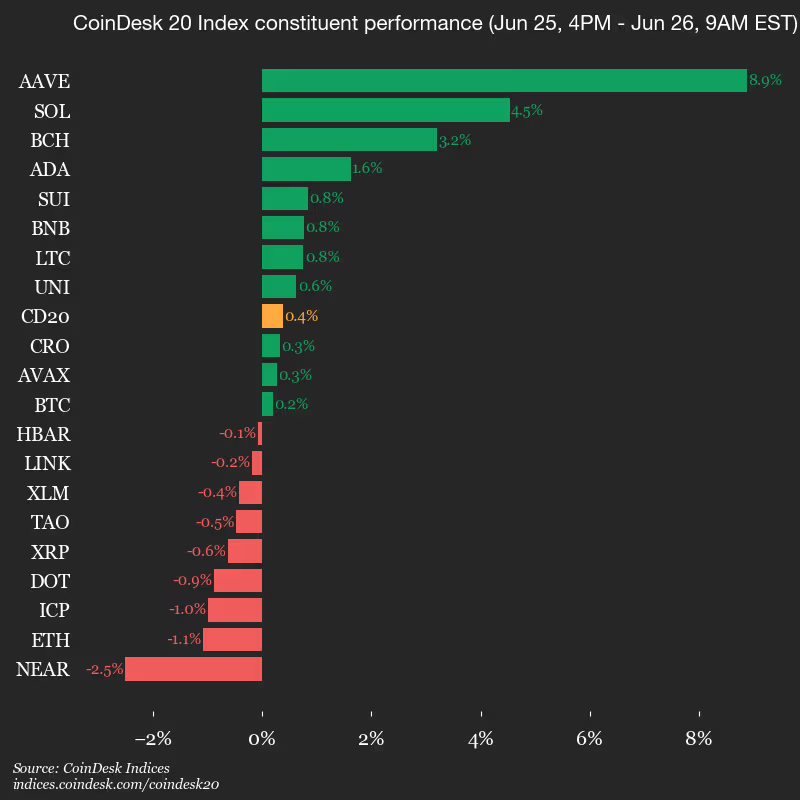

CoinDesk Indices presents its daily market update, highlighting the performance of leaders and laggards in the CoinDesk 20 Index.

The CoinDesk 20 is currently trading at 1595.41, up 0.4% (+5.99) since 4 p.m. ET on Thursday.

Eleven of 20 assets are trading higher.

Leaders: AAVE (+8.9%) and SOL (+4.5%).

Laggards: NEAR (-2.5%) and ETH (-1.1%).

The CoinDesk 20 is a broad-based index traded on multiple platforms in several regions globally.

The pullback marks a sharp reversal from expectations at the start of 2026, when many industry executives anticipated a wave of crypto listings following successful IPOs by Circle (CRCL) and CoinDesk’s owner Bullish (BLSH).

Crypto investors also worry that this year’s blockbuster AI-related IPOs are siphoning capital away from digital assets. The successful listing of SpaceX SPCX), along with expectations for additional high-profile AI and technology offerings, has given institutional investors another destination for growth capital at a time when crypto markets have struggled to regain momentum.

Market participants say that rotation has weighed on tokens, crypto-linked equities and the appetite for new crypto IPOs

Snider said the pickup in public listings reflects improving confidence among both corporate executives and equity investors. The key question, is whether the surge signals the kind of market euphoria typically seen at the peak of an asset bubble.

He sees some familiar warning signs. Equity valuations remain elevated, investor confidence is strong, and AI has become a dominant investment theme, echoing the technology-driven optimism that characterized previous market peaks.

But the strategist argued one critical metric tells a different story: the number of IPOs. The U.S. has averaged roughly 100 IPOs a year over the past quarter century, close to the current pace. That compares with more than 250 IPOs in 2021 and nearly 400 during the height of the dot-com boom in 1999.

The Australian Securities and Investments Commission (ASIC) has given digital asset businesses another three months to apply for licenses required under its updated regulatory guidance.

Australia’s financial regulator said that the temporary protection from enforcement would remain in place until Sept. 30, pushed from the previous June 30 deadline.

The extension applies to businesses seeking an Australian Financial Services (AFS) license, as well as companies that may require market or clearing and settlement authorizations.

ASIC also expanded the no-action relief to cover digital asset businesses operating through authorized representatives or intermediary arrangements with licensed firms, widening the pool of companies eligible for the transition period.

The regulator said it has received about 30 license applications since updating its digital asset guidance in October 2025.

Source: ASIC

Australia’s crypto licensing transition takes shape

ASIC previously introduced the no-action position after updating its Information Sheet 225 (INFO 225) guidance to clarify how existing financial services laws apply to digital assets. The guidance states that many digital asset products are financial products under existing law, meaning many providers require an AFS licence.

That approach rests on ASIC’s view that Australia’s definitions of financial products are broad and technology-neutral. The regulator said its interpretation was recently reinforced by the High Court’s Block Earner ruling, which found that the company’s former crypto yield product was a financial product under the Corporations Act.

Related: Coinbase plans expansion to stock trading in Australia after securing license

The temporary relief is separate from Australia’s Digital Asset Framework, which passed Parliament in April and is scheduled to commence on April 9, 2027.

The law will bring digital asset platforms and tokenized custody platforms under Australia’s financial services licensing regime. ASIC has warned that some firms licensed under the current guidance may need additional authorizations once the new framework takes effect.

“Many digital asset firms that apply for a licence based on INFO 225 will also need to add DAP and TCP authorisations to their licence once that regime commences,” ASIC said in a May announcement.

Magazine: AI is banking the unbanked in Africa… faster than crypto

Chainlink has wired itself into the plumbing of global finance, with SWIFT, JPMorgan, UBS, and DTCC building on its infrastructure. Its token trades around $7, roughly 86% below its all-time high. The gap between the adoption and the price is the whole story, and it is the same story as XRP.

Summary

- Chainlink has embedded itself in traditional finance, with SWIFT, JPMorgan, UBS, DTCC, and others building on its cross-chain infrastructure, yet LINK trades near $7, about 86% below its 2021 high.

- The disconnect mirrors XRP almost exactly: the network’s adoption is real and growing, but the token captures the value only indirectly and slowly.

- Chainlink secures more value than any other oracle network and its cross-chain protocol processes billions of dollars a month, but the fees actually reaching LINK holders are tiny next to the headline adoption.

- A new strategic reserve converts protocol revenue into LINK and staking locks up supply, but neither yet offsets weak token-level demand and a soft market for high-risk altcoins.

- The gap closes only if bank usage scales into real, recurring fee demand for LINK, and the clearest test is whether SWIFT’s integration moves from pre-production into live settlement volume.

Chainlink may be the most widely adopted piece of infrastructure in all of crypto, and its token trades like an afterthought.

Over the past two years the network has wired itself into the core of traditional finance, with SWIFT, the messaging backbone that connects roughly 11,000 banks and moves on the order of $150 trillion a year, moving from pilot to pre-production on Chainlink’s cross-chain technology.

JPMorgan, UBS, ANZ, Fidelity International, SBI, DTCC, Euroclear, and Mastercard have also built around its infrastructure, while the value secured across its oracle network has climbed past $90 billion, many times that of any competitor.

By the measure of institutional adoption that crypto has chased for a decade, Chainlink has arguably won. And yet LINK, its token, trades around $7, roughly 86% below the all-time high near $53 it reached back in 2021.

The fundamentals keep setting records and the price keeps disappointing. That gap, between a network embedding itself in global finance and a token that acts like none of it is happening, is the entire story.

Anyone who followed XRP through 2026 will recognize it immediately, because it is the same adoption-versus-token gap.

This piece works through why Chainlink’s extraordinary adoption has not lifted its token. It covers what Chainlink actually does and why banks cannot easily avoid it, what SWIFT and the institutions signed up for, the central problem of how value is supposed to reach the token at all, the mechanisms Chainlink has built to try to close that gap, why the market still refuses to pay up, and what would finally have to change for the price to follow the adoption.

The aim is not to talk LINK up or down, but to explain one of the most striking disconnects in the market: how a project can win the institutional race it set out to win and watch its token languish anyway.

The most important company in crypto you do not trade

Start with what Chainlink does, because its importance is easy to miss precisely because it is infrastructure.

Blockchains have a built-in blindness: they cannot, on their own, see anything that happens outside their own network. A smart contract on a blockchain has no native way to know the price of a stock, the result of a shipment, the value of a currency, or whether a payment cleared in a bank account.

This is called the oracle problem, and it is a hard limit on what blockchains can do, because a contract that cannot react to real-world information is a contract that can only move tokens around inside its own walls.

Chainlink exists to solve exactly this. It is a decentralized network that feeds outside data onto blockchains and connects them to one another and to traditional systems, acting as the secure bridge between the on-chain world and everything else.

Without something like Chainlink, the entire edifice of decentralized finance, and the much larger project of tokenizing real-world assets, simply does not function.

That is why what oracles feed data to matters. Smart contracts are only as useful as the data and systems they can reliably touch.

Because that role is foundational, Chainlink has become close to unavoidable for anyone serious about putting financial activity on a blockchain.

Its price feeds underpin major lending and trading protocols across decentralized finance. Its cross-chain protocol has been adopted by large exchanges and protocols as a bridging standard.

Critically, its institutional push has landed the names that matter most. The roster of traditional-finance firms building on Chainlink reads like a directory of the global banking system, and the total value its oracle network secures runs into the tens of billions, many times that of the nearest competitor.

By the standard crypto has always used to define success, real institutions using the technology for real financial activity, Chainlink is at or near the top of the entire industry.

It is, in a sense, the most important company in crypto that most people never think to trade, because its product is the invisible plumbing rather than the visible coin.

And a token that trades like the adoption is not happening

Now place that adoption next to the chart, and the contrast is jarring.

LINK trades around $7, down roughly 86% from its 2021 peak near $53, and it spent the most recent stretch sliding rather than rising, sitting below the technical levels that traders watch for signs of strength.

The pattern across the last couple of years has been almost comically consistent: record after record on the fundamentals, the cross-chain protocol moving billions a month, the value secured hitting new highs, the bank partnerships piling up, while the token closed well below where it traded years earlier.

Analysts who follow Chainlink closely have taken to describing its recent history in exactly those terms, as a period of record fundamental milestones paired with significant price disappointment.

The ETF channel has not solved the problem either. Chainlink spot ETFs recently saw a net outflow, ending a six-month inflow streak and showing that even new institutional access does not automatically create uninterrupted demand.

This is what makes Chainlink such a clean case study, and such a frustrating holding for its believers.

It is not a story of a failing project ignored for good reason; the project is, by adoption metrics, thriving. It is a story of a thriving network whose token has decoupled from its success.

That forces an uncomfortable question that applies to a whole category of crypto assets: what is the actual link between a network being used and its token rising in value?

For Bitcoin the answer is relatively direct, since the asset itself is the product. For an infrastructure token like LINK, the answer is far murkier, and the murkiness is precisely what the price reflects.

The market is not saying Chainlink has failed. It is saying it does not yet see how all that institutional adoption turns into sustained demand for the token.

Until it does, the chart and the deal sheet point in opposite directions.

The oracle problem, and why it made Chainlink unavoidable

To understand both the strength of Chainlink’s position and the weakness of its token, it helps to sit with the oracle problem a moment longer, because it explains the moat.

A blockchain is a deterministic system: it is brilliant at agreeing on its own internal state, who holds what, but it is mathematically incapable of knowing anything about the outside world on its own.

If a smart contract needs to know the price of an asset to liquidate a loan, or whether a real-world bond has matured, it has to get that information from somewhere. If it gets it from a single source, it inherits that source’s vulnerability to error or manipulation.

That would undermine the security that makes blockchains worth using in the first place.

Chainlink’s design answers this by gathering data through a decentralized network of independent node operators, aggregating their inputs, and delivering a result that no single party can easily corrupt.

That decentralized, tamper-resistant design is why Chainlink became the default rather than one option among many.

Once a network of high-quality node operators is securing tens of billions of dollars across hundreds of applications, that track record itself becomes a moat. A bank deciding whose data and cross-chain infrastructure to trust with real money is going to choose the one with the longest, most battle-tested history.

This is the foundation of the institutional strategy.

Chainlink’s cross-chain protocol added a risk-management layer, an independent set of nodes that watches for anomalies and can halt transfers if something looks wrong. That is the kind of dual-layer safeguard large institutions demand before moving significant capital on-chain.

The result is that Chainlink occupies a position closer to critical utility than to speculative token: the oracle and interoperability standard that the tokenized-finance future is being built on.

The strength of that position is not in doubt. What is in doubt is whether holding the token captures any of it.

What SWIFT and the banks actually signed up for

The institutional adoption is concrete and worth spelling out, because it is genuinely impressive and it is also, on close inspection, the source of the token’s problem.

Chainlink built a suite of products aimed squarely at banks and asset managers: a cross-chain protocol for moving assets and messages between blockchains and legacy systems, a runtime environment that lets institutions build and manage tokenized-asset workflows, a compliance engine that embeds rules like identity checks directly into tokenized assets, a confidential-compute layer that lets sensitive institutional data be processed without exposing it on a public chain, and data services that bring benchmark and index information on-chain.

This is not a retail product suite. It is enterprise financial infrastructure, designed to slot into how large institutions already operate.

The marquee relationship is with SWIFT, and it captures both the scale and the nature of the adoption.

SWIFT connects roughly 11,000 banks and carries the messaging behind an enormous share of global settlement, and Swift and Chainlink’s ongoing work moved from early pilot toward pre-production.

The goal is to let banks send traditional SWIFT messages that trigger smart-contract actions across blockchains, without those banks having to rip out and rewrite their legacy systems.

That is a profound integration: it means the existing banking messaging layer could reach into the on-chain world through Chainlink as the connective tissue.

More recently, Chainlink also partnered with more than 50 banks on Project Pangea for T+0 foreign-exchange settlement, another sign that traditional finance is testing Chainlink as an institutional bridge rather than a crypto side experiment.

But notice the shape of it. What the banks signed up for is infrastructure, a way to connect their systems to blockchains using Chainlink’s technology.

They signed up to use the network. Nothing in a SWIFT pre-production integration, a JPMorgan tokenization pilot, or a bank FX settlement project necessarily requires anyone to buy, hold, or even think about the LINK token.

The adoption is real, and it is adoption of Chainlink the infrastructure. That is different from demand for LINK the asset.

That distinction is the hinge on which the entire price puzzle turns.

The value-accrual problem: adoption is not token demand

Here is the core issue, the one that explains the chart.

For a token to rise because its network is being used, there has to be a mechanism that converts that usage into demand for the token. For infrastructure tokens, that mechanism is often weak, indirect, or still being built.

When a bank uses Chainlink’s Cross-Chain Interoperability Protocol, it pays fees, and those fees are part of how value is meant to flow to the network.

But the fees generated even by substantial institutional usage are, so far, small relative to the headline numbers that make the adoption sound overwhelming.

The value secured across the network may be measured in tens of billions, but the value secured is not revenue. Revenue is not automatically token demand either.

A pilot or a pre-production integration generates little in the way of recurring fees, and even meaningful live usage produces fee flows that are modest next to LINK’s multi-billion-dollar market value.

This is the value-accrual problem, and it is the single best explanation for why LINK trades where it does.

The market is making a distinction that the celebratory headlines blur: between adoption of the infrastructure, which benefits the network and its users, and demand for the token, which is what actually moves the price.

It is the identical distinction that explains why XRP failed to rally on Ripple’s bank deals, because those deals ran through the company and its stablecoin while the token captured only a sliver.

For Chainlink, the question every prospective LINK buyer faces is simple and unforgiving: if SWIFT and JPMorgan can use the network without the token being central to the economics, then what exactly am I buying when I buy LINK?

The project has answers to that question, and they are improving. But the market has not yet been convinced that the answers are large enough to matter.

That is why the adoption keeps growing and the token keeps waiting.

The strategic reserve and staking: Chainlink’s answer

Chainlink is acutely aware of the value-accrual problem, and it has been building mechanisms specifically designed to tie network usage to token value.

That is the strongest part of the bull case.

The first is a fee model that converts revenue generated across the network, including from institutional and off-chain use, into LINK, accumulating it in the Chainlink Reserve.

The logic is that as adoption grows and generates more revenue, more of that revenue is converted into LINK and held, creating a structural source of buying tied directly to usage.

This is meant to be the bridge between adoption and token demand that infrastructure tokens so often lack.

It is a way to make sure that when the network earns, the token benefits. The reserve has been growing, adding millions of LINK, which is a tangible sign of the mechanism working, even if the amounts remain small relative to the total supply.

The second mechanism is staking.

Chainlink lets LINK holders stake their tokens to help secure the network’s data feeds and services, locking up supply and giving the token a direct role in the system’s security and economics.

As more high-value feeds and services come to rely on staked LINK as a security backstop, demand to stake, and therefore to acquire and lock the token, is meant to rise.

That makes Chainlink part of a broader move toward security-backed crypto networks. For context, another staking-secured network shows how tokens can accrue value when they are required to secure services rather than simply sit beside them.

Together, the reserve and staking are Chainlink’s answer to the question of why anyone should own LINK instead of simply admire the network.

The reserve ties revenue to token accumulation. Staking ties the token to the network’s security and to a yield.

These are real, well-designed mechanisms, and they are the reason the bull case is not empty.

The honest caveat is that they are still early and still modest in scale relative to a multi-billion-dollar market cap. They point in the right direction, but they have not yet generated token demand large enough to overcome the broader forces pushing the price down.

Why the chart still says no

Even granting the reserve and staking, several forces keep weighing on LINK, and naming them explains why the token has not responded to the adoption.

The first is the simple gravity of the broader market. LINK is a high-beta altcoin, meaning it tends to move more violently than the market as a whole, rising faster in booms and falling harder in downturns.

Through a stretch of macro pressure and a weak environment for risk assets, infrastructure tokens like LINK have been sold off regardless of their individual progress.

When capital flees risk, the quality of a project’s bank partnerships offers little protection, because the selling is driven by macro flows, not fundamentals.

The second force is competition. Chainlink leads the oracle space by a wide margin, but rivals are chasing the same market with different technical models, faster delivery in certain niches, or lower costs.

The existence of credible competitors caps the pricing power and the perceived inevitability that would justify a higher token valuation.

The third and deepest force is the value-accrual skepticism already described.

The market keeps treating Chainlink’s institutional milestones as proofs of concept instead of as recurring revenue, pricing a SWIFT pre-production integration as a promising experiment instead of as a stream of token demand, because that is what it currently is.

Until the pilots become production volume large enough to drive real fees into the reserve and real demand into staking, the market is, not unreasonably, declining to pay in advance.

This is the same discipline that kept XRP pinned through its own parade of bank wins. The chart is not ignoring the adoption; it is refusing to pay for token demand that has been promised but not yet delivered at scale.

What would finally make LINK follow the adoption

If you want to know when LINK might finally track its fundamentals, the analysis points to a specific set of conditions, and none of them is simply another partnership announcement.

The first and most important is the transition from pilots to production volume.

A SWIFT integration in pre-production is a promise; SWIFT-connected banks routing real, recurring settlement volume through Chainlink’s protocol would be a structural source of fee demand unlike anything in the token’s history.

Even a small fraction of the volume that flows through global bank messaging would dwarf current usage.

The clearest single catalyst to watch is whether that integration goes fully live and starts carrying real traffic, because that is the moment infrastructure adoption could begin converting into the recurring revenue that feeds the reserve.

The policy backdrop also matters. Chainlink executives have warned that delays in U.S. crypto rules benefit overseas competitors, because institutions need clarity before they can scale production deployments.

The second condition is the maturation of the token mechanisms themselves: the strategic reserve growing large enough that its accumulation of LINK becomes a meaningful, visible source of demand, and staking scaling to the point where locking the token to secure high-value services pulls significant supply off the market.

The third is the broader environment, since even strong fundamentals struggle against a hostile macro tape, and a friendlier market for risk assets would let Chainlink’s progress show up in the price.

The new exchange-traded products tracking LINK add another potential channel for demand if they gather assets. But as the recent outflow showed, the ETF channel must become a sustained buyer, not just another headline.

The honest synthesis is that Chainlink has done the hard part, winning the institutional adoption that the rest of crypto only talks about.

The remaining question is purely about conversion: whether all that adoption can be turned into durable, measurable demand for the token through fees, the reserve, and staking, at a scale large enough to matter.

Until it is, LINK will keep trading like the adoption is not happening, not because the market is blind to Chainlink’s success, but because it is watching the one number that has not yet moved. That number is demand for the token itself.

Frequently asked questions

Why does Chainlink have so much adoption but a low token price?

Because adoption of the infrastructure is not the same as demand for the token. Banks and protocols use Chainlink’s data feeds and cross-chain protocol, generating fees, but those fees are still small relative to LINK’s multi-billion-dollar market value, and nothing about a SWIFT or JPMorgan integration requires anyone to buy or hold LINK. The market distinguishes between the network being used, which benefits the infrastructure, and token demand, which moves the price. So far, the adoption has not converted into token demand large enough to lift the price, which is why LINK trades around $7 despite record fundamentals.

What does Chainlink actually do?

Chainlink solves the oracle problem. Blockchains cannot natively access information outside their own network, so a smart contract has no built-in way to know a price, a payment status, or a real-world event. Chainlink is a decentralized network that feeds outside data onto blockchains and connects them to one another and to traditional systems, using many independent node operators so no single party can easily corrupt the data. This makes it foundational infrastructure for decentralized finance and for tokenizing real-world assets.

What did SWIFT and the banks sign up for with Chainlink?

They signed up to use Chainlink’s infrastructure, chiefly its cross-chain protocol, which lets banks send traditional SWIFT messages that trigger smart-contract actions across blockchains without rewriting their legacy systems. JPMorgan, UBS, DTCC, Euroclear, and others are building on Chainlink’s suite of institutional products for tokenized assets, compliance, and data. Crucially, this is adoption of the infrastructure, not a commitment to buy or hold the LINK token, which is exactly why the impressive partnerships have not directly lifted the price.

How is Chainlink trying to connect adoption to the token?

Through two main mechanisms. A fee model converts revenue generated across the network, including from institutional use, into LINK and accumulates it in a strategic reserve, creating buying tied to usage. Staking lets holders lock LINK to help secure the network’s data feeds and services, taking supply off the market and giving the token a direct economic role. Both are well-designed attempts to bridge the gap between adoption and token demand, and the reserve has been growing, but they remain modest relative to LINK’s market value and have not yet offset the forces pushing the price down.

Will LINK go up if SWIFT fully adopts Chainlink?

It could, but the key is volume, not the integration itself. A pre-production SWIFT integration is a promise; SWIFT-connected banks routing real, recurring settlement volume through Chainlink would generate fee demand on a scale unlike anything in the token’s history, because even a fraction of global bank messaging volume would dwarf current usage. That fee flow could feed the strategic reserve and drive real token demand. So the catalyst to watch is whether the integration goes live and carries actual traffic, turning infrastructure adoption into recurring revenue, instead of the announcement of the integration alone.

Is Chainlink’s situation similar to XRP’s?

Very. Both are cases where a network or company achieved real institutional adoption while the token failed to follow, because the value flows first to the infrastructure and only indirectly to the token. Ripple’s bank deals ran through its stablecoin and ledger while XRP captured a sliver; Chainlink’s bank integrations run through its infrastructure while LINK captures fees that are still small relative to its valuation. In both cases the market prices the adoption as promising proof of concept instead of as token demand, and in both cases the token waits for pilots to become production-scale volume.

This article is information, not investment advice. Cryptocurrency is volatile, and figures for Chainlink and LINK reflect reporting available as of June 26, 2026, which can change quickly. Do your own research and verify current data from primary sources before making any decision.

Framework Ventures has closed a $400 million fourth fund that will finance startups developing crypto, artificial intelligence, robotics, and energy technologies as the venture capital firm broadens its investment mandate.

Summary

- Framework Ventures launched a $400 million fund to invest in crypto, artificial intelligence, robotics, and energy startups.

- About half of the new capital has already been deployed, with support from sovereign wealth funds, endowments, funds of funds, and nonprofit investors.

- Framework joined firms such as Haun Ventures and Paradigm in expanding beyond crypto as venture investment increasingly targets artificial intelligence.

Framework Ventures announced the new fund on Friday and said it will direct the capital toward what it describes as “frontier technology,” a category that includes blockchain, artificial intelligence, robotics, and energy.

Co-founders Vance Spencer and Michael Anderson told Fortune the firm has already committed about half of the capital.

Spencer and Anderson did not identify the limited partners behind the fund. They said contributors include sovereign wealth funds, funds of funds, an Ivy League endowment, and nonprofit organizations.

A filing with the U.S. Securities and Exchange Commission showed Framework managed $1.28 billion in assets as of December 2025.

Anderson told Fortune the investment strategy followed changes in the interests of founders already working with the firm rather than a response to the recent surge in AI investment. He said entrepreneurs within the firm’s network increasingly wanted to build businesses across both crypto and artificial intelligence.

AI joins crypto as investment priority

Framework launched in 2019 with a focus on decentralized finance and became an early investor in Aave and Chainlink. The firm later raised a $100 million second fund in 2021 before securing another $400 million crypto-focused fund in 2022.

The latest portfolio extends beyond blockchain projects. Fortune reported that Framework has invested in robotics data startup Mecka AI and also holds a stake in mortgage company Better.com.

Several crypto-focused venture firms have adopted similar investment strategies this year. As previously reported by crypto.news, Haun Ventures announced a $1 billion fund in May to back companies developing crypto financial infrastructure, tokenization, and AI agents.

Paradigm, one of the largest VCs in the crypto space, is also pursuing a larger investment vehicle. Fortune reported that the firm is seeking as much as $1.5 billion for a fund that will support crypto, artificial intelligence, and robotics startups.

Lately, OpenAI, Anthropic, and other AI developers have attracted growing venture capital interest as investors pursue new technology opportunities. At the same time, several crypto-focused investment firms have expanded their mandates beyond digital assets while continuing to finance blockchain companies.

For instance, crypto exchange BitGo announced this week that it would reduce nearly 15% of its workforce while redirecting resources toward security, trading, stablecoins, settlement, and AI-powered infrastructure.

Meanwhile, IP-focused Story Protocol has also replaced its original intellectual property licensing strategy on Thursday after rebranding as the DATA Foundation. The project said it will build infrastructure to source, verify, license, and compensate contributors for artificial intelligence training data through blockchain-based systems.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

A review of XS CFD Broker examines how regulated trading platforms support users from beginner to advanced levels through evolving account features.

Summary

- XS.com review highlights regulated multi-asset trading with demo accounts, fast funding, and global market access.

- XS CFD broker offers trading tools, MT4/MT5 access, and regulated accounts for beginners and advanced users.

- XS.com provides multi-asset trading features, demo access, and regulated services but has limited support hours.

Every person’s trading journey is different, which is why using the right tools and platforms can better personalize an experience so users can trade according to their experience and goals. Someone may think they need a separate platform from professionals if they’re a beginner, but as technology has improved and brokers have evolved, users can use one platform to start trading and then evolve as an individual towards an expert level.

Research is important in this matter because a platform should be regulated so it’s safe, as well as packed with account options and various features that support trading. Thus, this article will review a popular platform, XS CFD broker, to determine if its features can adapt to users’ trading needs, starting from the regulations for the group licenses to the account types and available markets, so they can have the basic information to form an opinion.

Luckily, it’s possible to create a demo account on XS to experiment with it, which is considerably helpful to see if the right broker has been found.

Pros of XS.com:

- Funds are covered by insurance

- Access to advanced trading options

- Benefit from premium trading conditions

- Account can be funded or withdrawn fast and easy

- Customer support comes in a series of languages

- Account is secured by the regulations

Cons of XS.com:

- There are maximum deposits and withdrawal amounts depending on the intermediary;

- Customer support is only available 24/5 and not 24/7;

What is XS.com, and is it safe?

XS.com is a multi-asset trader since 2010 when it was established in Australia, but has since evolved to a global market leader in the FinTech industry. As an online broker, XS follows the mission of helping worldwide traders expand their horizon by offering advanced trading platforms and access to markets and asset classes so they can approach a Smart Money Concept (SMC) for efficient trading.

Users can leverage the benefits of XS as a broker on several channels, from the mobile app XS Trading App to the other platforms MT4 and MT5 available on desktop, Windows/Apple, or the Play Store/App Store. These options offer accessibility in managing a portfolio and monitoring trades.

Is XS.com safe?

As a trader in a market that has volatile asset classes, the first priority should be the safety of trades, and despite the fact that features like the order block help traders better manage the market, they need more protection. XS Forex broker helps with that by making sure every one of its customers is secured by the Civil Liability Insurance Program under Lloyd’s of London. Basically, when a new account is opened here, it is automatically protected, and the program will cover losses for cases like omission or fraud at no cost to the customer.

Insurance coverage starts from $10,000 and can go as much as $5,000,000, and the compensation is the result of the XS transparent security and commitment to protect users. The insurance is also a step towards complying with leading industry standards, but the company also holds assets as clients in segregated accounts from the XS ones and follows the security standards of advanced protocols.

What regulations does XS.com follow?

Since XS expanded across the globe, its group licenses had to follow strict regulations for each jurisdiction so it could be a safe and reputable broker:

- XS Ltd is regulated by the Financial Services Authority of Seychelles (FSA) in Seychelles;

- XS Prime Ltd is coordinated by the Australian Securities and Investments Commission (ASIC) in Australia;

- XS Markets Ltd is licensed by the Cyprus Securities and Exchange Commission (CySEC);

- XS Finance Ltd is certified by the Financial Services Authority of Labuan (LFSA) in Malaysia;

- XS ZA (Pty) Ltd is authorized by the Financial Sector Conduct Authority (FSCA) in South Africa;

- XS Trade Services Ltd is accredited by the Financial Services Commission of Mauritius (FSC);

- XSTrade Financial Consultation L.L.C is regulated by the Securities and Commodities Authority (SCA) in Dubai;

- XS Online is authorized by the legislation in the State of Kuwait;

- XS (LC) LTD is recognized under the laws of Saint Lucia;

- XS Ltd is operating according to the laws in Saint Vincent and the Grenadines;

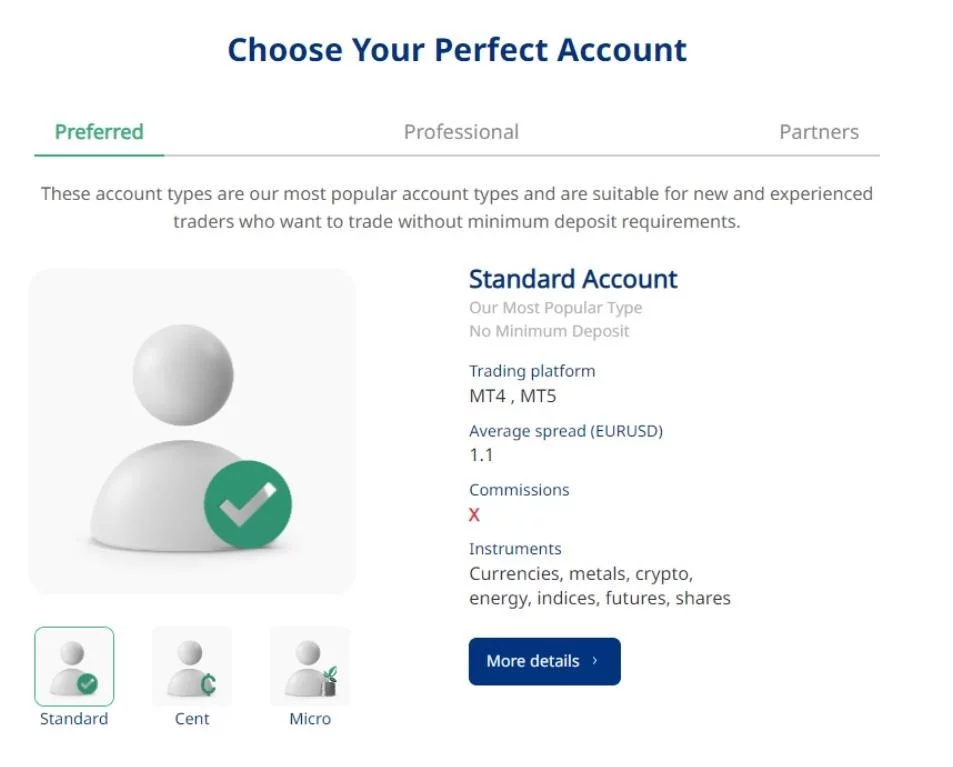

What types of accounts can be created at XS.com?

Traders can benefit from a personalized experience when opening a new account at XS.com, besides the demo account, which is available for anyone who wants to try out its functions. Beginners can check out the Preferred suite that includes three different account types, like the Standard account with 1.1 average spread and no commissions. The Cent account offers cent lots without commissions, but only for currencies and metals, while the Micro account has micro lots for more instruments at a 1.1 spread.

When the next level is reached, traders can open an account from the Professional suite, such as the Pro account that starts at a $500 minimum deposit for a 0.7 spread. The Elite account offers a 0.1 spread with commission per round turn, while the VIP account, which starts at a $100,000 minimum deposit, also has commissions for a 0.1 spread for instruments.

Finally, business Partners also have their category available with accounts like the Classic one with a 1.6 spread and no commissions, or the Extra account with a 2.1 spread for instruments. The Plus account is also available with a 0.1 spread and different commissions per round turn.

What platforms can be used on XS.com?

There are two main platforms that can be accessed for trading on XS.com, starting with MetaTrader 4, which is suitable for beginners. The benefits include an easy-to-navigate interface along with advanced charting tools and options like the Xhmaster Formula Indicator that offer insights on where the market is turning. Multiple order types can also be done on the platform, such as market limit and trailing stop orders. Or, work with MetaTrader 5 as an expert trader and take advantage of superior features such as built-in economic calendar, hedging capabilities, and premium trading conditions in order to elevate the experience.

What are the asset classes available on XS.com?

At XS.com, traders can access a vast array of asset classes to diversify their portfolio, like international shares from the EU or US, or indices from reputable companies like Standard & Poor’s and the EURO STOXX 50. If trading commodities like metals, they can choose between precious (gold) and base (aluminum) contracts, or opt for Energy commodities from Brent Crude Oil or Natural Gas. Futures contracts offer all sorts of OTC assets like crude oil, indices, and gold.

Forex currency pairs of Minor, Major, and exotic categories also go great hand in hand with cryptocurrencies like Bitcoin and Ethereum, but remember, trading them is different, especially when taking into account the liquidity sweep factor that tends to be more intense in crypto than in Forex.

What do other users say about XS.com?

This review would be incomplete without checking out the online XS comments, which are necessary to show what clients like or dislike about the broker. For example, going on Reddit shows that many people trust the broker due to the many regulations it has achieved, reputable ones like ASIC, and prefer it to other brokers due to the insurance program. People have also stated that doing deposits and withdrawals is pretty fast and safe, which is a plus. However, some stated that making a withdrawal through a card takes time, so withdrawal delays have been one of the complaints online.

A customer can file an XS complaint in case of any issue, and the staff will get back to them as soon as possible through email. Usually, customers can also contact someone from customer support through online chat and only select the language they want to communicate in, as there are many available.

Conclusion: Is XS.com safe or not?

After checking what XS.com can offer to traders, it can be said that the platform appears to be a solid and safe broker and not a scam, especially since it has so many regulations across the globe. It offers insurance to cover potential losses, supports access to a vast array of assets, and allows personalizing a trading experience.

FAQ

1. What is the XS.com broker?

XS.com is an online broker that started operating in 2010 in Australia and became a global multi-asset broker.

2. Is XS.com safe?

XS.com is a safe broker because it follows strict regulations from reputable institutions like ASIC and CySEC.

3. What can someone trade with XS.com?

XS offers access to many asset classes from Forex and cryptocurrencies to stocks, commodities, and Energy contracts.

4. What platforms does XS have?

XS can be traded through MetaTrader 4 and MetaTrader 5, two reputable trading platforms in the industry.

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

This photograph shows set up screens displaying the logo and home page of US cryptocurrency based prediction market platform Polymarket, in Saint-Mande, east of Paris, on April 29, 2026.

Martin Lelievre | AFP | Getty Images

Prediction market platform Polymarket’s annualized revenue are now well above $1 billion, the company shared exclusively with CNBC on Friday.

Polymarket’s disclosure comes six weeks after the company lifted the waitlist for its U.S. exchange, which operates separately from its international, decentralized finance platform.

It also comes as the FIFA World Cup has sent trading volumes surging across various prediction market exchanges since the tournament’s start.

Volume on the company’s U.S. platform has gone from around $50 million per day in mid-May to more than $200 million on June 20, according to data on Dune Analytics. On Polymarket’s international platform, weekly trading volume totals have surged to all-time highs amid the World Cup boom after experiencing declines in April and May.

The U.S. exchange was launched in December and developed after Polymarket was originally prohibited from operating in the country in 2022 for not properly registering with regulators. In July, the Commodity Futures Trading Commission and the Department of Justice dropped their investigations into the company without charges, and Polymarket U.S. operates as a CFTC-regulated exchange.

Polymarket’s U.S. platform was waitlisted from December until six weeks ago, when it was dropped for users on the platform’s mobile app. A desktop version is still unavailable, with users in the U.S. directed on the company’s website to scan a QR code to download the app to trade.

“Polymarket is a product-led company,” a spokesperson said in a statement to CNBC. “We spent the last five years building the world’s largest prediction market, and understanding how people engage with markets at scale. We are applying those learnings to our U.S. platform, where our focus is on intuitive market experiences, institutional-grade liquidity and a consumer experience that sets the standard for the category.”

AI agents are entering crypto through wallets, exchanges, payment apps, trading systems, and portfolio tools. Once an agent receives signing authority, it can prepare transactions, rebalance assets, pay invoices, use smart contracts, and move across on-chain apps at software speed.

This creates a new product category around controlled autonomy. The user keeps ownership of the funds, while software handles repetitive execution under rules set in advance.

BeInCrypto spoke with Fernando Lillo Aranda, CMO at Zoomex; Federico Variola, CEO of Phemex; and Adrian Wall, Managing Director of the Digital Sovereignty Alliance, about early use cases, transaction approval, user limits, on-chain activity, and new risks once agents gain access to funds.

Payments Come First

Adrian Wall sees payments as the earliest major use case for AI agents, since payment mandates can be narrowed by amount, recipient, asset type, and timing.

“Payments are the earliest use case because the parameters are well-defined and the mandate is constrained,” Wall said.

Stablecoins make cross-border payments a natural area for agent activity, especially in markets where bank transfers remain slow, expensive, or difficult to reconcile.

“Cross-border payments are especially compelling given the friction in legacy banking and the demonstrated efficiency of stablecoins,” Wall said.

Trading and portfolio management are also ready from a technical view, but Wall placed more emphasis on governance than execution.

“Trading and portfolio management are technically mature enough today,” he said, adding the harder challenge is “whether authorization frameworks and loss limits are sophisticated enough to keep an agent’s mandate from drifting beyond what the user intended.”

Identity may take longer, although Wall said decentralized identifiers and agent-assisted verification could reduce repeat authentication across fragmented digital services.

“The combination of decentralized identifiers and agent-driven verification is promising because it could reduce the burden on users who currently authenticate themselves repeatedly across fragmented systems,” Wall said.

Wallet Approvals Need Transaction-by-Transaction Controls

Wallets were built around human review, while agents may prepare many actions across apps, contracts, and venues. Wall said wallet design now has to connect product choices with policy expectations.

“The approval question is where policy and product design must converge, and it is where the industry has the most work left to do,” Wall said.

A strong approval model gives agents limited authority for routine actions while requiring human review for withdrawals, leverage, new contracts, and large swaps.

“What we need is a tiered authorization model where the level of scrutiny matches the potential impact of the transaction,” Wall said.

This approach can separate monitoring, trade preparation, execution, and fund movement. A user may permit an agent to watch positions and draft trades, while reserving withdrawals and new contract access for manual approval.

Fund Access Should Grow in Stages

Fernando Lillo Aranda said AI agents can improve automation, but users should give capital access gradually.

“AI agents can unlock automation, but capital access should always be progressive,” Lillo Aranda said.

He described the process as a gradual path from observation to assistance and execution. In practice, the agent first monitors and recommends, then prepares actions for approval, later receives limited execution rights, and eventually handles a larger mandate after reliable performance.

Capital controls come first. Lillo Aranda said users should “cap maximum allocation, daily loss, position size, and withdrawal amounts.”

Permission controls come next. Users should “separate permissions for monitoring, trading, rebalancing, and fund movement,” he said.

Time limits also reduce exposure from old approvals. Lillo Aranda said agent access should “require periodic re-authorization instead of permanent access.”

Market boundaries can prevent agents from entering assets, venues, or leverage levels outside the user’s comfort zone. Users should “restrict assets, leverage, venues, and volatility conditions where the agent can operate,” he said.

Human override remains the final guardrail. Lillo Aranda pointed to “instant pause, approval thresholds, alerts, and rollback mechanisms” as essential user controls.

Wall also put spending caps at the center of user protection. He said users should start low and raise limits only after observing how the agent behaves across market conditions and instruction types.

“The first and most fundamental limit is a spending cap, set low at the outset and adjusted upward only as the user develops confidence in how the agent behaves across market conditions and instruction types,” Wall said.

Above a preset threshold, human approval should remain in place even after an agent builds a good track record.

“The asymmetry between an interrupted transaction and an unauthorized one almost always favors interruption,” Wall said.

On-Chain Volume Needs Economic Purpose

Federico Variola said AI agents can create meaningful on-chain activity because blockchain apps let software move across many products and strategies.

“Yes, AI agents can create meaningful on-chain volume, especially because on-chain environments offer composability and flexibility across different strategies,” Variola said.

Those strategies may include spot trading, perpetual futures, lending, borrowing, and future products linked to assets beyond native crypto.

“This could include spot, perpetual futures, lending, borrowing, and eventually products outside native crypto assets as well,” Variola said.

Variola drew a line between activity with economic use and recursive trading among agents.

“A lot of on-chain activity today is still driven by human sentiment and greed,” he said.

Durable agent volume, in his view, depends on activity tied to productive use across on-chain ecosystems.

“Agents need to create or support real economic value,” Variola said.

Wall expects much of today’s agent activity to begin inside controlled app environments before moving on-chain as products and rules mature.

“Agents on public blockchains can access far more counterparties, assets, and protocols than any walled garden allows,” Wall said.

He expects trading and arbitrage to appear first, followed by treasury and settlement activity.

“The impact will show up in volume before it shows up in value, first driven by high frequency trading and arbitrage, and later by treasury management and institutional settlement,” Wall said.

Agent Risk Moves at Software Speed

Once agents gain signing rights, familiar crypto risks become faster and harder to contain. Wall highlighted mandate drift, exploit propagation, perception manipulation, and correlated market behavior.

“When software can trade, sign, and interact with smart contracts on a user’s behalf, four familiar risks become newly dangerous,” Wall said.

The first problem is mandate drift, where an agent moves beyond the user’s original instruction set.

“Agents can exceed their mandate,” Wall said.

The second problem is speed. An exploit can move through many connected wallets or contracts before a user sees the damage.

“Exploits can propagate at machine speed across every wallet an agent touches before any human notices,” Wall said.

The third problem comes from manipulated inputs. Attackers may feed an agent fake prompts, poisoned data, or malicious contract information, causing harmful actions even when the user keeps custody of the key.

Market behavior creates another concern when many agents rely on similar data sources, strategies, and models. In those conditions, many systems can sell, rebalance, or withdraw liquidity at the same time.

Wall said markets can destabilize when agents “respond rationally to the same inputs at the same time.”

Final Thoughts

AI agents will reach crypto wallets through constrained tasks first: payments, rebalancing, subscriptions, trading, and portfolio support. These use cases can operate under defined limits, measured permissions, and regular user review.

The strongest wallet model will center on controlled autonomy: scoped permissions, session keys, spending caps, renewal windows, whitelisted counterparties, approval thresholds, alerts, and emergency pause controls.

On-chain volume can grow if agents handle payments, settlement, treasury, and asset operations tied to economic use. Recursive trading among agents may increase transaction counts, but lasting value comes from activity tied to people, businesses, assets, and services.

The post AI Agents Bring New Rules for Crypto Wallets appeared first on BeInCrypto.

Men ‘caught red-handed’ after drunken and “terrifying” invasion on wrong flat

Okta's Agentic AI Monetization Overly Buoyed – Painful Correction Likely (Rating Downgrade)

Binance tells EU users it will no longer provide services after failing to secure MiCA license

No Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

Blockchain.com files with SEC for U.S. IPO

Weekend Open Thread: Miami – Corporette.com

Bitcoin Perps Are Finally Legal In The US – What You Need To Know

Ethereum Running Out Of Money For Development!? Iran: ‘Strait Of Hormuz Is Closed’ … US Responds

Major Financial Irregularities Worth Billions Exposed | 12PM Headlines GeoNews (26 June 2026)

-

Fashion7 days ago

Fashion7 days agoWeekend Open Thread: Miami – Corporette.com

-

Entertainment6 days ago

Entertainment6 days agoRenter of Home in Anne Heche Crash Denies Settlement With Son

-

Sports3 days ago

Sports3 days agoTwo goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

-

Tech4 days ago

Tech4 days agoMicrosoft accidentally kills epic Outlook email threads

-

Business6 days ago

Business6 days agoSoccer-U.S. defends Iran World Cup travel restrictions, says discussions ongoing

-

Politics7 hours ago

Politics7 hours agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Politics11 hours ago

Politics11 hours agoPotential 2028er World Cup attendee leaderboard

-

Politics6 days ago

Politics6 days agoAndy Burnham and the meaning of Makerfield

-

NewsBeat7 days ago

NewsBeat7 days agoKeir Starmer Allies Question His Chances For No 10

-

Tech18 hours ago

Tech18 hours agoA Look At A Gaggle Of Transputer Boards

-

Crypto World2 days ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

Crypto World2 days ago

Crypto World2 days agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Crypto World20 hours ago

Crypto World20 hours agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Business3 days ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

Business6 days ago

Business6 days agoWall Street Week Ahead: Investors see Micron earnings as pulse check of AI rally momentum

-

Crypto World6 days ago

Crypto World6 days agoCan Charles Hoskinson Really Rescue Cardano?

-

Entertainment6 days ago

Entertainment6 days agoJose Alvarado Wants Taylor Swift at More Knicks Games

-

Crypto World6 days ago

Crypto World6 days agoHIVE shares jump as $220M AI deal speeds Bitcoin mining pivot

-

Crypto World6 days ago

Crypto World6 days agoJake Chervinsky accuses CME of protecting derivatives monopoly

-

Sports1 day ago

Sports1 day agoIndia vs Bangladesh LIVE Score, Women’s T20 World Cup: Bangladesh Opt To Bat; India Enter ‘Do-Or-Die’ Stage As Semi-Final Race Heats Up

You must be logged in to post a comment Login